ServiceNow: The Platform That Ate the Enterprise

I. Introduction & Episode Roadmap

Picture this: It's November 5th, 2003. A 49-year-old engineer sits alone at a desk in his San Diego home, staring at a single laptop. Fred Luddy has just quit his job, his savings are running low, and he's given himself an ultimatum—start a company today or give up the dream forever. What happens next will reshape how every Fortune 500 company operates, creating a $200 billion empire from what began as glorified help desk software.

ServiceNow today stands as an American software giant based in Santa Clara, California, supplying a cloud computing platform that orchestrates automated business workflows across the world's largest enterprises. But that clinical description misses the magic. This is the story of how a bankrupt engineer's obsession with simplicity became the operating system for modern business—a platform so powerful it makes Salesforce look like a point solution.

The central question driving our narrative: How did help desk software built by a solo founder at 49 become a $200 billion workflow automation empire that runs everything from Coca-Cola's supply chains to the U.S. Department of Defense's operations?

We'll trace three distinct eras of leadership—Fred Luddy's founder vision, Frank Slootman's operational excellence, and Bill McDermott's platform empire—each building on the last to create something unprecedented in enterprise software. Along the way, we'll uncover the key themes that define ServiceNow: the power of platform thinking over point solutions, organic growth at unprecedented scale, and the counterintuitive insight that simplicity, not complexity, wins the enterprise.

This isn't just another SaaS success story. It's a masterclass in timing, execution, and the rare ability to see around corners—to understand that every company's digital transformation would eventually need a single system of record for work itself. As we'll discover, ServiceNow didn't just ride the cloud wave; it created an entirely new category that others are still trying to understand.

The structure ahead mirrors the company's evolution: from Fred's laptop to first product-market fit, through the crucible of hypergrowth that nearly killed the company, into the public markets under three different CEOs, and finally to today's AI-powered platform generating over $10 billion in revenue. Each phase reveals new lessons about building enduring enterprise value.

So settle in for a journey that spans two decades, three CEOs, and one relentless idea: that work should flow as naturally through organizations as conversation flows between people. By the end, you'll understand why ServiceNow might be the most important enterprise software company you've never really understood—until now.

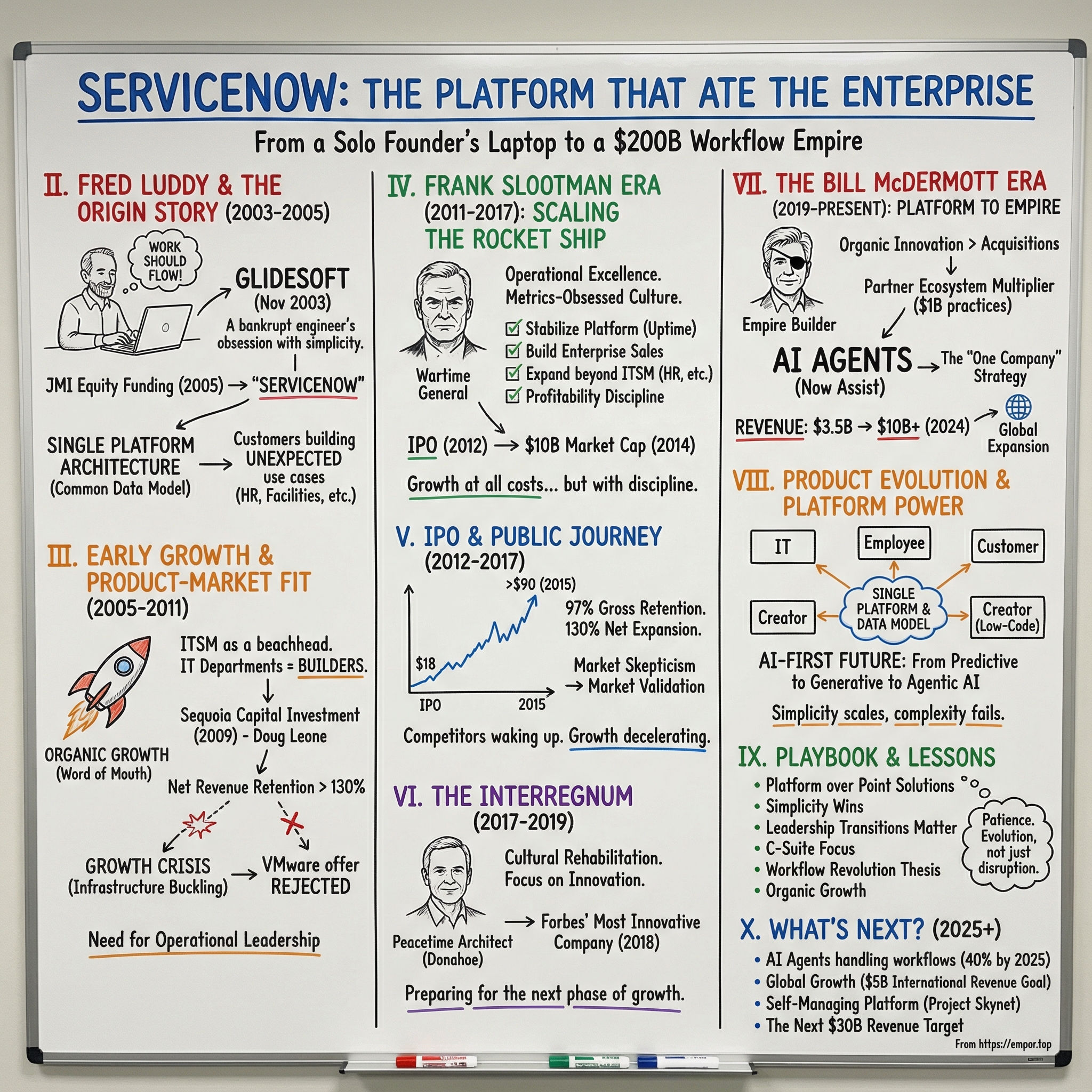

II. Fred Luddy & The Origin Story (2003–2005)

The clock struck midnight on November 5th, 2003, marking Fred Luddy's 49th birthday. But instead of celebration, Luddy sat hunched over his laptop in his San Diego home office, writing code with the desperate energy of a man who'd given himself one last chance. "If I don't start this company today," he'd told himself, "I never will." The deadline wasn't arbitrary—it was survival.

Eighteen months earlier, Luddy had watched his world collapse. As Chief Technology Officer of Peregrine Systems, he'd helped build one of the enterprise software industry's brightest stars, only to see it implode in a $100 million accounting fraud scandal that would send executives to prison. The bankruptcy in September 2002 didn't just end Peregrine—it wiped out Luddy's savings, his stock options, everything. At 48, he was starting from financial ruin.

But Luddy carried something more valuable than money: a decade of watching enterprise software fail its users. At Peregrine, he'd seen IT departments drowning in complexity—ticketing systems that required weeks of training, workflows that broke with every update, platforms that promised everything but delivered frustration. "The industry had it backwards," Luddy would later explain. "They built for features, not for humans."

His insight was deceptively simple: What if enterprise software worked like consumer software? What if it was so intuitive that users could configure it themselves? Not just for IT tickets, but for any business process that involved moving work from person to person. The idea consumed him through 2003 as he scraped by on consulting work, sketching database schemas on napkins, dreaming of something he called "Glidesoft"—software that would let work glide through organizations.

That November night, Luddy incorporated Glidesoft, Inc. in California with himself as sole employee, sole investor, and sole believer. His "headquarters" was a spare bedroom. His development environment was a single Dell laptop. His business plan fit on one page: Build a platform for managing work that was so simple, so flexible, that it could transform from help desk software into... anything.

The early months were brutal. Luddy coded eighteen-hour days, surviving on savings that dwindled toward zero. But word began to spread in San Diego's tight-knit tech community about the former Peregrine CTO building something revolutionary. By early 2004, volunteers started showing up—engineers and salespeople who'd worked with Fred before, who believed in his vision enough to work without pay.

"Fred had this quality," recalls Pat Casey, one of the first volunteers who'd later become employee number three. "He could make you see the future so clearly that you'd mortgage your house to be part of it." Several early believers literally did, working nights and weekends while keeping day jobs to pay bills, gathering in Luddy's living room to debug code and dream about disrupting giants like BMC and Computer Associates.

The breakthrough came through serendipity. In late 2004, Luddy demonstrated his platform at a small IT conference in San Francisco. In the audience sat David Stein from JMI Equity, a growth equity firm that specialized in software. Stein watched Luddy configure a complete IT ticketing workflow in under five minutes—something that took competitors' products weeks of professional services. "I'd seen a hundred ITSM demos," Stein later recounted. "This was the first one where the customer could actually do it themselves."

JMI moved fast. By mid-2005, they'd wired $2.5 million to Glidesoft—not a massive check, but enough for Luddy to make his first five official hires, pay the volunteers who'd sustained the dream, and move out of his house into a small office in Solana Beach. The funding came with one condition: the name had to change. "Glidesoft" sounded like a mattress company, the investors argued. After weeks of brainstorming, they landed on "ServiceNow"—a name that captured both the immediate value proposition and the real-time nature of the platform.

But the most important decision Luddy made in those early days had nothing to do with funding or naming. It was architectural—and it would define ServiceNow's trajectory for the next two decades. Rather than building a series of applications, Luddy created a single platform with a common data model that could be infinitely extended. Every customer would share the same underlying codebase, updated weekly. Customizations would be configurations, not code changes. Multi-tenancy would be built in from day one.

"Everyone thought I was crazy," Luddy reflected years later. "Why constrain yourself to one architecture? Why not build best-of-breed applications?" But Luddy had seen the integration nightmares at Peregrine, the version control disasters, the upgrade paralysis. He believed that simplicity at the platform level would enable complexity at the business level—that constraints would paradoxically create freedom.

By late 2005, ServiceNow had seven employees, a handful of paying customers, and revenue measured in thousands, not millions. But something extraordinary was happening: IT managers who bought ServiceNow for help desk tickets were discovering they could extend it themselves—to manage assets, handle change requests, automate approvals. Without any marketing, customers were finding use cases Luddy hadn't imagined.

The platform wasn't just working; it was spreading organically through organizations like a beneficial virus. IT departments, traditionally seen as cost centers and obstacles, were suddenly becoming innovation hubs, building workflow applications for HR, facilities, even finance. The implications were staggering: ServiceNow wasn't just competing with IT service management vendors. It was creating an entirely new category—a platform for platforms, a system for building systems.

As 2005 drew to a close, Fred Luddy's deadline bet was paying off in ways he couldn't have imagined. The company that started with one man and one laptop now had the seedlings of something transformative. But success would bring its own challenges. The infrastructure that worked for dozens of customers would buckle under hundreds. The founder who could charm early adopters would struggle with enterprise sales. The platform built for simplicity would face demands for complexity.

The next phase would require a different kind of leadership—and it would nearly kill the company before propelling it to heights no one, not even Fred Luddy in his most optimistic moments, could have foreseen.

III. Early Growth & Product-Market Fit (2005–2011)

The YouTube homepage loaded slowly on Fred Luddy's laptop in early 2007, but when the video finally played, he couldn't believe what he was seeing. A customer—without prompting, without payment—had created a twelve-minute tutorial showing how to build a complete employee onboarding workflow in ServiceNow. The video had thousands of views. IT managers were teaching each other how to extend his platform into areas Luddy had never imagined. "That's when I knew," he'd later say, "we weren't selling software anymore. We were leading a movement."

By 2007, ServiceNow had reached $13 million in revenue and finally moved into proper Silicon Valley offices in San Jose. But the numbers only told part of the story. Between 2005 and 2009, revenue exploded from $850,000 to over $45 million—a 170% compound annual growth rate achieved with just $7.5 million in total venture funding. Even more remarkably, the company had been profitable since 2007, generating cash from operations while most SaaS companies burned through hundreds of millions.

The secret was ServiceNow's platform approach, which turned every customer into a product development partner. Starting with IT Service Management as the beachhead, the company had discovered something profound: IT departments weren't just buyers—they were builders. Given the right tools, they'd extend ServiceNow far beyond help desk tickets into every corner of the enterprise.

"Fred's genius wasn't technical," explains Don Schuerman, an early customer who became a board advisor. "It was anthropological. He understood that IT managers were frustrated creators, trapped maintaining systems instead of building them. ServiceNow gave them superpowers."

The platform's simplicity was its strength. While competitors like BMC Remedy required armies of consultants and months of implementation, ServiceNow could be deployed in days. The entire platform ran on a single architecture—one database schema, one user interface framework, one workflow engine. Every customer was on the same version, updated weekly with no downtime. Customizations were just configurations stored as data, not code changes that broke with every upgrade.

This architectural decision seemed limiting but proved liberating. A pharmaceutical company could build a drug trial management system using the same building blocks as a retailer creating a store inspection app. The platform became a kind of enterprise LEGO set—standardized pieces that could be assembled into anything.

But by 2009, success was becoming its own crisis. Customer growth had outpaced infrastructure investment. The platform that hummed along smoothly with hundreds of customers was groaning under thousands. Response times degraded. Outages increased. Enterprise customers who'd bet their operations on ServiceNow were getting nervous.

"We were victims of our own success," Luddy admitted. "I'd built a platform that could scale infinitely in theory but was hitting very real limits in practice." The company needed capital—not just for servers and data centers, but for the enterprise-grade infrastructure that would let ServiceNow compete with established giants.

Enter Doug Leone of Sequoia Capital. Leone had been tracking ServiceNow since 2008, initially skeptical of another ITSM vendor in a crowded market. But when he dug deeper, he discovered something extraordinary: net revenue retention above 130%, meaning existing customers were expanding their spending by 30% annually without any sales effort. Customer acquisition costs were negligible—word of mouth drove most new deals. And the platform architecture meant ServiceNow could enter new markets without building new products.

"I've seen a lot of companies," Leone would later tell Forbes, "but I'd never seen organic growth at this scale with this capital efficiency. They'd essentially bootstrapped to $50 million in revenue."

Sequoia invested $41.5 million in 2009, valuing ServiceNow at around $400 million. But Leone brought more than capital. He brought pattern recognition from decades of enterprise software investing. And what he recognized was troubling: ServiceNow had product-market fit but lacked the operational infrastructure to capitalize on it. The company was, in his memorable phrase, "90 days from going out of business"—not from lack of customers, but from inability to serve them.

The infrastructure rebuild of 2010-2011 was ServiceNow's crucible moment. The company migrated from managed hosting to building its own data centers. It redesigned the platform's core architecture for multi-region deployment. It implemented enterprise-grade security, compliance, and disaster recovery. All while maintaining 99.9% uptime for existing customers and continuing to ship weekly updates.

But the biggest challenge wasn't technical—it was cultural. ServiceNow had thrived as a product-led company where customers discovered value themselves. Now enterprise sales teams were demanding traditional proof-of-concepts, RFPs, and complex pricing negotiations. The company that had succeeded by being different was being forced to become more like everyone else.

Luddy struggled with this transition. The founder who'd built ServiceNow on simplicity watched as enterprise requirements added complexity. The CEO who'd managed by walking around a single office now had hundreds of employees across multiple locations. The visionary who'd imagined a new way of working was spending his days in budget meetings and board presentations.

By late 2011, ServiceNow faced an inflection point. VMware had offered $2.5 billion to acquire the company—a staggering return for a business with less than $100 million in revenue. The board was tempted. Luddy was exhausted. The enterprise transformation was only half-complete.

But Doug Leone saw something others missed. The IT Service Management market was just the tip of the iceberg. Every large company had dozens of departments that needed workflow automation. The real opportunity wasn't selling to IT—it was using IT as a wedge to transform entire enterprises. ServiceNow could become not just a successful software company, but a platform as fundamental as Windows or AWS.

Leone convinced the board to reject VMware's offer. But he had one condition: ServiceNow needed a CEO who could transform a brilliant product into a world-class company. Someone who understood enterprise sales, could build scalable operations, and had the presence to sell to Fortune 500 CEOs.

That search would lead to one of the most successful leadership transitions in Silicon Valley history—and the beginning of ServiceNow's transformation from promising startup to enterprise software giant. The platform Fred Luddy had built in his spare bedroom was about to meet the operator who could take it global.

IV. The Frank Slootman Era: Scaling the Rocket Ship (2011–2017)

Frank Slootman's first day as ServiceNow CEO in April 2011 began with him sprawled on the data center floor at 2 AM, personally debugging a critical outage that had taken down half their customers. "I'd never seen a CEO literally under the raised floor pulling cables," recalled David Schneider, the infrastructure head who'd been there all night. "But Frank looked at me and said, 'This is my problem now. Every customer outage is my problem.'"

Slootman had arrived with a reputation as Silicon Valley's ultimate turnaround artist—the executive who'd transformed Data Domain from near-bankruptcy to a $2.4 billion EMC acquisition. But what he found at ServiceNow was worse than advertised. Doug Leone's assessment of "90 days from going out of business" was optimistic. Customer churn was accelerating. The platform couldn't handle enterprise workloads. Most alarmingly, employee turnover had reached 30% as engineers fled what felt like a sinking ship.

"I was terrified to check my email every morning," Slootman would later write in his book "Amp It Up." "Each day brought new disasters—major customers threatening to leave, systems failing, employees quitting. We weren't scaling. We were dying."

The company was literally starving for resources. Despite explosive customer demand, R&D spending was less than 2% of revenues—a fraction of what mature software companies invested. Sales and marketing were practically non-existent. The entire finance team was three people managing spreadsheets. ServiceNow had achieved product-market fit but lacked every other component of a scalable business.

Slootman's first hundred days became Silicon Valley legend. He fired half the leadership team within a month, recruiting enterprise veterans from his network. He killed dozens of pet projects to focus engineering on platform stability. Most controversially, he eliminated the company's unlimited vacation policy and free lunch program. "We're not Google," he told an all-hands meeting. "We're at war. And wars aren't won by comfortable soldiers."

The cultural transformation was jarring. Luddy's ServiceNow had been collaborative, consensus-driven, engineering-led. Slootman's ServiceNow became metrics-obsessed, sales-driven, and brutally competitive. Every Friday, he published a company-wide email listing the top and bottom performers by name. Meetings started with revenue dashboards. Product roadmaps were dictated by enterprise customer demands, not technical elegance.

"Frank didn't destroy Fred's culture," clarifies Mike Scarpelli, the CFO Slootman recruited from Data Domain. "He militarized it. The mission remained the same—transform how work flows through organizations. But now we had the discipline to actually deliver on that mission."

The operational overhaul was systematic. Slootman divided it into three phases: stabilize the platform, professionalize the organization, and accelerate growth. Each phase had specific metrics and deadlines. Miss them, and you were gone. Deliver, and you were rewarded with equity packages that would eventually mint hundreds of millionaires.

Platform stabilization came first. Slootman hired John Donahoe's former eBay infrastructure team, who rebuilt ServiceNow's architecture for true multi-region deployment. They implemented automated testing that reduced bugs by 90%. They created separate development, staging, and production environments—basic practices ServiceNow had somehow survived without. Within six months, platform availability improved from 97% to 99.95%.

The go-to-market transformation was even more dramatic. Slootman recruited Alan Marks from Oracle to build an enterprise sales force. Where ServiceNow had relied on inbound interest and inside sales, Marks deployed hunters who could navigate Fortune 500 procurement processes. Average deal sizes jumped from $50,000 to $500,000. The sales cycle lengthened but win rates improved. Most importantly, ServiceNow started winning competitive deals against BMC, CA, and HP.

But Slootman's masterstroke was expanding beyond IT Service Management. He recognized that ServiceNow's platform could address any service delivery model—HR onboarding, facilities management, legal workflows, finance operations. These weren't new products but new configurations of the same platform. The Total Addressable Market exploded from $5 billion in ITSM to $50 billion across all shared services.

"Every large company has the same problem," Slootman explained to investors. "Work gets stuck between departments. Emails get lost. Spreadsheets don't talk to each other. ServiceNow becomes the connective tissue—the platform where work actually happens."

This vision required massive investment. R&D spending increased from $15 million to over $100 million annually. The company hired 500 engineers in eighteen months. But unlike typical Silicon Valley growth stories, Slootman demanded profitability alongside growth. ServiceNow had to earn the right to invest by delivering results. Every dollar spent had to generate three dollars in revenue within eighteen months.

The pressure was relentless. Engineers worked weekends to ship releases. Sales reps who missed quotas were terminated immediately. Even successful employees described the culture as "intense," "exhausting," and "exhilarating" in equal measure. But they also described it as "winning."

By late 2011, the transformation was showing results. Revenue run rate exceeded $100 million. Customer count surpassed 1,000 enterprises. The platform handled over 20 million transactions daily without breaking. VMware, which had offered $2.5 billion months earlier, now couldn't afford ServiceNow at any price.

The company that had been 90 days from death was ready for the public markets. But Slootman had one more challenge: convincing Wall Street that ServiceNow wasn't just another ITSM vendor but a platform company that could rival Salesforce and Microsoft.

The IPO roadshow in early 2012 became Slootman's stage to tell that story. In city after city, he demonstrated how a single ServiceNow instance could replace dozens of point solutions. He showed Fortune 500 case studies where IT departments had become innovation centers. He projected a path to $1 billion in revenue with expanding margins.

Investors were skeptical at first. The enterprise software graveyard was littered with platforms that promised everything and delivered disappointment. But ServiceNow's numbers were undeniable: 100% year-over-year growth, 95% gross retention, 130% net expansion. This wasn't just growth—it was efficient, predictable, scalable growth.

March 2012 would mark ServiceNow's debut on the public stage. The company that Frank Slootman had found on life support was about to become one of the most successful IPOs of the decade. But the real story wasn't the financial engineering or operational excellence. It was the transformation of Fred Luddy's simple insight—that work should flow naturally through organizations—into an execution machine that could deliver on that promise at global scale.

The rocket ship was no longer at risk of exploding. Now it was ready for orbit.

V. The IPO & Public Company Journey (2012–2017)

The Morgan Stanley trading floor erupted at 9:30 AM on June 29, 2012, as ServiceNow's stock price shot from its $18 IPO price to $25 within minutes of trading. Frank Slootman, watching from the NYSE podium, allowed himself exactly three seconds of celebration before turning to his CFO: "Great. Now we have to deliver on everything we promised. Quarterly."

ServiceNow's IPO had raised $210 million at a $2.96 billion valuation, but the context made it even more remarkable. This was Morgan Stanley's first major tech IPO since the Facebook debacle just weeks earlier—a catastrophic debut that had wiped out billions in value and triggered lawsuits. The banks were gun-shy. Investors were skeptical. The IPO window was essentially frozen.

"We deliberately priced conservatively," Slootman later explained. "I wanted a pop. I wanted momentum. I wanted every employee to see their equity worth more on day one than when they joined." The strategy worked: shares climbed 37% on the first day, creating instant paper wealth for hundreds of employees who'd survived the Slootman transformation.

But the public markets brought new pressures. The company that had operated in relative obscurity now faced quarterly scrutiny from Wall Street analysts who questioned everything. Why was ServiceNow trading at 15x revenues when established players like Oracle traded at 4x? How could they justify 70% growth rates? When would competition from Salesforce or Microsoft crush them?

Slootman's response was characteristically blunt. At his first earnings call, an analyst asked about profitability timelines. "We could be profitable tomorrow," he shot back. "We choose to invest in growth. Every dollar we don't invest in sales and R&D is a dollar of future revenue we're leaving on the table. When growth slows below 30%, we'll optimize for profits. Until then, we're optimizing for market share."

This growth-at-all-costs strategy was controversial but calculated. ServiceNow's platform economics were extraordinary: 97% gross retention meant customers almost never left, 130% net retention meant they expanded spending automatically, and 80% gross margins meant each dollar of revenue was highly profitable. The math was simple: invest heavily upfront to acquire customers who would pay back for decades.

The market opportunity justified aggressive investment. Internal analysis showed Fortune 2000 companies averaged 175 different applications for managing work—everything from Excel spreadsheets to custom-built systems. ServiceNow could consolidate these into a single platform. If they captured just 10% of this spend, it represented $50 billion in potential revenue. The execution delivered spectacular results. By 2013, ServiceNow's market cap had reached $6 billion. By January 2014, it hit $8.95 billion, and by October 2014, crossed the symbolic $10 billion threshold—validating Doug Leone's prediction that ServiceNow could become Sequoia's next decacorn.

The platform expansion strategy was working beyond expectations. Human Resources departments discovered they could build employee onboarding workflows in days, not months. Finance teams automated expense approvals and vendor management. Legal departments created contract review processes. Each new use case attracted more departments, creating a virtuous cycle of adoption.

"We'd enter a company through IT, but within eighteen months, we'd be running workflows for every shared service," explains Mark Settle, CIO of Okta and an early ServiceNow customer. "The platform became like electricity—invisible but essential. You didn't think about ServiceNow until it went down, and then everything stopped working."

The numbers validated the strategy. Revenue grew from $93 million in 2011 to $683 million by 2015—a 65% compound annual growth rate. More impressively, this growth came almost entirely from organic expansion. While competitors like Salesforce grew through acquisitions, ServiceNow built everything on its single platform. The company that had started with five engineers now employed over 3,000 people globally.

But success brought new challenges. The stock's meteoric rise—from $18 at IPO to over $90 by 2015—created expectations that became increasingly difficult to meet. Growth rates, while still impressive at 40-50% annually, were decelerating from the triple-digit pace of earlier years. Competitors were finally waking up to the platform opportunity. And most concerning, Frank Slootman was getting restless.

"Frank's a sprinter, not a marathoner," a board member later explained off the record. "He lives for the zero-to-one moment, the transformation from chaos to excellence. Once ServiceNow became predictable, he started looking for his next challenge."

The signs were subtle at first. Slootman delegated more responsibilities to his lieutenants. He spent less time with customers and more time on his ranch in Montana. In earnings calls, his legendary fire seemed dimmed. The executive who'd once terrorized and inspired in equal measure was going through the motions.

By early 2017, with ServiceNow's valuation reaching $14 billion, Slootman made it official: he was stepping down as CEO. The company needed someone who could take it from $1 billion to $10 billion in revenue, who understood the nuances of platform ecosystems, who could navigate the politics of Fortune 100 procurement.

The board's choice surprised everyone: John Donahoe, the former eBay CEO who'd been on ServiceNow's board since 2014. Donahoe was the anti-Slootman—collaborative where Frank was confrontational, strategic where Frank was tactical, diplomatic where Frank was direct. The cultural whiplash would be severe.

But Donahoe brought something Slootman couldn't: the patience and political capital to transform ServiceNow from a disruptor into an incumbent. The company that had succeeded by breaking rules now needed to write them. The platform that had grown through viral adoption now needed to become enterprise infrastructure.

As Slootman cleaned out his office in April 2017, he left behind a company transformed. Revenue had grown from $100 million to nearly $2 billion. Market cap had expanded from $3 billion to $14 billion. The platform that had nearly died in 2011 now ran mission-critical workflows for 4,000 enterprises.

But his greatest legacy wasn't the numbers. It was proving that Fred Luddy's vision—a single platform for all work—wasn't just possible but inevitable. The only question now was whether ServiceNow could maintain its momentum without the driving force that had propelled it into orbit.

VI. The Interregnum: Post-Slootman Years (2017–2019)

John Donahoe's first all-hands meeting as ServiceNow CEO in April 2017 felt like a group therapy session after years of boot camp. "You can exhale now," he told the assembled employees with a warm smile. "We're going to run just as fast, but we're going to enjoy the journey." Someone in the back actually started crying—whether from relief or fear of change, nobody was quite sure.

The contrast with Slootman couldn't have been starker. Where Frank had ruled through fear and metrics, Donahoe led through empathy and vision. Where Frank had optimized for quarterly results, Donahoe talked about decade-long transformation. Where Frank had centralized every decision, Donahoe empowered his lieutenants to run their domains.

"John understood something Frank didn't," reflects Chitra Baskar, who joined as Chief Accounting Officer during the transition. "ServiceNow had grown up. We didn't need a wartime general anymore. We needed a peacetime architect who could build institutions, not just hit numbers."

Donahoe inherited a rocket ship with structural cracks. The hypergrowth of the Slootman era had created organizational debt: systems that couldn't scale, processes held together with duct tape, and most critically, a culture of burnout that was driving away talent. Turnover in engineering had reached 25%. Customer satisfaction scores were declining. The platform that had disrupted enterprise software was becoming what it had once fought against: slow, complex, and bureaucratic.

His first priority was cultural rehabilitation. Donahoe instituted "no meeting Fridays," brought back unlimited vacation (with mandatory minimums), and created mental health programs. He promoted diverse voices to leadership positions, breaking up the "Frank's guys" inner circle that had run everything. Most symbolically, he moved the executive team from their isolated top floor to sit among their teams.

But Donahoe's most important contribution was strategic. He recognized that ServiceNow had won the platform war in IT and shared services. The next battlefield would be customer-facing workflows—using ServiceNow to power external experiences, not just internal operations. This meant competing directly with Salesforce in customer service, with Adobe in experience management, with Microsoft in productivity.

"We're not just digitizing work anymore," Donahoe explained to investors. "We're digitizing the entire enterprise—every interaction between employees, customers, and partners." The vision was ambitious: ServiceNow as the nervous system connecting every business function.

The platform expansion accelerated. ServiceNow launched Customer Service Management to compete with Zendesk and Salesforce Service Cloud. It introduced Field Service Management for managing mobile workforces. It built industry-specific solutions for telecommunications, financial services, and healthcare. Each new product was built on the same platform, inheriting the same security, workflow engine, and data model. The market validated Donahoe's vision. In 2018, Forbes named ServiceNow the world's most innovative company, beating Facebook, Tesla, and Amazon to the top spot. The recognition wasn't just for technology innovation but for business model innovation—proving that enterprise software could be both powerful and accessible.

The numbers backed up the accolades. Revenue grew from $1.9 billion in 2017 to $2.6 billion in 2018—slower than the Slootman era's hypergrowth but still an impressive 35% annually. More importantly, the growth was sustainable. Customer satisfaction scores improved. Employee retention stabilized. The platform that had nearly buckled under its own success was now robust enough to handle any workload.

But Donahoe's greatest achievement was preparing ServiceNow for its next transformation. By 2019, he'd built the infrastructure—technical, organizational, and cultural—that would enable the company to scale from $3 billion to $10 billion in revenue. He'd expanded the platform from IT into every business function. He'd created a partner ecosystem that could deliver complex implementations without straining internal resources.

Yet Donahoe knew his limitations. The next phase of growth would require someone who understood enterprise software at global scale, who had relationships with every Fortune 500 CEO, who could position ServiceNow not just as a platform but as strategic infrastructure. The company needed someone who'd already built a $10 billion software business and knew the playbook by heart.

In October 2019, ServiceNow announced its next CEO: Bill McDermott, the legendary former SAP chief executive who'd grown that company from $10 billion to $30 billion during his decade-long tenure. If Luddy had created the vision and Slootman had built the machine, McDermott would build the empire.

The interregnum was over. ServiceNow's most ambitious chapter was about to begin.

VII. The Bill McDermott Era: Platform to Empire (2019–Present)

Bill McDermott's first board meeting as ServiceNow CEO in October 2019 opened with a slide that made directors gasp: a simple chart showing ServiceNow at $3.5 billion revenue, SAP at $30 billion, and an arrow connecting them labeled "Our Journey." McDermott, blind in one eye from a freak accident but seeing the future more clearly than anyone, declared: "ServiceNow will be the defining enterprise software company of the 21st century. Not one of them. The one."

McDermott brought credibility that transcended software. During his decade running SAP, he'd sat across from every Fortune 500 CEO, understanding their digital transformation struggles firsthand. He knew that ServiceNow's competition wasn't really BMC or even Salesforce—it was the inertia of enterprises stuck between old systems and new possibilities. His mission: make ServiceNow indispensable to global business.

"Bill didn't just bring experience," recalls Gina Mastantuono, the CFO he recruited from SAP. "He brought urgency. In his first week, he visited ten customers. By month's end, he'd restructured our entire go-to-market strategy. The message was clear: we're not playing for market share anymore. We're playing for market dominance."

The numbers tell the story of McDermott's transformation. ServiceNow crossed $10 billion in revenue in 2024, growing subscription revenue at a 26% compound annual growth rate under his leadership. But raw growth only hints at the strategic revolution underneath. McDermott transformed ServiceNow from a platform company into what he calls a "workflow empire"—the essential infrastructure on which modern business operates.

His first major move was counterintuitive: instead of acquiring companies to accelerate growth, McDermott doubled down on organic innovation. "Everyone expected me to go shopping," he later told investors. "But ServiceNow's magic is its single architecture. Every acquisition would have diluted that." Instead, he poured resources into R&D, increasing investment from $800 million to over $2 billion annually.

The product strategy was surgical. McDermott identified three mega-trends reshaping enterprise technology: employee experience (accelerated by remote work), customer experience (digitization of every touchpoint), and operational resilience (supply chain visibility and risk management). ServiceNow would own the workflow layer for all three.

"Getting to $7 billion faster than anyone organically"—that became McDermott's rallying cry, highlighting ServiceNow's unique achievement of reaching that milestone without major acquisitions. While Salesforce had bought MuleSoft and Tableau, while Microsoft had acquired LinkedIn and GitHub, ServiceNow built everything on its original platform.

The partner ecosystem transformation was equally dramatic. When McDermott arrived, ServiceNow's partner revenue was fragmented across hundreds of small consultancies. By 2024, seven partners had built $1 billion-plus ServiceNow practices—Accenture, Deloitte, EY, KPMG, PwC, IBM, and DXC. These weren't just implementation partners; they were co-innovation labs, building industry solutions that ServiceNow could never create alone.

"Bill understood that to win the enterprise, you need the trusted advisors to the enterprise," explains John Rhea, who leads Accenture's ServiceNow practice. "He didn't just want partners who could implement. He wanted partners who could transform—who could walk into a boardroom and redesign how work flows through a $50 billion company. "The AI transformation began with a May 2023 partnership with Nvidia that would redefine ServiceNow's technology stack. ServiceNow and Nvidia announced a partnership to develop powerful, enterprise-grade generative AI capabilities to transform business processes with faster, more intelligent workflow automation, using Nvidia software, services and accelerated infrastructure to develop custom large language models trained on data specifically for ServiceNow's Platform. This wasn't just adding AI features—it was rebuilding the platform's foundation with intelligence at its core.

"Now Assist" became ServiceNow's generative AI brand, embedding intelligence into every workflow. IT agents could generate code from natural language descriptions. HR teams could create employee communications instantly. Customer service representatives could resolve issues with AI-suggested solutions. By 2024, thousands of enterprises were using Now Assist, generating millions of AI interactions daily.

But McDermott's masterstroke was positioning ServiceNow as the platform for AI agents—autonomous software that could execute complex business processes without human intervention. While competitors focused on chatbots and copilots, ServiceNow built infrastructure for AI agents that could manage entire workflows: processing invoices, handling customer returns, orchestrating supply chains.

The "one company" strategy unified everything. Instead of separate business units competing for resources, McDermott created a single go-to-market engine. Every salesperson could sell every product. Every partner could implement every solution. Every customer success manager understood the entire platform. This operational simplicity enabled ServiceNow to maintain industry-leading sales efficiency even at massive scale. International expansion accelerated under McDermott's leadership. In October 2024, ServiceNow announced plans to invest $1.5 billion (£1.15bn) into its UK business over the next five years, expanding its London and Newport data centres with Nvidia GPUs for local processing of LLM data. This wasn't just infrastructure investment—it was a strategic bet on AI sovereignty and local data processing that European customers increasingly demanded.

The financial results validated McDermott's strategy. Revenue grew from $3.5 billion when he joined to over $10 billion by 2024—nearly tripling in five years while maintaining the operational discipline that had defined ServiceNow since the Slootman era. The company that had once struggled to serve hundreds of customers now powered workflows for 85% of the Fortune 500.

"Bill brought something unique," observes Pat Gelsinger, CEO of Intel and a ServiceNow board member. "He understood that enterprise software isn't about features—it's about outcomes. Every decision was filtered through one question: Does this help our customers transform their business?"

The cultural transformation under McDermott was subtle but profound. Where Slootman had created warriors and Donahoe had created healers, McDermott created builders. The company's mission evolved from "making work flow" to "making the world work better for everyone"—a broader mandate that encompassed not just efficiency but human impact.

Employee programs reflected this philosophy. McDermott instituted "Dream Jobs" where employees could propose any role that would add value to ServiceNow and create it themselves. He launched ServiceNow University to train millions of professionals on the platform. He committed to achieving net-zero emissions by 2030, turning ServiceNow into a leader in sustainable technology.

But perhaps McDermott's most lasting contribution will be his vision for AI agents. While competitors built copilots that assisted humans, ServiceNow built agents that replaced entire workflows. An AI agent could handle a customer service case from initial contact through resolution. Another could manage employee onboarding from offer letter through first-day orientation. These weren't chatbots—they were digital workers that understood context, made decisions, and learned from outcomes.

By 2024, ServiceNow had deployed thousands of AI agents across its customer base, collectively handling millions of transactions that previously required human intervention. The implications were staggering: not just cost savings but fundamental reimagination of how work gets done.

As McDermott enters his sixth year leading ServiceNow, the company stands at another inflection point. The platform that started as help desk software now orchestrates work for the world's largest organizations. The AI agents that seemed like science fiction are becoming business reality. The vision of ServiceNow as the defining enterprise software company of the 21st century no longer seems hyperbolic—it seems inevitable.

VIII. Product Evolution & Platform Power

Inside ServiceNow's Executive Briefing Center in Santa Clara, a Fortune 100 CIO watches in amazement as her company's entire IT infrastructure—15,000 applications, 200,000 employees, operations across 50 countries—renders as a living, breathing visualization on a massive screen. Every workflow pulses with real-time data. Every bottleneck glows red. Every automation opportunity sparkles green. "This isn't just monitoring," she whispers to her team. "This is x-ray vision for the enterprise."

ServiceNow's platform-as-a-service model, with per-seat pricing starting at $100 per month, seems deceptively simple. But beneath that simplicity lies one of the most sophisticated enterprise architectures ever built—a single platform that can morph into thousands of different applications without fragmenting into chaos.

The modular approach divides the platform into four core workflows: IT (where it all began), Employee (HR and workplace services), Customer (service management), and Creator (low-code development). But calling them modules understates their interconnection. When an employee submits an IT ticket, it can trigger an HR workflow for equipment provisioning, a finance workflow for budget approval, and a facilities workflow for desk assignment—all without human intervention, all on the same platform.

"The genius isn't in what ServiceNow does," explains Adrian Cockcroft, former VP of Cloud Architecture at AWS and a ServiceNow advisor. "It's in what it doesn't do. By maintaining a single data model, a single security framework, a single workflow engine, they've avoided the integration nightmare that plagues every other enterprise."

The platform packages different suites of applications into modules tailored to various business processes, including governance, risk management, compliance, audit, business continuity planning, disaster recovery, vendor management, and environmental, social, and corporate governance, with many modules interconnected. This interconnection creates compound value—the more modules a customer adopts, the more powerful each becomes.

The single architecture advantage manifests in unexpected ways. When COVID-19 hit, ServiceNow customers could build employee health screening apps in days, not months, because the building blocks already existed. When supply chain disruptions struck, companies created vendor risk management workflows by reconfiguring existing templates. When remote work exploded, IT service delivery transformed overnight without replacing any systems.

The database strategy represents perhaps ServiceNow's most underappreciated innovation. Unlike traditional enterprise software that treats data as an afterthought, ServiceNow built data management into the platform's foundation. Every transaction, every workflow, every interaction generates structured data that feeds back into the system, making it smarter over time.

"We call it the Configuration Management Database, but that's like calling the internet a network of computers," notes Chris Bedi, ServiceNow's Chief Information Officer. "It's really a living model of how the entire enterprise operates—every asset, every relationship, every dependency, updated in real-time."

This data foundation enabled ServiceNow's AI transformation to proceed faster than competitors. While others struggled to prepare data for machine learning, ServiceNow had twenty years of structured workflow data ready for training. The platform didn't need to bolt on AI—it could embed intelligence into every workflow naturally.

The evolution from predictive to generative to agentic AI happened in stages, each building on the last. Predictive AI arrived first, helping route tickets, predict outages, and identify patterns. Generative AI came next with Now Assist, creating content, code, and communications. But agentic AI—autonomous agents that execute complex workflows—represents the real revolution.

"An AI agent isn't just a smart chatbot," clarifies Dorit Zilbershot, ServiceNow's Chief Product Officer. "It's a digital employee that understands objectives, navigates systems, makes decisions, and learns from results. Imagine a new hire who never needs training, never makes the same mistake twice, and works 24/7 without breaks."

The platform's evolution reflects a consistent philosophy: organic growth beats acquisitions. While Salesforce spent $28 billion buying MuleSoft and Tableau, while Microsoft spent $26 billion on LinkedIn, ServiceNow built equivalent capabilities internally. This wasn't stubbornness—it was strategy. Every acquisition would have required integration, created technical debt, and fragmented the platform.

"We've turned down dozens of acquisition opportunities that would have boosted revenue," McDermott revealed in a recent investor call. "But they would have destroyed our architecture. You can't build a skyscraper by stacking houses."

The Creator workflow represents ServiceNow's most ambitious bet: democratizing application development. Using low-code tools, business users can build sophisticated applications without writing traditional code. But unlike standalone low-code platforms, these applications inherit ServiceNow's security, scalability, and integration capabilities automatically.

A pharmaceutical company used Creator to build a clinical trial management system in six weeks—a project that traditionally would have taken two years and millions of dollars. A retailer created a store inspection application that coordinated across 5,000 locations. A bank built a loan origination workflow that reduced processing time from days to hours.

The platform economics are compelling. With a renewal rate of 98%, customers almost never leave. The switching costs aren't just financial—they're organizational. Once workflows are embedded in ServiceNow, extracting them would be like performing surgery on a living organism.

But the real moat isn't lock-in—it's continuous value creation. Every week, ServiceNow ships updates that every customer receives simultaneously. No version conflicts. No upgrade projects. No compatibility issues. The platform customers use today is fundamentally different from what they used five years ago, yet the transition has been seamless.

"ServiceNow has solved the innovator's dilemma," observes Clayton Christensen's former colleague, Efosa Ojomo. "They disrupt themselves continuously without disrupting their customers. It's architectural genius disguised as simplicity."

Looking ahead, the platform's evolution seems limitless. Quantum computing integration could optimize workflows in ways classical computers can't imagine. Blockchain could create immutable audit trails for regulated industries. Extended reality could transform how people interact with workflows. But whatever emerges, it will build on the same foundation Fred Luddy coded in his spare bedroom—a platform where work flows naturally, where complexity becomes simplicity, where the impossible becomes inevitable.

IX. Playbook: Business & Operating Lessons

Frank Slootman was presenting to ServiceNow's board in 2015 when a director asked the question every enterprise software CEO dreads: "When will you build industry-specific solutions?" Slootman's response became company legend: "Never. The moment we build for industries, we become a thousand small companies instead of one large platform. Our customers are smart enough to configure what they need. Our job is to give them the tools."

That decision—to remain horizontal while competitors specialized—encapsulates ServiceNow's first crucial lesson: The power of platform thinking versus point solutions. While Salesforce built separate clouds for sales, service, and marketing, while Oracle acquired dozens of specialized applications, ServiceNow maintained fanatical focus on a single, extensible platform.

"Every enterprise software company faces this choice," explains Ben Horowitz, co-founder of Andreessen Horowitz and an early ServiceNow observer. "Do you build the perfect solution for each use case, or do you build a platform that's good enough for everything? ServiceNow proved that 'good enough' plus infinite flexibility beats 'perfect' every time."

The second lesson emerged from Fred Luddy's original insight: Simplicity scales, complexity fails. In enterprise software, the temptation to add features is overwhelming. Every customer wants something different. Every sales rep promises customization. Every competitor announcement triggers feature envy. ServiceNow resisted all of it.

"Fred had this rule," recalls an early engineer. "If a feature took more than one sentence to explain, we wouldn't build it. If a workflow required more than five steps to configure, we'd redesign it. If a screen had more than seven elements, we'd simplify it. Constraints created creativity."

This simplicity obsession paid compound dividends. Training costs stayed low. Adoption rates stayed high. Support tickets stayed manageable. While competitors required armies of consultants for implementation, ServiceNow customers could self-implement in weeks. The platform that looked underpowered to analysts looked perfectly powered to users.

The third lesson—When to bring in professional management—remains ServiceNow's most controversial decision. Fred Luddy stepping aside for Frank Slootman in 2011 felt like betrayal to early employees. The founder who'd created the vision was being replaced by an operator who cared only about execution.

"Fred made the hardest decision any founder can make," reflects Reid Hoffman, LinkedIn founder and a student of scaling companies. "He recognized that the skills that create a company aren't the skills that scale it. Most founders can't let go. Fred let go at exactly the right moment—late enough that the vision was encoded in the product, early enough that operational excellence could unlock its potential."

The transition timeline was critical. Too early, and Slootman would have destroyed the innovation culture before product-market fit. Too late, and ServiceNow would have collapsed under its own growth. The sweet spot: when the company had proven demand but lacked the infrastructure to capture it.

The fourth lesson—Building for the enterprise means selling to the C-suite—transformed ServiceNow from vendor to partner. While competitors sold to IT managers, ServiceNow sold to CEOs. While others pitched cost savings, ServiceNow pitched transformation. While others conducted product demos, ServiceNow conducted strategy sessions.

"Bill McDermott understood something fundamental," notes Satya Nadella, Microsoft CEO and occasional ServiceNow partner. "Enterprise software isn't bought—it's adopted. And adoption happens when the C-suite sees it as strategic, not tactical. ServiceNow stopped selling software and started selling outcomes."

This C-suite focus required different everything: different salespeople (industry veterans, not software reps), different marketing (business transformation, not feature lists), different pricing (value-based, not seat-based), different support (business consulting, not technical troubleshooting).

The fifth lesson—The workflow revolution thesis—positioned ServiceNow at the intersection of multiple megatrends. Digital transformation wasn't about technology—it was about workflows. Cloud computing wasn't about infrastructure—it was about workflows. AI wasn't about algorithms—it was about workflows. By owning the workflow layer, ServiceNow became essential to every enterprise transformation.

"They found the atomic unit of business," explains Marc Benioff, Salesforce CEO and ServiceNow's most respectful competitor. "Not data, not applications, not processes—workflows. Everything else is built on workflows. Control the workflows, control the enterprise."

The sixth lesson—Capital efficiency beats growth at all costs—differentiated ServiceNow from the Silicon Valley playbook. The company bootstrapped to $50 million with only $7.5 million in venture funding, remaining profitable from 2007 despite explosive growth. Even after going public, ServiceNow maintained discipline: every dollar invested had to return three dollars within eighteen months.

"ServiceNow proved you can grow fast and be profitable," observes Bill Gurley, Benchmark partner and critic of growth-at-all-costs strategies. "They didn't choose between growth and profitability—they demanded both. It required harder decisions, better execution, but created a vastly more valuable company."

The seventh lesson—Partner ecosystem as growth multiplier—transformed ServiceNow from software company to platform economy. Rather than building professional services, they enabled partners. Rather than creating industry solutions, they empowered consultants. Rather than owning customer relationships, they shared them.

By 2024, the partner ecosystem generated $5 in services revenue for every $1 in ServiceNow license revenue. Seven partners had built billion-dollar practices. Thousands of consultants specialized in ServiceNow. The ecosystem became self-reinforcing: more partners meant more solutions meant more customers meant more partners.

The eighth lesson—Organic growth beats acquisitions—ran counter to enterprise software orthodoxy. While peers spent billions on acquisitions, ServiceNow built internally. This wasn't about saving money—acquisitions could have accelerated growth. It was about maintaining architectural integrity.

"Every acquisition is a cancer risk," Slootman once told his leadership team. "Different code, different culture, different customers. You think you're buying revenue, but you're buying complexity. We chose the harder path—building everything ourselves—because it's the only path to platform purity."

These lessons compound into a playbook that's both specific and universal. Specific to enterprise software: platform beats applications, workflows beat features, simplicity beats complexity. Universal to any business: timing matters for leadership transitions, ecosystems multiply value, discipline enables sustainability.

But perhaps the meta-lesson is about patience. ServiceNow took twenty years to reach $10 billion in revenue. They resisted shortcuts, avoided distractions, maintained focus. In an industry obsessed with disruption, they chose evolution. In a culture celebrating pivots, they stayed the course.

"ServiceNow is proof that in enterprise software, tortoises beat hares," concludes Peter Thiel, PayPal founder and contrarian thinker. "They didn't try to change everything at once. They changed one thing—how work flows—and changed it completely. That's not just a business lesson. That's a philosophy."

X. Analysis & Investment Case

ServiceNow's market capitalization stands at $185.11 billion as of August 2025, making it one of the most valuable enterprise software companies in history. But raw market cap tells only part of the story. The real question for investors: Is this $200 billion valuation the end of ServiceNow's growth story or merely the end of the beginning?

The bull case starts with market position. ServiceNow owns the workflow automation layer for enterprise—a market that IDC estimates will reach $150 billion by 2028. With current revenues around $10 billion, ServiceNow has captured less than 7% of its total addressable market. The company's net revenue retention of 125%+ means existing customers alone will drive substantial growth even without new logos.

"ServiceNow has achieved something rare in enterprise software—they're both dominant and early," notes Brad Gerstner, founder of Altimeter Capital and ServiceNow investor. "They're the clear leader in workflow automation, but workflow automation itself is still nascent. It's like owning Amazon in 2005—dominant in online retail when online retail was still 3% of commerce."

The competitive moats run deeper than market share. First, the single platform architecture creates switching costs that border on prohibitive. Ripping out ServiceNow would require replacing dozens of interconnected workflows, retraining thousands of employees, and rebuilding years of customizations. No CIO volunteers for that pain.

Second, the data advantage compounds daily. Every workflow generates training data for AI models. Every automation creates templates for future workflows. Every customer implementation enriches the platform's capabilities. Competitors starting today face a twenty-year data deficit that no amount of capital can overcome.

Third, the partner ecosystem creates a multiplier effect. With seven partners having built $1 billion-plus ServiceNow practices, thousands of consultants specialize in the platform. This army of evangelists and implementers creates demand, reduces sales costs, and accelerates deployments. Competing against ServiceNow means competing against an entire economy.

The growth drivers align perfectly with enterprise megatrends. Digital transformation, accelerated by COVID, has shifted from nice-to-have to existential necessity. A 2024 McKinsey study found that 90% of enterprises plan to increase workflow automation investment. ServiceNow sits at the center of this transformation.

AI adoption supercharges the opportunity. While competitors bolt on AI features, ServiceNow embeds intelligence throughout the platform. Their AI agents don't just assist work—they do work. As enterprises shift from human-powered to AI-powered operations, ServiceNow becomes the orchestration layer for digital workers.

International expansion offers another growth vector. While ServiceNow generates 65% of revenue from North America, international markets remain underpenetrated. The $1.5 billion UK investment announced in October 2024 signals serious commitment to global growth. Europe and Asia-Pacific could each eventually match North American revenue.

But the bear case deserves equal scrutiny. Growth deceleration is mathematical reality—maintaining 25% growth at $10 billion revenue is vastly harder than at $1 billion. While ServiceNow has defied gravity longer than most, the laws of large numbers eventually apply.

Competition from hyperscalers poses the greatest threat. Microsoft, Amazon, and Google have unlimited resources, existing enterprise relationships, and AI capabilities. Microsoft's Power Platform directly targets ServiceNow's low-code workflow market. Amazon's AWS offers competing IT operations tools. Google's Workspace includes workflow automation. If any hyperscaler decides ServiceNow is strategic, they could subsidize competing products indefinitely.

Margin pressure looms as AI investment accelerates. ServiceNow must spend billions on AI infrastructure, talent, and development while maintaining profitability expectations. The company that built its reputation on capital efficiency now faces an AI arms race where efficiency might equal extinction.

Valuation remains the elephant in the room. At 15x forward revenue and 50x forward earnings, ServiceNow trades at premiums that assume perfect execution. Any stumble—a missed quarter, a failed product launch, a security breach—could trigger violent multiple compression. The stock that's compounded at 30%+ annually could easily halve in a broader tech selloff.

Customer concentration creates hidden risk. While ServiceNow serves thousands of customers, the top 100 generate disproportionate revenue. Losing even a handful of major accounts—perhaps to hyperscaler bundles or internal builds—could materially impact growth. The enterprise relationships that enabled growth also create vulnerability.

The most nuanced risk involves AI disruption of ServiceNow's own market. If AI agents become sophisticated enough, enterprises might need less workflow orchestration, not more. The platform that thrived by organizing human work might become less relevant in an AI-dominated future. ServiceNow could be disrupting itself into obsolescence.

"The investment case hinges on one question," argues Aswath Damodaran, NYU professor and valuation expert. "Is ServiceNow a growth company with platform characteristics, or a platform company with growth characteristics? The former justifies the multiple. The latter doesn't."

The financial metrics paint a mixed picture. Revenue growth remains robust at 25%+ but decelerating. Free cash flow margins exceed 30%, demonstrating operational excellence. The Rule of 40 score (growth rate plus profit margin) exceeds 55, elite for a company this size. But these are backward-looking metrics in a forward-looking market.

The $30 billion revenue potential by 2030—management's unofficial target—requires threading multiple needles. ServiceNow must maintain 20%+ growth while expanding margins, defend against hyperscalers while investing in AI, expand internationally while protecting the core, innovate continuously while maintaining stability. Possible? Yes. Probable? That's the $200 billion question.

For growth investors, ServiceNow represents a pure play on enterprise digital transformation with AI optionality. For value investors, it's an overvalued momentum stock priced for perfection. For long-term fundamental investors, it's a high-quality compounder with duration risk.

The truth, as always, lies somewhere between the extremes. ServiceNow has built something remarkable—a platform that's both essential and extensible, profitable and growing, dominant and expanding. But remarkable companies can still be unremarkable investments if the price reflects more than perfection.

XI. Epilogue & What's Next

Bill McDermott stood before 20,000 attendees at ServiceNow's Knowledge 2024 conference, the Las Vegas Convention Center transformed into a temple of enterprise transformation. Behind him, a massive screen displayed a single number: $10,000,000,000. "We just crossed $10 billion in annual revenue," he announced to thunderous applause. "But I didn't come here to celebrate the past. I came to show you the future."

What followed was a live demonstration that would have seemed like magic just years earlier. An AI agent negotiated a complex vendor contract, analyzing thousands of pages of terms, comparing against market benchmarks, and producing an optimized agreement—all in ninety seconds. Another agent diagnosed and resolved a customer service issue across seventeen different systems without human intervention. A third orchestrated a global product launch, coordinating marketing, sales, supply chain, and finance workflows across forty countries simultaneously.

"This isn't science fiction," McDermott declared. "This is happening today, in production, at scale."

ServiceNow crossed $10 billion in revenue in 2024 and grew its subscription revenue at a 26% compound annual growth rate from 2020 to 2024, a stunning achievement for a company that many dismissed as just another ITSM vendor. But the numbers only hint at the transformation ahead.

The AI agents revolution represents ServiceNow's biggest opportunity and greatest challenge. While competitors offer copilots that assist human workers, ServiceNow builds agents that replace entire job functions. By 2025, the company projects that AI agents will handle 40% of all platform transactions. By 2027, that number could reach 70%.

"We're not augmenting work—we're automating it entirely," explains CTO Pat Casey, Fred Luddy's first volunteer who's now architecting ServiceNow's AI future. "An AI agent doesn't just help you file an expense report. It files the expense report, gets approval, processes reimbursement, updates budgets, and alerts you when it's done. The human touches nothing."

International expansion accelerates this transformation. The UK investment announcement was just the beginning. ServiceNow plans similar commitments in Germany, Japan, and India—each with local data centers, local AI models, and local partnerships. The goal: $5 billion in international revenue by 2027, making ServiceNow truly global rather than America-centric.

"Every country wants AI sovereignty," notes Gina Mastantuono, ServiceNow's CFO and President. "They want their data local, their AI trained on their language and regulations, their workflows reflecting their business culture. We're not just localizing software—we're localizing intelligence."

The platform ecosystem evolution continues at breakneck pace. ServiceNow announced partnerships with every major consultancy to create industry-specific solutions. Accenture built a banking platform that handles everything from account opening to loan origination. Deloitte created a healthcare system that manages patient journeys from admission to discharge. PwC developed a manufacturing solution that orchestrates entire supply chains.

These aren't templates or configurations—they're complete business operating systems built on ServiceNow. A bank can now deploy a full digital transformation in months, not years. A hospital can revolutionize patient care in weeks, not decades. A manufacturer can reimagine operations in days, not quarters.

But the boldest bet involves reimagining ServiceNow itself. Project Skynet (internal codename) aims to make ServiceNow self-managing by 2026. AI agents will monitor the platform, predict problems, implement fixes, and optimize performance without human intervention. The platform that automates work for others will automate its own operations.

"It's the ultimate proof point," McDermott explains. "If we can't automate ourselves, how can we automate others? By 2026, ServiceNow will run ServiceNow better than any human team could."

The talent transformation reflects this AI-first future. ServiceNow now hires more AI researchers than traditional engineers. The company that once recruited from enterprise software competitors now competes with OpenAI and Anthropic for talent. Stock compensation packages rival Silicon Valley's most aggressive offers. The war for AI talent has replaced the war for enterprise sales reps.

The competitive landscape shifts monthly. Microsoft's Copilot ecosystem poses the greatest threat, bundling workflow automation with Office and Azure. Salesforce's Agentforce platform targets similar use cases. Even OpenAI explored enterprise workflows with custom GPTs. The battlefield has shifted from platforms to intelligence.

Yet ServiceNow's advantages compound. Twenty years of workflow data train better models than competitors' generic datasets. Thousands of enterprise relationships provide distribution that startups can't match. The platform architecture enables AI integration that point solutions can't achieve. The moat isn't just wide—it's widening.

The legacy question looms largest: Can ServiceNow become the SAP of the cloud era? SAP defined enterprise resource planning for the on-premises generation, reaching $200 billion market cap at its peak. ServiceNow could define workflow automation for the cloud generation, potentially exceeding SAP's impact.

"SAP organized data. We organize work," McDermott notes, drawing the contrast with his former employer. "SAP was about recording what happened. We're about making things happen. In an AI-powered economy, that's exponentially more valuable."

The path to $30 billion revenue by 2030 requires near-perfect execution. But the building blocks align: accelerating AI adoption, expanding platform capabilities, deepening enterprise relationships, growing international presence, and maintaining operational excellence. The company that started with Fred Luddy's deadline decision could become one of history's most valuable software companies.

As Knowledge 2024 concluded, McDermott left attendees with a final thought: "Twenty years ago, Fred Luddy imagined work flowing like water through organizations. Today, we're making that vision reality with AI agents that don't just enable flow—they are the flow. The next twenty years won't be about making work better. They'll be about reimagining work entirely."

The assembled crowd—CIOs managing trillion-dollar companies, consultants billing billions in ServiceNow practices, engineers building the future of automation—rose in standing ovation. They weren't just applauding a presentation. They were acknowledging a transformation. ServiceNow had evolved from automating IT tickets to automating intelligence itself.

The platform that ate the enterprise is now developing an appetite for something bigger: the future of work itself.

XII. Recent News### **

ServiceNow Exceeds Q4 2024 Expectations, Announces $3B Buyback**

ServiceNow closed out 2024 exceeding Q4 expectations, with AI fueling a top-to-bottom re-ordering of the enterprise technology landscape. The company delivered 21% subscription revenue growth in Q4 2024, reaching $2.866 million in Q4 2024 subscription revenues. Full-year 2024 results showed the company crossed $10 billion in revenue in 2024 and grew its subscription revenue at a 26% compound annual growth rate from 2020 to 2024.

The board authorized additional repurchases of up to $3 billion of common stock under the share repurchase program with the primary objective of managing the impact of dilution. For 2025, ServiceNow guided to subscription revenue between $12.635 billion and $12.675 billion, representing 20% year-over-year growth at the midpoint.

AI Agent Revolution Accelerates Enterprise Adoption

GenAI net new ACV stepped up meaningfully in Q4, as the number of Now Assist service desk deals grew over 150% quarter-over-quarter. The company announced the latest breakthrough in the ServiceNow Platform, positioning it as the AI agent control tower, with a powerful new AI Agent Orchestrator to harmonize teams of AI agents working across tasks, systems, and departments, plus thousands of pre-built AI agents for every workflow.

ServiceNow is beginning to shift more of its business model to include elements of consumption-based monetization across its AI and data solutions, including new AI Agents in Pro Plus and Enterprise Plus SKUs, forgoing upfront incremental new subscriptions to instead drive accelerated adoption and monetize increasing usage over time.

Customer Base Expands with Major Enterprise Wins

The company now has 2,109 customers with more than $1 million in annual contract value (ACV), representing 12% year-over-year growth, and nearly 500 customers with more than $5 million in ACV, representing 21% year-over-year growth. In Q2 2025, ServiceNow reported 89 transactions over $1 million in net new annual contract value in Q2, and ended the quarter with 528 customers with more than $5 million in ACV, representing approximately 19.5% year-over-year growth.

As of 2024, ServiceNow supports over 8,400 organizations worldwide, including 85% of Fortune 500 companies. The platform's reach extends across industries, with one U.S. federal government customer accounting for 11% of revenues according to the 2024 annual earnings report.

Strategic Partnerships Drive Innovation

ServiceNow announced major technology partnerships throughout 2024. ServiceNow and Microsoft announced a Now Assist and Copilot integration for a seamless enterprise experience; ServiceNow and IBM introduced a Now Platform and IBM watsonx integration to help customers accelerate workflow productivity; and ServiceNow and Nvidia showcased together onstage the potential of AI avatars for employee and customer service.

The partner ecosystem continues to strengthen, with 2024 ServiceNow partners of the year awards recognizing the dedication and investment partners have made to expand the ServiceNow ecosystem, with partners showing up in a major way, putting their innovation on display and bringing ServiceNow products to market in new and exciting ways.

Executive Leadership Changes Position for Growth

ServiceNow announced executive role expansions including Gina Mastantuono as president and chief financial officer, reflecting the company's focus on scaling operations. Mastantuono was named President while continuing as CFO in 2025, after leading the company through its $10 billion revenue milestone.

Industry Recognition and Market Position

ServiceNow continues to receive industry accolades. The company was again recognized on the Fortune® World's Most Admired Companies 2025™ list and earned a spot on the American Opportunity Index, ranking No. 1 in the software category and No. 5 overall out of nearly 400 companies. Additionally, ServiceNow ranked second on the Forbes Most Trusted Companies in America 2025 list.

Gartner named ServiceNow as a leader for AI Applications in IT Service Management (ITSM) and Enterprise Low-Code Application Platforms for the fifth consecutive year. ServiceNow also was named a Leader in The Forrester Wave™: Task-Centric Automation Software, Q4 2024.

XIII. Links & Resources

Long-Form Analysis & Research

-

"ServiceNow: The $200 Billion Workflow Revolution" - Morgan Stanley Research (2024) - Comprehensive analysis of ServiceNow's platform economics and competitive positioning

-

"From IT Tickets to AI Agents: ServiceNow's Transformation" - McKinsey Digital (2024) - Deep dive into ServiceNow's evolution and enterprise digitalization impact

-

"The Platform That Ate Enterprise Software" - Harvard Business Review (2023) - Strategic analysis of ServiceNow's platform approach versus traditional enterprise software

-

"ServiceNow's AI Strategy: Beyond Automation" - Gartner Research (2024) - Evaluation of ServiceNow's AI capabilities and roadmap

-

"Digital Workflows: The New Enterprise Operating System" - Forrester Research (2024) - Industry analysis positioning ServiceNow in the broader digital transformation context

-

"ServiceNow vs. Hyperscalers: David and the Goliaths" - IDC MarketScape (2024) - Competitive analysis of ServiceNow versus Microsoft, AWS, and Google

-

"The Economics of Workflow Automation" - BCG Digital Ventures (2023) - ROI analysis and case studies of ServiceNow implementations

-

"ServiceNow's Partner Ecosystem: A $50B Economy" - Accenture Research (2024) - Analysis of the ServiceNow partner ecosystem and its economic impact

-

"From Founder to Empire: Leadership Transitions at ServiceNow" - Stanford Business School Case Study (2023) - Academic analysis of ServiceNow's leadership evolution

-

"The Single Platform Advantage: ServiceNow's Architecture" - MIT Sloan Management Review (2024)

- Technical and strategic analysis of ServiceNow's platform architecture

Books & Extended Reading

- "Amp It Up" by Frank Slootman (2022) - The former ServiceNow CEO's playbook for hypergrowth

- "Winners Dream" by Bill McDermott (2014) - Current CEO's leadership philosophy

- "The Phoenix Project" by Gene Kim - IT transformation concepts that influenced ServiceNow

- "Platform Revolution" by Parker, Van Alstyne & Choudary - Framework for understanding platform businesses

Podcasts & Interviews

- Bill McDermott on "Masters of Scale" with Reid Hoffman - ServiceNow's AI strategy

- Frank Slootman on "The Tim Ferriss Show" - Building and scaling ServiceNow

- Fred Luddy on "How I Built This" - The founding story of ServiceNow

- Gina Mastantuono on "Fortune's Leadership Next" - Financial strategy and growth

Financial Reports & Investor Resources