OS Therapies: The Listeria Bet on Rare Cancers

I. Introduction & The "40-Year Drought"

Picture a pediatric oncology ward. A teenager—fifteen, maybe sixteen—has just finished a brutal regimen of surgery and high-dose chemotherapy for osteosarcoma, the most common bone cancer in children and young adults. The primary tumor is gone. The scans look clean. And then the doctors deliver the part that has gutted families for two generations: there is nothing else to give. No maintenance therapy, no consolidation drug, no immunotherapy approved to stop the cancer from coming roaring back in the lungs. They simply wait and watch.

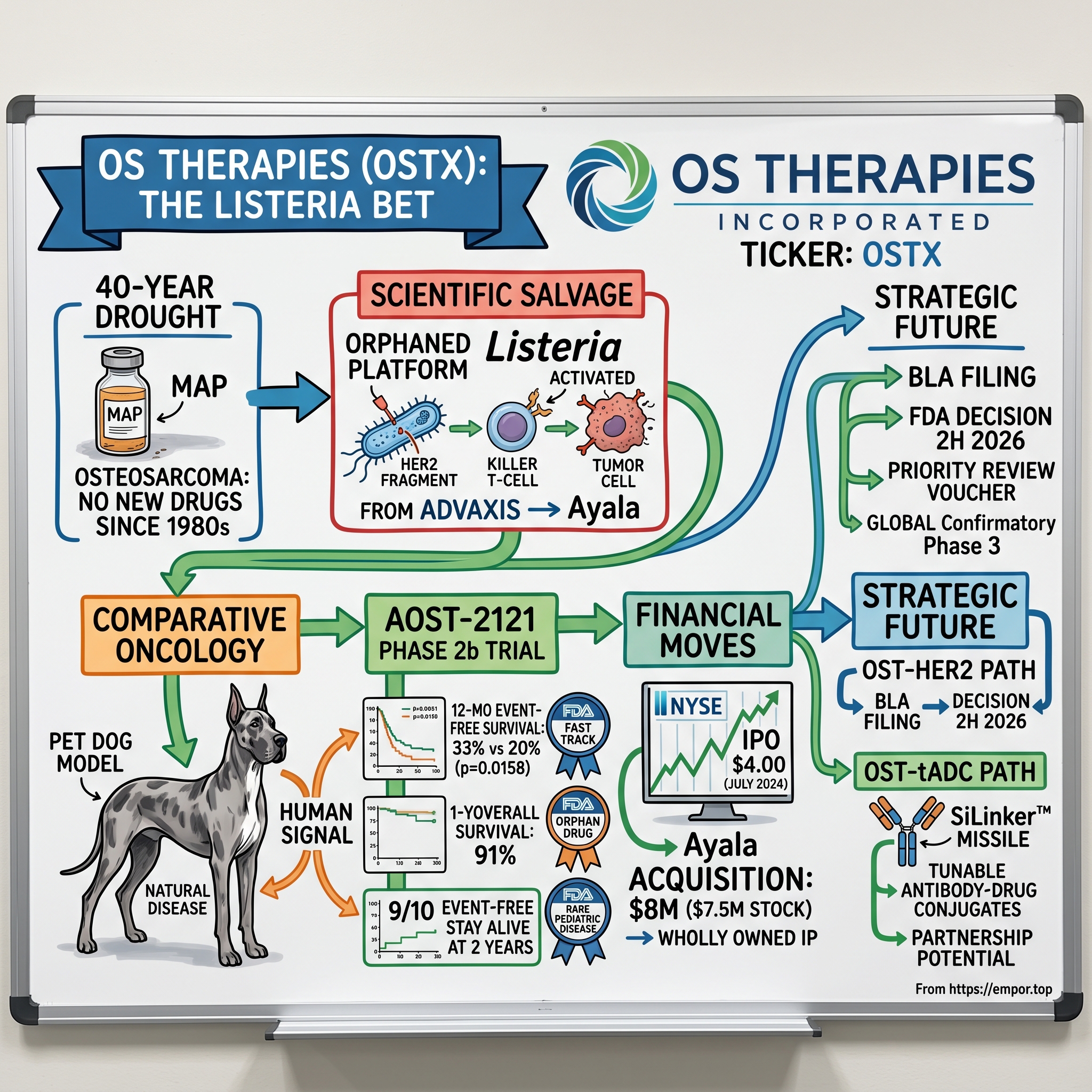

That waiting room has not changed in a very long time. The standard chemotherapy backbone for osteosarcoma—a cocktail known by the brutal acronym MAP (methotrexate, doxorubicin, cisplatin)—was essentially locked in place in the 1980s. The U.S. Food and Drug Administration has not approved a genuinely new osteosarcoma drug in roughly four decades. In a field where lung cancer and melanoma have been transformed by waves of targeted therapies and checkpoint inhibitors, osteosarcoma has been a scientific orphan. The reason is unsentimental: the disease is rare. Only around 1,000 new cases are diagnosed in the United States each year, the majority in children and adolescents. There is no blockbuster waiting at the end of that road, so Big Pharma walked away.

Into that drought stepped a company most investors had never heard of until recently: OS Therapies Incorporated (NYSE American: OSTX), a clinical-stage biotech whose very name—"OS" for osteosarcoma—announces its singular obsession. In January 2025, this tiny company reported something that almost never happens in rare-cancer trials: a clean sweep of positive data from its Phase 2b study of its lead drug, OST-HER2. The trial hit its primary endpoint with statistical significance, and the survival numbers were the kind that make oncologists lean forward.12

Here is the Acquired hook. OS Therapies did not invent its core technology. It did not spend a decade and hundreds of millions of dollars discovering a molecule. Instead, a former pharmaceutical executive named Paul Romness took a platform that a previous public company had spent years and a fortune failing to commercialize—a bizarre, almost science-fiction idea of using live, weakened Listeria bacteria as a cancer vaccine—and pointed it at the one disease Big Pharma had abandoned. He then waited, watched the original owner collapse into a distressed micro-cap, and in early 2025 bought the entire global platform back for roughly the price of a nice house in Palo Alto.

This is a story about scientific salvage, about dogs, about regulatory arbitrage, and about the strange economics of rare disease—where a single FDA approval can generate a tradeable voucher worth more than the entire company's market value. Over the next two hours, we will trace the science of weaponized bacteria, the canine connection that de-risked the human trial, the bargain-basement buyout of Israel's איילה Ayala Pharmaceuticals, and the hidden second platform that could turn a niche bone-cancer player into something much larger. Let us start where the science started—in a Petri dish, with one of the most feared foodborne pathogens on earth.

II. The Science: Weaponizing Listeria

Every parent of a newborn knows the warning: pregnant women should avoid soft cheeses, deli meats, and unpasteurized milk. The reason is Listeria monocytogenes, a bacterium so good at invading human cells that it can cross the placenta and the blood-brain barrier. It causes listeriosis, a foodborne illness that kills a meaningful fraction of those it seriously infects. It is, on paper, the last organism you would want to inject into a sick child.

Which is exactly why it makes a brilliant cancer vaccine—if you can defang it.

Here is the elegant, almost perverse logic. The human immune system has spent millions of years learning to recognize and violently attack Listeria. When the bacterium gets inside a cell, it triggers the body's most powerful weapons: the cytotoxic "killer" T-cells that hunt down and destroy infected cells. Cancer's central trick, by contrast, is invisibility—tumors descend from the body's own cells and learn to whisper "nothing to see here" to the immune system. So the scientific bet was this: what if you took a Listeria bacterium, genetically gutted it so it could no longer cause disease, and then engineered it to carry a piece of a tumor protein on its back? The immune system would charge in to kill the bacteria—and in the chaos, it would also be trained to recognize and attack any cell displaying that tumor protein. You essentially hijack the body's anti-bacterial fury and redirect it at cancer.

The protein OS Therapies' platform targets is HER2, and this is where the story connects to one of oncology's biggest franchises. HER2 is a growth-signaling receptor that, when overexpressed, drives aggressive cancers. It is the target of multibillion-dollar blockbusters: Roche's Herceptin, and more recently the wildly successful エンハーツ Enhertu from AstraZeneca and Japan's 第一三共 Daiichi Sankyo. What most investors do not realize is that osteosarcoma cells frequently express HER2 too—just at lower levels than breast cancer. The HER2 expressed on osteosarcoma is too low for antibody drugs like Herceptin to work well, but it is more than enough for a Listeria vaccine to flag as a target. OST-HER2, then, is a live-attenuated Listeria strain engineered to present a fragment of HER2, teaching the immune system to patrol for and destroy HER2-expressing osteosarcoma cells before they can re-seed in the lungs.3

The platform itself was born not at OS Therapies but at a company called Advaxis Immunotherapies, a New Jersey biotech that spent the better part of two decades championing Listeria as a cancer-vaccine vector. Advaxis built a genuine science—the underlying technology traces to academic work at the University of Pennsylvania—and it ran an ambitious clinical program. But Advaxis made a classic biotech mistake: it aimed at the biggest possible markets. It chased cervical cancer, head-and-neck cancer, and prostate cancer—large indications swarming with competition from far better-capitalized rivals brandishing checkpoint inhibitors. In those crowded, big-market settings, the Listeria platform struggled to differentiate, trials disappointed, and Advaxis bled cash. By the late 2010s the company was a walking cautionary tale, its stock decimated, its platform branded a failure.

But "failed in big markets" is not the same as "failed." The science still worked; it had simply been pointed at the wrong targets. And in 2018, one observer looked at that orphaned platform and saw not a graveyard but a perfectly good engine that needed a different car to drive. That observer was Paul Romness, and the car he had in mind was the disease nobody else wanted. From the wreckage of a big-market strategy, OS Therapies would build a rare-disease company—and that pivot is where our founding story truly begins.

III. Founding & The "Comparative Oncology" Playbook

Paul Romness did not come up through the lab. He came up through the commercial and policy side of big pharmaceuticals, with more than 25 years across Johnson & Johnson, Amgen, and Boehringer Ingelheim—the kind of executive who understands not just whether a drug works, but how it gets reimbursed, how the FDA thinks, and how a small asset can be positioned to matter.4 That blend of commercial instinct and regulatory literacy turned out to be exactly the skill set a salvage operation required.

What gave OS Therapies its emotional engine, though, was not a boardroom—it was the pediatric cancer advocacy community. Osteosarcoma strikes children and teenagers, and the families who live through it form some of the most fiercely motivated patient-advocacy networks in all of medicine. These are parents who have buried children for lack of a second option, and who fundraise relentlessly to change that. Romness formed OS Therapies with a mandate that came, in effect, from those families: take a technology that already showed signals of working, and drive it through the one indication everyone else had written off as too small to bother with. The company's identity—down to its ticker—was built around a single promise to a single community.

But here is where the strategy got genuinely clever, and where OS Therapies' real intellectual edge lives. To de-risk an expensive, ethically fraught trial in children, the company leaned on one of the most underappreciated tools in modern oncology: comparative oncology, the use of pet dogs as a model for human cancer.

Why dogs? Because for osteosarcoma, dogs are the Goldilocks model—not too different, not too artificial, but just right. The laboratory mouse, the workhorse of cancer research, is almost useless here: scientists have to artificially implant tumors into immune-compromised mice, creating an artificial disease in an artificial animal. Pet dogs, by contrast, develop osteosarcoma spontaneously and naturally—same biology, same aggressive metastasis to the lungs, same fundamental disease—but at roughly ten times the human rate. A large dog like a Great Dane or a Rottweiler gets the human disease, in a body with a fully intact immune system, living in the same homes and breathing the same air as people. If an immunotherapy works in a pet dog with naturally occurring osteosarcoma, that is a vastly more credible signal than any mouse could ever provide.

The canine chapter is also the platform's longest track record. Years before OS Therapies existed, Advaxis had licensed its Listeria-HER2 construct to a veterinary biotech called Aratana Therapeutics for animal-health use, where it was developed as AT-014. The pivotal canine work was led by Dr. Nicola Mason at the University of Pennsylvania School of Veterinary Medicine. The results in pet dogs with spontaneous osteosarcoma were striking: in one study, treated dogs achieved a median survival of 956 days versus 423 days for a historical control group—more than doubling survival in a naturally occurring version of the exact disease.5 On the strength of that data, the USDA's Center for Veterinary Biologics granted a conditional license for the canine osteosarcoma immunotherapy in December 2017.6 In plain terms: the platform had already earned a regulatory green light in dogs before it ever faced the FDA in children.

That canine de-risking is the quiet foundation under everything that followed. And to carry the science forward, Romness recruited the one person who knew the molecule better than anyone: Robert Petit, PhD, who had served as Advaxis's chief science officer and now became OS Therapies' Chief Medical and Scientific Officer.7 Petit, in the truest sense, "followed the molecule"—leaving the platform's birthplace to shepherd it into the indication where it might finally matter. With the science in hand, a canine proof point on the books, and a scientist who had lived with the technology for a decade, OS Therapies was ready for the moment that would define it: the human trial.

IV. Clinical Drama: The AOST-2121 Trial

To understand why the next set of numbers mattered so much, you have to understand the specific, merciless setting OS Therapies chose to test in. The trial did not enroll newly diagnosed patients. It enrolled the hardest cases imaginable: patients aged 12 to 39 with recurrent, fully resected, lung-only metastatic osteosarcoma.2

Decode that clinical language and it is harrowing. These are young people whose osteosarcoma already came back at least once and spread to the lungs. Surgeons cut out every visible tumor—"fully resected" means scans show no remaining disease—but everyone in the room knows the statistics. In this population, the cancer almost always returns, and when it does, it is usually fatal. Historically, the one-year event-free survival in this setting—the share of patients who go twelve months without the cancer recurring—hovers around 20%. Four out of five relapse within a year. This is, bluntly, the deadliest stage of an already deadly disease, and it is precisely the setting where a maintenance immunotherapy could prove its worth: the tumor burden is at its lowest, leaving the immune system its best possible shot.

A second-order detail reveals how serious this little company was: its trial partner. OS Therapies ran the study, designated AOST-2121, in collaboration with the Children's Oncology Group (COG)—the National Cancer Institute–supported consortium that is the gold standard for pediatric cancer research in North America. For a micro-cap biotech to run a registrational-grade trial through COG is the clinical equivalent of an unknown band recording at Abbey Road. It lent the data a credibility that no in-house study could match, and it meant the trial was embedded in the academic centers that actually treat these children.

Then came the readout, reported in January 2025—and it was the clean sweep. OST-HER2 hit the primary endpoint: a 12-month event-free survival rate of 33%, versus the 20% historical control benchmark, a difference that reached statistical significance (P = 0.0158).12 In a vacuum, jumping from 20% to 33% might sound modest. In context, it is the difference between one in five and one in three young patients staying cancer-free through the critical first year—in a disease with no approved options at all. The survival data were even more arresting. The one-year overall survival rate reached 91% versus 81% for controls, and as the data matured, the two-year overall survival rate came in at roughly 75%—against historical controls in the 40% range.1 Strikingly, every patient who stayed event-free for at least a year was alive at the two-year mark. For a population expected to be decimated, those are the kinds of numbers that change conversations in oncology clinics.

Just as important as the efficacy was the safety profile and the regulatory scaffolding the program had assembled. Because it works by gently nudging the immune system rather than carpet-bombing the body with cytotoxic chemo, OST-HER2 was generally well tolerated—critical in children who have already endured the "toxic soup" of MAP chemotherapy. And the FDA had stacked the program with the full suite of rare-disease incentives: Fast Track designation (which speeds review and allows rolling submissions), Orphan Drug designation (with its years of market exclusivity and tax benefits), and—most valuable of all—Rare Pediatric Disease designation, the golden ticket that makes the program eligible for a tradeable Priority Review Voucher upon approval.1 We will return to why that voucher may be the single most important asset on the balance sheet. For now, understand that a tiny company had just generated registrational-grade data in an unmet-need indication with every regulatory tailwind the agency offers. The science was no longer the question. The question was ownership—because OS Therapies did not yet fully own the platform it had just validated.

V. The IPO & The Strategic "Clean Up"

By the summer of 2024, OS Therapies needed two things that often work against each other: public capital, and the leverage to clean up its own capital structure. It went after both within the span of six months, and the sequencing was a small masterclass in opportunistic finance.

First, the listing. On July 31, 2024, OS Therapies priced its initial public offering of 1,600,000 shares at $4.00 per share, and the stock began trading on the NYSE American under the ticker OSTX the following day.8 The raise was tiny—roughly $6.4 million in gross proceeds.9 To put that in perspective, $6.4 million would not cover a single mid-sized Phase 3 trial at a typical biotech; it is closer to a seed round than a conventional biotech IPO. But the modest size tells you something about the strategy. OS Therapies was not raising a war chest to discover drugs from scratch. It already had a validated asset and a clear regulatory path. It needed just enough public currency—a liquid, tradeable stock—to fund the run-up to a filing and, crucially, to use its shares as acquisition currency.

Which brings us to the move that defines the company's financial sophistication. Remember that the Listeria platform OS Therapies had just validated in children was not originally its own. The intellectual property had passed, through the wreckage of the Advaxis era, into the hands of איילה Ayala Pharmaceuticals, a company with roots in Rehovot, Israel, that had absorbed the Advaxis assets. OS Therapies had been operating on licensed rights—meaning that if OST-HER2 became a commercial product, a meaningful slice of its future economics would leak away in royalties and milestone payments to Ayala.

So in January 2025—within days of the triumphant Phase 2b readout—OS Therapies struck. It agreed to acquire all of Ayala's Listeria-based immuno-oncology programs and the underlying IP, including direct ownership of the technology behind OST-HER2, plus a Phase 2 lung cancer program and a Phase 1 prostate cancer program as bonus assets.10 The price was the part that makes a financier smile: $8 million total—just $0.5 million in cash and $7.5 million in stock.10 The deal completed in April 2025, leaving OS Therapies the outright owner of the entire global Listeria immuno-oncology platform.11

Sit with the timing and the structure for a moment, because this is the whole game. OS Therapies waited until its lead asset had been de-risked by spectacular clinical data, then bought the platform outright for a sum that, in pharma terms, is a rounding error. And it paid almost entirely in its own freshly minted public stock—using paper, not precious cash, to consummate the deal. In one stroke it eliminated the double-digit royalties and multimillion-dollar milestone payments that would otherwise have shadowed every future dollar of revenue. In effect, the company bought back its own future profit margins at a bargain-basement price, capturing for its shareholders economics that would have flowed to a third party. It is the kind of counter-cyclical, distressed-asset purchase that legendary capital allocators are made of—done by a clinical-stage biotech most of the market had never heard of.

The incentive structure reinforces the alignment. Romness, as CEO, president, and chairman, holds a meaningful equity stake reported in the mid-single-digit-percentage range—he wins big only if shareholders do—and management's compensation has been geared toward hitting the regulatory milestones on the road to a Biologics License Application. With the platform now wholly owned and a clean path to filing, OS Therapies had set the table. But a curious thing happened on the way to the BLA: the company quietly revealed that it had been building a second business in the background—one with nothing to do with bacteria at all.

VI. The "Hidden" Business: The tADC Platform

In September 2024, just weeks after going public, OS Therapies dropped an announcement that, at first glance, seemed to have wandered in from a different company entirely. Alongside its live-bacteria cancer vaccine, it unveiled work on a completely separate modality: tunable antibody-drug conjugates, or OST-tADC.12 For a company defined by Listeria and bone cancer, this was a plot twist—and a window into much larger ambitions.

To appreciate why it matters, you need to understand the antibody-drug conjugate, one of the hottest categories in all of oncology. An ADC is best understood as a guided missile. You take a powerful chemotherapy payload—so toxic you could never inject it freely into the body—and you chemically tether it to an antibody that homes in on a specific protein found on cancer cells. The antibody is the guidance system; the chemo is the warhead; the chemical tether holding them together is called the "linker." The blockbuster Enhertu is exactly this: a HER2-targeting antibody carrying a chemo payload. ADCs have become a multi-tens-of-billions-of-dollars market precisely because they promise to deliver poison to tumors while sparing healthy tissue.

The problem with first-generation ADCs is that the linker is imperfect. Payloads leak off the antibody while it is still circulating in the bloodstream, spilling toxic chemo into healthy organs before the missile ever reaches its target—the dreaded "toxic soup" effect that produces brutal side effects. This is where OS Therapies' twist comes in. Its tADC platform uses a proprietary silicon-dioxide-based, pH-sensitive linker, branded the SiLinker™, plus a pH-sensitive coating over the whole package.13 The trick exploits a quirk of tumor biology: the microenvironment inside and around a solid tumor is more acidic—lower pH—than the rest of the body. The SiLinker is engineered to stay locked shut in the neutral pH of the bloodstream and release its payload only when it senses the acidic conditions of the tumor. It is, in effect, a missile with a fuse that arms itself only over enemy territory. The "tunable" part means the platform can be dialed to release multiple therapeutic agents selectively where they are needed, in theory widening the safety margin dramatically.

Early preclinical data have been encouraging. The first candidate, OST-tADC-FRA-H, pairs a folate-receptor-alpha targeting molecule with a potent exatecan-class payload and showed strong antitumor activity in mouse models of ovarian cancer.14 And in February 2025, OS Therapies formalized the effort by spinning the technology into a dedicated subsidiary, OS Drug Conjugates, while launching a review of strategic options—including joint ventures with clinical-stage ADC companies that could pair their assets with the SiLinker chemistry.13

Strategically, the tADC platform is the company's bridge from "niche orphan" to "big market." Osteosarcoma is a noble but tiny indication; ADCs go after the giants—breast, ovarian, and lung cancers measured in hundreds of thousands of patients. By housing the platform in a separate subsidiary and shopping it for partnerships or licensing, OS Therapies created optionality the market arguably does not yet price in: a second shot on goal in a vastly larger arena, fundable in part by someone else's balance sheet. Whether that optionality becomes real value depends on partners and data still to come. But it reframes what OS Therapies is—not a single-asset bone-cancer bet, but a two-platform company. That reframing sets up the strategic analysis, where we can finally war-game the powers and the risks.

VII. Playbook: Business & Investing Lessons

Strip away the science and OS Therapies is, at its core, a study in strategic positioning—a small player exploiting structural gaps that larger, richer competitors cannot or will not fill. Run it through Hamilton Helmer's 7 Powers framework and two powers stand out clearly.

The first is Counter-Positioning. Big Pharma's business model is built around blockbusters—drugs that can address huge patient populations and justify the billion-dollar cost of development. That model structurally repels rare diseases like osteosarcoma, where the patient count is too small to move a giant's earnings. AstraZeneca and Merck are not going to retool their oncology machines to chase 1,000 American patients a year. OS Therapies counter-positions directly into that blind spot: it pursues the very HER2 target that anchors blockbusters like Enhertu, but in the indication those blockbusters' owners find too small to bother with. The incumbents cannot easily follow without cannibalizing focus and capital from their core franchises—the textbook condition for a counter-positioning advantage.

The second power is a Cornered Resource. After the Ayala buyout, OS Therapies owns the global intellectual property for the Listeria-based immuno-oncology platform outright—the accumulated fruit of two decades of Advaxis's research, plus the canine track record, plus the FDA designations, consolidated under one roof for $8 million. It is, today, positioned as the world leader in Listeria-based cancer immunotherapy. That ownership is not something a competitor can replicate by spending money; it is a specific, hard-won asset that now sits in one company's vault.

But the most distinctive item in the playbook is the "orphan arbitrage"—and it deserves explanation because it is the financial engine that could fund this company without crushing dilution. Under the FDA's Rare Pediatric Disease program, a company that wins approval for a qualifying pediatric drug receives a Priority Review Voucher (PRV)—a transferable coupon that entitles its holder to an expedited FDA review of any future drug, shaving months off the timeline. Crucially, these vouchers can be sold on an open market to large pharmaceutical companies, for whom a few months of earlier launch on a blockbuster is worth a fortune. PRVs have historically traded around the $100 million mark, and the most recent sale, in April 2026, fetched $195 million.15 Consider what that means for a company whose market value has at times been comparable to that single number: an FDA approval could generate, in one non-dilutive stroke, a windfall rivaling the entire enterprise—cash that funds the pipeline without selling a single new share. That is the orphan arbitrage, and it is the reason a rare-disease strategy that looks commercially marginal can be financially explosive.

The final lesson is the comparative oncology model itself. Using spontaneous canine disease to generate credible biological proof before betting on an expensive human trial is a form of cheap, ethical, real-world de-risking that most biotechs never exploit. It accelerated OS Therapies' regulatory path and gave the FDA a richer evidentiary picture—biomarker and survival data from naturally occurring osteosarcoma in dogs running in parallel with the human program. For investors, the meta-lesson is that OS Therapies has repeatedly found leverage in places others ignore: abandoned platforms, abandoned indications, abandoned animal models, and an underused regulatory incentive. Whether that cleverness translates into durable value, though, comes down to the case for and against—which is where the war-gaming gets real.

VIII. Analysis & Bear vs. Bull Case

Every micro-cap biotech is a probability-weighted bet, and OS Therapies is an unusually sharp one—a binary outcome wrapped around a single regulatory decision, with real upside optionality and real existential risk on either side. Let us game both sides honestly.

The bull case starts with the data and ends with the voucher. OST-HER2 has generated statistically significant survival benefits in a lethal indication with zero approved competitors, carrying every regulatory designation the FDA offers. If the agency grants accelerated approval—which management has guided toward the second half of 2026—several things cascade at once.16 First, OS Therapies becomes the company that ended a 40-year drought, with orphan exclusivity protecting a monopoly position. Second, it would become eligible for a Priority Review Voucher that, at recent market prices, could deliver a nine-figure, non-dilutive cash injection—potentially refilling the treasury without diluting shareholders. Third, the wholly owned platform offers expansion shots: the acquired lung and prostate programs, additional HER2 indications, and global filings, with the company having already secured meetings with the FDA, the UK's MHRA, the EMA, and Australia's TGA to design a confirmatory Phase 3 trial.17 And fourth, the hidden tADC platform sits as a free call option—if OS Drug Conjugates lands a partnership with a larger ADC player, the market gets a second reason to re-rate the stock. In the bull scenario, this is the genesis of a durable, multi-asset immuno-oncology platform.

The bear case is equally coherent, and it begins with the thing that makes the science so elegant: live bacteria are hard to make. Manufacturing a live-attenuated Listeria product to pharmaceutical-grade consistency and sterility is genuinely complex—far harder than stamping out small-molecule pills—and chemistry, manufacturing, and controls (CMC) issues are a classic reason the FDA delays or rejects biologics. Second is single-asset risk: despite the second platform, the company's near-term fate rides overwhelmingly on one BLA for one drug. Any delay, any request for additional data, any regulatory stumble, and the entire thesis is in jeopardy. Third is the balance sheet. The first quarter of 2026 showed an operating loss of roughly $10.4 million, more than triple the prior-year quarter, as biomarker and regulatory spending ramped.18 The company raised about $11.2 million in early 2026 and, combined with UK VAT refunds and R&D tax credits, guided to a cash runway "into 2027"—but that is a thin cushion, and a clinical-stage biotech that misses its approval window can be forced into dilutive financing at exactly the worst moment.18 Fourth, the NYSE American listing itself is a structural headwind: it is a less liquid venue than the Nasdaq or the NYSE main board, which can mean wider spreads, thinner institutional ownership, and sharper volatility around news.

Running Porter's Five Forces sharpens the picture. The threat of new entrants into osteosarcoma is paradoxically low—the same tiny market that repels Big Pharma also discourages newcomers, protecting an approved player. Buyer power (here, payers and the small treating-physician community) is muted by the sheer absence of alternatives; a drug that works in a no-option disease commands pricing respect. Substitutes are, today, essentially just chemotherapy and watchful waiting. But the threat of rivalry within the broader immunotherapy and comparative-oncology space is real and worth watching. The most pointed comparison is ELIAS Animal Health, which in March 2025 received full USDA approval for its ELIAS Cancer Immunotherapy in canine osteosarcoma—a different mechanism (a personalized cancer-vaccine-plus-killer-T-cell cell therapy) but the same disease and the same comparative-oncology logic.19 ELIAS validates that the dog-to-human bridge is a crowded idea, and it is a reminder that OS Therapies' efficacy will ultimately be judged not only against historical chemotherapy controls but against an evolving field of immunotherapy approaches. The "supplier" force is embodied in CMC and the live-bacteria manufacturing chain—a genuine concentration of qualitative risk that prudent diligence should weigh heavily.

If an investor watches only a few things on this story, watch these. First and above all, the BLA outcome and its timing—accelerated approval (or not) before the September 30, 2026 window that governs PRV eligibility is the single fact that determines whether the orphan-arbitrage engine fires. Second, the cash runway against the burn rate—with losses now in the eight-figures-per-quarter range, the gap between the current treasury and the next non-dilutive catalyst (approval, a PRV sale, or a tADC partnership) is the company's true survival metric. Those two KPIs, more than any revenue line, are the dials that move this stock.

IX. Epilogue & Final Reflections

As of this writing in May 2026, the countdown is on. OS Therapies has submitted its BLA modules to the FDA under a rolling review, initiated a parallel conditional marketing application with the EMA, and is racing toward a regulatory decision expected in the back half of the year.1618 Maturing survival data—the 2.5-year overall survival readout—is slated for presentation at the ASCO 2026 oncology meeting, the field's premier stage.18 The next two quarters will likely settle, one way or another, whether the 40-year osteosarcoma drought finally breaks.

It is worth pausing on the human core of all this, because it is unusual in biotech. Most drug companies are founded by scientists or financiers chasing a market. OS Therapies was effectively willed into existence by the parents and advocates of children with bone cancer, who refused to accept that "nothing more we can do" was a permanent answer. The company salvaged a discarded technology, validated it first in beloved family dogs, and carried it into a trial run through the gold-standard pediatric cancer consortium—all in service of giving a teenager in that quiet hospital room something the previous generation never had: a next step. There is an emotional clarity to that mission that is rare in the sector.

The investing question that remains is the genuinely hard one, and it resists a tidy answer. Is OS Therapies the seed of the next great oncology platform—a two-modality company that ends a drought, monetizes a nine-figure voucher, and parlays a tunable-ADC technology into the big markets? Or is it a clever, well-executed niche play whose fate hangs on a single regulatory signature and a manufacturing process for live bacteria that has tripped up better-funded companies before? The data are real, the strategy is unusually shrewd, and the optionality is asymmetric. But the binary nature of the bet is equally real. What is not in dispute is the elegance of the underlying maneuver: a tiny company took a pathogen the world fears, a disease the industry abandoned, and a platform a public company gave up on—and bet that, pointed in exactly the right direction, the combination could save children's lives and create real value in the process. By the end of 2026, the world should know whether the bet paid off.

References

-

OS Therapies Announces Statistically Significant Positive Final 2-Year Overall Survival Data from Phase 2b Trial of OST-HER2 — BioSpace, 2025 ↩↩↩↩

-

OS Therapies Announces Phase 2b Clinical Trial of OST-HER2 Achieves Primary Endpoint with Statistical Significance — Business Wire, 2025-01-15 ↩↩↩

-

OST-HER2 Meets Primary End Point of Phase 2b Trial in Lung-Only Metastatic Osteosarcoma — OncLive, 2025 ↩

-

Advaxis's Cancer Immunotherapy Delays Progression of HER2+ Canine Osteosarcoma — PR Newswire, 2015 ↩

-

Aratana Therapeutics Granted Conditional License for a Canine Osteosarcoma Therapeutic — Aratana Therapeutics, 2017-12-20 ↩

-

OS Therapies Completes Acquisition of Advaxis Immunotherapies Clinical, Pre-clinical and IP Assets from Ayala Pharmaceuticals — Business Wire, 2025-04-09 ↩

-

OS Therapies Announces Pricing of its Initial Public Offering on NYSE American — Business Wire, 2024-07-31 ↩

-

OS Therapies Closes $6.4M Initial Public Offering on NYSE American — Olshan Frome Wolosky LLP, 2024 ↩

-

OS Therapies Agrees to Acquire All Listeria Monocytogenes-based Immuno-Oncology Programs and IP Assets from Ayala Pharmaceuticals — Business Wire, 2025-01-29 ↩↩

-

OS Therapies (OSTX) Completes Acquisition of Advaxis Immunotherapies Assets from Ayala Pharmaceuticals — StreetInsider, 2025 ↩

-

OS Therapies Announces Development of Two Novel Tunable Antibody Drug Conjugate (tADC)-Based Therapeutic Candidates — Business Wire, 2024-09-13 ↩

-

OS Therapies Forms Subsidiary OS Drug Conjugates and Initiates Review of Strategic Options for its tunable ADC & Drug Conjugates Platforms — Business Wire, 2025-02-24 ↩↩

-

OS Therapies Announces Positive Efficacy and Safety Data for Ovarian Cancer Therapeutic Candidate Developed Based on tADC Platform Using Proprietary Silicone Linker Platform — BioSpace, 2025 ↩

-

OST-HER2 osteosarcoma drug faces 2026 FDA and EMA decisions — StockTitan, 2026 ↩

-

OS Therapies Initiates US FDA BLA Filing for OST-HER2 in the Prevention or Delay of Recurrent, Fully Resected, Pulmonary Metastatic Osteosarcoma — BioSpace, 2025 ↩↩

-

OS Therapies Granted Meetings with U.S. FDA, U.K. MHRA, EMA and Australian TGA to Review Global Confirmatory Phase 3 Trial for OST-HER2 — Newsfile Corp, 2025 ↩

-

OS Therapies Reports First Quarter 2026 Financials and Provides Corporate Update — StockTitan, 2026 ↩↩↩↩

-

ELIAS Animal Health Receives Full Approval from USDA for the ELIAS Cancer Immunotherapy (ECI) — PR Newswire, 2025-03-19 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube