Nu Skin Enterprises: The Multi-Level Marketing Empire That Went Digital

I. Introduction & Episode Roadmap

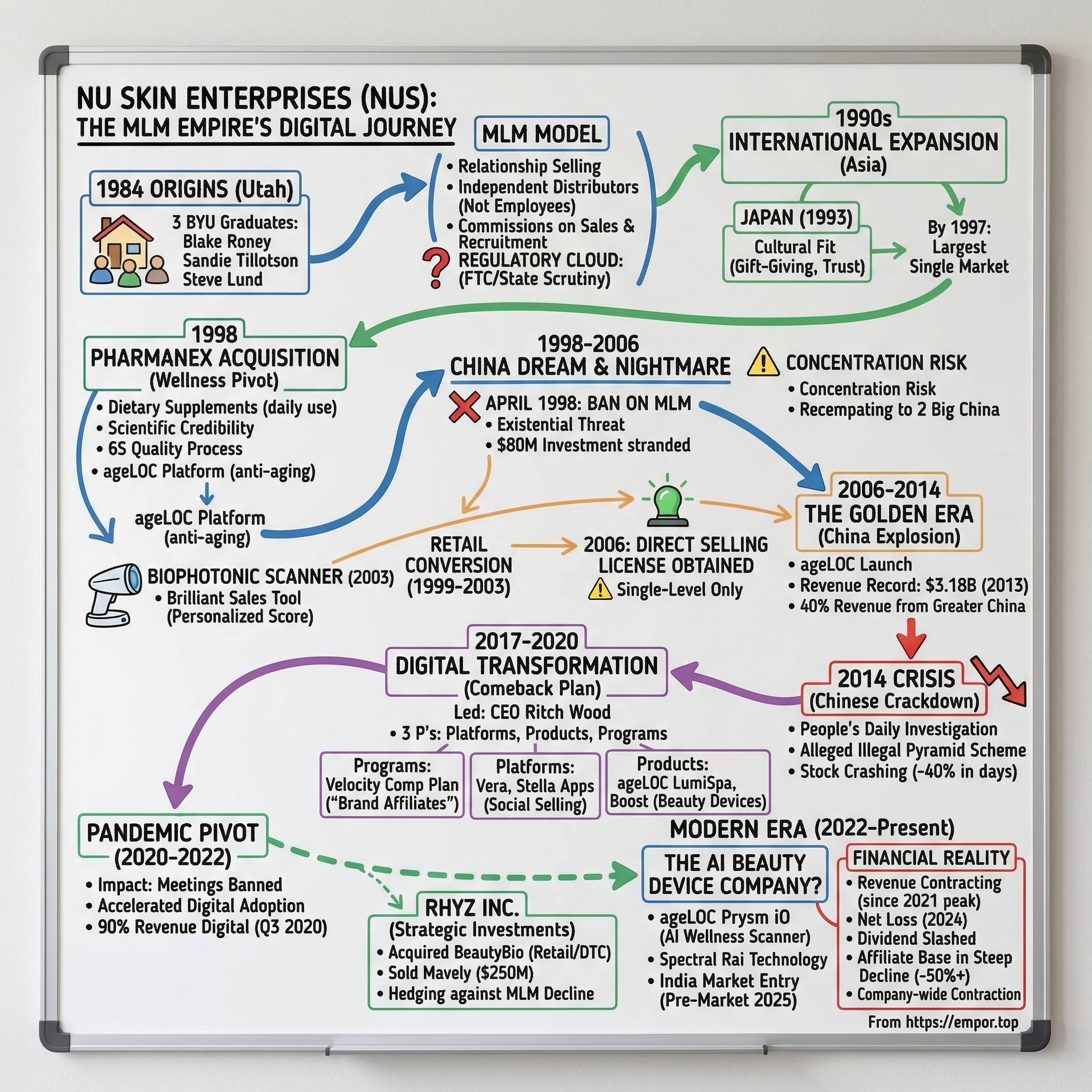

Picture a conference hall in Provo, Utah, sometime in 2019. Thousands of brand affiliates—the company refuses to call them distributors anymore—are on their feet, cheering as a sleek handheld beauty device spins on a giant screen behind the stage. The energy is part tech launch, part revival meeting, part Amway convention circa 1985. This is Nu Skin Enterprises, a company that has spent four decades straddling a fault line between legitimate consumer products business and the most controversial distribution model in American capitalism.

Here is a company that once generated over three billion dollars in annual revenue, saw its stock touch $140, then watched it all collapse when the Chinese government published a single newspaper article. A company that survived not one but two existential crises in the world's second-largest economy, paid tens of millions in legal settlements, weathered an FCPA bribery scandal, and emerged on the other side rebranding itself as a "social commerce technology platform." Today, Nu Skin trades around seven dollars a share with a market capitalization smaller than a mid-tier Silicon Valley Series C round—roughly $350 million for a business still generating north of a billion dollars in annual revenue.

How did a Utah skincare company built on the multi-level marketing model navigate the Chinese government shutdown, the global MLM backlash, the rise of direct-to-consumer brands, and a pandemic—and what does its current reinvention as an AI-powered beauty device company tell us about whether legacy distribution models can survive the creator economy age?

The answer involves three BYU graduates, a controversial compensation structure, one of the most dramatic stock collapses in consumer products history, and a bet on a handheld scanner that reads nutritional health from a fingertip. The themes that run through this story—regulatory survival, geographic concentration risk, digital transformation under duress, and the eternal question of whether MLM is a legitimate business or an elaborate transfer of wealth from the bottom to the top—are relevant far beyond Nu Skin itself. They touch every company operating in emerging markets, every legacy business facing distribution disruption, and every investor trying to distinguish between a business model in transition and one in terminal decline.

II. The MLM Industry Context & Nu Skin's Origins (1984–1990s)

Before diving into Nu Skin's founding, it helps to understand the soil from which it grew. Multi-level marketing—or MLM, or network marketing, or direct selling, depending on who is doing the branding—traces its modern lineage to the Amway Corporation, founded in 1959 in Ada, Michigan. The basic idea is elegantly simple and endlessly controversial: instead of spending money on retail stores and advertising, a company recruits independent salespeople who sell products directly to consumers and earn commissions not only on their own sales but on the sales of people they recruit into the network. Think of it as turning every customer into a potential salesperson, and every salesperson into a potential recruiter. The model exploded in the postwar decades, spawning hundreds of companies and generating billions in revenue globally. By the 2020s, the Direct Selling Association reported the U.S. market alone at roughly $36 billion in annual retail sales with over six million active sellers.

The legal distinction between a legitimate MLM and an illegal pyramid scheme hinges on a deceptively simple question: Is the money flowing primarily from product sales to end consumers, or from recruitment fees paid by new participants? The FTC has wrestled with this distinction for decades, and the line remains blurry enough to keep armies of compliance lawyers employed. This ambiguity is the permanent cloud hanging over every MLM, Nu Skin included.

Now, Utah. If you were going to design a laboratory for direct selling companies, you could hardly do better than the Beehive State. The intersection of Latter-day Saint culture—with its emphasis on community networks, missionary experience, entrepreneurial self-reliance, and large social circles—created a uniquely fertile ground for relationship-based selling. By the 1980s, Utah had become the Silicon Valley of MLM, home to dozens of direct selling companies and a deep bench of executives who understood the model.

Into this ecosystem walked Blake Roney, a 26-year-old BYU business finance graduate with $5,000 in savings and a conviction that the skincare industry was broken. Roney's insight was straightforward: department store skincare was overpriced and filled with ingredients that did nothing useful—mineral oil, synthetic fillers, harsh chemicals—while the products that actually worked were buried under layers of retail markup and marketing spend. What if you could create premium skincare with genuinely effective ingredients, strip out the retail middlemen, and distribute it through personal relationships? The tagline crystallized the vision: "All of the good, none of the bad."

Roney recruited two co-founders. Sandie Tillotson, also a BYU graduate, brought product development expertise and helped design both the original formulations and the compensation plan that would incentivize distributors. Steve Lund, a BYU-trained attorney, provided the legal architecture—critical for a business model that operated in permanent regulatory gray zone. There was also Nedra Roney, Blake's sister, whose apartment served as the company's first headquarters. She helped crystallize the concept before the company formally incorporated on October 15, 1984, in Provo.

The early days were scrappy in the way that only 1980s startups could be. An Arizona manufacturer produced the first products in ten-gallon containers. The founding team hand-filled jars. Early customers sometimes brought their own containers. The original lineup consisted of just thirteen products—cleansers, moisturizers, and treatments—each formulated without the fillers that dominated mass-market skincare. But the real product was the opportunity. The compensation plan offered commissions on personal sales plus overrides on the sales of recruits, creating the multi-level structure that would define Nu Skin's economics for the next four decades.

Growth came fast, fueled by the LDS social networks that gave distributors instant access to large, trust-based communities. By 1989, monthly sales were doubling. But rapid growth attracted regulatory attention. In 1991, Michigan's attorney general and multiple state investigations scrutinized whether Nu Skin's compensation plan crossed the line into pyramid scheme territory. ABC's Nightline ran a critical segment. By 1992, five states had extracted settlements. In 1994, the FTC imposed a $1.2 million penalty, followed by another $1.5 million in 1997. These were not mortal wounds—the fines were small relative to revenue—but they established a pattern that would follow Nu Skin throughout its history: grow fast, attract scrutiny, settle, adjust, and grow again.

By the mid-1990s, Nu Skin had evolved from a Provo apartment operation into a serious business generating hundreds of millions in annual revenue. The company went public on November 27, 1996, listing its Asia Pacific subsidiary on the NYSE at $23 per share and raising approximately $209 million. Revenue had grown from $359 million in 1995 to $679 million in 1996 to $891 million in 1997—a trajectory that suggested the real story of Nu Skin was not happening in Utah living rooms but thousands of miles across the Pacific.

III. International Expansion & The Asian Opportunity (1990s–2000s)

The conference room where Nu Skin's leadership debated international expansion in the early 1990s contained a map that told a story most American MLMs were ignoring. While competitors like Amway and Mary Kay were pouring resources into saturating the North American market—fighting over the same suburban demographics, the same kitchen-table presentations, the same PTA-mom networks—Roney and his team saw something different. Asia was experiencing the fastest middle-class expansion in human history, and the cultural dynamics of the region were practically engineered for relationship-based direct selling.

The Japan launch in April 1993 proved the thesis spectacularly. Japanese culture placed enormous value on gift-giving, personal recommendations, and social obligation—the exact behaviors that make MLM work. When a trusted friend recommended a skincare product in Tokyo, the social weight of that recommendation was fundamentally different from the same interaction in suburban Denver. By 1997, Japan had become Nu Skin's largest single market, with roughly 297,000 distributors generating an estimated $600 million in revenue. The company had found its sweet spot: premium Western skincare products sold through Asian relationship networks.

Taiwan and Hong Kong followed quickly, serving as beachheads into the broader Chinese-speaking world. South Korea launched in 1996, Thailand in 1997, Singapore in 2000, and Malaysia in 2001. Each market required cultural adaptation—the hard-sell American approach had to be softened, product formulations adjusted for local skin types and beauty standards, and compensation plans modified to comply with varying regulatory frameworks. But the underlying formula remained consistent: premium products, personal relationships, and the aspirational promise that selling Nu Skin could provide financial independence.

The timing was extraordinary in retrospect. The 1990s and 2000s saw hundreds of millions of Asians enter the middle class for the first time, with discretionary income to spend on skincare and wellness products. Asia's skincare culture was not merely a preference—it was an obsession. The multi-step Korean skincare routine, the Japanese devotion to sun protection, the Chinese fascination with anti-aging—these were deeply rooted cultural practices that made beauty products a daily necessity rather than an occasional luxury. When Nu Skin's distributors showed up with clinical-looking products promising "all of the good, none of the bad," they were selling into genuine demand, not creating it.

The revenue numbers reflected this alignment. From $359 million in 1995, total company revenue nearly tripled to approach $900 million by 1997, with the vast majority of growth coming from Asian markets. By the turn of the millennium, Nu Skin had established itself as one of the few American MLMs with a genuinely global footprint, and Asia was not merely a growth market—it was the center of gravity.

But the biggest prize of all—the market that would make Nu Skin's fortune and nearly destroy it, not once but twice—was the one behind the Great Wall. In 1998, the company made the fateful decision to enter mainland China, investing roughly $80 million in manufacturing plants and research centers. It was the largest market entry investment in Nu Skin's history by a factor of ten. The timing, as it turned out, could not have been worse.

IV. The China Dream & Nightmare (1998–2006)

Imagine being a Nu Skin executive in early 1998, standing in a gleaming new manufacturing facility outside Shanghai. Five plants, two R&D centers, $80 million invested. The Chinese cosmetics market had exploded from $25 million in 1982 to over $4 billion, growing at fifteen percent annually. American direct selling companies had already built nearly a billion dollars in retail sales in China, employing more than two million salespeople. Everything pointed to China becoming the greatest growth engine in Nu Skin's history.

Then, in April 1998, China's State Council dropped the hammer. The "Notice on Prohibiting MLM Business Activities" banned all direct selling and multi-level marketing nationwide—every company, every distributor, overnight. The government's rationale was twofold: rampant pyramid fraud schemes had caused "considerable economic damage to consumers," and officials feared that large distributor gatherings could become vehicles for religious or political organizing. The ban caused approximately $200 million in losses across the entire direct selling industry. For Nu Skin, which had just committed the largest capital investment in its history, the timing was catastrophic.

This was not a regulatory adjustment or a compliance fine. This was an existential threat. The company's entire business model—the model that had propelled it from a Provo apartment to nearly a billion dollars in revenue—was now illegal in the world's most populous nation. Every dollar of that $80 million investment sat stranded behind a regulatory wall that showed no signs of coming down.

What followed was a masterclass in strategic patience—or, depending on your perspective, an eight-year exercise in sunk-cost stubbornness. Within two months of the ban, Beijing offered a narrow lifeline: "conversion regulations" that allowed certain foreign-owned companies to resume operations through fixed retail outlets with registered, non-employee sales representatives. No multi-level compensation. No distributor meetings. No recruitment bonuses. Just straightforward retail, which was the antithesis of everything Nu Skin had built.

The company took the deal. Its first retail outlet opened in December 1999 in Shanghai, but the full retail rollout did not come until January 2003, when Nu Skin opened over one hundred retail centers across five Chinese provinces in a single month. Corey Lindley, then president of Nu Skin Greater China, acknowledged the contradiction directly: "We've developed a retail model. But because we're a direct-selling company in other parts of the world, it creates confusion." China generated perhaps $20 to $30 million in revenue during these years—a rounding error for a company doing over a billion globally.

Why stay? Because China's accession to the World Trade Organization in December 2001 included commitments to eventually lift restrictions on direct selling. Nu Skin, along with Amway and other major players, maintained their physical presence and infrastructure investments as a bet that the regulatory environment would eventually open. It was a calculated wager on patience, government relationships, and the belief that China's consumer market was simply too large to abandon.

The bet paid off. In 2005, the State Council approved comprehensive direct sales regulations, and in 2006, Nu Skin received one of ninety-two direct selling licenses issued by the Ministry of Commerce. The license came with significant constraints—single-level compensation only, limited product categories, approved geographic areas—but it represented nothing less than a corporate resurrection. After eight years in the wilderness, Nu Skin could sell directly to Chinese consumers again.

The fundamental tension, however, was now embedded in the operating model. Nu Skin ran a global multi-level compensation structure, but Chinese law permitted only single-level direct selling. The company structured compensation in China using single-level "service fees" rather than multi-level distributor allowances. Whether the actual economic incentives still functioned as a multi-level system would become the central question of the crisis that was still years away. For now, the license was a triumph—and it set the stage for the most profitable period in company history.

V. The Pharmanex Acquisition & Wellness Pivot (1998)

While the China drama unfolded, Nu Skin made a strategic move that would reshape its product identity for decades. In October 1998, the company acquired Generation Health, the parent company of Pharmanex, a Simi Valley, California-based dietary supplement company. The acquisition was motivated by a clear strategic logic: skincare alone was a narrow product category with limited replenishment frequency. Nutritional supplements, by contrast, were consumed daily, ordered monthly, and tapped into the emerging wellness megatrend that was beginning to reshape consumer spending.

Pharmanex was not a typical supplement company. It positioned itself around clinical research and a pharmaceutical-style quality control approach it called the "6S Quality Process." Its flagship product, LifePak, was a comprehensive daily nutritional supplement pack that aimed to distinguish itself from the vitamin aisle commodity products through clinical studies and dosage precision. For Nu Skin, this was a credibility play as much as a revenue play. The acquisition transformed the company from a single-brand skincare MLM into a dual-platform business: beauty products under the Nu Skin brand, nutrition and wellness under Pharmanex.

The strategic genius was in the cross-sell. A distributor who previously had one conversation—"try this cleanser"—now had two: skincare and daily nutrition. Monthly supplement subscriptions created automatic reorder revenue that smoothed out the boom-bust cycles inherent in device and skincare launches. And the combined beauty-plus-nutrition pitch laid the foundation for what would become Nu Skin's most powerful product concept: ageLOC, the idea that aging could be addressed at a cellular level across both skin and body.

But the Pharmanex acquisition's most lasting contribution was arguably not a supplement at all. In 2003, Nu Skin introduced the BioPhotonic Scanner, a device that measured carotenoid levels in skin tissue using a technique called Resonant Raman Spectroscopy. In plain language: the scanner shined a low-power laser on a person's palm and read the backscattered light to produce a "Skin Carotenoid Score"—a numerical proxy for antioxidant levels. Think of it as a thermometer, but instead of measuring temperature, it measured how well-nourished your cells were based on the carotenoid pigments from fruits, vegetables, and supplements.

As a sales tool, the scanner was brilliant. It gave distributors a scientific-looking device that produced an immediate, personalized health score in thirty seconds. It created a before-and-after narrative: "Start taking LifePak for ninety days and rescan to see your score improve." It turned a subjective supplement pitch into an apparently objective measurement. Nu Skin did not sell the scanner to consumers—it remained a tool distributed to sales leaders as a business builder. Over two decades, the device generated a database of more than twenty-one million scans from over ten million people across roughly fifty countries. That database, as it would turn out, became the training data for something far more ambitious two decades later.

The wellness pivot proved prescient. As the global wellness economy grew from a niche market into a multi-trillion-dollar industry, Nu Skin's dual beauty-and-nutrition positioning gave it a broader addressable market than pure skincare competitors. The Pharmanex brand provided a scientific veneer that helped differentiate Nu Skin's offerings from the commodity supplements flooding mass retail shelves. And the monthly subscription revenue from LifePak and other Pharmanex products provided a financial cushion that would prove critical when the company's device and skincare revenue proved more cyclical than expected.

VI. The Golden Era & Mainland China Explosion (2006–2014)

The years following the China license approval were the closest thing to a golden age that any MLM company has ever experienced. With the direct selling license in hand and the ageLOC anti-aging platform ready for launch, Nu Skin was about to ride the greatest consumer spending wave in Chinese history.

The numbers tell a staggering story. In 2010, total company revenue stood at $1.54 billion. By 2012, it had reached $2.13 billion, with Greater China contributing $551 million. Then 2013 happened. Greater China revenue exploded to $1.36 billion—a 148 percent increase in a single year. Total company revenue hit $3.18 billion, an all-time record that has never been matched. In the span of twelve months, Nu Skin added over a billion dollars in revenue, with virtually all of the growth coming from mainland China.

What drove this explosion? The ageLOC product line—particularly the ageLOC R2 and ageLOC Body Galvanic Spa, which began taking orders in China in May 2012, followed by the ageLOC TR90 weight management system launched in the second half of 2013. These were not commodity lotions. They were premium anti-aging systems positioned at the intersection of science and aspiration, priced at levels that signaled status and exclusivity. For China's newly wealthy middle class, buying ageLOC was simultaneously an act of self-care and social signaling—a way to demonstrate sophistication and purchasing power.

The distributor network in Greater China doubled in six months, from roughly 30,000 sales leaders at mid-2013 to approximately 60,000 by year's end. Active distributors grew even faster. The ageLOC product line generated more than $700 million in sales over three years globally, with the lion's share coming from Chinese consumers who were spending more per capita on anti-aging products than consumers in any other market.

Wall Street loved the story. NUS stock surged from the mid-$40s in 2012 to an all-time intraday high of $140.50 on January 13, 2014. The company was a rare thing in the consumer products world: a mid-cap with emerging market growth rates, high margins, and a distribution model that required minimal capital expenditure. Analysts published glowing reports about the "China consumer megatrend" and the "ageLOC innovation pipeline."

But the warning signs were hiding in plain sight. By late 2013, mainland China alone represented roughly thirty-two percent of total revenue, and the percentage was climbing. Greater China, including Hong Kong and Taiwan, was approaching forty percent. This was not diversified growth—it was concentration risk masquerading as a growth story. The same dynamic that made the numbers so exciting—explosive growth from a single market—also made the company extraordinarily vulnerable to anything that went wrong in that market. And in China, things can go very wrong, very fast.

The fundamental contradiction also remained unresolved. Chinese law permitted single-level direct selling but explicitly prohibited multi-level compensation. Nu Skin structured its Chinese compensation using single-level "service fees," but the actual incentive architecture—the meetings, the recruiting events, the upline-downline dynamics—looked suspiciously similar to the multi-level model that operated everywhere else. Whether the company was operating within the letter and spirit of Chinese law, or merely within the letter while violating the spirit, was about to become the most expensive question in Nu Skin's history.

VII. Crisis & The Chinese Crackdown (2014–2017)

On January 15, 2014—just two days after NUS stock touched its all-time high—the People's Daily, the official newspaper of the Chinese Communist Party, published an investigative report that read like a corporate death sentence. The article asserted that Nu Skin's operations in China violated Chinese law and constituted a suspected illegal pyramid scheme. The specific allegations were devastating: the company was organizing "brainwashing gatherings" that resembled MLM recruiting events, passing advertisements as news reports, selling 104 products in China when regulations permitted only 84, and operating multi-level marketing activities in direct violation of its direct selling license.

To understand the gravity of this moment, you need to understand what the People's Daily is. It is not an independent newspaper. It is the official organ of the Chinese Communist Party. A negative report in People's Daily carries implicit government sanction and is almost always a precursor to regulatory action, not merely journalism. When the People's Daily calls you a suspected pyramid scheme, the Chinese government is telling you something.

The market understood immediately. On January 15, NUS shares fell fifteen percent. The following day, two Chinese agencies simultaneously announced formal investigations, and the stock cratered another twenty-six percent. By January 17, shares had fallen to $79.47—a decline of roughly forty percent from the peak just four days earlier. More than $3 billion in market capitalization evaporated in less than a week.

On January 21, 2014, Nu Skin China voluntarily suspended all business promotional meetings and halted applications for new sales representatives. For a direct selling company, suspending meetings is the equivalent of a restaurant closing its dining room—the entire business model runs on human gatherings. Without meetings, there was no recruitment, no product demonstrations, no team building. The distributor network went dormant.

The financial damage cascaded through the next three years. By the second quarter of 2014, China revenue had fallen twelve percent and active sales representatives had dropped thirty-two percent. The distributor base in Greater China collapsed from roughly 60,000 sales leaders to 26,000 within six months. At a company expo in August 2014 intended to rebuild momentum, only 13,000 new customers were attracted—against what had been a billion-dollar annual revenue run rate—and just 1,500 previously-departed distributors accepted reinstatement offers.

The financial penalties from Chinese regulators were surprisingly modest—approximately $540,000 in fines for selling unapproved products through direct channels and making unsubstantiated claims. But the real damage was reputational and structural. The distributor exodus created a death spiral: fewer distributors meant fewer sales, which meant lower commissions, which meant more distributors leaving, which meant even fewer sales.

Then came the FCPA scandal. It emerged in September 2016 that during the 2014 investigation, Nu Skin China had donated approximately $154,000—one million renminbi—to a charity associated with a high-ranking Communist Party official, in an attempt to influence the outcome of a regulatory investigation. The donation was improperly recorded as charitable rather than as a payment to influence an official. Nu Skin paid $765,688 to the SEC to settle Foreign Corrupt Practices Act violations. Separately, a shareholder class-action lawsuit alleging that management had concealed illegal MLM operations in China resulted in a $47 million settlement in February 2016.

Revenue fell from the $3.18 billion peak in 2013 to $2.57 billion in 2014, then $2.25 billion in 2015, bottoming at $2.21 billion in 2016—a thirty percent decline that the company has never recovered from. The stock, which had touched $140.50 in January 2014, traded in the $30 to $50 range by 2016. The working capital crisis was equally severe: in the first quarter of 2014, operating cash flow turned negative by $160 million, and the company breached debt covenants requiring emergency lender extensions.

The crisis was not unique to Nu Skin. When the People's Daily attacked Nu Skin, Herbalife stock dropped ten percent in sympathy and USANA fell twelve percent, demonstrating that investors viewed MLM China risk as a sector-wide issue. Bill Ackman, who had been shorting Herbalife since December 2012, held a two-and-a-half-hour conference call in March 2014 specifically alleging that Herbalife was violating Chinese direct-selling laws. The FTC opened a formal investigation into Herbalife the very next day. The entire MLM industry was under siege, and Nu Skin—with the highest China concentration of any major player at roughly a third of revenue—was the most exposed.

The existential question hanging over the company was stark: Could Nu Skin survive without China dominance? The answer would require new leadership, a fundamentally different strategy, and a willingness to reinvent a forty-year-old business model.

VIII. The Comeback Plan: Digital Transformation & Social Commerce (2017–2020)

Ritch Wood was an unlikely turnaround CEO. A thirty-year Nu Skin veteran who had served as Chief Financial Officer for fourteen years, Wood had the accountant's temperament—methodical, risk-aware, deeply familiar with every line of the income statement. When he took the CEO role in 2017, the conventional wisdom was that Nu Skin needed a visionary outsider to break free from its MLM roots. Instead, Wood brought something arguably more valuable: institutional knowledge and a clear-eyed framework he called the "3 P's"—Platforms, Products, and Programs.

The diagnosis was blunt. Nu Skin's traditional distribution model—home parties, hotel meeting rooms, hand-drawn compensation plan diagrams on whiteboards—was dying. Millennials did not attend Tupperware parties. They did not want to cold-call friends and family. They lived on Instagram and YouTube, and if they were going to sell anything, they wanted to do it through a screen, not across a kitchen table. The direct selling industry's median participant age was creeping upward, and recruitment of younger sellers was collapsing industry-wide. Nu Skin needed to digitize or die.

The Velocity compensation plan, launched in June 2018, was the centerpiece of the Programs pillar. It restructured how sellers earned money, introducing a Retailing Bonus paid on direct sales to retail customers—with Nu Skin handling fulfillment—and creating clearer distinctions between being a product seller and a team builder. Critically, Velocity rebranded all distributors as "Brand Affiliates," borrowing the language of the influencer and creator economy rather than the MLM lexicon of "uplines" and "downlines." The Direct Selling Association recognized Velocity as an industry-leading innovation, though skeptics noted that the underlying multi-level commission structure remained fundamentally intact.

On the Platforms side, Nu Skin built a digital selling infrastructure from scratch. The Vera app provided AI-driven selling recommendations. Stella enabled social content sharing and product promotion. MyShop gave affiliates personalized storefronts. The My Nu Skin app consolidated business management tools for tracking sales, customers, and orders. By the third quarter of 2020, approximately ninety percent of Nu Skin's revenue was transacting digitally—a transformation that would have seemed impossible three years earlier.

The Products pillar was where Wood's strategy got genuinely interesting. Rather than competing on lotions and serums—categories where Nu Skin was a mid-tier player against giants like L'Oreal and Estee Lauder—the company leaned hard into connected beauty devices. The ageLOC LumiSpa, a handheld oscillating silicone cleansing device launched in 2017 at roughly $185, became a breakout hit. It was followed by the ageLOC Boost, a variable pulse microcurrent device priced around $259 that launched in January 2021. These were not commodity products. They were premium hardware that required proprietary consumables—treatment cleansers, activating serums—creating a razor-and-blade recurring revenue model.

The device strategy was elegant for multiple reasons. First, beauty devices carried higher margins than skincare products and were harder for competitors to copy quickly. Second, they created genuine differentiation—Euromonitor International ranked Nu Skin as the world's number-one brand for beauty device systems for six consecutive years. Third, devices required consumable refills, turning a one-time hardware sale into an ongoing subscription relationship. And fourth, a two-hundred-dollar device gave affiliates a fundamentally different sales conversation than a thirty-dollar moisturizer—it elevated the perceived value of the entire product line.

Geographic diversification became an explicit strategic priority. After the China crisis demonstrated the catastrophic risk of concentration, management worked to grow the Americas and EMEA segments while stabilizing Asian markets. The goal was not to abandon China but to ensure that no single market could ever again threaten the company's survival. This was easier said than done—the Americas had always been Nu Skin's smallest contributor relative to Asia—but by 2021, the Americas had grown to roughly twenty percent of total revenue, up from low-teens percentages during the China peak years.

The cultural transformation inside Nu Skin was perhaps the hardest part. Convincing a forty-year-old direct selling company to think like a technology platform required changing not just tools but mindsets. Executives who had built careers on hotel ballroom presentations had to learn to talk about customer acquisition costs and digital funnels. The headquarters in Provo started hiring engineers and data scientists alongside the traditional product development and sales leadership teams. Whether this transformation was genuine or cosmetic remained an open question—but Wood's tenure demonstrated that the company was at least willing to try.

IX. The Pandemic Pivot & Rhyz Launch (2020–2022)

When COVID-19 lockdowns swept the globe in March 2020, a company built on in-person selling should have been devastated. The first quarter confirmed the fear—revenue fell seventeen percent as China, still the largest single market, shut down completely. But what happened next surprised almost everyone.

The pandemic did not kill Nu Skin's model. It accelerated a digital transformation that had been proceeding too slowly for years. With in-person meetings banned worldwide, the affiliate base was forced to adopt the digital tools that many had been resisting. Zoom replaced hotel ballrooms. Instagram stories replaced kitchen-table demonstrations. The ninety percent digital transaction rate that Nu Skin achieved by Q3 2020 was not the result of a brilliant strategic initiative—it was the result of millions of affiliates having no other option.

Full-year 2020 revenue came in at $2.58 billion, up seven percent from the 2019 trough that had been caused by yet another Chinese government crackdown—the "100 Days of Action" campaign that had knocked the stock down twenty percent in a single day in July 2019. The fourth quarter of 2020 was particularly strong at $748 million, up twenty-eight percent, with customer growth running at thirty-four percent. The home-based affiliate opportunity became more attractive to people who had lost jobs or needed supplemental income, and demand for at-home beauty devices surged as consumers sought alternatives to closed salons and spas.

But the pandemic sugar rush obscured a deeper problem. When lockdowns eased and consumers returned to pre-pandemic routines, much of the surge dissipated. Revenue in 2021 reached $2.695 billion—a modest four percent gain that masked sharp divergence between regions. The Americas grew twenty-one percent and EMEA grew twenty-three percent, but China fell nine percent as Beijing maintained strict COVID controls and continued monitoring direct selling activities. The bifurcation foreshadowed the serious deterioration that followed.

Meanwhile, Nu Skin made its most ambitious structural bet. Rhyz Inc., originally founded in 2018 as a collection of manufacturing and technology companies supporting Nu Skin's supply chain, evolved into a separate strategic investment arm. The vision was to build an ecosystem of consumer, technology, and manufacturing businesses that could operate independently of the traditional MLM channel. In November 2021, Nu Skin acquired Mavely, a social commerce and affiliate marketing platform, for approximately $50 million. In August 2023, Rhyz acquired BeautyBio, a Dallas-based skincare and device brand with patented microneedling tools sold through conventional channels including Sephora and Nordstrom—no MLM compensation structure involved.

The Rhyz strategy represented a philosophical admission: the traditional MLM channel alone might not be enough. By building or acquiring brands that sold through conventional retail and direct-to-consumer channels, Nu Skin was hedging against the possibility that its core distribution model was in structural decline. Rhyz revenue grew from $216.6 million in 2023 to $286.6 million in 2024, adding meaningful scale outside the affiliate network.

Then came a revealing pivot. In January 2025, Nu Skin sold Mavely to Later for approximately $250 million—roughly five times its acquisition price. The sale generated cash that management used primarily to pay down debt, and it signaled a strategic retreat from the ambition of building a standalone social commerce technology platform. Instead of trying to become a tech company, Nu Skin appeared to be refocusing on what it actually knew how to do: developing beauty and wellness products and distributing them through its affiliate network, augmented by conventional retail through Rhyz portfolio brands like BeautyBio.

The creator economy bet—the idea that Nu Skin could attract Gen Z influencers through Mavely's platform—had not panned out as hoped. The sale was a pragmatic acknowledgment that building a social commerce technology platform from scratch was a different business entirely from selling beauty devices through relationship networks. Sometimes the most important strategic decisions are knowing what you are not.

X. Modern Era: The AI Beauty Device Company (2022–Present)

The conference rooms at Nu Skin's Provo headquarters tell a different story today than they did a decade ago. Where PowerPoint decks once featured charts of Chinese distributor counts climbing exponentially, the presentations now center on a device that looks like it belongs in a dermatologist's office: the Prysm iO, an AI-powered nutritional wellness scanner that represents the company's biggest product bet since ageLOC.

But the optimism in those conference rooms exists in tension with the financial reality. Revenue has declined every year since the 2021 peak of $2.695 billion: $2.225 billion in 2022, $1.97 billion in 2023, $1.73 billion in 2024, and $1.49 billion in 2025. That is a forty-five percent revenue decline over four years. The stock, which touched the mid-$60s during the pandemic recovery, now trades around $7.31 with a market capitalization of approximately $350 million. The company recorded a net loss of $146.6 million in 2024. The dividend was slashed eighty-five percent in 2024, from $1.56 to $0.24 per share.

The geographic story has shifted dramatically. China, once nearly forty percent of revenue, contributed roughly $235 million in 2024—approximately sixteen percent of the Nu Skin segment. The Americas became the largest single segment. But this is not a story of successful diversification replacing Chinese growth with American growth. Every region declined in 2024. South Korea fell thirty-one percent. The Americas fell nineteen percent. This is a company-wide structural contraction, not a geographic rotation.

The most alarming metric is the affiliate base itself. From the end of 2021 to 2025, paid affiliates declined from roughly 270,000 to 129,000—a drop of more than fifty percent. Sales leaders fell from 61,500 to 30,000. Customers declined from 1.37 million to 749,000. The engine that drives the entire business model is shrinking at an accelerating rate.

Against this backdrop, management under CEO Ryan Napierski—a career Nu Skin executive who joined in 1995 and took the CEO role from Ritch Wood in September 2021—has placed an enormous bet on the Prysm iO device. Announced in December 2025, Prysm iO is the next-generation evolution of the original Pharmanex BioPhotonic Scanner, but dramatically upgraded. It uses patent-pending "Spectral Rai Technology" to capture over 70,000 hyperspectral absorption measurements per scan—more than 6,000 per second—from a simple fifteen-second finger scan. Think of it as a fitness tracker for your nutritional health: it produces a personalized "Prysm Score" across four health domains—diet, fitness, lifestyle, and supplementation—and uses AI trained on the twenty-one-million-scan database accumulated over two decades to generate personalized wellness recommendations.

The device is portable and consumer-grade, unlike the original scanner which was a larger tool used only by distributors. As of the fourth quarter 2025 earnings call, over 20,000 devices had been deployed to sales leaders, generating more than 700,000 scans. Management targets 100,000 devices placed by the end of 2026, with broader consumer availability rolling out throughout the year. The India market entry, with pre-market operations beginning in November 2025 and formal launch targeted for late 2026 through an Infosys partnership for digital-first infrastructure, adds another potential growth vector.

One bright spot in the recent results: gross margin improved to 70.7 percent in the fourth quarter of 2025, up from 62.7 percent a year earlier. The Mavely sale proceeds reduced debt. And management's 2026 guidance of $1.35 to $1.50 billion in revenue suggests the rate of decline may be slowing, though the range still implies further contraction.

Napierski has reframed the company's identity from "the world's leading direct sales company" to "the world's leading integrated beauty and wellness company powered by a dynamic affiliate opportunity platform." The language is deliberate—"social commerce" replaces "MLM," "Brand Affiliates" replaces "distributors," and the emphasis shifts from the compensation structure to the technology platform. The reality, however, is that Nu Skin remains legally and operationally a multi-level marketing company. Brand Affiliates earn retail bonuses on their own sales and performance bonuses based on the sales of their recruited downlines. The rebrand is a marketing and narrative repositioning, not a structural change to the compensation model. SEC filings continue to describe the company accurately as an MLM.

For investors, the central question is whether the Prysm iO device cycle, the India expansion, and the gross margin improvements can stabilize or reverse the affiliate base decline before the shrinking network becomes too small to sustain meaningful revenue. The company still generates over a billion dollars in annual sales with improving margins—there is a real business here. But the trajectory of the affiliate count is the single most important variable determining whether this is a turnaround story or a managed decline.

XI. Porter's Five Forces Analysis

To understand Nu Skin's competitive position structurally, it helps to apply Michael Porter's framework to the intersection of direct selling and beauty-wellness—two industries that are individually difficult and, in combination, create a particularly challenging competitive environment.

The threat of new entrants is moderate to low for the distribution model itself. Building a multi-level distributor network with hundreds of thousands of active sellers across fifty-plus markets takes decades and requires navigating a maze of regulatory frameworks. The China direct selling license alone, which Nu Skin spent eight years and tens of millions of dollars to obtain, represents a genuine barrier. But on the product side, barriers are collapsing. Direct-to-consumer brands can launch skincare or supplement lines with minimal capital, sell through Amazon or TikTok Shop, and reach consumers without building any distributor network at all. The barrier is high to replicate Nu Skin's distribution, but low to compete for the same consumer's wallet.

Supplier bargaining power is low. Nu Skin controls its own formulations and manufacturing relationships, beauty and wellness ingredients are widely available from multiple sources, and electronics manufacturing for devices can be sourced from multiple Asian contract manufacturers. The Rhyz manufacturing acquisitions further reduced dependence on third-party suppliers.

The bargaining power of buyers—both distributors and end consumers—is where the model gets interesting. Distributors represent a unique buyer class: they are simultaneously customers, salespeople, and recruiters. They can switch to competing MLMs, start their own DTC brand, or simply stop selling. The switching costs are moderate—years of training, built relationships, and accumulated compensation structure rank create inertia—but the declining affiliate counts demonstrate that these switching costs are not sufficient to prevent attrition when the value proposition weakens. End consumers have almost unlimited alternatives in beauty and wellness, from The Ordinary's ten-dollar serums to La Mer's three-hundred-dollar creams, making their bargaining power very high.

The threat of substitutes is arguably the most significant force. Nu Skin faces substitution at two levels: product substitution (hundreds of beauty and wellness competitors) and model substitution (the MLM distribution approach being replaced by influencer marketing, social commerce platforms, and DTC brands). When a TikTok creator with two million followers can launch a skincare brand through Shopify and reach more consumers in a week than a Nu Skin affiliate reaches in a year, the entire distribution model faces existential substitution pressure.

Competitive rivalry is intense on every front. Among MLM peers, Nu Skin competes with Amway (roughly $7.4 billion in revenue), Herbalife (approximately $5 billion), USANA, Arbonne, and dozens of smaller players. Against traditional beauty, the company faces L'Oreal, Estee Lauder, and Procter & Gamble—companies with marketing budgets larger than Nu Skin's entire revenue. In beauty devices specifically, Foreo, NuFace, and CurrentBody compete directly. And in supplements, the market is so fragmented that Nu Skin's Pharmanex brand barely registers against the hundreds of brands available on Amazon.

The net assessment from Porter's framework is sobering: Nu Skin operates in a structurally difficult competitive environment where supplier power is the only consistently favorable force.

XII. Hamilton's Seven Powers Framework

Hamilton Helmer's Seven Powers framework asks a more pointed question than Porter: not just "what is the competitive environment?" but "what durable competitive advantages does the company actually possess?" For Nu Skin, the honest answer is: fewer than management would like.

Scale economies are limited. Nu Skin gets some benefit from spreading manufacturing and corporate overhead across its revenue base, but the MLM sales model does not scale with decreasing unit costs the way a software business or even a traditional retailer does. Each incremental sale requires an active affiliate to make it, and affiliate productivity does not systematically improve as the network grows.

Network effects exist but are asymmetric and weaker than in true network-effect businesses. A larger distributor network theoretically creates more recruitment potential and broader consumer reach. But unlike Facebook or Uber, where each additional user makes the platform more valuable for everyone, MLM network effects are complicated by the fact that distributors in the same network compete with each other for the same customers and recruits. The social commerce pivot aims to strengthen network effects by making the affiliate platform more valuable through shared content and tools, but the results so far have not demonstrated meaningful network-effect dynamics.

Counter-positioning offers perhaps the most interesting theoretical advantage. Traditional beauty conglomerates cannot easily adopt the MLM model without creating channel conflict with their retail partners and risking brand damage from the MLM stigma. This means L'Oreal and Estee Lauder are unlikely to replicate Nu Skin's distribution approach. But the counter-position works both ways: DTC brands are counter-positioned against everyone, including Nu Skin, by offering the "direct" relationship without the MLM baggage.

Switching costs are weak for end consumers—a $30 moisturizer is trivially replaceable—and moderate for distributors, whose investment in training, relationships, and compensation rank creates some friction but clearly not enough to prevent the ongoing affiliate exodus. The subscription model creates mild stickiness but nothing approaching true lock-in.

Branding power is weak. Nu Skin lacks the consumer brand recognition of prestige beauty houses. It is primarily a distributor-focused brand, not a consumer-focused one, and the MLM association actively works against brand equity in many markets. The LumiSpa device has built some standalone recognition, and the Prysm iO may create a new brand identity around wellness technology, but these are emerging assets rather than established power sources.

Cornered resources are hard to identify. Nu Skin has no proprietary ingredients, and beauty patents are notoriously difficult to defend. The China direct selling license was a genuine cornered resource from 2006 through 2014, but its value diminished dramatically after the crackdown. The twenty-one-million-scan biometric database powering the Prysm iO's AI algorithms may represent the closest thing to a cornered resource the company possesses today—it is genuinely proprietary and difficult to replicate—but its commercial value remains unproven.

Process power is moderate and perhaps the company's most defensible advantage. Four decades of managing global MLM operations across fifty-plus markets, navigating regulatory environments from Beijing to Brasilia, launching products simultaneously across dozens of countries, and managing complex multi-level compensation structures represent institutional knowledge that cannot be easily copied. The regulatory navigation expertise, particularly in China, has kept Nu Skin operating in markets where less experienced companies would have been forced out.

The overall assessment is that Nu Skin operates with weak-to-moderate competitive power. The company's best sources of durable advantage are its process power in regulatory navigation and global operations management, combined with whatever network effects its affiliate base provides. The transformation to beauty tech and devices represents an attempt to create new power sources—branding through devices, switching costs through consumable ecosystems, and potentially a cornered resource through the Prysm biometric database—but these remain aspirational rather than proven.

XIII. Business Model Deep Dive & The MLM Question

No honest analysis of Nu Skin can avoid confronting the MLM question directly. The multi-level marketing model is the most debated distribution structure in capitalism, and Nu Skin sits squarely at the center of that debate.

Here is how the compensation structure actually works. Brand Affiliates earn money in two ways: retail bonuses on products they sell directly to customers, and performance bonuses based on the sales generated by their recruited downlines—the people they bring into the network, and the people those people bring in, cascading through multiple levels. Affiliates progress through ranks—from Brand Affiliate to Sales Leader to Executive and beyond—based on a combination of personal sales volume and team sales volume. Higher ranks unlock higher commission percentages on downline sales.

The math, however, is where the controversy ignites. According to FTC guidelines, companies must disclose income statistics for their participants. The data across the MLM industry is consistent and stark: the vast majority of participants earn little to nothing, and many lose money. At Nu Skin specifically, income disclosure statements have historically shown that a large majority of active participants earn less than their annual product purchases would cost, meaning they are net spenders rather than net earners. The median income for active Brand Affiliates in the United States is typically in the low hundreds of dollars annually. The high earners at the top of the compensation structure can earn six or seven figures, but they represent a tiny fraction of the total participant base.

The ethical debate falls along predictable lines. Critics argue that MLM is a wealth transfer mechanism from the many at the bottom to the few at the top, where the primary "product" being sold is the opportunity itself rather than the skincare or supplements. Defenders counter that MLM provides genuine entrepreneurial opportunity, flexible work arrangements, community belonging, and access to premium products at wholesale prices—and that failure rates are comparable to any small business venture.

The legal distinction remains the critical variable. The FTC's framework distinguishes legitimate MLMs from illegal pyramid schemes based on whether compensation is primarily derived from product sales to end consumers or from recruitment of new participants. Nu Skin has been on both sides of this line at different moments in its history. The 1994 and 1997 FTC penalties, the 2014 China crisis, and the ongoing requirement to demonstrate that affiliate compensation is tied to genuine retail sales rather than recruitment create a permanent regulatory overhang.

Nu Skin's Velocity compensation plan explicitly tried to shift the emphasis toward retail customer sales by introducing the Retailing Bonus and tracking distinct "Customer" metrics separate from affiliate purchases. Whether this represents a genuine structural change or a cosmetic relabeling is debated. The social commerce rebranding changes the language—"affiliates" instead of "distributors," "social selling" instead of "network marketing"—but the multi-level compensation structure that defines the business model remains intact in its fundamental architecture.

For investors, the MLM question matters for two concrete reasons. First, regulatory risk: a single FTC enforcement action or foreign government crackdown can destroy billions in market value overnight, as the 2014 China crisis demonstrated. Second, structural sustainability: if the affiliate model is in secular decline—if younger generations simply will not participate in multi-level compensation structures—then the entire revenue generation engine is eroding regardless of how good the products are. The declining affiliate counts across the industry, not just at Nu Skin, suggest this is not a company-specific problem but a generational shift in how people want to earn and spend.

XIV. Playbook: Business & Investing Lessons

Nu Skin's four-decade journey offers a remarkably dense set of lessons for both operators and investors, many of which extend far beyond the direct selling industry.

The single most important lesson is that geographic concentration risk is a silent killer. During the golden era, when China was growing at triple-digit rates and the stock was approaching $140, it was nearly impossible to find an analyst report that flagged concentration as a primary risk. The growth was too intoxicating, the margin expansion too compelling, the China consumer story too seductive. But the company was building a skyscraper on a single foundation—and when that foundation cracked in January 2014, the entire structure wobbled. The lesson is not that companies should avoid large markets. It is that no single market should ever represent more than twenty to twenty-five percent of revenue without an explicit, funded, measurable diversification plan.

The corollary lesson is about regulatory risk in emerging markets. Nu Skin's experience in China—the 1998 ban, the eight-year wilderness, the 2006 license, the 2014 crackdown, the 2019 "100 Days" campaign—reads like a textbook on how governments in developing economies can upend foreign business models overnight. The company navigated these crises better than most, demonstrating genuine process power in government relations and regulatory compliance. But the central insight is that regulatory risk in markets like China is not a tail risk that can be modeled and hedged. It is a permanent feature of the operating environment that must be priced into every investment decision.

The transformation question—when to defend an existing model versus pivoting to something new—is one Nu Skin has answered in real time. The Velocity plan, the digital tools, the device strategy, and the social commerce rebranding all represent genuine attempts to evolve. But the financial trajectory since 2021 suggests the transformation may have come too late, or may not have been radical enough. The affiliate base is shrinking faster than digital tools can compensate, and the Prysm iO device—while genuinely innovative—must sell through the same declining network of affiliates.

The cash generation lesson is particularly relevant for mature MLM businesses. Even as revenue has declined significantly, Nu Skin continues to generate positive cash flow from operations in most years, maintains a dividend (albeit reduced), and recently deleveraged using the Mavely sale proceeds. For a certain type of value investor, the question is whether the stock price—at roughly one-quarter of trailing revenue—adequately compensates for the risks. The company is not going to zero; it has real products, real revenue, and improving margins. Whether it can stabilize is the billion-dollar question.

Capital allocation decisions tell their own story. The aggressive share buybacks during the peak years—when the stock was high and China growth seemed infinite—look painful in hindsight. The dividend cuts signal financial pragmatism but erode the income investor base. The Mavely acquisition and sale—buying at $50 million and selling at $250 million—was actually a shrewd trade that demonstrated management's ability to create value outside the core MLM model. The question is whether that opportunism can be repeated.

XV. Bear vs. Bull Case & Investment Considerations

The bull case for Nu Skin rests on several pillars. The Prysm iO device represents a genuinely differentiated product that combines proprietary biometric data, AI-powered personalization, and a razor-and-blade consumable model. If the 100,000-device deployment target for 2026 is achieved and each device drives recurring supplement subscriptions, it could stabilize or reverse the revenue decline. Gross margins improving to over seventy percent suggest the product mix is shifting toward higher-value offerings. The India market entry, if executed through the digital-first Infosys partnership, could provide the first major new market in years. The stock trades at a fraction of revenue with a market cap of $350 million for a business generating $1.5 billion in sales—if the decline stabilizes, the valuation multiple expansion could be significant. And the Mavely sale demonstrated management's willingness to make pragmatic capital allocation decisions.

The bear case is equally compelling. The affiliate base has declined by more than fifty percent in four years, and there is no evidence that the decline has bottomed. Every region is contracting simultaneously—this is not a single-market problem but a global structural issue. The MLM model faces generational headwinds as younger demographics gravitate toward creator economy platforms, DTC brands, and social commerce models that offer "direct" relationships without multi-level compensation structures. Regulatory risk remains ever-present: one People's Daily article or FTC enforcement action could devastate the stock again. The company posted a net loss of $146.6 million in 2024. And the competition for consumer attention and wallet share in beauty and wellness has never been more intense—TikTok Shop, Amazon, Sephora, and hundreds of DTC brands all compete for the same consumer dollars without the overhead of maintaining a multi-level distributor network.

The competitive moat analysis reinforces the bear case more than the bull. Porter's framework reveals intense rivalry, very high substitution threat, and powerful buyer alternatives. Helmer's Seven Powers framework identifies only moderate process power and weak-to-moderate network effects as defensible advantages. The Prysm iO biometric database could become a cornered resource, and the device ecosystem could create switching costs, but these remain speculative rather than proven. Nu Skin competes against Amway at four to five times its size, Herbalife at three times its size, and traditional beauty conglomerates at fifty times its size—scale is not on its side.

The three KPIs that matter most for tracking Nu Skin's trajectory are: first, active paid affiliates and sales leaders—this is the leading indicator that drives everything else, and its stabilization or continued decline will determine whether the company has a growth story or a managed decline story. Second, revenue per affiliate—if the total affiliate base is shrinking, the only way to maintain revenue is to make each remaining affiliate more productive, which means tracking whether Prysm iO, devices, and subscriptions are actually increasing per-capita output. Third, customer-to-affiliate ratio—a rising ratio means more genuine retail customers relative to the sales force, which addresses the FTC's core concern about whether revenue comes from actual consumer demand or from affiliate self-consumption and recruitment.

XVI. Epilogue: What Does the Future Hold?

The existential question facing Nu Skin is not really about Nu Skin at all. It is about whether the multi-level marketing distribution model can survive in an age where every smartphone owner is a potential direct seller, every social media account is a potential storefront, and every creator with a thousand followers can launch a competing product line overnight. The MLM model was revolutionary in the 1960s because it solved a distribution problem: how do you get products to consumers in an era before e-commerce, before social media, before the internet? The answer was human networks. But what happens when technology solves that distribution problem more efficiently, at lower cost, and without the controversial compensation structure?

Nu Skin's answer—transform into a beauty tech and wellness device company distributed through a social commerce platform—is the most ambitious attempt any MLM has made to evolve. The Prysm iO device, with its AI-powered biometric analysis and personalized wellness recommendations, genuinely represents a product that would be difficult for a traditional MLM to conceive and equally difficult for a DTC startup to replicate without decades of biometric data. If the device gains traction, if India opens a meaningful new market, and if the affiliate base stabilizes, Nu Skin could emerge as something genuinely new: a wellness technology company that happens to use relationship-based distribution rather than an MLM company that happens to make devices.

The alternative scenarios are less rosy. A continued affiliate decline leads to slow but steady revenue erosion, eventually making the company an acquisition target. Private equity firms have historically shown interest in MLM businesses for their cash generation characteristics—the distribution network can be maintained with declining investment while squeezing out cash flows. A strategic acquirer in beauty or wellness—someone who wants the device technology, the Pharmanex brand, or the Asian distribution infrastructure—could find value in the pieces even if the whole is struggling.

The beauty tech convergence offers a genuine tailwind. AI-powered skin analysis, personalized product recommendations, connected devices that monitor health metrics in real time—these are real trends backed by real consumer demand. Nu Skin's bet that the future of beauty and wellness lies in technology-enabled personalization rather than commodity products is directionally correct, even if the execution through an MLM distribution model remains unproven.

What makes Nu Skin's story worth studying is not whether it succeeds or fails—it is what the attempt reveals about business model adaptation under pressure. Here is a company that has survived a Chinese government ban, a Chinese government investigation, an FCPA scandal, a $47 million class-action settlement, a pandemic, and a ninety-five percent stock price decline from its peak—and it is still standing, still generating over a billion dollars in revenue, still trying to reinvent itself. Whether that persistence represents admirable resilience or the denial stage of a dying business model is the question that makes Nu Skin one of the most fascinating case studies in modern business history.

XVII. Further Reading & Resources

FTC Business Guidance on Multi-Level Marketing — The regulatory framework that defines legal boundaries for the entire industry (ftc.gov)

"Multi-Level Marketing Unmasked" by Jon M. Taylor — The most comprehensive academic critique of MLM economics and participant income distributions

Nu Skin 10-K Annual Reports (2014, 2017, 2020, 2024) — The primary source documents tracing the China crisis, transformation strategy, and recent financial trajectory (investor.nuskin.com)

"The Dream" Podcast by Jane Marie — An accessible and deeply reported investigation into the MLM industry's promises and realities

"Direct Selling in China: The Revolution of Distribution" — Academic research on the unique regulatory and cultural dynamics of direct selling in China's market

WSJ and Bloomberg coverage of the 2014 China crisis — Real-time financial journalism capturing the People's Daily bombshell and its market impact

Beauty Tech Reports from CB Insights and Euromonitor — Industry analysis on the convergence of technology and beauty that underpins Nu Skin's device strategy

Social Commerce Market Analysis from McKinsey and Bain — Framework for understanding whether "social commerce" is a meaningful category or a rebranding exercise

Ritch Wood and Ryan Napierski investor presentations — Management's own articulation of the transformation strategy, available through the company's investor relations site and YouTube

Direct Selling Association industry statistics (dsa.org) — Aggregate data on the direct selling industry's size, participant demographics, and growth trends that provide context for Nu Skin's position within the broader ecosystem

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube