ONEOK: The Midstream Giant's Evolution

I. Introduction & Episode Roadmap

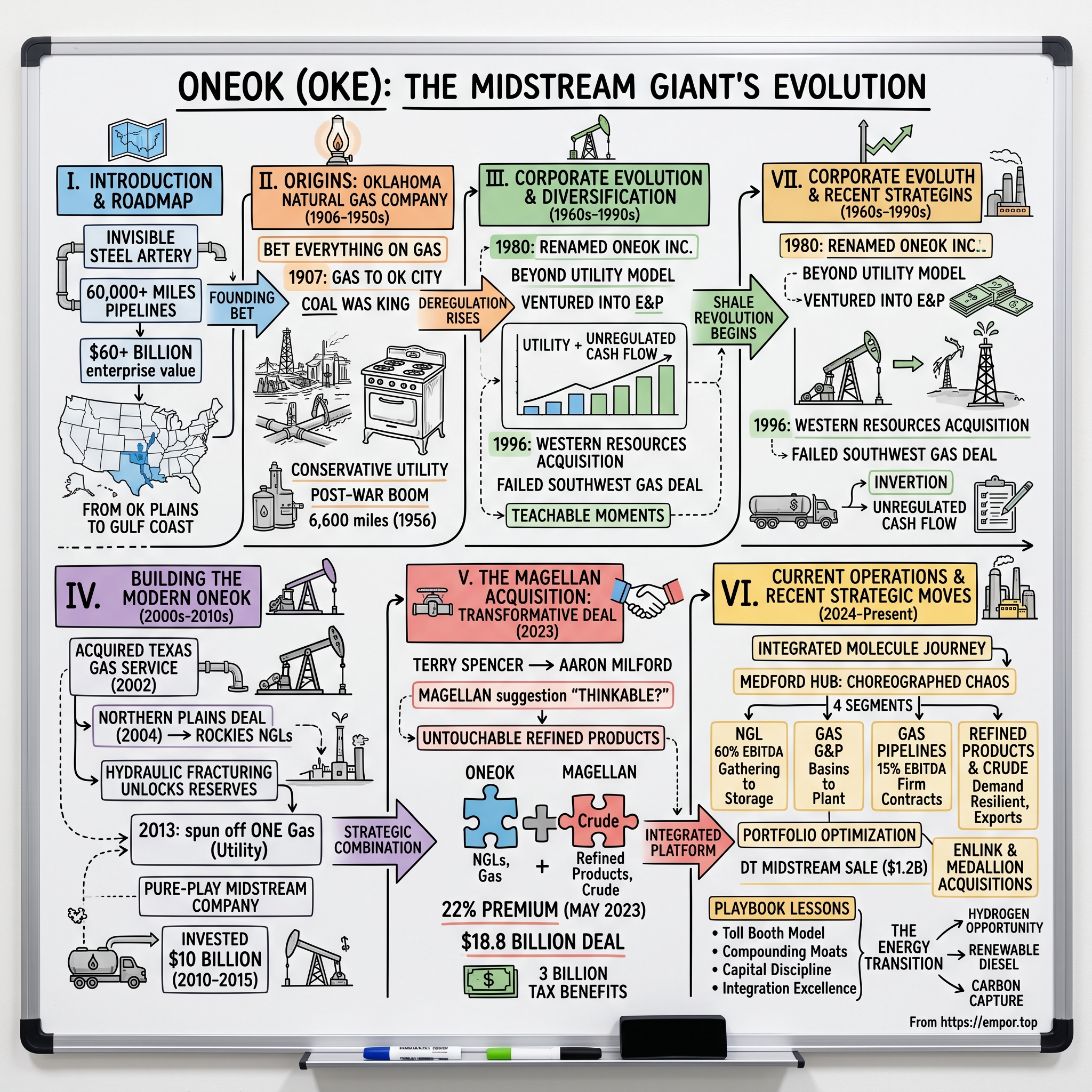

The pipeline snakes across the Oklahoma plains like a steel artery, invisible to most who drive over it on Interstate 44. But beneath the red dirt and prairie grass lies the beating heart of American energy infrastructure—60,000 miles of it, to be precise. This is ONEOK's domain, a $60+ billion enterprise value colossus that most Americans have never heard of, yet whose infrastructure touches their lives every time they turn on a stove, fill up their tank, or heat their home.

Picture this: In 1906, when Oklahoma was still Indian Territory, two businessmen named Dennis Flynn and Charles Ames stood on a windswept hill outside Tulsa with a radical idea—pipe natural gas from the Osage County fields to the growing towns of Sapulpa and Oklahoma City. The automobile had barely been invented. The Wright Brothers had flown at Kitty Hawk just three years prior. And these men were betting everything on invisible energy flowing through steel tubes buried in the ground.

Today, that audacious bet has evolved into something far more complex and valuable. ONEOK isn't just a pipeline company—it's the crucial middleman in America's energy ecosystem, the connector between the Permian Basin's gushing wells and the Gulf Coast's hungry refineries, between Rocky Mountain gas fields and Midwest heating demand. As a Fortune 500 and S&P 500 stalwart, the company processes, transports, and stores the lifeblood of modern civilization: natural gas, natural gas liquids, refined products, and crude oil.

But here's what makes ONEOK's story particularly fascinating for students of business history: This isn't a tale of Silicon Valley-style disruption or Wall Street financial engineering. It's about the patient accumulation of irreplaceable physical assets, the strategic navigation through boom-bust commodity cycles, and most recently, a transformative $18.8 billion acquisition that reshaped the entire North American midstream landscape.

The question we're exploring isn't just how a regional utility became a continental giant. It's about understanding the hidden infrastructure layer that powers modern life—and why, in an era obsessed with digital transformation and energy transition, owning pipes in the ground might be one of the most durable business models ever created.

Over the next few hours, we'll trace ONEOK's evolution through five distinct eras: the utility origins when natural gas was considered a nuisance byproduct; the diversification years when deregulation created opportunity; the shale revolution that transformed American energy; the strategic pivot from utility to pure-play midstream; and finally, the Magellan acquisition that created today's integrated giant.

We'll examine how management teams across decades made bold bets—some that paid off spectacularly, others that nearly sank the company. We'll decode the economics of fee-based contracts, the strategic value of NGL fractionation, and why location matters more than technology in the pipeline business. And we'll wrestle with the existential question facing every energy infrastructure company: What happens when the world transitions away from fossil fuels?

For investors, ONEOK presents a fascinating case study in competitive advantage through physical assets, the power of network effects in infrastructure, and the delicate balance between growth investment and shareholder returns. For business strategists, it's a masterclass in portfolio optimization, knowing when to buy versus build, and the art of integration.

But most importantly, this is a story about permanence in an impermanent world—about building something that lasts not for quarters or years, but for generations.

II. Origins: Oklahoma Natural Gas Company (1906–1950s)

October 12, 1906. The rain had been falling for three days straight in northeastern Oklahoma, turning the construction site into a muddy morass. Dennis T. Flynn, his boots caked with red clay, stood beside a massive trench that would soon hold the first segment of pipeline connecting the Osage County gas fields to the growing settlements to the south. His partner, Charles B. Ames, held the incorporation papers under his coat, protecting them from the drizzle. They had just formed the Oklahoma Natural Gas Company with $1.7 million in capital—a staggering sum for the time, equivalent to about $60 million today.

The timing was either brilliant or insane. Oklahoma wouldn't achieve statehood for another thirteen months. The territory was still wrestling with its identity—part frontier, part Native American lands, part oil boomtown. Natural gas itself was considered largely worthless, often flared off at oil wells as a dangerous nuisance. But Flynn and Ames saw something others missed: a rapidly urbanizing territory that would need energy, and lots of it.

Their first pipeline was an engineering marvel for its time. Starting from the Cleveland gas field in Osage County, the line stretched 100 miles south through Sapulpa and into Oklahoma City. Construction crews worked through the brutal summer of 1907, laying pipe by hand, fighting rattlesnakes and summer storms. The project consumed every dollar of their initial capital, but on December 28, 1907—just one month after Oklahoma achieved statehood—natural gas began flowing to Oklahoma City for the first time.

The early customers were skeptical. Natural gas was new, untested. Coal was king, and electricity was the exciting new technology. But Flynn, a natural showman, organized demonstrations at the territorial fairgrounds, showing housewives how gas stoves could cook faster and cleaner than coal. He promised businesses that gas heating would eliminate the need for coal deliveries and ash removal. Slowly, customer by customer, the company built its base.

By 1910, Oklahoma Natural Gas had constructed the state's first compressor station—a mechanical marvel that could push gas through pipelines at higher pressures, extending their reach. This wasn't just infrastructure; it was nation-building. Each new mile of pipe meant another town could industrialize, another neighborhood could have streetlights, another factory could operate more efficiently.

The company's growth trajectory was staggering. By 1919—just thirteen years after incorporation—Oklahoma Natural Gas supplied thirty-seven communities across more than one thousand miles of pipeline. The company had become the circulatory system of Oklahoma's economy, as essential as the railroads but far less visible. Their pipeline maps looked like spider webs spreading across the state, connecting dots that would become cities: Tulsa, Norman, Enid, Stillwater.

But growth came with challenges that would define the company's DNA for decades. The 1920s brought wild speculation in oil and gas, followed by spectacular busts. The company survived by focusing ruthlessly on its utility operations—steady, regulated, predictable. When wildcatters went bankrupt chasing the next big strike, Oklahoma Natural Gas kept laying pipe, connecting homes, maintaining compressor stations.

The Great Depression tested this model to its limits. As factories closed and families struggled to pay bills, gas consumption plummeted. The company's workforce, which had swelled to over 400 employees by 1929, was cut nearly in half. Yet management made a crucial decision that would echo through decades: they kept building infrastructure. While competitors retrenched, Oklahoma Natural Gas used the downturn to acquire distressed assets cheaply, expanding into rural areas that others had abandoned.

This contrarian strategy paid off magnificently during World War II. As defense plants sprouted across Oklahoma—including the massive Douglas Aircraft facility in Tulsa—industrial gas demand exploded. The company's existing infrastructure, built during the lean years, was perfectly positioned to serve this surge. By 1945, Oklahoma Natural Gas was moving more molecules through more miles of pipe than anyone had imagined possible in 1906.

The post-war boom transformed everything. Suburban development, powered by returning GIs and government loans, created thousands of new residential customers annually. The company's engineering department, once a handful of surveyors with slide rules, grew into a sophisticated operation designing high-pressure transmission systems and urban distribution networks. By 1956, the company employed 600 people and maintained 6,600 miles of pipeline—a hundred-fold increase from its founding.

But perhaps the most important development of this era was cultural. Oklahoma Natural Gas had evolved from a speculative venture into an institution. Its blue-collar workers—the pipeline welders, compressor operators, and meter readers—formed the backbone of middle-class Oklahoma. The company's conservative financial management, its focus on safety and reliability, its deep roots in local communities—these became organizational touchstones that would survive every subsequent transformation.

As the 1950s drew to a close, Oklahoma Natural Gas stood at an inflection point. The age of simple utility operations was ending. Deregulation loomed on the horizon. New technologies like interstate pipelines and cryogenic processing would soon reshape the entire industry. The company that Flynn and Ames had founded to serve a territory was about to become something entirely different—though exactly what, no one could yet imagine.

III. Corporate Evolution & Diversification (1960s–1990s)

The boardroom at Oklahoma Natural Gas Company's Tulsa headquarters was thick with cigarette smoke on that December morning in 1980. CEO John Gaberino stood before a wall-mounted map of the United States, red pins marking their existing operations, blue pins showing potential acquisitions. "Gentlemen," he said, stubbing out his Marlboro, "Oklahoma Natural Gas Company is a name that limits us. We're thinking too small." With that, he unveiled the new corporate identity: ONEOK Inc.—a modernist amalgamation that sounded more like a computer company than a utility. The gas service division would keep the Oklahoma Natural Gas name, but the parent company was positioning for something bigger.

This wasn't just rebranding—it was a declaration of intent. The 1970s had been brutal for utilities. The Arab oil embargo, stagflation, and the first whispers of deregulation had shaken the industry's comfortable monopolistic foundations. Gaberino and his team recognized that the old utility model—regulated returns on regulated assets—was dying. The future belonged to companies that could operate across the energy value chain, from wellhead to burner tip.

The transformation started with a series of calculated risks that old-timers at the company found alarming. In 1982, ONEOK created its first non-regulated subsidiary, venturing into oil and gas exploration—a dramatic departure from the steady utility business. The timing seemed terrible; oil prices were collapsing from their 1980 peaks. But management saw opportunity in distress, acquiring drilling rights and mineral interests at fire-sale prices.

By 1985, this contrarian strategy was paying dividends. While pure-play exploration companies struggled with $10 oil, ONEOK's diversified model provided stability. The regulated utility operations generated steady cash flow that funded higher-risk, higher-return ventures. It was financial engineering before that term became fashionable—using the boring to fund the bold.

The real acceleration came with the Natural Gas Policy Act of 1978 and subsequent deregulation throughout the 1980s. Suddenly, interstate pipelines could be owned by non-utilities. Gas could be bought and sold as a commodity, not just delivered as a service. ONEOK's management, led by new CEO Larry Brummett, saw this as their moment to break out of Oklahoma's borders.

The 1996 acquisition of Western Resources' natural gas operations for $660 million in stock was the company's coming-out party as a regional powerhouse. In one stroke, ONEOK gained 1,575 employees, 624,000 customers in Kansas, and 36,000 in northeast Oklahoma. But more importantly, they acquired expertise in deregulated markets and interstate pipeline operations. The integration was messy—two different corporate cultures, incompatible IT systems, regulatory complexities across state lines—but ONEOK emerged stronger, having learned valuable lessons about large-scale M&A.

The Kansas expansion also brought ONEOK its first taste of midstream operations beyond traditional utility service. Western Resources owned processing plants and gathering systems that collected gas from producers and prepared it for pipeline transport. This was ONEOK's introduction to the fee-based model that would eventually become its core: earning money for moving and processing molecules, regardless of commodity prices.

But not every bet paid off. The attempted acquisition of Southwest Gas in 1999 for $1.8 billion turned into a costly debacle. ONEOK announced the deal in August, promising to create a super-regional utility spanning from Oklahoma to Nevada. But Southwest's shareholders revolted, regulatory approvals proved elusive, and by January 2000, the merger was dead. The termination triggered lawsuits, breakup fees, and a management credibility crisis that took years to fully resolve.

Yet even this failure taught valuable lessons. ONEOK's post-mortem revealed they had underestimated cultural differences, overestimated synergies, and moved too fast without proper due diligence. Future CEOs would reference the Southwest Gas fiasco as a cautionary tale, insisting on more thorough integration planning and conservative synergy estimates.

Throughout the 1990s, ONEOK was also quietly building technological capabilities that would prove crucial later. They invested heavily in SCADA (Supervisory Control and Data Acquisition) systems, allowing remote monitoring and control of far-flung pipeline assets. They developed sophisticated gas scheduling and nomination systems, essential for managing complex interstate movements. This wasn't sexy stuff—no one wrote Harvard Business School cases about pipeline telemetry—but it created operational advantages that competitors couldn't easily replicate.

The company's corporate culture was also evolving. The old utility mindset—risk-averse, procedure-bound, government-like—was giving way to something more entrepreneurial. ONEOK started recruiting from oil majors and trading houses, bringing in talent comfortable with commodity volatility and complex financial instruments. The company headquarters, once filled with engineers in short-sleeved white shirts, now housed traders watching NYMEX screens and MBAs building financial models.

By the late 1990s, ONEOK had transformed from a regional utility into a diversified energy company with operations in multiple states, a growing midstream portfolio, and aspirations for national reach. Revenue had grown from $500 million in 1980 to over $2 billion by 1999. The company had learned to navigate deregulated markets, execute acquisitions (and survive failed ones), and operate across the energy value chain.

But the biggest transformation was still ahead. The shale revolution was about to begin, and ONEOK's position—with gathering systems in key basins, processing expertise, and interstate pipeline connectivity—would prove remarkably prescient. The company that Dennis Flynn and Charles Ames founded to serve Oklahoma City was about to become a continental energy infrastructure giant.

IV. Building the Modern ONEOK (2000s–2010s)

John Gibson stepped into the CEO role at ONEOK in January 2007 with oil at $60 per barrel and natural gas at $7 per thousand cubic feet. Within eighteen months, oil would spike to $147 before crashing to $30, gas would swing from $13 to $3, and the financial system would nearly collapse. "I knew the job would be challenging," Gibson would later joke, "but I didn't expect to manage through the energy market equivalent of a hurricane while the house was on fire." Yet this period of extreme volatility would forge the modern ONEOK—leaner, more focused, and positioned perfectly for the shale revolution.

The transformation began even before Gibson's arrival. In October 2002, ONEOK acquired Southern Union Gas's Texas division for $420 million, instantly becoming a major player in the Lone Star State with what they renamed Texas Gas Service. This wasn't just geographic expansion; it was a bet on Texas's booming economy and growing energy production. The Barnett Shale, centered near Fort Worth, was beginning to demonstrate that hydraulic fracturing could unlock massive gas reserves previously thought uneconomical.

Then came the deal that would reshape ONEOK's DNA: the September 2004 acquisition of Northern Plains Natural Gas Company for $175 million. On paper, it looked modest—some pipeline assets in the Williston Basin, processing plants in the Rockies. But buried in the deal was a controlling interest in Northern Border Partners, with 6,600 miles of interstate pipeline, five processing plants, and two fractionation facilities. Suddenly, ONEOK wasn't just moving gas locally; they were a major interstate player with assets spanning from Canada to Texas.

The real value of Northern Plains became apparent as the shale revolution accelerated. Those processing plants in the Rockies? They were perfectly positioned to handle gas from the emerging Bakken formation. The fractionation facilities? Essential for separating valuable natural gas liquids (NGLs) from raw gas streams. ONEOK's management, perhaps through luck as much as foresight, had acquired exactly the right assets at exactly the right time.

But Gibson recognized that ONEOK was trying to be too many things. The company operated regulated utilities, interstate pipelines, gathering systems, processing plants, and even some exploration assets. This complexity made the company hard for investors to value and harder for management to optimize. "We were like a department store," Gibson explained to analysts, "when the market wanted boutiques."

The solution was radical simplification. In July 2013, ONEOK spun off its natural gas distribution businesses—Oklahoma Natural Gas, Kansas Gas Service, and Texas Gas Service—into a separate company called ONE Gas. This wasn't just financial engineering; it was strategic focus. The utility business, steady but slow-growing, appealed to income-focused investors. The midstream business, volatile but high-growth, attracted a completely different shareholder base.

The separation was complex, involving 3,400 employees, millions of customers, and regulated assets across three states. But when ONE Gas began trading independently in January 2014, the market's reaction was emphatic: both companies saw their valuations increase. ONEOK, now a pure-play midstream company, could pursue aggressive growth without worrying about utility regulators. ONE Gas could focus on safe, reliable service without the volatility of commodity markets.

The timing of this transformation was exquisite. The shale revolution was reaching escape velocity. U.S. oil production, which had declined for decades, suddenly reversed course. Natural gas, once scarce and expensive, became abundant and cheap. But this created a new problem: infrastructure bottlenecks. Producers could drill wells, but they needed someone to gather, process, and transport their production. Enter ONEOK.

Between 2010 and 2015, ONEOK invested over $10 billion in growth capital, building an integrated network that could handle the shale boom's output. They constructed the Bakken NGL Pipeline, moving valuable liquids from North Dakota to their fractionation complex in Kansas. They expanded their West Texas system to handle Permian Basin growth. They built NGL storage caverns in Kansas, creating strategic flexibility in volatile markets.

The economics of these investments were compelling. Unlike exploration companies that faced commodity price risk, ONEOK's midstream model was primarily fee-based. Producers paid fixed fees to move molecules through pipes, regardless of commodity prices. When oil crashed from $100 to $30 in 2014-2015, exploration companies hemorrhaged cash, but ONEOK's revenues remained relatively stable. Their contracts included minimum volume commitments, dedication agreements, and cost-of-service provisions that provided downside protection.

This period also saw ONEOK master the art of dropdown transactions with their master limited partnership, ONEOK Partners. The structure was elegant: ONEOK would build new assets at the parent level, then "drop them down" to the MLP once operational, recycling capital for new projects while maintaining control. This financial architecture allowed rapid growth without constantly diluting shareholders or taking on excessive debt.

By 2017, when Gibson handed the CEO reins to Terry Spencer, ONEOK had become one of North America's premier midstream companies. They owned 38,000 miles of pipelines, dozens of processing plants, and critical fractionation infrastructure. Annual adjusted EBITDA had grown from $800 million in 2007 to over $3 billion. The company that once primarily served Oklahoma gas customers now moved 15% of America's natural gas and 20% of its NGLs.

But Spencer inherited challenges alongside these assets. The MLP structure, once a financing advantage, had become a complexity discount in the market. Environmental opposition to pipeline construction was intensifying. And while ONEOK had built an impressive NGL and gas business, they had minimal exposure to crude oil and refined products—increasingly important parts of the energy value chain.

The stage was set for the next chapter: a transformative acquisition that would address these challenges while creating one of North America's most integrated midstream companies.

V. The Magellan Acquisition: Transformative Deal (2023)

Terry Spencer's phone rang at 5:47 AM on a Saturday morning in March 2023. On the line was Aaron Milford, Magellan Midstream Partners' CEO, with a simple question: "Terry, what would you think about combining our companies?" Spencer, still in his kitchen making coffee, nearly dropped his mug. Magellan—with its refined products empire and sterling reputation—had been considered untouchable, a crown jewel of American energy infrastructure. Yet here was Milford, suggesting the unthinkable.

The backstory was compelling. Magellan, despite its operational excellence and 9,800 miles of refined products pipelines, faced a strategic dilemma. The company had limited growth opportunities in its core refined products business, minimal exposure to high-growth NGL markets, and a partnership structure that increasingly looked antiquated. Meanwhile, activist investors were circling, demanding either a sale or radical restructuring. Milford and his board recognized that independence might no longer be the best path forward.

For ONEOK, Magellan represented something close to a perfect strategic fit. Where ONEOK was strong in NGLs and natural gas, Magellan dominated refined products and crude oil. ONEOK's assets were concentrated in production basins; Magellan's stretched to demand centers and export terminals. ONEOK had growth but needed stability; Magellan had stability but needed growth. On Spencer's whiteboard in Tulsa, the combination looked like puzzle pieces clicking together.

The negotiations that followed were a masterclass in complex dealmaking. The initial price discussions ranged from $60 to $70 per unit, but Magellan's board, led by longtime director Jim Montague, proved formidable negotiators. They understood their leverage: Magellan's infrastructure was irreplaceable, their cash flows rock-solid, their operational reputation impeccable. Any buyer would need to pay a premium for such quality.

By May 2023, the terms were crystallizing: $25 in cash plus 0.6670 shares of ONEOK stock per Magellan unit, valuing the company at $18.8 billion—a 22% premium to Magellan's pre-announcement trading price. The structure was crucial. The cash component, funded by debt and asset sales, provided certainty for Magellan unitholders. The stock component aligned interests, making Magellan investors significant ONEOK shareholders with continued upside exposure.

But the real financial engineering came from an unexpected source: the tax code. By structuring the deal as a taxable transaction, ONEOK could step up Magellan's tax basis, creating approximately $3 billion in total tax benefits with a net present value of $1.5 billion. Moreover, this structure would defer ONEOK's corporate alternative minimum tax from 2024 to 2027, preserving near-term cash flow for debt reduction and growth investment.

The synergy math was equally compelling. ONEOK identified $200+ million in annual cost synergies—not from the typical playbook of mass layoffs and office closures, but from operational optimization. Magellan's refined products could move through ONEOK's terminals. ONEOK's NGL supplies could reach new markets via Magellan's infrastructure. Combined purchasing power would reduce procurement costs. Integrated scheduling would optimize pipeline utilization.

Spencer presented the deal to Wall Street on May 14, 2023, with a compelling narrative: this wasn't just about getting bigger, but about building resilience. "Look at the cash flow stability," he told analysts, pulling up slides showing projected earnings. The combined company would generate 80% of EBITDA from fee-based contracts. Magellan's refined products business, tied to non-discretionary gasoline and diesel demand, would balance ONEOK's more volatile NGL exposure. The deal would create immediate EPS accretion of 3-7% annually and free cash flow per share accretion averaging over 20%.

Yet skeptics raised valid concerns. The integration would be massive—combining 5,000 employees, harmonizing different IT systems, merging distinct corporate cultures. ONEOK's cowboys-and-wildcatters mentality would need to mesh with Magellan's button-down operational excellence. The combined company's debt would initially spike to over $20 billion, pushing leverage ratios above 4x EBITDA—uncomfortable territory for a investment-grade company.

The regulatory approval process proved surprisingly smooth. Unlike previous pipeline megamergers that triggered antitrust scrutiny, ONEOK and Magellan operated largely complementary assets. The Federal Trade Commission cleared the deal with minimal conditions. State regulators, recognizing the importance of energy infrastructure, offered no significant objections. Even environmental groups, typically opposed to pipeline consolidation, remained relatively quiet—perhaps recognizing that combining existing assets was preferable to building new ones.

September 25, 2023, marked the closing—one of the largest energy infrastructure deals in U.S. history. The integration began immediately, led by a carefully selected team drawing talent from both companies. The cultural merger proved less challenging than feared; both companies shared deep operational expertise, safety-first cultures, and Midwestern roots. Within months, the promised synergies were materializing ahead of schedule.

The Magellan acquisition transformed ONEOK's financial profile. Pro forma 2023 adjusted EBITDA reached $6.5 billion, making ONEOK one of the largest midstream companies by earnings. The diversified asset base reduced earnings volatility by 40%, according to company models. Credit rating agencies, initially concerned about leverage, grew more comfortable as management demonstrated integration expertise and commitment to debt reduction.

But perhaps the most important change was strategic. ONEOK now owned infrastructure spanning the entire hydrocarbon value chain—from wellhead gathering to refined products delivery. They could offer integrated solutions to customers, capturing more value per molecule. They had options in an energy transition world: their refined products pipelines could carry renewable diesel, their NGL infrastructure could handle petrochemical feedstocks, their storage assets could support energy security initiatives.

Six months post-close, Spencer reflected on the deal's impact: "We didn't just buy assets; we bought optionality. Whatever the energy future looks like—more petrochemicals, renewable fuels, hydrogen corridors—we now have the infrastructure platform to participate." The company that started moving natural gas in Oklahoma had evolved into an integrated energy infrastructure giant, ready for whatever came next.

VI. Current Operations & Business Segments

Stand at the Medford Hub in northern Oklahoma on a cold January morning, and you'll witness the choreographed chaos of American energy in motion. Natural gas streams in from the Anadarko Basin at 800 pounds per square inch. NGL pipelines converge from the Permian, Bakken, and Rockies. Refined products flow toward Kansas City and Chicago. Control room operators, watching walls of screens, orchestrate molecular movements across thousands of miles. This is ONEOK's nerve center—one of many—where the company's four business segments converge in a symphony of steel and software.

The Natural Gas Liquids segment remains ONEOK's crown jewel, contributing roughly 60% of adjusted EBITDA. But calling it an "NGL business" understates the complexity. ONEOK operates the entire value chain: gathering systems that collect raw NGLs from processing plants, 40,000 miles of pipelines that transport them, fractionation facilities that separate them into purity products (ethane, propane, butane, natural gasoline), and storage caverns that hold millions of barrels in underground salt formations.

The economics are beautifully simple yet operationally complex. A barrel of mixed NGLs entering ONEOK's system at Mont Belvieu might be worth $30. After fractionation into purity products, those same molecules could be worth $45—a $15 spread that ONEOK captures through processing fees and optimization strategies. But executing this requires precise temperature control, pressure management, and quality specifications measured in parts per million. One contamination event can shut down an entire petrochemical plant, making operational excellence non-negotiable.

The Natural Gas Gathering and Processing segment tells a different story—one of direct connection to America's shale revolution. ONEOK's gathering systems stretch like capillaries across the Permian, Bakken, and Powder River basins, connecting to thousands of individual wells. These aren't just pipes; they're relationships. ONEOK's field personnel know producers by name, understand each basin's unique characteristics, respond to emergency calls at 2 AM when compressors fail or wells freeze.

Processing plants, the workhorses of this segment, perform modern alchemy. Raw gas from wells—a mixture of methane, NGLs, water, hydrogen sulfide, and other impurities—enters these facilities. Through a combination of cooling, compression, and chemical treatment, plants separate pipeline-quality natural gas from valuable NGLs and waste products. ONEOK's 19 active plants can process 2.2 billion cubic feet per day, enough to serve 20 million homes.

The Natural Gas Pipelines segment, generating about 15% of EBITDA, might seem like the sleepy utility cousin. But these assets—including the Viking, OkTex, and ONEOK Gas Transportation systems—provide the crucial connectivity between supply basins and demand centers. The business model is contractually bulletproof: long-term firm transportation agreements where customers pay for capacity whether they use it or not. It's like selling airplane seats where passengers pay full fare even if they don't fly.

The newest addition, Refined Products and Crude Oil (via Magellan), adds a completely different dimension. This isn't about molecules from wells; it's about finished products consumers actually see—gasoline, diesel, jet fuel. Magellan's 9,800-mile refined products system connects refineries along the Gulf Coast to markets throughout the Midwest and Rocky Mountains. The Houston distribution system alone can handle 1.2 million barrels per day, serving the nation's largest refining complex.

What makes this segment particularly valuable is its demand resilience. Natural gas and NGL consumption fluctuate with weather and industrial activity. But refined products demand—Americans driving to work, Amazon trucks making deliveries, airlines flying passengers—remains remarkably stable. Even during COVID-19 lockdowns, refined products demand only fell 30% at the trough and recovered within months. This stability provides ballast to ONEOK's earnings profile.

The integration of these four segments creates competitive advantages that transcend individual assets. Consider a Permian Basin producer who needs gathering services for raw gas, processing to extract NGLs, fractionation to create purity products, and pipelines to reach Gulf Coast markets. ONEOK can provide the entire solution, capturing fees at each step. This integrated offering creates customer stickiness—it's far easier to work with one sophisticated midstream partner than coordinate among multiple providers.

Technology increasingly differentiates ONEOK's operations. The company's Integrated Operations Center in Tulsa looks more like NASA Mission Control than traditional pipeline operations. Artificial intelligence algorithms predict equipment failures before they occur. Satellite imagery monitors right-of-ways for encroachment. Automated pig launchers clean pipelines without human intervention. This isn't just efficiency; it's safety and reliability at scale.

The commercial strategy has also evolved toward sophistication. ONEOK's marketing team doesn't just move molecules; they optimize margins through complex strategies. They might store propane in summer when prices are low, selling in winter when demand spikes. They arbitrage location differentials, moving products from oversupplied to undersupplied markets. They blend different NGL streams to meet specific customer specifications. These optimization activities, while small individually, generate hundreds of millions in additional annual income.

Environmental and safety performance, once afterthoughts in the midstream sector, now define operational excellence. ONEOK's leak detection systems can identify releases of less than 1% of flow within minutes. Methane emissions have decreased 40% per unit of throughput since 2015. The company conducts 50,000+ safety observations annually, creating a culture where every employee owns safety outcomes. This isn't just regulatory compliance; it's social license to operate in an increasingly environmentally conscious world.

Looking at ONEOK's current operations, you see a company that has evolved far beyond its pipeline roots. It's a logistics network, a processing complex, a storage system, and a market maker all rolled into one. The 60,000 miles of pipeline are just the visible infrastructure. The real value lies in the integrated capabilities, commercial expertise, and operational excellence that transform raw hydrocarbons into the energy products that power modern life.

VII. Recent Strategic Moves & Portfolio Optimization (2024–Present)

The email from DT Midstream arrived at ONEOK headquarters on a quiet Monday morning in October 2024, but the number it contained was anything but quiet: $1.2 billion cash for three interstate natural gas pipeline systems. Terry Spencer read it twice, then called an emergency executive committee meeting. "This is our chance," he told his team, "to prove we're serious about capital discipline and strategic focus."

The assets on the block—Guardian Pipeline, Midwestern Gas Transmission, and Viking Gas Transmission—weren't dogs. They generated steady EBITDA, served reliable utility customers, and required minimal maintenance capital. But in ONEOK's post-Magellan portfolio, they had become orphans. Located primarily in the upper Midwest, disconnected from ONEOK's core basins and growth markets, these pipelines represented the old ONEOK—the utility-adjacent, slow-growth infrastructure company Spencer was determined to leave behind.

The negotiation with DT Midstream was refreshingly straightforward. Both sides understood the assets' value and strategic fit. For DT Midstream, these pipelines perfectly complemented their existing Great Lakes footprint. For ONEOK, the proceeds would accelerate deleveraging and fund higher-return growth projects. The deal closed on December 31, 2024—New Year's Eve—allowing ONEOK to enter 2025 with a cleaner portfolio and stronger balance sheet.

But Spencer wasn't just selling; he was simultaneously buying assets that fit ONEOK's integrated strategy. In May 2024, while Magellan integration was still in full swing, ONEOK announced the acquisition of Easton Energy's Gulf Coast NGL pipeline system for $280 million. To outsiders, the timing seemed odd—why add complexity during a massive integration? But Spencer saw opportunity where others saw chaos.

The Easton assets—450 miles of NGL pipelines connecting Texas and Louisiana petrochemical complexes—were the missing link in ONEOK's Gulf Coast strategy. Combined with Magellan's refined products infrastructure and ONEOK's NGL logistics, these pipelines created an integrated Gulf Coast franchise serving the world's largest petrochemical complex. The acquisition price, at less than 8x EBITDA, reflected distressed seller dynamics that ONEOK could exploit given their strong balance sheet and operational expertise.

This portfolio optimization extended beyond buying and selling assets. ONEOK fundamentally restructured how it allocated capital across its business segments. The old model—spreading investment evenly across all regions and products—gave way to surgical focus. The Permian Basin, generating 40% of America's oil and 20% of its gas, received 60% of growth capital. The Bakken, despite its distance from markets, warranted expansion due to its NGL richness and ONEOK's dominant position.

Meanwhile, mature assets faced a different calculus. Rather than growth investment, ONEOK implemented aggressive cost reduction and efficiency programs. Automated pig launchers reduced maintenance costs by 30%. Predictive analytics decreased unplanned outages by 50%. Organizational restructuring eliminated redundant positions post-Magellan integration. These weren't headline-grabbing initiatives, but they generated $150 million in annual savings—equivalent to a $1.5 billion acquisition at typical multiples.

The capital allocation framework Spencer implemented was almost algorithmic in its discipline. Every project required 15% unlevered returns in base cases, 10% in downside scenarios. Growth capital was capped at 80% of adjusted free cash flow, ensuring organic deleveraging. Asset sales proceeds were earmarked 50% for debt reduction, 50% for high-return growth projects. Dividend growth was targeted at 3-5% annually—enough to reward shareholders but not so much as to constrain flexibility.

This discipline was tested in early 2025 when private equity firms approached ONEOK about selling its Powder River Basin assets for $2 billion. The price was compelling—nearly 12x EBITDA—but Spencer resisted. These assets, while subscale alone, provided crucial feedstock for ONEOK's Rockies NGL system. Selling would generate a one-time gain but permanently impair ONEOK's integrated value chain. The board backed Spencer's decision to hold, prioritizing strategic coherence over short-term financial engineering.

The optimization strategy also extended to commercial contracts. ONEOK systematically renegotiated agreements to reduce volumetric risk and increase fee certainty. Minimum volume commitments increased from 60% to 75% of contracted capacity. Contract tenors extended from 5 to 7 years average. Pricing mechanisms shifted from commodity-linked to fixed-fee structures. These changes reduced EBITDA volatility by an estimated 25%, making ONEOK more utility-like without the regulatory constraints.

Technology investments, often overlooked in midstream companies, became a strategic priority. ONEOK's $200 million "Digital Transformation Initiative" wasn't just IT modernization—it was competitive advantage construction. Machine learning algorithms now optimize NGL fractionation spreads in real-time. Blockchain technology streamlines custody transfer documentation. Digital twins of critical assets enable predictive maintenance. The payback? Over $50 million in annual benefits, with expectations of doubling within three years.

Environmental considerations increasingly shaped portfolio decisions. ONEOK committed to net-zero Scope 1 and 2 emissions by 2050, requiring systematic asset evaluation. Older, less efficient compressor stations faced replacement or retirement. Methane detection technology was deployed across all facilities. Renewable power purchases increased to 30% of electricity consumption. These weren't just ESG checkbox exercises; they were strategic positioning for a carbon-constrained future.

The human capital optimization proved equally important. Post-Magellan, ONEOK had redundant expertise in some areas, gaps in others. Rather than across-the-board cuts, the company implemented strategic workforce planning. Commercial teams expanded to capture optimization opportunities. Engineering resources shifted from new construction to efficiency enhancement. Digital expertise was hired from technology companies, bringing fresh perspectives to a traditional industry.

By early 2025, the portfolio optimization strategy was yielding tangible results. Net debt fell from $20 billion post-Magellan to $17 billion. Return on invested capital increased from 9% to 11%. EBITDA margins expanded 300 basis points through operational improvements. The market noticed: ONEOK's enterprise value multiple expanded from 8x to 10x EBITDA, reflecting increased confidence in management's capital allocation prowess.

But Spencer knows the optimization journey never truly ends. Energy markets evolve, new technologies emerge, regulatory landscapes shift. The company that once owned everything from gas utilities to exploration assets has learned the value of focus—and the discipline required to maintain it.

VIII. Financial Performance & Metrics

The numbers tell a story of transformation, but you have to know how to read them. When ONEOK reported full-year 2024 net income of $3.1 billion against revenue of $21.7 billion, the 14% net margin might seem pedestrian compared to software companies or luxury brands. But in the midstream sector—where moving molecules through steel pipes is the business model—these numbers reflect something more profound: the compounding power of essential infrastructure combined with disciplined execution.

Start with the revenue trajectory. The 23% year-over-year growth from 2023 to 2024 wasn't just Magellan acquisition math. Organic growth contributed 8%, driven by Rocky Mountain NGL volumes up 8% and natural gas processed volumes increasing 6%. This organic expansion in a mature industry reveals the ongoing infrastructure deficit created by the shale revolution. Producers keep drilling, consumption keeps growing, and ONEOK's pipes remain the crucial connection between supply and demand.

The adjusted EBITDA of $6.78 billion deserves deeper examination. Strip away the accounting noise—depreciation of 50-year assets, amortization of acquired intangibles, one-time integration costs—and you see the business's true cash-generating power. The EBITDA margin of 31% places ONEOK in the upper tier of midstream operators, above Kinder Morgan's 28% but below Enterprise Products' 35%. This positioning reflects ONEOK's balance between growth investment and operational efficiency.

But the real story lies in the quality of these earnings. Approximately 80% of EBITDA comes from fee-based contracts—fixed payments for moving or processing molecules regardless of commodity prices. This isn't the volatile, commodity-exposed model of upstream producers. When oil crashed from $120 to $30 in 2014-2015, Chesapeake Energy's EBITDA fell 80%. ONEOK's dropped just 20%, and most of that decline came from lower NGL optimization opportunities, not core fee revenue.

The capital efficiency metrics reveal management's discipline. Return on invested capital (ROIC) of 11% might not excite growth investors accustomed to 30% returns from technology companies. But consider the context: ONEOK's assets have 30-50 year useful lives, require minimal technological obsolescence risk, and generate returns through multiple commodity cycles. That 11% ROIC, sustained over decades, creates enormous value—especially when funded at 5% weighted average cost of capital, generating 600 basis points of spread.

Cash flow analysis shows where rubber meets road. Operating cash flow of $4.8 billion in 2024 funded $2.2 billion in capital expenditures, leaving $2.6 billion in free cash flow. This 54% free cash flow margin on EBITDA ranks among the best in midstream, reflecting the Magellan assets' lower capital intensity. Management allocated this free cash flow with Swiss precision: $1.6 billion to dividends, $800 million to debt reduction, $200 million to opportunistic unit buybacks.

The dividend story deserves its own chapter. At $3.96 per share annually (99 cents quarterly as of April 2024), ONEOK yields approximately 4.5% at current prices. But yield alone understates the dividend's strategic importance. The 3-5% annual growth target, modest by historical standards, reflects newfound discipline. The old ONEOK chased 10%+ dividend growth, stretching balance sheet capacity. Today's management prioritizes sustainability and flexibility over headline-grabbing increases.

Leverage metrics show the Magellan integration's financial impact. Net debt to EBITDA of 3.8x at year-end 2024 remains above management's 3.5x target but well below the 4.5x peak immediately post-acquisition. The trajectory toward target—expected by mid-2026—comes from both EBITDA growth and absolute debt reduction. Interest coverage of 5.2x provides comfortable cushion even in downside scenarios. Credit rating agencies maintain investment-grade ratings (BBB+ from S&P, Baa2 from Moody's) with stable outlooks.

Peer comparison illuminates ONEOK's market position. Enterprise Products Partners, the sector's blue chip, trades at 11x EBITDA versus ONEOK's 10x—a modest premium for EPD's superior diversification and balance sheet. Kinder Morgan, at 9x EBITDA, reflects its natural gas pipeline concentration and regulatory overhang. Williams Companies, at 10.5x, mirrors ONEOK's multiple despite less NGL exposure, suggesting ONEOK might be relatively undervalued.

The segment-level performance reveals portfolio dynamics. NGL segment EBITDA of $4.1 billion dominated contributions, but margins compressed from 42% to 39% as producer netbacks tightened. Natural Gas Gathering and Processing generated $1.2 billion EBITDA on higher volumes but lower per-unit margins as processing spreads narrowed. The Refined Products and Crude segment, contributing $1.0 billion in partial-year results, showed remarkable stability with 95% capacity utilization and minimal volume volatility.

Working capital management, often overlooked in capital-intensive businesses, has become a hidden strength. Days sales outstanding improved from 45 to 38 days through systematic collections enhancement. Inventory turns increased 20% via better NGL storage optimization. Payables management extended payment terms while maintaining vendor relationships. These improvements released $500 million in cash—equivalent to a small acquisition but without integration risk.

The forward outlook embedded in management guidance suggests continued momentum. 2025 adjusted EBITDA guidance of $6.9-7.2 billion implies 3-6% growth despite minimal growth capital deployment. This organic expansion comes from contracted volumes coming online, efficiency initiatives bearing fruit, and commercial optimization maturing. The implied 2027 EBITDA of $7.5-8.0 billion would represent a 10% compound annual growth rate from 2024—remarkable for an infrastructure company of ONEOK's scale.

But numbers only tell part of the story. The financial metrics reflect strategic choices: the decision to prioritize fee-based contracts over commodity upside, to maintain investment-grade ratings over aggressive leverage, to return capital to shareholders over empire building. These choices might limit upside in commodity bull markets but provide resilience through cycles—a trade-off that widows, orphans, and pension funds appreciate even if hedge funds don't.

IX. Playbook: Business & Investing Lessons

The conference room at ONEOK headquarters has a wall of photographs—black and white images of early pipeline construction, color shots of modern facilities, portraits of past CEOs. Terry Spencer often brings investors here, not to impress with corporate history, but to make a point: "Every picture represents a bet someone made on infrastructure that would last generations. Most of those bets paid off. The key is understanding why."

The midstream advantage starts with the most powerful force in business: necessity. You can choose not to buy an iPhone, skip your Netflix subscription, or drive a Toyota instead of a Tesla. But if you heat your home with natural gas, cook with propane, or drive a gasoline-powered car, you need midstream infrastructure. This isn't discretionary spending; it's essential service. During the 2020 pandemic, when entire economies shut down, ONEOK's pipelines kept flowing. Volume dropped 15%, not 80%. That's the difference between nice-to-have and need-to-have.

But necessity alone doesn't create value—ask any water utility trading at book value. The magic happens when necessity meets barriers to entry. Try building a new interstate pipeline today. The Keystone XL saga—over a decade of permitting battles, $8 billion spent, ultimately cancelled—shows the near-impossibility of new construction. Environmental opposition, regulatory complexity, and NIMBY resistance create what Warren Buffett calls a "moat"—except this moat is filled with lawyers, protestors, and federal judges.

ONEOK's consolidation strategy offers a masterclass in when and how to acquire. The pattern is consistent: buy during distress, integrate methodically, optimize relentlessly. The Northern Plains acquisition in 2004 came when natural gas prices were volatile and sellers desperate. The Magellan deal in 2023 happened when refined products growth was questioned and activists circled. In both cases, ONEOK paid fair prices for great assets rather than great prices for fair assets—a crucial distinction.

The integration excellence that follows acquisition separates winners from destroyers of capital. When ONEOK bought Magellan, they didn't just smash two companies together and hope for synergies. They created 47 integration workstreams, each with defined leaders, metrics, and timelines. They retained key Magellan personnel by offering retention bonuses and career paths. They communicated obsessively with customers, ensuring no service disruption. The result: $200 million in synergies achieved ahead of schedule with minimal customer attrition.

Portfolio optimization—knowing what to sell—proves as important as knowing what to buy. ONEOK's sale of three natural gas pipelines to DT Midstream for $1.2 billion seemed counterintuitive—why sell cash-flowing assets? But these pipelines, disconnected from ONEOK's core network, offered limited growth potential and consumed management attention. The proceeds, redeployed into higher-return projects and debt reduction, created more value than holding forever. Sometimes the best deal is the one you don't keep.

The commodity cycle navigation strategy deserves its own MBA course. ONEOK doesn't try to predict oil and gas prices—a fool's errand that has bankrupted countless energy companies. Instead, they structure their business to survive any price environment. When prices are high, they capture some upside through optimization activities. When prices crash, their fee-based contracts provide stability. This "heads we win, tails we don't lose much" approach lacks the excitement of leveraged commodity bets but creates sustainable value through cycles.

The importance of scale in energy infrastructure can't be overstated. ONEOK's 60,000-mile pipeline network creates network effects similar to technology platforms. Each new pipeline connection makes the entire system more valuable. Producers want to connect to ONEOK because they reach the most markets. Consumers prefer ONEOK because they access the most supply sources. This virtuous cycle—more connections creating more value creating more connections—drives organic growth without massive capital investment.

Capital allocation discipline separates long-term winners from periodic blowups. ONEOK's current framework—growth capital limited to 80% of free cash flow, 15% hurdle rates, systematic return of capital to shareholders—seems obvious in hindsight. But the energy industry graveyard is full of companies that chased growth at any cost, levered up during booms, and collapsed during busts. ONEOK's boring discipline creates exciting returns over time.

The regulatory and environmental considerations increasingly determine competitive advantage. ONEOK's proactive approach—investing in methane detection, committing to emission reductions, engaging constructively with regulators—costs money upfront but creates option value. When carbon taxes arrive (not if, but when), ONEOK's lower emission intensity will translate into competitive advantage. When pipeline permitting gets even tougher, ONEOK's operational track record will matter. This isn't virtue signaling; it's strategic positioning.

The human capital dimension often gets overlooked in infrastructure businesses. ONEOK's ability to attract and retain talent—from field operators who know every valve to commercial teams who optimize every molecule—creates sustainable competitive advantage. The company's systematic succession planning, competitive compensation, and strong safety culture mean that institutional knowledge compounds over time. When a senior pipeline operator retires, their replacement has been training for years, not weeks.

The financial engineering lessons are subtle but powerful. ONEOK's evolution from MLP structure to C-corp, from variable distribution to fixed dividend, from growth-at-any-cost to return-focused capital allocation, shows that financial structure must evolve with business strategy. The Magellan acquisition's tax benefits—$3 billion in value from basis step-up—demonstrate that how you buy matters as much as what you buy.

For investors, ONEOK offers several mental models. First, the "toll booth" model: owning essential infrastructure that charges fees for usage, similar to toll roads or airports but with higher barriers to entry. Second, the "picks and shovels" approach: profiting from activity regardless of winners and losers, like selling supplies during a gold rush. Third, the "compound returns" framework: accepting lower but more certain returns that compound over decades rather than chasing moonshots.

The bear case lessons are equally instructive. ONEOK's strategy assumes continued hydrocarbon demand for decades, a bet that energy transition advocates challenge. The company's leverage, while manageable, limits flexibility during severe downturns. The regulatory landscape could shift dramatically with political changes. Understanding these risks—and how management addresses them—is as important as appreciating the opportunities.

X. Analysis & Bear vs. Bull Case

The investment committee at a major pension fund is debating ONEOK. The energy analyst pounds the table: "This is essential infrastructure with 50-year assets generating 11% returns on capital. It's a no-brainer." The ESG specialist shoots back: "You're betting billions on fossil fuel infrastructure while the world transitions to renewable energy. It's a stranded asset waiting to happen." Both are right. Both are wrong. The truth, as always, lies in the nuanced middle.

The Bull Case: Essential Infrastructure Monopoly

Start with the moat—not the Buffett metaphor, but literal competitive advantage. Try to replicate ONEOK's infrastructure today. You'd need $60 billion in capital, decades of construction, thousands of right-of-way agreements, and regulatory approvals that might never come. The Keystone XL Pipeline spent 13 years and $8 billion trying to build one pipeline and failed. ONEOK owns hundreds of pipelines, already built, already operating, already cash-flowing. This isn't disruption-prone technology; it's physical infrastructure with no practical substitute.

The diversification post-Magellan creates resilience that bulls find compelling. Natural gas heats homes—demand rises in cold winters. NGLs feed petrochemical plants making everything from plastics to pharmaceuticals—demand tied to global GDP. Refined products fuel transportation—even with EV adoption, gasoline and diesel demand remains robust for decades. Crude oil pipelines serve refineries producing not just fuels but thousands of products. This diversification means ONEOK wins regardless of which hydrocarbon stream dominates.

The free cash flow generation story is arguably the strongest bull argument. ONEOK generates $2.6 billion in annual free cash flow on $60 billion enterprise value—a 4.3% yield. But this understates the opportunity. As growth capital needs moderate with infrastructure build-out complete, free cash flow could reach $3.5 billion by 2027. At a 5% free cash flow yield—reasonable for stable infrastructure—that implies a $70 billion enterprise value, 17% upside from current levels.

The energy transition, counterintuitively, might help ONEOK. Renewable diesel and sustainable aviation fuel require feedstocks that move through ONEOK's pipelines. Hydrogen production, whether blue (from natural gas) or green (from renewable electricity), needs transportation infrastructure—and retrofitting existing pipelines beats building new ones. Petrochemicals, essential for everything from wind turbine blades to solar panels, depend on NGL feedstocks. ONEOK isn't betting against energy transition; they're positioning to profit from it.

The consolidation opportunity remains enormous. The midstream sector includes dozens of subscale operators with aging infrastructure, limited capital access, and succession challenges. ONEOK, with its strong balance sheet and operational expertise, can acquire these assets at reasonable multiples, integrate them efficiently, and generate immediate returns. The pipeline (pun intended) of potential acquisitions could drive growth for years without stretching balance sheet capacity.

The Bear Case: Structural Decline Risk

But bears see storm clouds gathering. The energy transition isn't theoretical—it's happening. Electric vehicle adoption accelerates annually. Heat pump installations replace gas furnaces. Renewable electricity generation surpasses coal and challenges natural gas. While complete hydrocarbon elimination might take decades, demand destruction could begin much sooner. A 20% decline in refined products demand—plausible with aggressive EV adoption—would devastate utilization rates and pricing power.

The regulatory and environmental pressures intensify constantly. Carbon taxes, though not yet implemented in the U.S., seem inevitable. Pipeline permitting, already difficult, becomes impossible in many jurisdictions. Environmental litigation, once dismissed as nuisance suits, now shutters major projects. ONEOK might own great assets, but if society decides those assets shouldn't operate, ownership becomes liability, not advantage.

The leverage situation, while manageable, limits flexibility. At 3.8x net debt to EBITDA, ONEOK can handle normal volatility. But what about abnormal shocks? Another pandemic, a severe recession, or a credit market seizure could stress debt service. The company's investment-grade rating provides some cushion, but fallen angels—former investment-grade companies downgraded to junk—litter energy sector history. Leverage amplifies returns in good times but can destroy equity value in bad times.

The commodity price exposure, despite fee-based contracts, remains material. While 80% of EBITDA comes from fees, that remaining 20% tied to commodity optimization and volume variability can swing wildly. Moreover, when commodity prices crash, producers struggle, volumes decline, and even fee-based contracts face renegotiation pressure. The 2015-2016 energy crash, when ONEOK's stock fell 75%, reminds investors that fee-based doesn't mean risk-free.

The execution risk from the Magellan integration shouldn't be minimized. While early results look promising, large acquisitions often disappoint over time. Cultural clashes emerge. Key employees leave. Promised synergies evaporate. Competitors poach customers during integration disruption. The history of large M&A is littered with failures that looked successful initially. Only time will tell if ONEOK avoided these pitfalls.

Competitive Analysis

ONEOK's positioning versus peers illuminates both opportunity and challenge. Enterprise Products Partners, the sector leader with $130 billion enterprise value, trades at modest premium to ONEOK despite superior diversification and balance sheet strength. This suggests either EPD is undervalued or ONEOK is fairly priced—neither interpretation excites bulls.

Kinder Morgan, once the sector darling before a catastrophic dividend cut, now trades at a discount to ONEOK despite similar assets and improving fundamentals. KMI's valuation suggests investors remain scarred by past disappointments, a reminder that credibility, once lost, takes years to rebuild. ONEOK's steady execution maintains credibility, but one major misstep could trigger KMI-style derating.

Williams Companies, focused primarily on natural gas pipelines, offers interesting comparison. WMB trades at similar multiples to ONEOK despite less NGL exposure and fewer growth opportunities. This might suggest ONEOK's Magellan acquisition and NGL leadership deserve premium valuation not yet reflected in market pricing.

Enbridge, the Canadian giant with extensive U.S. operations, provides the bull case for patient infrastructure investing. ENB's 7% dividend yield and utility-like stability attract income-focused investors despite minimal growth. ONEOK could follow similar path—accepting lower multiple in exchange for reliable income generation.

The Verdict

The truth is that ONEOK represents a bet on the pace of energy transition. Bulls believe hydrocarbons remain essential for decades, providing ample time for ONEOK to generate returns, adapt infrastructure, and potentially pivot toward energy transition opportunities. Bears see stranded asset risk accelerating, making today's cash flows poor compensation for tomorrow's obsolescence.

For long-term fundamental investors, the key question isn't whether energy transitions—it will—but how quickly and completely. If hydrocarbon demand declines 1-2% annually, ONEOK can adapt through efficiency, consolidation, and alternative uses. If demand craters 5-10% annually, no amount of operational excellence saves stranded infrastructure. The billion-dollar question: which scenario unfolds?

XI. Future Outlook & Strategic Questions

Terry Spencer stands before ONEOK's board in March 2025, presenting his vision for 2030. The slide reads: "From Pipeline Company to Energy Solutions Platform." Half the directors look intrigued; half look skeptical. "We're not abandoning hydrocarbons," Spencer clarifies quickly. "We're expanding our definition of energy infrastructure to capture emerging opportunities while maximizing traditional assets." It's a delicate balance—evolution without revolution, adaptation without abandonment.

The hydrogen opportunity looms largest in ONEOK's future planning. The Inflation Reduction Act's production tax credits make blue hydrogen (produced from natural gas with carbon capture) economically viable. ONEOK's natural gas infrastructure could feed hydrogen plants, while their pipelines—with modifications—could transport hydrogen blends. The company's preliminary engineering studies suggest 20% hydrogen blending in existing pipelines is feasible without major modifications. Pure hydrogen transportation would require new infrastructure or substantial retrofitting, but the right-of-ways alone have enormous value.

The Gulf Coast hydrogen hub, announced with federal backing, sits perfectly within ONEOK's footprint. Their Mont Belvieu complex could become a hydrogen production and distribution center, leveraging existing storage caverns and pipeline networks. Early partnerships with industrial customers—refineries, ammonia plants, steel producers—are exploring hydrogen supply agreements. The economics remain uncertain, but the option value is enormous.

Renewable fuels present a nearer-term opportunity. Renewable diesel and sustainable aviation fuel, chemically similar to petroleum products, can flow through existing Magellan pipelines with minimal modification. ONEOK is already transporting small volumes, and management projects this could reach 5-10% of refined products volumes by 2030. The margins are attractive—renewable fuel producers pay premium rates for guaranteed transportation—and the environmental credentials help ONEOK's ESG narrative.

Carbon capture and sequestration infrastructure represents another growth vector. ONEOK's pipeline expertise translates directly to CO2 transportation. Their geological knowledge from decades of NGL storage development applies to CO2 sequestration site selection. Early-stage discussions with emitters and sequestration developers suggest ONEOK could play the same midstream role for CO2 that they currently play for hydrocarbons—gathering, transporting, and storing molecules for a fee.

But these opportunities require capital that could otherwise return to shareholders. The board debates constantly: should ONEOK be a growth company investing in energy transition or a cash cow maximizing near-term returns? Spencer's answer is nuanced: maintain discipline on traditional hydrocarbon investment while allocating 10-15% of capital toward energy transition opportunities. It's enough to build option value without betting the company.

The consolidation landscape continues evolving. Private equity, once aggressive midstream buyers, now seeks exits as fund lives expire. Strategic buyers like ONEOK have advantages—operational synergies, lower cost of capital, patient investment horizons. Spencer's team maintains a "shadow pipeline" of potential acquisitions, continuously updated with valuation estimates and integration plans. When opportunities emerge, ONEOK can move quickly and decisively.

International expansion remains conspicuously absent from ONEOK's strategy. While peers like Enterprise and Kinder Morgan pursue international projects, ONEOK remains purely North American. Spencer defends this focus: "We understand U.S. regulatory frameworks, have established customer relationships, and see ample domestic opportunities. Why accept foreign exchange risk, political uncertainty, and operational complexity for marginal returns?" It's a defensible position, but some investors wonder if ONEOK is missing global growth opportunities.

Technology and digitalization offer efficiency gains that could transform economics. ONEOK's "Digital Pipeline Initiative" envisions autonomous pipeline operations by 2030—AI-controlled compressors, self-healing pipeline networks, predictive maintenance preventing all unplanned outages. The technology exists; the challenge is implementation across 60,000 miles of aging infrastructure. Early pilots show 20-30% efficiency improvements, suggesting billions in potential value creation.

The ESG transformation extends beyond emissions reduction. ONEOK's 2030 sustainability targets include 50% emissions intensity reduction, 40% female and minority employment, and zero significant environmental incidents. These aren't just corporate responsibility goals; they're business imperatives. Institutional investors increasingly screen for ESG performance. Regulators tie permitting to environmental track records. Communities support or oppose projects based on corporate citizenship. ONEOK's social license to operate depends on ESG excellence.

Stakeholder capitalism considerations complicate traditional shareholder value maximization. ONEOK must balance investor returns with employee safety, customer reliability, community impact, and environmental stewardship. The recent Colonial Pipeline cyberattack reminds everyone that critical infrastructure companies have responsibilities beyond profit generation. ONEOK's investments in cybersecurity, physical security, and system redundancy might not generate returns but are essential for systemic stability.

The regulatory outlook remains the wildcard. A carbon tax, long discussed but never implemented, could fundamentally alter midstream economics. Pipeline safety regulations continue tightening, requiring capital investment without revenue generation. Environmental justice concerns increasingly influence permitting decisions. ONEOK's regulatory team has expanded 40% in three years, reflecting the growing importance of government relations.

What would success look like in 2030? Spencer's vision is clear: ONEOK operates the premier North American energy infrastructure platform, transporting molecules whether hydrocarbon or hydrogen, fossil or renewable. The company generates $10 billion in EBITDA, split 70/30 between traditional and transition infrastructure. Leverage stays below 3.5x, maintaining financial flexibility. Dividends grow steadily, providing reliable income to millions of retirees. The stock trades at utility-like multiples, reflecting infrastructure stability rather than commodity volatility.

But alternative futures are equally plausible. Aggressive energy transition could strand hydrocarbon assets, forcing write-downs and dividend cuts. Technological disruption—fusion energy, advanced batteries, synthetic fuels—could obsolete pipeline infrastructure. Economic recession could crater energy demand, stressing debt service and forcing asset sales. These scenarios aren't probable, but they're possible—and prudent management plans for them.

The strategic questions facing ONEOK have no easy answers. How fast will energy transition? Should they lead or follow? Is consolidation or capital return more valuable? Can they maintain hydrocarbon cash flows while building transition infrastructure? These questions will determine whether ONEOK thrives, survives, or struggles in the coming decade.

XII. Recent News## **

XII. Recent News**

The evolving ONEOK story continues to unfold with transformative deals and strategic expansions that reshape the North American energy infrastructure landscape.

EnLink Acquisition Completed (January 2025)

ONEOK completed its acquisition of EnLink Midstream on January 31, 2025, following approval by EnLink unitholders on January 30. The all-stock transaction valued at $4.3 billion saw EnLink unitholders receive 0.1412 shares of ONEOK common stock for each outstanding EnLink common unit. This follows ONEOK's October 2024 acquisition of Global Infrastructure Partners' 43% stake in EnLink for $14.90 per unit plus the managing member interests for $300 million, totaling approximately $3.3 billion.

The strategic rationale extends beyond simple consolidation. The acquisition strengthens ONEOK's integrated midstream platform with its 60,000-mile pipeline network for transporting natural gas, NGLs, refined products, and crude oil. EnLink brings critical infrastructure in the Permian Basin, Louisiana, Oklahoma, and North Texas, along with emerging CO2 transportation capabilities for carbon capture and sequestration—positioning ONEOK for energy transition opportunities.

Medallion Midstream Integration (October 2024)

ONEOK successfully completed its acquisition of Medallion Midstream from Global Infrastructure Partners for approximately $2.6 billion cash on October 31, 2024. The acquisition includes more than 1,200 miles of crude oil gathering pipelines providing approximately 1.3 million barrels per day of capacity and approximately 1.5 million barrels of crude oil storage in the Permian Basin.

This deal represents ONEOK's strategic push into crude oil infrastructure, complementing its traditional strength in natural gas and NGLs. The Medallion system, the largest privately held crude gathering network in the Permian's Midland Basin, connects directly with ONEOK's existing long-haul crude pipelines, creating immediate commercial synergies.

Texas City LPG Export Terminal Joint Venture (February 2025)

ONEOK and MPLX LP announced a joint venture to build a 400,000-barrel-per-day LPG export terminal in Texas City, Texas, along with a 24-inch pipeline connecting to ONEOK's Mont Belvieu storage facility. The project represents a total investment of $1.4 billion, with each company contributing $700 million. Expected completion is early 2028.

The terminal will primarily handle low-ethane propane and normal butane, with each company reserving 200,000 bpd for their respective customers. This project addresses the critical infrastructure gap in LPG export capacity as U.S. NGL production continues to grow, particularly from the Permian Basin.

Financial Performance Update (Q2 2025)

ONEOK reported second quarter 2025 net income of $853 million, with net income attributable to ONEOK of $841 million ($1.34 per diluted share), and adjusted EBITDA of $1.98 billion. Performance was driven by an 11% increase in Rocky Mountain region NGL raw feed throughput volumes and contributions from recent acquisitions.

Notably, ONEOK declared a quarterly dividend of $1.03 per share, or $4.12 per share annualized in July 2025, reflecting confidence in cash flow generation. The company also repaid nearly $600 million of senior notes, demonstrating commitment to deleveraging post-acquisitions.

ESG Recognition

In May 2025, ONEOK received an MSCI ESG Rating of AAA. In June 2025, ONEOK was included in the FTSE4Good Index. These recognitions validate ONEOK's environmental and governance improvements, increasingly important for institutional investors and long-term stakeholder value creation.

2025 Financial Guidance

ONEOK expects 2025 net income including noncontrolling interests midpoint of $3.45 billion, an 11% increase year-over-year, with net income excluding noncontrolling interests midpoint of $3.36 billion. The guidance includes approximately $250 million of incremental commercial and cost synergies related to acquisitions.

Total 2025 capital expenditures are expected to range between $2.8 billion to $3.2 billion, with key projects including ONEOK's Medford fractionator rebuild, Denver-area refined products expansion, the relocation of a natural gas processing plant to the Permian Basin from North Texas, and the Texas City export terminal joint ventures.

These developments collectively paint a picture of aggressive but disciplined growth, with ONEOK systematically building scale, expanding its value chain, and positioning for both traditional energy infrastructure and emerging transition opportunities. The successful integration of multiple large acquisitions while maintaining operational excellence and financial discipline will be the key test for management in the coming quarters.

XIII. Links & Resources

Company Resources - ONEOK Investor Relations: https://ir.oneok.com/ - Annual Reports & SEC Filings: https://ir.oneok.com/financial-information/sec-filings - Quarterly Earnings Presentations: https://ir.oneok.com/financial-information/quarterly-results - ESG & Sustainability Reports: https://www.oneok.com/sustainability/

Industry Analysis & Research - Energy Information Administration (EIA) - Midstream Infrastructure: https://www.eia.gov/ - Interstate Natural Gas Association of America (INGAA): https://www.ingaa.org/ - American Petroleum Institute - Pipeline Resources: https://www.api.org/ - IHS Markit Midstream Research: https://ihsmarkit.com/industry/oil-gas.html

Key Books on Energy Infrastructure - "The Quest" by Daniel Yergin - Essential reading on global energy evolution - "The Frackers" by Gregory Zuckerman - The shale revolution that transformed ONEOK's business - "Pipeline: Letters from My Father" by Peter Schoeffer - Personal account of pipeline development - "Energy Infrastructure: A Guide for Facility Managers" by Ryan Colker - Technical infrastructure overview

Regulatory & Policy Resources - Federal Energy Regulatory Commission (FERC): https://www.ferc.gov/ - Pipeline and Hazardous Materials Safety Administration (PHMSA): https://www.phmsa.dot.gov/ - Environmental Protection Agency - Oil and Gas Sector: https://www.epa.gov/controlling-air-pollution-oil-and-natural-gas-industry

Historical & Archival Materials - Oklahoma Historical Society - Oil & Gas Collection: https://www.okhistory.org/ - "History of Natural Gas in Oklahoma" - University of Oklahoma Libraries - Tulsa Historical Society - Energy Industry Archives - Corporate History Collection - Baker Library, Harvard Business School

Financial Analysis Tools & Data - S&P Capital IQ - Midstream sector analysis - Bloomberg Terminal - OKE US Equity - Morningstar Direct - Infrastructure sector comparisons - FactSet - Energy infrastructure databases

Industry Associations & Conferences - GPA Midstream Association: https://gpamidstream.org/ - North American Energy Infrastructure Summit - Hart Energy Midstream Conference Series - CERAWeek by S&P Global

Competitor Resources - Enterprise Products Partners: https://www.enterpriseproducts.com/ - Kinder Morgan: https://www.kindermorgan.com/ - Williams Companies: https://www.williams.com/ - Enbridge: https://www.enbridge.com/

Academic & Think Tank Research - Columbia University Center on Global Energy Policy - Rice University's Baker Institute for Public Policy - Energy Studies - MIT Energy Initiative - Infrastructure Research - Resources for the Future - Energy Economics

Trade Publications - Pipeline & Gas Journal: https://pgjonline.com/ - Oil & Gas Journal: https://www.ogj.com/ - Midstream Business Magazine: https://www.midstreambusiness.com/ - Hart Energy Publications: https://www.hartenergy.com/

Energy Transition Resources - International Energy Agency - Energy Transition Indicators - BloombergNEF - Energy Transition Investment Trends - Wood Mackenzie - Energy Transition Service - Rocky Mountain Institute - Carbon-Free Energy Systems