Mettler-Toledo: The Precision Scale of Global Science and Industry

I. Introduction and Episode Roadmap

There is an invisible infrastructure beneath modern science, modern food safety, and modern manufacturing. Every pill that leaves a pharmaceutical plant, every piece of chicken weighed at the deli counter, every chemical compound measured in a research laboratory — somewhere in that chain, a Mettler-Toledo instrument is doing its quiet, essential work. It is the kind of company that most investors walk past without a second glance. Weighing scales. Pipettes. Checkweighers. These are not the products that generate breathless CNBC coverage or viral tweets. And yet, Mettler-Toledo International has been one of the most consistent compounders in the history of the New York Stock Exchange.

Revenue approaching four billion dollars. Operations spanning roughly forty countries. A customer base so diversified that no single end-customer accounts for more than one percent of sales. Adjusted operating margins that consistently clear the high-twenties. A share price that has compounded at roughly twenty percent annually over the past two decades, dwarfing the S&P 500 and most of its more glamorous peers. This is a company that has turned the mundane act of measurement into a precision-engineered profit machine.

The question at the heart of this story is deceptively simple: how did two companies from opposite sides of the Atlantic — one born in the industrial heartland of Ohio, the other in the watchmaking culture of Switzerland — come together to dominate the unsexy but essential world of weighing and precision measurement? The answer involves a century of mechanical ingenuity, a parade of strategic acquisitions, the disciplined hand of Swiss pharmaceutical conglomerates, a brief but consequential detour through private equity, and an operating culture that treats margin expansion as a kind of religious calling.

The company reports through five geographic segments: U.S. Operations, Swiss Operations, Western European Operations, Chinese Operations, and Other Operations. Its products fall into four broad categories — laboratory instruments, industrial weighing solutions, product inspection systems, and food retail scales — each serving distinct end markets but sharing the common thread of precision measurement. Roughly forty-two percent of revenue comes from the Americas, twenty-nine percent from Europe, and twenty-nine percent from Asia and the rest of the world, with China alone representing about sixteen percent of total sales.

What makes this story compelling is not just the financial record. It is the way Mettler-Toledo has built a business where nearly every competitive advantage reinforces every other one — regulatory compliance creates switching costs, switching costs enable pricing power, pricing power funds R&D, R&D deepens the moat, and the service business turns one-time product sales into decades-long customer relationships. Understanding how this flywheel was constructed, piece by piece over more than a century, reveals a playbook for building enduring value in industries that most people would never think to look at.

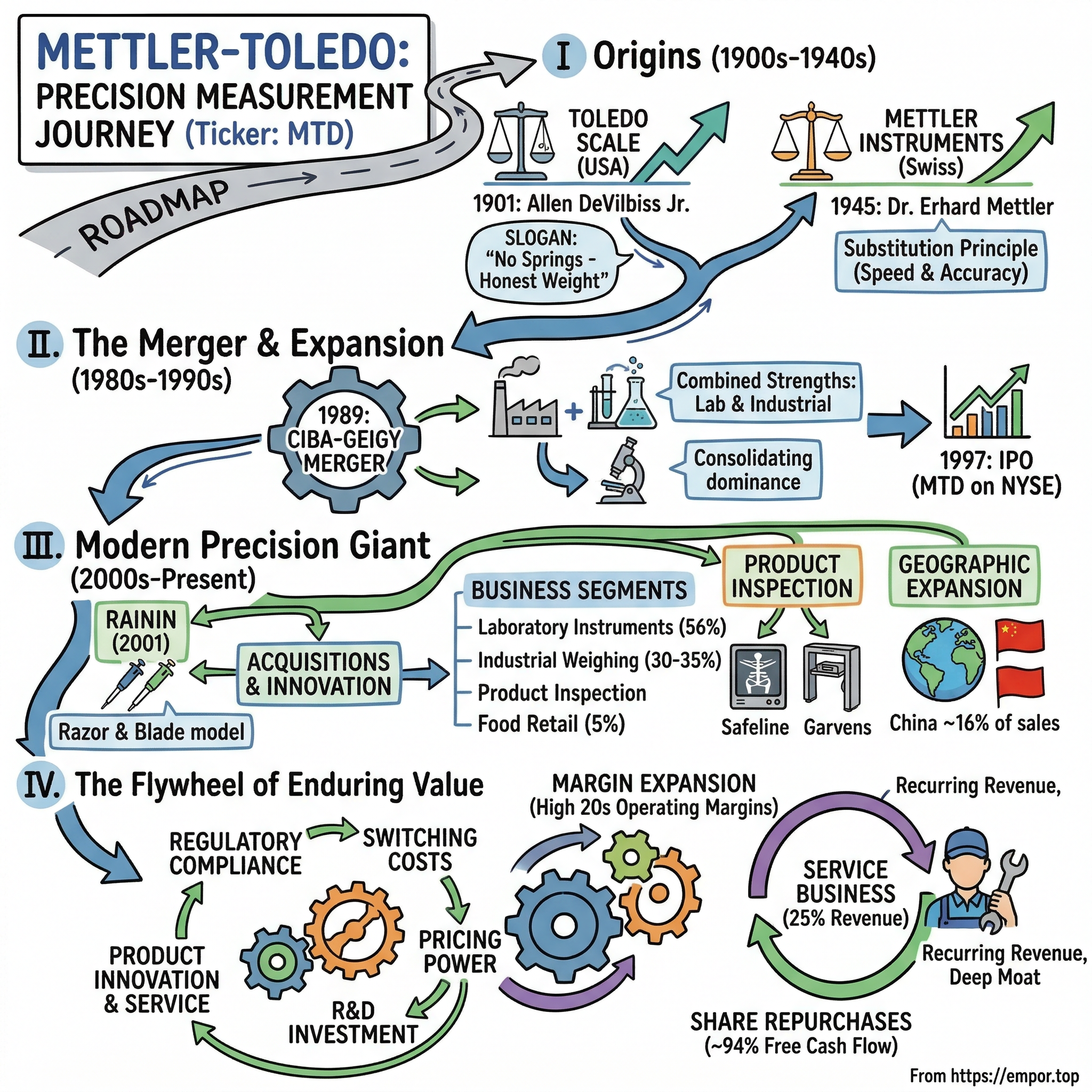

II. Two Origin Stories: Toledo Scale and Mettler Instruments

Toledo Scale Company (1901-1989)

Picture Toledo, Ohio, at the turn of the twentieth century — a booming industrial city on the western edge of Lake Erie, home to glass factories, oil refineries, and the restless energy of American manufacturing. In 1897, a local inventor named Allen DeVilbiss Jr. was tinkering with a problem that had vexed merchants for generations: how to weigh goods quickly and accurately without relying on spring-tension scales that degraded with temperature and wear. Springs lie. Gravity does not. DeVilbiss built a prototype pendulum-based scale that used actual gravitational force as its counterbalance, and by 1900, he had secured a patent for what he called the "automatic computing pendulum scale."

The concept was elegant. Traditional spring scales lost accuracy over time as the metal fatigued. Balance beam scales were accurate but painfully slow — a grocer had to slide weights back and forth, compute prices in his head, and hope the customer trusted the arithmetic. DeVilbiss's pendulum scale did the calculation automatically, displaying both weight and price on a visible dial. Legend has it that the first butcher to try the device was thrilled not because it saved time, but because it eliminated the suspicion of overcharging. Customers could see the weight for themselves. Trust was built into the mechanism.

Henry Theobald, a local businessman, recognized the commercial potential and purchased the DeVilbiss Computing Scale Company around 1900, formally founding the enterprise in 1901 under the name Toledo Computing Scale and Cash Register Company. Theobald was a marketing genius as much as a businessman. He coined the slogan that would define the brand for a century: "No Springs — Honest Weight." He hired DeVilbiss as the first factory manager, turning the inventor into the production overseer of his own creation. By 1902, the company had been renamed Toledo Computing Scale Company, and by 1912, simply Toledo Scale Company.

Growth was explosive. Within five years, Toledo scales were appearing on grocery counters across America — a pace of adoption that was remarkable by any standard. Consider the sales challenge: Theobald's salesmen were essentially asking grocers to spend six to ten times more than the simple balance scales they had been using for generations. The pitch required a fundamental reframing of value. A cheap scale might cost two or three dollars. A Toledo pendulum scale might cost twenty or thirty. But Theobald understood something his competitors did not: the hidden cost of an inaccurate scale was not borne by the grocer alone — it was shared by every customer who felt cheated and every honest merchant who lost business to a less scrupulous competitor.

The "Honest Weight" campaign became one of America's earliest examples of cause marketing — Toledo Scale positioned itself not just as a product manufacturer but as a champion of fair commerce, focusing public attention on the importance of accuracy in food retailing. The campaign had a moral dimension that resonated deeply in Progressive Era America, where consumer protection and anti-corruption sentiments were gaining political force. Toledo Scale was selling more than a device. It was selling trust — the same intangible that would remain the company's core value proposition more than a century later.

The company's product line expanded steadily. In 1906, the first cylinder scale appeared — bright blue with gold filigree, distinctly pendulum-type — establishing an aesthetic identity. In 1912, the double-pendulum industrial portable scale, the famous Toledo 800, created the foundation for the entire industrial weighing line. World War I proved a turning point: the military's insatiable demand for speed and accuracy in industrial weighing catapulted the company from retail counters into factories and warehouses.

World War II brought ordnance contracts and a new production facility completed fortuitously in the summer of 1939. Toledo Scale built precision fire-control equipment alongside its commercial scales, demonstrating the versatility of its engineering capabilities. By the postwar era, the company had cemented its position as the dominant American manufacturer of industrial and food retailing scale systems.

The postwar decades brought corporate transactions that would have bewildered the company's founders. In 1957, Toledo Scale merged with the Haughton Elevator Company, another venerable Toledo institution, forming Toledo Scale Corporation with combined annual sales exceeding forty million dollars. The logic was industrial diversification — a common strategy of the era, though the synergies between scales and elevators were, to put it charitably, abstract.

A decade later, in 1967, Reliance Electric Company of Cleveland acquired Toledo Scale Corporation for approximately seventy million dollars in stock. Operations moved to Columbus, Ohio, and Toledo Scale became a division of an electrical and mechanical equipment conglomerate. It was a decent fit — Reliance served similar industrial customers — but Toledo Scale was now one piece of a much larger portfolio, subject to capital allocation decisions made by executives whose primary expertise was in electric motors and drives, not precision weighing.

Then came the era of peak conglomerate fever. In December 1979, Exxon Corporation — the world's largest oil company — purchased Reliance Electric for one-point-two-four billion dollars. The rationale was Exxon's belief that it could apply a proprietary energy-saving motor technology across Reliance's electric motor business. The Toledo Scale division, representing perhaps fifteen to twenty-five percent of Reliance's revenue, was essentially an afterthought — acquired accidentally as part of a larger strategic bet. By the mid-1980s, Exxon's diversification strategy had proven disappointing across the board. The oil giant began unwinding its non-petroleum holdings, and in 1986, Reliance was sold through a highly leveraged buyout. Toledo Scale, the "No Springs — Honest Weight" company that had served American grocers and factories for nearly nine decades, was now a division of a leveraged buyout vehicle. It was a strange, circuitous corporate journey — but it was about to have a very happy ending.

Mettler Instruments (1945-1989)

Six time zones east and an ocean away, a very different origin story was unfolding. In 1945, as Europe emerged from the devastation of war, a Swiss engineer named Dr. Erhard Mettler started a precision mechanics company in Küsnacht, a small lakeside town near Zurich. Switzerland, with its centuries-old tradition of watchmaking and precision engineering, was the natural birthplace for what would become the world's most respected name in laboratory measurement.

Mettler's breakthrough was both conceptual and mechanical. For centuries, laboratory balances had used two pans — you placed your sample on one side and known weights on the other until the beam was level. It was accurate but slow, cumbersome, and required the scientist to handle individual calibration weights. Mettler invented what became known as the substitution principle: a single-pan analytical balance where internal calibrated weights were systematically removed until equilibrium was achieved with the sample. This could be produced in series for the first time — a critical manufacturing insight that turned precision balances from artisanal instruments into scalable products. By 1946, large-scale production was underway.

The single-pan balance gradually replaced conventional two-pan balances in laboratories worldwide. Scientists loved it because it was faster, more intuitive, and could be manufactured to exacting tolerances. By 1952, increasing demand forced Mettler to expand into a production facility in Stafa, Switzerland. The company was building what would become the gold standard in laboratory weighing — the instrument that every chemistry student, pharmaceutical researcher, and materials scientist would encounter throughout their career.

The next revolution arrived in 1973 with the PT1200 — the industry's first fully electronic precision balance. With a capacity of zero to twelve hundred grams and sensitivity to one-hundredth of a gram, the PT1200 eliminated mechanical components entirely, replacing levers and knife-edges with electromagnetic force restoration. Think of it as the transition from mechanical watches to quartz — the underlying physics changed completely, delivering faster readings, greater reproducibility, and lower maintenance. The PT1200 proved immediately successful and positioned Mettler at the vanguard of a digital transformation that would sweep through the entire instrument industry.

In 1980, the Swiss pharmaceutical and chemical conglomerate Ciba-Geigy acquired Mettler Instruments. Dr. Erhard Mettler, the founder, retired knowing that his company now had the resources and corporate backing to expand far beyond its laboratory roots. Ciba-Geigy understood something important: precision measurement was not just a product category — it was the connective tissue of the pharmaceutical and chemical industries they already dominated. Owning the instruments that verified the quality of their own products was a form of vertical integration that also happened to be a standalone business with attractive margins.

The Ciba-Geigy years would transform Mettler from a respected laboratory balance company into a diversified precision instruments powerhouse, setting the stage for the most consequential acquisition in the industry's history.

There is a beautiful symmetry in these two origin stories. DeVilbiss in Ohio solved a trust problem — how do you prove to a customer that the weight is honest? Mettler in Switzerland solved a speed problem — how do you give a scientist a precise measurement without making them wait? Both men understood that measurement is not really about numbers. It is about confidence. And the companies they built would spend the next century finding ever more sophisticated ways to deliver that confidence to ever more demanding customers.

III. The Art of Scientific Acquisitions (1960s-1980s)

Under the protective umbrella of Ciba-Geigy's resources, Mettler embarked on a two-decade acquisition campaign that reads like a chess grandmaster methodically controlling the board. Each move was deliberate, each target carefully chosen to fill a specific gap in the product portfolio or extend the company's reach into an adjacent market. The strategy was not to build an empire through blockbuster deals but to assemble a precision instruments conglomerate through a series of small, synergistic acquisitions — each one adding a new capability, a new technology, or a new customer relationship.

The first acquisition came in 1962 with the purchase of Dr. Ernst Rüst AG, a maker of high-precision mechanical scales. The company was renamed Mettler Optic AG, signaling Mettler's ambition to move beyond weighing into broader optical and measurement technologies. This was a modest deal, but it established the acquisition playbook: identify small, technically excellent companies with strong positions in narrow niches, bring them into the Mettler fold, and leverage the combined R&D and manufacturing capabilities to accelerate growth.

The 1970 acquisition of Microwa AG strengthened Mettler's core balance business while the simultaneous introduction of automated titration systems marked the company's first serious diversification beyond weighing. Titration — the process of determining the concentration of a dissolved substance — is fundamental to analytical chemistry, and entering this market gave Mettler its first product line that was used alongside its balances rather than as a substitute. The strategic logic was powerful: a laboratory that already trusted Mettler for weighing would naturally consider Mettler for titration, especially if the instruments could share data and software platforms.

The 1971 acquisition of August Sauter KG in Albstadt-Ebingen, Germany, was the most transformative move of the decade. Sauter specialized in industrial and retail scales, areas where Mettler had virtually no presence. With more than five hundred employees, this was not a small technology tuck-in — it was a strategic bet that precision measurement had commercial potential far beyond the laboratory. Sauter brought manufacturing capability, distribution relationships, and deep expertise in the rugged, high-volume world of industrial weighing. For the first time, Mettler had a credible presence on factory floors and in retail stores.

In 1986, Mettler acquired the Ingold Firmengruppe, a fellow Swiss company with a line of laboratory and industrial-use electrodes and sensors. This extended Mettler's reach beyond weighing and titration into pH measurement, dissolved oxygen sensing, and other critical analytical parameters. Electrodes and sensors are consumable products — they degrade with use and must be regularly replaced — introducing Mettler to the economics of recurring revenue that would later become central to the company's financial model.

The following year, 1987, brought Garvens Automation GmbH, a company based near Hanover, Germany, that manufactured dynamic checkweighers, dosage control systems, and processing equipment. Checkweighing — the act of verifying that packaged products meet weight specifications — is a regulatory requirement in food and pharmaceutical manufacturing. By acquiring Garvens, Mettler entered the product inspection business and gained its first foothold in the high-speed production line environment. The Garvens brand remains a key product line within Mettler-Toledo's product inspection division today, nearly four decades later.

Step back and observe the pattern. Over twenty-five years, Mettler moved from laboratory balances (1945) to optics (1962), to broader balance manufacturing (1970), to industrial and retail scales (1971), to electrodes and sensors (1986), to checkweighing and production line inspection (1987). Each acquisition expanded the addressable market while reinforcing the company's core competency in precision measurement. None of these deals was large enough to be risky. All of them were technologically adjacent. And collectively, they transformed Mettler from a single-product laboratory company into a diversified precision instruments platform with exposure to pharmaceutical, chemical, food, and manufacturing end markets. For investors, the lesson is that the most durable competitive advantages are often built not through one transformational deal but through patient, disciplined accumulation of complementary capabilities over decades.

IV. The Mega-Merger: Creating Mettler-Toledo (1989-1992)

By the late 1980s, the global weighing industry had an obvious problem: its two most respected brands operated on opposite sides of the Atlantic with almost perfectly complementary strengths and almost zero overlap. Mettler was the undisputed laboratory standard — the name that appeared on virtually every precision balance in every serious research laboratory in the world. Toledo was the undisputed American industrial and retail champion — the company that weighed everything from boxcars of grain to deli meat in supermarkets. One dominated the lab, the other the factory floor. One was Swiss, the other as American as the Ohio River.

The catalyst for their union was Exxon's retreat from diversification. When the oil giant decided in the mid-1980s to shed its non-petroleum assets, Reliance Electric — and with it, Toledo Scale — became available. Ciba-Geigy, already the owner of Mettler Instruments, saw the opportunity with the clarity that only a strategic buyer can have. In 1989, Ciba-Geigy acquired Toledo Scale Corporation from Reliance Electric, immediately merged it with Mettler, and rechristened the combined entity Mettler-Toledo AG.

The strategic logic was compelling on multiple levels. Toledo brought what Mettler lacked: massive brand recognition in North America, deep relationships with industrial and retail customers, and a manufacturing and service infrastructure scaled for high-volume production. Mettler brought what Toledo lacked: world-class laboratory technology, a reputation for Swiss-engineered precision, and a diversified analytical instrument portfolio that extended well beyond weighing. Together, they created a company with a uniquely complete product line — from ultra-microbalances that could measure a fraction of a microgram in a pharmaceutical R&D lab to heavy-duty industrial platform scales that weighed trucks.

The cultural integration was perhaps the greater challenge. Swiss precision culture — methodical, consensus-driven, engineering-obsessed — met American industrial pragmatism — faster-moving, sales-oriented, focused on throughput and market share. The merged company had to reconcile these different approaches to quality, innovation, and customer relationships without losing the distinctive strengths of either heritage. The "No Springs — Honest Weight" ethos of Toledo and the substitution-principle elegance of Mettler were not just engineering philosophies; they were organizational identities.

The newly formed Mettler-Toledo AG wasted no time expanding. In 1990, the company acquired Contraves AG's rheology and laboratory automation systems division in Zurich, adding viscosity measurement and laboratory workflow automation to the portfolio. The same year brought the acquisition of Ohaus Corporation, a laboratory balance manufacturer that had been one of Mettler's competitors. By absorbing Ohaus, Mettler-Toledo consolidated its dominance in laboratory balances while eliminating a rival — a classic strategic move that simultaneously strengthened market position and reduced competitive pressure.

In 1992, the company was formally incorporated as Mettler Toledo, Inc., establishing the legal structure that would carry it through its eventual public listing. By this point, the combined entity had achieved something rare in industrial M&A: a merger that was genuinely greater than the sum of its parts. Laboratory customers now had access to Toledo's industrial products when they needed to scale processes from bench to plant. Industrial customers now had access to Mettler's analytical precision when they needed laboratory-grade measurement. The cross-selling opportunities were enormous, and they were grounded in real technical complementarity rather than financial engineering.

For Ciba-Geigy, the merger had been a masterful piece of portfolio construction. They had taken a strong but narrow laboratory balance company and, through a decade of disciplined acquisitions followed by the transformative Toledo deal, built a global precision instruments platform with multiple revenue streams, geographic diversification, and a product line that touched virtually every point in the value chain of their core pharmaceutical and chemical customers.

V. The Private Equity Interlude and IPO (1996-1997)

The mid-1990s brought a tectonic shift in the Swiss pharmaceutical landscape that would reshape Mettler-Toledo's ownership structure. Ciba-Geigy and Sandoz, two of Switzerland's largest pharmaceutical companies, were negotiating what would become one of the largest corporate mergers in history — the creation of Novartis. When massive pharmaceutical companies merge, the focus is ruthlessly simple: consolidate drug pipelines, eliminate redundancies, and shed non-core assets. A precision instruments company, no matter how profitable, was definitionally non-core for a combined pharmaceutical giant.

In October 1996, AEA Investors, a New York-based private equity firm with a reputation for disciplined investing in industrial businesses, orchestrated a management buyout of Mettler-Toledo. The transaction was valued at four hundred and two million dollars — a price that, in retrospect, looks like one of the great bargains in industrial private equity history. AEA's playbook was straightforward: partner with existing management, professionalize the capital structure, and prepare the company for a public offering.

The management buyout was significant for reasons beyond the change in ownership. For the first time in decades, Mettler-Toledo's leadership team had direct economic incentives tied to the company's performance. Under Ciba-Geigy, the company had been a well-run division of a conglomerate — profitable, technically excellent, but ultimately subject to the strategic priorities and capital allocation decisions of a parent company focused on pharmaceuticals. Independence meant that every dollar of free cash flow could be reinvested in the business, spent on acquisitions, or returned to shareholders rather than being redirected to fund drug development pipelines.

The IPO followed swiftly. In November 1997, Mettler-Toledo International Inc. began trading on the New York Stock Exchange under the ticker symbol MTD. The holding company was domiciled in the United States — Columbus, Ohio — for listing purposes, while operational headquarters remained in Greifensee, Switzerland. The dual identity reflected the company's transatlantic heritage: legally American, culturally Swiss, and operationally global.

Going public provided three critical advantages. First, it gave Mettler-Toledo access to the deepest capital markets in the world, enabling the company to pursue larger acquisitions than would have been possible under conglomerate or private equity ownership. Second, the public listing created a liquid currency — publicly traded stock — that could be used for acquisitions, executive compensation, and employee retention. Third, the discipline of quarterly reporting and public market scrutiny created accountability structures that, when combined with the company's engineering-driven culture, would produce one of the most consistently impressive operational records in the industrial sector.

The transition from conglomerate division to private equity holding to independent public company took less than eighteen months but fundamentally altered Mettler-Toledo's trajectory. The company was now free to allocate capital according to its own strategic priorities, set its own pace of innovation and acquisition, and build a shareholder base that valued long-term compounding over quarterly pharmaceutical pipeline updates.

To put the magnitude of the value creation in perspective: AEA Investors paid four hundred and two million dollars for the business in 1996. At the time of this writing, Mettler-Toledo's market capitalization exceeds twenty-eight billion dollars. The IPO price of roughly sixteen dollars per share, adjusted for subsequent stock appreciation, has compounded at approximately eighteen to nineteen percent annually over nearly three decades — making the 1997 IPO one of the most rewarding public market entries for patient investors in the history of American industrials.

The IPO was not merely a liquidity event — it was the beginning of Mettler-Toledo's modern era as a precision compounding machine. And for AEA Investors, it validated a private equity thesis that would be repeated across industries for decades to come: that well-managed industrial businesses with strong market positions, trapped inside unfocused conglomerates, could create extraordinary value when liberated and properly capitalized.

VI. Building the Modern Precision Giant (1998-2010s)

With the constraints of conglomerate ownership removed and public market capital available, Mettler-Toledo entered the twenty-first century with a clear strategy: become the undisputed global leader in precision instruments through targeted acquisitions, relentless geographic expansion, and the systematic build-out of a high-margin service business.

The most consequential post-IPO acquisition came in 2001 with the purchase of Rainin Instrument for two hundred and ninety-two million dollars — the largest deal in the company's history. Rainin was the leading manufacturer of pipetting solutions: manual and electronic pipettes, pipette tips, and liquid handling accessories used in pharmaceutical, biotechnology, and medical research laboratories. The strategic significance of this deal cannot be overstated. Pipettes are the workhorse tools of modern biology — every experiment that requires transferring precise volumes of liquid depends on them. And pipette tips are classic consumables: single-use, disposable, and purchased in enormous quantities. By acquiring Rainin, Mettler-Toledo gained its first true razor-and-blade business model, where the instrument sale was merely the gateway to years of recurring tip revenue.

Beyond Rainin, the company pursued a steady stream of smaller technology acquisitions designed to fill specific gaps in the product portfolio. Each deal followed the same disciplined template established in the 1960s and 1970s: identify a technically excellent company in an adjacent niche, acquire it at a reasonable price, integrate it into the Mettler-Toledo sales and service infrastructure, and leverage the combined platform to accelerate growth. The most recent notable acquisitions include PendoTECH in 2021 — a Princeton, New Jersey maker of single-use sensors and control systems for bioprocess applications, acquired for approximately one hundred and eighty-five million dollars plus contingent consideration — and Acme Scale in 2023, adding industrial precision measurement and calibration services.

Geographic expansion followed a deliberate pattern. Mettler-Toledo invested heavily in building direct operations in high-growth markets rather than relying on distributors. The company established a substantial presence in China over thirty-five years, building seventeen entities including manufacturing sites, R&D centers, and sales offices. China grew to represent approximately sixteen percent of total sales. Similar investments in India, Southeast Asia, Latin America, and the Middle East created a direct presence in roughly forty countries, with products reaching more than one hundred and forty nations.

The decision to invest in direct sales and service rather than distributor relationships was expensive but strategically brilliant. A direct field force of approximately nine thousand sales and service professionals creates intimate customer relationships that distributors cannot replicate. When a Mettler-Toledo service technician calibrates a laboratory balance every six months, that visit is not just a revenue event — it is a competitive moat deepened, a switching cost reinforced, and a pipeline for the next instrument upgrade opened. The service business crossed a symbolic milestone in 2025 when it surpassed one billion dollars in annual revenue, representing approximately twenty-five percent of total sales and growing faster than the product business.

The internal operating culture deserves attention. Mettler-Toledo's management system, known internally as "Spinnaker," emphasizes lean manufacturing, continuous improvement, and disciplined pricing. Combined with a complementary initiative called "SternDrive," focused on sales force effectiveness and go-to-market efficiency, these programs have driven adjusted operating margins from the low twenties at the time of the IPO to nearly thirty percent in recent years. This is exceptional for a diversified industrial company and speaks to a culture that treats every basis point of margin as hard-won territory that must be defended.

The company's R&D investment has been remarkably consistent: approximately five percent of revenue every year, amounting to roughly five hundred and fifty million dollars over the three most recent years. This spending supports a portfolio of over five thousand four hundred patents and ensures that Mettler-Toledo maintains its technological edge in an industry where precision, reliability, and regulatory compliance are non-negotiable requirements. The investment in R&D is not a growth bet in the startup sense — it is a maintenance expenditure on the moat, ensuring that competitive advantages do not erode as technology evolves.

The leadership transition in 2021 is worth noting. Patrick Kaltenbach joined as CEO in April 2021, succeeding Olivier Filliol who had led the company for over a decade. Kaltenbach brought a distinctly life sciences pedigree — he had led the Life Sciences Segment at Becton Dickinson and before that served as President of the Life Sciences and Applied Markets Group at Agilent Technologies, with a career tracing back to Hewlett-Packard in 1991. His appointment signaled the board's view that Mettler-Toledo's future growth would be increasingly tied to pharmaceutical, biotechnology, and life sciences customers — the highest-margin, most regulation-intensive segments in the portfolio. CFO Shawn Vadala, who joined the company in 1997 — the same year as the IPO — provides continuity and institutional memory, with particular expertise in the pricing discipline that has been central to margin expansion.

One innovation that illustrates the company's approach to leveraging technology is Good Weighing Practice, or GWP — a risk-based global weighing standard that Mettler-Toledo created and then successfully positioned as an industry-recognized framework. By establishing the standard by which weighing processes are evaluated, the company effectively wrote the rules of the game it dominates. When pharmaceutical quality departments adopt GWP, they are adopting Mettler-Toledo's methodology, documentation, and calibration framework — embedding the company's intellectual property into the customer's compliance infrastructure. It is a masterclass in turning domain expertise into institutional lock-in.

VII. The Business Model: Razors, Blades, and Lab Coats

To understand why Mettler-Toledo has been such a remarkable compounder, it helps to break down the business model into its component parts and examine how each one generates revenue, creates switching costs, and reinforces the others.

The laboratory instruments division, representing roughly fifty-six percent of net sales, is the heart of the company. This encompasses analytical balances so sensitive they can detect the weight of a human fingerprint, precision balances for everyday laboratory work, pipetting systems from the Rainin brand, automated chemical reactors, titrators, pH meters, thermal analysis instruments, UV/VIS spectrophotometers, and moisture analyzers. Each of these instruments comes with embedded software and often connects to proprietary data platforms, creating an ecosystem that becomes progressively harder to leave as a laboratory invests more deeply.

Consider the economics of a pharmaceutical research laboratory. A single analytical balance might cost five thousand to fifteen thousand dollars and last ten to fifteen years. But during that lifespan, the laboratory will spend multiples of the purchase price on calibration services (typically two to four times per year at several hundred dollars per visit), compliance verification documentation, software licenses for data management, and replacement parts. A Rainin pipette might cost three hundred to two thousand dollars, but the laboratory will consume tens of thousands of dollars in disposable tips over the instrument's lifetime — tips that must be purchased from Rainin because third-party alternatives risk compromising the validated pipetting procedure.

The initial sale is the least profitable part of the relationship — the real value accrues over years of service and consumables revenue. Think of it this way: selling the instrument is like selling a printer, while calibration, tips, and compliance services are the ink cartridges. Except in this case, the ink cartridges are mandated by federal regulators, and using off-brand alternatives could invalidate your FDA approval.

The industrial weighing division, roughly thirty to thirty-five percent of revenue including product inspection, serves pharmaceutical, chemical, food, and discrete manufacturing customers with scales, weighing terminals, and related software for applications ranging from formulation and filling to inventory management. In a pharmaceutical factory, for example, every ingredient in a drug formulation must be weighed with documented precision. The weighing system is not just a tool — it is part of the regulatory record, connected to batch documentation and quality management systems that the FDA reviews during inspections. Replacing that system means revalidating the entire process, a costly and time-consuming undertaking that most manufacturers simply prefer to avoid.

Product inspection — metal detection, X-ray inspection, checkweighing, and vision systems — accounts for another meaningful share of revenue and operates on a similar logic of regulatory necessity. Food manufacturers must demonstrate that their products are free from metal contamination, correctly weighted, and properly packaged. These are not optional quality checks — they are legal requirements in virtually every developed market. The Safeline metal detection and X-ray brands, the Garvens and Hi-Speed checkweighers, and the CI-Vision inspection systems are embedded in production lines where removing them would halt manufacturing.

Food retail, approximately five percent of revenue, is the smallest but most visible division. These are the scales at the supermarket deli counter, the self-service produce scales, and the checkout weighing systems. While less profitable than the laboratory or industrial divisions, food retail creates brand visibility and serves as the modern expression of Toledo Scale's original "Honest Weight" mission.

The recurring revenue model is the financial engine that powers the entire enterprise. Service contracts generate predictable, high-margin revenue while creating regular touchpoints with customers. Calibration visits are not merely maintenance — they are opportunities to assess the customer's future needs, recommend upgrades, and deepen the relationship. Management has noted that the company has penetrated only about one-third of its approximately three-billion-dollar serviceable installed base, suggesting significant remaining runway for service revenue growth even without any new product sales.

The regulatory lock-in deserves special emphasis because it represents a competitive advantage that is nearly impossible to replicate. In industries governed by Good Manufacturing Practice, Good Laboratory Practice, and similar regulatory frameworks, every piece of measurement equipment must be validated, calibrated according to documented procedures, and maintained with full traceability. Switching vendors means revalidating instruments, rewriting standard operating procedures, retraining staff, and potentially inviting regulatory scrutiny during the transition. The cost of switching is not just financial — it is operational risk in environments where a compliance failure can shut down a production line or invalidate years of clinical trial data.

VIII. Market Position and Competitive Dynamics

Mettler-Toledo operates from a position of strength that most industrial companies can only envy. In laboratory balances, the company commands an estimated global market share exceeding fifty percent. Across virtually all of its product categories, it holds the number one or number two position globally. This dominance did not happen by accident — it was constructed over decades through the strategic acquisitions described earlier, continuous R&D investment, and the painstaking build-out of a direct sales and service infrastructure that competitors have found nearly impossible to replicate.

The competitive landscape varies by segment but shares common characteristics. In laboratory instruments, the primary competitors include Sartorius, the German precision instruments company that has carved out a strong position in bioprocess and laboratory weighing; Shimadzu, the Japanese analytical instrument manufacturer with particular strength in Asian markets; and A&D Company, another Japanese manufacturer offering competitive pricing in the precision balance market. In the broader analytical instruments space, giants like Thermo Fisher Scientific, Danaher, and Agilent Technologies compete in overlapping categories, though each has a different product focus.

In industrial weighing, the competitive field includes Minebea Intec (formerly Sartorius Industrial), Avery Weigh-Tronix (part of Illinois Tool Works), and various regional players. The product inspection market features Ishida, a Japanese manufacturer with strong checkweighing capabilities, alongside numerous smaller specialists in metal detection and X-ray inspection.

What makes Mettler-Toledo's competitive position so durable is the interaction between multiple moat layers. The brand moat — over a century of the Toledo name in industrial and retail weighing, nearly eight decades of the Mettler name in laboratories — creates trust that new entrants cannot buy. The switching cost moat — driven by regulatory validation requirements, software integration, and service relationships — makes customers rationally reluctant to change. The service network moat — nine thousand professionals in forty countries — provides a coverage density that no startup or regional competitor can match. And the R&D moat — five percent of revenue invested annually, over five thousand patents — ensures that the technology stays current.

A question that sophisticated investors often ask is: why has not Amazon or another technology giant disrupted this space? The answer reveals something important about the nature of these markets. Precision measurement in regulated industries is not a commodity that can be optimized through logistics and scale. A laboratory balance is not a consumer product where the cheapest adequate option wins. It is a component of a regulated quality system where accuracy, traceability, regulatory compliance, and ongoing service support matter more than price. The value proposition is not "we measure weight" — it is "we provide documented, defensible measurement that will satisfy an FDA inspector." That is a fundamentally different competitive game, and it is one where incumbency, regulatory expertise, and customer intimacy matter enormously.

The customer base itself is a source of resilience. No single end-customer accounts for more than one percent of total sales — a level of diversification that is almost unheard of among industrial companies of this size. This means that the loss of any individual customer, even a major pharmaceutical company, would have negligible impact on consolidated results. The diversification extends across industries as well — pharmaceutical, chemical, food, academic, industrial manufacturing — reducing exposure to any single end-market cycle.

There is a common myth about Mettler-Toledo that deserves debunking: the idea that it is "just a scale company." This framing misses the essential truth of the business. Mettler-Toledo is not selling measurement devices — it is selling regulatory compliance, operational confidence, and data integrity. The physical instrument is merely the delivery mechanism for a much more valuable package of software, services, documentation, and institutional trust. A scale from a no-name manufacturer might measure weight just as accurately in a laboratory test. But it will not come with FDA-compliant data integrity software, installation and operational qualification documentation, a globally accredited calibration service, or a field engineer who understands the customer's specific regulatory requirements. The instrument is perhaps thirty percent of the value proposition. The other seventy percent is everything that surrounds it.

This distinction matters enormously for understanding the company's pricing power. Mettler-Toledo's instruments carry a fifteen to twenty percent premium over comparable Asian alternatives. At first glance, this seems like a vulnerability — why would a cost-conscious procurement officer pay more? The answer is that the procurement officer is not the buyer. The quality assurance director is. And for a quality assurance director at a pharmaceutical company, the cost of a weighing instrument is trivial compared to the cost of a compliance failure. An FDA warning letter, a product recall, or a clinical trial invalidation can cost tens or hundreds of millions of dollars. In that context, paying a twenty percent premium for the industry-standard instrument with the best regulatory support infrastructure is not a luxury — it is risk management.

IX. Financial Performance and Capital Allocation

Mettler-Toledo's financial record reads like a case study in disciplined operational execution. Full year 2025 revenue reached four-point-zero-three billion dollars, a three percent increase in local currency terms over 2024, with reported growth of four percent after currency effects. The year showed a clear acceleration from a weak first quarter — when tariff disruptions and trade uncertainty dragged local currency sales down three percent — through progressively stronger performance, culminating in a fourth quarter where local currency sales grew five percent and reported sales jumped eight percent.

Adjusted earnings per share for 2025 came in at forty-two dollars and seventy-three cents, a four percent increase over the prior year and above the high end of management's earlier guidance range. The adjusted operating margin for the full year was approximately twenty-nine-point-six percent — impressive by any industrial standard, though down about one hundred and forty basis points from the prior year due primarily to fifty million dollars of incremental tariff costs that compressed margins across all segments.

The quarterly progression tells a story of resilience and recovery. First quarter adjusted EPS of eight dollars and nineteen cents was down eight percent year-over-year as tariffs hit hardest. By the fourth quarter, adjusted EPS had climbed to thirteen dollars and thirty-six cents, up eight percent, with broad-based growth across all regions. Americas local currency sales grew seven percent in the fourth quarter, Europe grew four percent, and Asia and the rest of the world grew four percent. Product inspection surged seven percent organically, and food retail jumped nineteen percent in the fourth quarter, suggesting that replacement cycles in these segments are accelerating.

The capital allocation philosophy is where Mettler-Toledo most clearly distinguishes itself from industrial peers. The company generates roughly eight hundred and fifty to nine hundred million dollars in annual free cash flow. In 2025, management deployed eight hundred million dollars — ninety-four percent of free cash flow — to share repurchases. Since launching its initial buyback program in 2010, the company has repurchased nearly eighteen million shares for a cumulative nine-point-five billion dollars. The diluted share count has declined approximately three percent annually, systematically converting even modest organic revenue growth into meaningful per-share earnings growth.

This capital allocation strategy is both the company's greatest financial innovation and its most debated characteristic. Bulls point to the mathematical elegance: in a business that generates high-twenties operating margins and converts virtually all earnings into free cash flow, aggressive buybacks create a powerful compounding engine for per-share value. A company growing revenue three to four percent, expanding margins modestly, and shrinking the share count three percent annually can deliver high-single-digit to low-double-digit EPS growth year after year without any heroic assumptions.

Bears counter that the strategy has left the balance sheet leveraged — the company carries approximately two-point-one billion dollars of debt against only about sixty million in cash, resulting in negative shareholders' equity. This makes the business more sensitive to economic downturns and leaves little cushion if a large acquisition opportunity or unexpected crisis demands capital. The philosophical tension between relentless buybacks and balance sheet prudence is a recurring theme in analyst discussions.

For 2026, management has guided to local currency sales growth of approximately four percent, adjusted EPS of forty-six dollars and five cents to forty-six dollars and seventy cents (implying eight to nine percent growth), and free cash flow of approximately nine hundred million dollars. The company plans to spend eight hundred and twenty-five to eight hundred and seventy-five million dollars on share repurchases, continuing the pattern of deploying nearly all free cash flow to buybacks.

The tariff story deserves attention because it illustrates the company's operational agility. When trade tensions escalated in early 2025, management initially estimated gross incremental tariff costs of one hundred and fifteen million dollars — a meaningful hit to a company with roughly one-point-two billion dollars in adjusted operating profit. Within months, the company reduced that estimate to sixty million dollars through a combination of manufacturing diversification (including expansion in Mexico to reduce reliance on high-tariff regions), supply chain restructuring, and pricing actions. The ability to offset more than half of the initial tariff impact through operational responses — rather than simply absorbing the cost or passing all of it to customers — speaks to the flexibility embedded in the company's global manufacturing footprint and the pricing power inherent in its market position.

The return on invested capital merits emphasis. Mettler-Toledo's ROIC has expanded from approximately thirty percent in 2019 to the mid-to-high thirties in recent periods — figures that place it among the elite cohort of industrial companies in terms of capital efficiency. The asset-light nature of the business, with capital expenditure running at only three to four percent of revenue, means that the company requires very little incremental investment to grow. This combination of high returns on invested capital and low capital intensity is the fundamental engine of the compounding machine — every dollar of retained earnings generates outsized returns, and there are few capital-hungry projects competing for those dollars, leaving free cash flow available for buybacks.

X. Playbook: Business and Investing Lessons

The Mettler-Toledo story distills into several powerful lessons that extend far beyond the precision instruments industry.

The first lesson is the power of boring, mission-critical products. Weighing and measurement will never generate the excitement of artificial intelligence, electric vehicles, or social media. But that dullness is precisely the point. Boring industries attract fewer competitors, face less regulatory scrutiny around market concentration, and rarely experience the kind of technological disruption that destroys value overnight. When your products are embedded in customers' regulatory compliance systems, the cost of displacement is not just the price of a new instrument — it is the price of operational disruption, regulatory risk, and institutional inertia. These switching costs compound over time, creating durability that flashier businesses often lack.

The second lesson is the strategic value of serial acquisition in fragmented markets. Mettler-Toledo did not build its portfolio through one or two transformational deals. It assembled its capabilities through dozens of targeted acquisitions over six decades — each one small enough to integrate without cultural trauma, each one technologically adjacent enough to leverage existing distribution and service infrastructure. This approach requires patience and discipline that most management teams and boards lack, but the cumulative effect is a competitive position that no single acquisition could have created. The acquisition of Rainin in 2001 illustrates the template perfectly: a two-hundred-and-ninety-two-million-dollar deal for a company that was the clear leader in its niche, with a consumables business that would generate recurring revenue for decades. No bidding wars, no hostile takeovers, no empire building — just the steady accumulation of complementary businesses that fit naturally into the existing platform.

The third lesson is the transition from product revenue to service revenue. Every mature industrial company faces the challenge of commoditization as products age and competitors close the technology gap. Mettler-Toledo's answer has been to make the product sale the beginning of the customer relationship rather than the end. Calibration contracts, compliance services, software subscriptions, and consumables like Rainin pipette tips create recurring revenue streams that are higher-margin, more predictable, and more resistant to economic cycles than instrument sales alone. The service business is still under-penetrated relative to the installed base, providing a visible growth runway that does not depend on new market creation.

The fourth lesson is that geographic diversification, when executed through direct investment rather than distributor relationships, creates both growth opportunities and risk management benefits. By building direct operations in forty countries, Mettler-Toledo has insulated itself from dependence on any single market while creating deep customer relationships that distributors simply cannot provide.

The fifth lesson, specifically relevant for investors, is the power of disciplined capital allocation in asset-light businesses. Mettler-Toledo's management has demonstrated that in a high-margin, high-cash-conversion business, consistent share repurchases can create extraordinary long-term compounding. The company's stock has been one of the best-performing industrials over the past two decades, and the buyback program has been a significant contributor to that performance. Whether this strategy is sustainable at current valuations is a matter of ongoing debate, but the historical record is undeniable.

The sixth lesson is the counterintuitive power of the PE-to-public transition for industrial businesses. Mettler-Toledo's ownership journey — from independent company to conglomerate division (Ciba-Geigy) to private equity holding (AEA Investors) to publicly traded company — illustrates how the right ownership structure at the right time can unlock value. Under Ciba-Geigy, the company had access to capital for acquisitions but lacked operational autonomy. Under AEA, it gained management alignment through equity incentives but needed public market access for larger ambitions. As a public company, it got both — plus the discipline of quarterly accountability. The lesson for founders is that ownership structure is not merely a financial question; it is an operational one.

Finally, there is the regulatory moat lesson. In industries where government agencies dictate measurement standards, documentation requirements, and equipment validation procedures, the regulatory framework itself becomes a competitive barrier. Companies that invest in understanding and embedding regulatory requirements into their products create advantages that cannot be overcome by technology alone — because the barrier is not technical, it is institutional. Mettler-Toledo's creation of the Good Weighing Practice standard took this one step further: the company did not merely comply with regulations; it wrote the compliance methodology that the industry adopted, making its own expertise the standard against which all weighing processes are evaluated.

XI. Analysis: Bear vs. Bull Case

Bull Case

The bull case for Mettler-Toledo rests on the durability and self-reinforcing nature of its competitive advantages, analyzed through the lens of Hamilton Helmer's Seven Powers framework. The company possesses at least four of Helmer's powers in meaningful strength.

Switching costs are perhaps the strongest power. The regulatory validation requirements in pharmaceutical and food manufacturing create rational lock-in that persists for the lifetime of the equipment and beyond. When a pharmaceutical manufacturer validates a Mettler-Toledo analytical balance within its Good Manufacturing Practice quality system, the revalidation cost to switch to a competitor's instrument can range from fifty thousand to five hundred thousand dollars per instrument type per manufacturing site. FDA inspectors review specific equipment calibration records during audits. Lab technicians are trained on Mettler-Toledo's specific software interfaces. Data integrity trails are tied to individual instrument serial numbers. The cost of switching vastly exceeds the cost of the instrument itself — a classic Helmer switching cost power.

Process power is evident in the Spinnaker operating system and SternDrive sales effectiveness programs that have driven adjusted operating margins from the low twenties to nearly thirty percent over a fifteen-year span. This operational excellence has been refined iteratively over two decades and is embedded in institutional culture — it cannot be copied by reading a case study or hiring a few executives. The gross margin of approximately fifty-nine percent is extraordinary for an industrial company and roughly sixty-five percent above the industrial sector average, reflecting process power in both manufacturing and pricing.

Branding power exists in both the Mettler and Toledo names, which carry decades of trust in their respective markets. In pharmaceutical quality control, specifying Mettler-Toledo on equipment lists has become almost reflexive — similar to how architects specify certain trusted building material brands. The brand commands a fifteen to twenty percent price premium over comparable Asian instruments, and that premium has proven durable even as competitor quality has improved.

Scale economies operate through the company's global manufacturing footprint and nine-thousand-person direct service force. Spreading two hundred million dollars of annual R&D across a dominant market share gives Mettler-Toledo a per-unit R&D cost advantage that smaller competitors cannot match. The global service infrastructure creates economies of density — each additional customer in a city or region is served at lower marginal cost because the service technician is already nearby.

The company also has a partial claim to cornered resource power through its deep institutional expertise in precision metrology — knowledge accumulated over eight decades that cannot be hired away or reverse-engineered. The creation of the Good Weighing Practice standard is a tangible example: by writing the rules of the game, Mettler-Toledo has made its own institutional knowledge into an industry resource that competitors must engage with on Mettler-Toledo's terms. The two powers the company clearly lacks are network effects (one customer's use of a balance does not make it more valuable to another customer) and counter-positioning (its strategy is now well understood and does not surprise competitors).

From a Porter's Five Forces perspective, the industry structure is equally favorable. The threat of new entrants is low — a new entrant would need three to five years and tens of millions of dollars to achieve the regulatory certifications, ISO accreditations, and FDA compliance capabilities that Mettler-Toledo has built over decades. Buyer power is limited because no single customer represents more than one percent of sales, and customers in regulated industries face high switching costs that make them reluctant to negotiate aggressively on price. Supplier power is manageable because Mettler-Toledo outsources commodity components while keeping proprietary technology in-house, giving it multiple qualified suppliers for most inputs. The threat of substitutes is minimal — you cannot replace an analytical balance with software or a different technology. And competitive rivalry, while it exists, is disciplined: a small number of established players compete primarily on technology, service quality, and regulatory expertise rather than price, which protects margins across the industry.

Comparing against specific competitors sharpens the picture. Sartorius, the closest direct rival in laboratory balances, has carved out a strong position in bioprocess applications and holds an estimated twenty-two percent share versus Mettler-Toledo's estimated forty to forty-five percent in high-precision analytical balances. However, Sartorius lacks Mettler-Toledo's breadth in industrial weighing, product inspection, and food retail. Shimadzu and A&D Company offer instruments at fifteen to twenty percent price discounts, making inroads in cost-sensitive segments like academic research and developing markets. But they lack the global service infrastructure, regulatory compliance documentation, and brand trust that command premium pricing in pharmaceutical and food manufacturing. Thermo Fisher Scientific and Danaher, while orders of magnitude larger, compete in adjacent rather than core Mettler-Toledo segments and do not match the company's focus and depth in precision weighing.

The specific growth drivers are compelling. The service business, still under-penetrated at roughly one-third of the serviceable installed base, offers years of visible growth at margins above the company average. Laboratory automation trends — driven by pharmaceutical companies' need to increase throughput and reduce human error — play directly to Mettler-Toledo's strengths in automated reactors, liquid handling, and integrated software platforms. The company has invested in Industry 4.0 connectivity, including intelligent load cells with integrated microprocessors and IoT-enabled instruments that connect to manufacturing execution systems and enterprise resource planning platforms. Emerging market expansion, particularly in Asia, offers secular growth as developing economies build pharmaceutical, food safety, and manufacturing infrastructure that requires precision measurement. And the company's pricing power — demonstrated by consistent annual price increases of two-point-five to three-point-five percent — provides a natural hedge against cost inflation.

Bear Case

The bear case begins with valuation. At roughly thirty-two to thirty-five times trailing earnings, Mettler-Toledo is priced for continued perfection. The stock carries a premium to virtually all industrial peers, and any sustained deceleration in growth or margin compression could lead to a meaningful re-rating. The aggressive share repurchase program, while accretive at lower valuations, becomes less compelling as the price-to-earnings multiple expands — buying back stock at thirty-five times earnings is a fundamentally different proposition than buying at fifteen times earnings.

Cyclical exposure is a genuine risk. While the service business provides some stability, the majority of revenue comes from instrument sales that are inherently tied to capital expenditure cycles. When pharmaceutical companies or industrial manufacturers defer capital spending — as happened during parts of 2024 and early 2025 — Mettler-Toledo's topline growth decelerates. The first quarter of 2025, with its three percent local currency decline, illustrated this vulnerability.

China, representing approximately sixteen percent of total sales, presents both opportunity and risk. The country's economic deceleration, real estate sector difficulties, and pharmaceutical sector softness contributed to flat or declining local currency sales through much of 2024 and 2025. While management has guided to low-single-digit growth in China for 2026, the trajectory remains uncertain and highly dependent on macroeconomic factors beyond the company's control.

The balance sheet warrants scrutiny. With negative shareholders' equity, two-point-one billion dollars in debt, and a policy of deploying nearly all free cash flow to buybacks rather than debt reduction, the company has limited financial flexibility. In a severe recession or credit market disruption, this leverage could constrain strategic options at precisely the moment when competitors' distress creates acquisition opportunities.

Tariff and trade policy risks are elevated. The company absorbed approximately fifty million dollars in incremental tariff costs in 2025 and has taken mitigation actions including manufacturing expansion in Mexico. However, an escalation of trade disputes — particularly between the United States and China — could create further margin pressure that is difficult to offset through pricing alone without risking competitive position.

There is also a subtler risk that deserves mention: the gradual improvement in quality from Asian competitors. Shimadzu, A&D Company, and a growing cohort of Chinese instrument manufacturers are slowly closing the technology gap in the mid-range segment. While they cannot yet match Mettler-Toledo's precision at the ultra-high end or replicate its regulatory compliance infrastructure, the lower and middle tiers of the market — university research labs, smaller industrial customers, and price-sensitive emerging market buyers — are increasingly contested. If these competitors continue to improve while maintaining their price advantage, Mettler-Toledo could face margin pressure in segments that have historically been comfortable.

Finally, the management transition from long-tenured predecessor Olivier Filliol to Patrick Kaltenbach, while smooth so far, represents an ongoing execution risk. The company's operating culture — the Spinnaker system, the pricing discipline, the capital allocation philosophy — was built under prior leadership. Maintaining that culture while also evolving the business to address new technological trends and competitive dynamics requires a balance that is easy to describe but difficult to execute.

Key KPIs for Investors to Track

Two metrics matter most for monitoring Mettler-Toledo's ongoing performance: local currency sales growth and adjusted operating margin. Local currency sales growth strips out the noise of currency fluctuations and reveals the underlying demand trajectory across end markets and geographies. Adjusted operating margin tracks the company's ability to maintain and expand its pricing and cost discipline, which is the fundamental driver of cash flow generation and per-share value creation. A sustained deterioration in either metric — below two percent local currency growth or below twenty-eight percent adjusted operating margin — would signal that the competitive advantages are eroding or that end-market headwinds are more structural than cyclical.

XII. Epilogue and Reflections

What would Allen DeVilbiss Jr. and Dr. Erhard Mettler think if they could see the company that bears their combined legacy? The Toledo inventor, working in his Ohio workshop in 1897, was trying to build a scale that grocers and their customers could trust. The Swiss engineer, starting his precision mechanics firm in 1945, was trying to give scientists a faster, more accurate way to weigh chemicals. Neither could have imagined that their innovations would converge into a four-billion-dollar global enterprise with thirty percent operating margins and a market capitalization approaching thirty billion dollars.

And yet, the core mission has not changed. Mettler-Toledo still does what DeVilbiss and Mettler set out to do: measure things accurately, document the results reliably, and give customers confidence that their measurements are trustworthy. The technology has evolved from pendulums and knife-edge balances to electromagnetic force restoration and digital data platforms, but the fundamental value proposition — precision you can trust — remains unchanged.

Perhaps the biggest surprise from researching this company is the sheer depth of its competitive position. Many investors classify Mettler-Toledo as a simple industrial company and move on. The reality is far more nuanced. The combination of regulatory lock-in, direct service relationships, geographic breadth, technological leadership, and razor-and-blade economics creates a competitive position that would take any new entrant decades and billions of dollars to replicate — and even then, without any guarantee of success. This is a business where the competitive advantages are invisible to casual observers but unmistakable to anyone who has tried to switch vendors in a GMP-regulated pharmaceutical facility.

For founders building businesses in what the world considers boring industries, Mettler-Toledo offers a powerful template. Do not apologize for the lack of glamour. Embrace it. Build products that become embedded in customers' regulated workflows. Invest relentlessly in service and support infrastructure. Acquire patiently and integrate carefully. Let compound interest do its work over decades.

Consider the timeline: from DeVilbiss's first patent in 1900 to the merger in 1989 to the IPO in 1997 to four billion dollars in revenue in 2025 — this is a story that unfolded over one hundred and twenty-five years. The most important decisions were often the ones that looked least exciting at the time: the 1971 acquisition of an obscure German scale maker, the 1987 purchase of a checkweigher manufacturer, the patient build-out of a direct service force in forty countries. None of these moves made headlines. All of them compounded.

There is a final irony worth savoring. In an age obsessed with disruption, with platforms, with network effects and winner-take-all dynamics, one of the greatest wealth creators of the past three decades has been a company that makes weighing scales. No algorithms. No virality. No two-sided marketplace. Just precision, trust, and the relentless accumulation of small advantages over a very long time. Henry Theobald's original promise — "No Springs — Honest Weight" — turned out to be more than a marketing slogan. It was a business philosophy. And the most enduring businesses are not the ones that capture headlines — they are the ones that capture measurement data, calibration records, and compliance documentation. In the end, the most honest weight is the weight of accumulated competitive advantage.

XIII. Recent News

Mettler-Toledo reported fourth quarter 2025 results on February 5, 2026, with reported sales of one-point-one-three billion dollars representing eight percent year-over-year growth. Local currency sales increased five percent, including a one percent contribution from acquisitions. Regional performance was balanced, with Americas up seven percent, Europe up four percent, and Asia and rest of the world up four percent in local currency. Adjusted EPS of thirteen dollars and thirty-six cents beat analyst expectations and rose eight percent over the prior year period.

For the full year 2025, the company crossed the four-billion-dollar revenue threshold for the first time, reaching four-point-zero-three billion dollars. Adjusted EPS for the full year was forty-two dollars and seventy-three cents, up four percent despite a fifty-million-dollar headwind from incremental tariff costs that compressed adjusted operating margins by approximately one hundred and thirty basis points.

Management provided 2026 guidance projecting approximately four percent local currency sales growth, adjusted EPS of forty-six dollars and five cents to forty-six dollars and seventy cents, and free cash flow of approximately nine hundred million dollars. CEO Patrick Kaltenbach noted that the guidance assumes current tariff levels remain in effect and no significant market recovery, describing the outlook as cautious given ongoing trade policy uncertainty.

The company completed its share repurchase program originally launched in 2010, having bought back nearly eighteen million shares for nine-point-five-one billion dollars over the life of the program. In the third quarter of 2025, the board authorized an additional two-point-seven-five billion dollars for future share repurchases, signaling continued commitment to aggressive capital returns.

On the tariff front, management reduced its estimated gross incremental tariff cost to sixty million dollars annually, down from an initial estimate of one hundred and fifteen million, reflecting mitigation actions including manufacturing expansion in Mexico and supply chain restructuring. Pricing benefits are expected to be approximately two-point-five percent in 2026, down from three-point-five percent in 2025.

The third quarter of 2025 had been a turning point in the year's trajectory. Revenue of roughly one-point-zero-three billion dollars represented eight percent reported growth and six percent local currency growth, with adjusted EPS of eleven dollars and fifteen cents rising nine percent year-over-year. The board used the strong third quarter results as the backdrop for authorizing an additional two-point-seven-five billion dollars in share repurchases, signaling confidence in the company's cash generation trajectory. CEO Kaltenbach highlighted "very good growth, especially in Industrial" during the quarter, and the process analytics business showed particular strength driven by biopharma trends.

The service business continued its momentum throughout 2025, growing six percent in local currency in the first quarter and maintaining mid-single-digit growth through the year. Having crossed the one-billion-dollar annual milestone, service revenue now represents a meaningful and growing share of the company's value proposition — higher margin, more predictable, and more resistant to the capital expenditure cycles that create volatility in instrument sales.

Looking at the competitive landscape, BofA Securities upgraded Mettler-Toledo to Buy with a sixteen hundred and forty dollar price target, citing strong execution and quality. Stifel maintained its Buy rating with a sixteen-hundred-dollar target. Analyst consensus as of early 2026 stands at a moderate buy with a mean target of roughly fifteen hundred and fourteen dollars, with the range spanning from twelve hundred dollars at the low end to seventeen hundred at the high end — reflecting the genuine uncertainty about whether the stock's premium valuation can be sustained in a period of moderate topline growth.

Michael J. Tokich, former senior vice president and CFO of STERIS with over seventeen years of service, joined the board of directors effective February 5, 2026 — an addition that brings relevant experience in high-quality industrial businesses with strong service revenue models.

XIV. Links and Resources

Company investor relations: investor.mt.com

Mettler-Toledo corporate website: mt.com

SEC filings (10-K, 10-Q, proxy): sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001037646

Historical source on Toledo Scale: "Honest Weight: The Story of Toledo Scale" — available through VII Capital Management and Victori Capital archives

Toledo's Attic exhibition on Toledo Scale: toledosattic.org

FundingUniverse company history: fundinguniverse.com/company-histories/mettler-toledo-international-inc-history/

Fisher Scientific historical article on laboratory balances: "A Weighty History" — fishersci.com publications

Encyclopedia.com company profile: encyclopedia.com — Mettler-Toledo International Inc.

Wikipedia: en.wikipedia.org/wiki/Mettler_Toledo

BizModelMastery analysis: "Inside Mettler-Toledo: How 24% of Sales from Recurring Services Anchor Its Global Compliance Moat"

MacroTrends financial data: macrotrends.net/stocks/charts/MTD

Seeking Alpha earnings transcripts: seekingalpha.com — Mettler-Toledo quarterly earnings call transcripts

StockTitan news aggregation: stocktitan.net/news/MTD

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube