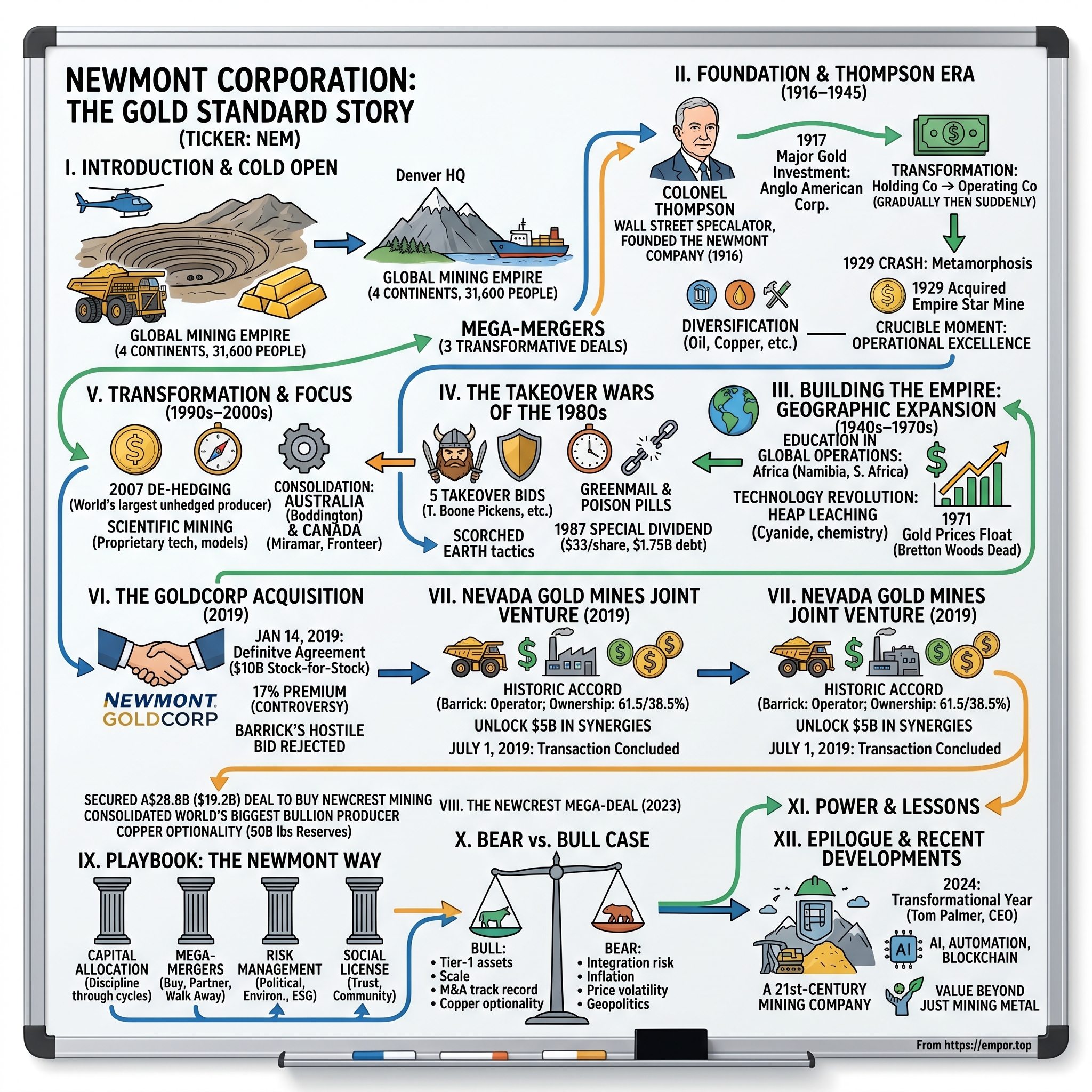

Newmont Corporation: The Gold Standard Story

I. Introduction & Cold Open

The helicopter descends through morning mist over the Carlin Trend in Nevada, revealing an otherworldly landscape of terraced earth that looks more like an ancient amphitheater than a mine. Below, massive haul trucks—each worth $5 million and carrying 400 tons of ore—crawl like beetles along spiraling roads carved into the earth. This is the heart of the world's most prolific gold mining district, where invisible gold particles, measured in parts per billion, hide within ordinary-looking rock. Welcome to the empire of Newmont Corporation, where modern alchemy transforms stone into the ultimate store of value.

In the boardrooms of Denver, far from these dusty pits, executives oversee an operation that spans four continents, employs 31,600 people, and produces roughly 6 million ounces of gold annually—enough to mint 120 million American Eagle coins or forge 1,500 standard gold bars every single day. This is Newmont, the only gold mining company in the S&P 500, a $40+ billion colossus that has survived world wars, hostile takeovers, commodity supercycles, and emerged as the undisputed king of gold mining through three transformative mega-mergers.

But here's what's remarkable: Newmont didn't start as a mining company at all. When Colonel William Boyce Thompson founded it in 1916, he created a financial holding company—a vehicle for speculation and investment, not operation. The name itself tells the story: "Newmont" is a portmanteau of "New York" and "Montana," bridging Wall Street sophistication with Western frontier ambition. Thompson, a Montana mining magnate who'd made his fortune in copper, envisioned something different—a company that would use financial engineering to unlock value in global mineral resources.

The question that drives our story today is deceptively simple yet profoundly complex: How did a financial holding company, founded by a Wall Street speculator, transform itself into the world's premier gold mining operator through a century of calculated risks, hostile battles, and ultimately, three industry-defining mergers that each reset the competitive landscape?

This isn't just a story about digging holes in the ground. It's about financial engineering meeting geological expertise, about surviving five hostile takeover attempts in a single decade, about turning bitter rivals into partners, and about building an empire that spans from the Nevada desert to the Australian outback, from Ghana's tropical forests to Peru's Andean peaks. It's about understanding when to fight, when to merge, and when to completely reimagine what cooperation looks like in a cutthroat industry.

Over the next several hours, we'll journey from Thompson's original vision through the takeover wars of the 1980s—where Newmont deployed poison pills and scorched earth tactics to fend off corporate raiders like T. Boone Pickens. We'll examine how the company shed everything except gold to become a pure-play bet on humanity's oldest store of value. We'll dissect three transformative deals: the $10 billion Goldcorp acquisition that created controversy and opportunity in equal measure, the revolutionary Nevada joint venture with arch-rival Barrick that unlocked $5 billion in value, and the recent $19 billion Newcrest acquisition that cemented Newmont's position as the undisputed industry leader.

Think of Newmont as the Microsoft of mining—not necessarily the most innovative or aggressive, but the most disciplined, the most systematic, and ultimately, the most successful at turning M&A into sustainable competitive advantage. While others chased growth at any cost or bet everything on single assets, Newmont played a longer game, building a portfolio of tier-one assets that generate cash through the entire commodity cycle.

The roadmap ahead takes us from Wall Street to mine shafts, from hostile takeovers to joint ventures, from financial engineering to operational excellence. We'll explore how a company founded in the Gilded Age adapted to the ESG age, how it manages political risk across multiple jurisdictions, and what its story teaches us about building enduring value in the most cyclical of industries. Because understanding Newmont isn't just about understanding gold—it's about understanding how great companies navigate uncertainty, transform industries, and create value across generations.

II. Foundation & The Thompson Era (1916–1945)

Picture New York City in 1916: the Great War rages in Europe, sending commodity prices soaring. Wall Street buzzes with speculation as American industry feeds the Allied war machine. Into this fevered atmosphere steps Colonel William Boyce Thompson—copper magnate, financial speculator, and visionary who sees opportunity where others see only chaos. On May 2, 1916, Thompson establishes The Newmont Company at 14 Wall Street, just steps from the New York Stock Exchange. But this isn't another mining venture—it's something far more ambitious.

Thompson wasn't your typical mining entrepreneur. Born in Virginia City, Montana, in 1869—literally in a mining camp during the territory's gold rush—he'd studied at the Columbia School of Mines before making his fortune in copper. By 1916, at age 47, he'd already built and sold multiple mining ventures, served as a director of the Federal Reserve Bank of New York, and would soon head the American Red Cross mission to revolutionary Russia. He understood both the operational complexities of mining and the financial leverage of Wall Street. His vision for Newmont reflected this duality: a holding company that would apply sophisticated financial analysis to global mineral opportunities.

The original Newmont Company was incorporated with $8 million in capital—substantial money in 1916, equivalent to roughly $220 million today. But Thompson wasn't interested in just buying stocks. He wanted control, influence, and the ability to reshape entire mining districts. The company's early portfolio reflected this ambition: oil interests in Texas, copper properties in Arizona, and most significantly, global mining investments that spanned continents. The year 1917 marked a pivotal moment. Newmont made its first major gold investment, acquiring a founding 25 percent stake in the Anglo American Corporation of South Africa. This wasn't just any investment—Anglo American had just been founded that same year by Ernest Oppenheimer with backing from J.P. Morgan & Co., making Newmont a founding investor in what would become one of the world's mining giants. Thompson's ability to identify and partner with emerging winners would define Newmont's strategy for decades.

The transformation from holding company to operating company happened gradually, then suddenly. In 1921, the Newmont Company reincorporated as Newmont Corporation, signaling a shift from pure investment to active management. But the real metamorphosis came with the 1929 stock market crash—a disaster that paradoxically launched Newmont's operational future.

In 1929, Newmont became a mining company with its first gold product by acquiring California's Empire Star Mine. The timing seems counterintuitive—buying an operating mine just as the global economy collapsed. But Thompson and his team understood something fundamental: when paper assets evaporate, hard assets endure. As banks failed and stocks became worthless, gold's value soared. The U.S. government would soon revalue gold from $20.67 to $35 per ounce in 1934, a 69% increase that transformed the economics of gold mining overnight.

The Empire Star Mine acquisition wasn't just about owning a hole in the ground. It represented a philosophical shift—from financial engineering to operational excellence, from trading mining stocks to actually mining. The company had to learn entirely new competencies: geology, metallurgy, labor management, environmental considerations (primitive as they were in 1929). This was Newmont's crucible moment, where Wall Street sophistication met Western frontier reality.

By the mid-1930s, Newmont had become a gold mining machine. The company's exploration geologists, led by Fred Searls—who would later become president—scoured the American West for opportunities. They weren't looking for get-rich-quick schemes but for deposits that could be mined profitably over decades. By 1939, Newmont was operating 12 gold mines in North America, a remarkable expansion in just one decade.

The operational philosophy that emerged during this period would define Newmont for generations: diversification across multiple mines to reduce risk, investment in geological expertise to find new deposits, and patient capital allocation that prioritized long-term value over short-term gains. While other companies chased the latest hot prospect, Newmont built a portfolio.

Thompson's health began declining in the late 1920s, and he died in 1930, just as his vision of Newmont as an operating company was taking shape. But the foundation he laid—the combination of financial sophistication and operational discipline—would carry the company through the Depression, World War II, and beyond. His successor team, including Searls and others who'd learned at Thompson's side, understood that in mining, as in investing, the real money isn't made in the boom times but in having the discipline and capital to buy when others are selling.

Beginning in 1925, Newmont had also acquired interests in a Texas oil field, demonstrating early on that the company wouldn't be a one-commodity player. This diversification strategy—gold as the core, but with strategic positions in oil, copper, and other commodities—would become a defining characteristic of Newmont's approach to risk management.

The World War II years tested this model. Gold mining was declared non-essential to the war effort, and many mines were forced to close as workers were drafted or moved to copper and lead production. But Newmont's diversified portfolio and strong balance sheet allowed it to survive where pure-play gold miners failed. The company emerged from the war with its operations intact and capital ready to deploy in what would become one of the greatest expansion periods in mining history.

III. Building the Empire: Geographic Expansion (1940s–1970s)

The DC-3 touches down on a dirt airstrip in South West Africa (modern-day Namibia) in 1946. Newmont executives step out into the blazing sun to inspect what locals call the "green hill"—Tsumeb, a geological miracle where copper, lead, zinc, silver, and germanium all converge in concentrations that defy belief. The mine had been worked since 1905, but post-war chaos created an opportunity. Newmont would spend the next four decades extracting wealth from this African treasure, learning hard lessons about operating in complex political environments that would prove invaluable decades later.

For decades around the middle of the 20th century, Newmont had a controlling interest in the Tsumeb mine in Namibia and in the O'Okiep Copper Company in Namaqualand, South Africa. These weren't just international investments—they were Newmont's education in global operations. In Nevada, you dealt with the Bureau of Land Management. In Namibia, you navigated apartheid politics, international sanctions, and eventually, liberation movements. The company was learning that technical excellence in mining meant nothing without political and social sophistication.

Fred Searls became president in 1947, after serving as the company's exploration geologist. Searls represented a new breed of mining executive—technically trained but strategically minded. Under his leadership, Newmont didn't just dig holes; it built an intellectual framework for finding and developing mineral deposits globally. Searls institutionalized the company's exploration methodology: systematic geological surveys, patient capital deployment, and portfolio diversification across geographies and commodities.

The diversification strategy accelerated through the 1950s and 1960s. Eventually, Newmont's oil interests included more than 70 blocks in the Louisiana Gulf of Mexico area and oil and gas production in the North Sea. This wasn't random empire building—it was calculated risk management. When gold prices were fixed at $35 per ounce by Bretton Woods, you needed other revenue streams. When African politics turned volatile, you needed North American stability. When metal prices crashed, oil might boom.

But the African operations weren't just about extraction—they became a laboratory for dealing with complex social and political dynamics. The Tsumeb mine employed thousands of contract workers from across southern Africa, creating a microcosm of the region's racial and ethnic tensions. In 1971-72, these tensions exploded into strikes as Namibian contract workers protested both the contract labor system and apartheid itself. Newmont found itself caught between its operational needs, international pressure to divest from apartheid states, and its responsibilities to local workers and communities.

The company's response revealed both the limitations and evolution of corporate thinking in this era. While Newmont didn't abandon its African operations—the assets were too valuable—it began developing more sophisticated approaches to stakeholder management, worker relations, and political risk assessment. These hard-won lessons in Namibia would later inform Newmont's approaches in Peru, Indonesia, and Ghana.

Meanwhile, back in North America, Newmont was quietly revolutionizing gold mining technology. The company's geologists had identified massive low-grade gold deposits in Nevada that couldn't be mined profitably with traditional methods. But what if you could process millions of tons of ore with just grams of gold per ton? What if you could use chemistry—specifically heap leaching with cyanide solutions—to extract gold from rock that previous generations of miners had written off as waste?

This technical revolution coincided with a political one. In 1971, President Nixon ended the convertibility of dollars to gold, effectively killing the Bretton Woods system. For the first time since 1934, gold prices could float freely. They exploded from $35 to over $800 per ounce by 1980. Suddenly, those massive low-grade deposits in Nevada weren't just viable—they were gold mines in the most literal sense.

The international expansion of this era also taught Newmont about the importance of joint ventures and partnerships. The company rarely entered new jurisdictions alone, instead partnering with local companies that understood the political and social landscape. This approach—which seemed cautious compared to the go-it-alone swagger of some competitors—would prove prescient as resource nationalism swept through developing countries in the 1970s.

By the late 1970s, Newmont had transformed from a North American gold miner with some international investments into a truly global resources company. Operations spanned from the Arctic to the Equator, from sea-level oil platforms to Andean mountain peaks. The company had learned to navigate everything from apartheid protests to OPEC embargoes, from environmental regulations in California to traditional land rights in Papua New Guinea.

But this global footprint came with a cost. The company had become a conglomerate—profitable but unfocused, successful but vulnerable. As the 1980s dawned, a new breed of financial predator began circling, seeing in Newmont's diverse assets not a strength but an opportunity. The empire Newmont had built over four decades was about to face its greatest existential threat.

IV. The Takeover Wars of the 1980s

The mahogany-paneled boardroom at 1700 Lincoln Street in Denver felt like a war room in September 1987. Maps covered the walls—not of gold deposits but of shareholding structures, poison pill provisions, and defensive strategies. Gordon Parker, Newmont's CEO, stood before his board with grim news: T. Boone Pickens, the most feared corporate raider in America, had just disclosed a 9.9% stake in Newmont. The barbarians weren't just at the gate—they were already inside, and they wanted to tear apart everything Newmont had built over seven decades.

In the 1980s, Newmont thwarted five takeover bids—from Consolidated Gold Fields (ConsGold), T. Boone Pickens, Minorco, Hanson Industries and James Goldsmith. Each attack was different, each predator more sophisticated than the last. This wasn't business—this was war, fought with junk bonds and hostile tender offers instead of bullets and bombs.

The Pickens assault was the most dramatic. Here was a man who'd already taken down Gulf Oil, one of the Seven Sisters, forcing its sale to Chevron for $13.2 billion. His modus operandi was simple and ruthless: buy a significant stake, agitate for board seats, then either take control or force the company to buy him out at a premium—"greenmail," in the parlance of the era. With Newmont trading at a significant discount to the value of its assets, Pickens smelled blood.

In 1987, defending against a $6.3 billion bid by T. Boone Pickens, the company paid a US$33 per share special dividend to all shareholders, US$2.2 billion in cash, of which US$1.75 billion was borrowed. This was corporate defense at its most extreme—essentially, Newmont set itself on fire to avoid being captured. The special dividend represented nearly half the company's market value, paid out in one massive check to all shareholders, including Pickens.

The strategy was brilliant in its audacity. By borrowing $1.75 billion to fund the dividend, Newmont loaded itself with debt, making it far less attractive as a takeover target. It was the corporate equivalent of a retreating army burning crops and poisoning wells—scorched earth tactics that left nothing valuable for the invader. Pickens got his money, but he didn't get Newmont.

But the cost was staggering. To reduce this debt the company undertook a divestment program involving all of its copper, oil, gas, and coal interests. Four decades of careful diversification, undone in months. The oil blocks in the Gulf of Mexico—gone. The copper mines in Africa—sold. The coal properties—divested. It was like watching a master chef forced to sell his kitchen equipment piece by piece to pay off loan sharks.

The divestitures fundamentally transformed Newmont's identity. No longer a diversified resources company, it became a pure-play gold miner almost by accident—or rather, by necessity. Gold was what remained after everything else had been sold to pay down the defensive debt. Sometimes strategy emerges not from planning but from survival.

As a further step in the restructuring, the company moved its headquarters from New York City to Denver in 1988. This wasn't just about saving money on Manhattan real estate. It was a symbolic break from Newmont's Wall Street origins, a declaration that this was now an operating company, not a financial vehicle. Denver put them closer to their Nevada operations, closer to the engineers and geologists who actually found and extracted gold, further from the investment bankers who saw mines as merely assets to be traded.

The battles of the 1980s taught Newmont crucial lessons about corporate governance and shareholder value. The raiders had a point—the company had been trading at a massive discount to its asset value. Management had been too comfortable, too focused on empire building rather than returns. The attacks forced a discipline that would serve Newmont well in coming decades: every asset had to earn its keep, every acquisition had to be accretive, every ounce of gold had to generate returns above the cost of capital.

The human toll was significant. Hundreds of employees lost their jobs in the divestitures. Entire divisions that had been built over decades disappeared overnight. The company culture shifted from that of a paternalistic conglomerate to a lean, focused competitor. The old Newmont—patient, diversified, genteel—was dead. What emerged from the takeover wars was harder, more focused, and ultimately more successful.

But perhaps the most important outcome was the clarity of purpose that emerged from crisis. By 1990, Newmont knew exactly what it was: a gold mining company, period. Not a resources conglomerate, not a financial holding company, not a vehicle for diversification. This clarity would drive every decision for the next three decades—which mines to buy, which partnerships to pursue, which technologies to develop. The raiders had failed to capture Newmont, but they had succeeded in transforming it into something more valuable than they'd ever imagined.

V. Transformation & Focus (1990s–2000s)

Wayne Murdy looked out at the sea of skeptical faces at the Denver Gold Forum in September 2007. As Newmont's CEO, he was about to announce something that would either be seen as visionary or foolish: Newmont would eliminate its entire 1.5 million ounce hedge book, making it the world's largest unhedged gold producer. In an industry where hedging—locking in future gold prices—was considered prudent risk management, Murdy was betting the company's future on his belief that gold prices would rise. The murmurs in the audience were audible. Had Newmont lost its mind?

In 2007, the company eliminated its 1.5 million ounce legacy hedge book to make Newmont the world's largest unhedged gold producer. This wasn't just an accounting decision—it was a philosophical statement about what Newmont had become. Pure-play gold exposure meant that investors buying Newmont stock were making an unfiltered bet on gold prices. No hedges, no derivatives, no financial engineering. When gold rose, Newmont would capture every dollar of upside. When it fell, there would be no protection.

The de-hedging decision looked prescient almost immediately. Gold prices, which had languished around $400 per ounce in the early 2000s, began their historic run, reaching $1,900 by 2011. Every dollar of increase flowed directly to Newmont's bottom line. Competitors who'd locked in lower prices through hedging watched in agony as Newmont captured windfalls they'd signed away years earlier.

But the transformation of the 1990s and 2000s went far beyond financial strategy. This was when Newmont became truly scientific about gold mining. The company pioneered new extraction technologies, developed proprietary geological models, and most importantly, began thinking about mines not as individual assets but as portfolios to be optimized.

The following year, Newmont acquired Miramar Mining Corporation and its Hope Bay deposit in the Canadian Arctic. Hope Bay represented a new frontier—gold mining in one of the world's most challenging environments, where the ground was permanently frozen and supply ships could only reach the site during a brief summer window. But Newmont's engineers saw opportunity where others saw impossibility. The frozen ground that made construction difficult also provided stability for underground mining. The isolation that increased costs also meant minimal local opposition.

The Boddington acquisition in Australia showed Newmont's evolving M&A philosophy. In 2009, Newmont purchased the remaining one-third interest in Boddington Gold Mine from AngloGold Ashanti, bringing its ownership to 100 percent. Rather than entering a bidding war for new properties, Newmont consolidated control of assets it already partially owned. It's easier to create value by optimizing operations you understand than by integrating unfamiliar assets. In April 2011, the company acquired Canada's Fronteer Gold Inc. for CA$2.3 billion. This made the company the world's second-largest gold producer. The Fronteer acquisition was particularly strategic—it brought Newmont the Long Canyon project in Nevada, essentially doubling down on the company's most profitable region. While competitors were chasing growth in politically risky jurisdictions, Newmont was consolidating its position in the world's most mining-friendly district.

The technological revolution of this period can't be overstated. Newmont's metallurgists developed proprietary processes for extracting gold from refractory ores—rock where gold is locked inside sulfide minerals and invisible to conventional processing. The company's autoclaves, essentially giant pressure cookers, could liberate gold that had been uneconomical to extract for centuries. This technology opened up billions of tons of previously worthless rock to profitable mining.

Environmental and social considerations also evolved dramatically during this period. The old model of mining—extract value and leave—was no longer acceptable. Newmont began investing heavily in community development, environmental remediation, and stakeholder engagement. The company learned, sometimes painfully, that a mine's social license to operate was as valuable as its mineral reserves.

The 2008 financial crisis tested this new model. Gold prices initially crashed along with everything else, falling from over $1,000 to under $700 per ounce in a matter of months. But as central banks worldwide began printing money to combat the recession, gold found new purpose as a hedge against currency debasement. Prices began their historic run to $1,900 by 2011, validating Newmont's unhedged strategy spectacularly.

This period also saw Newmont perfect its capital allocation framework. Every potential acquisition was evaluated through multiple lenses: geological potential, political risk, operational synergies, and most importantly, return on invested capital. The company walked away from numerous auctions where competitors overpaid, choosing instead to invest in expanding existing operations where they had information advantages.

By 2010, Newmont had transformed from the besieged conglomerate of the 1980s into a disciplined, focused gold mining machine. The company produced over 5 million ounces annually from operations spanning six continents. Its unhedged position meant it captured full value from rising gold prices. Its technological leadership allowed it to process ores competitors couldn't touch. Most importantly, it had developed the operational excellence and financial discipline that would enable the next phase of growth through transformative M&A.

VI. The Goldcorp Acquisition: Creating a Giant (2019)

Gary Goldberg stood before a packed auditorium at Newmont's Denver headquarters on January 14, 2019, his voice steady but carrying the weight of history. "Today," he announced, "we are creating the world's leading gold company." The room erupted—not in celebration, but in a cacophony of questions. Outside, protestors from John Paulson's hedge fund held signs reading "NO PREMIUM FOR MEDIOCRITY." The irony wasn't lost on anyone: Newmont was paying $10 billion for Goldcorp just three months after rival Barrick had merged with Randgold, instantly relegating Newmont to second place. This wasn't just about reclaiming the crown—it was about survival in an industry undergoing radical consolidation.

On January 14, 2019, Newmont announced they have entered into a definitive agreement in which Newmont will acquire all of the outstanding common shares of Goldcorp in a stock-for-stock transaction valued at $10 billion. The timing was no coincidence. Barrick's September 2018 merger with Randgold had changed everything, creating a new industry giant that threatened Newmont's position as the sector leader. The gold mining industry was consolidating rapidly, and standing still meant falling behind.

Newmont will acquire each Goldcorp share for 0.3280 of a Newmont share, which represents a 17 percent premium based on the companies' 20-day volume weighted average share prices. That 17% premium became the lightning rod for controversy. In an industry where overpaying for acquisitions had destroyed billions in shareholder value, why was Newmont repeating history's mistakes?

Hedge fund billionaire John Paulson was among the shareholders objecting to the deal, stating that the 17% premium Newmont was paying for Goldcorp was too high. Paulson wasn't just any investor—he'd made billions betting against subprime mortgages in 2008 and owned roughly 1% of Newmont. His opposition carried weight, and he wasn't alone. The market's initial reaction was brutal: Newmont shares fell 8.9%, wiping out over $2 billion in market value on the announcement day.

But Goldberg and his team saw something the critics missed. Goldcorp brought world-class assets in the Americas—including the massive Peñasquito mine in Mexico and the high-grade Éléonore mine in Quebec. More importantly, it brought scale at a time when scale mattered more than ever. The combined company would produce 6-7 million ounces annually, have the industry's largest reserve base, and most crucially, have the financial firepower to develop the next generation of mines while others struggled.

The real genius of the deal emerged in what happened next. The biggest deal in the gold mining industry's history comes just three months after Barrick Gold Corp.'s move to buy Randgold Resources Ltd. in a $5.4 billion transaction, which instantly spurred speculation that rivals would have to respond. Barrick's CEO Mark Bristow, never one to miss an opportunity, launched a hostile bid for Newmont in February 2019, offering to acquire the company in an all-stock nil-premium merger. It was audacious—trying to hijack Newmont's Goldcorp deal to create an even larger mega-miner. But Newmont's board, led by Goldberg, wasn't intimidated. They rejected Barrick's offer outright, calling it "desperate" and proposing instead something revolutionary: why not combine just the Nevada operations? After weeks of public acrimony—Bristow called Goldberg a "loser" in a Reuters interview, while Goldberg questioned Bristow's "credibility and experience"—the two CEOs met secretly in New York and Toronto.

What emerged was extraordinary. Historic joint venture designed to unlock $5 billion in synergies with Barrick to be Operator, Ownership to be 61.5% Barrick; 38.5% Newmont. The joint venture is an historic accord between the two gold mining companies, which have operated independently in Nevada for decades, but have previously been unable to agree terms for cooperation. The joint venture will allow them to capture an estimated $500 million in average annual pre-tax synergies in the first five full years of the combination, which is projected to total $5 billion pre-tax net present value. This wasn't defeat—it was strategic brilliance. Newmont got to complete its Goldcorp acquisition while capturing massive synergies in Nevada without ceding control of the entire company.

The Goldcorp acquisition closed successfully in April 2019, creating Newmont Goldcorp (later simplified back to Newmont Corporation). The combined entity became the world's leading gold producer with operations in favorable jurisdictions, producing 6-7 million ounces annually from a portfolio that included more tier-one assets than any competitor.

But the integration wasn't without challenges. Cultural differences between Newmont's methodical, process-driven approach and Goldcorp's more entrepreneurial style created friction. The promised $100 million in annual synergies proved conservative—the company ultimately delivered more—but achieving them required painful decisions, including workforce reductions and mine closures.

The real vindication came with gold prices. From the announcement in January 2019 through 2020, gold surged from $1,280 to over $2,000 per ounce, driven by pandemic-related monetary stimulus. Every ounce of increased production from the Goldcorp assets generated windfall profits. The critics who'd lambasted the 17% premium went quiet as Newmont's stock outperformed.

Looking back, the Goldcorp acquisition represented a masterclass in strategic M&A. Newmont didn't just buy assets—it reshaped the entire industry landscape, forcing its biggest rival into a cooperative venture while consolidating its position as the sector leader. The deal proved that in mining, as in chess, sometimes the best offense is a sophisticated defense that turns your opponent into your partner.

VII. The Nevada Gold Mines Joint Venture

The signing ceremony took place in Elko, Nevada, on March 11, 2019, in a nondescript conference room at the Red Lion Hotel & Casino. Outside, the temperature hovered near freezing, typical for March in the high desert. Inside, two men who'd spent weeks publicly insulting each other sat side by side, pens in hand. Mark Bristow and Gary Goldberg were about to sign away 20 years of corporate rivalry, creating something neither company could have built alone: Nevada Gold Mines, the world's largest gold mining complex.

The joint venture will allow them to capture an estimated $500 million in average annual pre-tax synergies in the first five full years of the combination, which is projected to total $5 billion pre-tax net present value over a 20-year period. These weren't just paper synergies dreamed up by investment bankers. They were real, operational improvements that had been obvious to engineers on both sides for decades but impossible to capture due to corporate pride.

The geography told the story better than any PowerPoint deck. Barrick's Goldstrike complex and Newmont's Carlin operations sat literally adjacent to each other, separated by chain-link fences and corporate stubbornness. Ore trucks from one company would drive past the other's processing facilities to reach their own mills 50 miles away. Both companies maintained separate teams of geologists studying the same ore body, separate procurement departments buying from the same suppliers, separate maintenance crews servicing identical equipment.

"The Barrick-Newmont ownership split announced on Monday will be 61.5 per cent in favour of Barrick with the Toronto-based miner also named as the operator. The agreement will see gigantic mines, including Barrick's Goldstrike and Cortez operations, along with Newmont's Carlin, unite under one roof. Both companies say the combination will generate an average of US$500-million in cost savings over the first five years through the common sharing of processing facilities, eliminating duplicate costs and co-ordinating on mine plans".

The operational structure was elegant in its simplicity. Nevada Gold Mines would operate as an independent entity, with Barrick as the operator leveraging its technical expertise while Newmont maintained significant influence through board representation and technical committees. It was a structure designed to minimize ego and maximize value—a rarity in the mining industry.

On July 1, 2019, Barrick Gold Corporation and Newmont Corporation successfully concluded the transaction establishing Nevada Gold Mines LLC. The speed of implementation—from hostile takeover attempt to operational joint venture in less than six months—was unprecedented in mining history. Both companies understood that delay meant value destruction. Every day the assets operated separately was money left on the table.

The synergies materialized almost immediately. By combining operations, Nevada Gold Mines could optimize processing routes, sending ore to the nearest and most appropriate facility regardless of historical ownership. The Carlin roasters, previously running below capacity, could now process refractory ore from Barrick's operations. Goldstrike's autoclaves could handle Newmont's sulfide ores. This wasn't just efficiency—it was alchemy, turning previously marginal ore into profitable production.

The human side of integration proved surprisingly smooth. Engineers and geologists who'd spent careers competing suddenly found themselves collaborating. The joke in Elko was that the only thing that changed was the color of the hard hats. But the cultural shift was profound. Decades of "not invented here" syndrome evaporated as teams realized they were working toward the same goal.

The technical achievements were remarkable. By combining geological databases, Nevada Gold Mines created the most comprehensive understanding of the Carlin Trend ever assembled. Patterns invisible to separate companies became obvious when data was integrated. New ore bodies were identified in areas previously thought barren. Deposits written off by one company proved profitable when processed through the other's facilities.

The financial performance exceeded even the most optimistic projections. The joint venture generated over $600 million in synergies in its first full year, well above the $500 million five-year average target. Free cash flow surged as duplicate costs disappeared and production optimized. Both parent companies benefited proportionally, validating the ownership structure.

But perhaps the most important outcome was the precedent it set. Nevada Gold Mines proved that even the fiercest rivals could cooperate when the value creation opportunity was large enough. It showed that operational excellence trumped corporate ego, that shareholder value could be created through collaboration rather than conquest.

The joint venture also transformed Nevada's mining landscape. With stable, long-term ownership and massive capital resources, Nevada Gold Mines could undertake projects neither company would have attempted alone. Deep exploration programs, technological innovations, and infrastructure investments that required 20-year payback periods suddenly made sense.

Environmental and community relations improved as well. Instead of two companies negotiating separately with regulators and communities, Nevada Gold Mines presented a unified front, simplifying stakeholder engagement and ensuring consistent standards across all operations. The joint venture committed to Nevada for the long term, investing in local education, infrastructure, and economic development.

The success of Nevada Gold Mines raised an obvious question: if cooperation worked so well in Nevada, why not elsewhere? Both Barrick and Newmont had operations in other jurisdictions where collaboration might create value. But Nevada was unique—the geographic concentration, the scale of operations, the favorable regulatory environment. Replicating the model elsewhere would prove more challenging.

VIII. The Newcrest Mega-Deal (2023)

Tom Palmer sat in the CEO's office—the same one Gary Goldberg had occupied, the same one Gordon Parker had defended against corporate raiders—staring at the preliminary offer letter from Newcrest Mining on his desk. It was February 2023, and gold prices were hovering around $1,900 per ounce. The Australian mining giant Newcrest, with its crown jewel Cadia mine producing over 700,000 ounces annually at industry-leading costs, represented the final piece of Newmont's global consolidation strategy. But Palmer knew this would be his defining deal—either cementing Newmont's position for a generation or destroying shareholder value in a spectacular overreach.

Gold giant Newmont Corp. secured a A$28.8 billion ($19.2 billion) deal to buy Australian rival Newcrest Mining Ltd., consolidating its position as the world's biggest bullion producer with mines across the Americas, Africa, Australia and Papua New Guinea. The transaction, now unanimously approved by Newcrest's board but pending regulatory approval, is the gold mining sector's largest deal to date, surpassing Newmont's purchase of rival Goldcorp Inc. in 2019.

The strategic logic was compelling. Newcrest brought assets Newmont couldn't replicate: Cadia in Australia, one of the world's lowest-cost gold mines that also produced significant copper; Lihir in Papua New Guinea, a massive island operation with decades of reserves; and Brucejack in British Columbia's Golden Triangle. But more than assets, Newcrest brought copper—50 billion pounds of copper reserves that would transform Newmont from a gold company with copper byproducts into a true precious metals and critical minerals producer.

The negotiations were delicate. Newcrest had rejected Newmont's initial offer of 0.380 shares per Newcrest share, holding out for better terms. The Australian government watched closely—this was their largest gold producer being acquired by an American company. The Foreign Investment Review Board would scrutinize every detail. Environmental groups questioned whether Newmont could manage Newcrest's complex operations, particularly in sensitive areas like Papua New Guinea.

Under the terms of the agreement, Newcrest shareholders will be entitled to receive 0.400 Newmont shares for each Newcrest share held. In addition, Newcrest will be permitted to pay a franked special dividend of up to $1.10 per share on or around the implementation of the scheme of arrangement. The improved offer, combined with the special dividend, valued Newcrest at a premium that satisfied its board while maintaining discipline on Newmont's side.

This time, unlike with Goldcorp, shareholder opposition was muted. The market had learned that Newmont's M&A track record, while not perfect, was better than most. The acquisition received strong support from Newcrest Mining shareholders, with 92.63% of votes cast in favour of the deal. Newmont shareholders in the U.S. voted over 96% in favour of the acquisition.

The completion in November 2023 created something unprecedented: This transaction has expanded Newmont's industry-leading portfolio in the most favorable mining jurisdictions—now including more than half of the world's Tier 1 gold mines. No other gold company came close to this concentration of world-class assets. The combined entity would produce over 8 million gold equivalent ounces annually, with the flexibility to optimize production based on commodity prices.

But the real genius of the Newcrest deal wasn't just scale—it was optionality. With significant copper production, Newmont was positioned for the energy transition. As electric vehicles and renewable energy infrastructure demanded more copper, Newmont's Newcrest assets would become increasingly valuable. The company that had started as a gold investment vehicle in 1916 was now positioned for the commodities that would define the next century.

Integration proceeded with the precision Newmont had developed over multiple acquisitions. Annual pre-tax synergies of $500 million are expected within the first 24 months. At least $2 billion in cash improvements through portfolio optimization are expected in the first two years after closing. The company applied lessons learned from Goldcorp: move quickly, communicate clearly, retain key talent, and focus relentlessly on operational excellence.

The cultural integration proved smoother than expected. Australian mining culture, with its emphasis on technical excellence and safety, meshed well with Newmont's systematic approach. The companies shared similar values around sustainability and community engagement. Unlike the Goldcorp integration, where cultural clashes created friction, Newcrest's team integrated seamlessly.

Palmer's strategic vision extended beyond just owning assets. Newmont announced plans to divest $2 billion in non-core assets, focusing the portfolio on the highest-return operations. This wasn't empire building—it was portfolio optimization, ensuring every asset earned its cost of capital and contributed to overall returns.

The Newcrest acquisition also transformed Newmont's geographic footprint. With major operations in Australia and increased exposure to Asia-Pacific markets, Newmont was no longer just an Americas-focused miner. The company now had natural hedging against regional political and economic risks, with production distributed across stable jurisdictions.

Looking at the three transformative deals—Goldcorp, the Nevada JV, and Newcrest—a pattern emerges. Each deal was controversial at announcement, each faced skepticism about price and execution, yet each ultimately created significant value. The key was Newmont's disciplined approach to integration, its focus on operational synergies over financial engineering, and its willingness to divest non-core assets to maintain portfolio quality.

The Newcrest deal marked the end of an era of mega-consolidation in gold mining. With Newmont controlling the industry's best assets, Barrick focused on its portfolio, and few remaining independents of scale, the next phase of industry evolution would be different—focused on technology, sustainability, and operational excellence rather than transformative M&A.

IX. Playbook: The Newmont Way

Capital Allocation in a Cyclical Industry

The conference room in Denver feels different from those in New York or London. Here, the walls display core samples instead of abstract art, and the executives wear steel-toed boots as often as Italian leather. This is where Newmont's capital allocation decisions get made—decisions that must balance the realities of geology with the demands of Wall Street, the 20-year life of a mine with the quarterly earnings cycle.

Newmont's capital allocation framework, refined over decades of boom and bust cycles, operates on a simple principle: in a cyclical industry, discipline during the good times determines survival during the bad. When gold hit $1,900 in 2011, competitors rushed to develop marginal projects. Newmont held back, maintaining its hurdle rate of 15% IRR at $1,200 gold. This conservatism looked foolish when gold was soaring but proved prescient when prices crashed to $1,050 in 2015.

The company's approach to project development exemplifies this discipline. Every potential mine goes through five decision gates, with increasing scrutiny at each stage. A project that looked attractive at gate one might be killed at gate three if costs escalate or ore grades disappoint. This willingness to write off sunk costs—to admit mistakes before they become disasters—distinguishes Newmont from peers who throw good money after bad.

The portfolio approach extends to operations. Newmont runs its mines like a mutual fund manager runs a portfolio—constantly rebalancing based on performance and potential. Underperforming assets get one chance to improve. If they fail, they're sold or closed, regardless of emotional attachment or historical significance. This ruthlessness ensures capital flows to the highest-return opportunities.

The Art of Mega-Mergers: When to Buy, When to Partner

Newmont's M&A playbook, written in the blood of failed mining mergers, contains hard-won lessons. The first rule: never buy for growth alone. Every acquisition must be accretive on a per-share basis—more reserves per share, more cash flow per share, more NAV per share. The Goldcorp and Newcrest deals both met these criteria, despite their premium prices.

The second rule: integration planning starts before the deal closes. Newmont maintains a standing integration team that begins work the moment a deal is announced. They identify the top 100 decisions that need to be made in the first 100 days, from organizational structure to system integration. This preparation enables rapid value capture once the deal closes.

The third rule: culture matters as much as geology. Newmont walks away from deals where cultural misalignment would destroy value. The company learned this lesson painfully in smaller acquisitions where technical synergies were overwhelmed by organizational friction. Now, cultural due diligence is as rigorous as technical evaluation.

The Nevada joint venture revealed another dimension of Newmont's M&A strategy: sometimes the best deal isn't an acquisition but a partnership. By structuring the JV with Barrick, Newmont captured billions in synergies without the cost and disruption of a full merger. This flexibility—knowing when to buy, when to partner, and when to walk away—defines sophisticated M&A strategy.

Managing Political and Environmental Risk

With approximately 31,600 employees and contractors worldwide, and is the only gold company in the S&P 500 stock market index, Newmont operates at a scale where political and environmental missteps can destroy billions in value. The company's risk management framework treats these "above-ground" risks as seriously as geological challenges.

Political risk management starts with jurisdiction selection. Newmont concentrates its operations in stable democracies with strong rule of law—the U.S., Canada, Australia. When operating in riskier jurisdictions like Ghana or Peru, the company maintains strict investment limits and higher return hurdles. This geographic discipline has protected Newmont from the nationalization and expropriation that has plagued competitors.

Environmental management has evolved from compliance to competitive advantage. Newmont's environmental investments—in water treatment, land reclamation, emissions reduction—often exceed regulatory requirements. This over-investment pays dividends in faster permitting, stronger community support, and lower long-term liabilities. The company learned that environmental excellence is cheaper than environmental remediation.

Community relations follow a similar philosophy. Newmont invests in local communities before production begins, building schools, hospitals, and infrastructure. These investments create stakeholders in the mine's success, transforming potential opponents into supporters. The company's community development programs have become a model for the industry.

Building and Maintaining Social License

The concept of "social license to operate" sounds abstract until you've seen a mine shut down by community protests. Newmont has learned that legal permits mean nothing without community support. This reality has transformed how the company approaches new projects and manages existing operations.

Social license begins with transparency. Newmont publishes detailed reports on its environmental impact, community investments, and economic contributions. This transparency builds trust and makes it harder for opponents to spread misinformation. The company learned that secrets create suspicion, while openness creates credibility.

Employment practices reinforce social license. Newmont prioritizes local hiring, even when it requires extensive training. A mine that employs 1,000 local workers has 1,000 families invested in its success. The company's training programs have created a generation of skilled workers in communities that previously had few economic opportunities.

The approach to indigenous relations has evolved dramatically. Newmont now negotiates comprehensive agreements with indigenous groups before exploration begins. These agreements share economic benefits, protect cultural sites, and establish grievance mechanisms. What once was seen as a cost is now recognized as investment in operational stability.

Technology and Innovation in Traditional Mining

Mining seems like the ultimate old-economy industry—digging holes in the ground hasn't changed since ancient times. But Newmont's operations showcase cutting-edge technology that would seem like science fiction to miners of previous generations.

Autonomous haul trucks operate 24/7 in several Newmont mines, guided by GPS and collision-avoidance systems. These trucks never get tired, never take breaks, and never have accidents caused by human error. One operator in a control room can manage multiple trucks, dramatically improving productivity and safety.

Data analytics has transformed exploration. Newmont's geologists use machine learning algorithms to identify patterns in geological data that human eyes would miss. These models can predict where gold deposits might exist based on subtle correlations in rock chemistry, structure, and mineralization. What once took decades of trial and error now takes months of computational analysis.

Processing technology continues to evolve. Newmont's metallurgists have developed proprietary techniques for extracting gold from refractory ores that competitors can't process economically. These innovations—often involving complex chemistry and high-pressure physics—turn waste rock into profitable ore.

But perhaps the most important innovation is in integrated operations centers. Newmont's mines are monitored in real-time from central control rooms where experts can identify and solve problems instantly. A processing bottleneck in Ghana can be diagnosed by an expert in Denver. This integration improves efficiency and enables rapid knowledge transfer across operations.

The company's approach to innovation balances revolution with evolution. While investing in breakthrough technologies, Newmont also focuses on incremental improvements—a 1% increase in recovery rates, a 2% reduction in energy consumption. These small gains, multiplied across massive operations, create enormous value.

X. Bear vs. Bull Case

Bull Case: The Dominant Franchise

The bull case for Newmont starts with an unassailable fact: the company owns more tier-one gold assets than any competitor. These aren't just mines—they're franchises that will generate cash for decades. Cadia, Carlin, Tanami, Peñasquito—each represents billions in net present value. In an industry where grade is king and discovery rates are plummeting, Newmont's portfolio provides unmatched exposure to gold prices.

Scale creates competitive advantages that compound over time. Newmont's purchasing power drives lower input costs. Its technical expertise solves problems smaller miners can't tackle. Its balance sheet enables countercyclical investment when competitors are forced to retrench. These advantages create a virtuous cycle where success begets success.

The M&A track record, despite skeptics' concerns about premiums paid, has created enormous value. The Goldcorp acquisition brought world-class assets and enabled the Nevada JV. The Newcrest deal added copper optionality just as the energy transition accelerates demand. Each deal was controversial at announcement but vindicated by execution. This proven integration capability means Newmont can continue consolidating the industry profitably.

Gold's investment thesis has never been stronger. Central banks are buying gold at the fastest pace in decades, seeking alternatives to dollar reserves. Inflation remains structurally higher than the past decade, increasing gold's appeal as a hedge. Geopolitical tensions—from Ukraine to Taiwan—drive safe-haven demand. Meanwhile, gold supply faces structural challenges, with discoveries declining and ore grades falling globally.

The copper optionality from Newcrest transforms Newmont's growth profile. As electric vehicles and renewable energy drive copper demand, Newmont's 50 billion pounds of copper reserves become increasingly valuable. The company can optimize production based on relative commodity prices, mining more gold when gold outperforms or more copper when copper leads.

Environmental, social, and governance (ESG) leadership translates into tangible value. Newmont's industry-leading ESG practices attract institutional capital that's increasingly restricted from investing in poor ESG performers. This creates a valuation premium that should persist as sustainable investing mainstreams.

Bear Case: The Challenges of Scale

The bear case begins with integration risk. Newmont has absorbed two massive acquisitions in five years, fundamentally transforming its operational footprint. While management claims smooth integration, the full challenges may not be apparent until the next downcycle. Cultural clashes, system incompatibilities, and organizational complexity could emerge when market conditions deteriorate.

Rising costs plague the entire mining industry, but scale doesn't provide immunity. Labor costs are surging as mining struggles to attract workers. Energy costs remain elevated despite recent moderation. Environmental compliance costs only move in one direction—up. Even tier-one assets face margin pressure when all inputs inflate faster than gold prices.

Gold price volatility remains the fundamental risk. Newmont's unhedged position means full exposure to price swings. A return to $1,500 gold—not unrealistic if real interest rates rise or the dollar strengthens—would slash cash flows and potentially trigger asset impairments. The company's high fixed costs mean earnings volatility exceeds price volatility.

Geopolitical risks have intensified, not diminished. Operations in Ghana, Peru, and Mexico face increasing resource nationalism. Even stable jurisdictions like Australia and Canada are raising mining taxes and environmental standards. The concentration of value in a few key assets means a single political disruption could materially impact results.

ESG challenges lurk beneath the positive narrative. Legacy environmental liabilities from acquired companies could emerge. Indigenous relations remain contentious at several operations. Water scarcity threatens desert operations. Climate change regulations could dramatically increase costs. These risks are difficult to quantify but potentially enormous.

The technology disruption thesis cuts both ways. While Newmont invests heavily in innovation, breakthrough technologies could obsolete traditional mining. Laboratory-grown diamonds devastated that mining sector—could synthetic gold face similar acceptance? More realistically, technologies that make low-grade deposits viable could destroy the value of Newmont's tier-one assets by flooding the market with supply.

Shareholder return expectations may prove unsustainable. Newmont has promised sector-leading dividends while also investing in growth and maintaining balance sheet strength. Something must give if gold prices disappoint or costs surge. The company's history of dividend cuts during downturns suggests shareholder returns are the adjustment variable.

The Verdict: Asymmetric Risk-Reward

The bear and bull cases reveal a fundamental tension: Newmont offers the best assets and execution in gold mining, but it operates in an industry facing structural challenges. The company has successfully navigated these tensions for over a century, suggesting institutional resilience that transcends temporary setbacks.

For fundamental investors, Newmont represents a rare combination: exposure to a monetary asset with industrial discipline. The company's portfolio approach, proven integration capability, and operational excellence create value through the cycle. While risks are real and substantial, they're arguably more than compensated by the quality of assets and management.

The key insight is that Newmont has transformed from a price-taker to a price-maker. Through consolidation, the company has gained sufficient scale to influence industry dynamics. This market power, combined with tier-one assets and execution excellence, creates sustainable competitive advantages that should compound over time.

XI. Power & Lessons

The Power of Patient Capital and Long-Term Thinking

In the basement of Newmont's Denver headquarters sits a remarkable artifact: a leather-bound ledger from 1921, recording the company's first operational gold purchase. The meticulous handwritten entries—ounces produced, costs incurred, prices realized—tell a story of patient capital at work. This ledger, and thousands like it, embody Newmont's greatest power: the ability to think in decades while executing in quarters.

Patient capital in mining means accepting that value creation follows geological time, not Wall Street time. Newmont's Carlin Trend operations took 20 years to reach full potential. The Tanami expansion required a decade of development. Cadia's underground extension won't reach full production until 2030. These timelines would horrify Silicon Valley, but they're the reality of extractive industries. Newmont's power lies in aligning capital, strategy, and expectations with these geological realities.

The company's long-term thinking manifests in exploration spending during downturns. When gold crashed in 2013, competitors slashed exploration budgets to preserve cash. Newmont maintained spending, acquiring prospective land when others retreated. These countercyclical investments, invisible in quarterly earnings, created billions in option value that materialized when prices recovered.

Long-term thinking also means accepting short-term pain for long-term gain. The decision to eliminate hedging in 2007 reduced earnings visibility and increased volatility. But it positioned Newmont to capture full upside when gold soared. The Nevada JV with Barrick required surrendering operational control of prize assets but created value that solo operation never could have achieved.

How to Survive and Thrive Through Commodity Cycles

Newmont has survived 30 major commodity cycles since 1921—from the Depression to the Great Recession, from $35 gold to $1,900 gold. This survival isn't luck; it's the product of a systematic approach to cyclical risk management that treats downturns as inevitable rather than unexpected.

The first principle: maintain balance sheet strength during booms. When gold hit record highs, competitors leveraged up to fund marginal projects. Newmont paid down debt and accumulated cash. This conservatism looked foolish at cycle peaks but provided the flexibility to act decisively during downturns. The ability to invest when others are forced to sell creates extraordinary returns.

The second principle: diversify across the cycle's natural hedges. Geographic diversification protects against regional downturns. Asset quality diversification—maintaining both low-cost and high-grade operations—provides flexibility as prices fluctuate. The recent addition of copper exposure through Newcrest creates commodity diversification. These multiple layers of protection ensure survival regardless of specific cycle dynamics.

The third principle: use downturns to upgrade the portfolio. Newmont's best acquisitions happened during industry distress. The company bought Normandy during the 2001 gold bear market. It acquired Fronteer when juniors couldn't access capital. The Newcrest deal materialized as inflation fears drove strategic consolidation. Buying quality assets from distressed sellers is the ultimate cyclical strategy.

The Importance of Operational Excellence in M&A

The mining industry graveyard is littered with failed mergers—Barrick-Placer, Kinross-Red Back, Vale-Inco. These disasters teach a crucial lesson: in mining, operational excellence matters more than financial engineering. Newmont's successful M&A track record stems from prioritizing operations over abstractions.

Operational excellence in M&A starts with realistic synergy estimates. Newmont's integration teams include mine managers, not just investment bankers. They understand that theoretical savings become real only through operational changes—combining maintenance crews, optimizing truck routes, standardizing procurement. These granular improvements, invisible in merger models, determine success or failure.

The company's integration methodology, refined over multiple acquisitions, follows a proven sequence. First, stabilize operations—ensure mines keep producing during transition. Second, capture quick wins—eliminate obvious duplications and inefficiencies. Third, optimize the portfolio—identify which assets to keep, improve, or divest. This disciplined approach ensures value capture while minimizing disruption.

Cultural integration receives equal emphasis with operational integration. Newmont learned that imposing a single culture destroys value. Instead, the company preserves beneficial local practices while establishing common standards for safety, environmental management, and financial controls. This balance between autonomy and alignment enables rapid integration without organizational trauma.

When Cooperation Beats Competition

The Nevada joint venture represents a profound lesson: sometimes the best strategy isn't winning but transforming the game. For decades, Barrick and Newmont competed fiercely in Nevada, duplicating infrastructure and bidding up costs. The JV ended this value-destroying competition, creating billions in shareholder value for both companies.

Cooperation works when structural factors align interests. In Nevada, geology created interdependence—ore bodies don't respect property lines. Operations created inefficiencies—separate mills processing identical ore. Competition created waste—duplicate teams, redundant infrastructure, bidding wars for talent. The JV aligned interests around value creation rather than value division.

The lesson extends beyond mining. In industries with high fixed costs, long development cycles, and interdependent operations, cooperation can create more value than competition. But cooperation requires overcoming profound psychological barriers—admitting you can't do everything yourself, sharing credit for success, trusting former rivals.

Newmont's approach to cooperation is ruthlessly pragmatic. The company partners when partnership creates value and competes when competition drives performance. This flexibility—knowing when to fight and when to embrace—represents strategic sophistication that transcends traditional competitive doctrine.

Building a Sustainable Mining Company in the 21st Century

Sustainability in mining seems oxymoronic—how can extracting non-renewable resources be sustainable? Newmont's answer reframes the question: sustainability isn't about the resources but about the business model, the communities impacted, and the value created.

Building a sustainable mining company starts with portfolio management. Newmont maintains a 20-year reserve life, ensuring the company's future isn't mortgaged to current production. Continuous exploration and strategic acquisition replenish depleted reserves. This self-renewing portfolio creates institutional permanence despite finite individual assets.

Environmental sustainability requires accepting that every mine has environmental impact while minimizing that impact through technology and investment. Newmont's water recycling systems, renewable energy projects, and progressive reclamation transform environmental management from cost to investment. The company learned that environmental excellence creates option value—the ability to develop future projects depends on past environmental performance.

Social sustainability means creating value for all stakeholders, not just shareholders. Newmont's community development programs, local employment priorities, and economic linkage programs ensure mining creates lasting benefits. The company measures success not just in ounces produced but in communities transformed.

The ultimate lesson is that sustainable mining requires systems thinking. Every decision—from exploration to closure—affects long-term value creation. Short-term optimization that compromises long-term sustainability destroys value. This holistic perspective, viewing mining as part of broader economic and social systems, enables true sustainability.

These lessons—patient capital, cyclical resilience, operational excellence, strategic cooperation, and sustainable development—constitute the "Newmont Way." They're not revolutionary insights but evolutionary wisdom, accumulated over a century of success and failure. For investors and operators, they offer a roadmap for creating value in capital-intensive, cyclical industries where time horizons span decades and mistakes prove costly.

XII. Epilogue & Recent Developments

Standing at the observation deck of the Boddington mine in Western Australia, you can watch 100-ton haul trucks spiral down into one of the Southern Hemisphere's largest open pits. The scale defies comprehension—the pit could swallow multiple football stadiums. Yet from Newmont's Denver headquarters, executives can monitor every truck, every crusher, every ounce produced in real-time. This marriage of massive physical operations with digital oversight represents what Newmont has become: a 21st-century mining company built on 20th-century assets with 19th-century roots. The current market position tells a story of successful transformation. Newmont Corporation maintained its position as the world's leading gold producer in 2024. The Company delivered strong production results while executing a strategic transformation. By divesting non-core assets and consolidating its Tier 1 portfolio, Newmont strengthened its operational and financial foundation. The company has evolved from crisis survivor to industry consolidator to value creator, all while maintaining the operational discipline that defines its culture.

The Company reported total gold production of 6.8 million attributable ounces for the year. Of this, 5.7 million ounces came from its refreshed Tier 1 portfolio. During the December 2024 quarter, Newmont produced 1.9 million attributable ounces, underscoring its operational efficiency and commitment to high-value assets. These aren't just production numbers—they represent the successful integration of three major acquisitions and the optimization of a global portfolio.

Financial performance reflects operational success. Newmont produced nearly 1.7 million ounces of gold and 430,000 gold equivalent ounces from other metals in Q3 2024. The company generated $1.6 billion in cash flow from operations and $760 million in free cash flow during the quarter. The ability to generate substantial free cash flow even while integrating major acquisitions demonstrates the quality of the asset base and the effectiveness of management.

Looking forward, the future of gold mining will be defined by three forces: technology, sustainability, and geopolitics. On technology, Newmont continues pushing boundaries. Artificial intelligence now predicts equipment failures before they occur. Automated drilling rigs operate with precision impossible for human operators. Blockchain technology tracks gold from mine to market, ensuring ethical sourcing. These aren't futuristic concepts—they're operational realities at Newmont mines today.

Sustainability has moved from corporate social responsibility to core strategy. The gold market remained strong in 2024, supported by global economic conditions and rising demand. Gold prices averaged around $1,940 per ounce, reflecting investor confidence in the metal as a hedge against inflation and geopolitical risks. Central banks continued to increase their gold reserves, further driving demand. In this environment, Newmont's ESG leadership becomes a competitive advantage, attracting capital and talent while competitors struggle with legacy issues.

The geopolitical landscape continues evolving. Resource nationalism is rising, but so is recognition that mining investment drives economic development. Newmont's approach—deep community engagement, transparent benefit sharing, local capacity building—has become the template for responsible mining. The company that started as a vehicle for American capital in foreign mines has become a truly global enterprise, with stakeholders on every continent.

What would the next chapter look like? The era of mega-mergers has likely ended—Newmont already owns the best assets, and regulatory scrutiny of further consolidation would be intense. Instead, the future lies in optimization: using technology to extract more value from existing assets, developing next-generation processing techniques, and perhaps most importantly, preparing for the post-carbon economy where copper becomes as important as gold.

The company also faces generational transition. The mining workforce is aging, and attracting young talent to an industry often seen as environmentally destructive and technologically backward presents challenges. Newmont's response—emphasizing technology, sustainability, and purpose-driven work—aims to reposition mining as essential to the energy transition and technological progress.

Newmont president and chief executive officer Tom Palmer described 2024 as a "transformational" year. The Company focused on integrating the Newcrest portfolio, divesting non-core assets, and transitioning to a stable operational platform. It aims to maximise the potential of its Tier 1 portfolio by optimising operational efficiency and financial returns. Palmer's vision extends beyond just operational excellence to positioning Newmont as the essential precious metals company for the 21st century.

For investors, Newmont represents a unique proposition: exposure to monetary gold, industrial copper, and operational excellence, all wrapped in an ESG-compliant package. The company trades at a premium to net asset value, reflecting market confidence in management's ability to create value beyond just mining metal. This premium is earned through consistent execution, disciplined capital allocation, and strategic vision.

The key takeaways for both investors and operators are clear. First, in cyclical industries, survival requires thinking beyond the current cycle. Second, operational excellence trumps financial engineering every time. Third, the best M&A creates value for all stakeholders, not just the acquirer. Fourth, sustainability isn't a cost but an investment in long-term value creation. Finally, even century-old industries can reinvent themselves through technology and innovation.

As gold prices hover near historic highs and copper demand accelerates with the energy transition, Newmont stands uniquely positioned. The company that Colonel Thompson founded to invest in mining has become mining's premier operator. The financial holding company has become an operational powerhouse. The American upstart has become the global leader.

Yet challenges remain real and substantial. Labor cost inflation is a significant challenge, with an industry-standard labor inflation rate of about 4% for 2024. Climate change threatens water supplies at desert operations. Ore grades continue declining globally. Young people increasingly question mining's social license. These aren't problems that can be solved through acquisition or financial engineering—they require fundamental innovation in how mining operates.

Newmont's response to these challenges will define not just its future but the future of gold mining itself. The company that survived the Depression, defeated corporate raiders, and consolidated a fragmented industry now faces its next test: proving that large-scale mining can be sustainable, profitable, and essential to human progress. Based on a century of adaptation and evolution, betting against Newmont seems unwise.

The Newmont story ultimately transcends mining. It's about American capitalism's evolution from financial speculation to operational excellence. It's about globalization's promise and perils. It's about how traditional industries can reinvent themselves for new centuries. Most fundamentally, it's about value—how it's created, captured, and distributed across stakeholders and through time.

From Thompson's vision in 1916 to Palmer's leadership today, from a holding company named after two states to the world's premier gold miner, from surviving hostile takeovers to orchestrating industry consolidation—Newmont's journey mirrors American business history itself. The gold standard isn't just what Newmont mines; it's what Newmont has become.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube