Nordson Corporation: The Invisible Sticky Compounder

I. Introduction & Episode Roadmap

Somewhere in the last twenty-four hours, you almost certainly held a Nordson-made product in your hands and never knew it. The tight, tamper-proof seal on your cereal box was laid down by a hot-melt adhesive gun that fired a bead of molten glue in a few thousandths of a second. The microchip inside your phone was joined to its circuit board by solder paste squeezed through a dispensing nozzle finer than a human hair, then photographed by a 3D inspection sensor hunting for defects invisible to the eye. The catheter a surgeon threaded through a patient's artery this morning was extruded on tooling designed to hold tolerances measured in microns. Even the crop-protection chemical misted onto a field of strawberries flowed through a spray computer and a bank of precision valves. None of it carries a Nordson logo a consumer would ever see, yet a roughly $16 billion company headquartered in Westlake, Ohio sits quietly inside all of it.1

Consider how strange that is. Nordson makes almost nothing a consumer would recognize, advertises to essentially no one outside its industrial customers, and yet has embedded itself so thoroughly into the machinery of modern manufacturing that its equipment touches products across food, packaging, electronics, medical devices, and agriculture. It is one of those rare companies that is simultaneously everywhere and invisible — a supplier to the suppliers, sitting one or two layers behind the brands you actually buy. That invisibility is not an accident of marketing; it is the natural state of a company whose value lies in being a mission-critical component of someone else's process rather than a product in its own right.

Here is the idea that makes Nordson worth a long, careful look: it is one of the purest expressions of the industrial razor-and-blade model in existence. A Nordson dispensing head might cost a few thousand dollars and represent well under one percent of the capital in a factory. But that head governs the throughput of an entire production line running hundreds of units a minute. If it clogs, drips, or fails, the line stops, and a stopped line can burn tens of thousands of dollars an hour. That brutal asymmetry — a cheap component whose failure is catastrophically expensive — is the source of Nordson's pricing power, its customer stickiness, and the recurring stream of parts and consumables that management says now make up roughly 60% of the company's sales.2

The financial residue of that model is a compounding record most companies can only envy. In fiscal 2025 the Nordson board raised its dividend for the 62nd consecutive year — an unbroken streak dating back to 1963 that places it in the tiny club of "Dividend Kings."3 The company converts far more than 100% of its net income into free cash flow, ran segment EBITDA margins as high as 37% in its best businesses, and generated record free cash flow of $661 million in fiscal 2025.4 Yet — and this is the tension worth holding onto — the same period saw organic growth stall into the low single digits, three of the largest acquisitions in company history land in quick succession, and a debt load balloon on a balance sheet that had been famously pristine. A compounder does not stop being interesting when it starts spending; it becomes more interesting, because the question shifts from "is the machine good?" to "is management still disciplined enough to deserve it?"

It is worth naming the paradox precisely, because it is what separates Nordson from the average industrial. Most capital-goods companies live and die by the order book — they sell a big machine, book the revenue, and then pray the customer comes back in seven years to replace it. Their income statements heave with the economy. Nordson looks different under the hood: a large share of what it sells is not the machine at all but the stream of parts and materials the machine devours in normal operation, which means a meaningful slice of revenue arrives whether or not a single new system is ordered that quarter. That is the difference between selling printers and selling ink, between selling the razor and selling the blade — and it is why a company most investors have never heard of has quietly out-compounded far more famous names for decades. It is also why the stock rarely looks cheap: the market has long understood that this is a quality business, and quality businesses are priced accordingly.

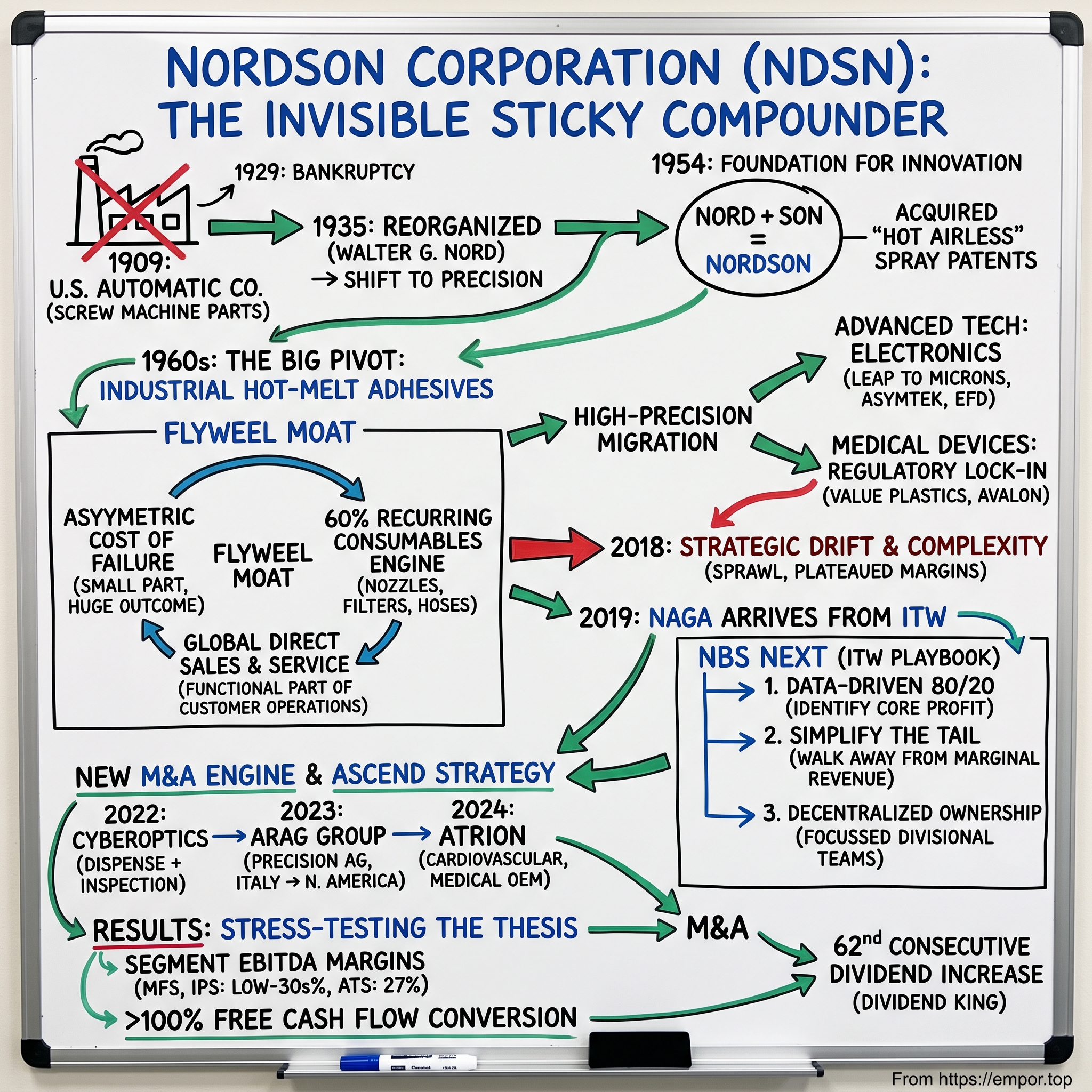

This is the story we will tell. First, the Ohio origin: how a bankrupt screw-machine shop became the inventor of industrial hot-melt adhesives. Then the anatomy of the moat itself — the cost-of-failure asymmetry, the consumables engine, and the direct-sales network that competitors have never managed to copy at scale. We will follow Nordson's high-precision migration into electronics and medical devices, the strategic drift that crept in by 2018, and the 2019 arrival of Sundaram "Naga" Nagarajan, a 23-year veteran of Illinois Tool Works who imported the famous "80/20" operating discipline under the banner of NBS Next. We will benchmark the new, larger M&A engine — CyberOptics, ARAG, and Atrion — and stress-test whether the deals were smart capital allocation or expensive cover for a slowing core. Then a segment-level deep dive, the durable lessons, the bull-and-bear war-game, and the handful of numbers that actually tell you whether the story is still on track. Throughout, the posture is independent: management's claims are treated as claims, tested against filings, earnings calls, and the arithmetic of the balance sheet, not accepted because they are confidently made. Let's start in Amherst, Ohio, with a company that was already bankrupt before the Nord family ever touched it.

II. The Ohio Roots: Screws, Paint, and the Invention of Hot-Melt (1909–1960s)

The company that became Nordson began its life failing at something else entirely. The U.S. Automatic Company was founded in 1909 to make screw-machine parts for the young automobile industry — the small, precisely turned metal components that the exploding car business consumed by the millions.5 It was a decent enough trade until the economy turned, and in 1929 the firm went bankrupt. Into that wreckage stepped Walter G. Nord, a businessman who acquired control and, in 1935, reorganized it as the U.S. Automatic Corporation, shifting its emphasis toward lower-volume, higher-precision parts.5 It was an unglamorous pivot, but it planted a cultural seed that would matter for the next ninety years: a shop-floor obsession with holding close tolerances, with making a part exactly right rather than merely cheap. When World War II arrived, that capability found a ready customer in the U.S. military, and the company scaled up producing precision components for the war effort.5

But a job shop, however skilled, lives a hard life. It makes what its customers ask, on its customers' terms, at margins its customers dictate, and when orders soften the machines go quiet. There is no repeat revenue baked into a run of custom screws; each order is won fresh, priced against every other shop that owns a lathe. Walter's sons, Eric and Evan Nord, lived that reality on the factory floor and understood the trap intimately. Eric in particular — an engineer's engineer who would go on to lead the technical work that defined the company — grasped that the way out was not to run the machines better than the next shop, but to own something the next shop could not make at all. What they wanted was the opposite of a job shop: a proprietary, branded, patented product that the company itself owned and could sell on its own terms. The hunt for that product is the real origin of Nordson, and it is a hunt that would repeat, in different forms, for the rest of the company's life.

They found it in 1954, and it had nothing to do with screws. The brothers acquired patents covering a "hot airless" method of spraying paint and industrial coatings — a technique that heated the coating so it could be atomized and sprayed without the usual blast of compressed air.5 The advantage was less waste and a cleaner, more controlled finish, and the Nords launched it as the Nordson Division of U.S. Automatic — a name stitched together from "Nord" and "son."1 For the first time, the company had something that was theirs.

The airless spray business was a success, but it was the byproduct of that expertise — a deep, hard-won understanding of how to heat, melt, and precisely apply fluids — that turned into the real franchise. In the mid-1960s, Nordson's mastery of heated-coating technology led it into thermoplastic adhesives, the "hot melts" that were about to remake manufacturing.5 Consider the problem hot melt solved. Packaging lines were speeding up, but they were still gluing boxes shut with slow-drying, water-based adhesives, or stapling them, or relying on manual labor — all of it a bottleneck. A hot-melt adhesive is a solid at room temperature; heat it and it flows; let it cool for a fraction of a second and it sets into a strong bond almost instantly. That instant grab was exactly what a high-speed automated line needed. But applying it was genuinely hard: you had to melt the adhesive, keep it molten in heated hoses without letting it char, and fire it through a nozzle thousands of times a minute without clogging, dripping, or stringing. Eric Nord's engineers built the melting tanks, the heated hoses, and the automated applicator guns that made it reliable — and in doing so, they didn't just sell a product, they created a category.

The strategic genius of that move was not obvious at the time, and it is worth dwelling on because it is the template for everything Nordson later became. By solving the application problem for hot melt, Nordson made itself the indispensable partner of every manufacturer that wanted to switch to the new adhesive — and once a plant had standardized its high-speed line around a Nordson applicator, the nozzles, filters, hoses, and heating elements it burned through became a recurring order that flowed back to Cleveland year after year. The company had accidentally discovered the business model it would spend the next six decades refining: sell a precisely engineered system that becomes woven into a customer's production process, and then sell, in perpetuity, the consumable parts that keep it running. It was the antithesis of the screw shop. Where the screw shop had to re-win every order, the hot-melt franchise re-won customers automatically, through the simple physics of wear.

There is a cultural note worth adding here, because it explains the company's temperament. The Nord family were serious philanthropists — the Nord Family Foundation would become a significant force in northern Ohio — and they built a company with a long-term, low-drama, engineering-led ethos that persists in Nordson's disclosure style and capital discipline to this day. This is not a company that chased fashion; it is one that found a very good business model early and had the patience to keep compounding it. That patience is the connective tissue between the 1966 hot-melt applicator and the 2024 acquisition of a cardiovascular-device maker.

In 1966, the transformation was formalized: the entire U.S. Automatic operation was merged into the subsidiary, and Nordson Corporation as we know it was born.5 The screw-machine shop was gone. In its place stood a company that had learned the single most important lesson of its history — that the durable money is not in the machine you sell once, but in the precisely engineered, consumable-hungry system a customer can never quite stop buying from. Understanding why that is true, and why it has proven so hard to attack, is the whole game.

III. Inside the Moat: The Anatomy of the Razor-and-Blade Flywheel

Picture a beverage plant at three in the morning. A filling and packaging line is running flat out — cartons streaming past at a rate the human eye can barely track, each one sealed by a Nordson adhesive gun firing a precise bead of hot glue. Now picture that gun failing. Not catastrophically, just a partial clog that starts laying down a slightly imperfect bead. Cartons begin to fail their seals downstream. Within minutes the line supervisor faces a choice no one envies: keep running and ship defective product, or stop the line. Either way, the clock is now running against thousands of dollars an hour in lost throughput, spoiled product, and idle labor. In that moment, the price of the Nordson part is the last thing on anyone's mind.

This is the cost-of-failure asymmetry, and it is the beating heart of Nordson's business. The dispensing equipment is a rounding error in the plant's capital budget, yet it sits directly astride the flow of everything the plant produces. When the thing that governs 100% of your output costs less than 1% of your investment, you do not shop it on price, and you do not experiment with an unproven alternative to save a few dollars. You buy the equipment you trust, and you keep buying whatever it needs to keep running. For a plant manager, choosing a cheaper, unproven dispensing system to shave costs is a career-defining gamble with almost no upside and a catastrophic downside — which is precisely why so few of them take it.

That psychology feeds the second, more important engine: consumables. A hot-melt system runs hot — often well above 300°F — and under pressure, and its wear parts live short, violent lives. Nozzles erode. Filters foul. Heating elements degrade. Hoses and seals give out. All of it must be replaced on a schedule, and the customer buys those replacements from the company that built the system, because compatibility and reliability are non-negotiable when a line stoppage is the alternative. On the fiscal 2026 second-quarter earnings call, Nordson's CFO Daniel Hopgood put a number on it: roughly 60% of the company's business is consumables and single-use products, the kind that turn over continuously regardless of whether customers are buying new equipment.2 In the flagship Industrial Precision Solutions segment, the split between new systems and recurring parts runs around 60/40.2 This is what analysts mean when they call Nordson a razor-and-blade business — except here the blades are consumed under heat and pressure, and there is no third-party razor that fits.

The third pillar is distribution, and it is the one competitors find hardest to replicate. Most industrial-equipment makers sell through regional distributors, which is cheaper to run but puts a layer of margin and a wall of distance between maker and user. Nordson went the other way, building an expensive, global, direct sales-and-service network. When a dispensing head goes down in a plant in Lyon or Busan, a Nordson field engineer — someone who already knows that plant's line — can be on site within hours. That model costs more to operate, but it does two things no distributor network can. It makes Nordson's people a functional part of the customer's operations, and it captures the full margin and the full flow of information about what the customer needs next. On the Q2 FY2026 call, management returned again and again to the phrase "close to the customer" as the organizing idea of the whole company.2

It is worth pausing on the economics of that service network, because they are more elegant than they first appear. A field-service engineer is a fixed cost — a salary Nordson pays whether or not the phone rings. In a distributor model, that cost is spread thin and the relationship is transactional. In Nordson's model, that same engineer is a walking annuity: every visit is an opportunity to diagnose wear, recommend the correct replacement part, spot the next upgrade, and reinforce the customer's sense that no one else understands their line as well. The cost is real and it does depress the reported operating margin relative to an asset-light peer — but it purchases something an asset-light peer cannot buy at any price: presence. The economics only work at scale, which is itself a barrier. A new entrant would have to fund a global service force before it had the installed base to justify it — carrying years of losses to build a network that Nordson already amortizes across tens of thousands of installations. That chicken-and-egg problem is why, decades on, no challenger has replicated the model wholesale.

Myth versus reality. The consensus story treats Nordson as a boring "picks-and-shovels" industrial whose moat is simply "good engineering." That undersells it in one direction and oversells it in another. It undersells the moat because good engineering is copyable; what is not copyable is the combination of engineered consumables, regulatory or process lock-in, and direct service that makes a Nordson component nearly impossible to displace mid-life. But it also oversells the moat in the sense that skeptics sometimes imagine Nordson can grow at will — it cannot. The company is still bolted to the capital-spending and volume cycles of its customers. A moat protects share and margin; it does not manufacture demand. When a customer's factory slows, Nordson's consumables slow with it. Holding both of those truths at once — durable competitive position, cyclical demand — is the key to valuing the business honestly.

Run these mechanisms through Hamilton Helmer's 7 Powers framework and two powers stand out clearly. The first is switching costs. A Nordson system is not a bolt-on appliance; it is integrated into the customer's production-line layout and often wired into the proprietary controls that sequence the whole line. Ripping it out to install a rival's system means re-engineering the line, re-validating the process, and risking downtime — a cost and risk almost always larger than any savings on offer. The second is process power (sometimes called cornered resource in adjacent forms): decades of accumulated, hard-to-copy know-how in fluid dynamics, thermal control, and precision extrusion, embodied in both the products and the engineers who deploy them. A well-capitalized competitor can copy a nozzle; copying forty years of application expertise and a global service footprint at once is a different order of problem. A useful piece of live evidence for how deep the lock-in runs came on the Q2 FY2026 call, when management noted it had cut lead times on some systems from 16–18 weeks to under 7–8, and could compress them to four when a customer demanded it — the kind of responsiveness that only a company embedded inside its customers' planning can offer, and exactly the thing a distributor-based rival cannot match.2

None of this makes the moat invulnerable — it does not protect Nordson from the cyclicality of its end markets, and it does not stop a determined rival from competing hard in a specific niche, as we will see. But it does explain the single most important fact about the business: its revenue does not so much get sold each year as it recurs. That durability is exactly what let Nordson spend the 1990s and 2000s reaching for far more demanding, and far more lucrative, applications than gluing cereal boxes.

IV. The High-Tech and Medical Pivot (1990s–2018)

By the 1990s, the world Nordson served was shrinking — literally. Consumer electronics were racing toward miniaturization, and the fluids that held them together had to be deposited in droplets smaller than a grain of sand, in exactly the right place, thousands of times a minute, with zero tolerance for error. A dab of solder paste misplaced by a fraction of a millimeter could short a circuit board; too little underfill adhesive beneath a chip could let it crack under thermal stress. Human hands and crude pneumatic valves simply could not operate at that scale. This was a dispensing problem — Nordson's native language — but spoken at a level of precision that dwarfed anything in a packaging plant.

So Nordson bought its way to the frontier. Its acquisition of Asymtek, a specialist in automated fluid dispensing for electronics assembly, made it a gold standard for depositing microscopic, precisely metered drops of adhesive, solder paste, and protective coating onto circuit boards. It layered on EFD, a leader in precision fluid-dispensing valves and syringes, extending the same competency into a vast range of small-scale industrial and electronics applications. The strategic logic was elegant: the same core competency that laid down a glue bead on a carton, refined by orders of magnitude, could serve the semiconductor and electronics industry — a market growing far faster, and paying far more for precision, than industrial packaging ever would. This became the seed of what is today the Advanced Technology Solutions segment.

The technical leap here is easy to underestimate. Dispensing a controlled bead of hot glue onto a cardboard box is hard; dispensing a repeatable droplet of underfill adhesive a few thousandths of an inch across, into the gap beneath a flip-chip, without voids or overflow, tens of thousands of times an hour, is a different universe of difficulty. Get it wrong and the chip fails a thermal-cycling test months later in a customer's phone. Nordson's willingness to chase that difficulty — to compete on precision rather than price — is precisely what kept it out of the commoditized middle of the market where margins go to die. The company was, in effect, running the same play it ran with hot melt in the 1960s: find the hardest version of the fluid-application problem, solve it, and let the difficulty itself be the moat.

The second, and in hindsight shrewder, migration was into medical devices — and the reasoning behind it reveals how Nordson's leadership actually thought about the world. Look past the surface differences between an industrial glue gun and a heart catheter and the underlying economics are nearly identical. Both demand extreme precision. Both live under strict quality regimes — regulatory in medical, reliability-driven in industrial. In both, the component itself is cheap relative to the cost of its failure, except in medicine the "cost of failure" can be a patient's life, which makes the barriers to switching suppliers even higher. A medical component that has been designed into an FDA-approved device and validated through clinical use cannot be swapped for a cheaper alternative without re-opening the entire regulatory approval — a process so costly and slow that, once designed in, a supplier is effectively locked in for the life of the product. That is switching cost expressed as regulation, and it is arguably the most durable form of the moat Nordson had already built in industry.

Through a patient string of bolt-on acquisitions — including the plastic-component maker Value Plastics and the cardiac and catheter specialist Avalon Laboratories — Nordson assembled a medical platform supplying high-tolerance components, tubing, catheters, and fluid-management parts to the device OEMs who then designed them into approved procedures. It was a quieter business than electronics, less cyclical, and structurally more profitable, because the regulatory lock-in did the pricing work that competition erodes elsewhere.

By 2018, though, the strategy of "buy precision niches and add them to the pile" had produced a subtler problem — the kind of problem that only afflicts companies that have been successful for a long time. Nordson had become a federation of acquired businesses, each with its own plants, product lines, engineering culture, and habits. Complexity had accumulated the way it always does in acquisitive companies: a long tail of low-volume, high-touch custom SKUs that consumed engineering and factory capacity while contributing little profit; plants configured for yesterday's product mix; and a portfolio managed more as a collection of divisions than as a single strategic whole. Every acquisition had been individually sensible, yet the aggregate had grown unwieldy — the classic "diworsification" risk, where breadth quietly erodes the returns that made the core great.

The symptoms showed up where they always do: in the margin trend. The moat was intact and the cash still flowed, but operating margins had begun to plateau, and the sprawl was starting to cost more than it returned. Management attention was spread across too many small things; the vital few products that generated most of the profit were not getting a proportionate share of resources, while the marginal many soaked up factory changeovers and working capital. This is a subtle failure mode, because nothing is visibly broken — the company is profitable, the customers are happy, the dividend keeps rising. It is precisely the kind of slow drift that a founder-led culture, comfortable and cash-rich, can fail to notice for years. Nordson did not need a new market or a new product. It needed an operating system, and a leader ruthless enough to impose it. In 2019, it hired someone who had spent his entire career building one.

V. Naga's Arrival & The ITW Playbook: NBS Next

When Nordson named Sundaram Nagarajan its president and chief executive effective August 1, 2019, the appointment read, on paper, like a straightforward succession — he took over from Michael Hilton, who had run the company since 2010.6 But the choice of who signaled a deliberate strategic decision by the board. Nagarajan — universally known as "Naga" — arrived from Illinois Tool Works, where he had spent 23 years, most recently as executive vice president of ITW's $3-billion-plus Automotive OEM segment.7 ITW is not just any industrial conglomerate. It is the company that turned a single management philosophy — the "80/20" principle — into one of the most admired decentralized operating models in American manufacturing. Hiring Naga was, in effect, hiring the playbook.

His own path helps explain how he thinks. Nagarajan earned a bachelor's degree from South Gujarat University in India, an MBA from Wright State University, and both a master's and a doctorate in materials science from Auburn University.7 He began his career in 1991 at Hobart Brothers designing welding consumables — quite literally a maker of the "blades" in someone else's razor-and-blade business — before Hobart was absorbed into ITW and he spent two decades climbing through its welding and automotive businesses.7 He is an engineer by training and a disciple of operating discipline by formation, and that combination is the through-line of everything he has done at Nordson.

To appreciate why the board reached for an ITW alumnus specifically, you have to understand what ITW is famous for. Under a lineage of leaders stretching back to the "80/20" evangelist teachings of the late twentieth century, ITW turned a simple statistical observation into a company-wide religion and one of the best long-run total-return records in the industrial sector. The idea is deceptively plain, and it is the philosophy Nagarajan imported wholesale.

That philosophy rests on an uncomfortable observation: in most industrial businesses, roughly 80% of the profit comes from roughly 20% of the customers and products. The other 80% — the long tail of marginal accounts and niche SKUs — does not merely earn less; it actively destroys value by consuming a disproportionate share of engineering time, factory changeovers, inventory, and management attention. The tail feels like revenue but functions like a tax. The genuinely hard part is not seeing this — plenty of managers can draw the Pareto chart — but having the nerve to act on it, because acting means voluntarily shrinking parts of the business, telling some customers their orders are no longer worth serving on the old terms, and absorbing the near-term revenue hit in exchange for a structurally healthier company. That takes a leader with the credibility and the stomach to trade visible short-term sales for invisible long-term returns. It is culturally the opposite of the "grow the top line at any cost" reflex.

Nagarajan branded Nordson's version of this NBS Next — the Nordson Business System Next — and made it the operating core of a multi-year plan he called the Ascend strategy.2 In practice it works in three moves. First, identify the core: use data to isolate the highest-volume, highest-margin products and customers, and pour disproportionate R&D, sales, and service resources into them. Second, simplify the tail: re-price, outsource, or discontinue the low-margin custom work and small high-touch accounts that drag down factory efficiency — a deliberate willingness to walk away from revenue that does not pay its way. Third, push ownership down: decentralize decisions to focused divisional teams and hold them accountable for their own growth and margins, rather than running everything through a corporate center. It is less a restructuring than a re-wiring of incentives and attention.

Did it work? The evidence, on the operating line, is real. By fiscal 2025 Nordson was running consolidated EBITDA margins in the low-30s percent, with its two best segments — Industrial Precision and Medical — throwing off segment EBITDA margins around 37%.4 Free-cash-flow conversion has run above 100% of net income for years, hitting 136% in fiscal 2025 and staying above 100% for four consecutive quarters through the first half of fiscal 2026.42 On the Q2 FY2026 call, management pointed to the Advanced Technology segment — historically the most volatile and lowest-margin of the three — reaching a record 27% EBITDA margin, and explicitly credited "the sustainable operational and footprint changes we've made within the segment in prior years, guided by the NBS Next growth framework."2 That is the playbook doing exactly what it promised: taking the messiest, most cyclical business and making it structurally more profitable through the cycle.

But an independent reading requires a caveat management does not volunteer. Margin expansion driven by pruning complexity is powerful, and it is also finite — you can only cut the unprofitable tail once. The harder question, which the next chapter forces, is what happens when the easy operating gains are banked and growth has to come from somewhere. Nordson's answer was to go shopping, at a scale it had never attempted before.

A word on management credibility, because it is the variable that ultimately decides whether NBS Next is a durable system or a slogan. The evidence across earnings calls from fiscal 2024 through the first half of fiscal 2026 is reasonably consistent: management uses the same vocabulary ("close to the customer," "NBS Next growth framework," "Ascend strategy") quarter after quarter, ties specific operating outcomes to specific framework actions, and — importantly — has been willing to name misses concretely. On the Q2 FY2026 call, for instance, the CFO did not paper over a margin dip in the medical segment; he attributed it precisely to a regulatorily required product changeover and explained how it would reverse, the kind of specific, falsifiable disclosure that is a positive credibility signal.2 Consistency of narrative and willingness to explain misses are not proof of a great business, but they are the behavioral markers of a management team that is describing reality rather than selling one — and they are worth more than any single quarter's numbers.

On alignment, the structure is at least pointed in the right direction. Nagarajan's incentive pay is tied to organic growth, EBITDA margin, and return on invested capital — a deliberate design meant to discourage empire-building and "growth for the sake of growth," since acquisitions that dilute returns on capital would work against his own compensation.8 He is also subject to a stock-ownership requirement set at a multiple of his base salary, part of a broader governance framework meant to keep management's net worth moving with shareholders' rather than with the size of the enterprise.8 The skeptic's caveat is fair, though: ROIC-linked pay is common, and it did not stop the company from paying full multiples for its recent acquisitions, because incentive plans typically measure ROIC on a lag and against adjustable targets. Whether those incentives actually held under the pressure of a billion-dollar deal is a question we can now test directly.

VI. The New M&A Engine: CyberOptics, ARAG, and Atrion

For most of its history, Nordson did M&A the way a careful gardener prunes: small bolt-ons, quietly absorbed, rarely large enough to move the story. Under the Ascend strategy, that changed. Confident that NBS Next gave it a repeatable machine for wringing margin out of acquired assets, Nordson began writing much bigger checks to buy dominance in high-barrier niches. Three deals in three years redefined the company's scale — and its balance sheet.

The first was CyberOptics, acquired in late 2022 for approximately $380 million net of cash.910 The strategic logic was almost too neat. Nordson already dispensed the microscopic drops of solder and adhesive that hold electronics together; CyberOptics made the high-precision 3D optical sensors that inspect that work, using a proprietary technique — Multi-Reflection Suppression, or MRS — designed to see past the optical distortions that plague measurement of shiny, contoured solder joints. Buying it let Nordson close the loop: dispense the material, then verify it in real time on the same line, a genuinely more valuable proposition to a semiconductor-packaging customer than either capability alone. The price was rich — by various estimates well into the high-teens as a multiple of trailing EBITDA — and that premium is the point of tension. Paying up for a small, fast-growing technology asset only makes sense if you can either grow it much faster or run it much leaner than the seller could. Nordson was betting NBS Next could do both.

The second deal was the boldest departure. In June 2023 Nordson agreed to acquire the Italian firm ARAG Group at an enterprise value of roughly €960 million — approaching a billion dollars, and by a wide margin the largest acquisition in its history at the time.11 ARAG is a global leader in precision-agriculture components: the valves, nozzles, flow controls, and spray computers that let a farmer apply crop chemicals with far greater accuracy. The industrial logic mapped cleanly onto Nordson's DNA — this was, at its core, precision fluid dispensing, just aimed at a field instead of a circuit board — and it rode a real secular tailwind, as agriculture moves toward "precision" application to cut chemical use, control cost, and meet tightening environmental rules. But it also took Nordson into an entirely new end market with its own weather-driven cyclicality and its own competitors, funded with new debt. Management moved quickly to apply the playbook, optimizing ARAG's European manufacturing footprint and using it as a platform to push into North America — a push it reinforced in fiscal 2026 with the small, $13-million bolt-on of Kansas-based CapstanAG, bought at a disciplined 9 times adjusted EBITDA, precisely the kind of price the earlier deals were not.2

The third deal put the discipline question most sharply. In May 2024 Nordson agreed to acquire Atrion Corporation, a maker of proprietary infusion-fluid-delivery and interventional cardiovascular products, for about $815 million; the deal closed that August.1213 Atrion slotted logically into the Medical and Fluid Solutions segment, and the strategic case was coherent: take Atrion's differentiated, regulatory-protected products and run them through Nordson's global medical-OEM sales force and its NBS Next margin toolkit. But Atrion was a competitive, high-priced auction, and skeptics were right to flag the multiple paid. The honest way to frame Nordson's answer — which is really management's answer — is that it is a thesis, not yet a result: the deal is justified if, and only if, Nordson can accelerate Atrion's organic growth and expand its margins by more than the premium implied. That is a claim about future execution, and it should be judged against outcomes, not press releases.

There is a quieter counterpoint to the "Nordson only buys, never sells" caricature, and it matters for judging capital discipline. Alongside the big acquisitions, the company also pruned — divesting a lower-margin medical contract-manufacturing business in the fourth quarter of fiscal 2025, a move that trimmed reported revenue but improved the mix and margin of the Medical and Fluid Solutions segment.2 That willingness to shrink a business that no longer fit the NBS Next profile is a small but genuine signal that the pruning discipline is not just rhetoric applied to acquired assets — it is applied to the legacy portfolio too. A management team that only ever adds is running an empire; one that adds and subtracts is running a portfolio. Nordson, at least on this evidence, is doing the latter.

Step back and the pattern is clear. In roughly a year, Nordson deployed on the order of $1.8 billion on ARAG and Atrion alone, transforming a company famous for a fortress balance sheet into one carrying real leverage. The scale of the shift deserves emphasis: this is a company that historically ran with almost no net debt, and it chose — deliberately, at a moment of relatively high interest rates — to lever up to buy growth and diversification. That is either conviction or overreach, and the two are indistinguishable at the moment of purchase; only time and returns tell them apart. The bull reading is that a proven operator bought three defensible franchises at the moment its operating system was primed to improve them, funding the deals with a balance sheet that had spent decades earning the right to be used. The bear reading is that a company facing slowing organic growth in its legacy businesses reached for acquisitions to keep the top line moving — and paid up, near a cycle peak in private-market valuations, to do it. Both readings are alive, and the way to adjudicate between them is to look, segment by segment, at where the money is actually made.

VII. Segment-Level Deep-Dive: Where the Money is Made

Nordson reports as three businesses, and the fastest way to understand the company is to see that they are not equally good — they differ in margin, in cyclicality, and in competitive exposure, and the mix is the story. Together they generated fiscal 2025 revenue of roughly $2.8 billion, up about 4% on the year, a record but a modest one that captures the central tension of the whole thesis: excellent profitability, unspectacular growth.4

Industrial Precision Solutions (IPS) is the cash engine and the largest of the three, home to the original adhesive-dispensing franchise, packaging, nonwovens, industrial coatings, polymer processing, and now the ARAG precision-agriculture business. In fiscal 2025 it produced segment EBITDA of about $494 million at a 37.1% margin — best-in-class economics that reflect the deepest version of Nordson's moat, where the installed base is oldest and the consumables flywheel spins fastest.14 In the fiscal 2026 second quarter it delivered record segment sales of $350 million at a 35% EBITDA margin, with management noting that the systems-versus-parts mix held steady near 60/40 — a reminder that the recurring engine, not big new-equipment orders, carries this business.2 Its rivals are focused specialists — ITW's own Dynatec adhesive-dispensing unit and Valco Melton chief among them — and Nordson's edge over them is less about the hardware than about the unmatched density of its direct service footprint. A useful signal of the segment's health surfaced on the Q2 FY2026 call, where a Nordson analyst probed whether persistent input-cost inflation might actually drive demand: because Nordson's systems are sold on material savings and precision, a world of scarce, expensive raw materials makes waste-reduction more valuable, not less — a genuinely counter-cyclical wrinkle in an otherwise economically sensitive business.2

Medical and Fluid Solutions (MFS) is the crown jewel, and the reason is structural rather than cyclical. In fiscal 2025 it earned segment EBITDA of roughly $312 million at a 37.3% margin — the highest of the three — on the back of the regulatory lock-in described earlier: components designed into approved devices that cannot be easily displaced.14 It is also the least cyclical business Nordson owns, tied to secular demand from an aging population, chronic disease, and the long shift toward minimally invasive procedures. But "least cyclical" is not "frictionless." On the Q2 FY2026 call, management disclosed a near-term margin headwind in selected interventional product lines caused by a regulatorily required material change — a customer-driven reformulation that forced an operational changeover and temporarily dented efficiency.2 It is a small, honest example of how even a protected medical business carries execution risk, and of the kind of specific, non-defensive disclosure worth rewarding when management offers it. Atrion is now folded into this segment, and MFS is where Nordson has signaled its next large acquisitions will focus.2

Advanced Technology Solutions (ATS) is the high-torque, high-variance engine: electronics dispensing, surface treatment, semiconductor test and inspection, and the CyberOptics business. Its economics are the weakest of the three — a 23.5% EBITDA margin in fiscal 2025 — because it faces the most R&D-intensive, most globally contested markets, including capable Asian specialists such as 武蔵エンジニアリング Musashi Engineering in Japan.14 It is also the most cyclical, whipsawed by the capital-spending cycles of semiconductor and electronics manufacturers. The counterpoint, and it is a real one, is what NBS Next did to the segment during the last downturn. Management used the trough to diversify away from a couple of large customers, broaden from pure dispensing into test and inspection, and reposition its manufacturing footprint closer to customers — and the payoff showed up in fiscal 2026, when ATS posted an all-time record quarter, $178 million in sales, an 8% organic gain, and a record 27% EBITDA margin, riding what Nagarajan called the "early stages" of a semiconductor cycle driven by AI infrastructure, panel-level packaging, and rising optical-fiber content.2

It is worth translating those buzzwords, because they are the actual mechanism of the bull case for this segment. As AI accelerator chips grow more powerful, they generate more heat and require more electrical connections than a traditional chip package can support. The industry's answer is "advanced packaging" — stacking and interconnecting chips in ever-denser arrangements — and one frontier is panel-level packaging, where instead of processing chips on a round silicon wafer, manufacturers build them up on a large rectangular panel to fit more units per production run and cut cost. Each of those steps requires depositing tiny, precise dabs of adhesive and underfill, treating surfaces so materials bond correctly, and inspecting the results for microscopic defects — exactly the trio of dispense, surface treatment, and test-and-inspection that Nordson sells. Separately, as AI data centers move to optical interconnects (using light instead of copper to move data between chips and servers, because light is faster and cooler), the number of optical components that must be precisely assembled and bonded rises sharply — another dispensing-and-inspection problem. In plain terms: the physical build-out of AI infrastructure creates more of the exact precision-fluid tasks Nordson has spent decades mastering. If that thesis holds, the segment that has historically dragged on the average is inflecting into a genuine growth driver. The essential caveat — which management itself volunteered — is that semiconductor cycles are notoriously hard to call, capacity gluts follow booms, and "early innings" is a claim that can only be confirmed in the rear-view mirror. A skeptic should treat the record margin as a cycle-aided high, not a new permanent baseline, until it survives a downturn.

It is worth making the competitive war-game explicit for each segment, because "who can hurt Nordson here" differs by business. In IPS, the threat is a focused adhesive-dispensing rival — ITW's Dynatec unit, Valco Melton, Graco in adjacent spray applications — competing on price for a specific application; Nordson's defense is the service density and consumables lock-in that make price a secondary consideration for a customer who cannot afford downtime. In MFS, the "competition" is mostly the fragmented universe of small, single-product medical-component shops; Nordson's edge is being a single-source, scaled, regulatory-savvy OEM partner that a device maker can design in once and rely on for the life of the product — a value proposition small suppliers structurally cannot match. In ATS, the competition is fiercest and most global, including capable Asian specialists and the in-house capabilities of large electronics manufacturers; here Nordson does not enjoy the same comfortable moat, which is exactly why the segment's margins are lower and its fortunes more cyclical. Reading the three together, the safest economics sit in Medical, the deepest moat in Industrial, and the most upside — and most risk — in Advanced Technology.

The important synthesis is portfolio-level. Management now describes more than half of Nordson's revenue as exposed to structural growth markets — semiconductor, electronics, and medical — with the remainder in steadier "GDP-plus" industrial demand.2 That is a genuine improvement in the quality of the revenue base, and it is the strategic purpose behind the recent M&A: to tilt the portfolio toward markets that grow faster than global GDP without sacrificing the consumables-and-service model that makes any of it profitable. It does not, however, resolve the core question, which is whether the whole enterprise can grow organically at a rate that justifies its valuation and its recent spending. That is where the bulls and bears actually collide.

VIII. Playbook: Business & Investing Lessons

Strip Nordson down to its transferable lessons and four stand out — each one a principle a sophisticated investor can carry to other companies.

Lesson 1: Asymmetric cost of failure is the most underrated moat in industry. The durable pricing power here does not come from a brand consumers love or a patent thicket, but from a simple structural fact: Nordson sells the cheap thing whose failure is catastrophically expensive. When a component is trivial as a share of cost but decisive as a share of outcome, the buyer stops optimizing for price and starts optimizing for certainty — and certainty is a product only the incumbent can credibly sell. Whenever you find that asymmetry — a small part governing a large outcome — you have found a candidate for real pricing power.

Lesson 2: Direct distribution is a moat that hides on the income statement. Nordson's global field-service network looks, in any given quarter, like an expensive cost line a more "efficient" competitor could undercut by selling through distributors. That framing is backwards. The direct model is precisely what makes the company inseparable from its customers' operations and what feeds it the information to sell the next system. It is costly to build and slow to scale — which is exactly why, once built, it is so hard to attack. Some of the best moats are the ones that masquerade as inefficiency.

Lesson 3: Even great compounders accumulate complexity, and an operating system can unlock it. By 2018 Nordson was a good company weighed down by its own sprawl. The NBS Next episode is a clean demonstration that disciplined portfolio pruning — the willingness to fire unprofitable revenue and concentrate resources on the vital few — can expand margins meaningfully without a dramatic strategic pivot. The caution rides alongside the lesson: complexity-reduction is a one-time reservoir of margin, not a perpetual growth engine. Investors should applaud it and then immediately ask what drives the next leg.

Lesson 4: M&A discipline is proven by operating synergy, not purchase price. The reason Nordson could rationally pay high-teens EBITDA multiples for CyberOptics or a full price for Atrion is that it believed it owned a repeatable system for improving what it buys. That belief is only as good as its results. The right way to judge acquisitive compounders is not the multiple paid on day one — which always looks expensive for a quality asset — but the return on invested capital those assets earn three and five years later, once the playbook has either worked or failed. Paying up is defensible; paying up without a repeatable edge is just hope.

The common thread is that Nordson's advantages are structural and behavioral rather than flashy — and structural advantages are exactly the kind a skeptic should insist on stress-testing rather than taking on faith.

IX. Stress-Testing the Bull vs. Bear Case

Put Nordson in front of a sharp activist investor and the challenges come fast. The first is leverage and the pace of capital deployment. A company that built its identity on a fortress balance sheet spent roughly $1.8 billion on ARAG and Atrion inside about a year, and it did so heading into a higher-rate world.1112 The fair pushback: if integration stalls or rates stay elevated, interest expense becomes a persistent drag, and a company that once had all the financial flexibility in the world has spent a chunk of it. The reassuring counter-evidence is in the numbers Nordson has since posted. By the fiscal 2026 second quarter, net debt was about $1.8 billion and the leverage ratio had fallen to 1.9 times EBITDA — actually below the low end of the company's own long-term target range — thanks to the cash-generation machine that pays down debt fast.2 Management also opportunistically annuitized about 30% of its U.S. pension obligation on favorable terms during the quarter, retiring a long-term liability with no cash outlay.2 These are the moves of a company de-levering on schedule, not one in distress. The leverage bet, so far, is being managed.

The second, and more serious, challenge is growth. For years Nordson's organic growth has run in the low-to-mid single digits — and fiscal 2025 was a case in point, with roughly 4% total sales growth and organic sales actually declining 1% in the fourth quarter.4 The uncomfortable question is whether the big acquisitions were partly a way to mask a maturing core: buy revenue when you cannot grow it. It is a fair charge, and the honest answer is that for a stretch of 2023–2025 it had real force. Here, though, the more recent evidence cuts genuinely in Nordson's favor and deserves to be stated plainly: in the first half of fiscal 2026 the company delivered 7% organic growth with all three segments contributing, backlog up 18% organically, and enough order momentum that management raised full-year guidance to sales of roughly $2.93–3.01 billion and adjusted EPS of $11.30–11.80.2 That is not the profile of a stagnant business. The skeptic's rejoinder is that a single strong half, powered substantially by an early-stage and famously unpredictable semiconductor upcycle, is not yet proof of a durable step-change — and management itself hedged, saying it would take only "a meaningful slowdown in order activity" to push results toward the low end of the range.2 The intellectually honest position is that the "growth masking" critique was valid for the recent past and is now genuinely being tested; the next four quarters will show whether the core can grow on its own or whether it needs the next deal.

A note on valuation discipline, since it frames everything. Nordson has rarely been a cheap stock, and it is not one now — it trades at a healthy premium to the broad industrial group, reflecting its margins, its consumables model, and its Dividend King pedigree. That premium is the double-edged sword of a quality compounder: it is deserved by the business, but it also means the market has already priced in continued excellence, so the stock can be a mediocre investment even if the company keeps executing well. This is not a reason to like or dislike the shares — it is simply the reason that, for Nordson specifically, the interesting analytical question is rarely "is this a good business?" (it plainly is) but "is the good business improving faster, or slower, than the price already assumes?" The recent organic re-acceleration and the semiconductor cycle are the swing factors on that question.

The risk radar for Nordson is specific rather than generic. The largest is semiconductor and electronics cyclicality: the ATS segment's newfound strength is real but rides a cycle that has humbled every participant before, and a prolonged tech downturn would compress the very segment now driving the upside. Second is capital-cost and integration risk on the acquisition debt — less about solvency, which is not in question, and more about whether Atrion and ARAG earn their keep on invested capital. Third is competitive pressure in the core: well-run rivals like ITW and Graco are perfectly capable of pricing hard into Nordson's high-margin niches, and input-cost inflation — including tariffs, which management flagged as part of a broader inflationary environment squeezing incremental margins toward the low-30s percent rather than the historical mid-to-upper-30s — is a live pressure on the P&L.2

Fourth, and easy to overlook, is geopolitical and supply-chain exposure. Nordson is a genuinely global company: it sells into Chinese, Korean, Japanese, and European electronics and industrial customers, manufactures across multiple continents, and depends on a supply chain for electronic components and specialty materials that the same trade tensions could disrupt. A serious escalation in U.S.–China technology restrictions could cut both ways — dampening Chinese demand for its electronics equipment on one side, and complicating its own component sourcing on the other. On the Q2 FY2026 call the CFO named exactly this as the thing that worries him most: not tariffs in isolation, which he called immaterial on their own, but the risk that broader macro disruptions create "raw material shortages or issues for our customers" that ripple back into Nordson's order book.2 That is a candid articulation of the real mechanism — Nordson's fortunes are downstream of its customers' ability to keep their own factories running. A fifth, more contained risk is execution on the transformation itself: NBS Next and three simultaneous integrations demand management bandwidth, and integration fatigue is a real phenomenon in acquisitive industrials.

Run the Porter's Five Forces frame and the picture is coherent. Rivalry is real but fragmented across niches, and Nordson's service model blunts it. The threat of new entrants is low, protected by the switching costs, process knowledge, and distribution density already described. Buyer power is muted precisely because the cost-of-failure asymmetry disarms price negotiation. Supplier power is modest for a company of Nordson's scale. Substitutes are the subtlest risk — not a rival dispenser, but a customer redesigning a product or process to need less dispensing, or automating around it — though the direction of travel in electronics and medicine is toward more precision fluid management, not less. On Helmer's 7 Powers, the two that were durable a decade ago — switching costs and process power — remain the load-bearing walls; scale economies and cornered resources (proprietary technology like MRS) reinforce them at the segment level.

The bull case, then, is a company whose operating system is now digesting three defensible franchises while its most cyclical segment inflects into a secular AI-driven upswing, all funded by cash flow that de-levers the balance sheet on autopilot — a Dividend King compounding quietly through the cycle. The bear case is that the organic recovery proves cyclical rather than structural, the semiconductor tailwind reverses, and the acquisition premiums paid at the top of a private-market cycle weigh on returns on capital for years — leaving an excellent business whose stock had already priced in the good version. Both cases are honestly available on today's evidence.

Which is why the discipline for an investor is to watch a small number of things and let them adjudicate. Three KPIs matter most, and the logic of choosing exactly these three is worth spelling out, because tracking the wrong numbers is how investors talk themselves into and out of good businesses at the wrong times.

First, organic sales growth ex-M&A. This is the single cleanest test of whether the core franchises are growing on their own merits or being flattered by deals. Reported revenue growth blends organic performance, acquisitions, and currency into one number that can flatter or mislead; stripping out M&A and FX isolates the question that actually matters — is the underlying business winning more customers and shipping more volume? The re-acceleration to 7% organic in the first half of fiscal 2026 is the datum the whole bull case now rests on, and it is the first thing that would need to fade for the bear case to reassert itself.

Second, segment EBITDA margins in MFS and ATS. Watch Medical because it is where the highest-quality earnings live and where the expensive Atrion integration must prove itself — if the ~37% margin holds or expands as Atrion is absorbed, the premium paid was justified; if it slips, the deal is diluting the crown jewel. Watch Advanced Technology because its record margin is the most cycle-dependent number in the company; a margin that holds through a softer semiconductor quarter would signal that the NBS Next repositioning made the segment structurally better, while a sharp reversal would confirm that recent strength was mostly the cycle.

Third, free-cash-flow conversion. This is the metric that quietly does the heavy lifting: it funds the dividend, pays down the acquisition debt, and finances the next deal, all without diluting shareholders. As long as it stays above 100% of net income — as it has for years, hitting 136% in fiscal 2025 and running above 100% for four straight quarters into fiscal 2026 — the balance-sheet bet effectively de-risks itself over time, because the cash arrives fast enough to retire the debt on schedule.42 Everything else is commentary.

X. Epilogue & Outro

There is a pleasing symmetry to Nordson's arc. It began as a company that made precise metal parts for other people's products and hated the powerlessness of it — a job shop at the mercy of its customers' budgets. Ninety years later it is a company that makes the precise parts inside other people's products, and has arranged its business so that those customers can barely function without it. The screw-machine shop learned to sell not the machine but the dependency, and the dependency has compounded, dividend by dividend, for more than six decades.

The Nagarajan era added the missing operating discipline to that inheritance. NBS Next did not reinvent Nordson so much as clean it — pruning the complexity that a lifetime of acquisitions had deposited, concentrating the company on its most valuable customers and products, and, in the process, proving the balance sheet could support a larger, bolder kind of M&A. Whether that boldness is vindicated depends on execution still in progress: on ARAG and Atrion earning their premiums, on the semiconductor cycle behaving, and on organic growth proving that the strong first half of fiscal 2026 was a step-change rather than a spike.

For the long-term investor, Nordson resists a tidy verdict, and it should. It is a genuinely high-quality industrial franchise, protected by moats that are structural rather than promotional, run by management whose incentives and recent conduct point the right way. It is also a company that spent heavily near the top of a capital-markets cycle and now must convert those bets into returns while its most exciting segment rides a wave no one can time. The invisible compounder in Westlake, Ohio has earned its reputation. The next chapters will be written in the three numbers above — and in whether a razor-and-blade machine built for cereal boxes can keep compounding as it reaches for circuit boards, catheters, and the AI factories being built right now.

References

-

Nordson's History | Founded in 1954 — Nordson Corporation ↩↩

-

Nordson Corporation (NDSN) Q2 Fiscal 2026 Earnings Call Transcript — The Motley Fool, 2026-05-21 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Nordson Corporation Board of Directors Increases Dividend 5 Percent, Marking 62 Consecutive Years of Annual Dividend Increases — Nordson Investor Relations, 2025 ↩

-

Nordson Q4 2025 slides: Record EPS despite organic sales challenges, optimistic 2026 outlook — Investing.com, 2025-12-11 ↩↩↩↩↩↩

-

Nagarajan Named President and CEO of Nordson — Adhesives & Sealants Industry, 2019-07-11 ↩

-

Nordson Corporation Names Sundaram Nagarajan as President and Chief Executive Officer, Effective August 1, 2019 — Business Wire, 2019-06-14 ↩↩↩

-

Nordson Corporation 2025 Proxy Statement (Form DEF 14A) — SEC EDGAR, 2025 ↩↩

-

Nordson Corporation Announces Agreement to Acquire CyberOptics Corporation — Nordson Investor Relations, 2022-08-08 ↩

-

Nordson Corporation Completes Acquisition of CyberOptics Corporation — Nordson Investor Relations, 2022-11-03 ↩

-

Nordson Corporation Announces Agreement to Acquire ARAG Group — Nordson Investor Relations, 2023-06-26 ↩↩

-

Nordson Corporation Announces Agreement to Acquire Atrion Corporation — Nordson Investor Relations, 2024-05-28 ↩↩

-

Nordson Corporation Completes Acquisition of Atrion Corporation — Nordson Investor Relations, 2024-08-21 ↩

-

Nordson Reports Record Fourth Quarter and Fiscal Year 2025 Results (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2025-12 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube