Oceaneering International: From Subsea Pioneers to Robotics Powerhouse

I. Introduction & Episode Roadmap

Picture a robot the size of a small car, tethered to a ship by a fiber-optic umbilical, working a mile beneath the Atlantic Ocean. Its manipulator arms are torquing a bolt on a subsea wellhead in near-total darkness, guided by cameras and a pilot sitting in a control room thousands of miles away in Stavanger, Norway. Now picture a nearly identical robot trundling across the Martian surface, operated by NASA engineers in Houston. The company behind both of those machines is the same: Oceaneering International.

Oceaneering generated approximately $2.8 billion in revenue in 2025, employs over ten thousand people across more than twenty countries, and operates the largest fleet of work-class remotely operated vehicles on the planet. Yet most people outside the energy industry have never heard of it.

The company does not make consumer products. It does not advertise during football games. Its customers are oil majors, navies, and space agencies. And that anonymity, paradoxically, is part of what makes the story so fascinating.

The core question driving this episode is deceptively simple: How does a company that started with a handful of commercial divers in the Gulf of Mexico in 1964 become essential infrastructure for offshore oil production, space exploration, military operations, and the emerging autonomous systems revolution?

The answer involves a sixty-year journey through boom-and-bust energy cycles, a technological pivot from human divers to undersea robots, near-death experiences during oil price collapses, and a strategic transformation that remains very much in progress.

The themes that emerge are ones any investor or operator will recognize: technical moats built over decades, the danger of dependence on a single end market, the agonizing pace of genuine strategic diversification, and the question of whether a legacy industrial company can reinvent itself as a technology platform before its original market shrinks away.

Oceaneering's story is not a neat Silicon Valley narrative of disruption. It is a story of survival, adaptation, and the compounding power of deep expertise applied in environments where failure is not an abstraction but a matter of life and death.

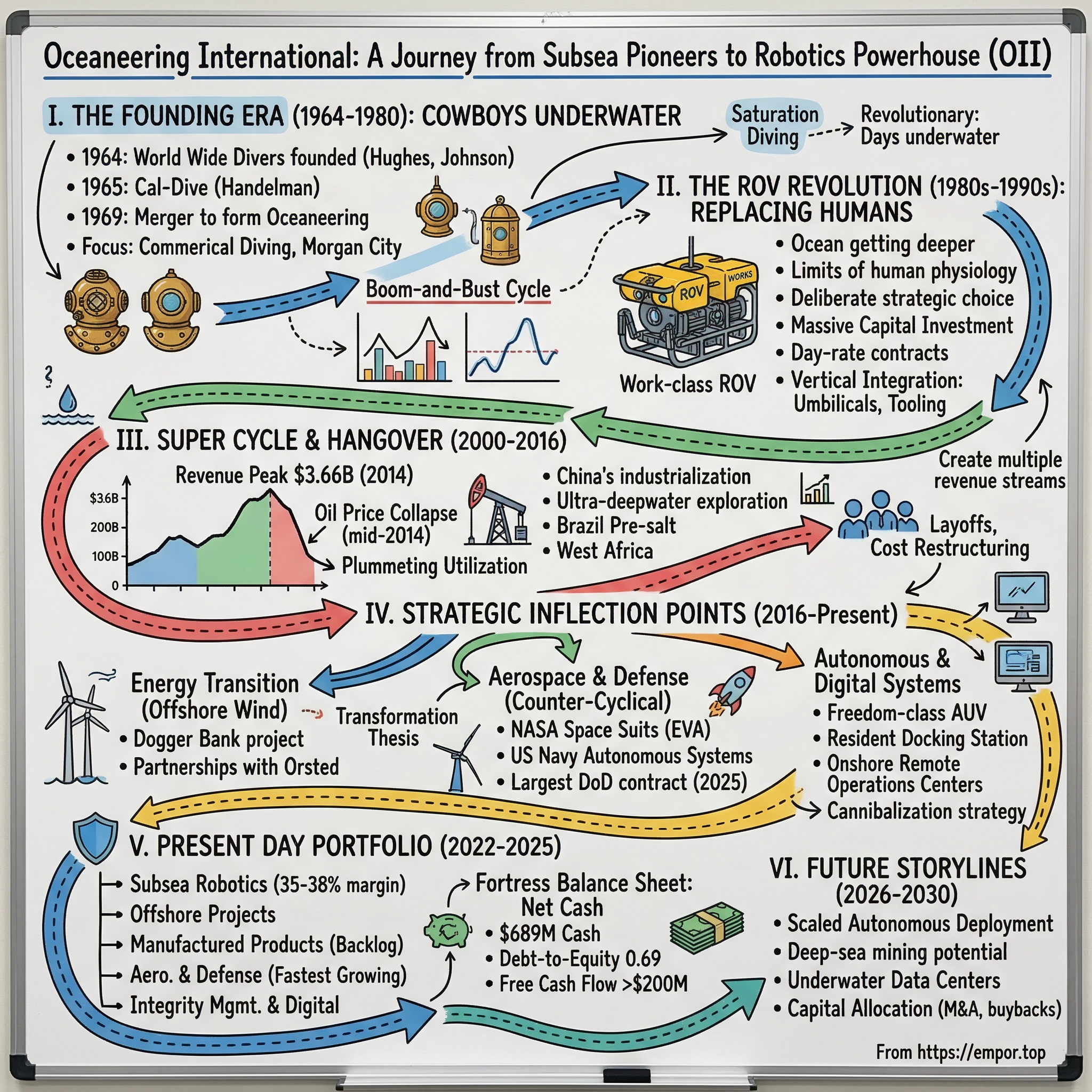

II. The Founding Era: Cowboys Underwater (1964-1980)

In the early 1960s, commercial diving in the offshore oil fields was one of the most dangerous jobs on earth and one of the least regulated. The men who did it were a particular breed: tough, adventurous, often reckless, drawn by the lure of high pay for work that terrified most people. They descended into the murky waters of the Gulf of Mexico wearing heavy brass helmets and canvas suits, breathing air pumped from the surface through rubber hoses, inspecting and repairing the legs of oil platforms in conditions that would make a modern safety inspector faint. Fatalities were grimly common. Equipment failed. Procedures were improvised. The industry attracted a cowboy culture where physical courage mattered more than formal credentials, and where the line between bravery and recklessness was drawn only in hindsight, usually after something went terribly wrong.

Morgan City, Louisiana was the epicenter of this world in the 1960s. A small town on the bayou, it became the staging ground for America's offshore oil rush, its docks crowded with supply boats, its bars full of roughnecks and divers spending money as fast as they earned it.

This was where D. Michael Hughes landed after an unlikely start. A civil engineering student at the University of Tennessee, Hughes began his diving career doing contract work for the Tennessee Valley Authority, inspecting dams and underwater structures in the freshwater rivers of Appalachia. The work was unglamorous but it taught him the fundamentals: how to work methodically in zero visibility, how to trust your equipment, how to stay calm when things went sideways underwater.

After graduation, he moved to Morgan City and plunged into the Gulf. In 1964, Hughes and John T. "Johnny" Johnson co-founded World Wide Divers, Inc. Johnson, who would remain with the company for four decades until his retirement in 2004, brought the operational grit that complemented Hughes's engineering mind.

Hughes later described the early days in his 2023 memoir "Oceaneer: From the Bottom of the Sea to the Boardroom," a book whose cast of characters includes, improbably, connections to the world's richest man, the Mafia, and the world's oldest bank robber. It was that kind of industry.

Meanwhile, on the California coast, Lad Handelman was carving out a parallel career. Handelman had risen through the ranks of California's legendary "Black Fleet" abalone divers, a community that prized physical toughness and underwater instinct.

In 1962, he joined General Offshore Divers, the first helium diving company in the United States, a crucial distinction because helium-oxygen breathing mixtures were the key innovation that would eventually enable saturation diving at depths that would kill a diver breathing compressed air. By 1965, Handelman and several of his abalone-diving partners had left to form Cal-Dive, entering the offshore oilfield diving business just as it was becoming a glamour industry, if a lethally dangerous one.

To understand why these diving companies existed, you need to understand what saturation diving made possible. The basic problem of deepwater diving is that gases dissolve into human tissue under pressure. Come up too fast, and those gases form bubbles in your blood, causing decompression sickness, known as "the bends," which can be crippling or fatal.

Traditional diving limited bottom time severely because each dive required hours of decompression. Saturation diving solved this by keeping divers under pressure for days or weeks at a time, living in pressurized chambers on the surface and commuting to the work site in diving bells. Think of it like this: if you owe a toll every time you cross a bridge, you minimize crossings. But if the toll is the same regardless of how long you stay on the other side, you stay as long as possible. Once your tissues are fully saturated with gas, you owe the same decompression time whether you have been down for one day or thirty.

It was revolutionary. It meant divers could actually do productive work at depths of several hundred feet, which was exactly where the oil industry needed them.

In 1969, the three companies merged: World Wide Divers, California Divers, and the Canadian firm Can-Dive Services Ltd. The name for the combined entity was Handelman's invention. He thought "Oceaneering" better captured what the company actually did, a neologism that blended "ocean" with "engineering," and it stuck. Hughes assumed the role of Chairman of the Board, while Handelman served as President and CEO. The partnership between Hughes and Handelman was a study in contrasts: Hughes the methodical Tennessee engineer who understood infrastructure and capital allocation, Handelman the charismatic California diver who understood people and markets. Together, they built something larger than either could have alone.

The newly formed Oceaneering International went public and grew rapidly, reaching $52 million in sales by 1975 and operating in more than twenty-four countries. The geographic expansion was driven by a simple reality: wherever oil companies were drilling offshore, they needed divers. The Gulf of Mexico was the home base, but the North Sea was booming as Britain and Norway developed their massive reserves, and new frontiers were opening in Southeast Asia, the Middle East, and West Africa. Each new region required not just divers but equipment, logistics, safety procedures, and local knowledge, an operational complexity that favored companies with scale and experience.

The 1973-1974 OPEC oil embargo, which devastated so many industries, was paradoxically a boon for offshore oil services. With oil prices spiking and the United States desperate to reduce dependence on imported crude, investment in domestic offshore exploration surged. Every additional dollar spent on offshore drilling meant more work for diving companies. Oceaneering's revenue grew sharply through the mid-1970s on the back of this spending boom.

But the good times carried the seeds of conflict. In 1978, a downturn in the oil industry hammered Oceaneering's profits, and Handelman had a falling out with the Board of Directors that forced him out of the company he had named. Less than a year later, Handelman resurrected Cal-Dive, building it to $16 million in sales before selling it to Diversified Energies in 1983. That company would eventually become Helix Energy Solutions, a significant player in the subsea industry in its own right.

The late 1970s and early 1980s were brutal for Oceaneering. The company relocated its headquarters from Santa Barbara to Houston in 1980 to be closer to the center of the oil industry, a pragmatic move that signaled where the future lay. But the offshore oil market was in a vicious downturn, and Oceaneering cycled through leadership.

Edward Wardwell succeeded Handelman, then J. Wesley Rogers took over as CEO in 1982. When Rogers died in a plane crash in 1986, the company's third leadership transition in less than a decade, John R. Huff assumed control. Huff brought a different kind of pedigree: a Rice University and Georgia Tech-trained civil engineer who had attended Harvard Business School and held positions at Western Oceanic and Zapata Offshore.

Between 1982 and 1987, the company lost approximately $70 million. Huff led a recapitalization in 1987 that stabilized the ship. By 1990, revenues had clawed back to $183 million with $10 million in net income. The company had survived, but barely.

What kept Oceaneering alive during this dark period was a combination of two things.

First, a series of acquisitions that diversified the business: Marinav Corp, a Canadian offshore surveying firm acquired in 1982 for $3 million; Steadfast Marine, a U.S. Navy search contractor purchased in 1983 and renamed the East Coast Division; and Solus Ocean Systems, acquired in 1984 in a $37 million stock swap.

Second, high-profile government work that burnished the company's technical reputation and provided revenue that did not depend on oil prices. Oceaneering participated in the underwater recovery of wreckage from the Space Shuttle Challenger disaster in 1986 and the search for Korean Air Lines Flight 007, shot down by a Soviet interceptor in 1983. These were not huge contracts, but they demonstrated a level of technical capability that few competitors could match.

These government projects planted the seeds for what would eventually become Oceaneering's Aerospace and Defense Technologies segment, a business that decades later would become the company's fastest-growing division and sign the largest initial contract in its history. The lesson was clear even then: when the oil market abandons you, having a customer that does not care about oil prices, like the U.S. government, can be the difference between survival and bankruptcy.

III. The ROV Revolution: Replacing Humans with Robots (1980s-1990s)

The single most important technological shift in Oceaneering's history began in the 1980s, and it was driven by a simple, grim reality: the ocean was getting too deep for divers. As oil companies pushed exploration beyond the continental shelf into water depths of a thousand feet, then two thousand, then five thousand, the limits of human physiology became a hard constraint. Saturation diving was dangerous enough at five hundred feet. At the depths where the industry wanted to go, it was simply impossible.

Enter the Remotely Operated Vehicle, or ROV. Think of it as an underwater drone, though the technology predates consumer drones by decades. A work-class ROV is roughly the size of a compact car, weighing several thousand pounds, equipped with cameras, lights, sonar, and manipulator arms that can perform tasks ranging from turning valves to cutting steel. It is connected to a surface vessel by a tether called an umbilical, which carries power, video, and data. The pilot sits in a control room on the ship, watching video feeds and operating the ROV's arms and thrusters with joystick-like controls. To understand the scale of what these machines do, consider that some operate at depths where the water pressure exceeds two hundred atmospheres, roughly equivalent to having a large SUV parked on every square inch of the vehicle's surface. Everything about ROV design, from the hydraulic systems to the camera housings to the electrical connectors, must withstand this crushing force while performing precision mechanical work that rivals a human hand.

For Oceaneering, the pivot from divers to ROVs was existential. The company's entire business model was built on putting human beings underwater. Now it was building a business around keeping them on the surface. This was not a gradual evolution but a deliberate strategic choice, and it required massive capital investment. A single work-class ROV system costs three to five million dollars, and operating one requires a support vessel, a crew of pilots and technicians, spare parts, and a global logistics infrastructure. The learning curve was steep: early ROV operations were plagued by mechanical failures, tangled umbilicals, and the sheer difficulty of performing complex tasks by remote control in environments where visibility might be measured in inches.

But the upside was transformative. ROVs could work at depths no diver could reach, operate around the clock without rest, and perform tasks that would be impossibly dangerous for humans. They could stay on the bottom for days or weeks at a time. They did not get the bends. They did not panic. And when they broke, the cost was measured in dollars, not lives. The business model shifted from hiring brave individuals to deploying expensive capital assets, from dive-rate billing to day-rate contracts where customers paid for the ROV and its crew by the day. The economics favored companies that could achieve high utilization rates on their fleet, spreading the fixed costs of ownership across the maximum number of billable days.

Oceaneering committed to building the world's largest ROV fleet, a strategy rooted in a straightforward insight about competitive advantage. Scale in ROV services matters because oil companies need global coverage. A subsea emergency off the coast of Angola cannot wait for an ROV to be shipped from the Gulf of Mexico.

Having the largest fleet, spread across the world's major offshore basins, meant Oceaneering could offer customers rapid response, spare capacity, and the ability to staff multiple simultaneous projects. It also meant spreading the enormous fixed costs of R&D, training, and maintenance across a larger revenue base. In an industry where the fixed costs of fleet ownership are high and the marginal cost of deploying an additional ROV day is low, the math relentlessly favors the largest operator.

Through the 1990s, Oceaneering built this fleet systematically, and the timing was perfect. Deepwater exploration was booming. Brazil's Petrobras was discovering enormous oil fields in the pre-salt formations beneath the Santos Basin. The Gulf of Mexico was pushing into ultra-deep water. West Africa, particularly Nigeria and Angola, was becoming a major offshore province. All of these markets required ROV services, and Oceaneering was there to provide them.

The company also began a critical process of vertical integration, moving beyond pure service provision into manufacturing the products that went alongside ROV operations. This meant subsea umbilicals, which deserve a moment of explanation because they are central to Oceaneering's story. An umbilical in the offshore context is not a single cable but a complex bundle of tubes, wires, and fibers, sometimes dozens of individual elements wrapped into a single sheathed assembly that can stretch for miles across the ocean floor. These umbilicals carry power, hydraulic fluid, fiber-optic communications, and chemical injection fluids from surface facilities to subsea wellheads and processing equipment. They are custom-engineered for each application, manufactured in facilities that resemble enormous rope factories, and installed in operations that require precision engineering and specialized vessels. Once installed, they become permanent infrastructure that must be maintained, monitored, and eventually replaced, creating a long-tail revenue opportunity.

Beyond umbilicals, Oceaneering built capabilities in subsea control systems, which manage the flow of oil from underwater wells, and specialized tooling, the purpose-built equipment that ROV manipulators use to perform specific subsea tasks. Every new piece of subsea hardware that Oceaneering designed and installed became a node in an expanding network of equipment that only Oceaneering fully understood how to service. This vertical integration was strategically brilliant because it created multiple revenue streams from the same customer relationship and deepened the technical moat around the business. A competitor could build an ROV, but could they also manufacture the umbilical, design the control system, build the tooling, and integrate the entire package into a functioning subsea production system? The answer, for most, was no.

By the late 1990s, Oceaneering had established itself as the clear category leader in ROV services, a position it has never relinquished. The fleet grew from dozens of vehicles to over a hundred by the early 2000s, each generating day-rate revenue that compounded into a business capable of generating hundreds of millions in annual sales. The company's revenue trajectory tells the story: from $330 million in 1996 to nearly a billion dollars by 2005. The ROV revolution had transformed a struggling diving company into a global subsea technology leader, and the vertical integration strategy had transformed a pure services company into one that owned proprietary products with recurring revenue characteristics.

IV. Diversification 1.0: Beyond ROVs (1990s-2008)

Even as the ROV business was delivering spectacular growth, Oceaneering's leadership recognized a vulnerability that would haunt the company for decades: excessive dependence on the offshore oil and gas cycle. When oil prices rose, exploration spending surged and ROV demand boomed. When oil prices fell, the cycle reversed with painful speed. The question was whether Oceaneering could build businesses that would provide revenue and earnings even when the oil market turned south.

The first major diversification move was Subsea Products, which evolved out of the vertical integration efforts of the 1990s. Oceaneering built manufacturing capabilities in umbilicals, subsea connection systems, and specialized hardware at facilities in Panama City, Florida, Rosyth, Scotland, and Houston.

Unlike ROV services, which generated day-rate revenue tied to current activity levels, Subsea Products generated project-based revenue from longer-term contracts to design and manufacture equipment for new subsea developments. The margins were higher, the revenue more predictable, and the installed base of equipment on the seabed created a stream of aftermarket service revenue that compounded over time.

Think of it as the difference between running a taxi service and manufacturing the taxis, then servicing them for their entire operational life. The taxi service revenue disappears the moment demand drops. The manufacturer has a product in the field that needs maintenance regardless of market conditions.

The second diversification vector was the Advanced Technologies segment, later renamed Aerospace and Defense Technologies. The government and military work that had kept Oceaneering alive during the dark days of the 1980s was formalized into a dedicated business unit.

The logic was compelling: Oceaneering's core competencies in operating complex robotic systems in harsh, unforgiving environments were directly transferable to space and defense applications. After all, what is space if not another extreme environment where complex machines must work flawlessly under conditions that would kill a human being?

In 2008, the company won its first major NASA spacesuit contract, a cost-plus-award-fee deal worth approximately $184 million over six years to develop components for the Constellation program's extravehicular activity systems. The contract established Oceaneering Space Systems as a credible participant in the aerospace supply chain, a position that would pay enormous dividends decades later.

Oceaneering also expanded into inspection, maintenance, and repair services, leveraging its global presence and technical workforce to offer customers ongoing support for their offshore infrastructure. And it pursued mobile offshore production systems, temporary production equipment that could be deployed to smaller offshore fields.

The diversification strategy was sound in theory, but its execution was incomplete. By the mid-2000s, Oceaneering was generating revenue from multiple business segments, but the underlying reality was that sixty to seventy percent of total revenue still depended, directly or indirectly, on the price of oil and the level of offshore exploration and production spending. The non-energy businesses were growing, but they were growing from a small base. The company had planted seeds, but the harvest was still years away.

V. The Supercycle and Its Hangover (2000-2016)

The 2000s were an extraordinary period for offshore oil services, driven by a confluence of forces that created the kind of supercycle that comes along once or twice in a century. China's industrialization was driving insatiable demand for commodities. India was not far behind. Oil prices climbed from the twenties to above one hundred dollars per barrel, and at those prices, the economics of ultra-deepwater exploration, which had always been marginal, became wildly attractive. Oil companies began sanctioning projects in water depths that would have been inconceivable a generation earlier: five thousand feet, then eight thousand, then ten thousand feet below the ocean surface. Brazil's pre-salt formations, buried under miles of water, rock, and salt, contained some of the largest oil discoveries in decades. The Gulf of Mexico's Lower Tertiary play promised enormous reserves beneath geological formations so complex that each well cost hundreds of millions of dollars. West Africa, particularly deepwater Nigeria and Angola, became a major production province. Every one of these projects required ROVs, umbilicals, subsea controls, and the full suite of services that Oceaneering provided.

The financial results were staggering. Revenue grew from $540 million in 2002 to $1.97 billion in 2008, nearly quadrupling in six years. The 2009 financial crisis caused a brief pause, but the underlying demand was so strong that growth resumed almost immediately.

Revenue reached $2.78 billion by 2012, then $3.29 billion in 2013, and an all-time peak of $3.66 billion in 2014. Net income in that peak year hit $428 million, or $4.00 per diluted share, with the highest annual operating income margin in the company's history. EPS had grown seventeen percent in a single year.

The ROV fleet expanded from 125 work-class vehicles in 2004 to 318 at its peak, with utilization rates running above eighty percent, meaning the vast majority of this enormous fleet was working and billing every day. The stock price rode this wave from single digits in the early 2000s to above eighty dollars. For shareholders who bought in 2002 and sold in 2014, it was roughly a tenfold return.

This was Oceaneering's golden age, and it felt like it would last forever.

The Subsea Products segment was also booming, with a backlog that reached all-time highs as oil companies sanctioned one ultra-deepwater project after another. Oceaneering was manufacturing umbilicals as fast as its Panama City and Rosyth factories could produce them. The combination of high day-rates for ROV services and fat margins on subsea hardware created a profitability machine. At its peak, the Subsea Products segment was generating operating margins of twenty-four percent, exceptional for an industrial manufacturing business. In Q3 2012 alone, the company reported record quarterly earnings on revenue of $734 million, with Subsea Products margins at an all-time high.

And then the floor dropped out.

Starting in mid-2014, oil prices began a collapse that would take crude from above one hundred dollars to below thirty dollars per barrel by early 2016. The causes were structural: surging U.S. shale production, OPEC's decision to maintain output to defend market share, and slowing demand growth in China.

For onshore shale producers, the downturn was painful but survivable. Shale wells have short cycle times and can be restarted quickly when prices recover. For offshore oil, the impact was devastating. Offshore projects have long lead times, high upfront costs, and multi-year development cycles. When oil companies slashed capital budgets, offshore spending was the first casualty because it was the easiest to defer.

For Oceaneering, the consequences cascaded through every business line. ROV utilization plummeted as drilling rigs were stacked and subsea construction projects were deferred. Subsea Products saw order cancellations and backlogs evaporate.

Revenue fell from the 2014 peak of $3.66 billion to $2.27 billion in 2016 and continued declining to $1.92 billion in 2017, nearly halving in three years. The company swung from record profits to operating losses. The stock cratered from above eighty dollars to the low teens, destroying billions in shareholder value.

Management responded with the playbook that every cyclical company reaches for in a downturn: layoffs, cost restructuring, and fleet optimization. ROVs were stacked, parked idle in yards around the world, their maintenance costs eating into cash flow. Non-essential capital expenditure was eliminated. The workforce shrank as thousands of experienced engineers and technicians were let go, people with decades of specialized knowledge who could not easily be replaced.

The human cost was substantial. Oceaneering had cultivated a culture of technical excellence and loyalty over decades. Many employees had spent their entire careers with the company, progressing from junior ROV pilots to supervisors to project managers. The layoffs broke something in that culture, a sense of mutual commitment that is easy to destroy and hard to rebuild. Competitors faced the same pressures, and the industry-wide carnage reshaped the competitive landscape. Companies merged, smaller players exited, and those who survived emerged leaner but fundamentally scarred by the experience.

But the 2014-2016 downturn was different from previous oil busts in a crucial respect. For the first time, serious questions emerged about whether offshore oil would ever fully recover. The shale revolution had demonstrated that enormous volumes of oil could be produced onshore, at lower cost, with shorter development timelines. The Paris Agreement on climate change, signed in 2015, signaled a global commitment to reducing fossil fuel consumption. The early stirrings of the energy transition, with growing investment in renewables and tightening emissions regulations, raised the possibility that offshore oil's best days were permanently behind it. This was not just a cyclical downturn. It felt structural. And that changed the strategic calculus for Oceaneering's leadership.

VI. Inflection Point #1: The Strategic Pivot Begins (2016-2018)

The years immediately following the oil crash forced a reckoning at Oceaneering that went far beyond cost-cutting. The question confronting the board and senior management was existential: Was Oceaneering fundamentally an oil services company riding an industry in secular decline, or was it something more, a robotics and engineering company whose capabilities happened to have been forged in the offshore oil business?

Rod Larson, who took over as CEO in 2017, came to embody the transformation thesis. Larson was not an outsider brought in to shake things up. He was a company veteran who had risen through the ranks, giving him credibility with the engineering-heavy workforce that an external hire would have struggled to earn. But his vision was genuinely different from his predecessors. In earnings calls and industry interviews, he reframed the way Oceaneering described itself. The company, he argued, was not really in the oil business. It was in the business of operating complex robotic systems in extreme environments, of engineering solutions for problems where failure was not an option, of providing expertise at the intersection of hardware, software, and human judgment. As he put it in one interview, the focus needed to shift from "the cheapest barrels" to the "cleanest, safest barrels," and ultimately beyond barrels entirely. If that description sounded like it could apply to Mars as easily as to the Gulf of Mexico, that was precisely the point.

Larson liked to describe Oceaneering's future as "hybrid oil and gas," a company that would help develop fossil fuel fields in the most environmentally responsible way possible while simultaneously building capabilities in entirely new markets. It was a pragmatic vision that acknowledged the reality of the energy transition without abandoning the core business that still generated the majority of revenue and cash flow. The transformation would be funded by the oil business, not a replacement for it.

Larson's strategic framework centered on several pillars.

First, accelerate growth in non-energy markets by leveraging capabilities that were directly transferable: robotics expertise for defense applications, precision engineering for aerospace, remote operations for any industry where sending humans to the work site was dangerous, expensive, or impossible.

Second, continue investing in the core offshore business, but with a focus on efficiency, technology, and the emerging opportunities in offshore wind and decommissioning. The oil business would fund the transformation, not be abandoned.

Third, build out digital capabilities, from data analytics to autonomous systems, that could create new revenue streams and differentiate Oceaneering from competitors stuck in the old service-company model.

One of the more unexpected manifestations of this strategy was Oceaneering's entertainment systems business. The same engineering capabilities that enabled the company to build complex robotic systems for the deep ocean turned out to be applicable to theme park attractions. Oceaneering built animatronic figures, flying rigs for superhero-themed rides, and other entertainment hardware for major theme park operators.

There was something delightfully incongruous about a company whose primary customers were oil majors and the U.S. Navy also building the mechanism that made Spider-Man fly through the air at Universal Studios. The same engineers who designed manipulator arms for ROVs working at four thousand meters of depth were designing motion systems for animatronic dinosaurs. It was a vivid demonstration that Oceaneering's capabilities were genuinely transferable.

The entertainment business was eventually divested in May 2025 when Oceaneering sold it to Falcon's Beyond, a decision that reflected a strategic narrowing of focus toward higher-value industrial and defense applications. Not every diversification bet works, and knowing when to exit is as important as knowing when to enter.

The Aerospace and Defense Technologies segment, by contrast, became central to the transformation story. Building on the NASA spacesuit contracts and military work that dated back decades, Oceaneering pursued government contracts with increasing aggression.

The logic was straightforward: government and defense spending is counter-cyclical to oil prices, the technical requirements map closely to Oceaneering's existing capabilities, and the contracts tend to be long-term and sticky. A company that could operate robots at four thousand meters of ocean depth had credibility it could not manufacture when bidding for contracts to build underwater mine countermeasures systems or maintain International Space Station hardware.

The defense opportunity was also growing rapidly. As the U.S. Navy and other military forces shifted toward unmanned and autonomous systems, the demand for companies with deep expertise in remote-operated and autonomous vehicles was expanding. Oceaneering's decades of experience building and deploying robots in the most extreme underwater environments on earth made it a natural fit for a defense establishment that was increasingly interested in unmanned underwater vehicles for mine detection, surveillance, and other missions.

The cultural challenge of this transformation should not be underestimated. For decades, Oceaneering had recruited, trained, and promoted people who identified as part of the oil and gas industry. Telling them they now worked for a "diversified robotics and technology company" required more than a press release. It required different hiring profiles, different sales processes, different risk frameworks, and a willingness to compete in markets where Oceaneering was the newcomer rather than the established leader. Selling ROV services to a Chevron procurement team that had worked with Oceaneering for twenty years was fundamentally different from bidding on a Department of Defense contract against Lockheed Martin.

VII. Inflection Point #2: Offshore Wind and the Energy Transition (2018-2021)

While Oceaneering's leadership was debating internal transformation, the external energy landscape was undergoing its own revolution. Europe and Asia were making massive commitments to offshore wind power. The United Kingdom's waters were being dotted with wind farms of increasing scale. Germany, the Netherlands, Denmark, and Taiwan were all investing heavily. And the realization dawned on Oceaneering and its competitors that offshore wind infrastructure required many of the same subsea services as offshore oil: installation, inspection, maintenance, and repair of underwater structures, cables, and foundations.

The parallels were striking. Offshore wind turbines stand on foundations driven into the seabed, connected by submarine power cables that need to be surveyed, laid, and maintained. The structures are subject to the same harsh marine environment, biofouling, corrosion, and storm damage, that offshore oil platforms endure.

ROVs and autonomous underwater vehicles are used to inspect foundations, check cable integrity, and perform maintenance that would be impossible from the surface. Oceaneering's core toolkit was directly applicable. The same ROV that inspected a subsea wellhead for Shell could inspect a wind turbine foundation for Orsted. The same umbilical manufacturing expertise that produced power and control cables for deepwater oil could produce submarine power cables for wind farms.

There were important differences, however, that made offshore wind attractive in ways that offshore oil could never be.

Offshore wind projects tend to be more predictable and less cyclical than offshore oil. Wind farm operators commit to twenty-five-year operating lives and need maintenance services for the entire period. Government subsidies and long-term power purchase agreements provide revenue visibility that the oil industry, with its commodity price volatility, cannot match.

For a company trying to reduce its exposure to oil price swings, offshore wind was almost too good to be true.

Oceaneering positioned itself as an early mover in the offshore wind services market, establishing partnerships with wind developers and turbine manufacturers and focusing geographically on the most active markets: the United Kingdom, continental Europe, Taiwan, and the emerging U.S. offshore wind industry. Between 2023 and early 2024, the company completed a yearlong maintenance program for the Dogger Bank A Wind Farm, the world's largest, covering ninety-five turbines, offshore substations, and cable infrastructure. It was precisely the kind of reference project that demonstrated capability and opened doors for future contracts.

The offshore wind push also contributed to a broader narrative shift. Oceaneering began positioning itself not as an "oil services company" but as an "energy services company," a subtle but important distinction that resonated with ESG-minded investors and opened the company to a broader investor base. The rebranding was more than cosmetic. It reflected a genuine strategic reorientation that touched everything from the company's investor presentations, which began featuring wind turbines alongside drilling rigs, to its hiring practices, which increasingly sought candidates with renewable energy experience.

But the pace of change was slower than the most optimistic projections. The U.S. offshore wind market, which many expected to boom during this period, was plagued by permitting delays, rising interest rates, and project cancellations as developers struggled to make the economics work with inflation-era costs. European markets were more mature but also faced headwinds. Non-energy revenue grew as a share of total sales, eventually approaching thirty percent, but the core business remained firmly rooted in offshore oil and gas. The energy transition was providing new opportunities, real ones with real revenue, but it was not yet transformative enough to change the fundamental character of the company.

VIII. Inflection Point #3: Autonomous Systems and Digital (2019-Present)

Perhaps the most intriguing dimension of Oceaneering's transformation is the one that is least understood by the market: the company's push into autonomous underwater systems. The insight driving this effort is simple but powerful. Oceaneering has been building and operating underwater robots for over forty years. The next generation of those robots does not need a human pilot. It does not need a surface vessel. It can live permanently on the seabed, recharging from a docking station, performing inspections and interventions autonomously, transmitting data back to shore. If you are an investor trying to figure out the future of subsea operations, this is the bet that matters most.

The centerpiece of Oceaneering's autonomous strategy is the Freedom-class Autonomous Underwater Vehicle, developed over a five-year program in collaboration with oil majors Chevron, Equinor, and TotalEnergies. The Freedom AUV entered commercial operations in 2023 and won the Innovation Award at TotalEnergies' 2024 Supplier Day.

Unlike traditional AUVs that are designed primarily for survey work, essentially underwater drones that swim a preprogrammed path collecting data, the Freedom is built to combine the data collection capabilities of an AUV with the intervention capabilities of an ROV. It can perform tool changes, recharge, and offload data at a subsea docking station without being recovered to the surface.

This is a meaningful advance because vessel costs are one of the largest expense items in subsea operations. A typical subsea support vessel costs tens of thousands of dollars per day to charter, crew, and operate. Eliminating the need for that vessel, by having an autonomous robot that lives on the seabed and performs its work independently, fundamentally transforms the economics of routine inspection and maintenance.

Complementing the Freedom AUV is the Liberty Resident Docking Station, a fully self-contained subsea infrastructure node with 550 kilowatt-hours of battery power that communicates with Oceaneering's Onshore Remote Operations Centers via integrated buoy or subsea connections.

One Liberty system deployed on the Norwegian Continental Shelf has accumulated nearly twenty-one thousand operational hours and saved over eight hundred fifty vessel days. Eight hundred fifty saved vessel days, at typical charter rates, represents tens of millions of dollars in cost avoidance for the customer. That kind of value proposition does not require a salesperson to explain. The math sells itself.

The Isurus ROV, designed for harsh environments with severe currents and challenging operating conditions, is specifically marketed for renewable energy applications.

Since commencing operations in late 2019, it has achieved zero downtime due to breakdown and increased operating windows by up to six hours per day compared to conventional systems. In the wind industry, where weather windows are narrow and vessel costs are high, those extra six hours per day translate directly into faster project completion and lower costs.

On the surface, Oceaneering acquired a DriX uncrewed surface vessel from Exail for deepwater geophysical and asset inspection operations. It also upgraded its Ocean Intervention II vessel in early 2025 to serve as a cloud-connected "mothership" capable of coordinating USVs and AUVs simultaneously, a floating command center for autonomous operations.

The company has established four Onshore Remote Operations Centers in the United States, United Kingdom, Brazil, and Norway, creating a global network for remote piloting and monitoring. These centers represent a fundamental shift in how subsea work is performed. Instead of a pilot sitting in a control van on a pitching ship in the North Sea, the pilot sits in a climate-controlled office in Stavanger or Houston, operating the same equipment with the same precision but without the fatigue, seasickness, and crew rotation logistics that make offshore work so expensive.

The digital layer is equally important. In October 2024, Oceaneering acquired Global Design Innovation Ltd. for approximately $33 million, adding AI-powered remote visual inspection capabilities and the only UKAS-certified provider of remote inspections using point cloud data and photographic images.

The company's Vision platform provides interactive 2D/3D digital twin workspaces for subsea infrastructure, enabling real-time collaboration, anomaly tagging, and condition-based maintenance planning. Think of it as Google Maps for the ocean floor: a digital replica of every piece of subsea infrastructure that Oceaneering has inspected, complete with historical data, wear patterns, and predictive maintenance schedules.

The defense application of these autonomous capabilities is also accelerating. The U.S. Navy selected Oceaneering to build a Freedom AUV and Onshore Remote Operations Center through the Defense Innovation Unit, a program aimed at autonomous sensing in undersea environments.

This is not coincidental. Autonomous underwater vehicles are becoming increasingly central to naval strategy as mine countermeasures, intelligence, surveillance, and reconnaissance capabilities shift from manned platforms to unmanned systems. The geopolitical environment, with rising tensions in the South China Sea, the submarine arms race, and growing concern about undersea infrastructure vulnerability, is creating defense demand that aligns precisely with Oceaneering's technological trajectory.

The long-term vision is for Oceaneering to evolve from a company that operates robots underwater to a company that deploys autonomous systems across multiple domains: subsea, surface, space, and defense. The common thread is expertise in robotics, remote operations, and harsh-environment engineering.

Whether the market will recognize and value this transformation is one of the central investment questions surrounding the stock. The risk is that Oceaneering remains permanently categorized as "oil services" and trades at oil services multiples, even as the composition of its revenue and capabilities shifts decisively toward technology and defense.

IX. Present Day: Portfolio and Performance (2022-2025)

Oceaneering's current business is organized into five reporting segments, each representing a different facet of the company's capabilities and strategy. Understanding these segments and their relative economics is essential for any investor trying to model the company's future.

Subsea Robotics, the largest segment at approximately $855 million in 2025 revenue, encompasses the traditional ROV services business along with the newer AUV and USV operations. The segment currently operates a fleet of around 250 work-class ROVs with utilization rates in the sixty-two to sixty-seven percent range and average revenue per day utilized of approximately $11,200, up seven percent year over year. The segment's operating margins run in the thirty-five to thirty-eight percent range, the highest of any business unit, reflecting the pricing power that comes with operating the world's largest fleet in an oligopolistic market.

The Offshore Projects Group, generating approximately $616 million, provides vessel-based intervention, installation, and construction services. This is the segment most directly tied to active offshore development activity and therefore the most sensitive to E&P capital spending cycles.

Manufactured Products, at roughly $569 million, produces subsea umbilicals, clamps, connectors, and other hardware from facilities in Florida, Scotland, and Texas. This segment benefits from the long-term nature of subsea development projects, with backlog providing multi-year revenue visibility.

Aerospace and Defense Technologies, the fastest-growing segment, generated approximately $460 million. This is the segment investors should watch most closely for evidence of the diversification thesis working.

And Integrity Management and Digital Solutions, at about $284 million, provides asset integrity inspection, digital analytics, and software services. Though the smallest segment, IMDS plays a critical role in the digital transformation strategy and carries the company's Vision digital twin platform and AI-powered inspection capabilities.

The financial recovery since the 2020 trough has been steady and accelerating. Revenue grew from $1.83 billion in 2020 to $2.8 billion in 2025, marking five consecutive years of growth. Adjusted EBITDA reached $401 million in 2025, the seventh consecutive year of EBITDA growth, a remarkable streak that spans both the COVID-era oil price collapse and the subsequent recovery.

Free cash flow more than doubled to $208 million, demonstrating the operating leverage inherent in a business with high fixed costs and improving utilization. The balance sheet has been transformed: year-end cash stood at $689 million against total debt of approximately $483 million, putting the company in a net cash position for the first time in years.

The debt-to-equity ratio improved from 1.68 in 2021 to 0.69 in 2025, a dramatic deleveraging that gives management financial flexibility they have not had in a decade. This matters enormously for a cyclical company: having a fortress balance sheet heading into a potential downturn is the difference between playing offense, making acquisitions, investing in growth, and buying back stock at depressed prices, versus playing defense and hoping to survive.

Total backlog at year-end 2025 stood at $2.7 billion, providing meaningful revenue visibility. The order activity was broad-based: $180 million in Petrobras ROV contracts, a large riserless light well intervention contract from bp in the Caspian Sea, and multiple umbilical awards. In a single quarter, the company booked $854 million in inbound orders, a book-to-bill ratio that suggests continued growth ahead.

But the headline development of 2025 was the Department of Defense contract awarded in March for a maritime mobility system, described by management as the largest initial contract value in Oceaneering's history. While the exact dollar value was not disclosed, the multi-year nature and Oceaneering's characterization suggest it is transformative for the ADTech segment.

Combined with a $33 million five-year Virginia-class submarine support contract and an $86 million Navy corporate component repair program, the defense business is building a backlog that extends beyond the company's traditional five-year planning horizon. For a company that spent decades pitching itself as an oil services player, having its largest-ever contract come from the Department of Defense tells you everything you need to know about how far the transformation has come.

For 2026, management guided for low to mid-single-digit revenue growth, EBITDA of $390 million to $440 million, and free cash flow of $100 million to $120 million.

The lower free cash flow guidance reflects higher capital expenditure of $105 million to $115 million as the company invests in growth, particularly in autonomous systems and defense capabilities. ADTech is expected to be the primary growth engine, with energy-facing segments softer in the first half before improving in the second half.

X. Business Model Deep Dive

Oceaneering's business model sits at the intersection of capital intensity and specialized expertise, a combination that creates both barriers to entry and the cyclical vulnerability that has defined the company's financial history. Understanding how this model generates returns, and where it is vulnerable, is critical for assessing the investment case.

The ROV services business, which remains the economic engine, operates on a day-rate model. Revenue equals the number of ROVs deployed, multiplied by the number of days they work, multiplied by the rate charged per day.

This creates a leverage equation that amplifies both booms and busts. When utilization rates are high and day-rates are strong, the fixed costs of maintaining the fleet are spread across more revenue days, and incremental margins are enormous. When utilization drops, those same fixed costs become a drag on profitability.

To put this in concrete terms: the difference between sixty percent and seventy-five percent utilization on a 250-vehicle fleet, at $11,000 per day, represents hundreds of millions in annual revenue, almost all of which flows to the bottom line because the incremental cost of deploying an already-maintained ROV is modest. This is why ROV utilization rate is the single most important operating metric for understanding Oceaneering's near-term earnings trajectory.

The Manufactured Products segment operates on a project basis, with revenue recognized as umbilicals and other equipment are designed, built, and delivered. These projects tend to be lumpy, with large orders creating revenue peaks and valleys that can make quarterly results volatile. But the margins are attractive, and the installed base of Oceaneering equipment on the world's seabeds creates a recurring aftermarket revenue stream as customers need replacements, upgrades, and maintenance.

Government contracts in the ADTech segment operate under a mix of cost-plus and fixed-price structures. Cost-plus contracts, where the government reimburses costs plus a negotiated fee, provide lower risk but also lower margin. Fixed-price contracts offer higher potential returns but carry execution risk. The government contracting business has fundamentally different characteristics from the energy business: longer sales cycles, more bureaucratic procurement processes, and different competitive dynamics. But it provides valuable counter-cyclicality and, increasingly, a growth trajectory that is independent of oil prices.

The cyclicality challenge remains Oceaneering's Achilles heel. Despite the diversification progress, an estimated sixty to sixty-five percent of revenue still ties back to offshore oil and gas spending. The correlation between Oceaneering's financial performance and oil prices and E&P capital budgets remains strong. The ADTech segment, now roughly sixteen percent of total revenue, provides a meaningful buffer but is not yet large enough to fully offset a severe downturn in energy-facing segments.

The competitive landscape reinforces the durability of Oceaneering's position but also highlights its constraints. The ROV services market is effectively an oligopoly, with Oceaneering, TechnipFMC (which owns Schilling Robotics, the dominant supplier of ROV manipulator arms), and a handful of other players including DOF Group, Fugro, and the soon-to-be-merged Saipem-Subsea 7 entity.

The barriers to entry are substantial: building a global ROV fleet requires hundreds of millions in capital, developing safety records and certifications takes years, and the long-term relationships with oil majors cannot be manufactured overnight. An interesting nuance here is TechnipFMC's position: through its Schilling Robotics subsidiary, it supplies the manipulator arms used on nearly every work-class ROV in the industry, including Oceaneering's. This creates a supplier dependency that Oceaneering manages through long-term supply agreements and its own vertical integration efforts, but it is a dynamic worth noting.

XI. Competitive Position: Porter's Five Forces and Hamilton's Seven Powers

The competitive dynamics of Oceaneering's markets reveal a business with genuine but not impregnable advantages.

Competitive rivalry in the ROV services market is moderate to high. The market is consolidated among a handful of major players, but pricing discipline evaporates during downturns when operators compete aggressively for a shrinking pool of work. During the 2014-2016 crash, day-rates fell sharply as companies with stacked ROVs undercut each other to maintain utilization. In boom periods, the dynamics reverse, and pricing power returns.

The competitive landscape is also in flux. The February 2025 announcement of a binding merger between Saipem and Subsea 7, creating a combined entity with approximately EUR 21 billion in revenue and a $43 billion backlog, would reshape competitive dynamics significantly. However, the merger faces opposition from ExxonMobil, Petrobras, and TotalEnergies on antitrust grounds, reflecting customer concerns about reduced competition in subsea services. If the merger proceeds, the resulting entity would be a formidable competitor in vessel-based subsea construction, though Oceaneering's ROV-centric model is differentiated enough that the direct competitive impact may be limited.

Barriers to entry remain high in traditional subsea services. A work-class ROV system costs three to five million dollars. Oceaneering's fleet of 250-plus vehicles represents hundreds of millions in deployed capital. Beyond the hardware, the safety certifications, trained pilots, global logistics infrastructure, and customer relationships take years to develop. Oceaneering's 99 percent ROV uptime rate in 2024 and its total recordable incident rate of 0.29, with a 56 percent reduction in high-potential incidents, represent operational benchmarks that new entrants cannot quickly match. However, technology startups in autonomy and software can enter adjacent spaces without replicating the full ROV fleet, creating a different kind of competitive threat from below.

Buyer power is high. Oil majors and large E&P companies are sophisticated, price-sensitive purchasers who run competitive tenders for virtually every significant contract. During downturns, the pricing pressure is brutal, with customers renegotiating existing contracts and demanding rate reductions. The partial offset is that technical requirements and safety qualifications create meaningful switching costs, and long-term framework agreements provide some revenue stability.

The threat of substitutes is moderate and growing, but here Oceaneering's strategy is particularly clever. The primary substitutes for traditional ROV services are autonomous systems, resident subsea vehicles, and remote operations, precisely the technologies Oceaneering is investing in most aggressively. By developing the substitutes itself, the company aims to cannibalize its own business before competitors do, a classic innovator's dilemma strategy. The risk is that pure-play robotics startups or defense technology companies could develop superior autonomous platforms, but Oceaneering's decades of operational data and customer relationships provide a meaningful head start.

Through the lens of Hamilton Helmer's Seven Powers framework, Oceaneering's most durable competitive advantages are scale economies, process power, and cornered resources.

The scale economies are straightforward: the world's largest ROV fleet provides global coverage, fixed cost absorption, and spare capacity that smaller competitors cannot match. When a customer needs three ROVs in Brazil, two in Angola, and one in the Gulf of Mexico, all at the same time, the list of companies that can deliver is very short.

Process power is perhaps the most underappreciated advantage. Fifty-plus years of operating complex robotic systems in safety-critical environments have embedded operational excellence into the company's DNA in ways that cannot be easily replicated. This shows up in uptime metrics, safety records, project execution, and the ability to operate twenty-four-seven across six continents. Oceaneering's total recordable incident rate of 0.29 and its ninety-nine percent ROV uptime rate are not numbers that can be achieved by reading a manual. They reflect thousands of small improvements made over decades, each one driven by an incident, a near-miss, or a lesson learned the hard way.

Cornered resources include the deep expertise of the workforce, the intellectual property portfolio in subsea technology, and the hard-won relationships with NASA, the Department of Defense, and major oil companies that took decades to build. These assets do not appear on the balance sheet, but they represent some of the most valuable and difficult-to-replicate competitive advantages the company possesses.

Network effects are weak, as the subsea services market does not have platform dynamics. There are emerging data network effects, more equipment deployed means more operational data, which feeds better predictive maintenance and autonomous algorithms, but these are nascent and have not yet created meaningful competitive differentiation. Switching costs are moderate to high due to proprietary control system interfaces, safety qualifications, and multi-year framework agreements. When an oil major integrates Oceaneering's ROVs into its operations on a particular field, the crew training, operating procedures, and equipment compatibility create friction that makes switching painful. But switching does happen, especially during downturns when price trumps convenience. Counter-positioning is moderate and perhaps growing: Oceaneering is pivoting into autonomous systems and defense faster than some traditional competitors, who may be reluctant to cannibalize their existing vessel-based service businesses. The Saipem-Subsea 7 merger, if consummated, would create a massive integrated subsea contractor, but one whose business model remains anchored in the traditional vessel-and-crew paradigm that autonomous systems could eventually disrupt. Brand power is moderate, strong within the industry but not a decisive factor in procurement decisions that are ultimately driven by price, capability, and availability.

One framework element worth lingering on is counter-positioning, because it captures the most interesting strategic dynamic in Oceaneering's story. The company is simultaneously the industry incumbent and the would-be disruptor. Its autonomous systems, remote operations centers, and resident subsea vehicles are designed to reduce the need for the very surface vessels and deployed ROV crews that generate the majority of its current revenue. This creates a classic innovator's dilemma: do you cannibalize your own profitable business to build the future, or do you protect the status quo and let someone else eat your lunch? Oceaneering has chosen cannibalization, which is the historically correct strategic choice but one that creates short-term financial tension as old revenue streams are displaced before new ones reach scale.

XII. The Bull/Bear Debate and Key Questions

The bear case for Oceaneering starts with the math of energy exposure. Despite years of diversification effort, roughly sixty to sixty-five percent of revenue is still tied to offshore oil and gas. If the energy transition accelerates and offshore oil enters structural decline, the company's core business shrinks permanently.

The 2014-2016 downturn demonstrated how quickly revenue can collapse when the oil market turns, and there is no guarantee that the next cycle will be followed by a recovery. The secular argument against offshore oil is straightforward: onshore shale is cheaper, faster to develop, and faces fewer regulatory hurdles. Renewable energy costs continue to decline. Climate policy is tightening globally. Each of these trends reduces the long-term addressable market for traditional offshore oil services.

Bears also point to the capital intensity of the business: heavy assets in a cyclical industry translating to volatile returns on capital. The ROV fleet, the manufacturing facilities, the vessels, these are expensive assets that generate strong returns at the peak but become dead weight at the trough. And the execution risk inherent in the transformation strategy cannot be dismissed.

Diversification is hard. Many companies that attempt it destroy shareholder value. Oceaneering's entertainment systems business, ultimately divested, is a cautionary reminder that not every adjacency works. In new markets like aerospace and defense, Oceaneering is competing against entrenched players: Lockheed Martin, Northrop Grumman, L3Harris, and other defense primes with resources and relationships that dwarf Oceaneering's ADTech segment.

The bull case is built on three pillars.

First, the market still categorizes Oceaneering as an oil services company and is therefore undervaluing the robotics, autonomy, and defense capabilities that represent the company's future. The ADTech segment, growing faster than any other business unit and backed by the largest initial contract in company history, is a differentiated asset that few peer companies possess. If the market were to re-rate Oceaneering's defense business at defense industry multiples rather than oil services multiples, the implied value would be meaningfully higher.

Second, the autonomous systems strategy positions Oceaneering to capture a secular trend in unmanned systems that transcends any single end market. Freedom-class AUVs, resident subsea systems, and remote operations centers are not cyclical oil plays; they are technology platform investments that apply across energy, defense, and other domains. The total addressable market for autonomous underwater systems is growing rapidly, and Oceaneering has a head start that pure-play startups cannot easily replicate.

Third, the balance sheet and cash flow trajectory have improved dramatically, with the company now in a net cash position and generating over $200 million in annual free cash flow, providing flexibility for acquisitions, share repurchases, or continued investment in growth.

There is also meaningful optionality in several emerging areas that the market may not be pricing in. Deep-sea mining, while still awaiting regulatory approval from the International Seabed Authority, represents a potentially enormous total addressable market for the exact capabilities Oceaneering possesses. Polymetallic nodules containing nickel, copper, cobalt, and rare earth elements sit at ocean depths of four thousand to six thousand meters, precisely where Oceaneering's deep-rated work-class ROV fleet operates. The International Seabed Authority's negotiations on the Mining Code through 2025 failed to reach consensus, but the underlying demand for these critical minerals, essential for batteries, electronics, and defense applications, grows stronger each year. If regulations eventually permit commercial exploitation, companies with deep-ocean operational capability would be positioned for a market that some estimates value in the trillions.

Underwater data centers represent another intriguing possibility. Microsoft's Project Natick demonstrated that sealing servers in pressurized vessels and sinking them to the ocean floor improved reliability, reduced cooling costs, and enabled deployment near coastal population centers. If the concept achieves commercial scale, the installation, inspection, and maintenance of underwater data center infrastructure would require precisely the kind of subsea engineering that Oceaneering has been performing for decades. Decommissioning of aging offshore infrastructure is perhaps the most certain of the emerging opportunities. Thousands of offshore platforms and wells in the Gulf of Mexico, the North Sea, and other mature basins are approaching end of life. Regulatory requirements mandate their removal, creating a multi-decade, multi-billion-dollar market for companies with the technical capability to safely dismantle and remove structures that were built to last but not to last forever.

The key uncertainties center on three questions.

Can Oceaneering grow its non-energy revenue fast enough to offset potential decline in offshore oil spending? Will the autonomous systems bet translate into large-scale commercial deployment, or remain a promising technology that struggles to cross the chasm from pilot projects to widespread adoption? And can the company's capital allocation, balancing investment in growth with returns to shareholders, deliver attractive risk-adjusted returns through the cycle?

There is also a myth versus reality dimension worth addressing. The consensus narrative is that Oceaneering is "just another oil services company." The reality is more nuanced. With ADTech contributing roughly sixteen percent of revenue and growing, with autonomous systems in commercial deployment, and with the largest-ever contract coming from the Department of Defense rather than an oil major, the company's identity is genuinely shifting. Whether the shift is fast enough is debatable. But the direction is not.

For investors tracking Oceaneering's ongoing performance, two KPIs matter most.

The first is ROV utilization rate, which is the single best real-time indicator of offshore activity levels and pricing power. The difference between the mid-sixties and mid-seventies in utilization has an outsized impact on profitability. This metric is reported quarterly and provides an immediate read on whether the operating environment is improving or deteriorating.

The second is the ratio of non-energy revenue to total revenue, which measures the pace of the diversification that will ultimately determine whether Oceaneering successfully transforms or remains tethered to the oil cycle. Both metrics are disclosed regularly and provide a clear signal of whether the transformation thesis is working.

XIII. Lessons and Takeaways

Oceaneering's sixty-year journey offers a rich set of lessons for both operators and investors, lessons that extend well beyond the offshore services industry.

For operators, the most important lesson is that survival through cycles requires diversification, but diversification takes far longer than anyone expects. Oceaneering first recognized its excessive dependence on oil in the 1990s. It began serious diversification efforts in the mid-2000s. A decade later, during the 2014-2016 crash, the company nearly went under because diversification had not progressed far enough. It took until the mid-2020s for non-energy revenue to reach a meaningful percentage of total sales. The transformation from oil services company to diversified technology platform is a multi-decade project, not a multi-year initiative. Any operator in a cyclical industry who thinks they can diversify in three to five years is almost certainly wrong. The sales cycles are different, the customer relationships must be built from scratch, and the organizational capabilities take years to develop. Oceaneering had been doing government work since the 1980s, and it still took until 2025 for the ADTech segment to sign its largest-ever contract.

Technical moats, once established, are remarkably durable. Oceaneering's core competency in operating complex robotic systems in extreme environments has been the common thread through every era of the company's history, from saturation diving in the 1960s to Mars rover components today. This kind of deep, accumulated expertise is nearly impossible to replicate quickly, which is why Oceaneering's process power, in Helmer's framework, is among its strongest competitive advantages. New entrants can build ROVs, but they cannot build fifty years of operational know-how. The safety records, the procedures manual that runs to thousands of pages, the institutional memory of what went wrong on a project in Angola in 2007 and how to prevent it from happening again, these are assets that do not appear on a balance sheet but are among the most valuable the company owns.

Asset-heavy businesses must be managed with extraordinary capital discipline. Oceaneering's golden era of 2010-2014 created enormous temptation to overbuild, expanding the ROV fleet to 318 vehicles in anticipation of continued growth. When the market collapsed, those idle assets became an expensive liability. The lesson is not that asset-heavy businesses are inherently bad, they can generate excellent returns when managed well, but that the capital deployment cycle must be managed for the through-cycle average, not the peak. The siren song of "this time is different" is loudest precisely when it is most dangerous. The companies that survive cycles are not the ones that grow fastest during booms but the ones that maintain financial flexibility through busts.

For investors, Oceaneering in 2016 offered what may have been a generational entry point for those willing to underwrite a cyclical recovery and a transformation story simultaneously. The stock traded in the low teens against a replacement value of assets that far exceeded the market capitalization. The risk was that the recovery might never come, or that the company might not survive long enough to see it. Those who bought at the trough and held through the recovery would have seen meaningful returns, though the stock remains well below its 2014 peak, a reminder that cyclical recoveries in structurally challenged industries are often incomplete. The market's willingness to pay eighty-plus dollars at the peak and ten dollars at the trough for fundamentally the same company, with the same assets and capabilities, is a powerful illustration of how much cyclical sentiment drives valuation in asset-heavy industrials.

The broader insight is that transformation stories in traditional industries are inherently difficult to underwrite. The market tends to discount them heavily, pricing the risk that the transformation will fail, while the potential upside if it succeeds can be enormous. Oceaneering's autonomous systems strategy, its defense business expansion, and its offshore wind positioning are all real capabilities with genuine commercial traction. Whether they add up to enough to fully escape the oil cycle is the open question that will define the stock's trajectory for the next decade.

A note on services businesses building product moats: Oceaneering's trajectory from a pure diving services company to one that owns proprietary subsea products, autonomous vehicles, and digital platforms is a masterclass in how to evolve a services business. The common wisdom is that services businesses are inherently commoditized, competing on price and availability. Oceaneering's experience shows that deep domain expertise in a services context can be parlayed into proprietary products and technology platforms that create switching costs, recurring revenue, and intellectual property barriers. The key is that the product development is informed by decades of firsthand operational experience, something that a pure-play manufacturer or software company cannot replicate without years of learning.

XIV. The Future and Emerging Storylines (2026-2030)

Standing at the midpoint of the 2020s, Oceaneering is at a genuine strategic crossroads. The transformation story that began in the depths of the 2016 oil crash has produced real results, non-energy revenue approaching forty percent, a defense business with transformative contracts, an autonomous systems portfolio with commercial deployments, but the destination has not yet been reached. The next five years will determine whether Oceaneering's transformation succeeds or stalls. Several potential inflection points deserve close attention.

If U.S. offshore wind development accelerates, it could be transformative for Oceaneering's revenue mix. The current U.S. offshore wind market has been plagued by project cancellations and permitting delays, but the underlying policy commitment remains. If even a fraction of the planned East Coast capacity gets built, the demand for subsea services, from cable installation to turbine maintenance, would create a new revenue stream measured in hundreds of millions of dollars.

Space commercialization offers another growth vector. Oceaneering's position on the Collins Aerospace team for NASA's $3.5 billion xEVAS spacesuit program provides a direct role in the Artemis lunar missions. It is a remarkable arc for a company that started with men in heavy diving suits in the Gulf of Mexico to now be helping build the suits that will be worn on the Moon.

As commercial space activity expands, the demand for EVA systems, ISS-certified hardware, and space robotics could grow well beyond current projections.

The autonomous systems bet is approaching a critical juncture. The Freedom AUV, Liberty docking stations, and remote operations centers have demonstrated technical viability. The question is whether they can achieve the kind of large-scale commercial adoption that justifies the investment. If autonomous resident systems become the standard model for subsea inspection and light intervention, displacing the traditional approach of deploying ROVs from expensive surface vessels, the economic transformation for both Oceaneering and its customers would be profound.

Deep-sea mining remains the most speculative but potentially the most consequential optionality. The International Seabed Authority has been negotiating the Mining Code for commercial exploitation of polymetallic nodules in international waters, but negotiations through 2025 failed to reach consensus. If regulatory approval eventually comes, the scale of the opportunity, trillions of dollars worth of critical minerals sitting on the ocean floor, could dwarf Oceaneering's current addressable market.

Risk remains omnipresent.

Another severe oil price decline would pressure the core business. Offshore wind policy changes could slow the renewable energy opportunity. Technology disruption from well-funded AI and robotics startups could erode Oceaneering's competitive position in autonomous systems. And geopolitical instability, from the Middle East to the South China Sea, continues to inject unpredictability into the energy markets that drive the majority of the company's revenue.

Capital allocation will be a defining issue. Oceaneering ended 2025 in a net cash position with over $200 million in annual free cash flow. The question of how to deploy that capital, more acquisitions in autonomous systems and software, organic investment in defense capabilities, share repurchases to return value to long-suffering shareholders, or some combination of all three, will shape the company's trajectory more than any single contract win or technological breakthrough. Management has signaled a willingness to pursue acquisitions, and the GDi deal in late 2024 showed the appetite for software and digital capabilities. But the history of industrial companies making technology acquisitions is littered with overpaid deals and failed integrations, and investors will be watching closely to see whether Oceaneering can execute without repeating those mistakes.

What does success look like in five years? Non-energy revenue consistently above fifty percent of total sales. Free cash flow that remains strong regardless of oil price fluctuations. An autonomous systems business that has crossed from pilot projects to scaled commercial deployment. And a stock that the market values as a robotics and industrial technology platform rather than an oil services company. That would mean the transformation that began in 2016 had finally, after a decade, reached its destination. Whether Oceaneering gets there remains one of the more compelling open questions in the industrial sector.

XV. Epilogue

In February 2026, Oceaneering reported fourth-quarter and full-year 2025 results that beat analyst expectations by a wide margin, with earnings per share of $0.45 against consensus estimates that were roughly forty percent lower. Full-year revenue reached $2.8 billion, adjusted EBITDA hit $401 million, and free cash flow more than doubled to $208 million. The stock rose more than eight percent on the earnings release, pushing above thirty-three dollars.

The results capped a remarkable run: seven consecutive years of EBITDA growth, through one of the most turbulent periods in the energy industry's history. The balance sheet showed $689 million in cash and a net cash position for the first time in memory. The Defense Innovation Unit contract for the Freedom AUV, the largest-ever DoD maritime mobility system contract, and the Petrobras ROV awards all signaled that the diversification strategy was gaining traction.

Analyst sentiment remains mixed, with price targets ranging from $22 to $34, reflecting genuine uncertainty about whether the stock's current trading range above $37 is pricing in too much optimism or still undervaluing the transformation.

TD Cowen recently raised its target to $34, citing ADTech growth potential, while other analysts maintain more cautious stances given the cyclical headwinds facing energy-exposed segments in early 2026. The spread between the most bullish and most bearish price targets is unusually wide, which itself is a signal: the market has not reached consensus on what kind of company Oceaneering is becoming.

Oceaneering's story is ultimately a case study in something rare in corporate America: a company that faced an existential threat from its market's structural decline and, rather than denial or acquiescence, chose to transform.