Blue Owl Capital: Building the Next Alternative Asset Management Giant

I. Introduction & Episode Roadmap

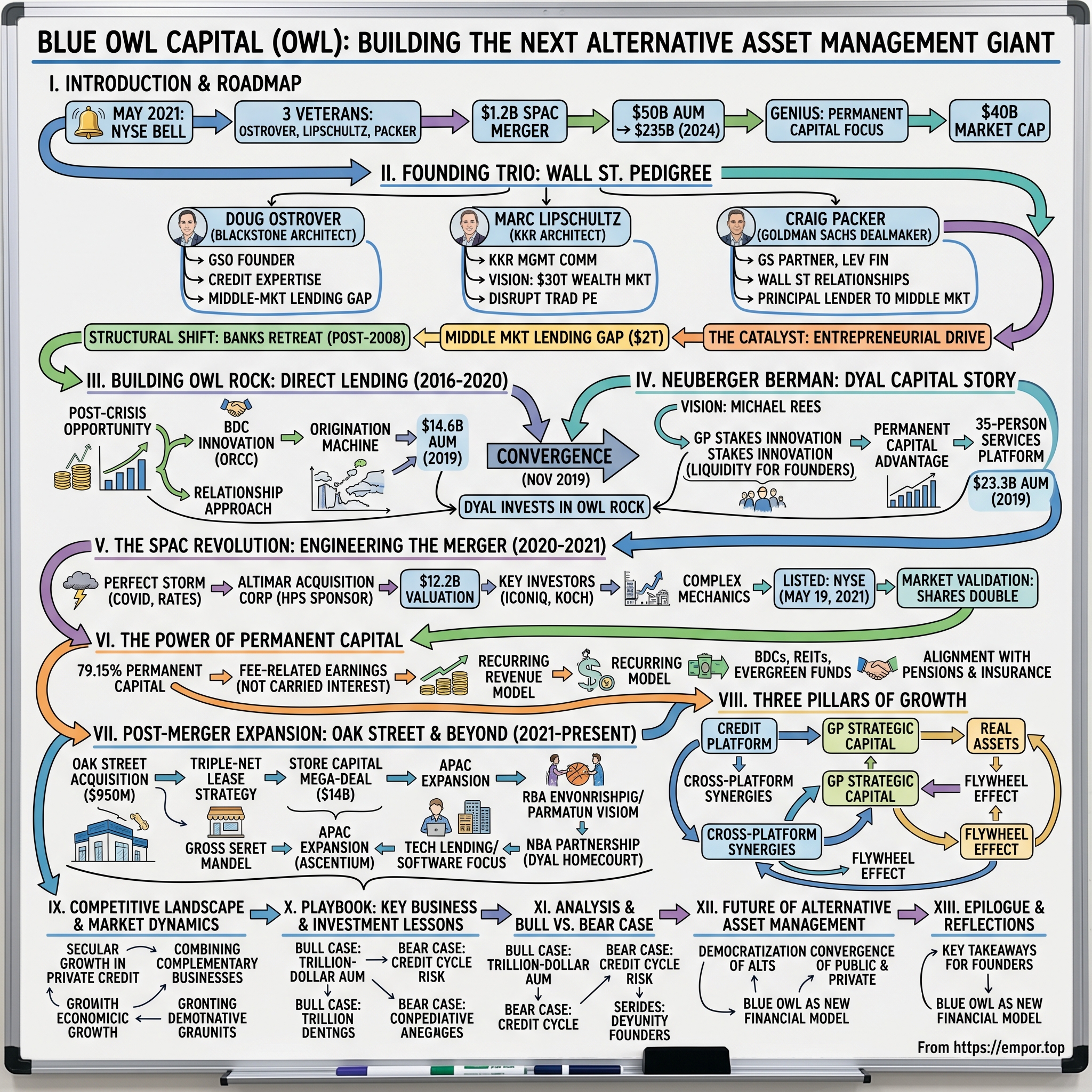

Picture this: It's May 2021, and three Wall Street veterans are about to ring the opening bell at the New York Stock Exchange. Doug Ostrover, Marc Lipschultz, and Craig Packer—collectively responsible for over $1 trillion in deals across their careers—are taking their five-year-old company public through one of the most audacious SPAC mergers in financial history. The entity they're creating, Blue Owl Capital, would instantly become one of the largest alternative asset managers in America with over $50 billion under management. Today, just three years later, that figure has exploded to $235 billion, the stock has more than doubled, and the firm sports a $40 billion market cap that rivals institutions built over decades.

How did three financiers who'd already reached the pinnacle of Wall Street—partners at Blackstone, KKR, and Goldman Sachs—decide to leave their gilded perches to build something new? And more intriguingly, how did they engineer a business model that's fundamentally different from the Blackstones and KKRs of the world, one built on permanent capital rather than the traditional fund cycle?

This is the story of Blue Owl Capital—a company that shouldn't exist according to conventional wisdom. In an era when the mega-firms dominate everything, when scale advantages seem insurmountable, and when starting a new alternative asset manager requires billions in seed capital, these three men found a different path. They identified a massive market dislocation in middle-market lending abandoned by banks post-2008, pioneered new structures to access retail capital through BDCs, and ultimately merged with another innovative firm to create something entirely new in asset management.

The genius wasn't just in the strategy—it was in the timing and execution. While everyone else was raising traditional drawdown funds, Blue Owl focused on permanent capital vehicles. While competitors chased the biggest deals, they built relationships in the overlooked middle market. And when the SPAC boom created a once-in-a-generation opportunity to go public quickly, they seized it with both hands.

What emerges is a playbook for building in highly competitive, capital-intensive industries: find the structural inefficiency, build where others won't, and when the window opens, move faster than anyone thinks possible. This is how you build a $40 billion financial empire in less than a decade.

II. The Founding Trio: Origins & Wall Street Pedigree

The Blackstone Architect: Doug Ostrover

In 2005, Stephen Schwarzman made a bet that would reshape Blackstone's future. He acquired GSO Capital Partners, a credit-focused hedge fund co-founded by Doug Ostrover, for more than $1 billion. At the time, private equity firms buying credit platforms was unusual—most stuck to their leveraged buyout knitting. But Ostrover had built something special at GSO: a platform that could deploy capital across the credit spectrum, from distressed debt to mezzanine financing. Under Blackstone's umbrella, GSO would grow to become one of the world's largest credit platforms, managing over $100 billion by the time Ostrover left. But here's what made Ostrover different: he understood credit from every angle. Before co-founding GSO in 2005, he'd been Managing Director and Chairman of the Leveraged Finance Group at Credit Suisse First Boston, where he was responsible for all of CSFB's origination, distribution, and trading activities relating to high yield securities, leveraged loans, high yield credit derivatives, and distressed securities. He'd seen cycles, blown-up deals, and the evolution of credit markets from the inside.

By 2015, after a decade of building GSO into one of the largest alternative managers in the world with approximately $75 billion of assets under management, Ostrover was ready for something new. The success of GSO as the leading alternative credit platform was "in no small measure the result of Doug's creative thinking and energy", his partners would later say. But Ostrover saw an opportunity that even Blackstone, with all its resources, wasn't positioned to capture: the massive gap in middle-market lending that banks had abandoned post-financial crisis.

The KKR Architect: Marc Lipschultz

If Ostrover brought the credit expertise, Marc Lipschultz brought the institutional gravitas. He'd spent more than two decades at KKR, serving on the firm's Management Committee and as the Global Head of Energy and Infrastructure, joining the firm as one of the first 20 employees. Think about that trajectory: from employee number 20 to running one of KKR's most important divisions, watching Henry Kravis and George Roberts build the private equity playbook from the inside.

Prior to joining KKR, he was with Goldman, Sachs & Co., where he focused on mergers and acquisitions and principal investment activities. But after decades at the pinnacle of private equity, Lipschultz saw what others missed: the next wave of institutional capital wouldn't come from raising bigger and bigger buyout funds, but from creating products that could tap into the $30 trillion wealth management market.

His departure from KKR in 2015 shocked the industry. Here was someone who'd helped build KKR's energy and infrastructure platform from nothing into a multi-billion dollar business, walking away at the peak of his influence. But Lipschultz understood something fundamental: the traditional PE model—raise a fund, deploy it over 3-5 years, harvest returns, repeat—was ripe for disruption. The future belonged to permanent capital vehicles that could provide steady income to an aging demographic desperate for yield in a zero-interest-rate world.

The Goldman Sachs Dealmaker: Craig Packer

As a Partner and Co-Head of Leveraged Finance in the Americas at Goldman Sachs & Co., Packer brought Wall Street relationships and capital markets expertise crucial to Owl Rock's success. He'd overseen billions in leveraged finance transactions and served on key committees—the Firmwide Capital Committee, Investment Banking Division Operating Committee, IBD Client and Business Standards Committee, and IBD Risk Committee—positioning him at the epicenter of Wall Street's deal flow.

Craig joined Goldman Sachs & Co. as a Managing Director and Head of High Yield Capital Markets in 2006 and was named Partner in 2008. Prior to joining Goldman Sachs & Co., he was the Global Head of High Yield Capital Markets at Credit Suisse First Boston, and before that he worked at Donaldson, Lufkin & Jenrette. Notice the pattern here: like Ostrover, Packer had roots at DLJ and Credit Suisse. These weren't just colleagues—they were battle-tested partners who'd worked together through multiple cycles.

But Packer saw something his Goldman colleagues didn't: the future of credit wasn't in arranging syndications for mega-deals; it was in becoming the principal lender to America's middle market. The banks had retreated, the companies still needed capital, and whoever could build the platform to serve them would capture enormous value.

The Catalyst: Why Leave?

The question everyone asked in 2016: Why would these three leave the comfort and prestige of their positions to start from scratch? The answer lay in a structural shift that only insiders could fully appreciate. Post-financial crisis regulations—Dodd-Frank, Basel III, the Volcker Rule—had fundamentally changed the economics of bank lending. Banks were pulling back from middle-market corporate lending, creating a $2 trillion gap in the market.

But there was another, more personal motivation. As Marc Lipschultz would later explain, after decades at KKR and having joined as one of the first 20 employees, he wanted to build something from the ground up again. These weren't executives looking for their next job; they were entrepreneurs who saw a once-in-a-generation opportunity to build the next great financial institution.

The trio had complementary skills that made them formidable: Ostrover understood credit structuring and risk management from his GSO days; Lipschultz brought institutional credibility and a vision for accessing new pools of capital; Packer had the Wall Street relationships and capital markets expertise to execute deals at scale. Together, they weren't just starting another credit fund—they were architecting a new model for asset management.

III. Building Owl Rock: The Direct Lending Platform (2016–2020)

The Post-Crisis Opportunity

When Ostrover, Lipschultz, and Packer launched Owl Rock in 2016, they weren't entering a vacuum—they were positioning themselves at the center of one of the greatest capital market dislocations in modern history. The 2008 financial crisis hadn't just damaged banks; it had fundamentally rewired how corporate America accessed capital. Banks that once held $2 trillion in middle-market loans on their balance sheets were now constrained by Basel III capital requirements and Volcker Rule restrictions. A JPMorgan or Bank of America that might have eagerly financed a $500 million leveraged buyout in 2007 was now focused on investment-grade lending and fee income. The founders understood this wasn't a temporary disruption but a permanent structural change. Middle-market companies—those with EBITDA between $10 million and $250 million—still needed capital for growth, acquisitions, and recapitalizations. But with banks retreating, who would fill the void? This was Owl Rock's opening.

The BDC Innovation

At a time when annual sales of nontraded BDCs had fallen from $6 billion four years ago to less than $1 billion by the end of 2017, Owl Rock Capital Partners was able to buck the trend. With the launches of Owl Rock Capital Corporation ("ORCC"), a private BDC, and Owl Rock Capital Corporation II ("ORCC II") a nontraded BDC program, the firm succeeded in raising capital from institutional and individual investors at a rate that far exceeded any other BDC manager. ORCC, launched in early 2016, raised $5.5 billion of equity commitments from institutional investors such as the State of New Jersey Common Pension Fund, Brown University and MSD Private Capital Investments (the family office of Michael Dell), and through wealth management platforms like Merrill Lynch and Ameriprise. ORCC II launched in April 2017 and, as of August 31st, has raised $300 million since inception, and accounted for almost 75% of the equity capital raised in the sector year-to-date.

The genius of Owl Rock's approach wasn't just in raising capital—it was in how they structured it. Business Development Companies (BDCs) offered a unique regulatory structure that allowed them to access both institutional and retail capital while providing significant tax advantages. By electing to be regulated as BDCs, Owl Rock's vehicles could avoid corporate taxes as long as they distributed 90% of their taxable income to shareholders.

But Owl Rock did something different from traditional BDC managers. As a manager of institutional capital with a captive distribution team, Owl Rock could better manage costs and ensure that individual investors were afforded the same investment opportunities as institutional investors, which would hopefully result in better investment outcomes. Another important feature of ORCC II was the lack of a distribution servicing fee. This was a common cost added to other non-traded BDCs and REITs and had historically eroded distribution yields. By not charging this fee, ORCC II allowed investors to retain more of their distribution income and it also made ORCC II eligible to be purchased in advisory accounts.

Building the Origination Machine

Owl Rock grew rapidly since it began managing money in 2016 to have over $7 billion in assets under management by mid-2018. But assets under management was just one metric—what mattered was the quality of the deals they were originating. The founders leveraged their decades of relationships to build a proprietary deal flow that bypassed the traditional syndication markets.

The strategy was simple but powerful: while other lenders were fighting over broadly syndicated deals, Owl Rock focused on bilateral relationships with private equity sponsors. They could commit $500 million to $1 billion for a single transaction—scale that few competitors could match. This size advantage meant they could be the sole or lead lender on deals, giving them better economics and stronger documentation.

In partnership with financial sponsors and private companies, Owl Rock could lead or anchor highly customized financings across a variety of industries and provided investors with access to alternative investment strategies that offer the potential to generate income and attractive risk-adjusted returns. This wasn't just about deploying capital; it was about becoming the go-to financing partner for the middle market.

The Relationship-Oriented Approach

What distinguished Owl Rock from other direct lenders wasn't just their capital—it was their approach to relationships. The founders understood that in private credit, reputation and reliability matter more than pricing. A sponsor running a competitive auction process cares about certainty of close as much as the interest rate. Owl Rock built its reputation on never re-trading deals and always closing on time.

From a risk management perspective, the strategy of using floating rate loans that benefit from higher cash coupons when rates rise protects investors from interest rate risk. Risk is also mitigated by investing in more senior parts of the capital structure as well as having stronger protections and loan documentation compared to debt syndications in the public high yield or leveraged loan markets.

This conservative approach to risk management would prove prescient. While competitors chased yield by moving down the capital structure or loosening covenants, Owl Rock maintained discipline. They focused on first-lien senior secured loans to companies with strong cash flows and defensive business models. The portfolio was built to weather storms, not just capture upside in good times.

Early Wins and Momentum

By 2019, just three years after launch, Owl Rock had become one of the fastest-growing alternative asset managers in history. The firm's success attracted attention from an unexpected source: Dyal Capital Partners, the GP stakes business within Neuberger Berman. In November 2019, Dyal acquired a passive, non-voting minority stake in Owl Rock Capital—a validation of the platform's potential and a preview of the transformative merger to come.

The Owl Rock model was working: permanent capital vehicles providing predictable fee streams, strong credit performance even in volatile markets, and a growing reputation as the lender of choice for middle-market sponsors. But the founders knew they were still subscale compared to the giants of alternative asset management. To truly compete with Blackstone, Apollo, and KKR, they would need to get bigger—much bigger.

IV. Meanwhile at Neuberger Berman: The Dyal Capital Story

The Vision of Michael Rees

While Ostrover, Lipschultz, and Packer were building Owl Rock's direct lending machine, another innovation was taking shape within the walls of Neuberger Berman. Michael Rees, who had joined the firm in 2010, saw an opportunity that others had missed: the growing liquidity needs of alternative asset managers themselves. Prior to founding Dyal Capital, Michael was a founding employee and shareholder of Neuberger Berman Group, transitioning from Lehman Brothers as part of the management buyout transaction in May 2009, and was the first Chief Operating Officer of Neuberger's alternatives business. The Lehman collapse had taught Rees a crucial lesson: even the most successful financial institutions needed liquidity options for their owners.

Think about the typical alternative asset manager's dilemma: the founders have built billion-dollar businesses, but their wealth is entirely tied up in illiquid equity stakes. They can't sell without losing control, and traditional buyers—strategic acquirers or public markets—come with strings attached that could fundamentally alter the firm's culture and investment approach.

The GP Stakes Innovation

Dyal Capital was formed in 2011 by Michael Rees and Sean Ward, both formerly of Lehman Brothers. The concept was elegantly simple: acquire minority, non-voting stakes in established alternative asset managers, providing liquidity to founders and early employees while allowing them to maintain control and continue running their businesses.

"The investments we make are typically in the USD500 million to USD1 billion range," Rees would later explain. This wasn't venture capital betting on unproven managers; this was providing liquidity solutions to the titans of the industry—firms managing tens of billions in assets with decades-long track records.

Building the Portfolio

By 2019, Dyal had raised four permanent capital vehicles, providing minority equity capital to more than 40 well-established private equity and hedge fund firms. Dyal's latest vehicle—Dyal Capital Partners IV—attracted over $9.0 billion of committed capital from its global network of investors, which included some of the biggest pension funds, sovereign wealth funds and insurance companies. Aggregate commitments across all Dyal funds and co-investment vehicles totaled more than $21.6 billion.

The genius of Dyal's model was its alignment structure. Unlike traditional private equity, which seeks control and operational changes, Dyal was a passive investor. They weren't trying to tell Vista Equity how to run software buyouts or Providence Equity how to structure media deals. They were simply providing liquidity and strategic support while participating in the firms' future growth.

The Business Services Platform

A key feature of the firm was its Business Services Platform, headed by John Dyment. The primary goal of the platform, which had grown to a team of 35 people and was widely recognized as best-in-class, was to forge close collaboration with each and every GP the firm partnered with and enable them to reach their business objectives. The platform was built on five pillars: talent management, operational advisory services, business strategy, product development and client development & marketing support.

"We wanted to build a business that could become a leading partner to some of the best GPs in the world," Rees explained. "For that to happen we needed substantial long-dated capital and a strategic platform in place."

The Permanent Capital Advantage

What made Dyal particularly powerful was its focus on permanent capital. Dyal has $23.3 billion in AUM, 100% of which is permanent capital. Unlike traditional private equity funds that have to return capital to LPs after investments are realized, Dyal's permanent vehicles could hold stakes indefinitely, providing stable, long-term capital to its partner firms.

This structure perfectly aligned with the needs of alternative asset managers. They got liquidity without losing control, Dyal got exposure to the growth of the alternative asset management industry, and LPs got access to a diversified portfolio of the world's best alternative managers—a win-win-win scenario that had never been executed at this scale before.

The Strategic Investment in Owl Rock

In November 2019, the paths of Dyal and Owl Rock converged in a way that would foreshadow their eventual merger. Dyal acquired a passive, non-voting minority stake in Owl Rock Capital in November 2019. The investment, reportedly around $500 million for a 20% stake, provided Owl Rock with additional permanent capital while giving Dyal exposure to one of the fastest-growing direct lending platforms in the market.

"We are very excited to be partnering with Owl Rock," said Michael Rees, Head of Dyal Capital. "Owl Rock has become a leading private credit firm with an outstanding reputation for origination and underwriting and the second-largest BDC platform in the world with approximately $14.6 billion in assets under management across its vehicles."

This wasn't just a financial investment—it was a strategic alignment of two complementary business models. Owl Rock needed permanent capital to fund its growth; Dyal needed exposure to the booming direct lending market. The relationship would prove so successful that within a year, the two firms would be discussing something far more ambitious: a full merger.

V. The SPAC Revolution: Engineering the Merger (2020–2021)

The Perfect Storm

By late 2020, the stars had aligned for something unprecedented in alternative asset management. The COVID-19 pandemic had created massive market dislocations, the Federal Reserve's zero-interest-rate policy had made yield more precious than ever, and the SPAC boom had created a new path to public markets that bypassed the traditional IPO process. For Owl Rock and Dyal, it was the perfect moment to strike.

Owl Rock Capital Group ("Owl Rock") and the Dyal Capital Partners ("Dyal") division of Neuberger Berman Group LLC ("Neuberger Berman") announced they entered into a definitive business combination agreement with Altimar Acquisition Corporation (NYSE: ATAC) ("Altimar") to form Blue Owl Capital Inc. ("Blue Owl"), an alternative asset management firm with over $45.0 billion in assets under management.

The tie-up between Dyal and Owl Rock had been long in the making: the firms had a relationship before Dyal acquired a stake in the direct lending firm over a year ago. Deal talks heated up late in the summer of 2020, as both firms recognized the transformative potential of combining their complementary platforms.

Why SPAC? Speed and Certainty

The decision to go public via SPAC rather than traditional IPO was strategic. Altimar Acquisition Corporation, sponsored by HPS Investment Partners—itself a portfolio company of Dyal—offered unique advantages. First, speed: a SPAC merger could be completed in months rather than the year-plus timeline of a traditional IPO. Second, certainty: the valuation was negotiated upfront rather than subject to market volatility during a roadshow. Third, capital: the SPAC structure allowed them to raise additional funding simultaneously.

The deal valued at about $12.2 billion and includes a combined $1.5 billion commitment from ICONIQ Capital, CH Investment Partners, $6.8 billion Koch Companies Defined Benefit Master Trust, the Federated Hermes Kaufmann Funds and Liberty Mutual Investments.

The investor roster read like a who's who of sophisticated capital: ICONIQ, the family office that manages money for Mark Zuckerberg and other tech billionaires; the Koch pension fund; Federated Hermes; Liberty Mutual. These weren't SPAC tourists—they were long-term investors betting on the structural transformation of asset management.

The Complex Mechanics

The transaction structure was intricate, reflecting the multiple stakeholders involved. Assuming no redemptions by Altimar's existing public stockholders, the existing equityholders of Owl Rock and Dyal (including Neuberger Berman) will hold approximately 85% of Blue Owl immediately following the closing of the business combination.

Neuberger Berman, which had incubated Dyal since 2011, would receive $1.1 billion representing a partial sale of its interest in Dyal, while remaining a meaningful shareholder in Blue Owl. The founders and senior managers would retain their equity stakes through the transition, ensuring continued alignment with public investors.

Navigating Approvals

The path to closing wasn't simple. The transaction required approvals from multiple constituencies: Altimar's stockholders, the equity holders of each of the Owl Rock business development companies, and Dyal-sponsored fund's limited partners. Each group had different concerns and incentives that needed to be addressed.

For the BDC shareholders, the question was whether the merger would affect the management and strategy of their investments. Owl Rock assured them there would be no changes to the investment process or fee structure. For Dyal's LPs, the concern was whether combining with a credit platform would create conflicts or change the GP stakes strategy. The answer: the two businesses would operate independently within Blue Owl, maintaining their distinct strategies while benefiting from shared infrastructure.

The Moment of Truth

On May 19, 2021, the transaction was completed and Blue Owl was listed on the New York Stock Exchange. The opening bell ceremony wasn't just a celebration—it was a declaration that alternative asset management had entered a new era. The combined entity had over $50 billion in assets under management, nearly 80% in permanent capital vehicles, and a clear path to explosive growth.

Doug Ostrover, now Co-CEO of Blue Owl, captured the significance: "You will hear a lot of alternative managers talk about their net assets grew by X. We don't have this phenomenon. Our assets start at $50 billion to $60 billion, and they will only grow from there."

The market's reaction was immediate and positive. Blue Owl's shares would more than double over the next three years, validating the thesis that permanent capital and fee-related earnings were what sophisticated investors wanted from alternative asset managers.

VI. The Power of Permanent Capital

Redefining the Asset Management Model with Permanent Capital Focus

Blue Owl Capital's predominant focus on permanent capital in its AUM sets it apart from other alternative asset managers. As of the end of the first quarter, 79.15% of the total AUM was permanent capital, accounting for approximately $114.3 billion. This concentration of permanent capital reduces volatility and enables steady growth in AUM against disruptive macroeconomic backdrops.

To understand why this matters, consider the traditional private equity model: raise a fund, deploy capital over 3-5 years, harvest returns, return capital to LPs, repeat. This creates inherent volatility—AUM can swing dramatically based on fundraising cycles, realizations, and market conditions. Management fees fluctuate, making it difficult to build a stable, predictable business.

Blue Owl's operational model does not depend on the traditional 20% carried interest but rather on management fees from this ever-growing base of permanent capital. This creates a fundamentally different economic model—one based on recurring revenue rather than episodic performance fees.

BDCs, REITs, and Evergreen Funds

The architecture of Blue Owl's permanent capital strategy rests on three main structures: Business Development Companies (BDCs), Real Estate Investment Trusts (REITs), and evergreen funds. Each serves a different purpose but shares the common characteristic of perpetual capital.

BDCs, which form the core of Blue Owl's credit platform, are publicly traded or non-traded vehicles that provide financing to middle-market companies. By electing to be regulated as BDCs, these vehicles can avoid corporate taxes by distributing 90% of taxable income to shareholders. This creates a powerful alignment: investors get regular income distributions, Blue Owl gets permanent fee-paying capital, and portfolio companies get patient, long-term financing.

The REIT structure, utilized primarily through the Oak Street acquisition, operates similarly for real estate investments. These vehicles own properties under long-term triple-net leases, generating predictable cash flows that can be distributed to investors while the capital base remains permanent.

Evergreen funds, the newest addition to Blue Owl's toolkit, offer daily liquidity with quarterly redemption windows but maintain a permanent capital base through continuous fundraising. These structures bridge the gap between traditional drawdown funds and fully liquid mutual funds.

The Recurring Revenue Model

"You will hear a lot of alternative managers talk about their net assets grew by X. We don't have this phenomenon. Our assets start at $50 billion to $60 billion, and they will only grow from there," Ostrover explained. This wasn't hyperbole—it was math.

With permanent capital, Blue Owl's AUM could only grow through two mechanisms: raising new capital or appreciation of existing investments. There were no fund expirations, no return of capital requirements, no J-curves to navigate. Every dollar raised was a dollar that would generate fees in perpetuity.

The implications for valuation were profound. While traditional alternative managers traded at multiples based on volatile carried interest projections, Blue Owl could be valued more like a software company with recurring revenue. The predictability of cash flows justified higher multiples and lower cost of capital.

Alignment with Long-Term Investors

Blue Owl's permanent capital base consists mainly of pensions and insurance companies. The goals of these groups align well with the permanent capital approach as the perpetual cash flows match well with the payout requirements of pensions and insurance companies, which have regular, predictable liabilities.

This wasn't just about duration matching—it was about risk alignment. Insurance companies and pension funds don't want volatility; they want steady, predictable returns that match their liability streams. Blue Owl's floating-rate loans, defensive sector focus, and senior position in the capital structure delivered exactly that: 8-10% returns with minimal volatility.

The model created a virtuous cycle: permanent capital enabled patient investing, patient investing generated stable returns, stable returns attracted more permanent capital. While competitors fought over the same pool of traditional LPs, Blue Owl was tapping into the $30 trillion insurance and pension market that had been largely shut out of alternatives due to liquidity mismatches.

VII. Post-Merger Expansion: Oak Street & Beyond (2021–Present)

The Oak Street Acquisition: Adding Real Estate

Just five months after going public, Blue Owl announced in October 2021 that it would acquire Oak Street Real Estate Capital for $950 million, funded through cash and Blue Owl common units (up to 39 million units). Oak Street equity holders would be eligible for additional earnouts up to $650 million upon meeting performance thresholds.

Oak Street was founded in 2009 by Marc Zahr and James Hennessey. The Chicago-based firm had built a unique niche in the real estate market, focusing on structuring sale-leasebacks with $12.4 billion of assets under management as of September 30, 2021. The firm focuses on structuring sale-leasebacks, which includes triple net leases, as well as providing seed and strategic capital.

Marc Zahr, who would join Blue Owl as Co-President and board member, had built Oak Street into one of the premier net lease platforms in the country. Prior to founding Oak Street, Marc served as Vice President at American Realty Capital where he was responsible for the analytics and acquisition activities within the company's real estate portfolios.

The Triple-Net Lease Strategy

Oak Street's business model was elegantly simple yet powerful: they would buy properties from corporations, healthcare systems, universities, and government entities, then lease them back under long-term triple-net lease agreements. The tenant would be responsible for all property expenses—taxes, insurance, and maintenance—while Oak Street collected steady rental income.

This wasn't speculative real estate development or opportunistic investing. It was predictable, contractual cash flows from creditworthy tenants—exactly the kind of income-generating assets that fit Blue Owl's permanent capital model. The Net Lease platform focused on acquiring properties net-leased to investment grade and creditworthy tenants.

"There is a strong fit between Blue Owl and Oak Street," Marc Zahr explained, "highlighted by our mutual drive to be market leaders in what we do, our shared deep appreciation for the value of long-duration capital, and our focus on downside protection and robust income generation for our investors."

The STORE Capital Mega-Deal

In September 2022, Oak Street and GIC agreed to acquire Store Capital for $14 billion—one of the largest real estate transactions of the year. STORE Capital, a publicly traded REIT with a portfolio of single-tenant operational real estate, would dramatically expand Blue Owl's real estate footprint. The acquisition brought over 3,000 properties and relationships with hundreds of tenants into the Blue Owl ecosystem.

Expanding the Product Suite and Asia Presence

Blue Owl wasn't stopping with Oak Street. In December 2021, it acquired Ascentium Group, a business development office based in Hong Kong as part of its plans to expand in Asia. Ascentium's Founder and CEO, James Lee, would serve as the Head of Blue Owl's Institutional Sales Team in Asia, strengthening the firm's presence in the Asia-Pacific region alongside its recently opened Singapore office.

"There is tremendous opportunity for GP stakes, direct lending, and real estate solutions in the APAC region," Doug Ostrover explained. The acquisition gave Blue Owl its ninth office globally and positioned the firm to tap into the rapidly growing Asian alternatives market.

Technology Lending and Software Focus

Blue Owl also began expanding into specialized lending verticals. Technology lending, particularly to software companies, became a major focus. These businesses offered attractive characteristics for lenders: recurring revenue models, high margins, and mission-critical products that customers couldn't easily replace.

The firm launched dedicated software lending products, recognizing that technology companies had different financing needs than traditional industrial or consumer businesses. By 2024, Blue Owl had three products dedicated solely to software lending, positioning itself as a leader in this rapidly growing segment.

The NBA Partnership: Exclusive Rights to Purchase Team Stakes

Blue Owl has formed an exclusive partnership with the National Basketball Association, becoming the only approved buyer of minority equity stakes in the 30 NBA teams. Through its Dyal HomeCourt Partners fund, Blue Owl could acquire stakes in an unlimited number of NBA franchises—a unique privilege that other investors don't have.

"We're proud to be a partner, an exclusive partner, with the NBA," Michael Rees explained. "That business is just being launched, and we're hoping to have our first closing in the not-too-distant future. We think we can grow certainly a very attractive basketball strategy off of this platform."

The fund has invested in teams including the Phoenix Suns (which it exited at a 158% gain when Mat Ishbia purchased the team), Sacramento Kings, Atlanta Hawks, and Minnesota Timberwolves. As of late 2024, the NBA fund had about $900 million in assets, with valuations soaring as professional sports franchises became increasingly valuable trophy assets.

VIII. The Business Model: Three Pillars of Growth

Credit Platform: The Direct Lending Engine

Direct lending involves non-bank creditors providing loans to businesses without the use of intermediaries. Blue Owl focuses on lending to defensive businesses in recession-resistant industries or non-cyclical markets. Direct lending investments typically have floating-rate, short terms to maturity, strong covenants, and low correlation with public markets.

The scale of Blue Owl's credit platform is formidable. Direct Lending Gross Origination reached nearly $13 billion for the year, with $4.5 billion for Q1 2025. Direct Lending Portfolio Returns were 3.1% for Q1 2025 and 13.3% over the last 12 months. What distinguishes Blue Owl's approach is not just volume but quality—the firm's direct lending strategy has shown robust performance, with a low average annual realized loss rate of 13 basis points, indicating strong credit quality.

GP Strategic Capital: The Innovation Engine

With extensive experience providing long-term minority equity and financing to private capital investment managers, Blue Owl has established itself as an innovator within the industry. The GP Strategic Capital platform partners with alternative managers who want to add to their success and continue to be leaders in their space.

This isn't just passive investing—it's strategic partnership. The platform provides liquidity solutions to the most successful alternative asset managers while maintaining their independence and operational control. The genius of this model lies in its alignment: Blue Owl participates in the growth of these firms without interfering in their investment processes.

Real Assets: The Triple-Net Lease Machine

Blue Owl's Real Assets platform focuses on sale-leaseback and triple-net lease strategies, primarily through the Oak Street acquisition. This business model involves purchasing properties from corporations, healthcare systems, and universities, then leasing them back under long-term agreements where tenants handle all property expenses.

The platform's expansion has been dramatic. With the STORE Capital acquisition bringing over 3,000 properties into the portfolio, Blue Owl has become one of the largest net lease operators in the country. These aren't speculative real estate plays—they're contractual cash flows from investment-grade tenants, perfectly aligned with the permanent capital model.

Cross-Platform Synergies

The true power of Blue Owl's three-pillar model lies in the synergies between platforms. A company that takes a direct loan from the Credit platform might later need a sale-leaseback for its real estate through the Real Assets platform. A GP that receives investment from the Strategic Capital platform might co-invest with Blue Owl's credit funds. These interconnections create a flywheel effect that drives growth across all segments.

With $250 billion in assets under management as of December 31, 2024, Blue Owl invests across three multi-strategy platforms: Credit, GP Strategic Capital, and Real Assets. The growth trajectory has been remarkable—total equity raised in 2024 reached $27.5 billion, a 75% increase from 2023.

IX. The Competitive Landscape & Market Dynamics

The Private Credit Boom: From Niche to Mainstream

The transformation of private credit from a niche corner of finance to a mainstream asset class represents one of the most significant shifts in capital markets since the financial crisis. What was once a $300 billion market in 2010 has exploded to over $1.5 trillion today, with projections suggesting it could reach $3 trillion by 2030.

Blue Owl has positioned itself at the forefront of this secular trend. Despite volatility, the private wealth channel continues to grow due to low penetration and high demand. The firm expects institutional fundraising to accelerate as the year progresses, driven by flagship funds like GP Stakes 6 and Real Estate 7, while also exploring new products and expanding into new markets.

Competition from Traditional Banks and Mega PE Firms

The competitive dynamics in private credit have shifted dramatically. Traditional banks, once retreating from the market, are now attempting to re-enter through partnerships and joint ventures. Meanwhile, every major private equity firm—Apollo, Ares, KKR, Blackstone—has built or acquired massive credit platforms.

In June 2024, Blue Owl Capital ranked 26th in Private Equity International's PEI 300 ranking among the world's largest private equity firms. While this might seem modest compared to the giants, it represents extraordinary growth for a firm that didn't exist eight years ago.

Differentiation Through Scale, Speed, and Certainty

Blue Owl's competitive advantage isn't just size—it's the combination of scale, speed, and certainty. The firm can commit $500 million to $1 billion for a single transaction, move from initial discussion to closing in weeks rather than months, and provide certainty of execution that sponsors value above marginal differences in pricing.

In dislocated environments, Blue Owl's business benefits as the syndicated market has shut down, increasing reliance on private credit. This counter-cyclical strength means Blue Owl gains market share precisely when competitors pull back.

The Rising Rate Environment Advantage

The Federal Reserve's rate hiking cycle, which took rates from near zero to over 5%, created a perfect environment for Blue Owl's floating-rate loan portfolio. Approximately 90% of Blue Owl's management fees come from permanent capital, providing revenue resilience even as market conditions fluctuate.

Regulatory Tailwinds

Post-crisis banking regulations continue to create opportunities for non-bank lenders. Basel III endgame rules, still being finalized, will require banks to hold even more capital against corporate loans. The Volcker Rule continues to restrict proprietary trading. These structural headwinds for banks are structural tailwinds for Blue Owl.

X. Playbook: Key Business & Investment Lessons

The Power of Combining Complementary Businesses

The Owl Rock + Dyal merger wasn't just about scale—it was about combining two businesses with perfect strategic fit. Owl Rock brought direct lending expertise and BDC structures; Dyal brought GP stakes and permanent capital vehicles. Together, they created something neither could have built alone.

This teaches a crucial lesson: in mature industries, transformative growth often comes not from organic expansion but from finding the perfect merger partner whose strengths complement your weaknesses.

Permanent Capital as a Competitive Moat

Blue Owl's focus on permanent capital vehicles—BDCs, REITs, evergreen funds—creates a moat that's nearly impossible for traditional fund managers to replicate. While competitors must constantly fundraise and return capital, Blue Owl's AUM only grows. This structural advantage compounds over time, creating increasingly wide gaps between Blue Owl and traditional players.

Building in Counter-Cyclical Markets

The founders launched Owl Rock in 2016, well into the economic recovery when many thought the credit opportunity had passed. They understood that the best time to build isn't at the bottom of the cycle but when you can attract talent, raise capital, and establish systems without the pressure of crisis.

The Importance of Founder Alignment

Blue Owl has four private credit billionaires: founders Doug Ostrover, Marc Lipschultz, Michael Rees and Craig Packer. As a group, they own 17% of Blue Owl, worth $6.8 billion. This isn't just skin in the game—it's entire careers bet on one outcome. This alignment ensures decisions are made for long-term value creation, not quarterly earnings management.

Platform Economics and the Flywheel Effect

Blue Owl's model creates multiple reinforcing loops: more AUM enables larger deals, larger deals attract better talent, better talent generates superior returns, superior returns attract more capital. Each turn of the wheel makes the next turn easier.

When to Use SPACs Strategically

Blue Owl's SPAC merger in 2021 was perfectly timed—executed at the peak of the SPAC boom but before the bust. The key insight: SPACs aren't inherently good or bad; they're tools that can provide speed and certainty when traditional IPO markets are uncertain. Blue Owl used the SPAC not as a shortcut but as a strategic accelerant.

XI. Analysis & Bull vs. Bear Case

Bull Case: The Path to Trillion-Dollar AUM

The bull case for Blue Owl rests on several powerful trends. First, the secular growth in private credit shows no signs of slowing. Banks continue to retreat from middle-market lending, creating an ever-larger addressable market. Second, Blue Owl's permanent capital advantage becomes more valuable over time as the firm compounds AUM without the drag of capital returns.

Since its public listing in 2021, its shares have more than doubled, achieving a market value of almost $40 billion. The market clearly believes in the story, and recent results justify that confidence. Management Fees grew 31% over the last 12 months, FRE grew 23%, and DE grew 20%.

Multiple growth levers remain untapped. Geographic expansion into Asia through the Ascentium acquisition opens massive new markets. Product expansion into technology lending, opportunistic credit, and strategic equity creates new revenue streams. The wealth management channel, still dramatically under-penetrated in alternatives, could drive decades of growth.

Strong founder alignment ensures long-term thinking. The firm anticipates about 20% growth in FRE per share over the next five years, suggesting management sees a clear path to sustained expansion.

Bear Case: The Risks Ahead

The bear case begins with credit cycle risk. Blue Owl has never been tested through a true credit crisis as an independent company. While the founders have decades of experience, the firm's rapid growth means much of the portfolio was originated in benign credit conditions. A severe recession could expose weaknesses in underwriting standards.

Competition from larger players intensifies daily. Apollo has $650 billion in AUM; Blackstone manages over $1 trillion. These giants have deeper pockets, broader platforms, and longer track records. As they push into middle-market lending, Blue Owl's competitive advantages could erode.

Regulatory changes pose constant threats. BDC and REIT structures exist because of specific tax regulations that could change. The SEC continues to scrutinize private credit, and new regulations could increase compliance costs or limit growth.

Valuation and growth expectations create pressure. Trading at premium multiples, Blue Owl must deliver consistent growth to justify its valuation. Any stumble—a large credit loss, a failed acquisition, key person departures—could trigger multiple compression.

Key person risk looms large. While having four billionaire founders provides depth, they're all of similar vintage. The next generation of leadership hasn't been clearly established, creating succession risk.

The Balanced View

The truth likely lies between these extremes. Blue Owl has built something genuinely differentiated in asset management, but it's not immune to cycles and competition. The permanent capital model provides stability, but credit losses could still damage returns and reputation. The growth opportunity is real, but execution risk remains high.

General and administrative expenses increased by 41% in 2024, partly due to merger costs and higher distribution expenses, showing that growth comes with costs. The key question: can Blue Owl maintain its growth trajectory while managing expenses and credit risk?

XII. The Future of Alternative Asset Management

Democratization of Alternatives

The next decade will see alternative investments move from institutional portfolios to individual investors. Blue Owl is perfectly positioned for this shift, with BDC structures that provide retail access and partnerships with wealth management platforms. As baby boomers seek yield in retirement and millennials gain wealth, demand for alternative investments will explode.

The Convergence of Public and Private Markets

The lines between public and private markets continue to blur. Companies stay private longer, public companies go private more frequently, and investors demand access to both. Blue Owl's permanent capital vehicles bridge this gap, offering liquidity features that traditional private funds can't match while providing returns that public markets struggle to deliver.

Technology and Direct Origination

Technology will transform direct lending from a relationship business to a data-driven science. Machine learning will enhance credit underwriting, blockchain will streamline loan documentation, and platforms will connect borrowers directly with lenders. Blue Owl's scale provides the resources to invest in these technologies while maintaining the relationship focus that defines the firm.

ESG and Impact Integration

Environmental, social, and governance considerations are moving from nice-to-have to must-have. Blue Owl's focus on middle-market companies positions it to drive ESG improvements where they matter most—in the businesses that form America's economic backbone. The firm's permanent capital model enables long-term thinking about sustainability that short-term fund structures can't support.

The Path to $500 Billion and Beyond

Blue Owl reported record fundraising and deployment, ending 2024 above $250 billion dollars of AUM. To reach $500 billion, the firm must roughly double in size—ambitious but achievable given historical growth rates. The roadmap includes expanding internationally, particularly in Asia where private credit remains nascent; building new product categories like venture debt and real estate credit; and continuing strategic acquisitions to add capabilities and scale.

XIII. Epilogue & Reflections

Is Blue Owl the Next Blackstone or Something Different?

Blue Owl isn't trying to be the next Blackstone—it's building something fundamentally different. While Blackstone epitomizes the traditional alternative asset manager with its focus on buyout funds and carried interest, Blue Owl represents a new model based on permanent capital and fee income. It's less cyclical, more predictable, and arguably more valuable in a world seeking stability.

The question isn't whether Blue Owl will match Blackstone's $1 trillion in AUM—it's whether Blue Owl's model will prove more resilient through cycles. Early evidence suggests it might. While traditional PE firms saw fundraising slow dramatically in 2022-2023, Blue Owl continued growing steadily.

The Transformation of Wall Street

Blue Owl's story reflects a broader transformation of Wall Street. The power has shifted from investment banks to alternative asset managers. The talent has followed—the best and brightest no longer dream of making partner at Goldman Sachs but of launching their own funds. The capital has moved too—institutional investors now allocate more to alternatives than to public equities.

This transformation isn't complete. As banks continue retreating from risk-taking and alternatives become mainstream, firms like Blue Owl will capture increasing shares of global financial activity. The winners won't be the largest or oldest firms but those with the best models for the new reality.

Key Takeaways for Founders

For entrepreneurs considering building in financial services, Blue Owl offers several lessons. First, timing matters more than being first—Owl Rock wasn't the first direct lender, but it launched at the perfect moment. Second, structure can be strategy—the choice of permanent capital vehicles wasn't incidental but fundamental to Blue Owl's success. Third, in mature industries, innovation often comes from combining existing pieces in new ways rather than inventing something entirely new.

Most importantly, Blue Owl proves that even in the shadow of giants, there's room to build something transformative. The founders didn't accept that Blackstone and KKR had permanently won—they found a different game to play.

XIV. Recent News & Developments

Record-Breaking 2024 Performance

Blue Owl reported record fundraising and deployment in 2024, ending the year above $250 billion dollars of AUM. These achievements reflect the ongoing diversification of the business, which stem from product innovation and strategic M&A. The firm's ability to raise capital in a challenging fundraising environment demonstrates the strength of its permanent capital model.

Strategic Acquisitions Reshaping the Platform

Blue Owl's 2024 acquisition spree fundamentally reshaped its capabilities. The firm completed its acquisition of alternative credit manager Atalaya Capital Management, previously announced in July 2024. As of June 30, 2024, Atalaya managed over $10 billion of assets under management. The acquisition price of $450 million is comprised of $350 million of Blue Owl equity and $100 million of cash, with potential for up to $350 million of earnout consideration in the form of equity.

Blue Owl also completed its acquisition of Kuvare Insurance Services LP (KAM), a boutique investment management firm with approximately $20 billion of assets under management as of May 31, 2024. The firm paid $750 million for KAM through a combination of $325 million in cash and $425 million in Blue Owl Class A common stock, with potential for up to a $250 million earnout.

Additionally, Blue Owl completed its acquisition of Prima Capital Advisers from Stone Point Capital. Prima, founded in 1992 by Gregory White, is a real estate lender focused primarily on investing in commercial mortgage-backed securities with approximately $10 billion of assets under management as of March 31, 2024.

Dividend Growth and Shareholder Returns

The company declared a quarterly dividend of $0.18 per Class A Share, payable on February 28, 2025. The annual fixed dividend for 2025 is $0.90, up 25% from the prior year, demonstrating management's confidence in sustainable cash flow generation.

Looking Ahead: The Five-Year Plan

Blue Owl plans to present a detailed 5-year growth plan at their upcoming Investor Day. The announcement of a comprehensive 5-year growth plan signals management's confidence in sustainable long-term expansion. With the integration of recent acquisitions and continued momentum in fundraising, Blue Owl appears positioned to continue its remarkable growth trajectory.

XV. Links & Resources

Blue Owl Investor Relations - Quarterly earnings presentations and financial reports: ir.blueowl.com - SEC filings and prospectuses - Investor Day presentations and strategic updates

Industry Research & Analysis - Private Equity International's PEI 300 rankings - Preqin reports on private credit growth - McKinsey Global Private Markets Review - Cambridge Associates private credit benchmarks

Founder Interviews & Insights - Bloomberg interviews with Doug Ostrover and Marc Lipschultz - Institutional Investor profiles of the founding team - Wall Street Journal coverage of the SPAC merger - Financial Times analysis of the permanent capital model

Books on Alternative Asset Management - "King of Capital" by David Carey and John Morris (Blackstone's story) - "The Masters of Private Equity and Venture Capital" by Robert Finkel - "Private Equity at Work" by Eileen Appelbaum and Rosemary Batt - "The New Tycoons" by Jason Kelly

Regulatory Resources - SEC regulations on Business Development Companies - REIT taxation guidelines from the IRS - Basel III framework and bank capital requirements - Dodd-Frank Act implications for non-bank lenders

Academic Research - "The Growth of Private Credit" - Harvard Business School - "BDC Performance and Structure" - Journal of Financial Economics - "GP Stakes and Alternative Asset Management" - Stanford Graduate School of Business - "Permanent Capital Vehicles in Asset Management" - Wharton Finance

Podcast Episodes & Video Content - "Masters in Business" with Barry Ritholtz featuring alternative asset managers - "The Acquirers Podcast" episodes on private credit - Milken Institute panels on the future of alternative investments - SuperReturn conference presentations on private credit trends

Final Word: Blue Owl Capital's journey from startup to $40 billion market cap giant in less than a decade represents more than just a business success story—it's a blueprint for building in the new financial economy. While the firm faces real challenges and fierce competition, its innovative model, experienced leadership, and structural advantages position it to potentially become one of the defining financial institutions of the 21st century. Whether Blue Owl ultimately reaches its ambitious goals or stumbles along the way, its impact on asset management is already indelible: permanent capital, once a niche strategy, is now the future of alternatives. And three Wall Street veterans who could have coasted to comfortable retirements instead built something that will outlast them all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube