NRG Energy: The Power Player's Reinvention Story

I. Introduction & Opening Hook

Picture this: It's December 2022, and Mauricio Gutierrez, CEO of NRG Energy, is about to make a call that would have gotten him laughed out of the boardroom just five years earlier. He's acquiring Vivint Smart Home—a company that installs doorbell cameras and smart thermostats—for $2.8 billion. The traditional energy executives on Wall Street are bewildered. Here's a company that owns coal plants and natural gas turbines, buying a home automation business? The stock drops 16% on the announcement.

But Gutierrez sees something the market doesn't—or at least, not yet. In an era where every kilowatt-hour counts and every customer touchpoint matters, NRG is betting that the future of energy isn't just about generating electrons. It's about owning the entire customer relationship, from the power plant to the smart plug.

Today, NRG Energy stands as a $29.7 billion market cap colossus, generating $29.3 billion in annual revenue. It's simultaneously one of America's largest power producers and one of its biggest retail energy providers, serving 7 million customers across North America. Yet this company's journey—from a Minneapolis utility spinoff to bankruptcy, from coal baron to would-be solar revolutionary, and now to essential home services platform—reads like a business school case study in strategic pivots, failed transformations, and the brutal realities of energy market evolution.

The paradox at the heart of NRG's story mirrors the broader American energy transition itself: How do you transform a fossil fuel-dependent business model while keeping the lights on and investors happy? How do you innovate in an industry where a single power plant can cost billions and operate for decades? And perhaps most intriguingly, how do you convince Wall Street that a coal plant operator can become a tech-enabled consumer services company?

This is the story of NRG Energy—a company that has died and been reborn multiple times, led by visionaries who were either too early or too late, and which today stands at yet another crossroads. It's a tale of boom and bust, of billion-dollar bets and spectacular failures, of activist investors and ousted CEOs. Most importantly, it's a window into the messy, complicated, and utterly fascinating business of keeping America powered in the 21st century.

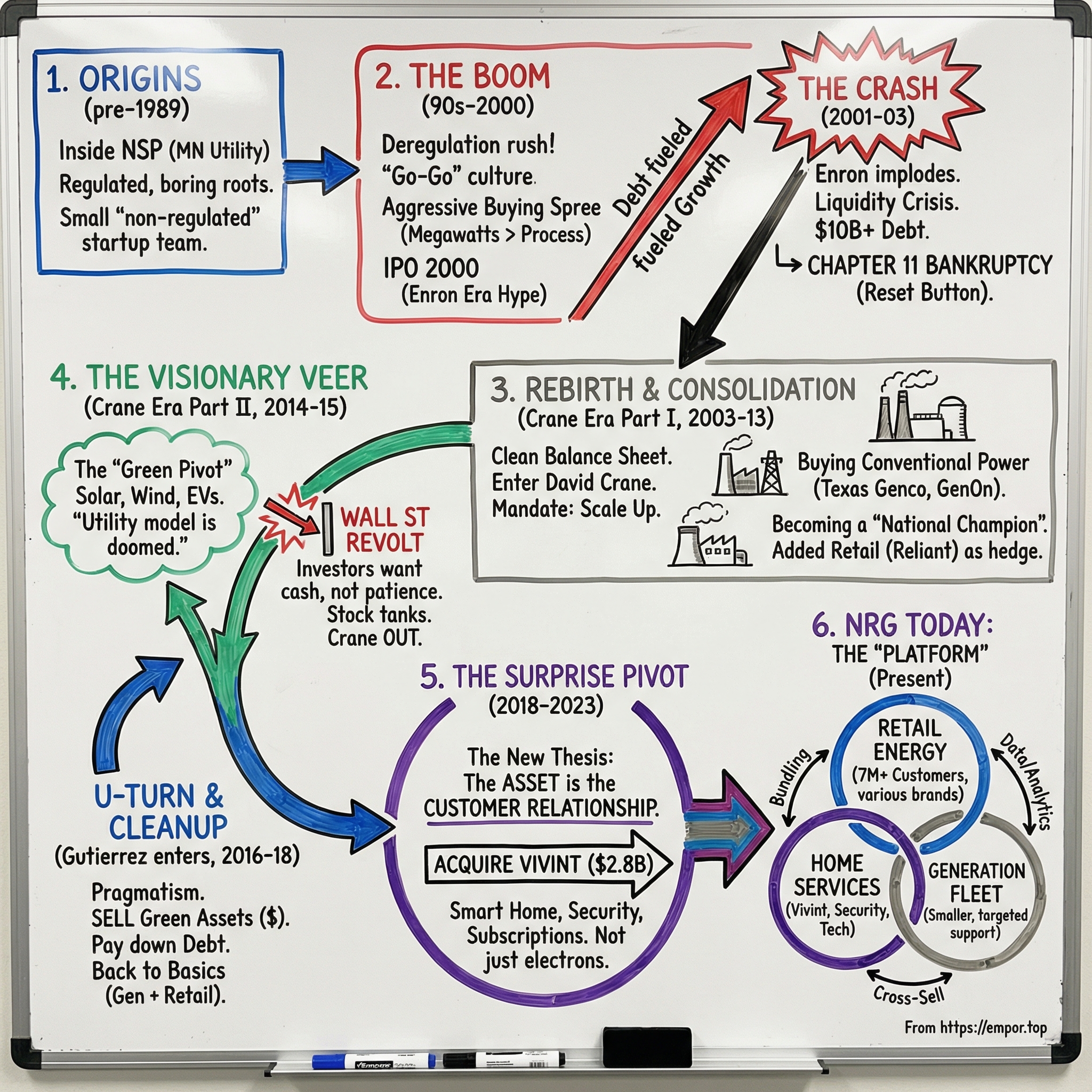

II. Origins: The NSP Spinout Story (1989-2000)

The year was 1989, and inside the corporate offices of Northern States Power Company in Minneapolis, executives were having conversations that would have been unthinkable just a few years earlier. The Federal Energy Regulatory Commission had just opened the door to something revolutionary: non-utility companies could now own and operate power plants. For the staid, regulated utility industry, this was like discovering a new continent.

Northern States Power wasn't just any utility—it carried the DNA of Henry Marison Byllesby, an electrical engineering pioneer who had worked directly with both Thomas Edison and George Westinghouse before striking out on his own. In 1916, Byllesby founded what would become Northern States Power Company, building it into a Midwest powerhouse that served millions across Minnesota, Wisconsin, and the Dakotas. The company culture was conservative, methodical, focused on reliability above all else. But now, seventy-three years later, deregulation was cracking open a world of possibilities.

NSP's leadership made a decision that would prove either prescient or disastrous: they formed NRG Energy as a wholly owned subsidiary to venture into this brave new world of unregulated power generation. The mandate was clear—acquire, build, own, and operate power plants outside NSP's traditional regulated territory. It was like a utility company deciding to become a merchant adventurer.

Dave Peterson was tapped to lead this new venture, heading up an initial team of just ten people operating out of a modest office space in Minneapolis. Peterson wasn't your typical utility executive. He cultivated what insiders described as a "go-go, entrepreneurial culture"—a stark contrast to the button-down conservatism of the parent company. While NSP measured success in decades of reliable service, NRG measured it in megawatts acquired and deals closed.

For the first few years, NRG operated quietly, making small acquisitions and learning the ropes of the merchant power business. But in 1998, something shifted. The company went on an acquisition tear that would make even the most aggressive private equity firms take notice. They started buying power plants from established utilities who were eager to shed assets in the newly deregulated environment—Niagara Mohawk's facilities in New York, San Diego Gas & Electric's generation assets in California, Consolidated Edison's plants on the East Coast.

Each acquisition told a story about the changing American energy landscape. These weren't just power plants; they were the castoffs of a regulated monopoly system that was being dismantled piece by piece. NRG was positioning itself as the buyer of choice, the company that could take these orphaned assets and run them more efficiently in the competitive marketplace.

The pace was breathtaking. By 1999, NRG had accumulated a portfolio of power plants across the United States and had even begun expanding internationally. Revenue exploded from $104 million in 1996 to over $500 million by 1999. The Minneapolis startup was becoming a national player.

Then came the moment that would transform NRG from subsidiary to standalone company: the IPO of 2000. On a crisp spring morning, NRG Energy went public, raising $423 million in what was then the largest IPO of a Minnesota company in history. The offering was oversubscribed, with investors clamoring for a piece of this high-growth power company that seemed perfectly positioned for the deregulated future.

The numbers were intoxicating. NRG now controlled over 20,000 megawatts of generation capacity. To put that in perspective, that's enough power to supply about 15 million homes. The company was valued at over $2 billion, making early employees and executives paper millionaires overnight. In the go-go atmosphere of the late 1990s energy boom, NRG looked unstoppable.

But there was a darker number lurking in the financial statements, one that few were paying attention to amid the euphoria: debt. To fund its aggressive expansion, NRG had borrowed heavily. From $212 million in 1996, the company's debt load had ballooned to over $3 billion by the time of the IPO. It was a leverage ratio that would work brilliantly as long as energy prices stayed high and capital markets remained open.

As Peterson and his team celebrated their public market debut, storm clouds were already gathering. In California, energy prices were starting to spike wildly. In Houston, a company called Enron was pushing the boundaries of energy trading in ways that would soon shock the world. And in Minneapolis, Northern States Power was beginning to have second thoughts about its high-flying subsidiary.

The stage was set for one of the most spectacular collapses in American corporate history. But on that triumphant IPO day in 2000, with champagne flowing and stock prices soaring, nobody at NRG could have imagined that within three years, they would be in bankruptcy court.

III. The Enron Effect: Bankruptcy & Phoenix Rising (2001-2003)

By the summer of 2001, NRG Energy's Minneapolis headquarters had the atmosphere of a trading floor crossed with a war room. Executives were working eighteen-hour days, fielding calls from bankers, negotiating new acquisitions, and watching energy prices spike across deregulated markets. Revenue had exploded to $3 billion—a mind-boggling 2,800% increase from just five years earlier. The company was adding power plants to its portfolio like a collector acquiring rare stamps.

But something was fundamentally wrong with the math. While revenue had grown thirty-fold, debt had grown forty-fold—from $212 million to an astronomical $8.3 billion. NRG had become a highly leveraged bet on energy deregulation, and that bet was about to go spectacularly wrong.

The first domino fell in Houston. On December 2, 2001, Enron filed for bankruptcy in what was then the largest corporate collapse in American history. The energy trading giant's fraud-fueled implosion sent shockwaves through the entire power sector. Suddenly, every energy company that had embraced trading, leverage, and aggressive accounting was suspect. Credit markets, which had been throwing money at power companies just months earlier, slammed shut.

For NRG, the timing couldn't have been worse. The company needed to continuously refinance its massive debt load, and now nobody would lend to them. Energy prices, which had been soaring, began to collapse as the economy weakened. Power plants that NRG had bought at premium prices were suddenly worth a fraction of what the company had paid. It was like watching a Jenga tower wobble in slow motion—everyone knew it was going to fall, but nobody knew exactly when.

Parent company Xcel Energy (the renamed Northern States Power) tried desperately to stop the bleeding. They pumped in emergency capital, guaranteed loans, and even considered merging NRG back into the regulated utility. But it was like trying to bail out the Titanic with a teacup. By early 2003, NRG's auditors were warning of "substantial doubt" about the company's ability to continue as a going concern.

On May 14, 2003, the inevitable happened. NRG Energy filed for Chapter 11 bankruptcy protection, listing $11 billion in assets and $9.4 billion in liabilities. The Minneapolis success story had become a cautionary tale. Employees who had watched their stock options soar were now holding worthless paper. Creditors who had funded the expansion were looking at massive losses.

But here's where the story takes an unexpected turn. Unlike Enron, which was revealed to be built on fraud and would be liquidated, NRG's core business was real. The company owned actual power plants that generated actual electricity for actual customers. The problem wasn't criminality—it was capital structure. NRG had good assets buried under bad debt.

Enter David W. Crane, a Harvard-educated lawyer who had spent years at Lehman Brothers financing power projects. In December 2003, just as NRG was emerging from bankruptcy, Crane was named CEO. He would later describe walking into NRG as "like entering a MASH unit after a particularly bloody battle." Morale was shattered, the best employees were fleeing, and the company's reputation was in ruins.

Crane's first moves were swift and decisive. The bankruptcy had eliminated $5.2 billion of corporate debt plus another $1.2 billion of claims—a massive deleveraging that gave the company breathing room. Xcel Energy, eager to distance itself from the disaster, relinquished ownership entirely. NRG became a fully independent public company, free from its parent but also alone in the harsh competitive marketplace.

The turnaround was almost miraculous in its speed. In 2004, NRG's first full year out of bankruptcy, the company generated $2.36 billion in revenue and $185.6 million in net income—exceeding even the most optimistic projections. The power plants were running well, energy markets had stabilized, and the drastically reduced debt load meant that cash flow could actually accumulate rather than disappear into interest payments.

Crane would later reflect that bankruptcy, paradoxically, had been the best thing that could have happened to NRG. It forced the company to focus on operational excellence rather than financial engineering. It eliminated the crushing debt burden that would have made transformation impossible. And it created a battle-tested culture that knew how to survive the worst.

The employees who stuck through the bankruptcy became the core of the new NRG—scarred but stronger, wary of leverage but hungry for growth. They had learned a brutal lesson about the dangers of debt-fueled expansion, but they had also proven that their underlying business model worked.

As 2004 dawned, NRG Energy was essentially starting over with a clean slate, experienced management, and a portfolio of power plants in an industry that was still sorting itself out after deregulation. David Crane had bigger ambitions than just survival. He was about to embark on one of the most aggressive expansion campaigns the power industry had ever seen—but this time, he would do it differently.

IV. The David Crane Era: Traditional Power Consolidation (2003-2010)

David Crane's first executive decision as CEO might have seemed minor, but it signaled everything about his vision for NRG's future. In 2004, he moved the company's headquarters from Minneapolis to Princeton, New Jersey. "We need to be closer to our markets, closer to Wall Street, closer to the action," he told the board. The Midwest utility subsidiary was dead; in its place would rise an East Coast power conglomerate with national ambitions.

Crane himself was a fascinating character—a lawyer by training who spoke like a visionary, a Wall Street veteran who quoted poetry in earnings calls, and a pragmatist who could be ruthlessly focused on returns. Employees described him as brilliant but mercurial, capable of inspiring devotion and frustration in equal measure. He would often show up to power plants in jeans and sneakers, chatting with operators about turbine efficiency, then fly back to Princeton to negotiate billion-dollar deals in a boardroom.

His strategy in those early years was deceptively simple: consolidate the fragmented American power market while everyone else was still recovering from the Enron hangover. But unlike NRG's pre-bankruptcy acquisition spree, Crane insisted on what he called "financial discipline with strategic vision." Every acquisition had to be immediately accretive to earnings, every plant had to fit into the portfolio, and debt levels would never again approach dangerous territory.

The 2005 expansion set the template. NRG added 7,600 megawatts of domestic capacity in a series of surgical strikes, including acquiring Dynegy's 50% stake in a massive 1,800-megawatt California facility. While other companies dithered, Crane moved fast, often completing due diligence in weeks rather than months. "Speed is our competitive advantage," he would tell his team. "While our competitors are still analyzing, we're already operating."

But the deal that truly announced NRG's return to the big leagues came in 2006: the acquisition of Texas GenCo for $5.8 billion. This wasn't just buying some power plants—it was buying the crown jewels of the Texas electricity market. Texas GenCo owned massive coal and natural gas facilities that powered Houston, Dallas, and San Antonio. Overnight, NRG became the second-largest power generator in Texas, the most deregulated and competitive electricity market in America.

The Texas GenCo acquisition revealed Crane's strategic genius. Texas had fully deregulated its electricity market, meaning power generators could sell directly to consumers through retail electricity providers. Crane saw what others missed: whoever controlled both generation and retail distribution in Texas would have an enormous competitive advantage. You could hedge your generation with your retail book, smooth out price volatility, and capture margin at both ends of the value chain.

This insight drove the next phase of expansion. In 2009, NRG acquired Reliant Energy's Texas retail business for $287.5 million, instantly gaining 1.6 million customers. The following year, they bought Green Mountain Energy, the nation's largest residential provider of renewable energy plans, for $350 million. By 2011, NRG wasn't just generating power—it was selling directly to millions of American homes and businesses.

The numbers from this era are staggering. When Crane took over in 2003, NRG operated about 15,000 megawatts of generation. By 2011, the portfolio had grown to 25,135 megawatts, focused almost entirely on U.S. markets. The company could power roughly 20 million American homes—about one in every six households in the country. Revenue had grown from $2.4 billion to over $9 billion. Market capitalization had increased five-fold.

The 2012-2013 period marked the apex of Crane's traditional power consolidation strategy. First came the acquisition of GenOn Energy for $1.7 billion, adding 21,000 megawatts of generation capacity. Then Edison Mission Energy for $2.6 billion, bringing another 8,000 megawatts. By the end of 2013, NRG controlled an astounding 46,000 megawatts of generation capacity—roughly 4% of all U.S. electricity generation.

To put this in perspective, NRG had become larger than most state utility systems. The company operated 95 power plants across the country, from California to Maine. It employed over 9,000 people. It was, by any measure, one of the largest and most successful independent power producers in American history.

But Crane was already growing restless with this success. At investor conferences, he would show slides of coal plants and natural gas turbines, then suddenly pivot to images of solar panels and electric vehicles. "This," he would say, pointing at the traditional assets, "is our present. But this," gesturing at the renewable technology, "is our future."

In private, Crane was even more direct with his leadership team. "We're building yesterday's energy company to perfection," he said in one strategy session. "But yesterday's perfection is tomorrow's obsolescence." He could see the writing on the wall: renewable costs were plummeting, distributed generation was becoming viable, and climate concerns were moving from the fringe to the mainstream.

By 2013, NRG was generating massive cash flows from its traditional power business. The company had the scale, the market position, and the financial resources to do almost anything. The question was: what would Crane do with this platform he had built? His answer would shock the industry, infuriate investors, and ultimately cost him his job.

V. The Renewable Revolution Attempt (2010-2015)

The scene at NRG's 2013 investor day was electric—and not just because of the subject matter. David Crane stood before a packed auditorium in New York, his usual suit replaced by a black turtleneck that seemed deliberately Jobs-esque. Behind him, instead of the usual slides showing power plant efficiency metrics, was an image of an American suburban home covered in solar panels, a Tesla in the driveway, and a smart meter on the wall.

"Ladies and gentlemen," Crane began, his voice carrying the fervor of a tent revival preacher, "I'm here to tell you that the company you invested in—the one that owns all those coal plants and natural gas turbines—that company is going to disrupt itself before someone else does it for us."

The room was silent. Fund managers who had bought NRG for its stable cash flows and dividend yield looked at each other nervously. One analyst would later describe it as "watching the CEO of McDonald's announce they were going to become a health food company."

Crane's vision was breathtakingly ambitious. He saw a future where every American home would be its own power plant, generating electricity from rooftop solar panels, storing it in basement batteries, and feeding it into electric vehicles. The traditional grid—and traditional power plants—would become backup systems, used only when distributed resources couldn't meet demand. And NRG, rather than fighting this future, would lead it.

The company had already been moving in this direction since 2010, but mostly under the radar. They had quietly assembled a portfolio of 21 clean energy assets with over 2.5 gigawatts of capacity—solar farms in California, wind projects in Texas, and even some experimental battery storage systems. But Crane was ready to go all-in.

In 2014, NRG reorganized itself into three distinct divisions, each with its own leadership and strategic mandate. NRG Energy would manage the traditional fleet of 49,400 megawatts of coal and gas plants—the cash cow that funded everything else. NRG Renew would develop and operate renewable generation, targeting 3,200 megawatts of wind and 1,300 megawatts of solar. And NRG Home—Crane's particular passion—would be the consumer-facing innovation lab, offering everything from rooftop solar installations to home energy management systems.

The Home division was where Crane's vision became most radical. He partnered with Tesla to become one of the first distributors of the Powerwall home battery system. The company launched a rooftop solar installation business that would compete directly with SolarCity. They even developed a smart thermostat called "NRG Echo" that would optimize home energy usage based on real-time electricity prices.

"We're positioning to succeed during a prolonged period where the traditional grid coexists with distributed generation," Crane explained to skeptics. "We'll make money from the old system while building the new one." It was a hedge, he argued—if distributed energy took off, NRG would profit. If it didn't, they still had their traditional business.

The operational momentum was impressive. By 2014, NRG was installing over 100 megawatts of distributed solar annually. The company had signed partnerships with major retailers like Home Depot to offer solar installations. They were even experimenting with peer-to-peer energy trading platforms that would let neighbors sell excess solar power to each other.

But Wall Street was not impressed. The stock price, which had reached $35 in early 2014, began a steady decline. Investors saw Crane pouring capital into unproven technologies while the traditional power business—which generated virtually all of NRG's profits—was being neglected. The renewable projects had long development timelines and uncertain returns. The home services business was burning cash competing with venture-backed startups.

The criticism became increasingly public. During a 2014 earnings call, one analyst asked bluntly: "David, are you running a power company or a science experiment?" Crane's response was defiant: "The stone age didn't end because we ran out of stones. It ended because we found something better. The fossil fuel age won't end because we run out of coal and gas. It will end because we find something better. And I intend for NRG to be the company that finds it."

By late 2015, the situation had become untenable. NRG's stock had tumbled more than 60% from its peak. The company had spent billions on renewable development and home services with little to show for it in terms of profits. Traditional investors were fleeing, and the promised green investors hadn't materialized. Activist shareholders were circling, demanding changes.

The irony was painful. Crane had been right about the direction of the energy transition—solar costs were plummeting, electric vehicle adoption was accelerating, and distributed energy was becoming viable. But he had been too early, had moved too fast, and had failed to bring investors along for the ride. In the stock market, being right too early is indistinguishable from being wrong.

Internal tensions were also mounting. The traditional power generation team felt marginalized and underinvested. The renewable team was frustrated by the constant pressure to show immediate returns. The home services division was hemorrhaging talent to Silicon Valley startups that could offer equity upside without the baggage of a coal plant portfolio. Crane's vision of three businesses working in harmony had devolved into three businesses barely speaking to each other.

The November 2015 board meeting was Crane's last stand. He presented a five-year plan that would double down on the transformation—more solar, more batteries, more consumer services. The board, facing a full-scale investor revolt, gave him an ultimatum: abandon the transformation strategy or resign.

David Crane's decision revealed the depth of his conviction. Rather than betray the vision he believed in, he chose to walk away from the company he had rebuilt from bankruptcy.

VI. The Fall of David Crane & Strategic Reversal (2015-2018)

The December 3, 2015 announcement hit the newswires at 4:01 PM, one minute after market close. "NRG Energy Announces CEO Transition," the headline read—corporate speak for a forced exit. Within seconds, NRG's stock price jumped 6% in after-hours trading. Wall Street was literally celebrating David Crane's departure.

Crane's farewell letter to employees, leaked to the press within hours, was extraordinary in its candor and pain. "I did not succeed in leading you, as I had hoped, to making NRG that shining city on the hill, that beacon of light in an industry that is in need of a path forward," he wrote. "Your new management will have the benefit of rebuilding the foundation we've laid without having to bear the burden of my vision."

The imagery was deliberately biblical, positioning himself as a Moses figure who had led the company toward the promised land but wouldn't be allowed to enter it. Employees who had bought into Crane's transformation vision were devastated. One solar division manager described the mood as "like finding out your startup was being acquired by IBM."

Mauricio Gutierrez, the company's Chief Operating Officer, was named CEO and President. Where Crane was a visionary who quoted poetry, Gutierrez was an operator who quoted EBITDA margins. He had spent his entire career in traditional power generation, rising through the ranks with a reputation for operational excellence and financial discipline. His first all-hands meeting set the tone: "We are a power generation and retail energy company. Period. Full stop."

The strategic reversal was swift and brutal. Within weeks, Gutierrez announced that paying down debt would be the company's top priority—a clear signal that the cash-burning renewable and home services ventures were on the chopping block. "We need to return to our core competencies," he told investors, promising to "optimize our conventional generation fleet and retail platforms."

The dismantling of Crane's vision proceeded with surgical precision. First, the home services division was essentially shut down, with hundreds of employees laid off and partnerships terminated. The smart thermostat project was killed. The rooftop solar installation business was sold for pennies on the dollar. The peer-to-peer energy trading platform disappeared without explanation.

Then came the renewable asset sales. In 2018, NRG announced it would sell its renewable energy development and operations platform to Global Infrastructure Partners for $1.375 billion. The portfolio included 6.6 gigawatts of renewable projects—five years of Crane's work undone in a single transaction. The buyer got world-class solar and wind assets at a discount; NRG got cash to pay down debt and buy back stock.

The numbers tell the story of the transformation. In 2015, under Crane, NRG's generation portfolio was 12% renewable. By 2019, under Gutierrez, it had shrunk to less than 1%. The company that Crane had tried to position as a clean energy leader now generated nearly 90% of its electricity from coal and natural gas—a higher fossil fuel percentage than before his transformation attempt.

But here's the uncomfortable truth: Gutierrez's strategy worked, at least from a shareholder perspective. The stock price, which had bottomed out at $9 in early 2016, recovered to $40 by 2018. The company's credit rating improved. The dividend, which had been cut during Crane's tenure, was restored and then increased. Traditional energy investors returned, appreciating the predictable cash flows and rational capital allocation.

Gutierrez also benefited from market dynamics that Crane had correctly predicted but mistimed. Natural gas prices remained low, making NRG's gas-fired plants highly profitable. The Texas retail energy market, which Crane had built through acquisitions, became a cash machine as the company leveraged its generation assets to offer competitive retail prices. Even as renewable energy grew nationwide, NRG was making more money than ever from fossil fuels.

The cultural transformation was equally dramatic. The Princeton headquarters, which under Crane had taken on a Silicon Valley vibe with meditation rooms and electric vehicle charging stations, reverted to traditional corporate aesthetics. The company stopped attending renewable energy conferences and returned to power generation industry events. The website, which had featured images of happy families with solar panels, now showed industrial power plants and corporate handshakes.

Yet even as Gutierrez executed his back-to-basics strategy, the energy transition Crane had predicted continued to accelerate. Tesla's market cap surpassed that of traditional automakers. Solar became the cheapest form of new electricity generation in most markets. States began mandating aggressive renewable energy targets. The question wasn't whether the energy transition would happen, but whether NRG would be a leader or a laggard when it did.

Some employees who lived through both eras describe a company with a split personality—publicly committed to conventional generation while privately acknowledging that transformation was inevitable. "We all knew David was right about where the industry was heading," one senior executive confided. "He was just wrong about when and how fast. Mauricio bought us time, but he didn't change the destination."

By 2018, with the renewable assets sold and the company refocused on traditional generation, Gutierrez had completed his reversal of Crane's strategy. NRG was once again a conventional power company with a retail arm, generating reliable profits from coal and natural gas. But the world around it was changing faster than ever, and Gutierrez would need a new strategy for the 2020s.

VII. The Pivot to Essential Home Services (2018-2023)

The PowerPoint slide that Mauricio Gutierrez showed the NRG board in September 2022 was deceptively simple. On the left side: a traditional power plant. On the right side: a suburban home with a smart doorbell, intelligent thermostat, and solar panels. In the middle, connecting them: a single word—"Customer."

"Gentlemen and ladies," Gutierrez began, having learned to avoid Crane's messianic tone, "I'm not here to transform the energy industry. I'm here to talk about customer lifetime value and recurring revenue streams."

It was classic Gutierrez—taking a potentially revolutionary idea and wrapping it in the language of MBA textbooks. But what he was proposing was arguably more radical than anything Crane had attempted: NRG would acquire Vivint Smart Home, a home automation and security company, for $2.8 billion.

The journey to this moment had been gradual and deliberate. After selling off Crane's renewable assets, Gutierrez hadn't simply retreated to managing coal plants. Instead, he had been quietly studying what he called "the Amazon model"—starting with one service, then expanding to own the entire customer relationship. If Amazon could go from selling books to controlling half of American e-commerce, why couldn't NRG go from selling electricity to managing the entire home?

The Vivint opportunity emerged almost by accident. Gutierrez had been meeting with Blackstone, which owned Vivint, about a completely different transaction. But as he learned about Vivint's business model, he became intrigued. Here was a company with 1.9 million customers paying an average of $40-60 per month for home security and automation services. The average customer stayed for nine years. The recurring revenue was predictable, the churn was low, and the margins were attractive.

"Think about it," Gutierrez told his leadership team. "We already send an electricity bill to 6 million homes every month. Vivint sends a security bill to 2 million homes. Why not combine them? Why not offer the complete essential home services package?"

The strategic rationale went deeper than just cross-selling. Vivint's smart home devices generated enormous amounts of data about energy usage patterns. When do people come home? When do they adjust their thermostats? When do they turn on their lights? This data, combined with NRG's energy expertise, could enable unprecedented optimization of home energy consumption.

On December 6, 2022, NRG announced the acquisition: $2.8 billion at $12 per share, a 55% premium to Vivint's closing price. The market reaction was brutal. NRG's stock dropped 16% in a single day, erasing $2 billion in market value. Analysts were scathing. "NRG is buying a subscale home security company at a premium price in a competitive market," one wrote. "This is diversification for the sake of diversification."

But Gutierrez had done his homework. He had studied how European utilities like Centrica had successfully expanded into home services. He had analyzed how telecom companies bundled services to reduce churn. He had even hired consultants from Amazon to design the integration strategy.

The March 10, 2023 closing of the acquisition created a unique entity in American business: a company that could power your home, secure it, and automate it. The combined company served 7.4 million customers across North America. It generated over $30 billion in annual revenue. It had relationships with roughly one in every twenty American households.

The integration challenges were formidable. Vivint's door-to-door sales culture clashed with NRG's utility mindset. The technology stacks were incompatible. Regulatory issues arose in states where utilities were restricted from offering non-energy services. But Gutierrez pushed forward, convinced that the long-term opportunity outweighed the short-term pain.

Early results were mixed but encouraging. Cross-selling proved harder than expected—only about 3% of NRG energy customers added Vivint services in the first year. But customer retention improved for both businesses. Vivint customers who also bought NRG energy stayed 18% longer. NRG energy customers who added Vivint services were 25% less likely to switch providers.

The real innovation came from unexpected synergies. Vivint's smart thermostats could be programmed to pre-cool homes when electricity prices were low, saving customers money while helping NRG optimize its generation portfolio. Security cameras could detect when homeowners were away and automatically adjust energy settings. The combined data from both businesses enabled personalized energy plans that no competitor could match.

By late 2023, Gutierrez was ready to unveil his vision for what he called "Essential Home Services 2.0." Beyond electricity and security, NRG would offer home insurance (partnering with carriers who valued the security monitoring), HVAC services (leveraging the smart thermostat data to predict maintenance needs), and even electric vehicle charging (as Vivint's installers were already in homes).

"We're not trying to be a utility or a tech company," Gutierrez explained to investors who were finally warming to the strategy. "We're building the first essential home services platform. Every home needs power. Every home needs security. Every home needs climate control. We're the only company that can deliver all three in an integrated package."

The transformation wasn't without casualties. Traditional power plant operators felt even more marginalized than they had under Crane. Some longtime energy traders left for pure-play generation companies. But new talent was flowing in—data scientists from Google, product managers from Ring, customer experience experts from Netflix.

As 2023 drew to a close, NRG stood transformed yet again. It still owned 13 gigawatts of mostly fossil fuel generation. It still served millions of retail energy customers. But now it also had a direct relationship with millions of homes, generating data, delivering services, and building what Gutierrez called "the operating system for the American home."

Whether this transformation would succeed where Crane's had failed remained an open question. But one thing was clear: NRG had evolved from a power company that happened to have customers into a customer company that happened to generate power.

VIII. Modern NRG: The Multi-Business Platform (2023-Present)

Inside NRG's Houston headquarters on a humid August morning in 2024, Larry Coben, the company's Chairman and CEO, stands before a wall of screens displaying real-time data from across the company's empire. On one screen: power generation metrics from 13 gigawatts of mostly natural gas plants across Texas, the East Coast, and California. On another: customer acquisition numbers from 7 million retail customers across 24 US states and eight Canadian provinces. On a third: home security alerts from 2 million Vivint Smart Home subscribers.

"Every data point you see here," Coben tells a group of visiting analysts, "represents a touchpoint with an American household or business. We're not just in the electron business anymore. We're in the essential services business."

The transformation is remarkable. NRG's brand portfolio now includes Reliant Energy, XOOM Energy, Green Mountain Energy, Stream Energy, Discount Power, and Cirro Energy—each targeting different customer segments and geographies. In Texas alone, where deregulation has created the most competitive electricity market in America, NRG commands a dominant position through multiple brands, allowing it to segment the market from budget-conscious consumers to premium green energy buyers.

The numbers tell a story of operational excellence that would have seemed impossible during the Crane era. NRG's Smart Home segment delivered over 5% net subscriber growth, 6% margin expansion, and a record-high retention rate of 90% in 2024. The retail energy business continued to deliver strong margins while the company's generation fleet achieved an excellent 88% In-the-Money-Availability—industry jargon for plants being available when electricity prices make them profitable to run.

The Vivint integration, despite initial skepticism, is beginning to show results. The combined platform now offers what Gutierrez calls "the complete home ecosystem"—electricity, natural gas, home security, smart home automation, and even HVAC services through partnerships. A customer in Dallas can get their electricity from Reliant, their home security from Vivint, and their air conditioning maintained through NRG's service partners, all on a single monthly bill.

The data advantage is becoming increasingly apparent. Vivint's smart home devices generate terabytes of information about energy usage patterns—when people wake up, when they leave for work, when they return home, how they respond to temperature changes. This data, combined with NRG's energy market expertise, enables unprecedented optimization. The company's SpaceTag analytics platform can now predict with 92% accuracy when a customer will need HVAC maintenance based on usage patterns, potentially saving hundreds of dollars in emergency repairs.

But perhaps the most intriguing development is NRG's quiet positioning for the artificial intelligence boom. The company has entered into Letters of Intent with two leading data center developers, Menlo Equities and PowLan, targeting 400 MW of retail supply in the initial phase, with potential to scale to 6.5 GW, with work expected to start in 2026. Data centers, which power everything from ChatGPT to Netflix, are becoming the new industrial energy consumers, requiring massive amounts of reliable, 24/7 power.

NRG has signed a strategic Project Development Agreement with GE Vernova and Kiewit to develop up to 5.4 GW of new gas-fired, combined cycle generation projects, with priority given to Texas and East region sites, expected to commence operations by the end of 2029. This isn't a return to fossil fuels for ideology—it's a pragmatic response to the reality that renewable energy alone cannot meet the baseload demands of a digital economy.

The retail energy business, often dismissed by analysts as a commodity operation, has become a sophisticated customer acquisition and retention machine. By bundling energy with home services, NRG has reduced customer churn to historic lows. The average customer lifetime value has increased by 40% since the Vivint acquisition, as customers who bundle services are significantly less likely to switch providers.

The geographic footprint is equally impressive. In deregulated markets across Texas, the Northeast, and parts of the Midwest, NRG can offer competitive energy prices by optimizing between its generation assets and wholesale market purchases. In regulated markets, the Vivint platform provides entry without the need for generation assets. The 2021 acquisition of Direct Energy for $3.625 billion added more than 3 million retail customers across 50 US states and 6 Canadian provinces, making NRG truly North American in scope.

Yet challenges remain formidable. The company still operates significant coal and natural gas generation in an era of increasing climate consciousness. Young consumers, particularly in urban markets, are increasingly choosing providers based on environmental credentials. NRG's answer has been to maintain Green Mountain Energy as a 100% renewable brand while using its traditional brands for price-conscious consumers—a strategy that works but feels increasingly antiquated.

Competition is intensifying from unexpected quarters. Amazon is experimenting with energy services. Google is investing in renewable energy and smart home technology. Tesla's energy division is growing rapidly. These tech giants have deeper pockets, stronger brands, and more advanced technology capabilities than NRG. The question is whether NRG's deep energy market expertise and existing customer relationships will prove more valuable than Silicon Valley's innovation engine.

As Larry Coben noted in the latest earnings call: "NRG had a stellar year, executing across all our strategic priorities. Our Adjusted EPS exceeded the top end of raised guidance, we announced the first-of-its-kind residential VPP of scale through our Renew Home and Google Cloud partnerships, and we delivered on our capital allocation commitments". The virtual power plant (VPP) initiative, which aggregates thousands of home batteries and smart devices to create a distributed power resource, represents the kind of innovation that even Crane might have admired.

Financial performance has been robust. For 2024, the company reported Adjusted EBITDA of $3.8 billion and Free Cash Flow before Growth of $2.1 billion. The company returned $1.263 billion to shareholders through $925 million in share repurchases and $338 million in dividends, demonstrating the cash-generative nature of the business model.

Looking at NRG today, one sees a company that has learned from its past—both its successes and failures. It's neither the aggressive acquirer of the pre-bankruptcy era nor the visionary renewable champion of the Crane years. Instead, it's something more pragmatic and perhaps more sustainable: a platform company that monetizes essential services to American homes and businesses, using whatever mix of generation, retail, and services makes economic sense.

IX. Playbook: Strategic Lessons & Business Model Analysis

The conference room at Harvard Business School is packed with MBA students, all eager to dissect what one professor calls "the most fascinating case study in American energy." On the board, she's written a simple question: "What is NRG Energy's sustainable competitive advantage?" The answers from students range wildly—vertical integration, customer relationships, data analytics, financial engineering. The professor smiles. "You're all right," she says, "and you're all wrong."

The NRG story offers a masterclass in the conglomerate curse—that peculiar corporate affliction where the sum of the parts appears less valuable than the whole, at least in the eyes of Wall Street. David Crane learned this lesson painfully. His vision of an integrated clean energy company made strategic sense, but it violated a fundamental rule of public markets: investors want predictability, not revolution. They buy energy stocks for dividends, not disruption.

Yet Mauricio Gutierrez's subsequent strategy suggests the conglomerate model can work—if executed with discipline. The key insight: in commodity businesses like energy, the only sustainable advantages are scale, operational excellence, and customer relationships. Everything else is arbitrage that eventually gets competed away.

Consider the retail energy arbitrage opportunity that forms the core of NRG's business model. In deregulated markets, NRG can source power from three places: its own generation fleet, bilateral contracts with other generators, or spot markets. By dynamically optimizing across these sources, the company can offer competitive retail prices while maintaining healthy margins. It's a complex optimization problem that requires sophisticated trading capabilities, deep market knowledge, and significant capital—barriers that keep smaller players out.

The genius of the Vivint acquisition becomes clearer when viewed through the lens of platform economics versus generation economics. A power plant is a 30-40 year asset that requires massive upfront capital and generates returns based on volatile commodity prices. A customer relationship is a renewable asset that generates predictable monthly cash flows and actually becomes more valuable over time as switching costs increase. By shifting the business mix toward customer relationships, NRG is transforming its economic profile from cyclical to recurring.

The data play is perhaps the most underappreciated aspect of NRG's strategy. Every smart thermostat, doorbell camera, and energy management system is a sensor generating valuable information. When aggregated across millions of homes, this data becomes a moat. NRG knows when neighborhoods are likely to experience peak demand, which customers are price-sensitive versus convenience-oriented, and how weather patterns affect consumption. This information advantage compounds over time.

But let's address the elephant in the room: why would a power company buy a home security company? The answer lies in what venture capitalists call "customer acquisition cost" (CAC) and "lifetime value" (LTV). In the retail energy business, CAC can exceed $300 per customer, and average customer life is just 2-3 years. In the home security business, CAC is similar, but customers stay for 8-9 years. By cross-selling between the two, NRG can dramatically improve unit economics.

The capital allocation framework reveals another layer of sophistication. Unlike Crane, who poured capital into speculative renewable projects, Gutierrez has maintained strict return hurdles. Every investment must generate returns above the cost of capital within a defined timeframe. This discipline has allowed NRG to fund growth while returning significant capital to shareholders—a balance that eluded previous management teams.

Managing through energy transition uncertainty requires a portfolio approach that NRG has finally mastered. The company maintains optionality across multiple scenarios: if renewable adoption accelerates, they can leverage their retail platform to source green power; if natural gas remains dominant, their generation fleet provides advantage; if distributed energy takes off, their customer relationships become even more valuable. It's not betting on a single future but positioning to win in multiple futures.

The role of regulation and policy in shaping strategy cannot be overstated. NRG operates in a patchwork of regulated and deregulated markets, each with different rules, incentives, and competitive dynamics. In Texas, where full deregulation exists, NRG can leverage its integrated model fully. In regulated states, it must operate differently, focusing on services rather than commodity energy. This regulatory arbitrage—operating different models in different markets—is a core competency that took decades to develop.

One fascinating aspect is how NRG has learned to manage activist investors and market expectations. After the Crane debacle, the company has been careful to under-promise and over-deliver, setting conservative targets and beating them consistently. This has rebuilt credibility with investors who were burned by previous management's moonshot ambitions.

The competitive response strategy shows evolved thinking. Rather than trying to out-innovate tech companies or out-subsidize renewable developers, NRG has chosen to be a "fast follower"—letting others prove new technologies and business models, then acquiring or partnering once the path is clear. This approach sacrifices first-mover advantage but dramatically reduces risk.

The human capital strategy has also evolved. Where Crane tried to hire Silicon Valley technologists who didn't understand energy markets, Gutierrez has built a hybrid team—energy market veterans who appreciate technology and technologists who understand energy. This cultural bridge-building, while less sexy than hiring from Google, has proven more effective.

Perhaps the most important lesson from NRG's journey is about timing in capital-intensive industries. Being right too early is indistinguishable from being wrong. Crane's renewable vision was correct—solar and wind are now the cheapest forms of new generation in most markets. But he moved before the economics made sense, before investors were ready, and before the technology was mature. Gutierrez's more modest transformations have succeeded precisely because they're incremental rather than revolutionary.

X. Bear vs. Bull Case & Valuation

The Zoom call connects institutional investors from Boston to Singapore, all waiting for the star analyst from Morgan Stanley to deliver her verdict on NRG Energy. "Ladies and gentlemen," she begins, "NRG is either the most undervalued utility in America or a melting ice cube dressed up as a platform company. Let me explain why reasonable people can reach opposite conclusions."

The Bull Case: Essential Services Platform with Compounding Advantages

The bulls see NRG as a misunderstood platform company trading at utility multiples. Start with the customer base: 7+ million relationships across energy and home services, generating predictable monthly revenue with improving retention metrics. This isn't your grandfather's utility—it's a subscription business with energy attached.

The cross-sell opportunity alone could double the company's earnings. Currently, less than 5% of energy customers have Vivint services, and fewer than 10% of Vivint customers buy NRG energy. If the company can increase penetration to even 20%—well below what telecom companies achieve with bundling—the incremental revenue would be enormous. Every 1% increase in cross-sell penetration adds approximately $50 million in annual recurring revenue.

The data center and AI electricity demand surge represents a generational opportunity. As noted in their latest filing, "The electric industry is anticipating enhanced demand in future years driven by new manufacturing, industrial, and data center facilities". NRG's existing infrastructure, grid connections, and development expertise position it perfectly to capture this demand. A single large data center can consume as much electricity as 50,000 homes—and they need 99.999% reliability that only sophisticated operators can provide.

The home electrification megatrend is another massive tailwind. As electric vehicles, heat pumps, and home batteries proliferate, residential electricity consumption could double by 2035. NRG isn't just selling more electrons—it's becoming the orchestrator of increasingly complex home energy systems. The company that manages this complexity while providing simple solutions to consumers will capture enormous value.

Valuation metrics support the bull case. NRG trades at roughly 8x forward EBITDA, compared to regulated utilities at 12x and home services companies at 15x. If the market rerates NRG as a hybrid platform rather than a traditional generator, the stock could double. With $2.1 billion in annual free cash flow and a market cap of $30 billion, the company yields nearly 7% on a free cash flow basis—extraordinary for a company with secular growth drivers.

The capital allocation strategy creates a virtuous cycle. By returning 80% of free cash flow to shareholders while investing 20% in high-return growth projects, NRG can compound value while maintaining investor confidence. The recent share buyback authorization of $3 billion represents 10% of market cap—a massive vote of confidence from management.

The Bear Case: Stranded Assets in a Disrupting Industry

The bears see a fossil fuel dinosaur trying to dress up as a tech company. Start with the core generation business: 90% fossil fuels in an era of aggressive decarbonization. These aren't just stranded assets—they're future liabilities. Carbon pricing, emissions regulations, or changing social attitudes could render these plants worthless long before their mechanical lives end.

The distributed energy disruption threat is existential. Every rooftop solar installation, every Tesla Powerwall, every community microgrid reduces demand for centralized generation and traditional retail energy. NRG is trying to platform-ize a business model that technology is fundamentally disrupting. It's like Blockbuster buying Netflix in 2005—too little, too late.

Regulatory and policy risk looms large. A change in administration, a shift in state policies, or federal renewable mandates could devastate NRG's economics overnight. The company operates in a political environment where energy policy has become increasingly partisan and unpredictable. One legislative stroke could strand billions in assets.

Integration execution challenges are mounting. Combining an energy company with a home services company isn't just operationally complex—it's culturally impossible. The door-to-door sales culture of Vivint clashes with the engineering culture of power generation. Customer service expectations differ. Technology stacks don't communicate. The promised synergies may never materialize.

The debt burden from acquisitions constrains flexibility. While leverage ratios look manageable at 2.5x-2.75x net debt to EBITDA, this assumes stable cash flows. A sustained period of low power prices, a recession reducing demand, or integration failures could quickly make the debt unsustainable. The company has less financial flexibility than it appears.

Competition from deep-pocketed tech giants poses an existential threat. Amazon, Google, and Apple have all shown interest in home energy management. They have better technology, stronger brands, and infinite capital. When they decide to enter seriously, NRG's advantages could evaporate overnight.

The customer acquisition cost math may not work. While bundling theoretically reduces CAC, in practice, selling multiple products increases complexity and potentially reduces close rates. The company might be trading higher margins for higher costs, with no net benefit to unit economics.

The Valuation Reality

The truth, as it often does, lies somewhere in between. NRG is neither a pure platform play nor a pure fossil fuel company. It's a transitional business model—generating significant cash from legacy assets while building options for multiple futures.

Using a sum-of-the-parts analysis reveals the complexity. The generation business, despite ESG concerns, probably warrants 6-7x EBITDA given its Texas concentration and operational excellence. The retail energy business deserves 8-10x given its scale and customer relationships. The Vivint business could command 12-15x based on recurring revenue and growth profile. Blended together, fair value sits around 9-10x EBITDA, suggesting modest upside from current levels.

The key variables for investors to monitor: cross-sell penetration rates, customer acquisition costs, renewable energy adoption curves, and data center demand materialization. Each could swing the valuation by 20-30%.

Risk-adjusted returns appear favorable for patient investors. The 3% dividend yield provides income while waiting for the transformation thesis to play out. The aggressive buyback program provides support during volatility. And the platform transformation, while uncertain, offers significant optionality.

XI. Epilogue: What Would We Do?

Imagine you're sitting in Mauricio Gutierrez's chair, looking out over Houston's energy corridor, contemplating NRG's next chapter. The board has given you full authority. Shareholders trust your judgment. You have $2 billion in annual free cash flow to deploy. What would you do?

The energy transition dilemma presents the fundamental strategic question. You know fossil fuels will decline—the question is when and how fast. Moving too early, as Crane learned, destroys value. Moving too late risks obsolescence. The answer isn't to bet on timing but to build optionality. Keep the gas plants running and generating cash, but invest those proceeds in building capabilities for multiple futures.

The platform versus pure-play strategy debate misses the point. NRG will never be valued like a software company, and it shouldn't try. But it also can't remain a traditional generator. The sweet spot is being an "essential services" provider—not sexy, but indispensable. Every home needs electricity, security, and climate control. The company that provides all three with simplicity and reliability will endure regardless of technology changes.

Capital allocation priorities should follow a clear hierarchy. First, maintain the dividend—it attracts a stable shareholder base and enforces discipline. Second, buy back stock opportunistically when the market undervalues the transformation. Third, invest in high-return projects that strengthen the platform—customer acquisition, technology upgrades, strategic bolt-on acquisitions. Finally, preserve flexibility for major strategic moves when opportunities arise.

The innovation versus optimization balance requires nuance. NRG shouldn't try to out-innovate Google or Tesla. But it also can't simply optimize yesterday's business model. The approach should be "practical innovation"—adopting proven technologies that enhance customer value and operational efficiency. Be a fast follower, not a bleeding-edge pioneer.

Here's what we would do: Double down on the platform strategy but with radical simplification. Create a single brand for consumers—"NRG Home"—that encompasses energy, security, and home services. Invest heavily in technology integration to make the customer experience seamless. Build or acquire capabilities in electric vehicle charging, home battery systems, and energy management software.

On the generation side, we'd be ruthlessly pragmatic. Keep the efficient gas plants running—they'll be needed for decades to balance renewable intermittency. But commit to no new fossil fuel development. Instead, partner with renewable developers to secure long-term clean energy supplies for retail customers. The goal isn't to own renewable generation but to control customer relationships.

The data strategy needs acceleration. Every customer touchpoint should generate actionable intelligence. Invest in artificial intelligence and machine learning capabilities to predict customer needs, optimize energy procurement, and identify new service opportunities. The company with the best algorithms will win the customer relationship battle.

Geographic expansion should focus on deregulated markets where the integrated model works best. Texas, the Northeast, and select Midwest markets offer the best opportunities. Avoid regulated states except through the Vivint platform. International expansion is a distraction—North America offers sufficient growth for decades.

The cultural transformation might be the hardest but most important change. NRG needs to evolve from an asset operator to a customer company. This means different metrics (lifetime value over megawatts), different capabilities (software over hardware), and different people (customer experience experts alongside engineers).

Most critically, we'd prepare for discontinuous change. The energy industry will face step-function disruptions—mass electric vehicle adoption, viable long-duration storage, carbon pricing, or breakthrough technologies. NRG can't predict which will happen when, but it can build resilience to survive and adaptability to thrive regardless.

The final reflection on transformation attempts reveals a profound truth: In industries with massive installed bases and essential services, revolution usually fails while evolution succeeds. Crane tried revolution and failed spectacularly. Gutierrez is attempting evolution and succeeding modestly. The next leader will need to accelerate evolution without triggering revolution—a delicate balance that will determine whether NRG becomes the energy platform of the future or the last great fossil fuel company.

Looking at NRG's journey from Minneapolis utility subsidiary to Houston-based platform company, from bankruptcy to billions in market value, from coal plants to smart homes, one thing becomes clear: this is a company that has died and been reborn multiple times, each incarnation shaped by the energy realities of its era. The current incarnation—part generator, part retailer, part platform—may not be elegant, but it's adapted to the messy reality of American energy in the 2020s.

The question for investors isn't whether NRG is a perfect company—it's not. The question is whether it's positioned to generate attractive returns while navigating an uncertain energy transition. On that measure, NRG Energy might just be one of the most interesting bets in American business today.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube