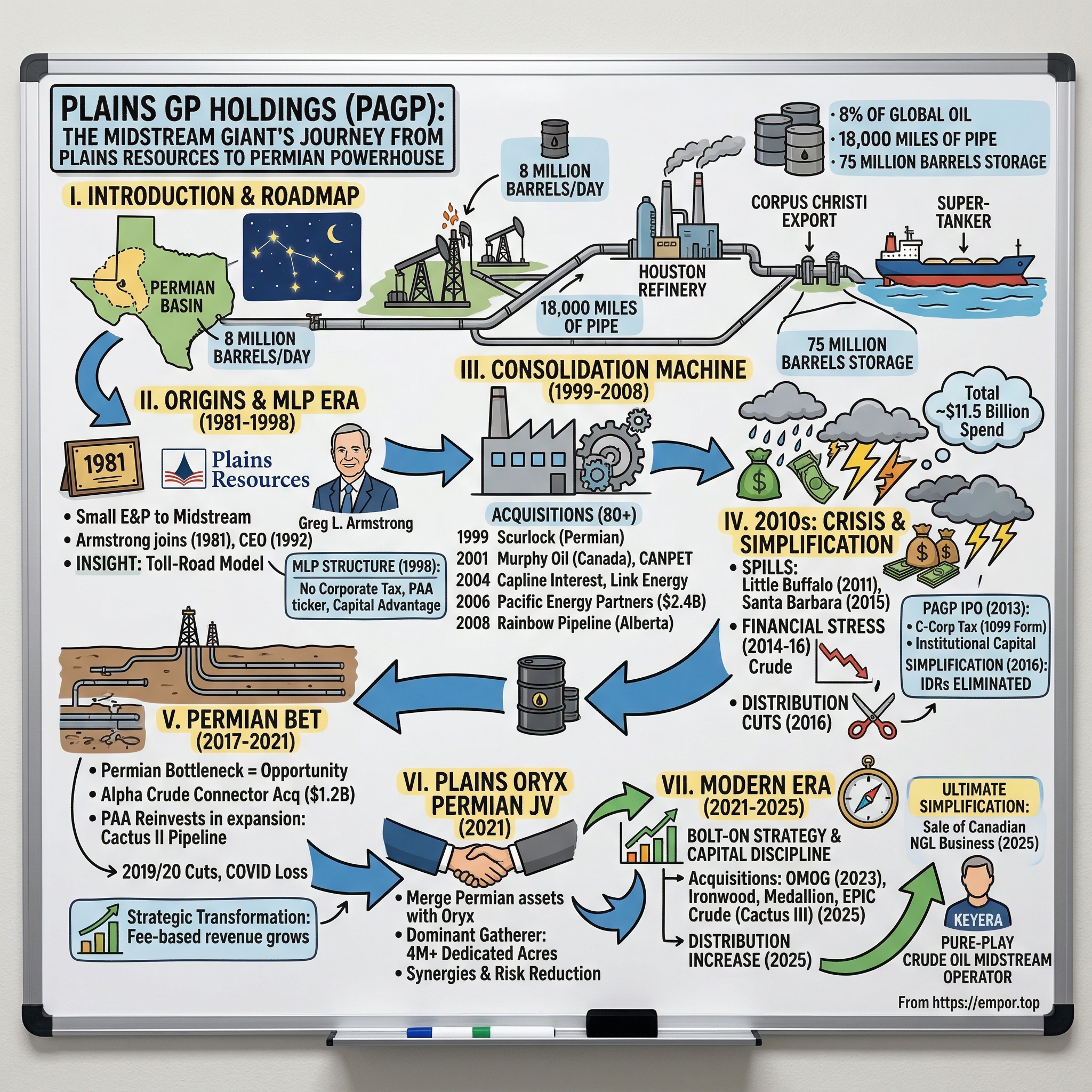

Plains GP Holdings: The Midstream Giant's Journey from Plains Resources to Permian Powerhouse

I. Introduction & Episode Roadmap

Picture a map of the United States at night, the kind taken from the International Space Station. The bright clusters are obvious — New York, Chicago, Los Angeles. But look at West Texas and southeastern New Mexico, and you will see something strange: a constellation of light in the middle of nowhere, glowing as intensely as some major cities. That is the Permian Basin, the single most productive oil field on Earth, responsible for roughly six million barrels of crude per day and counting. Now ask yourself: how does all that oil get from a wellhead in Loving County, Texas — a place with fewer than seventy permanent residents — to a refinery in Houston, an export terminal in Corpus Christi, or a supertanker bound for Asia?

The answer, in large part, is Plains All American Pipeline. And the publicly traded vehicle that sits atop that empire — the entity that most investors actually buy — is Plains GP Holdings, ticker PAGP. Together, this system handles more than eight million barrels per day of crude oil and natural gas liquids. That is roughly eight percent of total global oil production flowing through a single company's network every single day. If Plains All American were a country, it would rank among the top ten oil-producing nations by throughput alone.

But Plains is not just big. It is a case study in almost every major theme of American energy over the past four decades: the rise of the master limited partnership, the shale revolution, the infrastructure bottleneck, the painful distribution cuts that punished yield-chasing investors, and now the disciplined simplification that has turned Plains into something approaching a pure-play Permian crude oil toll road. Think of it as the turnpike authority of American oil — collecting fees every time a barrel moves through its eighteen thousand miles of pipe, its seventy-five million barrels of storage, its terminals stretching from Alberta to the Gulf of Mexico.

The story begins in 1981 with a tiny exploration company in the shallow Permian fields. It runs through more than eighty acquisitions, two catastrophic oil spills, three distribution cuts, a pandemic-driven loss of nearly three billion dollars, and a governance structure so byzantine that it required its own publicly traded holding company just to make the tax math work. The themes that emerge — consolidation, simplification, and the generational bet on the Permian Basin — are not just relevant to Plains. They are the themes of the entire midstream energy sector, and understanding them is essential for anyone trying to evaluate whether America's pipeline infrastructure represents a durable investment or a slowly melting ice cube in an electrifying world.

II. Origins & The Master Limited Partnership Era (1981-1998)

In 1981, Ronald Reagan had just taken office, oil prices were near their inflation-adjusted highs following the Iranian Revolution, and a small company called Plains Resources incorporated in the state of Texas with a simple mission: find oil and pump it out of the ground. The company went public as a traditional exploration and production outfit working the shallow, well-understood formations of the Permian Basin, producing roughly a hundred barrels per day. It was, by any measure, unremarkable.

What made Plains Resources consequential was not what it drilled but who it hired. A twenty-two-year-old accountant named Greg L. Armstrong joined the company shortly after that 1981 incorporation. Armstrong, a graduate of Southeastern Oklahoma State University with degrees in accounting and management, was the kind of person who understood that the real money in oil was not in finding it — that was geology's gamble — but in moving it. Over the next decade, Armstrong rose through Plains Resources as chief accounting officer, chief financial officer, and chief operating officer before becoming CEO in 1992, at the age of thirty-four, one of the youngest chief executives of any publicly traded energy company in America.

Armstrong's insight was structural, not geological. He recognized that upstream oil production — the act of drilling wells and extracting crude — was inherently volatile. Commodity prices swung wildly, wells declined naturally, and the capital expenditure treadmill never stopped. But the infrastructure that moved crude oil from wellhead to refinery operated on an entirely different economic logic. Pipelines, storage tanks, and gathering systems were capital-intensive to build but cheap to operate once in place. They earned fees based on volume, not price. A barrel of oil at forty dollars and a barrel at eighty dollars paid roughly the same tariff to flow through a pipeline. This was, in essence, a toll road — and toll roads, as any infrastructure investor knows, are among the most durable businesses ever invented.

In 1989, Plains Resources formalized this thinking by establishing a midstream subsidiary to handle crude oil transportation, storage, and marketing. The subsidiary grew quietly through the 1990s as major integrated oil companies — the Chevrons and Exxons of the world — began divesting their logistics operations, viewing them as non-core. Armstrong saw an opportunity to buy these assets at reasonable multiples and stitch them into a growing network.

The watershed moment arrived in 1998. Armstrong and his team decided to spin out the midstream operations into a Master Limited Partnership — a structure that deserves a moment of explanation because it shaped everything that followed. An MLP is a publicly traded partnership that avoids corporate income tax entirely. Instead of paying taxes at the entity level and then again when shareholders receive dividends (the "double taxation" that afflicts regular corporations), an MLP passes all income directly to its unitholders, who pay taxes on their individual returns. The tradeoff is that MLPs are required to distribute substantially all of their available cash to unitholders, which makes them attractive to income-seeking investors but limits the cash available for growth.

Plains All American Pipeline, L.P. — ticker PAA — completed its initial public offering in November 1998 on the New York Stock Exchange. The IPO raised capital to acquire the All American Pipeline System, a 1,233-mile crude oil pipeline running through California that had been bringing offshore crude to inland markets. Armstrong became chairman and CEO of both the new MLP and the parent company, a dual role he would hold for two decades. The founding acquisition gave PAA its name, its initial geographic footprint, and its identity: this was not going to be a natural gas pipeline company or a diversified energy conglomerate. Plains All American was going to be the crude oil infrastructure company of North America.

The timing proved fortuitous. The late 1990s and early 2000s saw a wave of asset divestitures by major oil companies, and PAA's MLP structure gave it a cost-of-capital advantage that traditional corporations could not match. The toll-road model was about to become a toll-road empire.

III. The Consolidation Machine: Building the Network (1999-2008)

The first deal after the IPO set the tone for everything that followed. In 1999, Plains acquired Scurlock Oil Company's Permian Basin and West Texas pipeline and gathering assets from Chevron for thirty-five million dollars. Scurlock had been a significant crude oil gatherer, and the acquisition gave PAA immediate scale in the basin it would eventually dominate. The playbook was elegant in its simplicity: find pipeline and gathering assets owned by major oil companies that considered them non-core distractions; buy them at modest multiples; integrate them into a growing network where the combined system was worth more than the sum of its parts.

Think of it like buying individual subway lines from different operators and connecting them into a single transit system. Each line has value on its own, but the network — the ability to move passengers (or barrels) seamlessly from origin to destination — creates value that no single line can capture alone. Armstrong understood this intuitively, and he executed it relentlessly.

The pace accelerated quickly. In 2001, PAA made two significant moves: acquiring Murphy Oil's midstream operations for a hundred and fifty-five million dollars, which gave it a foothold in the Canadian crude oil market, and simultaneously purchasing CANPET Energy Group, a Calgary-based crude oil and liquefied petroleum gas marketing company, for forty-two million dollars. The Murphy deal brought physical pipeline and gathering assets in Alberta; CANPET brought the commercial expertise and trading relationships to make those assets productive. Together, they established Plains Midstream Canada and gave PAA a North American footprint that extended well beyond its Permian and California roots.

The year 2004 brought two transformative acquisitions. First, PAA secured a twenty-two percent interest in the Capline Pipeline System for approximately two hundred and twenty-eight million dollars. Capline is a six-hundred-and-thirty-two-mile crude oil artery running from St. James, Louisiana, to Patoka, Illinois — one of the most important crude oil corridors in the United States, connecting Gulf Coast imports and production to Midwest refineries. In the same year, PAA acquired the Link Energy pipeline system for two hundred and seventy-three million dollars, broadening its reach across the Mid-Continent and Southwest. These two deals, completed within months of each other, transformed PAA from a regional gatherer into a national infrastructure operator.

But the defining deal of the consolidation era came in 2006, when PAA acquired Pacific Energy Partners for two billion four hundred million dollars — roughly three times the cumulative value of every prior acquisition combined. Pacific Energy operated crude oil and refined products pipelines in California and on the Gulf Coast, and its integration dramatically expanded PAA's California operations while providing critical Gulf Coast infrastructure. This was no longer a scrappy MLP picking up orphaned assets. This was a large-cap consolidator making billion-dollar bets.

The Canadian expansion continued in 2008 with the acquisition of the Rainbow Pipeline in northern Alberta from Imperial Oil, ExxonMobil, and Shell for approximately five hundred and forty million Canadian dollars. Rainbow was a seven-hundred-and-eighty-one-kilometer crude oil gathering and transmission system connecting northwest Alberta's Peace River oil sands to Edmonton — the dominant crude oil pipeline in the region, handling approximately two hundred thousand barrels per day. The deal cemented Plains Midstream Canada as a premier operator in the Alberta crude oil market, though the Rainbow system would later become the site of one of the company's darkest chapters.

By the end of 2008, Armstrong had completed the construction phase of his vision. PAA operated thousands of miles of pipeline across the United States and Canada, handled millions of barrels per day, and had established itself as the go-to consolidator of crude oil midstream assets in North America. The company had completed more than eighty acquisitions totaling approximately eleven and a half billion dollars, alongside nearly eight billion dollars in organic expansion projects. It was a remarkable run — but the next decade would test the entire model, and the man who built it, in ways no one anticipated.

IV. The 2010s: Crisis, Distribution Cuts, and the Simplification Journey

On the morning of April 29, 2011, a section of the Rainbow Pipeline ruptured in the boreal forest of northern Alberta, about ten kilometers from the Lubicon Cree community of Little Buffalo. Over the following hours, approximately twenty-eight thousand barrels of crude oil poured into the wilderness — the largest land-based oil spill in Alberta in thirty-six years. The regulatory investigation that followed was devastating: Alberta's Energy Resources Conservation Board found that Plains Midstream Canada had restarted the leaking pipeline four times after problems were first detected, likely making the spill significantly worse. Regulators characterized the company's response as displaying a "bias toward inaction." Residents of Little Buffalo reported fumes causing nausea and burning eyes. Children fell ill at school. The school itself was not formally notified about the spill until six days after it happened.

Plains Midstream Canada ultimately pleaded guilty and was fined 1.3 million Canadian dollars — an amount widely criticized as woefully inadequate. The fine may have been small, but the reputational damage was enormous. For a company whose entire business model depends on the social license to operate pipelines across other people's land, the Little Buffalo spill was an existential wake-up call.

Four years later, it happened again — this time in front of television cameras and the national press. On May 19, 2015, a twenty-four-inch crude oil pipeline known as Line 901, owned by a PAA subsidiary, ruptured near Refugio State Beach on California's Gaviota Coast. Approximately a hundred and forty-three thousand gallons of heavy crude oil spilled, flowing through a storm drain and into the Pacific Ocean. The images of oil-soaked pelicans and blackened beaches became a symbol of pipeline safety failures at a time of growing public scrutiny of fossil fuel infrastructure.

Federal investigators concluded that Plains had failed to address external corrosion on the pipeline and that control room procedures were inadequate. The legal consequences accumulated over years: a federal criminal settlement requiring twenty-four million dollars in civil penalties plus tens of millions more in natural resource damages and cleanup costs; a two-hundred-and-thirty-million-dollar class action settlement in 2022 to compensate fishermen and affected residents; and a seventy-two-and-a-half-million-dollar settlement with the California State Lands Commission in 2024. All told, the Santa Barbara spill cost Plains well over three hundred million dollars in direct financial penalties, plus incalculable reputational harm.

These operational crises unfolded against a backdrop of financial stress. The oil price collapse of 2014-2016 hammered the entire energy sector, and PAA was not immune. Unit prices plummeted from sixty dollars in mid-2014 as crude oil crashed from over a hundred dollars per barrel to under thirty. Distribution coverage — the ratio of cash generated to cash distributed — fell to a dangerously thin 0.86x by 2016, meaning PAA was paying out more than it was earning.

The painful decision came in the third quarter of 2016: PAA cut its quarterly distribution by twenty-one percent, from seventy cents to fifty-five cents per unit. For an MLP whose investors had bought in specifically for the yield, this was a betrayal. But it was also, in hindsight, an act of discipline that preserved the company's financial flexibility when others in the sector were drowning.

Meanwhile, the corporate structure itself had grown baroque. In October 2013, Plains GP Holdings — ticker PAGP — had completed its own IPO, raising approximately two billion eight hundred million dollars in what was the largest IPO on U.S. markets that year. PAGP existed solely to own the general partner interest and the incentive distribution rights in PAA. Those IDRs were the most controversial feature of the MLP model: as PAA's distributions grew above certain thresholds, the GP received a progressively larger share of incremental cash flow, eventually reaching fifty percent of every additional dollar distributed. This created enormous leverage for PAGP — a ten percent increase in PAA's distribution could translate to a twenty percent increase in PAGP's cash flow — but it also created an inherent conflict between the GP and the limited partners.

The crucial innovation of PAGP's structure was its tax election. Although organized as a limited partnership, PAGP chose to be taxed as a corporation. This meant investors received a familiar 1099 form rather than the dreaded K-1 that PAA unitholders had to wrestle with at tax time. The distinction sounds technical, but it was enormously consequential: K-1s are complex, arrive late, can create tax obligations in multiple states, and generate unrelated business taxable income that makes them unsuitable for retirement accounts and institutional portfolios. PAGP's 1099 structure opened the door to pension funds, endowments, foreign investors, and anyone with an IRA — a vastly larger pool of potential capital.

By 2016, the IDR structure had become untenable. In a falling distribution environment, the IDRs were not generating meaningful cash for the GP anyway, but they remained a structural overhang that raised PAA's cost of equity capital. In July 2016, Plains executed the Simplification Transaction: PAA issued two hundred and forty-five million new units to eliminate the IDRs and GP economic interest, a transaction valued at approximately seven billion two hundred million dollars. Each PAGP share became backed by one PAA unit, and the misaligned incentives that had plagued the MLP model were removed. In 2021, the company went further, eliminating legacy director designation rights. The message was clear: the era of complex, GP-favoring governance was over. The question was whether investors would believe it after three years of broken promises on distributions.

V. The Permian Bet: Transformation Through Infrastructure (2017-2021)

To understand what Plains did next, you need to understand the Permian Basin — not just as a geographic feature, but as an economic phenomenon without parallel in the history of energy production. The Permian stretches across roughly seventy-five thousand square miles of West Texas and southeastern New Mexico, a region so flat and dry that early settlers considered it worthless. Beneath that arid surface lie stacked layers of oil-bearing rock formations — the Wolfcamp, the Bone Spring, the Spraberry — that the horizontal drilling and hydraulic fracturing revolution of the 2010s unlocked with staggering productivity. By the mid-2020s, the Permian was producing more than six million barrels of oil per day, making it more productive than every OPEC member except Saudi Arabia.

But there was a problem. The Permian's production surge massively outpaced the pipeline infrastructure needed to move all that crude to refineries and export terminals on the Gulf Coast. In 2017 and 2018, the bottleneck became so severe that Permian crude traded at discounts of more than fifteen dollars per barrel below Gulf Coast prices. Producers were literally drowning in oil they could not ship. Some resorted to trucking crude at vastly higher cost. Others curtailed production. The message to midstream operators was unambiguous: whoever built the pipes to relieve this bottleneck would earn outsized returns for decades.

Plains made its Permian bet in February 2017 with the acquisition of the Alpha Crude Connector for one billion two hundred and fifteen million dollars. The ACC was a five-hundred-plus-mile crude oil gathering system running through the heart of the northern Delaware Basin in southeastern New Mexico, precisely where the shale revolution was hitting hardest. Greg Armstrong, still CEO at the time, projected that crude production on the system's dedicated acreage would double within two to three years. He was right.

But the Permian build-out required enormous capital, and that capital had to come from somewhere. PAA reinvested aggressively in expansion projects — long-haul pipelines like Basin Pipeline, Sunrise Pipeline, and the massive Cactus II system stretching five hundred and seventy-five miles from the Midland Basin to Corpus Christi. These projects consumed billions of dollars in capital expenditure and required two additional distribution cuts beyond the 2016 reduction: one in the second half of 2019, slashing the quarterly payout from fifty-five cents to thirty-six cents, and another savage fifty-percent cut in the spring of 2020 when the COVID-19 pandemic annihilated global oil demand virtually overnight.

The 2020 numbers were staggering. PAA recorded a net loss of two billion five hundred and ninety million dollars for the year, driven by approximately three billion two hundred million dollars in non-cash impairment charges as the pandemic forced the company to write down the value of assets whose throughput had collapsed. The supply and logistics segment — PAA's commodity-exposed trading business — saw its adjusted EBITDA decline by ninety-nine percent in the second quarter alone. It was the worst year in the company's history, and it came after half a decade of distribution cuts and spill-related reputational damage. Investor sentiment toward Plains bordered on contempt.

Yet beneath the carnage, the strategic transformation was working. The Permian infrastructure was being built. Cactus II came online. Gathering networks expanded. Fee-based, long-term contracted revenue grew as a share of the business while volatile commodity-exposed trading shrank. Plains was enduring the pain of building while bleeding — investing billions in long-lived infrastructure at precisely the moment when its stock price and public credibility were at their lowest. It was a gamble that only made sense if you believed the Permian would remain America's swing producer for decades. Management believed exactly that, and they bet the company on it.

The turnaround, when it came, was decisive. As pandemic restrictions eased and global oil demand recovered through 2021 and into 2022, Plains' newly expanded Permian infrastructure was perfectly positioned to capture surging volumes. Throughput climbed. Fee-based revenue grew. The balance sheet began to heal as strategic divestitures and debt reduction took hold. The company that had been left for dead by many investors was suddenly generating robust free cash flow from the largest crude oil gathering network in America's most important oil basin.

VI. The Joint Venture Era: Plains Oryx Permian Basin (2021)

In the summer of 2021, as vaccine rollouts brought the world tentatively back from the pandemic, Plains All American made a move that would reshape the competitive landscape of Permian Basin midstream. On July 13, the company announced a definitive agreement to merge its Permian Basin gathering and transportation assets with those of Oryx Midstream Holdings, a portfolio company of Stonepeak Infrastructure Partners, one of the largest infrastructure-focused private equity firms in the world.

The deal was elegant in its construction. It required no cash from either party. Plains contributed approximately thirty-nine hundred miles of pipeline and acreage dedications covering roughly two million eight hundred thousand acres. Oryx brought approximately sixteen hundred miles of pipeline and dedications covering about one million three hundred thousand acres. The combined entity — Plains Oryx Permian Basin LLC — controlled over four million dedicated acres across the Delaware and Midland basins with an average remaining contract tenor of approximately seven years. Plains owned sixty-five percent; Oryx owned thirty-five percent under a tiered distribution-sharing arrangement.

The strategic logic was compelling on multiple levels. First, scale: the combined system was the dominant crude oil gatherer in the Permian, with no close second. Second, synergies: the companies projected approximately fifty million dollars in near-term operational and capital efficiencies from eliminating redundant infrastructure, optimizing truck-to-pipeline transfers, and coordinating gathering routes, with potential to reach a hundred million or more over time. Third, risk reduction: by merging complementary footprints, the JV reduced concentration risk — if production shifted from one part of the basin to another, the combined system was more likely to capture the volumes regardless.

Perhaps most importantly, the deal brought credibility. Stonepeak's willingness to contribute Oryx's assets — which the private equity firm had assembled through its own aggressive acquisition program — into a joint venture controlled by Plains signaled to the market that sophisticated infrastructure investors saw Plains' Permian network as a best-in-class asset. The transaction closed on October 5, 2021, and the JV was consolidated into Plains' financial statements from that point forward.

The structure also revealed a strategic division within Plains' thinking. The company contributed its intra-basin gathering and transportation assets — the smaller-diameter pipes that collect crude from individual well sites — but retained its long-haul pipeline systems (Cactus I, its seventy-percent interest in Cactus II, and its terminalling assets). This separation made strategic sense: gathering systems are operationally intensive, relationship-driven businesses where scale and density create competitive advantages; long-haul pipelines are higher-margin, lower-touch assets where capacity and connectivity matter most. By merging gathering with Oryx while retaining long-haul, Plains optimized each business for its distinctive competitive dynamics.

The JV model also introduced a new paradigm for capital efficiency in midstream. Rather than financing growth entirely from its own balance sheet — the approach that had led to painful leverage problems during the 2016-2020 period — Plains now had a partner sharing the capital burden of Permian gathering expansion. New well connections, compression facilities, and pipeline extensions could be funded proportionally, reducing Plains' individual capital commitment while maintaining its dominant market position. It was growth without balance sheet strain, a lesson learned the hard way during the years of building while bleeding.

VII. Modern Era: Bolt-on Strategy and Capital Discipline (2021-2025)

The Plains that emerged from the pandemic and the Oryx JV formation was a fundamentally different company than the one that had entered the 2010s. The growth-at-all-costs mentality that characterized the Armstrong consolidation era had been replaced by a disciplined, returns-focused approach under CEO Willie Chiang. Every acquisition had to clear hurdle rates. Every capital project needed long-term contracted support. The distribution would grow, but only after the balance sheet was right.

The new playbook showed up clearly in the string of bolt-on acquisitions that followed. In 2023, Plains acquired Diamondback Energy's forty-three percent interest in the OMOG joint venture for two hundred and twenty-five million dollars, consolidating another gathering system in the Permian. Then, in January 2025, the company announced three deals simultaneously: Ironwood Midstream Energy's Eagle Ford gathering system for four hundred and seventy-five million dollars, expanding Plains' footprint in the South Texas basin where it had historically been underweight; Medallion Midstream's Delaware Basin gathering business for a hundred and sixty million dollars through the Plains Oryx JV; and the remaining fifty percent of Midway Pipeline from CVR Energy for ninety million dollars, giving Plains full ownership and operational control of a Mid-Continent asset.

The January 2025 announcement also included a twenty-percent distribution increase and the repurchase of eighteen percent of PAA's outstanding Series A preferred units for three hundred and thirty million dollars — a capital structure optimization that reduced the preferred distribution burden and signaled confidence in the company's cash generation. The total net acquisition spend of roughly six hundred and seventy million dollars was funded from existing liquidity without meaningful leverage impact.

But the biggest deal of 2025 dwarfed the bolt-ons. In September, Plains announced the acquisition of a fifty-five percent interest in EPIC Crude Holdings from Diamondback Energy and Kinetik Holdings for approximately one billion five hundred and seventy million dollars, including assumed debt. Simultaneously, it arranged to acquire the remaining forty-five percent from an Ares Private Equity portfolio company for approximately one billion three hundred and thirty million dollars. The combined transaction, totaling roughly two billion nine hundred million dollars, gave Plains full ownership of the EPIC Crude Oil Pipeline — an eight-hundred-mile system running from the Permian Basin and Eagle Ford to Corpus Christi with more than six hundred thousand barrels per day of capacity and significant export infrastructure.

Plains rebranded the system as Cactus III, creating a formidable three-pipeline export corridor to the Gulf Coast: Cactus I (three hundred and ten miles, wholly owned), Cactus II (five hundred and seventy-five miles, seventy percent owned with Enbridge), and now Cactus III (eight hundred miles, fully owned and operated). Together, these systems provided redundant, high-capacity connectivity from the Permian wellhead to tidewater — the "wellhead to water" positioning that management had been articulating for years, now fully realized.

The 2025 financial results validated the strategy. Full-year adjusted EBITDA came in at two billion eight hundred and thirty-three million dollars, with distributable cash flow of approximately two billion sixty-three million dollars and a distribution coverage ratio of 1.72 times — meaning Plains generated nearly seventy-two percent more cash than it paid out, a dramatic improvement from the sub-1.0 coverage ratios of the mid-2010s.

Then came the move that completed the transformation. In June 2025, Plains announced the sale of substantially all of its Canadian NGL business to Keyera Corporation for approximately three billion seven hundred and fifty million dollars. Expected to close in the first quarter of 2026, the Keyera divestiture would strip away the natural gas liquids segment entirely, leaving Plains as the purest large-cap crude oil midstream operator in North America. Management projected approximately a hundred million dollars in annual cost savings from the simplified structure and guided to 2026 adjusted EBITDA of approximately two billion seven hundred and fifty million dollars, reflecting the loss of NGL contribution offset by growth in the core crude oil business and the Cactus III addition. The company also announced an annualized distribution of a dollar sixty-seven per unit, with a target of fifteen cents per unit annual increases going forward.

VIII. Business Model Deep Dive: The Midstream Advantage

To truly understand Plains, imagine the American crude oil supply chain as a river system. At the headwaters, thousands of individual oil wells produce crude in varying quantities and qualities. These wells connect to gathering systems — the creeks and streams of the network — small-diameter pipelines that collect crude from multiple well pads and funnel it to central collection points. From there, the crude flows into intra-basin transportation systems — the tributaries — that move it to storage hubs and pipeline interconnection points. Finally, long-haul transmission pipelines — the great rivers — carry the crude hundreds of miles to refineries on the Gulf Coast or export terminals where supertankers wait.

Plains operates across this entire river system. Its eighteen thousand three hundred and seventy miles of pipeline span gathering, intra-basin transportation, and long-haul transmission. Its seventy-five million barrels of crude oil storage capacity sit at critical nodes — Cushing, Oklahoma, the physical delivery point for the WTI benchmark crude contract, and St. James, Louisiana, the Gulf Coast pricing hub. When a producer in the Permian Basin needs to move crude from wellhead to export dock, Plains can often handle every link in that chain through its own integrated network. That is the network effect in action: the more producers and buyers that connect to the system, the more valuable each additional connection becomes for everyone.

The economic model rests on the distinction between fee-based and commodity-exposed revenue. In its early years, PAA earned a significant portion of its income from crude oil marketing and trading — buying barrels in one location, transporting them, and selling them at a higher price elsewhere. This activity generated attractive returns in good times but was inherently volatile, tied to crude oil price spreads and market dislocations. The 2020 collapse, when supply and logistics EBITDA fell ninety-nine percent in a single quarter, demonstrated just how dangerous commodity exposure could be.

Under Chiang's leadership, Plains has systematically shifted toward fee-based revenue underpinned by long-term contracts. The Plains Oryx JV, for example, operates under acreage dedication agreements with an average remaining tenor of approximately seven years, meaning producers have committed to ship all crude from their dedicated acreage through the JV's gathering systems for years into the future. Many of these contracts include minimum volume commitments — "take-or-pay" provisions that guarantee a baseline revenue stream even if actual production falls short. Built-in inflation adjustments ensure that tariff rates rise with the general price level over time.

This is the toll-road analogy made literal. A highway toll operator does not care whether the cars passing through are Hondas or Ferraris, or whether gasoline costs two dollars or five dollars per gallon. The operator cares about traffic volume and the toll rate. Plains' fee-based business works the same way: the company does not care whether crude oil costs forty dollars or a hundred dollars per barrel. It cares about how many barrels flow through its pipes and what tariff they pay. Post-Keyera divestiture, the company expects its business to be overwhelmingly crude oil-focused, with fee-based revenue comprising the vast majority of earnings.

The PAGP wrapper adds a layer of accessibility to this model. Because PAGP elected to be taxed as a corporation, its investors receive a simple 1099 form at tax time rather than the complex K-1 partnership schedule that PAA unitholders must navigate. For institutional investors — pension funds, endowments, sovereign wealth funds — and anyone holding shares in a retirement account, this distinction is not just convenience; it is a prerequisite. K-1s can generate unrelated business taxable income that subjects tax-exempt entities to actual tax liability, and they create filing obligations in every state where the MLP operates. PAGP eliminates all of those headaches while providing economically equivalent exposure to PAA's cash flows.

IX. Leadership & Culture: From Armstrong to Chiang

The leadership transition at Plains represented more than a change of personnel — it was a philosophical pivot that reshaped how the company allocates capital, communicates with investors, and thinks about its role in the energy landscape.

Greg Armstrong built Plains through the force of his personality and the clarity of his vision. Trained as an accountant, he approached dealmaking with the rigor of a financial analyst — never overpaying, always seeking incremental network value from each acquisition. His tenure produced an extraordinary track record: more than eighty acquisitions, billions in organic growth capital, and the transformation of a hundred-barrel-per-day exploration company into a continental infrastructure platform. But Armstrong's era was also defined by the distribution culture that prevailed across the MLP sector in the 2000s and early 2010s — a culture that prioritized distribution growth above nearly everything else, including balance sheet conservatism and capital investment in safety systems. The spills and the distribution cuts were, in some sense, the bill coming due for a decade of optimizing for yield.

Willie Chiang brought a different background and a different temperament. Where Armstrong was the accountant-turned-dealmaker, Chiang was the engineer-turned-operator. He spent the first three decades of his career inside major integrated oil companies — beginning with Chevron in 1981, the same year Armstrong joined Plains Resources, then moving to ConocoPhillips where he rose to senior vice president of refining, marketing, transportation, and commercial operations, and finally to Occidental Petroleum as executive vice president of operations. This career path gave Chiang something Armstrong did not have: the perspective of the customer. He understood how refineries consumed crude, what reliability meant to downstream operations, and why operational excellence was not just a safety imperative but a commercial advantage.

Chiang joined Plains' board as an independent director in 2015, was appointed COO in January 2018, and became CEO in October of that year when Armstrong retired. He assumed the chairmanship in January 2020 — just months before the pandemic tested his leadership in the most extreme way imaginable. His response to COVID-19 was characteristically operational: cut the distribution quickly and deeply, preserve cash, protect the balance sheet, and position for recovery. The fifty-percent cut in the spring of 2020 was agonizing for unitholders but prevented the kind of financial distress that claimed several other midstream operators.

The shift in midstream investor expectations under Chiang's watch has been profound. In the Armstrong era, the market rewarded distribution growth — the faster you grew the payout, the higher your unit price. By the time Chiang took over, investors had been burned so badly by distribution cuts across the MLP sector that the calculus had inverted entirely. What mattered now was distribution coverage — how much excess cash the company generated beyond what it paid out. Plains' current coverage ratio of 1.72 times represents a substantial cushion, meaning nearly half of distributable cash flow is retained for debt reduction, buybacks, or opportunistic investment. The company has also completed significant governance reforms, including the elimination of legacy director designation rights in 2021, further aligning its structure with modern corporate governance standards.

On the environmental front, Plains has invested significantly in pipeline integrity, monitoring systems, and spill prevention since the twin disasters of 2011 and 2015. The federal settlement following Santa Barbara required the implementation of safety improvements across the entire pipeline network, not just the California operations. While no pipeline operator can guarantee zero incidents, the operational posture has shifted meaningfully from the reactive approach that regulators criticized in the early 2010s.

X. Competitive Landscape & Industry Dynamics

The North American midstream sector is dominated by a handful of large-cap operators, each with distinctive competitive positioning. Understanding where Plains fits in this landscape requires examining the major players and the structural dynamics that govern their rivalry.

Enterprise Products Partners remains the gold standard. With 2024 adjusted EBITDA of approximately nine billion eight hundred million dollars — more than three and a half times Plains' figure — and a diversified portfolio spanning natural gas processing, NGL fractionation, crude oil transportation, and petrochemical services, Enterprise has never cut its distribution. Its balance sheet is among the strongest in the sector, with leverage consistently below three times. Enterprise is the company that every midstream operator aspires to emulate, and its track record creates a credibility gap that competitors must work to close.

Energy Transfer is the sprawling, debt-tolerant giant — the largest midstream company by EBITDA, with a trailing figure in the fourteen-to-sixteen-billion-dollar range and a bewilderingly complex corporate structure that includes natural gas, NGL, crude oil, and refined products operations across the country. Energy Transfer cut its distribution by fifty percent in 2020 and has rebuilt it, and its competitive overlap with Plains is primarily in crude oil pipelines in Texas and the Mid-Continent. ONEOK, historically a natural gas and NGL specialist, transformed itself through the 2023 acquisition of Magellan Midstream Partners and the 2024 acquisition of EnLink Midstream, becoming a diversified operator with expected 2025 EBITDA of approximately eight billion dollars. Kinder Morgan, meanwhile, is primarily a natural gas pipeline and storage operator whose crude oil exposure is limited.

Plains' competitive differentiation rests on three pillars. First, Permian Basin dominance: no competitor matches Plains' integrated gathering-to-export crude oil network in the Permian. The Plains Oryx JV's fifty-five hundred miles of intra-basin pipeline, combined with the Cactus I, Cactus II, and Cactus III long-haul systems, create a "wellhead to water" connectivity that would take a competitor decades and tens of billions of dollars to replicate from scratch. Second, crude oil specialization: following the Keyera NGL divestiture, Plains is the purest large-cap crude oil midstream operator in North America, offering investors a cleaner exposure than diversified peers. Third, commercial intelligence: PAA's longstanding crude oil marketing activities, while now a smaller portion of earnings, provide unmatched insight into crude oil flow dynamics, quality differentials, and logistical bottlenecks across the system.

The barriers to entry in midstream are formidable. Building a competing pipeline network requires securing right-of-way across hundreds of miles of privately owned land, obtaining state and federal regulatory permits that can take years, negotiating long-term contracts with producers who may already be committed to existing operators, and deploying billions of dollars in capital before earning a single dollar of revenue. Environmental scrutiny has intensified dramatically since Plains' own spill experiences, making new pipeline construction politically and legally challenging in many jurisdictions. These barriers protect incumbents but also limit their ability to expand through greenfield construction, which is why bolt-on acquisitions and joint ventures have become the preferred growth model.

The existential question hanging over the entire sector is the energy transition. How long will fossil fuel infrastructure remain relevant in a world moving toward electrification and renewable energy? The base-case scenarios from the International Energy Agency and most major forecasters project continued growth in global oil demand through the 2030s, driven primarily by petrochemicals, aviation, and developing-world transportation. But the tail risks are real: a faster-than-expected EV adoption curve, aggressive carbon pricing, or technological breakthroughs in battery storage could accelerate the timeline for peak oil demand. For Plains specifically, the crude oil concentration that is its strength could become its vulnerability if the crude oil demand outlook deteriorates faster than the natural gas outlook, since natural gas is widely viewed as a transitional bridge fuel with a longer demand runway.

XI. Structural Analysis: Porter's Five Forces

The most useful analytical lens for midstream infrastructure is Michael Porter's Five Forces framework, which evaluates an industry's profitability based on competitive dynamics.

The threat of new entrants is low — arguably the lowest of any major industry in the United States. Building a pipeline network that competes with Plains' Permian system would require securing rights-of-way across thousands of miles of private land, obtaining regulatory approvals from multiple state and federal agencies (a process that routinely takes three to five years per project), investing billions of dollars in steel, construction, and compression, and then convincing producers who have already dedicated their acreage to existing operators to switch. The environmental and political opposition to new pipeline construction has grown substantially over the past decade, adding further protection for incumbents. This is about as close to an impregnable barrier as exists in any industry.

The bargaining power of suppliers — in this context, the E&P producers whose crude oil flows through Plains' systems — is medium to high and represents the most significant competitive threat. Large producers like ExxonMobil, Chevron, and ConocoPhillips have enormous negotiating leverage, and the wave of E&P consolidation in recent years (Diamondback acquiring Endeavor Energy, ConocoPhillips merging with Marathon Oil) has increased producer concentration, giving fewer, larger companies more power to negotiate tariff reductions or build captive midstream infrastructure. Plains mitigates this through long-term take-or-pay contracts with an average remaining tenor of approximately seven years, but contract renewals remain a periodic risk.

Buyer power — from refiners and export terminal operators — is medium. Refiners have some optionality in sourcing crude, but in practice their choices are constrained by geography, crude quality requirements, and existing pipeline connections. Plains' strategic storage positions at Cushing and St. James, plus its export capacity at Corpus Christi, give it leverage with downstream buyers.

The threat of substitutes is moderate in the near term and potentially significant over the longer term. Rail and truck transport exist as alternatives to pipelines, but at substantially higher cost — typically three to five dollars per barrel more than pipeline tariffs for long-haul movements. The more meaningful substitute threat comes from the energy transition: if electric vehicles, efficiency improvements, and policy changes reduce long-term crude oil demand, pipeline utilization rates would fall and the entire business model would face structural pressure. This is the crucial temporal question for midstream investors.

Competitive rivalry among existing operators is medium-high but generally rational. The major midstream companies compete for new contracts and producer dedications, but the competitive dynamic in the Permian has generally been accommodative rather than predatory. The enormous capital requirements and long lead times for capacity additions prevent the kind of rapid competitive escalation that characterizes more asset-light industries. Competitors are differentiated by geography and customer relationships, and the industry has broadly shifted from growth-oriented strategies to returns-focused capital discipline.

XII. Hamilton Helmer's Seven Powers

Hamilton Helmer's Seven Powers framework, drawn from his influential strategy work, identifies the specific sources of durable competitive advantage. Applied to Plains, the analysis reveals a company with genuine power in several dimensions.

Scale economies are Plains' most obvious source of structural advantage. The Plains Oryx JV controls over four million dedicated acres of Permian Basin territory, and the fixed costs of operating this gathering network — maintenance crews, compression facilities, monitoring systems, right-of-way management — are spread across massive throughput volumes. A smaller competitor gathering thirty thousand barrels per day from a limited acreage position faces essentially the same per-mile operating costs as Plains gathering several hundred thousand barrels per day across its integrated system. The scale advantage compounds over time as Plains adds new well connections at marginal cost to an already-existing network.

Network economies are moderate to strong. Each new producer that connects to the Plains system adds value for every other participant by increasing the optionality and flexibility of the network. A producer connected to a gathering system that feeds into Cactus I, Cactus II, and Cactus III has three long-haul routes to the Gulf Coast, plus connections to Cushing-bound pipelines — optionality that a smaller, standalone gathering system cannot provide. This hub effect creates a gravitational pull that attracts additional volumes, reinforcing the cycle.

Switching costs are perhaps Plains' strongest single power. Multi-year take-or-pay contracts contractually bind producers to the system. But the switching costs go beyond the contractual: physically disconnecting from one gathering system and connecting to another requires capital expenditure, operational disruption, and the risk of transportation interruptions during the transition. Producers who have optimized their operations around Plains' system — including scheduling, quality management, and destination flexibility — face significant operational switching costs even when contracts expire. The approximately seven-year average remaining contract tenor provides extraordinary visibility by the standards of most industries.

Cornered resource is moderate to strong. The specific right-of-way positions, land access agreements, and regulatory permits that Plains holds across the Permian Basin represent assets that cannot be replicated through any amount of capital investment. You cannot build a pipeline across land to which you do not have legal access, and obtaining that access requires negotiations with thousands of individual landowners, each of whom can block or delay construction. Plains' decades of accumulated right-of-way positions, combined with its producer relationships and regulatory track record, constitute a resource base that no new entrant can quickly assemble.

Counter-positioning is weak — incumbents like Enterprise Products or Energy Transfer could, in theory, replicate Plains' crude oil focus — and branding is not a primary moat in this B2B context, though operational reputation matters. Process power is moderate: Plains has developed genuine expertise in integrating acquired pipeline assets, managing complex crude oil logistics across multiple basins, and operating the combined Plains Oryx system, but these capabilities, while valuable, are not insurmountable barriers.

The overall assessment: Plains' competitive moat is real but geographically concentrated. In the Permian Basin, the combination of scale, switching costs, network effects, and cornered resource creates a genuinely durable competitive position. Outside the Permian, the moat is narrower and more dependent on specific asset positions and customer relationships.

XIII. Bull vs. Bear Case

The bull case for Plains rests on the Permian Basin's continued centrality to global oil supply and Plains' unmatched infrastructure position within it. The Permian has multi-decade drilling inventory remaining, and the ongoing shift toward longer-lateral horizontal wells and improved completion techniques continues to drive per-well productivity gains. With the Cactus pipeline system providing three independent routes from the Permian to the Gulf Coast, Plains is positioned to capture growing export volumes as international crude demand — particularly from Asia — continues to expand. The company's shift to disciplined capital allocation under Chiang has produced robust distribution coverage, declining leverage, and a pathway to sustained distribution growth. The Keyera NGL divestiture simplifies the story and positions Plains as a pure-play crude oil infrastructure company — a relatively rare offering in the midstream sector that could attract a broader investor base and a potential valuation re-rating. Energy security concerns following the disruptions of 2022 have reinforced political support for U.S. oil production and export infrastructure, providing a policy tailwind that was absent a decade ago.

The bear case centers on the energy transition and Permian concentration risk. If electric vehicle adoption accelerates beyond current forecasts — and the pace of EV cost declines and battery technology improvement suggests this is at least plausible — global crude oil demand could plateau or begin declining within the next decade. Plains, with approximately sixty percent of its adjusted EBITDA derived from the Permian Basin, is essentially a leveraged bet on continued Permian production growth. If the basin's output plateaus as operators prioritize capital returns to shareholders over volume growth — a trend already underway among the major E&P companies — Plains' throughput volumes could stagnate. The company's three distribution cuts between 2016 and 2020 have created a permanent credibility deficit with some income-oriented investors, and the leverage ratio at 3.9 times (pro forma for the Cactus III acquisition, before Keyera proceeds) remains above the target range. Regulatory risk is ever-present: carbon pricing, methane regulations, and the increasing difficulty of permitting new pipeline construction could constrain growth. And the 2020 pandemic loss demonstrated that even a toll-road business can suffer catastrophically when traffic drops to zero.

The most important KPIs for tracking Plains' ongoing performance distill to two numbers that encapsulate both sides of this debate. The first is Permian Basin throughput volume — the actual barrels per day flowing through Plains' Permian gathering and transportation systems. This is the most direct measure of whether the company's core asset base is growing, stagnating, or declining, and it serves as an early warning indicator for both the bull and bear cases. The second is distribution coverage ratio — currently targeting at least 1.50 times — which captures the balance between returning cash to investors and retaining financial flexibility. As long as throughput volumes are growing and coverage remains robust, the investment thesis is intact. Any deterioration in either metric warrants immediate attention.

XIV. The PAGP/PAA Structure: Why Two Securities?

The existence of two publicly traded securities — PAA and PAGP — for what is essentially the same underlying business is one of the more unusual features of the Plains universe, and understanding it is critical for investors evaluating the opportunity.

PAA is the operating entity. It owns the pipelines, the storage tanks, the gathering systems, and the employee relationships. It generates the revenue, pays the expenses, and produces the distributable cash flow. But because PAA is a master limited partnership, its investors receive a Schedule K-1 at tax time — a document that reports each unitholder's share of the partnership's income, deductions, and credits. K-1s are complex, frequently arrive late (sometimes not until mid-April or later), can create filing obligations in multiple states where the MLP operates, and generate unrelated business taxable income that makes them problematic for tax-exempt institutional investors, retirement accounts, and foreign holders. These frictions are not trivial; they effectively exclude a substantial portion of the potential investor universe from owning PAA.

PAGP was created in 2013 specifically to solve this problem. Although organized as a limited partnership, PAGP elected to be taxed as a corporation, which means its investors receive a standard 1099 form — the same document they would get from owning shares of Apple or Johnson & Johnson. Each PAGP Class A share is economically linked to one PAA common unit through the ownership chain, and distributions per share are identical to distributions per PAA unit. The difference is purely administrative and tax-related, but it opens the door to pension funds, endowments, IRAs, and foreign investors who cannot or will not deal with K-1 complexity.

There is a meaningful tax nuance investors should be aware of. Historically, PAGP distributions were characterized as non-taxable return of capital to the extent of the investor's tax basis — a significant advantage that deferred tax liability until the shares were sold. However, the Keyera NGL divestiture announced in 2025 is expected to generate sufficient earnings and profits at the PAGP level that distributions payable in 2026 may be treated as taxable dividends rather than return of capital. This is a one-time acceleration, not a permanent change, but it alters the near-term tax calculus for existing holders.

The question of why Plains does not simply merge PAGP and PAA into a single corporate entity — as Kinder Morgan did in 2014 — is primarily one of tax efficiency and investor base preservation. A full merger would likely trigger tax consequences for existing PAA unitholders and could eliminate the tax advantages that attract certain investor constituencies to the MLP structure. Management has indicated openness to further simplification over time, and the Keyera divestiture's impact on PAGP's tax status may accelerate these conversations. For now, the dual structure persists, offering investors a choice between two functionally equivalent securities differentiated by their tax wrapper.

XV. What's Next: The 2025-2030 Horizon

Plains enters 2026 in the midst of the most consequential transformation in its history. The Keyera NGL divestiture, expected to close in the first quarter of 2026, will complete the company's evolution into a pure-play crude oil infrastructure operator. The approximately three billion dollars in net proceeds from the sale will be deployed toward debt reduction — bringing the leverage ratio back within the target range of 3.25 to 3.75 times — and potentially toward bolt-on acquisitions in the core crude oil business. Management has also indicated a potential one-time special distribution of approximately thirty-five cents per unit to help offset the tax implications of the sale for individual unitholders.

The near-term integration challenge is significant. Plains must absorb the Cactus III pipeline system, realize the projected synergies from operational optimization across its three-system export corridor, and complete the organizational restructuring that accompanies the NGL divestiture. The company has guided to approximately a hundred million dollars in annual cost savings through 2027 from the simplification, with roughly half expected to materialize in 2026. These savings come from eliminating redundant corporate overhead, consolidating field operations, and streamlining commercial functions that previously served both crude oil and NGL business lines.

The Permian Basin's production trajectory is the central variable. The basin's current output of approximately six million barrels per day represents a remarkable achievement, but the growth rate has moderated as operators prioritize free cash flow generation over production growth. Whether Permian production can continue climbing — perhaps reaching seven or eight million barrels per day by the end of the decade — or will plateau near current levels depends on oil prices, operator capital discipline, service-sector capacity, and the ongoing productivity of the Wolfcamp and Bone Spring formations. For Plains, the distinction matters enormously: growing production means growing throughput, growing tariff revenue, and a clear pathway to distribution increases. Flat production means Plains must compete more aggressively for market share or find growth in other basins.

Export infrastructure represents a significant opportunity. The Cactus pipeline corridor terminates at Corpus Christi, one of the fastest-growing crude oil export hubs in the world. As international demand for medium and light sweet crude continues to grow — driven by refinery expansions in India, China, and Southeast Asia — the value of wellhead-to-tidewater connectivity increases. The potential expansion of Cactus III capacity to nine hundred thousand barrels per day (with an associated earnout payment of a hundred and ninety-three million dollars if sanctioned before year-end 2027) would position Plains to capture a larger share of the growing export market.

The energy transition remains the horizon risk. Plains has not positioned itself as a leader in alternative energy infrastructure — carbon capture, hydrogen transport, or renewable fuels — and management has been transparent that the company's strategy is anchored in crude oil demand extending for decades. This is a calculated bet: if crude oil demand persists at or above current levels through the 2030s, Plains' infrastructure will generate enormous value. If the transition accelerates beyond base-case forecasts, the company's concentrated crude oil exposure becomes a liability. The possibility of a complete PAGP/PAA merger remains on the table, as does further industry consolidation — Plains could be either acquirer or target in a sector that continues to rationalize.

XVI. Lessons for Founders and Investors

The Plains story illuminates several principles that extend well beyond the energy sector.

Infrastructure endures when products and technologies do not. Plains Resources started as an exploration company — a business where the product literally depletes with every barrel extracted. Armstrong's genius was recognizing that the infrastructure moving that product was fundamentally more durable than the product itself. Pipelines built in the 1960s still operate today. Storage tanks constructed decades ago still hold crude. The lesson is applicable across industries: whenever a sector is characterized by rapidly changing products but stable distribution needs, the infrastructure layer often captures the most durable returns.

Complex structures eventually demand unwinding. The MLP model, with its IDRs, GP/LP conflicts, and K-1 tax complexity, was a brilliant innovation for its time — it channeled enormous capital into building America's energy infrastructure during the shale revolution. But structural complexity creates friction: it limits the investor base, creates governance conflicts, raises the cost of capital, and generates suspicion among investors who cannot fully understand the cash flow waterfall. Plains' multi-year simplification journey — eliminating IDRs, aligning GP and LP interests, creating the PAGP corporate wrapper, and eventually divesting non-core businesses — is a case study in the inevitable gravitational pull toward structural clarity.

Cutting payouts early preserves long-term credibility. Plains' three distribution cuts were individually painful and collectively devastating to its reputation among income investors. But the alternative — maintaining unsustainable payouts until the balance sheet broke — would have been far worse. Companies that cut dividends or distributions proactively, when they still have financial flexibility, preserve their ability to recover. Companies that wait until they are forced to cut by lenders or liquidity crises often never recover their standing with investors.

Geography is destiny. Plains' decision to concentrate its infrastructure in the Permian Basin was the single most important strategic choice in the company's history. When the shale revolution transformed the Permian into the most productive oil field on Earth, Plains' decades of accumulated gathering infrastructure, producer relationships, and right-of-way positions became extraordinarily valuable. A similar infrastructure investment in a basin that underperformed — the Bakken, for instance, or the Utica — would have generated far inferior returns. For investors evaluating infrastructure companies, understanding the quality and longevity of the geographic resource they serve is paramount.

Joint ventures offer a capital-efficient growth model. The Plains Oryx JV demonstrated that growth does not require dilution or leverage — it can come from combining complementary assets in structures that create value through scale and synergy. This model has become increasingly popular across the midstream sector as operators seek to grow without repeating the balance sheet mistakes of the 2010s.

XVII. Epilogue: The Midstream Endgame

Plains GP Holdings, as it exists today, is both a monument to forty-five years of energy infrastructure building and a bet on the future of crude oil in the American economy. The company that began as a hundred-barrel-per-day exploration outfit in the Permian Basin has become the dominant crude oil gatherer in that basin, the operator of three major export pipelines to the Gulf Coast, and the holder of strategic storage positions at the most important crude oil hubs in North America.

The midstream sector as a whole stands at an inflection point. The wave of MLP simplifications, corporate conversions, and distribution resets that characterized the late 2010s and early 2020s has largely run its course. What remains is a smaller, more disciplined group of large-cap operators generating robust free cash flow, returning capital to investors, and growing selectively through bolt-on acquisitions and joint ventures. Whether this mature, returns-focused model can persist — or whether the energy transition will ultimately strand these assets — is the defining question for the sector over the coming decades.

The most surprising aspect of the Plains story is not any single acquisition or crisis, but the arc from complexity to simplicity. A company that began as an upstream operator became a midstream consolidator, created a GP holding company with IDRs, built a dual-listed security structure, expanded into NGL operations across two countries, suffered catastrophic operational failures, cut distributions three times, and then systematically unwound every layer of complexity until what remained was a focused crude oil infrastructure business with a clean balance sheet and a clear strategy. That arc — from ambition to overreach to discipline — is not unique to Plains. It is the arc of the entire North American midstream sector, compressed into a single company's journey.

The infrastructure that Plains has built — the pipes buried under the desert, the tanks standing sentinel at Cushing and Corpus Christi, the gathering lines snaking across the Delaware Basin — will outlast every executive, every analyst report, and every market cycle. Whether the crude oil flowing through them represents a growth business or a sunset industry is a question that only time can answer. What is certain is that for as long as the world burns oil, someone will need to move it. And in the Permian Basin, that someone is, overwhelmingly, Plains.

XVIII. Further Reading and Resources

For those looking to go deeper on Plains All American, the Permian Basin, and the midstream energy sector, the following resources provide excellent starting points.

The Plains All American Investor Relations site at ir.plains.com contains annual reports, quarterly earnings presentations, and the detailed segment disclosures that reveal how the company's crude oil and NGL businesses perform independently. The 2016 Simplification Transaction proxy statement, available through SEC filings, provides an unusually detailed look at the economics of IDR elimination and GP/LP alignment.

RBN Energy's Permian Basin Pipeline Analysis Series offers granular, pipeline-by-pipeline coverage of the takeaway capacity build-out that has defined Permian midstream over the past decade. The Energy Infrastructure Council (eic.energy) provides educational materials on MLP structures that help investors understand the tax and governance complexities of entities like PAA and PAGP. East Daley Analytics publishes detailed midstream industry reports that benchmark Plains against peers on metrics including throughput growth, leverage, and distribution sustainability.

The EIA's Drilling Productivity Reports track Permian Basin production and rig counts — the fundamental drivers of Plains' throughput volumes. The IEA's annual World Energy Outlook provides the long-range demand scenarios that frame the energy transition risk facing the entire crude oil value chain. For pipeline safety and regulatory context, the Pipeline and Hazardous Materials Safety Administration (PHMSA) publishes incident data and enforcement actions.

Several books provide valuable context for understanding the broader energy landscape. Russell Gold's "The Boom" chronicles the shale revolution that transformed the Permian. Gregory Zuckerman's "The Frackers" profiles the entrepreneurs who pioneered horizontal drilling and hydraulic fracturing. Daniel Yergin's "The New Map" examines the geopolitical implications of America's emergence as an energy exporter. And Vaclav Smil's "Energy and Civilization" provides the long-historical perspective on how energy systems evolve — a useful corrective for anyone tempted to predict too-rapid a transition away from fossil fuels.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube