The onsemi Metamorphosis: How a Sleepy Commodity Player Became the Sovereign of Power & Sensing

I. Introduction & Episode Roadmap

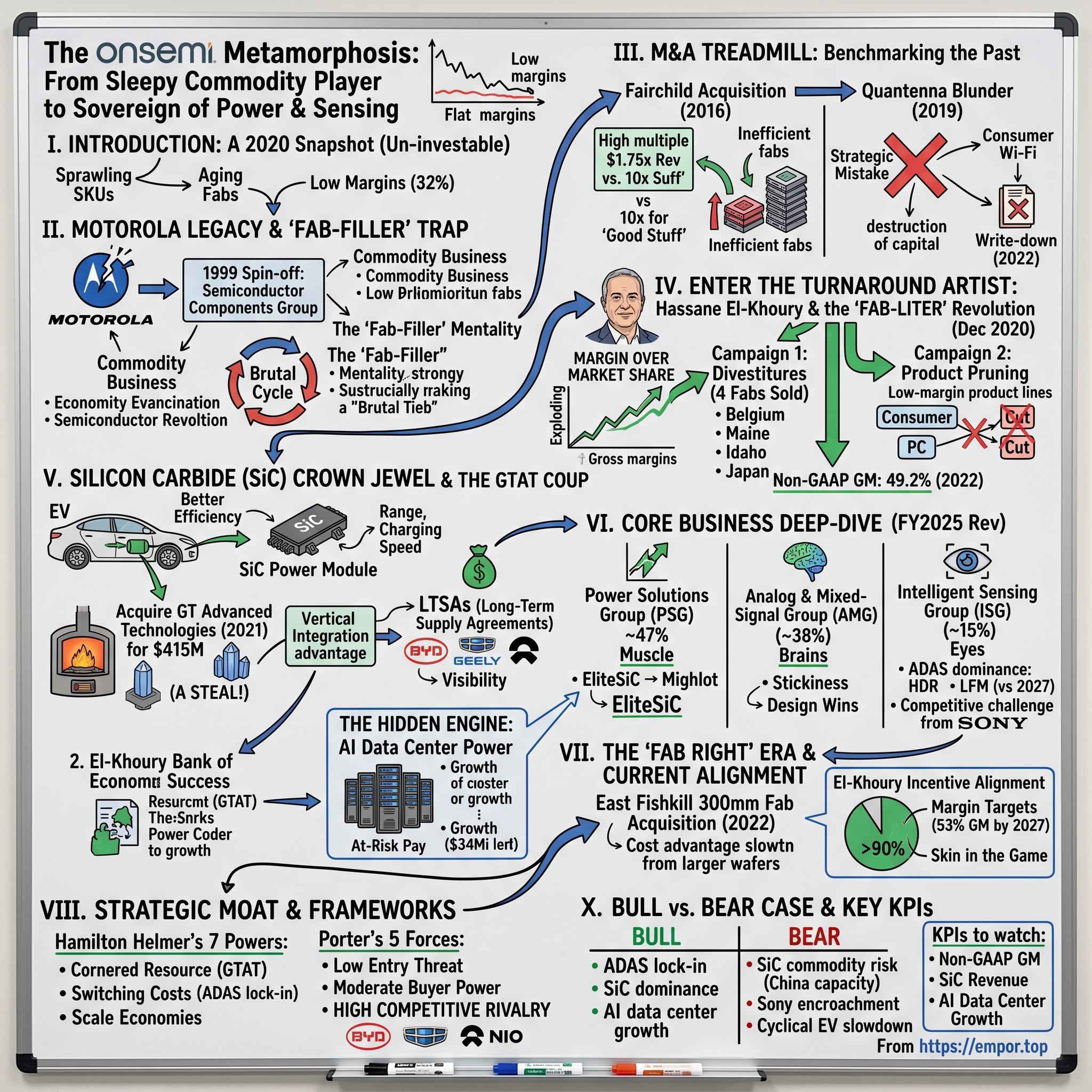

Picture a semiconductor company in 2020. Its stock had gone essentially nowhere for the better part of a decade. Its gross margins hovered in the low thirties — the kind of number that, in chip-industry terms, screams "I sell undifferentiated parts and pray the cycle is kind to me." It carried roughly 80,000 distinct product SKUs, a catalog so sprawling that even its own salesforce struggled to describe what the company actually did. It owned a patchwork of small, aging factories scattered across Belgium, Maine, Idaho, and Japan, many of them running technology nodes that were obsolete before the iPhone existed. Wall Street had a word for this kind of company: un-investable.

That company was ON Semiconductor — a 1999 spin-off from Motorola's least glamorous division, the part of Motorola nobody wanted. For two decades it had played the role of the industry's discount bin, churning out diodes, transistors, and simple power chips by the billions, competing almost entirely on price, and surviving by keeping its factories stuffed with whatever low-margin silicon it could find to run through them.

Now fast-forward to today, June of 2026. The company has rebranded itself — lowercase, deliberately — as "onsemi." It describes itself not as a chipmaker but as a leader in "intelligent power and sensing." Its non-GAAP gross margins peaked near 49% in 2022,1 a number that would have been literally unimaginable to the management team running the place five years earlier. It owns the single hardest-to-replicate asset in the entire silicon carbide supply chain. It controls more than 70% of the image sensors that let cars see the road.[^2] And it has signed multi-billion-dollar, multi-year supply agreements with the biggest electric-vehicle makers on the planet.

How does that happen? How does a company go from being Motorola's trash bin to being the indispensable heart of electrification, autonomy, and — in a plot twist nobody saw coming — the AI data center buildout?

That is the story of this episode. And it is, at its core, a story about one of the most underappreciated corporate turnarounds in modern semiconductor history — a turnaround built not on inventing some magical new technology, but on the far less glamorous, far more difficult art of saying no. Saying no to revenue. Saying no to volume. Saying no to the comfortable, deeply ingrained habit of filling factories at any cost.

Here is where we are going over the next several hours. First, the Motorola legacy and the structural trap — what we'll call the "fab-filler" mentality — that doomed the company to mediocrity for twenty years. Second, the M&A treadmill: the Fairchild acquisition and the Quantenna blunder, two deals that tell you everything about the old onsemi's strategic confusion. Third, the arrival of the turnaround artist, Hassane El-Khoury, and his "fab-liter" revolution. Fourth, the silicon carbide story and the GT Advanced Technologies acquisition — one of the great capital-allocation masterclasses of the decade. Fifth, a deep dive into the three operating segments, the competitive structure of each, and the hidden AI power business. Sixth, the "fab right" era and how management's pay is wired to shareholders. Seventh, the strategic moat, run through Hamilton Helmer's 7 Powers and Porter's 5 Forces. And finally, the bull case, the bear case, the KPIs that actually matter, and the broader playbook lessons.

Let's begin where every good origin story begins: with the parent company that didn't want this business.

II. The Motorola Legacy & The "Fab-Filler" Trap (1999–2010s)

In 1999, Motorola was a giant wrestling with its own identity. It wanted to be the company of the future — of cellular handsets, of high-performance microprocessors, of the digital revolution. And the future, as Motorola's leadership saw it, did not include the grubby, low-margin business of making discrete semiconductors: the humble diodes and transistors and standard analog parts that had been the bread and butter of its Semiconductor Components Group for generations. These were the oldest products in the building, the lowest-margin lines, the ones that competed on pennies. So Motorola did what large companies do with divisions they've fallen out of love with: it carved them out.

ON Semiconductor was born from that carve-out, taking the discrete, standard analog, and standard logic operations and setting them loose as a standalone company. Think about the psychology of that founding moment for a second. You are not being spun out because you are a crown jewel with too much potential to stay inside. You are being spun out because you are the part the parent has decided is beneath its ambitions. That origin shaped the company's culture and strategy for the next two decades.

What did the new company actually sell? Commodities, in the truest sense of the word. A diode is a diode. A transistor is a transistor. A simple power-management chip from one vendor is, for most applications, interchangeable with the equivalent part from another. When your product is functionally indistinguishable from your competitor's, you have no pricing power. The customer's purchasing department holds all the cards, and every negotiation is a race to the bottom. This is the structural condition that defined old onsemi: enormous volume, razor-thin differentiation, and margins permanently pinned to the floor.

Now here is the part that turned a difficult business into a genuinely dangerous one — the "fab-filler" trap. To understand it, you need to understand the economics of a chip factory, a "fab." A fab is a fantastically expensive asset. It costs billions to build and a fortune to operate, and the overwhelming majority of those costs are fixed — they exist whether the factory is running flat-out or sitting idle. The depreciation, the clean-room maintenance, the skilled engineers, the utilities to keep a sterile environment humming: all of it has to be paid regardless of how many wafers you actually push through.

That fixed-cost reality creates an almost gravitational pull on management. If your factory costs the same to run whether it's at 60% capacity or 100% capacity, then every additional wafer you can cram through it looks "profitable" on a marginal basis — even if you're selling the resulting chips for barely more than the raw materials cost. So the logic becomes seductive and self-reinforcing: fill the fab. Take any order. Make any commodity part. Keep utilization high, because empty capacity is pure waste. Fabs, in this worldview, are not strategic assets to be deployed thoughtfully — they are mouths to be fed.

The problem is what happens when the music stops. The semiconductor industry is brutally, famously cyclical. Demand surges and collapses in waves driven by inventory cycles, end-market booms and busts, and macro shocks. And when the down-cycle arrives — as it always does — the chips you were happily stuffing into your fabs suddenly have no buyers. Utilization craters. And because your costs are fixed, every point of underutilization flows straight to the bottom line as a charge. The very strategy that looked so clever on the way up becomes a wrecking ball on the way down.

This is why old onsemi was un-investable. Its gross margins sat stubbornly in the 30-to-32% range, the structural signature of a commodity player. Its earnings whipsawed violently with the cycle. And it had no durable source of differentiation to escape the trap — no proprietary technology, no irreplaceable position, nothing that would let it command a premium price or protect it when demand softened. It was, in the language of the industry, a price-taker. The market told it what its products were worth, and the answer was always: not much.

For twenty years, the answer to this predicament was the same answer most struggling commodity companies reach for. If you can't get more profitable, get bigger. Buy scale. Roll up competitors. And so onsemi climbed onto the M&A treadmill — which is where our story turns next.

III. The M&A Treadmill: Benchmarking the Past

There is a particular kind of corporate strategy that emerges when a company is stuck in a commodity trap and can't see a way out. It goes like this: if our margins are bad because we're sub-scale, then the solution is more scale. Buy a competitor, take out duplicate costs, become the number one or number two player, and surely the improved market position will translate into pricing power and better economics. It is a tempting logic. It is also, as onsemi discovered, frequently a trap of its own — because adding horizontal scale to a commodity business often just makes you a bigger commodity business.

The defining deal of this era was the acquisition of Fairchild Semiconductor in 2016.

Now, Fairchild is not just any company. To anyone who knows Silicon Valley history, the name is sacred. Fairchild Semiconductor was the original — the company founded by the "traitorous eight" who left William Shockley in 1957, the birthplace of the commercial integrated circuit, the corporate ancestor from which Intel, AMD, and an entire genealogy of Valley royalty descended. Fairchild is the reason it's called Silicon Valley. So when onsemi acquired it for $2.4 billion in cash in 2016,2 there was a certain poetry to it — the commodity spin-off acquiring the legendary grandfather of the entire industry.

But strip away the romance and look at the numbers, and you see what kind of deal this really was. onsemi paid roughly 1.75 times revenue for Fairchild, which was generating about $1.37 billion in annual sales. To understand whether that's expensive or cheap, you have to benchmark it against what other power and analog deals were fetching in that same era — and the contrast is stark. Around the same time, Analog Devices acquired Linear Technology for a breathtaking multiple north of 10 times revenue. Microchip bought Micrel at roughly 3.3 times. Against those comparables, onsemi bought Fairchild on the cheap, at a fraction of what differentiated analog assets were commanding.

And that tells you something important. You don't buy a company for 1.75x revenue when the market is paying 10x for the good stuff. The low price was the market's verdict on Fairchild's quality. Fairchild was a neglected, operationally bloated asset — a once-great name that had been starved of investment, saddled with its own collection of sub-scale, aging fabs. Yes, the acquisition vaulted onsemi to the number-two position in global power discretes, exactly the scale prize that management was chasing. But it did so by bolting another set of inefficient factories and another mountain of operational debt onto a company that already had too much of both. The deal made onsemi bigger. It did not make onsemi better. Corporate gross margins stayed mired in the low thirties, and the fundamental disease — commodity products run through sub-scale fabs — was now simply larger in scale.

If Fairchild was a flawed deal executed with sound logic, the next acquisition was a strategic mistake almost from conception. In 2019, onsemi acquired Quantenna Communications for $1.07 billion in cash.3 Quantenna made Wi-Fi chips — specifically, high-end connectivity silicon for consumer routers and access points. The thesis, presumably, was that onsemi could bolt "connectivity" onto its portfolio and ride the wave of an increasingly connected world.

The problem was that consumer Wi-Fi had almost nothing to do with onsemi's actual strengths or its most attractive markets. The company's center of gravity was automotive and industrial — long product lifecycles, demanding reliability requirements, sticky customer relationships. Consumer Wi-Fi was the opposite: brutally competitive, fast-moving, commoditizing rapidly, dominated by entrenched players with far greater scale in that specific niche. onsemi paid more than a billion dollars to enter a fight it was poorly positioned to win, in a market adjacent to nothing it did well. It was an expensive answer to a question nobody at the company's best customers was actually asking.

The clean-up came later, and it came under new management. In 2022, onsemi formally recognized the destruction of capital, taking an impairment of roughly $387 million against the goodwill and intangibles tied to the Wi-Fi business and beginning to wind down the legacy consumer connectivity operations.4 We'll return to that decision, because the willingness to take that write-down — to admit a predecessor's mistake and stop the bleeding rather than throw good money after bad — is itself a window into the philosophy of the person who, by then, had taken the wheel.

Because by the time that write-down hit the books, onsemi was no longer the same company. In December of 2020, the board had brought in an outsider — an engineer with a very particular reputation for doing the one thing onsemi had never been willing to do: subtract.

IV. Enter the Turnaround Artist: Hassane El-Khoury & the "Fab-Liter" Revolution

When a board hires a turnaround CEO, the choice itself is a confession. It is an admission that the existing playbook has failed and that incremental tinkering won't fix it. In December 2020, onsemi's board made exactly that confession when it appointed Hassane El-Khoury as chief executive officer.5

El-Khoury was not a typical big-company semiconductor CEO. A Lebanese-American engineer, he had spent his career at Cypress Semiconductor, rising from an embedded-systems engineer to become its CEO in 2016 at the remarkably young age of 38. At Cypress, he had earned a reputation as a disciplined operator and a clear-eyed strategist — someone who could look at a sprawling, unfocused portfolio and ruthlessly decide what mattered and what didn't. His tenure there culminated in the sale of Cypress to Germany's 英飞凌 Infineon Technologies for roughly $10 billion, a deal that closed in 2020 and validated his ability to build and crystallize shareholder value. He was, in other words, a man who had already proven he could take a muddled chip company and impose focus on it.

That was precisely the skill onsemi needed, because focus was the one thing it had never possessed.

The legend of the turnaround begins, as these things often do, with a diagnostic. In his first ninety days, El-Khoury did what any good operator does: he opened the hood and looked at what was actually inside. What he found was staggering even by the standards of a known problem company. onsemi was managing something on the order of 80,000 distinct product SKUs.6 Eighty thousand. To put that in human terms, that is not a product portfolio — it is a hoarder's basement. No engineering organization on Earth can meaningfully invest in, support, and differentiate eighty thousand products. The vast majority of them were low-margin commodity parts generating trivial revenue, each one consuming a sliver of factory capacity, support engineering, and management attention.

And those products were spread across a fragmented network of small, sub-scale fabs, many running ancient process technology — the accumulated geological strata of two decades of "fill the fab" acquisitions and additions. El-Khoury looked at this and made a decision that, to the old onsemi culture, must have sounded like heresy. He halted the fab-filler strategy. The new mandate, repeated until it became a mantra, was simple and brutal: margin over market share.

Let that sink in, because it inverts the entire logic of the prior twenty years. For two decades, the implicit goal had been to maximize volume to keep factories full, accepting whatever margin the market would bear. El-Khoury's order was the exact opposite: we will walk away from revenue — real, booked, today's revenue — if that revenue does not earn an acceptable margin. We would rather have a smaller, more profitable company than a larger, structurally unprofitable one.

This translated into two parallel campaigns. The first was the divestiture of factories — what came to be known internally as the "fab-liter" strategy. If sub-scale fabs were the source of the underutilization risk that destroyed profitability in every downturn, then the answer was to own fewer of them. Over 2021 and 2022, onsemi systematically sold off four sub-scale fabrication facilities. The Oudenaarde fab in Belgium went to BelGaN Group. The South Portland, Maine facility was sold to Diodes Incorporated. The Pocatello, Idaho fab went to LA Semiconductor. And the Niigata, Japan facility was transferred to JS Foundry K.K.7 Each sale did something subtle but powerful: it permanently removed a chunk of fixed-cost overhead from the company's structure, which is to say it removed a chunk of the downside risk that had made the old onsemi so terrifying to own through a cycle.

The second campaign was product pruning — methodically exiting low-margin consumer, PC, and white-goods commodity lines, the very products that had been clogging those fabs. This is harder than it sounds. Every one of those product lines had a customer, a salesperson defending it, and some revenue attached to it. Killing a product means killing revenue, and killing revenue is the thing most managers are constitutionally incapable of doing. El-Khoury did it anyway, narrowing the company's focus down to two great secular megatrends where differentiated power and sensing silicon could command real premiums: electrification — the global shift to electric vehicles — and autonomy — the rise of advanced driver-assistance and self-driving systems.

And then the numbers did something the old onsemi had never managed. Gross margins, which had spent two decades trapped around 32%, exploded upward. By 2022, the company posted a record non-GAAP gross margin of 49.2%.1 That is not an incremental improvement; that is a structural rewrite of the company's financial DNA. A seventeen-point gross-margin expansion is the difference between a barely-investable cyclical and a genuine quality compounder. It is the financial fingerprint of subtraction — of all the low-margin revenue walked away from, all the fixed costs shed, all the complexity pruned.

But margin expansion through subtraction can only take you so far. To become a great business rather than merely a healthier one, onsemi needed something to grow into — a differentiated, supply-constrained, high-value franchise where it could play offense. That franchise was silicon carbide, and securing it required one of the boldest capital-allocation moves the company ever made.

V. The Silicon Carbide (SiC) Crown Jewel & The GTAT Coup

To appreciate why onsemi's next move mattered, you first need to understand why silicon carbide is such a big deal — and to do that, let's set aside the jargon and talk about what's actually happening inside an electric car.

When you press the accelerator on an EV, electricity has to flow from the big battery pack to the electric motor. But it can't flow directly. The battery stores direct current, the motor wants alternating current, and the voltages and currents involved are enormous. Sitting between them is a device called an inverter, and inside that inverter are power switches that flip on and off thousands of times per second to shape the raw battery power into something the motor can use. Every time one of those switches operates, a little bit of energy is lost as heat. Multiply a tiny loss by thousands of switching cycles per second, across the whole life of the car, and those losses add up to real range, real battery weight, and real money.

For decades, those switches were made of ordinary silicon, in devices called IGBTs. Silicon carbide changes the physics. It is a compound of silicon and carbon, far harder and more thermally robust than silicon alone, and it can handle much higher voltages while wasting dramatically less energy as heat. Swap silicon IGBTs for silicon carbide power modules and you unlock a cascade of benefits: you can move to higher-voltage architectures — 800-volt and 900-volt systems instead of 400-volt — which means faster charging, lighter wiring, a smaller and lighter battery for the same range, and an extension of driving range on the order of 5% to 10%.8 In an industry where every mile of range and every kilogram of battery weight is fought over ferociously, that is an enormous prize. Silicon carbide is, quite literally, what lets a modern premium EV charge fast and go far.

There was just one catch, and it's the catch that makes this whole story interesting. Silicon carbide is monstrously difficult to manufacture. The hardest step is the very first one: growing the raw crystal. To make silicon carbide chips, you first have to grow a cylindrical crystal called a boule, in a furnace, at temperatures above 2,000 degrees Celsius, in a process that takes a very long time and produces a material so hard it's used as an industrial abrasive. Growing large, defect-free silicon carbide boules consistently is one of the genuine black arts of materials science. The crystal-growth step is the bottleneck of the entire supply chain — the place where scarcity lives, and therefore the place where value and pricing power concentrate.

Which brings us to GT Advanced Technologies, and one of the most colorful backstories in the industry.

GTAT is a company most people, if they remember it at all, remember for a spectacular failure. Back in 2014, GTAT had signed a massive deal with Apple to supply synthetic sapphire — the ultra-hard material Apple wanted for iPhone screens. The deal went catastrophically wrong, GTAT couldn't deliver at the scale and yield required, and the company filed for Chapter 11 bankruptcy in dramatic fashion, becoming a cautionary tale about betting your whole company on a single demanding customer. It was, by any measure, a humbling collapse.

But here is the thing about companies that have mastered hard materials science: the expertise doesn't evaporate just because the business model failed. GTAT reorganized, refocused, and turned its furnace and crystal-growth know-how toward a more promising material — silicon carbide. By the time onsemi came knocking, GTAT had built genuine, hard-won expertise in growing silicon carbide crystal boules, the exact bottleneck step that mattered most.

In 2021, onsemi acquired GT Advanced Technologies for $415 million in cash.9 And this is where the capital-allocation story becomes a masterclass.

Think about what onsemi actually bought. For under half a billion dollars, it acquired vertical integration into the single scarcest, most technically demanding link in the silicon carbide value chain. While competitors were buying their silicon carbide substrates on the open market — paying merchant suppliers for the raw wafers and accepting both the cost and the supply risk that came with it — onsemi now controlled its own crystal growth in-house. It owned the bottleneck.

Benchmark the price against what others paid for comparable ambitions and the brilliance sharpens. STMicroelectronics, the European power giant, had acquired a controlling stake in the silicon-carbide specialist Norstel AB for around $137.5 million — but Norstel was a far smaller, earlier-stage operation. Coherent, the materials company formerly known as II-VI, spent billions over the following years to build out its substrate footprint. Against that landscape, onsemi's $415 million purchase of an elite, high-volume-capable crystal manufacturing operation — anchored by a major facility in Hudson, New Hampshire — looks like a steal. They acquired the crown jewel of the supply chain for the price of a rounding error on what rivals were spending.

What did onsemi do with this advantage? It built a brand and a business model around it. The company launched its EliteSiC family of silicon carbide products and used its vertical integration — owning everything from the crystal boule all the way through to proprietary chip packaging — to offer something its merchant-substrate-dependent competitors could not: supply security. In an industry where silicon carbide supply was the limiting constraint on every automaker's EV ambitions, the ability to guarantee supply was worth a fortune. onsemi converted that guarantee into a series of long-term supply agreements, or LTSAs — multi-year, multi-billion-dollar commitments in which customers locked in volume and pricing in exchange for assured supply. Among the marquee wins were agreements with leading Chinese EV champions, including 比亚迪 BYD, 吉利汽车 Geely, and 蔚来 NIO.10

These LTSAs are worth pausing on, because they are the financial expression of the entire strategy. A long-term supply agreement transforms the most terrifying feature of the semiconductor business — cyclical, unpredictable demand — into something closer to a subscription. Instead of hoping customers show up each quarter, onsemi now had contractual visibility into years of volume at agreed prices. The very thing that had made the old onsemi un-investable — demand volatility — was being engineered out of the new onsemi's most strategic franchise. Crystal growth was the cornered resource; the LTSAs were how onsemi cashed it in.

With the high-value growth engine secured, the question became one of execution and structure: what does this transformed company actually look like under the hood, segment by segment? That's where we turn next.

VI. Core Business Deep-Dive: Materiality, Segments & Competitive Structure

Let's open up the machine and see how the pieces fit together. As of fiscal 2025, onsemi generated roughly $5.99 billion in total revenue,11 and it organized itself into three operating segments of very different sizes and very different strategic characters.

The largest by far is the Power Solutions Group, or PSG, which brought in about $2.81 billion — roughly 47% of the company.11 Next is the Analog & Mixed-Signal Group, AMG, at about $2.26 billion, or 38%. And the smallest of the three, but in some ways the most dominant in its niche, is the Intelligent Sensing Group, ISG, at about $0.93 billion, or roughly 15%.11 Three segments, three stories. Let's take them in turn.

The Power Solutions Group — the beating heart. This is the high-voltage muscle of the company: the discrete power devices, the silicon IGBTs, the silicon carbide modules built on that EliteSiC franchise, and the emerging gallium nitride devices. If onsemi has a center of gravity, this is it — the segment that contains the silicon carbide crown jewel and that rides most directly on the electrification megatrend.

The competitive structure here is what economists call consolidated, and that's good news for the players who've earned a seat. This is not a fragmented free-for-all; it's an oligopoly of well-capitalized giants. The market leader is Germany's 英飞凌 Infineon Technologies, a power-semiconductor titan operating at a revenue scale well above onsemi's. Then there's STMicroelectronics, the Franco-Italian champion that famously supplied the silicon carbide for early Tesla vehicles and built an early lead in automotive SiC. And the Japanese legacy powerhouses, ローム株式会社 Rohm and 富士電機 Fuji Electric, round out the field with deep engineering heritage in power devices. These are formidable, deep-pocketed competitors — nobody wins here by accident.

So how does onsemi win against them? The answer comes down to two things: packaging and integration. Here's the subtle point that's easy to miss. In power electronics, the raw silicon carbide chip is only part of the value. How you package that chip — how you build it into a module that pulls heat away efficiently and minimizes electrical losses — is often what separates a great product from a mediocre one. A power module with lower thermal resistance lets the customer run more power through a smaller, cheaper, lighter system. onsemi's vertical integration, running from GTAT crystal growth through its own proprietary packaging, gives it a structural cost advantage over rivals who have to buy their substrates on the merchant market — while still letting it sustain premium margins. It can, in effect, undercut on cost and hold margin, the holy grail of any manufacturing business.

The Analog & Mixed-Signal Group — the brains behind the brawn. If PSG is the muscle that switches the big currents, AMG is the nervous system that tells the muscle what to do. This segment makes precision analog chips, high-voltage gate drivers, and power-management ICs — the controllers that orchestrate the high-power switches in PSG. A gate driver, for instance, is the chip that actually commands a power transistor to turn on and off at exactly the right instant; get it wrong and the expensive power module fails. These are the parts that make the whole power system work intelligently.

The economics of AMG are gorgeous in a quiet way, and they rest on one word: stickiness. Analog and mixed-signal designs are highly customized and deeply embedded. When a part gets "designed in" to a customer's product — say, the inverter of a specific EV platform or the control system of an industrial robot — it becomes woven into the entire system's engineering. Ripping it out and replacing it with a competitor's part means redesigning, re-qualifying, and re-testing the whole subsystem, a process that can take years and carry enormous risk. So customers don't switch. Once you're in, you tend to stay in for the full multi-year life of that platform, collecting revenue the whole way. This is the switching-cost engine that gives onsemi durable, predictable franchises inside its customers' designs — a theme we'll formalize later when we get to the moat.

The Intelligent Sensing Group — the eyes of the autonomous car. This is the smallest segment by revenue, but don't let the size fool you, because in its niche, onsemi isn't just a leader — it's the hegemon. The company controls more than 70% of the market for ADAS image sensors — the cameras that feed advanced driver-assistance systems — and roughly 40% of the broader automotive camera market.[^2] When your car reads a speed-limit sign, sees the lane markings, or spots the pedestrian stepping off the curb, there's a very good chance it's onsemi silicon doing the seeing.

The competitive dynamics here are fascinating because the most dangerous rival is a household name from an entirely different world. ソニーグループ株式会社 Sony is the undisputed king of smartphone image sensors — the camera in your phone is very likely Sony's — and it has been pushing aggressively into automotive, publicly targeting a 40% share of the automotive image-sensor market.12 Meanwhile, 豪威科技 OMNIVISION dominates the lower-margin, high-volume "viewing" camera segment, especially in China — the backup cameras and surround-view systems where the bar is showing a human a picture rather than feeding a safety algorithm.

So why hasn't the smartphone camera king simply steamrolled onsemi? Because automotive ADAS sensing is not about megapixels — it's about safety-critical performance under brutal conditions. Two specs matter enormously here, and they're worth explaining in plain terms. The first is high dynamic range, or HDR: the ability to capture detail in both the blinding glare of oncoming headlights and the deep shadow of an underpass in the same frame, the way the human eye does but a cheap camera can't. The second, and this one is delightfully specific, is LED flicker mitigation, or LFM. Modern traffic lights, road signs, and car taillights are made of LEDs that don't shine continuously — they flicker on and off many times per second, faster than the human eye notices. But a naïve camera sensor, sampling at the wrong rate, can catch a traffic light in its "off" instant and conclude the light is dark. For a self-driving system, misreading a green light as off is not a glitch — it's a catastrophe. onsemi's sensors are engineered to defeat this flicker, and its Hyperlux platform has become the standard-bearer for exactly this kind of safety-critical imaging.[^2] Sony can match the resolution; matching the decades of automotive-grade qualification and safety-spec dominance is a far slower climb.

The hidden engine — AI data center power. And now for the plot twist nobody had on their onsemi bingo card. Tucked inside the Power Solutions Group is a small but explosively growing business: power semiconductors for AI data centers. In the first quarter of 2026, onsemi's AI data center power revenue more than doubled year-over-year and grew 30% sequentially — quarter over quarter.13 Those are not the growth rates of a mature business; those are the growth rates of something catching fire.

Here's why it's happening, and why it's such a natural fit. The latest generation of AI accelerator chips — think NVIDIA's Blackwell-class clusters — consume staggering amounts of power, drawing thousands of amps of current and demanding power density that would have seemed absurd a few years ago. Delivering clean, efficient power to these liquid-cooled AI servers requires sophisticated, custom multi-phase power stages and smart power modules — precisely the kind of high-performance power electronics that onsemi already builds for cars. The same core competencies that win EV inverters translate directly to feeding the insatiable appetite of AI racks. It is a textbook cross-selling adjacency: a new, large, fast-growing, non-automotive demand source that leverages the existing PSG franchise without requiring onsemi to become a different company. For a business whose bull case had been almost entirely tethered to the fate of electric vehicles, the emergence of AI power as a second growth leg is strategically enormous.

Owning the right businesses is one thing. Running the factories behind them at world-class efficiency is another — and that operational discipline is the next chapter of the turnaround.

VII. The "Fab Right" Era & Current Management Alignment

By 2023, the easy part of the turnaround — if shedding factories and killing products can ever be called easy — was largely done. onsemi had gone "fab-liter," stripping out the sub-scale facilities and the commodity complexity that had dragged on margins for two decades. But subtraction has a natural limit. You can only sell so many factories before you've sold the ones you actually need. The next phase required a different mindset, and management gave it a different name: "fab right."

The philosophy of "fab right" is about optimization rather than amputation. Having pruned the footprint down, the goal shifted to making the remaining assets work as hard as possible — concentrating production in the most modern, lowest-cost facilities to maximize return on invested capital. And the centerpiece of this strategy was a deal that, in its own quiet way, was as shrewd as the GTAT coup.

In December 2022, onsemi completed the acquisition of a 300-millimeter wafer fabrication facility in East Fishkill, New York, from GlobalFoundries.14 To understand why this mattered, you need one piece of manufacturing arithmetic. Chips are made on circular silicon wafers, and the bigger the wafer, the more chips you can make in a single pass through the factory. The industry's commodity power and sensing products had historically been made on 200-millimeter wafers — eight inches across. A 300-millimeter wafer is twelve inches across. Because area scales with the square of the diameter, that jump from 200mm to 300mm yields roughly 2.25 times as many chips per wafer.

Sit with that number for a moment. More than double the output from a single wafer processed through a single factory run, with much of the processing cost essentially fixed per wafer. That is a structural, permanent reduction in unit cost — exactly the kind of durable efficiency advantage that separates a margin leader from the pack. East Fishkill became onsemi's largest U.S. site and its only 300mm facility for power discretes and image sensors,14 giving the company a manufacturing cost structure that its 200mm-bound competitors would struggle to match. In a commodity-tinged industry, the lowest-cost producer who also has differentiated products holds a genuinely powerful hand.

All of this — the fab-liter divestitures, the fab-right optimization, the GTAT integration, the margin transformation — flowed from the strategic clarity of one leader. So let's talk about the architect of it, and crucially, about whether his incentives are pointed in the same direction as a long-term owner's.

Hassane El-Khoury is, by every account, a no-nonsense, operationally obsessive executive — a non-founder leader who runs the company with the cold discipline of an engineer reading a yield report. His defining trait is the willingness to make unpopular subtractive decisions: walking away from revenue, killing products, taking write-downs on his predecessors' mistakes. That last point matters more than it might seem. It takes a particular kind of intellectual honesty to look at an acquisition like Quantenna, recognize it as a value-destroying error, and publicly take the impairment rather than quietly hoping it works out. That decision — to clean up rather than to defend — is a tell about the man's relationship with reality.

But character is reassuring; alignment is verifiable. So look at the structure of his stake and his pay. El-Khoury directly owns 1,015,610 shares of onsemi common stock, representing roughly 0.26% of the company — a holding valued at approximately $76 million as of early 2026.15 That is real, meaningful skin in the game; this is a man whose personal net worth rides substantially on the stock he is responsible for.

More telling still is how his compensation is structured. Over 90% of his total pay is "at-risk" — meaning it is not guaranteed salary but contingent on performance.15 And the performance metrics that govern his equity are precisely the ones a long-term owner would choose. His performance stock units are tied to achieving non-GAAP gross-margin targets — with the company publicly aiming for 53% by 202716 — alongside operating-expense discipline and relative total shareholder return against peers. The mechanism is unforgiving by design: if the margin and return hurdles aren't met, the equity simply doesn't vest, and annual cash incentive payouts can go to zero. There is no participation trophy. El-Khoury gets paid handsomely if and only if onsemi keeps expanding margins and outperforming its peer group — the exact outcomes that would make an outside shareholder happy. When a CEO's pay is wired this tightly to the metrics that define the strategy, you worry a lot less about whether the strategy will be pursued with conviction.

Strategy and incentives are aligned. The harder question for any investor is whether the resulting franchise is genuinely defensible — whether onsemi has built a moat that can withstand the well-capitalized giants circling it. To answer that, we need to bring out the analytical frameworks.

VIII. Strategic Moat: The 7 Powers and Porter's 5 Forces Analysis

Every great business needs a moat — some durable structural advantage that protects its profits from the relentless erosion of competition. onsemi spent twenty years with essentially no moat at all, which is why its margins lived in the basement. The turnaround was, in a real sense, the project of building a moat where none had existed. Let's pressure-test how well it succeeded, using two of the sharpest frameworks in business strategy: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Hamilton Helmer's 7 Powers. Helmer's framework asks a simple question of any claimed advantage: is it a power, meaning something that simultaneously creates a benefit and is genuinely hard for competitors to replicate? onsemi can credibly claim three.

The first is Cornered Resource, and it traces directly to the GTAT acquisition. By owning the proprietary crystal-growth IP, the specialized high-temperature furnaces, and the advanced wafer-slicing technology required to produce silicon carbide boules at volume, onsemi controls a scarce input that competitors cannot simply go buy or quickly recreate. Crystal growth is the supply-chain bottleneck, and onsemi owns its own. A rival can't replicate years of furnace know-how with a checkbook; this is the textbook definition of a cornered resource, and it is the single most distinctive element of onsemi's moat.

The second is Switching Costs, the deepest and most pervasive of onsemi's powers. We touched on this with the analog business, but in automotive it reaches an almost absurd magnitude. To get a chip qualified for use in a car, a supplier must pass three to five years of rigorous testing by Tier-1 suppliers and the automakers themselves — validation against heat, vibration, electrical stress, and functional-safety standards, because a chip failure in a moving vehicle can kill someone. Once a part survives that gauntlet and gets designed into an EV inverter or an ADAS platform, swapping it out mid-generation is almost unthinkable. The customer would face fresh qualification costs, program delays, and — most damning — liability risk on a safety-critical system. The result is that onsemi's design wins are extraordinarily durable, locking in years of revenue per platform. This is the power that turns a single design victory into an annuity.

The third is Scale Economies. The 300mm manufacturing capability at East Fishkill and the build-out of gigafab-scale silicon carbide production — including operations centered in Rožnov, Czech Republic — let onsemi spread its enormous R&D and capital expenditure across high volumes, driving down unit costs in a way smaller players simply cannot match. In a business this capital-intensive, scale is not vanity; it is a structural cost advantage that compounds.

Porter's 5 Forces. Where the 7 Powers describe onsemi's specific advantages, Porter's framework maps the broader competitive weather it operates in.

Start with the Threat of New Entrants, which is very low — and that's a structural gift. Building a modern, vertically integrated 300mm power and silicon carbide fab requires billions of dollars of upfront capital and deep, scarce expertise in high-temperature chemical engineering and materials science. You cannot venture-fund your way into this industry over a weekend. The capital intensity and know-how barriers that once trapped onsemi in a low-margin grind now work for it, keeping new competitors out.

The Bargaining Power of Buyers is moderate, and it's a genuine tension in the model. Automotive OEMs are legendarily ruthless about squeezing their suppliers on price — extracting annual cost-downs is practically a sport in Detroit, Stuttgart, and Hangzhou alike. A company like Geely or NIO has real leverage. But onsemi blunts that power with the very long-term supply agreements we discussed: by trading volume and pricing floors for guaranteed supply, it converts an adversarial annual price negotiation into a multi-year partnership where both sides have committed. When supply is the scarce thing, the supplier of scarce silicon carbide holds more cards than the typical commodity vendor.

And finally, the Intensity of Competitive Rivalry, which is unambiguously high — this is the force that keeps onsemi management awake at night. In power, Infineon and STMicroelectronics are formidable, deep-pocketed giants with their own scale and their own silicon carbide ambitions. In sensing, Sony is a high-R&D predator explicitly hunting onsemi's automotive share. This is not a sleepy industry where a leader can coast; it is a knife fight among well-armed combatants. onsemi's moat is real, but it is a moat that must be defended continuously, with relentless reinvestment, rather than one that can be dug once and forgotten.

That tension — a genuine moat under genuine, well-funded assault — is exactly what makes the investment case a live debate rather than a foregone conclusion. So let's distill the broader lessons before we war-game the bull and bear cases directly.

IX. The Playbook: Business & Investing Lessons

Step back from the specifics of silicon carbide and image sensors, and the onsemi turnaround offers a set of lessons that travel well beyond semiconductors. Three stand out.

Lesson one: beware the margin-over-volume fallacy. The deepest trap in any capital-intensive, cyclical industry is the seductive belief that volume is always good — that filling the factory, capturing share, and growing the top line are self-evidently worth pursuing. onsemi's first two decades are a monument to where that belief leads: a bigger and bigger company earning worse and worse returns, because chasing volume meant accepting commodity products at commodity margins, and accepting those meant absorbing devastating underutilization charges every time the cycle turned. The counterintuitive truth El-Khoury proved is that subtraction creates value. By deliberately walking away from billions in low-margin revenue, onsemi became smaller for a while — and vastly more valuable. For investors, the lesson is to be deeply suspicious of management teams that celebrate revenue growth and market share without a corresponding story about returns. Growth that destroys margin is not success; it's just a more expensive way to lose.

Lesson two: vertical integration is a tool, not a religion. It would be easy to draw the wrong conclusion from the GTAT story — to decide that vertical integration is simply good and that more of it is always better. onsemi's own behavior refutes that. The very same management team that aggressively integrated backward into silicon carbide crystal growth was, at the exact same time, selling off its standard silicon fabs. Why integrate one and divest the other? Because the strategic logic isn't about integration per se — it's about scarcity and criticality. Silicon carbide crystal growth was a genuine bottleneck, a supply-constrained, technically forbidding choke point where ownership conferred real power. Standard silicon fabrication was a commodity capability available from anyone. The discipline is to integrate only what is strategic and supply-constrained, and to ruthlessly outsource or exit everything that isn't. Integration as ideology destroys value; integration as targeted strategy creates it.

Lesson three: have the courage to clean up legacy mistakes. Perhaps the subtlest leadership lesson here is about ego. When a new CEO inherits a predecessor's failed acquisition, the path of least resistance is to defend it, to keep funding it, to hope it eventually works out — because admitting it was a mistake feels like an admission of institutional failure. El-Khoury did the opposite with Quantenna. Rather than throw more R&D dollars at a consumer Wi-Fi business that didn't fit the new high-margin automotive and industrial roadmap, he took the $387 million write-down and wound the operation down, redeploying that capital and engineering talent back to the core.4 Great capital allocators are unsentimental about sunk costs. They ask not "how do we justify what we already spent?" but "where does the next dollar earn the best return?" — and they act on the answer even when it stings.

These lessons sound clean in retrospect. But the forward-looking question for an investor is whether the strategy that produced them will keep working — which means honestly weighing what could go right against what could go wrong.

X. The Bull vs. Bear Case & Key KPIs

Every compelling investment is an argument, and the onsemi argument has two articulate sides. Let's give each its strongest form.

The bull case rests on three pillars, each tied to a powerful secular trend.

The first is automotive ADAS lock-in. As safety regulations tighten and Level 2-plus and Level 3 driver-assistance systems proliferate, the number of cameras per vehicle is climbing steadily — from perhaps two on an older car toward twelve or more on a modern, sensor-laden one. Every one of those ADAS cameras is a socket for onsemi's high-margin, safety-critical sensing silicon, in a market it already dominates. This is content growth layered on top of unit growth, protected by the switching-cost moat we described — a durable, expanding annuity.

The second pillar is silicon carbide vertical dominance. If the global EV transition continues its march toward higher-voltage 800V and 900V architectures, the EliteSiC portfolio — uniquely backed by in-house crystal growth — is positioned to capture that shift while preserving premium gross margins. The cornered resource at the heart of the moat pays off precisely as silicon carbide demand scales.

The third pillar is the AI power explosion — the wildcard that could rerate the whole story. If onsemi successfully cross-sells its custom power stages and power-management ICs into liquid-cooled AI data centers, it gains a massive, fast-growing growth leg that has nothing to do with cars. Given the early triple-digit growth rates,13 this is the optionality that could transform onsemi from "the EV power and sensing company" into something broader and more resilient.

The bear case is equally serious, and it attacks each pillar directly.

The first bear argument is silicon carbide commodity risk. Here's the uncomfortable possibility: China is building out enormous domestic silicon carbide substrate capacity. If that capacity comes online faster than demand, the result could be a glut — an oversupply of silicon carbide substrates that sparks a global price war and erodes the very margins that make PSG attractive. The cornered resource is only valuable as long as the resource stays scarce. A flood of cheap Chinese substrate would commoditize the bottleneck and undercut onsemi's central thesis.

The second bear argument is Sony's encroachment. Sony is not a sleepy incumbent; it is the best image-sensor company in the world, and it has explicitly set its sights on automotive. If Sony translates its smartphone sensor dominance into ADAS share — bringing its R&D firepower and manufacturing scale to bear — onsemi's 70%-plus market share has nowhere to go but down. A share leader being hunted by a stronger generalist is a precarious position, however good the current numbers look.

The third bear argument is cyclical EV slowdown. onsemi's bull case leans heavily on continued EV adoption. But EV demand has proven lumpy and politically sensitive, subject to subsidy changes, charging-infrastructure bottlenecks, and shifting consumer enthusiasm. A prolonged slump in global EV adoption would delay the payoff on the very capacity investments — East Fishkill, Rožnov — that the company has made to serve that demand, pressuring returns just when fixed costs are highest. The fab-right footprint is leaner than the old one, but it is not immune to the cycle that has always defined this industry.

Notice how neatly the bull and bear cases mirror each other: each of onsemi's three powers — the sensing dominance, the silicon carbide cornered resource, the scale-driven cost structure — is simultaneously the source of the bull thesis and the target of the bear thesis. That symmetry is what makes onsemi a genuine debate rather than a layup in either direction.

The KPIs that actually matter. Given all this, what should a long-term owner actually watch? Not the endless parade of quarterly noise, but a small number of metrics that cut to the heart of whether the strategy is working. Three rise above the rest.

The first is non-GAAP gross margin, tracked against management's stated target of 53% by 2027.16 This single number is the scoreboard for the entire transformation. It captures whether the margin-over-volume discipline is holding, whether the fab-right cost structure is delivering, and whether pricing power is intact. If gross margin keeps marching toward and past the low fifties, the strategy is working; if it stalls or reverses, something in the thesis is breaking.

The second is the silicon carbide (EliteSiC) revenue run-rate, watched relative to peers like STMicroelectronics and Infineon. This is how you confirm whether onsemi is preserving or losing share in its most strategic growth market — and, by extension, whether the cornered-resource advantage is translating into the commercial wins the bull case requires.

The third is AI data center sequential revenue growth. Because this business is so new, sequential — quarter-over-quarter — growth is the cleanest read on whether the AI power opportunity is becoming genuinely material or fizzling out as a one-off. Sustained sequential growth validates the second growth leg; a stall would deflate the most exciting part of the forward story.

Watch those three, and you'll understand onsemi's trajectory better than any headline could tell you. Which brings us, finally, to the bigger picture.

XI. Epilogue & Outro

There's a temptation, looking at onsemi today, to attribute the transformation to luck — to the happy accident of being positioned in front of electrification and autonomy and AI just as those waves crested. But that reading misses the real lesson. Plenty of companies sat in front of the same waves and drowned. What separated onsemi was not its end markets but its discipline — the willingness to do the genuinely hard things that the old management, for twenty years, could not bring itself to do.

The whole story, stripped to its essence, is about the power of focus. It's about a leader who looked at 80,000 products and a continent of sub-scale factories and understood that the path to greatness ran through subtraction, not addition. It's about treating capital allocation as the central act of management — buying the one scarce thing that mattered for $415 million, selling the factories that didn't, and taking the write-down on the mistake that never fit. It's about wiring management's pay so tightly to margins and returns that strategy and self-interest became the same thing.

A company born from Motorola's trash bin — the unwanted discrete business, the part nobody believed had a future — reinvented itself into something close to indispensable: the silicon that lets electric cars go farther, that lets autonomous systems see the road, and that increasingly feeds the power-hungry data centers training the world's artificial intelligence. The metamorphosis from sleepy commodity player to sovereign of power and sensing was not magic. It was discipline, courage, and clarity, applied relentlessly over five years. Whether that discipline can withstand the well-armed rivals now circling — Infineon and STMicroelectronics in power, Sony in sensing, and an entire Chinese supply chain in silicon carbide — is the question that will define onsemi's next chapter. But the company that will fight those battles is unrecognizable from the one that limped into 2020. And that, more than any single product or deal, is the achievement worth remembering.

References

-

onsemi Outlines Strategy for Gross Margin Expansion to 53% — onsemi Analyst Day Presentation, 2023-05-16 ↩↩

-

ON Semiconductor Completes Acquisition of Fairchild Semiconductor for $2.4 Billion — Business Wire, 2016-09-19 ↩

-

ON Semiconductor to Acquire Quantenna Communications for $1.07 Billion — Business Wire, 2019-03-27 ↩

-

Onsemi Reports Impairments and Restructuring of Quantenna Business — Reuters, 2022-11-07 ↩↩

-

How onsemi's CEO Swapped 'Fab Filler' for Focus — Forbes, 2022-09-14 ↩

-

onsemi Form 10-K for Fiscal Year Ended Dec 31, 2024 — SEC EDGAR, 2025-02-10 ↩

-

onsemi to Acquire GT Advanced Technologies — Business Wire, 2021-08-25 ↩

-

onsemi to Acquire GT Advanced Technologies — Business Wire, 2021-08-25 ↩

-

onsemi Form 10-K for Fiscal Year Ended Dec 31, 2025 — SEC EDGAR, 2026-02-09 ↩

-

onsemi Form 10-K for Fiscal Year Ended Dec 31, 2025 — SEC EDGAR, 2026-02-09 ↩↩↩

-

Global Power Semiconductor Market Share and Rankings — Yole Group, 2024-11-12 ↩

-

onsemi Q1 2026 Financial Results Press Release — onsemi, 2026-05-04 ↩↩

-

onsemi Completes Acquisition of East Fishkill 300mm Fab from GlobalFoundries — Business Wire, 2022-12-31 ↩↩

-

onsemi Form 10-K for Fiscal Year Ended Dec 31, 2025 — SEC EDGAR, 2026-02-09 ↩↩

-

onsemi Outlines Strategy for Gross Margin Expansion to 53% — onsemi Analyst Day Presentation, 2023-05-16 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube