Myriad Genetics: The Rise, Fall, and Reinvention of Precision Medicine

Introduction and Episode Roadmap

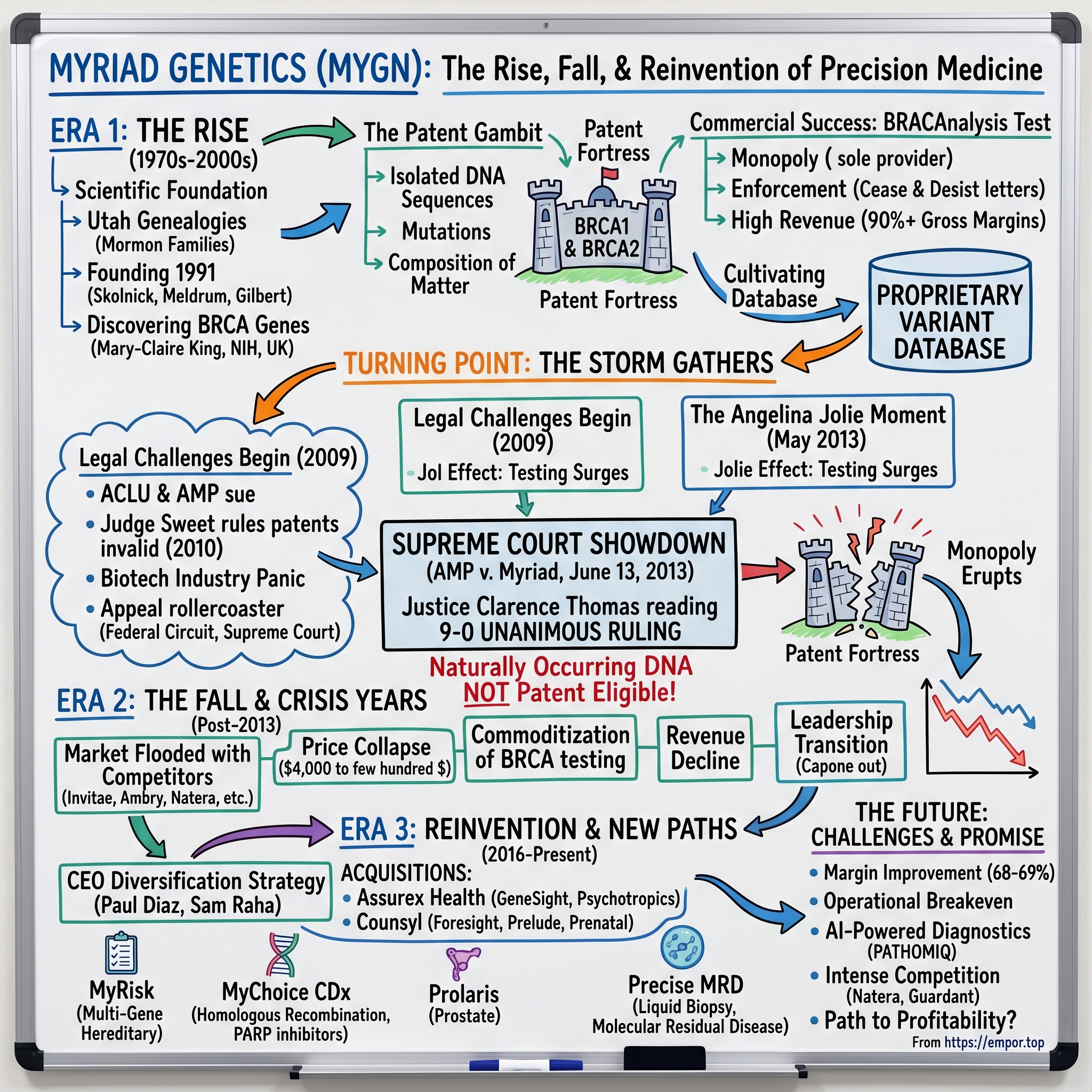

Picture a conference room in Washington, D.C., on a warm June morning in 2013. Lawyers, journalists, patent attorneys, cancer researchers, and patient advocates crowd the hallways of the Supreme Court building, waiting for a ruling that will reshape American biotechnology. At exactly ten-thirty, Justice Clarence Thomas begins reading an opinion that nine justices — every single one of them — have agreed upon. The words are measured, precise, and devastating for one company in particular: "A naturally occurring DNA segment is a product of nature and not patent eligible merely because it has been isolated."

At the center of that opinion sat a company from Salt Lake City, Utah, that had done something remarkable and deeply controversial: it had claimed ownership of two human genes. The company was Myriad Genetics.

Founded in 1991, Myriad had built one of the most extraordinary business moats in the history of healthcare. For nearly two decades, if a woman wanted to know whether she carried a mutation in the BRCA1 or BRCA2 genes — mutations that could dramatically increase her lifetime risk of breast and ovarian cancer — she had exactly one option. She could pay Myriad roughly four thousand dollars for a test called BRACAnalysis, and no one else in the United States could legally offer her that information. That is what a true monopoly looks like.

At its peak, Myriad generated more than eight hundred million dollars in annual revenue, employed thousands, and had accumulated over two and a half billion dollars in cumulative BRCA testing revenue. Then, in a single morning in June 2013, the legal foundation of that entire business model evaporated. The Supreme Court ruled unanimously that naturally occurring DNA segments are products of nature and cannot be patented, no matter how brilliantly they were discovered or how much money was spent isolating them.

The central question of this story is deceptively simple: How did a company go from owning the most valuable genes in medicine to losing it all — and can it survive? The answer takes us through the Mormon genealogies of Utah, an international scientific race, one of Hollywood's most famous women, a landmark Supreme Court case, a pandemic, corporate reinvention, and the ongoing battle for the future of genetic testing.

This is a story about intellectual property, scientific ambition, monopoly power, and the tension between innovation and access that defines American healthcare. It is also a story about resilience, because despite everything, Myriad Genetics is still here — publicly traded on the NASDAQ at roughly five dollars a share as of early 2026, a fraction of its former glory, but still employing thousands of people, still processing hundreds of thousands of tests annually, and still trying to find its place in a world it helped create but can no longer control.

For investors, the Myriad story is a masterclass in distinguishing between temporary and permanent competitive advantages. For founders, it is a cautionary tale about building businesses on legal moats rather than operational ones. For the healthcare industry, it is a case study in the inevitable collision between innovation incentives and patient access. And for anyone interested in the future of medicine, it is a window into the forces that will shape how we use — and who will profit from — the most personal information in existence: the code written in our DNA.

The Scientific Revolution: Genomics Comes of Age

To understand Myriad Genetics, you have to start with a woman named Mary-Claire King and an obsession that consumed seventeen years of her life. Beginning in the early 1970s at the University of California, Berkeley, King set out to prove something that many geneticists at the time considered either obvious or impossible: that certain breast cancers run in families because of inherited mutations in a single, identifiable gene.

The scientific establishment was skeptical. Breast cancer was common, messy, and multifactorial. The idea that a single gene could be responsible for a meaningful fraction of cases seemed reductive. But King had a crucial insight. When she reorganized her family data by age of onset, the signal leaped out of the noise. Early-onset breast cancer — women getting the disease in their thirties and forties — showed a dramatically stronger pattern of inheritance than later-onset cases. In 1990, after nearly two decades of painstaking pedigree analysis and linkage mapping, King published a landmark paper demonstrating that a region on chromosome 17q21 was linked to hereditary breast and ovarian cancer. She named this locus BRCA1.

To put this in plain terms: imagine you know that somewhere in a particular city there is a building that, when faulty, causes disasters. King had identified the city and the neighborhood, but she had not found the exact building or understood its blueprints. That set off one of the most intense races in the history of molecular biology — a sprint to find the actual gene, read its complete sequence letter by letter, and understand which mutations caused disease.

Multiple international teams competed, including researchers at the National Institutes of Health, a UK consortium led by Michael Stratton at the Institute of Cancer Research, and several other academic laboratories. The stakes were enormous: whoever sequenced the gene first would have first claim to patents and commercial applications.

This is where the story moves to Utah, and specifically to a geneticist named Mark Skolnick who had been sitting on one of the most valuable scientific resources on the planet.

Skolnick had spent years at the University of Utah building an enormous genealogical database of Mormon families. The Utah population offered a geneticist's dream: large families, meticulous record-keeping stretching back generations, low geographic mobility, and deep pedigrees maintained by the Church of Jesus Christ of Latter-day Saints. Skolnick's database eventually encompassed information on two hundred thousand Mormon family groups and most of the 1.6 million descendants of the initial roughly ten thousand Utah settlers. This was an unparalleled resource for tracing inherited disease genes through generations. Think of it as having a massive, pre-built family tree with medical records attached — the kind of data that other researchers would need decades to assemble from scratch.

In May 1991, Skolnick co-founded Myriad Genetics with three partners who brought complementary strengths to the venture. Peter Meldrum, who became Myriad's first CEO in 1992 and would lead the company for over two decades, was the operational and business mind. Kevin Kimberlin, chairman of Spencer Trask and Company, provided the venture capital connections and strategic direction. And Walter Gilbert, the 1980 Nobel laureate in Chemistry for his pioneering work on DNA sequencing methods — and a co-founder of Biogen — brought world-class scientific credibility. Having a Nobel laureate as co-founder was not just a credibility play; Gilbert understood the intersection of academic science and commercial biotechnology in a way that few people on Earth did. He joined the board in March 1992 and served as Vice Chairman until his retirement in 2020.

The founding thesis was elegant and aggressive: take the academic research happening at the University of Utah, combine it with Skolnick's genealogical goldmine, add private capital that moved faster than government grants, and commercialize the resulting discoveries. This was the early 1990s — the Human Genome Project was just getting underway, the biotech industry was still young, and the idea of turning academic gene discoveries into commercial products was genuinely novel. Myriad was, in essence, a bet that the genomics revolution could be monetized.

In August 1994, Skolnick's team — working alongside colleagues at the University of Utah, the National Institutes of Health, and McGill University — published the complete sequence of BRCA1. They won the race. Myriad filed a patent application covering the gene and its mutations on August 12, 1994, with the University of Utah and the U.S. Department of Health and Human Services as co-assignees.

Just over a year later, the BRCA2 gene on chromosome 13 was sequenced by a team led by Michael Stratton at the UK's Institute of Cancer Research and the Wellcome Trust Sanger Centre, with forty co-authors from six countries contributing. Myriad sequenced the gene almost simultaneously and filed patents on BRCA2 as well. The company was now sitting on patent claims covering both of the most important hereditary cancer genes known to science.

The science itself deserves explanation for those unfamiliar with molecular biology. BRCA1 and BRCA2 are what scientists call tumor suppressor genes. Think of them as quality-control inspectors in a factory. Their job is to produce proteins that repair double-strand breaks in DNA — the most dangerous type of DNA damage, where both strands of the double helix are severed. When these genes work properly, they catch and fix errors before cells divide, preventing mutations from accumulating. When they carry pathogenic mutations — inherited errors that break the gene's function — the repair system fails. Damaged DNA accumulates unchecked, and the risk of cells becoming cancerous rises dramatically. For BRCA1 mutation carriers, the lifetime risk of breast cancer can reach roughly 85 percent, and the risk of ovarian cancer up to 50 percent. For context, the general population lifetime risk of breast cancer is about 12 percent.

Understanding these genes represented a genuine breakthrough in cancer biology. For the first time, physicians could identify women at dramatically elevated cancer risk before they ever developed disease, enabling preventive interventions that could save lives.

But from the very beginning, there was a fundamental tension embedded in Myriad's DNA — both literally and figuratively. The company had raced ahead of publicly funded researchers, used private capital to move faster, and filed patents before the academic community could fully process what was happening. Mary-Claire King, whose seventeen years of work had made the discovery possible, was not a Myriad co-founder and did not share in the patents. The question that would haunt Myriad for the next two decades was already forming: Who owns a discovery about human biology?

The Patent Gambit: Owning Human Genes

Myriad's patent strategy was not just aggressive — it was revolutionary in its ambition. The company did not simply patent a method of testing for BRCA mutations. It patented the genes themselves, the isolated DNA sequences, the mutations within those genes, and methods for detecting those mutations. On December 2, 1997, the United States Patent and Trademark Office granted Myriad a patent covering forty-seven separate mutations in the BRCA1 gene. Across approximately seven key patents, Myriad had assembled what amounted to a patent fortress around two of the most medically important genes ever discovered.

The legal logic, while counterintuitive, had precedent in patent law at the time. The argument went like this: a gene as it exists inside a human cell is indeed a product of nature. But when a scientist isolates that gene — extracting and purifying the DNA sequence from its chromosomal context — the resulting isolated molecule is different from what exists in nature. It is, in patent terminology, a composition of matter that has been created through human intervention.

An analogy helps illustrate why this was so controversial. Imagine someone discovers a new medicinal plant deep in the Amazon rainforest. Under traditional patent law, you cannot patent the plant itself — it is a product of nature. But you can patent a purified extract of the plant's active compound, because the purified version does not exist in nature in that form. Myriad's argument applied this same logic to DNA: the BRCA genes as they exist on human chromosomes are natural, but the isolated, purified gene sequences used in testing are human-made compositions. Critics countered that unlike a plant extract, which has a different chemical structure than the raw plant material, isolated DNA has the same nucleotide sequence as the DNA inside your cells — the information content is identical. The scientific and legal communities argued bitterly over this distinction for nearly two decades.

This reasoning had been accepted by the USPTO for decades, and thousands of gene patents had been granted under this framework. At its peak, roughly twenty percent of the human genome was covered by some form of patent claim. The practice was widespread, but that did not make it settled.

Myriad launched BRACAnalysis commercially between 1996 and 1998, making it the first widely available clinical test for hereditary breast and ovarian cancer risk. The test analyzed the full coding sequences of both BRCA1 and BRCA2 for deleterious mutations. And because Myriad held the patents, no other laboratory in the United States could legally offer the same test. This was not a competitive advantage — it was a monopoly in the purest sense of the word.

The pricing reflected it. Initially set at roughly twenty-four hundred dollars, the combined BRACAnalysis and BART test eventually reached approximately four thousand dollars by 2013. Myriad was the sole provider, and the company enforced its exclusivity with vigor, sending cease-and-desist letters to university laboratories and research hospitals that attempted to develop their own BRCA testing. When researchers at the University of Pennsylvania tried to offer clinical BRCA testing, Myriad shut them down. When Oncormed, a competitor, attempted to enter the market, Myriad's patent wall proved impenetrable.

This enforcement strategy accomplished its business objective but created a growing army of enemies — and the intensity of that opposition is hard to overstate. Academic geneticists were furious. Researchers who had contributed to the broader scientific understanding of BRCA genes found themselves unable to work on two of the most important sequences in cancer biology without Myriad's permission. Laboratories that wanted to offer confirmatory testing — a second opinion on a Myriad result — were legally prohibited from doing so. This meant that a woman who received a positive BRCA result from Myriad had no way to get an independent verification from a different laboratory, a situation that violated a basic principle of medical practice.

Patient advocates pointed out that women who could not afford Myriad's test, or whose insurance would not cover it, were effectively denied access to potentially life-saving information about their own bodies. This was not an abstract concern — real women with strong family histories of breast and ovarian cancer were unable to learn whether they carried mutations that could be addressed through preventive measures. International researchers chafed at the idea that an American company could claim ownership over sequences that exist in every human being on Earth. The European patent on BRCA1 was challenged and partially revoked in 2004, limiting Myriad's ability to enforce its monopoly outside the United States.

Meanwhile, Myriad was building something beyond just patent protection. Every test the company performed generated data — specifically, information about genetic variants and their clinical significance. Over the years, Myriad accumulated the world's largest proprietary database of BRCA variants, including thousands of variants of uncertain significance whose clinical meaning could only be determined by studying large numbers of patients. This database became a secondary competitive moat, because even if the patents were eventually challenged, no competitor would have equivalent data to interpret rare mutations.

The business was spectacularly profitable. Gross margins north of 90 percent. Revenue doubling and redoubling. A product with no substitute and infinite switching costs because there was literally no one to switch to. But Myriad was building its fortune on a foundation that many in the scientific and civil liberties communities believed was fundamentally unjust — the idea that a corporation could own information encoded in every cell of every human body.

Building the Machine: Commercial Success and Clinical Adoption

Myriad went public on October 5, 1995, listing on the NASDAQ under the ticker MYGN. The company was still in the early stages of commercializing its BRCA testing, and initial revenues were modest — just under nine million dollars in 1996. But what followed was one of the most impressive revenue trajectories in diagnostic testing history, a trajectory that would see the company grow revenues nearly a hundredfold in less than two decades.

The commercial buildout required solving problems that were genuinely novel. In the late 1990s, most physicians had never ordered a genetic test. The concept of hereditary cancer risk assessment barely existed as a clinical workflow. Myriad had to educate an entire medical profession about what BRCA testing was, who should get it, and what the results meant. The company built a specialized sales force that called on oncologists, gynecologists, and primary care physicians, teaching them to identify patients with family histories suggestive of hereditary breast and ovarian cancer. This was not pharmaceutical sales — it was closer to missionary work, converting skeptics to a new paradigm of medicine.

This was harder than it sounds. Genetic testing raises uncomfortable questions about risk, probability, and family inheritance that most physicians were not trained to navigate. A positive BRCA result does not mean a patient will get cancer — it means her risk is dramatically elevated. Communicating this distinction, and helping patients make life-altering decisions based on probabilistic information, required a new kind of clinical infrastructure. Myriad invested heavily in genetic counseling, clinical education materials, and result interpretation services, creating a workflow that extended from patient identification through result interpretation to clinical decision-making. The company did not just sell a test — it sold an entire clinical paradigm.

The insurance reimbursement story was perhaps the most consequential commercial challenge. In the early days, most insurance companies viewed genetic testing as experimental and refused to cover it. Myriad had to wage a multi-year campaign to demonstrate clinical utility — that BRACAnalysis results actually changed clinical outcomes, that women who tested positive and pursued risk-reducing surgery or enhanced screening had meaningfully better survival rates. This required funding clinical studies, engaging with medical guideline organizations, and building relationships with insurance company medical directors. The eventual wins on reimbursement proved to be the true unlock for commercial scale, transforming BRCA testing from a niche offering available to the wealthy or well-insured into a broadly accessible medical tool.

Revenue accelerated dramatically in the mid-2000s as insurance coverage expanded and physician adoption deepened. From roughly forty-two million dollars in 2000, Myriad grew to nearly two hundred million by 2007, then nearly doubled again to three hundred eighty-six million in 2008. By fiscal year 2013, annual revenue had reached seven hundred thirty-seven million dollars. The company was processing hundreds of thousands of tests annually, and its proprietary variant database was growing with every single one of them.

The vertical integration strategy was a textbook example of competitive moat-building. Myriad controlled the entire value chain: patent protection ensured exclusivity, the clinical laboratory performed all testing in-house, the sales force owned physician relationships, the genetic counseling infrastructure managed the patient experience, and the proprietary database made results more accurate with every test performed. This created a genuine network effect — every test made Myriad's database better, which made its results more reliable, which attracted more physicians to order the test, which generated more data. It was a virtuous cycle reinforced by legal monopoly.

The proprietary database deserves special attention because it became central to Myriad's competitive strategy even beyond the patents. When a laboratory sequences a patient's BRCA genes, it sometimes finds mutations that have never been seen before, or that have been seen so rarely that their clinical significance is unknown. These are called variants of uncertain significance, or VUS. Interpreting a VUS correctly — determining whether it is pathogenic and cancer-causing, or benign and harmless — requires comparing it against a large database of previously characterized variants and their associated clinical outcomes. Because Myriad was the only laboratory performing BRCA testing for nearly two decades, it had assembled the world's largest database of BRCA variants. No competitor could match this interpretive advantage, even if they could legally offer the same test.

The company also expanded beyond BRCA testing during this period, launching tests for melanoma susceptibility, colon cancer risk, and other hereditary conditions. But BRACAnalysis remained the dominant revenue driver, accounting for the vast majority of the company's income.

The stock reflected the business success, reaching an all-time high of $55.43 on November 6, 2000, during the genomics bubble. Even after the dot-com correction, Myriad remained a highly profitable, fast-growing company with what appeared to be an impregnable competitive position. The company was printing money — but as any student of business history knows, monopoly profits attract not just competitors, but crusaders.

The Storm Gathers: Legal Challenges Begin

The legal challenge to Myriad's gene patents had been building for years, but it crystallized in 2009 when an unlikely alliance came together to take on the company. The American Civil Liberties Union — better known for fighting free speech and civil rights cases — teamed up with the Public Patent Foundation to file what would become one of the most consequential patent cases in American history.

The ACLU's involvement was itself surprising and deliberate. Chris Hansen and Sandra Park, the ACLU attorneys who led the litigation, understood that framing gene patenting as a civil liberties issue rather than a technical patent dispute would dramatically change the public narrative. Their argument was not simply that Myriad's patents were technically invalid. It was that no corporation should be allowed to control information that exists in every person's DNA — that gene patents violated the First Amendment right to access information about one's own body and the Fourteenth Amendment guarantee of equal protection.

The case was styled Association for Molecular Pathology v. Myriad Genetics, Inc. with AMP, a professional organization representing pathologists and laboratory professionals, as lead plaintiff. But the plaintiff list read like a who's who of the genetics establishment: individual researchers who had been blocked from studying BRCA genes, breast cancer patients who could not afford Myriad's test or who wanted a confirmatory second opinion that no other lab could provide, women's health organizations, and medical professional societies. It was a broad coalition united by the conviction that Myriad's monopoly was both legally indefensible and ethically wrong.

The case was filed in May 2009 in the U.S. District Court for the Southern District of New York, and it was assigned to Judge Robert Sweet — a then-eighty-seven-year-old Nixon appointee who would prove to be anything but predictable. In March 2010, Judge Sweet delivered a 152-page ruling that stunned the biotechnology industry: he declared all of Myriad's BRCA gene patents invalid. His reasoning was sweeping and unambiguous — he held that isolated DNA was not materially different from DNA in the body and therefore constituted an unpatentable product of nature. The decision was so broadly written that it threatened not just Myriad's patents but the entire framework under which thousands of gene patents had been granted.

The biotech industry reacted with something approaching panic. Thousands of gene patents had been granted under the same legal framework that Myriad relied upon. If Judge Sweet's reasoning stood, the patent portfolios of companies across the industry could be at risk. The Biotechnology Industry Organization and other trade groups filed amicus briefs supporting Myriad's appeal.

Myriad's counterargument was straightforward and not unreasonable: without patent protection, no company would invest hundreds of millions of dollars in discovering disease genes. The patents were the incentive that made the BRCA discoveries possible. Eliminate that incentive, and future genetic discoveries would languish in underfunded academic laboratories, never reaching patients who needed them.

This argument had genuine force. The pharmaceutical industry's patent-driven innovation model had produced life-saving drugs for decades, and the biotech industry had adopted the same framework. Myriad's defenders pointed out that the company's private capital had moved faster than government-funded research, and that BRACAnalysis had been available to patients for nearly two decades precisely because the patent incentive had motivated the investment. The counterargument was that academic researchers — including Mary-Claire King — had done much of the foundational work with public funding, and Myriad had essentially privatized the final stage of a publicly funded discovery.

The case spent the next three years bouncing between courts. The Federal Circuit Court of Appeals partially reversed Judge Sweet's ruling in July 2011, reinstating some patent claims. The Supreme Court vacated that decision in March 2012 and sent it back down in light of its ruling in Mayo v. Prometheus, another important patent eligibility case. The Federal Circuit again upheld gene patents on remand in August 2012. In November 2012, the Supreme Court agreed to hear the case directly.

During this entire period, Myriad's stock gyrated with every legal development. The business remained profitable and growing — patients and physicians still needed BRCA testing, and Myriad was still the only game in town — but the existential uncertainty was unmistakable. Every quarterly earnings call became a dual exercise in reporting strong numbers while reassuring investors that the patent portfolio would survive.

The years of legal limbo created a peculiar dynamic. Myriad was simultaneously the most profitable company in genetic testing and the most vulnerable. Revenue kept growing because the patents were still technically in force during the appeals process — no competitor could legally enter the market until the final ruling. But the market's assessment of the company's long-term value swung wildly with each judicial decision. It was the corporate equivalent of a condemned building that keeps generating rent while the demolition order works its way through the courts.

Meanwhile, the broader landscape of genetic testing was evolving rapidly. Next-generation sequencing technology was plummeting in cost, making it possible for smaller laboratories to offer sophisticated genetic tests at a fraction of the price Myriad charged. Companies like Invitae, founded in 2012, were explicitly building business plans around the assumption that gene patents would not survive judicial scrutiny. The competitive dam was ready to burst — it was just a matter of when the Supreme Court would open the floodgates.

The Angelina Jolie Moment and Cultural Inflection

On May 14, 2013 — exactly one month before the Supreme Court would rule on Myriad's patents — Angelina Jolie published an op-ed in the New York Times that fundamentally changed the public conversation about genetic testing. Titled "My Medical Choice," the piece disclosed that Jolie carried a pathogenic BRCA1 mutation, that her estimated lifetime risk of breast cancer was 87 percent, and that she had undergone a preventive bilateral mastectomy to reduce her risk to below 5 percent.

The impact was immediate and measurable. The National Cancer Institute's fact sheet on preventive mastectomy received 69,225 page views on May 14 alone — a 795-fold increase compared to the previous Tuesday. BRCA testing referrals surged not just in the United States but globally. Researchers would later document statistically significant and sustained increases in both genetic testing uptake and risk-reducing surgeries among women without prior cancer diagnosis. The phenomenon was so significant that the medical literature gave it a name: the Jolie Effect.

Myriad's stock spiked to fifty-two-week highs. Testing demand surged. From a narrow business perspective, Jolie's announcement was the greatest free marketing event in Myriad's history. But the irony was exquisite: the very public attention that Jolie brought to BRCA testing also intensified scrutiny of Myriad's monopoly pricing. If this test was so important that one of the world's most famous women was willing to have a preventive double mastectomy based on its results, why should a single company control access to it at four thousand dollars a pop?

The media coverage that followed Jolie's announcement was overwhelmingly sympathetic to the idea that all women should have access to BRCA testing, not just those who could afford Myriad's price or navigate the insurance reimbursement labyrinth. Op-eds, television segments, and magazine features explored the tension between Myriad's intellectual property rights and patient access to life-saving medical information.

What made the Jolie Effect so powerful was its combination of celebrity, vulnerability, and actionable medical information. Jolie did not simply disclose a diagnosis — she explained the science, described the decision-making process, and framed her choice as empowerment rather than victimhood. She wrote about her mother, who had fought cancer for nearly a decade before dying at age fifty-six, and connected her own testing and surgery to a desire to give her children a different future. The emotional resonance was irresistible. Genetic counselors reported being overwhelmed with appointment requests. Testing laboratories saw referral volumes surge by double-digit percentages essentially overnight.

The timing could not have been more consequential — the Supreme Court was about to deliver its ruling in a case that would determine the future of gene patenting, and the entire country was suddenly paying attention to BRCA testing. Jolie's announcement had, perhaps inadvertently, created the most powerful public argument against Myriad's monopoly: if this knowledge was important enough to save Angelina Jolie's life, then surely every woman deserved access to it.

Supreme Court Showdown: AMP v. Myriad

On the morning of June 13, 2013, at approximately ten-thirty, Justice Clarence Thomas delivered the opinion of a unanimous Supreme Court. The decision was nine to zero, a rare display of complete judicial consensus on a scientifically complex case, and it changed biotechnology forever.

The core holding was stated with unusual clarity for a Supreme Court opinion on a technical subject: "A naturally occurring DNA segment is a product of nature and not patent eligible merely because it has been isolated." With that sentence, the legal foundation of Myriad's monopoly dissolved. The Court held that Myriad had indeed made a genuine scientific breakthrough in discovering the precise location and genetic sequence of BRCA1 and BRCA2. But "groundbreaking, innovative, or even brilliant discovery does not by itself satisfy the patent eligibility inquiry." Myriad had found something extraordinary in nature, but finding something is different from inventing it.

The Court did carve out one important exception. Complementary DNA — cDNA — remained patent-eligible because it is synthetically created in the laboratory through reverse transcription, does not occur naturally, and has had the non-coding intron sequences removed. For non-scientists, cDNA is essentially a laboratory-made copy of a gene that has been edited to remove the non-functional sections, leaving only the protein-coding portions. Because this edited version does not exist anywhere in nature, the Court reasoned that it qualified as a human creation eligible for patent protection. This distinction had limited practical value for Myriad's diagnostic business — testing typically works with natural genomic DNA, not cDNA — but it preserved at least some intellectual property frameworks for the biotech industry more broadly.

The Court explicitly declined to rule on several related issues, including method patents, applications of BRCA knowledge, or the patentability of new uses of genetic information. These limitations would later prove important as companies sought alternative patent strategies in the post-Myriad landscape. The decision was deliberately narrow in scope but revolutionary in impact — it answered one specific question about gene patents while leaving many related questions for future courts to resolve.

The market reaction was swift and devastating. Within ninety minutes of the ruling — literally before the Court had moved on to its next case — Gene by Gene and Ambry Genetics announced they were immediately offering commercial BRCA testing. Their tests were already developed and validated, waiting only for legal clearance. By the end of the day, multiple laboratories had publicly committed to entering the market. Some offered BRCA testing as part of broader multi-gene panels that simultaneously analyzed dozens of cancer susceptibility genes, an approach that immediately made Myriad's single-gene test look narrow and outdated.

Prices that had been set by monopoly power were about to meet competition for the first time, and the result was exactly what economic theory would predict: a rapid race to the bottom.

The ruling's significance extended far beyond Myriad. Before the decision, roughly twenty percent of the human genome was covered by some form of patent claim. After it, naturally occurring gene sequences were permanently off-limits to patent holders. The decision forced the entire biotechnology industry to rethink its approach to intellectual property. Companies shifted their patent strategies toward methods, applications, synthetic constructs, and proprietary databases rather than naturally occurring biological sequences. The ruling also had international implications, influencing patent law discussions in Europe, Australia, and Canada, where similar cases were being litigated. An entire era of biotechnology IP strategy — one built on the premise that isolating a natural molecule was sufficient to claim ownership — was over. For Myriad's competitors, the ruling was a starting gun. For Myriad itself, it was an extinction-level event.

For Myriad, the ruling eliminated not just a revenue source but the defining characteristic of the business. The company's moat had not been operational excellence, superior technology, or brand loyalty. It had been a legal monopoly granted by the patent system. When that monopoly disappeared, Myriad was suddenly just another laboratory competing on price, speed, and quality — except that it had been built, staffed, priced, and structured for a world without competition. The analogy is a castle whose walls have been removed — the castle itself still stands, but it is now exposed to every attacker on the field.

The Collapse and Crisis Years

The post-ruling competitive flood was even faster than pessimists had predicted. Ambry Genetics, GeneDx, Invitae, Color Genomics, Gene by Gene, Quest Diagnostics, and LabCorp all launched BRCA testing within months. Many of these competitors did not just replicate Myriad's test — they improved upon it by offering multi-gene panels that tested for BRCA1 and BRCA2 alongside dozens of other cancer susceptibility genes simultaneously. Myriad's single-gene approach, which had been the only option available, suddenly looked outdated.

The price collapse was dramatic and swift. Testing that Myriad had priced at roughly four thousand dollars was suddenly available from competitors for a few hundred dollars. Color Genomics would eventually offer a multi-gene hereditary cancer panel for $249 — a 94 percent reduction from Myriad's monopoly-era pricing. To put this in perspective, imagine a world where a gallon of gasoline dropped from four dollars to twenty-five cents in the space of a few months. The ninety-plus percent gross margins that had characterized Myriad's monopoly era were a relic of a vanished world.

This price collapse was actually a triumph for patients and healthcare access, even as it devastated Myriad's business. Studies published in the years following the Supreme Court ruling showed significant increases in BRCA testing rates across all demographics, with the largest gains among underserved populations who had previously been unable to afford or access the test. The public health impact of the ruling was exactly what the ACLU and its co-plaintiffs had argued it would be — more testing, more prevention, more lives saved. The irony for Myriad was that the broader market for BRCA testing actually grew substantially after the ruling, but the company captured a shrinking share of that larger pie at much lower margins.

What made the competitive onslaught particularly devastating was the data-sharing dynamic. Myriad had maintained its proprietary variant database as a secondary competitive moat, and the company initially refused to share variant classifications with public databases like ClinVar. Competitors, by contrast, collectively adopted an open data philosophy, sharing their variant interpretations publicly. Over time, this collaborative approach eroded Myriad's interpretive advantage as the public databases grew. Myriad eventually began sharing some data as well, but by then the competitive landscape had permanently shifted.

The initial revenue impact was surprisingly modest — fiscal year 2014 revenue of roughly $725 million represented only a slight decline from the 2013 peak. But this was somewhat misleading. Myriad was already pivoting toward its myRisk Hereditary Cancer test, a multi-gene panel that tested for mutations in twenty-eight genes associated with eight hereditary cancers. The company was also benefiting from the residual momentum of physician relationships built over two decades and from the continued growth of genetic testing awareness, partly fueled by the Jolie Effect.

Under the surface, however, the business was under severe pressure. Market share in hereditary cancer testing, which had been effectively 100 percent, was eroding steadily. The company's cost structure — designed for a monopoly business with monopoly margins — was far too heavy for a competitive market. The sales force that had been educated to sell a premium product with no substitutes now had to compete against lower-priced alternatives. And the company's leadership, which had spent two decades managing a monopoly, needed to learn a fundamentally different set of competitive skills.

The stock began a multi-year decline that would ultimately take it from the mid-thirties range around the time of the ruling to single digits. Investors who had priced in the perpetuity of patent protection now had to value a company facing intense competition, margin compression, and strategic uncertainty. The decline was not a crash but a slow bleed — each quarter bringing slightly worse competitive metrics, each year bringing new competitors with better technology or lower prices or both.

There is a useful analogy in media. When newspapers lost their classified advertising monopoly to Craigslist and online competitors, they did not collapse immediately. Print advertising revenue declined slowly at first, then accelerated as the competitive alternatives gained traction. The newspapers that survived were the ones that found alternative revenue models quickly. The ones that did not are gone. Myriad was living through its own version of this story — a monopoly-era business model being disrupted by abundant, low-cost alternatives, with survival depending on whether management could find new sources of value before the old ones ran out.

The existential question was clear: Myriad had been a one-product company protected by an impregnable legal wall. The wall was gone, and the product was being commoditized. Could the company find something else to sustain it?

Reinvention Part One: Beyond BRCA

The answer, or at least the attempt at an answer, came through a combination of internal product development and acquisitions. Mark Capone, who had joined Myriad in 2002 and risen to become president of Myriad Genetic Laboratories, took the helm as CEO with a mandate to diversify the company beyond its dependence on hereditary cancer testing. Capone's strategy was to transform Myriad from a single-test company into a broad precision medicine platform.

The most significant acquisition came in September 2016, when Myriad purchased Assurex Health for $225 million upfront, plus up to $185 million in performance milestones. Assurex's key product was GeneSight Psychotropic, a cheek-swab pharmacogenomic test designed to help clinicians personalize psychiatric medication selection. The test analyzed genetic markers related to how a patient's body metabolizes certain antidepressants, antipsychotics, and other psychotropic medications, aiming to reduce the trial-and-error process that characterizes much of psychiatric prescribing.

GeneSight was an ambitious bet on a compelling premise. The mental health pharmacogenomics market was estimated at over three billion dollars, and the product addressed a genuine clinical pain point. The typical psychiatric patient tries multiple medications before finding one that works effectively — a frustrating process that can take months or years, during which patients endure side effects, worsening symptoms, and the psychological toll of treatments that fail. GeneSight promised to short-circuit this trial-and-error process by analyzing how a patient's genes affect drug metabolism, theoretically allowing psychiatrists to choose the right medication faster.

But GeneSight was also controversial from the start. The core scientific question — whether pharmacogenomic testing actually improves psychiatric outcomes in a clinically meaningful way — remained contested. Some studies showed benefits; others were inconclusive. The FDA issued a safety communication in 2018 cautioning against using pharmacogenomic tests to make drug selection decisions, a move that cast a shadow over the entire category. Major insurance companies, including UnitedHealthcare, initially refused to cover GeneSight, citing insufficient evidence of clinical utility. Myriad invested heavily in clinical trials, most notably the GUIDED study, which showed improvements in response and remission rates for patients whose medication choices were guided by GeneSight results. But critics questioned the study's methodology, and the debate continues to this day. The tension between GeneSight's commercial promise and its evidence base would become a recurring theme in Myriad's post-BRCA identity — and a reminder that in diagnostics, clinical evidence is the ultimate currency.

Two years later, Myriad made an even larger acquisition, purchasing Counsyl in July 2018 for $405.9 million — $278.5 million in cash plus approximately three million shares of stock. Counsyl was a Silicon Valley-based company that had built a popular expanded carrier screening test called Foresight, used by couples planning pregnancies to determine whether they carried mutations for hundreds of inherited conditions. Counsyl also brought Prelude, a non-invasive prenatal test later rebranded as Prequel, which could screen for chromosomal abnormalities like Down syndrome through a simple maternal blood draw. This gave Myriad a meaningful position in reproductive health, a large and growing market adjacent to its hereditary cancer franchise.

The combined price tag for GeneSight and Counsyl — over $630 million — represented a massive bet that diversification could replace what the Supreme Court had taken away. But acquisitions are easier to announce than to integrate, and each new product line came with its own competitive dynamics, reimbursement challenges, and operational requirements.

The internal product development pipeline also expanded meaningfully during this period. MyChoice CDx, a companion diagnostic for homologous recombination deficiency testing, became increasingly important as PARP inhibitor drugs gained traction in ovarian cancer treatment. PARP inhibitors work by exploiting the DNA repair deficiency in cancer cells with homologous recombination deficiency — essentially attacking cancer cells at their weakest point. MyChoice CDx identifies which patients are most likely to benefit from these drugs, creating a direct commercial link between Myriad's testing and pharmaceutical companies' drug sales.

Prolaris, a prognostic test for prostate cancer, offered entry into the men's health market — a significant addressable market given that prostate cancer is the most commonly diagnosed cancer among American men. EndoPredict provided a breast cancer prognostic tool that competed with Exact Sciences' more established Oncotype DX. The product portfolio was diversifying, but each new product required its own clinical validation, insurance reimbursement battles, and commercial buildout — and none had the kind of patent protection that had made BRACAnalysis so profitable.

By fiscal year 2019, Myriad's total revenue reached approximately $851 million — its all-time peak and modestly above the pre-ruling highs, suggesting that the acquisition strategy had at least replaced lost revenue in absolute terms. But the topline number masked a fundamentally different business underneath.

Hereditary cancer testing was still the largest segment but no longer growing — the franchise that had once been a monopoly was now just one competitor among many in a commoditized market. GeneSight was ramping but facing clinical utility questions that created reimbursement uncertainty. Prenatal testing was competitive and lower-margin, with Natera emerging as a formidable rival. The company was broader but not necessarily stronger, and the margins on the new businesses were nowhere near the levels the old monopoly had generated.

The deeper strategic question remained unresolved: Could Myriad build a durable competitive advantage in any of these new markets, or was it simply trading one set of competitive challenges for another? The answer would have to wait, because the year 2020 was about to deliver the most severe stress test that Myriad — and the entire healthcare industry — had ever faced.

The Pandemic and Leadership Transition

The year 2020 delivered a one-two punch that nearly knocked Myriad out.

First, Mark Capone resigned as CEO in February 2020, creating a leadership vacuum at the worst possible moment. The departure was abrupt and came without a permanent successor in place — a troubling signal for a company already navigating strategic uncertainty. Then COVID-19 hit.

The pandemic's impact on Myriad was severe and immediate. Genetic testing is largely an elective, non-emergency medical service. When hospitals and clinics shut down non-essential procedures, when patients avoided in-person doctor visits, and when the entire healthcare system pivoted to pandemic response, Myriad's testing volumes collapsed. Fourth-quarter fiscal 2020 revenue plummeted 57 percent year-over-year to $93.2 million. Hereditary cancer screening in that quarter alone fell 66 percent. Full fiscal year 2020 revenue came in at $638.6 million, a 25 percent decline from the prior year's peak.

The damage was broad-based and relentless. GeneSight, which required in-person psychiatric visits for ordering, fell 34 percent to $74.1 million. Prenatal testing dropped 27 percent to $76.7 million. Hereditary cancer tests — still the company's largest revenue contributor — fell 28 percent to $347.4 million. The company withdrew its financial guidance and entered crisis mode — cutting costs, furloughing employees, and scrambling to preserve cash.

The pandemic exposed a fundamental vulnerability in Myriad's business model: genetic testing depends on patients visiting doctors, doctors ordering tests, and samples being collected and shipped to laboratories. When any link in that chain breaks down — as happened when clinics closed, patients stayed home, and healthcare systems redirected resources to COVID-19 — test volumes collapse immediately. Unlike software companies that can continue to generate revenue during lockdowns, or pharmaceutical companies whose patients continue taking medications, genetic testing companies have zero recurring revenue. Every dollar must be earned anew through a new patient interaction, a new physician order, and a new sample. For a company that was already navigating the aftermath of losing its monopoly, the pandemic was a near-death experience.

Into this chaos stepped Paul J. Diaz, appointed president and CEO on August 13, 2020. Diaz brought a different profile than Myriad's previous leaders. His background was in healthcare operations and private equity rather than genetics or laboratory science. He had previously served as president and CEO of Kindred Healthcare, the largest post-acute healthcare provider in the United States — a company with over forty thousand employees and billions in revenue — then moved into healthcare-focused private equity at Cressey and Company. He held a law degree from Georgetown and brought a business-first approach to transformation that was less about scientific innovation and more about operational discipline.

Diaz launched what he called a strategic transformation plan, focusing on four pillars: operational efficiency, margin improvement, portfolio rationalization, and disciplined growth. The plan involved streamlining the product portfolio — exiting underperforming product lines and doubling down on growth areas — investing in next-generation technology platforms including liquid biopsy and AI-enhanced diagnostics, and rebuilding commercial capabilities with a more focused sales approach.

Under Diaz, Myriad began to show signs of stabilization. Fiscal years 2023 and 2024 each delivered approximately 11 percent year-over-year revenue growth, and the company's adjusted gross margins began to recover. The hereditary cancer franchise stabilized as Myriad's MyRisk multi-gene panel gained traction. GeneSight continued to grow despite clinical utility debates. And the tumor profiling segment, particularly Prolaris for prostate cancer and myChoice CDx for ovarian cancer, showed promising momentum.

However, GAAP profitability remained elusive. Myriad continued to report net losses, and the stock continued its long decline. From the mid-thirties at the time of the Supreme Court ruling, shares had fallen to single digits — a decline of more than 85 percent that reflected the market's skepticism about Myriad's ability to build sustainable competitive advantages in any of its chosen markets. The market capitalization, which had once exceeded two billion dollars, hovered around five hundred million — a fraction of competitors like Natera and Guardant Health.

Diaz stepped down effective April 30, 2025, returning to Cressey and Company as Managing Partner but continuing to serve as a consultant to the CEO and board. His successor, Sam Raha, had been serving as COO since December 2023 and had played a central role in shaping the company's long-term growth strategy. The transition was orderly — a contrast to the abrupt Capone departure five years earlier — and Raha inherited a company that was more diversified than the pre-2013 Myriad, more operationally efficient, but still searching for the kind of durable competitive position that would justify a sustained rerating by the market. In an early signal of the new administration's priorities, Myriad hired Brian Donnelly — a veteran of Amazon and Illumina — as Chief Commercial Officer in May 2025, signaling an intent to bring world-class commercial execution to the company's go-to-market strategy.

The Science and Product Portfolio Today

As of early 2026, Myriad operates across four business segments, each representing a distinct market opportunity and competitive dynamic.

Hereditary cancer testing remains the company's largest segment. The flagship MyRisk test is a multi-gene panel that analyzes dozens of genes associated with hereditary cancers, a far cry from the single-gene BRACAnalysis test that built the company. Fourth-quarter 2025 showed encouraging volume trends — 14 percent growth in the affected-patient market and 11 percent in the unaffected market. BRACAnalysis CDx continues as a companion diagnostic, and the original BRACAnalysis test persists in various forms.

Tumor profiling represents Myriad's most strategic growth area. MyChoice CDx, which tests for homologous recombination deficiency to guide PARP inhibitor therapy decisions in ovarian cancer, has become increasingly important as pharmaceutical companies expand their PARP inhibitor indications. Prolaris, the prostate cancer prognostic test, showed 16 percent year-over-year revenue growth in the fourth quarter of 2025. EndoPredict serves the breast cancer prognostic market. Most ambitiously, Myriad launched Precise MRD — a tumor-informed circulating tumor DNA test for molecular residual disease detection — in limited clinical launch on March 2, 2026, initially targeting breast cancer with plans to expand to colorectal and renal cancers later in the year.

The MRD launch is particularly significant because it puts Myriad in direct competition with Natera's Signatera and Guardant Health's Reveal in one of the fastest-growing segments of oncology diagnostics. MRD testing — which stands for molecular residual disease, sometimes called minimal residual disease — is conceptually straightforward but technically demanding. After a cancer patient undergoes surgery or completes treatment, the critical question is whether any cancer cells remain in the body. Traditional imaging cannot detect tiny amounts of residual disease, but liquid biopsy approaches can identify circulating tumor DNA fragments in the blood at extraordinarily low concentrations, potentially detecting cancer recurrence months before it would appear on a scan.

The clinical and commercial implications are enormous. If MRD testing becomes standard of care for major cancer types — and the clinical evidence is moving in that direction — it could represent a market worth billions of dollars annually. Natera's Signatera already has a substantial head start, with established clinical evidence, broad insurance coverage, and over 800,000 oncology tests performed in fiscal year 2025. Whether Myriad can compete effectively against these larger, faster-growing rivals in liquid biopsy will be a defining test of the company's reinvention strategy. The answer will reveal whether Myriad's brand recognition, physician relationships, and twenty-plus years of oncology testing data can offset its late entry and smaller scale.

The prenatal and reproductive health segment includes Prequel for non-invasive prenatal testing, Foresight for expanded carrier screening, and SneakPeek, an early gender DNA test. This segment faces stiff competition from Natera, which has built a dominant position in prenatal testing through its Panorama platform and aggressive commercial execution. FirstGene, a new prenatal test that entered limited access rollout in 2025, is expected to achieve full commercial launch in 2026 and represents Myriad's attempt to differentiate in this crowded market.

GeneSight Psychotropic, the pharmacogenomic test for psychiatric medications, generated $36.6 million in fourth-quarter 2025 revenue with 9 percent volume growth year-over-year. The product continues to face questions about the strength of its clinical evidence base, but it has built a meaningful franchise among psychiatrists who have experienced its utility in clinical practice. For Myriad, GeneSight represents both a significant revenue contributor and an ongoing risk — if insurers or regulators further restrict coverage based on clinical utility concerns, the revenue impact could be substantial.

The most notable recent development in Myriad's pipeline is the partnership with PATHOMIQ for AI-powered prostate cancer assessment, expected to launch in the first half of 2026. This collaboration represents a bet that artificial intelligence applied to pathology images can enhance the clinical utility of Myriad's existing Prolaris test, creating a combined offering that provides more actionable information to urologists and their patients. If successful, it could differentiate Myriad's prostate cancer franchise from competitors and demonstrate the company's ability to integrate AI capabilities into its testing platform.

Across these segments, Myriad reported full-year fiscal 2025 revenue of $824.5 million and fourth-quarter test volume of 382,000 — up 2 percent year-over-year, suggesting steady but not spectacular growth. Revenue guidance for fiscal 2026 stands at $860 to $880 million, implying mid-single-digit growth. Adjusted gross margins are guided to 68-69 percent — respectable for a diagnostic testing company, but a far cry from the monopoly-era margins above 90 percent. In the fourth quarter of fiscal 2025, Myriad reported a GAAP net loss of $7.9 million and adjusted EBITDA of $14.3 million.

Full-year adjusted EBITDA guidance of $37 to $49 million on over eight hundred million dollars in revenue translates to an EBITDA margin of less than 6 percent — extraordinarily thin for any business, and a reminder of how dramatically the economics of genetic testing have changed since the monopoly days. This level of profitability suggests a company that is approaching operational breakeven but not yet generating the kind of cash flows that would support aggressive reinvestment, significant debt paydown, or meaningful shareholder returns. The path from here to robust profitability requires either meaningful revenue growth on a relatively fixed cost base, significant further cost reductions, or both.

The Competitive Landscape and Industry Evolution

The genetic testing industry that Myriad once dominated has exploded into a multi-billion-dollar market with dozens of competitors, each pursuing different technological approaches and market segments. Understanding Myriad's competitive position requires understanding who it is fighting and how the battlefield has shifted.

The most cautionary tale in the industry belongs to Invitae, which pursued an aggressive growth-over-profitability strategy that ultimately proved fatal. Invitae's story is worth examining in detail because it represents the road not taken — the anti-Myriad approach to building a genetic testing company.

Where Myriad had charged premium prices behind patent walls, Invitae's strategy was to price tests below cost to gain market share, betting that scale would eventually bring profitability. Backed by SoftBank and Ark Investment Management — two of the most prominent growth-at-all-costs investors of the era — Invitae peaked at a seven-billion-dollar valuation and $56.60 per share in 2020. The company acquired competitors, expanded its test menu aggressively, and offered panels at prices that made it nearly impossible for competitors to match.

But profitability never arrived. The genetic testing business, it turned out, did not have the unit economics that support a lose-money-to-gain-share strategy. Unlike software, where marginal costs approach zero at scale, every genetic test requires physical sample processing, sequencing, and interpretation. Invitae filed Chapter 11 bankruptcy in February 2024 with liabilities exceeding one billion dollars and a stock price of less than two cents — a staggering destruction of shareholder value. Labcorp acquired its oncology and rare disease assets for $239 million at the bankruptcy auction, while Natera purchased the reproductive health portfolio for just $10 million upfront plus milestones. Invitae's collapse was a stark demonstration that in genetic testing, growth without a path to profitability is a death sentence — and a vindication, in a strange way, of Myriad's more conservative approach to pricing and margins, even as the company continued to struggle with its own profitability challenges.

Natera represents perhaps Myriad's most formidable competitor and offers a striking contrast in execution and market positioning. While Myriad has struggled to rebuild after losing its monopoly, Natera has grown rapidly by focusing on two high-growth areas: prenatal testing and oncology. The company processed approximately 3.5 million tests in fiscal year 2025, with oncology volumes reaching 800,800 tests — up 52 percent year-over-year, a growth rate that Myriad can only envy. Natera's Signatera MRD test is the market leader in molecular residual disease monitoring, directly competing with Myriad's newly launched Precise MRD.

Critically, Natera became cash-flow positive in 2025, generating over $100 million in operating cash flow. It has crossed the profitability threshold that has eluded Myriad for years. Natera is larger, faster-growing, and better-capitalized than Myriad in the oncology testing market — and its momentum shows no signs of slowing.

Guardant Health is the dominant player in liquid biopsy, with its Guardant360 comprehensive genomic profiling test and Guardant Reveal MRD test. Fiscal year 2025 revenue was projected at approximately $981 million — substantially larger than Myriad's entire business — with 33 percent year-over-year growth and approximately 276,000 oncology tests performed.

Perhaps most importantly for the industry's future, Guardant's Shield test for multi-cancer early detection received FDA Breakthrough Device designation in June 2025, potentially opening an enormous screening market. If multi-cancer early detection through liquid biopsy becomes standard screening — analogous to how mammograms became routine for breast cancer screening — the addressable market could be worth tens of billions of dollars annually. This is a market that Myriad is not currently positioned to address.

Exact Sciences, the company behind Cologuard for colorectal cancer screening and Oncotype DX for breast cancer recurrence risk assessment, competes with Myriad primarily in breast cancer prognostics. Exact Sciences has built something that Myriad lost in 2013: a product with brand recognition not just among physicians but among patients. Cologuard's direct-to-consumer advertising has made it one of the most recognizable diagnostic brands in America. With over one million Cologuard and Oncotype DX test results in a single quarter, Exact Sciences operates at a scale and brand strength that Myriad cannot currently match.

Beyond the pure-play genetic testing companies, Myriad faces competition from diversified laboratory giants and technology-driven newcomers. Foundation Medicine, owned by Roche, offers its FoundationOne CDx and FoundationOne Liquid CDx platforms backed by the resources of one of the world's largest pharmaceutical companies. Tempus has attracted significant private investment for its AI-driven genomic profiling approach, betting that machine learning applied to large clinical datasets can create differentiation that pure sequencing cannot. Quest Diagnostics and LabCorp bring massive scale advantages — they process millions of tests annually across all categories, and their existing physician relationships give them distribution advantages that smaller companies struggle to match. Color Health has partnered with major health systems to provide low-cost, population-scale hereditary cancer screening, attacking the market from the accessibility and affordability angle.

The technology landscape has also shifted dramatically. Next-generation sequencing costs have fallen by several orders of magnitude since Myriad's founding, making genetic testing increasingly accessible and reducing the capital barriers to entry. To appreciate the scale of this change, consider that sequencing a single human genome cost roughly three billion dollars when the Human Genome Project was completed in 2003. Today, whole genome sequencing is approaching the hundred-dollar price point. That is a cost reduction of more than ten million fold in just over two decades — faster than Moore's Law in semiconductors. This raises fundamental questions about the long-term viability of panel-based testing approaches like those Myriad relies upon. Why pay several hundred dollars to test thirty genes when you could sequence all twenty thousand protein-coding genes for a similar price?

Liquid biopsy — detecting cancer-associated signals through simple blood draws rather than invasive tissue biopsies — has emerged as perhaps the most transformative technology shift in oncology diagnostics. The appeal is obvious: a blood draw is simpler, less painful, repeatable, and can be done in any clinical setting. Companies like Guardant and Natera have built large businesses around liquid biopsy approaches, and the technology is expanding from advanced cancer monitoring into early detection and screening applications that could eventually represent markets worth tens of billions of dollars.

The direct-to-consumer segment, once dominated by 23andMe, has also evolved significantly. 23andMe's struggles — including data breaches that compromised millions of users' genetic information and persistent financial difficulties — have demonstrated the limits of consumer genomics as a standalone business model. But the broader trend toward patient empowerment and health data accessibility continues to put downward pressure on pricing and increase expectations for accessibility across the entire testing industry.

Across this landscape, the competitive dynamics are intense. Pricing pressure from insurance companies, technology commoditization, and the constant need for clinical validation studies create an environment where sustainable profitability is difficult to achieve. The genetic testing market is growing rapidly — projected to reach over forty billion dollars by 2035 — but the value may be captured by a relatively small number of winners. The Invitae bankruptcy demonstrated that market share without profitability is worthless, while Natera's ascent proved that focused execution in high-growth segments can create enormous value. Myriad's challenge is to find its own version of that formula.

Business Model and Unit Economics

Myriad's business model has evolved considerably since the monopoly days, but the fundamental economics of genetic testing remain challenging.

Revenue is driven by a deceptively simple equation: test volumes multiplied by average revenue per test. But that simplicity is misleading. The average revenue per test is determined not by list prices but by reimbursement rates negotiated with — or imposed by — insurance companies, Medicare, and Medicaid. This distinction is critical and often misunderstood by investors unfamiliar with healthcare economics. Myriad can set whatever list price it wants, but the actual revenue it collects depends on complex negotiations with payers who have enormous bargaining power. The "list price" of a genetic test bears about as much relation to the price actually paid as the sticker price of a hospital stay bears to what an insurer negotiates — which is to say, very little.

The insurance reimbursement game is one of the most important dynamics in the business. Each test must be mapped to specific CPT (Current Procedural Terminology) codes, and coverage depends on insurance companies accepting that the test has clinical utility — that it actually changes medical decisions in ways that improve patient outcomes. Getting a favorable coverage determination from a major insurance company can take years of clinical evidence generation, committee reviews, and negotiations. Losing coverage can destroy a product line overnight.

Prior authorization requirements add another layer of friction. Many insurers require physicians to obtain approval before ordering genetic tests, creating administrative burdens that reduce test volumes and increase Myriad's customer acquisition costs. The company employs a substantial team dedicated to navigating insurance coverage and prior authorization requirements.

On the cost side, Myriad operates centralized laboratory facilities in Salt Lake City that process hundreds of thousands of tests annually. Lab operations involve multiple cost layers: sequencing equipment (predominantly Illumina platforms, which represent a significant supplier dependency), reagents and consumables that must be purchased for every test, bioinformatics analysis that converts raw sequencing data into clinically actionable results, variant interpretation by Ph.D.-level scientists who evaluate the clinical significance of identified mutations, and quality control systems that ensure accuracy and regulatory compliance.

The sales force that educates and serves physicians remains a significant cost center, as does the R&D organization that develops new tests and generates the clinical evidence needed to win reimbursement. Unlike many technology businesses where R&D is discretionary, in genetic testing, R&D spending is essentially mandatory — without continuous investment in clinical validation studies, existing products lose reimbursement coverage and new products cannot enter the market.

The gross margin story tells the history of the company in a single number. During the monopoly era, gross margins exceeded 90 percent — a reflection of the extraordinary pricing power that comes from having no competitors. Today, adjusted gross margins are in the 68-69 percent range, which is respectable for a diagnostics company but represents a fundamentally different economic reality. The difference between a 90 percent gross margin and a 68 percent gross margin, applied to over eight hundred million dollars in revenue, represents hundreds of millions of dollars in lost annual profit.

The pathway to profitability in the current competitive landscape runs through a combination of volume growth, operational efficiency, and portfolio mix shift toward higher-margin products. Companion diagnostics represent the most promising margin opportunity. In this model, Myriad partners with pharmaceutical companies to provide testing that determines whether a patient is eligible for a specific targeted therapy. The economics are different from standard testing because the pharmaceutical partner has a direct financial interest in identifying eligible patients — every positive test result is a potential drug sale. This alignment means pharma companies often co-invest in clinical trials, support reimbursement efforts, and sometimes subsidize the testing directly. Myriad's myChoice CDx for PARP inhibitor guidance is the best current example, and the expansion of PARP inhibitor indications could drive meaningful growth in this high-margin segment.

Data monetization represents another potential revenue stream that Myriad has barely tapped. The company's database of millions of test results, spanning over two decades of clinical history, contains information that pharmaceutical companies would pay significant sums to access for drug development, clinical trial design, and real-world evidence studies. Several competitors have begun exploring data licensing as a business line, and Myriad's historical dataset could be valuable — if the company can navigate the privacy, consent, and regulatory complexities involved in commercializing patient data.

The capital intensity question is also worth noting. Unlike software companies that can scale with minimal incremental investment, genetic testing requires physical laboratories, expensive sequencing equipment, trained scientific personnel, and ongoing quality control. Each new test requires clinical validation studies that can cost millions of dollars and take years to complete. This capital intensity limits the speed at which the business can grow and constrains the returns available even to successful operators.

Strategic Analysis: The Moat That Was and What Remains

The Myriad story is one of the most dramatic examples in business history of a company losing its competitive moat. Analyzing the company through the lens of both Porter's Five Forces and Hamilton Helmer's Seven Powers reveals not just what happened, but why recovery has been so difficult.

In the pre-2013 world, Myriad's competitive position was almost absurdly strong. The threat of new entrants was zero — patent protection meant no one could legally offer competing tests. Supplier power was irrelevant against monopoly pricing. Buyer power was limited because physicians had no alternative to recommend. Substitutes did not exist. And competitive rivalry was a concept that simply did not apply. This was not a competitive market — it was a franchise with legal protection.

Today, every one of those forces has reversed. The threat of new entrants is high because sequencing technology is increasingly commoditized and post-Supreme Court, there are no patent barriers to gene testing. Regulatory complexity and reimbursement relationships create some friction, but they are obstacles, not moats. Buyer power is high because insurance companies negotiate aggressively, hospital systems demand lower prices, and patients with high-deductible plans are increasingly price-sensitive. The threat of substitutes is moderate to high as whole genome sequencing, liquid biopsy, and AI-driven risk assessment offer alternative approaches to genetic information. And competitive rivalry is intense, with numerous well-funded competitors fighting for market share in every segment Myriad serves.

Through Helmer's framework, the picture is even starker. Myriad's pre-2013 advantage was the ultimate cornered resource — ownership of the BRCA genes themselves through patent protection. When the Supreme Court ruled that naturally occurring DNA cannot be patented, that cornered resource became a public good overnight. No business in recent history has experienced a more complete destruction of its primary competitive advantage through a single legal decision.

What remains? Scale economies exist in laboratory operations — Myriad processes hundreds of thousands of tests per year, and each incremental test has a low marginal cost once laboratory infrastructure is in place. But these scale economies are not winner-take-all. Regional labs can be cost-effective at more modest volumes, and competitors like Quest and LabCorp have far greater scale across their entire testing businesses.

Network effects from the data generated by testing are moderate. More tests genuinely do improve variant interpretation — when Myriad encounters a rare mutation, it can compare it against its historical database to better predict its clinical significance. But competitors have built similar databases, and the open sharing of variant data through ClinVar has democratized much of this knowledge. The network effect exists but is not strong enough to create winner-take-all dynamics.

Counter-positioning, which Myriad held when its monopoly model was unreplicable, is gone now that everyone can offer similar tests. Switching costs are low because physicians can order from any laboratory with a simple change in their ordering system. Brand recognition exists among oncologists — the Myriad name still carries weight in hereditary cancer genetics — but branding provides limited pricing power in a commoditized market where insurers and health systems make most purchasing decisions.

Process power from decades of testing experience is perhaps Myriad's most durable remaining advantage. The company has accumulated deep expertise in sample handling, variant interpretation workflows, turnaround time optimization, and quality control that newer competitors take years to build. But process power is inherently replicable given enough time and investment, and it does not provide the kind of structural barrier that prevents competition.

The honest assessment is that Myriad went from having one of the strongest competitive positions in biotechnology — a true cornered resource that no competitor could legally replicate — to having modest, contested advantages that provide limited pricing power and no structural barriers to competition. This transformation explains the stock's decline from the mid-thirties to five dollars better than any earnings analysis could. It is a textbook case study in what happens when a company's entire competitive advantage is concentrated in a single dimension that can be eliminated by external forces.

Bull versus Bear Case

The bull case for Myriad centers on the company's data heritage and diversified portfolio. Twenty-plus years of clinical testing data, encompassing millions of test results and variant interpretations, represents a genuine asset that newer competitors cannot replicate. The established relationships with thousands of oncologists, built through decades of sales force investment, provide distribution advantages. The diversified product portfolio — spanning hereditary cancer, tumor profiling, prenatal testing, and pharmacogenomics — reduces dependence on any single product.

The precision medicine market continues to grow rapidly, driven by advancing science, increasing clinical adoption, and expanding insurance coverage. Myriad's companion diagnostics partnerships with pharmaceutical companies offer potentially high-margin growth as new targeted therapies gain approval. The launch of Precise MRD represents a credible entry into the fast-growing liquid biopsy segment. Technology improvements, including AI-enhanced variant interpretation and the partnership with PATHOMIQ for AI-powered prostate cancer assessment, could create new sources of differentiation. Under new CEO Sam Raha, the company has guided for fiscal 2026 revenue of $860 to $880 million, suggesting continued top-line momentum.