Netflix: The Story of How the Algorithm Ate Hollywood

I. Introduction & Episode Roadmap

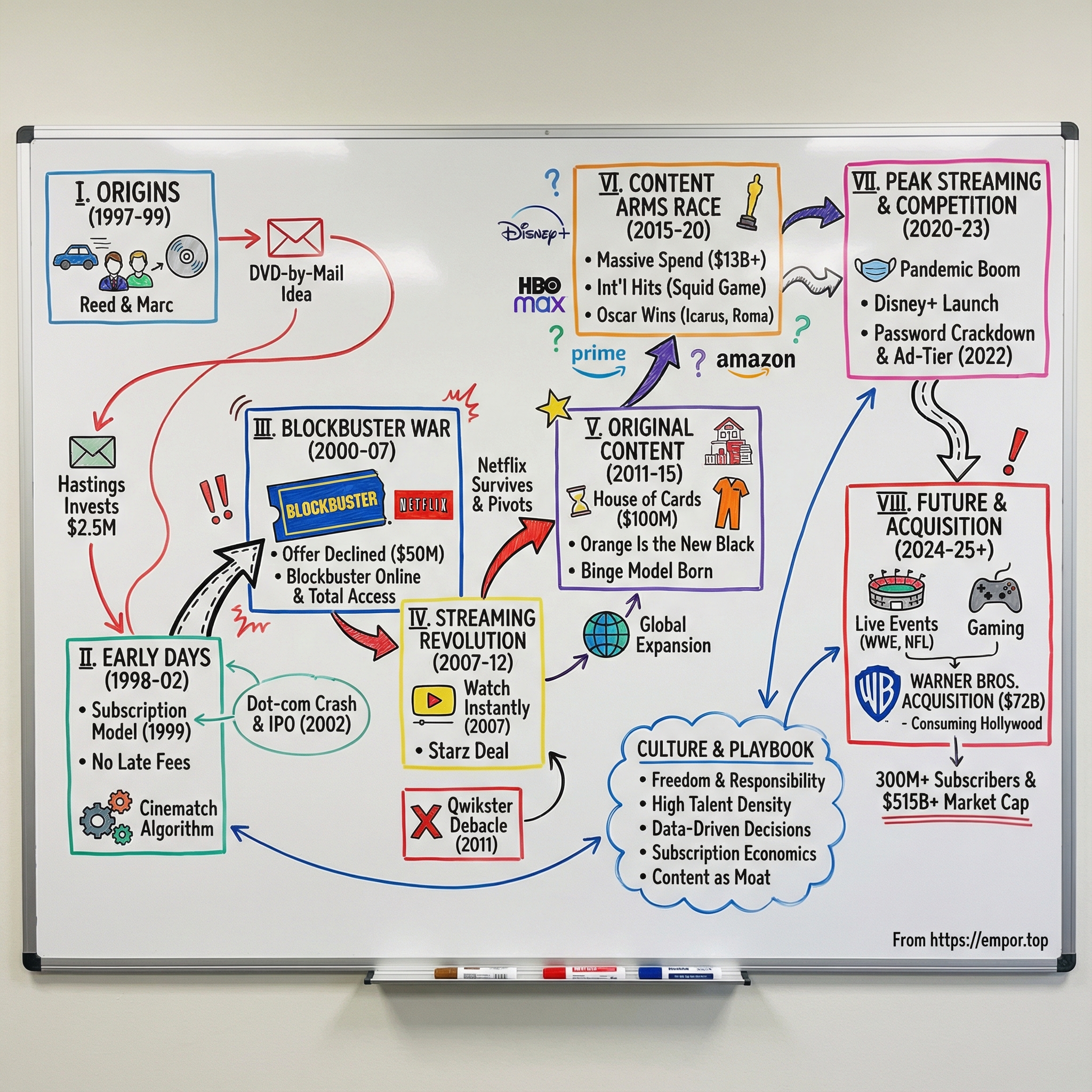

Picture this: It's 1997, and two tech executives are carpooling between Santa Cruz and Silicon Valley, tossing around startup ideas like tennis balls. One of them, Marc Randolph, is obsessed with the new DVD format—these shiny discs that could hold an entire movie and slip into a greeting card envelope. The other, Reed Hastings, has just pocketed millions from selling his software company and is itching for the next big thing. Neither could have imagined that their car-ride brainstorming would birth a company that would one day be worth more than Disney, Warner Bros, Paramount, and Comcast combined.Today, Netflix commands 301.6 million paid memberships across more than 190 countries. With a market cap hovering around $515.80 billion, the streaming giant's valuation surpasses those of Disney, Warner Bros. Discovery, Paramount Global, and Comcast combined—a stunning achievement for a company that started by mailing DVDs in red envelopes. And in a move that stunned Hollywood, Netflix recently agreed to acquire Warner Bros. for $72 billion, gaining some of the industry's most iconic properties including HBO and franchises from Harry Potter to DC Comics.

How did a DVD-by-mail startup become the company that redefined entertainment? The answer lies not just in technology or timing, but in a series of calculated risks, near-death experiences, and a relentless focus on what consumers wanted before they knew they wanted it. This is the story of how Netflix didn't just disrupt Hollywood—it consumed it, algorithm by algorithm, subscriber by subscriber, until the entire entertainment industry had no choice but to play by its rules.

Over the next several hours, we'll explore Netflix's journey from those carpooling conversations to its current dominance. We'll dissect the strategic pivots, the culture that made it possible, and the lessons for founders and investors watching the next wave of disruption unfold. Because while Netflix has won the streaming wars thus far, its acquisition of Warner Bros. signals that the company isn't just competing anymore—it's consuming Hollywood itself.

II. Origins: Reed Hastings, Marc Randolph, and the DVD Experiment (1997–1999)

The Netflix origin story begins not in Silicon Valley's gleaming offices, but in the distinctly unglamorous setting of a commuter car traversing Highway 17 between Santa Cruz and Silicon Valley. For four months in 1997, Reed Hastings and Marc Randolph carpooled together while waiting for their previous company's merger to finalize. These daily drives would become the incubator for one of the most transformative companies in entertainment history.

Reed Hastings' path to entrepreneurship was anything but conventional. Born in Boston to an attorney father who served in the Nixon administration and a mother from a Boston Brahmin family who taught her children to disdain high society, Hastings inherited both establishment credentials and an anti-establishment streak. After graduating from Bowdoin College, he joined the Marine Corps—an unusual choice for an Ivy League mathematics major. Following his military service, Hastings joined the Peace Corps, teaching math in Swaziland from 1983 to 1985. It was there, in rural Africa, that he discovered his gift for breaking down complex problems into simple, teachable concepts—a skill that would prove invaluable in Silicon Valley.

Returning to the States, Hastings enrolled at Stanford for a master's in computer science. In 1991, he founded Pure Software, a debugging tool company that would grow to 700 employees before merging with Atria Software in 1996 for $700 million. The combined entity, Pure Atria, was then acquired by Rational Software in 1997 for $900 million. But Hastings' experience at Pure taught him a painful lesson: rapid growth without cultural discipline leads to dysfunction. He later described Pure's culture as having become "a cesspool of infighting" as it scaled. This scar tissue would profoundly shape how he built Netflix.

Marc Randolph, Hastings' carpooling companion, was a serial entrepreneur with a marketer's instincts and a fascination with emerging technologies. During those Highway 17 commutes, Randolph pitched idea after idea—personalized baseball bats, customized dog food, you name it. But the concept that stuck involved the brand-new DVD format, introduced in the United States just months earlier in March 1997.

DVDs were revolutionary for their time: they could hold an entire movie on a disc the size of a CD, offered superior picture quality to VHS, never needed rewinding, and—crucially—were light enough to mail cheaply. Randolph wanted to replicate Amazon's e-commerce model (the company had IPO'd just months earlier in May 1997) but with entertainment instead of books. Hastings was intrigued but skeptical. Would DVDs survive mailing?

The answer came via a simple experiment that has since become Silicon Valley legend. Hastings and Randolph bought a CD (DVDs were still rare) and mailed it to Hastings' house in a greeting card envelope. When it arrived intact, Randolph later recalled, "If there was an aha moment, that was it." The physical properties of the medium—flat, light, durable—made it perfect for mail-order distribution. Hastings invested $2.5 million into Netflix from the sale of Pure Atria, which had been acquired by Rational Software in 1997 for $750 million. The financing structure was telling: Hastings secured a massive 68% equity stake as the primary investor, while Randolph, despite being co-founder, owned only about 30% since he didn't contribute capital. This imbalance would shape the company's future leadership dynamics. Netflix launched as the first DVD rental and sales website on April 14, 1998, with 30 employees and 925 titles available—nearly all DVDs published at the time. The early business model was simple: customers paid $4 per rental plus $2 for shipping. But this was 1998, the height of the dot-com boom, and everyone was trying to figure out how to make atoms-to-bits businesses work.

Randolph and Hastings met with Jeff Bezos, where Amazon offered to acquire Netflix for between $14 and $16 million. Fearing competition from Amazon, Randolph thought the offer was fair, but Hastings, who owned 70% of the company, turned it down on the plane ride home. It was a decision that would prove either genius or foolish—only time would tell.

III. Early Days: Building the Machine (1998–2002)

The late 1990s were a crucible for Netflix. Revenue grew explosively—$1 million in 1998, $5 million in 1999, then $35 million, $75 million, $150 million, reaching almost $300 million by 2002. But beneath these impressive numbers lay a scrappy operation fighting for survival.

In those first years, Netflix was less Silicon Valley unicorn and more guerrilla operation. Early employee Cindy Holland compared acquiring DVDs to "shoveling coal in the side door of the house." Executives routinely made runs to Walmart and Costco, buying DVDs at full retail price just to meet customer demand. The company's logistics were held together with duct tape and determination.

The breakthrough came in September 1999 when Netflix introduced its revolutionary subscription model. For $19.95 per month, customers got unlimited rentals with no due dates, no late fees, and a queue system that automatically sent the next DVD when the previous one was returned. By early 2000, Netflix dropped the per-rental option entirely, betting everything on subscriptions.

Three innovations made this model sing. First, the Queue allowed customers to create a wish list of movies, turning selection from a chore into entertainment. Second, the serialized delivery system meant DVDs arrived automatically—customers never had to remember to order. Third, and perhaps most importantly, Cinematch, Netflix's recommendation algorithm, learned what you liked and suggested what to watch next. In a pre-algorithmic world, this felt like magic.

The power dynamics within Netflix shifted dramatically in 1999. Randolph, recognizing his limitations as the company scaled, ceded the CEO position to Hastings and pivoted to head of product development. It was a rare display of ego-free leadership in Silicon Valley. Hastings brought operational discipline from his Pure Software days—but this time, he was determined not to repeat his cultural mistakes.

The dot-com crash of 2000 nearly killed Netflix before it could flourish. While Netflix experienced fast growth in early 2001, the continued effects of the dot-com bubble collapse and the September 11 attacks caused the company to hold off plans for its initial public offering (IPO) and to lay off one-third of its 120 employees. DVD players were a popular gift for holiday sales in late 2001, and demand for DVD subscription services were "growing like crazy", according to chief talent officer Patty McCord.

Against this backdrop of crisis and opportunity, Netflix made a fateful decision. In September 2000, with the company hemorrhaging cash and the market in freefall, Hastings and Randolph approached Blockbuster with an audacious proposal.

IV. The Blockbuster Wars: David vs. Goliath (2000–2007)

The scene was almost cinematic in its corporate awkwardness. In September 2000, during the dot-com bubble, while Netflix was suffering losses, Hastings and Randolph offered to sell the company to Blockbuster for $50 million. John Antioco, CEO of Blockbuster, thought the offer was a joke and declined, saying, "The dot-com hysteria is completely overblown."

Randolph later described the meeting in more painful detail: "The pitch was 'we would join forces, run the online business, they run the stores.' There was perfect silence, their words were 'we'll consider it' but you could tell they were fighting to suppress laughter. The meeting went downhill fast." Netflix executives left Dallas empty-handed, facing an uncertain future against a competitor with 9,000 stores and $6 billion in revenue.

But something extraordinary happened over the next eighteen months. The company went public on May 23, 2002, opening on NASDAQ at US$15.00 per share with a sale of 5.5 million shares of common stock. Netflix had survived the dot-com crash and found its footing. Meanwhile, Blockbuster, fat and happy with late fees that generated $800 million annually, barely noticed the red envelope upstart.

By 2004, Blockbuster finally woke up. They launched their own DVD-by-mail service, leveraging their massive store footprint for returns and exchanges. Then in 2007 came Total Access—a hybrid model that let customers rent DVDs online and exchange them in stores for free rentals. The service attracted 2 million online subscribers in its first year, but there was a fatal flaw: Blockbuster was losing $2 on every disc rented through the program.

The 2007 battle nearly broke Netflix. In one quarter, Netflix lost 55,000 subscribers while Blockbuster's online base continued growing. "Things got very scary for Netflix," Randolph admitted. "They were hurting us." The stock price plummeted. Wall Street smelled blood.

But then came one of the most consequential boardroom dramas in business history. Blockbuster CEO John Antioco, who finally understood the existential threat Netflix posed, wanted to continue investing in Total Access despite the losses. But activist investor Carl Icahn, who had taken a major position in Blockbuster, disagreed violently. The dispute came to a head over Antioco's bonus. In March 2007, Antioco stepped down, replaced by James Keyes, a retail executive from 7-Eleven who had little experience with digital transformation.

Keyes immediately reversed course, pulling funding from Total Access to refocus on brick-and-mortar stores. He believed Blockbuster's future lay in becoming a "convenience retailer" selling popcorn and soda alongside movie rentals. It was a catastrophic misreading of where the market was heading.

While Blockbuster retreated, Reed Hastings was preparing for the next phase of warfare. His goal had always been streaming—DVD-by-mail was merely a waystation. By the mid-2000s, broadband penetration had reached critical mass. YouTube, despite its grainy videos, was proving consumers would watch anything online if it was convenient enough.

V. The Streaming Revolution: From Atoms to Bits (2007–2012)

Hastings reportedly told colleagues in the late 1990s that his goal was always streaming media, and that Netflix rented DVDs only to grow its customer base for streaming. By the mid-2000s data speeds and bandwidth costs improved sufficiently to allow customers to download movies from the internet. The original idea was a "Netflix box" that could download movies overnight, and be ready to watch the next day. By 2005, Netflix had acquired movie rights and designed the box and service. But after witnessing how popular streaming services such as YouTube were despite the lack of high-definition content, the concept of using a hardware device was scrapped and replaced with a streaming concept. In January 2007, the company launched a streaming media service, introducing video on demand via the Internet. However, at that time it only had 1,000 films available for streaming, compared to 70,000 available on DVD.

The launch was deliberately quiet—no press releases, no fanfare. Netflix simply added a "Watch Instantly" tab to its website. Subscribers on the $17.99 plan got 18 hours of streaming per month. The selection was pitiful: old movies, obscure documentaries, content nobody particularly wanted. But Hastings knew something his competitors didn't: convenience beats quality until quality catches up.

The real breakthrough came in 2008 when Netflix struck a deal with Starz for roughly $30 million annually. Suddenly, Netflix could stream recent theatrical releases like "Ratatouille" and "Superbad." It was a steal—Starz executives had no idea they were handing Netflix the keys to Hollywood's future. Ted Sarandos, Netflix's content chief who joined in 2000, knew this was just the beginning. He saw Starz as a stopgap measure, understanding that studios wouldn't always share their crown jewels. Looking at HBO's model, he saw no reason Netflix couldn't produce its own watercooler shows.

The path to streaming dominance wasn't smooth. In 2011, Netflix committed one of the greatest unforced errors in corporate history: Qwikster. Hastings announced that Netflix would split into two companies—Netflix for streaming, Qwikster for DVDs. Prices would increase 60% for customers who wanted both. The backlash was immediate and brutal. Netflix lost 800,000 subscribers in a single quarter. The stock cratered from $298 to $53.

Hastings' response was remarkable for a Silicon Valley CEO: he admitted complete failure. In a blog post titled "An Explanation and Some Reflections," he wrote: "I messed up. I owe everyone an explanation." He killed Qwikster before it launched, kept the services together, and learned a crucial lesson about customer psychology: never make people feel like they're losing something they already have.

What seemed like disaster was actually liberation. The Qwikster debacle forced Netflix to commit fully to streaming. With the stock in the toilet and nothing left to lose, Hastings made the boldest bet of his career: Netflix would become a content studio.

VI. Original Content: The House of Cards Gambit (2011–2015)

The meeting in 2011 was unlike anything Hollywood had seen. Netflix executives sat across from the biggest names in television—David Fincher, Kevin Spacey, the team behind a proposed American adaptation of the British political thriller "House of Cards." Other networks wanted pilot episodes, focus groups, executive notes. Netflix made a different offer: $100 million for two guaranteed seasons, 26 episodes, no pilot needed, complete creative control.

Netflix outbid several major cable networks including HBO and AMC for House of Cards. The traditional players were stunned. Who greenlights two seasons without seeing a single episode? But Netflix had something the others didn't: data. They knew their subscribers loved Fincher's films, political thrillers, and Kevin Spacey. The algorithm had already focus-grouped the show.

House of Cards debuted February 1, 2013. It earned rave reviews, attracted waves of new subscribers, and showed Netflix could produce glossy, highbrow TV that made HBO famous. But the real innovation wasn't the quality—it was the delivery. Netflix released all 13 episodes at once, inventing the binge-watch. Traditional TV executives called it insane. Viewers called it addictive.

Ted Sarandos had perfectly articulated the strategy: "Part of our goal is to become like HBO faster than HBO can become Netflix." HBO had prestige but required cable subscriptions and appointment viewing. Netflix had convenience, data, and now, quality content. The race was on.

House of Cards received nine nominations for the 65th Primetime Emmy Awards in 2013, becoming the first original online-only streaming television series to receive major nominations. The significance couldn't be overstated—the Television Academy had just legitimized streaming as equal to traditional broadcasting.

Six months later came "Orange Is the New Black," which premiered in July 2013. Where House of Cards targeted prestige drama fans, Orange went for a different audience—younger, more diverse, hungrier for representation. Netflix stated it had been their most-watched original series so far, with viewership comparable to successful cable and broadcast TV.

The one-two punch of House of Cards and Orange Is the New Black triggered a gold rush. Over the ensuing years, filmmakers and showrunners flocked to Netflix, lured by creative freedom and vast sums of money. "Stranger Things" became a global phenomenon. "The Crown" gave Netflix British prestige. "Narcos" proved they could produce in any language for any market.

By 2015, Netflix's strategy was clear: become the first truly global television network. Not through satellites or cable boxes, but through the internet. Every TV show, every movie, available everywhere, all the time, perfectly personalized for each viewer. Traditional studios, still protecting regional distribution windows and cable relationships, couldn't match this vision even if they wanted to.

VII. The Content Arms Race: Scaling the Mountain (2015–2020)

The numbers were staggering and borderline insane. Netflix produced 240 new original shows and movies in 2018, which climbed to 371 in 2019. The content budget ballooned—$13.6 billion in 2021 with projections of $18.9 billion by 2025. By August 2022, original productions comprised 50% of Netflix's overall library in the United States.

This wasn't just spending; it was strategic carpet bombing. Netflix needed content for every taste, every demographic, every mood, in every country. A Korean series here ("Kingdom"), a Spanish heist drama there ("La Casa de Papel"), a Bollywood spectacular over there ("Sacred Games"). The algorithm would sort out who watched what.

The international expansion strategy was brilliant in its simplicity: enter a market, license local content, study what works, then produce original local content that could travel globally. "Squid Game," a South Korean series that cost $21 million to produce, generated nearly $900 million in value for Netflix. No Hollywood studio saw that coming.

But scaling this mountain required more than money—it demanded technological innovation. Netflix built one of the world's most sophisticated content delivery networks, with servers positioned strategically worldwide to minimize buffering. The recommendation algorithm became so advanced it essentially created a unique version of Netflix for each of its hundreds of millions of users.

Competition was heating up. Amazon Prime Video, launched in 2006, was gaining ground with hits like "The Marvelous Mrs. Maisel." Hulu, jointly owned by Disney, Fox, and Comcast, offered next-day TV content Netflix couldn't match. But the real threat was still organizing in corporate boardrooms.

In 2018, a seemingly small achievement carried massive symbolic weight: "Icarus" became the first Netflix production to win an Oscar for Best Documentary Feature. The following year, "Roma" won three Academy Awards including Best Director for Alfonso Cuarón. Netflix had conquered television; now it was coming for cinema.

Traditional Hollywood finally understood the threat. Bob Iger, Disney's visionary CEO, revealed plans for a Netflix competitor in 2017, calling it "extremely important, a very significant strategic shift." Disney would pull all its content from Netflix and launch Disney+ in late 2019. The streaming wars were about to begin in earnest.

VIII. Peak Streaming: The Pandemic & Competition (2020–2023)

When COVID-19 locked down the world in March 2020, Netflix was perfectly positioned to benefit. With movie theaters closed and production halted globally, Netflix's library of finished content became entertainment's lifeline. The company added 36 million subscribers in 2020 alone—nearly as many as it had added in the previous three years combined.

But the pandemic accelerated competitive dynamics too. Disney+ launched in November 2019 with an aggressively low price point and the most valuable content library in entertainment—Marvel, Star Wars, Pixar, and a century of family entertainment. It reached 100 million subscribers in just 16 months, a milestone that took Netflix a decade to achieve. During quarantine, when 58% of internet users watched more paid video, every media company suddenly wanted in.

The land grab was unprecedented. HBO Max, Peacock, Paramount+, Apple TV+—every studio rushed to launch their own streaming service, pulling content from Netflix to stock their own shelves. The industry joke was that there were more streaming services than shows worth watching. Netflix, once the disruptor, was now the incumbent being disrupted.

Netflix's response was quintessentially Hastings: double down on what differentiated them. They promised to release a new original movie every week of 2021. They expanded into gaming, interactive content, and live events. Most controversially, they cracked down on password sharing—a practice they had previously tolerated as a form of marketing.

The password-sharing crackdown was a masterclass in strategic timing. Netflix waited until they had sufficient market power and content differentiation to weather the backlash. They rolled it out gradually, country by country, learning and adjusting. Despite predictions of mass cancellations, it worked—Netflix added millions of subscribers who had previously been freeloading.

In November 2022, facing slowing growth and increased competition, Netflix did something Hastings had sworn they'd never do: launched an ad-supported tier. At $6.99 per month, it was Netflix's acknowledgment that the premium-only strategy had hit its ceiling. The purists were horrified. The stock market loved it.

Leadership was evolving too. In July 2020, Netflix appointed Ted Sarandos as co-CEO alongside Hastings. Then in January 2023, Greg Peters and Ted Sarandos were named co-CEOs with Hastings assuming the role of executive chairman. After 25 years, Hastings was stepping back from day-to-day operations, though his influence remained paramount.

Despite the competition, Netflix maintained its crown. While Disney+ grabbed headlines and Apple TV+ won Oscars, Netflix kept adding subscribers and generating cash. The entertainment world had resigned itself to a new reality: everyone was chasing Netflix, and Netflix remained far ahead. Disney even stopped publicly reporting subscription numbers, following Netflix's playbook yet again.

IX. Culture & Management Innovation

The Netflix Culture Deck might be the most influential corporate document ever created. First published internally in 2009, it's been viewed over 20 million times and Sheryl Sandberg called it "the most important document ever to come out of the Valley." But it wasn't really a manual—it was a manifesto.

"Freedom and Responsibility" wasn't just a slogan; it was an operating system. No vacation policy—take what you need. No expense policy—"act in Netflix's best interest." No approval processes for decisions. But with radical freedom came radical accountability. Netflix reportedly offers mediocre employees large severance packages to ensure that employees are consistently working to further the company's innovative environment.

The most controversial principle: "adequate performance gets generous severance." Netflix operated like a professional sports team, not a family. They hired fully-formed adults, paid top-of-market compensation, and expected exceptional performance. Those who delivered stayed; those who didn't left with dignity and a check.

This culture wasn't accidental—it was precisely engineered from Hastings' Pure Software trauma. Where Pure had become a "cesspool of infighting" as it scaled, Netflix would maintain a high talent density at any cost. The solution wasn't more process but better people. Not more rules but more context.

The "Keeper Test" became legendary: managers were asked, "If this person told you they were leaving for another company, would you fight hard to keep them?" If the answer was no, that person should receive a generous severance immediately. As one observer noted, Netflix's culture meant that if an employee wasn't worth fighting to keep, out they went. Brutal? Perhaps. Effective? Undeniably.

Radical transparency meant sharing information most companies kept secret. Financial data, strategic plans, even board meeting presentations were available to all employees. The logic: if you hire smart people and give them context, they make smart decisions. If you treat employees like children, they act like children.

Hastings created an internal culture guide for Netflix by meeting with employees to discuss the company's culture. But this wasn't corporate propaganda—it was a living document, constantly evolving based on what worked and what didn't. When something failed, they discussed it openly, learned from it, and updated the culture accordingly.

The decision-making framework was elegantly simple: push decisions down to the lowest competent level. Don't seek consensus; seek the best answer. Disagree openly, then commit fully. "Farming for dissent" became a crucial leadership skill—actively soliciting disagreement to avoid groupthink.

In 2020, Hastings released "No Rules Rules: Netflix and the Culture of Reinvention," co-authored with business professor Erin Meyer. The book revealed even more radical practices: the "360 reviews" where anyone could give feedback to anyone, including the CEO; the "sunshining" of mistakes where errors were discussed openly without blame; the compensation philosophy of paying top-of-personal-market for each individual.

Critics called Netflix's culture harsh, Darwinian, unsuitable for most companies. They were probably right. But Hastings never claimed it was for everyone—just that it was optimal for a company trying to reinvent entertainment while moving at internet speed.

X. Playbook: Business & Investing Lessons

The numbers tell a staggering story of value creation. Since its IPO in 2002 at $15 per share, Netflix has delivered a 33,668% return—turning every $1,000 invested into $337,680. But the real lessons aren't in the returns; they're in the strategy that generated them.

The Power of Subscription Economics

Netflix transformed entertainment from a transactional to a relational business. Instead of fighting for each purchase decision, they secured permission to bill monthly. This predictable revenue allowed massive content investments that transaction-based competitors couldn't match. The lifetime value of a subscriber dwarfed the cost of acquisition, creating a flywheel that accelerated with scale.

Content as Moat

The evolution was counterintuitive: Netflix started with no content, licensed everything, then became one of the world's largest content producers. The lesson: when your suppliers become competitors, become your own supplier. A large contributor to returns has been original content production and adoption of the "studio cash flow model"—producing content that lives forever on the platform, appreciating rather than depreciating over time.

Platform Dynamics Without Network Effects

Unlike social networks, Netflix doesn't get stronger as more users join—your experience doesn't improve if your neighbor subscribes. Instead, Netflix created "data network effects": more users mean better recommendation data, which means better content decisions, which attracts more users. It's a subtler but equally powerful dynamic.

International as Destiny, Not Option

Most US companies treat international expansion as opportunistic. Netflix treated it as existential. They understood that content travels better than ever, that local productions can find global audiences, and that the US represents only 5% of the world's population. This wasn't expansion; it was completion.

Technology Leverage

Netflix looks like a media company but operates like a technology company. They automated everything automatable: recommendations, streaming quality, even content production decisions. This allowed them to scale to 300 million subscribers with only 13,000 employees—a ratio traditional media companies can't comprehend.

When to Burn Cash

Netflix burned cash for years, reaching negative $3 billion in free cash flow in 2019. But this wasn't reckless spending—it was strategic investment during a land-grab period. They understood that content was a fixed cost that could be amortized across an expanding subscriber base. Once they reached scale, the cash generation machine kicked in.

Disruption Patterns

Netflix followed the classic disruption playbook: start with an inferior product (limited DVD selection) for an overlooked market (people who hated late fees), then improve rapidly while incumbents ignore you, finally attacking the core market with a superior solution. Blockbuster never saw it coming because Netflix started by serving customers Blockbuster didn't want.

XI. Analysis & Bear vs. Bull Case

Standing in August 2025, Netflix looks simultaneously invincible and vulnerable. With 301.63 million subscribers globally and a market cap exceeding $515 billion, they've won the streaming wars' first phase. But wars have multiple phases.

Bull Case: The Scaled Incumbent

Netflix's advantages compound with scale. They can spend $18.9 billion on content because they can amortize it across 300 million subscribers. No competitor matches this math. The recommendation algorithm has a decade's head start and billions of data points. The brand has become synonymous with streaming—it's the default choice, the safe choice, the checkbox every household checks.

International expansion still has runway. Despite presence in 190 countries, penetration remains low in massive markets like India and Southeast Asia. As internet infrastructure improves and smartphone adoption increases, Netflix's addressable market expands by hundreds of millions.

The advertising tier changes the equation. In Q3 2024, the ads plan accounted for over 50% of sign-ups in ads countries and membership grew 35% quarter over quarter. Netflix is on track to reach critical ad subscriber scale for advertisers in all ads countries in 2025. This isn't just incremental revenue—it's a new business model that could eventually rival subscription revenue.

Gaming and live events offer optionality. While nascent, these initiatives leverage existing infrastructure and relationships. If Netflix can crack interactive entertainment, they add another growth vector without adding another cost structure.

Bear Case: The Maturing Giant

Growth is decelerating. Adding the next 100 million subscribers will be harder than the last 100 million. The easy markets are saturated; the remaining markets have lower income, requiring lower prices. The math gets harder.

Content costs keep inflating. Every studio now competes for the same talent, driving prices skyward. Netflix must feed the content beast constantly—any slowdown risks subscriber defection. The $18.9 billion content budget might not be a competitive advantage but a competitive requirement.

Competition is no longer sleeping. Disney reorganized around streaming. Apple has infinite capital. Amazon has Prime bundling. YouTube has free ad-supported content. The exclusive content that drove subscriptions is now scattered across a dozen services.

Password-sharing crackdown has limits. Netflix extracted value from freeloaders, but that's a one-time gain. They've pulled forward future growth, potentially creating harder comparisons ahead.

Technology disruption looms. AI-generated content could democratize production. Virtual reality could change consumption patterns. The next platform shift might not favor Netflix's model.

Market saturation is real. In mature markets like the US and Canada, Netflix has penetrated most households willing to pay. Price increases become the primary growth driver, but elasticity has limits.

XII. Epilogue & "If We Were CEOs"

The future of Netflix isn't being written in Los Angeles or Silicon Valley—it's being written in boxing rings and football stadiums. Netflix's November 2024 Jake Paul vs. Mike Tyson fight and Christmas Day NFL games represent more than diversification; they're acknowledgments that appointment viewing still matters, that shared cultural moments still drive value.

Netflix is becoming the new home for WWE Raw starting January 6, 2025—a weekly live show that transforms Netflix from an on-demand library into a destination for live entertainment. This isn't just adding content; it's adding urgency, community, conversation—elements the algorithm can't manufacture.

Netflix's gaming strategy is focusing on narrative games based on Netflix IP and party and couch co-op games delivered from the cloud to TV. "We think of this as a successor to family board game night," says co-CEO Greg Peters. The vision is compelling: Netflix becomes not just what you watch but what you do.

If we were running Netflix, the strategic priorities would be clear but contrarian:

Embrace Bundling's Return. The streaming wars' dirty secret is that unbundling has failed consumers—too many services, too much complexity, too much cost. Netflix should lead re-bundling efforts, partnering rather than competing where it makes sense. Better to give up margin than lose relevance.

Develop True Franchises. Netflix creates hits but rarely franchises. Where's their Marvel? Their Star Wars? They need intellectual property that transcends the platform, that creates cultural staying power beyond the next binge.

Monetize the Algorithm. Netflix's recommendation engine is arguably the world's best at predicting entertainment preferences. This capability has value beyond Netflix—for theaters, game publishers, music platforms. License it carefully.

Go Deeper, Not Wider. Instead of making content for everyone everywhere, dominate specific verticals completely. Own comedy. Own true crime. Own anime. Depth creates defensibility that breadth cannot.

Solve Discovery Paradox. Netflix has so much content that finding something to watch has become work. The interface needs radical reimagination—perhaps AI-powered, perhaps social, perhaps something entirely new.

The biggest surprise in Netflix's journey isn't that they disrupted Hollywood—disruption was inevitable once distribution went digital. The surprise is how they've maintained leadership despite every major media company gunning for them—and now, with the Warner Bros. acquisition, Netflix isn't just disrupting Hollywood anymore but buying it outright. They've proven that execution beats strategy, that culture beats process, that speed beats perfection.

For founders, Netflix teaches that timing matters but persistence matters more. Hastings pursued streaming for a decade before technology caught up. For investors, it demonstrates that dominant platforms create winner-take-most dynamics even without traditional network effects. The moats are different but no less deep.

The ultimate lesson might be the simplest: Netflix won by giving customers what they wanted before they knew they wanted it. No late fees became unlimited streaming became binge-watching became personalized entertainment. Each evolution seemed obvious in retrospect, revolutionary in the moment.

XIII. Recent News**

Latest Quarterly Earnings (Q4 2024)** Netflix delivered blockbuster Q4 2024 results, with earnings per share of $4.27 versus $4.20 expected and revenue of $10.25 billion versus $10.11 billion expected according to LSEG. The company surpassed 300 million paid memberships during the quarter, adding a record 19 million subscribers, driven by its content slate, improved product and typical fourth-quarter seasonality.

For the full year 2024, revenue grew 16% and operating margin expanded six points to 27%, with operating income exceeding $10 billion for the first time in Netflix's history.

New Content Announcements Looking ahead to 2025, Netflix has the return of "Stranger Things" and "Wednesday," two of its biggest hits. Additionally, the streamer will release a collection of new films from top directors including Daniel Craig and Rian Johnson's third "Knives Out" film, a Russo Brothers project called "The Electric State" starring Millie Bobby Brown, "Happy Gilmore 2" with Adam Sandler and a new take on "Frankenstein" from Guillermo del Toro.

Warner Bros. Acquisition In a landmark deal that stunned Hollywood, Netflix agreed to acquire Warner Bros. for $72 billion after the entertainment company splits its studios and HBO Max streaming business from its cable networks. The deal gives Netflix a massive vault of TV and movie franchises—from Harry Potter to DC Comics—plus the iconic Warner Bros. lot in Burbank. Netflix beat rival bidders Paramount and Comcast, with the winning bid coming together at breakneck pace after Paramount's aggressive unsolicited approaches prompted Warner Discovery to put itself up for sale. Netflix has said it would continue Warner Bros. operations, including selling shows to other networks and releasing Warner films in theaters. The companies expect the regulatory review process to take at least a year, and a senior Trump administration official indicated that advisers are concerned about the deal.

Strategic Partnerships & Live Events Q4 2024's live events outperformed expectations: Squid Game season 2 is on track to become one of Netflix's most watched original series seasons, Carry-On joined the all-time Top 10 films list, the Jake Paul vs. Mike Tyson fight became the most-streamed sporting event ever and on Christmas Day Netflix delivered the two most-streamed NFL games in history.

Competitive Developments Netflix's cheaper, ad-supported tiers accounted for more than 55% of sign-ups in countries where the option is offered. Netflix also noted that memberships on its ad-supported plans grew around 30% quarter over quarter. The company stated it's on track to reach sufficient scale for ads members in all of its ads countries in 2025, with a top priority being to improve its offering for advertisers to substantially grow advertising revenue.

For 2025, Netflix now forecasts revenue of $43.5-$44.5 billion (up $0.5 billion versus prior forecast, despite the strengthening of the US dollar) and an operating margin of 29%, up one point from its prior forecast.

XIV. Links & References

Essential Long-Form Reading - "That Will Never Work" by Marc Randolph (2019) - The co-founder's insider account of Netflix's early days - "No Rules Rules" by Reed Hastings and Erin Meyer (2020) - Deep dive into Netflix's radical culture - "Netflixed" by Gina Keating (2012) - The definitive account of the Netflix-Blockbuster war - "The Netflix Effect" edited by Kevin McDonald and Daniel Smith-Rowsey (2016) - Academic analysis of Netflix's impact on media

Key Interviews & Profiles - Reed Hastings Stanford Graduate School of Business interview (2014) - Strategic thinking revealed - Ted Sarandos New Yorker profile (2021) - Inside the content strategy - Marc Randolph "How I Built This" podcast (2017) - Origin story from the co-founder

Industry Reports & Analysis - Matthew Ball's "The Netflix Manifesto" series - Strategic analysis of Netflix's evolution - Ben Thompson's Stratechery analyses on Netflix - Business model deep dives - MoffettNathanson streaming reports - Financial analysis and industry context - Ampere Analysis streaming market reports - Global competitive dynamics

Academic Studies - "The Netflix Recommender System: Algorithms, Business Value, and Innovation" (ACM, 2015) - "Streaming, Sharing, Stealing: Big Data and the Future of Entertainment" by Michael D. Smith and Rahul Telang (MIT Press, 2016) - "Platform Revolution" by Parker, Van Alstyne, and Choudary - Netflix as platform case study

The Netflix story continues to be written daily, with each earnings call, content launch, and strategic pivot adding new chapters to one of business history's most remarkable transformations. From DVD mailer to global entertainment platform, from startup to $500 billion giant, and now to owner of Hollywood's crown jewels, Netflix didn't just adapt to the future—it invented it, one algorithm-powered recommendation at a time. As co-CEO Ted Sarandos said upon announcing the Warner Bros. deal: "We can't stand still, we need to keep innovating and investing in stories that matter most to audiences."

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube