News Corp: The Empire Built on Ink and Pixels

I. Introduction & Episode Roadmap

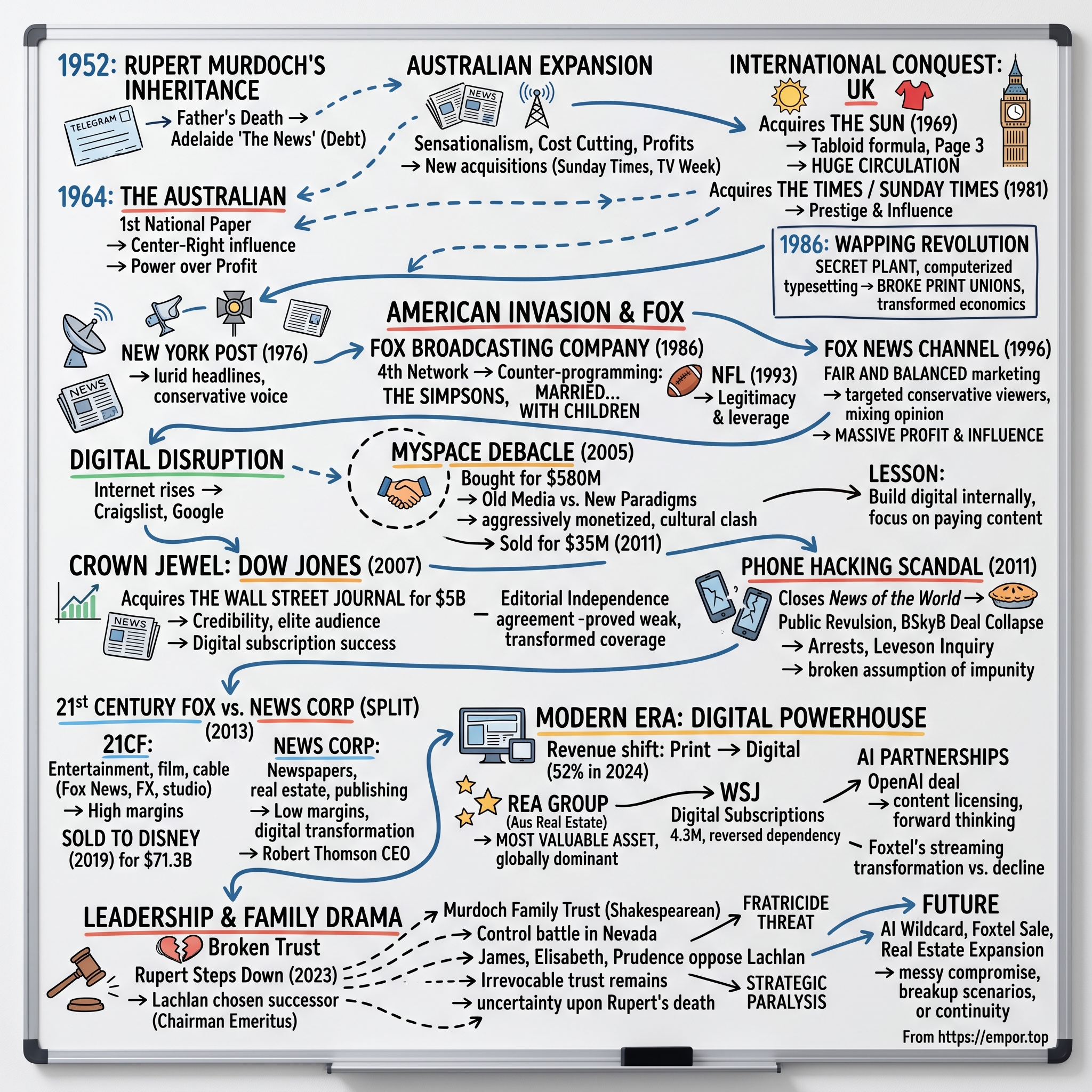

The year is 1952. A 21-year-old Oxford philosophy student receives a telegram that will redirect the course of media history: his father has died, leaving him a small Adelaide newspaper drowning in debt. Most would have sold it. Rupert Murdoch flew home to Australia and began building what would become the most controversial media empire of the modern era.

Today, News Corporation stands as a $10.09 billion colossus, its tentacles reaching from Australian real estate platforms to American cable news, from British tabloids to global book publishing. The company that Murdoch incorporated in 1980 has survived phone hacking scandals, MySpace's spectacular implosion, the digital decimation of print media, and family succession battles worthy of Shakespeare. Through it all, one question persists: How did a small Adelaide newspaper, The News, transform into one of the world's most influential—and polarizing—media conglomerates?

The answer lies not just in aggressive acquisitions or political maneuvering, though both played crucial roles. It's a story of understanding power—who has it, who wants it, and how information can be weaponized to obtain it. Murdoch didn't just report news; he manufactured influence, trading headlines for access, circulation for clout. His empire wasn't built on journalism's lofty ideals but on a grittier truth: people will pay for stories that confirm their beliefs, shock their sensibilities, or simply entertain them during their morning commute.

This journey takes us from Adelaide's quiet streets to London's Fleet Street revolution, from Fox's audacious challenge to American broadcasting giants to the digital disruption that nearly broke the empire. We'll explore how Murdoch turned tabloid sensationalism into a business model, transformed political coverage into a profit center, and navigated the treacherous transition from print to pixels—stumbling spectacularly with MySpace before finding redemption in digital subscriptions and real estate platforms.

The modern News Corp, split from its entertainment assets in 2013, generates approximately 52% of revenues from digital sources. Its crown jewel, The Wall Street Journal, competes with The New York Times for America's business elite. Its Australian real estate platform, REA Group, dominates down under. Yet the empire faces its greatest transition: the post-Murdoch era. With Rupert stepping down in September 2023 and family control battles playing out in Nevada courtrooms, the fundamental question becomes whether this media empire can survive without its emperor.

What follows is the definitive business story of News Corporation—a tale of ambition, scandal, reinvention, and the relentless pursuit of influence. It's about understanding not just what Murdoch built, but why it mattered, how it shaped modern media, and what happens when the architect finally steps away from his creation. This isn't just the story of a company; it's the story of how information became weaponized, democratized, and ultimately, digitized. And it all started with a young man, a telegram, and a newspaper nobody wanted.

II. The Murdoch Dynasty Origins

Keith Rupert Murdoch's story doesn't begin with him—it begins with his father, and understanding Sir Keith Murdoch is essential to understanding everything that followed. Picture Melbourne in 1915: a young journalist named Keith Murdoch visits Gallipoli, ostensibly to report on postal arrangements. What he witnesses—the catastrophic mismanagement of Australian and New Zealand forces—compels him to write a blistering letter to Australia's Prime Minister. That letter, smuggled past censors, helps end the disastrous campaign and transforms Keith from reporter to power broker. The lesson wasn't lost on his son: information, properly deployed, could topple generals and redirect nations.

When Rupert was born on March 11, 1931, Sir Keith had already parlayed his journalistic fame into newspaper ownership, controlling several regional papers including Adelaide's The News. The Murdoch household was one where dinner conversations revolved around circulation figures, political machinations, and the daily combat of newspaper competition. Young Rupert absorbed it all—the merger of journalism and influence, the careful cultivation of political relationships, the understanding that news wasn't just about informing but about shaping public opinion.

The defining moment came in 1952. Rupert, studying Philosophy, Politics and Economics at Oxford's Worcester College, seemed destined for an academic life. Then came the telegram: Sir Keith was dead at 66, leaving behind a modest newspaper empire and substantial death duties. The News, the Adelaide afternoon paper that would become Rupert's launching pad, was losing money. The family's advisers recommended selling. Rupert's mother, Dame Elisabeth, expected him to return briefly, settle affairs, then resume his Oxford life.

Instead, the 22-year-old Murdoch threw himself into The News with an intensity that shocked Adelaide's genteel newspaper establishment. He slashed costs ruthlessly—firing senior editors, cutting staff, redesigning the paper to emphasize crime, sex, and scandal. "I was a bit of a student rebel," he'd later recall, "and I wanted to do something different." Different meant sensational. A typical News headline from 1954: "Queen Eats a Rat." The story? Queen Elizabeth had dined at a restaurant that had once served rat meat during wartime. Technically true, utterly misleading, and circulation gold.

By 1954, Murdoch had turned The News profitable. But Adelaide was too small for his ambitions. He began what would become his signature move: leveraging success in one market to finance expansion into another. In 1956, he launched TV Week, riding Australia's television boom. In 1958, he bought his first expansion property, Perth's Sunday Times. Each acquisition followed the same playbook: cut costs, amp up sensationalism, use profits to fund the next target.

The masterstroke came in 1964 with the creation of The Australian, the country's first national newspaper. Here, Murdoch revealed his dual nature. While his tabloids trafficked in sensation, The Australian would be serious, center-right, and influential—Australia's answer to The Times of London. It lost money for years (some say decades), but Murdoch understood something his competitors didn't: The Australian wasn't about profit but power. It gave him a seat at the table with prime ministers and business titans. The tabloids made money; The Australian made Murdoch matter.

The Australian expansion years revealed Murdoch's emerging business philosophy. First, he understood that newspapers weren't just businesses but platforms for influence. Second, he recognized that different audiences wanted different products—highbrow broadsheets for elites, lowbrow tabloids for masses, but all sharing a conservative, populist bent. Third, and most importantly, he grasped that local market dominance could be leveraged into national, then international, expansion.

By 1968, News Limited controlled significant newspaper assets across Australia. The Adelaide newspaper boy had become a media magnate. But Australia, with its 12 million people, could only contain Murdoch's ambitions for so long. He began looking abroad, first to London, where Fleet Street's newspaper wars offered exactly the kind of brutal competition he relished. The boy from Adelaide was ready to take on the British establishment. What happened next would transform not just Murdoch's fortunes, but the entire model of newspaper publishing. The empire was about to go global.

III. Going International: UK Conquest

Fleet Street in 1969 was a fortress of tradition, controlled by powerful unions, hidebound by centuries-old practices, and ripe for disruption. When the 38-year-old Australian Rupert Murdoch arrived to bid for The Sun, a failing broadsheet owned by the International Publishing Corporation, the British newspaper establishment barely noticed. "Colonial," one Fleet Street editor supposedly sniffed. They'd learn soon enough that the colonial had come not to join their club, but to burn it down and rebuild it in his image.

The Sun that Murdoch acquired for £800,000 was hemorrhaging 70,000 pounds annually, its circulation below 850,000. Within a year, he'd transformed it into Britain's most controversial—and profitable—newspaper. The formula was pure Murdoch: shrink the broadsheet to tabloid size, slash the price to undercut rivals, and serve up a daily diet of sex, scandal, and sport. The coup de grâce came in 1970 with the introduction of Page 3 girls—topless models that became The Sun's signature feature. Feminists protested, intellectuals sneered, and circulation soared past 2 million.

But The Sun was more than just flesh and sensationalism. Murdoch understood British working-class culture with an outsider's clarity. While The Times and Guardian spoke to Oxbridge elites, The Sun spoke to factory workers, taxi drivers, and housewives in language they used and about topics they cared about. Its politics were populist-conservative, anti-establishment, and increasingly influential. The headline "GOTCHA!" celebrating the sinking of Argentina's Belgrano during the Falklands War captured both The Sun's jingoistic appeal and its political power.

The News of the World, which Murdoch had actually acquired just before The Sun in 1969 for £34 million in a dramatic takeover battle with Robert Maxwell, became The Sun's Sunday companion. Already Britain's highest-circulation newspaper at 6 million copies, the News of the World under Murdoch pushed even further into scandal and exposé. Its formula—sex scandals involving celebrities, politicians, or ideally both—would prove devastatingly effective for four decades before ultimately destroying the paper.

Yet Murdoch craved respectability alongside his tabloid profits. In 1981, he made his boldest UK move, acquiring The Times and The Sunday Times from the Thomson Organization. The Times, founded in 1785, was Britain's newspaper of record, read by prime ministers and powerbrokers. The Sunday Times was the country's most prestigious Sunday paper. Both were losing money, crippled by union disputes and antiquated production methods. The acquisition, controversial from the start, required government approval and promises about editorial independence that would haunt Murdoch for decades.

The Wapping Revolution of 1986 was Murdoch's British apotheosis. For over a century, Fleet Street's print unions had controlled newspaper production, demanding massive workforces, resisting new technology, and regularly shutting down papers with strikes. Murdoch spent years secretly building a modern printing plant in Wapping, East London, equipped with computerized typesetting that could operate with a fraction of the traditional workforce. On January 24, 1986, he moved all four newspapers overnight, leaving 6,000 print workers behind.

What followed was one of the most bitter industrial disputes in British history. Mass pickets, violent confrontations, 1,262 arrests. The print workers called it betrayal; Murdoch called it modernization. He kept publishing using non-union labor, bused through picket lines in vehicles with blacked-out windows. After a year, the unions surrendered. The victory didn't just transform News International's profitability—it broke the power of Fleet Street unions permanently. Within years, every major newspaper had fled Fleet Street for modern facilities. Murdoch had revolutionized British newspaper economics.

The political influence that flowed from this newspaper dominance was unprecedented. The Sun's endorsement became electoral gold—or poison. "It's The Sun Wot Won It," the paper bragged after John Major's surprise 1992 victory. When The Sun switched from Conservative to Labour in 1997, backing Tony Blair, it marked a seismic political shift. Blair, like many British politicians, learned that crossing Murdoch meant facing the wrath of newspapers read by millions of voters. The relationship was symbiotic: politicians got favorable coverage, Murdoch got access and influence over policy.

By the late 1980s, Murdoch's British newspapers weren't just profitable; they were a power base that stretched from Downing Street to Brussels. The Sun's relentless Euroscepticism helped shape British attitudes toward European integration. The Times gave Murdoch a voice among elites. Together, they made him perhaps the most powerful unelected figure in British public life.

But Britain, like Australia before it, was ultimately too small for Murdoch's ambitions. Even as he consolidated his UK empire, his eyes had turned west, to the United States, where three television networks dominated the airwaves and no one had successfully challenged them in decades. The lessons learned in Britain—that content could drive politics, that modernization could shatter old monopolies, that controversy meant circulation—would all apply. But America would require something more: Murdoch would have to become American himself. The colonial was about to attempt his greatest conquest.

IV. American Invasion & Building Fox

The San Antonio Express-News newsroom in 1973 had never seen anything like it. Their new owner, fresh from his British tabloid wars, stalked through the building rearranging furniture, literally tearing up page layouts, and barking orders in an Australian accent. "Too gray!" Murdoch shouted at the front page. "Where's the blood?" When a reporter protested that San Antonio wasn't a tabloid town, Murdoch replied: "Every town is a tabloid town. They just don't know it yet." Within months, circulation was up 10%. America was about to learn what Britain already knew: Murdoch played by different rules.

The San Antonio purchases—the Express and News for $19.7 million—were just Murdoch's American beachhead. His real target was New York, the media capital where reputations and empires were made. In 1976, he struck, acquiring the New York Post from Dorothy Schiff for $31 million. The Post, Alexander Hamilton's creation and once New York's most prestigious newspaper, had declined into a money-losing liberal broadsheet. Murdoch transformed it overnight into a screaming conservative tabloid. "HEADLESS BODY IN TOPLESS BAR" became the archetypal Post headline—lurid, memorable, and impossible to ignore.

But newspapers were yesterday's war. Murdoch understood that American media power centered on television, where three networks—ABC, CBS, and NBC—had operated an oligopoly since the 1950s. Breaking in seemed impossible; the last attempt, the DuMont Network, had collapsed in 1956. The networks controlled the affiliates, the programming, the advertisers. It was a closed system—until Murdoch found the crack.

In 1985, two opportunities converged. Twentieth Century-Fox, the legendary Hollywood studio, was for sale. Separately, John Kluge was selling his Metromedia chain of independent television stations in major markets. Murdoch saw what others missed: combine a studio with stations in New York, Los Angeles, Chicago, and other major markets, and you had the skeleton of a fourth network. The prices were staggering—$575 million for Fox, $2 billion for Metromedia—and required Murdoch to become an American citizen (foreign ownership rules limited TV station ownership). On September 3, 1985, at the federal courthouse in lower Manhattan, the Australian became an American.

The Fox Broadcasting Company launched October 9, 1986, with a single show: "The Late Show Starring Joan Rivers." Rivers bombed, lasting just six months. Critics called Fox "the coat-hanger network," predicting swift collapse. They underestimated Murdoch's strategy: he wasn't trying to beat the Big Three at their own game. Instead, Fox would counter-program, seeking audiences the networks ignored or underserved.

The breakthrough came with "The Simpsons" in 1989. Here was a show the networks would never air—animated, irreverent, satirical. It became a cultural phenomenon, proving Fox could create distinctive content. "Married... with Children" had already shown Fox would embrace what networks considered too risqué. Then came the masterstroke: NFL football. In 1993, Fox shocked the sports world by bidding $1.58 billion for NFC rights, 49% above CBS's offer. "They're crazy," CBS executives said. But Murdoch understood: sports brought male viewers, legitimacy, and leverage with affiliates. Overnight, Fox became a major network.

The programming philosophy was pure Murdoch—give audiences what they want, not what elites think they should watch. While networks chased upscale demographics with prestige dramas, Fox built its audience with reality TV ("COPS," "America's Most Wanted"), edgy comedies, and increasingly, conservative-leaning news programming. The formula worked: by 1995, Fox was profitable, reaching 95% of American households.

But Murdoch's American ambitions extended beyond entertainment. He saw how CNN had proven cable news could be profitable and influential. More importantly, he saw an opening: CNN and the broadcast networks all tilted liberal, or at least pursued traditional journalistic objectivity. What if a news channel explicitly targeted conservative viewers, mixing news with opinion, embracing rather than hiding its political perspective?

Fox News Channel launched October 7, 1996, with the tagline "Fair and Balanced"—a brilliant piece of marketing that simultaneously claimed objectivity while signaling to conservatives that this was their network. The initial audience was tiny, but Murdoch had learned patience from The Australian. He poured money into Fox News, hiring Roger Ailes from CNBC to run it, paying cable operators to carry it (reversing the traditional model), and gradually building an audience of viewers who felt marginalized by mainstream media.

The transformation was gradual, then sudden. By 2002, Fox News had passed CNN in ratings. By 2010, it was the most-watched cable news network by far, its prime-time hosts like Bill O'Reilly and later Tucker Carlson becoming conservative celebrities. The network didn't just report to conservatives; it shaped conservatism itself, its talking points becoming Republican orthodoxy, its endorsements moving markets and elections.

The financial success was staggering. Fox News generated over $1 billion in annual profit, with operating margins above 50%. But the influence was worth more than money. Fox News gave Murdoch something his newspapers never could: daily, direct access to millions of American homes, delivering not just news but worldview. Presidents called him. Senators courted him. The boy from Adelaide had become arguably the most powerful media figure in American history.

Yet even as Fox conquered American television, the internet was rising. A new generation of tech companies—Google, Facebook, and particularly a site called MySpace—threatened to disrupt traditional media just as Murdoch had once disrupted newspapers. The empire builder would have to evolve again, this time into the digital realm. What happened next would be his most expensive mistake.

V. The Digital Disruption & MySpace Debacle

Tom Anderson's smiling face—that ubiquitous default friend on every MySpace profile—seemed to mock Murdoch from every computer screen in 2005. Here was the future of media: social, interactive, user-generated. Here was the platform that had dethroned Friendster, was growing faster than Google had, and captured the coveted youth demographic that Fox Broadcasting desperately wanted. When Murdoch paid $580 million for MySpace in July 2005, he declared it "a place for personal expression." Wall Street loved it. "Murdoch Gets It!" proclaimed headlines. Six years later, he'd sell the wreckage for $35 million, calling it a "huge mistake." The story of how the empire builder got digitally destroyed is a masterclass in old media misunderstanding new paradigms.

The anxiety was palpable in News Corporation's executive suites by 2004. Google had gone public, its market cap soaring past traditional media companies. Craigslist was gutting classified advertising, newspapers' most profitable segment. Young people weren't watching TV or reading papers; they were living online. Murdoch, then 74, responded with characteristic aggression. If he couldn't build the future, he'd buy it. "We must be digital natives," he told investors, though the phrase sounded foreign in his Australian accent.

MySpace looked perfect. Founded in 2003 by Tom Anderson and Chris DeWolfe, it had rocketed to 25 million users by 2005. Musicians used it to share tracks, teenagers to express themselves, twentysomethings to connect. It was messy, customizable, and anarchic—everything Facebook, then limited to college students, wasn't. When Murdoch's team visited MySpace's Santa Monica offices, they saw the future: young employees, band posters, energy. The $580 million price seemed reasonable, even cheap if this was indeed the next generation of media.

The problems started immediately. Murdoch's first instinct was to monetize aggressively. News Corp executives pushed for more ads, faster revenue growth, integration with Fox properties. MySpace pages became cluttered with banners, pop-ups, and video ads. The site, already notorious for slow loading times due to customizable HTML profiles, became nearly unusable. Users complained that it felt like Times Square—garish, commercial, overwhelming.

Meanwhile, Facebook was executing the opposite strategy. Mark Zuckerberg, who'd studied MySpace's mistakes obsessively, kept Facebook clean, fast, and ad-light. When Facebook opened to everyone in September 2006, it offered what MySpace had abandoned: simplicity. The exodus began slowly, then became a flood. By 2008, Facebook had passed MySpace in global users. By 2009, in the U.S. too.

But the real disaster was cultural. News Corp executives, accustomed to controlling content, couldn't grasp user-generated platforms. They worried about inappropriate content, music piracy, predators—all legitimate concerns, but their responses strangled the platform's freewheeling culture that users loved. When they tried to make MySpace "safer," they made it boring. When they tried to make it profitable, they made it unbearable.

The MySpace Music joint venture of 2008, partnering with major labels, exemplified the confusion. Old media partnering with old media to compete with iTunes and emerging streaming services—it satisfied no one. Musicians decamped to Facebook and Twitter. Fans followed. MySpace became a ghost town of abandoned profiles and broken embedded videos.

Murdoch's attempts to fix MySpace revealed his fundamental misunderstanding. He replaced CEOs—DeWolfe out, former Facebook COO Owen Van Natta in, then him out too. He hired hundreds of engineers, marketers, and product managers. He spent hundreds of millions on infrastructure and marketing. But he was fighting the last war, trying to run a social network like a television network, with programming schedules and content control.

The numbers were brutal. From a peak of 75.9 million unique U.S. visitors in December 2008, MySpace collapsed to 34.8 million by March 2011. Advertising revenue evaporated. Losses mounted—estimated at $1.5 billion total including acquisition price and subsequent investments. In June 2011, News Corp sold MySpace to Specific Media and Justin Timberlake for $35 million, a 94% loss. Murdoch called it sobering: "We learned a lot of valuable, expensive lessons."

The lessons were indeed valuable. First, platforms and content were fundamentally different businesses. News Corp knew how to create and distribute content; it didn't understand providing infrastructure for others' content. Second, digital native companies had different DNA—engineering-driven, iterative, willing to sacrifice short-term revenue for long-term growth. News Corp's quarterly earnings pressure and traditional media mindset proved fatal. Third, and most importantly, in digital markets, network effects meant winner-take-all dynamics. Being second meant being nobody.

But failure taught Murdoch something crucial: digital transformation couldn't be bought; it had to be built internally. The empire's future digital strategy would focus on transforming existing properties—making newspapers digital-first, building paywalls, creating streaming services. Instead of acquiring platforms, News Corp would focus on what it knew: creating content people would pay for. The MySpace debacle had been expensive tuition, but the education would prove invaluable. The empire would go digital, just differently than anyone expected.

VI. The Crown Jewel: Dow Jones Acquisition

The Bancroft family gathering at Boston's Ritz-Carlton in April 2007 had the tension of a funeral and the stakes of a coronation. For 105 years, their family had controlled Dow Jones & Company, publisher of The Wall Street Journal, America's most prestigious business newspaper. Now Rupert Murdoch wanted it, offering $60 per share—a 67% premium—for their inheritance. Elisabeth Goth Chelberg, a Bancroft heir, spoke for many: "Murdoch will destroy The Journal's integrity." But Christopher Bancroft, seeing the $5 billion offer, had a different view: "At least we'll be rich when he does." The battle for Dow Jones would test whether journalistic independence could survive capitalism's logic.

Murdoch had coveted The Wall Street Journal for decades. Unlike his tabloids, The Journal represented unassailable credibility. Its readers were CEOs, investment bankers, and policy makers—the American elite Murdoch had spent forty years trying to influence. The Journal was profitable, prestigious, and powerful. It was everything The New York Times was, but with a conservative editorial page that aligned with Murdoch's worldview. If The Times was America's liberal conscience, The Journal was its capitalist brain.

The initial approach in 2006 had been rebuffed. But by spring 2007, with newspaper stocks cratering and digital disruption accelerating, Murdoch sensed opportunity. His April 2007 offer—$5 billion for a company trading at $36—was deliberately generous. He knew the Bancrofts, controlling 64% of voting shares through super-voting stock, held the keys. Money alone wouldn't work; he needed to address their fears about editorial independence.

The Bancroft resistance was fierce but fractured. Some family members, particularly those descended from Jessie Bancroft Cox, saw themselves as stewards of journalistic integrity. Others, especially younger generations who'd never worked at Dow Jones, saw a financial windfall. The family hired advisers, explored alternatives, and agonized. Michael Elefante, the family's trustee, became the key figure, shuttling between camps, trying to find consensus among 35 adult Bancrofts.

Murdoch played masterfully. He made concessions that seemed unprecedented: an independent editorial board to protect The Journal's newsroom, promises not to merge it with Fox Business, guarantees of editorial independence. He met personally with Bancroft members, deploying charm rather than confrontation. "I'm 76 years old," he told them. "This is about legacy, not profit." Some believed him. Others saw performance.

The public drama intensified everything. Journal reporters, watching their fate decided in Boston hotels, published increasingly desperate editorials defending independence. The Times gleefully covered every Bancroft squabble. Wall Street watched, bemused, as a family that hadn't run the company in decades agonized over its future. Share prices rose toward Murdoch's offer, making rejection financially painful.

The turning point came in July 2007. Three Bancroft family members—Leslie Hill, her brother Christopher, and their cousin Michael Elefante—agreed to meet with Murdoch. The meeting, intended to last an hour, stretched to three. Murdoch was deferential, respectful, talking about The Journal's history and importance. He agreed to an unprecedented editorial agreement: a five-person board, independent of News Corp, would have to approve any editor changes. It was more autonomy than he'd granted any property.

On August 1, 2007, the Bancroft family voted. The result: approval by holders of 37% of Dow Jones's overall shares, just enough when combined with other shareholders to reach the 50% threshold. The deal closed December 13, 2007, for $5.6 billion including debt. Murdoch finally owned his crown jewel. The Journal's staff wore black to work. The New York Times ran an obituary for independent journalism.

What followed confounded critics and vindicated skeptics simultaneously. Murdoch did invest heavily in The Journal—expanding coverage, hiring reporters, launching a New York edition to compete with The Times. The paper remained profitable and prestigious. But he also transformed it, exactly as the Bancrofts had feared. Business coverage shrank by a third as general news expanded. Political coverage tilted rightward. The editorial page became more stridently conservative. Investigations into News Corp allies disappeared.

The editorial independence agreement proved toothless. When Murdoch wanted to replace editor Marcus Brauchli in 2008, the independent board approved it. When he appointed Gerard Baker, who transformed news coverage to be more conservative-friendly, the board acquiesced. The agreement protected the forms of independence while the substance eroded. Journal veterans spoke of self-censorship, of knowing what stories wouldn't run, of gradual but unmistakable change.

Yet financially and competitively, the acquisition succeeded brilliantly. The Journal's digital subscriptions soared, reaching 2.2 million by 2019. Its paywall, launched before the acquisition but expanded under Murdoch, became the industry model. Integration with Dow Jones's other properties—Barron's, MarketWatch—created a financial news powerhouse. The Journal became News Corp's most valuable asset, generating hundreds of millions in annual profit.

The acquisition's real significance transcended one newspaper. Murdoch had proven that premium content, properly packaged and marketed, could thrive digitally. While his MySpace acquisition showed he couldn't build platforms, Dow Jones demonstrated he could modernize traditional media. The Journal's success would become the template for News Corp's digital transformation: paywalls, subscriptions, and leveraging brand prestige. The crown jewel hadn't just decorated the empire; it had shown the empire how to survive the digital age.

VII. The Phone Hacking Scandal & Fallout

The video is seared into British memory: Rupert and James Murdoch, father and son, walking into Parliament's Portcullis House on July 19, 2011, surrounded by cameras and protesters. Someone throws a foam pie at Rupert; his wife Wendi leaps up, slapping the attacker. It was absurdist theater masking genuine tragedy. Days earlier, Murdoch had shut down the 168-year-old News of the World, Britain's biggest newspaper. Thousands of jobs vanished overnight. An empire built on exposing others' secrets was being destroyed by its own. The phone hacking scandal didn't just threaten News Corp's reputation—it challenged the entire Murdoch mythology of invincibility.

The scandal's roots stretched back to 2005, when News of the World's royal editor Clive Goodman was caught hacking Prince William's voicemails. News International, Murdoch's UK subsidiary, insisted it was a "rogue reporter." They paid settlements, Goodman went to prison, and the story seemed contained. But Guardian journalist Nick Davies kept investigating, uncovering a pattern: hundreds of celebrities, politicians, and crime victims had their phones hacked. News International had paid millions in secret settlements, buying silence with shareholders' money.

The turning point came July 4, 2011. The Guardian revealed that News of the World had hacked the voicemail of Milly Dowler, a 13-year-old murder victim, while she was still missing. Reporters had deleted messages to free space for new ones, giving her parents false hope she was alive. Britain exploded in revulsion. Advertisers fled. Politicians who'd courted Murdoch for decades discovered moral outrage. Prime Minister David Cameron, whose former communications director Andy Coulson had edited News of the World during the hacking years, called it "absolutely disgusting."

Murdoch's response was unprecedented and desperate. On July 7, he announced News of the World would close after its July 10 edition. The final headline: "THANK YOU & GOODBYE." Two million copies sold—profits went to charity. But shutting Britain's best-selling newspaper couldn't contain the damage. Parliament launched inquiries. Police arrested senior executives. The Leveson Inquiry into press standards became a tribunal on Murdoch's entire UK operation.

The business implications cascaded immediately. News Corp had been pursuing its biggest deal ever: acquiring the 61% of British Sky Broadcasting it didn't own for £7.8 billion. BSkyB would have given Murdoch control of Britain's dominant satellite broadcaster, combining content creation with distribution. The deal had been progressing despite opposition. Now it was politically radioactive. On July 13, 2011, News Corp withdrew its bid. Billions in potential value evaporated.

The scandal revealed the dark mechanics of Murdoch's influence machine. The Leveson Inquiry exposed intimate dinners between News International executives and politicians, texts between Murdoch's lobbyists and Cameron's office, and a revolving door between government and News Corp. Rebekah Brooks, News International's chief executive and Murdoch's protégé, was arrested. She'd been texting Cameron about horse rides while her newspapers were being investigated. The coziness was nauseating.

For Murdoch personally, the Parliamentary testimony was humiliating. The 80-year-old mogul, who'd spent six decades never apologizing, called it "the most humble day of my life." He denied knowledge of widespread hacking, blamed subordinates, and insisted he'd been betrayed. Few believed him. His son James, being groomed as successor, gave lawyerly answers that satisfied no one. The appearance of dynastic rot was unmistakable.

The legal aftermath stretched for years. Brooks was acquitted in 2014, though Coulson was convicted. News Corp paid hundreds of millions in settlements—over £600 million by some estimates. But the reputational damage was incalculable. In America, the FBI investigated whether 9/11 victims' phones were hacked (they weren't). The Foreign Corrupt Practices Act implications threatened the entire company. Institutional shareholders revolted, nearly voting Murdoch out as chairman in 2011 and 2012.

Internally, the scandal triggered revolution. News Corp implemented rigorous compliance systems, ethics training, and oversight mechanisms—the infrastructure of corporate governance Murdoch had resisted for decades. The cowboy culture that had built the empire was forcibly domesticated. Old hands complained News Corp had lost its edge, become just another corporate bureaucracy. They were right. The scandal had broken something essential: the assumption of impunity.

The strategic consequences reshaped News Corp permanently. The BSkyB deal's collapse meant Murdoch would never achieve his British vertical integration dream. The Leveson Inquiry's recommendations led to press regulations Murdoch had spent decades preventing. Most significantly, the scandal accelerated the empire's split. Shareholders wanted distance between entertainment assets and toxic publishing. In 2013, News Corp divided into two companies, acknowledging what the scandal had proven: Murdoch's newspapers had become liabilities, not assets.

Yet Murdoch survived, as he always did. The Sun continued publishing. The Times maintained influence. Fox News was untouched. The stock recovered. By 2015, with memories fading and politicians needing his papers' support, Murdoch was back at Downing Street dinners. The empire had been bloodied but not broken. Still, something had changed. The phone hacking scandal marked the end of peak Murdoch—the moment when the emperor's clothes became visible, when the cost of his methods finally came due. The empire would continue, but the age of impunity was over.

VIII. The Great Split: Publishing vs. Entertainment

The PowerPoint slide on June 28, 2012, was deceptively simple: one company becoming two. News Corporation, the $33 billion conglomerate Murdoch had assembled over six decades, would split. On the left: 21st Century Fox, containing television, film, and cable assets. On the right: the "new" News Corporation, holding newspapers, publishing, and digital properties. Chase Carey, the mustached satellite TV pioneer who'd become Murdoch's operational maestro, called it "unlocking value." Murdoch preferred grander language: "unleashing the true potential of our creative enterprises." In reality, it was triage—separating the growing from the dying, the profitable from the problematic, the future from the past.

The pressure had been building for years. Fund manager activism was rising, and News Corp presented an obvious target. Why should Fox's 30% operating margins subsidize newspapers' single digits? Why should Fox shareholders bear litigation risk from phone hacking? The entertainment assets generated 75% of profits but traded at publishing multiples. The "Murdoch discount"—the reduced valuation due to corporate complexity and governance concerns—was estimated at 20-30%. Something had to give.

The boardroom dynamics were fascinating. Murdoch initially resisted, seeing the company as his life's work, indivisible. But James, then deputy COO and heir apparent, pushed for separation. He ran the entertainment side and was tired of newspaper scandals damaging his division. Lachlan, the older son who'd returned after years of Australian exile, would ultimately benefit most from the split. Daughter Elisabeth stayed neutral, focused on her independent production company. The family was dividing the empire before formally dividing it.

The mechanics were complex but revealing. Shareholders would receive one share of new News Corp for every four shares of old News Corp. The Murdoch family's voting control—maintained through super-voting shares—would continue in both companies. This wasn't democratization but reorganization. The entertainment company would keep the Fox name and most assets: the Fox broadcast network, cable channels including Fox News and FX, and the 20th Century Fox studio. Publishing got newspapers, HarperCollins, and critically, the Australian real estate websites and Dow Jones.

Wall Street's reaction was euphoric. The announcement drove shares up 10%. Finally, analysts could value Fox's entertainment assets properly, without newspaper drag. The split would "unlock $4-8 billion in value," Goldman Sachs estimated. Fox could pursue acquisitions without publishing baggage. News Corp could transform digitally without quarterly earnings pressure from entertainment investors. Everyone won—except those who believed in media convergence.

The June 28, 2013, split completion felt anticlimactic after a year of preparation. Employees showed up to the same offices, doing the same jobs, just for different corporate entities. But the strategic implications were profound. Fox, freed from publishing's problems, went acquisition hunting. The attempted Time Warner hostile takeover in 2014 ($80 billion bid, rejected) wouldn't have been possible pre-split. The Sky consolidation attempts accelerated. Fox became a pure entertainment play.

New News Corp faced a different reality. Revenue was $8.6 billion, but growth was challenging. Print advertising continued declining. The phone hacking settlements continued draining cash. But the portfolio wasn't entirely distressed. The Wall Street Journal remained profitable and prestigious. REA Group, the Australian real estate platform, was growing 20% annually. HarperCollins had backlist value. The strategy became clear: milk print profits while investing in digital transformation, use cash flow to buy growth, and hope digital subscriptions could replace advertising.

The cultural differences between the two companies emerged immediately. Fox maintained the swaggering Murdoch style—aggressive, political, confrontational. News Corp became more corporate, appointing Robert Thomson, a former Wall Street Journal editor, as CEO. Thomson was Murdoch-trained but smoother, more comfortable with digital evangelism than tabloid sensationalism. The companies' headquarters—Fox staying in Manhattan, News Corp moving to lower floors—symbolized the hierarchy.

Yet the split created unexpected problems. The synergies Murdoch had preached for decades—newspapers promoting shows, entertainment driving readership—vanished. Fox News and The Wall Street Journal, natural partners, became corporate strangers. Cross-promotion disappeared. More critically, the split coincided with accelerating cord-cutting. Fox's cable networks, profit engines for decades, faced secular decline. The entertainment assets Murdoch kept weren't as future-proof as believed.

By 2017, the logic reversed. Disney approached Fox about acquiring its entertainment assets. Murdoch, now 86, was ready to sell. Comcast entered a bidding war. The final price: $71.3 billion to Disney in 2019. The entertainment empire Murdoch had spent forty years building was sold. What remained was what he'd started with: newspapers, now digital, still losing money, still influential. The split that was supposed to unlock value had instead revealed a truth: the empire's parts were worth more than its whole.

The irony was exquisite. After everything—the acquisitions, scandals, transformations—Murdoch was back where he started, with publishing assets nobody else wanted. Except now they included digital real estate platforms, streaming services, and paywalled newspapers. The "new" News Corp wasn't his beginning but his ending, the empire distilled to its essence: information, influence, and the endless fight for relevance. The boy from Adelaide had come full circle.

IX. Modern Era: Digital Transformation

Robert Thomson's morning routine at News Corp headquarters begins at 5:30 AM with five screens: real-time subscriber data from The Wall Street Journal, user engagement metrics from Realtor.com, streaming numbers from Australia's Foxtel, book sales from HarperCollins, and the UK Sun's digital traffic. The Australian former Financial Times editor, who became CEO in 2013, doesn't look like a Murdoch lieutenant—he's soft-spoken, quotes poetry, and uses words like "algorithmic kleptocracy" to describe Google. But his mission is pure Murdoch: transform a print empire into a digital powerhouse before the money runs out. By 2024, he could claim victory: digital now generates 52% of News Corp's $10 billion revenue. The transformation wasn't smooth, but it worked.

The numbers tell the story. In fiscal 2024's fourth quarter alone, News Corp generated $2.58 billion in revenue, with digital real estate and subscriptions driving growth. The Wall Street Journal hit 4.3 million digital subscribers. REA Group, the Australian property platform, posted 37% revenue growth. Foxtel's streaming services—Kayo for sports, BINGE for entertainment—reached 3.2 million subscribers. Even The Sun, that tabloid dinosaur, had 400,000 digital subscribers. The company Murdoch split off as the "bad bank" had become surprisingly good.

REA Group emerged as the unexpected star. What started as a $44 million acquisition in 2001 became News Corp's most valuable asset, worth over $15 billion by 2024. The model was simple but powerful: dominate Australian real estate listings, charge agents for premium placement, expand internationally. REA's realestate.com.au commanded 70% market share in Australia. Its PropertyGuru subsidiary dominated Southeast Asia. The proposed $7.4 billion acquisition of Britain's Rightmove, though rejected in 2024, showed Thomson's ambition: build a global real estate platform rivaling any tech company.

The Wall Street Journal's transformation was equally dramatic but more complex. The paywall, launched in 1996 and mocked as suicide, became the template for newspaper survival. But Thomson pushed beyond simple subscriptions. The Journal created tiers—basic, professional, enterprise—with prices ranging from $38.99 monthly to thousands for corporate packages. Bundle deals with Barron's and MarketWatch. Student discounts. Corporate partnerships. The paper wasn't just selling news but intelligence, charging hedge funds $10,000 annually for real-time analysis. By 2024, circulation revenue exceeded advertising 3-to-1, reversing newspapers' historic dependency.

The technological transformation went deeper than paywalls. News Corp spent hundreds of millions on data analytics, artificial intelligence, and personalization engines. The Journal's recommendation algorithm analyzed reading patterns, suggesting stories to keep subscribers engaged. HarperCollins used predictive analytics to forecast bestsellers. REA deployed machine learning for property valuations. This wasn't your father's newspaper company; it was a data company that happened to publish news.

The landmark OpenAI partnership announced in May 2024 signaled Thomson's forward thinking. For five years, News Corp content would train AI models, with OpenAI paying tens of millions annually. Critics saw Faustian bargain—feeding the technology that could destroy journalism. Thomson saw opportunity: get paid for content tech companies had been stealing, influence AI development, and position News Corp for whatever came next. "We can either be roadkill or partners," he told investors.

Foxtel's streaming transformation showcased both success and limits. The Australian cable monopoly faced the same cord-cutting plaguing American providers. Thomson's response: unbundle cable into streaming services. Kayo for sports fanatics. BINGE for prestige drama. Flash for news junkies. The strategy worked—streaming subscribers grew 20% annually—but margins compressed. Netflix and Disney+ were formidable competitors. In 2024, News Corp explored "strategic options" for Foxtel, corporate speak for "please buy this before it dies."

The transformation wasn't without casualties. Print advertising revenue continued its terminal decline, falling 7% annually. Regional newspapers were shuttered or sold. Journalists were replaced by algorithms for basic financial reporting. The New York Post, despite digital growth, remained marginally profitable. News UK's papers struggled with Britain's hyper-competitive digital market. For every REA success, there was a MySpace memory.

The cultural transformation proved hardest. News Corp's newsrooms, built on scoops and sensationalism, had to embrace metrics and membership. Journalists who'd spent careers crafting headlines now studied engagement dashboards. Editors optimized for Google's algorithm rather than reader impact. The tabloid energy that built Murdoch's empire felt incompatible with subscription retention strategies. "We're becoming a utility company," one veteran complained. "Where's the fun in that?"

Yet the financial results vindicated Thomson's strategy. News Corp's stock rose 40% from 2020 to 2024, outperforming most traditional media. Operating income exceeded $1 billion annually. The company generated enough cash to pay dividends, buy back shares, and invest in growth. The "dying" newspaper company was very much alive, just different. The transformation wasn't complete—print still mattered, advertising still contributed, challenges remained—but News Corp had achieved what most legacy media couldn't: relevance in the digital age.

The question was sustainability. Digital subscriptions faced saturation—how many paywalls would consumers accept? Real estate platforms faced competition from tech giants. AI threatened to disintermediate publishers entirely. Thomson's transformation had bought time, not immortality. But for a company many had written off, survival itself was victory. The empire hadn't just adapted to digital disruption; it had thrived through it.

X. Leadership Transition & Family Drama

The photograph from September 21, 2023, captured a moment six decades in the making: Rupert Murdoch, 92, handing a ceremonial gavel to his son Lachlan at News Corp's annual meeting. The smile seemed forced, the gesture theatrical. After running the media empire since 1952, the patriarch was finally stepping aside—sort of. He would become Chairman Emeritus, keeping an office, attending board meetings, and calling daily with "suggestions." As succession plans go, this was less passing the torch than gripping it with both hands while letting someone else hold the handle. But the real drama wasn't in the boardroom—it was in a Reno courthouse where the family's future was being decided.

The Murdoch children had been auditioning for succession their entire lives. Lachlan, the chosen one, had fled to Australia in 2005 after corporate battles, only to return triumphant. James, the insurgent, had run Asian operations, British newspapers, and Fox entertainment before resigning in 2020 over "editorial disagreements"—code for opposing Fox News's political direction. Elisabeth, the only daughter in the trust, had built her own production company, selling it to Murdoch for $673 million before maintaining studied independence. Prudence, from Murdoch's first marriage, held trust votes but stayed away from operations. The family wasn't just divided by business philosophy but by fundamental worldview.

The trust structure was Shakespearean in complexity. The Murdoch Family Trust controlled 38.4% of News Corp voting shares through dual-class stock. Upon Rupert's death, control would pass equally to his four oldest children. This meant Lachlan, despite being chosen successor, could be outvoted 3-to-1 by siblings who opposed Fox News's conservative tilt. The arrangement, created during Murdoch's second divorce, was designed to prevent any one child from dominating. It had become a ticking time bomb.

In December 2023, the bomb exploded—quietly, in Nevada's secretive probate court. Rupert had petitioned to change the irrevocable trust, concentrating control with Lachlan. The legal argument was novel: maintaining Fox News's conservative editorial direction was financially essential, and only Lachlan would preserve it. James, Elisabeth, and Prudence united in opposition, hiring power lawyers, arguing their father was mentally diminished, and being manipulated by Lachlan. The trial, closed to media despite the irony, became a proxy war for the empire's soul.

The Nevada ruling in December 2024 was devastating for Rupert and Lachlan. Commissioner Edmund J. Gorman Jr. found the attempt to change the trust was pursued in "bad faith," driven by personal rather than financial motives. The opinion, though sealed, reportedly excoriated the plan as a "carefully crafted charade" designed to permanently entrench Lachlan's control. The irrevocable trust would remain irrevocable. Upon Rupert's death, the progressive children could theoretically unite to transform Fox News, sell assets, or dismantle the empire entirely.

James's July 2020 resignation letter had been the clearest signal of fraternal tensions. He cited "disagreements over certain editorial content published by the Company's news outlets and certain other strategic decisions." Translation: he opposed Fox News's Trump coverage, election denialism, and COVID misinformation. His wife Kathryn had tweeted criticism of Fox's climate coverage. James had donated to Biden, funded progressive causes, and publicly repudiated his family's media properties. If he gained control, Fox News as conservatives knew it would end.

Elisabeth remained enigmatic, avoiding public statements but privately allied with James against Lachlan. Her production company, Sister, created progressive-leaning content. She lived in London, far from family drama but close enough to engage when needed. Prudence, the eldest, had the least involvement but held crucial votes. Together, the three siblings represented not just majority control but repudiation of their father's legacy. The empire builder faced his worst nightmare: his children undoing his life's work.

Lachlan's position as sole chairman and CEO looked strong on paper but was precarious in practice. He lacked his father's charisma, relationships, and ruthlessness. Fox News hosts barely hid their disdain. Investors questioned his strategic vision. The stock price stagnated under his leadership. Most critically, he knew that upon his father's death, his siblings could fire him immediately. Every board meeting, every strategic decision, every editorial choice was shadowed by impending fratricide.

The family dynamics infected corporate governance. Board meetings became tense affairs, with independent directors navigating between warring Murdochs. Strategic decisions were paralyzed by succession implications. Would investing in streaming help Lachlan or provide assets for James to sell? Should Fox News moderate to appease Elisabeth or double down to preserve cash flow? The company was trying to operate while its owners fought a civil war.

The employees felt the uncertainty most. News Corp and Fox veterans who'd spent decades serving Rupert didn't know which prince to court. Journalists self-censored, unsure what editorial line would survive succession. Executives hedged bets, maintaining relationships with all siblings. The empire that had thrived on decisive leadership was frozen by indecision. "It's like working for a dying king with ambitious princes," one executive said. "Everyone's plotting, no one's leading."

The deeper tragedy was personal. Rupert had built an empire to create a dynasty, but the empire had destroyed the family. His children's relationships were poisoned by competition for his approval. His ex-wives lined up against him. His grandchildren grew up knowing their inheritance came with civil war. The man who'd spent seventy years accumulating power couldn't control what mattered most: his legacy. The empire would survive him, but whether as monument or mausoleum remained unknowable.

XI. Playbook: Business & Strategic Lessons

The conference room at Wharton Business School in 2018 was packed with MBA students eager to hear News Corp's CFO explain the company's strategy. Instead, she opened with a question: "How many of you have parents who watch Fox News?" Half the hands went up. "How many watch it yourselves?" Two hands, embarrassed. "That gap," she said, "is worth $2 billion in annual profit." The lesson was vintage Murdoch: serve the audience others ignore, regardless of elite opinion. After seven decades of empire building, the Murdoch playbook had become business school canon—studied, debated, and occasionally deplored, but impossible to ignore.

Regulatory Arbitrage as Competitive Advantage

Murdoch's genius wasn't just understanding media but understanding media regulation. Every expansion exploited regulatory gaps or changes. In Australia, he leveraged cross-ownership rules to build newspaper monopolies. In Britain, he became a citizen to circumvent foreign ownership limits. In America, he did it again to own television stations. The Wapping move exploited Thatcher's union laws. Fox News launched when cable regulations loosened. While competitors waited for rules to change, Murdoch changed himself to fit the rules. The lesson: regulation isn't a constraint but a puzzle—solve it faster than competitors, and temporary advantages become permanent moats.

Political Influence as Business Strategy

Most businesses lobby government; Murdoch made government his customer. The Sun's endorsement was worth votes; votes were worth access; access was worth regulatory favors. The formula worked globally. Tony Blair flew to Australia to court Murdoch. Donald Trump called him weekly. Scott Morrison, Australia's prime minister, texted him constantly. This wasn't corruption but symbiosis—politicians needed media support, Murdoch needed political protection. The 2011 phone hacking scandal revealed the danger: when influence becomes too obvious, it becomes toxic. But the strategy's effectiveness was undeniable. One study estimated Murdoch's political influence was worth $1.5 billion in regulatory benefits over two decades.

Vertical Integration in Media

Before Netflix or Disney+, Murdoch understood content's value chain. Own the creation (studios), distribution (networks), and last-mile delivery (cable systems). Fox combined all three, allowing cross-subsidization, bundling, and margin capture. When Fox News launched, Fox studios provided programming, Fox network provided promotion, and Fox's owned-and-operated stations provided distribution. Competitors had to negotiate at each level; Murdoch controlled the entire stack. The strategy culminated with the attempted Sky consolidation—combining content with satellite distribution across Europe. That it failed didn't invalidate the strategy; it proved its threat.

The Tabloid Formula

Murdoch's tabloid insight was profound: people say they want serious news but buy entertainment. The Sun's Page 3 girls, the Post's screaming headlines, Fox News's outrage machine—all exploited the gap between stated and revealed preferences. The formula had three components: simplify complex issues into moral battles, personalize abstract policies into human dramas, and always, always, pick a side. Critics called it dumbing down; Murdoch called it democratization. The highbrow papers informed elites; his properties influenced masses. In democracy, masses matter more.

Managing Family Control in Public Companies

The dual-class share structure—super-voting stock for family, regular shares for public—let Murdoch maintain control while accessing capital markets. With 38.4% voting control but 14% economic ownership, he commanded billions without owning them. This structure survived hostile takeover attempts, activist investors, and succession battles. The cost was persistent "Murdoch discount" in valuations, but control premium was worth it. The lesson: if you're building for generations, structure for control, not current valuations. Markets are temporary; family is permanent—until it isn't.

Crisis Resilience Through Compartmentalization

Phone hacking should have destroyed News Corp. MySpace's failure should have crippled it. The split should have weakened it. Each crisis was contained through strategic compartmentalization. Close News of the World, save The Sun. Sell MySpace, keep newspapers. Split the company, preserve both parts. Murdoch treated assets as expendable if the empire survived. This wasn't sentiment but mathematics: better to lose a limb than die. The strategy required emotional detachment from properties others would consider irreplaceable. Everything was negotiable except survival.

Platform vs. Content Lessons

MySpace taught Murdoch the hardest lesson: content and platforms require different DNA. Content companies create, control, and monetize. Platform companies facilitate, enable, and scale. News Corp knew how to produce news, entertainment, and opinion. It didn't know how to build technology infrastructure, manage user-generated content, or sacrifice short-term revenue for network effects. The failure cost billions but taught clarity: stick to content, let others build platforms, then charge them for content. The OpenAI deal vindicated this insight—get paid by platforms that need content, don't try to become them.

The Succession Paradox

Murdoch's greatest business failure was succession planning. By dividing control among children with different visions, he guaranteed civil war. The Nevada trust battle revealed the paradox: the structures that enabled empire building—family control, dual-class shares, irrevocable trusts—prevented smooth transition. The lesson is sobering: the same mechanisms that protect companies from markets can't protect them from families. Every family business faces this paradox; Murdoch just faced it on a $10 billion scale.

The Murdoch playbook wasn't ethical, elegant, or often even legal. But it was effective. In an industry where most companies died, News Corp survived and thrived for seven decades. The strategies—regulatory arbitrage, political influence, vertical integration, tabloid populism—were copied globally. Whether that's achievement or indictment depends on perspective. But as business strategy, it was undeniably masterful.

XII. Analysis & Investment Case

Trading at $27.30 in December 2024, News Corporation presents a fascinating paradox for investors: a "dying" newspaper company with growing digital revenues, trading at 11x forward earnings while tech companies with similar growth trade at 30x. The market can't decide if this is a value trap or a hidden gem. The numbers suggest it might be both—a melting ice cube with a surprisingly solid core, a legacy media company that actually navigated digital transformation, but faces existential questions about post-Murdoch leadership. Understanding News Corp as an investment requires disaggregating its contradictions.

Current Valuation and Market Position

At a $15.4 billion market cap, News Corp trades at compelling multiples: 1.5x book value, 8x EBITDA, with a 1.5% dividend yield. The balance sheet is fortress-like—$2.8 billion in cash, minimal debt, generating $1.2 billion in annual free cash flow. For comparison, The New York Times Company trades at 28x earnings despite slower growth. The "Murdoch discount" is real and quantifiable—analysts estimate 20-30% valuation penalty for governance concerns and succession uncertainty. Strip away the drama, and you have a business generating 12% operating margins, 15% return on equity, with 52% of revenues from digital sources.

Segment Performance Breakdown

The real story is in segment analysis. Digital Real Estate Services generated $1.8 billion in fiscal 2024, growing 25% annually with 35% margins. This segment alone—primarily REA Group—is worth $8-10 billion. Dow Jones delivered $2.1 billion in revenue with steady mid-teens margins, worth perhaps $4-5 billion. Subscription Video Services (Foxtel) contributed $1.9 billion but faces secular decline. News Media Services brought $4.2 billion but with single-digit margins. HarperCollins added $1.8 billion with improving margins. Do the math: the valuable segments (Real Estate, Dow Jones) are worth nearly the entire market cap. You're getting everything else—including The Sun, New York Post, and HarperCollins—essentially for free.

Digital Transition Progress

The digital transformation metrics are impressive. The Wall Street Journal's 4.3 million digital subscribers generate $800 million in recurring revenue. The Sun and Times of London added 800,000 digital subscribers combined. REA's platforms host 90 million monthly users. Even the New York Post reaches 100 million monthly unique visitors digitally. The company has successfully shifted from advertising dependency (now just 35% of revenues) to subscriptions and transactions. This isn't cosmetic digital lipstick on a print pig—it's fundamental business model transformation.

Competitive Threats

The bear case is compelling. Google and Facebook destroyed newspapers' advertising model and could enter real estate classification. Netflix and Disney+ are crushing Foxtel. The New York Times and Washington Post compete for digital subscribers. AI could make human journalism obsolete. Younger audiences don't read newspapers, watch cable news, or even know what News Corp is. The company is fighting on multiple fronts against better-capitalized tech giants. Every segment faces disruption.

Bull Case

Yet the bull case has merit. News Corp owns irreplaceable assets—The Wall Street Journal's brand, REA's Australian dominance, Fox News's political influence (through the Fox Corporation relationship). The subscription model provides predictable revenue. Real estate classification has proven surprisingly defensible against tech giants—Zillow hasn't killed anyone yet. The OpenAI partnership suggests News Corp can monetize content in the AI age. With $2.8 billion in cash, the company can acquire growth or return capital. At current valuations, the company could go private at a 50% premium and still be affordable for private equity.

Bear Case

The bear case extends beyond competition. Succession uncertainty paralyzes strategy—why invest for 10 years if ownership changes in two? The print newspaper business, still 48% of revenues, faces inexorable decline. Foxtel needs massive investment to compete with streaming giants but can't justify the spending. Regulatory scrutiny increases globally—Australia's media concentration laws, UK's post-Leveson regulations, American antitrust revival. ESG investors avoid News Corp due to Fox News association and governance concerns. The company could muddle along for decades, generating cash but never achieving multiple expansion.

Key Metrics to Watch

Smart investors track five metrics. First, digital subscriber growth—particularly WSJ and REA users. Deceleration would signal saturation. Second, Foxtel's strategic review—sale would remove an albatross and provide capital. Third, succession developments—any clarity would reduce discount. Fourth, capital allocation—buybacks suggest confidence, acquisitions suggest desperation. Fifth, REA's international expansion—success would validate platform strategy. These metrics matter more than quarterly earnings volatility.

Valuation Scenarios

In the optimistic scenario, News Corp splits further, spinning off REA Group and Dow Jones. REA could trade at 35x earnings as a pure-play proptech company—implying $20 billion value. Dow Jones could achieve New York Times multiples. The remaining assets would be worth something. Total value: $35-40 per share. In the pessimistic scenario, succession chaos leads to asset sales at distressed prices, print declines accelerate, and digital growth stalls. Value: $15-20 per share. The current $27 price suggests markets expect muddle-through.

Investment Recommendation

News Corp is a classic value-with-catalyst situation. The assets are clearly undervalued, but unlocking requires resolution of succession, strategic clarity, or corporate action. For patient investors comfortable with governance risk and succession uncertainty, it offers compelling risk-reward. For those seeking clean stories and growth momentum, look elsewhere. This isn't a business to fall in love with—it's a price to take advantage of. At $27, you're buying dollar bills for seventy cents, but those dollars come with drama. The question is whether the discount compensates for the dysfunction. For contrarian value investors, it probably does.

XIII. Power & Influence Assessment

The scene at 10 Downing Street in March 2016 was telling: Prime Minister David Cameron, desperate to win the Brexit referendum, hosting Rupert Murdoch for secret strategy sessions. The same scenario played out simultaneously in Washington, where Donald Trump called Murdoch almost daily, and in Canberra, where Malcolm Turnbull texted him constantly. Three continents, three leaders, one media mogul. No unelected individual in modern democracy has wielded comparable influence. The question isn't whether Murdoch has power—it's whether democracy can survive it.

Political Influence Across Three Continents

The ledger of political impact is staggering. In Britain, The Sun claimed credit for four election victories—1979, 1983, 1992, 1997. Its switch from Conservative to Labour in 1997 marked Tony Blair's landslide. In Australia, every prime minister since 1972 has courted Murdoch's papers. The Australian's opposition helped topple Kevin Rudd, Julia Gillard, and Malcolm Turnbull. In America, Fox News didn't just support Republicans—it created modern conservatism, from Tea Party to Trump. Academic studies estimate Fox News shifted vote share by 3-8 points in covered markets—enough to swing elections.

The mechanism is sophisticated. It's not just endorsements but narrative control. Murdoch's properties don't just report news; they create it. The Sun's "enemies of the people" headline about Brexit judges. Fox News's "migrant caravan" coverage before 2018 midterms. The Australian's relentless climate skepticism. These aren't coverage decisions but political interventions. The stories become reality through repetition, forcing politicians and rival media to respond. Agenda-setting power matters more than vote-counting.

Media Concentration Debates

News Corp's market share appears modest—single-digit percentages in most markets. But raw numbers obscure influence concentration. In Australia, News Corp controls 70% of newspaper circulation. The Australian is the only national broadsheet. In Britain, The Sun and Times dominate their segments. In America, Fox News commands 50% of cable news viewership. More critically, Murdoch properties dominate elite discourse—politicians, business leaders, and journalists read them disproportionately. The Wall Street Journal shapes financial opinion. The Times influences British establishment. Concentration isn't just about market share but mindshare.

The concentration enables coordination. During Brexit, The Sun, Times, and Wall Street Journal pushed similar narratives. During Trump's presidency, Fox News, New York Post, and The Australian aligned messaging. This isn't conspiracy but editorial alignment, but the effect is powerful—creating echo chambers that span continents. When Murdoch properties coordinate, they can make fringe ideas mainstream or mainstream ideas toxic. Climate denial, immigration panic, and populist nationalism all benefited from this amplification.

Editorial Independence vs. Owner Influence

The fiction of editorial independence pervades News Corp. Editors insist they operate freely; Murdoch claims he doesn't interfere. Both are lying and telling the truth simultaneously. Murdoch doesn't dictate daily coverage—he doesn't need to. He hires editors who share his worldview, promotes those who deliver results, and fires those who don't. It's management by anthropology, not instruction. Editors self-censor, knowing what Murdoch wants without being told. The system is more effective than direct control—it appears organic while being entirely orchestrated.

The Wall Street Journal's transformation post-acquisition exemplifies this. Murdoch promised editorial independence, even created a special committee to ensure it. Yet coverage shifted rightward, business coverage shrank, and political opinion expanded. No smoking-gun memo exists—it happened through personnel changes, resource allocation, and cultural pressure. Editors who pushed back found themselves reassigned or resigned. Those who aligned thrived. Independence existed in theory while influence operated in practice.

Impact on Democracy and Public Discourse

The democratic damage is measurable. Studies show Fox News viewers are systematically misinformed about factual issues—climate change, election integrity, COVID vaccines. The polarization isn't accidental but profitable—outrage drives engagement. The business model depends on creating information silos where consumers receive confirming rather than challenging information. Democracy requires informed citizens capable of good-faith disagreement. Murdoch's model produces the opposite: tribal armies armed with alternative facts.

Yet defenders argue Murdoch democratized media, giving voice to those ignored by liberal establishments. Before Fox News, conservatives felt marginalized by mainstream media. Before The Sun, working-class Britons were lectured by broadsheet elites. Murdoch didn't create these audiences—he served them. If his properties seem propagandistic, perhaps that's because all media is propagandistic, just usually for elite rather than populist causes. The critique of Murdoch often sounds like aristocratic horror at peasants finding their voice.

Comparison to Other Media Empires

History offers few parallels. William Randolph Hearst commanded similar reach but less political influence. Henry Luce's Time Inc. shaped American opinion but remained nationally bounded. Axel Springer built German media dominance but couldn't expand internationally. What makes Murdoch unique is the combination—global reach, political influence, and longevity. He's operated at the apex of media power for fifty years across three continents. No one else comes close.

The comparison to tech platforms is instructive. Mark Zuckerberg commands greater reach but less editorial control. Facebook amplifies existing content; News Corp creates it. Google organizes information; Murdoch manufactures it. The platforms have scale but lack voice. Murdoch has voice with sufficient scale. That combination—reaching millions with coordinated messaging—makes News Corp more politically potent than companies worth ten times more.

The ultimate question is whether such concentration of influence is compatible with democratic governance. Critics argue Murdoch represents information autocracy incompatible with democratic pluralism. Defenders counter that he's simply successful at competing in the marketplace of ideas. The truth is probably both—Murdoch has succeeded by exploiting democracy's weaknesses while claiming to defend its values. The empire he built reveals uncomfortable truths about how power operates in democratic societies. Information is power, power corrupts, and absolute information corrupts absolutely.

XIV. Recent Developments & Future

The December 2024 boardroom at News Corp felt like a wake interrupted by an auction. Rupert's succession plan had just been judicially eviscerated in Nevada, leaving the empire's future uncertain. Yet business continued: evaluating Foxtel bids, negotiating AI partnerships, exploring acquisitions. The company was simultaneously planning for tomorrow while unsure who would own it next week. This schizophrenic state—strategic momentum amid succession chaos—defines News Corp's current moment and future trajectory.

Foxtel's Strategic Review

The "strategic options" review for Foxtel announced in November 2024 was corporate-speak for distress sale. Third parties were circling, including British streaming company DAZN and various private equity funds. The streaming pivot—3.2 million subscribers across Kayo and BINGE—had worked tactically but failed strategically. Growth required massive content investment News Corp couldn't justify. Netflix and Disney+ were spending Foxtel's entire revenue on single shows. The review's outcome seems predetermined: sale to someone with deeper pockets or delusions of grandeur. Estimated price: $2-3 billion, far below the $6 billion valuation from 2012 but better than watching it die slowly.

AI Partnerships and Technology Integration

The OpenAI deal was just the beginning. News Corp is negotiating with every major AI company—Anthropic, Google, Meta—to license content for training. The strategy is shrewd: get paid now before courts decide if AI training constitutes fair use. Thomson estimates AI licensing could generate $200-300 million annually by 2027. More intriguingly, News Corp is building its own AI tools—automated financial journalism at Dow Jones, personalized content recommendation at The Times, property valuation models at REA. The company that bungled MySpace seems to be navigating AI intelligently, perhaps because it's enhancing existing business rather than building new platforms.

Streaming Consolidation Opportunities

With Foxtel likely exiting, News Corp needs new video strategy. Speculation centers on partnerships rather than ownership. A deal with Paramount+ for Australian content. Licensing Journal video to Apple TV+. Creating a conservative streaming service with Fox Corporation. The post-Netflix world is fragmenting into infinite niches—News Corp's brands could anchor several. But execution requires capital and focus the succession battle prevents. Every strategic option depends on who controls the company in five years.

Real Estate Platform Expansion

REA Group's failed Rightmove bid signals ambition and frustration. The Australian platform generates spectacular returns—40% margins, 20% growth—but Australia has only 25 million people. International expansion is essential but difficult. The U.S. market is dominated by Zillow and CoStar. Europe is fragmented among local players. Asia offers growth but regulatory complexity. The strategy emerging: acquire subscale players in fragmented markets, apply REA's technology, hope for synergies. It's risky but necessary—REA can't grow forever in Australia alone.

Post-Murdoch Strategic Questions

Everything depends on succession resolution. If Lachlan maintains control, expect continuity—conservative editorial lines, gradual digital transformation, and preservation of core assets. If James and siblings gain control, prepare for revolution—potential Fox News sale or transformation, aggressive digital investment, and possible merger with progressive media companies. If stalemate continues, expect paralysis—no major acquisitions, defensive posturing, and gradual decline. The Nevada court ruling didn't resolve succession; it merely delayed resolution until Rupert's death.

The intermediate scenario—most likely—is messy compromise. The siblings might agree to split assets rather than share control. Lachlan gets Fox properties and U.S. newspapers. James gets Dow Jones and REA. Elisabeth gets UK properties and HarperCollins. Everyone walks away with something, nobody gets everything. It would destroy synergies but end warfare. Investment bankers are already modeling scenarios, knowing the fees from such a breakup would be enormous.

Regulatory and Market Pressures

The external environment is increasingly hostile. Australia's government is considering new media concentration laws targeting News Corp. Britain's Online Safety Act imposes content moderation requirements affecting The Sun's digital operations. American antitrust authorities are scrutinizing the Fox-News Corp relationship despite technical separation. Meanwhile, advertisers are fleeing controversial content, subscription growth is slowing, and Gen Z doesn't know newspapers exist. The company faces headwinds from every direction.

The AI Wildcard