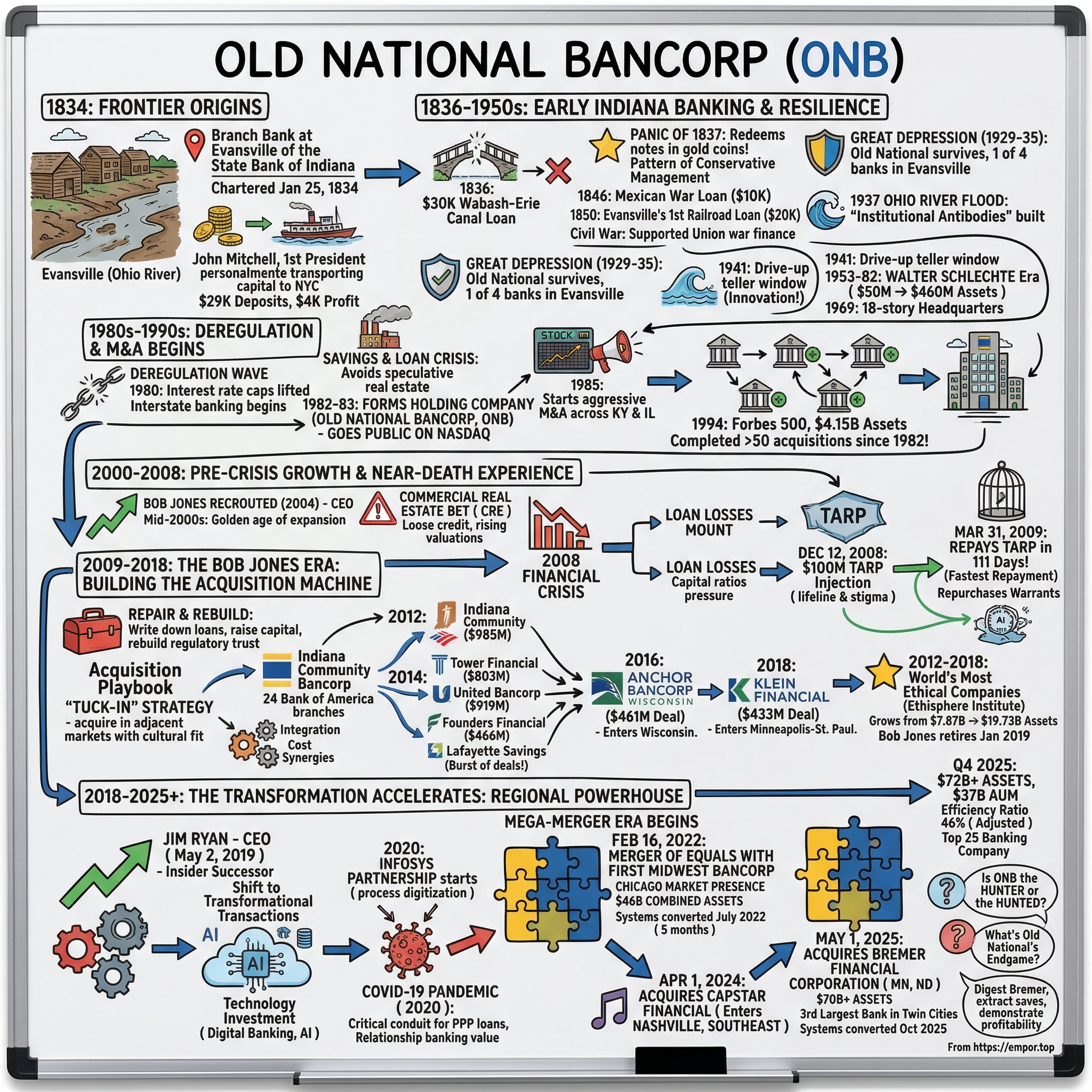

Old National Bancorp: The 186-Year Journey from Frontier Banking to Regional Powerhouse

The Frontier Origins and Early Indiana Banking (1834–1950s)

The bank's first real test came almost immediately. In 1836, Old National's predecessor extended a $30,000 loan toward the Wabash-Erie Canal—a massive infrastructure project that was supposed to connect the Great Lakes to the Ohio River. When the Panic of 1837 swept the nation, the canal project collapsed and the loan was never repaid. Banks across the country shuttered. But the State Bank of Indiana, Old National's parent system, did something extraordinary: it redeemed its notes in gold coins, making it the sole bank in Indiana offering hard currency during the panic. That decision—choosing credibility over convenience—established a pattern of conservative financial management that would define the institution for nearly two centuries.

The frontier bank proved remarkably useful to a young state. In 1846, it loaned Indiana's government $10,000 to clothe volunteers serving in the Mexican War. Four years later, it provided $20,000 to help fund Evansville's first railroad. These were not enormous sums, but they cemented the bank's role as a civic institution, not merely a commercial one.

When the Panic of 1857 hit, the bank again distinguished itself by redeeming all notes with cash while competitors closed their doors. This was becoming a pattern: panic after panic, depression after depression, the Evansville bank survived by doing the unglamorous thing—maintaining reserves, honoring obligations, avoiding speculation.

The Civil War tested the bank differently. Evansville sat on the border between Union and Confederate territory, and the cessation of southern river trade created genuine hardship. But the bank maintained operations and supported Union war finance. By 1873, when silver demonetization triggered another national crisis, the bank had survived enough panics to earn a reputation. When it took the name "Old National Bank of Evansville" in 1884, observers described it as having "a model banking history" with "the highest qualities" in the region. The name "Old" was not marketing—it was a statement of endurance.

The early twentieth century brought the Federal Reserve Act of 1913, and Old National joined the new system. Henry Reis assumed the presidency that year and guided the institution through World War I and the post-war adjustment. But the real test was the Great Depression. Of eleven banks operating in Evansville in 1929, only four survived through 1935—a failure rate that would have been shocking had it not been replicated in city after city across America. Old National survived because of the same conservative instincts that had protected it through every prior panic: adequate reserves, prudent lending, and a customer base that trusted the institution enough to leave their deposits in place rather than trigger a run.

Then came the catastrophic Ohio River flood of 1937, which inundated Evansville and temporarily displaced bank operations but did not interrupt service to customers. The flood was a different kind of crisis—not financial but physical—and Old National's response reinforced its identity as a community institution that would be there when it mattered most. The bank had developed what might be called institutional antibodies—an organizational immune system built through repeated exposure to crisis.

The post-war decades were the sleepy years of American banking. Glass-Steagall separated commercial and investment banking. Regulation Q capped deposit rates. Interstate banking was prohibited. In this protected environment, Old National grew steadily but unspectacularly under a series of capable leaders. Robert Mathias led through the 1940s, implementing pioneering personnel policies. In 1941, the bank installed its first drive-up teller window—an innovation that now seems quaint but represented the era's version of digital transformation.

The most consequential mid-century figure was Walter Schlechte, who led from 1953 to 1982. Under his nearly three-decade tenure, Old National grew from a $50 million institution to a $460 million one, becoming among the most profitable banks of its size in the country. Schlechte began diversifying through acquisitions in the 1960s—Carter Mortgage Company in 1961, a data processing operation called Tabco Corp. in 1964. In 1969, the bank opened an eighteen-story headquarters in Evansville, a symbolic declaration that this was no longer a sleepy community bank. These early moves planted the seeds for what would become the defining strategic capability of the modern institution.

For investors, the key insight from this century-plus of history is not the specific events but the organizational DNA they created. Old National embedded itself so deeply in Midwest communities that its deposit franchise became a genuine competitive moat—one built on relationships, not rates. That moat would prove critical when deregulation blew the doors open on American banking.

Deregulation and the S&L Crisis: Setting the Stage (1980s–1990s)

The American banking industry underwent a transformation in the 1980s that is difficult to overstate. The Depository Institutions Deregulation and Monetary Control Act of 1980 began dismantling the regulatory framework that had kept banking stable—and sleepy—since the Depression. Interest rate caps were lifted. Savings and loan institutions gained new powers. Interstate banking restrictions began to fall state by state. For a bank like Old National, rooted in a specific community for 150 years, this was both an existential threat and an unprecedented opportunity.

Old National's leadership made a pivotal structural decision in 1982-1983: they formed Old National Bancorp as a bank holding company and took it public on NASDAQ. The timing was deliberate. Management could see the deregulation wave coming and understood that accessing public capital markets was essential for survival in the new competitive landscape. Without the ability to issue stock for acquisitions and raise capital efficiently, Old National would remain a small community bank—increasingly vulnerable to larger competitors entering its markets.

When Indiana passed legislation permitting out-of-state banking expansion in 1985, Old National was ready. The holding company structure allowed it to launch an aggressive multi-state acquisition strategy across Kentucky and Illinois. Through the late 1980s and into the 1990s, the company was completing roughly three acquisitions per year—an extraordinary pace for a bank of its size.

The savings and loan crisis of the late 1980s and early 1990s reshaped the competitive dynamics around Old National. Hundreds of thrifts and community banks failed, creating both acquisition opportunities and competitive vacuums in local markets. Old National, with its conservative management philosophy, avoided the derivatives losses, speculative real estate investments, and problematic asset concentrations that destroyed competitors. By 1994, the bank ranked among the Forbes 500 institutions with $4.15 billion in assets. A year later, assets had grown another 16% to $4.82 billion through deals like the $18 million acquisition of Greencastle-based First United Savings Bank.

This period was essentially Old National's graduate school for M&A. Each deal taught the organization something about integration—how to merge technology systems, how to retain key employees, how to communicate with acquired customers, how to extract cost synergies without destroying the relationship banking culture that made acquired banks valuable in the first place. The 1996 acquisition of Bloomington-based Workingmens Capital Holdings, in an all-stock transaction, demonstrated that Old National could structure deals creatively while preserving capital.

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 further accelerated the possibilities, allowing banks to acquire branches across state lines. For Old National, this meant the artificial geographic barriers that had protected its home market were also the barriers that had limited its growth. The strategic choice crystallized during this decade: Old National would stay regional but grow aggressively within its expanding footprint. It would not try to become a national bank or a Wall Street player. It would stay in the Midwest, doing what it knew—relationship banking—but at ever-increasing scale. Since forming the holding company in 1982, Old National has completed more than fifty financial institution acquisitions. That number did not accumulate overnight. It was built one deal at a time, through the 1990s grind of small acquisitions in adjacent markets, each one teaching the organization how to do the next one better.

The 2000s: Pre-Crisis Growth and Near-Death Experience (2000–2008)

Bob Jones arrived at Old National as Chairman and CEO in September 2004, recruited from KeyCorp in Cleveland where he had spent twenty-five years rising through the ranks to run McDonald Investments, KeyCorp's brokerage subsidiary. Jones was a career banker, schooled in the disciplined credit culture of the Midwest, and he stepped into an institution with nearly $9 billion in assets and a hunger to grow.

The mid-2000s were a golden age for bank expansion—or so it seemed. Credit was loose, real estate values were climbing, and the Midwest was experiencing a commercial real estate boom that seemed to validate aggressive lending. Old National pushed into Kentucky, Illinois, and Michigan, building its loan portfolio and expanding its branch network. The commercial real estate bet felt like a sure thing at the time—occupancy rates were high, valuations were rising, and the competition was lending aggressively. Falling behind meant losing market share. This was the trap that ensnared hundreds of American banks: the incentive structure rewarded growth over prudence, and the consequences of conservatism—lost market share, lower returns, underperforming stock—were immediate and visible, while the consequences of aggression were distant and hypothetical. Until they weren't.

Then the music stopped. The 2008 financial crisis hit the banking system with a force that exposed every weakness in every balance sheet across America. For Old National, the stress was real. The bank's commercial real estate portfolio, which had seemed so prudent during the expansion years, suddenly carried significant risk. Loan losses mounted. Capital ratios came under pressure. The board faced a series of painful decisions about the institution's very survival.

On December 12, 2008, the U.S. Treasury purchased $100 million in preferred, non-voting stock from Old National Bancorp under the Troubled Asset Relief Program. The TARP injection was both a lifeline and a stigma—necessary for stabilization but deeply uncomfortable for an institution that had prided itself on conservative management for 174 years. The bank's total assets declined to $7.87 billion by year-end 2008, reflecting a deliberate strategic decision to shrink the balance sheet and shed risky exposures.

What happened next set Old National apart from hundreds of other TARP recipients.

On March 31, 2009—just 111 days after receiving the funds—Old National repurchased all $100 million of the outstanding preferred stock. It was one of the earliest and fastest TARP repayments in the country, a signal to regulators, investors, and the market that Old National intended to recover on its own terms. Then, on May 8, 2009, Old National paid $1.2 million to repurchase the TARP warrants. This transaction generated significant controversy: the warrants had been independently valued at approximately $5.8 million, meaning Old National paid roughly 21 cents on the dollar. Congressional leaders including Brad Miller and Senator Jack Reed formally objected, demanding fair-market pricing for subsequent warrant repurchases. Old National became the first publicly traded bank to complete a negotiated warrant repurchase under the Capital Purchase Program—a distinction that drew both admiration for its speed and criticism for its pricing.

The total TARP-related revenue to the government from Old National was $2.71 million—$1.51 million in dividends plus the $1.2 million in warrant proceeds. Modest, perhaps, but the rapid repayment signaled something important: Old National's balance sheet, while stressed, was not broken. The crisis had revealed vulnerabilities, but it had not destroyed the core franchise—the deep community relationships, the sticky deposits, the conservative credit culture that, despite the real estate missteps, had kept the bank fundamentally solvent.

The real inflection point was not financial but psychological. The near-death experience forced a fundamental rethinking of Old National's strategy. The leadership team realized that survival alone was not a strategy. In a consolidating industry, a $7.87 billion bank with a scarred balance sheet was neither big enough to be safe nor small enough to hide. Old National needed to transform—not just recover—and that transformation would require a playbook the bank had never used before.

The Bob Jones Era: Building the Acquisition Machine (2009–2018)

The years immediately following the crisis were about repair. Jones and his team systematically wrote down bad loans, raised capital, and rebuilt regulatory trust. This was grinding, unglamorous work—the banking equivalent of physical therapy after a serious injury. The goal was not just to stabilize the balance sheet but to earn back the regulatory credibility needed to resume acquisitions. For a bank that wanted to grow through M&A, the ability to receive regulatory approval for deals was everything.

By 2012, Old National had healed enough to start growing again. The first major post-crisis deal was the acquisition of Indiana Community Bancorp, announced in January 2012. Indiana Community, headquartered in Columbus, Indiana, held approximately $985 million in assets. The transaction was structured as a 100% stock deal—a critical detail, because it preserved Old National's cash while using its recovering stock as currency. Indiana Community shareholders received 1.90 shares of Old National for each share they held, valuing the deal at approximately $79.2 million. The Federal Reserve approved the transaction in August 2012, signaling that regulators were comfortable with Old National's recovery and growth plans.

That same year, Old National acquired 24 retail branches from Bank of America across Indiana and Michigan, adding significant deposit mass and customer relationships in a single stroke. Bank of America was rationalizing its branch network, shedding locations in markets it considered non-core. For Old National, those same markets were home territory.

The momentum accelerated in 2014 with a remarkable four-acquisition burst. Tower Financial Corporation in Fort Wayne, Indiana, brought $803 million in assets and six banking centers for approximately $107.7 million. United Bancorp of Ann Arbor, Michigan, added $919 million in assets and doubled Old National's presence in Michigan for $173.1 million. Founders Financial Corporation of Grand Rapids contributed another $466 million. And Lafayette Savings Bank filled in Indiana geography.

In a single year, Old National absorbed more than $2 billion in new assets through disciplined, adjacent-market acquisitions.

What made these deals distinctive was not their size but their logic. Each one followed what Old National would come to call the "tuck-in" strategy: acquire banks in adjacent markets where there was cultural fit, reasonable pricing, and competent existing management. The targets were community banks that had hit a natural ceiling—too small to invest in the technology and compliance infrastructure that post-Dodd-Frank regulation demanded, but too valuable as franchises to simply wind down. Old National offered these banks something their shareholders increasingly needed: an exit that preserved the community banking identity while delivering fair value.

Jones's approach during this period also benefited from a crucial structural advantage. The 2008 crisis had left many potential acquirers—larger banks with scarred balance sheets, tightened capital requirements, or distracted management teams—unable or unwilling to pursue deals. Old National, having repaired its balance sheet quickly and maintained regulatory favor, could buy when others could not. The competition for these community bank acquisitions was less intense than it had been in the pre-crisis era, allowing Old National to acquire at reasonable prices.

The defining deal of the Jones era came in 2016: the acquisition of Anchor BanCorp Wisconsin, the parent company of AnchorBank—the third-largest bank headquartered in Wisconsin. At approximately $461 million in cash and stock, structured as 60% stock and 40% cash, it was Old National's largest acquisition to date. The deal brought nearly four dozen banking centers throughout Wisconsin and represented Old National's first entry into a new state since the 1990s expansion into Kentucky and Illinois.

The Anchor deal embodied the evolving thesis. This was not a tuck-in—it was a geographic leap, a declaration that Old National would build a multi-state Midwest franchise, not merely fill in Indiana blanks. Management projected cost savings exceeding 30% of the target's expense base, a figure that reflected both genuine redundancies and Old National's growing confidence in its integration capabilities. The deal closed in May 2016, and Wisconsin became a core market.

The funding model for this acquisition spree deserves attention, because it reveals how Old National financed growth without destroying shareholder value. The vast majority of deals were structured as all-stock or predominantly stock transactions. This was strategic, not accidental. Stock deals preserved Old National's cash and capital ratios—critical for maintaining regulatory standing—while allowing the bank to use its own equity as acquisition currency. The risk, of course, was dilution: each stock deal issued new shares, potentially diluting existing shareholders' ownership. Old National managed this by targeting banks at reasonable valuations—typically in the range of 1.0 to 1.5 times tangible book value—and by realizing cost synergies quickly enough that the acquired earnings more than offset the dilution. The result was that tangible book value per share grew steadily through the acquisition cycle rather than being eroded by it.

Then came the Klein Financial acquisition in 2018, which pushed Old National into the Minneapolis-Saint Paul market—the largest metropolitan area in the Upper Midwest. Klein Financial, parent of KleinBank and headquartered in suburban Chaska, Minnesota, held $2 billion in assets with 18 banking locations across the Twin Cities. The all-stock deal was valued at approximately $433.8 million, making it Old National's second-largest acquisition after Anchor. On a pro forma basis, Old National held approximately $3.5 billion in deposits in Minnesota and the fifth-largest market share in the Minneapolis MSA. Minneapolis became Old National's largest deposit metro.

Throughout these years, Jones was building something beyond a collection of acquired banks. He was building a reputation—Old National as the acquirer of choice for Midwest community banks. The bank was recognized seven consecutive times, from 2012 through 2018, as one of the Ethisphere Institute's World's Most Ethical Companies. That designation was not window dressing. In community bank M&A, where sellers are often family owners or long-tenured managers who care deeply about what happens to their employees and customers, reputation matters enormously. Sellers chose Old National because they trusted that their people would be treated fairly, their communities would continue to be served, and the deal would actually close on the terms agreed.

Under Jones, Old National grew from a crisis-battered $7.87 billion bank to a $19.73 billion institution through eleven strategic acquisitions. He crossed the $10 billion Dodd-Frank threshold—which triggers enhanced regulatory requirements including stress testing—and used the regulatory infrastructure built to comply as a competitive advantage, arguing that the investment was worth it because it enabled continued acquisitions. When Jones announced his retirement in January 2019 after fourteen years as CEO, he had fundamentally transformed Old National's identity from a recovering community bank into a disciplined regional acquirer.

The Transformation Accelerates: Becoming a Top 50 Bank (2018–2021)

Jim Ryan's ascension to Chairman and CEO on May 2, 2019, was the opposite of a disruptive transition. Ryan had joined Old National in 2005, the year after Jones arrived, and had risen through a series of roles that gave him unmatched institutional knowledge: Treasurer, Director of Corporate Development and Mortgage Banking, Integration Executive, and ultimately Chief Financial Officer from 2016 to 2019. Before Old National, he had held senior finance positions at Wells Fargo Home Mortgage and Old Kent Financial Corporation. A graduate of Grand Valley State University in Michigan, Ryan was a Midwest banker through and through—the kind of leader who understood both the financial engineering of M&A and the human dynamics of integrating community banks.

The continuity was deliberate. Jones had spent his final years grooming Ryan, ensuring that the strategic direction would survive the leadership transition. But Ryan brought his own evolution to the playbook. Where Jones had built the acquisition machine through disciplined tuck-ins and adjacent-market deals, Ryan would shift to transformational transactions that could vault Old National into an entirely different competitive tier.

The Klein Financial acquisition, which closed in November 2018 just before Ryan took the helm, had already signaled the strategic shift. Old National was no longer just filling in its Indiana-Kentucky-Illinois-Michigan-Wisconsin footprint. It was targeting major metropolitan markets—Minneapolis-Saint Paul—where the growth dynamics were fundamentally different from small-town Midwest banking. The rationale was clear: while Old National's traditional markets provided stable, low-cost deposits and loyal commercial relationships, they also faced demographic headwinds. Population growth, business formation, and wealth creation were increasingly concentrated in larger metro areas. To build long-term franchise value, Old National needed urban density to complement rural stability.

Ryan also accelerated technology investment. The banking industry was undergoing a digital transformation that threatened to leave smaller institutions behind. Core systems modernization, digital banking platforms, mobile capabilities, and data analytics were no longer optional—they were table stakes. Consider what a modern bank needs to compete: a mobile app that rivals the consumer experience offered by neobanks like Chime or SoFi; real-time fraud detection systems; automated lending platforms that can approve commercial loans in days rather than weeks; sophisticated treasury management tools that help businesses optimize their cash flows. None of this is cheap, and none of it has a good return on investment for a bank with $10 billion in assets. But for a bank with $50 billion or $70 billion? The math changes entirely.

Old National deepened its partnership with Infosys, beginning a collaboration in 2020 that used a "self-funding model" where efficiency gains from technology investments paid for the next wave of improvements. The partnership focused on operations transformation through process digitization, automation, and eventually generative AI deployment.

Then COVID-19 hit. The pandemic, which shut down the American economy in March 2020, was an unexpected stress test for regional banks. Old National's response revealed the enduring value of relationship banking. The bank became a critical conduit for Paycheck Protection Program loans, processing applications from small businesses across its footprint that turned to their local banker in a moment of crisis. National banks and fintech lenders struggled with the volume and complexity of PPP. Community and regional banks, with their existing relationships and local knowledge, often processed loans faster and more effectively.

By the end of 2020, Old National stood at approximately $25 billion in assets—a respectable regional bank, but still subscale by the standards of an industry where the largest competitors measured assets in the trillions and even the biggest regionals exceeded $200 billion. The math was straightforward: fixed costs for technology, compliance, risk management, and regulatory infrastructure were rising inexorably, and they favored scale. A $25 billion bank faced essentially the same compliance burden as a $50 billion bank but had half the asset base over which to spread those costs. Ryan and his board concluded that the next phase required not tuck-ins but mega-mergers—deals that would fundamentally change Old National's competitive position.

The Mega-Merger Era: First Midwest and Beyond (2021–2025)

The story of Old National's mega-merger era begins with a simple but profound observation that Jim Ryan made as he surveyed the post-COVID banking landscape: at $25 billion in assets, Old National was big enough to carry the full regulatory burden of a major regional bank but not big enough to generate the returns that justified that burden. The math demanded a step-change in scale.

On June 1, 2021, Old National and First Midwest Bancorp jointly announced what they called a "merger of equals"—a phrase that carries enormous significance in banking. True mergers of equals are notoriously difficult to execute. They require egos to be sublimated, governance to be shared, and cultural integration to proceed without a clear victor. Most mergers described as "equals" are anything but. Yet the Old National-First Midwest combination was structured with unusual care.

First Midwest was a Chicago-market-centric bank with strong commercial lending capabilities and approximately $22 billion in assets. The all-stock transaction created a combined institution with approximately $46 billion in assets and $34 billion in assets under management. First Midwest shareholders received 1.1336 shares of Old National for each First Midwest share, giving them collectively about 44% of the combined company. The deal was valued at approximately $6.5 billion in total market capitalization, with the equity consideration for First Midwest shareholders aggregating roughly $2.5 billion.

The strategic logic was compelling. Old National gained a dominant presence in the Chicago metropolitan area—the largest banking market in the Midwest—along with First Midwest's deep commercial banking expertise. The combined institution became the sixth-largest commercial bank headquartered in the Midwest by asset size.

Management identified $109 million in cost savings, representing 11% of the combined noninterest expense base, with 75% targeted for realization in 2022. Projected earnings accretion of 22% for 2022 made the financial case clear.

But the merger faced complications. First Midwest had been subject to redlining allegations—accusations that it had systematically avoided lending in minority communities. Regulators addressed these concerns by requiring enhanced community reinvestment commitments as a condition of approval. The merger received final regulatory clearance on January 27, 2022, and closed on February 16, 2022. The combined bank established dual headquarters in Evansville and Chicago, with Ryan continuing as CEO and First Midwest's Michael Scudder serving as Executive Chairman.

Systems conversion—often the graveyard of bank mergers—was completed in July 2022, roughly five months after closing. This pace reflected Old National's integration playbook, refined through decades of acquisitions. The conversion unified technology platforms, consolidated overlapping operations, and merged customer accounts without the prolonged disruptions that have plagued other large bank combinations. To appreciate the difficulty of this, consider what a systems conversion actually involves: every customer account, every credit card, every automatic payment, every online banking login, every treasury management connection must migrate from one technology platform to another—simultaneously, without errors, over a single weekend. A botched conversion can leave customers unable to access their money for days, destroying trust that took decades to build. Old National's ability to execute this repeatedly, at scale, and on schedule is one of its most underappreciated competitive advantages.

The synergies materialized: cost saves hit targets, and the combined institution's efficiency ratio began improving as redundant systems and branches were rationalized.

With First Midwest digested, Ryan turned south. On October 26, 2023, Old National announced the acquisition of CapStar Financial Holdings, a Nashville-based bank with approximately $3.1 billion in assets. The all-stock transaction valued CapStar at approximately $344 million. CapStar brought 23 banking centers including seven in Greater Nashville, plus locations in Chattanooga, Knoxville, and Asheville, North Carolina.

The Nashville deal represented a strategic inflection. Old National had always been a Midwest story—Indiana, Illinois, Michigan, Wisconsin, Minnesota, Kentucky. CapStar marked its first entry into the Southeast—specifically into Nashville, one of the fastest-growing metropolitan areas in the United States. Nashville had added roughly 100 people per day during the 2010s, attracting corporate relocations from companies like AllianceBernstein, Amazon Operations, and Oracle. Population growth, business relocation, and wealth creation in the Sunbelt were reshaping the geographic logic of American banking. Old National had actually laid groundwork before the CapStar deal, recruiting a wealth management team in Nashville in 2022 followed by a commercial banking team. CapStar provided the branch infrastructure, retail deposit base, and local scale to complement those earlier investments. The deal closed on April 1, 2024, pushing Old National's total assets to approximately $52 billion.

Then came the boldest move yet. On November 25, 2024, Old National announced the acquisition of Bremer Financial Corporation, a $16.2 billion institution headquartered in St. Paul, Minnesota. The deal was valued at approximately $1.4 billion, structured as a combination of cash and stock—each Bremer share converting to 4.182 shares of Old National common stock plus $26.22 in cash.

Bremer was a complex target for a reason that went beyond banking: its unique ownership structure. The Otto Bremer Trust owned 92% of the bank's economic interest but controlled only 20% of the voting shares. Bremer employees held 80% of voting power but just 8% of the equity. This created significant internal tension between trust leadership, which favored a sale, and employee-shareholders who had substantial governance influence. The employee shareholders ultimately approved the merger at a special meeting on March 7, 2025.

Bremer was also significantly larger than CapStar—with $16.2 billion in assets, it was the kind of institution that would move the needle even on Old National's now-substantial balance sheet. More than 50 banking centers across Minnesota and Wisconsin, plus 13 cities in North Dakota, gave Old National density in markets where the Klein Financial deal had established a beachhead seven years earlier. On a pro forma basis, Old National would become the third-largest bank in the Twin Cities—a market that ranks among the most affluent and commercially active metropolitan areas in the Midwest.

The regulatory process was methodical: Federal Reserve Bank of St. Louis approved the holding company transaction on March 5, 2025; the OCC approved the bank merger on March 19, 2025. The deal closed on May 1, 2025, and Old National's total assets vaulted past $70 billion. The Otto Bremer Trust received approximately 11% ownership of Old National, with a trustee joining the board.

Systems conversion for Bremer was completed on October 20, 2025—again, roughly five months post-close, matching the First Midwest integration timeline. Bremer's wealth clients were onboarded to Old National Wealth, retirement plans transitioned to 1834 Investment Advisors, and Raymond James brokerage accounts converted by mid-November. By Q4 2025, Old National had realized 28% of targeted expense saves from Bremer, with full run-rate savings of over $115 million annually expected to hit in Q1 2026.

The post-2021 thesis was now clear. Through three transformational deals in four years, Old National had built a "super-regional" footprint stretching from North Dakota to North Carolina, anchored in the Midwest's largest metropolitan markets: Chicago, Minneapolis-Saint Paul, Indianapolis, and Nashville. The combined institution managed $37 billion in assets under management and operated as the fifth-largest commercial bank headquartered in the Midwest. Capital allocation discipline remained visible through it all—Old National balanced M&A spending with dividends and buybacks, increasing its share repurchase authorization from $200 million to $400 million alongside the Bremer integration.

The timing was also strategic. The 2023 regional banking crisis, which destroyed Silicon Valley Bank, Signature Bank, and First Republic, created both opportunities and urgency. Smaller banks facing depositor anxiety and regulatory scrutiny became more willing sellers. Larger banks distracted by their own crisis responses were less aggressive bidders. Old National, with its conservative balance sheet and proven integration capabilities, found a receptive market for deals.

The Regional Banking Crisis and Old National's Response (2023)

On March 10, 2023, Silicon Valley Bank collapsed—the third-largest bank failure in American history. Forty-two billion dollars in deposits fled in a single day, triggered by an uninsured depositor panic amplified through social media at a speed regulators had never anticipated. SVB's failure stemmed from a textbook asset-liability mismatch: pandemic-era deposit surges had been invested in long-duration bonds that cratered in value as the Federal Reserve hiked rates by 500 basis points. The FDIC, Fed, and Treasury backstopped all depositors on March 12. Signature Bank and First Republic Bank failed in quick succession.

The contagion sent regional bank stocks broadly lower, regardless of individual institution quality. Moody's placed six regional banks on review for downgrade. Bank of America alone absorbed over $15 billion in deposit inflows from the flight to safety. The KBW Regional Banking Index fell roughly 30% in a matter of days. For a bank like Old National, which shared the "regional bank" label with the failed institutions but virtually none of their risk characteristics, the crisis was a test of messaging and fundamentals simultaneously.

The distinction between Old National and the failed banks was not subtle—it was fundamental. To understand why, consider what actually killed SVB. Silicon Valley Bank had grown explosively during the pandemic, absorbing massive deposits from venture-backed startups and tech companies. These were large, uninsured deposits—often exceeding the $250,000 FDIC insurance limit by orders of magnitude—concentrated in a single industry. When SVB invested those deposits in long-duration Treasury bonds and mortgage-backed securities, it created a classic duration mismatch. As the Fed raised rates aggressively in 2022-2023, the market value of those bonds plummeted. When depositors—informed and connected through social media and group chats—realized the bank's bond portfolio was underwater, they withdrew $42 billion in a single day. It was a bank run at digital speed.

Old National weathered the storm for reasons rooted in its 189-year history of conservative banking. The bank's core deposit base was overwhelmingly composed of relationship-oriented retail and commercial deposits spread across a broad, diverse Midwest customer base—the polar opposite of SVB's concentrated, uninsured, venture-capital-ecosystem funding. Non-interest-bearing deposits constituted approximately 24% of core deposits. Brokered deposits, the most flighty form of institutional funding, remained below peer levels at 5.8% of total deposits. The loan portfolio was diversified across commercial real estate, commercial and industrial, consumer, and residential categories—no single sector concentration that could unravel in a stress scenario.

Management's public response was calibrated: the crisis "highlighted Old National's time-tested approach to banking" and required no changes to the company's strategic plan. This was not corporate spin—it was accurate. Old National's business model was fundamentally different from the failed banks. Where SVB had been a venture capital ecosystem bank with massive uninsured deposit concentration, Old National was a relationship community bank with granular deposits from millions of individual and small business customers. Where Signature Bank had concentrated on cryptocurrency-linked deposits, Old National served farmers, manufacturers, and Main Street businesses across the heartland.

The crisis validated something that Old National had been building for nearly two centuries: a deposit franchise so deeply embedded in communities that depositors did not flee at the first sign of industry stress. In fact, Old National likely benefited from flight-to-quality inflows as smaller community banks saw deposits leave for larger, perceived-safer institutions. Rather than retreating into defensive mode, Old National used the post-crisis environment to announce the CapStar acquisition in October 2023—a statement of confidence that few regional banks were positioned to make in that moment.

For investors watching the regional banking landscape, the 2023 crisis drew a bright line between banks with concentrated, rate-sensitive business models and those with diversified, relationship-driven franchises. Old National fell firmly in the latter camp, and the subsequent recovery in its operations and stock price reflected that distinction.

The Old National Playbook: How They Do M&A Differently

After fifty-plus acquisitions spanning four decades, Old National has developed an M&A methodology that functions as genuine organizational capability—a form of process power that competitors acknowledge even if they struggle to replicate. Understanding this playbook is essential to evaluating whether the bank's growth story can continue.

The screening criteria start with adjacency. Old National targets banks in markets that are geographically contiguous to its existing footprint—or, in the case of newer moves like Nashville, where the bank has already established commercial relationships. Cultural fit is non-negotiable. CEO Jim Ryan has been explicit: "Culture is what drives it. Culture will outstrip strategy any time." This is not executive platitude. In community bank M&A, where the most valuable assets are relationships—between bankers and their clients, between the bank and its community—cultural misalignment destroys value faster than any spreadsheet can predict. Reasonable pricing completes the screening trinity: Old National has walked away from deals where valuations exceeded disciplined thresholds, even when the strategic fit was attractive.

The negotiation approach is seller-friendly by design. Old National publicly refers to its acquisitions as "partnerships" rather than acquisitions or takeovers. This framing is not merely linguistic—it shapes how deals are structured and how integration proceeds. Acquired bank leaders often stay engaged rather than heading for the exits. The speed and certainty of close matters enormously to sellers, and Old National's track record of regulatory approvals and clean executions gives it an edge over competitors who may offer slightly higher prices but carry execution risk.

Integration follows a structured playbook that has been refined through decades of repetition. Systems conversion typically occurs within five to six months of closing—First Midwest converted in July 2022 (five months post-close), Bremer converted in October 2025 (five and a half months post-close). This pace is aggressive by industry standards but reflects organizational muscle memory. The conversion unifies technology platforms, consolidates overlapping operations, and migrates customer accounts with a rigor that comes from having done it dozens of times before.

Cost synergies typically target 30-40% of the acquired bank's expense base, with the majority realized within the first year. These savings come from branch consolidation where geography overlaps, elimination of redundant corporate functions, technology platform consolidation, and vendor contract renegotiation leveraging increased scale. Revenue synergies—cross-selling wealth management, treasury services, and capital markets capabilities to acquired customer bases—are harder to quantify but increasingly real as Old National's product suite has expanded.

Crucially, Old National preserves by targeting banks in new or adjacent markets rather than directly overlapping ones. The First Midwest deal had limited geographic overlap because First Midwest was Chicago-centric while Old National was Indiana-Wisconsin-Minnesota-centric. The CapStar deal opened an entirely new geography. The Bremer deal deepened Minnesota rather than duplicating existing markets. This approach minimizes branch closures and employee layoffs—which in turn minimizes customer disruption and community backlash, both of which can destroy the deposit franchise value that made the acquisition attractive in the first place.

How does Old National compare to other noted serial acquirers? M&T Bank, widely regarded as one of the most disciplined acquirers in banking, has a similar culture-first approach but operates in the Mid-Atlantic and Northeast with minimal geographic overlap. First Citizens BancShares made its name through the FDIC-assisted acquisition of Silicon Valley Bank in 2023—a different type of deal entirely, opportunistic rather than strategic. Huntington Bancshares, which acquired TCF Financial in 2021 and announced the $7.4 billion Cadence Bank deal in 2025, operates at a larger scale and increasingly targets transformational mergers.

Old National's edge lies in consistency and cultural credibility. Where competitors may pursue large deals periodically, Old National has built acquisition as an ongoing organizational competency. The bank has stumbled—integration timelines have occasionally stretched, and the ethical scrutiny around the TARP warrant repurchase pricing showed that the "most ethical company" brand required constant maintenance. But the overall track record is strong enough that community banks across the Midwest actively seek out Old National as a potential partner when they decide to sell.

Business Model Deep Dive: How Regional Banks Make Money

To understand Old National's competitive position, it helps to understand the basic machinery of regional banking—which is simpler than Wall Street often makes it sound.

A bank is, at its core, a spread business. It gathers deposits from customers at one interest rate and lends that money to borrowers at a higher rate. The difference—the net interest margin, or NIM—is the primary revenue engine. For Old National, NIM stood at 3.65% in Q4 2025, meaning the bank earned 3.65 cents of net interest income for every dollar of earning assets. That figure had expanded steadily throughout 2025, from 3.27% in Q1 to 3.65% in Q4, reflecting both the favorable interest rate environment and the bank's asset-liability management discipline.

Understanding how a bank constructs its loan portfolio is essential to evaluating its risk profile—and where its next crisis might come from. Old National's $48.8 billion loan portfolio breaks down across several categories. Commercial real estate, both owner-occupied and non-owner-occupied, represents approximately 45% of total loans—roughly $22 billion. Commercial and industrial lending accounts for about 31%, or $15 billion. Residential real estate comprises 17%, and consumer loans round out the remainder at 7%. Within commercial real estate, the exposure is diversified: multifamily at 13%, warehouse and industrial at 5%, retail at 4%, office at 4%, and senior housing at 1%. The office exposure—the sector that has kept bank investors awake at night since the pandemic accelerated remote work—is relatively modest at 4% of the total portfolio.

Geographically, Minnesota now represents the largest lending market at 21% of the portfolio (boosted by Bremer), followed by Illinois at 17%, Indiana at 11%, Wisconsin at 9%, and Michigan at 6%. This diversification across states and economic bases provides resilience against localized downturns.

The deposit franchise is where Old National's competitive moat lives. Total deposits of $55.1 billion fund the loan portfolio at a loan-to-deposit ratio of approximately 89%—conservative enough to provide liquidity buffers but efficient enough to generate solid returns. The cost of total deposits fell to 1.80% in Q4 2025, down from 1.97% in Q3, reflecting the benefit of Fed rate cuts flowing through the deposit base. Non-interest-bearing deposits—the cheapest form of funding, essentially free money from customers who keep checking accounts for transactional purposes—constitute roughly 24% of the core deposit base.

Beyond net interest income, Old National generates fee revenue from several business lines. Wealth management, with approximately $37 billion in assets under management, generates roughly $40 million per quarter. Capital markets revenue hit a record in Q4 2025, reflecting growing capabilities in interest rate hedging and advisory services for commercial clients. Mortgage banking contributes approximately $10 million quarterly. Treasury management—helping businesses manage cash flows, payments, and liquidity—is a growing area that management has identified as a "longer-term opportunity."

The efficiency ratio—the percentage of revenue consumed by operating expenses—is the metric that bank analysts obsess over. A lower ratio means more revenue drops to the bottom line. Old National's adjusted efficiency ratio hit a record low of 46% in full-year 2025, with Q4 at 46.0%. Management is targeting a sustained sub-50% ratio for 2026. For context, the best-in-class large regional banks typically operate in the 50-55% range. Old National's sub-50% performance places it among the most efficient operators in the industry and reflects both the scale benefits of recent acquisitions and disciplined cost management.

Think of it this way: every dollar of revenue that does not come from net interest income is a dollar that does not depend on the spread between lending rates and deposit costs. In a world where interest rates can shift dramatically—as they did in 2022-2023 when the Fed hiked 500 basis points in eighteen months—fee income provides stability and diversification. Old National's growing investment in wealth management, capital markets, and treasury services is fundamentally about reducing the bank's dependence on the rate cycle. Management has guided for $485-505 million in noninterest income for 2026, which would represent meaningful growth over prior years and an increasing share of total revenue.

Credit quality—the flipside of lending profitability—is where the lessons of 2008 remain most visible. Old National maintains an allowance for credit losses equal to 1.24% of total loans, a reserve cushion against potential defaults. Nonperforming loans stood at 1.07% of total loans at year-end 2025. Management has guided for net charge-offs of 0.25-0.30% of average loans in 2026, a range that reflects moderate credit stress consistent with a normalizing economic cycle rather than acute crisis.

The technology dimension of regional banking economics deserves attention. In 2020, Old National deepened a strategic partnership with Infosys to modernize its operations using a "self-funding model"—efficiency gains from digitization paying for the next wave of technology investment. By October 2024, that partnership had expanded to encompass process automation, generative AI deployment, and transformation of key business areas including lending, compliance, and customer service. The commercial loan pipeline reaching a record $3.4 billion in Q1 2025 reflected, in part, AI-powered underwriting tools that accelerated approvals while maintaining credit discipline. For a bank that once ran on paper ledgers and drive-up teller windows, the evolution is striking—and it is only possible at the scale Old National has achieved through its acquisition strategy. A $10 billion bank simply cannot invest in AI and automation at the level a $72 billion bank can, which is itself one of the strongest arguments for continued consolidation.

Leadership and Culture: The Old National Way

The leadership evolution at Old National follows a pattern that is instructive for any organization navigating transformation. Bob Jones was the turnaround CEO—recruited from outside, tasked with repairing crisis damage and building a growth engine from the wreckage. Jim Ryan was the insider successor—steeped in institutional knowledge, trusted by the organization, positioned to accelerate what Jones had started without the friction of a cultural outsider.

Ryan's background as Integration Executive—the person who actually oversaw the nuts and bolts of merging acquired banks—gave him a uniquely operational perspective on Old National's core strategic capability. He understood, at a granular level, what made integrations succeed or fail: the technology conversion timelines, the employee communication cadence, the branch rationalization decisions, the customer retention tactics. When he became CEO, he brought that operational fluency to the strategic level, enabling the shift from tuck-in acquisitions to transformational mergers.

The July 2025 appointment of Timothy Burke as President and COO signaled the next chapter. Burke came from KeyBank, where he had served as EVP of the Central Region and Field Enablement for the Commercial Bank, bringing nearly thirty years of Midwest commercial banking experience. The hire was significant: it brought an external perspective to a leadership team that had been predominantly homegrown, while the Midwest commercial banking pedigree ensured cultural compatibility. Burke's appointment also freed Ryan to focus on strategy, investor relations, and the high-level relationships that drive M&A origination.

Ryan's broader profile reflects deep community engagement beyond banking. He serves as Chairman of the Evansville Regional Economic Partnership, Vice Chairman of the Evansville Regional Business Committee, and Secretary/Treasurer of the Southwest Indiana Regional Development Authority. In October 2025, he was elected Vice Chair of the American Bankers Association Board of Directors and chairs the ABA's American Bankers Council—recognition that Old National's transformation has earned its leader a voice in shaping the industry's future direction. This is not a CEO who runs the bank from a corner office; it is a CEO embedded in the civic and industry infrastructure that shapes regional banking.

The cultural philosophy can be summarized as "Midwestern values"—conservative, relationship-driven, long-term thinking. This is not just marketing language. It manifests in specific organizational behaviors: disciplined underwriting that prioritizes credit quality over loan growth, patient capital allocation that resists the temptation to chase quarterly earnings, and a genuine commitment to community engagement that goes beyond compliance obligations.

Maintaining culture through dozens of acquisitions is perhaps Old National's most impressive organizational achievement. Each acquired bank brings its own history, its own leadership personalities, its own way of doing things. The integration playbook addresses this directly: Old National preserves local leadership where possible, maintains community banking identities during transition periods, and avoids the heavy-handed corporate mandates that have destroyed value in other bank mergers. The "partnership" framing is not incidental—it reflects a genuine organizational belief that acquired banks have something valuable to contribute, not just assets to absorb.

The board's role in this culture has been critical. Oversight of M&A strategy requires directors who understand both the financial engineering of deal-making and the human dynamics of integration. The addition of a Bremer Trust trustee to the board following the 2025 acquisition illustrates how Old National incorporates acquired institution perspectives into governance.

For investors, culture is notoriously difficult to evaluate from the outside. But in banking—where the most valuable assets walk out the door every night—culture is not a soft factor. It is the mechanism through which deposit relationships are maintained, loan officers are retained, and communities continue to trust their bank through ownership transitions. Old National's ability to preserve its cultural identity through a period of radical growth is a form of competitive advantage that does not appear on the balance sheet but shows up in every metric that matters.

Porter's Five Forces and Hamilton's Seven Powers Analysis

Understanding Old National's strategic position requires looking through two complementary lenses: the competitive forces shaping its industry and the sources of power that determine whether its advantages are durable.

Starting with the threat of new entrants: banking remains one of the most heavily regulated industries in America. Obtaining a bank charter requires navigating federal and state regulatory approval, meeting substantial capital requirements, and building the compliance infrastructure that post-Dodd-Frank regulation demands. The FDIC insures deposits, but that insurance comes with extensive oversight. The practical result is that new bank formation has slowed to a trickle—fewer than ten new bank charters have been approved annually in recent years, compared to hundreds per year before the financial crisis. Fintech companies have disrupted specific banking functions—payments, consumer lending, wealth management—but the core banking business of gathering insured deposits and making commercial loans remains firmly behind regulatory walls. For Old National, this barrier to entry protects its existing franchise.

Bargaining power of suppliers is limited. Banks' primary input is deposits, which are sourced from a broad, fragmented base of individual and commercial customers. Technology vendors, while important, operate in a competitive market—Old National's $72 billion scale gives it meaningful negotiating leverage on vendor contracts, a benefit that grows with each acquisition.

Bargaining power of buyers is moderate to high. Businesses and consumers have choices—other regional banks, national banks, credit unions, and increasingly fintech alternatives. Switching costs vary significantly by customer segment. A commercial client with a complex treasury management relationship, revolving credit lines, and years of established lending history faces high switching costs. A consumer with a checking account and a credit card faces low ones. Old National's strategy focuses on deepening commercial relationships to increase switching costs, while investing in digital capabilities to remain competitive for consumer deposits.

The threat of substitutes is moderate and growing. Fintech lenders have captured meaningful market share in consumer lending, particularly personal loans and point-of-sale financing. Non-bank lenders serve portions of the commercial real estate market. Credit unions, with their tax-exempt status, compete aggressively on deposit rates and consumer lending. Big tech companies like Apple and Google have entered payments and are experimenting with banking-adjacent services. But the substitution threat is concentrated in specific product categories rather than across the full banking relationship. No fintech has yet replicated the full-service commercial banking relationship that Old National offers its business clients.

Industry rivalry is intense—and this is the force that drives Old National's strategic imperative to grow. The Midwest banking market features aggressive competition from other regionals like Huntington, Fifth Third, KeyBank, and Regions, as well as national giants like JPMorgan Chase, Bank of America, and Wells Fargo. Credit unions have expanded aggressively. Net interest margin compression, rising regulatory costs, and technology investment requirements all favor scale—which means the industry is in a secular consolidation trend where banks must either grow or become acquisition targets themselves. The numbers tell the story: the FDIC counted roughly 14,000 banks in the United States in 1985. By 2025, that number had fallen below 4,200. The consolidation is not cyclical—it is structural, driven by the inexorable economics of scale in a heavily regulated, technology-intensive industry.

Turning to Hamilton Helmer's Seven Powers framework, Old National's position is more nuanced. Scale economies are moderate and growing. Fixed costs for technology, compliance, risk management, and regulatory infrastructure are spread over a larger asset base with each acquisition. Old National's adjusted efficiency ratio hitting 46%—among the lowest in regional banking—demonstrates that scale is translating into operating leverage. But regional banks cannot match the scale advantages of money-center banks with trillions in assets.

Network effects are limited but not absent. Banking is not a platform business in the traditional sense. But local network effects exist: business customers value banks that their suppliers, partners, and competitors also use, because shared banking relationships facilitate commerce. Treasury management and payment networks exhibit mild network effects that increase with market share density.

Counter-positioning is weak. Old National's relationship banking model is a genuine competitive position against national banks, but it is not counter-positioning in Helmer's strict sense—incumbents are not structurally prevented from copying the approach. Counter-positioning requires that matching the challenger's model would damage the incumbent's existing business. National banks choosing to ignore small-town Midwest markets is a strategic choice, not a structural inability.

Switching costs are moderate and represent one of Old National's key powers. In commercial banking, switching is genuinely painful. Treasury management integrations, credit line migrations, deposit account transitions, and the re-establishment of lending relationships create meaningful friction. Old National's strategy of deepening commercial relationships—adding wealth management, capital markets, and treasury services to basic lending—directly increases these switching costs. Consumer switching costs are lower but still meaningful when customers have mortgage, deposit, investment, and lending relationships at a single institution.

Brand power is moderate to strong regionally. The "Old National" name carries 186 years of trust in its home markets, and the community banking reputation matters for both deposit gathering and commercial relationship building. But brand does not travel well—it carries little weight outside the Midwest, which creates a natural geographic constraint on expansion.

Cornered resources are weak. In Helmer's framework, a cornered resource is something uniquely possessed by one company—a patent, a mine, a one-of-a-kind talent. Banking, almost by definition, does not produce cornered resources. The closest thing is Old National's deposit franchise in specific markets—once customers are banked, they tend to stay, and the local market knowledge and relationships built over decades are not easily replicated by a new entrant. Leadership and M&A expertise represent a form of human capital resource, but one that could theoretically be replicated by competitors with sufficient investment and patience.

Process power is moderate and improving—and this may be Old National's most distinctive power. The M&A integration capability, refined through fifty-plus transactions, is genuine process power in Helmer's framework: a set of organizational processes that have been honed through years of execution and that competitors cannot quickly replicate even if they understand what Old National does. The five-month systems conversion timeline, the structured synergy extraction, the employee communication and retention playbook—these are not strategies that can be copied from a PowerPoint deck. They are embedded in organizational routines, institutional knowledge, and muscle memory built through repetition. Competitors acknowledge it. Sellers seek it out. The underwriting discipline and credit culture that prevented a repeat of 2008's losses also qualify as process power. These processes are deeply embedded in organizational routines and difficult to replicate quickly.

The overall assessment: Old National's competitive powers are scale economies (growing with each deal), switching costs (strongest in commercial banking), and process power (M&A execution excellence). The moats are narrow by the standards of dominant technology companies, but they are real and reinforcing.

Each acquisition increases scale, which improves efficiency, which funds the next acquisition, which deepens market presence, which increases switching costs. It is a virtuous cycle—as long as the acquisitions are well-executed and reasonably priced. The strategic imperative is clear: keep growing scale through M&A to stay on the right side of the consolidation curve. The existential question, and one that investors must grapple with, is whether there is a terminal scale where Old National stops being the hunter and becomes the prey.

Bull vs. Bear Case

The bull case for Old National rests on a proven acquisition engine operating in an industry undergoing secular consolidation. The bank has executed three transformational deals in four years—First Midwest, CapStar, and Bremer—each one delivered on schedule with synergies materializing as projected. The deposit franchise, spanning eight states with 24% non-interest-bearing deposits and below-peer brokered funding, provides durable funding advantage. Credit quality has been managed conservatively since the 2008 lessons, and the allowance coverage at 1.24% of loans provides cushion against a normalizing credit cycle.

The financial trajectory supports the bull narrative. Full-year 2025 delivered record adjusted net income of $808.6 million, record adjusted EPS of $2.21, and a record-low 46% adjusted efficiency ratio. Management guided for 15% or greater earnings growth in 2026, targeting sub-50% efficiency, approximately 1.4% return on assets, and high-teens return on average tangible common equity. Tangible book value per share grew 15% year-over-year to $13.71, building intrinsic value for long-term holders. The CET1 ratio at 11.08% provides capital flexibility for organic growth, continued dividends, and the expanded $400 million share repurchase authorization.

The broader industry backdrop also favors Old National. Regional banking consolidation has hit a seven-year high in early 2026. Smaller banks face an impossible trinity: rising technology costs, increasing regulatory complexity, and competition from both larger banks and fintechs. Many will choose to sell, and Old National's reputation as a fair, culture-sensitive acquirer positions it as a preferred partner. The Basel III Endgame rules, as revised, largely exempt banks below $250 billion from the most punitive capital requirements—giving Old National room to grow without triggering severe regulatory constraints.

The interest rate environment adds another dimension to the bull case. Old National has positioned its balance sheet as moderately asset-sensitive, meaning it benefits when rates remain elevated. The NIM expansion from 3.27% in Q1 2025 to 3.65% in Q4 2025 demonstrates this positioning in action. As the Fed proceeded with measured rate cuts through 2025, Old National's deposit costs fell faster than its loan yields—a phenomenon that reflects the quality and stickiness of its core deposit franchise. In contrast, banks with heavy reliance on wholesale or brokered funding saw less NIM benefit because those deposits reprice immediately to market rates.

Scale benefits are inflecting. At $72 billion in assets, Old National can invest meaningfully in technology, cybersecurity, and product capabilities that were beyond reach at $20 billion. The Infosys partnership, AI-powered lending tools, and growing capital markets and treasury management capabilities demonstrate that the bank is evolving from a pure relationship bank into a full-service commercial bank with digital fluency. The Nashville and Twin Cities presences provide exposure to growth markets that offset the demographic challenges of traditional Midwest footprint.

The bank also carries optionality as a potential acquisition target. If the consolidation wave produces even larger super-regionals seeking Midwest density, Old National's franchise—well-run, well-integrated, strong deposit base—would be highly attractive.

The bear case begins with the structural challenges facing all regional banks.

Net interest margin is inherently cyclical, and the favorable rate environment that pushed NIM to 3.65% could reverse if the Fed cuts aggressively or the yield curve flattens. High regulatory costs, technology investment requirements, and compliance burdens create a fixed-cost drag that even a sub-50% efficiency ratio cannot entirely escape.

Old National lacks fundamental differentiation. Banking is a commodity business at its core—money is fungible, and customers can obtain similar products from dozens of competitors. The relationship banking advantage, while real, erodes with each generation of digital-native customers who have never stepped inside a branch and care more about app quality than banker familiarity.

Integration risk is real despite the strong track record. Old National absorbed three major acquisitions in four years, adding roughly $45 billion in assets through M&A since 2022. Each integration involved technology conversions, employee retention campaigns, customer communication, and cultural blending.

The cumulative strain on management attention and organizational bandwidth should not be underestimated. History shows that serial acquirers occasionally suffer an integration misstep that damages earnings and reputation far more than any single deal might suggest.

The geographic concentration in the Midwest carries demographic risk. Population growth, business formation, and wealth accumulation in the United States are disproportionately flowing to the Sunbelt and coastal markets. The Midwest offers stability but limited organic growth. Old National's Nashville entry partially addresses this, but it remains a small presence in a market dominated by larger institutions.

Commercial real estate exposure at 45% of total loans deserves ongoing scrutiny. The post-COVID shift to remote and hybrid work has structurally impaired office real estate, and while Old National's office CRE exposure is limited to 4% of the portfolio, the broader CRE category—including retail, multifamily, and other segments—could face stress in an economic downturn. Old National's 2008 experience began with a commercial real estate bet that seemed prudent until it wasn't.

Regulatory uncertainty persists. While Basel III Endgame rules have been softened, the regulatory framework continues to evolve. Stress testing requirements, liquidity rules, and capital standards could change with political administrations. The $100 billion asset threshold, which triggers enhanced prudential standards, is one more acquisition away for Old National at $72 billion—a crossing that would impose meaningful new compliance costs.

The existential bear question: Is Old National stuck in the "too small to matter, too big to be nimble" middle ground? At $72 billion, it is a fraction of the size of money-center banks and substantially smaller than the largest super-regionals. Yet it is too large to maintain the pure community banking intimacy that once defined its competitive advantage. The M&A pipeline may eventually thin—there are a finite number of attractive Midwest community banks left to acquire, and each deal makes the next one harder to move the needle on a larger balance sheet.

The ultimate bear scenario: Old National fails to achieve independent scale sufficient to sustain competitive technology investment, fee income diversification, and talent retention. In that world, it becomes the acquired rather than the acquirer—absorbed by a Huntington, a Fifth Third, or a national bank seeking Midwest density.

There is also a myth worth examining: the notion that Old National's community banking heritage makes it uniquely insulated from competitive pressure. The reality is more complicated. Community banking identity works well for deposit gathering and small business relationships, but it creates tension with the corporate efficiency demands of a $72 billion institution. Every acquired bank's employees were told their community identity would be preserved—and largely it has been—but the centralization of treasury, risk management, technology, and compliance functions inevitably changes the character of what was once a local institution. The question is not whether this tension exists but whether Old National manages it better than peers. The evidence suggests it does, but not perfectly.

The three KPIs that matter most for tracking Old National's ongoing performance are: the adjusted efficiency ratio, which measures whether scale is translating into operating leverage (target: sustaining below 50%); net interest margin, which captures the durability of the deposit funding advantage and asset-liability management discipline; and tangible book value per share growth, which reflects long-term value creation inclusive of M&A dilution, retained earnings, and capital management. These three metrics, taken together, tell investors whether the acquisition strategy is creating or destroying value.

The Future: What is Next for Old National

Management's near-term message is clear: digest Bremer, extract the full $115 million in annual cost saves, and demonstrate that $72 billion in assets can generate the efficiency, profitability, and return metrics that justify the growth. The 2026 guidance—net interest income of approximately $2.415 billion, noninterest income of $485-505 million, expenses of $1,435-1,455 million, and loan growth of 4-6%—outlines a year of integration harvest rather than further M&A.

Ryan has explicitly stated that future acquisitions face "a high hurdle" given the organic growth opportunities embedded in the current franchise. This is the right message after absorbing $45 billion in acquired assets over four years. Markets, regulators, and employees all need to see that Old National can run the enlarged institution effectively before the next deal.

But the longer-term question remains: What is Old National's endgame? Three scenarios frame the discussion.

In the first scenario, Old National continues acquiring toward $100 billion or more in assets, achieving genuine super-regional status. This path involves two or three more significant acquisitions over the next five to seven years, likely in the Upper Midwest or Sunbelt markets where the bank has emerging presence. At $100 billion-plus, Old National would rival Huntington, Regions, and M&T in scale, with the operating leverage and product breadth to compete as a top-tier commercial bank. The risk: crossing the $100 billion threshold triggers enhanced prudential standards that significantly increase regulatory costs, and each incremental acquisition beyond current scale becomes harder to generate acceptable returns.

In the second scenario, Old National becomes an attractive acquisition target for a mega-regional or national bank. The bank's franchise—well-integrated, strong deposit base, diversified Midwest footprint—would be highly valuable to a larger institution seeking density in the heartland. The Otto Bremer Trust, now holding roughly 11% of Old National, represents a significant but not controlling shareholder whose eventual disposition of shares could facilitate such a transaction.

In the third scenario, Old National pivots toward deepening its existing franchise rather than expanding it. This would involve investing heavily in digital capabilities, wealth management, capital markets, and treasury services to increase revenue per customer and switching costs. Organic growth in Nashville, Minneapolis, and Chicago—already high-growth markets within the portfolio—could drive expansion without acquisition risk.

The most likely path probably blends elements of all three: selective acquisitions that deepen existing markets or add Sunbelt exposure, combined with organic investment in fee-generating businesses and digital capabilities, with the implicit understanding that if a sufficiently attractive acquisition offer arrives, Old National's board would consider it.

The digital transformation question deserves particular attention. Old National's expanded Infosys partnership, announced in October 2024, represents a commitment to AI-driven operations, lending automation, and customer experience modernization. The bank has acknowledged the competitive threat from neobanks and fintech platforms and identified trends like agentic AI and Banking-as-a-Service platforms as key forces to monitor in 2026 and beyond. The generational wealth transfer—estimated at trillions of dollars moving from baby boomers to millennials and Gen Z over the coming decades—presents both opportunity and risk. Younger customers who have never stepped inside a bank branch will not choose Old National because of its 186-year history. They will choose it because of its app, its digital experience, and its integration with the financial tools they already use. Whether Old National can compete on that dimension against tech-native competitors with unlimited engineering budgets is an open question that will shape the next decade.

The commercial banking evolution also bears watching. Treasury management, which helps businesses manage cash flows, payments, and working capital, is a high-switching-cost product where Old National's growing scale provides genuine advantage. Specialized lending—healthcare, agriculture, municipal finance—offers opportunities to deepen expertise in verticals where relationship knowledge creates pricing power. Capital markets capabilities, which hit record revenue in Q4 2025, are expanding from simple interest rate hedging into more sophisticated advisory services for middle-market commercial clients.

The ESG and community impact dimension is worth noting. Old National's Community Reinvestment Act performance—historically strong and enhanced through merger commitments—provides a competitive advantage that is often overlooked. In an era when regulators scrutinize CRA compliance as a condition of merger approval, Old National's track record of genuine community engagement becomes a strategic asset. The bank has made specific community investment commitments as part of each major merger, building relationships with community organizations that facilitate future regulatory approvals.

What would Old National look like in 2030? At current growth rates—mid-single-digit organic loan growth supplemented by periodic acquisitions—total assets could reach $90-100 billion. The wealth management platform, already at $37 billion in AUM, could approach $50 billion. Fee income as a percentage of revenue would likely increase as treasury management, capital markets, and advisory services mature. The efficiency ratio, already best-in-class, could approach the low 40s. And the bank that started as a frontier institution in Evansville, Indiana, would operate as one of the twenty largest banking companies in America.

Lessons for Founders, Investors, and Operators

Old National's 186-year journey offers several lessons that extend well beyond banking.

The power of patient capital is the most obvious. Old National did not become a $72 billion institution through a single stroke of genius or a lucky break. It got there through decades of methodical, disciplined execution—making small acquisitions in the 1990s, building integration capabilities through repetition, surviving the 2008 crisis, and then accelerating when the competitive environment rewarded scale.

This is not a venture capital story of exponential growth. It is a story of compounding advantages over time—each acquisition making the next one slightly easier, each integration refining the playbook, each market entry deepening the franchise.

M&A as a core competency is rare and valuable. Most companies treat acquisitions as occasional events—high-stakes, high-anxiety episodes that disrupt normal operations. Old National treats them as an ongoing organizational function, with dedicated teams, refined processes, and institutional memory that spans decades. The Integration Executive role—held by Jim Ryan before he became CEO—is itself a sign of how seriously Old National takes this capability. Building it required sustained investment in people, systems, and relationships with potential sellers—investment that generates no immediate return. The payoff comes only when the capability is deployed repeatedly over time, and when the cumulative learning from fifty-plus transactions creates an organizational muscle that no new entrant can quickly replicate.

Culture is not a soft factor in consolidation industries—it is the primary determinant of integration success. The horror stories of failed bank mergers—destroyed deposit franchises, fleeing loan officers, demoralized staff, alienated communities—almost always trace back to cultural misalignment.

Old National's insistence on cultural fit as a non-negotiable screening criterion has not made every deal perfect, but it has prevented the catastrophic failures that have destroyed value at other serial acquirers.