Option Care Health: The Hidden Empire of Home Infusion

I. Introduction and Episode Roadmap

Somewhere in America right now, a nurse is pulling into a suburban driveway with a cooler full of immunoglobulin therapy. She will spend the next two hours setting up an IV line, monitoring a patient with a rare immune deficiency, and documenting everything in a proprietary clinical system that feeds data back to a pharmacy hundreds of miles away. That pharmacy compounded the drug this morning in a sterile cleanroom. A logistics team routed the delivery around weather delays. A care coordinator confirmed insurance authorization three days ago. And the patient never had to leave her living room.

This is the daily reality of Option Care Health, a company that most people have never heard of. Ticker symbol OPCH, headquartered in Bannockburn, Illinois, it is the largest independent provider of home and alternate site infusion therapy in the United States. It operates more than 190 infusion suite locations, employs over five thousand clinicians, and serves patients in all fifty states. In 2025, the company generated roughly $5.6 billion in revenue and completed more than 2.5 million infusion events for over 315,000 unique patients. Its market capitalization hovers around $4.7 billion.

And yet, if you stopped a hundred people on the street and asked them to name the company, you would get blank stares. That anonymity is, in many ways, the point. Option Care Health operates in the plumbing of the American healthcare system, the unsexy but essential infrastructure that moves extraordinarily expensive medications from manufacturers to patients' homes, couches, and kitchen tables. It is a business built on logistics, clinical expertise, and the relentless complexity of getting paid by insurance companies. It is not glamorous. But it is, by almost any measure, one of the most important healthcare businesses in the country.

The story of how Option Care Health got here is a case study in everything that makes American healthcare both maddening and fascinating: private equity rollups, regulatory dysfunction, corporate divestitures, compliance scandals, a once-in-a-century pandemic, and the quiet revolution of moving care out of hospitals and into homes. It is a story about two pharmacists in a small California town, a Walgreens subsidiary nobody wanted, a troubled public company called BioScrip that nearly imploded, and a Harvard-educated CEO who stitched the pieces together into something that actually works.

The big question at the center of this story is deceptively simple: How did a rollup of mom-and-pop pharmacies become the largest independent provider of infusion therapy in America? The answer involves understanding healthcare consolidation, the economics of site-of-care shifts, the private equity playbook in services businesses, and the explosive growth of specialty drugs that cost more per dose than most people earn in a month.

The themes that run through Option Care Health's story are the themes that run through all of American healthcare: the tension between consolidation and competition, the struggle between institutional inertia and innovation, the role of private capital in reshaping public services, and the fundamental question of whether the companies that deliver care should be owned by the companies that pay for it. These are not abstract questions. They determine where patients receive treatment, how much it costs, and ultimately, how well they do.

II. The Home Infusion Category: What Problem Does This Solve?

Picture a cancer patient who needs six weeks of intravenous antibiotics after surgery. Or a child with a primary immune deficiency who requires monthly immunoglobulin infusions for the rest of her life. Or a premature infant who cannot eat and needs total parenteral nutrition delivered directly into the bloodstream through a central line catheter to the heart. Twenty years ago, all of these patients would have sat in a hospital infusion center, sometimes for hours, sometimes overnight, surrounded by beeping machines and the antiseptic smell of institutional healthcare.

The fundamental insight behind home infusion is blindingly obvious once you hear it: most of these patients do not need to be in a hospital. They need the drug, they need a trained clinician to set up the infusion and monitor them, and they need a pharmacy that can compound sterile medications to exact specifications. But the building? The building is optional. Think of it this way: you would not go to a hotel every night just because you need a bed. If you have a bed at home, you sleep there. Home infusion applies the same logic to healthcare. If the medication can be safely administered outside a hospital, why force patients into one?

Home infusion therapy encompasses a wide range of treatments administered intravenously, subcutaneously, or through other parenteral routes outside of traditional hospital settings.

The major therapeutic categories include anti-infective therapies like IV antibiotics, which represent the highest volume category. There is immunoglobulin therapy for patients with immune deficiencies and autoimmune conditions. Total parenteral nutrition provides complete intravenous feeding for patients who cannot absorb nutrients through their digestive system. Chemotherapy and supportive cancer care can be administered at home. And increasingly, complex biologics for chronic inflammatory conditions, neurological disorders, and rare diseases are moving into the home setting.

The economics of this shift are staggering. The mean cost per day of home infusion therapy runs approximately $225, compared to $587 per day in a hospital setting. Put differently, every day a patient receives infusion therapy at home rather than in a hospital saves the healthcare system more than $350. For a six-week course of IV antibiotics, that difference compounds to tens of thousands of dollars. Studies have found that the mean total cost savings for home infusion patients reaches approximately $81,000 compared to inpatient administration. Medicare pays roughly 2.5 times more for identical therapies administered in hospital outpatient departments compared to physician offices or home settings. These are not marginal differences. They are the kind of gaps that get the attention of insurance companies, employers, and government payers who are collectively drowning in healthcare costs.

But cost is only part of the story. Patient outcomes are genuinely better at home. Infection rates are lower because patients are not exposed to hospital-acquired pathogens, a problem so severe that the CDC estimates 1.7 million hospital-associated infections occur in the United States annually. Comfort and compliance improve because people are in their own environment. Readmission rates decline. Patient satisfaction scores are dramatically higher. For chronic conditions requiring ongoing infusions, the quality-of-life difference between spending one day a month in a hospital versus receiving treatment at home while watching television is transformative.

The question, then, is why it took so long for home infusion to become mainstream. The answer lies in the byzantine complexity of American healthcare reimbursement.

Home infusion sits at the intersection of multiple payment systems. Some therapies are covered under the medical benefit of insurance plans, others under the pharmacy benefit. The distinction matters enormously because the authorization processes, reimbursement rates, and even the providers eligible to bill are different under each pathway. Think of it like having two separate toll roads that run to the same destination but charge different prices and require different transponders. Medicare, Medicaid, and commercial insurers each layer on their own rules, covered therapies, and payment schedules.

The Medicare Part B home infusion therapy benefit did not even take effect until January 2021, and it has been so poorly designed that by the second quarter of 2024, only 1,081 Medicare beneficiaries were using it nationally. That number is not a typo. Out of more than 65 million Medicare enrollees, barely a thousand were accessing a benefit specifically created for them. The regulations require a nurse to be physically present in the home for billing purposes, even though most home infusion patients self-administer after initial training. Bipartisan legislation called the Preserving Patient Access to Home Infusion Act has been introduced to fix this, but as of early 2026, it has not yet passed.

Despite these barriers, the U.S. home infusion therapy market reached approximately $19.6 billion in 2024 and is projected to grow to nearly $40 billion by 2035, a compound annual growth rate of roughly 7.3 percent. Every structural force in healthcare is pushing in the same direction: out of the hospital, into the home. Understanding whether Option Care Health can capture its share of that growth requires going back to the very beginning.

III. The Fragmented Origins: Regional Players and Industry Structure

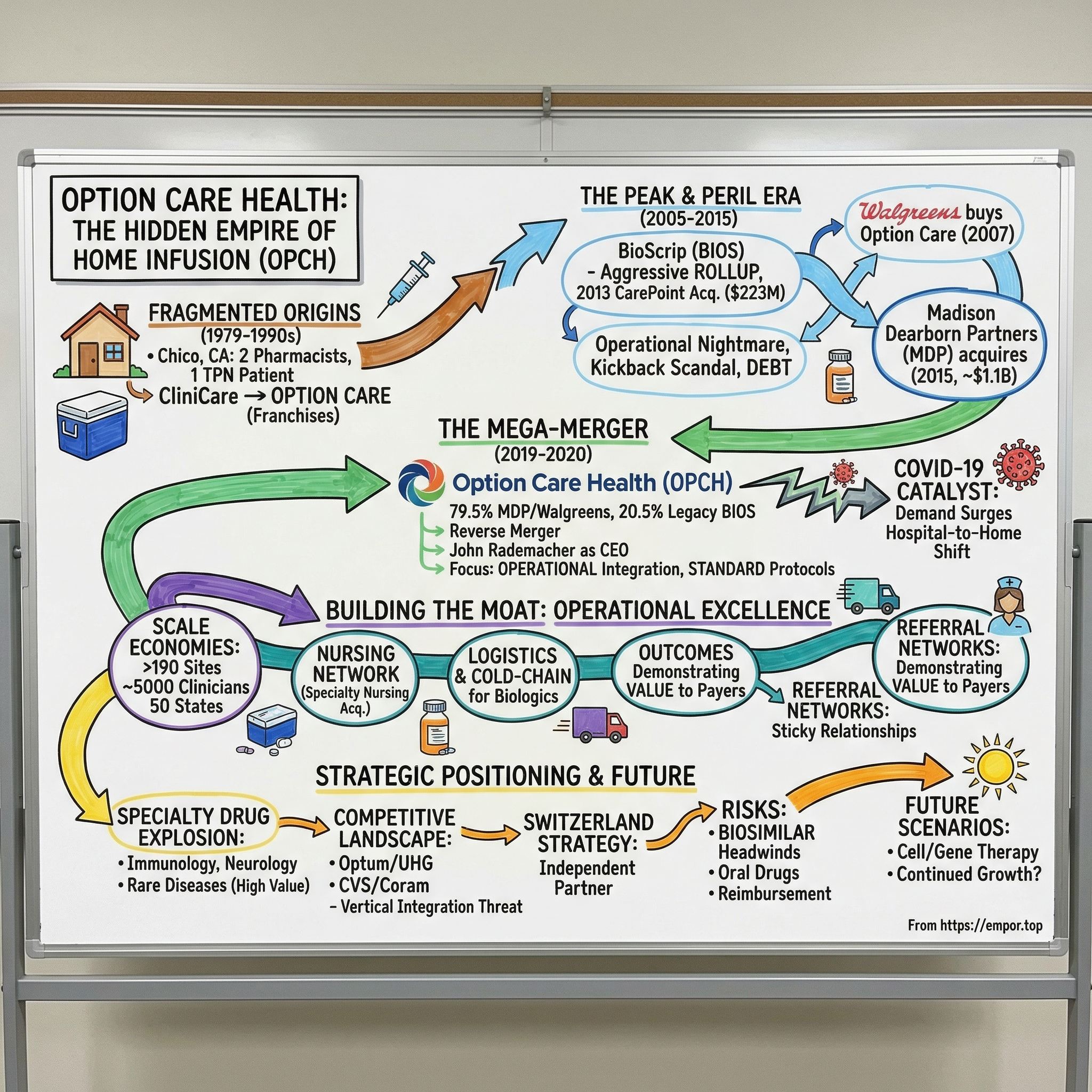

In 1979, in the small Northern California city of Chico, two pharmacists named Michael Prime and Mitchell Hoggard had a problem with a single patient. A young man injured in a car accident needed daily intravenous nutritional feedings, a treatment called total parenteral nutrition. The patient was making the trip to the hospital every single day to pick up sterilely prepared solutions that took twelve hours to infuse at home through a pump and central line catheter. It was miserable, inefficient, and expensive. Prime, who was part-owner of the oldest retail pharmacy in Chico, and Hoggard, who worked as a pharmacist at a small community hospital fifty miles north, looked at this situation and asked the question that would birth an industry: What if we just did this ourselves?

They started compounding the TPN solutions in their own pharmacy and delivering them directly to the patient's home. It was, in the most literal sense, a two-man operation solving a problem for a single family. When they were comfortable with their first two patients by 1981, they began marketing their services to local physicians, positioning themselves as a cheaper alternative to hospital care. Referrals trickled in, then flowed steadily. They expanded from TPN into IV antibiotics, chemotherapy, hydration, pain management, and enteral feedings.

The company was originally called CliniCare, a clean, clinical name that worked fine until Prime and Hoggard tried to license it for expansion and discovered it was already registered by another organization. A marketing team member devised a creative solution: the acronym O.P.T.I.O.N. Care, standing for Outpatient Parenteral Therapy Intravenous On-going Nutrition with Care. It was clunky, perhaps the most forced acronym in healthcare history, but it stuck. By the early 1990s, they had simplified it to just Option Care and were growing through a franchise model, expanding their footprint nationally.

What Prime and Hoggard had stumbled onto was not just a better way to deliver TPN. They had identified a structural gap in the American healthcare system: hospitals were extraordinarily expensive places to administer routine therapies, and there was no organized infrastructure to do it elsewhere. Throughout the 1980s and 1990s, hospital pharmacies across the country began spinning out home infusion services, and entrepreneurial pharmacists launched independent providers in their communities. The industry grew organically but chaotically, with hundreds of small regional players serving local markets.

The fragmentation was not accidental. Home infusion is a surprisingly complex business. It requires state-by-state pharmacy licensure, compliance with sterile compounding regulations from the FDA, cold-chain logistics for temperature-sensitive biologics, a network of trained nurses who can travel to patients' homes, twenty-four-hour clinical support, and the operational capacity to navigate dozens of different insurance reimbursement systems simultaneously. Local relationships mattered enormously. Physicians referred patients to providers they knew and trusted. Hospital discharge planners worked with the same home infusion pharmacy for years. These relationship-based switching costs kept the market local.

This complexity created both opportunity and barrier. Well-run local providers could build defensible positions in their communities, but scaling nationally was extraordinarily difficult. The operational challenges of managing clinical quality, logistics, and billing across multiple states kept the industry fragmented long after other healthcare services had consolidated. By the early 2000s, the home infusion landscape was a patchwork of more than eight hundred independent providers, a handful of struggling national chains, and a few health system-owned programs. It was a market that looked ripe for consolidation on a spreadsheet but resisted it in practice. The irony of the home infusion industry's early decades is that its fragmentation was both its greatest weakness and its greatest resilience. Small providers could not negotiate effectively with large payers, invest in technology, or achieve operational efficiencies. But they also could not fail spectacularly, because their local relationships and community roots provided a floor of demand that sustained them through economic cycles and regulatory changes. The question was whether anyone could capture the scale benefits of consolidation without destroying the local relationships that made the business work.

IV. The Private Equity Era: BioScrip's Rise and Fall

While Option Care was growing steadily under its franchise model and eventually attracting Walgreens' attention, a very different company was taking a very different approach to the home infusion market. BioScrip was born in 2005 from the merger of two companies that shareholders approved on March 9 of that year: MIM Corporation, a pharmaceutical healthcare organization with PBM and therapeutic management capabilities, and Chronimed Inc., a Minnetonka, Minnesota-based specialty pharmacy that distributed prescription drugs and operated thirty-three distribution centers. The combined entity, trading on NASDAQ under the ticker BIOS, was positioned as a diversified pharmacy services company with six product lines spanning specialty pharmacy, infusion, PBM services, and traditional pharmacy.

The thesis was classic rollup thinking applied to healthcare: consolidate fragmented assets, build scale, negotiate better rates with payers, and extract operational synergies. BioScrip's leadership saw the home infusion market the way a real estate developer sees a neighborhood of small houses: tear them down individually, build something bigger, and capture the premium that comes with scale.

But BioScrip made a fateful strategic choice in 2012 that would define its trajectory. The company sold its specialty and mail-order pharmacy divisions to Walgreens for $225 million, narrowing its focus exclusively to home infusion. It was a bold bet on a single market, and it required the company to grow aggressively to justify its public market valuation. With the proceeds burning a hole in its balance sheet, BioScrip went shopping.

The centerpiece of that growth strategy was the June 2013 acquisition of CarePoint Partners Holdings for $223 million in cash. CarePoint, backed by Chicago private equity firm Waud Capital Partners, had been formed in 2008 specifically to roll up smaller home infusion providers. On paper, the combination would create a formidable national platform. Management estimated the integration would take twelve to fifteen months.

What followed was a case study in everything that can go wrong with a healthcare rollup. Integration proved far more difficult than anticipated. Each acquired provider had its own clinical protocols, IT systems, billing practices, and local relationships. Standardizing operations across dozens of facilities while maintaining clinical quality and managing hundreds of payer contracts simultaneously was an operational nightmare. By the second quarter of 2014, BioScrip was reporting revenues of $247 million but net losses of $18.6 million. Revenue had jumped 43 percent year-over-year thanks to the CarePoint acquisition, but the company was bleeding money trying to digest it.

Then came the compliance disaster. BioScrip became embroiled in a kickback scheme involving Novartis Pharmaceuticals and the drug Exjade, approved by the FDA in late 2005 for chronic iron overload. Novartis leveraged its control over patient referrals to pressure specialty pharmacies, including BioScrip, to hire nurses who would call patients and encourage them to order more refills under the guise of education and clinical counseling. BioScrip employees made thousands of calls from a central call center in Ohio to Medicaid recipients, encouraging refills and, critically, downplaying Exjade's side effects. The joint state-federal investigation was triggered by a whistleblower lawsuit filed under the False Claims Act and involved the U.S. Attorney's Office for the Southern District of New York, the FBI, and multiple state attorneys general. BioScrip agreed to pay $15 million to settle claims, part of a broader resolution exceeding $75 million across federal and state claims. A July 2019 FDA inspection of a BioScrip facility in Chantilly, Virginia later found serious deficiencies in sterile drug product practices, resulting in a formal warning letter. For a company whose entire value proposition rested on safely compounding and delivering sterile medications, this was existential.

By 2017, BioScrip was in deep trouble: stock languishing, market share eroding, leadership turning over, debt load constraining investment. The aggressive rollup strategy had created scale without creating value. It was a cautionary tale that Option Care's future leaders would study carefully.

Meanwhile, Option Care was charting a quieter, steadier course. Walgreens had acquired the company in 2007 for $760.5 million, or $19.50 per share, with a total enterprise value of approximately $850 million. The strategic rationale was straightforward: expand Walgreens' patient care capabilities and compete with CVS, which had recently become the largest specialty pharmacy through its acquisition of Caremark. Option Care operated as Walgreens Infusion Services, running more than one hundred pharmacy locations nationwide.

But Walgreens, like many large corporations that acquire specialized healthcare businesses, struggled to integrate home infusion into its retail pharmacy model. Filling prescriptions at a drugstore counter and compounding sterile IV medications in cleanrooms for delivery to critically ill patients are fundamentally different operations. By 2015, Walgreens was ready to move on.

In January 2015, Madison Dearborn Partners, a leading Chicago-based private equity firm founded in 1992, acquired the majority of Walgreens Infusion Services for approximately $1.1 billion. Walgreens retained a minority ownership stake. The business was rebranded as Option Care in May 2015 and began operating independently from Bannockburn, Illinois. Under Madison Dearborn's ownership, the company invested heavily in its operating model, people, process, technology, and facilities, reimagining pharmacy, nursing, care management, logistics, and revenue cycle management. Unlike BioScrip's strategy of growth through acquisition, Madison Dearborn focused on operational improvement within the existing footprint. It was less exciting but far more sustainable. And it would set the stage for the most consequential transaction in the history of home infusion.

V. The Mega-Merger: Option Care Plus BioScrip

On March 15, 2019, the boards of Option Care and BioScrip announced what they carefully described as a merger of equals. It was, in reality, nothing of the sort. Option Care's owners, Madison Dearborn Partners and Walgreens, would control 79.5 percent of the combined company. Legacy BioScrip shareholders would hold the remaining 20.5 percent. The deal was structured as an all-stock reverse merger: Option Care, the private company, merged into BioScrip, the public company, with BioScrip issuing 542 million new shares to Option Care's shareholders. The surviving entity would be renamed Option Care Health.

The architecture of the deal was clever in a way that only healthcare finance nerds could fully appreciate. By merging into BioScrip's public shell, Option Care gained access to the public markets without going through the expense and uncertainty of a traditional IPO. BioScrip's shareholders got a lifeline for a company that had been slowly drowning. Madison Dearborn got a path to liquidity for its investment. And the combined company got something none of the individual entities could have achieved alone: true national scale to become the largest independent home and alternate site infusion services provider in America.

The strategic logic was compelling. Option Care and BioScrip had largely complementary geographic footprints. Combining them would create a network covering more than 90 percent of the U.S. population. Scale would bring negotiating leverage with payers and drug manufacturers, the ability to spread fixed costs across a larger revenue base, and the clinical depth to serve the most complex patients. Kirkland & Ellis advised Option Care on the transaction.

But the merger's success or failure would ultimately come down to one thing: execution. And that meant one man.

John Rademacher had been named CEO of Option Care in January 2018, after serving as interim CEO since August 2017 and as Chief Operating Officer since joining the company in 2015. His background was not in pharmacy or home infusion. He had spent nearly twelve years at Baxter International leading global businesses in renal care, including a stint living in Sweden as Global Franchise Head for In-Center Hemodialysis following Baxter's acquisition of Gambro. Before Baxter, he had been at Cardinal Health, running both the Ambulatory Care Division and the Nuclear and Pharmacy Services divisions. He started his career at Eli Lilly. He held a BA in economics from DePauw University and an MBA from Harvard Business School. He was, in short, a healthcare operations executive who knew how to run complex, logistics-intensive businesses at scale, exactly the profile needed for what was about to happen.

Rademacher brought a relentlessly operational mindset to the merger integration. Rather than pursuing the financial engineering approach that had characterized BioScrip's own failed strategy, he focused on the unglamorous work of standardizing clinical protocols, harmonizing IT systems, rationalizing facilities, and building a unified culture. BioScrip's culture had been shaped by years of financial distress, compliance problems, and leadership turnover. Option Care's culture, forged under Madison Dearborn's ownership, was more operationally focused. Merging them was as much a human challenge as a systems challenge.

The merger closed on August 7, 2019. Six months later, COVID-19 hit.

The pandemic could have been catastrophic for a company in the middle of a complex integration. Instead, it became an accelerant. As hospitals became overwhelmed with COVID patients and tried to discharge everyone who did not absolutely need to be there, demand for home infusion services surged. Patients who might have continued receiving infusions in hospital outpatient centers were suddenly highly motivated to stay home. Physicians who had been slow to refer patients to home infusion began sending them in droves. Payers who had been resistant to covering home infusion became eager to shift patients to lower-cost settings.

In February 2020, Option Care Health completed a one-for-four reverse stock split and began trading on the NASDAQ Global Select Market under the new ticker OPCH. The rebranding was complete. Within eighteen months of the merger closing, the combined entity had gone from two struggling companies to the clear market leader.

The results spoke in numbers that were impossible to argue with. Revenue grew from approximately $3 billion in the first full year post-merger to $3.44 billion in 2021, then to $3.94 billion in 2022. Adjusted EBITDA expanded from roughly $194 million in 2020 to over $260 million in 2021 and more than $310 million in 2022. The company was not just growing; it was growing profitably, demonstrating the operational leverage that comes from spreading fixed costs across a larger base. What had looked like a financial engineering deal turned out to be a genuine operational transformation, one driven not by spreadsheet magic but by the hard, patient work of making two companies actually function as one.

VI. Building the Moat: Operational Excellence and Network Effects

After the merger dust settled and COVID unexpectedly validated the home infusion thesis, Rademacher and his team turned to the long-term question that separates good companies from great ones: How do you build a durable competitive advantage in a business that, at its core, is about mixing drugs in a pharmacy and delivering them to people's homes?

The answer was not any single brilliant insight. It was the relentless accumulation of small advantages across every dimension of the business, what a manufacturing executive might call kaizen, continuous improvement, applied to healthcare logistics.

Start with the clinical operation. Option Care Health standardized clinical protocols across its entire network, creating consistent treatment guidelines for more than forty therapeutic categories. This was not just an efficiency play. Standardized protocols meant better outcomes data, which meant the company could demonstrate to payers and referral sources that its patients did better, had fewer complications, and cost less than patients treated in other settings. In healthcare, outcomes data is currency. The more patients you treat, the more data you generate. The more data you generate, the more convincingly you can demonstrate value. The more convincingly you demonstrate value, the more referrals you attract. It is not a traditional technology network effect, but in a clinical services business, it functions like a flywheel that accelerates with scale.

The nursing network became a strategic asset in its own right. Option Care Health employed more than five thousand clinicians, including pharmacists, nurses, and dietitians. In April 2022, the company deepened this advantage by acquiring the Specialty Pharmacy Nursing Network for $60 million in cash, adding more than four hundred specialty nurses to its roster. Having a large, trained, reliable nursing workforce matters enormously because the nationwide nursing shortage makes it progressively harder for smaller competitors to staff their operations. If a regional provider cannot find enough nurses, it cannot serve patients, regardless of how many referrals it receives. Option Care's scale gives it recruiting advantages, the ability to offer better compensation, benefits, and career development, that smaller competitors simply cannot match.

Technology investments compounded the advantage. The company built proprietary pharmacy management systems and invested in logistics optimization to coordinate the movement of temperature-sensitive medications across the country. A cold-chain logistics operation for biologics is nothing like shipping consumer goods. These drugs must be stored and transported within narrow temperature ranges, compounded in sterile environments following strict regulatory protocols, and delivered within precise time windows. Getting this wrong does not mean a returned package. It can mean a dead patient. The operational complexity creates a barrier to entry that is invisible to outsiders but formidable to anyone who has tried to build it from scratch.

Geographic density became a deliberate strategy. Rather than trying to be everywhere at once, Option Care Health focused on building deep coverage in major metropolitan areas and filling gaps between them. By 2025, the company operated 92 full-service pharmacies and 93 stand-alone ambulatory infusion suites across 43 states, contracted with 96 percent of insured patients in the United States. This density matters for two reasons. First, it reduces delivery costs because drivers and nurses are not covering vast distances between patients. Second, it makes the company a more attractive partner for national payers who want a single vendor that can serve their members across the country, rather than contracting with dozens of regional providers.

The referral network is perhaps the most underappreciated competitive advantage. In home infusion, patients do not choose their provider the way they choose a restaurant. Physicians, hospital discharge planners, and specialty clinics make the referral. Once a provider has established relationships with the referring institutions in a market, those relationships become sticky. A new entrant cannot simply open a pharmacy and expect patients to arrive. They must build trust one referral source at a time, which takes years. Just as Amazon spent years building warehouses, delivery networks, and software systems that eventually created a nearly insurmountable advantage in e-commerce fulfillment, Option Care Health has built pharmacies, nursing networks, clinical protocols, and payer relationships that create an increasingly difficult-to-replicate advantage in healthcare delivery. The individual components are not proprietary or patented. But building all of them simultaneously, at national scale, with consistent clinical quality, requires the kind of institutional knowledge that cannot be purchased overnight.

VII. The Specialty Drug Explosion and Strategic Positioning

To understand why Option Care Health's revenue nearly doubled in just five years, you need to understand what has been happening in the pharmaceutical industry. And what has been happening is, by any historical standard, extraordinary.

Walk into any hospital pharmacy today and compare the drug formulary to what was available in 2010. The transformation is dramatic. An entire generation of specialty drugs, biologics derived from living cells, monoclonal antibodies that target specific disease pathways, gene therapies that literally rewrite patients' DNA, has moved from the laboratory to clinical practice. These are drugs that do things that were science fiction two decades ago: halting the progression of multiple sclerosis, putting rheumatoid arthritis into remission, treating previously untreatable genetic diseases.

These drugs share a common characteristic that matters enormously for our story: most of them cannot be taken as a pill. They must be infused intravenously or injected subcutaneously, often by or under the supervision of a trained clinician. They frequently require cold-chain storage and transportation. And they often require ongoing patient monitoring for adverse reactions. In other words, they are perfect candidates for home infusion. If traditional IV antibiotics were the bread and butter of home infusion, specialty biologics are the filet mignon.

Option Care Health pivoted aggressively toward these higher-value therapies. The company's therapeutic portfolio expanded to encompass immunology, oncology support, neurology, anti-infectives, nutritional support, heart failure therapies, rare and orphan disease treatments, and chronic inflammatory conditions. The financial implications were profound. A course of immunoglobulin therapy for a patient with primary immune deficiency can cost $30,000 to $50,000 annually and continues for the patient's entire life. A biologic like Stelara for Crohn's disease can cost $20,000 or more per year. These are chronic, recurring revenue streams with high patient retention, the pharmaceutical equivalent of subscription revenue.

The company's revenue increasingly split between acute therapies, primarily anti-infectives and nutritional support representing roughly three-quarters of the portfolio, and chronic therapies including immunoglobulins and biologics representing about one-quarter but growing faster.

The chronic category carries the strategic significance because these patients remain on therapy for years or decades, providing predictable revenue that smooths out the inherent volatility of acute care referrals. In 2025, acute therapies grew at a mid-teens rate while chronic therapies grew at a low double-digit pace, but the chronic segment's stickiness and lifetime patient value make it the more strategically important category.

The partnership model with pharmaceutical manufacturers added another dimension. As drug companies launched new biologics, they needed infrastructure to get those drugs to patients outside of hospital settings. Option Care Health's national network, clinical expertise, and outcomes data made it an attractive partner for patient support programs and hub services. The company essentially became a distribution and clinical services platform that drug manufacturers needed, positioning itself as an essential node in the specialty drug supply chain.

However, the specialty drug pivot came with a significant risk that materialized starting in 2025: biosimilar competition. Biosimilars are essentially generic versions of biologic drugs. When lower-cost biosimilar versions of blockbuster biologics like Stelara entered the market, they created pricing pressure that flowed directly through to Option Care Health's revenue and margins. The company disclosed that Stelara biosimilar adoption created a 160-basis-point revenue headwind in 2025 and projected a roughly 400-basis-point revenue growth drag plus a $25 to $35 million gross profit hit in 2026. The FDA approved 19 biosimilars in 2024 alone, with 38 more applications under global review targeting the U.S. market, signaling that this dynamic will recur with other drugs.

This is the double-edged sword of the specialty drug opportunity. Higher-value therapies drive revenue growth and provide recurring patient relationships, but the same forces that make these drugs expensive eventually give way to lower-cost alternatives. The company's ability to manage this transition, growing volume faster than price declines, will be a defining challenge. There is a silver lining: biosimilars could expand the addressable market by making expensive therapies accessible to patients who could not previously afford them, driving more total infusion volume to home settings.

VIII. The Competitive Landscape and Market Dynamics

If you want to understand the strategic pressure facing Option Care Health, you need to understand one trend above all others: vertical integration. The American healthcare system is consolidating at a pace that would make Gilded Age industrialists raise an eyebrow. Insurance companies are buying providers. Pharmacy benefit managers are buying pharmacies. Hospital systems are buying physician practices. And at the apex of this consolidation sit a handful of vertically integrated healthcare conglomerates that control patients from insurance enrollment to drug delivery.

The most formidable is UnitedHealth Group, which through its Optum division operates one of the largest home infusion businesses in the country. When UnitedHealth acquired Amedisys after prolonged DOJ antitrust review, requiring the divestiture of 164 home health and hospice facilities across 19 states, it further cemented its dominance. Optum's BriovaRx infusion services division draws on a captive referral base of UnitedHealthcare's insurance members. Investigative reporting has shown that UnitedHealthcare pays Optum providers 17 percent more than non-Optum providers, a figure that rises to 61 percent more in markets where UnitedHealthcare has over 25 percent market share. This kind of patient steering represents an existential competitive threat to independent providers.

CVS Health presents a similar challenge through a different structure. Its Coram infusion services, operating approximately 85 locations and 65 ambulatory infusion suites, benefits from integration with the CVS pharmacy network and Aetna insurance plans. BrightSpring Health Services, which went public in 2024, has emerged as another significant competitor, reporting a 22 percent increase in infusion and specialty prescription volume between December 2023 and December 2024 through aggressive technology adoption. Elevance Health operates CarelonRx, Cigna has Accredo, and hospital systems increasingly develop their own home infusion capabilities.

So why has Option Care Health survived, and in many ways thrived, as an independent company in this consolidating landscape?

The answer is what might be called the Switzerland strategy. Because Option Care Health is not owned by a payer, PBM, or hospital system, it can credibly serve as a neutral partner to all of them. A hospital system that refers patients to Option Care Health does not worry that it is feeding a competitor's insurance business. A mid-size insurance plan that contracts with Option Care Health does not worry that patient data is flowing to a rival payer. A pharmaceutical manufacturer that partners with Option Care Health on patient support programs does not worry about conflicts of interest with a payer-owned competitor.

This neutrality is both a moat and a vulnerability. It is a moat because it provides access to relationships and contracts that vertically integrated competitors cannot access without creating conflicts. But it is a vulnerability because those same vertically integrated competitors have captive patient flow that Option Care Health must earn through quality, price, and relationships every single day.

The competitive landscape also includes more than eight hundred independent providers, mostly small regional operations. This fragmentation creates ongoing acquisition opportunities. The January 2025 acquisition of Intramed Plus, a South Carolina-based infusion provider, for approximately $120 million exemplified the tuck-in M&A strategy, outperforming initial expectations and contributing to a 25 percent increase in infusion clinic visits in the fourth quarter of 2025 on a pro forma basis.

The barriers to entry are real but not insurmountable. Regulatory complexity, clinical expertise requirements, cold-chain logistics, and payer contracting all create friction. But well-funded healthcare systems have the resources to clear these hurdles. The question is not whether competition will intensify but whether Option Care Health's scale and operational capabilities provide enough structural advantage to maintain leadership.

IX. The COVID Catalyst and Healthcare's Future

When COVID-19 arrived in the spring of 2020, Option Care Health had been a combined company for barely six months. The integration was still underway. Systems were still being harmonized. It was exactly the wrong time for a global pandemic. Except it was exactly the right time.

The pandemic did something that decades of healthcare policy had failed to accomplish: it made the case for home-based care so obvious that even the most entrenched institutional players could not ignore it. Hospitals, overwhelmed with COVID patients, needed to free up beds. Patients, terrified of contracting the virus in healthcare facilities, demanded alternatives. Payers, watching hospitalization costs explode, became suddenly interested in lower-cost care settings. Regulators, facing an emergency, loosened rules that had constrained home-based care for years.

Option Care Health responded with speed that belied its size. When monoclonal antibody infusions emerged as a treatment for COVID-19, the company rapidly scaled its capacity to administer these therapies in home and ambulatory settings. This was not a natural extension of its existing business. Monoclonal antibody infusions required new clinical protocols, different drug handling procedures, and the ability to identify and treat patients who might have adverse reactions to a therapy authorized under emergency use provisions. The company's ability to mobilize its clinical workforce and logistics infrastructure for this entirely new therapy demonstrated the operational flexibility that the post-merger investment in process and systems had created.

The pandemic accelerated several structural shifts that continue to benefit home infusion. Telehealth integration became standard rather than experimental. Remote patient monitoring technologies matured rapidly. Hospital systems, facing chronic labor shortages exacerbated by pandemic burnout, began outsourcing more services to specialized providers rather than trying to do everything in-house. Crucially, many temporary COVID-era regulatory flexibilities were made permanent. CMS expanded coverage for home infusion services, and the broader "hospital at home" movement gained legitimacy.

The aging of the American population provides a secular demand tailwind that will persist for decades. As the baby boomer generation enters its late seventies and eighties, the prevalence of chronic conditions requiring ongoing infusion treatment will accelerate. Value-based care arrangements, where providers are rewarded for outcomes rather than volume, further benefit home infusion. When a payer or health system is accountable for the total cost and quality of care for a patient population, the economic incentive to shift infusions from a $587-per-day hospital setting to a $225-per-day home setting becomes irresistible.

There is a myth worth debunking here. Some observers have attributed Option Care Health's post-merger success primarily to COVID, as though the pandemic handed the company a gift. The reality is more nuanced. COVID was an accelerant, not a cause. The company's operational investments in standardized protocols, technology, and logistics made it possible to capitalize on the surge in demand. A company that was still struggling with integration, as BioScrip had been with CarePoint for years, would not have been able to mobilize effectively when the pandemic hit. Option Care Health's ability to turn a crisis into a catalyst was a function of preparation meeting opportunity, not luck.

The question is no longer whether home infusion will grow. It is how fast, and whether the regulatory and competitive environment will allow independent providers like Option Care Health to capture their fair share.

X. The Business Model Deep Dive

Option Care Health's business model is deceptively simple on the surface: buy drugs, compound them in sterile pharmacies, deliver them to patients, send nurses to administer them, and bill insurance companies. In practice, every step in that chain is fiendishly complicated.

Revenue comes from three interrelated streams: pharmacy services, encompassing drug procurement, sterile compounding, and dispensing; nursing services, including clinical administration, monitoring, and patient education; and patient care coordination, covering insurance authorization, treatment planning, and ongoing case management. These functions are deeply intertwined, and the company does not disclose discrete revenue for each.

A typical patient episode illustrates the operational complexity. A physician decides that a patient needs intravenous immunoglobulin therapy. The physician or hospital discharge planner contacts Option Care Health. A care coordinator begins the insurance authorization process, which can take days and involves submitting clinical documentation to the patient's insurer for prior approval. Once authorized, the company's pharmacy compounds the medication in a sterile cleanroom environment, packages it with appropriate cold-chain protections, and coordinates delivery. A nurse arrives, sets up the IV, monitors the patient during the infusion, which can take several hours for immunoglobulin, documents the treatment, and provides education on self-administration if appropriate. After the visit, the company bills the insurer, navigating complex coding requirements that can take weeks or months to resolve. The entire cycle repeats on a regular schedule for as long as the patient requires therapy. Now multiply this by 315,000 patients across fifty states and you begin to understand why operational excellence matters so much.

The margin profile reflects this complexity. Gross margins peaked at 22.8 percent in 2023 and compressed to approximately 19.3 percent in 2025. This compression was driven primarily by mix shift rather than operational deterioration: as higher-revenue chronic therapies grow as a proportion of total revenue, they bring higher absolute gross profit per patient but lower percentage margins because the drug costs are a larger component. Adjusted EBITDA margins have been more stable, ranging from roughly 7.6 percent in 2021 to a peak of 8.8 percent in 2023, with a partial recovery to approximately 8.3 percent in 2025.

Payer mix directly affects reimbursement rates and collection speed. Approximately 88 percent of Option Care Health's revenue comes from commercial and managed care payers, where rates are negotiated and generally more favorable than government reimbursement. The remaining 12 percent comes from Medicare, Medicaid, and other sources. This heavy commercial mix is a double-edged sword: commercial rates are higher, but the company is heavily exposed to the negotiating leverage of a small number of large insurance companies.

Capital allocation has evolved significantly since the merger. The private equity inheritance left the company with meaningful debt, but management has been disciplined about deleveraging. By the end of 2024, the net debt leverage ratio had fallen to 1.6 times adjusted EBITDA. The September 2025 refinancing of the first-lien term loan at Term SOFR plus 1.75 percent with an extended maturity further improved the capital structure. Total debt at the end of 2025 stood at $1.176 billion.

The company has become increasingly aggressive about returning capital to shareholders. Share repurchases totaled $250 million in 2024 and exceeded $300 million in 2025. In January 2026, the board doubled the share repurchase authorization to $1 billion. Operating cash flow is guided to exceed $340 million in 2026.

Management has articulated a clear capital allocation priority: organic investment and technology first, followed by tuck-in M&A, followed by share repurchases. This ordering reflects a belief that the highest-return use of capital is internal reinvestment, but the company will not chase transformative M&A at the expense of financial discipline, a lesson reinforced by the terminated Amedisys deal.

For investors tracking this business, two key performance indicators matter most. First, organic revenue growth excluding biosimilar and Inflation Reduction Act headwinds, which strips out drug pricing noise and reveals the underlying demand trajectory. Management guided to approximately 8 percent organic growth on this basis for 2026. Second, operating cash flow, which captures the company's ability to convert revenue growth into actual cash. The trajectory from roughly $300 million in 2024 to over $340 million guided for 2026 tells a story about a business reaching a new level of financial maturity.

XI. Porter's Five Forces Analysis

The structural attractiveness of the home infusion industry can be evaluated through the lens of competitive forces, and the picture that emerges is one of a growing market with genuine structural challenges.

The threat of new entrants is low to moderate. The barriers are real: state-by-state pharmacy licensure, sterile compounding regulations, cold-chain logistics requirements, clinical staffing needs, and the complexity of payer contracting all create significant friction. A new entrant cannot simply hang a shingle and begin operating. Building the referral relationships that drive patient volume takes years of relationship-building with physicians and discharge planners. However, well-capitalized entrants, including hospital systems developing their own home infusion programs and technology-enabled startups backed by venture capital, can and do enter the market. The barrier is not impossibly high; it just takes substantial time and investment to clear.

The bargaining power of suppliers is moderate. Drug manufacturers are highly concentrated and powerful, but they need distribution infrastructure to reach patients, giving companies like Option Care Health some countervailing leverage. The nursing labor market presents a more challenging dynamic. Healthcare faces chronic staffing shortages, with the industry needing an additional 200,000 nurses annually through 2031. This creates persistent wage inflation pressure that disproportionately affects labor-intensive businesses like home infusion. Option Care Health's size helps with recruiting, but it cannot escape the structural pressure entirely.

The bargaining power of buyers is high, and this is perhaps the most important force shaping the industry. Payer concentration means that a small number of large insurance companies negotiate aggressively on reimbursement rates. Option Care Health's top managed care relationships collectively represent enormous revenue exposure. A single contract loss or network exclusion could materially affect financial results. The company's outcomes data and clinical quality create stickiness, but buyers ultimately hold significant leverage.

The threat of substitutes is moderate to high. Hospital outpatient infusion centers remain a significant alternative, though they are more expensive. Physician office administration is growing for certain therapies. The most important long-term substitute threat comes from oral formulations of drugs that currently require infusion. Pharmaceutical companies are actively developing oral versions of biologics. If successful at scale, these reformulations could reduce the addressable market for home infusion over time. Self-administration technologies are also advancing, enabling patients to manage more therapies independently without professional nursing support.

Competitive rivalry is high. Payer-owned providers, particularly Optum and Coram/CVS, create persistent pricing pressure and the risk of patient steering. Regional specialists compete effectively in specific therapeutic areas and geographic markets.

The overall dynamic is one of a growing market where competition for share is fierce, margins face pressure, and differentiation depends on clinical quality, operational efficiency, and relationship depth. The top three players, Option Care Health, Optum's infusion business, and CVS's Coram, together hold roughly 45 percent of the market, leaving the remaining 55 percent fragmented among hundreds of smaller providers. This fragmentation creates both competitive intensity and acquisition opportunity.

XII. Hamilton's Seven Powers Analysis

Hamilton Helmer's Seven Powers framework provides a complementary lens for evaluating whether Option Care Health possesses durable competitive advantages, looking beyond industry structure to company-specific sources of power.

Scale Economies are strong. Geographic density reduces per-unit delivery costs. Fixed costs including IT infrastructure, regulatory compliance, corporate management, and clinical protocol development are spread across a revenue base that has nearly doubled since the merger.

Negotiating leverage with payers and drug manufacturers improves with scale because larger providers can offer more complete geographic coverage and higher patient volumes. This is the most straightforward and powerful source of competitive advantage.

Network Effects are moderate. The dynamics are not as powerful as those in technology platform businesses, but they exist. More patients generate better clinical outcomes data, which attracts more referrals, which generates more data. Geographic coverage attracts national payer contracts, which drive volume to the network, which justifies further expansion.

These are positive feedback loops, but they are slower-acting and less defensible than the network effects found in marketplaces or social platforms.

Counter-Positioning is moderate. Payer-owned competitors like Optum and Coram are constrained by their parent companies' broader strategic interests. An insurance company that aggressively steers patients to its own infusion provider risks regulatory scrutiny, provider backlash, and loss of network adequacy.

Option Care Health's independence allows it to position itself as a neutral partner. However, this advantage is fragile because it depends on regulatory enforcement and payer behavior that could shift.

Switching Costs are moderate to strong. Clinical relationships and care continuity create real friction. When a patient is established with a home infusion provider, changing means disrupting care routines, building new clinical relationships, and navigating insurance re-authorization.

Physician and hospital referral patterns tend to be sticky once established. Payer contracts are typically multi-year. These switching costs are meaningful but not insurmountable.

Branding is weak to moderate. Option Care Health operates primarily as a business-to-business company. Most patients do not choose their provider; the choice is made by physicians and discharge planners. Consumer awareness is minimal.

Clinical reputation within the provider community matters, and quality metrics contribute to professional brand equity. But this is a limited source of durable advantage.

Cornered Resource is weak. The company has no proprietary drugs, patented technologies, or exclusive access to critical inputs. The nursing workforce, while a strategic asset, is accessible to competitors willing to pay competitive wages.

There is no single resource that competitors cannot access, which limits this dimension of competitive power.

Process Power is moderate to strong, and this may be the most important power for Option Care Health beyond scale. The company's operational excellence in logistics, care coordination, sterile compounding, payer contracting, and clinical protocol management has been built over years of integration and optimization. The post-merger integration forced the organization to develop institutional capabilities deeply embedded in its processes, systems, and culture. A competitor can hire talented individuals, but cannot instantly recreate the organizational learning that comes from managing millions of infusion events per year across all fifty states.

The overall assessment: Option Care Health's competitive position rests primarily on scale economies and process power, supplemented by moderate switching costs and the counter-positioning advantage of independence. The absence of strong network effects, cornered resources, or powerful branding means the moat is defensible but not unassailable. The company must continuously invest in operational improvement to maintain its position. In Helmer's language, this is a company that has "earned" its competitive advantages through sustained operational investment rather than "lucked into" them through proprietary technology or natural monopoly characteristics. That makes the advantages harder to build but also harder to destroy, because they are rooted in organizational capability rather than any single asset or market position.

XIII. The Bull Case Versus the Bear Case

The bull case for Option Care Health rests on the convergence of secular tailwinds that are as durable as any in healthcare.

Start with demographics. The aging of the baby boomer generation will drive steadily increasing demand for chronic disease management, including many conditions treated with infusion therapy. This demographic tailwind will persist for at least two more decades. Overlay the explosive growth of specialty drugs, particularly biologics that require professional infusion administration, and the addressable market is growing at a rate that should support high-single-digit organic revenue growth for years. Add the structural cost advantages of home infusion over hospital settings, a gap that only widens as healthcare costs continue to rise, and the demand picture is compelling.

Option Care Health's market leadership position, covering 96 percent of insured patients with a network spanning all fifty states, creates a platform for compounding growth. The company can add new therapeutic categories, expand into adjacent services, and execute tuck-in acquisitions that add density without proportional fixed costs. The $1 billion share buyback authorization provides a meaningful floor for shareholder returns.

The demonstrated execution since the 2019 merger is perhaps the strongest element of the bull case. Revenue grew from $3 billion to $5.6 billion. Adjusted EBITDA expanded from $194 million to $471 million. Free cash flow generation reached a level supporting both reinvestment and significant capital returns. The management team has proven it can integrate acquisitions, standardize operations, and grow profitably in a complex industry.

The bear case centers on structural risks that could erode the company's competitive position and margin profile.

Vertical integration is the most significant threat. If UnitedHealth, CVS, and Elevance continue steering patients toward their own infusion providers, the addressable market for independent providers contracts. Regulatory protection against patient steering is uncertain and political. A world in which payer-owned infusion providers collectively serve 50 or 60 percent of the insured population is one where independence becomes a liability rather than an asset.

Reimbursement pressure is persistent and intensifying. The 88 percent commercial payer mix means aggressive rate negotiation is a constant. Medicare Advantage rate increases have not kept pace with medical inflation. The Inflation Reduction Act's drug pricing provisions are creating additional pressure. Gross margin compression from 22.8 percent in 2023 to 19.3 percent in 2025 reflects the fundamental dynamics of a business where buyers hold significant negotiating leverage.

The biosimilar transition poses specific, quantifiable risk. As additional blockbuster biologics face biosimilar competition in coming years, dynamics similar to the Stelara headwind could repeat. Customer concentration amplifies these risks: while no single payer accounts for a majority of revenue, the top managed care relationships collectively represent enormous exposure. Labor cost inflation is a structural headwind. And the oral drug formulation threat, while long-term, is real: pharmaceutical companies are investing heavily in developing oral versions of currently infused drugs.

The reality sits somewhere between the extremes. Option Care Health is a solid infrastructure business in a growing market with demonstrated execution and improving financial metrics. But it faces structural headwinds from consolidation, reimbursement pressure, and the persistent challenge of maintaining margins in a business where buyers hold significant power. The closest historical analogy may be independent laboratory companies like Quest Diagnostics and LabCorp, which faced similar vertical integration threats from payer-owned competitors, similar reimbursement pressures, and similar questions about whether independence was sustainable. Those companies survived and thrived by achieving sufficient scale and operational excellence to remain essential partners. Whether Option Care Health follows the same trajectory will depend on whether it can continue executing at the level it has demonstrated since 2019.

XIV. What Would Have Happened Otherwise

Counterfactual thinking is a useful exercise for understanding why things turned out the way they did rather than another way. In Option Care Health's case, the counterfactuals reveal just how contingent the company's current position is on a series of decisions and events that could easily have gone differently.

If the Option Care-BioScrip merger had not happened, the most likely outcome for BioScrip was acquisition by a vertically integrated payer, probably Optum or CVS. BioScrip was struggling financially, its stock was depressed, and its clinical infrastructure, despite operational problems, was valuable to a buyer who needed geographic coverage. An Optum acquisition of BioScrip would have given UnitedHealth an even larger share of the home infusion market and further tilted the competitive landscape against independent providers. Option Care, still under Madison Dearborn's ownership, would have faced an even more concentrated competitive environment with fewer strategic options. The independent home infusion model might have effectively ended.

If private equity had not consolidated the industry through the Walgreens carve-out and subsequent merger, the home infusion market would likely have remained more fragmented. Hundreds of small providers would have continued operating independently, lacking the scale to negotiate effectively with payers or invest in technology. This fragmentation would have made the industry even more vulnerable to payer vertical integration, as individual providers would have been easy targets for acquisition or replacement. Paradoxically, private equity consolidation may have been what preserved the independent model.

If COVID-19 had not accelerated the hospital-to-home shift, adoption of home infusion would have continued but at a slower pace. The pandemic compressed years of behavioral change into months, forcing physicians, patients, and payers to embrace home-based care out of necessity rather than choice. Without that catalyst, Option Care Health's post-merger growth trajectory would have been flatter, and the strategic validation of its business model would have taken longer to materialize. The merger might have looked like a mediocre deal rather than a transformational one.

If specialty drugs had not exploded in volume and value, home infusion would have remained a lower-margin commodity business focused primarily on IV antibiotics and nutritional support. The specialty drug revolution transformed home infusion from a cost-saving convenience into a critical component of the pharmaceutical value chain, with higher revenue per patient and more complex clinical requirements that favor scale providers. Without this transformation, Option Care Health would be a much smaller, much less interesting company.

Perhaps the most interesting counterfactual involves the companies that chose not to stay in home infusion. Amazon explored healthcare delivery through Amazon Pharmacy and Amazon Clinic but never made a serious move into home infusion. Walgreens tried to operate it as a corporate subsidiary for eight years and ultimately sold it at a loss relative to the operational headaches it created. These exits by extraordinarily well-resourced companies underscore a fundamental truth about home infusion: it is not a business that can be disrupted by technology or brand alone. It requires clinical expertise, regulatory navigation, logistics infrastructure, and payer relationships that take years to build. The graveyard of failed entrants may be the strongest argument for the durability of Option Care Health's competitive position.

There is also the counterfactual of what happens if the Preserving Patient Access to Home Infusion Act actually passes. The current Medicare benefit is so dysfunctional that only about a thousand beneficiaries use it. If legislation fixes the reimbursement structure to pay providers on each day a drug is administered rather than only when a nurse is physically present, the addressable Medicare market for home infusion would expand dramatically overnight. That would be an unambiguous positive for the industry leader. Conversely, if the legislation stalls indefinitely, the Medicare opportunity remains largely theoretical, and commercial payers continue to drive virtually all of the company's economics.

XV. Lessons and Playbook

The Option Care Health story contains several lessons that extend well beyond home infusion and speak to broader patterns in business strategy and investment.

For operators in healthcare and other complex services industries, the most important lesson may be the power of operational excellence in businesses that are not inherently exciting. Home infusion does not have the narrative appeal of biotech drug discovery or digital health platforms. It does not attract breathless media coverage or command premium innovation multiples. But the combination of essential services, high barriers to entry, and relentless operational complexity creates an environment where companies that simply execute well can compound value over long periods. Rademacher's approach to the post-merger integration, focusing on standardizing processes, investing in people and technology, and building clinical quality rather than chasing the next acquisition, exemplifies this philosophy. The lesson is not that boring is better. It is that in industries where operational complexity is the primary barrier to entry, the company that executes best wins, regardless of how exciting or boring the business looks from the outside.

The merger execution itself offers lessons for anyone contemplating a transformative combination. The Option Care-BioScrip deal worked not because the financial structure was clever, although it was, but because the acquiring management team had a clear operational vision and the discipline to execute it. Too many healthcare rollups fail because the acquirer underestimates integration complexity or overestimates synergies. BioScrip's own history proved this point. Rademacher and his team understood that combining two home infusion companies was not a financial exercise but an operational one, and they invested the time and resources to do it properly. The contrast between BioScrip's failed CarePoint integration and Option Care Health's successful BioScrip integration, using the same industry, similar assets, and comparable scale, demonstrates that execution matters more than strategy in services businesses.

The strategic value of being "Switzerland" in a consolidating industry is another transferable insight. When competitors are being absorbed by larger entities with inherent conflicts of interest, maintaining independence can be a powerful differentiator. This applies across industries: in advertising, financial services, technology distribution, anywhere vertical integration creates conflicts that independent players can exploit. The caveat is that this advantage is only durable if the independent player has sufficient scale and quality to compete. Independence without excellence is just vulnerability.

For investors, Option Care Health illustrates the potential of infrastructure businesses in fragmented markets with secular tailwinds. A company with market leadership in a growing industry, improving operational metrics, strong cash flow generation, and disciplined capital allocation can compound wealth quietly and persistently. The key is identifying the right structural tailwinds and the right operational characteristics. Sometimes the best investments are in the pipes, not the content that flows through them.

The healthcare-specific lessons are equally instructive. The site-of-care shift from hospitals to homes is real, durable, and still in its early innings. The mismatch between Medicare's home infusion benefit design and clinical reality illustrates how policy dysfunction can simultaneously constrain and create opportunity. And the specialty drug revolution is reshaping not just what drugs are available, but how, where, and by whom they are delivered.

There is also a timing lesson embedded in the Option Care Health story that deserves emphasis. The company became the market leader not because it was first, not because it had the most capital, and not because it had the best technology. It became the leader because it executed the right merger at the right time, with the right management team, and then had the operational foundation to capitalize on a once-in-a-generation demand catalyst. Timing in business is often described as luck. But in Option Care Health's case, the "luck" of COVID coinciding with the merger was only valuable because of the operational investments made in the years leading up to it. Fortune favors the prepared, and Rademacher's team was prepared.

XVI. Recent Developments and Current State

The most recent chapter of the Option Care Health story is one of financial maturation and strategic discipline shaped by both bold ambition and calculated restraint.

In May 2023, the company announced an all-stock acquisition of Amedisys, a major home health and hospice provider, valued at approximately $3.6 billion. The combined entity would have created a comprehensive home-based healthcare platform spanning infusion, home health, and hospice, with more than 16,500 employees and roughly $6.2 billion in projected annual revenue. It was the most ambitious strategic move in the company's history.

Within weeks, UnitedHealth's Optum made an unsolicited $100-per-share cash offer that Amedisys's board determined was a superior proposal. The merger agreement was terminated in June 2023, and Option Care Health received a $106 million termination fee. The loss was disappointing, but some analysts argued the company was better off focusing on its core infusion business rather than diversifying into operationally distinct adjacent services. The termination fee was a meaningful consolation that flowed directly to the bottom line.

The CFO transition in late 2025 marked an important leadership change. Mike Shapiro, who had served as CFO for a decade spanning the BioScrip merger and the company's transformation into a public market leader, stepped down effective October 1, 2025, remaining as a strategic advisor. He was succeeded by Meenal Sethna, who brought more than thirty years of executive experience from roles as CFO of Littelfuse, corporate controller at Illinois Tool Works, and VP of Finance at Motorola. Her background in industrial companies with complex supply chains signaled continued emphasis on operational efficiency and financial discipline.

Full-year 2025 results demonstrated sustained momentum. Revenue reached $5.6 billion, up 13 percent year over year, with balanced growth across acute and chronic therapies. Adjusted EBITDA came in at $471 million with adjusted diluted earnings per share of $1.72. Management navigated the Stelara biosimilar headwind, which cost approximately $70 million in revenue for the full year, by driving volume growth across other therapeutic categories.

The Intramed Plus acquisition outperformed expectations, expanding the ambulatory infusion suite network and the advanced practitioner clinical model. Capital returns accelerated sharply, with share repurchases exceeding $300 million in 2025 and the January 2026 doubling of the buyback authorization to $1 billion signaling management's confidence.

For 2026, the company guided revenue of $5.8 to $6.0 billion, adjusted EBITDA of $480 to $505 million, adjusted diluted EPS of $1.82 to $1.92, and operating cash flow exceeding $340 million. Organic revenue growth excluding Stelara and Inflation Reduction Act impacts was guided at approximately 8 percent. The September 2025 debt refinancing at lower rates and extended maturities further strengthened the balance sheet.

The competitive environment continued to intensify, with Optum expanding through the Amedisys acquisition and BrightSpring investing aggressively in technology and scale. But Option Care Health's position as the market leader with the broadest geographic coverage and deepest clinical capabilities among independent providers appeared to be strengthening. Analyst coverage expanded meaningfully, with multiple firms initiating or upgrading their ratings, reflecting growing institutional awareness of the company's improving fundamentals and market position. The Harry Kraemer connection deserves mention here as well: the company's board chairman, Harry M. Jansen Kraemer Jr., is the former chairman, president, and CEO of Baxter International, where he served for twenty-three years. He is also a clinical professor of management and strategy at Northwestern University's Kellogg School of Management, holding degrees from Lawrence University and Kellogg. His deep healthcare executive experience and his connection to the Baxter alumni network from which Rademacher himself emerged give the board a level of healthcare operations expertise that is rare among companies of this size.

XVII. The Future: Where Does Option Care Go From Here?

The ultimate strategic question for Option Care Health is whether the independent model can survive and thrive in an industry moving relentlessly toward vertical integration. The answer will depend on which of several possible futures materializes.

In the optimistic scenario, the company continues growing organically at high-single-digit rates, executes tuck-in acquisitions that add density and capability, and uses growing free cash flow to buy back shares aggressively. Independence becomes an increasingly valued attribute as regulators scrutinize vertical integration practices and health systems seek neutral partners. New therapeutic categories, particularly cell and gene therapies, of which more than 4,000 are currently in development globally with dozens expected to reach approval in the coming decade, create new revenue streams leveraging the company's existing infrastructure. The number of patients treated with gene or cell therapy is projected to grow from 12,000 in 2020 to more than 340,000 by 2030, representing an entirely new category of extraordinarily complex, extraordinarily expensive therapies that require specialized administration and monitoring.

In the base scenario, the company continues to grow but faces persistent margin pressure from biosimilar adoption, payer negotiation, and labor costs. Revenue growth in the mid-to-high single digits is offset by modest margin compression. The buyback program supports per-share value creation, but the company executes competently rather than spectacularly in an increasingly competitive environment.

In the pessimistic scenario, vertical integration accelerates, payer-owned providers capture growing market share, and regulatory action against patient steering fails to materialize. Oral drug formulations begin displacing infusion therapies in key categories. The company's independence becomes a liability, and it is eventually absorbed by a larger healthcare company.

Technology will play an increasingly important role in all scenarios. Option Care Health has invested in AI for claims processing automation, expanded its partnership with WellSky for health data exchange and care coordination, and is building capabilities in remote patient monitoring. These investments are necessary to maintain the operational edge that underpins its competitive position.

International expansion is theoretically possible but unlikely in the near term. The U.S. market is large enough and growing fast enough that international diversification offers limited strategic benefit relative to its operational complexity. The hospital-at-home movement presents both opportunity and ambiguity: it could drive more demand for home-based clinical services, or it could create new hospital-affiliated competitors. The most likely outcome is some of each.

What seems clear is that home infusion is not going back into the hospital. The economic, clinical, and demographic forces pushing care into the home are too powerful, too broad-based, and too aligned with what patients actually want.

The question for Option Care Health is not whether the market will grow, but whether it can maintain its position as the leading independent player in a market where the largest companies in American healthcare are determined to own every link in the care delivery chain. The next five years will likely determine whether the independent home infusion model follows the path of independent laboratories, which survived and thrived despite vertical integration threats, or the path of independent physician practices, which were largely absorbed by hospital systems and payer-owned entities. The distinction may come down to whether regulators meaningfully constrain patient steering, and whether Option Care Health's operational advantages prove durable enough to win business on merit even when competitors can direct captive patient flow.

XVIII. Epilogue and Final Reflections

The biggest surprise of the Option Care Health story is not any single transaction or strategic decision. It is the distance between what the company does and how visible it is. This is a $5.6 billion revenue enterprise that serves over 315,000 patients across all fifty states, employs more than five thousand clinicians, and operates critical healthcare infrastructure. And unless you work in the industry, you have probably never heard of it.

That invisibility is, in a sense, the hallmark of a true infrastructure business. The best infrastructure is the kind you never think about until it stops working. The electricity that powers your home. The fiber optic cables that carry your internet traffic. The water treatment plant that makes your tap water safe. And the pharmacy, logistics, and clinical network that ensures a child with a primary immune deficiency gets her monthly immunoglobulin infusion at her kitchen table instead of in a hospital bed.

What makes Option Care Health's story uniquely American is the collision of forces that shaped it: the entrepreneurial initiative of two pharmacists in a small California town who just wanted to help one patient avoid daily hospital trips; the corporate ambition and subsequent retreat of Walgreens; the financial engineering and operational discipline of private equity; the compliance failures and cautionary tale of BioScrip; the once-in-a-century disruption of a pandemic; and the ongoing tectonic shifts in how Americans receive and pay for medical care. No other country has this particular combination of fragmentation, complexity, and opportunity in healthcare delivery. No other country's healthcare system creates the same incentives for the kind of specialized infrastructure business that Option Care Health has become.