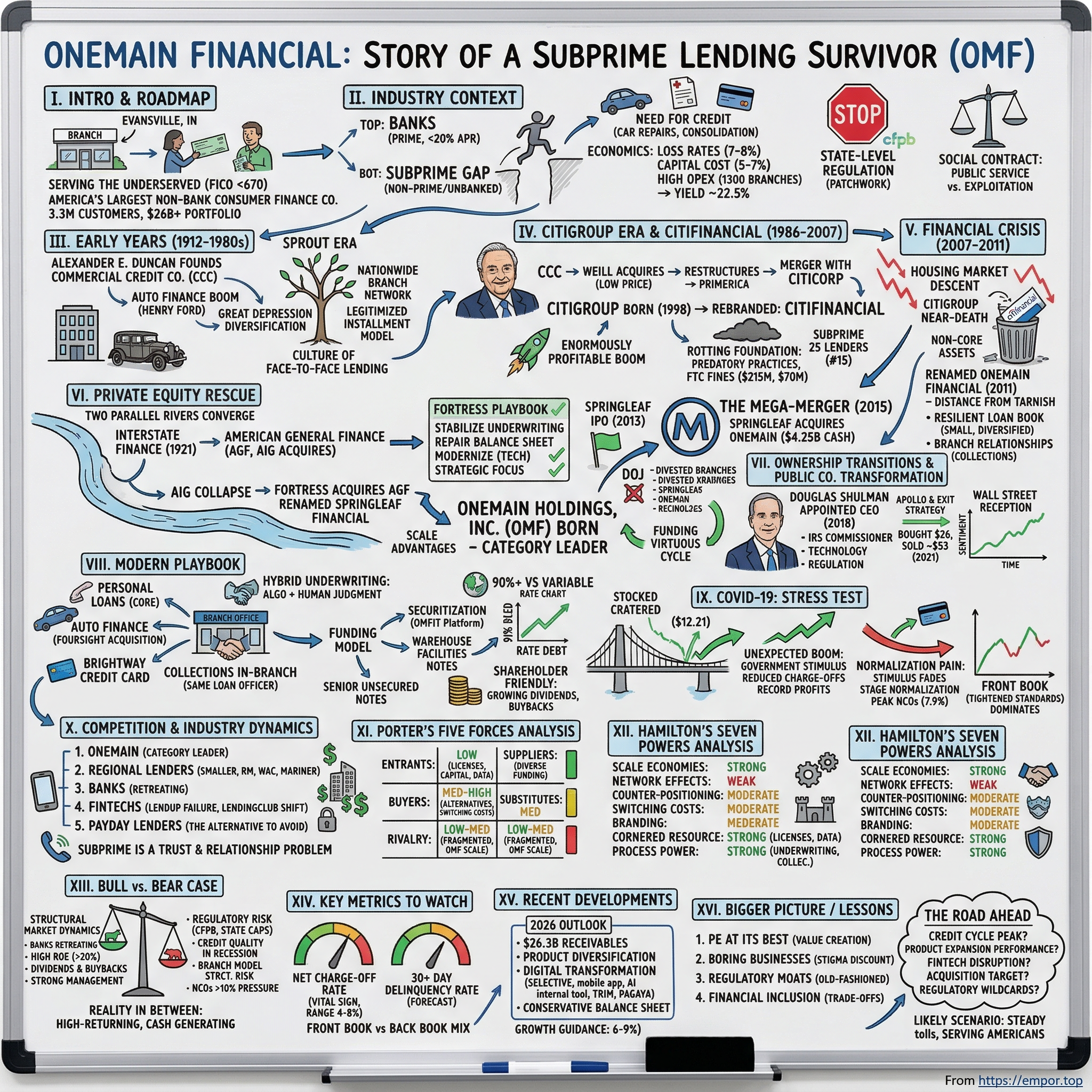

OneMain Financial: The Story of America's Subprime Lending Survivor

I. Introduction and Episode Roadmap

Picture a small branch office in Evansville, Indiana. No marble lobby, no velvet ropes, no investment bankers in bespoke suits. Just a loan officer sitting across a desk from a customer whose credit score starts with a five. The customer needs three thousand dollars for a car repair that will keep her commuting to work. She has been turned down by her bank, laughed off by credit card companies, and is one missed paycheck from financial catastrophe. The loan officer pulls up her file, reviews her employment history, checks the equity in her vehicle, and thirty minutes later, she walks out with a check.

This scene plays out thousands of times every day, across more than 1,300 branches in 44 states, inside a company called OneMain Financial. It is America's largest non-bank consumer finance company, managing a loan portfolio north of $26 billion, serving roughly 3.3 million customers who exist in the vast, uncomfortable space between "bankable" and "unbankable."

OneMain Holdings, traded on the NYSE under the ticker OMF, is the kind of company that most investors instinctively avoid and most analysts struggle to categorize. It is not a bank—it cannot take deposits. It is not a fintech—it runs 1,300 physical storefronts. It is not a payday lender—its average loan runs into the thousands, not the hundreds, and its APRs are a fraction of payday rates. It is something older, stranger, and more durable than any of those things.

The central question of this story is deceptively simple: How did a company with roots stretching back to 1912 survive the financial crisis, multiple ownership changes, private equity restructuring, a mega-merger, regulatory crackdowns, and a global pandemic to emerge as a thriving, dividend-paying public company?

The answer involves Sandy Weill's empire-building ambitions, Citigroup's near-death experience, a contrarian private equity bet, the largest consumer finance merger in American history, and a former IRS Commissioner who became a surprisingly effective CEO. It also forces a confrontation with one of the most uncomfortable questions in American finance: Is lending to people with bad credit a public service or exploitation?

What makes this story worth telling is that it touches every major theme in modern finance: the post-crisis regulatory reckoning, the private equity turnaround playbook executed to textbook perfection, the debate over financial inclusion versus predatory lending, and the surprising resilience of old-fashioned, branch-based business models in an era obsessed with digital disruption. This is not a company that will ever grace the cover of Wired magazine. But it might just be one of the most instructive case studies in American capitalism.

II. The Consumer Finance Industry Context

Before diving into OneMain's story, it helps to understand the landscape it operates in, because the economics of subprime lending are genuinely different from what most people imagine when they hear the phrase "consumer credit."

The American consumer credit market exceeds $18 trillion in total household debt. At the top of the pyramid sit the banks, serving prime and super-prime borrowers with credit cards at 15-20% APR, auto loans at 5-7%, and mortgages at prevailing rates. These are the customers with FICO scores above 670, steady employment histories, and sufficient assets to qualify for mainstream financial products. They represent roughly 70% of the population.

Then there is everyone else. Approximately 30% of American consumers carry FICO scores below 670, placing them in the "non-prime" or "subprime" category. According to the FDIC's 2023 National Survey, 5.6 million American households lack a bank account entirely, and another 19 million are "underbanked," meaning they have an account but rely heavily on non-bank financial services. Combined, that is roughly 25 million households existing partially or fully outside the traditional banking system. The demographics are not random: 10.6% of Black households and 9.5% of Hispanic households are unbanked, compared to 1.9% of white households. Financial exclusion in America runs along predictable lines of race, income, and geography.

These Americans still need credit. They need to fix cars, cover medical bills, consolidate debt from predatory credit card issuers, and bridge gaps between paychecks. They are not undeserving; they are underserved. And the gap between their needs and available options is enormous.

Consider the practical alternatives. A borrower with a 580 FICO score needs $5,000 for a car repair. She could try a credit card, but most card issuers decline applicants below 600 FICO, and those that approve her offer limits of $300-$500 at 28% APR with punitive late fees. She could visit a payday lender, but payday loans typically max out at $500-$1,000, carry effective APRs of 300-400%, and must be repaid in two weeks—a structure designed to create repeat borrowing cycles. She could ask family members, but most families in her economic cohort do not have $5,000 of spare capital. She could try to borrow from her 401(k), but she likely does not have one: only 56% of private-sector workers have access to employer-sponsored retirement plans. The "subprime gap" is not an abstraction. It is the distance between this borrower's needs and the financial system's willingness to serve her.

The economics of subprime lending explain why interest rates run between 18% and 36% APR, and why those rates are not primarily about greed but about math. Start with loss rates: OneMain charges off roughly 7-8% of its receivables annually. That means for every hundred dollars lent, about eight dollars simply disappear, never to be repaid. Compare that to a prime lender losing perhaps 1-2%.

Then add the cost of capital. Unlike banks, which fund themselves with federally insured deposits at near-zero cost, non-bank lenders like OneMain must borrow in the securitization and bond markets, paying 5-7% for their funding. Layer on operating costs: maintaining 1,300 physical branches, employing roughly 9,300 people, complying with licensing requirements in 44 different states, running collections operations, and absorbing the overhead of a public company. When a lender loses eight cents on every dollar, pays six cents for the money itself, and spends another seven cents running the operation, the required yield on the portfolio needs to exceed 20% just to break even. That is why the blended portfolio yield runs around 22.5%.

The regulatory environment adds enormous complexity. Consumer lending is regulated primarily at the state level, with each of the 50 states maintaining its own licensing regime, usury limits, and examination requirements. The Consumer Financial Protection Bureau, created by Dodd-Frank in 2010, provides federal oversight, but it is explicitly prohibited from imposing national usury limits. This creates a patchwork where a loan that is perfectly legal in one state may violate the law fifty miles away. Obtaining and maintaining licenses across 44 states is a years-long, millions-of-dollars process that serves as one of the most effective barriers to entry in all of financial services.

The social contract question haunts every player in this space. Critics argue that lending at 25-35% APR to financially vulnerable people is inherently exploitative, trapping borrowers in cycles of debt. Advocates counter that without these lenders, non-prime borrowers would have no options at all, or worse, would be forced to payday lenders charging effective APRs exceeding 400%, or to illegal loan sharks. The FDIC itself has acknowledged that "appropriately underwritten subprime loans are important and legitimate elements of the financial economy." The Pew Charitable Trusts has explicitly advocated for the transition from payday loans to installment loans as a policy objective, positioning companies like OneMain as the preferred alternative to worse options.

Investors need to understand both sides of this debate, because regulatory risk in this sector is real and existential, and it is driven as much by political sentiment as by economic logic. With that backdrop, the story of how one particular consumer lender navigated more than a century of American economic history becomes all the more remarkable.

III. The Early Years: Commercial Credit and the Sprout Era (1912-1980s)

In 1912, a year that also saw the sinking of the Titanic and Woodrow Wilson's election to the presidency, Alexander E. Duncan and eight fellow businessmen pooled $300,000 in Baltimore, Maryland, and founded the Commercial Credit Company. Their initial business was prosaic: lending working capital to manufacturers and building contractors, using their customers' accounts receivable as collateral. It was the kind of financial plumbing that makes economies function without anyone noticing—and the kind of business that would survive precisely because no one paid it much attention.

Four years later, CCC branched into auto finance, and the timing could not have been better. Henry Ford's assembly line was democratizing car ownership, and millions of Americans needed financing to bridge the gap between aspiration and affordability. Auto lending became CCC's greatest growth engine through the 1920s, when installment lending transformed American consumer culture. The idea that ordinary people could borrow money to buy refrigerators, washing machines, and phonographs was revolutionary. Before this era, consumer credit was the province of pawnbrokers and "loan sharks." CCC helped legitimize the installment model, building the institutional DNA of consumer underwriting that would persist for over a century.

The Great Depression crushed auto sales and forced CCC to diversify. The company acquired factoring companies, an accounts receivable insurer, and a casualty insurance firm. During World War II, it even manufactured war-related goods. Through the postwar decades, CCC continued expanding into consumer lending, insurance, and financial services, becoming a diversified conglomerate.

By the 1960s, CCC had evolved into something far larger and more complex than its founders envisioned. The company was among the first finance companies to access the commercial paper market, giving it cheaper funding than traditional bank borrowing. It had built a nationwide network of branch offices that served as storefronts for consumer lending—physical locations in strip malls and downtown districts where working-class Americans could walk in, apply for a loan, and leave with cash in hand. This was not glamorous finance. It was the financial plumbing of working-class America, serving the mechanic who needed $500 for tools, the secretary saving for a down payment, the family consolidating Christmas debts. The cultural foundation of face-to-face lending relationships was being laid, branch by branch, decade by decade.

The first major ownership drama came in 1968. Loews Theatres launched a hostile takeover bid for CCC, having quietly accumulated 10% of the company's stock. CCC's board rejected the overture and sought a "white knight," ultimately agreeing to be acquired by Control Data Corporation, a Minneapolis-based computer company that wanted a finance subsidiary to fund its expensive mainframe leasing operations. It was a strange marriage: a century-old lending business bolted onto a technology company. For nearly two decades under Control Data's ownership, CCC maintained a low profile, consolidating operations and steadily building its branch network across working-class America.

Why does this ancient history matter? Because it illustrates a crucial point: OneMain's competitive advantages did not materialize overnight. The branch locations that now generate $20 million in average receivables each were selected and optimized over decades. The underwriting models were trained on a century of credit performance data. The regulatory licenses that block new entrants were accumulated through generations of compliance work. When investors look at OneMain today, they are not just seeing a 2015 IPO; they are seeing the compounded institutional capital of a 114-year-old lending operation.

By the mid-1980s, though, Control Data was hemorrhaging money on its computer business, and CCC sat in corporate limbo, waiting for someone who could see its value. That someone turned out to be one of the most consequential figures in the history of American finance.

IV. The Citigroup Era and Rebirth as CitiFinancial (1986-2007)

Sandy Weill had a problem. In August 1985, the legendary dealmaker resigned from American Express after losing an internal power struggle. He was 52 years old, enormously wealthy, and unemployable at the top of any major financial institution. After failing to become CEO of BankAmerica Corp., Weill needed a vehicle—a corporate shell from which to rebuild his empire. He found it in Baltimore.

In 1986, Weill persuaded Control Data to sell him Commercial Credit Company for approximately $7 million. The price was almost absurdly low, reflecting both CCC's distressed parent and the market's dim view of consumer finance. But Weill was not buying a consumer lending business. He was buying a launchpad. He restructured ruthlessly, cutting costs, improving profitability, and taking CCC public. In six years, he multiplied CCC's profits nearly eight-fold, from $25 million to $193 million.

What followed was one of the most extraordinary acquisition sprees in financial history. In 1988, Weill acquired Primerica Corporation for $1.5 billion, gaining Smith Barney brokerage and the A.L. Williams insurance company. The combined entity adopted the Primerica name. In 1992, he bought a 27% stake in Travelers Insurance for $722 million, then reacquired his former Shearson brokerage from American Express for $1.2 billion. By 1993, after acquiring the remaining 73% of Travelers, the empire was renamed Travelers Group. Weill added Aetna's property and casualty operations and Salomon Brothers, creating Salomon Smith Barney. Each deal was bigger than the last, each one moving Weill closer to his ultimate prize.

The culmination came on April 6, 1998, when Weill announced a $76 billion merger with Citicorp, the parent of Citibank. Citigroup Inc. was born—the largest financial services organization in the world, with $994 billion in assets. The merger technically violated the Glass-Steagall Act of 1933, but a grace period allowed the combined entity to operate, and in 1999, Congress repealed Glass-Steagall entirely with the Gramm-Leach-Bliley Act.

Think about what happened here: the consumer lending business that Alexander Duncan founded in 1912 had become the seed from which the largest financial institution on earth grew. CCC's consumer lending operations were absorbed into Citigroup and rebranded as CitiFinancial—a small cog in the largest financial machine on earth.

Under the Citi umbrella, CitiFinancial had access to virtually unlimited capital and the imprimatur of the world's largest financial brand. The subsidiary operated thousands of branches across the United States, offering personal loans, home equity loans, and credit insurance to non-prime borrowers. At its peak, CitiFinancial had roughly 1,900 branch offices, making it far and away the largest branch-based consumer lender in the country. The business was enormously profitable during the mid-2000s credit boom—margins were wide, loss rates were low, and housing prices only went up. Citi's executives regarded CitiFinancial as a reliable profit center that served customers too small for the main bank to bother with.

But embedded within that profitability were practices that would come back to haunt not just Citigroup, but the entire industry. Under CitiFinancial's umbrella, the company grew aggressively during the subprime boom of the early 2000s. In November 2000, Citigroup acquired Associates First Capital Corporation, a major subprime lender already under regulatory scrutiny for predatory practices. The acquisition brought scale but also brought trouble.

In September 2002, Citigroup paid $215 million to settle FTC charges that Associates had engaged in "systematic and widespread abusive lending practices," the largest consumer protection settlement in FTC history at that time. Two years later, the Federal Reserve fined CitiFinancial an additional $70 million for abusive lending practices. A former CitiFinancial employee went public with allegations that loan officers were compensated for refinancing customers into higher-rate loans, raising interest rates on borrowers who could least afford it.

These scandals were not isolated incidents but symptoms of an industry-wide culture that prioritized volume over borrower welfare. CitiFinancial was later identified as number 15 on the Center for Public Integrity's "Subprime 25" list of lenders whose practices contributed to the 2008 financial crisis. The business had grown large and profitable, but the foundation was rotting.

For investors studying OneMain today, this period matters for two reasons. First, it illustrates the reputational and regulatory risks that are permanently embedded in subprime lending—risks that never fully disappear regardless of how responsibly the business is managed. Second, and more subtly, it demonstrates why the post-crisis regulatory cleanup actually benefited well-managed survivors. The worst actors were driven out of business, the CFPB was created to police the remaining players, and the reputational stigma discouraged new entrants. The crisis did not just damage subprime lending—it inadvertently created the conditions for a well-run survivor to build a durable franchise. But first, the industry had to survive the crisis itself.

V. The Financial Crisis and The Great Unraveling (2007-2011)

By the summer of 2007, the American housing market was beginning its descent, and the word "subprime" was about to become toxic. For CitiFinancial, the timing could not have been worse. The business was deeply embedded in home equity lending, and its parent company was about to experience one of the most spectacular corporate near-death experiences in history.

Citigroup had pursued high-risk strategies across multiple business lines simultaneously: originating and securitizing subprime mortgages, creating and marketing collateralized debt obligations, and originating leveraged corporate loans. The bank's leadership had prioritized growth over risk management, famously exemplified by CEO Chuck Prince's July 2007 remark that "as long as the music is playing, you've got to get up and dance."

By the time the music stopped, the losses were staggering. The firm's total allowance for loan losses reached $30.5 billion by the end of 2008. A $9.6 billion goodwill impairment charge hit in the fourth quarter alone. Between 2008 and 2009, Citigroup received $45 billion in capital from the U.S. Treasury, a loss-sharing agreement covering $301 billion of company assets, and $5.75 billion of FDIC-guaranteed senior unsecured debt. The government essentially prevented one of the world's largest banks from ceasing to exist.

Under intense political and regulatory pressure to shed non-core assets and simplify its structure, Citigroup designated CitiFinancial as non-core. The consumer lending arm—the very business that Sandy Weill had used as his springboard to build the empire—was now classified as dead weight to be disposed of. In 2011, CitiFinancial was renamed OneMain Financial, a fresh brand meant to distance the operation from Citigroup's tarnished image and prepare it for eventual sale.

But selling a subprime consumer lending business in 2011 was like trying to sell umbrellas during a drought. The entire concept of subprime lending had been demonized. Charge-offs spiked as unemployment rose and borrowers defaulted. Branches closed. Morale collapsed among employees who wondered if their jobs would exist next quarter. Potential buyers looked at the business and saw nothing but regulatory risk, credit losses, and reputational poison.

What kept OneMain from collapsing entirely was the nature of its loan book. Unlike the mortgage-backed securities that had blown up the global financial system, OneMain's loans were primarily small-dollar personal and auto loans, many of them secured by vehicle titles. The average loan was a few thousand dollars, not hundreds of thousands. The diversification across millions of small loans in 44 states provided a resilience that concentrated mortgage portfolios lacked. And the branch relationships—the loan officers who knew their customers personally and could modify payment terms before accounts deteriorated—provided a collections effectiveness that purely transactional lending models could not match.

The business was wounded but not dead. The infrastructure was intact: the branches, the licenses, the underwriting expertise, the customer relationships, the organizational knowledge of how to lend profitably to working-class Americans. These were not assets that appeared on the balance sheet, but they were the assets that mattered most. A building can be rebuilt; a century of institutional knowledge cannot be reconstructed from scratch.

The Citi saga also offered a lesson that would prove crucial for OneMain's future owners. Consumer subprime lending had not failed because the underlying business model was broken. It had failed because it was embedded in an organization that had catastrophically mismanaged risk at the enterprise level. The small-dollar consumer lending operation buried inside Citigroup was never the source of the bank's existential crisis; it was collateral damage. Strip away the corporate parent's toxic mortgage exposure, the CDO manufacturing, and the reckless balance sheet leverage, and what remained was a perfectly viable business serving a genuine market need.

That distinction—between a broken business model and a broken corporate context—would define the opportunity for the private equity investors who came next.

VI. The Private Equity Rescue: Fortress, Springleaf, and the Road to Reunion

The story of OneMain's resurrection actually begins with a separate company, in a separate city, with a separate lineage that would eventually converge in one of the most consequential mergers in consumer finance history. To understand how OneMain became the dominant force it is today, you have to understand that there were two rivers of corporate history flowing in parallel for nearly a century before they merged into one.

In 1921, Interstate Finance Corp. was established in Evansville, Indiana, to underwrite sales for the Inland Motor Truck Company. Interstate began issuing consumer loans in 1928 and writing credit-related insurance by 1929. Over the following decades, it grew through acquisitions, eventually becoming American General Finance, one of the largest consumer lending companies in the country.

In August 2001, AIG acquired American General Financial Group for $23 billion, folding it into its insurance empire. American General Finance operated roughly 1,400 branch offices across the United States, making it one of the two largest branch-based consumer lenders alongside CitiFinancial. Under AIG's ownership, the consumer lending division was a steady but unremarkable contributor to the conglomerate's earnings.

When AIG itself nearly collapsed during the financial crisis—requiring a $182 billion government bailout that remains the largest corporate rescue in U.S. history—American General Finance became another asset to be shed. The consumer lending arm had its own problems: its portfolio included home equity loans that were deteriorating rapidly, and the stigma of the AIG brand was toxic. In November 2010, an affiliate of Fortress Investment Group acquired an 80% economic interest in American General Finance from AIG. Fortress renamed it Springleaf Financial and set about the painstaking work of rebuilding.

The Fortress playbook was a masterclass in private equity turnaround execution, and it is worth examining in detail because it explains how OneMain was transformed from a distressed asset into a market leader.

Step one: stabilize the portfolio by tightening underwriting standards and cleaning up legacy loans that should never have been made. This meant accepting lower origination volumes in the short term to improve the quality of the book over time—a trade-off that requires patience from investors accustomed to growth.

Step two: repair the balance sheet by reducing leverage and rebuilding relationships with capital markets providers who had retreated from consumer ABS after 2008.

Step three: modernize operations by investing in technology, consolidating branches, and bringing in experienced management talent who understood both consumer lending and post-crisis regulatory requirements.

Step four: refocus strategically by exiting products and geographies that did not fit the core competency of secured consumer lending—shedding the home equity products that had caused so much trouble during the crisis and doubling down on personal loans and auto lending.

It worked, but not overnight. The turnaround required patience that is uncommon even in private equity. Fortress held American General Finance for three years before taking it public, investing continuously in the business while other PE firms might have demanded quicker returns. Cost structures were rationalized. Underwriting models were rebuilt with more conservative assumptions, rejecting the riskiest borrowers that pre-crisis lenders had eagerly served. The securitization program was restarted, cautiously at first, as the ABS market itself was still recovering from the crisis. Each successful securitization deal built credibility with investors and demonstrated that the revamped underwriting was producing better loan quality.

By October 2013, Springleaf completed an IPO at $17 per share, raising $358 million under the ticker LEAF. Fortress-controlled entities still owned approximately 77% of the common stock, but the public listing provided two critical things: validation from public market investors that the turnaround was real, and access to equity capital markets that would prove crucial for the next move.

Meanwhile, Citigroup was still trying to find a buyer for OneMain Financial, having filed an S-1 in October 2014 to potentially take the unit public while simultaneously exploring a sale. The dual-track process eventually resolved in Springleaf's favor. On March 2, 2015, Springleaf announced it would acquire OneMain Financial from Citigroup for $4.25 billion in cash.

The strategic logic was compelling but the execution risk was enormous. Both companies served non-prime borrowers through branch networks. Combining them would create the undisputed leader in consumer finance, with massive scale advantages in funding, operations, and technology. But the Department of Justice and seven state attorneys general raised antitrust concerns, finding that the merger would eliminate "substantial head-to-head competition" in personal installment lending in 126 towns across 11 states. As a condition of approval, the DOJ required the divestiture of 127 branches with over $600 million in loan receivables, which were sold to Lendmark Financial Services of Covington, Georgia.

The acquisition closed in November 2015. Springleaf Holdings was renamed OneMain Holdings, Inc. and adopted the ticker symbol OMF. For the first time, two legacy consumer lending businesses—one tracing its roots to Baltimore in 1912 and the other to Evansville in 1921—were unified under a single brand.

The integration was enormous. The combined entity had over 2,300 branches, overlapping systems, different corporate cultures, and two sets of everything. Management consolidated the branch network down to approximately 1,600 locations, merged technology platforms, harmonized underwriting models, and extracted cost synergies ahead of schedule. The combined company emerged with more than $20 billion in receivables, a national footprint, and unassailable market leadership in non-prime consumer lending.

This merger was the single most important event in understanding why OneMain exists in its current form. Before it, there were two mid-sized, wounded consumer finance companies. After it, there was a category leader with the scale to fund itself cheaply, the density to serve customers effectively, and the market position to set industry terms.

The financial logic was powerful. Scale in consumer lending creates a virtuous cycle: a larger portfolio attracts cheaper funding from capital markets, which enables more competitive loan pricing, which attracts better borrowers, which reduces charge-offs, which makes the portfolio more attractive to capital markets. OneMain's post-merger scale—more than $20 billion in receivables—gave it access to securitization markets on terms that no smaller competitor could match. It could issue larger deals, more frequently, with better credit enhancement structures, earning a reputation among ABS investors as a reliable, high-quality issuer. This funding advantage alone is worth several hundred basis points in competitive advantage—the difference between a profitable lending operation and a marginal one.

The merger also created what military strategists call "mass": the ability to concentrate resources at decisive points. With 1,600 branches, OneMain had density in markets that competitors could only cover sparsely. A customer in rural Georgia or small-town Ohio might have a OneMain branch as literally the only non-payday lending option within a 30-mile radius. That geographic density, combined with the brand recognition from being the only national player, created a local monopoly dynamic in hundreds of markets across the country.

VII. Ownership Transitions and Public Company Transformation

With the mega-merger complete, the ownership structure began its next evolution. Fortress Investment Group, which had orchestrated the combination, held a dominant stake but was looking toward an exit. In January 2018, an investor group led by Apollo Global Management and Varde Partners agreed to purchase Fortress's entire remaining 40.5% stake in OneMain Holdings for $26 per share, approximately $1.4 billion.

Seven months after the Apollo investment closed, OneMain made a leadership change that would prove consequential. In September 2018, Douglas H. Shulman was appointed President and CEO. Shulman's background was unusual for a consumer finance executive, and that was precisely the point.

From 2008 to 2012, Shulman had served as Commissioner of the Internal Revenue Service, where he oversaw an organization of 100,000 employees, led a major technology transformation, drove customer service metrics to historic levels, and made breakthroughs in combating international tax evasion. Before the IRS, he had been vice chairman of the Financial Industry Regulatory Authority. After leaving government, he served as a senior executive at BNY Mellon. The man knew regulation, technology, and large-scale operations. He did not come from the consumer lending world, but he understood the intersection of government, finance, and technology better than almost anyone available.

The Shulman appointment signaled OneMain's intent to operate as a sophisticated, technology-enabled, regulatory-compliant enterprise rather than a legacy consumer lender coasting on inertia. His government experience gave him credibility with regulators who might otherwise view a subprime lender with suspicion. His technology background informed a push to modernize OneMain's digital capabilities while preserving the branch model that differentiated it from fintech competitors. His compensation structure—with roughly 93% of total pay tied to equity and performance bonuses—aligned his interests tightly with long-term shareholder returns.

Apollo executed its exit strategy with characteristic efficiency, demonstrating the returns that a disciplined PE approach to subprime consumer lending could generate. In February 2021, Apollo sold 8 million shares at $53 per share. In May 2021, another 8 million shares at $53.50. And in October 2021, Apollo sold its entire remaining position of roughly 10 million shares, completing its exit.

The math was elegant: purchased at $26 per share, sold at approximately $53—a clean double in three years, plus substantial dividends collected along the way. The total return, including dividends, likely exceeded 120%. It was a textbook private equity return, generated not through financial engineering or leverage tricks, but through operational improvement and patient capital allocation. The IRR for Apollo's OneMain investment, while not publicly disclosed, almost certainly exceeded the firm's typical mid-teens target for credit investments by a wide margin.

The period from the 2015 merger through Apollo's 2021 exit represents one of the clearest examples of the PE turnaround playbook working exactly as designed. Fortress bought damaged assets from AIG, rebuilt them, combined them with Citigroup's discarded consumer lending arm, created category leadership, and sold to Apollo. Apollo provided fresh capital, installed new management, and rode the improving credit cycle to a lucrative exit. Each PE sponsor earned strong returns while leaving behind a healthier, more competitive company.

The Wall Street reception to this transformation was gradual, not instantaneous. Analysts who covered OMF in its early public life were accustomed to asking skeptical questions: "How is this different from pre-crisis subprime lending?" "What happens when the next recession hits?" "Why should investors own a company with 25%+ APRs on its loans?" Over time, management answered these questions not with promises but with results: consistent capital generation, improving portfolio quality, rising dividends, and transparent communication about credit trends. By 2020, the analyst consensus had shifted from "this might work" to "this works, but we worry about cycles." That is exactly the kind of grudging respect that long-term value investors should find encouraging.

VIII. The Modern Playbook: How OneMain Actually Works

Understanding OneMain requires understanding what happens inside those 1,300 branches, because the branch model is simultaneously the company's greatest competitive advantage and the feature that most confuses growth-oriented investors.

The typical OneMain customer has a FICO score somewhere between 580 and 650. She might be a nurse, a truck driver, a retail manager—someone with a steady job and a spotty credit history. Perhaps she went through a divorce, had a medical emergency, or simply mismanaged credit cards in her twenties. She needs $5,000 to consolidate high-interest debt, or $3,000 for a car repair, or $8,000 for home improvement. Her bank has declined her. Credit card companies reject her or offer predatory rates. Payday lenders will give her $500 at an effective APR exceeding 400%. OneMain offers her a structured installment loan at 18-35% APR, with fixed monthly payments over 24 to 60 months, often secured by the title to her vehicle.

The underwriting process is where OneMain's century-plus of institutional knowledge becomes tangible. The company employs a hybrid model combining algorithmic credit scoring with human judgment. Proprietary statistical models and machine learning assess creditworthiness using traditional credit bureau data supplemented by alternative signals: utility payment history, banking behavior, employment stability, and other non-traditional indicators. But the algorithm does not make the final decision alone. A branch-level loan officer reviews every application, often conducting a face-to-face or phone conversation with the borrower to evaluate what data scientists cannot easily quantify: character, stability, and genuine willingness to repay.

This human overlay is not sentimental; it is economically rational. In subprime lending, the difference between a borrower who will stretch to make payments and one who will default at the first inconvenience is often invisible to algorithms but apparent to experienced loan officers. Think of it like medical diagnosis: the best outcomes come not from AI or doctors in isolation, but from AI-augmented doctors. OneMain applies the same principle to credit decisions.

The loan portfolio has evolved significantly under Shulman's leadership into a multi-product platform. Personal loans remain the core, with amounts ranging from $1,500 to $20,000 over terms of 24 to 60 months. Auto finance has grown substantially since the April 2024 acquisition of Foursight Capital from Jefferies Financial Group for $115 million, bringing approximately $900 million in near-prime auto loan receivables and opening an indirect lending channel through franchise dealerships. By the end of 2025, auto finance receivables had reached $2.8 billion, supplemented by the Ally Financial ClearPass program now active in approximately 1,700 dealerships.

The BrightWay credit card, issued through WebBank, serves as both a customer acquisition tool and a credit-building product for non-prime borrowers. It offers unlimited 1% cash back on purchases and a "Milestone Benefits Program" rewarding six consecutive on-time payments with either a lower APR or higher credit limit. This clever incentive structure aligns OneMain's interests with the borrower's credit improvement. By end of 2025, BrightWay had $936 million in receivables across approximately 1.1 million accounts, though the card portfolio carries a net charge-off rate of 17.1%, nearly triple the personal loan book.

Collections deserve special attention. OneMain's approach is distinctive: loans are serviced in-branch by the same loan officers who originated them until 60 days past due. The customer knows the person calling about their late payment. The loan officer understands the customer's circumstances and can offer modified payment plans before accounts deteriorate further. Only after 60 days do accounts transfer to specialized centralized collections operations. The model is largely in-house and onshore, which costs more than outsourcing but produces materially better recovery rates. In the fourth quarter of 2025, recoveries reached $89 million, up 16% year-over-year.

The funding model merits explanation for investors unfamiliar with non-bank lending, because it is both the enabler of OneMain's business and a potential vulnerability. Unlike a bank that takes deposits from customers and lends them out—getting its raw material essentially for free—OneMain must borrow every dollar it lends from wholesale capital markets. It does this through three main channels.

First, securitization: OneMain packages pools of consumer loans into asset-backed securities and sells them to institutional investors. Think of it as a factory that turns individual loans into bonds. The OMFIT trust platform has executed 27-plus consumer loan securitizations since 2013, building deep relationships with pension funds, insurance companies, and asset managers who buy these bonds. Second, warehouse revolving facilities: credit lines from large banks that provide short-term funding for loans before they are packaged into securitizations—essentially a working capital facility. OneMain had $6.4 billion of committed undrawn capacity under these facilities. Third, senior unsecured notes: corporate bonds that OneMain sells directly to investors, most recently a $1 billion offering in the fourth quarter of 2025.

Total debt stood at $23 billion at end of 2025, with more than 90% of expected average debt for 2026 already locked in at fixed rates. This is a crucial risk management decision: by fixing its funding costs in advance, OneMain converts interest rate uncertainty into a known expense, protecting margins even if rates move sharply. The company intentionally reduced its secured debt ratio from 59% to 50%, trading some cost efficiency for greater financial flexibility—a signal that management prioritizes balance sheet resilience over marginal cost savings.

The capital allocation philosophy has been shareholder-friendly. OneMain has increased its quarterly dividend for six consecutive years, reaching $1.05 per share. The annualized dividend of approximately $4.20 per share yields roughly 7-8% at recent prices, placing OneMain among the highest-yielding stocks in the financial sector. On top of dividends, the board authorized a $1 billion share repurchase program in October 2025, extending through December 2028, following completion of a prior program that retired approximately 9 million shares for $371 million. In total, the company generated $913 million in capital in 2025, up from $685 million in 2024—a strong indicator of the business's cash-generating capability.

IX. COVID-19: The Unexpected Stress Test

When the pandemic hit in March 2020, OneMain's stock cratered to $12.21 on March 18, down from $38 just weeks earlier. The market's logic was straightforward: a subprime lender heading into the worst economic contraction since the Depression would be annihilated. If ordinary Americans were about to lose their jobs en masse, surely the Americans with the worst credit scores would default first and hardest. It was a reasonable fear.

What actually happened was one of the great surprises in recent financial history. OneMain tightened underwriting immediately, offered one-month reduced or deferred payments to affected borrowers, waived late fees through April 2020, and suspended negative credit bureau reporting for newly delinquent accounts. The company donated $1 million to pandemic relief efforts and transitioned its workforce to remote operations where possible while keeping branches open with safety protocols. Management prepared for the worst.

The worst never came. Government stimulus payments, enhanced unemployment benefits, and the CARES Act student loan pause flooded cash into exactly the households that OneMain serves. Subprime borrowers, who had been living paycheck to paycheck, suddenly had thousands of dollars in government support flowing into their bank accounts. Many used the money to pay down debt, including their OneMain loans.

Charge-offs, rather than spiking, actually declined. Net charge-off rates fell to approximately 4.2% in both 2020 and 2021, well below the historical average. In 2021, OneMain posted record net income of approximately $1.3 billion and earnings per share of $9.87, driven by historically low losses and strong origination volumes.

According to the CFPB, 43% of consumers with subprime credit scores moved up at least one credit tier during the pandemic, compared to just 37% in the preceding decade. The share of borrowers with subprime scores fell from roughly 23% to 18%. For OneMain, this temporarily shrank the addressable market as former subprime borrowers graduated to prime products.

But the grade inflation was exactly that: inflation. Many consumers who improved their credit scores did so through temporary government support, not genuine improvement in financial behavior. As stimulus effects faded and student loan payments resumed, subprime credit scores began reverting. By the third quarter of 2025, the share of consumers taking on subprime loans had risen to 14.4%, the highest since 2019, and subprime originations were growing at 32.5% year-over-year.

The post-pandemic credit normalization brought real pain. As government support programs expired, many borrowers who had been artificially propped up began to struggle. OneMain's net charge-off rate climbed from 4.2% in 2021 to roughly 6.9% in 2022, then 7.4% in 2023, peaking at 7.9% in 2024—above the pre-pandemic baseline of roughly 5.7% in 2019.

Net income declined from the 2021 peak of $1.3 billion to $878 million in 2022, then $641 million in 2023, bottoming at $509 million in 2024 with diluted EPS of just $4.24. The stock price, which had peaked above $52 during the stimulus-fueled euphoria, retreated as investors repriced the credit outlook. The bear case felt vindicated: subprime lending is inherently cyclical, and the good times were over.

But by 2025, the story was improving. Net income recovered to $783 million, a 54% increase, as the front book of tighter-underwritten loans began dominating the portfolio. Adjusted EPS of $6.66 grew 36% year-over-year. Critically, OneMain's "front book" loans—those originated under post-pandemic tightened standards—now comprise 90% of the portfolio and account for only 24% of delinquent receivables, down from 32% a year earlier. This vintage composition shift is the most important data point in the 2025 results, because it demonstrates that the current underwriting engine is producing measurably better loans than the pandemic-era vintage. As the remaining back book rolls off, overall credit quality should continue to improve.

The COVID episode demonstrated both the cyclical vulnerability of subprime lending and the business model's ultimate resilience. The government stimulus cushion means the test was not as severe as a traditional recession without fiscal intervention—a distinction that matters for forward-looking risk assessment. A conventional recession, with unemployment rising to 8-10% and no trillion-dollar stimulus packages, would be a more revealing test of OneMain's underwriting and collections capabilities.

But the stock tells its own story. From the March 2020 low of $12.21 to the all-time high of $71.93 in January 2026, investors who bought during the panic earned a nearly 6x return, plus dividends. That trajectory—from existential fear to record valuation—captures the essential risk-reward dynamic of investing in subprime consumer lending: the downside is terrifying but temporary, and the recovery, for a well-managed company with a durable business model, is dramatic.

X. The Competition and Industry Dynamics

OneMain's competitive position is best understood by examining who else operates in non-prime consumer lending and why none of them currently pose an existential threat.

The branch-based competitors are familiar names within the industry but dramatically smaller. Regional Management Corp., publicly traded under the ticker RM, operates about 350 branches in 19 states with roughly $2.1 billion in finance receivables—approximately one-twelfth of OneMain's portfolio. World Acceptance Corporation has approximately 1,000 branches but focuses on smaller-dollar loans and carries significant regulatory baggage: a 2020 SEC settlement of $21.7 million for Foreign Corrupt Practices Act violations, and a 2023 CFPB order establishing supervisory authority over the company. Mariner Finance, owned by Warburg Pincus, operates 480-plus branches with over $2 billion in loans, but faces a multistate lawsuit from 11 state attorneys general alleging predatory lending practices.

The broader trend favoring OneMain is that banks continue retreating from subprime. Post-Dodd-Frank capital requirements make small-dollar, high-risk lending uneconomical for bank holding companies. A bank must hold substantially more regulatory capital against a subprime loan than a prime loan, making the return on capital unattractive. The reputational costs are enormous, and the compliance burden is crushing. Every year that banks stay out of subprime is another year that OneMain's competitive position strengthens by default.

Fintech challengers represent the most intellectually interesting competitive threat, but real-world results have been underwhelming. The cautionary tale is LendUp, which launched in 2012 with backing from Google Ventures, Andreessen Horowitz, and Kleiner Perkins. LendUp promised borrowers could "climb the LendUp Ladder" to lower rates. But the CFPB found that tens of thousands of borrowers who climbed were actually offered similar or higher rates. The agency fined LendUp $3.63 million in 2016 and shut the company down entirely in 2021 for continued violations. It liquidated by 2022.

OppFi, one of the surviving subprime fintechs, has achieved profitability, but its net charge-off rate of 45.5% of revenue in the fourth quarter of 2025 illustrates the challenge of digital-only subprime lending without relationship infrastructure. LendingClub, often cited as a fintech disruptor, has moved away from subprime entirely, shifting toward prime borrowers with an average FICO around 730 after acquiring Radius Bank in 2021.

The credit card space presents a different kind of competitive dynamic. Major issuers like Capital One and Discover serve some of the same credit tiers as OneMain, but credit cards and installment loans are fundamentally different products serving different needs. A credit card is a revolving line of credit designed for ongoing transactions; an installment loan is a lump sum with a fixed repayment schedule designed for debt consolidation, major expenses, or emergency needs. Many of OneMain's customers carry credit cards but turn to installment loans when they need a larger sum than their card limit allows, or when they want to consolidate multiple card balances into a single, predictable monthly payment.

The payday lending industry, while operating at the bottom of the consumer credit market, represents what OneMain's customers are trying to avoid. Payday loans are typically $500 or less, carry effective APRs of 300-400%, and must be repaid in full within two weeks—a structure that frequently traps borrowers in renewal cycles. The Pew Charitable Trusts estimated that the average payday borrower pays $520 in fees annually to repeatedly borrow $375. OneMain's installment model, with monthly payments spread over years and APRs capped at 36% in most states, represents a fundamentally different value proposition despite the superficial similarity of serving non-prime borrowers.

The fundamental insight is that subprime lending is not a technology problem; it is a trust and relationship problem. Non-prime borrowers need human interaction to build trust, understand loan terms, and maintain payment discipline. The impersonal nature of digital interactions works against lender retention and collections effectiveness. OneMain's omnichannel approach—allowing customers to start online and finish in a branch, or vice versa—represents a more durable competitive strategy than pure digital models have so far demonstrated.

XI. Porter's Five Forces Analysis

Threat of New Entrants: LOW. The barriers to entering non-prime consumer lending at scale are formidable. State licenses in 44 jurisdictions took OneMain decades to accumulate. A new entrant applying today faces years of paperwork, legal fees, and regulatory examinations before opening a single branch. The capital requirements are substantial—OneMain carries $23 billion in debt to fund its $26 billion portfolio. Building branch infrastructure requires massive upfront investment with slow payback. And developing proprietary underwriting models requires credit performance data that only comes from years of actual lending. Fintech disruption has been limited by the need for human touch in subprime; algorithms alone cannot replicate the judgment of experienced loan officers who read borrowers' character and circumstances.

Bargaining Power of Suppliers: LOW. OneMain's primary "supplier" is the capital markets. With diverse funding sources spanning securitization, warehouse facilities, and senior unsecured notes, the company faces no dependency on any single capital provider. The 27-plus securitization deals since 2013 have built deep institutional investor relationships. Over 90% of expected 2026 debt is already at fixed rates. No unique inputs or proprietary technology from third parties create supplier leverage.

Bargaining Power of Buyers: MEDIUM-HIGH. This is the one force that works against OneMain. Customers do have alternatives: credit cards (though many do not qualify), other installment lenders (though smaller and fewer), payday lenders (though terms are far worse), and family or friends. Non-prime borrowers are price-sensitive and increasingly able to comparison-shop online. However, switching costs are real: refinancing requires a new application, new underwriting, and disruption of an established payment relationship. The fact that roughly 40% of OneMain's new originations come from existing customers suggests meaningful stickiness.

Threat of Substitutes: MEDIUM. Credit cards, payday loans, buy-now-pay-later products, and informal lending from family or friends all serve some of the same customer needs. But each substitute has significant limitations for OneMain's core customer. Credit cards require higher credit scores than most OneMain borrowers possess. Payday loans offer much worse terms and smaller dollar amounts. BNPL products are designed for retail purchases, not debt consolidation or car repairs. Bank re-entry into subprime remains unlikely given regulatory and reputational pressures.

Competitive Rivalry: LOW-MEDIUM. The industry is fragmented, and OneMain has two to three times the scale of its nearest branch-based competitor. Competitors tend to be rational, focused on profitability rather than market share wars. There is no Amazon or Walmart of consumer lending waging price wars to gain share. Regional players operate in limited geographies and do not threaten OneMain's national footprint. No competitor has both the scale and the national presence to challenge OneMain's position as the industry standard-bearer. The competitive dynamic is closer to regional utilities than to technology platforms—stable, predictable, and focused on returns rather than growth at any cost.

Overall Assessment: The industry structure is attractive for the incumbent leader. High barriers to entry, low supplier power, and limited competitive rivalry create a protected operating environment. The main risks come from buyer bargaining power and substitute products, but these are manageable given the structural limitations of alternatives for non-prime borrowers. This is not the kind of industry where a startup in a garage can disrupt the leader. It is the kind of industry where the leader's advantages compound over time, making its position more defensible with each passing year.

XII. Hamilton's Seven Powers Analysis

Scale Economies: STRONG. OneMain's 1,300-plus branches provide operating leverage that no competitor can match. Technology, compliance, and corporate overhead costs are spread across $26 billion in managed receivables. Funding advantages compound the scale benefit: OneMain's securitization program commands better terms than smaller issuers can achieve. The operating expense ratio of 6.7% of average managed receivables continues declining as receivables grow faster than costs.

Network Effects: WEAK. OneMain is not a platform business. The value of its service to any individual customer does not increase because other customers use it. There is no marketplace dynamic, no user-generated content advantage, no data network effect of the type that powers technology platforms. This is a straightforward limitation, not a flaw in the business model.

Counter-Positioning: MODERATE. Banks cannot profitably compete in non-prime lending due to regulatory capital requirements, compliance costs, and reputational risk. The math simply does not work within a bank holding company structure. Fintechs struggle with the economics of subprime collections and customer retention without physical presence. But these barriers are structural rather than permanent. A regulatory change making subprime lending more attractive for banks, or a technological breakthrough enabling effective digital collections, could erode this advantage.

Switching Costs: MODERATE. Once a customer has established a relationship and payment history with OneMain, refinancing elsewhere involves real friction. Existing customers representing roughly 40% of originations validates this stickiness. But subprime borrowers do shop around, particularly for rate improvements, so switching costs are not insurmountable.

Branding: MODERATE. OneMain has recognition within its target demographic, and trust matters enormously for financial services to vulnerable populations. But this is not a premium brand with pricing power. It is a known, reliable entity in a market where many alternatives are unknown or untrustworthy.

Cornered Resource: STRONG. This is OneMain's secret weapon. Regulatory licenses in 44 states represent decades of accumulated compliance capital. A century of credit performance data provides underwriting advantages that cannot be purchased. Branch locations in optimal neighborhoods were selected over generations. Institutional knowledge of state-by-state regulations creates compliance capabilities that function as intellectual property. These resources cannot be replicated quickly by any competitor, regardless of their financial resources.

Process Power: STRONG. The proprietary underwriting model combining algorithmic scoring with human judgment, the collections operation balancing empathy and effectiveness, the branch operations playbook refined over decades—these are embedded organizational processes that competitors cannot easily observe, let alone replicate. Process power is often the most durable competitive advantage because it resides in organizational culture and accumulated expertise rather than in assets that can be purchased.

Overall Assessment: OneMain possesses three to four strong competitive powers (Scale Economies, Cornered Resource, Process Power, and moderate Counter-Positioning), making it a durable business in an attractive industry structure. The absence of strong network effects and the moderate switching costs mean this is not an invincible franchise, but it is a defensible one that becomes stronger with each year of operation. For comparison, consider what would happen if a well-funded competitor—say, a major bank or a Silicon Valley fintech with $5 billion in capital—tried to replicate OneMain from scratch. They would need to obtain licenses in 44 states (3-5 years), build or lease 1,300 branch locations (2-3 years minimum), hire and train thousands of loan officers (1-2 years), build underwriting models without any credit performance data (impossible without actual lending history), and establish securitization relationships with institutional investors (multiple years of track record required). The total timeline to replicate OneMain's competitive position is measured in decades, not years. That is the definition of a durable moat.

XIII. The Bull vs. Bear Case

The Bull Case rests on structural market dynamics and proven execution. Approximately 30% of Americans are non-prime, representing a massive and persistent addressable market. Banks continue retreating from subprime, widening OneMain's moat each year. The business model has been tested through the 2008 crisis, the pandemic, and post-stimulus normalization, surviving each with its infrastructure intact.

Return on equity consistently runs above 20%, driven by the spread between a 22.5% portfolio yield and funding costs roughly half that level. Capital returns are substantial: a quarterly dividend of $1.05 per share yields approximately 7-8% annually, supplemented by a $1 billion share repurchase program authorized through December 2028. The stock typically trades at 8-11 times earnings, a meaningful discount to the broader market.

Management execution under Shulman has been strong. Full-year 2025 revenue reached approximately $6.2 billion. Capital generation hit $913 million. The product portfolio expanded into auto finance and credit cards without losing underwriting discipline. These are not speculative bets but adjacencies built on existing infrastructure.

The myth-versus-reality check on the bull case is important. The myth is that OneMain is "recession-proof" because subprime borrowers always need credit. The reality is more nuanced: demand is persistent through cycles, but the ability to lend profitably deteriorates during severe downturns as charge-offs spike. OneMain is recession-resistant in demand terms but cyclically exposed in credit quality terms.

The Bear Case should not be dismissed. Regulatory risk is existential and binary. The CFPB's May 2023 consent order, requiring $20 million in payments for deceptive add-on product sales to roughly 25,000 customers, demonstrated that OneMain is not immune to enforcement actions. The CFPB found that employees used high-pressure tactics to upsell credit insurance products, misrepresenting that add-ons were required to receive a loan. A more aggressive CFPB, or state-level APR caps, could compress margins or eliminate entire product categories.

Credit quality deterioration in a severe recession remains the fundamental risk. The net charge-off rate of 7.7% in 2025 already runs above the pre-pandemic baseline. Government stimulus during COVID cushioned the blow; a traditional recession without massive fiscal intervention would be a more revealing test. Any sustained move in net charge-offs above 10% would pressure earnings materially and could force dividend cuts.

The branch model carries long-term structural risk. Each branch incurs fixed costs for rent, staffing, and maintenance. If digital-only models eventually crack the subprime code, the branch network could shift from moat to millstone. The credit card portfolio, while growing, carries charge-off rates roughly double the personal loan book, introducing new volatility.

The New York Department of Financial Services also fined OneMain $4.25 million in 2023 for cybersecurity deficiencies—a manageable amount but a reminder that regulatory risk extends beyond lending practices.

The Reality falls between the extremes, and the honest assessment requires acknowledging the genuine uncertainty on both sides. OneMain is not a hypergrowth story, and the 2026 guidance of 6-9% managed receivables growth reflects a mature business in a slowly expanding market. But it is a high-returning, well-managed company that generates substantial free cash flow and returns it to shareholders through dividends and buybacks.

The comparison to a "cigar butt" stock—Warren Buffett's term for a company with one last good puff—does not quite fit. OneMain has been puffing for a decade and shows no signs of going out. A better analogy might be a toll bridge on the only road between two towns: not exciting, not growing rapidly, but earning steady tolls from traffic that has no alternative route. The risk is that someone builds a new road (fintech disruption), the government caps the toll (APR limits), or traffic dries up (severe recession). The opportunity is that none of those things happen, and the toll collector keeps quietly accumulating cash year after year.

The risk-reward ultimately depends on two variables: the trajectory of American consumer credit quality and the direction of the regulatory environment for non-prime lending. Investors who have a strong view on both can position accordingly. Those who do not should probably stay away, not because the company is bad, but because the sector requires conviction that most generalist investors do not possess.

XIV. Key Metrics: What to Watch

For investors monitoring OneMain's ongoing performance, two metrics matter more than all others, and they should be the first numbers checked every quarter.

Net charge-off rate as a percentage of managed receivables is the single most important number. It captures the ultimate output of underwriting quality, economic conditions, and collections effectiveness in a single figure. Think of it as the vital sign of the entire operation: it tells you whether the loans being made are performing, whether the economy is helping or hurting, and whether the collections team is doing its job.

OneMain's historical range has been roughly 4-8%, with the 2021 low reflecting pandemic-era stimulus and the 2024 high of 7.9% reflecting post-stimulus normalization. Management guided for 7.4-7.9% in 2026.

Any sustained move above 9% would signal genuine credit deterioration requiring portfolio adjustments and potential dividend cuts. Any move below 7% would signal improving economics and potential for accelerated capital returns. The number tells you more about the health of the business than revenue, earnings, or any other financial metric.

30-plus day delinquency rate is the leading indicator that previews where charge-offs are heading. If the net charge-off rate is the thermometer, the delinquency rate is the weather forecast. Delinquencies precede charge-offs by 60-120 days, making them an early warning system. At end of 2025, the 30-plus day delinquency rate stood at 5.65%, roughly flat year-over-year.

Within this number, the mix between front book and back book delinquencies is especially revealing. Front book loans accounted for only 24% of delinquent receivables at year-end 2025, down from 32% a year earlier, suggesting that current underwriting is producing better-quality loans than the pandemic-era vintage.

Together, these two metrics tell investors whether the core underwriting engine is functioning properly. Everything else—revenue growth, operating expenses, funding costs, dividend policy—is downstream of credit quality. A consumer lender can survive slow growth or elevated expenses, but it cannot survive a credit quality blowout. Get the underwriting right and the rest follows; get it wrong and nothing else matters.

One additional metric worth monitoring, though secondary to the two above, is the operating expense ratio as a percentage of average managed receivables. This number, which stood at 6.7% in 2025 with guidance for 6.6% in 2026, reveals whether OneMain is extracting operating leverage from its growing portfolio or whether cost creep is eroding the benefits of scale. A declining OpEx ratio against growing receivables is the hallmark of a well-managed consumer lender; a rising ratio would suggest that branch costs, technology investments, or regulatory compliance expenses are outpacing revenue growth.

XV. Recent Developments and Current State

OneMain enters 2026 from a position of operational strength. Full-year 2025 results showed managed receivables of $26.3 billion, up 6% year-over-year. Net income of $783 million represented a 54% increase from the prior year. Adjusted earnings per share of $6.66 grew 36%. Capital generation of $913 million exceeded the prior year's $685 million by a wide margin.

The product diversification strategy is gaining traction. Auto finance receivables reached $2.8 billion, with the Foursight Capital integration complete and technology platform migration finished during 2025. BrightWay credit card receivables of $936 million across 1.1 million accounts demonstrate the card is resonating with its target demographic. First-quarter 2025 total originations of $3.0 billion were up 20% year-over-year, partially driven by digital channel growth.

Digital transformation proceeds pragmatically rather than aspirationally—a distinction that matters. Where many financial companies have poured billions into digital transformation with unclear returns, OneMain has invested selectively in capabilities that enhance rather than replace its branch model. Customer calls per account declined 25% through digital self-service improvements, freeing branch staff to focus on origination and relationship management rather than routine servicing inquiries. The mobile app's financial wellness platform, bolstered by the 2021 acquisition of fintech startup Trim, saw a 36% increase in users during 2025. Trim's capabilities—helping customers negotiate bills, analyze spending patterns, cancel unused subscriptions, and automate savings—provide tangible value that strengthens the customer relationship beyond the loan itself.

An AI-powered internal tool launched in early 2026 gives branch and central team members faster access to internal policies and compliance guidelines, reducing the time spent navigating complex state-by-state regulations. The Pagaya Technologies partnership, announced in August 2024, applies AI-driven underwriting technology specifically to auto lending, enabling OneMain to serve qualified borrowers who might fall outside its existing credit criteria. These are measured technology bets, each tied to a specific business outcome rather than a vague "digital transformation" mandate.

The balance sheet is conservatively positioned. Over 90% of expected average debt for 2026 is locked at fixed rates. Unencumbered receivables of $11.8 billion and $1.1 billion of undrawn corporate revolver capacity provide substantial liquidity. The company increased its dividend for the sixth consecutive year, and the board authorized a new $1 billion share repurchase program in October 2025.

For 2026, management guided for 6-9% managed receivables growth, net charge-offs of 7.4-7.9%, and an operating expense ratio of approximately 6.6%. The guidance implies continued improvement in credit quality as the front book further seasons and the back book of pandemic-era loans rolls off.

Leadership stability has been a quiet advantage. Shulman has served as CEO since September 2018, providing continuity unusual in a sector where management turnover is common. His team has demonstrated discipline in capital allocation: returning cash to shareholders when credit conditions are favorable, tightening underwriting when risks emerge, and investing in product expansion only when the economics are proven. The December 2023 Investor Day laid out a multi-year strategic roadmap spanning personal loans, auto finance, and credit cards, giving investors visibility into the growth trajectory without overcommitting to aggressive targets.

The regulatory environment remains a variable. No CFPB enforcement actions have been reported since the May 2023 consent order, though broader political uncertainty around the agency's mandate persists. The Supreme Court upheld the CFPB's funding mechanism in 2024, removing one existential threat to the agency, but the direction of enforcement still depends on political appointments and the policy preferences of whichever party controls the White House.

XVI. The Bigger Picture: What OneMain Teaches Us

The OneMain story offers lessons that extend well beyond consumer finance.

The first lesson is about private equity at its best. Fortress bought damaged assets from AIG, rebuilt them, combined them with Citigroup's discarded consumer lending arm, created category leadership, and sold to Apollo. Apollo provided fresh capital, installed new management, and rode the improving credit cycle to a lucrative exit. This was not the caricature of PE that dominates popular imagination—loading companies with debt and stripping assets. This was genuine value creation through operational improvement, strategic combination, and patient capital allocation.

The second lesson is about boring businesses in stigmatized industries. Consumer subprime lending lacks the glamour of venture capital, the intellectual cachet of quantitative trading, or the cultural resonance of consumer technology. Yet OneMain has generated consistent returns on equity above 20%, pays a dividend yielding nearly 8%, and has compounded shareholder value through multiple economic cycles. The stigma creates a valuation discount that patient investors can exploit, precisely because most institutional investors are too uncomfortable to own the stock. ESG-conscious funds exclude it. Reputational risk makes it awkward for a pension fund to explain to beneficiaries. Media coverage is inevitably framed through the lens of predatory lending. All of this suppresses the multiple and creates opportunity for investors who think independently.

The third lesson is about regulatory moats. In an era when technology threatens to disrupt every industry, OneMain's most durable competitive advantages are the most old-fashioned: state licenses that take years to obtain, branch locations that take decades to optimize, and customer relationships that take generations to build. LendUp's failure, despite backing from Silicon Valley's most celebrated investors, illustrates that technology alone cannot solve the trust, compliance, and collections challenges of subprime lending.

The fourth lesson is about financial inclusion. Someone has to serve the 25 million American households that exist outside the banking mainstream. The question is not whether subprime lending should exist, but whether it can be conducted responsibly and transparently. OneMain's CFPB settlement demonstrates that even well-managed companies face constant pressure to cross ethical lines when employee incentives are poorly designed. The industry deserves both its critics and its defenders. The Americans who walk into OneMain's branches are not abstractions in a financial model; they are people with genuine needs who have been turned away by every other institution in the financial system.

XVII. The Road Ahead

Several questions will determine OneMain's trajectory over the coming years.

The most immediate is whether the current credit cycle has truly peaked. Management's 2026 guidance of 7.4-7.9% net charge-offs suggests stabilization, but a recession, tariff-driven inflation, or labor market deterioration could push losses above 9%. OneMain survived the pandemic stress test, but government stimulus provided a cushion that would not exist in a traditional downturn.

Product expansion offers both opportunity and risk. Auto finance at $2.8 billion is a natural adjacency. The BrightWay credit card at $936 million is growing rapidly but carries charge-off rates roughly double the personal loan book. How these newer products perform through a downturn will reveal whether they represent genuine diversification or incremental risk.

The fintech question remains open-ended. Today, digital-only models have not cracked subprime at scale. But technology improves relentlessly, and OneMain must avoid the trap of defending a legacy model past its expiration date.

Whether OneMain could be an acquisition target is an intriguing question that surfaces periodically in analyst reports and investor discussions. Private equity firms have demonstrated they can extract value from the business—Fortress and Apollo both generated strong returns. A large bank looking to re-enter consumer finance could acquire a turnkey platform with regulatory licenses in 44 states, a proven underwriting engine, and 1,300 branch locations that would take decades to replicate organically. An insurance company seeking diversification into predictable cash flows might find the business attractive. At a market cap around $7-8 billion, the company is large enough to be meaningful but small enough to be acquirable by any number of strategic or financial buyers.

Regulatory wildcards persist and deserve separate attention. State-level APR caps represent the most concrete threat. Several states have enacted or considered legislation capping consumer loan interest rates at 36% APR, which would compress margins on OneMain's higher-rate loans. Illinois enacted a 36% APR cap in 2021. If major states like Texas, Florida, or Pennsylvania followed suit, the impact on OneMain's revenue mix could be material. At the federal level, the CFPB's direction depends heavily on political appointments, and its enforcement priorities can shift dramatically between administrations. The agency's own funding structure faced a Supreme Court challenge, and its long-term institutional stability remains uncertain.

The question of technology's eventual disruption of branch-based lending deserves a nuanced answer rather than a binary one. The most likely outcome is not that branches disappear entirely, but that they evolve. OneMain is already moving in this direction: the Pagaya Technologies partnership announced in August 2024 uses AI-driven underwriting technology for auto lending, and the company's digital self-service investments have reduced customer calls per account by 25%. The future of the branch is probably not a place where every customer must physically visit, but rather a relationship hub that provides the human touch when it matters most—at origination, during financial difficulty, and at renewal—while routine transactions move online.

The most likely scenario is perhaps the most boring one: OneMain continues to do what it does—growing receivables at mid-single-digit rates, earning mid-twenties returns on equity, paying generous dividends, buying back shares, and gradually expanding its product suite. It will never be a momentum stock. It will never be a Silicon Valley darling. But it will continue serving the Americans that everyone else has forgotten, making money doing it, and proving that sometimes the oldest way is the right way for the right customer.

XVIII. Epilogue and Reflections

The surprising hero of this story is not a visionary founder or a celebrity CEO. It is patient capital and operational excellence—the willingness to buy unloved assets, fix them methodically, and hold them long enough for the market to recognize their value. Fortress, Apollo, and the management teams they installed did not reinvent consumer lending. They simply did the hard, unglamorous work of tightening underwriting, consolidating branches, modernizing technology, and building capital market relationships. There was no eureka moment, no paradigm shift, no disruptive innovation. Just years of grinding improvement.

What is most striking about OneMain is the tension between the necessity and the discomfort of what it does. America needs someone to lend to the nurse with a 590 FICO score who needs her car fixed to get to work. The alternative—payday lenders at 400% APR or no credit at all—is objectively worse for the borrower, the community, and the economy. Yet the service OneMain provides will never be celebrated. Every politician who rails against "predatory lenders" implicitly includes companies like OneMain, even though the Pew Charitable Trusts and the FDIC have specifically identified installment lending as the preferable alternative to payday loans.

This reputational burden is, paradoxically, one of OneMain's greatest competitive advantages. It keeps banks out. It keeps fintechs cautious. It keeps the stock price at a discount that rewards patient shareholders. And it ensures that OneMain's 1,300 branches will continue to be the places where millions of Americans access credit that no one else will extend to them.