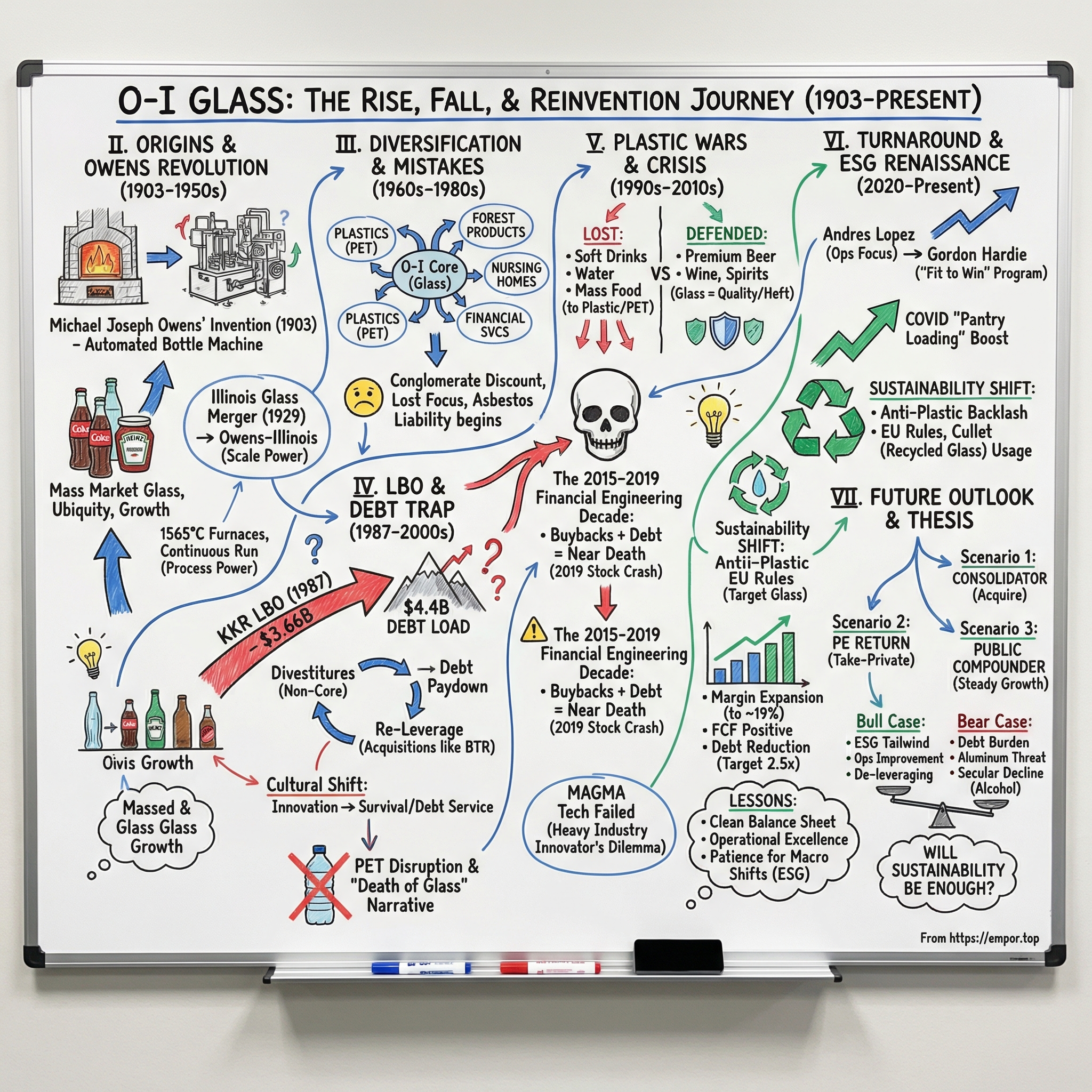

O-I Glass: The Rise, Fall, and Reinvention of the World's Largest Glass Bottle Maker

I. Introduction & Episode Roadmap

Picture this: a furnace the size of a small house, glowing white-hot at 1,565 degrees Celsius, running continuously, day and night, weekends and holidays, for ten to fifteen years without ever being shut off. That is the beating heart of glass manufacturing. And the company that operates more of those furnaces than anyone else on the planet is O-I Glass, a century-old manufacturer headquartered in Perrysburg, Ohio, that most consumers have never heard of despite the fact that roughly one in every four glass bottles produced worldwide comes from an O-I plant.

O-I Glass generates roughly six and a half billion dollars in annual revenue. It employs approximately 19,000 people across 64 plants in 18 countries. It is the world's largest glass container manufacturer, supplying the bottles that hold everything from Budweiser to Bordeaux, from Heineken to Hennessy.

And yet, for all that scale, O-I has spent the better part of three decades fighting for its financial life.

The central question of this story is deceptively simple: How did a hundred-year-old glass bottle company survive—and nearly not survive—a debt spiral, activist attacks, and the existential threat of plastic?

The answer takes us through one of the most important industrial inventions of the twentieth century, through the leveraged buyout madness of the 1980s, through decades of financial engineering that nearly destroyed the company, and finally into a sustainability-driven renaissance that no one saw coming.

This is a story about what happens when a capital-intensive commodity business tries to play private equity games. It is a story about the slow-motion disruption of plastic and the faster-than-expected backlash against it. And it is a story about operational excellence eventually winning out over financial wizardry, though the ending is not yet written.

What makes O-I compelling for investors is not that it is a growth story. It is not. This is a cyclical, capital-intensive manufacturer of a commodity product.

What makes it compelling is that it sits at the intersection of several powerful forces: the global sustainability movement, the premiumization of beverages, the consolidation of a fragmented industry, and the turnaround of a once-distressed balance sheet.

Whether those forces are enough to transform O-I from a perpetual value trap into a genuine compounder remains an open question, and answering it requires understanding the full arc of this remarkable company.

The key themes to watch: the danger of financial engineering in capital-intensive commodity businesses, the innovator's dilemma in heavy industry, and the question of whether sustainability is a genuine structural tailwind for glass or merely a temporary reprieve.

II. Origins & The Owens Bottle Machine Revolution (1903-1950s)

Michael Joseph Owens was born on New Year's Day 1859 in Mason County, West Virginia, to destitute Irish immigrants. His father was a coal miner. At the age of ten, an age when most children today are learning long division, Owens walked into a glassworks and started stoking coal into furnace "glory holes," the openings through which molten glass was manipulated. By fifteen, he had taught himself to blow glass. By his mid-twenties, he was one of the most skilled glass-blowers in America.

This was a man who did not learn his industry from textbooks. He learned it from the heat.

In 1888, Owens moved to Toledo, Ohio, to work for Edward Drummond Libbey, a Boston-born entrepreneur who had relocated his glass factory to take advantage of cheap natural gas in the Toledo area. Owens quickly became superintendent of Libbey's operation. He was a restless tinkerer—the kind of factory floor genius who could not look at a process without seeing ways to improve it. When Libbey won a contract to make glass bulbs for Edison General Electric's new electric lights, Owens was put in charge. He invented a mould-opening device operated by foot and a paste to prevent bulbs from sticking—small innovations that made production faster and cheaper. These were not headline-grabbing inventions, but they revealed a mind that was obsessed with eliminating inefficiency at every step of the process.

But his real obsession was the bottle. In the late 1890s, every glass bottle in the world was blown by hand. It was skilled labor, slow and expensive. A good crew could produce about 3,500 bottles per day at roughly $1.80 per bottle. The process had not changed fundamentally in centuries—a craftsman would gather molten glass on the end of a blowpipe, shape it with breath and tools, and hand it off to be cooled and finished. Owens believed he could mechanize the process entirely. Starting in 1899, with financial backing from Libbey and engineering help from William Emil Bock, Owens spent five years and approximately half a million dollars—an enormous sum at the time—developing a fully automated bottle-making machine. The project consumed Owens completely. He worked through failed prototypes, redesigned the suction mechanism that would gather molten glass, and engineered a rotating system that could form multiple bottles simultaneously.

On September 3, 1903, the Owens Bottle Machine Company opened for business. The machine could produce 13,000 bottles per day at ten to twelve cents per bottle.

Think about that math for a moment: nearly four times the output at roughly one-fifteenth the cost.

This was not an incremental improvement. It was the kind of step-change productivity gain that remakes entire industries. And it did. The automated bottle machine transformed the beverage, pharmaceutical, and food industries overnight, making glass containers cheap enough for mass-market products. Before Owens, glass bottles were a relative luxury; after him, they became ubiquitous. The Coca-Cola contour bottle, the Heinz ketchup bottle, the apothecary medicine bottle, the forms that defined twentieth-century consumer culture were all made possible by Owens' invention.

There was also a human dimension to this invention that Owens cared about deeply. The glass industry was infamous for child labor—Owens himself had been a child laborer. Mechanization eliminated the need for the armies of young boys who had worked the factory floors, carrying hot glass and breathing toxic fumes.

During his lifetime, Owens held 49 patents. His name lives on in three major companies: Owens-Illinois, Owens Corning, and Libbey-Owens-Ford. He died in Toledo on December 27, 1923, at the age of 64—wealthy, celebrated, and inducted posthumously into the National Inventors Hall of Fame.

The Owens Bottle Machine Company did not just manufacture bottles; it licensed its technology to other glass makers, creating a lucrative and defensible business model. But by the mid-1920s, the key patents were nearing expiration, threatening the substantial licensing revenue that had made the company enormously profitable.

Illinois Glass Company, founded in 1873 in Alton, Illinois, by William Eliot Smith and Edward Levis, was an Owens licensee with an aggressive sales team and modern, well-located facilities along the Mississippi River. On April 17, 1929, Owens Bottle Machine Company acquired Illinois Glass Company for $19 million, forming Owens-Illinois Glass Company—the largest merger in glass industry history at that time and the creation of the world's largest glass company.

The timing was terrible, the merger closed just months before the stock market crash, but the combined entity's scale and technological superiority carried it through the Depression without a production slowdown and positioned it perfectly for the post-World War II boom.

The company owned both the manufacturing technology and the production capacity, a vertical integration that gave it enormous pricing power.

As America's consumer economy exploded in the 1940s and 1950s, O-I became the glass backbone of the country: beer bottles, soda bottles, ketchup jars, medicine bottles, if it was glass, there was a good chance O-I made it. The company's competitive advantage was rooted in what Hamilton Helmer would call process power, manufacturing innovation that competitors could not easily replicate, combined with scale economies that made it the low-cost producer in market after market.

In 1935, Owens-Illinois and Corning Glass Works formed a joint venture that would become Owens-Corning Fiberglass, formally established as a separate entity in 1938. A 1949 antitrust ruling barred the two parents from controlling the venture, and Owens-Corning went public in 1952, eventually becoming a Fortune 500 company in its own right, a testament to the innovation engine that O-I had built.

But those same antitrust actions had a broader consequence: they effectively prevented O-I from growing further through domestic glass acquisitions. As the 1950s gave way to the 1960s, the company's leadership began to look beyond glass for growth. That decision would set in motion a chain of events that would haunt O-I for decades.

III. The Diversification Era & Conglomerate Mistakes (1960s-1980s)

The conglomerate craze of the 1960s and 1970s was one of the great collective delusions of American business. The theory was seductive: a well-managed company could apply its management talent to any industry, and diversification would smooth out cyclical earnings.

In practice, most conglomerates became sprawling, unfocused empires that destroyed shareholder value. O-I was no exception.

Starting in the 1950s, O-I pushed aggressively into plastics. By the 1970s, the plastics division had actually created and marketed the liter and two-liter plastic soft drink bottle—which, in a twist of dark irony, would eventually become one of the greatest threats to O-I's core glass business.

In 1956, the company acquired National Container Corporation, entering forest products. Later, it bought Lily Tulip Cups, a maker of wax-lined milk cartons and disposable cups. It partnered with Nippon Electric Glass to produce television tubes. Under CEO Robert Lanigan in the 1980s, it acquired two nursing home chains and a mortgage banking company. It even ventured into sugar cane farming in the Bahamas and phosphate rock mining in Florida.

In 1965, the company dropped "Glass" from its corporate name entirely, becoming simply Owens-Illinois, Inc., a symbolic acknowledgment that it no longer thought of itself primarily as a glass company.

By 1986, the numbers told the story of a company that had lost its way. Glass containers accounted for only 36 percent of O-I's profits, with plastics and closures contributing 23 percent and the rest scattered across the diversified portfolio.

The strategic logic was never coherent. What did nursing homes have to do with bottle-making? What did mortgage banking teach you about furnace optimization? The answer, of course, was nothing. These were classic conglomerate acquisitions: deals done because the cash was available and the investment bankers were persuasive, not because they made strategic sense. The result was a company that was mediocre at many things and excellent at nothing—a far cry from the focused manufacturing powerhouse that Michael Owens had built.

Investors were frustrated. The stock traded at a discount to peers. Returns on capital were lackluster. The company had lost its identity and its edge. The bloated portfolio also carried a hidden liability: in 1944, O-I had begun manufacturing Kaylo, an asbestos pipe and boiler insulation product, which it produced until 1958 before selling the division to Owens Corning. The first asbestos lawsuit was filed in 1981, and over the following decades, O-I would resolve approximately 210,000 asbestos-related claims at an estimated cost of roughly $5 billion—a staggering financial burden that would compound every other problem the company faced.

The performance drag was real and measurable. While focused competitors invested in furnace upgrades and manufacturing efficiency, O-I's capital was being allocated across nursing homes and mortgage banks. Management attention—perhaps the scarcest resource of all—was scattered across industries that had nothing in common except that they were owned by the same holding company.

The stock traded at a conglomerate discount, and activist investors of the era had not yet developed the tools and tactics that would later force change. O-I drifted, a company with a world-class core business buried under layers of strategic confusion.

By the mid-1980s, O-I was a textbook case of a conglomerate ripe for restructuring. The core glass business was still throwing off cash, but it was buried under layers of unrelated businesses, asbestos liabilities, and management distraction. The capital allocation lessons here foreshadow everything that would go wrong in the decades ahead: O-I's leadership consistently failed to recognize that focus and discipline—not diversification and financial complexity—were the keys to long-term value creation in a capital-intensive industry. The stage was set for one of the era's most consequential leveraged buyouts.

IV. The Leveraged Buyout & Debt Trap (1987-2000s)

In February 1987, Kohlberg Kravis Roberts made its move. KKR's leveraged buyout of Owens-Illinois closed at $3.66 billion, making it one of the era's mega-deals—a transaction that loaded $4.4 billion in debt onto a company that had never been built to carry that kind of financial burden.

The logic was pure LBO playbook: buy the company, strip out the non-core businesses, use the proceeds to pay down debt, refocus on the cash-generating core, and exit at a profit. And to be fair, KKR and management executed the early stages competently.

The divestitures came in rapid succession. The forest products division was sold to Great Northern Nekoosa Corporation in 1987. The mortgage banking unit was jettisoned. The nursing home group, Health Care and Retirement Corporation, was spun off to the public in October 1991, netting O-I nearly $250 million, and HCR went on to become a successful standalone company with over 300 facilities.

The Lily Tulip Cups business was sold. The television tube joint venture stake was sold to Nippon Electric Glass for $100 million in 1993. Libbey Glass, which had been part of the O-I family since 1935, was separated in 1994. One by one, the conglomerate was dismantled.

In December 1991, KKR took Owens-Illinois public again through an IPO that raised approximately $1.3 billion. By 1993, debt had been brought down to $2.5 billion from its peak of $4.4 billion. CEO Joseph Lemieux, who had been appointed in 1990 after spending his entire career at O-I, led the company through this difficult post-LBO period with a steady hand. Under Lemieux, annual revenue grew 65 percent from $3.6 billion to a projected $6 billion by the time he retired in 2003 after 46 years of service.

But here is the critical point that defined O-I's trajectory for the next three decades: the debt was reduced but never eliminated. O-I was now a focused glass company, exactly what the LBO was supposed to achieve, but it was a focused glass company with $2.5 billion in debt and limited ability to invest in its own future. Every dollar that went to interest payments was a dollar that did not go into furnace upgrades, new capacity, or technology development.

The company was stuck in a financial engineering loop: generate cash, service debt, repeat. Innovation took a back seat to survival.

Lemieux navigated the post-LBO landscape with debt discipline and aggressive international expansion. Major acquisitions included Brockway Inc. for $750 million, Italy's AVIR for roughly $586 million, and the transformative 1998 purchase of BTR plc's worldwide glass and plastics packaging for $3.6 billion, which added 43 manufacturing facilities in 11 countries.

The BTR deal made O-I a truly global company, but it also re-leveraged the balance sheet at precisely the moment when the company needed financial resilience most.

Meanwhile, the competitive landscape was shifting beneath O-I's feet. The 1990s brought the rapid ascendance of PET plastic bottles, and glass—the material that had defined O-I for nearly a century—was suddenly on the defensive. The "death of glass" narrative gained traction on Wall Street and in corporate boardrooms. Coca-Cola, Pepsi, and the other beverage giants were pivoting to plastic. And O-I, burdened by debt and focused on financial restructuring rather than strategic positioning, was not prepared for what came next.

KKR maintained a stake of approximately 26 percent well into the early 2000s. The LBO had technically worked, KKR made money and the company was refocused, but the debt overhang would shape O-I's strategic choices for the next three decades. The company culture shifted from industrial excellence to survival mode, from asking "How do we innovate?" to asking "How do we make the next interest payment?"

That cultural shift would prove extraordinarily difficult to reverse. Also worth noting: in December 1991, a federal jury found O-I, Brockway, and Dart Industries had conspired to fix glass container prices in the 1970s and 1980s, adding legal liability to an already strained balance sheet.

After Lemieux retired in 2003, the company appointed Steven McCracken as its first outside CEO in April 2004 after 30 years at DuPont. McCracken was supposed to bring fresh perspective, but he resigned in late 2006 due to health issues and died in February 2008. The brief and troubled external CEO experiment underscored how deeply O-I's identity was tied to its lifers, the people who had grown up inside the furnace rooms and risen through the ranks.

The revolving door at the top would become a recurring theme, destabilizing strategy precisely when consistency was needed most.

The debt legacy also compounded the asbestos liability problem. With billions in obligations from the Kaylo product manufactured decades earlier, O-I was fighting a two-front financial war, servicing LBO debt while settling thousands of asbestos claims. In 2019, the company employed the "Texas Two-Step" strategy, creating Paddock Enterprises LLC as a subsidiary to isolate legacy asbestos liabilities. Paddock filed Chapter 11 bankruptcy in January 2020. The Owens-Illinois Asbestos Personal Injury Trust was finally established in July 2022 with $610 million to handle remaining claims.

For decades, the combined weight of LBO debt and asbestos liability consumed resources that should have gone into the business. It was a perfect storm of financial burden: debt from a buyout, liability from a product made forty years earlier, and an industry being disrupted by a new material. Any one of these challenges would have been manageable in isolation. Together, they were nearly fatal.

V. The Plastic Wars & Existential Crisis (1990s-2010s)

The disruption of glass by plastic was not a sudden event. It was a slow-motion catastrophe that unfolded over decades, and the cruelest part was that O-I could see it coming—and in some cases, helped it happen.

As early as 1970, plastic soft drink bottles had been introduced to the market. By 1977, PET—polyethylene terephthalate, the same material used in most water bottles today—had arrived. The two-liter PET bottle, which O-I's own plastics division had helped develop and market, became the standard for soft drinks. By 1978, 62 percent of soft drink containers and 89 percent of beer containers were already non-returnable, a shift away from the deposit-and-return model that had favored heavy, durable glass bottles.

The cascade was relentless. Soft drinks went to plastic. Milk shifted to plastic jugs and cartons. Juice moved to plastic and aseptic packaging. Water, which would become one of the largest beverage categories in the world, went almost entirely to PET.

Many food categories followed. Glass was being pushed out of category after category, and each loss was permanent. Consumers liked plastic: it was lighter, it did not break, it was cheaper. The convenience factor was overwhelming.

Why did O-I not pivot? The answer lies in the economics of glass manufacturing itself. Those furnaces running at 1,565 degrees Celsius, 24 hours a day, for ten to fifteen years—they represented billions of dollars in sunk capital. You cannot repurpose a glass furnace to make plastic bottles. The entire manufacturing infrastructure, the workforce skills, the supply chains—everything was built around glass. Pivoting would have meant essentially starting a new company from scratch while continuing to service billions in debt. It was not realistic.

But glass had its defenders, and they turned out to be some of the most valuable customers in the beverage industry.

Beer stayed in glass. The major brewers, Anheuser-Busch, MillerCoors, and their global equivalents, continued to package their premium products in glass bottles. There was something about the weight of a cold glass bottle, the satisfying clink, the condensation on the surface, that plastic simply could not replicate. Beer drinkers cared about these things, and brewers knew it.

Wine and spirits became another fortress. Try to imagine buying a bottle of Dom Pérignon in plastic. The idea is absurd. Premium positioning and glass packaging were inseparable in consumers' minds. The weight, the clarity, the tactile experience of a glass bottle conveyed quality in a way that plastic never could. This insight—that glass's survival depended on products where brand perception and premiumization mattered more than convenience—became the foundation of O-I's defensive strategy.

By 2021, O-I's portfolio had consolidated around these strongholds: beer at 33 percent, wine at 21 percent, spirits at 14 percent, non-alcoholic beverages at 14 percent, and food at 18 percent. Alcoholic beverages—the categories where glass was most culturally entrenched—represented 68 percent of the company's business. This concentration was both a lifeline and a vulnerability.

Geographic diversification also helped. As U.S. volumes declined, O-I expanded aggressively into Latin America and Europe, where glass packaging remained more culturally embedded and plastic adoption was slower. The 2015 acquisition of Vitro's food and beverage glass business for $2.15 billion added five plants in Mexico and one in Bolivia, significantly expanding O-I's Latin American footprint and adding roughly $945 million in annual revenue.

But expansion required capital, and capital meant debt. The scramble to survive involved plant closures, layoffs, and cost-cutting programs that hollowed out the company's manufacturing base. O-I entered the 1980s with its production cost advantage eroded, having allowed many conventional glass plants to deteriorate while investing in plastic bottles. The irony was thick: the company had invested in the very technology that was killing its core business.

There is a myth-versus-reality dimension to the plastic disruption that deserves attention. The consensus narrative—"glass is dying"—was never entirely accurate. What actually happened was more nuanced: glass lost the high-volume, low-margin, convenience-driven categories where its physical properties (weight, fragility) were genuine disadvantages. But it retained and even strengthened its position in the categories where those same properties—the heft that signals quality, the transparency that showcases the product, the impermeability that preserves flavor—were valued by consumers and brand owners. The mistake O-I made was not failing to recognize this distinction; it was failing to lean into it aggressively enough. For too long, the company tried to compete in the categories it was losing rather than doubling down on the categories it could win.

The plastic wars taught O-I a brutal lesson about the innovator's dilemma in heavy industry. Unlike software companies that can pivot with a few lines of code, capital-intensive manufacturers are prisoners of their installed base. When the disruption arrives, the very assets that made you dominant become anchors that drag you down.

O-I survived the plastic wars, but it survived them diminished, a company defined by the categories it had lost rather than the markets it had won. The financial scars, however, were about to get much deeper.

VI. The Financial Engineering Decade: Buybacks, Debt, and Distress (2010-2019)

If the 2000s were about surviving the plastic disruption, the 2010s were about a different kind of self-inflicted wound: the belief that financial engineering could substitute for operational improvement in a capital-intensive commodity business. It could not, and the attempt nearly destroyed the company.

Albert Stroucken, a Dutch national who had spent 29 years at Bayer AG, took over as CEO and Chairman in December 2006. To his credit, Stroucken made the important decision to divest the plastics business entirely, selling the blow-molded container division to Graham Packaging for $1.2 billion and remaining plastics operations to Rexam, shedding roughly 2,800 employees and $760 million in annual revenue. O-I was finally a pure-play glass company.

But Stroucken also brought a chemical industry executive's mindset, an emphasis on shareholder returns through capital allocation rather than manufacturing innovation. During his tenure, O-I pursued share buybacks as a primary mechanism for returning value to shareholders, authorizing a $500 million repurchase program. He also pursued growth through acquisition, most notably the $2.15 billion purchase of Vitro's food and beverage glass business in 2015. Both moves were funded with debt.

The problem was arithmetic. O-I was a commodity business with cyclical margins, lumpy free cash flow, and a still-elevated debt load from the KKR era. Buying back shares with borrowed money in that context is like a farmer mortgaging his land to buy lottery tickets—it might work if everything goes right, but the downside is catastrophic.

And everything did not go right.

The 2015-2016 earnings crisis hit O-I like a freight train. Over a twelve-month period, consensus earnings-per-share estimates were downgraded by 36 percent. The stock, which had reached an all-time closing high of $58.71 on April 21, 2008, entered a prolonged decline from which it has never recovered. Stroucken retired at the end of 2015, leaving behind a company that had spent years optimizing its capital structure instead of its operations—and had succeeded at neither.

Activist investors smelled blood. Alexander Roepers of Atlantic Investment Management built a major position, eventually making O-I his fund's top holding at approximately 26 percent of assets with a 6.7 percent stake in the company. In October 2018, Roepers publicly called on O-I to sell its European business and initiate a $1 billion share buyback. He expressed open disappointment with the CEO—Andres Lopez, who had succeeded Stroucken in January 2016—and in June 2019 estimated O-I's fair value at double the then-current stock price of approximately $16.50.

But the real crisis was still ahead. On October 29, 2019, O-I reported third-quarter earnings that revealed a loss from operations of $536 million, compared to positive earnings of $168 million just a year earlier. The stock plunged 21.7 percent in a single day. Full-year guidance was slashed. By late November, shares had fallen 44 percent year-to-date.

With over $5 billion in total debt, serious questions arose about the company's viability. The stock bottomed near $9.88, a staggering 83 percent decline from the 2008 all-time high of $58.71.

To raise cash, O-I sold its Australia and New Zealand glass manufacturing business to Visy, an Australian recycling conglomerate, in a deal worth approximately $1 billion. That business had generated sales of roughly $754 million and EBITDA of about $124 million—it was a productive, profitable operation sold under duress to keep the parent company solvent.

The company also sold the rights to a $372.5 million ICSID arbitration award against Venezuela—which had expropriated O-I's glass plants—to an Irish investment fund for just $115 million, effectively monetizing a half-billion-dollar claim at a steep discount because it needed the cash immediately.

Meanwhile, in November 2019—just weeks after the catastrophic earnings report—O-I announced a $313 million increase to its existing $400 million share repurchase program, bringing remaining buyback authority to approximately $600 million. The timing was jarring. The company was selling productive assets to stay solvent while simultaneously authorizing hundreds of millions in buybacks. It was a signal of strategic incoherence at the board level—an attempt to placate activists and prop up the stock price when the priority should have been shoring up the balance sheet. The buyback authorization, in the context of $5 billion in debt and a stock in freefall, bordered on the absurd.

The revenue trajectory during this period told its own story. Revenue had been roughly $6.9 billion in 2017 and 2018, slipped to $6.7 billion in 2019, and would crater to $6.1 billion in 2020 as COVID hit. The Vitro acquisition in 2015 had added nearly a billion in revenue, meaning the organic business was actually shrinking. Growth through acquisition—funded by debt, in a declining industry, by a company already drowning in leverage—was a recipe for destruction, not creation.

The 2019 near-death experience was the culmination of thirty years of financial mismanagement. The KKR LBO had loaded the company with debt. The conglomerate-era diversification had distracted management. The share buybacks of the 2010s had consumed cash that should have gone to debt reduction or capital investment.

And through it all, the fundamental business, making glass bottles, had been neglected. The realization finally sank in: financial engineering cannot save a broken operating model. The only way forward was to fix the operations.

The question was whether it was too late.

VII. The Turnaround & ESG Renaissance (2020-Present)

Andres Alberto Lopez had been preparing for this moment his entire career. Born in Colombia, Lopez had joined O-I in 1986 as an engineer-in-training at a Colombian plant—the same year that KKR was circling the company for its leveraged buyout. He rose through the ranks with a factory-floor pragmatism that set him apart from the financial engineers who had dominated O-I's C-suite: General Manager of O-I Peru in 1999, VP of Finance and Administration for North America in 2004, VP of Manufacturing for North America in 2005, President of O-I Americas in 2014, COO in February 2015, and finally CEO in January 2016. His education—Stanford, Harvard Business School, MIT—gave him the strategic vocabulary, but his instincts were those of a manufacturing man. He understood furnaces, production schedules, and utilization rates in a way that his predecessors had not.

Lopez's early years as CEO were consumed by firefighting. The balance sheet was a mess, activists were circling, and the plastic threat had not abated. But he initiated a $1.5 billion portfolio optimization program that began the painful work of right-sizing the company's manufacturing footprint.

Plant closures, consolidation, and operational improvements took priority over financial maneuvers. The focus shifted from how to allocate capital to how to run a factory.

Then two things happened that no one predicted.

First, the COVID-19 pandemic, which initially devastated on-premise consumption, bars, restaurants, hotels, but then drove an unexpected surge in at-home consumption. Consumers bought more beer, wine, and spirits from retail stores, and they bought them in glass bottles. The pandemic-era "pantry loading" phenomenon gave O-I a temporary volume boost.

Second, and far more important, the global sustainability movement arrived at glass's doorstep, and glass was suddenly the hero instead of the villain.

The anti-plastic backlash had been building for years: ocean pollution documentaries, microplastics found in human blood, images of sea turtles tangled in plastic waste. But the regulatory response crystallized in the late 2010s and early 2020s. The EU's Single-Use Plastics Directive targeted a 50 percent reduction in single-use plastic consumption by 2025 and mandated 25 percent recycled content in PET bottles. Extended Producer Responsibility fees made plastic packaging more expensive. Glass—infinitely recyclable without quality degradation, inert, and free of microplastic concerns—suddenly had a powerful narrative tailwind.

O-I leaned into the sustainability story with substance, not just slogans. The company reduced greenhouse gas emissions by 20 percent from its 2017 baseline, achieving its interim 2025 target early. Global average cullet—recycled glass—use advanced to 40 percent in 2024. In Europe, where the regulatory environment was most favorable, cullet constituted approximately 70 percent of the batch mix.

The U.S. Department of Energy selected O-I to receive a $125 million investment for industrial decarbonization. Advanced furnace technologies like GOAT (gas-oxygen combustion and heat recovery) and hybrid-flex systems allowing up to 70 percent electricity in the melting process moved from lab to deployment.

Lopez retired in May 2024 after nearly 40 years at O-I, handing the CEO role to Gordon J. Hardie. Hardie's background was quite different from Lopez's: over 35 years of leadership experience, most recently as President of Food and Ingredients at Bunge Limited, with prior roles at Goodman Fielder, Southcorp Wines, and Foster's Brewing Group. He had been an O-I board member since 2015, so he knew the company well, but his operational philosophy was more aggressive than his predecessor's.

Hardie brought an outsider's perspective and a sense of urgency. He launched the "Fit to Win" program, a comprehensive restructuring that targeted $650 million in cumulative savings by 2027.

The results came faster than expected. In 2025, Fit to Win delivered $300 million in savings, exceeding the initial target of $175 million for the year. The three-year cumulative target was raised to at least $750 million. Approximately 13 percent of total capacity was permanently or indefinitely idled, with eight furnaces shut down and roughly 1,500 jobs eliminated. Europe bore the heaviest cuts, reflecting the most severe demand softness.

Adjusted EBITDA margins expanded from 16.8 percent in 2024 to 19.0 percent in 2025. Adjusted EPS nearly doubled from $0.81 to $1.60. Free cash flow swung from negative $128 million to positive $168 million—a roughly $300 million improvement in a single year.

Not everything went according to plan. The MAGMA technology program, O-I's proprietary Modular Advanced Glass Manufacturing Asset, had been a centerpiece of Lopez's long-term vision. The concept was revolutionary for the glass industry: modular, prefabricated furnace systems that could be deployed in half the time of heritage technology, could use biofuels and hydrogen, and could be moved and redeployed as demand shifted. Prototypes had been established in Perrysburg, Ohio, Streator, Illinois, and Holzminden, Germany, with a purpose-built plant planned in Bowling Green, Kentucky, at an investment of up to $240 million.

But in the second quarter of 2025, the company concluded that MAGMA "did not have a pathway to the operational or financial return requirements" and halted the program. O-I recorded $108 million in restructuring and impairment charges. The Bowling Green plant was slated for reconfiguration. It was a humbling acknowledgment that even promising technologies can fail the economics test in heavy industry.

For 2026, the company guided to adjusted EBITDA of $1.25 to $1.30 billion, adjusted EPS of $1.65 to $1.90, and free cash flow of approximately $200 million—despite an estimated $150 million step-up in energy costs from expiring European energy contracts. The path to approximately 2.5x net leverage by year-end 2027 remained on track. Net debt stood at $4.2 billion at year-end 2025, down from a leverage ratio of 3.9x to 3.5x in a single year.

The credit markets have responded to the improvement. S&P upgraded O-I to BB- from B+, with a stable outlook. Moody's maintains a Ba3 corporate family rating, also stable. Both ratings remain below investment grade—O-I is still a high-yield credit—but the trajectory is positive. The September 2025 refinancing of the bank credit agreement to $2.7 billion with Wells Fargo and other lenders extended maturities and provided enhanced liquidity. The debt stack includes a mix of senior notes at coupons ranging from 6.25 to 7.375 percent, along with green bonds issued in 2021 to fund sustainability projects—a $500 million green bond due 2031 from the U.S. subsidiary and a 600 million euro green bond due 2028 from the European subsidiary. These green bonds served a dual purpose: extending the maturity wall while aligning the capital structure with the ESG narrative.

The revenue trend, however, remains the nagging concern. From a peak of $7.1 billion in 2023, revenue has declined to $6.5 billion in 2024 and $6.4 billion in 2025. The company's guidance for 2026 does not assume volume recovery—the savings roadmap is designed to work even in a flat-to-declining volume environment. That is both a sign of management realism and a tacit acknowledgment that O-I cannot yet grow its top line. The turnaround, for now, is entirely a cost story. Whether it can become a growth story depends on forces largely outside the company's control: the pace of sustainability regulation, consumer preference shifts, and the trajectory of global beer and spirits consumption.

Most recently, on the February 10, 2026 earnings call, Hardie revealed a strategic portfolio reorientation: shifting toward non-alcoholic beverages, waters, juices, food, premium spirits, non-alcoholic beer, and ready-to-drink cocktails, and away from over-reliance on mainstream beer and wine. The sales force is being reorganized for the first time in ten to fifteen years. It is a recognition that glass's best growth opportunities lie not in defending legacy volumes but in capturing new categories where sustainability and premiumization intersect.

The turnaround is real but incomplete. O-I is no longer in survival mode, but it is not yet a business that generates the kind of returns on capital that attract long-term compounders. The next chapter depends on whether the sustainability tailwind strengthens, whether the Fit to Win savings hold, and whether the balance sheet can be de-risked enough to give management strategic flexibility.

VIII. The Business Model Deep Dive

To understand O-I, you have to understand how glass manufacturing actually works—because the economics of the business are dictated by physics in a way that few industries can match.

Glass containers are made from three naturally abundant ingredients: silica sand, soda ash, and limestone, mixed with cullet—recycled glass. These raw materials are blended, fed into a furnace, and melted at approximately 1,565 degrees Celsius. The molten glass—called "gobs"—is then cut into precise portions, dropped into moulds, and blown or pressed into bottle shapes using automated forming machines that are direct descendants of Michael Owens' 1903 invention.

The bottles are then annealed—slowly cooled in a controlled manner to relieve internal stresses—inspected, and shipped.

The furnace is the most critical asset. Once ignited, a glass furnace runs continuously for ten to sixteen years before requiring a complete rebuild, known as a "campaign." A rebuild of a 60-square-meter furnace takes approximately 55 days. Shutting down a furnace outside of a planned rebuild is catastrophic—the refractory lining can crack, and restarting takes weeks and millions of dollars. This means O-I's plants run 24 hours a day, 365 days a year, with no weekends off and no holidays. It also means that utilization rates are perhaps the single most important operating metric in the business. An underutilized furnace is still burning natural gas and consuming maintenance resources, but producing fewer bottles to spread those fixed costs across.

The cost structure is dominated by two categories. Raw materials represent 35 to 45 percent of operating expenses, while utilities—primarily natural gas for furnace melting—represent 40 to 50 percent. Approximately 80 percent of emissions come from natural gas combustion and 20 percent from virgin raw materials. Higher cullet percentages reduce both energy consumption and emissions, which is why the push toward recycled content is not just an ESG talking point—it is a cost reduction strategy.

Customer relationships in glass packaging are built around long-term supply agreements, annual or multi-year contracts, often with co-location arrangements where an O-I plant is built adjacent to or near a major customer's bottling facility. This matters because glass is heavy and fragile: a standard wine bottle weighs 400 to 500 grams, compared to about 90 grams for an equivalent aluminum container. Shipping it long distances is expensive and risky. Proximity to the customer is a meaningful competitive advantage.

O-I's major customers read like a who's who of global beverages: Anheuser-Busch InBev, Diageo, Heineken, Constellation Brands, Coca-Cola. The relationships are deep and often decades old. O-I also developed the MOGRA mobile glass recycling system, a truck-mounted unit that can process glass for recycling on-site at breweries and distillers, addressing one of the key bottlenecks in glass circularity.

The competitive landscape is more consolidated than you might expect for a commodity industry. The top three container glass producers—O-I, Verallia of France, and Ardagh Glass Packaging—together account for just over 55 percent of global shipments. But the industry remains regionally fragmented, with local players in nearly every market.

Verallia, which generates approximately 3.5 billion euros in annual revenue with sector-leading EBITDA margins above 24 percent, is a formidable competitor in European wine and spirits. Vidrala, a Spanish specialist, has been expanding its European footprint with a remarkably clean balance sheet—net debt was slashed by over 50 percent in 2025 to just 215 million euros. Ardagh, which operates in both glass and metal packaging, is the closest global peer to O-I but carries even higher leverage.

Why has consolidation been slow? Three reasons. First, capital intensity—acquiring a glass company means acquiring its furnaces, its debt, and its long-term customer commitments. Second, regulatory scrutiny—in concentrated regional markets, antitrust authorities watch glass packaging closely. Third, the fragmented nature of customer relationships means that a plant's value is often tied to its specific customer base and location, making integration complex.

The innovator's dilemma manifests uniquely in glass manufacturing. When your core asset is a furnace that runs for fifteen years without stopping, the appetite for radical innovation is inherently limited. You cannot experiment with a new melting technology on a furnace that is in the middle of a campaign—the risk of disrupting production is too high. Innovation tends to be incremental: slightly lighter bottles, improved coatings, better heat recovery systems. The MAGMA program represented O-I's most ambitious attempt to break this pattern with modular, flexible manufacturing—and its failure underscored how difficult it is to innovate fundamentally in an industry where the physics of production impose such rigid constraints.

The global glass packaging market was valued at approximately $71.5 billion in 2024, projected to reach over $100 billion by the early 2030s at a compound annual growth rate of roughly 4 to 5 percent. That growth rate is modest, and it masks significant regional variation: Asia-Pacific is the largest market by value, driven by China and India, while North America is expected to grow fastest through the next decade.

In Europe, the top five producers control approximately 65 percent of installed capacity. The premiumization trend, consumers trading up to higher-quality beverages, is arguably more important than overall market growth for O-I, because premium products overwhelmingly come in glass. A consumer who switches from mass-market beer to craft beer, or from blended whiskey to single malt, is switching to a product that is almost certainly packaged in glass. That trade-up dynamic has been one of the most powerful organic growth drivers for glass packaging over the past decade.

IX. Porter's Five Forces & Hamilton's Seven Powers Analysis

Understanding O-I's competitive position requires looking at the structural forces that shape the glass packaging industry—both the threats that constrain profitability and the sources of durable advantage.

Threat of New Entrants: Low. Building a new glass manufacturing plant costs $200 million or more, takes years to construct, and requires a furnace that must run continuously for over a decade to generate returns. The capital requirements alone are a formidable barrier. But it is not just about money. New entrants face established customer relationships backed by long-term contracts, quality certification processes that take years, and environmental compliance requirements that vary by jurisdiction. Co-location arrangements—where existing producers have plants physically adjacent to major customers—create additional switching friction. The result is that genuinely new entrants in glass packaging are exceedingly rare. Growth in the industry comes almost exclusively from existing players expanding capacity.

Bargaining Power of Suppliers: Medium. The raw materials for glass—silica sand, soda ash, limestone—are abundant commodities with multiple sources and low switching costs. O-I's scale gives it purchasing power. Energy is the more volatile input: natural gas prices fluctuate significantly, and gas represents the single largest cost component. Most energy costs are passed through to customers via contract provisions, but there is typically a lag, and not all contracts provide full pass-through. The $150 million step-up in energy costs that O-I guided for 2026, driven by expiring European energy contracts, illustrates this risk. Specialized equipment suppliers—furnace builders, forming machine manufacturers—have some leverage given the limited number of firms with the expertise to service glass plants, but this is a manageable constraint rather than a structural vulnerability.

Bargaining Power of Buyers: High. This is perhaps the most important structural challenge O-I faces. The customer base is concentrated among a handful of global beverage giants. AB InBev alone is a massive account. Diageo, Heineken, Constellation Brands, and Coca-Cola each represent significant volume. These customers negotiate aggressively on price, especially during periods of oversupply. They have alternatives—plastic and aluminum—that they can credibly threaten to switch to in many categories. However, buyer power is partially offset by switching costs: changing glass suppliers means requalifying bottle specifications, potentially disrupting co-location arrangements, and risking quality inconsistency in a product where the packaging is part of the brand experience. In premium spirits and wine, where the bottle is almost as important as the liquid inside it, switching costs are particularly high.

Threat of Substitutes: Medium-High. This is the force that has defined O-I's competitive life for three decades. PET plastic dominates soft drinks, water, and many food categories. Aluminum cans are gaining share in beer—the hard seltzer and ready-to-drink cocktail boom has been almost entirely an aluminum story—and are making inroads into wine and spirits with new can formats. In January 2025, the U.S. TTB removed fill-size barriers, legalizing a wider variety of can volumes for wine and spirits, further expanding aluminum's addressable market. California wineries have introduced 90-gram aluminum bottles versus 500-gram glass equivalents, dramatically reducing transport-phase carbon emissions. However, the sustainability backlash against plastic and the premium perception of glass provide meaningful counter-forces. In premium spirits, fine wine, and craft beer, glass remains the preferred and often the expected packaging format. The net assessment: substitutes are a real and ongoing threat, but the trend is more nuanced than the "death of glass" narrative suggests.

Competitive Rivalry: High. Glass packaging is fundamentally a commodity business. Within a given product category—say, 750ml wine bottles or 12-ounce beer bottles—there is limited scope for differentiation. Competition tends to be price-based, particularly during periods of oversupply when furnaces are running below capacity and producers are desperate to fill orders. The rivalry between O-I, Verallia, and Ardagh in Europe, and between O-I and Ardagh in North America, can be intense. Regional players add further competitive pressure in local markets. The saving grace is that the industry's high capital intensity and long furnace cycles prevent the kind of rapid capacity additions that create ruinous price wars in lighter industries. Consolidation—specifically, a more disciplined oligopoly structure—could stabilize pricing, but that scenario remains hypothetical.

Hamilton's Seven Powers Assessment. O-I's competitive power is concentrated in two areas.

First, scale economies: the company's global footprint, with 69 plants in 19 countries, creates purchasing power for raw materials and energy, spreads R&D costs across a larger revenue base, and provides geographic diversification that local competitors cannot match.

Second, moderate switching costs: co-location arrangements, quality certification processes, and the importance of packaging consistency in premium beverage branding create friction that makes it costly for customers to change suppliers mid-contract.

Process power—the operational expertise embodied in the Fit to Win and earlier MAGMA programs—provides some advantage, though it is more incremental than transformative. Network effects, counter-positioning, and branding are not applicable to O-I's B2B manufacturing model. Cornered resources are weak, though favorable plant locations near major customers have some strategic value.

The overall picture from this structural analysis is sobering but not hopeless. O-I operates in an industry with strong barriers to entry and moderate switching costs, but faces powerful buyers and meaningful substitute threats. The competitive rivalry is high but tempered by capital intensity. The company's scale is a genuine advantage, but it is not a moat in the traditional sense—it does not prevent competitors from undercutting on price or customers from threatening to switch. The sustainability shift is the wild card in this framework. If regulatory pressure on plastic intensifies and consumer preference for glass strengthens, it could effectively reduce the substitute threat while increasing O-I's switching costs—customers who commit to glass for sustainability reasons are less likely to switch back. That scenario would meaningfully strengthen O-I's competitive position. But it is not a certainty, and the aluminum industry is making its own compelling sustainability case—aluminum is highly recyclable, lighter than glass, and increasingly positioned as the "green" packaging alternative for beverages.

The comparison with Verallia is instructive for understanding what "good" looks like in this industry. Verallia's EBITDA margins above 24 percent, compared to O-I's 19 percent, suggest that a well-managed glass company focused primarily on Europe's premium wine and spirits markets can generate attractive returns. Vidrala's balance sheet, with net debt of just 215 million euros after slashing leverage by over 50 percent, shows what disciplined capital allocation looks like in glass manufacturing.

O-I's challenge is not that the industry is inherently unprofitable; it is that decades of debt, diversification, and financial engineering have put it at a structural disadvantage relative to cleaner, more focused competitors.

The gap between O-I and Verallia is not a gap in industry attractiveness. It is a gap in execution and balance sheet discipline.

X. The Strategic Playbook & Lessons

O-I's century-long journey offers a masterclass in both what to do and what not to do with a capital-intensive industrial business. Five lessons stand out with particular clarity.

The danger of financial engineering in capital-intensive businesses. The most expensive lesson O-I has taught its shareholders is that leverage and cyclicality are a toxic combination. The KKR LBO loaded the company with debt. The 2010s-era share buybacks added more. In a business where free cash flow is inherently lumpy—driven by commodity input costs, customer contract timing, and furnace rebuild cycles—every dollar of debt reduces the margin of safety. When earnings dipped in 2015 and again in 2019, the leverage amplified the decline into a near-death experience. The buybacks that were supposed to create shareholder value at $40 and $50 per share instead consumed cash that the company desperately needed when the stock was at $10. William Thorndike's "The Outsiders," which celebrates CEOs who used buybacks brilliantly, is the counterpoint: the CEOs Thorndike profiles had clean balance sheets and predictable cash flows. O-I had neither. Buybacks plus debt in a cyclical commodity business equals disaster—a lesson that sounds obvious in hindsight but that management and boards repeat with alarming regularity.

Technology transitions are slow but inevitable. O-I knew plastic was a threat for thirty years before the damage fully materialized. The company's own plastics division helped develop the two-liter PET bottle. Yet the response was inadequate—not because management was stupid, but because the innovator's dilemma is particularly vicious in heavy industry. When your competitive advantage is a $200 million furnace that must run for fifteen years, you cannot pivot nimbly. The installed base becomes a prison. The correct response—which O-I eventually arrived at through survival rather than strategy—was to abandon the categories lost to plastic and fortify the categories where glass remained essential. But it took decades of denial before that realism set in.

Sometimes the world comes back to you. The sustainability movement gave glass a second life that no one at O-I could have predicted in the dark days of the 1990s and 2000s. The anti-plastic backlash, driven by ocean pollution concerns and microplastic fears, suddenly made glass's heaviness and fragility—its greatest competitive disadvantages—seem like small prices to pay for infinite recyclability and material inertness. Patience, and more importantly survival, turned out to matter. Companies that die from leverage never get the chance to benefit from favorable macro shifts. O-I survived long enough for the pendulum to swing back. There is a lesson here about the value of optionality: staying alive, even in a diminished state, preserves the possibility of a comeback.

Operational excellence beats financial wizardry. Lopez's tenure and Hardie's Fit to Win program have delivered results that years of share buybacks and financial engineering never could. Margin expansion from 16.8 to 19.0 percent. Free cash flow swinging from negative $128 million to positive $168 million. EPS doubling in a single year. These improvements came from blocking and tackling: closing underperforming plants, consolidating operations, reducing SG&A, improving procurement, and optimizing the manufacturing network. None of it was glamorous. All of it was effective. The contrast with the Stroucken era, when the focus was on capital allocation tricks rather than operational improvement, could not be sharper.

Customer concentration is both moat and risk. O-I's deep relationships with global brewers and spirits companies kept the company alive during the plastic wars. AB InBev, Diageo, Heineken—these are customers that generate enormous volume and whose commitment to glass packaging is culturally and commercially entrenched. But concentration also means dependence. When a handful of customers represent a disproportionate share of revenue, their problems become your problems. A decline in global beer consumption, a shift toward aluminum cans by a major brewer, or contract renegotiations during a period of overcapacity can all disproportionately impact O-I. The company has limited pricing power precisely because its customers are so large and so few. This is the fundamental tension in O-I's business model: the same customer relationships that provide stability also constrain growth and profitability.

These five lessons are not abstract. They are playing out in real time as O-I navigates the current chapter of its story. The Fit to Win program is an explicit repudiation of the financial engineering approach. The focus on beer, wine, and spirits is the mature acceptance of what the plastic wars taught. The sustainability positioning is the company's best hope that macro trends will do what financial tricks could not. And the customer concentration—with AB InBev, Diageo, and Heineken at the center of the business—remains both the foundation of stability and the ceiling on ambition.

XI. Bull vs. Bear Case and Investment Thesis

The Bull Case. The argument for O-I begins with the sustainability tailwind, which is not a marketing slogan but a genuine structural shift backed by regulation, consumer preference, and corporate commitments.

The EU Single-Use Plastics Directive, Extended Producer Responsibility fees that make plastic more expensive, and consumer surveys showing 72 percent preference for recyclable packaging all favor glass. O-I has positioned itself credibly in this narrative, with emissions reductions of 30 percent from its 2017 baseline—achieved ahead of schedule—and new Paris-aligned targets. Major beverage companies are re-committing to glass as part of their own sustainability pledges.

The operational turnaround is tangible. Fit to Win delivered $300 million in savings in 2025, exceeding targets, and the cumulative three-year target was raised to at least $750 million. These savings do not depend on volume recovery—they are structural cost reductions from network optimization, procurement, and SG&A improvements. EBITDA margins have expanded meaningfully, EPS has doubled, and free cash flow has swung positive. The path to 2.5x net leverage by year-end 2027 is credible based on current trajectories.

The duopoly dynamics with Ardagh in key markets could stabilize pricing over time. Both companies have been rationalizing capacity, reducing the risk of destructive price competition. And the premiumization trend in beverages—craft beer, premium spirits, fine wine—structurally favors glass as the packaging format that conveys quality. The stock, trading near $15 and at low single-digit multiples of EBITDA, reflects considerable pessimism. If the turnaround continues and leverage declines, there is meaningful upside from multiple expansion alone.

Analyst sentiment has turned cautiously positive. Truist Securities raised its price target to $21 in early 2026. Wells Fargo upgraded the stock to Overweight with an $18 target. UBS maintained its Buy rating at $17. A wave of upgrades in early January 2026 drove a 6.8 percent stock price gain on the day. The consensus average target of approximately $17.29 implies roughly 15 percent upside from recent levels. The consensus view is shifting from skepticism to cautious optimism, though the stock remains under-owned by institutional investors—a classic turnaround setup where the improvement in fundamentals is running ahead of the improvement in sentiment.

The Bear Case. O-I is still a commodity business with limited pricing power and a customer base that negotiates aggressively. No amount of sustainability messaging changes the fundamental economics of selling bottles at thin margins to companies with enormous purchasing leverage.

The five billion dollars in total debt—carrying coupons of 6.25 to 7.375 percent—remains a significant burden, consuming cash that could otherwise be invested or returned to shareholders. The company has not paid a dividend in over five years and has no buyback program.

Aluminum is a serious and growing competitive threat. The aluminum beverage can market is growing at roughly 6 percent annually—faster than glass—and new regulations are expanding aluminum's addressable market into wine and spirits. The weight advantage of aluminum (a 90-gram aluminum bottle versus a 500-gram glass equivalent) translates directly into lower transport costs and lower transport-phase carbon emissions, undermining one of glass's sustainability arguments.

Revenue has declined from $7.1 billion in 2023 to $6.4 billion in 2025 with no volume recovery in guidance. European demand remains soft, requiring continued restructuring. The MAGMA technology write-off removes a prior differentiation narrative and represents a sunk cost.

Energy cost volatility—the $150 million step-up from expiring European contracts in 2026—illustrates the ongoing margin pressure. Secular trends in developed markets point toward declining alcohol consumption, particularly among younger demographics, which could erode O-I's largest end market over time. And the energy intensity of glass manufacturing means that future climate regulations could increase costs rather than provide tailwinds.

Key Metrics to Watch. For investors tracking O-I's trajectory, two KPIs matter above all else. First, net debt-to-EBITDA ratio: the company's target of 2.5x by year-end 2027 is the single most important milestone for de-risking the equity. At 3.5x today, the balance sheet still constrains strategic flexibility and amplifies earnings volatility. Progress toward 2.5x—or failure to reach it—will determine whether O-I becomes a genuine turnaround story or remains a perpetual value trap. Second, EBITDA margins: the expansion from 16.8 to 19.0 percent in 2025 demonstrated that Fit to Win savings are flowing through. Sustaining margins at or above 19 percent as energy costs step up and volumes remain soft will be the real test of whether the operational improvements are durable or merely transitory.

XII. Epilogue and Future Outlook

Where does O-I go from here?

Three scenarios frame the range of possibilities.

In the first scenario, O-I becomes the consolidator. As the largest player in a fragmented industry, with improving financial health and operational momentum, O-I could acquire distressed competitors or specific plant assets to further rationalize capacity and strengthen its market position. Ardagh's elevated leverage and ongoing restructuring could create opportunities. In this scenario, O-I gradually evolves into the dominant player in a more disciplined oligopoly, with pricing power that its current market structure does not support.

In the second scenario, private equity returns. Once leverage declines to manageable levels—perhaps below 3x—the steady cash flow generation of a right-sized glass manufacturing business could attract a take-private offer. The playbook would be different from the KKR era: buy a company that has already been restructured, optimize further, and harvest cash flows.

This scenario becomes more plausible as interest rates moderate and the sustainability narrative makes glass packaging a more attractive asset class.

In the third scenario—and perhaps the most likely—O-I continues as a public company, focused on sustainable growth, steady deleveraging, and incremental margin expansion. This is not a venture-scale outcome, but it could deliver solid risk-adjusted returns from current valuation levels. The 2026 guidance of $1.25 to $1.30 billion in adjusted EBITDA and approximately $200 million in free cash flow suggests a company on a credible, if unspectacular, trajectory.

The bigger question transcends O-I itself: Will glass genuinely win the sustainability war, or is the current narrative a temporary reprieve? The answer likely lies somewhere in between. Glass will not reclaim the mass-market beverage categories lost to plastic—those economics are too deeply entrenched. But in premium beverages, in markets with strong deposit return schemes, and in categories where the packaging is part of the brand experience, glass has a durable and possibly growing role.

Technology could reshape the equation. Hydrogen-powered furnaces, carbon capture and storage, and hybrid-electric melting technologies all have the potential to dramatically reduce glass manufacturing's carbon footprint, addressing the one sustainability argument that currently favors aluminum.

O-I's investments in GOAT furnaces and hybrid-flex technology, along with the $125 million DOE grant for industrial decarbonization, position it to benefit from these advances. Ultra-lightweight glass—bottles that deliver the same premium feel at lower weight—could narrow the transport cost gap with aluminum and plastic.

Emerging markets represent another growth vector. Beer and wine consumption continues to rise in Asia, Africa, and parts of Latin America, and glass remains the culturally preferred packaging format in many of these regions. O-I's geographic footprint, with 69 plants in 19 countries, provides a platform for capturing this growth, though capital discipline will be essential to avoid the mistakes of past expansions.

Regulation will play an increasingly important role. Extended Producer Responsibility schemes, deposit return systems, and recycled content mandates are spreading globally. Each of these policies changes the economics of packaging choice, and glass—with its infinite recyclability—generally benefits from a regulatory framework that prices in environmental externalities.

What would need to happen for O-I to become a true compounder rather than a cyclical value play? Three things: sustained margin expansion into the low-to-mid twenties, leverage below 2.5x with the ability to fund modest growth and shareholder returns, and evidence that the sustainability tailwind is translating into structural volume growth rather than just narrative support. None of those are guaranteed. All of them are plausible.

XIII. Closing Reflections

This is not a story about a tech unicorn or a disruptive startup. It is a story about survival, humility, and industrial evolution—about a century-old manufacturer that almost died from the debt its financial sponsors loaded onto it, the disruption of the material it had spent a hundred years perfecting, and the self-inflicted wounds of leaders who believed capital allocation tricks could substitute for operational excellence.

O-I Glass is a reminder that in capital-intensive industries, the fundamentals always win eventually. Fancy financial structures, aggressive buybacks, activist demands—none of them matter if the plants are not running efficiently, the costs are not controlled, and the product is not meeting customer needs.

The Fit to Win program's success, delivering $300 million in savings and nearly doubling EPS in a single year, is not a triumph of financial engineering. It is a triumph of blocking and tackling—of doing the hard, unglamorous work of optimizing a manufacturing business.

The comeback is not guaranteed. O-I still carries five billion dollars in debt. Its customers still have enormous bargaining power. Aluminum is a real and growing threat. Secular trends in alcohol consumption in developed markets are not favorable. But the operating improvements are real, the sustainability tailwind is strengthening, and the valuation reflects deep skepticism that may not be warranted.

For operators, the lesson is clear: operational excellence matters more than financial alchemy.

For investors, the lesson is more nuanced: turnarounds in capital-intensive industries require patience, a tolerance for volatility, and a willingness to look past the balance sheet to the underlying business dynamics.

O-I's biggest surprise is how a "dying" industry found new life through sustainability—a reminder that competitive advantages can emerge from the most unexpected places, and that the companies that survive long enough to benefit from macro shifts are the ones that never stopped improving their operations, even when the narrative was against them.

XIV. Further Reading and Resources

O-I Glass 10-K Annual Reports (2015-2025) — SEC filings remain essential for understanding the debt crisis and turnaround in granular detail. The year-over-year changes in leverage ratios, restructuring charges, and segment profitability tell the real story.

"The New Plastics Economy" by the Ellen MacArthur Foundation — The foundational document on circular economy thinking and the environmental case against single-use plastic. Essential context for understanding why the sustainability narrative shifted in glass's favor.

KKR Case Studies on Leveraged Buyouts — The 1987 O-I deal remains one of the most instructive examples of how LBOs interact with capital-intensive commodity businesses. The comparison with other KKR deals of the era illuminates what went wrong.

O-I Glass Investor Relations Site: CEO Presentations and Earnings Calls (2020-2026) — The evolution from Lopez's operational focus to Hardie's Fit to Win program is best tracked through the investor presentations, which provide detailed breakdowns of savings initiatives and capacity rationalization.

EU Single-Use Plastics Directive Documentation — The regulatory framework that is reshaping packaging economics across Europe. Understanding the directive's specific provisions—EPR fees, recycled content mandates, deposit return schemes—is critical for evaluating glass's competitive positioning.

Ardagh Group and Verallia Investor Materials — Understanding O-I requires understanding its primary competitors. Ardagh's higher leverage and Verallia's superior margins provide useful benchmarks for evaluating O-I's operational performance and strategic positioning.

"Barbarians at the Gate" by Bryan Burrough and John Helyar — The definitive account of the LBO era that produced the KKR-O-I deal. While the book focuses on the RJR Nabisco transaction, it provides essential context for understanding the financial engineering culture that shaped O-I's destiny.

"The Outsiders" by William Thorndike — The counterpoint to O-I's capital allocation mistakes. Thorndike's profiles of exceptional capital allocators illustrate what good buyback discipline looks like—a stark contrast with O-I's debt-funded repurchases.

Glass International and Packaging Dive Archives — Trade publications that provide the best ongoing coverage of industry trends, technology developments, and competitive dynamics. The Packaging Dive coverage of MAGMA's rise and fall is particularly instructive.

"Capitalism Without Capital" by Jonathan Haskel and Stian Westlake — A framework for understanding why tangible-asset-heavy businesses like O-I face structural disadvantages in an economy increasingly dominated by intangible assets. Essential reading for understanding why glass manufacturers trade at persistent discounts to asset-light businesses.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube