Newmark Group: The Story of Wall Street's Real Estate Services Powerhouse

I. Introduction and Episode Roadmap

Picture this: a twenty-seven-year-old commercial real estate broker in Midtown Manhattan, hustling to fill a struggling office building with toy companies and dinnerware manufacturers. Nobody gives him much thought. Fast forward four decades and that same broker, Barry Gosin, runs a publicly traded commercial real estate services giant generating more than three billion dollars a year in revenue, competing head-to-head with firms ten times its size. Along the way, his company was absorbed into a financial empire built by one of Wall Street's most controversial figures, survived the worst pandemic in a century, navigated the existential crisis facing the American office market, and emerged as the fastest-growing commercial real estate services firm in the world.

This is the story of Newmark Group, ticker NMRK, currently valued at roughly two and a half billion dollars with more than eight thousand employees across a hundred and sixty offices on four continents. It is a story about people, relationships, financial engineering, and the question every investor in commercial real estate must answer: what happens when the fundamental premise of your industry, that people need offices, gets challenged by a once-in-a-generation shift in how humans work?

But this is not just a story about offices. It is a story about how a scrappy New York City brokerage became BGC Partners' billion-dollar spin-off, challenged the dominance of CBRE and JLL, and positioned itself at the intersection of Wall Street and Main Street in ways few competitors can replicate. It is a story about immigrant ambition, family drama, corporate resurrection, and the peculiar alchemy of commercial real estate, an industry where relationships still matter more than algorithms, where a single broker can generate tens of millions in revenue, and where the line between boutique and bureaucracy determines who wins.

The cast of characters includes Barry Gosin, the longest-tenured CEO in commercial real estate who turned a family-owned brokerage into a public company powerhouse. Howard Lutnick, the Cantor Fitzgerald CEO who survived September 11th, built a financial technology empire, and ultimately left the private sector to become the forty-first United States Secretary of Commerce. And the Gural family, whose patriarch founded what would become one of Manhattan's most respected real estate firms, only to see it absorbed into a global platform they could never have imagined.

To understand Newmark, you need to understand three things: the economics of commercial real estate brokerage, the financial engineering that created and then liberated the company, and the structural forces reshaping the industry today. We will cover all three, starting from the very beginning.

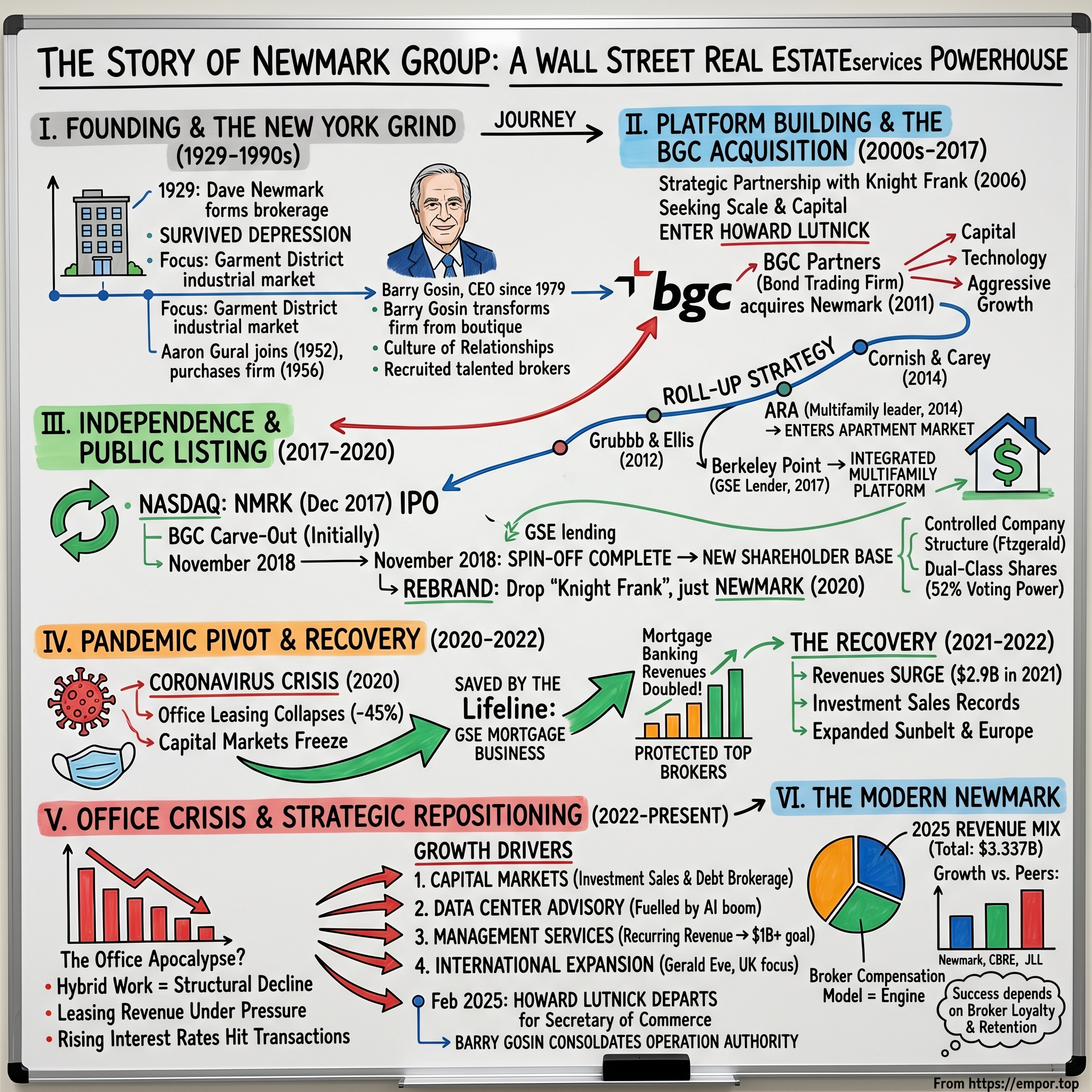

II. The Founding Story: Barry Gosin and the Newmark Name (1929-1990s)

In 1929, the same year the stock market crashed and the Great Depression began, a man named Dave Newmark hung out his shingle on a modest Manhattan office and started a commercial real estate brokerage. The timing could not have been worse. But commercial real estate, unlike stocks, does not evaporate overnight. Buildings still stand. Tenants still need space. And in the chaos of economic upheaval, there are always landlords who need someone to fill their vacant floors.

Newmark and Company survived the Depression by doing what small New York brokerages do: grinding. The firm concentrated on the city's industrial market, particularly the Garment District, helping landlords lease space to manufacturers, wholesalers, and the unglamorous businesses that kept Manhattan's economy functioning.

It was not prestigious work. The buildings were secondary. The tenants were price-sensitive. But it was honest, steady brokerage, and it established a presence that would prove durable. In commercial real estate, surviving your first decade is the hardest part. The business is inherently cyclical, relationships take years to build, and the temptation to quit during a downturn is overwhelming. That Newmark survived not just its first decade but the worst economic contraction in American history says something about the tenacity of its early practitioners.

Dave Newmark eventually sold the firm to a group of brokers that included a man named Aaron Gural, who had joined the company in 1952. By 1956, Gural and his partners had purchased Newmark outright, and by 1957, Aaron Gural assumed the role of Chairman, a position he would hold for more than four decades.

Gural transformed Newmark from a modest brokerage into something more ambitious. In 1958, he made the firm's first major property purchase: 230 Fifth Avenue. What made this notable was not just the building itself but the method. Gural was among the first in the industry to use a syndication model for acquisition, pooling capital from multiple investors to buy properties that no single buyer could afford. This was innovative for the late 1950s and foreshadowed the financial engineering that would later define the firm.

Through the 1960s, Newmark acquired increasingly prestigious properties, including 515 Madison Avenue, the historic DuMont building, its first Class A office property. Over his six-decade tenure, Aaron Gural was involved in the acquisition of more than six million square feet of buildings in the New York metropolitan area. He was also one of the first real estate executives to see the potential for restoring West Side industrial sites and abandoned lofts in the Garment District, a vision that anticipated the neighborhood transformations that would make those properties enormously valuable decades later.

Aaron's son, Jeffrey Gural, joined the family business in 1972 after working at Morse-Diesel Construction Company, where he had supervised the construction of more than one million square feet of new office space. Jeffrey was a civil engineer by training, a graduate of Rensselaer Polytechnic Institute, and brought a builder's sensibility to a firm run by deal-makers. He would eventually manage a real estate portfolio of approximately eight and a half million square feet worth roughly three billion dollars.

But the person who would truly shape Newmark's destiny arrived from outside the family. Barry Gosin, a graduate of Indiana University where he studied economics and history, was a young broker at a firm called H.L. Richer and Associates. His job was leasing space at 41 Madison Avenue for the Rudin family, one of New York's legendary real estate dynasties. He was good at it. Over three years, he filled a troubled Midtown South office building with toy companies and dinnerware companies, tenants that nobody else wanted to chase.

The origin story of Gosin's partnership with the Gurals has the quality of a commercial real estate parable. Jeffrey Gural discovered that the young upstart was poaching tenants from the Gural family's property at 230 Fifth Avenue. Rather than fight him, Gural decided to recruit him. In 1978, Jeffrey Gural and Barry Gosin purchased the management and brokerage company from Aaron Gural and his partners. In 1979, Gosin became Chief Executive Officer, a role he has held continuously for more than forty-six years.

To appreciate what Gosin built, you need to understand how commercial real estate brokerage differs from residential real estate. In residential, the product is relatively commoditized, margins are thin, and technology has increasingly disintermediated the agent. Commercial real estate is a different animal entirely. A single office lease can involve millions of square feet, hundreds of millions of dollars, and negotiations that stretch over months or years. The broker is not just matching buyer and seller. The broker is an advisor, a market intelligence source, a relationship manager, and often a dealmaker who structures transactions that require deep expertise in finance, law, and market dynamics.

The economics reflect this complexity. A top commercial broker can generate tens of millions of dollars in annual revenue, making them more like star athletes or investment bankers than traditional salespeople. They command guaranteed compensation, recruiting bonuses, and equity stakes. And they are fiercely loyal to firms that provide the right platform, the right culture, and the right deal flow. Losing a top broker is like losing a franchise quarterback.

Gosin understood this intuitively. His leadership philosophy centered on relationships, both with clients and with his own brokers. He built a culture that was boutique, deeply New York, and intensely personal. When the October 1987 stock market crash rattled the city's real estate market, Gosin persuaded Gural to reinvigorate their brokerage business rather than retreat into property ownership. It was a pivotal strategic decision. While competitors pulled back, Gosin invested in talent and market presence, a pattern he would repeat throughout his career.

There is a telling anecdote from Gosin's early days that reveals his instincts as a dealmaker. Newmark partnered with developer David Walentas to purchase buildings in DUMBO, the Brooklyn neighborhood that sits beneath the Manhattan Bridge, for ten dollars a square foot. They held those buildings for fifteen years as the neighborhood transformed from a forgotten industrial backwater into one of New York's most desirable residential and creative office markets. That patience, the willingness to bet on a neighborhood before anyone else saw its potential, would become a hallmark of Gosin's approach: build relationships, understand markets deeply, and be willing to wait for the payoff.

The 1990s were a difficult period for New York commercial real estate. The savings and loan crisis, a local recession, and the broader economic malaise kept both Gosin and Gural relatively inactive. But Gosin used the quiet years to build out Newmark's advisory capabilities, adding services beyond pure tenant representation and landlord leasing. By the time the market recovered in the late 1990s, Newmark had a more diversified platform than its size would suggest.

By the early 2000s, Newmark was a respected, mid-sized New York commercial brokerage. It was profitable, well-connected, and deeply embedded in the city's deal-making ecosystem. But it was also small. The industry was dominated by global giants: CBRE, JLL, and Cushman and Wakefield, firms with billions in revenue, thousands of brokers, and offices spanning every major market worldwide. Newmark was a boutique competing in a world that increasingly rewarded scale. To grow, it would need capital, infrastructure, and a partner willing to bet big on commercial real estate.

In 2006, Newmark found an interim solution by forming a strategic partnership with Knight Frank, a London-based global real estate consultancy with over a century of history. The firm rebranded as Newmark Knight Frank. The two firms worked together to service international clients without ever formally merging, maintaining separate legal structures while operating under the combined name. At its peak, the partnership operated from more than two hundred and forty offices across five continents with a combined staff exceeding seven thousand. It was a clever arrangement, providing global reach without the complexity of a true merger. But it was also inherently limited. Newmark needed something more transformative.

That transformation would arrive in the form of one of Wall Street's most polarizing figures.

III. Enter Howard Lutnick: The BGC Partners Acquisition (2011)

To understand how a bond trading firm ended up owning a commercial real estate brokerage, you need to understand Howard William Lutnick. Born on July 14, 1961, in Jericho, Long Island, into a Jewish family, Lutnick's early life was shaped by tragedy that would have broken most people. His father, Solomon Lutnick, taught history at Queens College. His mother, Jane, was a sculptor and art teacher. At sixteen, during his senior year of high school, his mother died of lymphoma. Then, as a freshman at Haverford College, his father died after accidentally receiving an overdose of a chemotherapy drug. In the span of two years, Lutnick was an orphan.

Haverford College stepped in with a full scholarship, allowing Lutnick to continue his education. He graduated with a degree in economics in 1983 and would later repay the institution with sixty-five million dollars in donations, making him Haverford's largest benefactor. The experience shaped his worldview: relentless, intense, and driven by an almost primal need to build and survive.

After college, Lutnick worked briefly at Noonan, Astley and Pierce as a broker for the U.S. dollar-Japanese yen exchange, where he met B. Gerald Cantor, the founder of Cantor Fitzgerald, one of Wall Street's most important government bond dealers. Cantor took Lutnick as his protege and hired him in 1983. Within eighteen months, Lutnick had risen to run a division that managed personal investments for Cantor and his associates, transforming it into one of the firm's most profitable units. By 1990, at twenty-nine years old, Lutnick became President and CEO of Cantor Fitzgerald.

Then came September 11, 2001. Cantor Fitzgerald's corporate headquarters occupied floors 101 to 105 of One World Trade Center, two to six floors above where American Airlines Flight 11 struck the building. The firm lost 658 employees that morning, including Howard's brother Gary. Lutnick survived only because he had taken his son to his first day of kindergarten. The company brought its trading markets back online within a week, partly through its London office. Lutnick established the Cantor Fitzgerald Relief Fund, which ultimately donated one hundred and eighty million dollars to victims' families.

What followed was a decades-long effort to rebuild and diversify Cantor Fitzgerald. In 1998, the firm had begun developing eSpeed, an electronic trading platform for Treasury bonds, investing two hundred and fifty million dollars. eSpeed launched in 1999 and became a model for electronic fixed-income trading. In 2004, Lutnick established BGC Partners as a separate partnership for Cantor's voice brokerage business. In 2008, he merged BGC Partners and eSpeed in a deal worth $1.3 billion, creating a financial technology powerhouse.

But Lutnick wanted diversification beyond financial services. The 2008 financial crisis had demonstrated the dangers of concentration in a single industry. Interdealer brokerage, BGC's core business, was under structural pressure from electronic trading and regulatory changes. Dodd-Frank and other post-crisis regulations were squeezing margins on the financial intermediation that had been BGC's bread and butter. The writing was on the wall: BGC needed a new growth engine or it would slowly atrophy as electronic platforms ate its core business.

Commercial real estate was the answer. Lutnick's reasoning was characteristically bold. He recognized that commercial real estate brokerage shared the same fundamental DNA as financial brokerage: connecting buyers and sellers in opaque, relationship-driven markets where information asymmetry creates value for intermediaries. But unlike fixed-income brokerage, where technology was rapidly eliminating human middlemen, commercial real estate remained stubbornly analog. Every building was unique. Every lease negotiation was different. Every market had its own dynamics. This was a business where technology would enhance human advisors rather than replace them, and where BGC's capital and infrastructure could create a platform for growth. On April 28, 2011, BGC Partners announced it had entered into an agreement to acquire the U.S. business of Newmark Knight Frank. The deal was structured with BGC's typical financial engineering: sixty-three million dollars in cash at closing, $2.3 million in BGC stock, and up to an additional $33.4 million in stock payable over five years if Newmark hit certain revenue targets. The maximum total consideration was approximately ninety-nine million dollars, significantly below industry estimates that had projected a price between $125 million and $200 million.

The transaction encompassed approximately 425 Newmark brokers and included the firm's New York business plus majority interests in more than twenty-five domestic offices and affiliated companies. The deal closed on October 14, 2011. Barry Gosin and Newmark's management team became partners in BGC, with Gosin continuing as CEO reporting to Lutnick. Jeffrey Gural became Chairman Emeritus.

The skepticism was immediate and understandable. What did a bond trading firm know about commercial real estate brokerage? The cultures could not have been more different. BGC's world was electronic trading, financial derivatives, and the frenetic pace of Wall Street. Newmark's world was long lunches with landlords, building tours with corporate tenants, and relationships cultivated over decades. As one industry observer put it, it was like asking a Formula One racing team to manage a landscaping business.

The deal price itself raised eyebrows. At under one hundred million dollars for a firm with four hundred and twenty-five brokers and twenty-five-plus offices, the implied price per broker was roughly two hundred thousand dollars, a figure that seemed low even by the standards of a market still recovering from the financial crisis. For context, individual top brokers at major firms command annual compensation packages worth several million dollars. Buying the entire firm for less than the cost of recruiting twenty star brokers from competitors seemed either brilliant or delusional, depending on who you asked.

But Lutnick saw something others did not. Both businesses were fundamentally about brokerage: connecting buyers and sellers, providing market intelligence, and earning commissions on transactions. BGC had built sophisticated technology platforms for financial markets. Newmark had deep relationships in commercial real estate. The question was whether those capabilities could be combined. Lutnick also saw something more fundamental: real estate brokerage was undergoing the same consolidation that financial services had experienced a decade earlier. The firms that invested in scale, technology, and cross-selling would win. The firms that remained local boutiques would gradually lose share. BGC had the playbook. Newmark had the starting position.

What made the deal work, against the odds, was a single decision: keeping Barry Gosin.

IV. The Transformation Begins: Building a Platform (2011-2017)

In most acquisitions, the founder or CEO of the acquired company leaves within a year or two. Cultural clashes, ego conflicts, and differing visions make coexistence difficult. The fact that Barry Gosin not only stayed but thrived under BGC's ownership is the single most important factor in Newmark's transformation.

Gosin understood something that many acquired CEOs miss: the acquirer's resources, combined with your own expertise, can create something neither party could build alone. BGC brought capital, technology infrastructure, and an aggressive growth orientation. Newmark brought relationships, market knowledge, and the trust of clients who had worked with the firm for decades. The key was using BGC's resources without destroying Newmark's culture.

The roll-up strategy began almost immediately, and the pace was remarkable. Within six years, Newmark would complete more than a dozen acquisitions, each one filling a geographic gap, adding a specialized capability, or bringing aboard a team of experienced brokers. The playbook was deliberate: identify targets that were undervalued, culturally compatible, or strategically essential, then integrate them into the Newmark platform while preserving the relationships and local market knowledge that made them valuable in the first place.

The first transformative deal came in 2012, when Grubb and Ellis, once one of America's largest commercial real estate firms, filed for Chapter 11 bankruptcy. Founded in 1958, Grubb and Ellis had listing approximately $150 million in assets against $167 million in debt, and the NYSE had delisted the company for falling below $15 million in average market capitalization. BGC served as the stalking horse bidder in the bankruptcy auction, having previously acquired roughly thirty million dollars of Grubb and Ellis's senior debt at a discount and provided $4.8 million in debtor-in-possession financing to keep the company operating.

The acquisition closed on April 13, 2012, and the combined entity was rebranded as Newmark Grubb Knight Frank. Overnight, Newmark went from a respected regional firm to a national platform. The deal gave Newmark a nationwide network of offices, an established client base across markets it had never served, and experienced brokers in cities far from Manhattan. Most importantly, BGC had acquired these assets at a fraction of what it would have cost to buy Grubb and Ellis as a going concern. It was the kind of opportunistic deal-making that defined the Lutnick playbook: aggressive, financially creative, and timed to capitalize on someone else's distress.

The acquisition spree continued with methodical precision. In 2014, Newmark acquired Cornish and Carey Commercial, Northern California's premier commercial real estate firm, establishing a dominant position in the San Francisco Bay Area and Silicon Valley. That same year, the firm made what would prove to be one of its most important strategic moves: the acquisition of Apartment Realty Advisors, known as ARA, for approximately $110 million. ARA was the nation's largest privately held investment brokerage network focused exclusively on the multifamily apartment market, generating annual revenues exceeding $100 million and pre-tax earnings above $20 million. This was Newmark's decisive entry into multifamily investment sales, a market that would become one of the most resilient and fastest-growing segments of commercial real estate.

Smaller deals filled geographic gaps and deepened capabilities: Excess Space Retail Services in 2015 added specialized retail expertise, regional firms in Cincinnati, Memphis, and other markets expanded the footprint, and multifamily brokerages in Tennessee and Florida strengthened the apartment platform. Each acquisition followed the same logic: buy relationships and expertise in markets where Newmark was underweight, integrate them into the platform, and cross-sell services.

The crown jewel came in 2017 with the acquisition of Berkeley Point Financial for $875 million, by far Newmark's largest deal. Berkeley Point was a leading commercial real estate finance company specializing in originating and selling multifamily loans through government-sponsored enterprise programs, specifically Fannie Mae, Freddie Mac, and FHA/HUD. For the trailing twelve months ended March 2017, Berkeley Point had generated $314 million in revenue, up fifty-five percent year over year, and $143 million in pre-tax income, up an astonishing one hundred and sixty-nine percent.

To understand why this deal mattered, you need to understand how GSE lending works in commercial real estate. Fannie Mae and Freddie Mac, the government-sponsored enterprises that most people associate with residential mortgages, also play a massive role in multifamily apartment financing. They provide a secondary market for apartment loans, which means that lenders who originate these loans can sell them to Fannie or Freddie, freeing up capital to make more loans. The firms that are approved to originate and sell these loans, known as DUS lenders in Fannie Mae's program, essentially operate as franchisees of the federal mortgage machine. They earn origination fees when they make loans and servicing fees for the life of the loan, which can be twenty or thirty years. Getting approved as a DUS lender takes years and requires demonstrating strong underwriting performance. It is not something you can replicate quickly, which makes it a genuinely scarce asset.

The strategic logic was elegant. Combined with the earlier ARA acquisition, Berkeley Point created a vertically integrated multifamily platform. Newmark's brokers could sell apartment properties through ARA and originate the financing through Berkeley Point in a single transaction. Think of it as a one-stop shop: the same firm that helped you buy the apartment complex could also arrange the mortgage. The GSE lending relationships also provided something critically important for a cyclical business: a stable, recurring revenue stream through loan servicing fees. Every mortgage originated continued generating fees for years after the initial transaction closed.

Throughout this period, Newmark was also fighting talent wars against its much larger competitors. Recruiting brokers from CBRE, JLL, and Cushman and Wakefield required offering not just competitive compensation but a cultural proposition. Gosin's pitch was essentially "boutique feel with big firm capabilities." At Newmark, a top broker would not be a number in a bureaucracy of forty thousand employees. They would have direct access to the CEO, the flexibility to structure deals creatively, and the backing of a public company's resources. It was a compelling value proposition, particularly for experienced brokers who had grown frustrated with the corporate machinery of the giants.

The technology investments during this period were real but measured. Newmark was never going to out-spend CBRE or JLL on technology. CBRE was investing hundreds of millions in platforms like its Vantage data analytics suite and its Hana flexible office technology. JLL was making similar bets with its JLL Technologies division, which made direct venture investments in proptech companies. For a firm Newmark's size, matching that spend dollar-for-dollar would have been financially reckless.

Instead, Newmark focused on tools that directly supported its brokers: data analytics for market intelligence, client relationship management systems, and cross-selling platforms that made it easy for a leasing broker to introduce a capital markets colleague to the same client. The philosophy was technology as enabler, not technology as substitute for human relationships. It was the difference between building a self-driving car and giving a professional driver better maps, navigation, and real-time traffic data. Both approaches have merit, but they reflect fundamentally different views of where value is created.

By 2017, Newmark had been transformed from a two-hundred-person New York City brokerage into a full-service national platform with thousands of professionals, diverse service lines spanning leasing, capital markets, valuation, property management, and mortgage brokerage, and a vertically integrated business model that few competitors could match. The question was what came next.

V. The IPO That Was Not Really an IPO: The 2017 Spin-Off

In December 2017, Newmark Group began trading on the NASDAQ Global Select Market under the ticker NMRK. The mechanics of how it got there tell you a great deal about the financial engineering that has defined this company's corporate life.

BGC Partners initially filed for a Newmark IPO with a placeholder of $100 million on October 23, 2017. Newmark Group, Inc. was created as a wholly owned subsidiary of BGC to hold the entire Real Estate Services business segment. The plan was to sell a minority stake to the public while BGC retained majority ownership, what Wall Street calls a "carve-out."

The original proposed price range was $19 to $22 per share, but during the roadshow, investor appetite proved more muted than expected. The range was revised downward to $14 to $15, a significant reduction that reflected challenging conditions for financial services IPOs and some investor wariness about the BGC/Cantor corporate structure.

The final pricing came in at $14 per share, the low end of the revised range. Twenty million shares were offered, raising approximately $280 million. The pricing discount was a humbling start for a company that had been growing rapidly and taking market share. It was a reminder that Wall Street investors care about corporate governance and control structures, not just growth rates and revenue targets.

Despite the pricing discount, the stock performed well on its first day of trading, December 15, 2017, gaining roughly eighteen percent and suggesting the shares had been meaningfully underpriced. Public stockholders initially owned only about fifteen percent of Newmark's Class A common stock, with BGC retaining the vast majority of ownership. Goldman Sachs, Bank of America Merrill Lynch, and Citigroup served as joint book-running managers for the offering.

The IPO's mixed reception reflected a broader challenge: commercial real estate services companies were not a high-demand IPO category. Investors who wanted real estate exposure could buy REITs, which offered direct asset ownership, dividend yields, and tax advantages. Commercial real estate services firms offered none of those things. Instead, they offered cyclical, fee-based revenue with heavy dependence on transaction volumes and broker compensation costs. The investment thesis required belief in management's ability to grow market share, cross-sell services, and build recurring revenue streams, a more complex story than simply owning buildings and collecting rent.

The real story, however, was not the IPO itself but what came a year later. On November 30, 2018, BGC Partners completed the distribution of all remaining Newmark shares through a special pro rata stock dividend. Stockholders of BGC Class A common stock received 0.464 shares of Newmark for every one share of BGC they held. The spin-off was structured to be generally tax-free to BGC stockholders for federal income tax purposes.

The impact on Newmark's trading dynamics was dramatic. Before the spin-off, roughly twenty-three million shares were in the public float. After, approximately one hundred and fifty million shares were freely tradeable. This massive increase in float was significant for institutional investor access and eventual index inclusion. More importantly, it eliminated the parent company discount that typically weighs on carve-out stocks, where investors apply a haircut because the parent can influence decisions in ways that do not benefit minority shareholders.

But "fully independent" was something of an overstatement. The spin-off severed the parent-subsidiary relationship, but it did not sever the web of connections between Newmark, BGC, and Cantor Fitzgerald. Howard Lutnick remained Executive Chairman of Newmark while serving as Chairman and CEO of both BGC and Cantor. Related-party relationships persisted through shared services agreements covering human resources, payroll, legal, and accounting functions. Tax agreements governed the allocation of historical tax liabilities. And most importantly, Cantor maintained significant influence through a dual-class share structure that gave its Class B shares ten votes per share compared to one vote per share for the publicly traded Class A stock.

This corporate structure is the kind of thing that gives governance-focused investors heartburn. Cantor held approximately fifty-two percent of voting power despite a smaller economic interest, meaning public shareholders could not outvote the controlling family on any matter, including board elections, mergers, or major transactions.

To put this in concrete terms: if Cantor wanted to approve a related-party transaction, elect a particular slate of directors, or block a merger proposal, public shareholders would have no ability to override that decision, regardless of how many shares they owned. The company's own SEC filings acknowledged that Cantor and its affiliates held interests "which may conflict with Newmark's and who may exercise their control in a way that favors their interests to Newmark's detriment." That is an unusually candid disclosure, and investors should take it at face value.

For investors comfortable with controlled companies, the trade-off is straightforward: you accept limited governance rights in exchange for alignment with an operator who has significant skin in the game and a track record of value creation. There is a long tradition of successful controlled companies in American business: Google, Facebook, Berkshire Hathaway, and many others operate with similar dual-class structures. The argument is that long-term strategic vision benefits from insulation against short-term market pressures.

For those who are not comfortable, it is a deal-breaker. Governance-focused institutional investors, including many index funds and pension funds that have adopted stewardship principles, have been increasingly vocal about opposing dual-class structures. This limits Newmark's potential institutional shareholder base and likely contributes to a persistent valuation discount. The tension has followed Newmark throughout its public life and continues to shape its investor base.

The spin-off did accomplish its primary goal of unlocking value by giving Newmark its own currency for acquisitions, its own capital allocation strategy, and a distinct narrative separate from BGC's financial services business. Commercial real estate investors and financial services investors are fundamentally different constituencies with different valuation frameworks. A real estate-focused fund manager wants to evaluate Newmark against CBRE and JLL, using metrics like revenue per broker, capital markets transaction volume, and recurring revenue growth. A financial services investor evaluating BGC cares about trading volumes, electronic execution rates, and regulatory capital. Forcing both to evaluate a single conglomerate meant neither could apply their preferred analytical framework cleanly.

By separating the two, BGC allowed each company to attract its natural investor base. It was a textbook example of the sum-of-the-parts thesis: two companies trading independently should, in theory, be worth more than the conglomerate.

Now independently listed and theoretically free, Newmark entered 2019 with momentum and ambition. But independence also meant accountability. There was no parent company to absorb losses or provide capital during a downturn. Newmark would have to stand on its own merits. The company also had to build credibility with a new class of institutional shareholders who cared deeply about governance, capital allocation, and strategic clarity, qualities that had been less important when BGC was the parent.

In October 2020, the company took a symbolic step that reflected its growing independence: Newmark formally dropped the Knight Frank name and rebranded simply as Newmark. CEO Gosin stated that the Knight Frank business had generated less than one percent of Newmark's annual revenue and that the partnership "restricted our growth." The rebranding signaled that Newmark no longer needed the credibility of a century-old London brand. It had built its own. Knight Frank subsequently partnered with Cresa, a tenant-only advisory firm, effectively ending a fourteen-year chapter in Newmark's history.

But well before the rebranding, a reckoning was coming that nobody anticipated.

VI. Independence and Growth: The Post-Spin Era (2018-2020)

The arrangement at the top of Newmark after the spin-off was unusual even by the standards of corporate America. Barry Gosin served as CEO, running day-to-day operations with the same hands-on, relationship-driven approach he had employed for four decades. Howard Lutnick served as Executive Chairman, maintaining strategic oversight and the connection to the broader Cantor/BGC ecosystem. The dynamic required both men to operate in their respective lanes: Gosin handled clients, brokers, and deal-making; Lutnick handled corporate strategy, capital markets relationships, and the financial engineering that had defined the company's structure.

It worked, largely because both men understood the arrangement's logic. Gosin had no interest in corporate finance and Lutnick had no interest in tenant rep leasing. Each needed the other, and the division of labor was relatively clean. But it also created a peculiar corporate personality: a company that spoke the language of Wall Street at the board level and the language of Midtown landlords on the deal floor.

In 2018, Newmark completed one of the most significant acquisitions of its post-spin history: RKF Retail Holdings, a New York-based retail real estate advisory firm that was one of the country's premier retail leasing specialists. Adding RKF deepened Newmark's position in the retail sector at a time when most firms were retreating from brick-and-mortar, a contrarian bet that assumed the retail apocalypse narrative was overdone for well-located properties. It was classic Gosin: buy when others are fearful, and trust that relationships and local knowledge will outlast macro trends.

Newmark continued its broader acquisition strategy, expanding geography and capabilities. The company built out service lines in property management, facilities management, and workplace strategy consulting, all of which generated more predictable, recurring revenue compared to the transactional leasing and capital markets businesses. The mortgage brokerage business, anchored by the Berkeley Point acquisition, became an increasingly important growth engine. Government-sponsored enterprise lending provided counter-cyclical stability: when economic uncertainty increased, government-backed financing became more attractive, not less.

The competitive landscape was intensifying. CBRE, already the world's largest commercial real estate services firm, was investing hundreds of millions in technology platforms, data analytics, and a vision of real estate as a technology-enabled managed service. JLL was pursuing a similar path, acquiring technology companies and building digital tools for occupiers. Cushman and Wakefield had gone public in 2018, adding another well-capitalized competitor with global ambitions.

The industry's direction was clear: bigger firms with broader capabilities would capture an increasing share of corporate clients who wanted to consolidate their real estate services with a single provider. A Fortune 500 company managing offices in fifty countries wanted one firm, one platform, one point of accountability. That favored scale in ways that made life harder for mid-size players.

Newmark's differentiation strategy threaded a needle. It aimed to offer the capabilities of a global full-service firm while maintaining the cultural identity of a boutique. In practice, this meant that top brokers at Newmark had more autonomy, more direct access to leadership, and more flexibility in structuring deals than their counterparts at larger firms. For certain clients, particularly entrepreneurial real estate owners and mid-market companies, this was a compelling proposition. For the largest corporate occupiers managing portfolios of hundreds of offices worldwide, the scale advantages of CBRE and JLL were harder to overcome.

By early 2020, Newmark had established real momentum. Revenue had grown to $2.2 billion in 2019, and the company was gaining market share in key segments. The multifamily platform was firing on all cylinders. The brand was strengthening outside New York. Margins were expanding as the acquisitions of prior years were integrated and synergies realized.

The stock, which had recovered from its initial post-spin volatility, was trading in the low teens, reflecting growing investor confidence. More importantly, the narrative was shifting. Newmark was no longer "BGC's real estate division" or "the firm Howard Lutnick bought." It was becoming Newmark, a company with its own identity, its own investor base, and its own strategic direction. The acquisitions had been integrated, the platform was working, and the growth trajectory was clear. For the first time in its public life, the company's story was its own to tell.

Then a novel coronavirus emerged in Wuhan, China, and within weeks, every assumption about commercial real estate was thrown into question.

VII. The Pandemic Pivot: Crisis and Opportunity (2020-2021)

On March 18, 2020, Newmark's stock hit $2.49, an all-time low that represented a decline of more than eighty percent from pre-pandemic levels. The speed of the collapse was staggering even by the standards of a market in freefall. Commercial real estate, the most physical of assets, had suddenly become the most uncertain.

Office leasing, the beating heart of the commercial real estate services industry, effectively stopped. Corporate tenants froze every decision. Nobody knew whether employees would ever return to offices, whether long-term leases made sense, or how to value buildings whose fundamental purpose was being questioned.

Think about what this meant for a company like Newmark. The core product of a commercial real estate brokerage is, at its simplest, helping a company find and lease office space or helping a landlord find tenants to fill a building. When nobody wants to lease office space, or nobody knows how much space they will need in six months, there is no deal to broker and no commission to earn. It is as if every restaurant in the country simultaneously stopped ordering food: the farmers, distributors, and wholesalers who depend on those orders have nothing to sell.

Leasing revenues collapsed forty-five percent in the second quarter alone. Capital markets transactions seized up as buyers and sellers could not agree on pricing when the outlook was completely unknowable. Investment sales revenues fell thirty percent.

But the picture was not uniformly bleak, and Newmark's earlier strategic decisions paid off in ways that even management could not have fully anticipated. The mortgage brokerage business, built on the Berkeley Point acquisition just three years earlier, became the company's lifeline. Government-sponsored enterprise lending not only continued during the crisis, it actually accelerated. Gains from mortgage banking activities increased fifty-three percent, and multifamily mortgage originations rose twenty-three percent versus fourteen percent for the industry overall. Fannie Mae and Freddie Mac kept the multifamily lending machine running even as private capital markets froze. This was the specific, tangible value of the Berkeley Point deal: when everything else broke, the GSE mortgage business held.

Management's response combined aggressive cost-cutting with strategic talent preservation. CEO Barry Gosin and Chairman Howard Lutnick each took fifty percent base salary reductions. CFO Michael Rispoli, Chief Legal Officer Stephen Merkel, and other senior managers took fifteen percent cuts.

These were not just symbolic gestures. In a company where broker morale and loyalty are the primary competitive assets, leadership taking visible pay cuts sent a message that the pain was being shared from the top. The company targeted approximately $100 million in support and operations cost reductions for 2020, achieving more than forty million dollars in savings by the second quarter alone. Non-essential travel was eliminated, hiring was frozen for support functions, and office space was consolidated. But the broker headcount was protected.

The more important decision was what Newmark did not cut: its top brokers. In a people business, your product walks out the door every evening. If your best brokers defect to competitors during a downturn, recovering market share in the upturn becomes exponentially harder. Gosin made a deliberate bet that the pandemic's impact on leasing was temporary and that protecting talent through the downturn would yield outsized returns when markets recovered.

Full-year 2020 revenue came in at approximately $1.9 billion, a fourteen percent decline from 2019. Adjusted EBITDA fell thirty-seven percent. It was painful, but it was survivable, largely because the mortgage business and management services provided ballast against the transactional revenue collapse. Management services and servicing fees, the most recurring parts of the business, declined only about twelve percent, demonstrating the value of contractual relationships that persist regardless of transaction activity.

To put the pandemic's impact in context, consider the bifurcation within Newmark's own business. Leasing commissions were down forty-five percent in the fourth quarter of 2020, with office leasing almost non-existent in cities like San Francisco and New York. Meanwhile, mortgage banking revenues doubled to $100 million in that same quarter. The company was simultaneously experiencing its worst business line performance and its best, in the same fiscal period. The diversification that the acquisition strategy had created, often criticized as unfocused, proved to be the company's salvation.

The thesis that the pandemic was a temporary disruption proved mostly correct, though not in the way the office market bulls had hoped. What roared back first was not office leasing but capital markets. By the fourth quarter of 2020, capital markets revenues grew more than fifteen percent year over year and mortgage banking revenues doubled to $100 million in the quarter. Investors were eager to deploy capital into real estate, particularly in sectors that benefited from pandemic-driven trends: industrial warehouses for e-commerce, multifamily apartments for a generation rethinking homeownership, and data centers for the digital infrastructure underlying remote work.

Newmark also made an opportunistic play during the crisis. Knotel, a flexible office space company in which Newmark had invested, struggled to pay rent and filed for Chapter 11 bankruptcy in early 2021. Newmark provided twenty million dollars in debtor-in-possession financing and ultimately acquired Knotel in March 2021, entering the flexible workspace sector at a steep discount. CEO Gosin called it "a benefit and an opportunity."

The recovery in 2021 was nothing short of extraordinary. Full-year revenues reached approximately $2.9 billion, a fifty-three percent increase from 2020 and significantly above the pre-pandemic 2019 level. Investment sales volumes were up more than two hundred percent in some quarters, reaching quarterly records that exceeded 2019 levels by seventy-six percent. Adjusted EBITDA more than tripled in some quarters.

The magnitude of the rebound reflected a commercial real estate market that was not just recovering but restructuring. Capital flooded into industrial properties to meet e-commerce demand. Multifamily apartment transactions surged as housing prices pushed more Americans toward renting. Data center investment accelerated as cloud computing and early AI workloads demanded more processing capacity. Even within the struggling office sector, trophy buildings in prime locations attracted attention from investors betting on the flight to quality.

Newmark did not just recover. It emerged materially stronger, with market share gains across multiple business lines, proof that the strategy of protecting talent and investing through the downturn had been the right call.

The company hired aggressively during the recovery, adding over a dozen senior executives to its Global Corporate Services division and earning more than two hundred new business assignments in the first half of 2021 alone. The company expanded its workplace strategy, emerging technology, and safety and wellness consulting services in direct response to post-pandemic corporate real estate needs. These were not peripheral offerings. They addressed the fundamental question every corporate tenant was asking: how much space do we need, how should it be configured, and how do we keep our employees safe?

By this point, Newmark had approximately 18,800 professionals across roughly five hundred offices worldwide. The scrappy New York brokerage had become a genuine global platform. Total revenues had grown from roughly $200 million at the time of the BGC acquisition to nearly $3 billion in just a decade, a compounding rate that justified the roll-up strategy, even accounting for the pandemic interruption. Newmark's multifamily origination market share had more than quadrupled since 2011, and its U.S. investment sales share had more than doubled.

But the office question lingered. And as 2021 gave way to 2022, the commercial real estate industry began to reckon with an uncomfortable reality: hybrid work was not going away.

VIII. The Inflection Point: Office Crisis and Strategic Repositioning (2022-2024)

The narrative in commercial real estate circles during 2021 had been cautiously optimistic. Yes, people were working from home, but surely they would come back. The return-to-office mandates would arrive. The cultural benefits of in-person collaboration would reassert themselves. The office market would normalize.

It did not normalize, at least not to pre-pandemic levels. By 2022, the data was undeniable. Office occupancy in major cities remained thirty to fifty percent below pre-pandemic levels. Not temporarily, not cyclically, but structurally. Walk through the financial district of any major American city on a Wednesday afternoon and it looks busy. Walk through on a Friday and it feels like a holiday. That is the new normal. Companies had discovered that many employees could be productive working from home, and that the cost savings from reducing office footprints were real and significant. The average lease size declined by nearly twelve percent from pre-pandemic levels. The office market experienced eighteen consecutive quarters of net absorption losses from mid-2020 through late 2024, meaning more space was being vacated than leased.

For Newmark, this was not an abstract market trend. It was a direct assault on a significant portion of the company's revenue. Office leasing commissions, historically the largest single component of commercial real estate brokerage revenue, were under structural pressure. Not cyclical pressure that would resolve with economic recovery, but structural pressure driven by a fundamental change in how companies used space.

The financial impact was visible in the numbers. Revenue declined from $2.9 billion in 2021 to $2.7 billion in 2022 and fell further to $2.47 billion in 2023, the trough year. The stock suffered accordingly, falling from a January 2022 high of approximately $18.43 to a low of $5.18 in May 2023, a seventy-two percent decline that reflected the market's growing fear that the office apocalypse would permanently impair the company's earning power.

The rising interest rate environment compounded the pain. The Federal Reserve's aggressive rate hiking cycle, which took the federal funds rate from near zero to over five percent in less than eighteen months, hit commercial real estate particularly hard. Higher rates increased borrowing costs, reduced property values, and froze transaction activity. Investment sales volumes across the industry declined sharply as the gap between buyer and seller price expectations widened. For a company like Newmark, which earns fees on transactions, the combination of structural office decline and cyclical capital markets weakness was a double blow.

Newmark's strategic response was to lean into the parts of the business that were growing while the office headwind played out. The company doubled down on capital markets, particularly investment sales and debt brokerage, where transaction activity was driven by interest rates and capital flows rather than tenant demand. Valuation and advisory services were expanded, benefiting from the growing complexity of real estate assets and the need for independent assessments in a uncertain market. The mortgage brokerage business continued to provide reliable cash flow through its GSE lending relationships.

Perhaps the most strategically significant move during this period was Newmark's aggressive push into data center advisory. The explosive growth of artificial intelligence and cloud computing had created insatiable demand for data center capacity, and Newmark positioned itself as a leading advisory firm in this niche. The company launched a dedicated Data Center and Digital Infrastructure Capital Markets practice and began facilitating some of the largest data center financing transactions in history. These included a $7.1 billion construction loan for Blue Owl Capital and Crusoe to develop a 1.2-gigawatt AI data center in Abilene, Texas, a $5 billion joint venture for AI and high-performance computing data centers, and a $3.4 billion joint venture for a one-million-square-foot Texas data center. Newmark's own research noted that AI-related data centers had directed $31.5 billion in annualized spending on new construction, making digital infrastructure the only commercial real estate segment in a genuine structural boom.

Geographically, Newmark accelerated its expansion into Sunbelt markets, where population growth and corporate relocations were driving demand for commercial real estate services. The company also pushed aggressively into international markets, particularly Europe. In 2023, it acquired Gerald Eve, a leading UK real estate advisory firm with nine offices, followed by BH2, a UK capital markets firm, in 2024. A Paris-based valuation firm, Catella Valuation Advisory, was acquired in 2025, along with Canadian Appraisals from Altus Group for North American valuation capabilities. In January 2025, the London-based firms began operating under the Newmark brand, consolidating the company's European presence. Newmark now has more than one thousand professionals across the UK, France, Germany, Ireland, the Netherlands, Belgium, Italy, and Poland.

The management services business quietly became the company's most important source of stability. Revenue from management services grew from $624 million in 2019 to $954 million in 2025, a fifty-three percent increase that transformed the segment into the company's most stable recurring revenue base. Newmark increased its square feet under management by seventy-four percent over just four years, an organic and acquisition-fueled expansion that provides contractual, multi-year revenue streams that do not fluctuate with transaction cycles. Combined with servicing fees, these recurring businesses now generate well over a billion dollars annually. The company has stated a goal of generating over two billion dollars in recurring revenue within five years, a target that would fundamentally shift Newmark's earnings profile from cyclical to more predictable.

In October 2025, Newmark acquired RealFoundations, a Dallas-based real estate consulting and managed services firm, further bolstering its recurring revenue base. The acquisition added capabilities in fund and asset management consulting, technology implementation, and managed services for institutional real estate investors, a client segment that prizes ongoing relationships over one-off transactions.

The international dimension of the strategy deserves emphasis. Newmark generated nearly $350 million in revenue from outside the United States in the twelve months through September 2024, representing a more than sixty percent compound annual growth rate since the 2017 IPO. The company had set a goal of having ten percent of revenue generated internationally by 2025, a target it exceeded. Expansion into Italy, France, Germany, and the Asia-Pacific region accelerated in 2025, with more than one hundred professionals added outside the U.S. since the start of 2024 alone.

And then, in a development nobody in commercial real estate saw coming, the company's controlling shareholder left for Washington.

IX. The Modern Newmark: Business Model Deep Dive (2024-Present)

In February 2025, Howard Lutnick was confirmed as the forty-first United States Secretary of Commerce. The appointment required him to divest his economic interests in Newmark under a government ethics agreement. In May 2025, Newmark repurchased approximately eleven million shares of Class A common stock from Lutnick at $11.58 per share, the closing price on May 16, for a total of roughly $127 million. Lutnick transferred his Cantor Fitzgerald ownership to trusts for the benefit of his sons Kyle and Brandon Lutnick, with Brandon, who became Chairman and CEO of Cantor, as controlling trustee.

The departure changed Newmark's power structure in meaningful ways. Barry Gosin assumed the additional role of Chairman of Newmark's operating company, consolidating his operational authority for the first time in the company's public history. Stephen Merkel, the firm's Executive Vice President and Chief Legal Officer, became Chairman of the Board of Directors. Luis Alvarado was named Chief Operating Officer in April 2025, and Richard Holden was promoted to President of Property and Facilities Management.

The question investors must grapple with is whether Lutnick's departure strengthens or weakens Newmark. On one hand, it eliminates the governance complexity of having a Chairman who was simultaneously running two other companies and removes a lightning rod for investor criticism. The conflicts of interest that came with Lutnick's dual roles are now structurally resolved, at least with respect to the man himself.

On the other hand, his departure raises succession questions about the next generation of controlling shareholders. Brandon Lutnick is now Chairman and CEO of Cantor, Newmark's controlling shareholder. Kyle Lutnick, age twenty-eight, sits on Newmark's board and previously ran Knotel, the company's flexible office business. Both are young and relatively untested in public markets. The transition from a battle-tested, if controversial, controlling figure to his adult children introduces a new and largely unknowable variable into the company's governance equation.

Today, Newmark's revenue mix reflects a diversified commercial real estate services platform. In fiscal year 2025, the company reported record total revenues of $3.337 billion, a twenty-two percent increase from the prior year. The fourth quarter alone generated more than one billion dollars in revenue, up fifteen percent from the prior year and beating analyst estimates.

Breaking down the full year: leasing and other commissions contributed just over one billion dollars, surpassing that threshold for the first time and growing seventeen percent, outpacing the company's publicly traded competitors. Management services generated $954 million, up fifteen percent. Capital markets investment advisory produced $559 million, growing thirty-four percent and significantly outpacing the roughly thirty to thirty-five percent industry growth in transaction volumes. Mortgage brokerage and debt placement contributed $254 million, up a remarkable fifty-four percent as the commercial real estate lending market thawed. Servicing fees and other revenue added $413 million.

Net income doubled to $126 million, and diluted earnings per share rose from thirty-four cents to sixty-eight cents. The company beat analyst earnings estimates in all four quarters of 2025, building credibility with institutional investors who had been skeptical of the company's ability to deliver consistent results.

The broker compensation model is the engine of this business, and understanding its economics is essential. Top commercial real estate brokers typically operate on a commission split, receiving a percentage of the commissions they generate. In practice, the economics look more like a professional sports franchise than a traditional corporation. Star brokers command guaranteed compensation packages, signing bonuses worth millions of dollars, and in some cases equity participation. They bring their client relationships with them when they move firms, which means that losing a top broker can mean losing millions in annual revenue. Conversely, recruiting a top broker from a competitor can immediately add millions to the top line.

This dynamic creates a fundamentally different cost structure than most service businesses. Compensation is the company's largest expense, and it is largely variable: when transaction volumes fall, broker commissions fall proportionally. This natural hedge provides some cyclical protection, as the company's largest cost automatically adjusts with revenue.

But guaranteed compensation packages create a floor that does not adjust downward, which can compress margins during downturns. When a firm has committed to paying a star broker five million dollars a year regardless of production, and that broker's market is in a slump, the economics can turn negative quickly. The art of running a commercial real estate services firm is managing this tension: paying enough to attract and retain talent while maintaining profitability across the cycle. Get it wrong in either direction, pay too little and lose your best people, pay too much and destroy margins, and the consequences are severe.

Technology investments have accelerated in recent years. The company's proprietary N360 platform provides market data, deal analytics, and client relationship management tools. Newmark has positioned itself as "tech-enabled" rather than "tech-first," a distinction that matters. The company uses technology to make its brokers more productive and better informed, not to replace them. This is in contrast to some proptech startups that have attempted to disintermediate the broker entirely, an approach that has largely failed in commercial real estate where deal complexity demands human expertise.

Where Newmark sits today relative to its competitors tells a clear story. CBRE generates roughly $40.5 billion in annual revenue. JLL generates $26 billion. Cushman and Wakefield generates $10.3 billion. Newmark generates $3.3 billion. By revenue, Newmark is one-twelfth the size of CBRE and less than one-third the size of Cushman and Wakefield. But the relevant metrics are growth rate and profitability. Newmark grew revenue twenty-two percent in 2025, compared to thirteen percent for CBRE, eleven percent for JLL, and nine percent for Cushman and Wakefield. And Newmark's net margin of 3.8 percent was actually the highest among the four, reflecting its asset-light model and strong execution.

For investors, the company guided fiscal 2026 revenue of $3.7 billion to $3.8 billion, representing roughly fourteen percent growth at the midpoint. Adjusted EBITDA guidance of $635 million to $675 million and adjusted earnings per share of $1.82 to $1.92 imply continued margin expansion. In February 2026, the board authorized a $400 million share repurchase program, a meaningful statement of confidence for a company with a market capitalization of roughly $2.5 billion. The quarterly dividend of three cents per share, while modest, has been consistent.

The relationship with Cantor Fitzgerald remains significant and complicated. Cantor is still Newmark's largest and controlling shareholder, holding approximately fifty-two percent of voting power through its super-voting Class B shares. An Administrative Services Agreement governs the provision of shared services between the two companies, auto-renewing annually. These arrangements are common among affiliated companies, but they create the potential for conflicts of interest that require careful monitoring. Each year's proxy filing discloses the terms and amounts of these related-party transactions, and investors who are evaluating Newmark should review these disclosures closely.

Institutional Shareholder Services has flagged governance concerns, assigning Newmark a high-risk audit pillar score of two on a ten-point scale, where one represents the highest risk. That score reflects concerns about board independence, audit committee composition, and the related-party relationships that come with the Cantor affiliation. These are real issues for institutional investors who prioritize governance quality, and they likely contribute to the valuation discount Newmark trades at relative to its growth rate. Whether that discount is warranted or represents an opportunity depends on one's view of whether the controlling family's interests are sufficiently aligned with public shareholders.

X. Strategy and Competitive Analysis Frameworks

To evaluate Newmark's competitive position rigorously, it helps to apply Porter's Five Forces and Hamilton Helmer's Seven Powers frameworks to commercial real estate services.

Threat of New Entrants: Moderate. Starting a commercial real estate brokerage requires virtually no capital. You need a license, a phone, and relationships. Regional boutiques enter the market constantly, and in certain local markets they can be formidable competitors. But building a scaled platform with national reach, mortgage brokerage capabilities, GSE lending relationships, property management infrastructure, and brand recognition is extraordinarily difficult. The barriers are not financial but relational and regulatory. It takes decades to build the trust and market intelligence that institutional clients demand, and GSE lending licenses require years of performance history. New entrants can compete locally but face enormous challenges scaling nationally, which protects the incumbents' position. The recent trend of large institutional clients consolidating their real estate services with a single provider further raises the bar for entry.

Supplier Power: Very High. This is the most important force in the industry. The "suppliers" in commercial real estate services are the brokers themselves. Top producers are free agents who can move between firms, taking their client relationships and deal flow with them. They command enormous compensation packages, often in the millions of dollars, and they know it. A single top broker might generate twenty to thirty million dollars in annual revenue, making them enormously valuable and incredibly expensive to replace. The implication for firms like Newmark is that broker retention and recruiting are not just operational tasks. They are existential priorities. The company that wins the talent war wins the market.

Buyer Power: Moderate to High. Large corporate occupiers increasingly consolidate their real estate services with a single provider, giving them significant negotiating leverage on fees. Fee compression has been a persistent industry trend, with commission rates gradually declining as clients become more sophisticated and competition intensifies. However, for complex transactions, specialized market knowledge, and relationship-intensive advisory work, clients are willing to pay premium fees. The tension between commoditized services where buyers have power and specialized advisory where they do not defines the industry's competitive dynamics.

Threat of Substitutes: Growing. Technology platforms like CoStar, VTS, and various proptech startups have created tools that allow some transactions to occur with less broker involvement. Flexible space operators like WeWork and IWG offer alternatives to traditional long-term leases. Direct deals between landlords and tenants bypass brokers entirely in some markets. But for large, complex transactions, the substitution threat remains low. Nobody buys a fifty-million-dollar office building using a smartphone app. The threat is real at the margin but has not fundamentally disrupted the broker's role in significant transactions.

Competitive Rivalry: Intense. The industry is an oligopoly at the top, with CBRE, JLL, Cushman and Wakefield, and Newmark competing for the same brokers, clients, and transactions in every major market. Below them sit hundreds of regional firms that compete aggressively on local knowledge and relationships. The rivalry is fierce because switching costs for clients are low and the product, at its core, is a commoditized service. Differentiation comes through broker talent, market intelligence, and the quality of advisory relationships, all of which are difficult to maintain at scale.

The overall picture from Porter's framework is an industry with moderate profitability and intense competition for the key input: broker talent. The most important strategic implication is that firms must win the talent war to win the market. Technology, brand, and scale matter, but they matter primarily because they help attract and retain the best people. Every other competitive advantage in commercial real estate services is downstream of this fundamental reality.

Applying Helmer's Seven Powers framework reveals Newmark's strategic position more clearly. The company has limited scale economies in the traditional sense because brokerage is fundamentally a local, relationship-driven business. A broker in Atlanta does not become more productive because Newmark also has a broker in Chicago. But there are emerging scale advantages in data, technology, and mortgage brokerage, where larger origination volumes create better pricing and more competitive loan products. Network effects are moderate and localized: more brokers in a market create more deal flow, which attracts more listings, which attracts more brokers. But these effects are geographically bounded. Counter-positioning is where Newmark has attempted to differentiate, pitching itself as "boutique with scale" against the bureaucratic giants. The success of this positioning depends on whether clients actually value the boutique culture or simply want the lowest fee.

Switching costs are low for clients, who can hire a different broker for every transaction. But they are surprisingly high for brokers, whose compensation structures, pending deals, and relationship networks create real friction in moving between firms. A broker with ten pending deals cannot easily walk away mid-transaction, and the guaranteed compensation structures that firms offer typically include clawback provisions that create golden handcuffs. Branding is strong in Newmark's home market of New York City but still developing elsewhere. The company's cornered resource, if it has one, is its concentration of top broker talent in key markets, particularly multifamily and capital markets. Process power is developing through technology investments and cross-selling disciplines but is not yet a durable competitive advantage.

The overall picture from Helmer's framework is a company with one genuinely powerful competitive asset: its people. Everything else, scale, technology, brand, process, is either moderate or still developing. That is both honest and somewhat sobering. It means Newmark's competitive position is only as durable as its ability to keep its best brokers happy, productive, and loyal. In a rising market with a rising stock price, that is relatively easy. In a prolonged downturn, it becomes the company's greatest vulnerability.

The key insight from these frameworks is that commercial real estate services is a people business first and a technology business second. The winner-take-most dynamics operate at the level of individual talent, not necessarily at the level of market share. A firm with the best brokers in a market will outperform regardless of its global scale, which is why Newmark can compete effectively against firms twelve times its size. But this also means the company's moat is inherently fragile. It depends on the continued satisfaction and loyalty of human beings who can walk out the door at any time. There is no patent, no proprietary algorithm, no network effect that prevents a top broker from accepting a competitor's recruiting offer next quarter. This is both the opportunity and the vulnerability at the heart of the Newmark story.

One myth worth examining is the idea that Newmark is "just a smaller version of CBRE." The reality is that the companies operate quite differently despite offering similar service categories. CBRE has built a massively scaled, technology-heavy platform that emphasizes process standardization, global consistency, and data-driven decision-making. It serves the world's largest occupiers with a turnkey solution for managing global real estate portfolios. Newmark, by contrast, emphasizes broker autonomy, deal creativity, and a flatter organizational structure. Its sweet spot tends to be the entrepreneurial owner, the mid-market company, and the complex transaction that requires customized structuring rather than process execution. These are different competitive positions serving partially overlapping but distinct client segments. Neither is inherently superior; they serve different needs in a large, fragmented market.

For investors tracking Newmark's performance, two KPIs matter more than any others. The first is capital markets transaction volume, which captures the firm's momentum in its fastest-growing and highest-margin business line. Strong volume growth signals market share gains and favorable macro conditions. The second is recurring revenue as a percentage of total revenue (management services plus servicing fees), which measures the company's progress toward a more stable, less cyclical earnings profile. As this ratio rises, the company's earnings quality improves and its valuation should expand. These two metrics, tracked quarterly, provide the clearest window into whether Newmark's strategic transformation is succeeding.

XI. Bull vs. Bear Case

The bull case for Newmark rests on several reinforcing pillars. The office market, after four years of decline, has shown nascent signs of stabilization. Net absorption turned positive for the first time in late 2024, representing the best performance since 2019. A massive wave of lease renewals is approaching: forty-nine percent of pre-pandemic office leases remain unrenewed, including 1.4 billion square feet scheduled for renewal between 2025 and 2027. Even if many tenants downsize, the sheer volume of renewal activity should drive leasing commissions higher. And the flight to quality is real: Class A properties captured fifty-two percent of all leasing despite representing only one-third of inventory, suggesting that demand for premium office space is returning even as secondary space languishes.

Capital markets represent perhaps the strongest element of the bull case. Transaction volumes are recovering from a cyclical trough, and Newmark has been gaining market share aggressively, with investment sales volumes up fifty-six percent in 2025 against roughly thirty to thirty-five percent industry growth. The data center advisory practice represents an entirely new revenue stream that barely existed three years ago but is already facilitating multi-billion-dollar transactions. As interest rates normalize, pent-up demand from investors sitting on dry powder should drive further transaction activity.

The mortgage brokerage business provides genuine counter-cyclical protection. GSE lending through Fannie Mae and Freddie Mac operates somewhat independently of private capital market cycles. During the 2020 crisis, this business grew while everything else contracted. The servicing portfolio generates recurring fees for years after origination, creating a steadily growing annuity stream. Revenue from this segment grew fifty-four percent in 2025 alone.

The company's growth rate relative to peers is notable. Newmark's twenty-two percent revenue growth in 2025 was roughly double the rate of CBRE and JLL, suggesting sustainable market share gains driven by talent acquisition, geographic expansion, and platform capability. The European expansion, which has added more than a thousand professionals and approximately $350 million in run-rate revenue in just three years, represents a long runway for international growth. Management services growth of fifty-three percent since 2019 demonstrates the company's ability to build recurring revenue streams that reduce earnings volatility.

On valuation, the stock trades at roughly 11.4 times trailing EBITDA and less than eight times the midpoint of 2026 adjusted EBITDA guidance, a discount to CBRE and JLL that reflects the governance concerns and cyclical uncertainty but may underestimate the company's growth trajectory. The $400 million share repurchase program authorized in February 2026 represents roughly sixteen percent of the current market capitalization, a meaningful level of capital return if executed.

The company's net leverage of 0.8 times, per management, is conservative for a services business and provides capacity for both additional acquisitions and shareholder returns. Adjusted free cash flow of $269 million in 2025, up thirty-eight percent year over year, demonstrates the company's ability to convert earnings into cash.

The bear case is equally substantive. The structural decline in office demand may be permanent and deeper than current estimates suggest. Hybrid work has become entrenched. Companies continue to reduce their footprints at renewal. Average lease sizes have declined nearly twelve percent from pre-pandemic levels, and there is no evidence this trend is reversing. If the forty-nine percent of unrenewed leases result in significant downsizing rather than renewal at comparable sizes, the lease renewal wave could disappoint expectations. Office represents a meaningful portion of Newmark's leasing revenue, and a prolonged secular decline in this segment would structurally impair earnings.

Fee compression is a persistent headwind. As technology reduces information asymmetry and corporate tenants become more sophisticated purchasers of real estate services, commission rates face downward pressure. The largest corporate occupiers increasingly demand volume discounts and competitive bidding, squeezing margins on precisely the clients that full-service firms most want to serve.

The talent defection risk is real and underappreciated. If Newmark's stock underperforms for an extended period, the equity component of broker compensation loses its retention power. Competitors with stronger stock performance or deeper pockets can recruit away key producers, potentially creating a negative spiral: lost brokers lead to lost revenue, which leads to weaker stock performance, which makes it harder to retain remaining brokers. In a people business, this dynamic can accelerate quickly.

Governance concerns deserve more weight than the market typically assigns. The dual-class share structure gives Cantor fifty-two percent voting control. The Lutnick family's interests may not always align with those of public shareholders, and the transition to a younger generation of controllers introduces uncertainty about future decision-making. Related-party transactions with Cantor affiliates create potential conflicts. ISS has flagged the company's audit oversight as high risk.