NXP Semiconductors: The Sovereign of the Software-Defined Vehicle

I. Introduction & Episode Roadmap

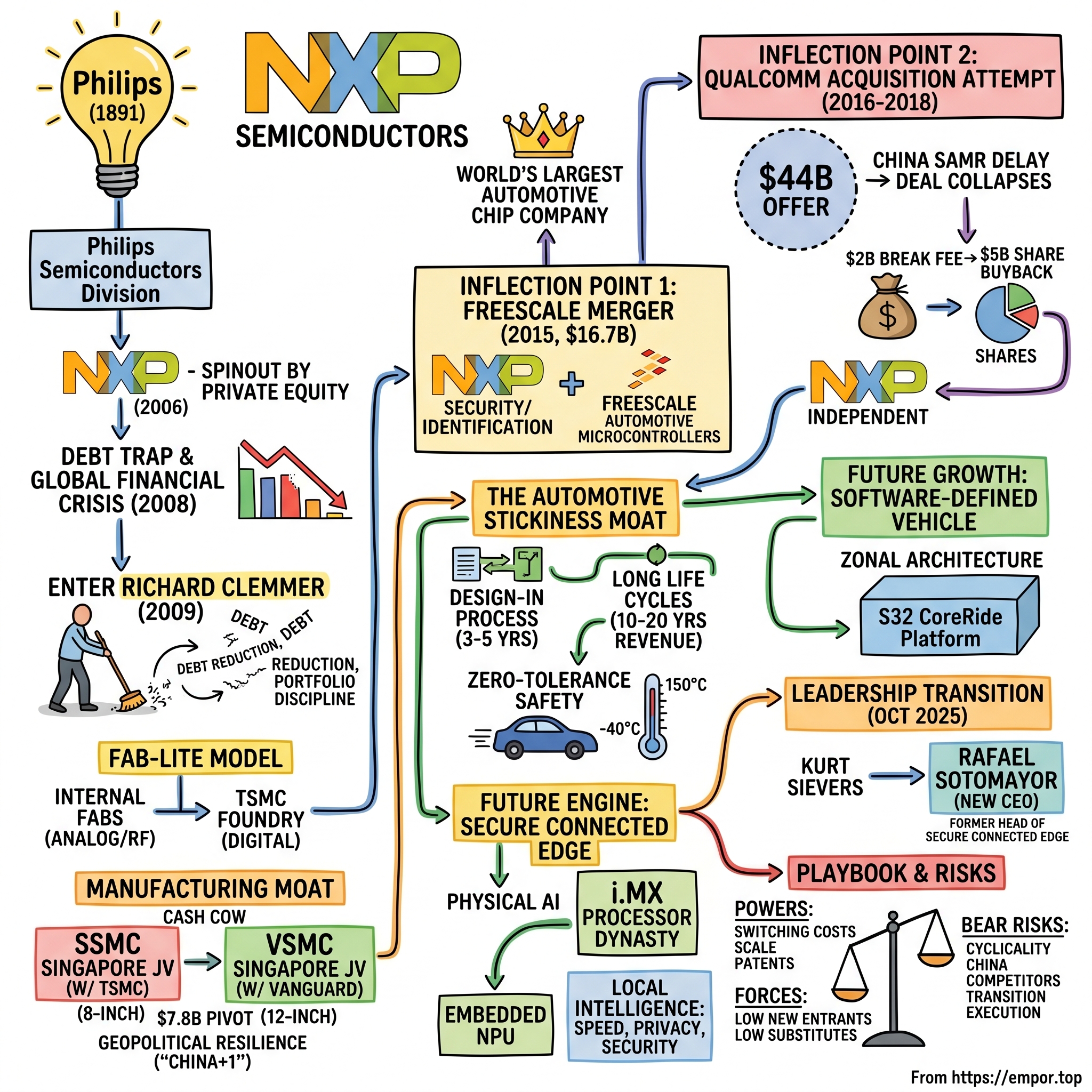

Picture the last car you sat in. Not the engine, not the leather, not the touchscreen you cursed at while trying to change the radio station. Picture the invisible nervous system underneath it all — the dozens of tiny silicon brains deciding, thousands of times per second, whether to fire the airbag, whether the key fob in your pocket is genuine, whether the radar at the front bumper has just spotted a child stepping off a curb. There is a decent chance that a meaningful fraction of those decisions are being executed on chips designed by a company most drivers have never heard of, headquartered in Eindhoven, the Netherlands, and born from the same Dutch conglomerate that once made the lightbulb in your grandmother's kitchen lamp.

That company is NXP Semiconductors N.V., and it trades on the NASDAQ under the ticker NXPI. In its 2025 fiscal year, NXP generated roughly $12.27 billion in revenue and carried a market capitalization north of $50 billion.1 It sits as the undisputed number two in one of the most consolidated, most defensible, and least glamorous corners of the entire technology economy: the automotive semiconductor market.

Here is the first thing to understand, and it cuts against every instinct trained by a decade of breathless coverage of Nvidia, TSMC, and the race to sub-3-nanometer process nodes. This is not that story. NXP does not win by building the smallest, fastest, most transistor-dense chip on Earth for a data center training a large language model. NXP wins in the opposite direction — in what we might call "Physical AI." These are the specialty, high-reliability, analog and mixed-signal chips that have to survive a Siberian winter and a Death Valley summer, that have to work flawlessly for fifteen years inside a vibrating steel box, that control braking, radar, secure entry, battery management, and the secure element in your contactless payment card. The miracle of NXP is not how small the transistor is. It is how absolutely, ruthlessly, life-or-death reliable the whole system has to be.

So how did a spinout of a Dutch lighting empire become the literal brains inside almost every modern car on Earth? That is the question this episode answers, and the answer runs through two of the most extraordinary corporate inflection points in modern semiconductor history.

The first was an act of creation: the $16.7 billion merger with Freescale Semiconductor in 2015, a deal that fused NXP's security and identification heritage with Freescale's automotive microcontroller dominance and, overnight, minted the world's largest automotive chip company.9

The second was an act of survival: the $44 billion acquisition attempt by Qualcomm that began in 2016, dragged through twenty-one months of geopolitical purgatory, and finally collapsed in July 2018 — leaving NXP with a $2 billion consolation cheque and a masterclass opportunity in capital allocation.78

Along the way we will dissect the unusual "fab-lite" manufacturing model anchored in Singapore, the new $7.8 billion fab joint venture that is NXP's bet on the next decade, the landmark October 2025 leadership transition to new CEO Rafael Sotomayor, and the playbook of high-barrier silicon — why, once an NXP chip is designed into a car, it is almost impossible to get out.

Let's start where every good origin story starts: with a lightbulb.

II. Origins: From Philips to the Birth of NXP

In 1891, in the small Dutch city of Eindhoven, Gerard Philips and his father Frederik bought a modest factory and began manufacturing carbon-filament lightbulbs. Over the following century, Koninklijke Philips — Royal Philips — became one of Europe's defining industrial conglomerates, a sprawling empire that made everything from electric shavers to medical scanners to the compact disc, which Philips co-invented with Sony in 1979. Somewhere inside that empire, almost as a tool-making afterthought, Philips built semiconductors. You cannot make sophisticated consumer electronics without chips, and rather than buy them, Philips made its own.

By the early 2000s, the global electronics business had changed underneath Philips's feet, and the conglomerate model was falling out of fashion. Investors wanted focus. The semiconductor division, capital-hungry and cyclical, was a poor fit inside a company that increasingly wanted to be a calm, high-margin health-technology business. So Philips did what conglomerates do when a limb no longer fits the body: it cut it loose.

In 2006, Philips sold an 80.1% stake in its semiconductor division to a consortium of private equity giants — Kohlberg Kravis Roberts (KKR), Bain Capital, Silver Lake, Apax, and AlpInvest — in a transaction valuing the unit at roughly €8.3 billion.2 The newly independent company needed a name. It chose NXP, short for "Next Experience." It was a clean break: a 115-year-old industrial pedigree, suddenly recast as a standalone, leveraged buyout.

The Debt Trap

Here is where the origin story turns dark, and where NXP's entire future strategy was forged in fire. A leveraged buyout, by definition, loads the acquired company with debt — the private equity owners borrow against the company's own future cash flows to fund the purchase. NXP emerged from the Philips carve-out saddled with billions of dollars of high-interest debt. And the timing could not have been worse. Within eighteen months of the spinout, the world fell off a cliff.

The 2008 Global Financial Crisis hit the semiconductor industry like a wrecking ball. Demand for chips collapsed as consumers stopped buying cars, phones, and televisions overnight. For a normal company, this would have been painful. For a company carrying a buyout-sized debt load with interest payments due regardless of revenue, it was nearly fatal. NXP's revenue cratered, its losses mounted, and the debt that had seemed manageable in 2006 became an anchor threatening to drag the whole enterprise under.

Enter Richard Clemmer

Into this crisis, in January 2009, walked a Texan named Richard Clemmer. Clemmer was a semiconductor industry veteran — he had run Agere Systems, the Lucent chip spinout, and had a reputation as a sharp, unsentimental operator who understood both the technology and the balance sheet. He was exactly the kind of executive you hire when the building is on fire and you need someone who will not flinch at hard decisions.

Clemmer's diagnosis was brutal and correct. NXP was trying to do too much. It was competing across an enormously broad portfolio, including in commodity digital logic where it had no structural advantage — segments where the company was a distant third or fourth player, burning cash to fight giants on their own terms. So Clemmer reached for a playbook borrowed, in spirit, from the great Hewlett-Packard and Agilent traditions of portfolio discipline.

The principle was simple and ruthless: if NXP could not be the clear number one or number two in a specific niche, with a credible path to high gross margins, it had no business being there at all. Everything else would be sold, shut, or starved. Out went commodity product lines. Out, eventually, went the home-electronics and cordless-phone businesses. NXP shed its low-margin, low-defensibility limbs and concentrated its remaining strength on the places where it had genuine technical moats: secure identification, automotive, and specialized analog and mixed-signal silicon.

The Fab-Lite Genesis

The most consequential decision of this era was about manufacturing, and to understand it you need to understand the brutal economics of building a chip factory. A leading-edge digital fab — the kind that makes the latest processors for phones and data centers — can cost ten, fifteen, even twenty billion dollars, and it becomes obsolete in a handful of years as the industry marches to ever-smaller transistors. To justify that spending, you need staggering volume. Only a tiny handful of companies on Earth — 台積電 TSMC, Samsung, Intel — can play that game.

Clemmer's NXP looked at this and concluded, correctly, that trying to compete in bleeding-edge digital fabrication was a fool's errand for a company of its size. So NXP committed to what the industry calls a "fab-lite" or hybrid model. The logic was elegant: keep in-house only the manufacturing that is genuinely proprietary and durable — the specialized analog, radio-frequency, and mixed-signal processes, often on mature nodes, where NXP had custom recipes refined over decades and where the factory stays useful for twenty years rather than three. For everything standardized and digital — the parts that needed cutting-edge nodes — outsource to foundries like TSMC and let someone else carry the capital risk.

This was not a temporary fix. It became NXP's permanent identity, and it is the single most important thing to understand about how the company makes money to this day. By 2010, the turnaround had stabilized the company enough to attempt the obvious next step. In August 2010, NXP went public on the NASDAQ, finally giving its private equity owners a path to exit and giving the reborn company a public currency.

But a public listing was only the beginning. NXP had survived. Now it needed to do something far more ambitious — it needed to become the king of a market that did not yet know it needed a king. And to do that, it would need to swallow a company nearly its own size, built from the bones of an American industrial legend.

III. Inflection Point 1: The $16.7B Freescale Merger

Eight hundred miles south of Silicon Valley, in Austin, Texas, sat a company with a story that rhymed eerily with NXP's own. Its name was Freescale Semiconductor, and if NXP was the chip child of Dutch lighting, Freescale was the chip child of American radio.

Freescale's lineage ran straight back to Motorola — the company that built the first car radios in the 1930s, the walkie-talkies of World War II, the equipment that carried Neil Armstrong's voice back from the Moon, and the first commercial cell phone. Motorola's semiconductor division was a crown jewel of American engineering, the place that built the 68000 microprocessor inside the original Apple Macintosh and, crucially, became the dominant supplier of the microcontrollers that ran the guts of automobiles. In 2004, Motorola spun the division off as Freescale.

And then, in a twist that should sound deeply familiar, Freescale was taken private in 2006 — the very same year NXP was carved out of Philips — by a private equity consortium of Blackstone, Carlyle, TPG, and Permira, in a buyout valued at roughly $17.6 billion, one of the largest tech LBOs in history at the time. Freescale, like NXP, walked straight out of its buyout and into the 2008 financial crisis carrying a crushing debt load. Two companies, born of two industrial legends, both leveraged to the hilt, both nearly drowned by the same wave. They were practically twins separated at birth.

By 2015, both had survived, both had gone public again, and both were looking at the same future and reaching the same conclusion: the automotive chip market was about to explode, and scale would decide the winners.

The Strategic Logic

On March 1, 2015, NXP announced it would acquire Freescale in a cash-and-stock transaction with an enterprise value of approximately $16.7 billion, with an equity value around $11.8 billion.9 The strategic fit was almost suspiciously perfect, the kind of complementarity that deal-makers dream about and rarely find.

Think of it this way. NXP brought two crown jewels to the table: the world's leading position in secure identification — the chips inside passports, payment cards, and transit passes — and a strong automotive franchise in things like in-car networking and radar. Freescale brought the other half of the car: it was a dominant force in automotive microcontrollers, the small but essential processors that act as the local brains for individual functions like engine timing, and in the broader processing silicon that ran a vehicle's systems. Put NXP's security and connectivity together with Freescale's microcontrollers and processing, and you had not just a bigger company — you had a company that could supply the entire electronic backbone of a modern vehicle, from the secure key fob to the radar to the central processor. Overnight, the combined entity became the world's largest supplier of automotive semiconductors, with a breadth no single competitor could easily replicate.

Was It a Good Deal? The Comps

Now, the question every investor should ask: did NXP overpay? To answer that, you have to put the deal in the context of 2015, which was the single most frenzied year of consolidation the semiconductor industry had ever seen — a wave of mega-mergers driven by exactly the same logic of scale.10

Let's translate the multiples into plain English. At announcement, NXP valued Freescale at roughly 3.6 times its trailing annual revenue and about 15.8 times its trailing EBITDA — EBITDA being a rough proxy for the cash earnings a business throws off before financing and accounting effects.9 On its own, 15.8 times earnings sounds rich.

But look at what everyone else was paying that same year. Intel bought the programmable-logic maker Altera at around 7.5 times revenue and nearly 25 times EBITDA — a colossal premium for a prized asset. Avago's industry-redefining acquisition of Broadcom, the deal that created the modern Broadcom, ran around 4.0 times revenue and 18.8 times EBITDA. Against that backdrop, NXP's 3.6 times revenue and 15.8 times EBITDA for Freescale was not extravagant at all. It was, if anything, on the cheaper end of the wave — a disciplined buyer picking up a strategically essential asset while rivals paid far more for theirs.

The Synergy Secret

But the headline multiple was only half the story, and here is where the deal went from "reasonable" to "genuinely shrewd." NXP committed to wringing out $500 million in annual cost synergies from the combination — eliminating duplicate overhead, consolidating manufacturing, and rationalizing overlapping product lines. And critically, NXP actually executed on that promise.

Here is why that matters so much. When you fold $500 million of recurring annual savings into the acquired company's earnings, you are effectively increasing the EBITDA you bought without paying a cent more. Run that math and the effective purchase multiple drops from that initial 15.8 times down to roughly 10.5 times EBITDA on a fully synergized basis. A 10.5 times multiple for the company that instantly makes you the global leader in the most defensible chip market on the planet is not a good deal — it is a steal. The synergies were the difference between paying a fair market price and paying a deeply accretive one.

The merger closed in December 2015, and the new NXP that emerged was a fundamentally different animal. It was no longer a turnaround story clawing its way out of a debt hole. It was the sovereign of automotive silicon, a company with a combined scale and product breadth that would take competitors a decade and tens of billions of dollars to even approach.

Which, naturally, made it a target. Because in the technology world, there is nothing more dangerous than building something valuable — someone always comes knocking. And in October 2016, the knock came from San Diego, in the form of a $110-per-share offer from one of the most powerful and most feared companies in the entire chip industry.

IV. Inflection Point 2: The $44B Ghost Deal & The $2B Consolation Prize

Qualcomm had a problem that most companies would kill for, and that is precisely why it was so dangerous. The San Diego giant sat atop a mountain of cash, minting royalties on essentially every smartphone sold on Earth through its dominance of cellular modem and patent licensing. But the smartphone market — Qualcomm's entire kingdom — was maturing. Growth was slowing. The board and management looked at the horizon and saw the same thing everyone in tech was seeing: the next decade of silicon growth would come from cars and connected devices, not from yet another phone. Qualcomm needed to diversify, and it needed to do it fast.

NXP was the obvious, perhaps the only, prize. It offered Qualcomm an instant, dominant position in automotive and a deep franchise in the Internet of Things — exactly the markets Qualcomm lacked and could not realistically build from scratch. So in October 2016, Qualcomm launched a bid to acquire NXP for $110 per share, a transaction valued at roughly $38 billion in equity, or around $47 billion including NXP's debt.7

Activists Force a Sweetener

A funny thing happened on the way to the merger. As the deal sat in regulatory review month after month, NXP's standalone business kept getting better and its shares became increasingly attractive, and a chorus of activist investors — led by Elliott Management — began arguing loudly that $110 a share dramatically undervalued the company. They were not wrong. The pressure worked. In February 2018, Qualcomm sweetened its offer to $127.50 per share in all cash, lifting the total deal value to roughly $44 billion.7 A significant majority of NXP shareholders tendered into the higher price. By early 2018, the deal looked done. Eight of the nine global antitrust regulators whose blessing was required had signed off.

There was just one signature missing. And it happened to be the most geopolitically loaded signature on the planet.

Twenty-One Months in Geopolitical Purgatory

The one regulator who had not approved the deal was China's State Administration for Market Regulation, known as SAMR. And by mid-2018, the Qualcomm–NXP merger had stopped being a business transaction and become a hostage in something far larger than either company.

The United States and China were sliding into a full-blown trade war. The Trump administration was imposing tariffs and, more pointedly, had moved to choke off the Chinese telecommunications champion ZTE by cutting its access to American components. Qualcomm — a crown jewel of American semiconductor power, and a company deeply dependent on the Chinese market — was the perfect lever. SAMR did not reject the merger. It did something more excruciating: it simply did nothing. The file sat. And sat. Month after month, SAMR declined to rule, holding the largest semiconductor acquisition in history in a state of suspended animation as a bargaining chip in a fight between two governments.

For NXP, this was twenty-one months of corporate limbo. The company could not fully plan as an independent entity, could not be fully integrated into Qualcomm, and watched as its fate was decided in rooms in Washington and Beijing that had nothing to do with chips.

The Midnight Deadline and the Break Fee

Every merger agreement has an outside date — a deadline past which either party can walk away. Qualcomm's agreement with NXP had been extended again and again, each time in the hope that Beijing would relent. By July 2018, with the trade war escalating rather than cooling, Qualcomm faced a decision. It could extend yet again and keep waiting on a Chinese government that had shown no inclination to move, or it could walk.

On July 25, 2018, Qualcomm walked.7 It terminated the agreement rather than extend it into an open-ended geopolitical wait. But walking away from NXP was not free. Buried in the merger agreement was a termination fee — a contractual penalty designed to compensate the target if the acquirer fails to complete the deal. Qualcomm owed NXP $2 billion in cash, and it paid it.8 In the same breath, having freed up the enormous capital it had reserved for the acquisition, Qualcomm announced a $30 billion share buyback of its own.8

So picture NXP's position in the summer of 2018. The deal it had spent nearly two years preparing for was dead. Its shares, which had been trading near the deal price, suddenly traded on standalone fundamentals again and dropped sharply. And it had, sitting in its bank account, a $2 billion cash windfall with no strings attached. What it did next is the part that belongs in a capital-allocation textbook.

A Masterclass in Capital Deployment

Here is the trap that a lesser management team falls into. You have $2 billion in unexpected cash and a wounded ego. The temptation is to spend it — to go make a splashy acquisition to prove you are still a growth story, to do something that looks decisive. NXP did the opposite, and it did so with cold discipline.

Management's view was simple: the most undervalued, highest-conviction asset NXP could possibly buy was NXP itself. Its own shares had been knocked down by the deal's collapse to levels management considered far below intrinsic value. So instead of chasing a desperate acquisition, NXP launched a massive $5 billion share buyback program — funded by the break fee plus its own strong cash generation and balance-sheet capacity — and executed it with stunning speed, repurchasing 54.4 million shares by the end of 2018.8

The effect was dramatic. By buying back its own deeply discounted stock so aggressively, NXP shrank its diluted share count by roughly 15% in a matter of months. Think about what that means for an owner. The company's profits were now divided among 15% fewer shares, which mechanically boosted earnings per share by a comparable magnitude — without selling a single additional chip. Every remaining shareholder suddenly owned a meaningfully larger slice of the same business, bought at what proved to be a low price.

It is one of the great quiet lessons of modern capital markets, and it sits at the heart of the NXP investment story: sometimes the best deal a company ever does is the one that falls apart. The failed Qualcomm acquisition, which at the time looked like a humiliation, set NXP up as a lean, independent, ferociously cash-generative machine — and freed it to keep building the automotive franchise that Qualcomm had wanted to own. Which brings us to the engine room itself.

V. Inside the Core Engine: The Automotive Stickiness Moat

To understand NXP, you have to internalize one number above all others. Of the company's roughly $12.27 billion in 2025 revenue, the Automotive segment accounted for about $7.12 billion — roughly 58% of the entire company.1 This is not a company with a car business. This is a car-chip company with some other interesting things attached. Everything else — the industrial, the mobile, the connectivity — orbits around this core. So if you want to know whether NXP will thrive or struggle, you have to understand why automotive silicon is such an extraordinary place to do business.

And the answer has almost nothing to do with the things that make headlines in the chip world. NXP does not win in cars by having the smallest transistor or the fastest clock speed. It wins on something far more durable and far harder to replicate: trust, reliability, and the most powerful lock-in mechanism in the entire industry.

The Twenty-Year Relationship

Let's walk through what it actually takes to get an NXP chip into a car, because the process itself is the moat.

When an automaker decides to design a new vehicle, it does not simply buy chips off a shelf. It enters into a multi-year engineering collaboration — typically three to five years before the car ever reaches a showroom — working hand-in-glove with its Tier-1 suppliers (the Bosches and Continentals of the world) and, increasingly, directly with the chipmaker. During those years, NXP's engineers and the automaker's engineers co-develop, test, and qualify the exact chip for the exact function in the exact vehicle. The chip gets woven into the car's circuit board layouts, its software, and its safety architecture.

Now here is the magic. Once that chip is "designed in," it is locked in for the entire life of the vehicle program. A car model, once launched, is typically manufactured for seven to ten years. And then — because cars need replacement parts — the automaker requires the chipmaker to keep supplying that exact component for another decade after the last car rolls off the line. Do the arithmetic and a single design win can mean a fifteen-to-twenty-year revenue relationship from one decision.

This is why automotive is so prized, and it is the textbook definition of switching costs. Once you are designed in, ripping you out is nearly unthinkable. To swap NXP's chip for a competitor's, the automaker would have to redo the software, redesign the circuit board, and re-run the entire battery of safety certifications — spending millions of dollars and years of time to save pennies per chip. No rational engineering organization does that. The incumbent simply keeps winning, year after year, program after program.

The Zero-Tolerance Standard

There is a second, related reason automotive silicon commands premium margins, and it comes down to the savage operating environment. The chip in your phone lives a pampered life — room temperature, no vibration, and if it crashes, you reboot and grumble. The chip controlling your brakes enjoys no such luxury. It must function flawlessly from minus 40 degrees Celsius in a Canadian winter to 150 degrees Celsius next to a hot engine block. It must survive years of relentless vibration, thermal cycling, and humidity. And it must do so while carrying rigorous functional-safety certifications under the ISO 26262 standard — the framework that governs how electronics in a car must be designed so that a failure cannot kill the occupant.

Meeting that standard is brutally hard, takes years of qualification, and only a small number of companies in the world have proven they can do it at scale. That difficulty is precisely the point. It is a barrier that keeps new entrants and commodity players permanently outside the gate, and it lets the incumbents earn the margins that fund the next generation of products.

The Competitive Landscape

NXP does not have this market to itself. Automotive semiconductors are an oligopoly — a small club of disciplined players who compete fiercely on technology but rarely on suicidal price wars, because everyone understands that the long design cycles and reliability demands reward stability over share-grabbing. The top five players together control roughly half of the global market.[^13]

At the top sits Infineon Technologies, the German power-semiconductor specialist and the global number one, with roughly a 13.7% share and around $8.2 billion in automotive revenue.[^14] Infineon's particular crown is power — especially silicon carbide, the next-generation material that makes electric-vehicle drivetrains more efficient. NXP sits at number two, with a 10.4% to 11.0% share and that ~$7.1 billion in automotive revenue, dominant in the car's processing, secure access and NFC entry, and radar.1[^13]

Behind them comes STMicroelectronics, the Franco-Italian giant at around 9% share, strong in silicon carbide and well known for its partnership supplying Tesla. Then Texas Instruments at roughly 8.4%, leveraging its enormous, low-cost 300-millimeter analog manufacturing to compete on price and breadth. And rounding out the top five, Japan's ルネサス エレクトロニクス Renesas Electronics at around 7%, historically NXP's fiercest rival in the automotive microcontroller business — the two have battled over the local "brains" of vehicles for decades.

What this structure tells an investor is encouraging: this is a rational, high-margin oligopoly where competitors largely respect one another's territory and compete on system-level integration and engineering rather than on destructive discounting. That discipline is a big part of why margins across the group stay healthy.

The Modern Battleground: Software-Defined Vehicles

But the ground is shifting, and the shift is the single most important growth driver for NXP's core business. For decades, a car's electronics evolved by accretion. Every time an automaker added a feature — power windows, anti-lock brakes, a backup camera — it bolted on another small dedicated computer, called an electronic control unit, or ECU. By the 2010s, a premium vehicle might contain a hundred or more of these little ECUs scattered throughout the chassis, each running its own software, all wired together in an increasingly unmanageable tangle. It was the automotive equivalent of a house that had been renovated one room at a time for fifty years with no master plan.

The industry's answer is the software-defined vehicle, built on what is called a "zonal architecture." Instead of a hundred isolated chips, the car is reorganized around a handful of powerful central and zonal processors that consolidate functions and run them as software, much the way a modern data center virtualizes what used to be dozens of separate servers. The car becomes a computer on wheels that can be updated over the air, with features added or changed long after it leaves the factory.

This transition is a profound opportunity for NXP, because it plays directly to the company's strengths in processing, networking, and power management all working together. NXP's answer is its S32 CoreRide platform — an integrated package that bundles the central processing, the in-vehicle networking that ties the zones together, and the power management into a single, software-defined system that automakers can build on.1 Rather than selling a hundred discrete chips, NXP increasingly sells the integrated backbone of the car's entire electronic nervous system — a far stickier, higher-value position. The company that owns that backbone owns the automaker for the next generation of vehicles.

But a platform is only as good as the factory that can actually build it, reliably, for fifteen years. And NXP's manufacturing strategy is just as unconventional, and just as deliberate, as everything else about the company.

VI. The Manufacturing Moat: Joint Ventures & The Singapore Strategic Hub

Roughly halfway around the world from Eindhoven, on the eastern edge of Singapore in a district called Pasir Ris, sits a chip factory that has been quietly printing money for over two decades. Most people have never heard of it. But it embodies the philosophy that lets NXP punch far above its capital weight — the idea, born in Richard Clemmer's turnaround, that you should own only the manufacturing that is genuinely proprietary, and share the cost and risk of everything else.

Recall the fab-lite model: NXP manufactures roughly 40% of its wafers internally, concentrating on the highly proprietary analog, RF, and mixed-signal chips where it has custom process recipes refined over decades and where the equipment stays useful for twenty years. The rest — the standardized digital logic that needs advanced sub-16-nanometer nodes — it outsources to foundries like TSMC, letting them carry the brutal capital burden of leading-edge fabrication. But the truly clever part is what NXP does with the manufacturing it does keep close: it rarely builds those factories alone. It builds them with partners.

SSMC: The Cash Cow

That factory in Pasir Ris is SSMC — Systems on Silicon Manufacturing Company — a joint venture founded back in 1998. Today it is owned 61.2% by NXP and 38.8% by TSMC.1 It produces 8-inch (200-millimeter) wafers full of the specialized mixed-signal chips that go into automobiles and secure connectivity products.

Here is why SSMC is such a beautiful asset. After more than two decades of operation, its equipment is fully depreciated — meaning NXP long ago finished paying off the machines on its books, so nearly every wafer it produces now drops to the bottom line at very high margin. It is a fully amortized cash cow, churning out exactly the kind of durable, mature-node specialty silicon that NXP's automotive customers will keep buying for years. By sharing it with TSMC, NXP got the capacity it needed without bearing the full cost or risk alone. This is the joint-venture blueprint in its mature, profitable form.

VSMC: The $7.8 Billion Pivot

But there was a problem looming over SSMC and every fab like it, and by 2024 NXP had to confront it. The 8-inch wafer is becoming obsolete. The equipment that makes 200-millimeter wafers is no longer being manufactured in volume; the industry has decisively moved to larger, more efficient 12-inch (300-millimeter) wafers, which yield far more chips per wafer and dramatically better economics. For NXP to keep manufacturing its specialty automotive and industrial chips for the next twenty years, it needed to migrate those mature processes onto modern 300-millimeter lines. The question was how to do it without blowing a multi-billion-dollar hole in the balance sheet.

The answer came on June 5, 2024, and it followed the playbook to the letter. NXP announced it would partner with Taiwan's 世界先進 Vanguard International Semiconductor — itself a company within the broader TSMC orbit — to build a brand-new 12-inch wafer fab in Singapore, in the Tampines district, through a joint venture named VisionPower Semiconductor Manufacturing Company, or VSMC.[^6]5 The total investment was projected at roughly $7.8 billion over the life of the project.[^6]56

The ownership structure tells you everything about NXP's risk discipline. Vanguard owns 60% of VSMC and will actually operate the fab; NXP owns 40% of the equity.[^6] NXP gets guaranteed access to modern 300-millimeter capacity for its specialty nodes — spanning from 130 nanometers down to 40 nanometers — while letting its partner run the factory and shoulder the majority of the capital and operational burden. First production is slated for 2027.[^6]5 It is the SSMC model, modernized for the next generation.

Geopolitical Resilience: "China + 1"

There is one more dimension to the VSMC decision that elevates it from clever financial engineering to genuine strategic foresight, and it goes back to the same trade-war dynamics that killed the Qualcomm deal. The world's automotive supply chain is dangerously dependent on Taiwan, where TSMC and the bulk of advanced manufacturing reside — and Taiwan sits in one of the most geopolitically fraught locations on the planet. Every automaker and every chipmaker spent the chip shortages of the early 2020s learning, painfully, what happens when a critical supply chain has a single point of failure.

By siting VSMC in Singapore — a stable, neutral, business-friendly nation outside the immediate geopolitical flashpoints, while still drawing on TSMC-derived technology and licensing — NXP and its automotive partners secure a resilient "China plus one" supply base for the decade ahead.5 In a world where supply-chain security has become a board-level and even national-security obsession, the ability to promise automakers a reliable, geographically diversified source of specialty silicon is itself a competitive weapon. The factory is not just an efficiency play; it is an insurance policy that customers will pay a premium for.

So NXP has the moat in automotive and the manufacturing strategy to defend it. But a company cannot live on one engine forever, however good. The most interesting question about NXP's future lies in its smaller, faster-growing businesses — and in a thesis the company calls the Secure Connected Edge.

VII. The Future Engine: Physical AI at the Secure Connected Edge

If automotive is the kingdom, the rest of NXP is the frontier — smaller in revenue today, but where much of the company's future optionality lives. In 2025, the Industrial & IoT segment represented about 18.5% of revenue, around $2.27 billion, and the Mobile segment contributed roughly 12.9%, about $1.58 billion.1 Add in Communication Infrastructure & Other, and you have the remainder of the business. These segments are dwarfed by automotive, but they carry an outsized share of the growth narrative — and they are the personal home turf of the man who, as we will see, now runs the entire company.

What Is the "Secure Connected Edge"?

NXP wraps much of this future in a phrase: the Secure Connected Edge. To understand it, you need to understand a shift happening in how artificial intelligence actually runs.

For the past decade, the mental model of AI has been the cloud. You speak to your phone, your words fly off to a massive data center somewhere, a giant model processes them, and the answer comes back. That works, but it has three real costs. It is slow — there is always a round-trip delay. It is dependent on a connection — no signal, no intelligence. And it is a privacy and security risk — your data has to leave the device and travel across networks to a server you do not control.

The "edge" thesis says: for a huge and growing class of tasks, the intelligence should not live in the cloud at all. It should live right there on the physical device — in the thermostat, the medical monitor, the factory machine, the door lock. This is "Physical AI," and it is the inverse of the cloud-AI story that dominates the headlines. Instead of bigger and bigger models in bigger and bigger data centers, it is smart-enough models running locally, instantly, privately, on cheap and power-sipping chips.

The i.MX Processor Dynasty

NXP has a not-so-secret weapon for this world, and it has been hiding in plain sight for years: the i.MX family of application processors. These are the workhorse brains of the embedded world — low-power, highly integrated processors that have quietly become an industry standard for edge computing. They turn up everywhere once you start looking: in medical monitors at a patient's bedside, in smart-home thermostats and displays, in industrial control panels, in point-of-sale terminals, in building automation. They are not glamorous. They are ubiquitous. And ubiquity, in the embedded world, compounds — because every product that designs in an i.MX processor tends to keep using the family for the next generation, for many of the same switching-cost reasons that make automotive so sticky.

The Physical AI Convergence

The newest chapter is where it gets strategically interesting. With the launch of the i.MX 9 series, NXP began embedding dedicated neural processing units — NPUs, specialized circuitry built to run machine-learning models efficiently — directly into these low-cost, low-power edge processors. In plain terms, NXP is putting a small, efficient AI engine right inside the cheap chip that already runs the device.

What does that unlock? It means a smart device can now run machine-learning tasks locally — recognizing a spoken voice command, performing simple computer vision to spot a defect on a production line, or predicting when a motor is about to fail from its vibration signature — all without sending a single byte to the cloud. The benefits stack neatly on top of one another: it is faster because there is no round-trip, it works without connectivity, and it is far more secure and private because sensitive data never leaves the device. And critically for NXP, security is the company's deepest heritage — the same secure-element and identification IP that protects payment cards can protect the edge device, making NXP one of the few players able to offer processing, AI, and hardened security in a single trusted package.

This is a high-margin, fast-growing business that leverages everything NXP already is, and it leans directly into where computing is heading. It is no accident that when NXP chose its next chief executive, it reached into exactly this part of the company. Which brings us to the new figure at the top.

VIII. Under New Command: Rafael Sotomayor & NXP's Modern Era

On October 28, 2025, one of the longest and most successful executive runs in modern semiconductor history came to a planned, dignified close. Kurt Sievers — who had spent roughly thirty years at NXP and its Philips predecessor, rising through the automotive ranks to lead the entire company as CEO since 2020 — stepped down.311 There was no scandal, no boardroom coup, no activist forcing the issue. It was a textbook succession, telegraphed well in advance and executed without a tremor. NXP had announced the transition months earlier, in April 2025, giving the market and the organization ample time to prepare.311

In a world where CEO transitions are so often messy, abrupt, or destabilizing, the smoothness of this one was itself a statement about NXP's institutional discipline. The company does not lurch. It plans.

The Pedigree of the New Commander

Sievers's successor was Rafael Sotomayor, and the choice of who replaces a beloved long-tenured CEO is one of the most revealing decisions a board ever makes — because it signals where the company believes its future lies.

Sotomayor was no outsider parachuted in to shake things up. He joined NXP in 2014 and rose to become Executive Vice President and General Manager of — of all things — the Secure Connected Edge business unit.311 Read that again, because it is the whole story. The board did not promote the head of the automotive juggernaut, the segment that is 58% of revenue. It promoted the leader of the smaller, faster-growing, edge-AI franchise. The message to anyone paying attention was unmistakable: NXP intends to defend and extend its automotive crown, yes, but it sees its next chapter of growth in the convergence of edge processing, on-device AI, and software-defined architectures — and it wanted a CEO who had personally built that business.

Sotomayor's background reinforces the point. Before NXP, he held senior leadership roles at Broadcom, at Motorola, and at Intel — a career spent across the connectivity, communications, and processing worlds rather than purely in legacy automotive analog.3 He is, in effect, a bet on NXP's evolution from a maker of discrete reliable chips into a platform company that sells integrated, intelligent, secure systems.

Aligning the Commander With the Owners

For investors, a new CEO raises an immediate and reasonable question: is this person's wallet pointed in the same direction as mine? NXP's proxy filings give a detailed answer, and the structure is worth understanding because it is designed specifically to discourage the short-term thinking that destroys long-term businesses.4

Sotomayor's base salary was set at $1,050,000 a year — a relatively modest fixed sum, which is exactly the point in modern executive pay: you want most of the compensation at risk and tied to performance, not guaranteed.4 On top of that sits a short-term Annual Incentive Plan with a target of 170% of base salary, a bonus that pays out based on company-wide financial results — revenue growth, operating margin, and free cash flow.4 In other words, the annual bonus is heavily geared to the very metrics that long-term owners care about, not to vanity measures.

The real alignment, though, lives in the long-term equity. Upon stepping into the CEO seat, Sotomayor received an equity grant valued at $10,500,000 — an order of magnitude larger than his salary, which tells you where the board wants his attention.4 And the structure of that grant is the clever part. It is split between standard Restricted Share Units, which vest over time, and Performance Restricted Share Units, which vest only if NXP actually delivers — specifically against relative total-shareholder-return targets (how NXP's stock performs versus its peers) and earnings-per-share metrics, measured over multi-year periods.4 If NXP underperforms its peer group or fails to grow EPS, a large chunk of that $10.5 million simply evaporates. This is precisely the design you want: it makes reckless short-term risk-taking financially irrational for the person at the top, because the big money only arrives if the company creates durable, multi-year value relative to the field.

As of mid-2026, Sotomayor directly held roughly 10,100 shares of NXP — a stake worth on the order of $2.4 million — a position that grows as his performance-based awards vest over the years ahead.4 It is early days for his personal ownership, as you would expect for a newly minted internal CEO, but the trajectory and the incentive design point the same way: the more value NXP creates for outside shareholders, the wealthier Sotomayor becomes. Owner and operator are pulling on the same rope.

With the leadership question settled, we can step back and ask the deeper structural question — the one that determines whether all of this is a genuinely durable business or merely a well-run one riding a good market. For that, we turn to the frameworks.

IX. Playbook: Seven Powers & Five Forces Analysis

Strip away the chips, the fabs, and the corporate drama, and the question every long-term investor ultimately wants answered is brutally simple: what stops a competitor from showing up and taking this business away? To answer it rigorously, we run NXP through two of the canonical frameworks of business strategy — Hamilton Helmer's Seven Powers and Michael Porter's Five Forces. They tell a remarkably consistent story.

Hamilton's Seven Powers Applied to NXP

The single most important power in the NXP story is switching costs, and we have already seen it in action — but it bears stating as a structural truth. Once an NXP microcontroller or processor is designed into a vehicle's electronic architecture, swapping it for an Infineon or Renesas part is not a procurement decision; it is a multi-million-dollar, multi-year engineering project requiring software rewrites, circuit-board redesigns, and a fresh round of safety certification. No automaker undertakes that to shave a few cents. This is the primary power, and it explains the bulk of NXP's pricing stability and margin durability. The fifteen-to-twenty-year design-in lifecycle is switching costs expressed as time.

The secondary power is scale economies, but with an NXP-specific twist. NXP is not the largest chipmaker on Earth, and in raw fab scale it is dwarfed by the leading-edge foundries. But its scale shows up in two subtler ways. First, it allows NXP to amortize an enormous annual research-and-development budget across a vast, diversified product portfolio — the cost of developing a new automotive platform is spread across thousands of design wins. Second, its scale lets it credibly enter shared mega-projects like the $7.8 billion VSMC fab as a 40% partner, securing the capacity it needs while letting a partner carry the majority of the cost.[^6] Smaller players cannot get a seat at that table at all.

The tertiary power is a cornered resource: NXP's deep, specialized patent portfolio in domains where it is genuinely world-leading — secure near-field communication (the NFC technology in payment and access systems), ultra-wideband precision tracking (the technology behind secure, centimeter-accurate digital car keys), and automotive radar. These are not commodity capabilities. They are the product of decades of focused R&D and they are protected by intellectual property that competitors cannot simply replicate. This is the legacy of the original Philips and Freescale franchises, compounded over twenty years.

Porter's Five Forces Applied to NXP

Run the same business through Porter's lens and the picture is, if anything, even more favorable.

The threat of new entrants is extremely low — arguably as low as anywhere in technology. To enter automotive semiconductors, a newcomer would need billions in capital, years to earn the necessary safety qualifications, and — the killer — deep, trust-based relationships with the world's Tier-1 suppliers and automakers that take a decade to build. Trust, in a business where a chip failure can kill someone, is not for sale.

The bargaining power of buyers is moderate, and the dynamic here is genuinely interesting. Automakers are huge, sophisticated, consolidated buyers, which should give them leverage. But the chip shortages of the early 2020s, which idled assembly lines around the world and cost the auto industry hundreds of billions in lost production, taught automakers a humbling lesson: they are acutely vulnerable to supply disruption, and the chip suppliers hold more power than the size mismatch would suggest. The shift to zonal, software-defined architectures only deepens that dependence, because the automaker is no longer buying a commodity component but committing to NXP's integrated hardware-software platform.

The bargaining power of suppliers is also moderate, and here NXP's hybrid model pays off. For leading-edge nodes, NXP depends on TSMC and other foundries, which are powerful suppliers. But for its core specialty analog and mixed-signal products — the heart of the franchise — NXP's own internal fabs and joint ventures like SSMC and VSMC insulate it from foundry pricing power and from the volatility of the merchant market. It controls the manufacturing that matters most.

The threat of substitutes is extremely low. There is, quite simply, no alternative to silicon for controlling a vehicle's brakes or running an industrial edge device. Software cannot replace the chip; it runs on it.

And competitive rivalry is high but, crucially, disciplined. The handful of major automotive chipmakers compete ferociously on engineering and system-level integration, but they have collectively learned that destructive price wars are mutual suicide in a market defined by long design cycles and high reliability demands. The result is a rational, high-margin oligopoly — the best kind of competitive environment an incumbent could ask for.

Put the two frameworks together and they converge on the same conclusion: NXP sits behind unusually deep and unusually durable moats, anchored by switching costs and reinforced at nearly every structural turn. That is the bull case in its purest, most analytical form. But no honest analysis stops there — every moat has a far side, and every durable business carries risks that could erode it. So let's war-game both sides.

X. The Investor's Ledger: Bull vs. Bear Case & KPIs to Watch

The Bull Case

The most powerful argument for NXP is what you might call the siliconization of the automobile, and it is a tailwind the company barely has to work for. As vehicles electrify, their semiconductor content explodes — an electric vehicle requires roughly twice the chip content of a comparable internal-combustion car, because batteries, inverters, charging systems, and electric drivetrains all demand sophisticated power and control silicon. Layer on top of that the move to software-defined vehicles, which concentrate enormous processing in central and zonal computers — exactly where NXP's S32 platform competes — and you have a structural rise in the dollar value of chips per car that lifts NXP regardless of whether total vehicle unit sales grow at all. More content per car, even with flat car sales, means a growing market.

The second pillar is Physical AI at the edge — the Secure Connected Edge thesis now championed from the very top by a CEO who built that business. On-device machine learning is a large, organically growing market with high gross margins, and it leverages NXP's existing processing and security IP rather than requiring it to buy growth.

The third pillar is capital allocation, which the failed Qualcomm episode proved NXP does exceptionally well. The company is a powerful free-cash-flow generator, returns capital through a rock-solid and growing dividend — set at $1.014 per share quarterly — and has a demonstrated history of opportunistic, value-accretive buybacks when its shares are cheap.14 Owners are rewarded in cash, not just in promises.

And the fourth pillar is the geopolitical safety net: the VSMC Singapore fab gives NXP and its customers a resilient, geographically neutral supply chain for the next decade, an increasingly valuable form of insurance in a fractured world.5

The Bear Case

Now the far side of the moat, because intellectual honesty demands it.

The first and most obvious risk is automotive cyclicality. NXP is 58% an automotive company, and the automotive industry is deeply cyclical, tied to consumer confidence, interest rates, and the broader economy. If global vehicle sales enter a prolonged downturn — as they periodically do — NXP's core engine stalls, and no amount of edge-AI growth in the smaller segments can fully offset it. Concentration is a source of strength in good times and vulnerability in bad ones. The same cyclicality has shown up recently in inventory corrections across the analog and microcontroller industry, which can compress revenue and margins for several quarters at a stretch.

The second risk is the most strategically serious over the long run: the rise of domestic Chinese competitors. China is the world's largest auto market and is pursuing an explicit, state-backed campaign to domesticate its semiconductor supply chain — to replace foreign suppliers like NXP, Infineon, and Renesas with home-grown champions, supported by substantial government subsidies. If Chinese chipmakers succeed in qualifying automotive-grade parts and winning design-ins with domestic automakers, NXP could face share erosion in a market it can scarcely afford to lose. This is a slow-moving but potentially profound threat, and the same trade-war dynamics that once held the Qualcomm deal hostage could resurface as tariffs or restrictions cutting the other way.

The third risk is transition execution. Migrating NXP's core specialty processes from obsolete 8-inch lines to the new 12-inch VSMC fab is technically demanding work. Process transitions can suffer yield problems and schedule slips, and with first production not slated until 2027, there is a multi-year window in which something could go wrong — leaving NXP either short of modern capacity or carrying costs ahead of the revenue to support them.[^6]

The Three KPIs That Matter Most

If you strip the NXP story down to the handful of numbers that genuinely reveal whether the thesis is working, three stand out. These are not predictions and not targets to be calculated here — they are the dials a long-term owner should watch quarter after quarter.

The first is non-GAAP gross margin. This is the single cleanest measure of NXP's pricing power and manufacturing efficiency — the proof that the switching-cost moat and the disciplined oligopoly are translating into real profitability. A gross margin holding at or above roughly 58% signals that the moat is intact; sustained erosion would be the first quantitative sign that competition or commoditization is biting.

The second is free-cash-flow margin — free cash flow as a percentage of revenue. This is the ultimate validation of the fab-lite model. The entire architecture of NXP, from the Clemmer turnaround to the joint-venture fabs, was designed to generate enormous cash without enormous capital spending. A free-cash-flow margin sustained around 25% or higher is the evidence that the capital-light strategy is delivering as designed; a structural decline would suggest the model is breaking, perhaps because NXP is having to spend more on manufacturing than the model promised.

The third is automotive segment year-over-year growth. This is the most direct read on whether NXP is winning or losing the central war. Because the segment is the majority of the company and the heart of every moat we have discussed, its growth rate — measured against both the prior year and against rivals like Infineon and Renesas — tells you in near-real-time whether NXP is gaining or ceding share in the platform battle that will define the next decade of the automobile.

Watch those three, and you are watching the soul of the business: the pricing power, the cash engine, and the core franchise. Everything else in the NXP story — the Dutch lighthouse heritage, the Freescale merger that crowned it, the Qualcomm deal that nearly swallowed it, the Singapore fabs that will sustain it, and the new commander betting it all on intelligence at the edge — ultimately flows through those three numbers. They are how the sovereign of the software-defined vehicle keeps, or loses, its crown.

References

-

NXP Semiconductors N.V. Form 10-K Annual Report for FY2025 — U.S. SEC, 2026-02-27 ↩↩↩↩↩↩↩

-

NXP Announces Planned CEO Transition to Rafael Sotomayor — U.S. SEC Form 8-K, 2025-04-22 ↩↩↩↩

-

NXP Semiconductors N.V. Definitive Proxy Statement Form DEF 14A — U.S. SEC, 2026-04-17 ↩↩↩↩↩↩↩

-

TSMC-backed Vanguard and NXP to build $7.8B wafer fab in Singapore — Reuters, 2024-06-05 ↩↩↩↩↩

-

Vanguard and NXP Jointly Invest $7.8 Billion in Singapore Semiconductor Plant — Bloomberg, 2024-06-05 ↩

-

Qualcomm terminates $44 billion NXP acquisition after Chinese regulatory delay — Wall Street Journal, 2018-07-25 ↩↩↩↩

-

Qualcomm to pay NXP $2 billion break fee, launches $30 billion share buyback — Reuters, 2018-07-26 ↩↩↩↩

-

NXP to buy Freescale for $11.8 billion to create automotive chip powerhouse — Reuters, 2015-03-02 ↩↩↩

-

The Great Semiconductor Consolidation Wave of 2015 — Financial Times, 2015-12-21 ↩

-

NXP CEO Kurt Sievers to retire; Rafael Sotomayor named successor — EE Times, 2025-04-22 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube