Omnicom Group: The Big Bang and the Consolidation Endgame

I. Introduction & Episode Roadmap

On the morning of November 26, 2025 — the day before Americans sat down to Thanksgiving — a press release crossed the wire that quietly rearranged the global advertising industry. Omnicom Group Inc., trading as OMC on the New York Stock Exchange, announced it had completed its all-stock acquisition of The Interpublic Group of Companies. Two of the storied "Big Four" holding companies, rivals for four decades, had become one.1 John Wren, Omnicom's chairman and chief executive, called it "a defining moment for our company and our industry."1 Coming from a man who has spent almost thirty years avoiding hyperbole, that was as close to a victory lap as Wren gets.

The arithmetic behind the moment is staggering. The combined company generates pro forma revenue in excess of $25 billion, vaulting past the long-reigning European giants — Britain's WPP and France's Publicis Groupe — to become, on a revenue basis, the largest marketing services company on earth.1 Omnicom on its own had closed 2025 with $17.3 billion in revenue; bolting on Interpublic added roughly another eight.2 In an industry that spent the 2010s terrified of being disintermediated by Google, Meta, and Amazon, the survivors decided the answer to platform scale was to build more scale of their own.

Here is the paradox worth sitting with before we go any further. Advertising is, at its romantic core, a craft business. It is copywriters staring at blank pages, art directors arguing over kerning, account people talking a nervous client off a ledge at midnight. It is Bill Bernbach telling Volkswagen to run an ad that said "Lemon." How does an industry built on individual creative genius, local relationships, and the fragile magic of a great idea end up as a consolidated, data-plumbed, corporate oligopoly of three? That transformation — from Madison Avenue's boutique culture to a holding-company machine measured in EBITA margins and run-rate synergies — is the story of this episode.

Four themes will run through it. The first is the long migration from creative-led advertising to technology-enabled precision marketing, where the deliverable is less a clever film than a closed loop connecting a consumer's data to a measurable sale. The second is the strangest structural feature of this business: conflict management as a business model, the counterintuitive idea that a company grows by keeping its own divisions rigorously separate so it can serve Coke and Pepsi at the same time. The third is the man at the center — John Wren, the longest-tenured non-founder chief executive in the industry, whose entire late career is now a bet on making this merger work. And the fourth is the defensive-offensive scramble against the twin threats of Big Tech and generative AI, forces that could either supercharge Omnicom's margins or hollow out the labor-hour billing model the whole industry rests on.

To feel the weight of the moment, it helps to understand what an advertising holding company actually is to the global economy. These are the toll collectors of consumer capitalism. Trillions of dollars of brand spending flow through the pipes they operate — the media plans that decide where a car company's billion-dollar budget lands, the creative that shapes how a soft drink is felt rather than merely known, the data that decides which human sees which message at which second. For most of the twentieth century, that machinery was invisible to the public and enormously profitable to its operators. What the past decade did was threaten to route the money around them: Google and Meta built self-serve tools that let a marketer buy audiences directly, and the terrifying question for every holding company became whether the client still needed a middleman at all. The Interpublic merger is, at its core, the largest single answer any of them has given to that question — a bet that the response to platform power is to become an indispensable platform of one's own.

We should be clear about posture from the start. Management says the combined Omnicom will win. This piece treats that as a claim to be tested, not a conclusion to be repeated. The interesting questions are the falsifiable ones: Do the promised synergies actually reach shareholders, or do clients claw them back as lower fees? Does fusing rival cultures create a powerhouse or a civil war? And does the data stack Omnicom is assembling constitute a genuine moat, or an expensive answer to a question the technology platforms have already stopped asking? To understand any of it, we have to go back to the first Big Bang — the one in 1986.

II. The "Big Bang" of 1986 & Genesis of the Holding Company Model

Madison Avenue in the early 1980s was a nervous place. The postwar model — a great agency, a founder's name on the door, a roster of blue-chip clients kept for decades — was colliding with globalization. Clients like Procter & Gamble, IBM, and Gillette were expanding across continents and expected their agencies to follow, opening offices in Frankfurt and Tokyo and São Paulo, staffing them, and coordinating a single brand voice across dozens of markets. That kind of build-out cost money that independent agencies, structured as partnerships living quarter to quarter on client retainers, simply did not have.

Into that anxiety marched the Saatchi brothers. Charles and Maurice Saatchi had turned their London shop, Saatchi & Saatchi, into a ravenous acquisition machine, buying up agencies on both sides of the Atlantic with the explicit goal of becoming the world's largest advertising company. To the proud independents of New York, Saatchi looked like a predator — a financially engineered roll-up that might swallow them whole and strip their names for parts. The message the industry absorbed was blunt: get big, or get eaten.

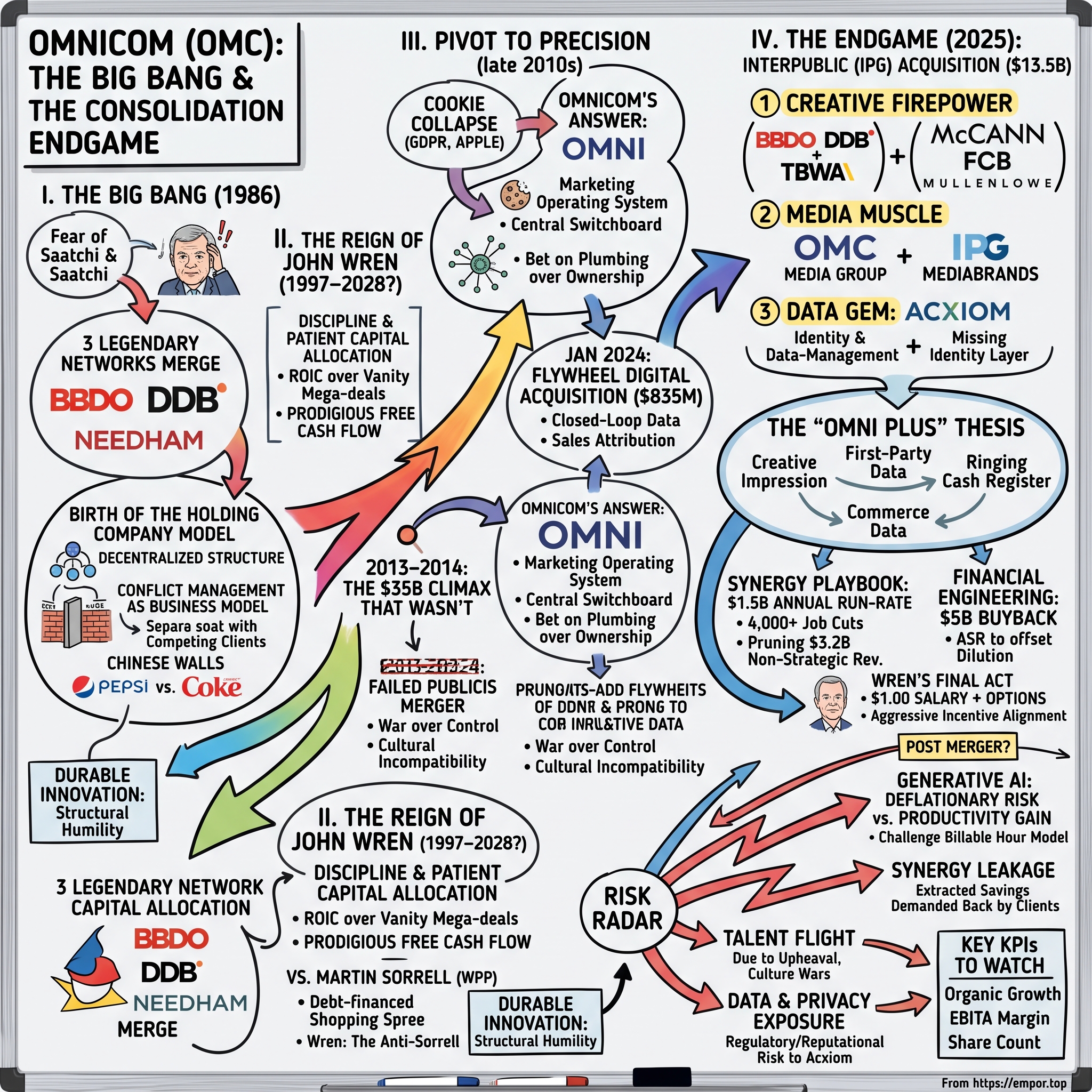

Three agencies decided to get big together. In April 1986, in what the trade press immediately dubbed the "Big Bang," Allen Rosenshine of BBDO, Keith Reinhard of Needham Harper, and the leadership of Doyle Dane Bernbach agreed to merge their three legendary networks into a single new entity called Omnicom Group. It was the largest merger the advertising business had ever seen. These were not minor shops. DDB was the house that Bill Bernbach built, the creative revolution behind Volkswagen's "Think Small" and Avis's "We Try Harder" — campaigns still taught in every advertising course as the moment the industry grew up. BBDO carried Pepsi and General Electric. Needham had McDonald's and its "You Deserve a Break Today." Combining them looked, on paper, like a recipe for chaos — and for losing clients who could not stomach sharing a corporate parent with a competitor.

The mechanics of the deal itself were as clever as the strategy. BBDO and Needham had overlapping conflicts that made a straight three-way creative merger impossible, so the architects did something subtle: they created Omnicom as a holding company and slotted BBDO and DDB Needham underneath it as separate networks, while spinning a cluster of smaller agencies into a third unit that would later become Diversified Agency Services, the home for the specialist marketing shops — direct marketing, public relations, promotional work — that clients increasingly wanted alongside their advertising. Even at birth, in other words, Omnicom was not one agency but a portfolio, deliberately structured so its parts would not collide. The third great creative network, TBWA — later fused with the West Coast wunderkind agency Chiat/Day, the shop behind Apple's "1984" Super Bowl commercial — would be folded in over the following decade, completing the triad of flagship creative brands that anchors the company to this day.

There is a useful irony in the origin story. The independents merged out of fear of a consolidator, and in doing so they built a consolidator far more durable than the one they feared. Saatchi & Saatchi, the predator that triggered the Big Bang, over-expanded, stumbled financially in the early 1990s, and was itself eventually broken up and absorbed — a cautionary tale about buying scale without the discipline to digest it. Omnicom, structured from the outset as a decentralized federation rather than a single swollen agency, survived precisely because it never tried to force its creative crown jewels into one building. That structural humility, born of a scramble to avoid being eaten, turned out to be the durable innovation.

The solution to that problem is the single most important structural idea in this entire industry, and it is worth slowing down to explain, because everything Omnicom does today descends from it. The problem is easy to state: Coca-Cola will not let its advertising be created by the same agency that handles Pepsi, because that agency would sit on both companies' launch plans, pricing strategies, and consumer secrets. Trust, in advertising, is not a soft value; it is the product. Breach it and the account walks.

Omnicom's answer was the decentralized holding company. Rather than fusing BBDO, DDB, and (later) TBWA into one mega-agency, Omnicom kept them as separate, autonomous networks — separate offices, separate leadership, separate cultures, separate client rosters, even separate rivalries. The holding company sat on top not as a creative director but as an owner and a banker. BBDO could work for PepsiCo while a sister agency worked for a competitor, and neither client had to worry, because the "Chinese walls" between the networks were real organizational walls: different buildings, different bosses, different email systems. Conflict management, in other words, became the load-bearing wall of the business model. The more autonomous the front-end agencies, the more competing giants a single holding company could quietly serve under one roof.

That produced a very particular economic shape. The creative power — the talent, the client love, the brand equity — lived downstairs in the operating agencies. The value the holding company added lived upstairs and was, frankly, unglamorous: pooled media-buying scale that let it negotiate better rates from television networks and publishers, shared back-office functions like finance, real estate, and human resources, and the balance-sheet muscle to fund international expansion and buy up specialist shops. It was, in essence, a private-equity structure wearing an advertising costume — lean corporate center, decentralized operating units, value created by aggregating purchasing power and squeezing overhead. That template, invented in 1986 out of fear of the Saatchis, is the one Omnicom would spend the next forty years refining. And the person who would refine it most relentlessly was a numbers man who joined the year of the Big Bang and never left.

III. The Reign of John Wren & The Discipline of Capital Allocation

John Wren does not look like an advertising legend. There is no Don Draper swagger, no cultivated eccentricity, no bestselling memoir. For most of his tenure he has avoided the press, skipped the industry's self-congratulatory galas, and let the numbers do the talking. Which is precisely the point: in a business full of showmen, Omnicom's defining executive is an accountant's idea of a chief executive — disciplined, patient, and almost pathologically consistent.

Wren rose through Omnicom's finance and corporate-development ranks in the years after the Big Bang, running Diversified Agency Services — the specialist-agency unit — before being named chief executive in 1997. That apprenticeship matters: he came up not through the creative side, writing headlines and winning awards, but through the machinery of buying, integrating, and financing agencies. He learned the company as a portfolio of cash flows to be allocated, which is exactly how he has run it ever since. And that start date matters too, because it means he has now steered Omnicom for nearly three decades — through the dot-com bust, the 2008 financial crisis, the mobile revolution, the pandemic, and now the largest deal of his career. He is the longest-serving non-founder chief executive in global advertising, and longevity of that kind is itself a strategy: it lets a leader compound a philosophy over enough cycles that the philosophy becomes the institution.

It is worth pausing on how unusual that tenure is in a business defined by churn. Advertising is an industry where star creatives decamp to start their own shops, where accounts move on a whim, and where the average chief marketing officer on the client side lasts only a few years. A chief executive who stays for a quarter-century accumulates something no org chart captures: relationships with the people who control the world's largest marketing budgets, cultivated over multiple economic cycles and multiple client regimes. When a global brand puts its account into review, the fact that Omnicom's leader has known its board for twenty years is not nothing. Wren's persistence is, in a real sense, part of the moat.

The clearest way to understand Wren's philosophy is by contrast with his great rival across the Atlantic, Sir Martin Sorrell of WPP. Sorrell was the industry's most public figure for thirty years — voluble, ubiquitous on business television, a serial acquirer who built WPP through a debt-financed shopping spree of trophy assets and paid himself accordingly, until governance controversies and a boardroom investigation ended his reign in 2018. Wren was the anti-Sorrell. Where Sorrell chased size and headlines, Wren chased return on invested capital. He largely avoided the vanity mega-deals that loaded WPP's balance sheet with debt and goodwill, preferring instead a steady diet of small, high-multiple "tuck-in" acquisitions: a digital shop here, a healthcare-marketing specialist there, a fast-growing regional agency somewhere else. The discipline was less about any single deal than about a refusal to overpay for scale that would dilute returns.

That capital-allocation temperament showed up in the metrics investors actually care about. Omnicom spent the 2010s throwing off prodigious free cash flow, returning most of it to shareholders through buybacks and a steadily rising dividend, and sustaining returns on equity that comfortably exceeded its cost of capital — the financial signature of a business that generates cash without needing to sink much capital back into plant and equipment. An advertising holding company owns almost no factories; its assets are people, contracts, and data, and its balance sheet reflects that asset-light reality. Wren's contribution was to run that machine without the empire-building impulse that wrecked returns elsewhere in the sector.

The mechanics of why the business is such a cash machine deserve a plain-English explanation, because they are the reason a services company can behave like a compounding financial asset. An agency collects fees from clients but also, in the media-buying business, briefly handles enormous sums of client money — paying media owners on the client's behalf and being reimbursed. Managed carefully, that working-capital cycle can actually be a source of cash rather than a drain, because the company often collects from clients around the same time it pays vendors. Combine favorable working capital with negligible capital expenditure — you do not need to build a semiconductor fab to run an ad agency, only to pay salaries and lease offices — and the result is a business that converts a high share of its operating profit into free cash flow. Wren's genius, such as it is, was recognizing that the scarce discipline in this industry was not creativity but the refusal to squander that cash on prestige acquisitions. For most of his tenure, when Omnicom could not find acquisitions that cleared its return hurdle, it simply bought back its own stock and raised the dividend — the behavior of management that treats shareholders' capital as if it were its own.

That is what makes the Interpublic era a genuine inflection, and worth watching skeptically rather than celebrating reflexively. For twenty-five years Wren was the executive who did not do the transformational deal — who watched Sorrell and Lévy swing for the fences and pointedly declined to follow. The man defined by capital discipline has now made the single largest capital-allocation decision in the company's history, an all-stock deal that dilutes the very shareholders he spent decades rewarding. A neutral observer has to sit with the tension in that: either the environment changed enough to justify abandoning a career-long stance, or a disciplined executive succumbed, late in his tenure, to the scale imperative he once resisted. The evidence for which reading is correct will accumulate over the next two years, not in any press release issued today.

Which makes his final act all the more revealing. In an amended employment agreement, Omnicom extended Wren's term as chairman and chief executive through December 31, 2028, and did something almost unheard of for a public-company chief: it cut his base salary to $1.00 a year, effective June 1, 2025.3 In place of cash, the board handed him a front-loaded grant of 4,000,000 stock options, struck at the grant-date share price and vesting over the remaining term — options that are worth nothing unless Omnicom's stock climbs from here.3 The structure valued his 2025 pay package at roughly $70 million, and it tied virtually the entire economic outcome of his last years to the one thing shareholders also care about: the share price after the Interpublic integration.4

It is a genuinely aggressive alignment of incentives — Wren's legacy and his net worth now rise and fall together with the merger's success. But independent observers were not uniformly charmed. When the package came up for an advisory vote, roughly 43% of votes cast were against it, an unusually large protest that reflected discomfort with the sheer size of the front-loaded grant and the concentration of reward in a single executive.4 Skin in the game and excessive pay are not mutually exclusive, and a neutral reading holds both thoughts at once: the incentive design is admirably pointed, and a large minority of owners thought the price of that alignment was too high. Either way, Wren has bet his own capstone on making the biggest deal in the industry's history work — which is fitting, because this is not the first time he tried to build a colossus. The first attempt was supposed to be even bigger, and it detonated.

IV. The $35B Climax That Wasn't: The Failed Publicis Merger of 2013–2014

By the summer of 2013, the mood inside the big holding companies had curdled from confidence into something closer to dread. The reason had two names: Google and Facebook. The digital platforms were vacuuming up an ever-larger share of global advertising dollars, and — worse — they dealt directly with marketers through self-serve tools that threatened to cut the agencies out of the loop entirely. For the first time, the middlemen of Madison Avenue could see a future in which they were no longer necessary. Fear, as in 1986, once again became the mother of consolidation.

So on a Sunday in July 2013, in a garden in Paris, John Wren and Maurice Lévy — the urbane, long-reigning chief of Publicis Groupe — stood together and announced something the industry could scarcely believe: Omnicom and Publicis would combine in a "merger of equals" to create Publicis Omnicom Group, a roughly $35 billion behemoth that would leapfrog WPP as the world's largest advertising company.5 The logic was defensive scale — pool the media-buying volume, pool the data, and confront Google and Facebook from a position of strength. The symbolism was extraordinary: the buttoned-down American and the elegant Frenchman, arm in arm, promising to bury a rivalry to face a common enemy.

The marriage never made it to the altar. In May 2014, after roughly ten months of mounting friction, the two companies jointly announced they were terminating the deal.5 The official language was gentle — difficulties completing the transaction "within a reasonable time frame" — but the real causes were anything but.

The first was a war over control dressed up as a merger of equals. In theory the two sides were equal partners; in practice, someone had to pick the chief financial officer, someone had to decide who would eventually be sole chief executive, and someone had to control the combined board. Wren and Lévy could not agree on any of it. Reporting at the time framed the collapse bluntly as a battle for control — Omnicom's insistence on holding the key posts ran headlong into Publicis's refusal to be, in effect, absorbed. Two proud men, two proud institutions, and no mechanism to break the tie.

The second cause was cultural, and it ran deeper than personalities. Omnicom was American corporate discipline — decentralized, numbers-driven, allergic to bureaucracy. Publicis was something else entirely: a centralized French champion with a founder's mythology and a whiff of national prestige, the kind of company the French establishment regards as strategic patrimony. Fusing them meant reconciling two incompatible theories of how a company should be run, and the theories would not reconcile. Layered on top were grinding operational problems — a plan to domicile the combined group in the Netherlands for neutrality while managing tax affairs elsewhere, and slow-grinding antitrust reviews across the United States, Europe, and China that dragged the timeline out long enough for the underlying tensions to fester. And as the uncertainty dragged on, clients grew nervous and put accounts into review; the two companies bled pitches they might otherwise have won.

The episode was also expensive in a way that never appears on a balance sheet. For ten months, the two companies' agencies had operated under a cloud of uncertainty, and clients hate uncertainty above almost all else — they responded by putting accounts into review and, in aggregate, moving substantial business elsewhere while the deal hung in limbo. The merger that was supposed to make both companies stronger left them weaker, having distracted their leadership, unsettled their people, and handed pitches to competitors, all for nothing. That is the hidden cost of a failed transformational deal in a trust business: the damage is done in the waiting, whether or not the deal ever closes. It is a lesson that should make any investor watch the pace of the Interpublic integration closely, because a slow, messy combination inflicts the same wound even when the deal is legally done.

No breakup fees changed hands — the deal simply dissolved.5 But the two sides drew opposite lessons, and the divergence is instructive. Lévy took Publicis on an aggressive data-acquisition tear, buying the digital consultancy Sapient for roughly $3.7 billion in 2015 and, more consequentially, the data-marketing firm Epsilon for about $4.4 billion in 2019 — purchases that would make Publicis the growth leader of the sector by the early 2020s. Omnicom went the other way. Chastened by the near-death experience of a transformational merger, Wren doubled down on building rather than buying the transformation, pouring resources into an internal technology platform called Omni. It was a quieter bet, and for a while a lonelier one. Whether it was the right one depended on a wave that was just beginning to break over the entire industry: the collapse of the very data infrastructure agencies had relied on for a generation.

V. Pivot to Precision: "Omni" and the $835M Flywheel Digital Acquisition

For twenty years, the invisible engine of digital advertising was a humble piece of code called the third-party cookie — a little file that followed you around the web, letting advertisers know that the person reading a car review yesterday was the same person browsing a travel site today. On that foundation the entire apparatus of digital targeting was built. And in the late 2010s, regulators and platform owners began, methodically, to tear it down.

Europe's GDPR and California's CCPA gave consumers legal rights over their data. Then Apple delivered the sharper blow: its App Tracking Transparency framework forced apps to ask users, in plain language, whether they wanted to be tracked — and the overwhelming majority said no. Google announced it would phase out third-party cookies in Chrome. Almost overnight, the tracking methods agencies had leaned on for a generation were being deprecated. For an industry whose pitch to clients was "we can find your customer," the ground was disappearing beneath its feet.

Omnicom's response was Omni. It helps to be concrete about what Omni actually is, because "marketing operating system" is the kind of phrase that means everything and nothing. Think of Omni as a central switchboard and control room for a client's marketing. Into it flow three kinds of information: anonymized data about how consumers behave, the client's own first-party data about its customers (who bought what, who churned, who opened the emails), and live information about available advertising inventory across media. Omni's job is to connect those streams — to identify an audience, decide where to reach it, orchestrate the creative and the media buy, and then measure what happened. Crucially, Omnicom chose to build the platform that links and activates data rather than to buy a giant proprietary database of its own, the path Publicis took with Epsilon. It was a bet on plumbing over ownership — on being the system that makes everyone's data useful rather than the owner of one big pile of it.

The problem with plumbing is that it needs something valuable flowing through it. And by the early 2020s, the most valuable stream in marketing was moving to a place Omni could not fully see: the retail media network. This is one of the most important shifts in modern advertising, so here is the plain-English version. When you search for a product on Amazon, Walmart's site, or Instacart and see a "sponsored" result at the top, that is retail media — an ad sold by the retailer, placed at the exact moment of purchase, right next to the "add to cart" button. It is the bottom of the funnel, where intent converts to sales, and it comes with something television advertising never could: proof. The retailer knows whether the ad led to a purchase, because it rings up the sale. Advertising dollars stampeded toward that certainty, away from the fuzzy, top-of-funnel brand-awareness spending that agencies had historically brokered.

To plug into that world, Omnicom made the largest acquisition in its history to that point. In October 2023 it agreed to buy Flywheel Digital, the digital-commerce arm of Britain's Ascential plc, for a net cash price of about $835 million, closing the deal on January 2, 2024.67 Flywheel was not a creative agency; it was a data-and-execution engine that helped brands sell across more than 400 digital marketplaces — Amazon, Walmart, and China's 阿里巴巴 Alibaba among them — optimizing product listings, pricing, and advertising against real-time sales results.7 Wren called Flywheel's tools "a game changer" for clients whose demand for retail-media solutions "continues to grow," and framed the strategic logic as building "end-to-end services" spanning brand and retail media, digital and in-store commerce.7

There is a second-order reason retail media matters so much to a holding company, beyond the measurement it offers, and it cuts against the incumbents. For a century, agencies made money brokering the scarce resource of attention — thirty-second slots on prime-time television, full pages in magazines, the billboard on the good corner. Retail media inverts that. The inventory is effectively infinite (every search result, every product page), the buying is automated, and the retailer, not the agency, owns the relationship with the shopper and the data. An agency that does not plug into that world does not just miss a growth category; it risks being disintermediated in the fastest-growing part of its own market. Buying Flywheel was, in that sense, as much defensive as offensive — a way to remain relevant to clients whose spending was migrating to a channel where the traditional agency added little value.

Strip away the executive gloss and the rationale is genuinely material to the investment case. What Flywheel gave Omnicom was closed-loop data — the actual transaction records showing which advertising drove which sales. Feed that back into Omni's targeting engines and you can, for the first time, prove to a brand that a dollar of media spend produced a dollar of shelf movement. In a world where clients increasingly refuse to pay for advertising they cannot measure, the ability to demonstrate sales attribution is the difference between a commodity service and a defensible one. Whether that constitutes a durable moat is a question we will stress-test later; platforms like Amazon sit on far richer transaction data than any agency ever will. But Flywheel gave Omnicom a credible seat at the table. It was, in retrospect, the second move in a three-move game — data platform, then commerce data, and then, once the machine was built, the scale acquisition that would run everyone else's accounts through it.

VI. The 2025 Endgame: The $13.5 Billion IPG Acquisition

By 2024, the competitive picture inside the Big Four had become uncomfortable for Omnicom. Publicis, propelled by the Epsilon data engine Lévy had bought after the failed 2014 merger, was posting the strongest organic growth and margins in the peer group — the belle of the sector. WPP, still digesting Sorrell's sprawling empire, was struggling under the weight of legacy creative agencies losing relevance. Omnicom was healthy but not spectacular, growing in the low-to-mid single digits, disciplined as ever, and increasingly aware that discipline alone would not close the gap with a data-rich rival that was pulling ahead. It needed a move that changed the board.

The move was Interpublic. In December 2024, Omnicom and IPG announced they would combine in an all-stock transaction, and after nearly a year of regulatory review — including clearance from the European Commission in November 2025 — the deal closed on November 26, 2025 at a value of approximately $13.5 billion.18 The mechanics were straightforward for an all-stock merger: each Interpublic share converted into 0.344 Omnicom shares, leaving legacy Omnicom holders with about 60.6% of the combined company and former IPG holders with about 39.4% on a fully diluted basis.1 Omnicom was clearly the acquirer, but it was paying entirely in its own equity — a choice that mattered enormously, because it meant issuing a mountain of new shares that would dilute existing owners, a problem we will see management scramble to reverse.

The contrast with 2014 is the whole point. Where the Publicis deal was a "merger of equals" that foundered on the question of who was really in charge, the Interpublic deal was structured from the first press release as an acquisition with an unambiguous acquirer, an unambiguous ownership majority, and an unambiguous chief executive: John Wren. There was no co-CEO fudge, no rotating chairmanship, no neutral tax domicile in a third country to placate wounded national pride — Interpublic is an American company bought by an American company, headquartered in New York, run by the buyer's management. The lesson of the failed French marriage had been absorbed and engineered out. Governance clarity is unglamorous, but it is precisely the variable that killed the last attempt, and getting it right this time is arguably Wren's single most important structural decision.

The regulatory path was its own quiet drama. Combining the industry's largest media-buying operations invited scrutiny from antitrust authorities on three continents, exactly as the Publicis deal had — and this time the platforms whose ad inventory Omnicom buys, and the clients whose accounts it holds, both had reasons to watch closely. That the European Commission cleared the transaction in November 2025 without the kind of protracted, remedy-laden review that can strangle a deal was a meaningful de-risking event, and it is why the closing followed within days.8 Regulators concluded, in effect, that even a combined Omnicom-IPG remained one buyer among several facing enormous, well-capitalized sellers in Google, Meta, and Amazon — a revealing judgment about who actually holds power in the modern advertising value chain.

What did that $13.5 billion in stock actually buy? Three things. The first was creative firepower: Interpublic brought McCann Worldgroup, FCB, and MullenLowe to sit alongside Omnicom's BBDO, DDB, and TBWA — one roof now sheltering an unprecedented concentration of the industry's most storied creative names. The second was media muscle: IPG's Mediabrands, with buying networks Initiative and UM, joined Omnicom Media Group's OMD, PHD, and Hearts & Science, combining two of the largest media-buying operations in the world into a single negotiating bloc facing the platforms.

But the third asset was the one that actually explains the deal, and it is not a creative agency at all. It is Acxiom — the first-party identity and data-management business that Interpublic had bought in 2018 for about $2.3 billion. Acxiom is, in effect, one of the most comprehensive consumer-data infrastructures in American marketing: a system for organizing who people are, what they do, and how to reach them without violating privacy rules, built on data a brand owns rather than on the third-party cookies that were being killed off. If Omni was the switchboard and Flywheel was the sales-proof engine, Acxiom was the missing identity layer — the connective tissue that resolves a scattered set of signals into a single, addressable human being.

Management's thesis is that fusing these three — Acxiom's identity graph, Omni's orchestration, and Flywheel's commerce data — creates something it has branded "Omni Plus": a single closed-loop system that can follow a consumer from the first creative impression all the way to the ringing cash register, and measure every step. In principle, that is the holy grail the whole industry has chased since the cookie began to crumble: creative, media, identity, and transaction data unified in one operating system. In practice, the phrase "Omni Plus" is doing a lot of work for a system that, as of mid-2026, has existed for barely half a year. The strategic logic of the assembly is coherent and, on paper, formidable. Whether Omnicom can actually integrate three complex technology stacks — each built by a different company with a different data model — into one working platform, while simultaneously firing thousands of people, is an execution question, not a strategy question. And execution is where the next chapter lives.

VII. The Post-Merger Reality: Synergy Playbook, Restructuring, and the $5B Buyback

The clock started ticking the moment the deal closed. When Omnicom first pitched the Interpublic merger to investors in late 2024, it promised $750 million in annual cost synergies — a respectable but unremarkable number. Then, reporting its fourth-quarter and full-year 2025 results, management did something that immediately reframed the deal: it doubled the target to $1.5 billion in annual run-rate synergies, to be achieved over roughly 30 months, with $900 million of that targeted for 2026 alone.2 On the Q1 2026 earnings call in April, Wren reaffirmed the doubled figure and walked analysts through the ramp.9 Doubling a synergy target within months of closing is a double-edged signal. Read charitably, it means integration is going better and faster than underwriting assumed. Read skeptically, it raises the question of why the original number was so conservative — and whether the new number is a genuine finding or a promise made to a market that was demanding one.

Where does $1.5 billion actually come from? Roughly $1 billion is labor — the elimination of duplicative corporate, administrative, and regional network functions that exist twice over in two merged companies.29 Translated into human terms, Omnicom announced about 4,000 job cuts in December 2025, immediately after closing, with the labor savings scheduled to ramp across the following two years.2 The remainder comes from the unglamorous back office: consolidating the co-located agency offices that two rivals kept blocks apart in New York, London, Chicago, and San Francisco, and centralizing procurement, software licenses, cloud hosting, and IT infrastructure across the combined group. It is the decentralized-front-end, centralized-back-end model of 1986 applied with a chainsaw — keep the creative brands, gut the duplicated plumbing.

Alongside the cuts came a portfolio purge. Management set out to shed agencies it deemed non-strategic or chronically underperforming, initially framing the target as roughly $2.5 billion in annual revenue to be sold or exited. By the Q1 2026 call that figure had climbed to about $3.2 billion, with roughly $1 billion of revenue already disposed of in the first quarter and more than 20 agency brands sunset or merged to simplify the client-facing lineup.9 The willingness to raise the exit target is a tell about how much overlapping, low-margin business the merger actually surfaced — and a reminder that a chunk of the combined "$25 billion" revenue headline is being deliberately amputated. Notably, management acknowledged on the call that the margins of the businesses being disposed of were lower than the 10% it had first guided, which is both a candid disclosure and a sign that the clean-up is messier than the initial pitch implied.9

Then there was the dilution problem to solve. Paying for Interpublic entirely in stock meant flooding the market with new shares; left unaddressed, that would depress earnings per share for years and blunt the whole rationale of the deal. So in February 2026 the board authorized a $5 billion share-repurchase program, front-loaded with an immediate $2.5 billion Accelerated Share Repurchase.2 An accelerated repurchase is financial engineering with a purpose: rather than dribbling buybacks into the market over months, the company hands an investment bank a lump sum and receives most of the shares back almost immediately, rapidly shrinking the count. By the Q1 2026 call, Omnicom had already repurchased about $2.8 billion of stock, including the $2.5 billion ASR, and guided to an 11%–12% reduction in weighted-average shares outstanding by year-end — more aggressive than the 7%–8% it had first floated.9

The accelerated repurchase deserves one more skeptical note, because it sits at the heart of how the deal will be judged. A buyback that offsets dilution is not the same as a buyback that creates value. When a company issues shares to buy a business and then borrows or spends cash to buy those shares back, it has, in economic substance, partly funded an all-stock deal with debt and cash after the fact — trading balance-sheet strength for a flattering share count. That can be entirely rational if the shares are cheap and the acquired cash flows are real, and Omnicom's stock jumped sharply on the announcements, suggesting the market approved.2 But it also means the headline "11%–12% share-count reduction" is not free money; it is a financing choice with a cost, and the per-share growth it manufactures should be read alongside what is happening to net debt and to the operating business, not in isolation. Management is doing exactly what a shareholder-focused board should do to neutralize dilution. Whether it is value-creating rather than merely EPS-flattering depends entirely on the operating results the engineering is designed to showcase.

The honest way to read this whole chapter is as a race between two clocks. On one clock, the buyback and synergies are engineering the per-share economics upward, fast. On the other, 4,000 departures, 20 dying brand names, and three half-integrated technology stacks are testing whether the underlying business can hold its clients and its talent while all of this happens at once. The financial machinery is real and is running ahead of schedule. Whether the operating business underneath survives the surgery intact is the question no buyback can answer — and it takes us into the guts of how Omnicom actually makes money.

VIII. Core Business Deep Dive: How Omnicom Wins and Segment-Level Economics

Strip away the drama of the merger and ask a simple question: when a multinational hands Omnicom a marketing budget, what exactly does it get, and where does the money go? The company reports its revenue not by legacy agency brand but by discipline — the type of work — and the fiscal 2025 mix, which folds in the first month of Interpublic, is the clearest X-ray of the business.2

The dominant engine is Media & Advertising, at 58.0% of revenue.2 This is the scaled, cash-generative heart of the company: planning where a brand's advertising should run and buying that space, increasingly through automated programmatic systems that purchase digital inventory in milliseconds. It is high-volume, and its economics improve with size, because buying $50 billion of media commands better terms than buying $5 billion. Next comes Precision Marketing at 11.2% — the Omni, Acxiom, and Flywheel complex — which is the smallest of the large segments but the fastest-growing and the most strategically prized, because it sells higher-margin technology and consulting rather than commoditized ad placement.2 Public Relations contributes 9.3%, the reputational-management business housed in shops like FleishmanHillard and Ketchum (with IPG adding Weber Shandwick and Golin).2

Then Healthcare, at 8.0%, deserves a moment because it is quietly one of the best businesses in the portfolio.2 Marketing prescription drugs and medical devices is a high-barrier specialty: it demands regulatory fluency, scientific literacy, and long-cultivated relationships with pharmaceutical clients whose spending is driven by drug launches rather than by consumer confidence or the economic cycle. That makes healthcare revenue unusually sticky and defensive — the kind of business that keeps paying while consumer brands are slashing budgets in a downturn. The remainder splits across Experiential (5.0%), Execution & Support (4.9%), and Branding & Retail Commerce (3.6%).2

A cautionary note on that snapshot: the 58% media figure blends legacy agency labels, and the post-merger reporting is already shifting. On the Q1 2026 call, management presented a cleaner "core operations" view in which integrated media ran about 52% of revenue, standalone advertising about 17% (and declining), PR about 12%, and health about 10% — with core revenue of $5.6 billion growing 3.9% organically and adjusted EBITDA margin of 14.8%, up 240 basis points year over year as early synergies landed.9 The direction of travel is unmistakable: media and precision marketing up, traditional standalone advertising down. The house is being rebuilt around data and buying scale, and away from the pure-creative craft that gave it its name.

So how does Omnicom actually win business? Two mechanisms, and it is worth applying Hamilton Helmer's 7 Powers framework to name them precisely. The first is Scale Economies. Media buying is a volume game: the more inventory you commit to buy from Google, Meta, and Amazon, the better the pricing, the earlier the access to new ad formats, and the more favorable the transparency terms you can extract — advantages you pass back to clients as a reason to stay. Fusing Omnicom's and IPG's media volumes creates the largest single buying engine on the planet, which in theory sharpens that edge. The second is Switching Costs. Once a multinational's first-party data, retail-commerce funnels, and programmatic buying are wired into Omni Plus, unwinding all of it to move to Publicis or WPP is expensive, risky, and slow — the deeper the integration, the higher the exit cost. That is the strategic bet behind the entire data-stack assembly: turn a services relationship, which can be reviewed and re-pitched every few years, into an infrastructure relationship that is painful to rip out.

It helps to name the other players on the board, because "Big Three" is a recent and still-contested label. Across the table sits Publicis Groupe, the French group whose Epsilon-driven data engine made it the growth pacesetter of the 2020s and the most direct competitor to Omnicom's precision-marketing thesis. Behind it, WPP — once the largest of all under Sorrell — has spent years shedding assets and cutting debt, a wounded giant whose troubles are part of why Omnicom moved to secure the top spot. Then a second tier: Japan's 電通 Dentsu, a domestic colossus in its home market still working to build a coherent international network; France's Havas, spun out of Vivendi and smaller but scrappy; and S4 Capital, the "new-model" digital-only venture that none other than Martin Sorrell built after his exit from WPP, explicitly designed to be the anti-holding-company — all data and content, no legacy agencies. And circling from outside the industry entirely is Accenture Song, the marketing arm of the giant consultancy, which attacks the business from the technology-and-transformation flank rather than the creative one. The competitive set, in other words, is not three cozy incumbents; it is a consolidating oligopoly being probed simultaneously by a resurgent French rival, a disrupted British one, national champions, digital insurgents, and consultants. Omnicom's scale is largest, but scale in a shrinking pie is not the same as safety.

But a war-game has to include the other side's forces, and Porter's framework is unforgiving here. The bargaining power of buyers is high and structural: large clients routinely put nine-figure accounts up for competitive "review," pitting holding companies against each other explicitly to compress fees. A media relationship worth hundreds of millions can move on a single procurement decision. And the threat of substitutes is arguably the most serious long-term force in the industry. Brands are increasingly bringing media and creative in-house, building their own trading desks and studios. Consultancies like Accenture Song attack from the technology-and-transformation flank. And generative AI threatens to let a small brand do in-house, for pennies, what once required an agency floor. The scale-and-switching-cost moat is real, but it is being probed from three directions at once — which is exactly why the bull and bear cases on this company are so sharply drawn.

IX. The Playbook: Durable Business & Investing Lessons

Step back from the deal noise and Omnicom's forty-year arc yields a few transferable lessons — the kind that outlast any single quarter's organic-growth print.

The first is the enduring genius of the decentralized front-end, centralized back-end architecture. It is, at bottom, a solution to a human-capital problem. Creative talent does not thrive inside a monolith; it needs the identity, culture, and autonomy of a named agency to do its best work and to retain the people who make it. But autonomy is expensive and duplicative if every agency runs its own finance department, leases its own trophy real estate, and buys its own software. Omnicom's answer — keep the brands sovereign at the front, ruthlessly consolidate everything the client never sees at the back — lets it protect creative culture and manage client conflicts while extracting the high-margin efficiencies of scale. The 1986 structure and the 2026 synergy plan are the same idea, forty years apart. The lesson generalizes to any business trying to combine boutique quality with industrial economics.

The second lesson is about M&A sequencing, and it is the most instructive part of the whole story. Omnicom did not acquire Interpublic out of nowhere. It first built the data platform (Omni), then bought the commerce-data engine (Flywheel), and only then — with the machine already assembled and running — bought the giant whose creative accounts and Acxiom identity data it could immediately pour through that machine. Sequence matters enormously in acquisitions. A company that buys scale before it has built the system to make scale productive tends to end up with WPP's problem: a sprawling collection of assets and no integrating logic. Omnicom, at least in theory, reversed that order. The caveat, which a skeptic should keep firmly in view, is that the sequencing thesis is only validated if the integration actually works; a beautiful sequence executed badly still produces a mess.

A third lesson hides inside the restructuring: the discipline of pruning while you grow. It is easy to celebrate the $13.5 billion acquisition and overlook that Omnicom simultaneously set out to sell or shut down billions of dollars of revenue it deemed non-strategic or underperforming. Most acquirers add; few subtract with equal vigor, because subtraction shrinks the headline revenue number that flatters management's ego. A company willing to amputate low-margin, low-growth business at the same moment it is integrating a giant is signaling that it cares about the quality of revenue, not just the quantity — a healthy instinct, provided it is executed honestly. The caution, again, is in the disclosure: when management quietly conceded that the businesses being sold carried lower margins than first guided, it was a reminder that "non-strategic" can be a polite label for "we did not fully understand what we were buying." Watch whether the pruning improves the margin mix as promised, or merely removes revenue.

The fourth lesson is the double-edged one about skin in the game. Wren's shift to a $1.00 salary in exchange for options that pay off only if the stock rises is a textbook demonstration of aligning a chief executive's incentives with shareholders' precisely at the moment of maximum risk — a dilutive, transformational merger where trust between owners and management is most fragile. But the same episode, with its 43% protest vote, is a lesson in the limits of that alignment: incentive design and pay restraint are different things, and a board can achieve the first while abandoning the second. The durable investing takeaway is not "aligned pay is good" but "watch what alignment costs, and who bears it." All three lessons, notably, are being tested in real time — which is why the skeptics deserve a full hearing.

X. Skeptics, Bears, and the GenAI Risk Radar

Put an activist short-seller in a room with Omnicom's management and the first thing they would attack is the synergy story — not because $1.5 billion is implausible, but because of where those savings tend to end up. Here is the uncomfortable history of agency holding companies: cost savings extracted from a merger are frequently demanded back by clients at the next contract renewal, in the form of lower fees. Procurement departments are not naive; they know when their agency has just taken $1 billion of cost out of the system, and they arrive at the renewal table expecting a share of it. The bear's sharpest question is therefore not "will Omnicom hit its synergy target?" but "will the synergies reach the operating margin, or will they be competed away as price?" If the latter, the whole restructuring becomes a transfer from Omnicom's employees to its clients, with shareholders holding the bag.

The second line of attack is talent. The product a client actually buys is the people — the creative directors, the strategists, the account leads who understand the brand. Cutting 4,000 jobs and sunsetting more than 20 agency names is precisely the kind of upheaval that sends the best of those people to competitors or to independent shops, taking client relationships with them. In a business where the assets ride the elevator down every night, aggressive consolidation is not a neutral cost exercise; it is a live risk to revenue. Integration friction compounds it. Merging historic rivals like BBDO and McCann under one owner can ignite internal culture wars over turf, leadership, and which brand survives — and unhappy senior people leaving in clusters is how holding-company mergers quietly lose accounts.

Then there is the threat that overshadows everything: generative AI. To see why it is genuinely existential rather than merely disruptive, you have to understand how agencies bill. A large share of traditional agency revenue is tied, directly or indirectly, to labor hours — the cost of the copywriters, designers, retouchers, and campaign-execution teams who produce the work. Generative AI attacks that model at its foundation. A tool that can draft fifty ad variations, resize them for thirty placements, and A/B-optimize the campaign in minutes turns work that once consumed hundreds of billable hours into a near-zero-marginal-cost commodity. If the price of producing creative content collapses, so does a chunk of the revenue base built on producing it. This is the deflationary case, and it is the single most important thing for a long-term investor to weigh: AI could either be the tool that lets Omnicom deliver more for less and expand margins, or the force that commoditizes the labor its business model has always monetized. Management's own framing — deploying "agentic AI" inside Omni to automate media buying and creative production — is a tacit admission that it must ride the wave or be drowned by it.9

It is worth being precise about what "agentic AI" means here, because it is easy to wave the phrase around without content. On the Q1 2026 call, management described deploying software "agents" — autonomous programs that can execute tasks rather than merely draft content — that can, for example, negotiate and place media buys machine-to-machine, or assemble and optimize campaigns with far less human intervention.9 The optimistic reading is that this is a productivity story: if Omnicom can produce the same client outcomes with fewer labor hours, and if it can shift its pricing away from time-and-materials toward outcome- or value-based fees, then AI expands margins rather than eroding revenue. The pessimistic reading is that the client, not the agency, captures that productivity gain — that once a marketer sees an ad produced by AI in minutes, it will refuse to pay agency rates for it, and the deflation lands on Omnicom's top line. Both readings can be true for different services at different times, which is why the AI question resists a tidy verdict. The one thing an investor should not accept is the framing that AI is unambiguously a tailwind for a business whose historical unit of sale was the billable hour.

There is a fourth risk that the merger actually increases, and it deserves a place on the radar precisely because management tends to present the same fact as an unalloyed positive: data and privacy exposure. The prize asset of the Interpublic deal, Acxiom, is a vast consumer-data business, and the entire "Omni Plus" thesis rests on wiring first-party identity data ever more deeply into everything Omnicom does. But regulators on both sides of the Atlantic are moving in the opposite direction — tightening consent requirements, restricting cross-context data sharing, and probing exactly the kind of identity-resolution that makes Acxiom valuable. A business whose competitive advantage is built on assembling detailed profiles of consumers is, by construction, a business with regulatory and reputational tail risk: a change in privacy law, an enforcement action, or a high-profile data incident could impair the very asset the merger was designed to acquire. The same data depth that management sells as a moat is also a concentration of legal and political risk, and a balanced investor holds both facts at once.

The neutral verdict is that all these risks are real and none is yet resolved. The synergy-leakage risk will show up in margins over the next several quarters; the talent risk in client wins and losses; the AI risk over years, not months. A skeptic does not have to believe the company is doomed to insist that the burden of proof sits squarely on management — and that the proof will be in operating results, not investor-day slides.

XI. The Investment Spine: Bull vs. Bear and Key KPIs

Lay the two cases side by side and the Omnicom debate resolves into a genuinely balanced contest, which is what makes it interesting.

The bull case runs like this. Omnicom executes the integration cleanly, capturing the full $1.5 billion of synergies and driving operating margins back toward the top of their historical range. The Omni-plus-Acxiom-plus-Flywheel data stack becomes a genuine differentiator, winning a disproportionate share of the global media reviews that reallocate billions of dollars of spend every year, because Omnicom can prove return on investment that rivals cannot. Retail media and precision marketing — the fast-growing, higher-margin segments — become a larger slice of the mix, lifting the whole company's growth rate and margin structure. And the $5 billion buyback shrinks the share count aggressively enough that even modest operating growth compounds into strong per-share earnings growth. In this world, the scale-economies and switching-costs powers prove durable, and Omnicom emerges as the structurally advantaged leader of a consolidated Big Three.

The bear case is equally coherent. Generative AI commoditizes the labor-hour billing model faster than precision marketing can grow to replace it, and the industry's revenue base structurally erodes. Client fee compression eats the synergies before they reach the margin line, so the pain of 4,000 job cuts buys shareholders nothing durable. Cultural friction and talent flight cost the company marquee accounts, and the very act of consolidating rivals under one roof reactivates the conflict-management problem the holding-company model was built to solve — a single owner cannot represent every competitor forever. In this world, Omnicom has bought scale into a shrinking, deflating market, and the buyback is financial engineering papering over a deteriorating business.

The truth will be visible in the numbers, which is why an investor should ignore the noise and watch a very short list of key performance indicators.

First, core organic revenue growth — the underlying, like-for-like growth of the business, stripped of acquisitions, currency, and the roughly $3.2 billion of revenue being deliberately divested. This is the single cleanest read on whether the combined company is actually gaining or losing ground with clients. If organic growth holds in the mid-single digits through the integration, the talent-and-conflict bears are wrong; if it stalls or turns negative, they are right.

Second, operating (EBITA) margin expansion. This is the direct scoreboard for the synergy fight described above. Rising margins mean the cost savings are reaching shareholders; flat or falling margins despite the promised $1.5 billion mean clients are clawing the savings back as fees. Watch the trend across several quarters, not any single print, and watch it against the divestiture noise.

Third, the weighted-average share count. The whole per-share case rests on the buyback outrunning the dilution from an all-stock deal. Management has guided to an 11%–12% reduction in 2026;9 tracking the actual pace of share-count reduction reveals whether the financial engineering is delivering the earnings-per-share support the equity story requires. If the count falls as promised, dilution is neutralized; if the buyback slows, the EPS math weakens quickly.

Three numbers, three questions — demand, cost capture, and dilution. Everything else in the Omnicom story, ultimately, resolves into how those three trend over the next two years.

XII. Epilogue & Outro

There is a particular kind of executive who spends an entire career building toward a single, defining act, and John Wren has arranged his so that the Interpublic merger is unmistakably his. Thirty years at the helm, a philosophy of discipline compounded across cycles, a rival merger that blew up in 2014 and taught him to build before he bought — and now, in his late seventies, a $1.00 salary and four million options staking his legacy and his fortune on making the biggest deal in advertising history work by the end of 2028. It is either the perfect capstone or the overreach that undoes a great record. As of mid-2026, it is genuinely too early to know, and anyone who tells you otherwise is selling something.

The larger question the episode leaves open is not really about one company. It is about whether service businesses built on human craft can survive the technologies that automate the craft. Advertising has consolidated from a fragmented industry of proud independents into an oligopoly of three, precisely because scale, data, and capital became the ways to defend against disintermediation. Omnicom's wager is that even more scale, fused with a unified data stack, is the answer to the next wave — the platforms and the generative machines. Maybe it is. But the same tools that give the holding company its new powers also threaten the labor model that made it rich, and the clients it consolidated to serve are learning to do more of the work themselves. The Big Bang of 1986 was a bet that bigger was safer. Four decades later, at far greater scale, Omnicom is making that bet again — and the industry, and its shareholders, will spend the rest of the decade finding out whether it still holds.

References

-

Omnicom Completes Acquisition of Interpublic, Forming the World's Largest Marketing Company — StockTitan, 2025-11-26 ↩↩↩↩↩

-

Omnicom Reports Fourth Quarter and Full Year 2025 Results — PR Newswire / Omnicom Group, 2026 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Omnicom Group Inc. Form 8-K — Amended Employment Agreement of John D. Wren — SEC EDGAR, 2025-05-12 ↩↩

-

Omnicom hit by 43% vote against John Wren's $70 million pay deal — Campaign Asia, 2026 ↩↩

-

Analysis: The Publicis Omnicom deal is off – so why did it fail? — The Drum, 2014-05-09 ↩↩↩

-

Omnicom to Acquire Flywheel Digital, the Digital Commerce Business of Ascential plc — Omnicom Group, 2023-10-30 ↩

-

Omnicom Announces Closing of Acquisition of Flywheel — PR Newswire / Omnicom Group, 2024-01-02 ↩↩↩

-

Omnicom and Interpublic Group to Combine in Landmark All-Stock Merger — Axios, 2024-12-09 ↩↩

-

Omnicom (OMC) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-04-28 ↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube