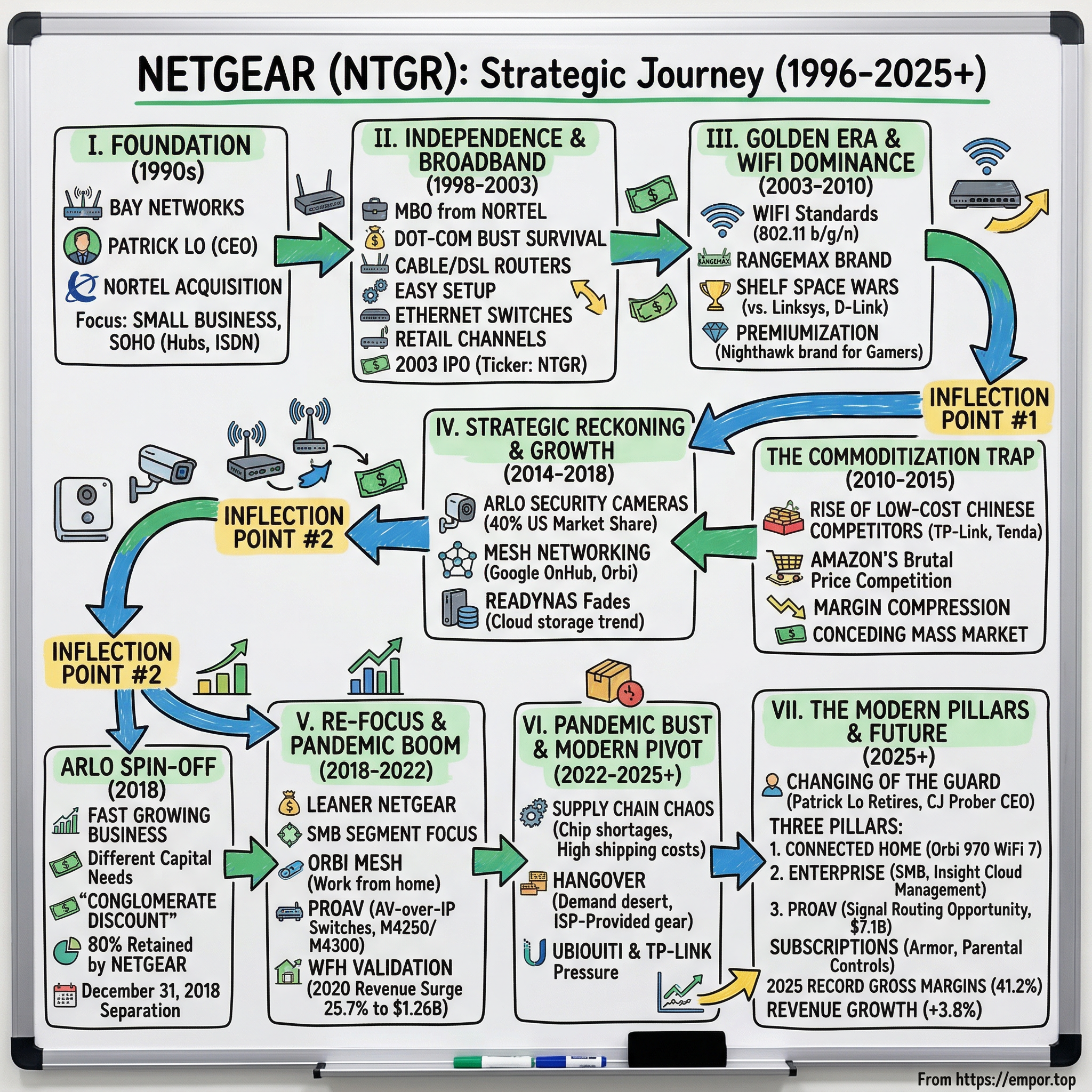

NETGEAR: From Router Pioneer to Smart Home and Network Infrastructure Player

I. Introduction & Episode Roadmap

Walk into any American home office, peer behind any small business reception desk, or glance at the shelf in a college dorm room, and chances are high you will spot a piece of NETGEAR hardware. That blocky black router with its stubby antennas. The compact unmanaged switch daisy-chaining a printer and a NAS. The sleek white Orbi mesh satellite perched on a bookshelf. For three decades, NETGEAR has been the quiet workhorse of connectivity, the brand that made networking approachable for people who had no interest in configuring VLANs or memorizing subnet masks.

But behind that ubiquity lies one of the most fascinating strategic journeys in consumer technology. NETGEAR started life as an internal project within Bay Networks, a company most people have forgotten. It survived being orphaned by Nortel, weathered the dot-com collapse, rode the broadband revolution to a successful IPO, and built a billion-dollar consumer electronics franchise during the golden age of Wi-Fi. Then it watched that franchise erode as Chinese manufacturers flooded the market with routers at half the price. It spun off its fastest-growing business, Arlo security cameras, right before the pandemic sent demand for home networking gear through the roof. It rode that wave, then crashed hard when the hangover arrived.

The central tension of the NETGEAR story is one that haunts every hardware company: how do you avoid becoming a commodity? When your product is a box that moves data packets from point A to point B, and your competitors can build that same box in Shenzhen for a fraction of the cost, what is your moat? Is it brand? Is it channel relationships? Is it moving upmarket to customers who value reliability over price? Or is it layering software and subscriptions on top of hardware to create recurring revenue?

NETGEAR has tried all of these strategies, sometimes simultaneously, sometimes sequentially, and sometimes contradictorily. The company that once generated $1.3 billion in annual revenue now operates at roughly half that level, yet it posted record gross margins in 2025 and is growing again for the first time in five years. The stock trades at a fraction of its historical highs, and the founder who ran the company for nearly three decades handed the keys to a new CEO in early 2024.

This is a story about the innovator's dilemma playing out in real time, about the agonizing choices hardware companies face when technology commoditizes faster than they can innovate, and about whether a thirty-year-old networking company can reinvent itself for an era of cloud-managed infrastructure, AI-driven security, and WiFi 7. It is also, fundamentally, a story about one man's vision for democratizing the internet and whether that vision can survive in a world where the internet has become so democratized that the hardware enabling it barely registers as a purchase decision.

The answer matters not just for NETGEAR shareholders but for anyone trying to understand how hardware companies create and sustain value in an industry that relentlessly drives toward zero margin. NETGEAR trades under the ticker NTGR on the NASDAQ, and with a market capitalization of approximately $783 million and annual revenue of roughly $700 million, it sits in a fascinating strategic no-man's-land: too large to be ignored, too small to dominate, and at a crossroads that could lead to either reinvention or slow decline.

Before diving in, a note on what makes the NETGEAR story particularly instructive. Most technology company narratives follow a familiar arc: founding, growth, dominance, disruption. NETGEAR's arc is different because the company has experienced multiple near-death moments and reinventions without ever achieving true dominance. It has always been the number two or number three player, the "other" option on the shelf, the reliable workhorse that never quite became a status symbol. And that positioning, in many ways, is both its greatest vulnerability and its most interesting strategic challenge.

II. Pre-History: Nortel, Bay Networks, and the Networking Boom (1990s)

To understand where NETGEAR came from, you need to understand the frenzy that gripped the networking industry in the mid-1990s. The internet was exploding from an academic curiosity into a commercial phenomenon, and every business in America suddenly needed to connect its computers. The companies that made the plumbing for this new digital infrastructure were printing money. Cisco Systems, founded in 1984 by a married couple at Stanford, had become the most valuable company on Earth by the late 1990s, worth more than half a trillion dollars at its peak. 3Com, founded by Ethernet inventor Bob Metcalfe, was a powerhouse in network adapters and hubs. And then there was Bay Networks.

Bay Networks was born in October 1994 from the merger of two pioneering networking companies: SynOptics Communications and Wellfleet Communications. SynOptics, based in Santa Clara, California, had been founded in 1985 by Andrew Ludwick and Ronald Schmidt, both alumni of Xerox PARC, the legendary research lab that birthed the graphical user interface, the laser printer, and Ethernet itself. SynOptics had commercialized the LattisNet product, which became a foundational technology for Ethernet hubs, the devices that connected multiple computers on a local network. Wellfleet, based in Bedford, Massachusetts, was founded in 1986 by Paul Severino and others, and had become a significant competitor to Cisco in the router market, the devices that directed traffic between networks.

The merger was supposed to create a networking superpower that could challenge Cisco across the full stack of networking equipment. Paul Severino became chairman and Andrew Ludwick became president and CEO. But the integration proved difficult. The two companies had different cultures, different product architectures, and different customer bases. By July 1996, Ludwick resigned as CEO amid slowing growth. Dave House, a twenty-two-year veteran of Intel where he had risen to senior vice president of the microprocessor division, was brought in as chairman, president, and CEO in October 1996.

It was within this turbulent Bay Networks environment that NETGEAR was born on January 8, 1996. Patrick Lo, a Hong Kong native who had earned his electrical engineering degree from Brown University and spent twelve years at Hewlett-Packard in various management roles across the U.S. and Asia, saw an opportunity that the big networking companies were ignoring. Cisco and Bay Networks sold expensive, complex equipment designed for enterprise IT departments staffed by certified network engineers. But what about the small business owner who just needed to share an internet connection among five computers? What about the dentist's office, the real estate agency, the home office? These customers did not need a $10,000 router. They needed something that cost $200, came in a box with clear instructions, and worked when you plugged it in.

Lo co-founded NETGEAR within Bay Networks alongside Mark Merrill, a Stanford-educated engineer who had worked at SynOptics from 1987 to 1995, designing system architecture for some of the company's earliest Ethernet products. Merrill had been present at the creation of modern Ethernet networking, working on the 10BASE-T products that standardized how computers connected over twisted-pair copper wiring, the same wiring that runs through the walls of virtually every office building and many homes today.

The founding duo embodied a deliberate pairing that would shape NETGEAR's identity for decades. Lo brought the commercial instinct, the channel relationships, and the marketing savvy honed during his twelve years at HP. He understood how large technology companies went to market, how retail distribution worked across multiple countries, and how to position a product for customers who did not speak the language of network engineering. Merrill brought deep technical knowledge of networking hardware, from analog circuit design to system architecture, and the engineering discipline to translate complex networking functionality into products that were reliable enough to sell without expensive technical support. Together, they set out to build networking equipment that was affordable, reliable, and above all simple.

NETGEAR's initial product line launched in Japan in 1996 with ten SOHO devices, including hubs, Fast Ethernet switches, and an ISDN router. The decision to launch first in Japan was telling: Lo understood Asian markets from his HP days and recognized that Japan's early adoption of broadband internet made it an ideal proving ground. The products were designed in Silicon Valley but manufactured in Taiwan, leveraging the island's deep expertise in electronics manufacturing and its cost advantages over American and Japanese production.

This was the DNA that would define NETGEAR for decades: Silicon Valley design married to Taiwanese manufacturing, sold through retail and distribution channels to customers who wanted enterprise-grade reliability at consumer-friendly prices. In the networking world of the 1990s, this was genuinely revolutionary. The idea that you could walk into a store and buy a router the way you bought a toaster was radical.

But NETGEAR's future as a Bay Networks subsidiary was short-lived. In June 1998, Nortel Networks, the Canadian telecommunications giant, acquired Bay Networks for $9.1 billion. It was a blockbuster deal driven by Nortel's desire to compete with Cisco in the data networking market. Nortel, headquartered in Brampton, Ontario, was one of the world's largest telecommunications equipment companies, a crown jewel of Canadian industry with roots stretching back to 1895 as the manufacturing arm of Bell Canada. Under CEO John Roth, Nortel was on an acquisition spree to transform itself from a traditional telecom equipment maker into an internet networking powerhouse. Bay Networks, with its router and switching portfolio, was the centerpiece of that transformation.

But Nortel's interest was in enterprise equipment and optical networking, not the little consumer switches and routers that NETGEAR was selling. Patrick Lo's division was a rounding error in a nine-billion-dollar acquisition. Nortel's executives were focused on selling hundred-thousand-dollar optical switching systems to telephone companies, not hundred-dollar routers to home offices. NETGEAR was an afterthought, and that would prove to be its liberation. The very obscurity that made NETGEAR irrelevant within Nortel's grand strategy also meant that Lo and his team were left largely alone to build their business, accumulating operational knowledge, customer relationships, and product expertise that would serve them well when independence finally arrived.

III. Independence & The Broadband Revolution (1998-2003)

Picture Patrick Lo in the year 2000, standing in Nortel's shadow. He had spent four years building NETGEAR into a $176 million revenue business within Bay Networks, only to see his parent company swallowed by a Canadian telecom giant that had no interest in consumer networking. Nortel was chasing the enterprise dream, selling optical networking equipment to telephone companies. A division that sold $99 Ethernet switches at Best Buy was not exactly a strategic priority.

Lo saw his chance. In 2000, he led a management buyout, convincing Nortel to let NETGEAR go. The deal was backed by $15 million in equity financing from Pequot Capital Management, a Connecticut-based investment firm. It was a modest sum, even by 2000 standards, but it was enough to give NETGEAR its independence. Lo became the CEO of a company he had built from scratch inside two different corporate parents, and now he could finally run it his way.

The timing, however, was spectacularly bad for one particular ambition. NETGEAR had been generating $176 million in revenue and was preparing for a $130 million IPO. Then the dot-com bubble burst. The NASDAQ peaked in March 2000 and began its nauseating descent, eventually losing nearly 80% of its value. Networking companies were hit especially hard. Cisco would write off $2.2 billion in inventory. Nortel itself would spiral toward bankruptcy. By February 2001, Lo officially withdrew NETGEAR's IPO filing. The investment bankers who had been eager to underwrite the offering were suddenly nowhere to be found.

But here is where Lo's operational discipline saved the company. Unlike the dot-com startups that were burning cash on Super Bowl ads and office foosball tables, NETGEAR was a real business selling real products to real customers. The broadband revolution was not a bubble. It was a structural shift in how Americans connected to the internet. Cable companies like Comcast and Time Warner were rolling out cable modem service. Telephone companies were deploying DSL. For the first time, millions of households had always-on, high-speed internet connections. And every one of those connections needed a router.

Think about what the internet looked like before broadband. You dialed up, you waited for the screeching modem sounds, you checked your email, maybe browsed a few web pages, and then you hung up because you were tying up the phone line. Broadband changed everything. Suddenly the internet was just there, always available, like electricity or running water. And if you had two computers in your house, a desktop in the den and a laptop on the kitchen table, you needed a way to share that connection. That meant you needed a router, a device that could take the single internet connection from your cable modem and distribute it to multiple devices.

NETGEAR's product strategy during this period was elegant in its simplicity. The company built cable and DSL routers, Ethernet switches, and wireless access points that were designed for people who did not know what any of those words meant. The packaging was consumer-friendly, with photos of smiling families and promises of "easy setup." The products were sold at Best Buy, Circuit City, CompUSA, and other retail chains where regular people shopped for electronics. This was a deliberate channel strategy: rather than selling through the IT value-added resellers and distributors that served enterprise customers, NETGEAR went where the consumers were.

Lo's Hewlett-Packard training was evident in the operational approach. At HP, Lo had learned a management philosophy that emphasized disciplined execution, customer focus, and what HP's founders called "management by walking around," staying close to the market rather than relying on abstract strategy documents. He later recalled being told at HP that success required "two forces: pull and push," meaning you needed both mentors above you pulling you up and your own drive pushing from below. Lo applied this lesson to NETGEAR's culture, building a lean organization that combined Silicon Valley engineering talent with the cost discipline of a Taiwanese manufacturing operation.

NETGEAR did not try to build the most technically advanced router on the market. Instead, it focused on reliability, ease of use, and price-performance. The products were designed in San Jose, manufactured by contract manufacturers in Taiwan and China, and shipped through a lean supply chain that kept costs low. The ProSafe line for small businesses included switches, firewalls, and wireless access points that combined enterprise-grade features with consumer-friendly setup. Gross margins in the mid-to-high thirties were healthy enough to fund R&D and marketing while keeping prices competitive.

By 2002, NETGEAR had grown revenue to $237 million and was posting net income of $8.1 million. The company was profitable, growing, and riding a wave of broadband adoption that showed no signs of slowing. Lo decided it was time to try the IPO again. In April 2003, he filed with the SEC during what was the slowest period of IPO activity since 1975. The markets were still shell-shocked from the dot-com crash and the 2001 recession, and few companies dared to go public.

That made NETGEAR's July 2003 IPO something of a bellwether. The company priced its shares at $14 and raised $98 million, with bids from eighteen underwriters, the same investment bankers who had shied away three years earlier. The offering was a success, valuing the company at a level that validated Lo's patient approach. While dozens of networking companies had flamed out during the bust, NETGEAR had survived by doing something unfashionable: selling useful products at reasonable prices to ordinary customers.

The IPO gave NETGEAR a war chest and a public currency for acquisitions, but more importantly, it gave the company credibility. Patrick Lo had taken a corporate orphan, navigated a bubble collapse, and delivered a profitable public company. The contrast with Nortel was stark: NETGEAR's former parent company would eventually file for bankruptcy in January 2009, one of the largest corporate failures in Canadian history. The company that had dismissed NETGEAR as insignificant had destroyed over $30 billion in shareholder value, while the little consumer networking division had become a thriving independent public company.

There is a lesson here about the relationship between ambition and sustainability. Nortel bet everything on being the next Cisco, spent lavishly on acquisitions and R&D, and collapsed when the market turned. NETGEAR bet on being useful to ordinary people, kept costs low, and survived. Sometimes the most valuable business is not the most exciting one but the most durable one.

The next chapter would be even more lucrative, as a new technology called Wi-Fi was about to transform home networking from a niche hobby into a mass-market necessity.

IV. The Golden Era: Wi-Fi, Gaming, and Consumer Dominance (2003-2010)

There is a moment in the history of consumer technology when a product category crosses from "thing that enthusiasts tinker with" to "thing that everyone owns." For home networking, that moment arrived with Wi-Fi. The Institute of Electrical and Electronics Engineers, better known as IEEE, had been developing wireless networking standards since the late 1990s, but the technology was initially expensive, unreliable, and slow. The 802.11b standard, ratified in 1999, offered theoretical speeds of 11 megabits per second, roughly comparable to a moderately fast wired connection, but actual performance was often much worse.

To understand Wi-Fi standards without getting lost in the alphabet soup, think of them as generations of wireless technology, each faster and more capable than the last. The "b" standard was like a two-lane country road. The "g" standard, which arrived in 2003, widened it to a four-lane highway. And the "n" standard, finalized in 2009, turned it into a superhighway with multiple lanes going in both directions. Each generation roughly tripled or quadrupled the speed of the previous one, and each generation made wireless networking more reliable, with better range and fewer dropped connections.

NETGEAR was perfectly positioned to ride this wave. The company had already established itself as the go-to brand for home networking equipment at retail, and it moved quickly to build Wi-Fi routers around each new standard. The product naming conventions reflected the marketing challenge: how do you sell a technical specification to someone who just wants their laptop to work in the bedroom? NETGEAR's answer was branding. The "RangeMax" line emphasized coverage area, promising strong signals throughout the home. As the 802.11n standard approached, NETGEAR launched "N" routers with aggressive marketing campaigns that emphasized speed and range.

The shelf space wars during this period were fierce and deeply personal. Walk into a Best Buy in 2006 and you would see an entire aisle dedicated to networking equipment, each brand fighting for the eye-level shelf position that consumer electronics companies covet like beachfront property. NETGEAR competed for attention against Linksys, D-Link, and Belkin, each with its own strategy and strengths. Linksys, which Cisco had acquired in 2003 for $500 million, was the primary rival. The Linksys WRT54G, a blue-and-black router that became one of the best-selling networking products of all time, had established Linksys as the default choice for many consumers. Cisco's acquisition gave Linksys the halo of enterprise-grade reliability, a powerful marketing advantage even though the products themselves were designed for consumers.

D-Link, a Taiwanese company founded in 1986, competed aggressively on price, willing to sacrifice margins for market share. Belkin occupied the lower end of the market with budget-friendly products. And in the background, a Chinese company called TP-Link, founded in Shenzhen in 1996, the same year as NETGEAR, was quietly building massive scale in Asian markets. TP-Link's founders, brothers Zhao Jianjun and Zhao Jiaxing, were building a vertically integrated manufacturing operation that would eventually make TP-Link the world's number one consumer Wi-Fi equipment provider by unit shipments. The story of NETGEAR versus TP-Link is really a story about two companies born in the same year, pursuing the same market, but with fundamentally different cost structures and growth strategies.

NETGEAR's strategy during the golden era was to occupy the sweet spot between cheap and premium. Its products were not the least expensive on the shelf, but they were not the most expensive either. They offered strong performance, decent build quality, and a brand that consumers recognized and trusted. Patrick Lo understood that in consumer electronics, the battle is won at the point of purchase, and he invested heavily in retail relationships, packaging design, and in-store merchandising. The packaging itself was a competitive weapon: bright blue boxes with clear product photos and benefit-oriented messaging ("300+ Mbps Speed!" "Works with all ISPs!") designed to reassure the overwhelmed consumer standing in the networking aisle trying to figure out which box would actually make their Wi-Fi work.

NETGEAR also built strong relationships with the major retail buyers at Best Buy, Walmart, Staples, and other chains. These relationships were not just about price negotiations; they involved joint marketing programs, endcap displays, seasonal promotions, and training for retail sales staff. In the pre-Amazon era, these retail relationships were a genuine competitive advantage. A buyer at Best Buy who trusted the NETGEAR brand and the NETGEAR sales team would give the company favorable shelf placement, which drove sales, which justified more shelf space, creating a virtuous cycle.

The company also began expanding beyond routers and switches. In May 2007, NETGEAR acquired Infrant Technologies, the creator of the ReadyNAS line of network-attached storage devices. NAS devices are essentially small file servers that sit on your home or office network, allowing you to store and access files from any device. The acquisition brought a loyal community of enthusiasts and prosumers who valued ReadyNAS for its reliability and Linux-based operating system. It was NETGEAR's first move toward the "prosumer" market, the segment of technically sophisticated users willing to pay premium prices for advanced features.

The prosumer play would become a defining strategic theme. Around 2013-2014, NETGEAR launched the Nighthawk brand, a line of high-performance routers aimed at gamers and power users. The Nighthawk R7000, with its aggressive angular design and external antennas, looked like a stealth fighter jet sitting on your desk. It was deliberately designed to stand out from the generic black boxes that dominated the market. The Nighthawk name evoked speed, power, and technical superiority, the kind of branding that resonates with gamers and tech enthusiasts who view their networking equipment as a performance tool rather than a utility appliance.

The design language and marketing all signaled: this is not your parents' router. It was a premiumization play, an attempt to move upmarket and capture customers willing to pay $200 or more for a router when competitors were selling basic models for $30. The strategy worked partly because gamers, streamers, and remote workers genuinely needed better networking equipment. Online gaming, video streaming, and video conferencing all demand consistent, low-latency connections, and a cheap router that drops packets or introduces jitter can mean the difference between winning a competitive match and losing it, or between a smooth video call and a frozen screen with garbled audio. Nighthawk promised to solve these problems, and for many users, it delivered.

NETGEAR also experimented with other product categories during this period. Powerline adapters, which used a home's electrical wiring to extend network connectivity, addressed the problem of thick walls and multi-story homes where Wi-Fi signals struggled to reach. IP cameras added to the portfolio before the Arlo brand was formalized. And the company continued to build out its ProSafe line of business networking products, laying the groundwork for the SMB strategy that would become central to the company's future.

The financial results during this era reflected the strategy's success. Revenue grew from $237 million in 2002 to nearly $500 million by 2006, and the company posted profits every year from 2002 through 2005, with net income climbing from $8.1 million to $33.6 million over that period. Patrick Lo was named the Ernst & Young National Technology Entrepreneur of the Year in 2006, a recognition of how he had built NETGEAR from a corporate castoff into a leading consumer technology brand.

By the end of the decade, NETGEAR had established itself as one of the top three home networking brands in North America, with a product portfolio spanning routers, switches, wireless access points, NAS devices, and powerline adapters. Revenue had crossed the billion-dollar mark, and the company was profitable and generating cash. But beneath the surface, forces were gathering that would fundamentally challenge NETGEAR's business model. The same dynamics that had made home networking a mass market were about to turn it into a commodity, and the company that had democratized networking was about to learn the harsh lesson that democratization and commoditization are often two sides of the same coin.

V. Inflection Point #1: The Commoditization Trap (2010-2015)

Imagine you are a NETGEAR product manager in 2012. You have spent months designing a new wireless router, negotiating with chipset suppliers, optimizing the antenna design, testing the firmware, and working with retail partners on shelf placement. Your router costs $89 at Best Buy and delivers solid 802.11n performance. Then you open Amazon and discover that TP-Link is selling a functionally identical router for $24.99 with free Prime shipping. Same chipset from Broadcom. Same basic feature set. Same wireless standard. A third of the price.

This was the commoditization trap, and it was closing on NETGEAR like a vise. The smartphone revolution had created an explosion of connected devices. Where a household might have had two or three devices connecting to Wi-Fi in 2008, by 2013 it had eight or ten: phones, tablets, laptops, smart TVs, streaming sticks, game consoles. This surge in demand was great for the networking industry overall, but it also attracted a flood of low-cost competitors, primarily from China. TP-Link, Tenda, Xiaomi, and dozens of smaller manufacturers could produce routers at dramatically lower costs because they benefited from China's manufacturing scale, lower labor costs, and in some cases, government subsidies.

The channel dynamics amplified the problem. Amazon was transforming from a convenient alternative to retail into the dominant channel for consumer electronics purchases. And Amazon's marketplace was brutally efficient at price competition. On a retail shelf, NETGEAR's superior packaging, brand recognition, and merchandising could justify a price premium. On an Amazon search results page, the product was reduced to a photo, a bullet list of specifications, a star rating, and a price. When the specifications were essentially identical, price won.

Revenue tells the story. NETGEAR peaked near $1.4 billion in 2014, then began a steady, dispiriting decline: $1.30 billion in 2015, a 6.7% drop; $1.14 billion in 2016, another 12% down; and $1.04 billion in 2017, falling another 9%. In just three years, the company had shed roughly a quarter of its revenue. Gross margins compressed as the company was forced to cut prices to compete. The consumer router market was becoming a race to the bottom, and NETGEAR was running in expensive shoes.

The margin compression was particularly painful because NETGEAR's cost structure had been built for a higher-revenue business. The company maintained a significant engineering organization in San Jose, with office leases, salary costs, and R&D expenditures that did not decline proportionally when revenue fell. This is the operating leverage problem that haunts hardware companies: fixed costs that feel manageable at $1.4 billion in revenue become burdensome at $1 billion. And unlike software companies, which can scale revenue with minimal incremental cost, hardware companies must continue investing in product development, certifications, supply chain management, and quality control for every new product generation.

The company's strategic response came on multiple fronts. The Nighthawk brand, launched around 2013-2014, was the most visible move. By creating a distinct sub-brand for high-performance routers, NETGEAR was trying to segment the market. The message was: yes, you can buy a $25 router from TP-Link, but if you are a gamer who needs low latency, or a family streaming Netflix on five devices simultaneously, or a professional working from home, you should spend $200 on a Nighthawk. This premiumization strategy worked in the sense that Nighthawk became a recognized brand with genuine enthusiast cachet. But it also meant conceding the mass market to lower-cost competitors.

NETGEAR also experimented with mesh networking, a technology that would prove transformative for the home Wi-Fi market. Traditional routers broadcast their signal from a single point, and performance degrades as you move farther away. Mesh systems use multiple interconnected nodes placed throughout the home, creating a blanket of coverage with seamless handoff as you walk from room to room. Think of it as the difference between having one powerful spotlight in the center of your house versus having multiple smaller lights in every room.

Google partnered with NETGEAR on the OnHub router in 2015, an early experiment in simplified, cloud-managed home networking. But Google would soon launch its own Google Wifi mesh system in 2016, and a startup called eero had already begun selling its mesh system in early 2016. NETGEAR responded with the Orbi system later that year, which differentiated itself by using a dedicated wireless backhaul channel between the router and its satellites, delivering better performance than competitors that shared their wireless capacity between device connections and inter-node communication.

Meanwhile, NETGEAR's security camera business was exploding. The company had launched Arlo, a wire-free battery-powered security camera, in 2014. It was an accidental hit. The product tapped into growing consumer demand for home security and smart home devices. By 2017, Arlo had captured roughly 40% of the U.S. consumer connected camera market. Revenue was growing at rates that dwarfed the core networking business. But Arlo was also capital-intensive, with its own manufacturing, cloud infrastructure, and subscription model. Running a high-growth hardware-plus-subscription security camera business alongside a mature, commoditizing networking equipment business was creating strategic tension.

The ReadyNAS business, once seen as a bright spot, was fading as consumer interest in local storage diminished. Cloud services like Dropbox, Google Drive, and iCloud were making it easier to store files without dedicated hardware, and the NAS market was increasingly dominated by Synology and QNAP, Taiwanese specialists that served the enthusiast and SMB segments more effectively. This was another example of the innovator's dilemma: NETGEAR had acquired Infrant and ReadyNAS to serve a growing market for local network storage, only to watch the market shift to cloud storage over the following decade. The technology was not obsolete, NAS devices still serve important use cases for data-intensive users and privacy-conscious individuals, but the addressable market was far smaller than it had appeared in 2007.

By 2015, NETGEAR faced a strategic reckoning. The consumer router business was commoditizing. The storage business was shrinking. The camera business was growing fast but consuming resources. And the company needed to decide what it wanted to be when it grew up. The answer would involve one of the more interesting corporate separations of the decade.

VI. Inflection Point #2: The Arlo Carve-Out & Refocus (2016-2018)

In February 2018, NETGEAR's board of directors voted unanimously to spin off Arlo Technologies as an independent public company. It was, on the surface, a paradoxical decision. Arlo was the fastest-growing part of NETGEAR, with revenue surging 58.5% to $96.2 million in the first quarter of 2018 alone. It had 1.9 million registered users, dominant market share, and a brand that consumers loved. Why would you spin off your best business?

The answer reveals the strategic calculus that faces every multi-product hardware company. Arlo and NETGEAR's networking business had almost nothing in common beyond sharing a corporate parent. They served different customers, required different go-to-market strategies, operated on different product cycles, and demanded different capital allocation priorities. Arlo needed heavy investment in cloud infrastructure, subscription services, and consumer marketing. The networking business needed investment in enterprise-grade features, channel development for SMB customers, and next-generation Wi-Fi technology. Every dollar spent on Arlo was a dollar not spent on networking, and vice versa.

There was also a valuation argument, and this is where the financial engineering gets interesting. Wall Street was struggling to value a company that was half-commodity router maker and half-high-growth smart home play. The networking business, with its declining revenue and compressing margins, deserved a mature hardware multiple, something in the range of 8-12 times earnings. Arlo, with its 50%+ revenue growth and expanding subscription base, arguably deserved a SaaS-like growth multiple, perhaps 5-8 times revenue. Combined, neither got appropriate credit: the growth investors who might have been attracted to Arlo were put off by the declining networking business, while value investors who might have been attracted to the networking cash flows were confused by the capital-intensive camera business.

This is a phenomenon that portfolio managers call a "conglomerate discount," and it is the primary financial justification for corporate separations. By splitting the two businesses, NETGEAR's board believed it could unlock hidden value by allowing each company to attract its natural investor base and be valued on its own merits.

Arlo Technologies filed its S-1 with the SEC in July 2018 and completed its IPO in August, with shares initially priced at $16. The offering valued Arlo at approximately $1.4 billion. NETGEAR initially retained approximately 80% ownership and completed the full separation by distributing its remaining shares to NETGEAR shareholders on December 31, 2018.

The post-Arlo NETGEAR was a leaner, more focused company, but also a smaller one. Without Arlo's revenue, the company had to articulate a compelling standalone story. Management doubled down on three pillars: the Connected Home segment (Orbi, Nighthawk, and other premium consumer products), the SMB business (managed switches, wireless access points, and the Insight cloud management platform), and an increasingly important niche called ProAV.

ProAV, short for Professional Audio-Visual, may sound obscure, but it represented one of NETGEAR's most strategically interesting moves. The professional AV industry, think corporate boardrooms, concert venues, sports stadiums, houses of worship, and university lecture halls, was undergoing a massive technology transition. Traditional AV systems used dedicated point-to-point cables for every audio and video connection. A single boardroom might have dozens of proprietary cables running from cameras, microphones, displays, and speakers to a central control system. The industry was shifting to AV-over-IP, which replaced all those dedicated cables with standard Ethernet networking. Instead of proprietary AV infrastructure, you could run everything over the same network switches and cables that carried your data traffic.

NETGEAR's M4250 and M4300 series switches were purpose-built for this application. To understand why this matters, consider the challenge that AV integrators face. A traditional IT network switch requires configuration through a command-line interface, using networking terminology like VLANs, QoS policies, IGMP snooping, and spanning tree protocols. AV integrators, who are experts in audio, video, and control systems but not necessarily in network engineering, found this intimidating and error-prone. NETGEAR's AV switches came pre-configured with settings optimized for AV traffic, with a management interface that used AV terminology (sources, displays, zones) rather than IT terminology (ports, VLANs, ACLs). The switches included preconfigured profiles for common AV protocols like Dante audio, NDI video, and various AV-over-IP standards. They were priced well below the Cisco and Aruba alternatives that dominated traditional enterprise networking. The ProAV market had several attractive characteristics for NETGEAR: higher margins than consumer products, stickier customer relationships (once an AV integrator standardizes on your switches, they tend to stay), and limited competition from the Chinese manufacturers who were hammering the consumer business.

The "work from home" thesis was another element of the strategy, though it would not receive its explosive validation until 2020. NETGEAR's management had observed that remote work was a growing trend and that home offices needed better networking equipment than what ISPs provided. The Orbi mesh system, with its premium positioning and strong performance, was designed partly for this market: the professional who needed reliable, high-speed Wi-Fi throughout their home for video conferencing, cloud applications, and VPN connections.

The financial impact of the Arlo separation was significant and immediate. Total revenue dropped from $1.06 billion in 2018 to $999 million in 2019, a mechanical effect of removing a fast-growing business from the consolidated results. But the remaining business had a cleaner margin profile and a more focused strategic direction. Investors could now evaluate NETGEAR purely as a networking equipment company, without trying to simultaneously value a consumer electronics subscription business.

The separation also freed up management attention, arguably the scarcest resource in any organization. Patrick Lo and his leadership team no longer had to split their time between Arlo product launches, cloud infrastructure investments, and subscription model optimization on one hand, and WiFi router engineering, switch product roadmaps, and retail channel management on the other. NETGEAR was now a networking company, period, with a clear hierarchy of priorities: protect and premiumize the consumer franchise, grow the SMB business, and build the ProAV niche into a meaningful contributor.

Whether that focus would translate into sustainable growth remained an open question, one that a global pandemic was about to answer in the most dramatic way imaginable.

VII. Inflection Point #3: The Pandemic Boom & Bust (2019-2022)

In March 2020, when governments around the world ordered their citizens to stay home, the global economy experienced a shock unlike anything in living memory. Restaurants closed. Offices emptied. Schools went remote. And suddenly, hundreds of millions of people needed their home internet connections to work flawlessly, because their livelihoods, their children's education, and their social lives all depended on it.

For NETGEAR, it was as if someone had flipped a switch on demand. The $79 router that had been sitting in a drawer as a backup was suddenly inadequate when two parents were on Zoom calls while two kids were attending virtual school and a teenager was gaming in the basement. Think about the networking load that scenario represents: two simultaneous video conferencing streams, each consuming 3-5 megabits per second of upstream bandwidth with strict latency requirements; two educational video streams; a gaming session demanding sub-20-millisecond latency; plus whatever other devices were connected. A cheap router simply could not handle that load without packet drops, buffering, and call failures.

Families rushed to upgrade their networking equipment. Orbi mesh systems, which could blanket a three-thousand-square-foot home with reliable Wi-Fi and intelligently distribute traffic across bands and nodes, flew off shelves. Nighthawk routers, with their more powerful processors, larger memory buffers, and advanced antenna arrays, became must-have purchases. Small businesses that had never considered their networking infrastructure were suddenly buying managed switches and access points to support remote employees who needed VPN access to corporate resources.

The work-from-home thesis that NETGEAR's management had been quietly building toward for years was suddenly and explosively validated. Every home office needed enterprise-grade reliability, and NETGEAR's product portfolio, spanning from premium consumer mesh systems to SMB-grade managed switches, was almost perfectly positioned for this moment.

Revenue surged 25.7% in 2020 to $1.26 billion, the highest growth rate in over a decade and a level that returned NETGEAR to territory it had not visited since before the Arlo spin-off. It was a remarkable validation of the company's product portfolio. But the boom came with a painful catch: supply chain chaos.

The global semiconductor shortage that began in late 2020 hit networking equipment manufacturers particularly hard. NETGEAR's routers and switches depend on chipsets from Qualcomm, Broadcom, and MediaTek, the same suppliers that were scrambling to meet surging demand from every electronics manufacturer on the planet. Lead times for key components stretched from weeks to months. Shipping containers that had cost $2,000 to send from Asia to the United States suddenly cost $15,000 or more. NETGEAR could not build products fast enough to meet demand, and when it could build them, it could not ship them fast enough to fill orders.

The financial mathematics were cruel. Revenue was up, but cost of goods sold was up even more. The same chipsets and components were being bid up by desperate buyers. Expedited shipping ate into margins. NETGEAR was selling more product at higher prices but making less profit per unit because the entire cost structure had inflated. This is a dynamic that many investors misunderstand about hardware companies during supply shortages: revenue growth does not automatically translate into profit growth when input costs are rising faster than selling prices.

The 2021 results illustrated this perfectly. Revenue declined modestly to $1.17 billion, a 6.9% drop from 2020, but the decline was not because of weakening demand. It was because NETGEAR literally could not build enough product. Orders were backlogged, customers were waiting months for deliveries, and competitors who had secured better supply allocations, either through larger volume commitments or more aggressive spot market purchasing, were gaining share. For a company whose entire value proposition was being the reliable, available choice at retail and online, this was an existential threat.

Then came the hangover. By 2022, the pandemic-driven demand surge had exhausted itself. Households that had upgraded their networking equipment in 2020 and 2021 did not need to buy again. The channel was stuffed with inventory that had been ordered during the shortage panic and arrived after the demand had peaked. Meanwhile, the competitive landscape had shifted during the pandemic years.

Ubiquiti, the New York-based networking company founded by Robert Pera in 2005, had built a cult following among prosumers and IT professionals with its UniFi product line. Pera, a former Apple engineer who had developed wireless networking products in his spare time, created a company that was philosophically different from every traditional networking equipment maker. Ubiquiti's model was radical: high-quality hardware at aggressive prices, sold direct-to-consumer with minimal marketing, and managed through elegant software that made network administration feel like using an Apple product. The company operated with roughly 1,600 employees, a tiny fraction of NETGEAR's workforce, and generated over $2 billion in revenue, delivering operating margins that put traditional networking companies to shame.

Ubiquiti was the ultimate counter-positioning story, and it is worth dwelling on because it represents the most significant competitive threat to NETGEAR's premium positioning. Traditional networking companies like NETGEAR, Linksys, and D-Link sell through retail and distribution channels, which add layers of markup and require expensive sales and marketing organizations. Ubiquiti stripped all of that out. It sold directly through its own website and through a network of enthusiast distributors. It spent almost nothing on advertising, instead relying on a passionate online community of IT professionals who evangelized the products through forums, YouTube reviews, and word of mouth. The result was enterprise-grade equipment at prices that were often lower than NETGEAR's consumer products, backed by software that was genuinely elegant and easy to use. With a market capitalization of roughly $22 billion, Ubiquiti was worth approximately twenty-eight times NETGEAR's valuation, a sobering comparison for a company with only modestly higher revenue.

TP-Link, now operating with an estimated 24,000 employees and generating approximately $2.8 billion in revenue, had expanded aggressively in the United States. Amazon eero, acquired for roughly $97 million in February 2019, had the backing of the world's largest e-commerce platform and could be bundled with Prime memberships and Alexa devices. Even ISPs themselves were becoming competitors, offering "free" router and mesh equipment bundled with internet subscriptions, a model that captured roughly 46% of the market by 2025.

The post-pandemic revenue decline was steep. From $1.26 billion in 2020, NETGEAR's revenue fell to $1.17 billion in 2021, then plunged to $932 million in 2022 and $741 million in 2023. In three years, the company lost more than 40% of its peak pandemic revenue. The stock price, which had traded above $40 during the pandemic boom, cratered along with the financials.

The bust raised an existential question: had the pandemic merely pulled forward demand that would have occurred over several years, or had it masked a structural decline in NETGEAR's addressable market? The answer, as it turned out, was a bit of both. The pandemic had certainly accelerated purchases that would have happened over three to five years, creating a "demand desert" once the pull-forward was exhausted. But the revenue decline was also structural: ISP-provided equipment was eliminating the need for standalone routers for a growing share of households, and TP-Link's aggressive pricing was making it increasingly difficult for NETGEAR to compete in the value segment.

Consider the math from an average consumer's perspective. Your internet provider offers you a combined modem-router for $10 per month as part of your subscription, or you can buy a standalone NETGEAR router for $100-200. Over a five-year router lifespan, the ISP option costs $600, more expensive in total but with zero upfront cost, no setup hassle, and automatic replacement if anything breaks. For many consumers, that convenience premium is worth paying, and it eliminates NETGEAR from the equation entirely. This ISP-provided equipment trend has become one of the most important structural headwinds facing the entire standalone router industry.

The company's response to the bust would determine whether NETGEAR could stabilize or continue its downward trajectory.

VIII. The Modern Pivot: SMB, ProAV, WiFi 6E/7, and Subscriptions (2022-Present)

On January 31, 2024, NETGEAR announced a changing of the guard that marked the end of an era. Patrick Lo, who had co-founded the company in 1996, led the management buyout from Nortel, navigated the dot-com bust, executed the IPO, built the billion-dollar consumer franchise, and steered the company through the Arlo spin-off and the pandemic roller coaster, retired as CEO and Chairman. His nearly three-decade tenure made him one of the longest-serving founder-CEOs in the technology industry. Few executives in the networking world could claim to have witnessed the entire arc from dial-up modems to WiFi 7.

His successor, Charles "CJ" Prober, brought a markedly different background. Prober had served as President of Life360, CEO of Tile (the Bluetooth tracker company, which was acquired by Life360), Chief Operating Officer at GoPro, and Senior Vice President of Digital Publishing at Electronic Arts, where he had been central to EA's transformation from a packaged software company to a digital services business. The appointment signaled NETGEAR's strategic direction: the company needed a leader who understood software, subscriptions, and digital transformation, not just hardware engineering and supply chain management.

NETGEAR's current strategy rests on three pillars, each with distinct economics and competitive dynamics.

The Connected Home segment encompasses Orbi mesh systems, Nighthawk gaming routers, and cable modems sold to consumers. This remains the largest revenue contributor, but it is also the most challenged. Consumer router average selling prices continue to face downward pressure from TP-Link and other low-cost competitors. NETGEAR's response has been to push further upmarket with WiFi 7 products, including the Orbi 970 series, which launched at price points above $1,000 for a multi-unit system. The bet is that a meaningful segment of consumers will pay premium prices for the latest technology, better performance, and stronger security features. Whether that premium segment is large enough to sustain the business remains an open question.

The SMB segment, which NETGEAR now classifies as part of its Enterprise business, includes managed and smart-managed switches, wireless access points supporting WiFi 6, 6E, and 7, and the Insight cloud management platform. Insight is particularly important because it represents NETGEAR's attempt to build recurring software revenue on top of hardware sales. Insight allows IT administrators to manage their entire NETGEAR network remotely through a cloud dashboard, monitoring performance, deploying firmware updates, and troubleshooting issues without being on-site. It is a subscription service that makes the hardware stickier: once a small business has deployed NETGEAR switches and access points managed through Insight, switching to a competitor requires not just replacing the hardware but migrating the management infrastructure.

The ProAV segment has emerged as the hidden gem that bulls point to. The AV-over-IP market is expected to grow significantly over the coming years, with some industry estimates projecting that AV-over-IP will account for 65% of professional AV deployments by 2030, up from approximately 38% today. NETGEAR's M4250, M4300, and newer M4350 and M4500 series switches have gained strong traction with AV integrators who appreciate the pre-configured AV profiles, the AV-friendly management interface, and the price point that is well below Cisco. The signal routing segment of the ProAV market alone represents approximately $7.1 billion in opportunity.

The subscription play extends across all segments. NETGEAR Armor, a cybersecurity service powered by Bitdefender, offers threat protection for all devices on a home network. Smart Parental Controls allows parents to manage children's internet access. And Insight cloud management serves the SMB segment. As of late 2024, NETGEAR had approximately 555,000 subscribers and was generating around $35 million in annual recurring subscription revenue, growing at roughly 22% year over year. These are modest numbers in absolute terms, but they represent a strategic shift from a one-time hardware sale to an ongoing customer relationship.

The financial results of this pivot are beginning to show. Full-year 2025 revenue totaled $699.6 million, a 3.8% increase that represented the first year of revenue growth since 2020. More significantly, non-GAAP gross margin reached an all-time high of 41.2%, an improvement of over 900 basis points. The Enterprise segment (which includes both SMB and ProAV) contributed 49% of the revenue mix in Q4 2025, up nearly 500 basis points year over year, with Enterprise gross margins reaching 51.4% in the fourth quarter. Full-year non-GAAP net income was $13.3 million.

The TP-Link patent settlement also provided a notable financial boost. In September 2024, NETGEAR reached a $135 million settlement with TP-Link over patent infringement claims, resulting in a net benefit of approximately $103.6 million before taxes. It was a significant windfall, but also an acknowledgment that intellectual property could be a source of value even as the hardware itself commoditized. Notably, TP-Link subsequently filed a lawsuit accusing NETGEAR of conducting a "smear campaign," adding a litigious dimension to the competitive rivalry.

A notable development in 2024 was TP-Link's corporate restructuring, which separated its international operations from TP-LINK Technologies Co., Ltd. in China. TP-Link established TP-Link Systems Inc. in Irvine, California, as its new global headquarters, with co-founder Jeffrey Chao and his wife Hillary as sole owners. This restructuring was widely interpreted as a defensive move against growing U.S. government scrutiny of Chinese technology companies. The U.S. Commerce Department and the Department of Justice had opened investigations into TP-Link over national security concerns, and the company was seeking to distance its international operations from its Chinese origins.

For NETGEAR, TP-Link's regulatory troubles could represent either opportunity or irrelevance. If regulators restrict TP-Link's ability to sell in the United States, NETGEAR could capture meaningful share in both consumer and SMB markets. But regulatory actions are unpredictable, and TP-Link's restructuring may be sufficient to satisfy regulators.

The competitive landscape remains intensely challenging beyond TP-Link. Ubiquiti continues to expand its product portfolio and its devoted community, with its UniFi ecosystem now encompassing cameras, access control, phones, and even electric vehicle chargers alongside its core networking products. Cisco's Meraki platform dominates the enterprise edge but is increasingly moving downmarket toward SMBs. And ISP-provided equipment continues to capture a large share of the home networking market.

NETGEAR held an investor day on November 17, 2025, where the new leadership team outlined long-term strategic priorities and a vision for shareholder value creation. The emphasis was on international expansion, customer-centricity, and innovation, with a particular focus on the software and subscription experience. The company's market capitalization stands at approximately $783 million, a fraction of where it was during the pandemic peak, reflecting both the revenue decline and investor uncertainty about the path forward.

For investors, the key question is whether the margin improvement and mix shift toward Enterprise represent a sustainable transformation or a temporary pause in a longer decline. The answer will depend largely on whether NETGEAR can grow its subscription base, hold its ProAV position against larger competitors, and navigate the WiFi 7 upgrade cycle successfully.

IX. Playbook: Business & Strategy Lessons

NETGEAR's thirty-year journey offers a masterclass in the challenges of building a durable hardware business in a technology market that relentlessly drives toward commoditization. Several strategic lessons stand out.

Hardware is Hard, and Getting Harder. Clayton Christensen's innovator's dilemma is often invoked to describe how startups disrupt incumbents, but NETGEAR's story illustrates a variant: what happens when the disruption comes not from a superior technology but from an inferior one at a much lower price point. TP-Link's routers were not better than NETGEAR's. They were cheaper, and for most consumers, "good enough and cheap" beats "better and expensive." The lesson for hardware companies is that product superiority alone is not a moat. When the underlying technology is standardized (same chipsets, same Wi-Fi standards, same manufacturing processes), differentiation must come from somewhere other than the product itself: brand, channel, software, services, or ecosystem.

Channel Mastery is an Underrated Competency. NETGEAR's ability to evolve its distribution strategy from retail shelves to e-commerce to commercial channels has been critical to its survival. Consider the economics of each channel transition. In the retail era, success required relationships with buyers at Best Buy, Circuit City, and Walmart; investment in packaging and point-of-purchase displays; management of return rates and restocking fees; and willingness to participate in seasonal promotions that compressed margins. In the e-commerce era, success required Amazon marketplace optimization, customer review management, pricing algorithms that responded to competitor movements in real time, and advertising spend on Amazon's platform. In the commercial channel, success requires training programs for IT resellers and AV integrators, technical pre-sales support, and certification programs that build loyalty.

Few companies have successfully navigated all three transitions. The fact that NETGEAR has adapted, even if imperfectly, to each successive channel shift is a testament to operational flexibility that deserves more credit than it typically receives from investors.

The Premiumization Gambit Has Limits. Nighthawk demonstrated that a hardware company can move upmarket through branding and product design, and Orbi showed that a genuinely differentiated product (dedicated wireless backhaul) can command premium prices. But premiumization only works under two conditions: the premium segment must be large enough to sustain the business, and competitors must not be able to easily replicate the differentiation. NETGEAR has faced challenges on both fronts. The premium router segment, while profitable, is inherently smaller than the mass market. And competitors have proven adept at matching NETGEAR's premium features. Asus's ROG gaming routers target the exact same gaming enthusiast demographic that Nighthawk serves, with comparable features and aggressive pricing. Ubiquiti's prosumer equipment offers what many consider superior software at comparable or lower hardware prices. Even TP-Link has moved upmarket with its Archer and Deco premium lines, narrowing the gap between "value" and "premium" products. In January 2025, Asus launched what it called the first AI-enabled gaming router with an integrated neural processing unit, raising the bar on what "premium" means in the category.

Know When to Let Go. The Arlo spin-off remains one of the most instructive corporate separation decisions of the past decade. It is tempting to second-guess the decision by pointing to the pandemic boom that followed: would NETGEAR have been better off keeping Arlo and riding the dual tailwinds of work-from-home networking demand and home security camera demand? Perhaps. But the spin-off freed NETGEAR to focus on its core networking strategy and removed the capital allocation conflicts that had constrained both businesses. NETGEAR recognized that running a high-growth consumer electronics business alongside a maturing networking equipment business created strategic confusion and valuation compression.

The spin-off allowed each business to pursue its own path. It is worth noting that Arlo's post-IPO journey has been rocky, with the company struggling to achieve sustainable profitability as a standalone entity despite strong revenue growth. This suggests that the challenges of the camera-plus-subscription business model were real, not imagined, and that separating the two businesses was strategically sound regardless of Arlo's subsequent performance.

Niche Dominance Can Be More Valuable Than Broad Market Share. NETGEAR's ProAV business illustrates the power of finding a specific, underserved market segment where the company can be the clear leader. The ProAV market has characteristics that the consumer router market lacks: professional buyers who value reliability and support over price, installation-based business models that create natural switching costs, and a technology transition (AV-over-IP) that is creating new demand rather than simply replacing existing demand.

ProAV integrators do not shop on Amazon. They specify products based on technical capabilities, compatibility with other AV equipment, manufacturer support quality, and training availability. They value pre-sales support, technical training, and product consistency across project timelines that can span months. The switching costs are meaningful because AV systems are installed in physical spaces, such as corporate boardrooms, university lecture halls, houses of worship, and sports venues, and expected to run reliably for five to ten years. An integrator who has standardized on NETGEAR's M4250 switches has built their installation templates, trained their technicians, and developed troubleshooting expertise around those specific products. Switching to Cisco or another vendor means retraining staff, rebuilding templates, and accepting the risk of unfamiliar product behavior. This is exactly the kind of market position that generates sustainable margins and loyal customers, and it is where NETGEAR's future may ultimately be decided.

Subscription Overlays on Hardware Are Necessary but Difficult. Every hardware company wants recurring revenue, and the reason is straightforward: Wall Street values recurring revenue much more highly than one-time product sales. A dollar of subscription revenue might be valued at 5-10 times in enterprise value, while a dollar of hardware revenue might be valued at 0.5-1.5 times. This valuation gap creates a powerful incentive for hardware companies to layer subscription services on top of their products.

But few achieve subscription scale, and NETGEAR's experience illustrates why. The company's 555,000 subscribers represent a start, but the attach rate, the percentage of hardware buyers who convert to subscribers, remains low. The challenge is that networking equipment is inherently functional: it either works or it does not. Convincing customers to pay an ongoing fee of $3-7 per month for security (Armor), parental controls, or cloud management requires continuous demonstration of value, and the willingness to pay varies dramatically across customer segments. Enterprise and SMB customers are more accustomed to subscription-based IT services, which is another reason the pivot toward Enterprise is strategically important: the customer base is simply more receptive to subscription models.

Founder Longevity Is a Double-Edged Sword. Patrick Lo led NETGEAR for nearly twenty-eight years, providing strategic continuity through multiple technology cycles. His tenure spanned the entire history of consumer internet: from dial-up modems to broadband to Wi-Fi to mesh networking to WiFi 7. Few executives in any industry can claim to have shepherded their company through that many technology transitions. Lo's deep industry knowledge, supplier relationships, and understanding of channel dynamics were invaluable assets.

But long CEO tenures can also breed incrementalism and resistance to radical change. By the time Lo retired, NETGEAR's culture was deeply rooted in hardware engineering and supply chain optimization. The software and subscription capabilities that the company needed to build for its next phase required different skills, different hiring profiles, and a different organizational culture. The appointment of CJ Prober, with his background in digital transformation and subscription businesses, signals that the board recognized the need for a different kind of leadership. Whether Prober can successfully transform a traditional hardware company into a software-enhanced platform remains to be seen, but the choice of a CEO whose defining professional experience was taking EA from boxed software to digital services is a clear statement of intent.

X. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Applying Michael Porter's competitive forces framework to NETGEAR reveals a challenging industry structure. The threat of new entrants is moderate to high in the consumer space, where any contract manufacturer in Shenzhen can produce a functional router, but meaningfully higher in the SMB and ProAV segments, where channel relationships, technical certification programs, and product reliability create genuine barriers. NETGEAR's ProAV business, for instance, benefits from the fact that AV integrators invest time learning specific product lines and building installation templates around them.

Supplier bargaining power is high and asymmetric. NETGEAR depends on a small number of chipset suppliers: Qualcomm for premium Wi-Fi silicon, Broadcom for networking processors, and MediaTek for value-tier components. These suppliers serve the entire networking industry, and during the semiconductor shortage of 2020-2022, they allocated chips based on volume commitments and willingness to pay premium prices. NETGEAR, as a mid-sized buyer, lacked the leverage of larger purchasers. This supplier concentration creates ongoing vulnerability, as chipset pricing and availability directly impact NETGEAR's gross margins and product launch timing.

Buyer bargaining power is high across all segments but particularly brutal in consumer markets. Amazon and Best Buy together account for a large share of consumer networking equipment sales. Online price transparency means that customers can instantly compare NETGEAR's products against cheaper alternatives. Even in the SMB segment, where customers value reliability and support more than the absolute lowest price, the proliferation of competitive options from Ubiquiti, TP-Link, and increasingly Cisco's downmarket offerings gives buyers significant leverage.

The threat of substitutes is real and growing. ISP-provided equipment, often included "free" with internet subscriptions, captured approximately 46% of the home networking market by 2025. For many consumers, the router their cable company provides is good enough, eliminating the purchase decision entirely. Software-defined networking and cloud-managed alternatives threaten traditional hardware-centric models. And 5G fixed wireless internet, while still nascent, could reduce demand for traditional home networking equipment if carriers offer integrated gateway devices.

Competitive rivalry is arguably the most punishing force. The wireless router market alone was valued at approximately $3 billion in 2024, growing at a 9.2% compound annual rate. But that growth is being captured unevenly. TP-Link leads with approximately 18% revenue share and an estimated $2.8 billion in total revenue across all networking products, followed by NETGEAR and Asus collectively holding about 25% of the premium segment. Ubiquiti, with over $2 billion in revenue and a $22 billion market cap, competes primarily in the prosumer and SMB space but increasingly overlaps with NETGEAR's target segments. D-Link generates approximately $449 million in revenue. Asus competes aggressively in the premium gaming segment with its ROG Rapture line. Linksys, now owned by Foxconn after being sold by Belkin, competes in both consumer and SMB markets.

At the enterprise edge, Cisco, Aruba (HPE), and Juniper/Mist represent formidable competitors with vastly greater resources. And tech giants Google and Amazon have ecosystem plays that integrate networking hardware (Nest Wifi and eero, respectively) with their broader smart home platforms, using networking equipment as a gateway to their ecosystems rather than as a standalone profit center.

Through Hamilton Helmer's 7 Powers framework, NETGEAR's competitive position looks sobering. Scale economies are weak to moderate: NETGEAR has some component purchasing power, but nothing that Chinese competitors with four times the volume cannot match. Network effects are essentially nonexistent, as networking hardware does not become more valuable as more people use it in the way that social networks or marketplaces do. Counter-positioning, once NETGEAR's strength when it offered enterprise-grade reliability at consumer prices, has faded as Ubiquiti now counter-positions against NETGEAR from below (prosumer quality at near-commodity prices) and TP-Link counter-positions on pure value.

Switching costs are the most promising power for NETGEAR to build, and this is why the Insight cloud management platform and ProAV strategy are so strategically important. When an SMB has deployed twenty NETGEAR switches and access points managed through Insight, with network configurations, access policies, firmware versions, and monitoring dashboards all configured in the Insight cloud, the cost of ripping out that infrastructure and migrating to a competitor is meaningful. It is not just the hardware cost; it is the labor cost of reconfiguring every device, retraining IT staff, and accepting the downtime risk during migration. Similarly, AV installations in boardrooms and auditoriums are designed to last five to ten years, creating sticky relationships with the AV integrator who specified and installed the equipment.

Brand power is moderate but uneven across segments. The Nighthawk name carries genuine recognition among gamers and enthusiasts, a community that discusses router performance with the same intensity that audiophiles discuss amplifier specifications. But NETGEAR lacks the brand moat of an Apple or even a Cisco, brands so powerful that customers pay significant premiums for the logo alone. In the SMB and ProAV segments, NETGEAR's brand is respected but not dominant, and brand loyalty is weaker than product performance and price-value relationships.

Cornered resources are weak: NETGEAR does not possess unique technology or patents that competitors cannot work around. The $135 million TP-Link patent settlement demonstrated that NETGEAR has meaningful intellectual property, but patents in the networking space tend to be narrow and work-aroundable rather than broad and defensible. Process power is moderate, reflecting decades of operational experience in supply chain management, channel development, and product lifecycle management, the kind of institutional knowledge that is difficult to replicate quickly but does not prevent competitors from eventually matching it.

The overall assessment is that NETGEAR operates in an industry with unfavorable competitive dynamics and lacks the kind of durable competitive moats that create long-term value. The comparison with Ubiquiti is particularly instructive. Ubiquiti, with a similar revenue base, commands a market capitalization nearly thirty times larger than NETGEAR's. The difference is that the market perceives Ubiquiti as having meaningful competitive advantages: a direct-to-consumer model that eliminates channel costs, a passionate community that drives organic demand, and software that creates genuine ecosystem lock-in. NETGEAR, by contrast, is perceived as a traditional hardware company operating in a commoditizing market. Whether that perception can change depends on the company's ability to build switching costs through Insight and ProAV, grow subscription revenue, and demonstrate that its gross margin expansion is sustainable.

The company's strategic pivot toward SMB, ProAV, and subscriptions is fundamentally an attempt to move into segments where switching costs, channel relationships, and technical expertise can create defensible positions. It is worth noting that this strategy is not without precedent. IBM successfully transformed from a hardware company to a services and software company over the course of two decades. Dell reinvented itself from a commodity PC maker into an enterprise infrastructure provider. But these transformations required enormous patience, significant investment, and willingness to endure years of revenue pressure while the new business scaled. NETGEAR is attempting a similar transformation on a much smaller scale, and whether it has the resources, the talent, and the market opportunity to pull it off is the central investment question.

XI. Bull vs. Bear Case

The Bull Case: A Leaner, Meaner, Higher-Margin NETGEAR

The most compelling bull argument centers on the mix shift toward Enterprise. In Q4 2025, Enterprise revenue reached 49% of the total, up from 44% a year earlier, and Enterprise gross margins exceeded 51%. If this trajectory continues, with Enterprise growing to 65% or more of revenue as management targets, NETGEAR's overall margin profile improves dramatically even if total revenue grows modestly. The company would effectively be leaving behind the low-margin consumer commodity business and transforming into a focused SMB and ProAV player.

The WiFi 7 technology itself deserves explanation because the upgrade cycle thesis depends on understanding what WiFi 7 actually delivers. WiFi 7 is not simply "faster Wi-Fi." It introduces three fundamental improvements. First, it supports 320 MHz channels, double the width of WiFi 6E, which means each wireless conversation between your device and the router carries twice as much data per exchange. Think of a channel width as a highway lane: WiFi 7 doubles the number of lanes. Second, it introduces multi-link operation, which allows a device to simultaneously use multiple frequency bands, such as both 5 GHz and 6 GHz at the same time. Previous generations forced devices to pick one band at a time. This is like being able to drive on two highways simultaneously and merge the traffic at your destination. Third, it introduces 4K QAM modulation, a technical improvement that packs more data into each wireless signal. The net result is theoretical speeds of up to 46 gigabits per second, roughly four times faster than WiFi 6E, with dramatically lower latency and better performance when dozens of devices are connected simultaneously.

The ProAV opportunity is genuinely exciting. The transition from traditional AV infrastructure to AV-over-IP is still in its early innings. NETGEAR has established itself as the go-to switch manufacturer for AV integrators, with purpose-built products, strong channel relationships, and a reputation for reliability in this niche. Unlike the consumer router market, ProAV has meaningful switching costs, limited low-cost competition, and growing total addressable market.

WiFi 7 represents the latest upgrade cycle bet. Every new Wi-Fi standard creates a replacement cycle as consumers and businesses upgrade their equipment to take advantage of faster speeds, lower latency, and better performance with multiple devices. WiFi 7, which offers theoretical speeds of up to 46 gigabits per second, support for 320 MHz channels, and multi-link operation that can use multiple frequency bands simultaneously, represents a significant performance leap. If adoption follows historical patterns, it could drive a meaningful revenue tailwind over the next two to three years.

The subscription business, while small, is growing at 22% year over year and adds recurring revenue that smooths the traditionally lumpy hardware revenue cycle. At 555,000 subscribers generating $35 million annually, the unit economics are improving, and there is significant room to increase attach rates as more products include subscription capabilities.

The TP-Link patent settlement demonstrated that NETGEAR's intellectual property portfolio has monetizable value. The $135 million settlement was a one-time event, but the portfolio of networking patents could be a source of ongoing licensing revenue or strategic leverage.

The company also continues to generate cash and has a history of returning capital to shareholders through buybacks. NETGEAR's balance sheet is relatively clean, and the company has maintained financial discipline even through the downturn years, avoiding the debt-fueled acquisitions that have saddled some hardware companies with unsustainable leverage.

Finally, the valuation is compelling if you believe in the transformation. At approximately $783 million in market capitalization, NETGEAR trades at barely one times revenue, a significant discount to the broader technology sector and to networking peers like Ubiquiti, which commands a market cap roughly twenty-eight times its revenue. If the market begins to view NETGEAR as a software-enhanced networking platform rather than a commodity hardware company, there is significant room for multiple expansion.

The Bear Case: Structural Decline That Premium Positioning Cannot Overcome

Bears argue that the consumer networking equipment market is in structural decline for branded manufacturers. ISP-provided equipment eliminates the purchase decision for a growing share of households. TP-Link's combination of low prices and steadily improving quality makes it increasingly difficult for NETGEAR to justify its price premiums. And Amazon's eero, with the world's most powerful e-commerce distribution platform behind it, can be bundled and cross-sold in ways that independent brands cannot match.