Nike: Just Do It - The Story of a Global Athletic Empire

I. Introduction & Episode Roadmap

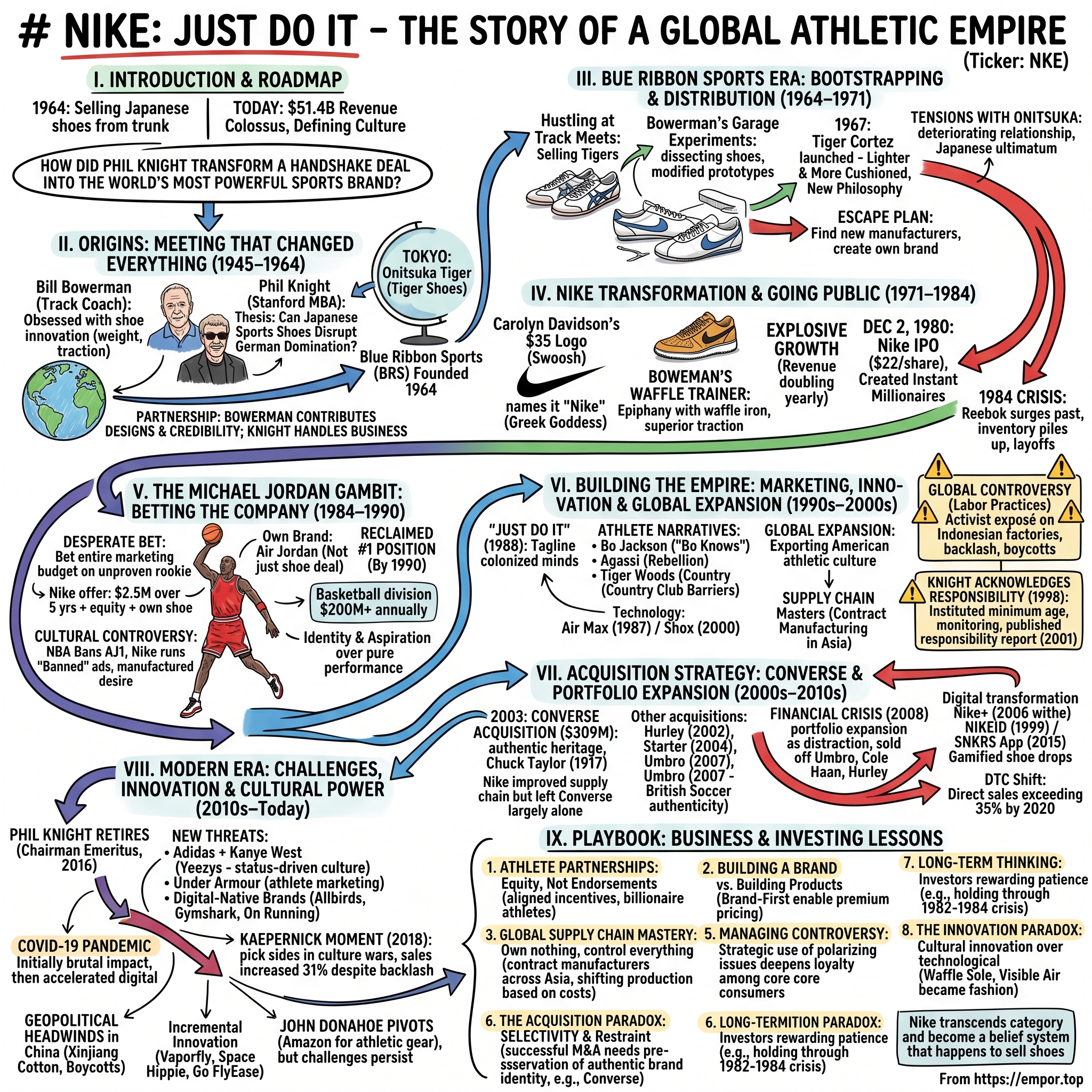

Picture this: It's 1964, and a young Stanford MBA grad is selling Japanese running shoes from the trunk of his beat-up Plymouth Valiant at track meets across Oregon. Fast forward six decades, and that trunk operation has morphed into a $51.4 billion revenue colossus that doesn't just dominate athletic apparel—it defines culture itself. The question that drives this entire story: How did Phil Knight transform a handshake deal over imported shoes into the world's most powerful sports brand?

Nike isn't just a company; it's a verb, a statement, a religion for sneakerheads and athletes alike. Its Swoosh logo carries more recognition than most national flags. Its "Just Do It" tagline has transcended marketing to become a life philosophy. And its market capitalization—hovering around $130 billion as of 2024—makes it larger than the GDP of many countries.

But here's what's fascinating: Nike's dominance wasn't inevitable. The company nearly died multiple times—once in the mid-1980s when Reebok was eating its lunch, again during various supply chain crises, and repeatedly when cultural controversies threatened to torpedo the brand. Each time, Nike didn't just survive; it emerged stronger, often by making bets so audacious they seemed insane at the time.

This is a story about more than shoes and apparel. It's about how a philosophy professor's son and an obsessive track coach built a machine that manufactures desire. It's about betting entire marketing budgets on unproven rookies, turning labor controversies into brand-building moments, and somehow making a 100-year-old basketball shoe company (Converse) feel fresh again. Most importantly, it's about understanding that in the business of sports, you're never really selling products—you're selling dreams.

We'll journey from those early days of hustling at track meets through the Michael Jordan gambit that changed everything, examine how Nike turned controversy into currency with Colin Kaepernick, and decode why some acquisitions like Converse thrived while others like Cole Haan got dumped. Along the way, we'll extract the playbook that transformed a distribution company into a cultural architect.

The throughline connecting every chapter? Nike has consistently understood something its competitors miss: athletic achievement isn't about equipment—it's about belief. And nobody has been better at manufacturing and monetizing belief than the company that tells us to Just Do It.

II. Origins: The Meeting That Changed Everything (1945–1964)

The Oregon rain was coming down hard that autumn day in 1955 when Phil Knight first walked onto Hayward Field at the University of Oregon. The lanky freshman from Portland's Eastmoreland neighborhood had dreams of running glory, but what he found instead was a coach who would change his life in ways he couldn't imagine. Bill Bowerman stood at the edge of the track, stopwatch in hand, studying his runners with the intensity of a scientist examining specimens. Knight would later describe that first meeting as "intimidating as hell"—Bowerman had a way of looking through you, not at you.

Bowerman's backstory reads like American mythology. Born in 1911 in Portland, he'd grown up in Fossil, Oregon, where his family ran the local bank until it failed during the Depression. That early lesson in financial fragility would shape his legendary frugality. After excelling as a student-athlete at the University of Oregon, Bowerman enlisted during World War II, serving in the 10th Mountain Division in Italy. He came back a decorated hero with a Bronze Star and four battle stars, but more importantly, he returned with an engineer's obsession for efficiency and innovation.

By the time Knight met him, Bowerman had already established himself as track royalty. His coaching philosophy was radical for the era: he believed that shaving ounces off a shoe could shave seconds off a time. Weekend nights would find him in his garage, tearing apart shoes and rebuilding them, testing different materials, adjusting spike placements. His wife Barbara learned to hide her kitchen appliances after too many had been requisitioned for shoe experiments. His runners were simultaneously his athletes and his guinea pigs.

Knight's own journey to that track was more conventional but equally formative. The eldest of three children born to Bill Knight—a lawyer turned newspaper publisher—and Lota Knight, Phil grew up in comfortable middle-class Portland. His father was demanding, withholding praise like it was currency in short supply. This created in Phil what he'd later describe as "a fundamental insecurity" that drove him relentlessly forward. At Cleveland High School, he was a good but not great athlete, the kind who made up for modest talent with obsessive preparation.

Under Bowerman's tutelage at Oregon, Knight became a respectable middle-distance runner, posting a personal best of 4:10 in the mile—fast enough to letter, not fast enough for glory. But Bowerman saw something else in Knight: a curious mind and a hunger that had nothing to do with running. The coach would invite Knight to join him on long drives to track meets, using the time to discuss everything from business to philosophy. These conversations planted seeds that would bloom years later.

After graduating from Oregon in 1959 with a degree in journalism, Knight felt adrift. Following his father's advice (or perhaps his father's expectation), he enrolled at Stanford Graduate School of Business in 1960. It was there, in Frank Shallenberger's entrepreneurship class, that lightning struck. The assignment was simple: write a business plan for a hypothetical company. Knight's paper carried a title that would prove prophetic: "Can Japanese Sports Shoes Do to German Sports Shoes What Japanese Cameras Did to German Cameras?"

The premise was elegant. Adidas and Puma dominated the athletic shoe market with German engineering and German prices. But Knight had noticed how Japanese cameras—once dismissed as cheap knockoffs—had systematically destroyed German camera manufacturers through a combination of quality improvement and cost advantage. Why couldn't the same disruption happen in athletic footwear? His professor gave him an A, but more importantly, gave him an idea he couldn't shake.

In 1962, fresh out of Stanford, Knight did something that seems insane by today's risk-averse standards: he bought a ticket to Japan with no connections, no Japanese language skills, and no real plan beyond his thesis. He spent weeks wandering Tokyo, visiting sporting goods stores, examining shoes. Eventually, he discovered Onitsuka Co., makers of Tiger running shoes, in Kobe.

Walking into that Onitsuka factory, Knight was struck by two things: the quality was remarkably good—not Adidas-level, but close—and the prices were shockingly low. When executives asked who he represented, Knight invented a company on the spot: Blue Ribbon Sports. The name came from his childhood, when his mother would pin blue ribbons from track meets to his bedroom wall. The executives, impressed by this young American who'd traveled so far, agreed to send him samples.

Months passed. Knight had almost given up when a shipment arrived: twelve pairs of Tigers. He kept two pairs for himself and, on instinct, mailed two pairs to Bowerman with a note: "These might interest you." What happened next surprised everyone, especially Knight. Bowerman didn't just order more shoes—he offered to become Knight's partner. "I've been trying to get shoe companies to listen to my ideas for years," Bowerman wrote. "Maybe we should be the shoe company."

The partnership they struck was classic Bowerman: practical, unsentimental, and slightly unusual. They'd split the company 50-50, each investing $500. But after thinking it over, Bowerman insisted on adjusting to 51-49, with Knight holding the majority. "Someone needs to break ties," he said, showing a pragmatism that would define their relationship. Bowerman would contribute designs and credibility in the track world; Knight would handle the business side.

On January 25, 1964, Blue Ribbon Sports was officially born. Neither man could have imagined they were launching what would become the world's most valuable athletic company. Knight was still living with his parents, working as an accountant at Price Waterhouse to pay the bills. Bowerman was focused on his team, viewing the shoe business as an extension of his coaching. But they shared something crucial: an obsessive belief that American runners deserved better shoes, and that they were the ones to provide them.

The irony wouldn't be lost on them later: Nike, a company that would come to embody American athletic dominance, began as an import business selling Japanese shoes. But that's the thing about creation myths—they're never as clean as we'd like them to be. The meeting that changed everything wasn't some lightning-bolt moment of inspiration. It was a teacher and student, separated by a generation but united by obsession, deciding to take a shot at giants. The rest, as they say, would require a lot more than just divine intervention.

III. Blue Ribbon Sports Era: Bootstrapping & Distribution (1964–1971)

The green Plymouth Valiant looked out of place among the Chevys and Fords at the Portland State track meet in spring 1964. Phil Knight popped the trunk, revealing boxes of Tiger running shoes arranged with obsessive precision. A few curious runners wandered over, and Knight launched into his pitch—part technical specification, part evangelical sermon about Japanese craftsmanship. By day's end, he'd sold seven pairs. Driving home, $49 richer, Knight couldn't shake the feeling that he was onto something, even if that something meant spending his weekends as a traveling shoe salesman.

This was the reality of Blue Ribbon Sports' first years: Knight, CPA by day, shoe hustler by night and weekend. He'd wake at 5 AM to squeeze in accounting work before his day job at Price Waterhouse, then teach accounting classes at Portland State University in the evenings. Weekends meant loading up the Valiant and driving to track meets across the Pacific Northwest—Eugene, Corvallis, Seattle, anywhere runners gathered. He became a fixture at these meets, the tall, earnest guy with the strange Japanese shoes.

The routine was grueling but oddly satisfying. Knight would set up a card table—later upgraded to a folding display—and arrange the Tigers with the care of a jeweler displaying diamonds. He learned to read runners like a pastor reads his congregation: the high school kid desperate to drop seconds, the college athlete nursing an injury, the weekend warrior chasing a personal best. For each, he had a specific pitch about how Tigers could help them achieve their goals.

Meanwhile, Bowerman was revolutionizing the product from his garage laboratory. His approach to shoe design was equal parts science and mad scientist. He'd film his runners in slow motion, studying how their feet struck the ground. He'd dissect shoes like a medical student dissecting cadavers, cataloging every component. Then came the experiments: removing a few millimeters of rubber here, adding a cushion there, repositioning spikes based on biomechanical data he collected himself.

In 1966, Bowerman sent Knight a modified Tiger with extensive notes: lighter upper material, repositioned spikes, modified heel counter. Knight forwarded the design to Onitsuka, half-expecting to be ignored. Instead, the company's founder, Kihachiro Onitsuka, was intrigued. A former military officer who'd started making basketball shoes in his living room after World War II, Onitsuka recognized a kindred spirit in Bowerman's obsessive innovation. He ordered his team to produce prototypes based on Bowerman's specifications.

The resulting shoe would become the Tiger Cortez, launched in 1967. Bowerman had essentially created a new category: a running shoe that was simultaneously lighter and more cushioned than anything on the market. The Cortez wasn't just a shoe; it was a philosophy made tangible—the idea that athletic equipment should enhance, not hinder, human performance. At track meets, runners would pass the Cortez around like a talisman, marveling at its impossibly light weight.

Success brought its own challenges. By 1969, Blue Ribbon Sports had sold $1 million worth of shoes—a staggering number for a company that was essentially two guys and a handful of part-time employees. Knight finally quit his accounting job, a decision that horrified his father. "You're leaving a secure career to sell sneakers?" Bill Knight asked, the disappointment palpable. But Phil had seen the numbers, understood the trajectory. This wasn't about selling sneakers; it was about riding a wave that was just beginning to build.

The company's first real employee was Jeff Johnson, a runner Knight had met at a track meet who became so evangelical about Tigers that Knight finally hired him as a salesman. Johnson was everything Knight wasn't: effusive, detail-oriented to the point of obsession, and a natural marketer. He would send Knight lengthy letters—sometimes multiple per day—with ideas for advertisements, store displays, and product improvements. Knight rarely responded, driving Johnson half-mad, but he read every word.

Johnson opened Blue Ribbon Sports' first retail store in Santa Monica in 1966, against Knight's explicit instructions. Knight had said to research the possibility; Johnson heard "open a store." The space was tiny—400 square feet—but Johnson transformed it into a shrine to running. He created handmade brochures, started a customer newsletter, and built a database of every serious runner in Southern California. When customers complained about blisters or fit issues, Johnson would document everything and send detailed reports to Knight and Bowerman.

But even as sales exploded, tensions with Onitsuka were building. The Japanese company had noticed Blue Ribbon Sports' success and began wondering why they needed this American middleman. In 1970, Onitsuka executives visited the United States and were stunned to discover that Blue Ribbon Sports had built a sophisticated distribution network, complete with retail stores and a sales force. They'd assumed Knight was still selling shoes from his car.

The relationship deteriorated quickly. Onitsuka began exploring deals with other American distributors, sometimes without telling Knight. They delayed shipments, changed payment terms, and increasingly treated Blue Ribbon Sports as a problem to be managed rather than a partner to cultivate. Knight, ever the chess player, began preparing for the inevitable: Blue Ribbon Sports would need to become more than just a distributor.

The breaking point came at a tense meeting in Japan in early 1971. Onitsuka executives presented Knight with an ultimatum: sell them 51% of Blue Ribbon Sports or lose distribution rights. Knight asked for time to consider, knowing he was really asking for time to execute his escape plan. On the flight home, he sketched out what would need to happen: find new manufacturers, create their own brand, and somehow convince retailers and runners to abandon Tigers for an unknown shoe.

Bowerman, typically pragmatic, saw the split as an opportunity. "We've been fixing their shoes for years," he told Knight. "Why don't we just make our own?" It was a simple question that would require a complex answer. They had no factories, no designs beyond Bowerman's modifications, and no brand identity. What they did have was a deep understanding of runners, a proven distribution network, and the kind of desperate motivation that comes from having no other choice.

The Blue Ribbon Sports era was ending, but not in defeat. Those seven years of bootstrapping had built something more valuable than a profitable distribution business. Knight and Bowerman had created a direct connection to runners, a laboratory for innovation, and most importantly, a belief that they understood American athletes better than any company in Germany or Japan ever could. The foundation was set. Now they just needed a name, a logo, and the audacity to take on the giants of global athletic footwear. Fortunately, audacity was one thing they had in abundant supply.

IV. The Nike Transformation & Going Public (1971–1984)

Carolyn Davidson was a Portland State University graphic design student juggling classes and freelance work when Phil Knight approached her in 1971 with an unusual request. "I need a logo," he said, "something that conveys motion." Her fee: $2 per hour. After 17.5 hours of work, she presented five options. Knight looked at them with the enthusiasm of someone selecting a tax form. He pointed to the checkmark-like design. "I don't love it," he said, "but maybe it will grow on me." That $35 logo—the Swoosh—would become one of the most recognized symbols on Earth.

The name came from Jeff Johnson, who had been badgering Knight with suggestions for weeks. Knight wanted something short, punchy—"Dimension Six" was his favorite, which tells you everything about why founders shouldn't always name their companies. Johnson woke up one morning with "Nike" in his head—the Greek goddess of victory. Knight wasn't thrilled with this either ("What kind of name is that?" he reportedly asked), but with production deadlines looming for their first shoes, Nike it was.

The transformation from Blue Ribbon Sports to Nike in 1971 was more than cosmetic. Knight had secured manufacturing in Mexico and Japan through new partners, essentially building a supply chain from scratch while still fulfilling final Tiger orders. The first Nike shoes were unveiled at the 1972 U.S. Olympic Trials in Eugene—Bowerman's home turf, where the company could count on a friendly audience. The reception was polite but not enthusiastic. Runners trusted Tigers; Nike was an unknown.

Then came Bowerman's breakfast epiphany. One Sunday morning in 1971, Bowerman was eating waffles when inspiration struck. The waffle iron's grid pattern could provide traction without adding weight. Barbara Bowerman watched in horror as her husband poured urethane into her waffle iron, destroying the appliance but creating the prototype for what would become the Waffle Trainer. The shoe debuted in 1974 and was an instant hit—it provided superior traction on the newly popular artificial tracks while being lighter than any competitor.

The numbers from this period tell a story of explosive growth that would make today's venture capitalists weep with envy. From less than $2 million in revenue in 1972, Nike climbed to $14 million by 1976, then $70 million by 1978. By 1979, the company hit $149 million in sales. Revenue and profits weren't just growing—they were roughly doubling every year, a pace that created constant cash flow crises even as the company appeared wildly successful.

Knight's solution to the cash crunch was audacious: go public. On December 2, 1980, Nike held its initial public offering at $22 per share, trading over-the-counter on the NASDAQ. The offering raised $58 million and created instant millionaires among early employees. Carolyn Davidson, who Knight had later gifted 500 shares (not yet disclosed at this time), saw her $35 logo work transformed into serious wealth. The IPO valued Nike at $386 million—not bad for a company that hadn't existed a decade earlier.

But success bred complacency, and complacency in the athletic market is death. By 1982, Nike had claimed nearly 50% of the U.S. running shoe market. Knight and his team assumed this dominance was permanent. They failed to notice that American consumers were shifting from running to aerobics, from performance to fashion. Reebok, with its soft leather aerobic shoes, understood this shift. Nike, still obsessed with shaving milliseconds off race times, didn't.

The numbers from 1984 paint a stark picture: Nike's market share had plummeted from 50% to around 30%. Reebok had surged past them to become number one. Inventory piled up in warehouses—shoes designed for serious runners that casual athletes didn't want. The company laid off 20% of its workforce, closed facilities, and watched its stock price crater. Industry observers began writing Nike's obituary.

Inside Nike's Beaverton headquarters, the mood was funeral. The company that had disrupted an entire industry was being disrupted itself. Knight later described this period as "like watching your child get sick." The hyper-growth years had masked fundamental problems: Nike had become too insular, too convinced of its own mythology, too dismissive of market changes it didn't initiate.

The crisis forced a reckoning. In management meetings that stretched long into the night, Knight and his lieutenants faced hard truths. They'd built a great company for serving athletes but had missed the larger market of people who wanted to look like athletes. They'd mastered performance technology but ignored fashion. They'd conquered running just as America stopped running.

It was Rob Strasser, Nike's marketing chief and Knight's right-hand man, who articulated what would become the survival strategy: "We need to stop thinking like a shoe company and start thinking like a sports company." This meant moving beyond running, embracing basketball and other sports, and most radically, accepting that most people who bought athletic shoes would never use them for athletics.

The boardroom debates were fierce. Bowerman, now in his 70s and semi-retired, argued for staying true to the company's roots in authentic athletic performance. Younger executives pushed for a complete reinvention—fashion-forward designs, celebrity endorsements, lifestyle marketing. Knight, characteristically, said little, absorbing the arguments while playing out scenarios in his head.

What emerged was a hybrid strategy that would define Nike's future: they would maintain credibility with serious athletes while expanding aggressively into the lifestyle market. They would sign endorsement deals not just with established stars but with rising talents. They would treat marketing not as an expense but as an investment in cultural relevance. Most importantly, they would never again assume their dominance was permanent.

The transformation period from 1971 to 1984 had taken Nike from startup to public company to the brink of irrelevance. The company that entered 1984 was battle-scarred, humbled, and desperate. It was also perfectly positioned for what would become the most important signing in sports marketing history. Rob Strasser had identified a rookie basketball player from North Carolina who was entering the NBA draft. The player's name was Michael Jordan, and he preferred Adidas.

What happened next would require Nike to bet everything on a player who had never played a professional game, in a sport where Nike had minimal credibility, at a time when the company could least afford to fail. It was exactly the kind of insane gamble that Phil Knight had been making since he first bought those plane tickets to Japan. The difference was that this time, the entire company's survival depended on getting it right.

V. The Michael Jordan Gambit: Betting the Company (1984–1990)

Sonny Vaccaro sat in the North Carolina gym watching Michael Jordan practice, and he saw something beyond the obvious athletic gifts. It was March 1984, and Vaccaro, Nike's basketball scout and consummate hustler, noticed how Jordan carried himself—the swagger, the competitiveness that bordered on pathological, the way he seemed to perform harder when he knew people were watching. "This kid doesn't just want to win," Vaccaro told Knight later. "He wants to embarrass you while winning." Knight, desperate and intrigued, gave Vaccaro a mission: get Jordan to Nike, whatever it takes.

The situation was beyond dire. Nike's basketball division was a joke—roughly $40 million in annual sales compared to Converse's $250 million and Adidas's dominant position. Nike was the seventh-ranked basketball shoe company. Seventh. Magic Johnson wore Converse. Larry Bird wore Converse. Every serious basketball player wore either Converse or Adidas. Nike was what you wore if you couldn't afford the real brands.

Jordan himself wanted nothing to do with Nike. He was an Adidas kid—had worn them since high school, loved the three stripes, planned to sign with them as soon as they made an offer. When his agent, David Falk, mentioned Nike's interest, Jordan's response was blunt: "I'm not wearing that garbage." He initially refused to even take the meeting. It was only after his mother, Deloris, insisted that he at least hear them out that Jordan reluctantly agreed to visit Beaverton.

The presentation Nike prepared was unlike anything in sports marketing history. They didn't just offer Jordan a shoe deal; they offered him his own brand within Nike—Air Jordan. Rob Strasser and his team had mocked up commercials, designed multiple shoe concepts, created marketing campaigns. They showed Jordan how they would build an entire mythology around him. When Adidas executive came to Jordan with their offer—$100,000 per year and no special shoe—Jordan was insulted. Converse offered $115,000. Nike's offer: $2.5 million over five years, Nike stock options, a percentage of all Air Jordan sales, and something no athlete had ever received—his own signature shoe from day one.

The number made Nike executives physically ill. The company's entire basketball marketing budget for 1984 was $500,000. The Jordan deal would consume five times that, leaving nothing for other players, advertisements, or promotions. Howard White, one of the few Nike executives who understood basketball culture, later admitted: "We were betting everything on a rookie who might blow out his knee in his first game. It was insanity."

But Knight saw it differently. In his Stanford business school way of thinking, Nike needed what he called a "transformative discontinuity"—something that would fundamentally reset market dynamics. Incremental improvement would mean slow death. Jordan represented the chance to leapfrog everyone, to go from seventh place to first in one shocking move. It was the same logic that had driven him to Japan in 1962: when you're behind, conventional strategies ensure you stay behind.

The Air Jordan 1 launched on April 1, 1985, in just six cities, priced at $65—expensive for the era. Nike projected first-year sales of $3 million. They did $126 million. But the real genius wasn't the shoe; it was the controversy Nike manufactured around it. The NBA initially banned the Air Jordan 1 for violating uniform color policies. Instead of redesigning, Nike had Jordan keep wearing them, happily paying the $5,000 per game fine while running ads with the tagline: "Banned by the NBA." Every fine generated headlines. Every headline sold shoes.

Jordan's on-court performance exceeded even Vaccaro's hype. He averaged 28.2 points per game his rookie season, winning Rookie of the Year. But more importantly, he played with a style that redefined basketball aesthetics—the tongue out, the acrobatic dunks, the clutch shots that seemed physically impossible. He wasn't just winning; he was creating moments that became cultural artifacts. The shoes on his feet during these moments became sacred objects for fans.

The cultural impact transcended sports. Air Jordans became street fashion in inner cities, status symbols in suburbs, and most surprisingly, artifacts collected by people who never played basketball. Spike Lee's "Mars Blackmon" commercials for Jordan ("It's gotta be the shoes!") created a new language for sports marketing—irreverent, funny, and completely divorced from traditional athletic performance claims. Nike wasn't selling shoes; they were selling membership in Jordan's kingdom.

By 1990, the transformation was complete. Nike had surged past Reebok to reclaim the number one position in athletic footwear. The basketball division alone was generating over $200 million annually, with Air Jordans accounting for the majority. Jordan's influence had lifted the entire Nike brand—even running shoes sold better because of the association with Jordan's excellence. The company that almost died in 1984 was now valued at over $2 billion.

The downstream effects reshaped the entire sports industry. Every brand started hunting for their own Jordan. Rookie contracts exploded as companies bet millions on unproven talent. The idea of athletes as brands—not just endorsers—became standard. Most significantly, Nike had proven that athletic footwear was really about identity and aspiration. Performance mattered, but narrative mattered more.

Jordan's success also transformed Nike's internal culture. The company developed what insiders called the "Jordan Standard"—the belief that one transcendent athlete could change everything. This would drive future bets on Tiger Woods, Serena Williams, LeBron James, and others. Each time, Nike would offer not just money but a promise: we will make you bigger than sports.

The irony wasn't lost on Knight. Nike had survived by abandoning everything Bowerman had preached about authentic athletic performance. They'd won by selling shoes to people who would never dunk a basketball, never run a marathon, never need the technology packed into their $150 sneakers. But Knight understood something Bowerman perhaps didn't: sports had become America's dominant cultural language, and Nike had positioned itself as that language's primary translator.

The numbers by decade's end were staggering. From near-death in 1984 to over $2 billion in revenue by 1990. From seventh place in basketball to complete dominance. From a company that made shoes to a company that made culture. And at the center of it all was Jordan, still wearing those banned sneakers, still sticking out his tongue, still making the impossible look inevitable. The gambit hadn't just worked—it had redefined what working meant in the business of sports.

VI. Building the Empire: Marketing, Innovation & Global Expansion (1990s–2000s)

Dan Wieden sat in Nike's Beaverton conference room in 1988, struggling to find a tagline that could unite the company's increasingly diverse advertising campaigns. The Portland ad executive had been reviewing Nike ads—Jordan doing the impossible, Bo Jackson playing every sport, everyday athletes pushing through pain. As the meeting dragged on, Wieden remembered Gary Gilmore, the convicted murderer whose last words before his 1977 execution were "Let's do it." Wieden softened it, made it active, and presented: "Just Do It." The room went quiet. Then Phil Knight, who rarely showed emotion, simply nodded. Those three words would become the most successful tagline in advertising history.

"Just Do It" launched during the 1988 Olympics, paired with footage of 80-year-old runner Walt Stack jogging across the Golden Gate Bridge. The genius wasn't in selling shoes—it was in selling permission. Permission to try, to fail, to push beyond comfort. Within a decade, Nike's share of the domestic sport shoe market would surge from 18% to 43%. The tagline didn't just advertise products; it colonized minds.

The athlete endorsement strategy that Jordan pioneered became a sophisticated machine. Nike didn't just sign athletes; they signed narratives. Bo Jackson wasn't just a two-sport athlete; he was superhuman—"Bo Knows" everything except how to be stopped. Andre Agassi wasn't just a tennis player; he was rebellion with a racket. Tiger Woods wasn't just a golfer; he was breaking down country club barriers. Each athlete became a character in Nike's larger story about transcending limitations.

The selection process was equally strategic. Nike executives developed what they called the "pyramid model"—sign hundreds of promising young athletes cheaply, develop the stars, discard the rest. For every Jordan who exploded, there were dozens of forgotten prospects whose contracts quietly expired. But the math worked: one transcendent star could pay for a hundred failures.

International expansion followed American cultural exports. As NBA games appeared on televisions from Barcelona to Beijing, so did Air Jordans. Nike didn't adapt to local markets as much as it exported American athletic culture and convinced the world to adapt to it. By 1995, international sales exceeded U.S. sales for the first time. The Swoosh became a universal symbol, as recognized in São Paulo as in Seattle.

But the international expansion exposed Nike's greatest vulnerability: its supply chain. In 1992, activist Jeff Ballinger published an exposé about Indonesian factories making Nike shoes, documenting workers earning 14 cents per hour—less than the Indonesian minimum wage. The report sparked a decade of controversy that would nearly destroy Nike's carefully cultivated brand.

The criticism escalated through the 1990s. Reports emerged of child labor in Pakistan, dangerous working conditions in Vietnam, poverty wages everywhere Nike manufactured. Protesters appeared at Nike events. Documentaries exposed horrific factory conditions. The company that told everyone to "Just Do It" was being asked what exactly their workers were being forced to do for $1 per day.

Knight's initial response was disastrous. He claimed Nike didn't own the factories, so conditions weren't their responsibility—technically true but morally tone-deaf. The backlash was fierce. University students organized boycotts. Celebrities distanced themselves. Nike stores were vandalized. The brand that represented achievement now represented exploitation.

The turning point came in 1998 when Knight finally acknowledged responsibility. In a speech at the National Press Club, he admitted Nike had become "synonymous with slave wages, forced overtime, and arbitrary abuse." The company instituted minimum age requirements, factory monitoring, and wage improvements. They published their first Corporate Responsibility Report in 2001, listing all factory locations—unprecedented transparency for the industry.

Technology innovation, meanwhile, never stopped. The Air Max, launched in 1987 with visible air cushioning, became both performance enhancement and fashion statement. The Shox system, introduced in 2000 after 16 years of development, looked like springs and performed like magic. Each innovation followed the same pattern: legitimate athletic benefit wrapped in unmistakable visual design. You didn't just feel the technology; everyone could see you had it.

The acquisition strategy during this period was scattershot but revealing. Nike purchased Cole Haan in 1988 for $95 million, attempting to enter the dress shoe market. They bought Bauer Hockey in 1994 for $395 million, trying to dominate winter sports. These moves reflected Knight's ambition to make Nike not just a sports company but a lifestyle conglomerate. Most would eventually fail or be divested, but they demonstrated Nike's cash-generating power and ambition.

Marketing innovations kept pace with technology. Nike.com launched in 1996, years ahead of most retailers. NIKEiD, introduced in 1999, let customers design their own shoes—mass customization before it had a name. Nike Town stores transformed retail into theater, with basketball courts and treadmills where customers could test products. Shopping became experience, purchase became participation.

The numbers by decade's end were stupefying. Revenue in 1990: $2.2 billion. Revenue in 2000: $9 billion. Nike had become the undisputed king of athletic apparel, with roughly 40% market share globally. The company employed 23,000 people directly and hundreds of thousands indirectly. The Swoosh appeared on everything from professional athletes to suburban soccer moms.

But the most significant achievement was cultural. Nike had successfully positioned itself as the arbiter of athletic authenticity while selling primarily to non-athletes. They'd weathered the labor controversy by essentially admitting guilt and promising reform—a playbook other companies would later copy. They'd proven that American sports culture could be packaged and sold globally without significant modification.

The foundation was now complete for Nike's next phase. The company entered the 2000s as more than a business—it was an institution, a language, a religion for those who worshipped at the altar of athletic achievement. The question was no longer whether Nike would survive but whether anything could stop its growth. The answer would come from unexpected places: a financial crisis that crushed consumer spending, new competitors who understood digital natives better than Nike understood millennials, and the retirement of the enigmatic founder who'd started it all selling shoes from his trunk.

VII. The Acquisition Strategy: Converse & Portfolio Expansion (2000s–2010s)

The Converse headquarters in North Reading, Massachusetts, looked nothing like Nike's gleaming Beaverton campus. In 2003, as Nike executives toured the facilities of the company they were about to acquire, they saw peeling paint, outdated equipment, and the remnants of a brand that had declared bankruptcy just two years earlier. Converse—the company that had invented basketball shoes, that had shod Magic and Bird, that had owned basketball before Jordan existed—was now generating barely $200 million in annual sales. Nike paid $309 million for it, and most industry observers thought they'd overpaid for nostalgia.

The acquisition was Phil Knight's idea, though he'd never admit to sentimentality. Converse represented something Nike couldn't create: authentic heritage. While Nike was barely 30 years old, Converse had been making Chuck Taylor All-Stars since 1917. The Chuck Taylor wasn't just a shoe; it was American history you could wear. Punks wore them. Artists wore them. Kurt Cobain died in them. This was cultural equity that no marketing budget could manufacture.

Nike's initial instinct was to Nike-fy Converse—add performance technology, sign athletes, compete directly with their own basketball lines. Wisely, they resisted. Instead, they did something almost unheard of in acquisitions: they left Converse largely alone. The Chuck Taylor remained technologically primitive, uncomfortably flat, objectively terrible for actual basketball. That was the point. Nike realized they hadn't bought a shoe company; they'd bought an anti-Nike, a brand for people who consciously rejected athletic performance culture.

The transformation was subtle but brilliant. Nike improved Converse's supply chain, reducing costs by 20% within two years. They expanded distribution without diluting exclusivity—Chucks appeared in Nordstrom but also kept their presence in vintage stores and punk shops. They created limited editions and collaborations with designers, artists, and musicians. They marketed Converse as creative expression rather than athletic achievement. "Shoes are boring, wear sneakers," became their tagline—a direct rejection of Nike's performance obsession.

By 2019, Converse's revenue had exploded to nearly $2 billion—almost 10 times what it generated at acquisition. The margin profile was even better than Nike's main brand because Converse spent virtually nothing on athlete endorsements or technology development. A shoe designed in 1917 was generating 21st-century profits. It was the most successful acquisition in Nike's history, validating a counterintuitive strategy: sometimes the best way to grow is to buy what you're not.

The Converse success emboldened Nike's acquisition appetite. In 2002, they'd purchased Hurley International, a surf apparel company, for an undisclosed sum (estimated around $120 million). The logic seemed sound—action sports were exploding, and Nike wanted exposure to the surf/skate culture that had always viewed them suspiciously. In 2004, they bought Starter, the company that had dominated sideline apparel in the 1990s, seeing opportunity in the retro trend.

The crown jewel was supposed to be Umbro, the British soccer company Nike acquired in 2007 for $580 million. Soccer was the world's game, and while Nike had made inroads with sponsorships and products, they lacked soccer authenticity. Umbro had been making soccer kits since 1924, had outfitted England's World Cup winners, represented heritage in the sport Nike most needed to conquer.

But the financial crisis of 2008 changed everything. Consumer spending collapsed. Nike's stock price fell by 30%. Suddenly, the portfolio expansion strategy looked less like diversification and more like distraction. The acquired brands, except for Converse, were underperforming. Hurley was losing money. Starter was irrelevant. Umbro was struggling to compete with Adidas's soccer dominance.

Mark Parker, who succeeded Phil Knight as CEO in 2006, made the hard decision: refocus on the core. In 2012, Nike sold Umbro to Iconix Brand Group for $225 million—a $355 million loss. In 2012, they divested Cole Haan to Apax Partners for $570 million. In 2019, they sold Hurley to Bluestar Alliance for an undisclosed but reportedly minimal sum. The message was clear: Nike would be about Nike (and Converse).

The digital transformation during this period was more successful than the acquisition strategy. Nike+, launched in 2006 in partnership with Apple, put sensors in shoes that communicated with iPods. Suddenly, every run could be tracked, shared, gamified. It was Nike's first serious foray into digital engagement, and while the technology seems primitive now, it established a crucial principle: Nike products should generate data, and that data should create community.

The Nike app ecosystem that followed—Nike Training Club, Nike Run Club, SNKRS—transformed Nike from a company you bought from into a company you interacted with daily. The SNKRS app, launched in 2015, gamified shoe drops, creating artificial scarcity and hysteria around limited releases. Shoes that cost $30 to make would retail for $200 and resell for $2,000. Nike had figured out how to manufacture desire as efficiently as they manufactured shoes.

The direct-to-consumer pivot accelerated through the decade. In 2010, direct sales (through Nike stores and Nike.com) represented about 15% of revenue. By 2020, it exceeded 35%. This wasn't just channel shift; it was a fundamental reimagining of Nike's business model. Direct sales meant higher margins, better data, and most importantly, control over the brand narrative. No more relying on Foot Locker to tell Nike's story.

But the most significant strategic development was Nike's embrace of controversy as marketing. When other brands ran from polarizing issues, Nike ran toward them. They kept sponsoring Tiger Woods through his scandal. They stood by Kobe Bryant. They signed Colin Kaepernick after he was effectively blacklisted from the NFL. Each controversy followed a pattern: initial backlash, calls for boycotts, then sales increases as Nike's core consumers rallied around the brand's stance.

The portfolio strategy of the 2000s and 2010s taught Nike valuable lessons. Converse proved that acquisition could work when you bought authentic brands and resisted the urge to over-manage them. The failed acquisitions proved that Nike's competencies—athlete marketing, performance innovation, cultural resonance—didn't automatically transfer to adjacent markets. The digital transformation proved that Nike could evolve from a wholesale manufacturer to a direct-to-consumer tech-enabled brand.

By the end of the decade, Nike's strategy was clear: one mega-brand (Nike), one heritage brand (Converse), and a digital ecosystem that turned customers into communities. The company that had tried to be everything—golf equipment manufacturer, hockey supplier, surf brand—had learned the power of focus. Sometimes the most strategic acquisition is the one you don't make, and sometimes the best way to grow is to shrink your ambitions to match your capabilities.

VIII. Modern Era: Challenges, Innovation & Cultural Power (2010s–Today)

The boardroom at Nike headquarters fell silent as Phil Knight stood up for what everyone knew was coming. It was June 2015, and the 77-year-old founder was finally ready to let go. "I'll be stepping down as chairman next year," he said simply, ending nearly five decades of control over the company he'd built from nothing. The succession had been carefully orchestrated—Mark Parker would remain CEO, Knight would stay involved as Chairman Emeritus—but everyone understood this was the end of an era. The question haunting Nike: could the company maintain its edge without its enigmatic founder pulling the strings?

Knight's final years as chairman had seen Nike reach heights he'd never imagined possible. In 2015, Nike's market capitalization crossed $100 billion for the first time—a psychological barrier that put it in the realm of tech giants rather than apparel companies. The kid who'd sold shoes from his Plymouth Valiant had built something worth more than Goldman Sachs, Boeing, or McDonald's. When Knight officially retired in June 2016, Nike was the undisputed emperor of athletic apparel, commanding roughly 27% of the global athletic footwear market.

But beneath the triumph, tectonic shifts were occurring. Adidas, written off as permanently second-tier, had found a weapon Nike hadn't anticipated: culture-first design. While Nike obsessed over performance metrics and athlete endorsements, Adidas collaborated with Kanye West on Yeezys, creating a shoe that had nothing to do with athletics and everything to do with status. The Yeezy phenomenon caught Nike completely flat-footed—suddenly, the coolest shoes in the world had three stripes, not a Swoosh.

Under Armour emerged as another threat, founded by a former Maryland football player who'd started making moisture-wicking shirts in his grandmother's basement. By 2014, Under Armour had surpassed Adidas in U.S. sales, becoming the number-two sports brand in America. Their strategy was pure Nike playbook—sign transcendent athletes (Stephen Curry), innovate on performance, build mystique—except executed by people who'd studied Nike's every move.

The digital-native brands were even more concerning. Companies like Allbirds, Gymshark, and On Running bypassed traditional retail entirely, building communities on Instagram and selling directly through websites. They didn't need hundred-million-dollar athlete endorsements; they had micro-influencers and authentic user-generated content. They were doing to Nike what Nike had once done to Adidas—attacking from an angle the incumbent couldn't see.

Then came the Kaepernick moment. In September 2018, Nike made Colin Kaepernick—the NFL quarterback who'd been effectively blacklisted for kneeling during the national anthem—the face of the 30th anniversary "Just Do It" campaign. The tagline: "Believe in something. Even if it means sacrificing everything." The backlash was immediate and visceral. Videos of people burning Nike shoes went viral. Politicians called for boycotts. Nike's stock initially dropped 3%.

But Nike had calculated correctly. Their core consumers—urban, young, diverse—supported Kaepernick's stance. Within days, Nike sales increased 31%. The stock not only recovered but hit all-time highs. More importantly, Nike had staked out cultural territory that no competitor dared enter. They weren't just selling shoes; they were picking sides in America's culture wars. The campaign won an Emmy, but more importantly, it proved Nike understood something fundamental: in an attention economy, controversy is currency.

The COVID-19 pandemic in 2020 should have devastated Nike. Stores closed globally. Sports stopped. Who needs athletic gear when gyms are shuttered and marathons canceled? Initially, the impact was brutal—fourth-quarter 2020 revenues fell 38%. Nike laid off employees, closed stores, and watched inventory pile up. The wholesale partners Nike depended on were in crisis. Foot Locker's stock crashed. Dick's Sporting Goods teetered.

But John Donahoe, who'd replaced Mark Parker as CEO in January 2020, saw opportunity in crisis. A former Bain consultant and eBay CEO, Donahoe accelerated Nike's digital transformation. The company poured resources into apps, online experiences, and direct sales. They turned living rooms into gyms through Nike Training Club. They made SNKRS drops into must-watch events during lockdown. By the end of 2020, digital sales had grown 84% year-over-year.

The recovery was swift and decisive. Full-year fiscal 2024 revenues hit $51.4 billion, surpassing pre-pandemic levels. But the revenue number obscured challenges. Nike's China business, representing nearly 20% of sales, faced headwinds from geopolitical tensions and COVID lockdowns. The company faced criticism for allegedly using forced labor in Xinjiang, leading to Chinese consumer boycotts when Nike expressed concern about human rights. Caught between Western values and Chinese markets, Nike discovered the impossibility of being apolitical when you're a cultural symbol.

Innovation continued but felt incremental rather than revolutionary. The Vaporfly running shoes, with their carbon-fiber plates, were so effective they sparked debates about technological doping. The Space Hippie line, made from recycled materials, addressed sustainability concerns. The Go FlyEase, hands-free shoes designed for accessibility, showed Nike thinking beyond traditional athletes. But none captured imaginations like the original Air Jordans or even the recent Yeezys.

The strategic pivots under Donahoe were dramatic. Nike announced they would stop selling through certain wholesale partners, preferring direct relationships with consumers. They invested heavily in logistics and fulfillment, essentially becoming their own Amazon for athletic gear. They acquired predictive analytics companies to better forecast demand. The message was clear: Nike wanted to control every aspect of the customer relationship.

But this created new tensions. Wholesale partners who'd built Nike's distribution for decades were suddenly competitors. Foot Locker's CEO publicly criticized Nike's strategy. Independent retailers felt abandoned. The direct-to-consumer model meant higher margins but also higher capital requirements and operational complexity. Nike was transforming from asset-light marketer to capital-intensive retailer, a transition fraught with risk.

The numbers remained impressive—Nike's market cap exceeded $200 billion by 2021, the stock had returned over 500% in the past decade, and the brand remained number one globally. But questions persisted. Could Nike maintain its cultural relevance as it became increasingly corporate? Could it balance growth in China with Western values? Could it compete with digital natives while managing legacy wholesale relationships?

Most fundamentally: what was Nike without Phil Knight? The company had professional management, sophisticated systems, and unmatched scale. But it had lost something ineffable—the founder's instinct for when to zig while others zagged, the willingness to bet everything on unproven talent, the paranoia that drove constant reinvention. Nike remained the empire, but empires, as history teaches, are most vulnerable when they feel most secure.

IX. Playbook: Business & Investing Lessons

The conference room at Stanford Business School in 2016 was packed beyond capacity as Phil Knight returned to the place where it all began. A student asked the question everyone wanted answered: "What made Nike different?" Knight paused, that characteristic long silence that drove his executives crazy, then responded: "We sold dreams, not shoes. Once you understand that, everything else makes sense." This wasn't just philosophy—it was the cornerstone of a playbook that transformed a distribution company into a $130 billion cultural architect.

The Power of Athlete Partnerships: Equity, Not Endorsements

Nike revolutionized athlete relationships by offering something more valuable than money: partnership. When they signed Michael Jordan, they didn't just pay him to wear shoes—they gave him equity in his own brand, a percentage of sales, and creative input. This aligned incentives in a way traditional endorsement deals never could. Jordan didn't just promote Air Jordans; he was personally invested in their success. This model—replicated with Tiger Woods, LeBron James, and others—created billionaire athletes while generating tens of billions for Nike.

The selection process was equally crucial. Nike didn't chase established stars; they bet on trajectory. Jordan was picked third in the NBA draft. Tiger Woods was a talented amateur. Serena Williams was a teenager. Nike's gift was seeing greatness before it fully manifested, then amplifying it through marketing. They understood that signing an athlete at their peak meant paying peak prices for diminishing returns. Signing them early meant growing together.

Building a Brand vs. Building Products

Most companies make products and hope they become brands. Nike built a brand and then made products to fulfill the brand promise. The Swoosh meant something before most people had worn Nike shoes. "Just Do It" resonated with non-athletes more than athletes. The brand was about human potential, about pushing limits, about the athlete in everyone. Products were just physical manifestations of these ideals.

This brand-first approach enabled premium pricing on functionally similar products. A Nike t-shirt costs $10 to make and sells for $35. A similar quality unbranded shirt might sell for $15. That $20 difference is pure brand value—the price people pay to associate themselves with Nike's mythology. Multiply that margin across billions of products, and you understand how Nike generates 45% gross margins in what should be a commodity business.

Global Supply Chain Mastery: The Asset-Light Revolution

Nike pioneered what would become the standard manufacturing model for consumer brands: own nothing, control everything. They never built factories; instead, they created a network of contract manufacturers across Asia. This asset-light model meant Nike could scale without massive capital investment, shift production based on costs, and focus resources on design and marketing rather than manufacturing.

The sophistication went beyond simple outsourcing. Nike embedded its own quality control staff in factories, dictated production processes, and created competition among suppliers. They pioneered "lean manufacturing" in footwear, reducing inventory and enabling rapid response to demand changes. When labor costs rose in one country, Nike shifted to another. When automation became viable, Nike invested in the technology but had contractors implement it.

Direct-to-Consumer: The Digital Transformation Playbook

Nike's pivot to direct-to-consumer, accelerated under John Donahoe, offers a masterclass in channel transformation. Rather than abandoning wholesale partners immediately, Nike gradually shifted mix—from 15% direct in 2010 to over 40% by 2024. They used data from direct sales to inform product development, creating a feedback loop that wholesale could never provide.

The SNKRS app weaponized scarcity. By making shoe drops events—complete with countdowns, lotteries, and exclusive access—Nike turned purchasing into entertainment. The app has over 30 million users who regularly fail to buy shoes but keep coming back for the thrill of the hunt. This gamification created a secondary market where Nike shoes trade like securities, maintaining brand heat even when retail sales slow.

Managing Controversy: The Kaepernick Calculus

Nike's approach to controversy—embrace it strategically—runs counter to conventional corporate wisdom. The Kaepernick campaign wasn't impulsive; it was calculated. Nike's internal data showed their core consumers (urban, young, diverse) supported athlete activism. Older, conservative consumers who threatened boycotts weren't buying Nike anyway. By taking a stand, Nike deepened loyalty among their target market while generating billions in free media coverage.

This strategy only works with authentic brand strength. Weaker brands that court controversy just generate backlash. Nike could weather the storm because consumers had decades of emotional investment in the brand. The lesson: controversy can be powerful marketing, but only if your brand equity can withstand the initial hit.

The Acquisition Paradox: Why Converse Worked

Nike's acquisition track record offers a crucial lesson: successful M&A requires restraint. Converse succeeded because Nike resisted the urge to Nike-fy it. They improved operations but preserved brand identity. Umbro failed because Nike tried to force it into their model. Cole Haan failed because athletic credibility doesn't transfer to dress shoes. The lesson is selectivity: buy companies whose competencies complement yours, then have the discipline to preserve what made them valuable in the first place.

Long-Term Thinking: The IPO Millionaire Math

If you had invested $10,000 at Nike's IPO in 1980, you would own 58,181 shares worth approximately $5,236,290 based on 2019 prices (the calculation assumes stock splits but not dividend reinvestment). The seven 2-for-1 stock splits turned one original share into 128 shares. But here's the crucial lesson: the real challenge for early investors would have been remaining patient during Nike's brutal mid-1980s period when growth dramatically slowed, revenue grew just 2.9% in fiscal 1985, profits dropped from $40.7 million to $10.3 million, and the stock plummeted 66% between 1982 and 1984.

The investors who held through that crisis—who believed in the brand even when the numbers screamed sell—were rewarded with one of the great wealth-creation stories in market history. This illustrates a fundamental truth: great investments often look terrible before they look great. The ability to distinguish temporary setbacks from permanent impairment is what separates successful long-term investors from everyone else.

The Innovation Paradox

Nike's R&D spending has consistently been among the lowest in the industry as a percentage of revenue—around 1-2% versus tech companies' 10-15%. Yet they're perceived as highly innovative. The paradox resolves when you understand Nike's innovation isn't primarily technological—it's cultural. The Waffle sole was innovative not because it required sophisticated engineering but because Bowerman thought differently about traction. Air Max succeeded not due to technical superiority but because visible technology became fashion.

This suggests a different innovation model: instead of investing heavily in R&D, invest in understanding cultural currents and consumer psychology. Nike's innovations work because they solve problems people didn't know they had (visible air cushioning) or create categories that didn't exist (lifestyle athletic wear). True innovation isn't always about technology—sometimes it's about imagination.

The Nike playbook ultimately teaches that building an enduring company requires multiple paradoxes: sell performance to non-performers, manufacture scarcity in mass production, embrace controversy while maintaining broad appeal, and build a global empire while feeling perpetually paranoid about competition. These contradictions aren't bugs in Nike's system—they're features that have enabled the company to transcend its category and become something more powerful: a belief system that happens to sell shoes.

X. Analysis & Bear vs. Bull Case

Bull Case: The Swoosh as Secular Religion

Walk through any major city on any continent, and you'll see it: the Swoosh on feet, chests, heads, bags. Nike hasn't just built brand power; they've created a visual language that transcends linguistics. This isn't marketing success—it's anthropological victory. When Chinese consumers boycotted Nike over Xinjiang statements, sales initially dropped 20%, but within quarters, young Chinese consumers returned because the Swoosh represents modernity and aspiration in ways local brands cannot replicate. The brand survives controversies that would kill weaker companies because consumers aren't just buying products—they're buying identity.

The innovation pipeline, while not revolutionary, remains robust enough to maintain premium pricing. The Vaporfly controversy—where World Athletics considered banning the shoes for providing too much advantage—was marketing gold. Every serious marathoner now needs Vaporflys, creating a $250 price point for what is essentially foam and carbon fiber. The Go FlyEase hands-free technology opens accessibility markets. The Space Hippie line addresses sustainability concerns. None of these are breakthrough innovations, but each creates a new reason to choose Nike over competitors.

Direct-to-consumer momentum fundamentally changes Nike's economics. At 40% of sales and growing, DTC means Nike captures retail margins that previously went to Foot Locker and others. A shoe that wholesales for $50 and retails for $100 now generates $100 for Nike, not $50. Multiply this across billions in revenue, and you understand why Nike's gross margins have expanded from 43% to 46% over the past decade despite increased competition. The SNKRS app alone generated an estimated $5 billion in 2023—revenue that barely existed a decade ago.

Emerging markets remain underpenetrated. Nike's revenue per capita in China is still one-fifth of the U.S. level. India, with 1.4 billion people and a growing middle class, barely registers in Nike's revenue. Africa, with the world's youngest population and rapidly urbanizing economies, represents decades of growth potential. As these markets develop, they tend to adopt Western brands as status symbols—and no Western athletic brand has more status than Nike.

The athletic participation megatrends are unstoppable. The global wellness industry has grown from $3.4 trillion in 2013 to $4.5 trillion in 2023. Athleisure has made athletic wear acceptable everywhere—offices, restaurants, even formal events. The pandemic accelerated home fitness adoption. Youth sports participation continues growing globally. Every trend points toward more people wearing more athletic apparel more often—and Nike owns 27% of this expanding market.

Bear Case: The Empire's Hidden Cracks

China dependency represents an existential risk that Nike cannot diversify away from. With roughly 20% of revenue from Greater China, Nike is essentially betting its growth on stable U.S.-China relations—a bet that looks increasingly precarious. The Xinjiang cotton controversy showed how quickly Chinese consumers can turn when nationalism is triggered. Local competitors like Li-Ning and Anta are improving quality while playing the patriotism card. If China decides to make Nike a symbol of Western imperialism, decades of market development could evaporate overnight.

Inventory challenges suggest deeper demand problems. Nike's inventory-to-sales ratio has increased 20% over the past three years. The company frames this as supply chain normalization, but the reality is more concerning: Nike is producing shoes that aren't selling at expected rates. The secondary market for limited releases has cooled—shoes that once resold for 5x retail now trade at 1.5x. When hype dies, what's left is $30 of materials selling for $150, and consumers are increasingly questioning that math.

Digital-native competitors are attacking Nike's cultural moat. Brands like Allbirds, On Running, and Hoka didn't exist 15 years ago but now capture mindshare among influential consumers. They don't need hundred-million-dollar athlete endorsements because they have authentic community engagement. They're doing to Nike what Nike did to Adidas—attacking from angles the incumbent doesn't recognize as threats until it's too late.

The wholesale relationship deterioration creates long-term strategic risk. By cutting out partners like Foot Locker, Nike gains margin but loses distribution and marketing leverage. Wholesale partners were Nike's ambassadors, curating products and educating consumers. Now Nike must do this itself, requiring massive capital investment in stores and digital infrastructure. If the DTC strategy stumbles, Nike will have destroyed relationships it took decades to build.

Fashion cycles are accelerating, and Nike looks increasingly corporate. The company that once defined cool now feels institutional. The Travis Scott collaborations and Off-White partnerships seem forced, like a parent trying to speak teenager. Gen Z consumers, raised on authenticity and skeptical of corporations, increasingly see Nike as The Man rather than rebellion against him. When Kanye West left Nike for Adidas, he said Nike treated him like a slave—hyperbolic but resonant with creators who see Nike as exploitative rather than collaborative.

Management transitions inject uncertainty at the worst time. John Donahoe, a tech executive running an apparel company, lacks the instinctive understanding of sports culture that defined Knight's leadership. The executive exodus—multiple senior leaders leaving for competitors—suggests internal turmoil. The company feels adrift, reactive rather than proactive, following trends rather than setting them.

The Verdict: Navigating the Paradox

Nike presents the classic large-cap dilemma: a dominant incumbent with massive advantages but limited growth potential facing nimble insurgents with inferior resources but superior innovation velocity. The bull case rests on Nike's brand moat proving impregnable—that cultural power accumulated over 50 years cannot be disrupted by DTC startups or Chinese nationalism. The bear case sees Nike as the next General Electric or IBM—a once-dominant company that confused temporary advantage with permanent moat.

The truth likely lies between extremes. Nike will probably remain the global athletic leader for the foreseeable future, but at lower margins and growth rates than the past decade. The brand is too powerful to collapse but too mature to explode. For investors, this suggests Nike is a wealth-preservation vehicle rather than a wealth-creation opportunity—appropriate for portfolios seeking ballast, dangerous for those seeking alpha.

The key variable is China. If Nike navigates the geopolitical minefield and maintains Chinese growth, the stock could appreciate 30-50% over five years. If China turns hostile, Nike could face its first revenue decline since the financial crisis. This binary outcome makes Nike essentially a leveraged bet on U.S.-China relations—a risk many investors don't fully appreciate.

XI. Epilogue & "If We Were CEOs"

Standing in Phil Knight's old office at Nike headquarters, you can still see the worn track from where he'd pace while thinking through problems. The office is preserved like a shrine—the same desk where he signed the Jordan deal, the same window overlooking the campus he built, the same quote from Prefontaine on the wall: "To give anything less than your best is to sacrifice the gift." The question facing Nike's next generation of leadership: what does "your best" mean when you're already the best?

If we were CEO, the first move would be radical: split Nike into two companies. Nike Performance would focus exclusively on serious athletes—the 10% who actually use athletic equipment for athletics. Nike Lifestyle would own fashion, culture, and the 90% who wear athletic apparel as identity. This isn't just organizational restructuring; it's philosophical clarity. The tension between performance and fashion has defined Nike for decades. Instead of managing this tension, weaponize it through competition between sibling brands.

The brand portfolio needs surgical precision, not scattershot acquisition. Converse proved that owning the anti-Nike is brilliant strategy. We'd acquire Outdoor Voices or similar brands that capture the wellness-over-performance segment Nike struggles to authenticate. We'd buy a European soccer brand—not for the products but for the credibility. We'd partner with gaming companies to create virtual shoes for the metaverse—absurd to boomers, essential to Gen Alpha. Each move would fill a specific gap in Nike's cultural portfolio.

Web3 and digital assets represent Nike's next frontier, but not in the way most imagine. The opportunity isn't selling NFT shoes for speculation—it's creating digital identity systems where your Nike achievements (runs completed, games won, communities joined) become portable social currency. Imagine if your Nike Run Club statistics unlocked exclusive products, experiences, or communities. The physical shoe becomes an entry point to a digital ecosystem where status is earned through participation, not just purchase.

Sustainability cannot be marketing; it must be strategy. We'd commit to carbon neutrality by 2030—not through offsets but through fundamental supply chain transformation. Every Nike product would have a visible sustainability score, like nutrition labels. We'd launch Nike Renewed as a premium line where returned shoes are disassembled and rebuilt into limited editions. Make sustainability cool, not preachy. The younger consumers Nike needs to capture don't want to be told to save the planet—they want to look good while doing it.

The retail experience needs complete reimagination. Nike stores should be temples to human potential, not shoe warehouses. Every store would have training facilities where customers work with coaches, biomechanical analysis that recommends products based on actual need, community spaces for run clubs and training groups. Shopping becomes training, purchase becomes membership, transaction becomes transformation.

On China, we'd execute a strategic hedge. Create a separate Chinese brand—managed by Chinese executives, designed for Chinese consumers, manufactured in China—that licenses Nike technology but operates independently. This provides optionality: if relations deteriorate, the Chinese brand can be spun off or sold without destroying Nike proper. If relations improve, Nike benefits from local expertise without seeming foreign.

The innovation strategy would shift from product to experience. Instead of marginally better cushioning, create entirely new categories of human performance. Partner with Peloton or acquire Mirror to own the home fitness experience. Develop AI coaches that provide personalized training through AirPods. Create Nike Clubs—physical spaces that combine fitness, retail, and social experiences. The goal: make Nike indispensable to daily life, not just special occasions.

Most radically, we'd embrace planned obsolescence in reverse. Launch Nike Forever—shoes guaranteed for life, repaired for free, upgraded regularly. Price them at $500, limit production, make them status symbols of sustainability. This seems insane until you realize it solves multiple problems: differentiation from cheap competitors, environmental credibility, and creation of a subscription-like relationship with consumers.

Knight's Long Shadow

The fundamental challenge facing any Nike CEO is escaping Phil Knight's gravitational pull. His philosophy—paranoid innovation, athlete obsession, marketing as mythology—built the empire. But what built the empire might not sustain it. Knight succeeded by breaking rules; his successors succeed by following his rules. This is the innovator's dilemma in human form.

If we were CEO, the ultimate goal would be making Nike more than a company—transforming it into infrastructure for human achievement. Every person who wants to improve physically would engage with Nike somehow—through products, apps, experiences, or communities. The Swoosh would represent not just victory but the attempt itself. Revenue would follow relevance.

The path forward requires acknowledging uncomfortable truths. Nike will never again grow like a startup. The moat around the core business remains strong but not impregnable. Chinese growth cannot be assumed. Digital natives won't automatically choose Nike. The brand that told everyone to Just Do It must now figure out what "it" means in a world where athletic achievement is just one form of performance among many.

Knight built Nike on a simple insight: athletes needed better shoes. The next chapter requires a different insight: humans need better reasons to move. Whether Nike provides those reasons will determine if the Swoosh remains on humanity's chest or becomes another logo in history's dustbin. The goddess of victory doesn't guarantee triumph—she merely rewards those who earn it.

XII. Recent News

The seismic shift at Nike headquarters came on September 19, 2024, when the board announced that John Donahoe would step down as CEO, to be replaced by Elliott Hill—a 32-year Nike veteran coming out of retirement to save the company he'd helped build. The Board of Directors announced that Elliott Hill will become President and Chief Executive Officer of NIKE, Inc., effective October 14, 2024. The move sent Nike shares soaring 8% in after-hours trading, a clear signal that investors saw this as more than a leadership change—it was a return to Nike's roots.

Under Donahoe's tenure, Nike grew annual sales from $39.1 billion in fiscal 2019 to $51.4 billion in fiscal 2024, but the headline numbers masked deeper problems. Full year revenues were $51.4 billion compared to $51.2 billion in the prior year, up 1 percent on a currency-neutral basis—essentially flat growth for a company that had historically delivered double-digit expansion. More troubling were the recent quarterly results showing accelerating decline.

The fiscal 2025 numbers painted an increasingly grim picture. First quarter revenues were $11.6 billion, down 10 percent on a reported basis compared to the prior year, with Nike Direct revenues down 13 percent—a stunning reversal for what was supposed to be the company's growth engine. The second quarter was even worse: Second quarter revenues were $12.4 billion, down 8 percent on a reported basis compared to the prior year and down 9 percent on a currency-neutral basis.

Hill's appointment represents a dramatic philosophical shift. Hill worked at Nike for 32 years before retiring in 2020, starting as a sales intern in 1988 and rising through the ranks to become president of consumer and marketplace. Unlike Donahoe, who came from the tech world with stints at eBay and ServiceNow, Hill bleeds Swoosh—he understands Nike's culture instinctively rather than intellectually.

The strategic missteps under Donahoe had become impossible to ignore. As Nike worked to cut off its wholesale partners, it paved the way for a slew of upstart competitors such as On Running and Hoka to take over that crucial shelf space and grab market share. Earlier this year, Donahoe acknowledged that Nike went too far in its efforts to move away from its wholesale partners. The direct-to-consumer strategy that looked brilliant during COVID had become an albatross as consumers returned to physical retail.

The restructuring efforts announced in December 2023 revealed the depth of Nike's challenges. In December, it also announced a broad restructuring plan to reduce costs by about $2 billion over the next three years. It later said it would shed 2% of its workforce, or more than 1,500 jobs. Nike said the plan will cost between $400 million and $450 million in pretax restructuring charges—a massive reorganization for a company that had rarely needed such drastic measures.

Geographic weakness compounded the problems. During the quarter, China sales came in at $1.86 billion, which fell short of the $1.95 billion analysts had expected. The China market, once Nike's most reliable growth driver, was stalling amid economic headwinds and resurgent local competition. European sales also disappointed, suggesting Nike's problems weren't regional but systemic.

Phil Knight's statement on the transition was telling. At the time, Nike co-founder Phil Knight said the company was standing by Donahoe's side and the executive had his "unwavering confidence and full support." But on Thursday, Knight said in a statement that he is excited to welcome Hill back to the team. "Leadership changes are never easy, they test you, they challenge you, but this transition has been handled with remarkable thoughtfulness and an unwavering commitment to Nike... His experience, understanding of Nike and leadership is exactly what's needed at this moment. We've got a lot of work to do but I'm looking forward to seeing Nike back on its pace".

The market's reaction suggests investors believe Hill can restore what Donahoe lost: Nike's connection to sport and culture. While Donahoe understood data and digital transformation, Hill understands sneakerheads and athletes. The question now is whether understanding the past is enough to navigate the future, or whether Nike needs something more radical than nostalgia to reclaim its crown.

XIII. Links & Resources

Essential Reading: - "Shoe Dog" by Phil Knight - The definitive memoir that reads like a thriller, detailing Nike's origin story through Knight's uniquely introspective lens - "Swoosh: The Unauthorized Story of Nike and the Men Who Played There" by J.B. Strasser and Laurie Becklund - The unvarnished account that Knight reportedly dislikes but insiders say captures the real chaos - "Just Do It: The Nike Spirit in the Corporate World" by Donald Katz - Written with Nike's cooperation, providing unprecedented access to the company's culture

Documentary & Film: - "Air" (2023) - Ben Affleck's dramatization of the Jordan signing, surprisingly accurate despite Hollywood treatment - "The Last Dance" (2020) - While focused on Jordan, episodes 5 and 6 provide crucial context for understanding the Nike-Jordan symbiosis - "Abstract: The Art of Design" Season 1, Episode 2 - Tinker Hatfield's design philosophy that shaped Nike's aesthetic

Academic & Industry Analysis: - Harvard Business School Case: "Nike, Inc.: Cost of Capital" (2001) - The classic valuation study - Stanford GSB Case: "Nike's Global Womens Fitness Business" - Examining Nike's struggle to authentically connect with female consumers - Morgan Stanley's "Sporting Goods Primer" (Updated Quarterly) - The definitive industry analysis for serious investors

Primary Sources & Investor Resources: - Nike Investor Relations (investors.nike.com) - Quarterly earnings, annual reports, and investor presentations - SEC EDGAR Database - All Nike filings including 10-Ks, 10-Qs, and proxy statements - Nike News (news.nike.com) - Official announcements, though heavily sanitized

Cultural & Historical Context: - Sneaker News (sneakernews.com) - The pulse of sneaker culture and resale market dynamics - Complex Sneakers - Where Nike's cultural relevance is actually determined - The Nike Archives at the University of Oregon - Knight's alma mater houses extensive historical materials