NASDAQ: The Infrastructure of Modern Markets

Introduction and Episode Roadmap

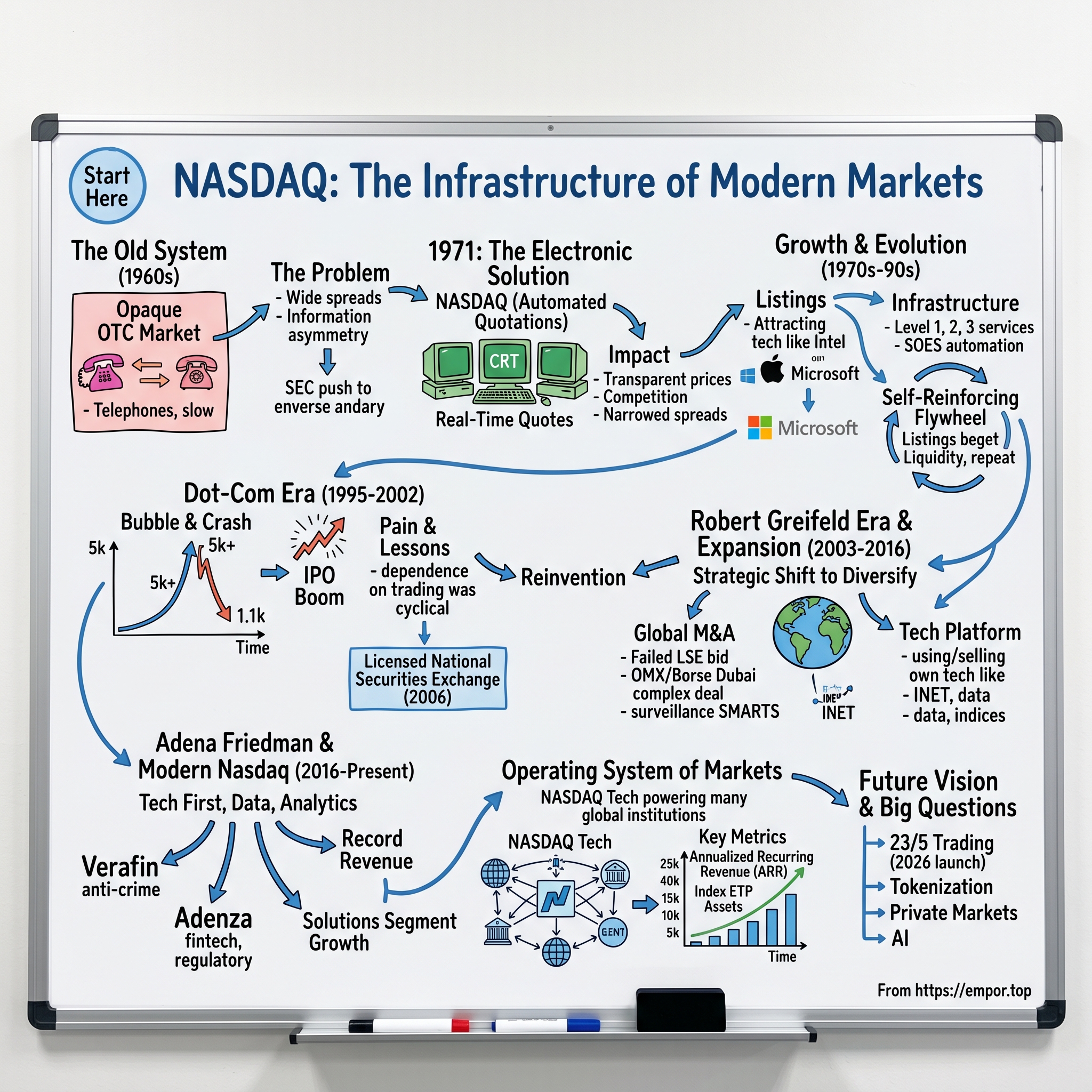

On a winter morning in early 2026, a trader in Tokyo opens a brokerage app and places an order for shares of an American technology company. The trade executes in microseconds, routed through matching engines humming in data centers across New Jersey, confirmed via protocols that span three continents. The trader barely notices. But every layer of that transaction—the exchange where the stock is listed, the surveillance system monitoring for manipulation, the index fund the shares might belong to, the regulatory compliance software the broker relies on—touches a single company. That company is Nasdaq.

Most people think of Nasdaq as a stock exchange, or perhaps an index. It is both, but it is also far more. Nasdaq, Inc. operates the second-largest stock exchange in the world by market capitalization, the most active stock trading venue in the United States by volume, and a sprawling technology business that sells trading infrastructure, surveillance systems, and anti-financial crime software to more than 130 markets and financial institutions across six continents. In 2025, the company exceeded five billion dollars in net revenue for the first time, a milestone that would have seemed absurd to the engineers who, in February 1971, flipped the switch on what was essentially an electronic bulletin board for over-the-counter stock quotes.

The central question of the Nasdaq story is deceptively simple: how did an electronic bulletin board become the backbone of global financial technology? The answer involves half a century of technology disruption, bitter rivalry with the New York Stock Exchange, billion-dollar acquisition gambles, and a relentless strategic pivot from exchange operator to platform company. Founded in 1971, Nasdaq is a much younger organization than the NYSE, which traces its roots to the Buttonwood Agreement of 1792. That youth turned out to be an advantage. Unencumbered by tradition, Nasdaq could embrace electronic trading, attract the companies defining the future economy, and ultimately reinvent itself as a technology provider whose customers include its own competitors.

What follows is the full story—from the pink sheets of the 1960s to the twenty-three-hour trading day Nasdaq plans to launch in 2026—told through the people, decisions, and turning points that built one of the most important institutions in global finance.

Origins and the Problem NASDAQ Solved (1960s–1971)

Picture the over-the-counter stock market in 1965. There is no centralized trading floor, no electronic screen, no real-time pricing. Instead, there are roughly five thousand members of the National Association of Securities Dealers scattered across the country, two-thirds of them working solely in this OTC market. When a broker in Cleveland wants to buy shares of a small industrial company, he picks up the phone, calls a market maker in New York, and asks for a quote. The market maker consults a printed document known as the "pink sheets"—so called because they were literally printed on pink paper—and offers a price. That price might be hours or even a day old. The broker has no practical way to compare it against other market makers without placing a dozen more phone calls. The spreads are wide, the information asymmetry is enormous, and the whole system depends on relationships, phone lines, and trust.

This was not a fringe market. By the mid-1960s, the OTC market handled trading in thousands of securities that were not listed on the NYSE or the American Stock Exchange. Many of these were smaller companies, but some were substantial. The OTC market was, in effect, a "virtual" exchange—an invisible network of broker-dealers linked by telephone, with no physical floor, no opening bell, and no closing gong. It was also wildly inefficient. Customers routinely received worse prices than they should have, and the lack of transparency made oversight nearly impossible.

The regulatory push for reform came from the SEC, which in the late 1960s began pressuring the NASD to modernize. The NASD, for its part, had been thinking about automation. The question was whether technology could do for the OTC market what the trading floor did for the NYSE: centralize information, compress spreads, and bring transparency to a market that badly needed it. The answer came from an unlikely partner. The NASD contracted with Bunker-Ramo Corporation, a defense and electronics firm, to build a computerized system that would display bid and ask quotes electronically, in real time, for the first time in the history of over-the-counter trading.

On February 8, 1971, the system went live. It was called the National Association of Securities Dealers Automated Quotations—NASDAQ, for short. The name was a mouthful, deliberately so: it signaled that this was not a stock exchange but an automated quotation system, a distinction that would carry regulatory and competitive implications for decades. In its first year, the system broadcast quotes to five hundred market makers trading nearly two billion shares in about 2,500 securities, with the newly created NASDAQ index averaging just over 100.

The technology was primitive by modern standards: cathode-ray terminals displaying green text, each screen showing the bid and ask prices for a given security along with the identity of each market maker willing to trade it. But for an industry accustomed to pink sheets and telephones, the impact was transformative. Gordon Macklin, then president of the NASD, called it "an absolute miracle" and "a huge leap forward, coming from over the counter to over the computer." For the first time, a broker could see competing quotes side by side, compare prices across market makers, and execute trades with something approaching informed confidence.

The reaction from the NYSE was predictably hostile. The Big Board viewed NASDAQ not as a complement to the existing market structure but as a competitive threat—an upstart electronic network that might eventually lure listings away from the floor. The NYSE's defenders argued that the specialist system, with its human market makers stationed at physical posts on the trading floor, provided deeper liquidity and better price discovery than any machine could. This argument would persist for three decades, growing weaker with each passing year as technology advanced and NASDAQ's electronic model proved its resilience.

What NASDAQ really solved was an information problem. Before February 1971, the OTC market was opaque by design—opacity protected the market makers who profited from wide spreads and uninformed customers. After February 1971, prices were visible, competition among market makers was transparent, and spreads began to narrow. The seeds of modern market structure had been planted.

Early Growth and Evolution (1971–1990s)

The first two decades of NASDAQ's existence were a slow, steady project of converting a quotation system into something that functioned increasingly like an exchange—without ever calling itself one. The process unfolded in three phases: building infrastructure, attracting the right listings, and fighting regulatory battles that would define its identity.

The infrastructure came first. NASDAQ launched three service levels that segmented its users in a way that now seems quaint but was revolutionary at the time. Level I provided newspaper-style quotes—a single best bid and best offer for each security—aimed at retail brokers and the general public. Level II offered wholesale quotes, displaying all the competing bids and offers from every market maker, essentially a digital version of the pink sheets but updated in real time. Level III went further, allowing authorized market makers to enter and update their own quotes and place limit orders directly into the system. The effect was immediate and measurable: spreads narrowed significantly as the transparency of Level II forced market makers to compete on price rather than on the strength of their phone relationships.

The second phase was about listings, and here NASDAQ caught a wave that no one fully anticipated. In 1971, the same year the system launched, a semiconductor company called Intel held its initial public offering. Intel chose to list on NASDAQ rather than the NYSE, a decision that might have seemed minor at the time but established a pattern that would define NASDAQ for generations. Technology companies—young, fast-growing, often unprofitable, and frequently unconventional in their corporate structures—gravitated toward NASDAQ because it was flexible, modern, and did not carry the establishment stuffiness of the Big Board. Apple listed on NASDAQ in 1980. Microsoft followed in 1986. By the late 1980s, NASDAQ had become synonymous with the technology sector in a way that no amount of marketing could have engineered. The association was organic, built company by company, IPO by IPO.

In 1984, NASDAQ introduced the Small Order Execution System, or SOES, which automated the execution of small retail orders against the best available market-maker quotes. SOES was created in response to the 1987 market crash, during which many market makers had simply stopped answering their phones, leaving retail investors unable to trade at any price. The system was a regulatory mandate born of crisis, and it had an unintended consequence: it enabled a new breed of day trader—the so-called "SOES bandit"—who exploited the automated system to pick off stale quotes from slow-to-update market makers. The SOES bandits infuriated the established broker-dealer community, but they also demonstrated something important about electronic markets. Automation does not merely replicate existing processes faster; it creates entirely new behaviors and market participants. This lesson would repeat itself throughout NASDAQ's history.

By 1991, NASDAQ's share of U.S. securities market transactions had reached 46 percent, a remarkable figure for a system that was only twenty years old and still technically operated as a quotation service rather than an exchange. The internet boom of the mid-1990s accelerated NASDAQ's growth further. In 1998, NASDAQ became the first U.S. stock market to trade online, adopting the slogan "the stock market for the next hundred years." The phrase was audacious, perhaps even tempting fate, but it captured the confidence of an institution that had built its identity around being first in electronic innovation.

Behind the scenes, NASDAQ was also racing to build the physical infrastructure that electronic trading demanded. Data centers, network capacity, redundant systems, disaster recovery—all the unsexy plumbing that makes electronic markets possible. The irony of NASDAQ's story is that a "virtual" market requires enormous physical infrastructure. Server farms, fiber-optic connections, colocation facilities—the invisible architecture of electronic trading is as capital-intensive as any factory floor. NASDAQ invested heavily throughout the 1990s, building the capacity that would be tested, severely, in the decade to come.

For investors evaluating NASDAQ as a business rather than a market, the lesson of this era is clear: the company's early decisions to embrace electronic trading and attract technology listings created a self-reinforcing flywheel. Technology companies listed on NASDAQ because it was the technology exchange; NASDAQ attracted more technology companies because the best ones were already there. Liquidity begets liquidity, listings beget listings, and the flywheel spun faster with each turn.

The Dot-Com Era: Glory and Pain (1995–2002)

No institution was more closely identified with the late-1990s technology boom than NASDAQ. The exchange had spent a decade cultivating its brand as the home of the new economy, and by the mid-1990s, that brand was paying off spectacularly. Every hot internet IPO—Amazon, Yahoo, eBay, Qualcomm—listed on NASDAQ. The exchange's marketing tagline, "The stock market for the next 100 years," was plastered across Times Square on a massive digital billboard that became an icon of the era. NASDAQ was not just an exchange; it was a cultural symbol of the idea that technology was going to change everything.

And for a while, it seemed like it would. The NASDAQ Composite Index, which had languished below 1,000 for most of the 1990s, began a parabolic ascent in 1998. It crossed 2,000 in July 1998, 3,000 in November 1999, 4,000 in December 1999, and peaked at 5,132.52 on March 10, 2000. In eighteen months, the index had more than tripled. Companies with no revenue, no profits, and sometimes no discernible business model were going public at billion-dollar valuations. Pets.com, Webvan, eToys—the casualties are well-documented. But the frenzy was not just about bad companies. It was about a genuine technological revolution—the commercialization of the internet—that was being priced as though every possible outcome would be positive and every timeline would be accelerated.

For NASDAQ as a business, the bubble was enormously profitable. More IPOs meant more listing fees. Higher trading volumes meant more transaction revenue. The brand association with technology meant that every investor who wanted exposure to the new economy was, by definition, trading on NASDAQ. But the exchange was also a hostage to its own success. When the bubble burst, the NASDAQ Composite fell 78 percent from its peak over the next two and a half years, bottoming near 1,100 in October 2002. Trillions of dollars in market capitalization evaporated. The reputational damage was immense. NASDAQ went from being the market of the future to the market where people lost their life savings.

The institutional consequences were equally significant. The Financial Industry Regulatory Authority, which had owned a controlling stake in NASDAQ, sold that stake between 2000 and 2001, severing the last formal link between the exchange and its regulatory parent. NASDAQ was now a private, for-profit company. On July 2, 2002, with the NASDAQ Composite still near its post-crash lows, the company went public—listing, with characteristic defiance, on its own exchange under the ticker symbol NDAQ. The timing was terrible from a valuation perspective but symbolically perfect: NASDAQ was betting on itself at the moment of maximum pessimism.

The dot-com crash taught NASDAQ a lesson that would shape its strategy for the next two decades. Being a pure-play exchange—dependent on listing fees and trading volumes—was inherently cyclical. When the market boomed, NASDAQ boomed. When the market crashed, NASDAQ suffered. The company needed to diversify its revenue streams, reduce its dependence on transaction-based income, and build businesses that generated recurring revenue regardless of market conditions. This insight would drive every major strategic decision from 2003 onward.

In 2006, NASDAQ completed another long-awaited transition: it changed its status from a stock market to a licensed national securities exchange, registered with the SEC. This was more than a regulatory formality. As a national securities exchange, NASDAQ could set its own listing standards, enforce its own rules, and operate with full regulatory autonomy. It was no longer just a quotation system or a dealer market. It was, at last, an exchange in every sense of the word—fifty-five years after the NYSE and thirty-five years after its own founding.

The Greifeld Era and Global Expansion (2003–2016)

When Robert Greifeld became CEO of NASDAQ in 2003, the company's primary business was operating a single equity market in the United States. When he left thirteen years later, NASDAQ operated exchanges on three continents, sold technology to competitors around the world, and had nearly quadrupled its revenue while growing annual operating profits by more than twenty-four times. The transformation was not a straight line—it involved failed bids, complex three-way deals, and the occasional public embarrassment—but the trajectory was unmistakable.

Greifeld came from the electronic trading world. A Queens native with an English degree from Iona College and an MBA from NYU Stern, he had spent the 1990s at Automated Securities Clearance, where he helped build BRASS, one of the first electronic stock order matching systems, and Brut, an early electronic communication network. He understood, at a visceral level, that the future of trading was electronic, and that exchanges would either embrace technology or be consumed by it. His graduate thesis at Stern had been about the operation of the NASDAQ stock market. When he took the top job, he was stepping into a role he had been studying for decades.

Greifeld's first major strategic move was geographic expansion. In 2006, NASDAQ made an unsolicited bid for the London Stock Exchange, accumulating a 28.75 percent stake. The bid failed—the LSE's board rejected it—but it signaled NASDAQ's ambition to become a global player. The LSE stake would later prove useful as a bargaining chip in a more consequential deal.

That deal came on May 25, 2007, when NASDAQ agreed to buy OMX, the operator of eight stock exchanges across Scandinavia and the Baltic states, for $3.7 billion. OMX was attractive for two reasons. First, it gave NASDAQ a footprint in European markets. Second, and arguably more important, OMX had a financial technology division that developed and licensed trading systems to other exchanges worldwide. Buying OMX meant buying a technology business that could be scaled globally.

But the OMX deal did not go smoothly. In August 2007, Borse Dubai—a newly created entity consolidating the Government of Dubai's exchange investments—launched a competing bid at a higher price. What followed was one of the more creative pieces of financial engineering in exchange history. Rather than engage in a destructive bidding war, the three parties negotiated a three-way transaction. Borse Dubai would acquire 97.2 percent of OMX's outstanding shares, then sell them to NASDAQ in exchange for approximately 60.6 million NASDAQ shares, about $11.4 billion in cash, and NASDAQ's 28 percent stake in the London Stock Exchange. Borse Dubai ended up with a 19.9 percent stake in the combined company and 5 percent of the voting rights. NASDAQ also took a 33 percent stake in the Dubai International Financial Exchange, which was subsequently rebranded as NASDAQ Dubai.

The newly merged company, renamed the NASDAQ OMX Group, completed the transaction on February 27, 2008, and was considered the world's largest exchange company at closing. The timing was unfortunate—the global financial crisis was months away from its peak—but the strategic logic proved durable. NASDAQ now had a diversified geographic footprint and, crucially, a technology licensing business that generated revenue even when trading volumes declined.

Greifeld continued the acquisition spree through the financial crisis. In 2008, NASDAQ OMX acquired the Philadelphia Stock Exchange—the oldest exchange in America, founded in 1790—and the Boston Stock Exchange. In 2010, the company bought SMARTS, a market surveillance technology provider, adding another strand to the growing technology business. In 2011, there was speculation about a joint bid with Intercontinental Exchange for NYSE Euronext, which would have combined the two largest U.S. exchanges. The numbers were staggering: NYSE was valued at $9.75 billion, NASDAQ at $5.78 billion, and ICE at $9.45 billion. The bid ultimately did not materialize, and ICE went on to acquire NYSE Euronext on its own in 2013.

Not everything went smoothly under Greifeld. In May 2012, technical glitches during Facebook's $16 billion IPO—the most anticipated listing in NASDAQ's history—delayed trading by thirty minutes and caused widespread order processing failures. The SEC fined NASDAQ $10 million, and the reputational damage lingered. The Facebook debacle was a reminder that technology-first does not mean technology-perfect, and that the complexity of electronic markets creates failure modes that are difficult to predict and costly to remediate.

Despite the stumbles, Greifeld's tenure was transformative. He took a single-market exchange and turned it into a global technology and market infrastructure company. By the time he handed the reins to Adena Friedman at the end of 2016, NASDAQ's market value exceeded $11 billion, and the company had established a strategic template—technology plus data plus global reach—that his successor would extend further.

Technology Platform Evolution and Market Services

Behind the brand and the listings, NASDAQ's most consequential strategic decision over the past two decades has been its transformation from a market operator into a technology provider. This is the part of the business that most casual observers miss, and it is arguably the most durable source of competitive advantage.

The technology story begins with INET, a next-generation trading platform that NASDAQ acquired in 2005 when it bought Instinet's electronic trading arm. INET was fast—among the fastest matching engines in the world at the time—and NASDAQ used it to rebuild its core trading infrastructure. Speed matters in electronic markets not because faster is inherently better, but because the fastest venue attracts order flow, and order flow attracts liquidity, and liquidity attracts listings. The matching engine is the heart of the flywheel.

But the real insight was that NASDAQ's technology did not have to be used only by NASDAQ. If the company could build world-class trading systems, surveillance tools, and data platforms for its own markets, it could also sell those systems to other exchanges. And that is exactly what it did. Today, NASDAQ's technology powers more than 130 markets and clearinghouses globally, including exchanges that compete directly with NASDAQ for listings and order flow. The company is, in effect, the operating system of the global exchange industry—a position analogous to Microsoft selling Windows to Dell and HP, companies that compete fiercely with each other but all run on the same underlying platform.

The data business is equally significant. NASDAQ produces and licenses real-time market data feeds that are consumed by traders, hedge funds, banks, and technology companies worldwide. The data business has high margins, recurring revenue characteristics, and powerful network effects: the more participants who trade on NASDAQ, the more valuable the data becomes, and the more customers are willing to pay for it.

The NASDAQ-100 index, launched on January 31, 1985, is another piece of the platform. The index consists of the hundred largest non-financial companies listed on NASDAQ, weighted by market capitalization. It includes technology, retail, telecommunications, and biotechnology companies—essentially the growth engine of the American economy. The NASDAQ-100 has become one of the most widely tracked indices in the world, and the exchange-traded products that track it—most notably the QQQ ETF—hold hundreds of billions of dollars in assets. Index licensing fees flow to NASDAQ in perpetuity, a classic tollbooth business model.

In 2010, NASDAQ acquired SMARTS, an Australian company specializing in market surveillance technology. SMARTS provided automated systems for detecting insider trading, market manipulation, and other forms of misconduct. The acquisition was strategic in two ways: it gave NASDAQ better tools to police its own markets, and it created another product to sell to exchanges worldwide. Market surveillance is a regulatory requirement in virtually every jurisdiction, which means the addressable market is large, the demand is non-cyclical, and switching costs for clients are extremely high.

The colocation business—renting physical space in NASDAQ's data centers to high-frequency trading firms that want to minimize the distance between their servers and NASDAQ's matching engines—is another high-margin revenue stream. Colocation is controversial because it gives well-resourced firms a speed advantage measured in microseconds, but it is also highly profitable and deeply embedded in modern market structure.

More recently, NASDAQ has pivoted toward cloud infrastructure and software-as-a-service delivery. The company's Nasdaq Financial Framework is a cloud-based platform that allows exchanges and market operators to deploy NASDAQ's technology without building their own data centers. This pivot from on-premise software licensing to SaaS is still in its early stages, but it follows the same playbook that has transformed enterprise software companies across every industry: lower upfront costs for clients, higher lifetime revenue for the provider, and stickier customer relationships.

The key metric to watch in this business is Annualized Recurring Revenue, or ARR, which reached $3.1 billion in 2025, growing 10 percent year over year. ARR captures the predictable, subscription-like portion of NASDAQ's revenue and provides the clearest signal of the company's progress in its transformation from a transaction-dependent exchange to a recurring-revenue technology platform.

Modern NASDAQ: Beyond Exchange (2016–Present)

Adena Friedman became CEO of NASDAQ on January 1, 2017, making her the first woman to lead a major U.S. stock exchange. Her appointment was not a surprise—she had spent the better part of two decades at the company, joining as an intern in 1993, rising through roles in corporate strategy, data products, and finance, and serving as CFO before a three-year detour as CFO and Managing Director of The Carlyle Group, where she helped take the private equity firm public in 2012. She returned to NASDAQ in 2014 as President and was elevated to COO in late 2015.

Friedman's background shaped her strategic vision in specific ways. Her experience at Carlyle gave her an outsider's perspective on NASDAQ's strengths and weaknesses—she could see the company through the eyes of a sophisticated institutional investor. Her years in corporate strategy and data products gave her conviction that NASDAQ's future lay not in trading commissions but in technology, data, and analytics. And her tenure as CFO gave her the financial discipline to pursue that vision through capital allocation rather than wishful thinking.

Under Friedman, NASDAQ has reorganized around three reporting segments: Capital Access Platforms, Financial Technology, and Market Services. The shift in language is deliberate. "Market Services"—the traditional exchange business of matching buyers and sellers—is now just one of three segments, and not the fastest growing. Capital Access Platforms encompasses listings, index licensing, and corporate governance services. Financial Technology includes the trading technology, surveillance, and regulatory compliance businesses.

The most significant acquisition of the Friedman era—and the largest in NASDAQ's history—came in June 2023 when the company agreed to buy Adenza from Thoma Bravo for $10.5 billion. Adenza was itself a combination of two fintech firms: Calypso, which provides treasury, risk management, and collateral management software to capital markets participants, and AxiomSL, which specializes in regulatory and compliance software for financial institutions. The deal was structured as $5.75 billion in cash and 85.6 million shares of NASDAQ common stock, giving Thoma Bravo a 14.9 percent stake in the combined company and making the private equity firm one of NASDAQ's largest shareholders.

The market reaction was harsh. NASDAQ shares fell nearly 10 percent on the announcement, as investors questioned whether the company was overpaying at roughly 31 times Adenza's EBITDA. The strategic rationale, however, was clear: Adenza extended NASDAQ's serviceable addressable market by $10 billion, to $34 billion total, and deepened the company's relationships with banks, asset managers, and central banks. Calypso's software serves 24 central banks globally, a client base that is about as sticky as any business can hope for. The acquisition closed on November 1, 2023, and by the end of 2025, NASDAQ had achieved 42 cross-sells across its combined product portfolio and surpassed $160 million in expense efficiencies.

The earlier acquisition of Verafin, completed in February 2021 for $2.75 billion, added another dimension. Verafin, founded in 2003 in St. John's, Newfoundland, provides cloud-based anti-money laundering and fraud detection software to more than 2,000 financial institutions in North America. The United Nations estimates that up to $2 trillion in laundered money flows through the global financial system annually, making anti-financial crime technology a large, growing, and structurally non-cyclical market. Verafin gave NASDAQ a credible position in this space and reinforced the company's pivot toward mission-critical software that clients cannot easily replace.

On the listings front, NASDAQ capped a record-setting year in 2025. The crown jewel was Walmart, the world's largest retailer, which transferred its listing from the NYSE to NASDAQ in November 2025. With a market value of approximately $852 billion, the Walmart transfer was the largest exchange switch in history. Walmart's CFO explained the decision by saying it "aligns with the people-led, tech-powered approach to our long-term strategy"—a statement that, however corporate in its phrasing, captured the essence of NASDAQ's brand evolution. Other notable switches to NASDAQ in 2025 included Shopify, Kimberly-Clark, and Thomson Reuters. In total, $1.2 trillion in market value switched to NASDAQ during the year.

Perhaps the most forward-looking initiative is NASDAQ's plan to extend its U.S. equities trading hours to 23 hours per day, five days per week. The proposal, filed with the SEC in early 2026, would add a "Night" session running from 9:00 PM to 4:00 AM Eastern Time, complementing the existing pre-market, regular, and post-market sessions. The motivation is straightforward: the U.S. stock market represents almost two-thirds of the market value of listed companies globally, while foreign holdings of U.S. equities reached $17 trillion. Investors in Tokyo, Singapore, and London want to trade American stocks during their own business hours. NASDAQ expects to launch the extended hours in the second half of 2026, pending SEC approval and the readiness of critical infrastructure providers like the DTCC, which plans to begin 24/5 clearing by the second quarter of 2026.

The initiative is not without controversy. Critics argue that near-continuous trading could worsen liquidity fragmentation, increase volatility during off-peak hours, and put operational stress on broker-dealers and market makers who would need to staff and fund their desks around the clock. Major Wall Street banks have expressed caution. But NASDAQ is betting that the globalization of capital markets is irreversible, and that the exchange that offers the most access will capture the most order flow.

Market Structure and Regulatory Navigation

NASDAQ exists at the intersection of technology and regulation, and navigating that intersection has been one of the defining challenges—and competitive advantages—of the business. Every innovation, every new product, every expansion of trading hours requires regulatory approval. And every regulatory change creates both risks and opportunities.

The most consequential regulatory event in modern market structure was Regulation NMS, implemented by the SEC in 2007. Reg NMS established the principle that investors are entitled to the best available price across all exchanges, regardless of where their order is originally routed. The regulation created a national market system in which all exchanges are interconnected, orders are automatically routed to the venue offering the best price, and no exchange can operate as a walled garden. For NASDAQ, Reg NMS was a double-edged sword. It legitimized NASDAQ's electronic model by putting it on equal footing with the NYSE's floor-based system. But it also fragmented order flow across dozens of competing venues—exchanges, alternative trading systems, dark pools—that all competed for the same trades.

Dark pools—private trading venues that match orders without displaying them publicly before execution—have been a persistent source of tension. At their best, dark pools allow institutional investors to execute large orders without revealing their intentions to the market, reducing market impact. At their worst, they divert order flow away from public exchanges, reducing the quality of price discovery and making the public markets less informative. NASDAQ has generally argued that too much trading in dark pools undermines market quality, a position that is self-interested but not without merit.

High-frequency trading is another fault line. NASDAQ has embraced high-frequency firms as a source of liquidity and a driver of tighter spreads, while critics argue that the speed arms race creates systemic fragility. The Flash Crash of May 6, 2010—when the Dow Jones Industrial Average plunged nearly 1,000 points in minutes before recovering—exposed the risks of algorithmic trading in fragmented, high-speed markets. In response, the exchanges implemented circuit breakers: automatic trading pauses triggered when a stock's price moves too far, too fast. Circuit breakers are a crude but effective tool for preventing cascading failures, and they have been refined and expanded in the years since the Flash Crash.

Payment for order flow—the practice in which retail brokers sell their customers' orders to wholesale market makers like Citadel Securities or Virtu Financial, rather than routing them to public exchanges—has emerged as one of the most contentious issues in market structure. The practice reduces NASDAQ's share of retail order flow and, critics argue, creates conflicts of interest between brokers and their customers. The GameStop episode of January 2021 brought payment for order flow into the mainstream spotlight, and the SEC has considered reforms that could redirect some retail flow back to public exchanges. For NASDAQ, any such reform would be a significant tailwind.

Throughout these debates, NASDAQ has positioned itself as both participant and referee. The company operates markets, sells surveillance technology to regulators, and advocates for regulatory changes that happen to benefit its business model. This is not unusual in financial services—banks, exchanges, and clearing houses all play dual roles—but it requires careful management of conflicts and a sophisticated approach to government relations. NASDAQ employs a substantial team dedicated to regulatory affairs across multiple jurisdictions, and Friedman herself sits on the board of the Federal Reserve Bank of New York, a position that provides both insight and influence.

Playbook: Business and Technology Lessons

NASDAQ's fifty-five-year history offers a masterclass in platform economics, technology disruption, and the art of reinvention. Several lessons stand out.

First, the power of first-mover advantage in network businesses. NASDAQ was the first electronic market in the United States, and that early lead created a self-reinforcing cycle of liquidity, listings, and brand association that competitors have never fully overcome. Being first gave NASDAQ the technology companies, and the technology companies gave NASDAQ the growth-stock brand, and the growth-stock brand attracted more technology companies. First-mover advantage in network businesses is not insurmountable—the NYSE is still larger by market capitalization—but it is extremely durable.

Second, the strategic value of selling to competitors. NASDAQ's decision to license its trading technology and surveillance systems to other exchanges was counterintuitive. Why help your competitors operate more efficiently? The answer is that technology licensing creates revenue streams that are decoupled from NASDAQ's own trading volumes, generates switching costs that lock in clients for years, and positions NASDAQ as the indispensable infrastructure layer beneath the entire exchange industry. When your competitors depend on your technology, you have a form of leverage that transcends any single market.

Third, the exchange flywheel. Listings attract liquidity. Liquidity attracts more listings. More listings generate more data. More data creates more index products. More index products attract more passive capital. More passive capital increases trading volumes. And the cycle repeats. Understanding this flywheel is essential to understanding why exchange businesses tend toward natural monopoly or duopoly, and why NASDAQ and the NYSE have maintained their dominant positions despite decades of competition from upstart venues.

Fourth, the discipline of M&A strategy. NASDAQ's acquisitions fall into two categories: geographic expansion (OMX, Philadelphia, Boston, Dubai) and capability acquisition (SMARTS, Verafin, Adenza). The geographic acquisitions extended the flywheel across borders. The capability acquisitions diversified revenue and reduced cyclicality. The company has generally been disciplined about integration, though the Adenza deal tested investor patience with its size and valuation multiple. The key lesson is that M&A in infrastructure businesses should be additive to the platform, not diversionary.

Fifth, the importance of managing regulatory relationships. Exchanges are among the most heavily regulated businesses in the world. Every product, every rule change, every expansion requires regulatory approval. NASDAQ's ability to navigate this environment—maintaining credibility with the SEC while simultaneously lobbying for changes that benefit its business—is a core competency that is difficult to replicate and easy to underestimate.

Analysis and Investment Case

NASDAQ's business model generates revenue from four primary sources: transaction fees from matching trades, listing fees from companies that trade on its exchanges, data and index licensing fees, and technology and software subscription fees. The strategic direction of the business has been to increase the share of revenue coming from the latter two categories—data, indices, and technology—while maintaining and optimizing the transaction and listing businesses.

This shift is visible in the numbers. In 2025, NASDAQ's Solutions revenue—which encompasses everything except transaction-based market services—reached $4.0 billion, growing 12 percent year over year. ARR hit $3.1 billion, growing 10 percent. Index revenue grew 23 percent in the fourth quarter alone, driven by record assets in index-linked ETPs and strong net inflows. The company's operating margin expanded to 56 percent, reflecting the inherent scalability of software and data businesses. Full-year adjusted earnings per share grew 23 percent to $3.48.

The competitive moats are formidable. Network effects in listings and liquidity create a barrier that no new entrant has successfully breached at scale. Regulatory barriers—the cost and complexity of becoming a licensed national securities exchange—limit new competition. Switching costs in technology and surveillance products are high, particularly for the Calypso and AxiomSL products that are deeply embedded in clients' risk management and compliance workflows. And the index business benefits from a form of intellectual property moat: the NASDAQ-100 is a recognized brand, and the licensing fees it generates are recurring and high-margin.

Through the lens of competitive strategy, NASDAQ benefits from several of Hamilton Helmer's Seven Powers. Scale economies in trading technology mean that the marginal cost of processing an additional trade approaches zero once the infrastructure is built. Switching costs in enterprise software—particularly in regulatory compliance and risk management—lock in clients for years. Network effects in listings and liquidity create a flywheel that strengthens with scale. And the NASDAQ brand, while less tangible, carries meaningful value in attracting IPOs and listing switches.

The threats are real but manageable. Zero-commission retail trading has shifted order flow to wholesale market makers and away from public exchanges, though regulatory reform could reverse this trend. Direct listings and SPACs have intermittently challenged the traditional IPO model, though IPO activity tends to recover with market sentiment. Crypto-native exchanges like Coinbase represent a potential long-term disruptive threat, particularly if tokenized securities gain regulatory approval. And the trend toward decentralized finance, while still nascent, could theoretically disintermediate centralized exchanges entirely—though this remains speculative.

The growth drivers are compelling. International expansion, particularly the 23/5 trading initiative, targets a massive pool of global capital that currently trades U.S. equities through suboptimal channels. Cloud migration of NASDAQ's technology stack creates opportunities to acquire new clients and increase revenue per client. The anti-financial crime business, anchored by Verafin, addresses a growing and regulation-driven market. And the cross-selling opportunity from the Adenza acquisition—42 cross-sells completed by end of 2025 with a target of $100 million in run-rate revenue by 2027—provides a visible growth runway.

For investors tracking this business, two KPIs matter above all others. The first is Annualized Recurring Revenue (ARR), which measures the predictable, subscription-like portion of NASDAQ's revenue and serves as the clearest indicator of the company's transformation from a cyclical exchange to a durable technology platform. The second is the index ETP assets under management tracking NASDAQ indices, which drives the high-margin index licensing revenue and serves as a barometer of NASDAQ's brand strength and the passive investing megatrend.

Future Vision and Strategic Questions

NASDAQ's stated ambition is to become the "trusted fabric of the world's financial system"—a phrase that sounds like corporate marketing but actually describes a coherent strategy. If NASDAQ can embed its technology in enough exchanges, clearinghouses, banks, and regulators worldwide, it becomes the infrastructure layer that everyone depends on but no one thinks about—until it stops working.

The most immediate strategic initiative is the 23/5 trading expansion, which represents NASDAQ's bet that the future of equity trading is global and continuous. If successful, it could capture significant order flow from international investors who currently trade U.S. equities through less efficient channels. If the SEC approves and infrastructure providers are ready, NASDAQ expects to launch in the second half of 2026.

Beyond extended hours, several longer-term questions will shape NASDAQ's trajectory. Tokenization—the process of representing traditional securities as digital tokens on a blockchain—could fundamentally change how securities are issued, traded, and settled. NASDAQ has been exploring digital asset infrastructure for years, and the exchange that successfully bridges traditional and tokenized securities could capture an enormous new market. Private market democratization is another frontier. As companies stay private longer, the demand for institutional-quality trading and data services in private markets is growing. NASDAQ's partnership with LSEG for private markets data access, announced in November 2025, is an early move in this direction.

Artificial intelligence and machine learning are already being deployed in NASDAQ's market surveillance and compliance products, and the potential for AI to enhance trading, risk management, and client services is substantial. Carbon markets and climate-related financial products represent another growth opportunity, particularly as regulatory requirements for climate disclosure increase globally.

The competitive landscape is intensifying. NYSE parent Intercontinental Exchange, Cboe Global Markets, and London Stock Exchange Group are all pursuing similar strategies of technology diversification and geographic expansion. The question is not whether NASDAQ can maintain its position as a leading exchange—it almost certainly can—but whether it can successfully complete its transformation into a technology company that happens to operate exchanges, rather than an exchange company that happens to sell technology. The distinction matters for valuation, for strategic flexibility, and for the kind of talent the company can attract and retain.

Recent News

NASDAQ reported fourth-quarter and full-year 2025 results on January 29, 2026, exceeding five billion dollars in net revenue for the first time. Full-year net revenue reached $5.2 billion, up 13 percent over 2024, with Solutions revenue growing 12 percent to $4.0 billion. Fourth-quarter adjusted earnings per share of $0.96 beat consensus estimates, and full-year adjusted EPS of $3.48 represented 23 percent growth year over year. ARR reached $3.1 billion, growing 10 percent. The company repaid $826 million of debt during the year, continuing its deleveraging following the Adenza acquisition. Market Services set new net revenue records, with index options revenue more than doubling for the second consecutive quarter.

The company filed its proposal with the SEC to extend U.S. equities trading hours to 23 hours per day, five days per week, with a target launch in the second half of 2026. The Federal Register published the proposed rule change in January 2026. Adena Friedman was appointed Chair of the Board in addition to her CEO role, effective January 1, 2023, and NASDAQ announced it will host its 2026 Investor Day on February 25, 2026, at its Global Headquarters in New York. NASDAQ's listings franchise continued its momentum, with Walmart's transfer from NYSE in November 2025 representing the largest exchange switch in history and contributing to $1.2 trillion in total market value switching to NASDAQ during the year.

Links and Resources

- Nasdaq Q4 2025 Earnings Press Release

- Nasdaq 2026 Investor Day Announcement

- SEC Filing: Nasdaq 23/5 Trading Hours Proposal

- Nasdaq Adenza Acquisition Details

- Walmart Listing Transfer Announcement

- Market Mover: Lessons from a Decade of Change at Nasdaq by Robert Greifeld (2019)

- Nasdaq Verafin Acquisition Details

- Nasdaq Inc. Investor Relations

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube