Navan: The Great Pivot, The Super App, and the Future of Corporate Travel

I. Introduction & Episode Roadmap

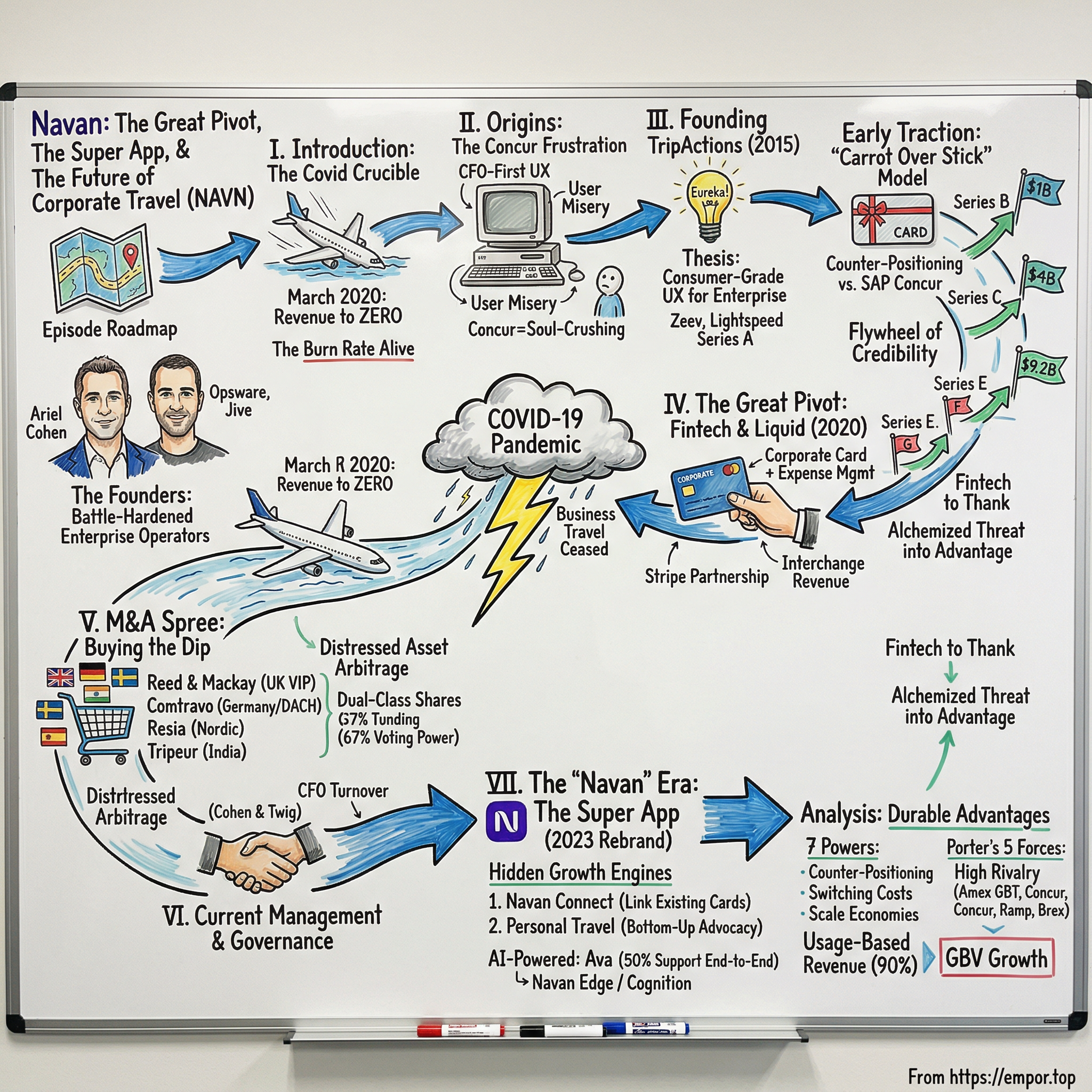

Picture this: it is March 2020, and every commercial flight on Earth is grounded. Airports that once hummed with the kinetic energy of a million road warriors each week sit silent, their departures boards flickering with a single word: CANCELLED. Now imagine you are the CEO of a company whose entire existence depends on people getting on those planes. Every booking is a zero. Every revenue line is a flatline. Your burn rate, however, is very much alive.

That was the reality facing Ariel Cohen and Ilan Twig, the co-founders of TripActions, the Silicon Valley darling that had raised over half a billion dollars on the promise of reinventing corporate travel. In the span of roughly seventy-two hours, the global pandemic transformed their rocket ship into a life raft. The question was not whether they would grow. The question was whether they would survive the quarter.

What happened next is one of the more remarkable corporate pivots of the last decade. The company that nearly died as a travel booking tool emerged from the pandemic as something far larger, far more ambitious, and far harder to categorize. Today, trading on the NASDAQ under the ticker NAVN, Navan is a sprawling platform that processes billions of dollars in gross bookings, issues corporate credit cards, automates expense reports, and even lets employees book their personal vacations. Its ambition is nothing less than to become the operating system for every dollar a company spends when its people move through the world.

But the story of Navan is not a clean arc of triumph. It is a story of near-death, aggressive acquisition, a brutal IPO, and an ongoing battle to prove that a travel-plus-fintech hybrid can command the kind of valuation that public markets reserve for pure software companies. It is also, at its heart, a story about two founders who refused to let a crisis define them, and instead used it to redefine their company.

To appreciate the scale of the opportunity and the challenge, consider the numbers. Global business travel spending peaked at approximately 1.43 trillion dollars in 2019, collapsed to roughly 670 billion during the pandemic, and has since recovered to an estimated 1.5 trillion dollars annually. The corporate expense management software market, a separate but adjacent category, is valued at roughly eight billion dollars and projected to more than double by the end of the decade. The top three traditional travel management companies, Amex GBT, BCD Travel, and the recently absorbed CWT, collectively account for less than a quarter of total industry revenue, meaning the market remains extraordinarily fragmented. And SAP Concur, the reigning software incumbent, commands nearly fifty percent of the expense management software market despite a user experience that its own customers routinely describe as archaic.

Into this landscape stepped a company that bet everything on a single premise: the person who actually books the trip and swipes the card matters more than the person who writes the company's travel policy. That bet nearly failed. And then it produced something genuinely new.

This is the story of the anti-Concur, the COVID crucible, the European shopping spree, and the hidden fintech engines powering one of the most ambitious vertical SaaS plays of the 2020s.

II. Origins: The Concur Frustration & Founding TripActions

To understand why Navan exists, you first have to understand what it was born to replace. And to understand that, you need to spend a few minutes inside the soul-crushing experience of booking a business trip on SAP Concur.

Concur Technologies was founded in 1993 by Steve Singh and his brother Rajeev, born from Steve's personal frustration with filing expense reports. The original product was a Windows-based software package sold for sixty-nine dollars. It was simple, it was useful, and it caught on. Concur survived the dot-com crash, pivoted brilliantly to a cloud model in the early 2000s, and grew into the undisputed king of corporate travel and expense management. In 2014, SAP acquired Concur for 8.3 billion dollars, and by the mid-2020s the platform controlled nearly half of the entire travel and expense management software market.

But here is the thing about Concur that matters for this story: it was built for the CFO, not the traveler. Every feature, every workflow, every approval chain was designed to satisfy the compliance needs of the finance department. The actual human being who had to use the software, the person sitting in an airport lounge trying to rebook a cancelled flight on their phone, was an afterthought.

Users described the interface as "straight out of 1980." One reviewer noted they could "book multiple flights using Google Flights faster than I can book one simple trip on Concur." Implementation took months. The billing portal looked like it had been designed by someone who had never used the internet. A forced UI update in the mid-2010s somehow made things worse, requiring "more clicks and more time to perform the same activity," according to user reviews. The pricing model was opaque, charging on a per-expense-report basis with add-on fees that ballooned as companies added features. And yet, despite all of this, companies kept paying. They kept paying because the CFO had signed a multi-year contract, because the IT department had spent months integrating Concur into the ERP system, and because nobody had presented a compelling alternative.

This was not a bug. It was the defining characteristic of an entire generation of enterprise software. The buyer (the CFO) was not the user (the employee), and since the buyer signed the check, the user's misery was simply not a product priority. It was the same dynamic that had played out in enterprise CRM before Salesforce, in enterprise communications before Slack, and in enterprise HR before Workday.

Enter Ariel Cohen and Ilan Twig. Both Israeli-born, both deeply technical, both serial entrepreneurs who had spent their professional lives living out of suitcases. They first met in the early 2000s at Mercury Interactive, a software testing company in Israel, where their paths overlapped in R&D. Cohen had joined Mercury in 1999, rising to director of R&D Enablement by 2001. Twig was building and leading engineering teams. When Mercury was acquired by Hewlett-Packard in 2006, both moved through the HP machine, and then through Opsware, the infrastructure automation company co-founded by Marc Andreessen and Ben Horowitz, two names that would prove fatefully important later in this story. Cohen eventually landed at Jive Software as a senior director of product management, completing an MBA at Northwestern's Kellogg School of Management along the way. Twig led large R&D teams at HP and then Rockmelt, a social web browser startup, earning a master's degree in computer science from Open University of Israel.

Their backgrounds matter because they shaped the lens through which both men saw the world. Cohen was the quintessential product-obsessed go-to-market leader: someone who had spent years selling enterprise software to skeptical buyers, who understood the gap between what procurement departments bought and what end users actually wanted, and who could walk into a boardroom and make people believe in a vision they had not yet seen. Twig was the complementary force: a deeply technical architect who could take a whiteboard sketch and transform it into production infrastructure that scaled globally. They were not the kind of founders who had a brilliant idea in a dorm room. They were battle-hardened enterprise operators who had lived inside the machinery of large software companies and knew exactly which parts were broken.

In August 2012, they launched their first joint venture: StreamOnce, a business multimedia integration platform. It was a modest success, reaching a million dollars in revenue before being acquired by Jive Software. But StreamOnce was not the point. The point was that Cohen and Twig proved they could build together, that their complementary skills, sales vision plus engineering depth, produced something greater than the sum of its parts. It was the dress rehearsal for the main act.

The founding myth of TripActions traces to a specific moment of frustration that anyone who has traveled frequently for work will recognize viscerally. Cohen was on a business trip to Ukraine, one of many trips in a career that had taken him to dozens of countries. His hotel booking was botched. The software his company used offered no real-time solution. No mobile app could fix the problem. No intelligent system rerouted him to an alternative property. He sat in a foreign city, exhausted and frustrated, staring at a clunky interface that could not help him, and thought: this is insane. Consumer travel had been transformed by Expedia and Booking.com into beautiful, intuitive experiences. You could book a vacation in Bali on your phone in ninety seconds. But corporate travel remained a clunky, miserable patchwork of archaic travel management companies, fax machines, and software that looked like it had been designed during the Clinton administration. The gap between what was possible and what existed was not incremental. It was a chasm.

On May 15, 2015, exactly two years after the StreamOnce acquisition, Cohen and Twig founded TripActions in Palo Alto with a simple thesis: build a consumer-grade user experience for enterprise travel. Make the business traveler love the tool as much as they loved booking a personal trip on their favorite travel app. And do it with the intelligence and policy controls that a CFO would demand.

The early fundraising was not easy. Corporate travel was widely perceived by Silicon Valley venture capitalists as a "solved problem." Concur had the market locked up. Travel management was a low-margin, operationally complex business that most VCs viewed as unattractive. But Cohen and Twig found believers. In January 2016, they raised a 14.6 million dollar Series A from Zeev Ventures and Lightspeed Venture Partners, with Group 11 also participating. Arif Janmohamed at Lightspeed would later describe the founding pitch as taking place over a "bowl of hummus" at a Palo Alto restaurant. He saw what Cohen and Twig saw: an enormous market dominated by software that everyone hated.

The money was in the bank. The vision was clear. Now they had to build something that could actually displace a fifty-percent market share incumbent backed by one of the largest enterprise software companies on Earth. In the annals of startup strategy, few bets have been this audacious: two Israeli-born founders with a fourteen-million-dollar Series A, going after SAP Concur, an eight-billion-dollar acquisition target with twenty-three thousand customers and fifty percent market share. It was David versus Goliath, except David was armed with a better mobile app and a radically different philosophy about who enterprise software should serve.

III. Early Traction & The Counter-Positioning Strategy

The genius of TripActions' early product was not just that it looked better than Concur. Plenty of startups can build a prettier interface. The genius was a single, deceptively simple insight about human behavior: instead of punishing employees for spending too much on travel, reward them for spending less.

This was the "carrot over the stick" model, and it was revolutionary in the context of corporate travel. Legacy systems enforced draconian policies. Book outside the approved list, and your expense report gets rejected. Choose a hotel above the nightly cap, and you face a compliance inquiry. The entire experience was designed around enforcement, which meant that employees viewed corporate travel software the way most people view the DMV: a necessary evil to be endured, never enjoyed.

TripActions flipped this dynamic on its head. The platform would show a traveler multiple hotel options for their destination, with the corporate-approved rate clearly marked. But next to a cheaper option, a three-star hotel instead of a four-star, there would be a small, tantalizing message: "Save your company $87 on this booking and earn a $50 Amazon gift card." It was elegant behavioral economics. The employee got a tangible personal reward. The company saved money. And both parties felt good about the outcome. The adversarial relationship between the corporate policy and the individual traveler was replaced by alignment.

Hamilton Helmer, the strategist who wrote "7 Powers," would recognize this immediately as counter-positioning. TripActions adopted a business model that its largest incumbent, SAP Concur, fundamentally could not copy. Concur's entire architecture, its pricing model (per expense report), its product design philosophy (CFO-first), and its customer relationships (built on compliance and control) made it structurally incapable of adopting an employee-first, rewards-driven approach without destroying the value proposition that its existing customers were paying for. It was the classic innovator's dilemma, playing out in real time.

The product caught fire. Between 2017 and 2019, TripActions became the darling of Silicon Valley startups and mid-market technology companies. These were organizations filled with young, tech-savvy employees who expected consumer-grade software in every part of their work lives. They had grown up on Uber and Airbnb. Being told to call a travel agent or navigate a Concur booking portal felt like being asked to use a fax machine.

The go-to-market strategy was equally shrewd. TripActions targeted the mid-market: companies with five hundred to five thousand employees, large enough to have significant travel spend but small enough that they were not locked into decade-long contracts with traditional TMCs or deeply embedded in Concur's ecosystem. These companies made purchasing decisions faster, implemented new tools more easily, and were far more receptive to a startup that promised both a better employee experience and measurable cost savings. The early customer list read like a who's who of late-2010s Silicon Valley: fast-growing technology companies that valued speed, design, and employee satisfaction. Each customer win became a reference point for the next sales conversation, creating a flywheel of credibility that accelerated growth quarter after quarter.

The fundraising trajectory tells the story of hypergrowth more vividly than any product review. After a twelve-and-a-half-million dollar bridge round in October 2017, the company raised a fifty-one-million dollar Series B from Lightspeed in March 2018. Just eight months later, in November 2018, Andreessen Horowitz led a massive 154 million dollar Series C that valued TripActions at over one billion dollars. Ben Horowitz, who had worked alongside Cohen and Twig in the Opsware days, joined the board personally. He knew these founders. He trusted their judgment. And he believed that corporate travel was ripe for the kind of disruption that Andreessen Horowitz had backed in dozens of other enterprise categories.

Seven months after that, in June 2019, a16z doubled down with a 250 million dollar Series D that pushed the valuation to four billion dollars. In less than four years, TripActions had gone from a bowl of hummus in Palo Alto to one of the most valuable private enterprise software companies in the world.

The growth was not just top-line hype. Real companies were deploying TripActions and seeing real results. Employees loved the interface. Finance teams loved the cost savings. IT teams loved the clean integrations with their existing accounting and HR systems. The net promoter scores were genuinely strong. The company was displacing legacy travel management companies at mid-market firms across the technology sector, and starting to push upmarket into larger enterprises that had been Concur strongholds for years.

What made the counter-positioning so lethal was that every attempt by Concur to respond only reinforced TripActions' advantage. Concur could not add employee rewards without undermining its compliance-first positioning. It could not rebuild its mobile experience without disrupting millions of users. It could not adopt a modern booking engine without renegotiating its GDS relationships. It was, as Clay Christensen would have recognized, the innovator's dilemma playing out in textbook fashion. The incumbent's greatest strength, its massive installed base and deep enterprise integrations, was also the anchor that prevented it from matching the newcomer's agility.

By the end of 2019, TripActions was sitting on top of the world. The venture capital was abundant. The product-market fit was undeniable. The competitive moat was deepening. Cohen and Twig had built exactly what they set out to build: the anti-Concur, the consumer-grade travel platform for the enterprise. The only risk that nobody was modeling, the only scenario that did not appear in any pitch deck or board presentation, was the one where business travel itself simply ceased to exist.

And then, in the first weeks of March 2020, that is exactly what happened.

IV. The Crucible: COVID-19 and the Fintech Pivot

On March 11, 2020, the World Health Organization declared COVID-19 a global pandemic. Within days, the dominoes fell in rapid succession. Italy locked down entirely on March 9. The United States declared a national emergency on March 13. By March 19, California had issued the first statewide stay-at-home order. Airlines slashed flight schedules by eighty to ninety percent. Hotels boarded up their lobbies.

The speed at which TripActions' business evaporated is difficult to overstate. This was not a gradual decline. This was not a recession where bookings fell twenty or thirty percent over several quarters. Business travel went to literal zero. In the span of days, governments around the world imposed travel bans, corporations grounded their employees, and the entire global infrastructure of commercial aviation essentially shut down. For a company that earned revenue on every booking, the math was brutally simple: zero bookings meant zero revenue.

Cohen later described those first weeks in language that bordered on existential. The company had roughly three hundred million dollars in the bank, a significant war chest by startup standards, but the burn rate was calibrated for a hyper-growth company with over a thousand employees, expensive office space, and aggressive sales targets. The cash runway, once seemingly infinite, suddenly had a very visible end.

The hard decisions came fast. Cohen and Twig cut their own salaries by fifty percent. Executive pay cuts cascaded through the organization. And then came the layoffs. In late March 2020, TripActions let go of roughly three hundred employees, approximately twenty-five percent of its workforce. The layoffs were conducted over Zoom, a grim detail that captured the surreal horror of that moment in corporate history. It drew public criticism, but the alternative, burning through the cash reserve while waiting for the world to reopen, was not a viable strategy. The remaining employees were asked to accept salary reductions. The company's luxurious Palo Alto office, once a symbol of its ascent, sat empty.

To understand how desperate the moment was, consider the broader context. The Global Business Travel Association estimated that the travel industry lost approximately 770 billion dollars in spending in 2020 alone, one of the most severe demand shocks in the history of any industry. Traditional travel management companies, many of which operated on thin margins even in good times, began collapsing. CWT, one of the world's three largest TMCs, would eventually file for Chapter 11 bankruptcy. Scores of smaller agencies simply vanished. Hotel chains furloughed hundreds of thousands of workers. Airlines burned through billions in government bailout funds. This was not an industry downturn. It was an industry near-extinction event, and TripActions was caught directly in the blast radius.

What happened next, however, is what separates the Navan story from the dozens of other travel companies that simply hibernated through the pandemic or went bankrupt. Cohen and Twig made a decision that would prove to be the most consequential strategic choice in the company's history. Instead of cutting engineering and retreating into survival mode, they doubled down on R&D. The logic was counterintuitive but clear-eyed: if employees were not traveling, they were still spending. Work-from-home stipends, software subscriptions, office equipment shipped to home addresses, shipping costs, meal deliveries, all of it was flowing through corporate expense processes that were just as broken as the travel booking experience had been. And unlike travel, this spending was actually accelerating during the pandemic, as companies scrambled to equip their newly remote workforces.

The product that emerged from this crucible was TripActions Liquid, a modern corporate card and expense management system.

The concept was straightforward but powerful: issue employees physical and virtual Visa corporate cards, powered by Stripe's issuing infrastructure, and wrap them in the same beautiful, intelligent software experience that had made TripActions' travel product so compelling. When an employee swiped their Liquid card at a restaurant, the transaction would appear instantly in the app, not days later on a paper statement. The system would automatically categorize the expense: dinner, client entertainment, with the correct GL code pre-populated. The employee would snap a photo of the receipt with their phone, and the receipt would be matched to the transaction automatically. If the expense fell within the employee's pre-approved budget, it would be approved without any human intervention. If it exceeded a threshold or triggered a policy flag, it would route to the appropriate manager for approval. The entire process, from card swipe to fully reconciled expense, happened in minutes rather than weeks.

Approval workflows would be smart and configurable. And the entire system would integrate seamlessly with the accounting and ERP systems that finance teams already used: NetSuite, QuickBooks, Xero, SAP, and others.

To understand why this was strategically transformative, you need to understand interchange economics. Think of it this way: every time you swipe a credit card at a store, the merchant pays a small fee, typically around one and a half to three percent of the transaction. A portion of that fee flows to the bank that issued the card. By issuing corporate cards through Stripe's infrastructure, Navan positioned itself to capture a slice of interchange revenue on every single transaction made by every employee at every customer company, whether that transaction was a flight to Chicago, a team dinner in San Francisco, or a box of printer paper ordered from an office supply website. Unlike travel booking commissions, which required someone to physically get on a plane, interchange revenue flowed every time an employee swiped a card. It was a fundamentally more resilient and diversified revenue stream, decoupled from the cyclical volatility of the travel industry.

The choice to build on Stripe's issuing platform was also deliberate and consequential. Rather than building card-issuing infrastructure from scratch, which would have required banking licenses, compliance frameworks, and years of development, Navan leveraged Stripe's existing infrastructure to move fast. This partnership with Stripe, combined with a partnership with Visa for the payment network, allowed Liquid to go from concept to market in months rather than years.

Liquid launched in 2020 and grew at a pace that stunned even its creators. By October 2021, transaction volume had grown over five hundred percent, with active users up nearly four hundred percent in just six months. Expense budget under management grew fourteen hundred percent from February 2020 to July 2021. The product achieved ninety-nine percent precision on automatic expense categorization, meaning that out of every hundred transactions, only one required manual review or correction. For finance teams accustomed to chasing down crumpled receipts and manually coding expense reports, this was revelatory. The pandemic, which had nearly killed TripActions the travel company, had given birth to a fintech platform with enormous potential.

The fundraising during this period tells an extraordinary story of investor conviction. In January 2021, with business travel still deeply suppressed, Andreessen Horowitz and Addition led a 155 million dollar Series E that valued TripActions at five billion dollars. Nine months later, in October 2021, Greenoaks Capital led a 275 million dollar Series F at a 7.25 billion dollar valuation. When TechCrunch asked Cohen how a company that had gone to zero revenue just eighteen months earlier could command such a valuation, his answer was revealing: "We have fintech to thank."

The crescendo came in October 2022, when TripActions raised a 304 million dollar Series G, though the structure of this round revealed the shifting dynamics of late-stage venture capital. Of the 304 million, only 154 million was traditional equity, led by Andreessen Horowitz and Premji Invest. The remaining 150 million came from Coatue's newly created Tactical Solutions fund as structured capital, a form of financing that sits between equity and debt and typically includes downside protections that traditional equity does not. The valuation was 9.2 billion dollars. It was the high-water mark.

In total, TripActions raised approximately 780 million dollars during the pandemic period, more than doubling its valuation from four billion to over nine billion while the travel industry around it was still struggling to recover. The company had entered the pandemic as a travel booking tool. It emerged as a travel-plus-fintech platform with over 1.3 billion dollars in total private funding. The near-death experience had not just been survived. It had been alchemized into the company's greatest strategic advantage.

The narrative arc here is worth pausing on, because it illuminates something important about how great companies are forged. Without COVID, TripActions would likely have continued its path as a very successful travel management company, growing steadily, taking share from Concur, and eventually going public as a travel-tech IPO. It would have been a good company. With COVID, it was forced to confront a fundamental vulnerability: being a single-product company in a cyclical industry is a fatal structural weakness. The pivot to Liquid did not just add a revenue stream. It transformed the company's identity, its total addressable market, and its long-term competitive positioning. The combined TAM of global business travel spending, over 1.5 trillion dollars, plus corporate expense management software, projected to reach sixteen billion dollars by 2032, was vastly larger than the travel booking market alone. Cohen and Twig had turned an existential threat into a structural advantage.

And they were not done. As the world began to reopen in 2021, and as business travel slowly returned, the founders looked at their war chest and saw an opportunity that might never come again.

V. M&A and Capital Deployment: Buying the Dip or ZIRP Overpay?

The global pandemic did not just ground flights. It devastated the traditional travel management industry. Brick-and-mortar agencies that had operated for decades, companies with deep client relationships and extensive supplier networks, found themselves bleeding cash with no revenue to stanch the wound. CWT, one of the world's largest TMCs with a lineage dating back to the Ask Mr. Foster travel agency founded in 1888, filed for Chapter 11 bankruptcy in November 2021. Smaller agencies simply closed their doors.

Cohen and Twig looked at this devastation and saw what Warren Buffett would call a "fat pitch." They had something that struggling traditional travel agencies did not: a highly valued technology company's equity, a massive venture war chest replenished by the Series E and F rounds, and the confidence of investors who believed the worst was behind them.

What the traditional agencies had, and what TripActions desperately lacked, was global reach, enterprise-grade VIP service capabilities, and deep relationships with the Fortune 500 companies that TripActions aspired to serve. The company had built a brilliant product for mid-market US tech companies. But the largest potential customers, the global banks, the consulting firms, the pharmaceutical multinationals with offices in forty countries, needed something TripActions could not yet provide: agents on the ground in London, Frankfurt, Stockholm, and Mumbai who understood local markets, spoke local languages, and had relationships with local suppliers. Building that infrastructure organically would take a decade. Buying it could happen in eighteen months.

The acquisition spree began in May 2021 with Reed & Mackay, a premium UK-based travel management company founded in 1962, known for its white-glove service to senior executives and high-end corporate clients. Reed & Mackay was exactly the kind of business that TripActions could not have built organically in a reasonable timeframe. Its customer base included major financial institutions, law firms, and multinational corporations that demanded a level of personalized service, think a dedicated agent who knows your seat preference on the red-eye to London, who has your passport details memorized, and who can get you into a sold-out hotel in Tokyo at midnight, that a purely self-service software platform could not deliver. Reed & Mackay had spent nearly six decades building those relationships. TripActions bought them in a single transaction.

The strategic logic of Reed & Mackay deserves special attention because it reveals something important about the limits of pure software disruption in travel. There is a tier of corporate client, typically large financial institutions and global consulting firms, where travel management is not just logistics. It is an executive perk, a retention tool, and a competitive advantage. The C-suite at these companies expects a level of service that no algorithm can fully replicate: a human being who anticipates needs, handles exceptions with judgment, and provides the kind of concierge experience that justifies a premium price. TripActions' self-service software was brilliant for a mid-market tech company where a product manager books their own flights. It was insufficient for a managing director at Goldman Sachs who needs a complex multi-city itinerary arranged with specific airline alliances and hotel loyalty programs, often with changes made hours before departure.

The acquisitions accelerated from there, each one filling a specific geographic or capability gap.

In February 2022, TripActions acquired Comtravo, a leading German travel management company with twenty-five hundred clients and two hundred fifty employees. Comtravo brought critical capabilities for the DACH region, the German-speaking markets of Germany, Austria, and Switzerland: domestic rail booking through Deutsche Bahn integration, connections to low-cost carriers like Ryanair and EasyJet that were not available through traditional GDS channels, and VAT reclamation technology, the kind of localized infrastructure that is maddeningly difficult to build from scratch. Anyone who has tried to navigate European VAT rules across multiple jurisdictions will understand why acquiring an existing solution was vastly preferable to building one.

A month later, in March 2022, they acquired Resia AB, a Swedish TMC founded in 1974 with half a century of Nordic market expertise. In November 2022, Atlanta Events & Corporate Travel, a high-end Spanish corporate travel and events company, became the fourth European acquisition in eighteen months. And in April 2023, already rebranded as Navan, the company acquired Tripeur, a Bengaluru-based travel and expense platform that provided a beachhead into India's thirty-five billion dollar travel market, complete with local low-cost carrier integration and GST reconciliation technology.

The total European investment alone exceeded four hundred million dollars within the first year. Individual acquisition prices were not publicly disclosed, but the scale of spending was unmistakable.

The strategic debate around these acquisitions is one of the most interesting aspects of the Navan story, and it cuts to the heart of how public market investors will ultimately value the company.

The bear case is straightforward and not unreasonable. TripActions was, at its core, a technology company with software-like gross margins and a compelling narrative about replacing legacy systems with elegant automation. Buying brick-and-mortar travel agencies, businesses that rely on human agents, earn thin margins on transaction fees, and operate with legacy technology stacks, diluted that narrative. Integration of acquired companies is notoriously difficult even in the best circumstances. Doing it across multiple countries, languages, regulatory environments, and technology platforms simultaneously, while also building a fintech product and managing a post-pandemic recovery, was an extraordinarily ambitious undertaking. And these acquisitions were made during the ZIRP era, when asset valuations were inflated by historically low interest rates. Did they overpay?

The bull case is equally compelling. Cohen and Twig executed a masterful arbitrage. They bought distressed assets at a moment of maximum dislocation, using highly valued technology equity as currency. They acquired something that money cannot normally buy quickly: local inventory, on-the-ground expertise in dozens of European markets, enterprise-grade VIP service capabilities, and massive customer bases that would have taken years to win through organic sales. Overnight, TripActions went from being a mid-market US technology tool to a global enterprise player capable of serving Fortune 500 companies with operations in dozens of countries. The Reed & Mackay acquisition alone opened doors to a tier of client that TripActions' self-service platform, however elegant, could never have reached on its own.

The result of this acquisition blitz was a company that looked fundamentally different from the one that had entered the pandemic. By 2023, Navan had offices and operations across the United States, United Kingdom, Germany, Sweden, Spain, India, and beyond. Its customer count exceeded ten thousand active accounts. Its gross booking volume was climbing toward eight billion dollars annually. It was no longer a Silicon Valley startup trying to disrupt corporate travel. It was a global platform, a hybrid of software automation and human expertise, competing head-to-head with the largest travel management companies in the world.

Whether the acquisitions were brilliant strategic plays or ZIRP-fueled overreach is a question that will ultimately be answered by how successfully Navan integrates these businesses onto a unified technology platform. The company announced plans to fold the Reed & Mackay brand entirely, migrating all customers to the Navan platform. That integration process is ongoing, and its success or failure will be one of the defining variables in Navan's trajectory as a public company.

There is an important precedent worth noting here. When SAP acquired Concur in 2014 for 8.3 billion dollars, it took years to fully integrate Concur's technology into SAP's broader enterprise suite, and many would argue the integration is still incomplete a decade later. Technology acquisitions of traditional service businesses are notoriously difficult because the two cultures, software engineering velocity versus relationship-driven client service, often clash in fundamental ways. Navan is attempting to do what SAP struggled with, but across five acquisitions simultaneously, in five different countries, and in a fraction of the time.

The international revenue mix tells the story of where the acquisitions have taken the company. By fiscal 2025, forty-one percent of Navan's total revenue, approximately 221 million dollars, came from outside the United States. That is a dramatic transformation from the pre-acquisition era, when the company was overwhelmingly a US-centric mid-market player. The question is whether that international revenue carries the same margin profile as the software-driven US business, or whether it is diluted by the higher cost structure of acquired TMC operations.

VI. Current Management & Governance

In an era when many high-profile technology companies have cycled through multiple CEOs, chief product officers, and strategic pivots by the time they reach the public markets, Navan remains firmly founder-led. Ariel Cohen serves as CEO, Co-Founder, and Chairman of the Board. Ilan Twig serves as CTO and Co-Founder. Their dynamic, Cohen as the relentless go-to-market visionary and Twig as the deeply technical product architect, has remained the company's operational spine since 2015.

The governance structure reflects this founder centrality in ways that are both unusual and consequential for public market investors. Navan operates a dual-class share structure, a governance mechanism that has become common among founder-led technology companies but remains controversial among institutional investors and proxy advisory firms.

Class A shares, the ones traded publicly on the NASDAQ, carry one vote per share. Class B shares, held by the founders and certain insiders, carry thirty votes per share. The arithmetic is stark: Cohen controls approximately twenty-four percent of total voting power, and Twig controls approximately forty-three percent. Combined, the co-founders hold roughly sixty-seven percent of the company's voting power, giving them effective majority control over all corporate decisions, from executive compensation to M&A strategy to capital allocation.

For investors, this structure cuts both ways. On the positive side, it insulates the company from short-term activist pressure and allows management to make long-term strategic decisions without fear of a hostile board challenge. Given that Navan's strategy requires patient execution, integrating five international acquisitions, building out a fintech platform, and driving toward profitability, having stable founder control can be an advantage. On the negative side, it means that public shareholders have essentially no recourse if they disagree with management's decisions. If Cohen and Twig decide to pursue an acquisition, a compensation plan, or a strategic pivot that public shareholders oppose, there is nothing those shareholders can do about it short of selling their stock. This is a structure that demands trust, and trust must be earned through execution.

The board itself reflects a blend of venture capital expertise and operational experience. Ben Horowitz of Andreessen Horowitz has been on the board since the Series C in 2018, a relationship that traces back to the founders' Opsware days. Arif Janmohamed of Lightspeed, who wrote the first check, remains on the board. Shai Weiss, the former CEO of Virgin Atlantic, was appointed in January 2026, bringing deep airline industry expertise. The remaining directors include Oren Zeev, Mike Kourey, Clara Liang, Sandesh Patnam, and Anre Williams.

One area that warrants particular attention is the CFO position. The chief financial officer is the single most important executive for a newly public company outside of the CEO. This is the person who sets the tone for investor communications, oversees financial reporting, and serves as the bridge between the operational reality of the business and the expectations of Wall Street. Stability in this role is critical, especially in the first year of public trading.

Since the company's IPO preparation, Navan has cycled through an unusual number of chief financial officers. Thomas Tuchscherer, formerly of Snowflake, stepped down in November 2023. Ram Bartov succeeded him. Amy Butte was then brought in specifically to shepherd the IPO process. She accomplished that mission, but departed effective January 9, 2026, just six weeks after the company's first public earnings report, receiving a 3.7 million dollar one-time cash payment and accelerated vesting of all unvested equity. Anne Giviskos served as interim CFO until Aurelien Nolf, formerly of Lyft, took over on March 2, 2026.

Four CFOs in roughly two years is not ideal for a newly public company, and it raises legitimate questions about internal dynamics, financial reporting complexity, and the relationship between the finance function and the founders who maintain operational control. The class action lawsuits filed in early 2026 add another layer of governance concern. Multiple law firms have filed claims alleging that the IPO documents failed to adequately disclose a thirty-nine percent increase in sales and marketing spending in the quarter immediately following the IPO, with a lead plaintiff deadline of April 24, 2026. These lawsuits are common for companies that experience significant stock declines in the months after an IPO, and many are ultimately dismissed or settled for modest amounts. But they create uncertainty and distract management attention at a critical period.

On the compensation front, the structural incentives have shifted notably from the growth-at-all-costs mentality of 2019 to a focus on unit economics and profitability. Management has publicly committed to achieving free cash flow positivity by fiscal year 2027, and guided for non-GAAP operating income of twenty-one to twenty-two million dollars in fiscal 2026, a meaningful milestone for a company that posted over three hundred million dollars in GAAP net losses just two years prior.

There is one data point that cuts against the governance concerns. Andreessen Horowitz, through Ben Horowitz's personal involvement on the board, has been actively buying shares in the open market. Horowitz purchased 3.57 million dollars worth of stock on December 23, 2025, and made additional purchases in January 2026, even as the stock was declining. Insider buying is one of the few signals that is genuinely hard to fake. Board members who are spending their own money at prices well below the IPO level are expressing a form of conviction that no earnings call commentary can replicate. It does not guarantee the stock will recover, but it does suggest that the people closest to the company's operations believe the market is mispricing it.

VII. The "Navan" Era & The Hidden Growth Engines

On February 7, 2023, TripActions ceased to exist. The company filed a trademark application in August 2022, and five months later, the rebrand was official: the company was now Navan. The name, a palindrome combining "navigate" and "avant," the French word for "forward," was designed to signal something fundamental. This was no longer just a trip-booking tool. The "Actions" in "TripActions" had been upgraded to a broader ambition: business software designed for people.

The rebrand was not cosmetic. It reflected a genuine expansion of the company's product surface area, and within that expansion lie the growth engines that make the Navan thesis most compelling. When a company changes its name, it is either running from something or running toward something. In TripActions' case, it was the latter. The word "Trip" in the name actively limited the company's ability to sell expense management, corporate cards, and payment processing. Customers and prospects kept pigeonholing TripActions as "the travel company," even as the Liquid fintech product was growing at triple-digit rates. The rebrand was an exercise in removing a strategic ceiling.

The name "Navan" itself was carefully chosen. It reads the same forwards and backwards, symbolizing the seamless loop the company was trying to create: from booking to payment to expense reconciliation and back again. The tagline became "Business Software Designed for People," a phrase that deliberately positioned the company against the entire legacy B2B software stack, not just travel or expense management, but the fundamental philosophy of enterprise software design.

The first of these is Navan Connect, and it might be the single most strategically important product the company has built. To understand why, you need to understand the biggest obstacle any fintech company faces when selling to enterprises: the switching cost of changing corporate cards.

Large companies have deep, complex relationships with their banks. They might have a twenty-year relationship with Citi or American Express, with corporate cards issued to thousands of employees, rewards programs negotiated at the institutional level, credit lines structured around the company's balance sheet, and integrations woven into their accounting systems. Telling a CFO to rip all of that out and switch to a Navan-issued card is, in many cases, a non-starter. The value of the Navan software is obvious, but the switching cost of the financial infrastructure is prohibitive.

Navan Connect solves this with a deceptively elegant approach. Instead of requiring companies to switch cards, it lets them link their existing Visa, Mastercard, or American Express corporate cards directly to the Navan platform.

Here is how it works in practice. Visa and Mastercard transactions stream in real time through direct integration with the card networks. American Express transactions are reported daily through a separate feed. When an employee books travel through Navan using their linked card, the platform generates a virtual card for each transaction, automatically matching payment details to the correct booking and invoice. The traveler never has to enter payment information manually, never has to front their own money, and never has to submit an expense report. The entire booking-to-reconciliation loop closes automatically, regardless of which bank issued the underlying card.

This is what Cohen calls the "Trojan Horse," and the metaphor is apt. Navan Connect eliminates the highest-friction barrier to enterprise adoption. A company's CFO does not have to change banks, does not have to renegotiate credit terms, does not have to give up their beloved Amex rewards. They simply get the Navan software layer on top of their existing financial infrastructure. And once the software is deployed, once employees are using it daily and the company's travel policies are configured and the ERP integrations are built, the switching costs start working in Navan's favor. Connect streams data from over two hundred fifty global banks and has partnerships with both Citi and American Express for card-linking capabilities.

The second hidden growth engine is personal travel, and it represents a form of product design genius that most enterprise software companies never consider.

Navan allows employees at customer companies to book personal vacations, weekend trips, and family holidays through the same app they use for business travel. The employee pays with their personal card, keeping the expense entirely separate from their employer's billing. But they get access to corporate-negotiated rates and discounts that are typically not available on consumer booking sites, plus Navan's twenty-four-seven customer support, plus the ability to earn rewards on both business and personal bookings. Think about what that means: an employee at a Navan customer company can book a flight to Cancun for their family vacation and pay less than they would on Expedia, because they are benefiting from the bulk rates that Navan negotiates with airlines on behalf of its corporate client base.

The strategic brilliance here is multifold and worth unpacking in detail, because personal travel may be the most underappreciated element of the Navan thesis.

First, it transforms usage patterns. Most B2B enterprise software gets used during working hours, for work purposes, and only when necessary. Nobody opens their expense management tool for fun on a Saturday morning. But personal travel changes that equation entirely. Employees open Navan to browse flights for their honeymoon, to find a weekend Airbnb, to price out a family ski trip. This creates what technology companies call daily active users, a metric that separates sticky platforms from shelf-ware. The more often someone opens the app, the more habitual it becomes, and the harder it is for a competitor to displace.

Second, it creates bottom-up advocacy. In traditional enterprise software sales, the decision to adopt a platform is made by the CFO or the head of procurement. Individual employees have little say. But when those employees are booking their personal vacations through Navan and genuinely enjoying the experience, they become advocates. If a procurement team evaluates switching to a cheaper competitor, the pushback from thousands of employees who love their personal travel experience creates a powerful internal resistance to change. It is switching costs generated through delight rather than contractual obligation.

Third, personal travel provides a high-margin revenue stream that is completely decoupled from the B2B sales cycle. In the first quarter of 2023, personal travel volume on the platform grew forty-four percent year over year, and by summer 2023, personal bookings were up fifty-three percent. This revenue does not require an enterprise sales team, does not require a procurement process, and does not depend on corporate travel budgets. It is consumer revenue flowing through an enterprise platform, a rare and valuable hybrid.

Looking at the overall segment dynamics, it is important to understand how Navan actually makes money, because the revenue model is more complex than a simple SaaS subscription.

Navan's revenue breaks down roughly ninety percent usage-based and ten percent subscription. The usage-based revenue has multiple components: per-booking fees charged to the customer company each time an employee books travel, supplier and partner transaction fees earned from airlines, hotels, and other travel suppliers, and interchange revenue from Navan-issued corporate cards. The subscription revenue comes primarily from Navan Expense, the expense management software, which charges a per-seat fee. The company processed 7.6 billion dollars in gross booking volume in fiscal 2025, up thirty-four percent year over year, with 3.7 billion dollars in payment volume flowing through its corporate card program.

This revenue model has important implications for how investors should think about the business. Unlike a pure SaaS company where revenue is highly predictable and contractual, ninety percent of Navan's revenue is tied to actual usage. If a customer company has a bad quarter and cuts its travel budget, Navan's revenue from that customer declines proportionally. If the economy enters a recession and companies broadly reduce travel spend, Navan's top line is directly exposed. This usage sensitivity is the trade-off for the upside: when companies increase travel spend, Navan benefits immediately without needing to renegotiate contracts.

The margin profile is improving steadily. GAAP gross margins expanded from sixty percent in fiscal 2024 to sixty-eight percent in fiscal 2025, and hit seventy-four percent on a non-GAAP basis in the most recent quarter. Revenue yield on gross booking volume runs approximately seven to eight percent, meaning that for every hundred dollars of travel booked through the platform, Navan captures seven to eight dollars in revenue. The international business, built largely through the acquisition spree, now represents forty-one percent of total revenue.

Most recently, Navan has begun deploying artificial intelligence in ways that have material implications for its cost structure. The company launched Ava, an AI-powered assistant built on OpenAI's models, which now handles fifty percent of customer support interactions end-to-end, replacing the work of hundreds of human agents. To put that in perspective: before Ava, every flight delay, every hotel rebooking, every expense policy question required a human support agent to respond. At Navan's scale, with over ten thousand active customer companies and millions of individual travelers, that meant a massive and growing customer support organization. When an AI agent can resolve half of those interactions autonomously, the cost savings flow directly to the bottom line. It is one of the clearest examples in enterprise SaaS of AI delivering measurable margin expansion rather than serving as a marketing buzzword.

In early March 2026, just days before this writing, Navan unveiled two new AI products. Navan Edge is an AI-powered executive assistant designed specifically for frequent business travelers, the kind of person who takes fifty or a hundred flights a year and needs an intelligent system that anticipates their needs, proactively rebooks around disruptions, and manages complex multi-city itineraries without human intervention. Navan Cognition is an agentic AI platform, a system designed to execute multi-step workflows autonomously rather than simply answering questions. The trajectory is clear: Navan is moving from "AI assists human agents" to "AI replaces human agents for the majority of interactions," and management has pointed to this shift as a primary driver of the path to free cash flow positivity by fiscal 2027.

The AI strategy also reinforces the switching cost moat. As Ava learns the preferences, policies, and patterns of each customer company, the AI becomes more valuable and more accurate over time. Switching to a competitor means losing that accumulated intelligence and starting the learning curve from scratch.

VIII. Analysis: 7 Powers & Porter's Five Forces

Step back from the product-level narrative for a moment and assess Navan's strategic position through two of the most rigorous frameworks available: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. These frameworks cut through marketing narratives and reveal whether a company's advantages are durable or ephemeral.

Through the lens of Hamilton Helmer's 7 Powers framework, Navan's strongest advantage is counter-positioning. This is arguably the most important of Helmer's seven powers because it is the one most available to challengers in the early stages of competition, and it is the one that is hardest for incumbents to neutralize.

In the early years, TripActions' employee-first UX and rewards-based incentive model represented something that SAP Concur fundamentally could not adopt without destroying its own business model. Concur's architecture, its pricing (per expense report), its product philosophy (CFO-first compliance), and its customer relationships were all built around enforcement and control. Adopting an employee rewards program or a consumer-grade mobile interface would require a ground-up rebuild that would disrupt its massive installed base, break thousands of enterprise integrations, and alienate the finance executives who write the checks.

The same dynamic applies to traditional TMCs like Amex GBT and BCD Travel, whose revenue depends on high-touch, labor-intensive agent services. Moving to a self-service software model would cannibalize the very service that justifies their fees. An Amex GBT executive cannot walk into a board meeting and propose eliminating travel agents, because travel agents are what Amex GBT sells. The counter-positioning is structural, not temporary.

The second significant power is switching costs, and these are increasing over time. Once an enterprise deploys Navan across its organization, integrating travel policies, corporate card issuance, expense workflows, ERP connections to systems like NetSuite, SAP, and Workday, HR system integrations, and employee adoption, the cost of ripping it out and replacing it with a competitor becomes substantial. The data layer compounds this: years of traveler preferences, booking history, negotiated rates, and policy configurations accumulate and create information-based lock-in. Navan reports platform adoption rates of eighty-two to ninety percent among deployed customers, meaning the software becomes genuinely embedded in daily operations.

Scale economies are emerging as the third power, and they operate on multiple levels simultaneously. At the supply level, with 7.6 billion dollars in annual gross booking volume and growing, Navan can negotiate better rates with airlines, hotels, and car rental companies than smaller competitors. This creates a virtuous cycle: better rates attract more customers, which increases volume, which enables even better rate negotiations. At the technology level, the AI and machine learning models that power Ava and automated expense categorization improve with more data, creating data-driven product advantages that new entrants cannot easily replicate. And at the cost level, the fixed costs of platform development, compliance infrastructure, and GDS integration are spread across a growing customer base, improving unit economics over time. The company's gross margin expansion from sixty percent to seventy-four percent in roughly two years is evidence that these scale effects are real and accelerating.

Network effects remain relatively weak compared to consumer platforms. Unlike a social network where each additional user directly improves the experience for all other users, or a marketplace where more sellers attract more buyers and vice versa, Navan's value proposition is fundamentally about the quality of its software and the breadth of its supply network rather than the size of its user base. There are emerging supplier network effects: more travelers on the platform give Navan more negotiating leverage with airlines and hotels, which enables better rates, which attracts more companies. But these are modest compared to the network effects enjoyed by true marketplace businesses, and they are shared with any competitor that achieves similar booking volume.

Through Porter's Five Forces lens, the competitive dynamics are complex and revealing.

Competitive rivalry is high and intensifying from multiple directions simultaneously. Navan faces a unique strategic challenge in that it competes across three distinct competitive fronts, each with formidable opponents.

In travel management, it faces SAP Concur, which holds nearly fifty percent of the expense management software market and has the backing of one of the world's largest enterprise software companies. It also faces Amex GBT, the world's largest TMC with 2.4 billion dollars in annual revenue, which recently absorbed CWT and announced a partnership with Concur.

In fintech and corporate cards, Navan competes with Ramp, which reached a staggering thirty-two billion dollar private valuation by late 2025 with revenue exceeding one billion dollars annualized and fifty thousand customers. It also faces Brex, which, while being acquired by Capital One for 5.15 billion dollars, will gain the backing of one of America's largest financial institutions.

And in the emerging "super app" category, Navan faces the risk that each of these competitors will converge on its integrated model. Travel companies are adding expense management. Card companies are adding travel booking. Everyone is layering in AI. Even Expensify, which started as a simple receipt-scanning app, has relaunched as a combined travel and expense platform. TravelPerk, a European competitor, rebranded itself as simply "Perk" to signal its expansion beyond travel. The competitive landscape is not static. It is converging from all directions.

Buyer power is moderately high, particularly among large enterprises that have significant negotiating leverage and can demand custom pricing, dedicated support, and bespoke integrations. The procurement process for enterprise travel and expense platforms is lengthy and involves multiple stakeholders, from the CFO to the IT department to the head of procurement, each with different priorities. Smaller companies have less individual leverage but are highly price-sensitive and can switch platforms more easily, making the SMB segment intensely competitive.

The threat of substitution is moderate but structurally important. Video conferencing platforms like Zoom and Microsoft Teams permanently replaced some categories of business travel after COVID, particularly internal meetings, routine check-ins, and training sessions. When adjusted for inflation, actual travel volumes remain below 2019 levels even as nominal spending has recovered to approximately 1.5 trillion dollars globally. The risk is not that video conferencing replaces all business travel, it clearly will not for client relationships, deal closings, or team offsites, but that it permanently reduces the ceiling of the market.

Supplier power is moderate. Airlines, hotels, and Global Distribution System providers like Amadeus, Sabre, and Travelport are essential inputs and have significant leverage. GDS providers in particular are concentrated, and their fees represent a meaningful cost for any travel platform. However, the shift toward NDC, or New Distribution Capability, an industry standard that allows airlines to distribute fares directly to booking platforms without going through a GDS, is gradually reducing this dependency. Navan has been building direct connections with airlines, which over time should improve both margins and the breadth of available fare options. The threat of new entrants is moderate: the barriers are meaningful, including GDS integration costs, regulatory complexity across jurisdictions, and the need for deep supplier relationships, but API-first architectures and partnership models are lowering technology barriers for companies that want to compete in one slice of the market rather than the whole thing.

IX. The IPO and Market Reality: Bear vs. Bull Case

The path to the public markets was neither smooth nor triumphant, and the IPO story itself reads like a case study in the gap between private market euphoria and public market reality.

Navan originally filed confidential IPO paperwork in 2022, during the final months of the ZIRP era, with plans to debut at roughly twelve billion dollars. Then the Federal Reserve began raising interest rates aggressively. The IPO window for high-growth, unprofitable technology companies slammed shut. Instacart, Klaviyo, and Arm all priced their IPOs below expectations in 2023. The message from public market investors was clear: growth without profitability was no longer sufficient. Navan shelved its IPO plans and went to work on its margin profile.

By the time the company filed its S-1 publicly on September 19, 2025, the target valuation had been cut nearly in half. The S-1 itself revealed a company in transition: 537 million dollars in fiscal 2025 revenue, up thirty-three percent year over year, with improving gross margins but still carrying a 181 million dollar GAAP net loss. The filing also disclosed the full scale of the company's stock-based compensation, a common concern for newly public tech companies where equity grants to employees can represent a significant ongoing dilution to public shareholders.

The IPO itself was historic for an unusual reason. Navan priced its offering at twenty-five dollars per share on October 29, 2025, during a United States government shutdown that had closed the Securities and Exchange Commission. With SEC staff furloughed and no one available to declare registration statements effective, most companies would have simply waited. Navan chose a different path. The company used a rarely invoked regulatory workaround under Section 8(a) of the Securities Act of 1933, which allows registration statements to become automatically effective twenty days after filing, bypassing the need for manual SEC review. The bulk of the S-1 had already been reviewed before the shutdown, and the company's legal team at Cooley was confident the approach was sound. It was a bold, lawyerly maneuver that underscored management's urgency to access the public markets before the window closed again.

On October 30, 2025, Navan began trading on the NASDAQ Global Select Market under the ticker NAVN. The company raised 923 million dollars from approximately thirty-seven million shares, with Goldman Sachs, JPMorgan, and Morgan Stanley serving as lead underwriters. But the first day was painful. The stock opened at twenty-two dollars, twelve percent below the IPO price, and closed down roughly twenty percent, valuing the company at approximately 4.7 billion dollars, well below both the six billion dollar IPO valuation and the 9.2 billion dollar last private round.

The IPO day decline was not unique to Navan. It reflected a broader skepticism that public market investors harbored toward high-growth, unprofitable technology companies in the post-ZIRP era. But it was particularly sharp for a company that had been valued at 9.2 billion dollars just three years earlier. The math was uncomfortable for late-stage private investors: shares that were worth 9.2 billion in aggregate on paper in October 2022 were now trading at less than half that amount in the public market. The Series G investors who purchased structured capital with downside protections may have fared better than the common equity holders, but the valuation compression was still significant across the cap table.

Matters deteriorated further in December 2025. When Navan reported its first public quarterly results on December 15, the headline numbers looked strong: revenue of 195 million dollars, up twenty-nine percent year over year, with gross booking volume of 2.6 billion dollars, up forty percent. Non-GAAP gross margins hit a record seventy-four percent. But investors focused on the negatives. GAAP loss from operations widened to seventy-nine million dollars from nineteen million in the prior year quarter, driven by a thirty-nine percent spike in sales and marketing expenses to ninety-five million dollars. The concurrent departure of CFO Amy Butte, just six weeks after the IPO, added fuel to the selloff. The stock fell nearly twelve percent in a single session.

By March 2026, NAVN traded around ten dollars, down more than sixty percent from its IPO price and roughly seventy-three percent below its last private valuation. Multiple class action lawsuits were filed, alleging that the IPO documents failed to adequately disclose the jump in post-IPO spending.

The bear case is built on several legitimate concerns, and responsible analysis requires taking each one seriously.

First, the total addressable market for business travel may be structurally smaller than it was pre-COVID. While nominal spending has recovered to approximately 1.5 trillion dollars, when adjusted for inflation in airfares, hotel rates, and ground transportation, actual travel volumes remain below 2019 levels. Companies have permanently replaced some travel with video conferencing. The internal quarterly business review that once required flying six regional directors to headquarters now happens on Zoom. The routine client check-in that once justified a cross-country flight now happens on Teams. The question is whether the remaining travel, the high-value sales meetings, the deal closings, the team offsites, is enough to sustain the growth assumptions embedded in Navan's valuation.

Second, the fintech side of the business faces ferocious competition. Ramp, valued at thirty-two billion dollars and growing revenue over one hundred percent annually, is aggressively moving into travel. Brex, though being acquired by Capital One, will gain the backing of one of America's largest banks. Navan's ten percent subscription revenue mix means the business is overwhelmingly usage-based and transactional, which public market investors tend to value at lower multiples than recurring SaaS revenue. A company with ninety percent usage-based revenue looks more like a payments processor than a software company, and payments processors trade at meaningfully lower multiples.

Third, the M&A integration risk is real and should not be minimized. Folding Reed & Mackay, Comtravo, Resia, Atlanta Events, and Tripeur onto a unified platform, across different countries, languages, currencies, and regulatory environments, while maintaining service quality and customer relationships, is an execution challenge of enormous complexity. Each acquired company brought its own technology stack, its own customer management processes, and its own organizational culture. Harmonizing all of that while simultaneously building new products and driving toward profitability is the kind of multi-variable challenge that has derailed many ambitious companies before.

Fourth, the CFO turnover and securities litigation create governance overhang that may weigh on institutional investor sentiment until resolved.

The bull case rests on a powerful structural argument that is worth articulating in full, because if it is correct, the current stock price represents a significant opportunity.

Navan is the only company that owns the entire lifecycle of corporate spend on travel and employee expenses within a single integrated platform. Think about what that means in practice. When a product manager at a Navan customer company books a flight to visit a client, the booking happens in Navan. The payment flows through a Navan-issued or Navan-connected card. The expense is automatically categorized and reconciled in Navan. The receipt is captured by Navan. The approval workflow runs through Navan. The data flows into the company's ERP system via Navan's integration layer. At no point in this entire journey does the user touch a second application. Every step generates data and revenue for Navan.

No competitor replicates this end-to-end chain. Ramp and Brex do not own travel booking infrastructure; Ramp's travel product relies on a partnership with Priceline rather than native inventory. Concur does not own modern fintech or card-issuing capabilities. Amex GBT does not own consumer-grade software. By combining booking, card issuing, and expense reconciliation into one super app, Navan captures the full chain of value creation, from the moment an employee searches for a flight to the moment the expense is reconciled in the company's general ledger. The market it addresses is enormous: global business travel spending alone exceeds 1.5 trillion dollars, and the corporate expense management software market is projected to grow to over sixteen billion dollars by 2032.

The financial trajectory, despite the stock performance, supports the thesis. Revenue grew thirty-three percent in fiscal 2025 to 537 million dollars, and management has guided for twenty-eight percent growth in fiscal 2026, reaching approximately 685 million dollars. That would put Navan on a path to approach one billion dollars in annual revenue within the next two to three years if current growth rates hold.

Gross margins have expanded from sixty percent to sixty-eight percent in two years, with the most recent quarter hitting seventy-four percent on a non-GAAP basis. The company achieved non-GAAP net income of nine million dollars in the most recent quarter, a meaningful inflection from the fourteen million dollar non-GAAP net loss in the prior year period. Management has committed to free cash flow positivity by fiscal 2027, and AI-driven automation, particularly the Ava assistant handling fifty percent of support interactions, provides a credible path to structural margin expansion.

The two KPIs that matter most for tracking Navan's trajectory going forward are gross booking volume growth and non-GAAP gross margin.

GBV growth is the vital sign of the platform's competitive health. It measures whether Navan is winning new customers, expanding within existing accounts, and taking share from competitors. Because roughly ninety percent of Navan's revenue is usage-based, tied directly to booking and payment transactions, GBV growth is the single best leading indicator of future revenue. In the most recent quarter, GBV grew forty percent year over year to 2.6 billion dollars, outpacing revenue growth of twenty-nine percent. That gap between GBV growth and revenue growth bears watching: it could indicate improving platform adoption (bull case) or it could indicate declining revenue yield per booking (bear case). Either way, GBV is the number to track.

Non-GAAP gross margin is the measure of Navan's transition from a hybrid technology-plus-services business to a software-driven platform. The trajectory has been encouraging: from sixty percent in fiscal 2024 to sixty-eight percent in fiscal 2025 to seventy-four percent in the most recent quarter. Every percentage point of gross margin expansion represents the replacement of human labor with software automation. If gross margins continue climbing toward seventy-five or eighty percent, it validates the thesis that Navan can achieve software-like economics despite operating in a traditionally services-heavy industry. If margins plateau or decline, it suggests the acquired TMC operations are dragging on the company's ability to scale efficiently.

The wild card is the competitive landscape, which is shifting rapidly. Amex GBT, having absorbed CWT for 540 million dollars in September 2025, is now the undisputed giant of traditional managed travel, with 2.4 billion dollars in revenue and operations in over 140 countries. In December 2025, Amex GBT announced a partnership with SAP Concur, effectively combining the world's largest TMC with the world's largest expense management software platform. On paper, this is the nightmare scenario for Navan: its two biggest legacy competitors joining forces. Navan's CEO responded by calling the partnership "antiquated" and "irrelevant," but the combination of Amex GBT's distribution and Concur's install base, nearly half of the enterprise expense management market, cannot be dismissed lightly. The question is whether a partnership between two legacy platforms can deliver the kind of integrated, consumer-grade experience that Navan offers natively, or whether it will be a clunky Frankenstein of bolted-together systems that reinforces Navan's counter-positioning advantage.

Meanwhile, Ramp's trajectory is breathtaking and demands serious attention. Founded in 2019, Ramp went from zero to a thirty-two billion dollar valuation by late 2025, with revenue hitting a billion dollars annualized, fifty thousand customers, and over a hundred billion dollars in annual purchase volume. Ramp started as a corporate card company, but it has aggressively expanded into bill payments, procurement, and most importantly for Navan, travel booking via a partnership with Priceline. Nearly half of Ramp's customers now use more than one Ramp product, demonstrating the power of the platform bundling strategy. Ramp's travel product is less mature than Navan's, relying on a third-party partnership rather than native inventory, but the trajectory of expansion is unmistakable.

The Capital One acquisition of Brex for 5.15 billion dollars, announced in January 2026, will create yet another formidable competitor with vast banking resources, an established enterprise customer base, and the ability to offer credit products that a standalone fintech cannot match. Navan's challenge is to stay ahead of converging competitors who are attacking from multiple directions simultaneously, each with significant resources and distinct structural advantages.

X. Epilogue & Playbook Lessons

The Navan story offers several lessons that extend well beyond the corporate travel industry, and they are worth examining because they illuminate patterns that are playing out across the broader enterprise software landscape.

The first is about the power of the pivot, and it challenges the conventional wisdom about how companies should respond to existential crises. When COVID-19 hit, the playbook for most venture-backed companies was straightforward: cut costs, conserve cash, and wait for the storm to pass. Cohen and Twig did cut costs, painfully, letting go of a quarter of their workforce in a single week. But they refused to simply wait. Instead of reducing engineering headcount, they redirected their remaining engineering talent toward a problem that was right in front of them: if people are not traveling, they are still spending, and the tools for managing that spending are just as broken as the tools for managing travel.

This is a critical distinction. TripActions Liquid was not a desperate Hail Mary. It was a disciplined identification of an adjacent market opportunity that shared the same customer base, the same integration points, and the same product philosophy. The same finance team that bought TripActions for travel booking was the natural buyer for an expense management tool. The same ERP integrations that connected travel bookings to the general ledger could connect corporate card transactions. The same employee who booked a flight could now swipe a corporate card at a restaurant. Everything connected. The COVID pivot did not just save the company. It expanded its addressable market by an order of magnitude and gave it a structural advantage that no competitor has yet replicated: the only truly integrated travel-plus-fintech-plus-expense platform built from the ground up.

The second lesson is about software eating services, and Navan is one of the clearest case studies of this phenomenon playing out in a traditionally human-intensive industry. The corporate travel industry was, for decades, defined by personal relationships between travel agents and their corporate clients. Booking a complex international itinerary required a trained travel agent with access to GDS terminals, supplier relationships, and deep knowledge of visa requirements, airline alliances, and fare rules. Dozens of phone calls, emails, and faxes might be exchanged for a single multi-city booking. The entire industry was built on human labor.