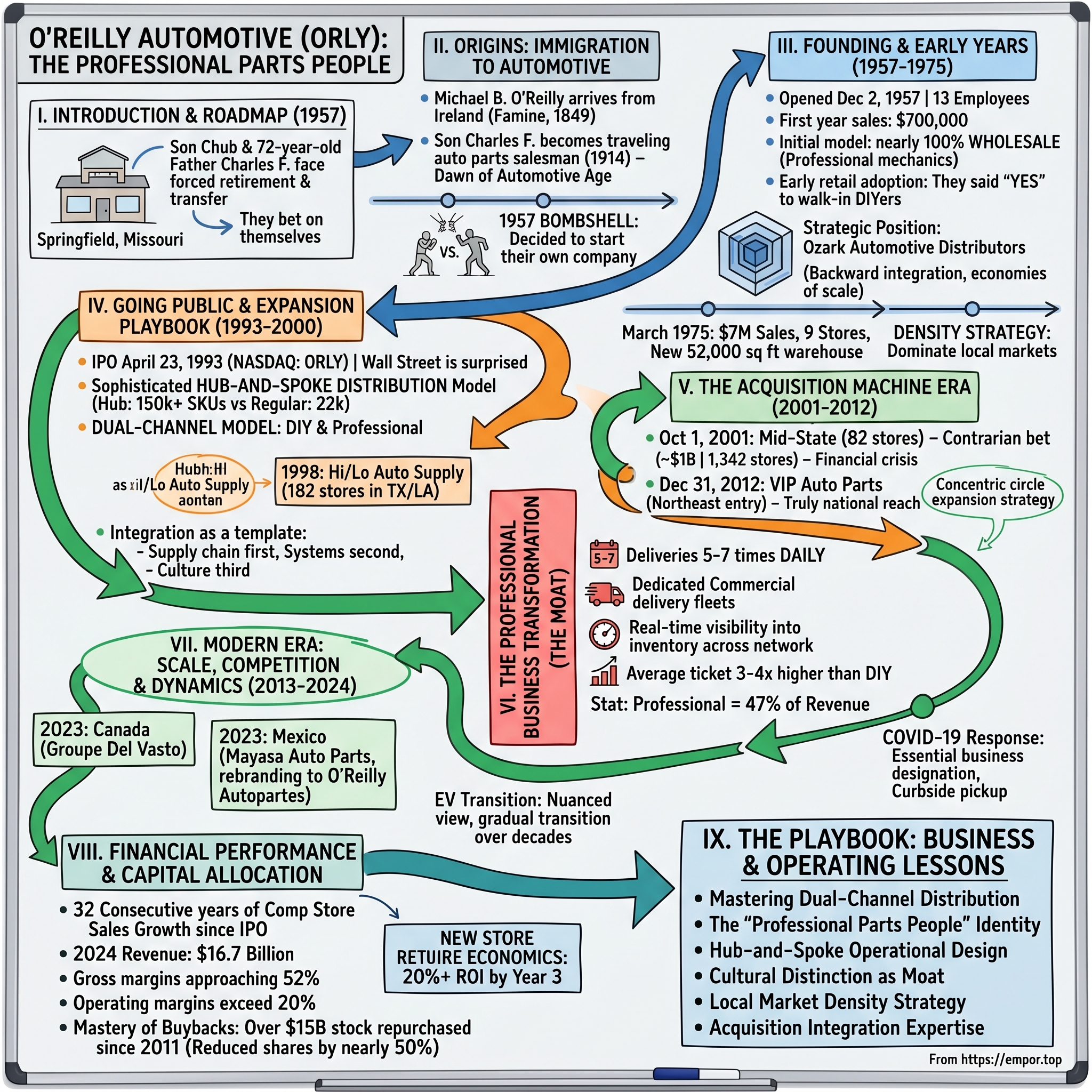

O'Reilly Automotive: The Professional Parts People

I. Introduction & Episode Roadmap

Picture this: It's 1957 in Springfield, Missouri. A 72-year-old auto parts salesman has just been told he's being forced into retirement. His son is being transferred to Kansas City—a corporate reshuffling that would separate a father-son team that had worked together for decades. Most people would accept their fate. The O'Reillys decided to bet everything on themselves instead.

That decision to walk away from secure corporate jobs and start from scratch would eventually build one of America's three dominant auto parts empires. Today, O'Reilly Automotive (NASDAQ: ORLY) operates over 6,000 stores across the United States and Mexico, generating more than $16 billion in annual revenue. The company serves both weekend warriors fixing their own cars (about 50% of sales) and professional mechanics who need parts delivered multiple times per day (47% of sales).

But here's what makes this story remarkable: In an industry dominated by national chains and facing disruption from Amazon, electric vehicles, and changing consumer habits, O'Reilly has delivered 32 consecutive years of comparable store sales growth since going public. While competitors struggle with integration issues and margin pressure, O'Reilly continues to gain market share through a deceptively simple formula that took three generations to perfect.

The central question isn't just how a family business from Missouri's Ozarks became one of the "Big Three" auto parts retailers alongside AutoZone and Advance Auto Parts. It's how they built a culture and operating system so robust that it thrives in an industry most investors consider boring, cyclical, and increasingly threatened by technological change.

This is the story of immigration and ambition, of family dynamics and corporate strategy, of building distribution networks one hub at a time. It's about recognizing that selling auto parts isn't really about inventory management—it's about relationships, speed, and being there when a professional mechanic needs exactly the right part to get a customer's car back on the road. As we'll discover, the O'Reillys understood something their competitors missed: in the auto parts business, professional doesn't just describe your customers—it defines who you need to become.

II. The O'Reilly Origins: Immigration to Automotive

The O'Reilly story begins not in Missouri but in Ireland during the Great Famine. In 1849, Michael Byrne O'Reilly made the journey that millions of Irish were making—escaping poverty and starvation for the promise of America. Landing in St. Louis, he did what ambitious immigrants have always done: worked multiple jobs, saved every penny, and invested in education. Michael worked his way through school to earn a law degree, eventually establishing himself as a title examiner—a respectable middle-class profession that provided stability for his growing family.

His son, Charles Francis O'Reilly, inherited his father's work ethic but found his calling elsewhere. After attending college in St. Louis, Charles F. entered the workforce in 1914 as a traveling salesman for Fred Campbell Auto Supply. This was the dawn of the automotive age—Henry Ford's Model T was transforming America, and with it came an entirely new industry: replacement parts. Charles F. spent his days calling on garages, service stations, and independent mechanics across Missouri, learning not just what parts they needed but understanding their businesses, their challenges, their relationships with customers.

The automotive aftermarket in those days was a relationship business. There were no computerized inventory systems, no overnight shipping from centralized warehouses. Success meant knowing which garage needed what parts, remembering which mechanic preferred which brands, and most importantly, being reliable when someone desperately needed a water pump or alternator to get a customer's car running. Charles F. excelled at this, eventually joining Link Motor Supply Company, one of the region's growing auto parts distributors.

At Link, Charles F. rose through the ranks over four decades, becoming a fixture in the Missouri auto parts scene. By the 1950s, he had brought his son Charles H. "Chub" O'Reilly into the business. Father and son worked as a team—Charles F. with his deep relationships and industry knowledge, Chub with fresh energy and ideas about how to modernize operations. Together, they helped Link expand across Missouri, building one of the state's most successful auto parts operations.

Then came 1957 and the bombshell that would change everything. Link's management announced a reorganization that included two non-negotiable decisions: Charles F., at 72, would be forced into retirement, and Chub would be transferred to the Kansas City office. For most corporate employees, this would be disappointing but acceptable—the price of working for someone else. But the O'Reillys saw it differently. They had spent decades building relationships with suppliers, understanding customer needs, perfecting the logistics of parts distribution. Why should all that knowledge and all those relationships benefit someone else?

The decision to leave Link and start their own company was both brave and calculated. Charles F. had the relationships—decades of goodwill with manufacturers' sales representatives and local garages. Chub had the operational expertise and energy to build something new. But they faced a David-versus-Goliath challenge: Link Motor Supply immediately moved to block them, pressuring manufacturers not to sell to the upstart O'Reilly operation. It was a classic attempt to strangle a competitor in the crib, and by all rights, it should have worked. Link was established, powerful, with leverage over suppliers who couldn't afford to lose such a major customer.

III. The Founding & Early Years (1957–1975)

The O'Reillys' counter-offensive was elegant in its simplicity: they went directly to the human beings they'd been working with for decades. While Link's executives fired off threatening letters from corporate headquarters, Charles F. and Chub were having coffee with the sales reps they'd known for years. "Look," they'd say, "you know us. You know we pay our bills. You know we'll move your product. Are you really going to let some corporate suit tell you who you can sell to?"

One by one, suppliers began to crack. A.C. Delco, one of the most prestigious battery brands, agreed to sell to O'Reilly. Other manufacturers followed. By the time O'Reilly Automotive opened its doors on December 2, 1957, at 403 Sherman Street in Springfield with 13 employees, they had secured enough supplier relationships to stock a competitive inventory. First-year sales in 1958 totaled $700,000—modest by today's standards but enough to prove the concept worked.

The early O'Reilly operation looked nothing like today's retail giants. When the company began, nearly 100% of sales went to wholesale customers—garages, service stations, and industrial accounts with professional mechanics. The retail revolution in auto parts—selling directly to consumers who wanted to fix their own cars—was still years away. O'Reilly was essentially a middleman, buying from manufacturers and selling to professionals who installed the parts.

But even in those early days, subtle shifts were happening that the O'Reillys noticed before their competitors. Americans were keeping cars longer, becoming more comfortable with basic maintenance, and increasingly interested in saving money by doing simple repairs themselves. Gradually, walk-in customers began appearing at the wholesale counter. "Can you sell me just one alternator?" they'd ask. Most wholesalers would have said no—retail customers were a hassle, requiring different inventory systems, different pricing, different service levels. The O'Reillys said yes.

By October 1960, the company had grown enough to backward-integrate through the creation of Ozark Automotive Distributors. This wasn't just expansion—it was strategic positioning. Ozark could buy directly from manufacturers in larger quantities, achieving better pricing and terms. It would then distribute to O'Reilly stores but also to independent jobbers throughout southwestern Missouri. This dual role—competing with customers while also supplying them—required delicate relationship management, but it gave O'Reilly economies of scale that pure retailers couldn't match.

The 1960s and early 1970s were years of steady, methodical growth. While other retailers rushed to open stores across the country, O'Reilly focused on dominating southwestern Missouri. By March 1975, when annual sales hit $7 million and the company built a new 52,000-square-foot warehouse facility, O'Reilly operated just nine stores—all within a tight geographic radius around Springfield.

This density strategy would become a hallmark of O'Reilly's expansion philosophy: dominate local markets before moving to new ones. It meant slower growth but higher profitability. When you have multiple stores in a small area, you can share inventory, transfer parts between locations quickly, and most importantly, afford to stock deep inventory because you're serving a concentrated customer base. A competitor might have 100 stores scattered across ten states; O'Reilly would have ten stores in one city and outsell them all.

IV. Going Public & The Expansion Playbook (1993–2000)

April 23, 1993, marked a watershed moment not just for O'Reilly but for understanding what the company had quietly built over 36 years. When ORLY began trading on NASDAQ and closed at $19.28 per share, Wall Street got its first real look under the hood. What they found surprised them: gross margins approaching 50%, inventory turns that beat most competitors, and a dual-channel model serving both DIY and professional customers that nobody else had successfully cracked.

The roadshow presentations revealed something else: O'Reilly had developed what would later be recognized as one of retail's most sophisticated hub-and-spoke distribution models. While competitors relied on direct shipments from distribution centers to stores, O'Reilly had created an intermediate layer—hub stores that could hold deeper inventory and make multiple daily deliveries to surrounding locations. A regular store might stock 22,000 SKUs; a hub store could access 150,000+ SKUs and get them to any surrounding store within hours.

But the real revelation was the professional business. By 1993, O'Reilly had figured out something that continues to elude many competitors: professional mechanics aren't just commercial customers buying in bulk—they're partners whose success depends on getting exactly the right part, exactly when they need it, at a price that lets them make a profit. O'Reilly's "Professional Parts People" weren't just order-takers; they were consultants who knew the difference between a Motorcraft and a Duralast alternator, who understood which parts could be substituted and which couldn't, who recognized that when a shop calls at 4 PM on a Friday needing a specific water pump, delivering it in 30 minutes versus 3 hours might mean the difference between keeping or losing that customer forever.

The IPO proceeds funded an acceleration of what had been working in Missouri. But rather than scattered expansion, O'Reilly continued its concentric circle strategy—moving into adjacent markets where they could leverage existing distribution infrastructure. Arkansas, Oklahoma, Kansas, Texas—each new market connected to an existing one, allowing the company to achieve distribution density before competitors realized what was happening.

Then came January 30, 1998—the day O'Reilly announced its acquisition of Hi/Lo Auto Supply. For a company that had grown organically for four decades, this was a massive bet: 182 stores across Texas and Louisiana, nearly doubling O'Reilly's footprint overnight. The acquisition price wasn't disclosed, but the strategic value was obvious: Texas was America's second-largest auto parts market, and Hi/Lo gave O'Reilly instant scale in cities like Houston, Dallas, and San Antonio.

The Hi/Lo integration became a template for future acquisitions. Rather than maintaining Hi/Lo as a separate brand or immediately converting all stores, O'Reilly took a measured approach. First, integrate the supply chain—connecting Hi/Lo stores to O'Reilly's distribution network to improve inventory availability. Second, upgrade systems—replacing Hi/Lo's point-of-sale and inventory management systems with O'Reilly's more sophisticated technology. Third, and most importantly, cultural transformation—training Hi/Lo employees in the O'Reilly way of serving both DIY and professional customers.

By 2000, the integration was complete and the results spoke for themselves: same-store sales at converted Hi/Lo locations were growing faster than legacy O'Reilly stores. The company had proven it could successfully acquire and integrate competitors—a capability that would soon be tested on a much larger scale.

V. The Acquisition Machine Era (2001–2012)

The morning of September 11, 2001, changed everything for American businesses. But while most retailers pulled back, O'Reilly closed its Mid-State acquisition on October 1—adding 82 stores across Alabama, Florida, Georgia, Indiana, and Kentucky, plus distribution centers in Nashville and Knoxville. It was a contrarian bet that revealed deep strategic thinking: when the economy weakens, people keep their cars longer and fix them more often. Auto parts is one of the few truly counter-cyclical retail categories.

Mid-State pushed O'Reilly into the Southeast and for the first time into the top five auto parts chains nationally. But the real importance was operational—Mid-State's stores were underperforming, averaging barely $1 million in annual sales versus O'Reilly's $1.8 million average. The transformation of these stores became a masterclass in operational excellence. Within 18 months, Mid-State locations were approaching O'Reilly averages through a combination of improved inventory availability (connected to O'Reilly's hub network), enhanced professional programs (delivery frequency went from once daily to 3-4 times), and cultural change (extensive training in O'Reilly's consultative selling approach).

But all of this was prelude to the deal that would transform O'Reilly from regional player to national powerhouse: CSK Auto. On July 11, 2008—in the depths of the financial crisis—O'Reilly announced it would acquire CSK's 1,342 stores for approximately $1 billion. CSK operated under multiple banners (Checker Auto Parts, Schuck's Auto Supply, Kragen Auto Parts) across 12 western states including California, Arizona, and Nevada. Overnight, O'Reilly would go from 3,219 stores to 4,561 stores, entering the critical California market where it had zero presence.

The timing seemed insane. Lehman Brothers would collapse two months later. Credit markets were freezing. Consumer spending was plummeting. But O'Reilly's leadership saw opportunity where others saw catastrophe. CSK was struggling—same-store sales declining, margins compressing, losing share to AutoZone and O'Reilly itself in overlapping markets. The company needed capital and operational expertise that only a strong acquirer could provide.

The CSK integration would take three years and test every aspect of O'Reilly's operational capabilities. Unlike previous acquisitions where O'Reilly could leverage nearby distribution centers, CSK's western markets required building new infrastructure from scratch. Four new distribution centers had to be integrated, thousands of employees retrained, and most challenging of all, O'Reilly had to prove itself in California—a market with different regulations, different customer preferences, and entrenched competitors.

The cultural challenges were immense. CSK's stores had operated with minimal central control—store managers had significant autonomy over inventory, pricing, and operations. O'Reilly's model was exactly opposite—centralized purchasing, standardized pricing, consistent operating procedures. Many CSK managers resisted, some quit, but those who stayed discovered something surprising: O'Reilly's systematic approach actually gave them more time to focus on customers rather than worrying about back-office operations.

By 2011, the integration was largely complete and the results were staggering: CSK stores that had been declining were now growing same-store sales mid-single digits annually. Professional business at converted stores had doubled. Most impressively, O'Reilly had gained significant market share in California, proving it could compete anywhere.

The December 31, 2012, acquisition of VIP Auto Parts seemed almost anticlimactic after CSK—just 56 stores in Maine, New Hampshire, and Massachusetts. But VIP represented something strategically important: O'Reilly's entry into the Northeast, the last major geographic region where it had no presence. With VIP, O'Reilly now operated in 42 states. The company that started with one store in Springfield now had truly national reach.

VI. The Professional Business Transformation

Inside the auto parts industry, there's a fundamental truth most outsiders miss: the professional business isn't just more profitable than DIY—it's the moat that separates winners from losers. A DIY customer might visit your store once a month; a professional shop might need deliveries four times per day. A DIY customer comparison shops on price; a professional values reliability above all else. And here's the key insight O'Reilly understood before its competitors: serving professionals well requires completely different capabilities than serving retail customers.

Consider a typical professional customer scenario: It's 2 PM on a Tuesday, and Mike's Auto Repair has a customer's Toyota Camry on the lift. Mike discovers the water pump is failing—not what the customer brought the car in for, but it needs immediate replacement. Mike calls his O'Reilly commercial specialist, who confirms they have the exact OEM-specification pump in stock at the hub store. Twenty-three minutes later, an O'Reilly driver walks into Mike's shop with the part. Mike completes the repair, the customer picks up their car at 5 PM as promised, and Mike adds another satisfied customer to his base.

This scene plays out thousands of times daily across O'Reilly's network, but the infrastructure making it possible took decades to build. Start with distribution: O'Reilly operates 29 regional distribution centers, but the real magic happens at the 350+ hub stores. These aren't just bigger stores—they're mini-distribution centers capable of holding 150,000+ SKUs versus the 22,000 in a typical store. When Mike needs an obscure part for a 2007 Volkswagen Passat, the hub store probably has it.

The logistics are mind-boggling. O'Reilly makes 5-7 deliveries daily from distribution centers to stores, and 90% of stores receive multiple deliveries per day. But for professional customers, even that isn't fast enough. So O'Reilly built out dedicated commercial delivery fleets—drivers who know every shop on their route, who understand that delivering to Bay 3 versus the front office might save a mechanic precious minutes, who build relationships that transcend mere transactions.

Technology amplifies these relationships rather than replacing them. O'Reilly's professional customers get dedicated account managers, specialized pricing, detailed purchase histories, and most importantly, real-time visibility into inventory across the entire network. When Mike's shop looks up a part, they see not just whether it's in stock, but exactly where—the store two miles away, the hub store downtown, or the distribution center that can deliver overnight.

The numbers tell the story: Professional business now represents 47% of O'Reilly's revenue, growing from less than 30% two decades ago. Average ticket sizes for professional customers run 3-4 times higher than DIY. And the stickiness is remarkable—once a shop standardizes on O'Reilly, switching costs (new account setup, learning new systems, rebuilding delivery relationships) create powerful retention.

But here's what O'Reilly understood that competitors struggled with: you can't serve professionals with retail employees who happen to answer commercial calls. O'Reilly's "Professional Parts People" undergo specialized training—learning not just parts knowledge but shop operations, warranty procedures, even basic business management. They know that when a shop calls with a comeback (a part that failed prematurely), how that claim is handled can make or break a relationship worth hundreds of thousands in annual purchases.

The investment required is substantial. Each delivery vehicle costs $30,000-40,000. Driver salaries and benefits add up quickly. The technology infrastructure—inventory management systems, B2B portals, electronic cataloging—requires continuous investment. Hub stores tie up millions in inventory. But the returns justify every dollar: professional customers generate higher gross margins (less price-sensitive), better working capital dynamics (commercial credit terms), and most importantly, competitive advantage that's nearly impossible to replicate quickly.

VII. Modern Era: Scale, Competition & Market Dynamics (2013–2024)

By 2013, the North American auto parts industry had crystallized into three giants: AutoZone with its DIY dominance, Advance Auto Parts rolling up regional chains, and O'Reilly with its balanced dual-channel model. But beneath this seemingly stable triumvirate, tectonic shifts were beginning that would test each company's strategy.

The competitive dynamics between the "Big Three" resemble a complex chess match. AutoZone, the largest by store count, doubled down on DIY customers and Mexico expansion. Advance grew through acquisition but struggled with integration—their purchase of General Parts (Carquest) in 2014 created operational challenges they're still unwinding. O'Reilly, meanwhile, chose organic growth and operational excellence, opening 200+ stores annually while maintaining industry-leading margins.

Then came December 18, 2023—O'Reilly's announcement that it would acquire Groupe Del Vasto (Vast-Auto), marking its entry into Canada. The Montreal-based company's 23 stores might seem negligible for a 6,000-store giant, but the strategic implications were significant. Canada's auto parts market remains fragmented, dominated by Canadian Tire and independent operators. O'Reilly's proven ability to consolidate fragmented markets through superior operations suddenly had a new theater.

Mexico represented an even bigger opportunity. O'Reilly had entered Mexico in late 2019 through the acquisition of Mayasa Auto Parts and its 21 ORMA-branded stores. By December 2023, when all 60+ Mexican stores were rebranded to O'Reilly Autopartes, the company had established a beachhead in Latin America's second-largest economy. The Mexican market offers compelling demographics: a growing middle class, aging vehicle fleet (average age over 13 years), and limited organized competition.

But the elephant in every strategic planning session is electrification. EVs require 30% fewer parts than internal combustion engines—no oil changes, no transmission fluid, no spark plugs. Tesla's vertical integration model bypasses traditional parts retailers entirely. The bear case writes itself: O'Reilly is selling buggy whips in the age of automobiles.

Yet the reality is more nuanced. EV adoption remains slower than headlines suggest—EVs represent less than 8% of U.S. new car sales and under 2% of vehicles on the road. The average vehicle age keeps climbing (now 12.5 years), meaning tens of millions of traditional vehicles will need parts for decades. And EVs aren't maintenance-free—they need tires, brakes, suspension components, cabin filters, and collision parts. O'Reilly has quietly built capabilities in EV-specific parts like battery coolants and specialized tools, positioning for a gradual transition rather than disruption.

COVID-19 tested every assumption about retail and supply chains. When lockdowns hit in March 2020, O'Reilly was designated an essential business—keeping America's cars running was critical infrastructure. The company's response showcased operational excellence: stores stayed open with enhanced safety protocols, curbside pickup launched within weeks, and professional delivery never stopped. While other retailers struggled with inventory shortages, O'Reilly's redundant supply chain—multiple distribution centers, hub stores with deep inventory, direct manufacturer relationships—kept shelves stocked.

The inflation surge of 2021-2023 created different challenges. Parts prices rose 20-30%, testing price elasticity. But O'Reilly's dual-channel model proved resilient—professional customers passed costs to consumers, while DIY customers traded down to good/better brands from best. The company's private label strategy, offering quality alternatives at 20-30% lower prices, captured price-conscious demand without sacrificing margins.

Supply chain resilience became a competitive weapon. When semiconductor shortages halted new car production, used car prices spiked, and consumers kept existing vehicles longer—driving parts demand. When overseas shipping delays created shortages, O'Reilly's domestic supplier relationships and inventory depth meant they had parts competitors couldn't source. The company emerged from the pandemic stronger, taking market share from smaller competitors who couldn't match their supply chain capabilities.

VIII. Financial Performance & Capital Allocation

The numbers tell a story of remarkable consistency in an industry known for cyclicality. O'Reilly has delivered 32 consecutive years of comparable store sales growth since its 1993 IPO—a record that spans recessions, recoveries, technological shifts, and a global pandemic. Annual revenue grew from $7 million in 1975 to $16.7 billion in 2024, a compound annual growth rate that would make any Silicon Valley unicorn envious.

The 2024 results exemplify this momentum: revenue of $16.708 billion (up 5.67%), with comparable store sales growing in both professional (mid-single digits) and DIY (low-single digits) segments. But revenue growth only tells part of the story. O'Reilly's operating margins consistently exceed 20%, best-in-class for hardlines retail. Gross margins approaching 52% reflect pricing power, favorable mix shift toward professional business, and growing private label penetration.

The margin architecture reveals sophisticated management. Start with gross margins: professional customers pay slightly less than DIY but buy higher-margin hard parts versus DIY's fluids and accessories. Private label penetration has grown to over 45% of sales, offering 10-15 percentage points better margins than national brands. The company's supply chain efficiency—industry-leading inventory turns despite carrying 150,000+ SKUs—minimizes working capital requirements.

Operating leverage amplifies these advantages. When a store goes from $1.5 million to $2 million in annual sales, most incremental revenue drops to the bottom line—rent doesn't change, you might add one employee, utilities barely budge. This leverage explains why mature O'Reilly stores (open 5+ years) generate EBITDA margins exceeding 30%. The company's ability to consistently grow same-store sales, even by low-single digits, generates enormous profit growth.

Capital allocation mastery distinguishes O'Reilly from retail peers. The company follows a clear hierarchy: first, invest in organic growth (new stores, hub upgrades, technology); second, maintain investment-grade balance sheet (2.5x debt/EBITDAR target); third, return excess cash to shareholders. This discipline has generated extraordinary returns—share repurchases totaling $2.08 billion in 2024 alone, reducing share count by 1.9 million shares.

The buyback program deserves special attention. Since 2011, O'Reilly has repurchased over $15 billion in stock, reducing shares outstanding by nearly 50%. This isn't financial engineering—it's recognition that the company's stable cash flows and modest growth capital requirements generate more cash than can be efficiently redeployed in the business. When your existing stores generate 30%+ returns on invested capital, buying back stock at 15-20x earnings is highly accretive.

Store economics illuminate why O'Reilly can be so aggressive with buybacks. A new store requires roughly $1.5-2 million in total investment (building, inventory, pre-opening expenses). By year three, that store typically generates $2.5-3 million in revenue and $300,000+ in EBITDA—a 20%+ return on investment. But here's the key: mature stores require minimal maintenance capital. Once established, a store might need $50,000 annually in upkeep while generating $500,000+ in cash flow.

Looking to 2025, management's guidance suggests confidence in the model's durability: comparable store sales growth of 2-4%, total revenue of $17.4-17.7 billion, and plans for 200-210 new stores. Diluted EPS guidance of $42.60-43.10 implies continued margin expansion and aggressive buybacks. The company's ability to provide such specific guidance reflects the predictability of the business—a function of market share gains, steady end-market demand, and operational excellence.

IX. Playbook: Business & Operating Lessons

The O'Reilly playbook contains lessons that transcend auto parts, offering insights for any business operating in mature, competitive markets. Start with the most fundamental: mastering dual-channel distribution isn't about serving two customer types—it's about recognizing that different customers have entirely different jobs to be done, and excellence requires distinct capabilities for each.

For DIY customers, the job is education and empowerment. They need confidence that they can complete the repair, access to knowledge (through O'Reilly's staff or online resources), and quality parts at fair prices. For professional customers, the job is speed and reliability—getting exactly the right part exactly when needed, with payment terms and pricing that support their business model. O'Reilly doesn't try to serve both with one model; they built parallel capabilities that share infrastructure but diverge in execution.

The "Professional Parts People" philosophy goes deeper than training. It's about identity—employees don't just work at an auto parts store; they're professional consultants helping other professionals succeed. This cultural distinction matters enormously in hiring, training, and retention. When a commercial specialist spends years building relationships with local shops, those relationships become O'Reilly's moat. Competitors can match prices and inventory, but they can't replicate decades of accumulated trust.

Hub-and-spoke distribution represents another masterclass in operational design. The genius isn't the hub stores themselves—it's the recognition that inventory velocity follows a power law. A few thousand fast-moving parts generate most sales; tens of thousands of slow-moving parts are still essential but unpredictable. By concentrating slow-movers in hubs while keeping fast-movers in every store, O'Reilly achieves seemingly impossible inventory availability without crushing returns on inventory investment.

The acquisition integration expertise developed over decades offers lessons for any serial acquirer. O'Reilly's approach—supply chain first, systems second, culture third—seems counterintuitive but proves brilliant in practice. When acquired stores suddenly have access to 150,000 SKUs instead of 50,000, when delivery frequency jumps from daily to multiple times per day, employees see immediate tangible benefits. This creates buy-in for the harder changes—new systems, new procedures, new cultural norms.

Local market density strategy challenges conventional expansion wisdom. While competitors rushed to plant flags nationwide, O'Reilly methodically dominated local markets before moving to adjacent ones. This density creates multiple advantages: marketing efficiency (one radio ad reaches ten stores not one), logistics optimization (delivery trucks travel shorter distances), inventory leverage (transfer parts between stores in minutes), and talent development (promote managers within the same market).

The company's approach to private label demonstrates sophisticated brand management. Rather than one house brand, O'Reilly maintains multiple private labels positioned at different quality/price points—Ultima (premium), Super Start (value), Precision (professional-grade). This portfolio approach captures consumer surplus across the demand curve while maintaining pricing power for national brands.

Technology adoption shows pragmatic innovation. O'Reilly wasn't first to launch e-commerce or mobile apps, but when they did, the execution was flawless. The company's inventory management system, constantly refined over decades, rivals any Silicon Valley startup's sophistication. But technology never replaces human judgment—store managers can still override automated replenishment for local conditions.

X. Bull vs. Bear Case & Future Outlook

The Bull Case: Compounding Machine in Disguise

The optimistic view starts with market structure. Despite three dominant players, the U.S. auto parts market remains surprisingly fragmented—independents still control 35% share. O'Reilly has proven repeatedly it can acquire and improve underperforming assets. With Advance Auto Parts struggling operationally and potentially divesting stores, O'Reilly could opportunistically add hundreds of locations at attractive valuations.

International expansion offers decade-long growth runway. Mexico's auto parts market is growing 8-10% annually, driven by an aging vehicle fleet and rising middle class. Canada remains highly fragmented with no dominant national player. O'Reilly's operational excellence—honed over 65 years—travels well to markets with similar characteristics but less sophisticated competition.

The EV transition, paradoxically, could strengthen O'Reilly's position. While EVs reduce some maintenance needs, they increase others—tires wear faster due to higher torque, brakes need different service approaches, and collision repair becomes more complex. More importantly, the transition will take decades. Even aggressive EV adoption scenarios show internal combustion vehicles dominating the fleet through 2040. This gives O'Reilly ample time to adapt while generating enormous cash flows from the existing business.

Vehicle dynamics strongly favor continued parts demand. Average vehicle age keeps climbing (now 12.5 years), and new vehicle prices have increased 30%+ since 2020, pushing consumers to keep cars longer. Modern vehicles last longer but require more sophisticated parts when they do need repair. The technical complexity benefits O'Reilly—shade-tree mechanics can't fix today's cars with basic tools, driving more business to professional shops who rely on O'Reilly's parts and expertise.

The Bear Case: Disruption in Slow Motion

The pessimistic view sees multiple threats converging. Amazon's expansion in auto parts—now offering millions of SKUs with same-day delivery in major markets—attacks O'Reilly's core value proposition. While O'Reilly maintains advantages in professional service and immediate availability, Amazon's logistics capabilities and customer reach pose long-term threats, especially for price-conscious DIY customers.

EV adoption might accelerate beyond expectations. If battery costs continue declining and charging infrastructure improves rapidly, the 2030s could see massive fleet transformation. O'Reilly's 6,000 stores and distribution centers could become stranded assets, too many locations for a shrinking parts market. The company's high fixed-cost structure—stores, distribution centers, delivery fleets—provides operating leverage in growth but amplifies pain in decline.

Market saturation looms as a real constraint. With the Big Three operating over 15,000 stores collectively, most attractive U.S. markets are already well-served. New store productivity has been declining—recent openings generate $1.5-2 million annual sales versus $2.5-3 million for stores opened a decade ago. This suggests diminishing returns to domestic expansion.

Autonomous vehicles represent an existential threat nobody fully understands. If self-driving cars become reality, fleet operators might handle all maintenance internally, bypassing traditional parts retailers entirely. Even partial automation could reduce accidents (fewer collision parts needed) and optimize driving patterns (less wear and tear).

The Synthesis: Resilient but Not Invulnerable

The truth likely lies between extremes. O'Reilly faces real challenges but possesses structural advantages and management capability to adapt. The company's 2025 guidance—2-4% comparable store sales growth, 200-210 new stores, EPS of $42.60-43.10—suggests management sees steady state rather than disruption or acceleration.

The business model's resilience has been tested repeatedly—through recessions, technological changes, and competitive threats—and survived each time. This isn't luck but the result of continuous adaptation: adding professional capabilities when DIY growth slowed, expanding private label when national brands got expensive, investing in technology when e-commerce emerged.

International expansion offers optionality without betting the company. If Mexico and Canada prove successful, they could add 5-10% annual growth for a decade. If not, the core U.S. business generates enough cash to fund experiments without jeopardizing dividends or buybacks.

The key insight is that O'Reilly doesn't need to grow rapidly to generate attractive returns. With returns on invested capital exceeding 30% and modest reinvestment requirements, even low-single-digit growth translates to substantial free cash flow. The company can return most earnings to shareholders while still investing for the future—a rare combination in retail.

XI. Epilogue & Final Reflections

Step back and consider what O'Reilly really built: a logistics company masquerading as a retailer, a relationship business hiding behind auto parts, a technology platform wrapped in Missouri practicality. The company that Charles Francis and Chub O'Reilly started in 1957 to escape corporate bureaucracy became one of America's great compounding machines—turning a $700,000 first-year business into a $17 billion enterprise.

What distinguishes O'Reilly from AutoZone and Advance isn't any single factor but the integration of multiple advantages. AutoZone might have more stores, but O'Reilly serves professionals better. Advance might have acquired more aggressively, but O'Reilly integrated more successfully. Both competitors chose focus—AutoZone on DIY dominance, Advance on roll-up economics. O'Reilly chose balance, building capabilities to serve everyone well rather than someone perfectly.

The family business that professionalized without losing its soul offers lessons beyond business. The O'Reillys could have sold out dozens of times—to strategic buyers, private equity, or through different capital structures. Instead, they maintained control long enough to build something lasting, then handed it to professional management who understood what made it special. Today's O'Reilly maintains the customer focus and operational discipline of a family business with the scale and sophistication of a Fortune 500 company.

The surprises in studying O'Reilly are numerous. Who would guess that auto parts retail has better economics than most technology businesses? That serving professional mechanics requires as much sophistication as enterprise software sales? That a company selling oil filters and brake pads would operate one of retail's most advanced distribution networks?

For founders building in "boring" industries, O'Reilly offers inspiration and instruction. You don't need to disrupt or transform or revolutionize—sometimes you just need to execute better than everyone else, every day, for decades. The company's success came not from one brilliant insight but from thousands of small improvements compounded over time. Better inventory systems, faster delivery, deeper product knowledge, stronger relationships—none revolutionary alone, but transformational in combination.

The most counterintuitive lesson might be this: in commodity businesses, culture is competitive advantage. Anyone can stock alternators and brake pads. Price and availability quickly converge among major players. But when a professional mechanic calls needing a part immediately, when a DIY customer needs help diagnosing a problem, when a store manager must decide whether to stock an unusual part—these moments require human judgment, expertise, and commitment that no algorithm can replicate.

O'Reilly understood early what many discover late: in the auto parts business, you're not really selling parts. You're selling confidence—confidence that the part will fit, will last, will solve the problem. You're selling time—getting professionals back to work, getting consumers back on the road. You're selling expertise—knowing which of seventeen different alternators fits a specific vehicle, understanding why one brand costs twice another.

The story that began with an Irish immigrant's son becoming a traveling salesman evolved into something uniquely American: a business built on relationships, scaled through operations, and sustained by culture. Three generations of O'Reillys built not just a company but an institution—one that will likely outlast the family members who created it.

As the automotive industry transforms—through electrification, automation, and changing ownership models—O'Reilly will face new challenges. But if history is any guide, the company will adapt as it always has: methodically, pragmatically, successfully. The professional parts people will continue serving customers who need them, whether those customers are fixing internal combustion engines, electric drivetrains, or technologies not yet invented.

The lesson for investors isn't that O'Reilly is invulnerable—no company is. It's that businesses serving essential needs with operational excellence and cultural strength can compound value for far longer than most expect. In a market obsessed with disruption and transformation, sometimes the biggest returns come from companies that simply execute the basics better than anyone else, year after year, decade after decade.

That's the O'Reilly story: not revolution but evolution, not disruption but execution, not genius but discipline. It's a story that suggests the best businesses aren't always the most exciting ones—sometimes they're the ones that quietly compound excellence while others chase the next big thing.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube