Natera: The Cell-Free DNA Testing Revolution

I. Introduction & Episode Roadmap

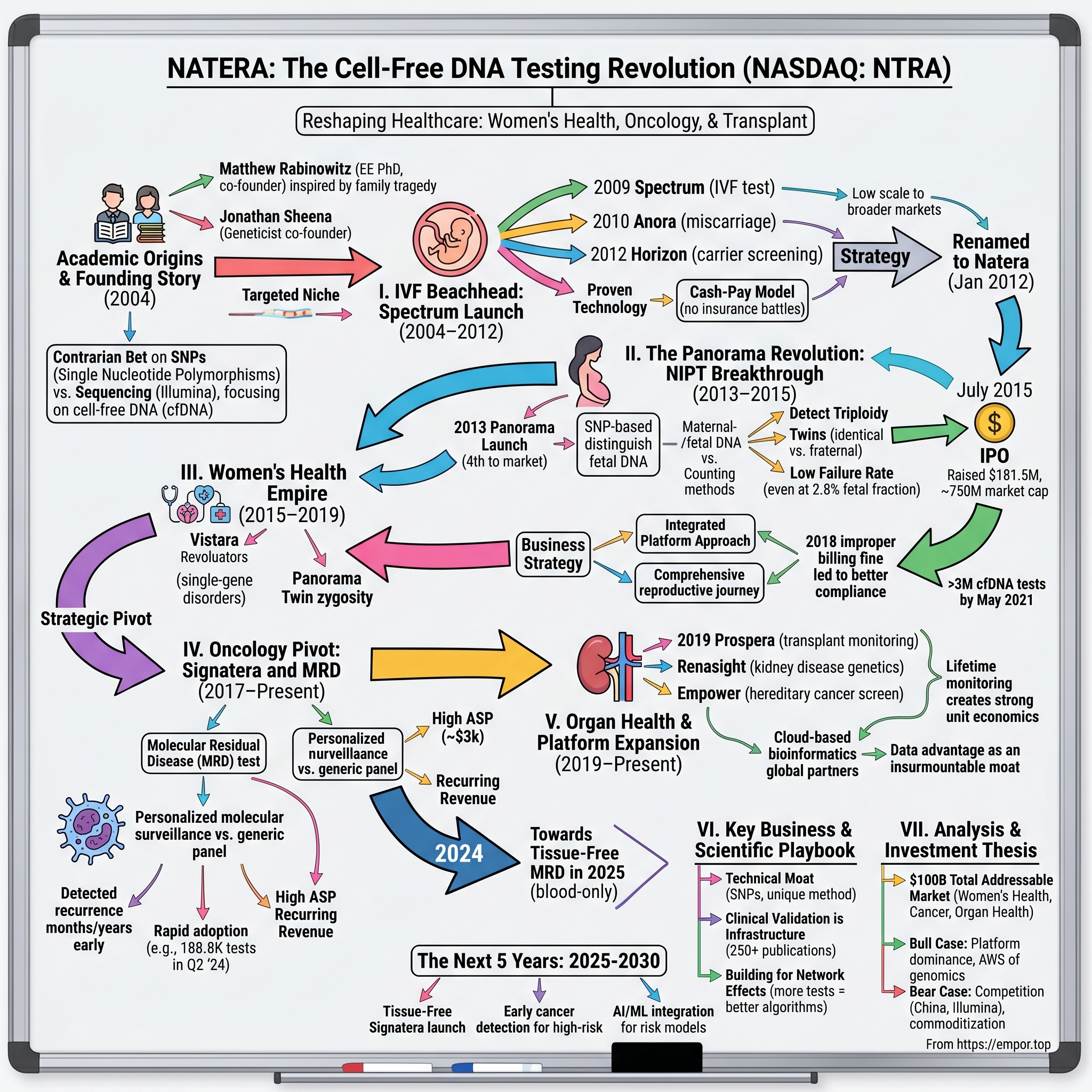

Picture this: A pregnant woman in 2010 faces an agonizing choice. Her doctor recommends amniocentesis to check for chromosomal abnormalities, but the procedure carries a 1-in-200 risk of miscarriage. She must literally risk her pregnancy to learn about her baby's health. Fast forward to today—that same woman can get more accurate results from a simple blood draw at 9 weeks, no needles near the baby, no risk whatsoever. This transformation didn't happen by accident. It happened because two Stanford PhDs saw the future of medicine written in fragments of DNA floating in our blood. Today, Natera (NASDAQ: NTRA) stands as a $22.8 billion genomics powerhouse, having transformed from a Stanford-born startup into one of the most innovative companies in genetic testing. But to understand how two PhDs turned fragments of DNA floating in blood into a diagnostic revolution, we need to go back to the beginning—to 2004, when the Human Genome Project had just been completed and the promise of personalized medicine was still mostly theoretical.

This is the story of how Matthew Rabinowitz and Jonathan Sheena built not just a prenatal testing company, but a platform that would reshape three massive healthcare markets: women's health, oncology, and organ transplantation. It's a tale of scientific breakthroughs, near-death corporate experiences, brutal competition with giants like Illumina, and ultimately, the creation of what may be the most sophisticated cell-free DNA testing platform ever built.

What makes Natera's journey particularly compelling isn't just the technology—though their SNP-based approach would prove revolutionary—but how they systematically conquered market after market, starting with the smallest niche (IVF) and expanding to tackle some of medicine's hardest problems. Along the way, they'd face regulatory battles, reimbursement wars, and competition from companies with 100 times their resources. Yet somehow, they not only survived but thrived.

The numbers tell part of the story: from zero revenue in 2009 to projecting nearly $2 billion in 2025. The science tells another part: over 250 peer-reviewed publications validating their technology. But the real story—the one we'll unpack over the next several hours—is about timing, persistence, and the power of platform thinking in healthcare.

We'll explore how Natera's early bet on SNPs over sequencing gave them a technological moat that competitors still struggle to match. We'll examine their brilliant go-to-market strategy of starting with IVF clinics before attacking the broader prenatal market. We'll dive deep into their audacious pivot into oncology with Signatera, which now generates nearly half their revenue. And we'll analyze what their future might hold as they push into early cancer detection and international markets.

This isn't just a business story—it's a masterclass in how to build a platform company in the most regulated, complex market on earth: human health. So let's start where all great company stories begin: with the founders, their motivations, and the problem they couldn't stop thinking about.

II. Founding Story & Academic Origins

The rain was coming down hard in Johannesburg that December evening in 2003 when Matthew Rabinowitz got the call. His sister had just given birth, but something was wrong. The baby had Down syndrome—a condition the prenatal screening tests had completely missed. Six days later, the child died. The family was devastated, blindsided by a medical system that had failed them at the most critical moment.

Matthew Rabinowitz's sister gave birth to a child with Down syndrome, who died six days later. The family was devastated--and entirely blindsided, as the screening tests available at the time had missed the baby's condition. For Rabinowitz, who had already co-founded and sold an online merchandising company for $100 million, this wasn't just a family tragedy—it was a calling. "There were inventions to be made in the area of biology," he says. "It was so much more meaningful than what I had been doing."

Natera (previously Gene Security Network) was founded by Matthew Rabinowitz and Jonathan Sheena in 2004. But this wasn't your typical Silicon Valley garage startup story. Rabinowitz brought a unique combination of credentials: a PhD in Electrical Engineering from Stanford, where he'd won both the Levin and Terman awards (the top academic honors in physics and engineering), and experience building and selling a tech company. He'd been serving as a consulting professor at Stanford's Department of Aeronautics and Astronautics since 2004, but genetics had captured his imagination.

Jonathan Sheena's path to Natera was equally unconventional. Jonathan Sheena joined Matt around 2004. He was finishing up a startup in the mobile space, and was tired of making phones beep and wanted to do something with more social value. As a molecular geneticist with deep technical expertise, Sheena would become the technical counterbalance to Rabinowitz's vision and business acumen.

The timing couldn't have been more perfect—or more challenging. The Human Genome Project had just been completed in 2003, opening unprecedented possibilities in genetic medicine. But the tools were primitive, the costs were astronomical, and the medical establishment was skeptical. Prenatal testing in 2004 meant either unreliable blood marker screening or invasive procedures like amniocentesis that carried real risks to the pregnancy.

Rabinowitz and Sheena saw an opportunity hidden in emerging science: cell-free DNA (cfDNA), tiny fragments of genetic material that float freely in the bloodstream. Scientists had discovered that during pregnancy, fragments of the baby's DNA circulate in the mother's blood. If you could isolate and analyze these fragments, you could learn about the baby's genetic health without ever touching the fetus. The concept was elegant. The execution would be brutally difficult.

Natera's proprietary technology combines novel molecular biology techniques with a suite of bioinformatics software that allows detection down to a single molecule in a tube of blood. This wasn't just about better testing—it was about completely reimagining how genetic information could be extracted and analyzed. While others were racing to sequence everything, Rabinowitz and Sheena made a contrarian bet: focus on single nucleotide polymorphisms (SNPs), the tiny variations that make each person's DNA unique.

The SNP approach was controversial. The sequencing giants like Illumina were pouring billions into next-generation sequencing platforms. Venture capitalists were skeptical of a approach that seemed to swim against the tide. But Rabinowitz and Sheena believed SNPs offered something sequencing couldn't: the ability to distinguish between maternal and fetal DNA with extraordinary precision, even when the fetal fraction was tiny.

Building the initial technology required assembling a team of world-class scientists, many poached from academia and big pharma. They needed molecular biologists who understood DNA at the deepest level, bioinformaticians who could build algorithms to parse genetic signals from noise, and clinicians who understood what doctors actually needed. The early team worked out of a small lab in San Carlos, California, often pulling 18-hour days to perfect their assays.

The funding landscape was brutal. This was 2004-2008, before the biotech boom, when most VCs wouldn't touch diagnostic companies. Hardware and software were sexy; blood tests were not. Rabinowitz and Sheena scraped together angel funding, maxed out credit cards, and convinced early believers to bet on their vision. Every dollar was precious, every hire critical.

By 2008, they had a working prototype and a crucial decision to make: where to launch first? The obvious market was general prenatal screening—millions of pregnant women who wanted to know if their babies were healthy. But that market was dominated by established players with deep pockets and entrenched relationships.

Instead, they made a brilliant strategic pivot: start with IVF.

III. The IVF Beachhead: Spectrum Launch (2004–2012)

Picture a couple sitting in a fertility clinic waiting room in 2008. They've already spent $30,000 on IVF treatments, endured months of hormone injections, and faced the emotional roller coaster of failed attempts. Now they have three viable embryos, and the doctor asks: "Which one should we transfer?" It's a question with no good answer—until Natera arrived.

Natera launched its first product, the Spectrum preimplantation genetic test, in 2009. This wasn't the prenatal testing revolution Rabinowitz had originally envisioned, but it was something arguably more clever: a perfect entry point into the broader genetic testing market. IVF clinics were sophisticated early adopters, desperate for better tools, and willing to pay cash upfront. No insurance hassles, no reimbursement battles—just pure product-market fit.

The Spectrum test could analyze a few cells from an embryo and determine which ones were chromosomally normal, dramatically improving IVF success rates. For clinics, this meant better outcomes and happier patients. For couples, it meant fewer failed transfers, fewer miscarriages, and higher chances of a healthy baby. The value proposition was crystal clear.

But Natera didn't stop there. In 2010, the company introduced the Anora miscarriage (POC) test. This addressed another painful reality of reproduction: roughly 15% of known pregnancies end in miscarriage, and most couples never learn why. Anora could analyze tissue from a miscarriage and identify chromosomal abnormalities, providing closure and informing future pregnancy attempts. It was another cash-pay market where emotional value translated directly into willingness to pay.

The IVF strategy was working, but it was also training wheels for something bigger. Every test they ran, every sample they processed, every algorithm they refined was building toward their ultimate goal: transforming prenatal care for all pregnant women. Natera's advanced carrier screening test, Horizon, launched in 2012. This test could identify whether prospective parents carried genetic mutations for conditions like cystic fibrosis or spinal muscular atrophy—critical information for family planning.

By this point, Natera had processed tens of thousands of samples and built something invaluable: a reputation. Fertility doctors, who are often the most demanding and sophisticated users of genetic testing, trusted them. The company had also refined its laboratory operations, building the infrastructure to handle complex samples at scale while maintaining accuracy rates that put competitors to shame.

The business model in the IVF market was elegant in its simplicity. Clinics would charge patients directly, often bundling genetic testing into their IVF packages. Natera would receive payment upfront, avoiding the byzantine world of insurance reimbursement that plagued most diagnostic companies. Average selling prices ranged from $1,500 to $4,000 per test, with gross margins north of 60%. The unit economics actually worked.

But scale was limited. The total IVF market in the U.S. was perhaps 200,000 cycles annually—meaningful, but not venture-scale. Natera was generating low tens of millions in revenue by 2011, enough to prove the technology but not enough to justify the grand vision. The team knew they needed to make the leap to the broader prenatal market, where millions of pregnant women could benefit from their technology.

The name change in January 2012 from Gene Security Network to Natera signaled this ambition. "Natera" combined "natal" (birth) with "terra" (earth), suggesting both new beginnings and global reach. It was aspirational, but also practical—Gene Security Network sounded like a cybersecurity company, not a healthcare innovator.

Behind the scenes, the company was preparing for its biggest launch yet. The competition was fierce: Sequenom had launched MaterniT21 in 2011, Ariosa had Harmony, and Verinata (soon to be acquired by Illumina) had launched their test. The NIPT wars were about to begin, and Natera was late to the party. But they had a secret weapon: their SNP-based technology could do things the sequencing-based tests simply couldn't match. The question was whether being better would be enough when competitors had a two-year head start.

IV. The Panorama Revolution: NIPT Breakthrough (2013–2015)

Matthew Rabinowitz remembers being curled up in the corner of his living room in fetal position, literally shaking because they needed more venture capital and had just learned that Illumina had bought their main competitor, Verinata. He didn't know how they were going to survive. It was late 2012, and Natera was facing an existential crisis. Their competitors had already captured much of the early NIPT market, Illumina—their main supplier—was now also their competitor, and they were running out of money.

In 2013, Natera launched the Panorama non-invasive prenatal test (NIPT). They were the fourth company to market in a space where first-mover advantage seemed insurmountable. When they developed Panorama, they were actually the fourth to market. The three other companies were educating the market and setting what was important in their own terms.

But Panorama wasn't just another NIPT test—it was a fundamentally different approach to prenatal screening. While competitors used "counting" methods (essentially tallying up DNA fragments to look for extra chromosomes), Natera's SNP-based approach could actually distinguish maternal from fetal DNA. It was like the difference between counting cars in a parking lot versus reading their license plates.

This technical distinction had profound clinical implications. Panorama could detect triploidy (three copies of every chromosome), which other tests missed entirely. It could accurately screen twin pregnancies, determining not just chromosomal abnormalities but whether the twins were identical or fraternal. It had the lowest failure rate in the industry—under 1% compared to 3-5% for sequencing-based tests. And perhaps most importantly, it maintained accuracy even when fetal fraction (the percentage of fetal DNA in the mother's blood) was as low as 2.8%.

The science was compelling, but science doesn't sell itself. They had to explain why this approach was better, demonstrate it, and invest in studies that would prove it. Natera launched an aggressive clinical validation campaign, partnering with leading medical centers to run head-to-head studies against competitors. The results were stunning: Panorama had the highest published positive predictive values in the industry.

The commercial strategy was equally aggressive. While competitors focused on large hospital systems and national lab networks, Natera went directly to obstetricians' offices. They hired an army of genetic counselors who could sit with doctors, explain the technology, and handle patient questions. It was expensive—each counselor cost $100,000+ annually—but it created deep relationships that pure sales reps couldn't match.

In July 2015, Natera conducted an initial public offering of common stock at a price of $18.00 per share. The IPO raised $181.5 million, valuing the company at roughly $750 million. It wasn't a blockbuster debut—the stock traded flat for months—but it provided the capital to fight the NIPT wars.

The market dynamics were brutal. Sequenom was imploding in a patent and accounting scandal. Ariosa was locked in patent litigation. Illumina was leveraging its sequencing dominance to bundle tests. And new entrants kept appearing, each claiming to be cheaper, faster, or better. Average selling prices were collapsing from $2,500 to under $1,000 as competition intensified.

Yet Natera kept gaining share. By the end of 2015, Panorama had captured approximately 15% of the U.S. NIPT market despite being last to launch. The key was their focus on the hardest cases—twin pregnancies, IVF pregnancies, cases with low fetal fraction—where their technology truly shined. These complex cases commanded premium prices and created passionate physician advocates.

The international opportunity was even more intriguing. While the U.S. market was becoming saturated, NIPT adoption in Europe, Asia, and Latin America was just beginning. Natera struck distribution deals in over 30 countries, leveraging partners' local relationships while maintaining control of the technology. The global footprint would prove crucial for long-term growth.

But perhaps the most important development in this period wasn't commercial—it was strategic. In 2017, Natera launched the Vistara single-gene NIPT. This test could detect conditions like Noonan syndrome and skeletal dysplasias that affected 1 in 600 pregnancies but were invisible to standard NIPT. It was a glimpse of where Natera was heading: not just chromosomal testing, but comprehensive genetic health assessment.

The NIPT wars had established Natera as a legitimate player in prenatal testing, generating over $200 million in annual revenue by 2016. But management knew that prenatal testing alone wouldn't build a $20 billion company. They needed to leverage their platform into new markets—and they had already begun laying the groundwork for their most ambitious pivot yet.

V. Building the Women's Health Empire (2015–2019)

The Post-IPO era began with Natera at a crossroads. Public markets demanded growth, but the NIPT market was rapidly commoditizing. The company's answer was to double down on what made them unique: their ability to handle the complex cases that others couldn't or wouldn't touch.

In 2017, Natera launched the Vistara single-gene NIPT, a test that could detect single-gene disorders like Noonan syndrome—conditions that affect 1 in 600 pregnancies but were completely missed by standard NIPT. This wasn't a large market, but it sent a powerful message: Natera was the technology leader, the company that could solve the hardest problems.

That same year came another breakthrough: Panorama expansion to twin pregnancies with zygosity determination. Twin pregnancies represented only 3% of all pregnancies but 10% of prenatal testing complexity. No other NIPT could reliably determine whether twins were identical or fraternal—critical information for pregnancy management. Natera owned this niche, commanding premium prices and earning fierce loyalty from maternal-fetal medicine specialists.

But building an empire requires more than just technology—it requires distribution, and that meant wrestling with America's byzantine healthcare reimbursement system. Every insurance company had different policies, different forms, different approval processes. Natera built a 200-person reimbursement team whose sole job was navigating this maze, fighting denials, and securing coverage. It was grinding, unglamorous work, but it was the difference between a $300 reimbursement and a $1,500 one.

The strategy was working. Revenue grew from $186 million in 2016 to $302 million in 2018. But success attracted scrutiny. In 2018 Natera paid a $11 million fine over allegations of improper billing to federal healthcare services. The fine stemmed from billing practices between 2013 and 2015, when the company was still learning the complexities of government reimbursement. It was a painful lesson, but one that forced Natera to build world-class compliance infrastructure.

The real innovation during this period wasn't in new products but in integration. Natera built a comprehensive women's health platform where a single patient might use multiple tests throughout their reproductive journey: Horizon carrier screening before pregnancy, Panorama during pregnancy, Anora if they miscarried, Spectrum if they pursued IVF. Each test generated data that made the next test better. It was a flywheel that competitors, focused on individual products, couldn't replicate.

The numbers told the story of increasing dominance. As of May 2021, Natera has performed over 3 million cell-free DNA tests. They had become trusted by one in three OB-GYNs in America. Their Net Promoter Score—a measure of customer satisfaction—was over 70, extraordinarily high for a diagnostic company. Physicians weren't just using Natera; they were evangelizing it.

The international expansion accelerated during this period. While U.S. growth was slowing to 15-20% annually, international markets were exploding at 50%+ rates. Natera's strategy was clever: partner with local distributors for commercial presence, but maintain control of sample processing in their U.S. labs. This kept quality high and margins healthy while minimizing capital investment.

The laboratory infrastructure had become a competitive advantage in itself. Natera operates CAP-accredited laboratories certified under CLIA in San Carlos, California and Austin, Texas. These weren't just testing facilities; they were technology platforms capable of processing hundreds of thousands of samples monthly with industry-leading turnaround times and accuracy rates.

By 2019, Natera had built the dominant franchise in high-complexity women's health genetic testing. Revenue reached $336 million, with gross margins expanding to 45%. The company was processing over 500,000 tests annually. But the biggest development was happening quietly in their research labs: a technology that could detect cancer DNA in blood with unprecedented sensitivity. The oncology pivot was about to begin.

VI. The Oncology Pivot: Signatera and MRD (2017–Present)

The conference room at MD Anderson Cancer Center was silent as the oncologist reviewed the data. A colorectal cancer patient, supposedly cured after surgery, showed no signs of disease on imaging. But Natera's experimental blood test had detected something: circulating tumor DNA, invisible to scans but harbinger of recurrence. Six months later, the imaging caught up. The cancer was back, exactly as the test predicted.

In 2017, Natera introduced the Signatera molecular residual disease test for research use only. This wasn't just another liquid biopsy—it was a personalized molecular surveillance system. While competitors looked for generic cancer mutations in blood, Signatera created a custom test for each patient, tracking the exact mutations from their specific tumor. It was like having a molecular fingerprint of someone's cancer, searchable in a single tube of blood.

The technology leveraged everything Natera had learned from prenatal testing. Detecting fetal DNA at 2% concentration in maternal blood had prepared them for finding tumor DNA at 0.01% concentration in cancer patients. The bioinformatics platforms built for distinguishing maternal from fetal DNA could be repurposed to distinguish tumor from normal DNA. The operational excellence required to deliver prenatal results in 5-7 days translated directly to cancer testing timelines.

The Signatera CLIA test was introduced for clinical use in 2019. The clinical validation data was extraordinary: 94% sensitivity for detecting molecular residual disease with virtually 100% specificity across multiple cancer types. Signatera has been clinically validated to detect colorectal cancer recurrence up to 16.5 months in advance of radiologic imaging and early-stage breast cancer up to two years earlier than imaging.

The market opportunity was massive but complex. Unlike prenatal testing, where the use case was clear, MRD testing required educating oncologists about an entirely new paradigm. Instead of waiting for tumors to grow large enough to see on scans, doctors could detect molecular recurrence when intervention was most effective. It meant transforming cancer from a disease we react to into one we anticipate.

Natera's go-to-market strategy in oncology was distinctly different from women's health. Instead of building a massive sales force, they focused on key opinion leaders at major cancer centers. They funded investigator-initiated studies, letting prestigious institutions validate the technology independently. By 2024, over 100 peer-reviewed studies had been published on Signatera, creating an evidence fortress that competitors struggled to match.

The reimbursement landscape in oncology was surprisingly favorable. Medicare, which covers most cancer patients, was eager for technologies that could reduce costs by catching recurrence early. In 2020, Signatera received final Medicare coverage in stage II-III colorectal cancer and draft coverage in immunotherapy response monitoring. Private payers followed Medicare's lead, establishing coverage for colorectal, breast, bladder, and ovarian cancers.

The business model transformation was remarkable. In Q2 2024, Natera performed 188,800 oncology tests, representing 50.6% year-over-year growth. Oncology ASPs (average selling prices) were roughly $3,000 per test, three times higher than prenatal testing. And unlike prenatal testing, which was typically one-and-done, cancer patients needed quarterly monitoring for years—a recurring revenue stream worth $12,000+ per patient annually.

The competitive landscape in liquid biopsy was fierce but fragmented. GRAIL, backed by Illumina's billions, was focused on early detection rather than monitoring. Guardant Health had a strong presence but used a generic panel approach rather than personalized testing. Foundation Medicine (owned by Roche) dominated tissue testing but was late to liquid biopsy. Natera's personalized approach and superior sensitivity gave them a unique position.

The most exciting development came in 2024-2025: tissue-free MRD capability. Traditionally, Signatera required tumor tissue to design the personalized test. But Natera developed technology to create personalized panels using only blood, eliminating the need for invasive biopsies. This would launch in mid-2025 for colorectal cancer, dramatically expanding the addressable market.

The Signatera story validated Natera's platform thesis: the same core technology that detected fetal abnormalities could be repurposed for cancer, organ transplants, and potentially any condition involving cell-free DNA. By 2024, oncology represented nearly 40% of Natera's revenue and was growing twice as fast as women's health. The company that started with IVF testing was becoming a cancer diagnostics powerhouse.

VII. Organ Health & Platform Expansion (2019–Present)

Dr. Sarah Chen was reviewing her kidney transplant patient's results when she noticed something unusual. Traditional markers showed the kidney functioning normally, but Natera's Prospera test had detected elevated donor-derived cell-free DNA—a molecular SOS from the transplanted organ. She adjusted the immunosuppression immediately. Two weeks later, when a biopsy confirmed early rejection, the intervention had already stopped it. The kidney was saved.

Natera launched the Prospera transplant assessment test in 2019. This wasn't just another product launch—it was validation of Natera's platform hypothesis. The same technology tracking fetal DNA in pregnant women and tumor DNA in cancer patients could monitor organ health in transplant recipients. The Prospera test is the first assay with high sensitivity to both T-cell-mediated and antibody-mediated rejection. In December 2019, the test received final Medicare coverage.

The transplant monitoring market was smaller than prenatal or oncology—roughly 40,000 organ transplants annually in the U.S.—but it was a perfect fit for Natera's capabilities. Transplant patients needed frequent monitoring for life, creating recurring revenue streams. The tests commanded premium prices ($3,000+), and nephrologists were sophisticated early adopters eager for better tools.

But organ health was just the beginning of Natera's platform expansion. In 2020, Natera launched Renasight, a test to determine if there is a genetic cause for kidney disease and if there may be other at-risk relatives. This moved beyond monitoring into disease causation, helping nephrologists understand why kidneys failed and whether family members were at risk.

That same year came Empower, a hereditary cancer test that screens for up to 53 genes associated with increased risk for common hereditary cancers. This might seem like a departure from Natera's cell-free DNA focus, but it was strategically brilliant. The same physicians ordering Panorama prenatal tests were counseling patients about hereditary cancer risk. The same genetic counselors supporting NIPT were explaining BRCA results. It was platform leverage at its finest.

The real magic was in the integration. Natera offers Constellation, a cloud-based bioinformatics platform allowing laboratories to access Natera's technology in their own facilities. This wasn't just software—it was Natera's entire analytical engine, available to partners worldwide. International laboratories could offer Natera-powered tests without shipping samples to California, dramatically expanding the company's global reach.

The data advantage was becoming insurmountable. Every test Natera ran—whether prenatal, cancer, or transplant—generated genomic data that improved their algorithms. By 2024, they had one of the largest clinical genomics databases in the world, with millions of samples and outcomes. This data moat was impossible for new entrants to replicate and gave Natera increasing accuracy advantages over time.

Platform synergies were everywhere. The operational infrastructure built for prenatal testing—sample logistics, lab automation, report generation—scaled across all products with minimal incremental cost. The commercial relationships with health systems opened doors for new products. The reimbursement expertise transferred across markets. Every new product made the platform stronger.

The financial impact was profound. Platform products (organ health, hereditary cancer, carrier screening) generated over $200 million in 2024 revenue with gross margins exceeding 65%. More importantly, they deepened Natera's relationships with health systems. A hospital using Natera for prenatal, cancer, and transplant testing was unlikely to switch vendors—the integration was too valuable.

The international opportunity for platform products was particularly intriguing. While NIPT faced local competition in many markets, Natera's specialized tests like Prospera and Signatera had no real alternatives. International distributors who started with Panorama inevitably expanded to the full portfolio, driving higher revenues per partner.

By 2024, Natera had transformed from a prenatal testing company into a comprehensive precision medicine platform. They processed over 3 million tests annually across dozens of indications. The platform strategy that seemed risky in 2015 had become their greatest competitive advantage—a fully integrated ecosystem that competitors couldn't match piece by piece.

VIII. Financial Performance & Business Model Evolution

The numbers were staggering: $1.7 billion in revenue for 2024, up 56.7% from 2023. For context, that's more revenue than Illumina generated in its first 15 years as a public company. But the real story wasn't just growth—it was the complete transformation of Natera's business model from a cash-burning startup to a profitable platform.

The gross margin evolution told the story of operational excellence. From 45.5% in 2023 to 60.3% in 2024, Natera had crossed the critical 60% threshold that separates great diagnostic companies from mediocre ones. This wasn't just about raising prices—it was about ruthless efficiency. Automation reduced labor costs by 30%. Proprietary chemistries cut reagent expenses in half. Scale negotiations with suppliers drove down materials costs. Every basis point was fought for and won.

As of March 3, 2025, Natera has a market capitalization of $19.35B. The market was valuing Natera at roughly 11x forward revenue, a premium multiple reflecting both growth and platform potential. For comparison, traditional diagnostic companies like Quest and LabCorp traded at 1-2x revenue. The market understood: Natera wasn't just another lab—it was a technology platform.

The test volume story was equally impressive: 3.06 million tests processed in 2024, up from virtually zero in 2009. But volume alone didn't drive value—mix did. Oncology tests, at $3,000+ ASPs, were growing at 50%+ annually. Women's health, while mature, maintained $800-1,000 ASPs through complexity focus. Organ health commanded premium pricing with 70%+ gross margins. The portfolio approach meant Natera could optimize for value, not just volume.

The path to profitability had been long and painful. Natera burned through nearly $1 billion in cumulative losses before achieving positive cash flow in 2024. But this wasn't reckless spending—it was deliberate investment. Every dollar burned in 2015 to build lab capacity enabled 2024's margins. Every genetic counselor hired in 2018 created physician relationships driving today's growth. The burns were investments, and they were finally paying off.

Reimbursement evolution was the unsung hero of the financial transformation. In 2015, Natera collected roughly 40% of billed charges. By 2024, that had risen to 65%+. This wasn't luck—it was systematic execution. Dedicated payer teams negotiated contracts with every major insurer. Prior authorization teams ensured clean claims. Appeals teams fought denials. Patient assistance programs eliminated bad debt. The reimbursement machine that took a decade to build had become a competitive moat.

The unit economics by product line revealed the platform power:

Women's Health: $800 ASP, 55% gross margin, 20% growth - Mature but stable, generating $800M+ annually - Recurring revenue from provider relationships - International expansion driving incremental growth

Oncology: $3,000 ASP, 65% gross margin, 50% growth

- Rapidly scaling, approaching $700M annually

- Recurring monitoring creates LTV of $12,000+ per patient

- Medicare coverage providing stable reimbursement

Organ Health: $2,800 ASP, 70% gross margin, 35% growth - Smaller but highly profitable, $200M+ annually - Lifetime monitoring creates exceptional unit economics - Limited competition enables premium pricing

The 2025 guidance showed confidence: $1.87-1.95 billion in revenue with sustained positive cash flow. Management was projecting 20%+ growth while maintaining profitability—a rare combination in diagnostics. The key drivers were clear: oncology volume growth, international expansion, and gross margin expansion through automation.

Capital efficiency had improved dramatically. In 2015, Natera needed $2 of investment to generate $1 of revenue. By 2024, that had flipped—every dollar invested generated $3 of revenue within 18 months. The platform was finally delivering the operating leverage investors had long awaited.

The balance sheet had also strengthened considerably. From near-bankruptcy in 2012 to over $400 million in cash by 2024, Natera had the resources to invest in R&D, expand internationally, and potentially acquire complementary technologies. The days of dilutive financing were over; the company was self-funding its growth.

IX. Innovation Roadmap & Future Vision

The prototype sitting in Natera's R&D lab in Austin looked unremarkable—just another genetic sequencer surrounded by computers. But what it represented was revolutionary: the ability to detect cancer before symptoms, before imaging, perhaps before the tumor even formed. This was Natera's moonshot, and it was closer to reality than anyone outside the company realized.

The next-generation Signatera platform launching in 2025 represented a quantum leap in capability. Using multiplex PCR combined with next-generation sequencing, the new assay could track 50 tumor mutations simultaneously with sensitivity down to 0.001% circulating tumor DNA. For context, that's finding one cancer cell's DNA among 100,000 normal cells—like identifying a specific grain of sand on a beach.

But the real breakthrough was tissue-free MRD. Signatera is the first circulating tumor DNA assay built for molecular residual disease detection and cancer recurrence monitoring. The new capability would eliminate the need for tumor tissue entirely, designing personalized cancer tests using only blood. This would expand the addressable market from post-surgical monitoring to active treatment monitoring, chemotherapy selection, and eventually, screening.

The early cancer detection ambitions were even more audacious. While GRAIL was spending billions on population-wide screening, Natera was taking a targeted approach: focus on high-risk populations where the clinical utility was clear. Start with hereditary cancer syndrome carriers, then expand to smoking populations for lung cancer, then broader screening. It was the same playbook that worked in prenatal: start narrow, prove value, then expand.

International expansion represented another massive opportunity. While Natera generated 85% of revenue in the U.S., the global genetic testing market was growing faster internationally. China alone performed 5 million NIPT tests annually. Europe was adopting cell-free DNA testing for cancer monitoring. The Middle East was investing heavily in precision medicine. Natera's strategy was partnerships rather than direct investment, leveraging local expertise while maintaining technology control.

The AI and machine learning applications were perhaps most exciting. With millions of samples and outcomes, Natera had one of the richest genomic datasets in existence. Machine learning models could predict which IVF embryos would successfully implant. AI could identify cancer recurrence patterns invisible to human analysis. Deep learning could discover new biomarkers in cell-free DNA. The data was becoming as valuable as the tests themselves.

Platform extensibility into new disease areas was accelerating. Neurological disorders, autoimmune conditions, infectious diseases—anywhere cell-free DNA provided information, Natera could potentially play. The company was exploring Alzheimer's detection through neural cell-free DNA, liver disease monitoring through hepatocyte DNA, and even prenatal detection of autism risk factors. Each application leveraged the same core platform, spreading R&D costs across multiple markets.

The competitive landscape was evolving but fragmented. Illumina's GRAIL spinout removed a major threat. Guardant remained focused on late-stage cancer. Exact Sciences was strong in colorectal but weak in liquid biopsy. Chinese competitors like BGI and Berry Genomics dominated their local markets but struggled internationally. No one else had Natera's breadth—spanning prenatal to cancer to organs—or their depth in cell-free DNA.

The technology roadmap for 2025-2030 was ambitious:

- Launch tissue-free Signatera across all major cancer types

- Introduce multi-cancer early detection for high-risk populations

- Develop cell-free RNA testing for real-time disease monitoring

- Create integrated software platforms for clinical decision support

- Build AI-powered risk prediction models across all disease areas

The vision was becoming clear: Natera wasn't just building better tests—they were creating an early warning system for human health. A world where disease was detected at the molecular level, where treatment was personalized to each patient's genetics, where prevention replaced reaction. It was the promise that started with prenatal testing but extended to the entire human condition.

X. Playbook: Key Business & Scientific Lessons

Studying Natera's journey reveals a masterclass in building platform companies in regulated markets. The lessons aren't just about science or business—they're about the intersection where breakthrough technology meets market reality.

The Power of Proprietary Technology Platforms

Natera's SNP-based approach seemed like a disadvantage when everyone else was using sequencing. But proprietary technology created defensibility that me-too approaches never could. The lesson: in diagnostics, being different is more valuable than being first. Your technology must do something competitors structurally cannot match, not just cannot match today.

Clinical Validation as Competitive Moat

Natera's tests are validated by more than 250 peer-reviewed publications that demonstrate high accuracy. This wasn't vanity publishing—it was strategic moat-building. Every study made switching costs higher for physicians. Every publication made regulatory approval easier. Every validation made payer coverage more likely. The lesson: in healthcare, evidence isn't just marketing—it's infrastructure.

Building in Regulated Markets

Natera operates ISO 13485-certified and CAP-accredited laboratories certified under CLIA in Austin, Texas, and San Carlos, California. These certifications weren't bureaucratic checkboxes—they were table stakes for credibility. But Natera went further, building quality systems that exceeded requirements. When FDA began regulating laboratory-developed tests, Natera was ready. The lesson: regulate yourself harder than regulators ever will.

Network Effects in Diagnostics

Every test Natera ran made the next test better. More data improved algorithms. More volume reduced costs. More physicians created referrals. More payers established coverage. This wasn't the instant network effects of software—it was slow, grinding, compound network effects. The lesson: in healthcare, network effects take years to build but decades to disrupt.

The Recurring Revenue Model

Prenatal testing seemed like a one-time transaction business. But Natera discovered recurrence everywhere: IVF patients with multiple cycles, cancer patients needing quarterly monitoring, transplant patients requiring lifetime surveillance. The lesson: in diagnostics, find the chronic conditions where monitoring creates subscription-like revenue.

Capital Efficiency vs. Growth Trade-offs

Natera burned $1 billion before profitability, but every dollar was strategic. Sales force investment in 2016 drove 2020 revenue. Lab capacity in 2018 enabled 2024 margins. R&D in oncology while prenatal was growing created today's diversification. The lesson: in platform businesses, burn isn't waste if it's building infrastructure that compounds.

Managing Multiple Stakeholders

Natera had to satisfy patients (who wanted accuracy), physicians (who wanted reliability), and payers (who wanted value). Most companies optimize for one stakeholder. Natera built systems to serve all three simultaneously. Genetic counselors helped patients. Medical affairs supported physicians. Health economics teams convinced payers. The lesson: in healthcare, you're only as strong as your weakest stakeholder relationship.

The playbook patterns were clear: 1. Start with a niche market where you can dominate (IVF) 2. Use early revenue to fund platform development 3. Expand to adjacent markets leveraging the same technology 4. Build evidence through systematic clinical validation 5. Create commercial infrastructure that becomes a moat 6. Diversify revenue streams before any single market matures 7. Maintain technology leadership through continuous R&D investment

These weren't sequential steps but parallel processes. Natera was building oncology capabilities while scaling prenatal. They were automating operations while expanding commercially. They were going international while deepening U.S. penetration. The complexity was overwhelming, but it was also the barrier to competition.

XI. Analysis & Investment Thesis

The fundamental question for investors isn't whether Natera is a good company—it clearly is—but whether it's a good investment at today's valuation. Let's examine both the bull and bear cases with the rigor this $20 billion market cap demands.

TAM Expansion: The $100 Billion Opportunity

The total addressable market arithmetic is compelling. Women's health genetic testing: $10 billion globally and growing. Cancer monitoring and MRD: $15 billion and accelerating. Organ health and transplant monitoring: $2 billion. Early cancer detection: $50 billion potential. Hereditary disease screening: $5 billion. Sum it up—even conservatively—and Natera is addressing $80-100 billion in market opportunity with only 2% penetration today.

But TAM alone doesn't make an investment case. The question is Natera's ability to capture disproportionate value. Here, the platform dynamics become critical. Unlike single-product companies that face commoditization, Natera's multi-product platform creates competitive advantages that compound over time.

Competitive Moats: Deep and Widening

The technology moat starts with SNP-based testing but extends far beyond. The proprietary algorithms trained on millions of samples. The operational excellence delivering 5-day turnaround at scale. The regulatory approvals that took years to obtain. The payer contracts negotiated over a decade. The physician relationships built counselor by counselor. These aren't moats a new entrant can cross with venture capital.

The data moat may be even more valuable. Every test generates information that improves accuracy, identifies new biomarkers, and enables new products. Competitors starting today would need decades to accumulate comparable clinical evidence. And by then, Natera would be decades further ahead.

Bull Case: Platform Dominance at Inflection Point

The optimistic scenario sees Natera as the dominant cell-free DNA platform globally. Oncology growth accelerates as tissue-free Signatera launches. International expansion doubles revenue within five years. Early detection products create entirely new markets. AI-powered diagnostics command premium pricing. The company reaches $10 billion revenue by 2030 with 40% EBITDA margins, justifying a $100 billion valuation.

The platform advantages make this plausible. Every cancer patient needs monitoring. Every pregnant woman wants reassurance. Every transplant recipient requires surveillance. These aren't optional tests—they're becoming standard of care. And Natera's technology lead means they capture premium pricing in each market.

Bear Case: Competition, Commoditization, and Execution Risk

The pessimistic scenario sees multiple challenges converging. Chinese competitors enter U.S. markets with dramatically lower pricing. Illumina leverages sequencing dominance to bundle competing tests. Payers squeeze reimbursement as testing becomes routine. New technologies like proteomics or methylation make cell-free DNA obsolete. Regulatory changes disrupt the laboratory-developed test model.

Execution risk is real. Natera is attempting to simultaneously scale oncology, expand internationally, launch new products, and maintain profitability. The complexity is staggering. One major clinical failure, one regulatory setback, one competitive breakthrough could derail the growth story. And at 11x revenue, the valuation leaves little room for error.

Valuation Framework: Growth vs. Multiple Risk

At current prices, Natera trades at premium multiples across all metrics:

- 11x 2025 revenue (vs. 2-3x for traditional diagnostics)

- 50x 2025 EBITDA (vs. 15-20x for profitable medtech)

- 5x book value (vs. 2-3x for healthcare services)

The valuation implies sustained 25%+ revenue growth and expanding margins. This isn't impossible—Natera has exceeded these metrics recently—but it requires flawless execution. Any growth deceleration or margin compression would trigger multiple compression, creating downside risk even if the business performs well.

Key Metrics for Monitoring

Investors should focus on leading indicators: - Oncology test volume growth (must sustain 40%+ for bull case) - Gross margin trajectory (needs to reach 65%+ for platform economics) - International revenue mix (should exceed 25% by 2027) - R&D productivity (new product launches must accelerate revenue) - Competitive win rates (market share gains validate technology advantages) - Payer coverage expansion (reimbursement drives adoption)

The investment thesis ultimately depends on whether you believe specialized platform companies can sustain premium economics in healthcare. If yes, Natera's combination of technology leadership, market position, and platform advantages justifies the valuation. If no, the multiple risk outweighs the growth opportunity.

XII. Epilogue & "What Would We Do?"

Steve Chapman took the CEO reins in 2019 not as a revolutionary but as an operator, tasked with scaling what Rabinowitz had invented. The transition was deliberate—Rabinowitz remained Executive Chairman, staying deeply involved in technology while Chapman focused on commercialization and operations. It was a partnership that acknowledged a fundamental truth: building a company and scaling a company require different skills.

Matthew Rabinowitz served as Natera's Chief Executive Officer from 2005 to 2019. His transition to Executive Chairman wasn't a step back but a step up—to the 30,000-foot view where platform strategy and technology vision matter more than quarterly earnings calls. Meanwhile, Chapman brought the operational rigor of his time at Roche and Bio-Rad, transforming Natera from a promising startup into a scaled platform.

The Next Five Years: Three Scenarios

Scenario 1: The Platform Dominator Natera becomes the "AWS of genomics"—the infrastructure layer that powers precision medicine globally. Every hospital runs Natera tests. Every oncologist uses Signatera. Every OB relies on Panorama. The company reaches $5 billion revenue by 2030 with expanding margins, commanding a $50+ billion valuation. International expansion accelerates through partnerships. Early detection products create new categories. The platform becomes indispensable.

Scenario 2: The Focused Leader Natera doubles down on core strengths—prenatal and oncology—while carefully expanding adjacencies. Growth moderates to 15-20% but margins expand to 70%+. The company generates substantial cash flow, returning capital to shareholders while maintaining technology leadership. Valuation stabilizes at 6-8x revenue as the business matures. It's less exciting but more predictable.

Scenario 3: The Disrupted Incumbent New technologies—perhaps protein detection, methylation patterns, or AI-powered imaging—obsolete cell-free DNA testing. Chinese competitors flood markets with $100 tests. Payers revolt against high prices. Natera's growth stalls, margins compress, and the platform thesis breaks. The company remains profitable but trades at 2-3x revenue like traditional diagnostics.

What Would We Do? Strategic Priorities

If we were running Natera today, five moves would be critical:

1. Accelerate International Through M&A Buy or build local presence in China, Europe, and India. The U.S. market is maturing; international is where the next billion tests will happen. Partner where possible, acquire where necessary, but establish Natera as the global standard before regional competitors emerge.

2. Build the Data Business Natera's genomic database is incredibly valuable but undermonetized. Create a pharmaceutical services division selling biomarker discovery and clinical trial services. License anonymized data for drug development. Build AI tools for clinical decision support. The data could be worth as much as the testing business.

3. Pursue Strategic Consolidation The diagnostics industry is fragmenting while platforms are consolidating. Acquire complementary technologies—proteomics, methylation, metabolomics—that extend the platform. Buy regional competitors to accelerate expansion. Roll up specialized testing companies that add new capabilities. Use the premium valuation as currency while it lasts.

4. Develop Consumer Strategy Today's model relies entirely on physicians and payers. But consumers increasingly want direct access to genetic information. Build a consumer brand—carefully, compliantly—that provides genetic insights beyond medical necessity. The 23andMe model failed in medical genetics, but there's opportunity for medically-credible consumer offerings.

5. Prepare for AI Transformation Artificial intelligence will revolutionize diagnostics within five years. Invest aggressively in AI capabilities—not just for test interpretation but for predictive modeling, treatment selection, and outcome prediction. The companies that combine superior data with advanced AI will dominate the next era of precision medicine.

Final Reflections: Lessons for Healthcare Entrepreneurs

Natera's journey from personal tragedy to $20 billion platform offers profound lessons for anyone building in healthcare:

First, mission matters. Rabinowitz's personal connection to prenatal testing created persistence through near-bankruptcy, competitive onslaughts, and regulatory challenges. You can't fake the commitment required to build in healthcare—it has to be personal.

Second, platform thinking pays. Every successful healthcare company eventually faces commoditization. Only platforms—with network effects, data advantages, and ecosystem lock-in—sustain premium economics. Build platforms from day one, even if it takes longer.

Third, evidence wins. In healthcare, being right isn't enough—you must prove you're right, repeatedly, in peer-reviewed journals. The companies that invest in clinical validation create moats that marketing can never match.

Finally, timing remains everything. Natera launched when cell-free DNA technology was ready, when sequencing costs had dropped sufficiently, when the market was prepared for non-invasive testing. Too early and you're Theranos. Too late and you're irrelevant. The window is narrow, but the rewards for hitting it are extraordinary.

The story of Natera isn't finished. The next chapters—early detection, international expansion, AI integration—are being written now. But the foundation is set: a platform that turns blood into knowledge, transforming how we detect, monitor, and treat disease. From that painful December evening in Johannesburg to today's molecular surveillance systems, it's been an extraordinary journey. And the best parts may be yet to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube