BeOne Medicines: The Global Oncology Company That Challenged Big Pharma

I. Introduction & Episode Thesis

Picture this: In a Beijing laboratory in 2012, a team of Chinese scientists huddles around molecular models, tweaking chemical structures late into the night. They're hunting for something that has eluded Big Pharma's billion-dollar R&D machines—a better BTK inhibitor, one that could challenge the cancer drug oligopoly dominated by AbbVie, Johnson & Johnson, and AstraZeneca. Fast forward to 2024, and that molecule, born in a Chinese lab, has generated $3.81 billion in revenue, marking a 54.96% surge from the previous year. The drug is Brukinsa, and the company is BeOne Medicines.

Here's the provocative question that drives our story: How did a company founded by an American McKinsey consultant and a Chinese-American biochemist build the first cancer drug from China to gain FDA approval—and then use it to mount a serious challenge to Western pharma's most lucrative franchises?

This isn't just another biotech success story. It's a masterclass in geographic arbitrage, founder-scientist partnership dynamics, and the art of building a truly global pharmaceutical company from emerging market roots. BeOne didn't just develop drugs in China for Chinese patients; they built a company designed from day one to compete on the world stage, with clinical trials spanning 45 countries and commercial operations across six continents.

The roadmap ahead takes us through three transformative acts: First, the unlikely partnership between John Oyler and Xiaodong Wang that defied conventional pharma wisdom. Second, the strategic chess moves—from the Celgene deal to the BTK breakthrough—that positioned BeOne as a global player. And third, the bold rebranding and Swiss redomiciliation that signals their ambitions for the next decade.

What makes BeOne particularly fascinating for students of business strategy is how they've systematically arbitraged the differences between East and West—not just in cost, but in speed, regulatory pathways, and clinical trial infrastructure. They've built what might be the template for 21st-century pharma: globally distributed, scientifically rigorous, and unencumbered by the legacy structures that slow down Big Pharma incumbents.

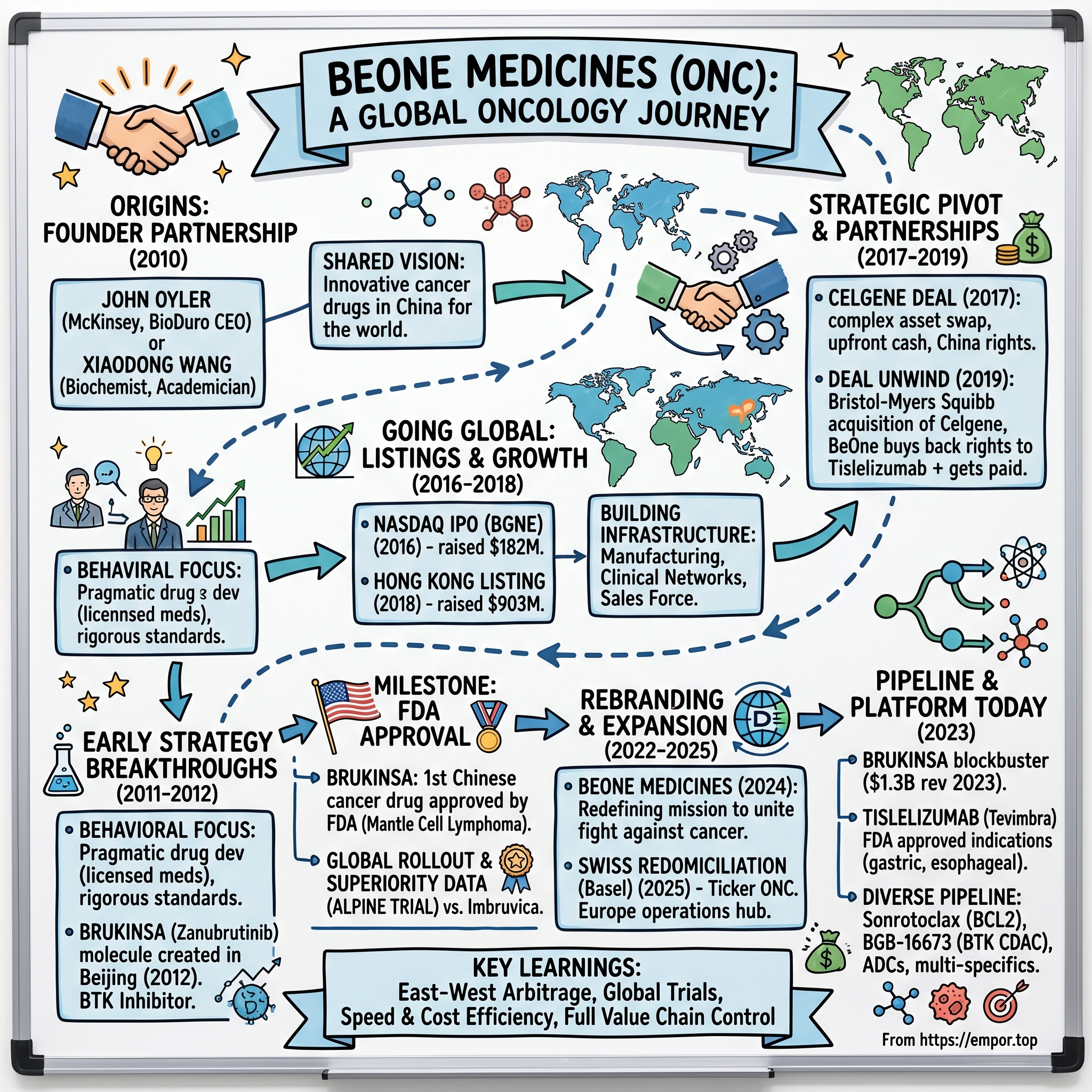

II. Origins: The McKinsey Consultant Meets the Scientist

The year is 2005, and John V. Oyler is running BioDuro, a contract research organization in Beijing. It's a typically hectic morning when an unexpected visitor walks into the lobby—Xiaodong Wang, one of the youngest members ever elected to the U.S. National Academy of Sciences. Wang, a Howard Hughes Medical Institute investigator and UT Southwestern professor who'd done groundbreaking apoptosis research alongside Nobel laureates, was running the nearby National Institute of Biological Sciences (NIBS). The proximity was coincidental; the meeting would prove fateful.

Oyler's path to that Beijing lobby was anything but conventional for a pharma executive. Growing up in Pittsburgh, Pennsylvania, he'd studied mechanical engineering at MIT—not the typical breeding ground for biotech CEOs. His early career took him through McKinsey's hallowed halls, where he learned to dissect businesses with surgical precision. But unlike his consulting peers who remained safely ensconced in PowerPoint and Excel, Oyler had developed an obsession with China's untapped potential in life sciences.

Wang represented the opposite archetype—the pure scientist who'd conquered American academia. His work on programmed cell death had earned him recognition as one of the world's premier biochemists. Yet despite his success in the U.S. academic system, Wang harbored ambitions that transcended publication in Nature and Cell. He wanted to build something that could translate breakthrough science into actual medicines. Their conversations in those early meetings centered on a shared frustration: why did cancer patients in emerging markets have to wait years—if ever—to access innovative treatments? Wang had the scientific chops to create world-class molecules. Oyler understood how to navigate the labyrinthine world of drug development, regulatory approval, and commercialization. Together, they sketched out something audacious: a company that would develop innovative cancer drugs in China but for the world.

In late 2010, they formalized their partnership, founding what would become BeOne with a vision for a global multinational biopharmaceutical company focusing on cancer treatment. Oyler invested $10 million of his own money to start the company and secured funding from angel investors and Merck & Co., becoming CEO and chairman while Wang took on the scientific leadership role.

The founding philosophy was radical for its time: build differently from Day 1. Instead of following the traditional biotech playbook of licensing molecules from Big Pharma and developing them for local markets, they would create their own molecules. Instead of building for China alone, they would design clinical trials and regulatory strategies for global approval from the outset. And instead of the typical biotech capital structure that diluted founders into oblivion, Oyler would maintain significant skin in the game throughout the company's growth.

This wasn't just geographic arbitrage—it was intellectual and strategic arbitrage. Wang brought a network of top-tier Chinese scientists eager to return home and build something meaningful. Oyler brought Western business acumen and an understanding of what it took to build a company that could compete globally. Together, they represented a new archetype: the hybrid East-West leadership team that could navigate both Beijing's regulatory corridors and the FDA's approval pathways with equal facility.

III. The Early Years: Building in China First

In 2011, with Merck's $20 million investment secured and offices established in Philadelphia and at Beijing's Zhongguancun Life Science Park, BeOne faced its first existential challenge: how to build a world-class drug development organization in a country where the pharmaceutical industry was still largely focused on generics and copycat drugs.

BeOne's early business model was pragmatic yet clever—obtaining rights to experimental medicines shelved by other pharmaceutical companies and taking them through early clinical trials at Chinese medical schools and hospitals. Successful formulas would either be sold to or co-developed with larger drugmakers who could fund the late-stage trials. This wasn't the glamorous work of breakthrough drug discovery, but it served multiple strategic purposes: generating early revenue, building relationships with Chinese hospitals and regulators, and most importantly, training a team in the rigorous processes of clinical development.

The recruitment challenge was formidable. Wang's reputation opened doors—his status as one of the youngest U.S. National Academy of Sciences members carried immense weight with Chinese scientists considering a return home. Within eighteen months, they'd assembled over 100 people, many of them returnees from top Western pharmaceutical companies and academic institutions who were drawn to the vision of building a global biopharmaceutical company with Chinese roots.

But assembling talent was only half the battle. The real challenge was navigating the Byzantine Chinese regulatory system while maintaining standards that would pass muster with the FDA and EMA. Oyler's approach was counterintuitive: instead of cutting corners to move faster in China, BeOne would exceed Western standards from day one. Every clinical trial protocol, every manufacturing process, every quality control measure would be designed to meet or exceed FDA requirements.

This over-engineering came at a cost. Early investors questioned why BeOne was spending so much on infrastructure and processes when competitors were moving faster with lower standards. The answer became clear only years later: by building to global standards from the beginning, BeOne could seamlessly transition from Chinese trials to global ones without rebuilding their entire operation.

The geographic positioning was deliberate. The company initially primarily operated in China, but with a twist—they established strategic beachheads in markets that would prove crucial for global expansion. BeOne conducted its first research in Australia in 2014, eventually becoming one of the largest clinical research organizations in the country. Why Australia? The country offered a unique combination of high regulatory standards, efficient approval processes, and significant R&D tax incentives. All first-in-human phase 1 trials of internally discovered assets at BeOne are conducted in Australia—a strategic choice that accelerated development timelines while maintaining credibility with global regulators.

The early years also saw BeOne begin work on what would become their crown jewel. In 2012, a team of Beijing scientists started tinkering with a molecule targeting Bruton's tyrosine kinase (BTK), a protein crucial for B-cell development that had become a hot target in oncology. The existing BTK inhibitor, Imbruvica, was showing remarkable efficacy but came with significant side effects. BeOne's scientists believed they could design a more selective molecule—one that would hit BTK harder while sparing other kinases that caused toxicity.

This wasn't just scientific ambition; it was strategic positioning. By choosing to compete in BTK inhibition, BeOne was deliberately picking a fight with Big Pharma's most profitable franchises. It was a declaration of intent: we're not here to fill gaps in the market; we're here to compete head-to-head with the best drugs in oncology.

The strategic positioning between East and West became BeOne's defining characteristic. They weren't a Chinese company trying to expand West, nor were they a Western company trying to crack China. They were something new—a truly global company that happened to have its largest operations in China. This positioning would prove crucial when navigating the geopolitical tensions that would emerge later in the decade.

IV. The NASDAQ IPO & Global Ambitions

The morning of February 3, 2016, marked a watershed moment. As the opening bell rang on NASDAQ, BeOne's ticker symbol "BGNE" flashed across screens for the first time. The stock, priced at $24 per American Depositary Share, immediately surged 19.25% to close at $28.62 on its first day of trading. For a Chinese biotech company with no approved drugs and burning through cash, this reception was nothing short of remarkable.

The company raised $182 million. The IPO, managed by Goldman Sachs and Morgan Stanley, was backed by Baker Brothers and Hillhouse BGN Holdings, which together planned to purchase half the shares offered. The involvement of Baker Brothers—legendary biotech investors with a track record of backing winners like Incyte and Acadia—sent a powerful signal to the market. This wasn't just another speculative Chinese IPO; it was a company that had passed the due diligence of the world's most sophisticated healthcare investors.

The timing was audacious. January 2016 had seen zero IPOs in the U.S. amid significant global market turmoil. Chinese companies were fleeing American exchanges—WuXi PharmaTech had just completed a management buyout to leave the NYSE, Mindray was planning a similar exit from NASDAQ, and Sinovac had announced its own privatization. Against this backdrop of Chinese companies retreating from U.S. markets, BeOne was swimming upstream, planting its flag on American soil.

Behind the scenes, the IPO preparation had been a masterclass in strategic positioning. Oyler and his team had spent months educating American investors about the Chinese pharmaceutical market's transformation. They didn't pitch BeOne as a Chinese company seeking Western capital; they positioned it as a global company that happened to have significant operations in China. The distinction was crucial for institutional investors wary of governance issues that had plagued other Chinese listings.

In a March 2018 follow-on offering, BeOne raised another $758 million. This wasn't just a capital raise; it was a vote of confidence from the market that BeOne's strategy was working. The company was advancing multiple molecules through clinical trials, and investors were beginning to see the potential for a pipeline that could rival established players.

But the real coup came in August 2018. In August 2018, the company had another IPO when it offered a secondary listing of its shares on the Hong Kong Stock Exchange, raising $903 million in the process. This dual listing strategy was brilliant—it gave BeOne access to both Western institutional capital and Asian investors who understood the company's regional advantages. The Hong Kong listing also provided a natural hedge against potential U.S.-China tensions that were beginning to simmer.

The capital structure that emerged from these offerings was deliberately designed for the long game. Unlike many biotechs that dilute founders into irrelevance through successive funding rounds, Oyler maintained significant ownership throughout. This wasn't just about wealth preservation; it was about maintaining the strategic flexibility to make bold, long-term decisions without being beholden to short-term investor pressures.

The infrastructure building that followed the IPO was remarkable in its ambition. While most emerging biotechs would have conserved cash and outsourced everything possible, BeOne went the opposite direction. They built their own manufacturing facilities, established their own clinical trial networks, and created their own commercial organization. To outside observers, it looked like capital inefficiency. To Oyler, it was building the foundation for a company that could compete globally without being dependent on partners who might not share their urgency or vision.

V. The Brukinsa Breakthrough: China's First Global Cancer Drug

November 14, 2019. The date is seared into the collective memory of China's pharmaceutical industry. FDA grants accelerated approval to BeiGene's BTK inhibitor Zanubrutinib, branded as Brukinsa, for the treatment of mantle cell lymphoma. It's the first approved drug of China in the U.S. This is a milestone in Chinese drug history. For decades, the flow of innovation had been unidirectional—from West to East. Now, for the first time, a cancer drug conceived and developed in China would be sold to American patients.

The molecule that would become Brukinsa had humble beginnings. BeOne developed Brukinsa (zanubrutinib), a Bruton's tyrosine kinase inhibitor for the treatment of cancer, from a formula its scientists created in Beijing in 2012. The team, working in BeOne's labs at Zhongguancun Life Science Park, had set out to solve a specific problem: Imbruvica, the first BTK inhibitor, was remarkably effective but came with significant off-target effects that limited its use in many patients.

BeOne's scientists believed they could design a more selective molecule—one that would bind more tightly to BTK while sparing other kinases. The chemistry was elegant: by modifying specific molecular structures, they created a compound with superior selectivity. In preclinical studies, zanubrutinib showed 10-fold greater selectivity for BTK compared to Imbruvica, suggesting it might deliver efficacy with fewer side effects.

Data from the phase-2 clinical trial conducted in China showed Brukinsa had higher efficacy than the other two similar drugs - AstraZeneca's Calquence and Johnson & Johnson and AbbVie's Imbruvica. The complete response for Brukinsa reached 59 percent among patients with relapsed or refractory MCL, while that for Calquence and Imbruvica were 40 percent and 21 percent respectively.

The FDA approval came months ahead of schedule, catching even BeOne's leadership by surprise. In November 2019, zanubrutinib became the first cancer drug developed in China to gain FDA approval; it received accelerated approval for the treatment of mantle cell lymphoma (MCL), a rare and aggressive form of non-Hodgkin lymphoma. The approval was based on an overall response rate of 84%, with patients experiencing tumor shrinkage that lasted a median of 19.5 months.

But the real battle was just beginning. Brukinsa was entering a market dominated by Imbruvica, which had generated $8.43 billion in global sales. The pricing strategy was crucial: The price tag at ex-factory level was at $12,935 upon launch in the US for 120 hard capsules of 80mg. This positioned Brukinsa competitively against Imbruvica's tablet formulation while undercutting AstraZeneca's Calquence, which was priced around $14,000 for a 30-day supply.

The commercial rollout demonstrated BeOne's global ambitions. Launch in its home market, China, occurred eight months after its first commercialisation in the US. This was quickly followed by launches or registrations in the United Arab Emirates, France (as part of a compassionate use programme), Germany, Saudi Arabia, Austria and Norway. The China pricing revealed the stark reality of global pharmaceutical economics—at just $915.90 for a 64-pack, Chinese patients paid a fraction of what Americans did for the same drug.

The momentum built steadily. By 2021, Brukinsa had received FDA approval for Waldenström's macroglobulinemia. In 2023, came the game-changing approval for chronic lymphocytic leukemia (CLL)—the largest indication for BTK inhibitors. This wasn't just another indication; it came with superiority data from the ALPINE trial showing Brukinsa beat Imbruvica head-to-head in progression-free survival.

Global sales soared to $413 million in Q4 and $1.3 billion for the full year 2023, up by 135% and 129% respectively. Brukinsa had crossed the blockbuster threshold—a feat achieved by only a handful of cancer drugs each decade. The drug is BeiGene's top product, accounting for $1.3 billion in revenue in 2023, a more than 128% increase over the product's sales in 2022.

The success of Brukinsa represented more than just financial milestones. It validated BeOne's entire strategic premise: that a company could develop world-class cancer drugs outside the traditional pharma hubs, leverage global clinical trial infrastructure, and compete successfully against entrenched incumbents. It also demonstrated that Chinese drug development had reached a level of sophistication where "Made in China" no longer meant copy—it could mean breakthrough innovation.

VI. The Celgene Deal & Strategic Pivot

July 2017. The boardrooms of Summit, New Jersey, where Celgene's headquarters resided, and Beijing's Zhongguancun district couldn't have been more different. Yet the deal struck between these two locations would reshape both companies' futures in ways neither fully anticipated.

In July 2017, BeOne entered into a partnership with Celgene to continue the development and commercialization of the cancer drug BGB-A317, also known as tislelizumab. BeOne also acquired Celgene's operations in China as well as the rights to commercialize Abraxane, Revlimid and Vidaza, Celgene's approved drugs in China. The structure was unlike anything the industry had seen: a complex swap where an emerging Chinese biotech would gain instant commercial credibility while a Western pharma giant would get a foothold in the PD-1 race.

As part of the deal, Celgene made a $150 million equity investment in BeOne and acquired the rights for the sale of tislelizumab overseas for $263 million, with another $980 million plus royalties contingent on future sales. For BeOne, the upfront cash was transformative—it meant runway to advance multiple programs without dilutive financing rounds. But the real prize was Celgene's China operations: an established commercial infrastructure with relationships at over 800 hospitals.

The genius of the deal lay in a single clause that most observers overlooked at signing. The deal stipulated that, if Celgene began work on a competitor drug, BeOne could buy back the rights to tislelizumab. Oyler's team had insisted on this provision, anticipating the consolidation wave sweeping through Big Pharma. It seemed like prudent lawyering at the time. It would prove to be worth billions.

Eighteen months later, the pharmaceutical world shifted on its axis. Bristol-Myers Squibb announced its $74 billion acquisition of Celgene—creating a combined entity with multiple PD-1 assets. The conflict was immediate and obvious: BMS's Opdivo was a direct competitor to tislelizumab. In January 2019, Celgene was acquired by Bristol-Myers Squibb, which is developing a similar cancer immunotherapy drug, Opdivo, allowing BeOne to regain its overseas rights to tislelizumab. Celgene returned the rights to the drug in June 2019 along with a payment of $150 million to conclude the deal.

The buyback clause that had seemed like a defensive provision became an offensive weapon. Not only did BeOne regain full global rights to tislelizumab, but they also received $150 million—effectively getting paid to take back their own drug. Meanwhile, they retained the Chinese rights to Abraxane, Revlimid, and Vidaza, which were generating hundreds of millions in revenue.

For BeOne, the Celgene partnership had served its purpose perfectly. They'd gained commercial capabilities, established themselves as a serious player in China's pharmaceutical market, and maintained control of their lead PD-1 asset. The $413 million in total proceeds from Celgene had funded the company through crucial clinical milestones without significant dilution.

The unwinding of the Celgene deal also taught BeOne a crucial lesson about partnership dynamics in an era of pharmaceutical consolidation. When they later partnered with Novartis on tislelizumab in 2021, they structured the deal differently—maintaining more control and ensuring clearer paths to commercialization regardless of future M&A activity.

Building commercial capabilities alongside R&D became BeOne's defining characteristic during this period. While most biotechs outsourced commercial operations until they had approved products, BeOne built a 600-person sales force in China before they had a single drug approval. This forward investment looked risky to Wall Street analysts but reflected Oyler's conviction that controlling the full value chain was essential for long-term success.

VII. Global Expansion & The Rebranding

The boardroom at BeOne's Cambridge headquarters was unusually full on November 14, 2024. After months of deliberation, the leadership team was ready to announce a decision that would fundamentally reshape the company's identity: On 14 November 2024 the company announced its intention to rebrand as BeOne Medicines. This wasn't merely cosmetic rebranding—it was a declaration of independence from the company's Chinese origins and an assertion of its global ambitions.

The strategic logic was compelling. By 2022, BeOne had evolved far beyond its Beijing roots. BeOne opened several new offices around the world in 2022, including a regional office in Basel, Switzerland, which serves as a hub for the company's operations in Europe. As of 2022, the company had enrolled patients from more than 45 countries, including 25 European countries, in clinical trials. The company had opened a new office in Sydney, Australia, in 2022, although it conducted its first research in the country in 2014. The company has become one of the largest clinical research organizations in Australia.

The name "BeOne" carried multiple layers of meaning. The "Be" represented the fundamental goal of any cancer patient—to simply be free of disease. The "One" symbolized unity in the fight against cancer. But there was also a clever visual trick: the logo stylized "One" to read as "Onc"—a nod to oncology that insiders would recognize. BeOne changed its stock ticker to ONC in January 2025 and redomiciled to Basel, Switzerland in May 2025.

The Swiss redomiciliation was particularly strategic. Basel wasn't just another European city—it was the global capital of pharmaceutical innovation, home to Roche and Novartis. By establishing legal domicile in Switzerland, BeOne gained several advantages: access to Switzerland's extensive network of double taxation treaties, proximity to European regulatory authorities, and perhaps most importantly, distance from the geopolitical tensions surrounding U.S.-China relations.

"BeOne represents more than a name change—it's not only a reflection of who we are today as a leading global oncology company, but also our ambition to redefine what's possible in oncology as we unite patients, families, scientists, physicians, governments, and other oncology public health stakeholders around the world in our shared mission against cancer," said John V. Oyler, Co-Founder, Chairman and CEO at BeOne. "While I know that our work is not done, I am extremely proud of the progress we have made with the explosive growth of BRUKINSA as the backbone of our hematology franchise, the expansion of our PD-1 inhibitor, TEVIMBRA, and our potentially transformative oncology pipeline of more than 50 investigational assets, one of the most prolific in the industry.

The transformation wasn't just corporate structure—it was operational excellence at scale. BeOne's entrepreneurial research team, comprising more than 1,100 colleagues, advanced 13 new molecular entities into the clinic in 2024 alone, outpacing even the largest pharmaceutical companies. Further, its nearly 3,700-strong clinical development team has active or planned trials across more than 45 countries and regions, accelerating early-stage innovation through its "Fast to Proof-of-Concept" approach. To date, the Company has enrolled more than 25,000 patients in more than 170 trials, delivering speed and cost advantages that set it apart from industry peers.

Recent FDA approvals validated the global strategy. In 2024, the U.S. FDA approved Tevimbra in combination with platinum and fluoropyrimidine-based chemotherapy for the first-line treatment of unresectable or metastatic HER2-negative gastric or gastroesophageal junction adenocarcinoma in adults whose tumors express PD-L1 (≥1). The European Commission (EC) also approved its use in combination with chemotherapy for the first-line treatment of esophageal squamous cell carcinoma and gastric or gastroesophageal junction adenocarcinoma. On 4 March 2025, BeOne Medicines announced the FDA's approval of Tevimbra for the first-line treatment of advanced esophageal squamous cell carcinoma in combination with chemotherapy.

The strategic rationale for Swiss headquarters went beyond symbolism. Switzerland offered stability in an increasingly fractured global pharmaceutical landscape. With manufacturing facilities in the U.S., China, and Europe, BeOne needed a neutral base from which to coordinate global operations. Basel provided that, along with access to a deep pool of pharmaceutical talent and proximity to the European Medicines Agency.

VIII. The Pipeline & Platform Today

Walk through BeOne's laboratories today, and you'll find something remarkable: a pipeline that would make companies five times their size envious. BeOne's entrepreneurial research team, comprising more than 1,100 colleagues, advanced 13 new molecular entities into the clinic in 2024 alone, outpacing even the largest pharmaceutical companies. This isn't just productivity—it's a fundamental rethinking of how drug development should work.

The clinical pipeline reads like a textbook of cutting-edge oncology approaches. Sonrotoclax is an investigational small molecule B-cell lymphoma 2 (BCL2) inhibitor. It belongs to a class of BCL2 homology 3 (BH3) mimetics. Sonrotoclax is more potent and selective for BCL2 relative to BCLxL than venetoclax and has potential for greater convenience than venetoclax. This isn't just another me-too drug; it's designed to address the limitations of AbbVie's blockbuster Venclexta while offering improved safety and dosing convenience.

But the real innovation lies in BeOne's CDAC (Chimeric Degradation Activation Compound) platform. BGB‑16673 is an orally available, brain-penetrating Bruton's tyrosine kinase (BTK) targeting chimeric degradation activation compound (CDAC) designed to promote the degradation, or breakdown, of both wildtype and mutant forms of BTK, including those that commonly result in resistance to BTK inhibitors in patients who experience progressive disease. This represents a paradigm shift—instead of just blocking BTK, the drug completely eliminates it from cancer cells, potentially overcoming the resistance that plagues current therapies.

BGB-16673 (BTK CDAC): Data from the Phase 1/2 CaDAnCe-101 CLL study (NCT05006716) demonstrated that treatment with BGB-16673 was generally well tolerated in this heavily pretreated population of patients. Promising antitumor activity was observed in patients with high-risk features, including in patients with BTK inhibitor-resistant mutations and those previously exposed to covalent BTK inhibitors, noncovalent BTK inhibitors, and BCL2 inhibitors. From the cohort of CLL/SLL patients, BGB-16673 demonstrated an ORR of 94% at the 200mg dose. These aren't incremental improvements—they're potentially transformative results in patients who have exhausted other options.

The combination strategy is particularly elegant. Meanwhile, early data show the combination of sonrotoclax and BRUKINSA has demonstrated compelling efficacy and the potential to offer a best-in-class fixed-duration treatment in CLL, setting the stage for a possible new standard of care. This addresses one of the major challenges in CLL treatment: the need for continuous, lifelong therapy that burdens patients financially and physically.

Beyond hematology, BeOne is building comprehensive franchises in solid tumors. The company's antibody-drug conjugate (ADC) platform has produced multiple candidates targeting validated cancer antigens with next-generation linker-payload technologies. Their multi-specific antibody platform is generating T-cell engagers and immune modulators that could compete with the best offerings from Genentech and Amgen.

Founded in 2010 by chief executive officer John V. Oyler and Xiaodong Wang, the company is headquartered in Cambridge, Massachusetts and has locations on six continents, in over 45 countries. BeOne has a large presence in the Chinese market. This global footprint isn't just about commercial reach—it enables BeOne to run parallel clinical trials across multiple geographies, accelerating development timelines and reducing costs.

The manufacturing infrastructure supporting this pipeline is equally impressive. BeOne has built state-of-the-art facilities for small molecules, biologics, and ADCs across multiple continents. This vertical integration provides control over quality, cost, and supply chain—crucial advantages when competing against companies that outsource most of their manufacturing.

With more than 10' 000 employees worldwide working on five continents, it has one of the largest oncology research teams in the industry with ~ 1'100 scientists, driving a treatment pipeline that covers 80% of the world's cancers by incidence. This scale, combined with the cost advantages of their China operations, allows BeOne to pursue multiple high-risk, high-reward programs simultaneously—a luxury most biotechs can't afford.

IX. Business Model & Competitive Strategy

The genius of BeOne's business model lies not in any single element but in how the pieces fit together to create competitive advantages that compound over time. While Western pharmaceutical companies built their empires on blockbuster drugs protected by patents, BeOne constructed something different: a fully integrated oncology company optimized for speed, cost efficiency, and global reach.

The "China for the world" strategy starts with clinical trials. Running a Phase 3 oncology trial in the United States can cost $100-200 million. In China, BeOne can conduct the same trial for a fraction of that cost—not by cutting corners, but by leveraging lower operational costs and a massive patient population eager to access innovative treatments. But here's the key: BeOne designs these trials to meet FDA and EMA standards from day one, allowing the data to support global registrations.

With more than 11,000 colleagues across six continents, the company has created a differentiated model through strategic investments in internal research, clinical development, manufacturing, and global commercial model. This enables BeOne to accelerate the development of its broad hematology and solid tumor oncology pipeline and bring innovative cancer medicines to patients faster. By controlling the value chain, BeOne is also tackling affordability, delivering strategic time and cost advantages.

The pricing strategy reveals sophisticated thinking about global markets. The price tag at ex-factory level was at $12,935 upon launch in the US for 120 hard capsules of 80mg. In the U.S., Brukinsa is priced competitively with Imbruvica—high enough to generate substantial margins but low enough to gain formulary access. In China, the same drug sells for a fraction of the price, but the volume opportunity compensates for lower margins. This dual-pricing model allows BeOne to maximize revenue while expanding access.

Building for global scale from Day 1 has been a defining characteristic. Most biotechs follow a predictable path: develop a drug, get it approved in one market, then slowly expand. BeOne inverted this model. They build global infrastructure before they have global products, betting that the efficiency gains from integrated operations would more than offset the upfront investment.

The commercial strategy demonstrates similar sophistication. In the U.S., BeOne doesn't try to outmuscle Big Pharma with army-sized sales forces. Instead, they focus on key opinion leaders and academic centers, leveraging clinical data and real-world evidence to drive adoption. The message is simple: equivalent or superior efficacy with better safety and competitive pricing.

Strategic investments in internal capabilities have created a virtuous cycle. By controlling manufacturing, BeOne can iterate quickly on process improvements, reducing costs that can be passed on as lower prices or higher margins. By running their own clinical trials, they accumulate expertise that makes each subsequent trial more efficient. By maintaining global regulatory teams, they can navigate multiple approval pathways simultaneously.

The competitive moat is multilayered. First, there's the cost advantage—BeOne can develop drugs for a fraction of what it costs Western competitors. Second, there's speed—their integrated model eliminates the friction that slows down traditional pharma development. Third, there's geographic diversification—unlike companies dependent on single markets, BeOne can optimize across multiple healthcare systems. Finally, there's the talent arbitrage—they can attract world-class Chinese scientists at lower costs than Silicon Valley or Cambridge wages.

Under John's leadership, the company's medicines have reached more than 1.7 million patients globally, and in the past year alone, advanced 13 new molecules into the clinic—outpacing industry peers. This isn't just operational excellence—it's a fundamental reimagining of how a global pharmaceutical company should be structured in the 21st century.

X. Bear vs. Bull Case

Bull Case: The Path to Pharmaceutical Nobility

The numbers tell a compelling growth story. In 2024, BeOne Medicines's revenue was $3.81 billion, an increase of 54.96% compared to the previous year's $2.46 billion. Losses were -$644.79 million, -26.87% less than in 2023. This isn't just growth—it's growth with improving fundamentals, the holy grail for biotech investors.

BRUKINSA continues to be the primary growth catalyst, with revenues doubling year-over-year to $828 million in Q4 and $2.6 billion for the full year. The drug has captured market leadership in new CLL patient starts in the U.S., demonstrating successful commercial execution against entrenched competitors. When a relatively unknown company takes market share from AbbVie and J&J in their core franchise, it signals something profound about competitive dynamics.

The pipeline depth provides multiple shots on goal. With 50+ potential medicines in development and the ability to advance 13 new molecules into the clinic in a single year, BeOne has de-risked its future through diversification. Even if half the pipeline fails—a reasonable assumption in oncology—the remaining programs could generate tens of billions in value.

The patent settlement with MSN Pharmaceuticals secures market exclusivity until at least 2037, effectively removing a significant long-term risk factor and providing over a decade of protected revenue potential. This visibility on Brukinsa's revenue stream alone could justify much of BeOne's current valuation.

Geographic diversification provides resilience. Unlike companies dependent on single markets, BeOne can navigate regulatory setbacks, pricing pressures, or competitive threats in one region while maintaining growth elsewhere. The Swiss redomiciliation further reduces geopolitical risk while maintaining operational flexibility.

The talent engine keeps producing. With over 1,100 scientists and the ability to attract top talent from both East and West, BeOne has built a sustainable innovation advantage. The company culture—entrepreneurial, fast-moving, scientifically rigorous—attracts researchers who might otherwise go to Genentech or Novartis.

Bear Case: The Shadows on the Horizon

Geopolitical tensions represent an existential risk that can't be diversified away. Despite the Swiss redomiciliation, BeOne remains operationally dependent on both the U.S. and China. A serious deterioration in U.S.-China relations could force the company to choose sides, potentially sacrificing major markets or facing regulatory restrictions.

Competition from established BTK inhibitors isn't going away. While Brukinsa has gained share, Imbruvica still generates billions in revenue, and AstraZeneca's Calquence continues to grow. The next generation of BTK inhibitors and degraders from Big Pharma could erode Brukinsa's differentiation advantage.

The company remains unprofitable despite massive revenue growth. While losses are decreasing, BeOne still burned through $644.79 million in 2024. The path to profitability requires either significant revenue growth or operating expense reductions—both challenging in the competitive oncology market.

Regulatory challenges multiply with geographic expansion. Managing clinical trials and regulatory submissions across 45+ countries creates complexity that could lead to delays, increased costs, or compliance issues. A single manufacturing problem or clinical trial failure could cascade across multiple markets.

The PD-1 franchise faces intense competition. Tevimbra enters a market dominated by Keytruda and Opdivo, with numerous biosimilars on the horizon. Without clear differentiation beyond price, gaining meaningful market share will require massive commercial investment with uncertain returns.

Pipeline attrition is inevitable in oncology. While BeOne has many shots on goal, the industry-wide success rate for oncology drugs entering clinical trials is less than 10%. The company's aggressive pipeline expansion could lead to significant write-offs if programs fail in late-stage development.

The Verdict

The bull case rests on execution and momentum—BeOne has demonstrated both. The bear case centers on external factors largely beyond the company's control. For investors, the question becomes: Is the potential for a global, fully integrated oncology powerhouse worth the geopolitical and competitive risks?

The answer may lie in BeOne's unique position. They're not just another biotech hoping for a buyout or a single drug approval. They're building something more ambitious—a new model for global pharmaceutical development. If successful, BeOne could become the template for how 21st-century pharma companies operate: globally distributed, vertically integrated, and optimized for both innovation and access.

XI. Recent News

The momentum continues to build. BeOne Medicines reported revenue of $1.3 billion for Q2 2025, representing 42% year-on-year growth. GAAP earnings per ADS grew by $2 from Q2 of last year, and the company generated $220 million of free cash flow in Q2. The growth was driven by strong commercial performance, particularly the success of BRUKINSA and geographic expansion.

In a significant showcase for the future, BeOne announced major advancements to its industry-leading oncology pipeline during its investor R&D Day in June 2025. The event came at a pivotal moment for the Company, which has more than 40 clinical and commercial stage assets in development, a signal of both scale and ambition.

The regulatory momentum has been particularly strong. On 4 March 2025, BeOne Medicines announced the FDA's approval of Tevimbra for the first-line treatment of advanced esophageal squamous cell carcinoma in combination with chemotherapy. On 31 March 2025, the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency issued a positive opinion recommending approval of Tevimbra (tislelizumab), in combination with etoposide and platinum chemotherapy, as a first-line treatment for adult patients with extensive-stage small cell lung cancer.

The pipeline continues to deliver. At the American Society of Clinical Oncology (ASCO) Annual Meeting in Chicago, BeOne announced new clinical data from its emerging breast cancer pipeline. Poster presentations featured preliminary results of the dose escalation studies of two investigational molecules: BG-C9074, a novel B7-H4-targeting antibody-drug conjugate (ADC) in patients with advanced solid tumors, including breast cancer, and BG-68501, a cyclin-dependent kinase-2 inhibitor (CDK2i), in HR+/HER2- breast cancer patients with prior CDK4/6i exposure.

XII. Links & Resources

Company Resources: - Official Website: www.beonemedicines.com - Investor Relations: https://ir.beonemedicines.com - Clinical Trials: ClinicalTrials.gov (search "BeOne" or "BeiGene")

Regulatory Filings: - SEC Filings: SEC EDGAR Database (Ticker: ONC) - Hong Kong Exchange Filings: HKEX (06160) - Shanghai Stock Exchange: SSE (688235)

Scientific Publications: - PubMed Database: Search "zanubrutinib" or "tislelizumab" - Major oncology journals featuring BeOne research

Industry Analysis: - Evaluate Pharma reports on BTK inhibitor market - GlobalData oncology pipeline analysis - BioCentury coverage of BeOne strategic moves

Key Interviews & Profiles: - John Oyler LinkedIn: Regular updates on company milestones - Acquired.fm-style analysis frameworks for pharmaceutical companies - Major investment bank initiation reports (Goldman Sachs, Morgan Stanley)

The story of BeOne Medicines is still being written. From a Beijing startup to a global oncology powerhouse, the company has defied conventional wisdom about how pharmaceutical companies should be built and operated. Whether BeOne becomes the template for 21st-century pharma or remains a unique product of its time and circumstances will depend on execution, external factors, and a measure of luck. What's certain is that they've already changed the conversation about what's possible when East meets West in the pursuit of conquering cancer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube