Occidental Petroleum: From Wildcatter to Carbon Pioneer

I. Introduction & Episode Roadmap

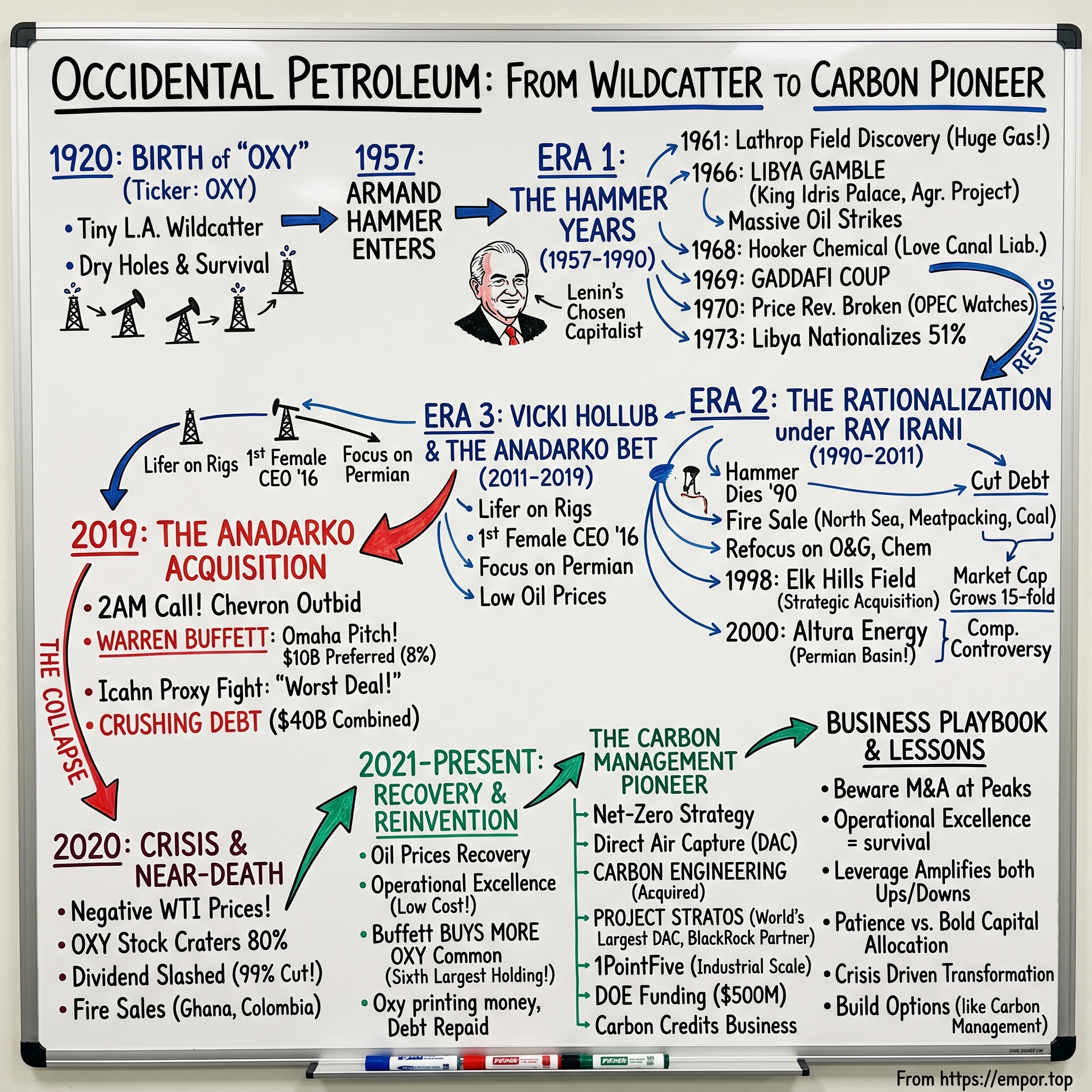

Picture this: It's May 2019, and Vicki Hollub is about to make the biggest bet in Occidental Petroleum's 99-year history. She's sitting across from Warren Buffett in Omaha, asking the Oracle for $10 billion to outbid Chevron—a company five times Occidental's size—for Anadarko Petroleum. The stakes? Control of the Permian Basin, America's oil heartland. The risk? Everything. Within a year, oil prices would turn negative for the first time in history, and Occidental's stock would crater 80%. Yet today, that same company is Buffett's sixth-largest holding, and Hollub is being hailed as both a visionary and a survivor.

How did we get here? How did a company that started as a nearly bankrupt California wildcatter in 1920 become a $50 billion oil major? How did it survive being run by Armand Hammer—a man who literally did business with Lenin and called himself a "communist capitalist"? And perhaps most intriguingly, how is this century-old oil company positioning itself as a leader in carbon capture technology?

This is the story of transformation, survival, and reinvention. It's about making massive bets at exactly the wrong time—and somehow living to tell the tale. It's about how operational excellence can save you when financial engineering nearly kills you. And it's about what happens when an industry facing existential questions about its future decides to rewrite its own narrative.

We'll journey through four distinct eras: the Armand Hammer years, where personal relationships with dictators mattered more than drilling technology; the rationalization under Ray Irani, who stripped away Hammer's empire-building to focus on oil and gas; the Vicki Hollub era, marked by the Anadarko gamble that nearly destroyed the company; and finally, the emerging carbon management story that might define Occidental's next century.

Along the way, we'll unpack business lessons that transcend the energy sector: when transformational M&A works (and when it spectacularly doesn't), how to manage commodity cycles with leverage, and why sometimes the best investment opportunities come from companies that nearly died. Because if there's one thing Occidental's history teaches us, it's that in the oil business, you're either drilling or dying—and sometimes you're doing both at once.

II. Origins & The Pre-Hammer Years (1920–1957)

The Los Angeles of 1920 was a city built on oil before it became synonymous with Hollywood. Derricks dotted the landscape from Signal Hill to Venice Beach, and the air hung thick with the smell of crude. It was here, amid the chaos of California's second great oil boom, that Occidental Petroleum Corporation was born—not with grand ambitions of global dominance, but as just another wildcatter trying to strike it rich in the shadows of Standard Oil's empire.

Founded with minimal capital and maximum hope, Occidental spent its first 37 years as what one contemporary described as "a corporate orphan"—perpetually undercapitalized, drilling dry holes more often than gushers, and surviving on the financial equivalent of fumes. The company's early shareholders were mostly small-time Los Angeles investors who viewed oil exploration like a sophisticated form of gambling. They weren't entirely wrong. The California oil scene in the 1920s was America's answer to a gold rush, except the treasure was black and buried thousands of feet underground. Founded in 1920 in Los Angeles, Occidental Petroleum was for many years a small, largely unprofitable driller. Unlike the majors who had established fields and steady production, Occidental represented the wildcatter's dream—and often, the wildcatter's nightmare.

The company's early shareholders were a colorful mix of Los Angeles dentists, real estate speculators, and small-time investors who treated oil exploration like a high-stakes poker game. They'd gather in downtown LA offices, poring over geological surveys that were more guesswork than science, debating whether to drill another thousand feet or cut their losses. Its early years as an oil-finding entity were largely undistinguished, with the company almost bankrupt by the mid-1950s.

What made Occidental particularly vulnerable was its complete lack of integration. While Standard Oil's descendants controlled everything from wellhead to gas pump, Occidental was purely an upstream player—and not a particularly successful one. The company would drill, hope for oil, and when they found it (which wasn't often), they'd immediately have to negotiate with pipeline companies and refiners who knew exactly how desperate they were for cash flow.

By the 1940s, Occidental had become what industry insiders called a "zombie company"—technically alive but functionally irrelevant. Its market capitalization was so low that its primary value wasn't its oil reserves or drilling equipment, but rather its accumulated tax losses. It was precisely its bleak prospects that first attracted the attention of Armand Hammer, a successful international businessman who hoped to use the ailing company as a tax shelter.

The irony wasn't lost on observers: a company named "Occidental" (meaning Western) was about to be taken over by a man whose fortune came from trading with the Soviet East. But in the oil business of the 1950s, stranger things had happened. The stage was set for one of the most unlikely corporate transformations in American business history—a transformation that would turn a tax shelter into a global energy empire.

III. Enter Armand Hammer: The Communist Capitalist (1957–1990)

The scene: a luxury suite at Moscow's Savoy Hotel, October 1921. A 23-year-old American medical school graduate sits across from Vladimir Lenin, leader of the world's first communist state. Between them lies an improbable proposition—that this son of a socialist revolutionary, who claims to have come to Russia with medical supplies for typhus victims, should become capitalism's ambassador to communism. According to Hammer, on his initial trip, he took $60,000 in medical supplies to aid in a typhus epidemic and made a deal with Lenin for furs, caviar, and jewelry expropriated by the Soviet state in exchange for a million bushels (27,216 tons) shipment of surplus American wheat.

"If he had ordered me to jump out of the window I'd have probably done so," Hammer would later recall of meeting Lenin. The charisma was real, but so was the calculation on both sides. "It's just fortunate that I was there at a time when Lenin was disillusioned with communism," Dr. Hammer recalled of those early days in Russia. "He told me that communism wasn't working and that was why he adopted the New Economic Policy, opening up private trade and giving concessions to foreigners to come and do business with Russia. He said to me, 'Why don't you come in and be the first? What we need is businessmen like you. You can have any concession you like.'"

This was Armand Hammer—the most unlikely oil executive in history. Armand Hammer (May 21, 1898 – December 10, 1990) was an American businessman and philanthropist. The son of a Russian Empire-born communist activist, Hammer trained as a physician before beginning his career in trade with the newly established Soviet Union. His father, Julius, had helped found the Communist Party USA and done time in Sing Sing for performing an illegal abortion that killed a patient. The younger Hammer inherited his father's connections to the Soviet apparatus but none of his ideological fervor. In 1956, when Hammer retired to California at age 58, having made millions from whiskey distilling and various ventures, he was looking for a tax write-off. A friend persuaded him to finance two wildcat oil wells being drilled in Bakersfield, California, by Occidental Petroleum Corporation, which was near bankruptcy. With Hammer's financial support, Occidental began drilling the wells. Unexpectedly, the wells struck oil. In 1956 Hammer and his wife Frances each invested $50,000 in two oil wells that Occidental planned to drill in California. At the time Hammer became involved with Occidental, the company was listed on very small stock exchanges on the West Coast; within several years, however, Oxy was on the American Stock Exchange, boosted by the 1959 Hammer-led acquisition of Gene Reid Drilling Company of Bakersfield, California.

At Hammer's first association with Occidental, the company was run by Dave Harris, Roy Roberts, and John Sullivan. Hammer's increased involvement, his strong personality, and his ability to raise money for oil drilling propelled him more and more into the limelight. By July 1957 Hammer had become company president. The net worth of the company increased from $175,000 in 1957 to $300 million in 1967.

But it was what happened next that transformed both Hammer and Occidental. Hammer thereupon acquired another drilling company, and in 1961 Occidental struck a huge natural gas deposit near Stockton in northern California. The Lathrop field discovery was Hammer's first major gamble, and it paid off spectacularly. In 1961 while working with Occidental employees Richard Vaughn, Robert Teitsworth, and the Reids, Hammer took a chance on drilling the Lathrop field, near San Francisco. It had been drilled previously for natural gas by Texaco and other companies, but only to a depth of about 5,600 feet. Reid and the others suggested that there was gas farther down, and at 6,900 feet they were proven correct. Occidental made one of the largest gas finds in California. Over the course of one night, the company found gas worth hundreds of millions of dollars.

By the end of 1961, Occidental was reporting a $1 million profit on revenues of over $4 million. Occidental has been publicly traded on the New York Stock Exchange since 1964.

Hammer's management style was autocratic, theatrical, and utterly unconventional. "Few Fortune 500 corporations have come so totally under the sway of one person, especially one who owned such a tiny percentage of stock." He would convene board meetings at midnight, negotiate billion-dollar deals from his private jet, and maintained a web of relationships that stretched from the Kremlin to the White House. He spent the next 33 years as chief executive officer and chairman of the company, overseeing its growth to become one of the largest companies in the U.S. Called "Lenin's chosen capitalist" by the press, he was also known for his art collection and his close ties to the Soviet Union.

The diversification strategy Hammer pursued was partly defensive—making Occidental too big to be swallowed by the oil majors—and partly opportunistic. From his earliest days as president of Occidental, one of Hammer's overriding drives was for Oxy to diversify. In his autobiography, Hammer reported that a prime rationale for diversifying was to make Oxy too big for the other major oil companies to take over. Acquisitions included energy and chemical companies, as well as meat-producing operations.

In 1968, Hammer made one of his most controversial acquisitions: Hooker Chemical Company, which would later become infamous for the Love Canal disaster. Occidental enters the chemical business with the acquisition of Hooker Chemicals. The deal made sense strategically—chemicals and oil were natural complements—but it would haunt the company for decades with environmental liabilities.

Occidental acquires Iowa Beef Packers, the largest meatpacker in the United States. This 1981 acquisition for $750 million seemed bizarre for an oil company, but Hammer saw synergies others missed. He would sell it six years later for nearly a billion dollars, pocketing a tidy profit while his critics scratched their heads.

By the time Hammer died in 1990 at age 92, still serving as CEO and chairman, he had transformed a $175,000 company into one worth billions. But his greatest coup—and the one that would define Occidental's trajectory—had come decades earlier in the deserts of Libya.

IV. The Libya Gamble That Changed Everything (1965–1986)

The scene opens in Tripoli, February 1966. Armand Hammer sits in King Idris's palace, watching other oil executives file out empty-handed. The Arabian oil industry at that time was the bastion of the so-called Seven Sisters cartel, consisting of Standard Oil of New York, Standard Oil of California, Standard Oil of New Jersey, Rockefeller Holding, Gulf Oil, Texaco, and Anglo-Persian Oil. Libya, with only one million people, an impoverished economy, and a vast desert waste-land, was a no-man's-land among petroleum speculators.

But Hammer saw opportunity where others saw only sand. Occidental did acquire a concession, in part because its bid involved a proposal to invest five percent of its profits in an agricultural project in Libya. This wasn't just drilling rights—it was classic Hammer, offering to build water wells for the King's parched ancestral village, promising agricultural development, and essentially buying goodwill with future profits that didn't yet exist.

Soon after the award of its concession in 1966, on land handed back by Oasis and Mobil, Occidental had survey teams operating and within six months had drilled its first well. In November of 1966 Occidental had brought in a fifteen thousand barrel per day well and in early 1967 had discovered a new oil field. The speed was breathtaking—from concession to production in less than a year, on acreage that Mobil and Oasis had abandoned as worthless.

By the end of April of 1967 the Occidental oil well on that field were producing sixty thousand barrels per day. In May of 1967 Occidental brought in a well on a new field that produced forty thousand barrels per day. In 1966 Oxy's potential skyrocketed, with a billion-barrel oil field find in Libya. The find was "vintage" Hammer, as he wined and dined important Libyan officials, and then took a risk on land previously drilled by others. The Libyan oil finds established Oxy as one of the largest petroleum companies in the world.

The numbers were staggering. When Occidental Petroleum Corporation was reorganized in 1959, its total oil production was some 100 barrels per day. By the time Moammar Gaddaffi nationalized the industry in 1969, Oxy Libya, the wholly owned subsidiary, was producing 800,000 barrels per day. Such an amount made Oxy Libya the eighth largest producer in the world. In a decade, Occidental had gone from producing less oil than a single Texas stripper well to pumping more crude than most nations.

From early 1967 until November of that same year, Oxy's stock doubled in value to more than $100 a share. Wall Street couldn't believe what it was seeing—a company that had been worth practically nothing was suddenly one of the hottest stocks on the exchange.

But Hammer's real genius wasn't finding the oil—it was keeping it when the world changed around him. Hammer's skills as a negotiator were put to the test when the Libyan king was overthrown in a bloodless coup in 1969 and replaced by the Revolutionary Command Council, soon to be headed by Moammar Khadafi. Many analysts feared the new government would nationalize the oil fields; however, Hammer negotiated in late 1970 an agreement by which Libya received an immediate increase of 30C per barrel of oil, with another ten-cent increase spread over five years.

This deal changed everything—not just for Occidental, but for the entire global oil market. The government of Muammar al-Qaddafi, who took over Libya in a bloodless coup in 1969, ordered Occidental to cut back production for refusing to agree to higher oil prices. Within three months, Hammer agreed to pay 30 cents more per barrel as well as a higher rate of taxes. Other companies followed his lead, touching off the oil price revolution of the early 1970s.

Hammer had inadvertently broken the Seven Sisters' grip on oil pricing. By capitulating to Qaddafi's demands, he showed every oil-producing nation that the majors could be pushed around. OPEC watched, learned, and within years would quadruple oil prices globally. Occidental had become the mouse that roared—and taught the lions they weren't invincible.

The relationship with Libya grew increasingly complex through the 1970s. In August 1973, Libya nationalized 51% of Occidental's assets in the country. In February 1974, the company announced a 35-year oil exploration agreement with Libya. 81% of the oil extracted by Occidental Petroleum was to go to the Libyan government, with 19% retained by Occidental Petroleum. Most companies would have walked away from such terms. Hammer stayed, calculating that 19% of Libyan oil was worth more than 100% of nothing.

In 1965, Occidental won exploration rights in Libya, where it operated until 1986 when United States economic sanctions led to the suspension of activities. For two decades, Libya had been Occidental's golden goose, transforming it from a minor player into a major international oil company. The sanctions meant walking away from fields that had defined the company's identity.

The Libya gamble had made Occidental, nearly destroyed it when Qaddafi took power, then sustained it through the 1970s oil crisis. It proved Hammer's fundamental insight: in the oil business, political relationships mattered as much as geology. You could find all the oil in the world, but if you couldn't navigate the politics, you'd never pump a barrel.

More importantly, the Libya experience taught Occidental a lesson it would never forget: geographic concentration was dangerous, no matter how profitable. The company that had bet everything on Libya would spend the next decades diversifying furiously—into chemicals, into North Sea oil, into U.S. properties. They'd learned that in the oil business, the biggest risk wasn't dry holes—it was putting all your wells in one country.

V. From Hammer to Modern Era: The Irani Years (1990–2011)

December 10, 1990. The day the music died at Occidental Petroleum. Armand Hammer, who had ruled the company with an iron fist for 33 years, passed away at 92, still clutching the CEO title he refused to relinquish. Wall Street held its breath. What would happen to a company so thoroughly dominated by one man's personality that some analysts couldn't separate Occidental from Hammer himself?

Enter Ray R. Irani—a Lebanese-born chemical engineer who spoke fluent Arabic and held 50 patents, but whose real talent was surviving in Hammer's shadow. According to Forbes.com, during his early years, he worked with Occidental CEO Armand Hammer, who at age 91, named Irani his successor in February 1990. Irani was brought to Occidental in 1983 to help its struggling chemicals division, and soon was promoted to president, replacing a series of presidents fired by Hammer.

The company Irani inherited was a financial disaster masquerading as an oil major. Occidental was carrying massive debt from Hammer's empire-building—the Cities Service acquisition alone had cost $4 billion. The stock was yielding 10% like a junk bond because the company couldn't cover its dividend from operating earnings. Occidental Petroleum Corp. is headed for a sweeping restructuring under Ray R. Irani, newly installed as chairman, president, and chief executive officer. Formerly president and chief operating officer, Irani was named to his new posts upon the death last month of Armand Hammer, Oxy chairman and CEO for 33 years.

Irani's first moves were surgical, almost ruthless in their precision. Irani said the restructuring program will focus on Oxy's strengths in oil, gas, and chemicals and establishment of a more prudent debt policy. The program will slash long term debt by 40% and significantly improve the company's liquidity. During his 20-year tenure, Irani reduced the company's debt burden and refocused its operations on profitable oil and gas production.

The asset fire sale was spectacular in scope. Occidental's interests in meatpacking, agricultural products, coal mining, the North Sea, and gas pipelines acquired from… were all put on the block. Businesses earmarked for sale to cut costs and reduce losses include interests in the An Tai Bao coal mine joint venture in China, oil shale research and development, cattle and horse breeding, land and hotel development, film production, and hybrid seed research and development. Everything Hammer had accumulated in his conglomerate-building frenzy—gone.

The North Sea assets, which Hammer had fought so hard to acquire, went to Elf Aquitaine for $1.35 billion cash. The pipeline assets acquired from Midcon were sold. Iowa Beef Packers, which Hammer had inexplicably bought for $750 million, was divested. It was corporate liposuction on an unprecedented scale. But Irani wasn't just selling—he was repositioning. In 1998, the U.S. government sold the Elk Hills Oil Field to Occidental for $3.65 billion after an auction process that involved selling the field in segments and offering it to multiple bidders. The U.S. Energy Department plans to sell its 78% interest in Elk Hills field, 15 miles west of Bakersfield, Calif., to Occidental Petroleum Corp. for $3.65 billion in cash. DOE said the sale would be the largest privatization in the history of the U.S. government.

The deal was vintage Irani—strategic, calculated, and transformational. In 1998 the company bought huge natural gas deposits in the Elk Hills Field of southern California (formerly part of the U.S. government's Strategic Petroleum Reserve), and in 2000 it bought Altura Energy, Ltd., a company with reserves in the Permian Basin of Texas and New Mexico. Occidental said the purchase of Elk Hills reserves will triple its U.S. oil reserves and more than double its U.S. gas reserves. Its total worldwide oil and natural gas reserves will increase by about 75% to 2.3 billion boe.

In 2000, Irani made another critical move, acquiring Altura Energy for $3.6 billion. The purchase of Altura Energy, Ltd., in the Permian Basin of West Texas and southeast New Mexico made Occidental the largest oil producer in Texas. The acquisition also added substantially to Occidental's debt, which exceeded $6 billion by the end of 2000. But this wasn't Hammer's reckless debt—it was strategic leverage backed by proven reserves in America's most prolific basin.

Irani's management style was the antithesis of Hammer's theatrical approach. Where Hammer convened midnight board meetings, Irani ran quarterly earnings calls. Where Hammer flew to Moscow to negotiate with commissars, Irani focused on drilling efficiency and return on capital. Dr. Irani was a graduate of American University in Beirut, Lebanon. He spoke fluent Arabic and was personally acquainted with many Middle Eastern rulers. But he used these connections for business, not spectacle.

The results spoke for themselves. By the time he left Occidental in 2011, he had increased Occidental's market capitalization 15-fold to more than $80 billion. Occidental justified the compensation by pointing to the stock price, which had risen from $9 a share when Irani succeeded Hammer to $48.60 at the end of 2006, and to the company's market capitalization, which grew from $32.1 billion at the end of 2005 to $42.5 billion at the end of 2006.

Yet Irani's tenure wasn't without controversy. His compensation became a lightning rod for corporate governance activists. In 2006, after a rise in oil prices, Irani earned a total of $460 million. Irani's salary was considered excessive and not truly performance based for decades by a number of corporate governance authorities who noted that Irani's compensation had exceeded that of the head of energy giant ExxonMobil, Rex Tillerson, who led a company that has a market cap that was five times larger than Occidental Petroleum.

When U.S. sanctions against Libya were lifted in the spring of 2004, Irani sent a negotiating team back to the country that had delivered one of Hammer's greatest successes. In January 2005, Libya awarded its first batch of 15 exploration sites—with nine going to Occidental. "That's not a bad batting average," Irani said in an interview. "I was pleasantly surprised."

Irani retired as CEO on May 10, 2011, after the California State Teachers' Retirement System and Relational Investors, two major institutional Occidental Investors, objected to the company's compensation policies and announced plans to replace long-term board members who were described as "ossified" in a letter written in protest of Irani's salary. Irani was succeeded by Stephen I. Chazen in 2011.

The Irani era had transformed Occidental from Hammer's personal fiefdom into a disciplined, focused energy company. Gone were the meatpacking plants and art collections. In their place was a company with premier positions in California and Texas, generating reliable cash flows from some of America's best oil and gas assets. But the company was about to enter its most dramatic chapter yet, under the leadership of its first female CEO.

VI. The Vicki Hollub Era Begins (2011–2019)

The scene: A drilling platform in rural Mississippi, 1981. A 21-year-old mineral engineering graduate from Alabama climbs the rig stairs, hard hat slightly askew, steel-toed boots clanging on metal grating. The roughnecks eye her skeptically—women on rigs were rarer than dry holes back then. Thirty-five years later, that young engineer would become the first woman to run a major American oil company.

Vicki Hollub's path to the CEO suite wasn't preordained by an Ivy League MBA or family connections. Initially working on oil rigs in Mississippi, Hollub started her career in 1981 with Cities Service, when it was a fully integrated oil and gas company. Cities Service was acquired by Occidental Petroleum Corporation in 1982. She subsequently held technical and management positions for Occidental in the United States, Russia, Venezuela, and Ecuador. She was, in industry parlance, a "lifer"—someone who'd spent their entire career at one company, working their way up from the field to the corner office.

When Stephen Chazen announced his retirement in 2015, the board faced a choice: bring in an outsider with a fresh perspective, or promote from within. In May 2015, Occidental's board of directors selected Hollub to succeed retiring chief executive officer (CEO) Stephen Chazen, basing their decision on Hollub's "strong track record of successfully growing [Occidental's] domestic oil and gas business profitably and efficiently."

Hollub officially became president and CEO of Occidental Petroleum in April 2016, with responsibility for operations, strategy and financial management. The appointment made her the first woman to head a major American oil company, and that year Fortune named her #32 on its annual list of the Most Powerful Women in business. But the timing couldn't have been worse. Hollub was appointed CEO during a severe downturn in the oil industry. Oil prices had crashed from over $100 per barrel in 2014 to below $30 in early 2016.

Under Hollub, Occidental cut production costs in response to falling crude prices but decided not to lay off employees. While competitors were slashing headcount, Hollub took a different approach. She focused on operational efficiency, wringing more oil from existing wells rather than drilling new ones. The company focused on existing core operations in the Middle East, the United States, and Colombia in Latin America, while continuing to sell low-yield fields.

But Hollub's real focus was the Permian Basin. Hollub placed "particular emphasis" on developing the Permian Basin in the southern United States, which had been a consistent driver of profits. Half of Occidental's output was coming from the Permian Basin by July 2017, while the other half came from Qatar, Oman, the United Arab Emirates and Colombia. The Permian wasn't just another oil field to Hollub—it was the future of American energy, a massive sedimentary basin where technology was unlocking oil that had been considered unrecoverable just years earlier.

At that time, Forbes wrote that Hollub's focus on high-producing oil fields had made Occidental "leaner" and "poised to gusher cash for the next half-century." The company was generating strong cash flows, reducing debt, and building a reputation for operational excellence. Wall Street was impressed. The stock price recovered from its 2016 lows, and analysts praised Hollub's disciplined approach. But beneath the operational excellence, Hollub was nurturing a vision that would have seemed heretical in Hammer's day—transforming an oil company into a carbon management company. Occidental has been working with Carbon Engineering on direct air capture (DAC) deployment since 2019. Acquiring Carbon Engineering aligns with Occidental's integrated net-zero strategy and provides Occidental, through its 1PointFive subsidiary, the opportunity to rapidly advance DAC technology breakthroughs and accelerate deployment of DAC as a large-scale, cost effective, global carbon removal solution.

The 1PointFive initiative wasn't just greenwashing—it was a fundamental rethinking of what an oil company could be. Oxy's subsidiary 1PointFive is developing Carbon Engineering's Direct Air Capture (DAC) technology at an industrial scale. 1PointFive's goal is to deliver solutions that help curb global temperature rise to 1.5°C by developing DAC facilities and sequestration hubs to capture and store CO2 captured from the atmosphere and from industrial facilities.

The scale of ambition was breathtaking. 1PointFive has announced a scenario of deploying 70 DAC facilities by 2035, each with an expected capacity of up to 1 million tonnes per year, under current policy and voluntary and compliance market scenarios. The company estimates that up to 135 DAC facilities could be deployed with an increase in global policy initiatives and demand in the voluntary market.

Hollub was positioning Occidental not just to survive the energy transition, but to lead it. "Large-scale direct air capture is one of the most important technologies that will help organizations and society achieve their net-zero goals," Hollub said in the Sept 12. release. This wasn't the language of a traditional oil executive—it was the language of transformation.

The STRATOS project exemplified this vision. Occidental announced today that BlackRock will invest $550 million on behalf of clients in the development of STRATOS, the world's largest Direct Air Capture (DAC) facility, in Ector County, Texas. Through a fund managed by its Diversified Infrastructure business, BlackRock has signed a definitive agreement to form a joint venture with Occidental through its subsidiary 1PointFive that will own STRATOS. STRATOS is designed to capture up to 500,000 tonnes of CO2 per year. Construction activities for STRATOS are approximately 30 percent complete and the facility is expected to be commercially operational in mid-2025.

The fact that BlackRock—the world's largest asset manager—was investing heavily in Occidental's carbon capture projects signaled something profound: the financial markets were beginning to see carbon management not as a cost center, but as a business opportunity. "We are excited to partner with BlackRock on this transformative facility that will provide a solution to help the world reach net zero," said Vicki Hollub, President and CEO, Occidental. "BlackRock is proud to partner with global energy leader Occidental to help build the world's largest direct air carbon capture facility in Texas," said Larry Fink, Chairman and CEO, BlackRock. "Occidental's technical expertise brings unprecedented scale to this cutting-edge decarbonization technology. STRATOS represents an incredible investment opportunity for BlackRock's clients to invest in this unique energy infrastructure project and underscores the critical role of American energy companies in climate technology innovation."

But as 2019 approached, Hollub faced a decision that would define her legacy: whether to make the biggest acquisition in Occidental's history. The Permian Basin was consolidating, and Anadarko Petroleum—with its premier acreage adjacent to Occidental's—was in play. Chevron had already made a bid. For Hollub, it was now or never. The disciplined operator was about to become the biggest gambler in the oil patch.

VII. The Anadarko Acquisition: Triumph or Disaster? (2019)

The phone call came at 2 AM on a Tuesday in April 2019. Anadarko's board had accepted Chevron's $33 billion offer. For most CEOs, that would have been game over. But Vicki Hollub wasn't most CEOs. Within hours, she was on a plane to Omaha.

Warren Buffett later described the meeting as one of the most remarkable pitches he'd ever heard. Hollub didn't just want to buy Anadarko—she wanted to fundamentally reshape the American oil industry. She laid out maps of the Permian Basin showing how Occidental's acreage and Anadarko's fit together like puzzle pieces, creating the most dominant position in America's most prolific oil field. She explained how operational synergies could generate billions in value. Most importantly, she convinced him that she could execute.

In 2019, Occidental Petroleum acquired Anadarko Petroleum and assumed its debt. Hollub was a major proponent of the deal, and personally enlisted financing from Warren Buffett in order to complete it. The Berkshire Hathaway chairman agreed to invest $10 billion—not in common stock, but in preferred shares paying 8% annually, with warrants to buy Occidental stock at $62.50 per share.

The revised offer was audacious: $76 per share, offering 78% cash and 22% stock—a massive premium to Chevron's $65 per share bid. Chevron, five times Occidental's size, could have easily topped it. But they didn't. They walked away with a $1 billion breakup fee, leaving Hollub standing alone on the battlefield.

Occidental did not allow shareholders to vote on the deal, which drew criticism from several major investors including sixth-largest shareholder T. Rowe Price. The structure of the deal—with Buffett's preferred financing allowing Occidental to avoid a shareholder vote—infuriated institutional investors. Carl Icahn, the legendary activist investor, launched a proxy fight, calling it "one of the worst acquisitions in the last decade."

The timing, in retrospect, was catastrophic. Oil prices were at $60 per barrel when the deal closed in August 2019. By April 2020, they had turned negative for the first time in history. Occidental's stock, which had been trading around $50 when the deal was announced, plummeted to under $10.

The debt burden was crushing. Occidental had taken on Anadarko's $40 billion in debt on top of its own, creating a combined debt load that exceeded the company's market capitalization. The dividend, which had been sacred for decades, was slashed from $3.16 annually to just 4 cents. Asset sales that were supposed to fund debt reduction became fire sales in a collapsed market.

But here's where the story gets interesting. While everyone was focused on the financial carnage, something remarkable was happening in the field. The operational synergies Hollub had promised were materializing faster than anyone expected. Wells that Anadarko had drilled but never completed were brought online at minimal cost. Occidental's superior completion techniques were applied to Anadarko's acreage, dramatically increasing production. The combined company was producing oil at some of the lowest costs in America.

By 2021, as oil prices recovered, Occidental was generating massive cash flows. The company that had nearly died was suddenly printing money. Debt was being paid down ahead of schedule. The stock began recovering. And Warren Buffett, who many thought had taken advantage of Occidental's desperation, started buying common stock—lots of it.

The acquisition that was supposed to destroy Occidental had instead created the premier Permian Basin operator. It controlled 2.8 million net acres across the Delaware and Midland basins. It had over 10,000 drilling locations with breakeven prices below $40 per barrel. Most importantly, it had survived the worst oil price collapse in history and emerged stronger.

Was it triumph or disaster? Perhaps it was both. The deal nearly killed Occidental, but it also transformed it into something more resilient, more focused, and more valuable. It proved that in the oil business, as in life, timing is everything—but execution matters more. And sometimes, the deals that almost destroy you are the ones that ultimately define you.

VIII. Crisis, Recovery & Reinvention (2020–Present)

April 20, 2020. The date is seared into the memory of every oil executive, trader, and investor. West Texas Intermediate crude for May delivery fell more than 100% to settle at negative $37.63 per barrel, meaning producers would pay traders to take the oil off their hands. This negative price has never happened before for an oil futures contract. For Occidental Petroleum, already reeling from the Anadarko debt burden, it was the perfect storm.

The numbers were apocalyptic. Occidental's stock, which had been at $45 when the Anadarko deal closed, plummeted to $8.52. The company that had just become America's fourth-largest oil producer was suddenly worth less than many mid-cap tech startups. Credit default swaps on Occidental's debt spiked, suggesting the market believed bankruptcy was a real possibility.

Vicki Hollub's response was swift and ruthless. The dividend, which had been $3.16 annually before the Anadarko deal, was slashed to 4 cents—a 99% cut that shocked longtime shareholders but preserved precious cash. Asset sales, which were supposed to be orderly dispositions at fair prices, became a fire sale. The company sold its Ghana assets, its Colombian properties, and parts of its prized Permian acreage—anything to raise cash and reduce debt. But the most dramatic development came from Omaha. Warren Buffett, who had provided the financing that enabled the Anadarko deal, began buying Occidental common stock. In March 2022, as oil prices recovered with Russia's invasion of Ukraine, Berkshire revealed it owned 91.2 million shares. As of Friday, Berkshire owns 91.2 million common shares of the oil giant. They're worth $5.1 billion at tonight's close of $56.15. The stock gained 18% today and 45% this week.

The buying continued relentlessly through 2022 and 2023. Warren Buffett's Berkshire Hathaway boosted its stake in Occidental Petroleum to 26.8% after getting the go-ahead last month from US regulators to buy as much as half of the oil giant. By 2023, Berkshire now owns 200.2 million shares of Occidental, worth $12.2 billion based on Tuesday's close of $60.85. The conglomerate now holds 22.2% of the oil company, up from 21.4% previously.

Buffett's rationale was simple: Occidental had the best assets in the best basin in America, and Hollub knew how to operate them. "We will not be making any offer for control of Occidental, but we love the shares we have," Buffett said. "We may or may not own more in the future but we certainly have warrants on what we got on the original deal on a very substantial amount of stock around $59 a share, and warrants last a long time, and I'm glad we have them."

The recovery was as dramatic as the collapse. Oil prices, which had been negative in April 2020, surged past $100 per barrel by 2022. Occidental was generating more than $10 billion in annual free cash flow. Debt was being paid down at a rate of billions per quarter. The dividend was gradually restored. The stock, which had bottomed at $8.52, climbed back above $60.

But more importantly, the crisis had accelerated Occidental's transformation. The carbon capture projects that had seemed like expensive distractions during the crisis were now attracting billions in investment. The Department of Energy committed up to $500 million for the South Texas Direct Air Capture hub. BlackRock invested $550 million in STRATOS. Major corporations were lining up to buy carbon credits.

The company that had nearly died was being reborn—not just as an oil company that survived a crisis, but as an energy company positioning itself for a carbon-constrained future. The permits, the first issued to sequester CO2 from a DAC project, allows Occidental to leverage its expertise managing large quantities of CO2 while advancing technology that strengthens the United States' energy security and furthers economic growth in Texas.

The crisis had done something remarkable: it had forced Occidental to become the company Hollub had always envisioned—leaner, more focused, and with a clear path to both generating cash from oil and gas while building the infrastructure for carbon management. Sometimes, the worst moments create the best opportunities for transformation.

IX. Playbook: Business & Investing Lessons

The Occidental saga offers a masterclass in both what to do and what not to do in corporate strategy, capital allocation, and crisis management. These aren't theoretical lessons from business school case studies—they're battle-tested insights forged in the crucible of negative oil prices, activist investors, and existential threats.

The Danger of Transformational M&A at Cycle Peaks

The Anadarko acquisition will be studied for decades as a cautionary tale of timing. Hollub wasn't wrong about the strategic logic—the combined acreage position in the Permian is arguably the best in America. But buying a cyclical asset at peak prices with maximum leverage is like surfing: catching the wave at the wrong moment doesn't just mean you miss the ride; it means you get crushed.

The lesson isn't to avoid big deals—it's to have the discipline to walk away when the price is wrong. Chevron did exactly that, taking their $1 billion breakup fee and preserving their balance sheet for better opportunities. Sometimes the best deal is the one you don't make.

Operational Excellence as Sustainable Competitive Advantage

Throughout its history, Occidental's superpower has been getting more oil from the ground at lower cost than competitors. This isn't glamorous—it's about completion techniques, water management, artificial lift optimization. But in a commodity business, being the low-cost producer is the only sustainable moat.

Hollub understood this viscerally. While others were cutting maintenance capex during the 2020 crisis, she kept the best engineers and continued efficiency improvements. The result? When prices recovered, Occidental's wells were producing at higher rates with lower decline curves than peers. In commodities, operational excellence isn't just an advantage—it's survival.

Capital Allocation: When to Be Bold vs. Disciplined

Hammer's approach was perpetual boldness—always levering up for the next big deal. Irani's was perpetual discipline—always paying down debt and returning cash. Hollub tried to thread the needle with the Anadarko deal, being bold when she thought the window was closing on Permian consolidation.

The lesson? In cyclical industries, capital allocation isn't about having a consistent philosophy—it's about matching your approach to where you are in the cycle. Be bold at the bottom (like Buffett buying Occidental at $10), be disciplined at the top (like Chevron walking away from Anadarko), and always keep enough dry powder to survive the unexpected.

The Role of Patient Capital

Buffett's investment in Occidental is a masterclass in patient capital. His preferred stock gave him downside protection during the crisis, while the warrants provided upside when things recovered. But more importantly, his continued buying of common stock sent a signal to the market: this company will survive and thrive.

For companies, the lesson is clear: the source of your capital matters as much as the cost. Having a patient, deep-pocketed investor who understands your business can be the difference between bankruptcy and recovery. For investors, the lesson is equally clear: the best returns often come from providing liquidity when others won't.

Transitioning Legacy Energy Companies for the Future

Occidental's carbon capture pivot isn't just greenwashing—it's a fundamental recognition that the energy business is changing. But unlike peers who are abandoning oil and gas for renewables, Occidental is using its core competencies (subsurface expertise, CO2 management, large-scale project execution) to build a new business that complements rather than replaces its traditional operations.

The playbook here is crucial: don't abandon what you're good at, but use those capabilities to build optionality for different futures. Occidental can make money at $100 oil, $40 oil, or in a carbon-constrained world where Direct Air Capture credits trade at $500 per ton. That's not hedging—that's strategic positioning.

Managing Commodity Cycles and Leverage

The iron law of commodity businesses: leverage amplifies both the ups and the downs. Occidental learned this the hard way—twice. First with Cities Service in the 1980s, then with Anadarko in 2019. Both times, debt taken on at cycle peaks nearly destroyed the company when prices collapsed.

The playbook for managing this is counterintuitive: be most conservative when prices are highest and most aggressive when they're lowest. It requires fighting every human instinct—our brains are wired to extrapolate current conditions forward. But in commodities, mean reversion isn't a possibility; it's a certainty.

The Power of Crisis-Driven Transformation

Perhaps the most important lesson from Occidental's story is that crises, while painful, can catalyze necessary changes that would never happen in good times. The 2020 collapse forced Occidental to: - Radically cut costs, finding efficiencies that had been hidden for years - Divest non-core assets that management had been sentimentally attached to - Accelerate the carbon capture strategy that might have remained a side project - Prove to stakeholders (including Buffett) that management could execute under extreme pressure

The company that emerged from the crisis was fundamentally stronger—not in spite of the near-death experience, but because of it. Sometimes you need to be pushed to the brink to discover what you're truly capable of.

X. Analysis & Bear vs. Bull Case

Bull Case: The Premier Energy Transformation Story

The bulls see Occidental as the best-positioned company for multiple energy futures. Start with the Permian position post-Anadarko: 2.8 million net acres in the most economic oil basin in the world, with breakevens below $40 per barrel and decades of drilling inventory. At current strip prices, this asset base alone can generate $8-10 billion in annual free cash flow.

But the real excitement is in carbon management. 1PointFive's Direct Air Capture facilities aren't science projects—they're infrastructure investments backed by the DOE, BlackRock, and major corporate buyers. If carbon credits trade at $200-500 per ton (as many models suggest they must for net-zero targets), Occidental's early-mover advantage in DAC could be worth more than its entire current market cap.

The balance sheet transformation is equally compelling. Debt has been reduced from crisis peaks, and at current commodity prices, Occidental could be net debt-free within 3-4 years. Berkshire Hathaway now holds 25.78% of the company—essentially a Warren Buffett seal of approval. When the Oracle of Omaha makes something his sixth-largest holding, betting against it requires enormous conviction.

Finally, there's the operational excellence story. Occidental's production costs are among the lowest in the industry. Its decline rates are better than peers. Its capital efficiency metrics lead the Permian. This isn't financial engineering—it's blocking and tackling, executed at an elite level.

Bear Case: Structural Headwinds and Execution Risks

The bears have equally compelling arguments. Start with the debt: while reduced from peak levels, Occidental still carries nearly $20 billion in net debt. In a sustained sub-$50 oil environment, servicing this debt while maintaining production and funding growth becomes challenging. The company is one commodity price collapse away from 2020-style distress.

The carbon capture bet, while visionary, faces massive execution risk. Direct Air Capture has never been deployed at scale. The technology works in labs and pilot plants, but scaling to millions of tons annually while achieving acceptable economics is unproven. If government subsidies disappear or carbon credit markets don't develop as expected, Occidental will have spent billions on stranded assets.

Oil demand peak concerns loom large. Whether it's 2030 or 2040, at some point, the world will need less oil. When that happens, high-cost producers will be shut in first—but even low-cost producers will face margin compression. Occidental's multi-decade drilling inventory becomes less valuable if there's no market for the oil.

The Anadarko acquisition, while now generating cash, remains a cautionary tale about capital allocation. Management that was willing to bet the company on a single deal might do so again. The same boldness that created the opportunity for transformation also created the near-death experience.

The Balanced View

The truth, as always, lies somewhere in between. Occidental is simultaneously a cash-flowing machine at current prices and a leveraged bet on commodity prices staying elevated. It's both a traditional oil company with premier assets and a technology company betting on an uncertain carbon future. It's a Buffett-backed comeback story and a reminder of the dangers of deal-making hubris.

What tips the scales for many investors is management's proven ability to execute under pressure. Hollub and her team navigated the company through the worst oil price environment in history, maintained operational excellence, advanced the carbon strategy, and attracted the world's most famous investor as a major shareholder. That track record earns them the benefit of the doubt.

The bear case essentially requires multiple things to go wrong simultaneously: oil prices to collapse, carbon markets to fail to develop, operational performance to deteriorate, and management to make another catastrophic capital allocation error. While possible, this seems less likely than the bull case of continued execution in a reasonably supportive commodity and policy environment.

For investors, Occidental represents a unique risk-reward proposition: upside exposure to both traditional energy and energy transition themes, backed by Buffett's implicit put option, but with real downside if commodity prices collapse or execution falters. It's not for the faint of heart—but then again, nothing in Occidental's 100-year history ever has been.

XI. Epilogue & "What Would We Do?"

Standing at Occidental's headquarters in Houston, looking out at the sprawling city built on oil, you can't help but wonder: what would Armand Hammer think of his company today? The man who bought a nearly bankrupt wildcatter as a tax shelter, who turned it into a global empire through sheer force of personality, who negotiated with Lenin and Qaddafi with equal ease—would he recognize the company that bears his legacy?

In some ways, absolutely. The audacity of the Anadarko acquisition was pure Hammer—betting everything on a transformational deal that others said was impossible. The relationship with Warren Buffett echoes Hammer's cultivation of powerful allies. The carbon capture moonshot has the same visionary grandeur as Hammer's Soviet pencil factories or Libyan oil concessions.

But in other ways, today's Occidental would be foreign to him. The operational discipline, the focus on returns on capital employed, the systematic approach to risk management—these weren't Hammer's strengths. He was a dealmaker, not an operator. He cared more about being in the room where it happened than optimizing drilling and completion techniques.

The transformation from Hammer's conglomerate to today's focused energy company teaches us something profound about corporate evolution. Companies, like people, can change—but it usually takes a crisis. Hammer's death freed Occidental from his personality-driven management. The 2020 collapse freed it from the debt-fueled growth model. Each crisis was painful, but each enabled necessary adaptation.

The carbon management bet represents something even more fundamental: an acknowledgment that the energy industry's social license to operate depends on addressing climate concerns. Hammer, the ultimate pragmatist, would probably appreciate this. He understood that business success required political and social acceptance. In his era, that meant dealing with communists and dictators. In our era, it means dealing with carbon.

What Would We Do?

If we were running Occidental today, the path forward would focus on three priorities:

First, complete the balance sheet restoration. The company doesn't need to be debt-free, but it needs enough financial flexibility to survive $30 oil without distress. This means reducing net debt to below $10 billion—achievable in 2-3 years at current prices. This isn't financial conservatism; it's buying the option to be aggressive when others can't be.

Second, maximize the value of the Permian position while you can. This means continued operational improvements, but also strategic asset high-grading. Sell the tail of the portfolio—the higher-cost, higher-decline assets—while prices are strong. Keep the core of the core. In 10 years, you want to own the assets that still make money at $40 oil, not the ones that need $70.

Third, build real options in carbon management without betting the farm. The Direct Air Capture investments should be staged, with clear milestones for technical and economic viability. If carbon credits become the new oil, Occidental will be perfectly positioned. If not, the losses should be manageable. This is venture capital thinking applied to heavy industry.

The next decade will determine whether Occidental becomes a case study in successful energy transition or another casualty of technological disruption. The company has the assets, the technology, and the backing to succeed. But success will require something that hasn't always been Occidental's strength: patience and discipline in good times, not just boldness in bad times.

What the next decade might hold for Occidental depends largely on factors beyond its control: oil prices, carbon prices, government policy, technological breakthroughs. But it also depends on choices within its control: capital allocation, operational execution, strategic positioning.

The company that survived Armand Hammer's death, Ray Irani's compensation controversies, the Anadarko acquisition, and negative oil prices has proven one thing above all: it's a survivor. In an industry where most independents from 1920 have long since disappeared—absorbed, bankrupt, or forgotten—Occidental endures.

Perhaps that's the ultimate lesson. In the energy business, as in evolution, survival doesn't go to the strongest or the smartest, but to the most adaptable. Occidental has adapted from wildcatter to major, from conglomerate to focused operator, from pure oil company to carbon manager. Whatever the future holds, bet on it adapting again.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube