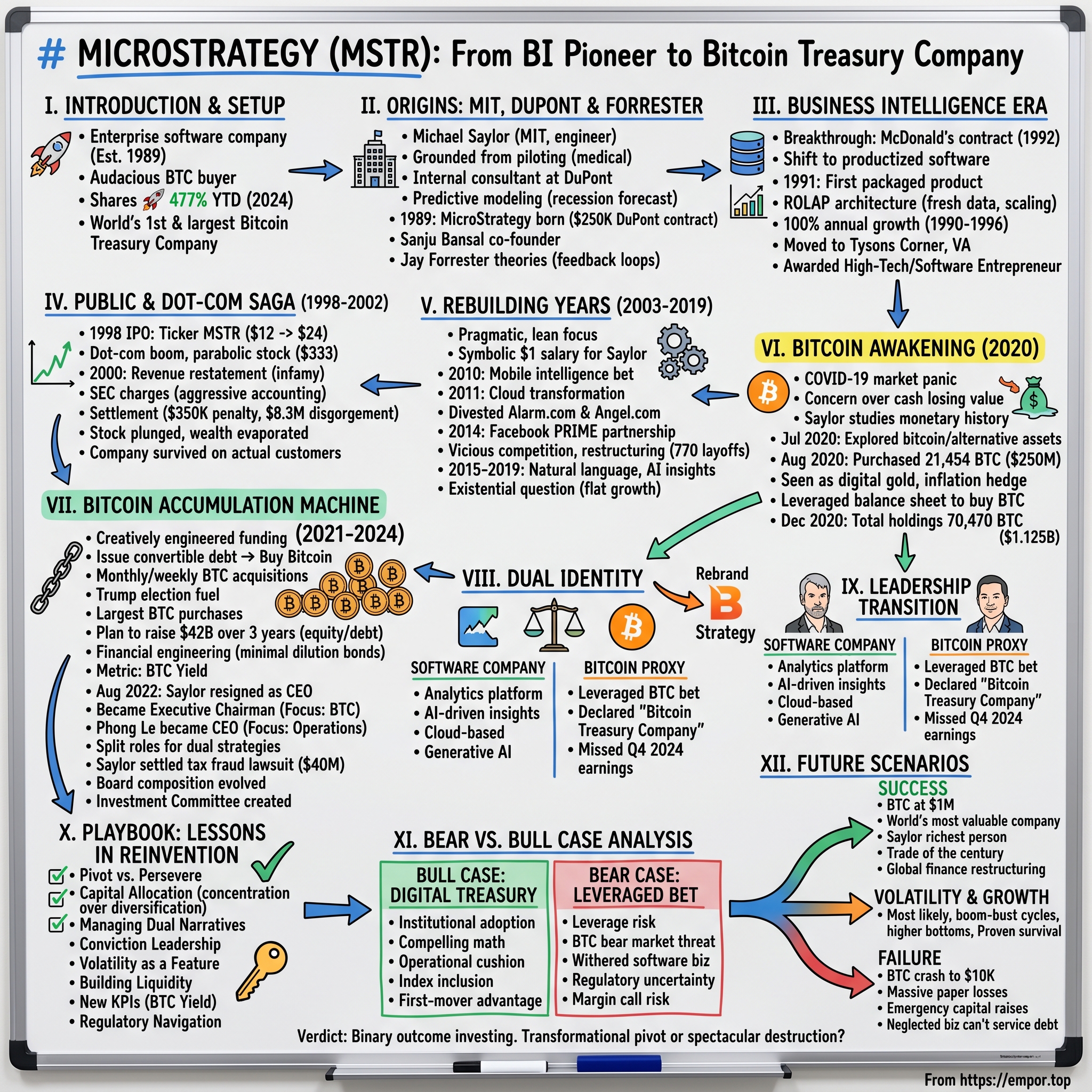

MicroStrategy (MSTR): From Business Intelligence Pioneer to Bitcoin Treasury Company

I. Introduction & Episode Setup

Picture this: A 35-year-old enterprise software company, founded when the Berlin Wall was still standing, becomes Wall Street's most audacious corporate Bitcoin buyer. By Friday's close, MicroStrategy's shares had rocketed 477% year-to-date—a performance that would make even the frothiest tech startup blush. Among U.S. tech companies valued above $5 billion, only AppLovin has delivered better returns in 2024.

The transformation defies conventional corporate playbooks. This is still technically a business intelligence software company, serving Fortune 500 clients with analytics platforms. Yet visit their website today, and you'll find the company proudly declaring itself the "world's first and largest Bitcoin Treasury Company." The duality is jarring—imagine if Microsoft suddenly announced it was primarily a gold vault that happened to make Windows on the side.

What you're about to read is the story of one of the boldest corporate pivots in modern business history. It's a tale that spans from MIT dorm rooms to DuPont's executive suites, from dot-com euphoria to SEC settlements, from mobile analytics to cryptocurrency evangelism. At its center stands Michael Saylor—aeronautical engineer turned software mogul turned Bitcoin maximalist—whose personal conviction has transformed a middling software firm into a $82 billion financial anomaly.

This is how a company built on helping corporations analyze data became the subject of Wall Street's most fascinating data point: What happens when you bet everything on Bitcoin?

II. Origins: MIT Fraternity Brothers & The DuPont Contract

The year was 1987, and Michael Saylor had a problem. The MIT graduate with dual degrees in aeronautical & astronautical engineering and history of science had dreamed of becoming a pilot. But a medical condition—benign heart murmur discovered during his physical—grounded those ambitions before they could take flight. Instead of soaring through clouds, Saylor found himself in the decidedly terrestrial world of consulting, joining The Federal Group, Inc., a systems integration firm.

Within a year, fate intervened through an unlikely channel: DuPont, the chemical giant wrestling with strategic planning in an increasingly volatile market. In 1988, Saylor became an internal consultant at DuPont's Wilmington headquarters, where he developed something revolutionary for its time—computer models that could anticipate market changes using nonlinear mathematics. His simulations delivered an uncomfortable prediction: a recession would hit DuPont's major markets by 1990.

The models proved prescient. More importantly, they convinced DuPont executives that this 24-year-old consultant was onto something transformative. When Saylor proposed spinning out to create a company focused on this predictive modeling approach, DuPont didn't just wave goodbye—they wrote a $250,000 check for a consulting contract and offered office space in Wilmington. It was 1989, and MicroStrategy was born.

Saylor needed a technical co-founder, someone who could translate mathematical theory into working code. Enter Sanju Bansal, his MIT fraternity brother from Theta Delta Chi, who shared Saylor's fascination with a systems-dynamics course they'd taken under Professor Jay Forrester. Forrester's theories about feedback loops and complex systems weren't just academic exercises—they became the intellectual foundation for what MicroStrategy would build.

The early vision was ambitious yet focused: create software for data mining and business intelligence using nonlinear mathematics. While competitors were building static reporting tools, Saylor and Bansal imagined dynamic systems that could model complex business scenarios. They weren't just organizing data; they were teaching it to predict the future.

Those first months in DuPont's Delaware offices were a blur of coding marathons and client presentations. The duo's approach—applying chaos theory and nonlinear dynamics to business problems—sounded either brilliant or insane, depending on who you asked. But with DuPont's imprimatur and that initial contract as proof of concept, they had something more valuable than venture capital: credibility with Fortune 500 decision-makers.

III. The Business Intelligence Era: Building a Software Empire (1990s)

The breakthrough came from an unexpected source: hamburgers. In 1992, McDonald's was drowning in data from thousands of franchises but had no way to measure which promotions actually moved the needle. They needed someone who could turn cash register receipts and inventory reports into strategic insights. MicroStrategy won a $10 million contract—massive for a three-year-old startup—to build custom analytics applications.

The McDonald's project was Saylor's road-to-Damascus moment. Standing in McDonald's headquarters, watching executives struggle with basic questions about promotional effectiveness, he realized the opportunity wasn't in custom consulting—it was in productized software. Every major corporation had the McDonald's problem: mountains of data, no meaningful insights. MicroStrategy would build the bridge between those two shores.

Their first packaged product, launched in 1991, was radically different from existing executive information systems. While competitors required IT departments to hard-code every report, MicroStrategy's platform let business users create their own graphical analyses without writing a line of code. It was democratization through design—putting analytical power directly in the hands of decision-makers.

The technical differentiation came through ROLAP (Relational Online Analytical Processing), a mouthful of an acronym that represented a fundamental architectural choice. While competitors pre-calculated and stored every possible data combination in proprietary cubes, MicroStrategy queried relational databases directly. This meant fresher data, more flexibility, and critically, the ability to scale without exponential storage costs. It was a bet that computing power would get cheaper faster than storage—a bet that paid off handsomely.

Revenue numbers told the story: 100% growth every year from 1990 to 1996. Not doubling every few years—doubling every single year for six straight years. The company was adding blue-chip clients at a stunning pace: Merck, Pfizer, NBC, even competitors like IBM. Each success story became marketing ammunition for the next sale.

By 1994, the company had outgrown Delaware. With 50 employees and ambitions to scale further, Saylor moved headquarters to Tysons Corner, Virginia—closer to government contracts and the growing Northern Virginia tech corridor. The new offices buzzed with MIT and Ivy League graduates, creating what employees described as "the most intense intellectual environment outside academia."

Recognition followed results. In 1996, KPMG named Saylor Washington's High-Tech Entrepreneur of the Year. Ernst & Young followed with Software Entrepreneur of the Year in 1997. Red Herring Magazine's 1998 list of top entrepreneurs featured Saylor prominently. The boy genius narrative was irresistible: MIT whiz kid builds better mousetrap, Fortune 500 beats path to door.

But beneath the accolades, Saylor was already thinking bigger. In interviews from this period, he spoke not just about business intelligence but about "information democracy"—a world where every person could access and analyze information like a Fortune 500 CEO. The ambition was breathtaking, borderline megalomaniacal. It was also perfectly timed for what was about to happen next.

IV. Going Public & The Dot-Com Saga (1998-2002)

June 11, 1998. The NASDAQ opening bell rings, and MicroStrategy begins trading under ticker symbol MSTR at $12 per share. By market close, the stock had doubled to $24. The 4 million share offering raised $48 million, but more importantly, it anointed MicroStrategy as a legitimate player in the enterprise software gold rush. Saylor retained 56% ownership—a stake that would soon make him one of America's youngest billionaires.

The timing was exquisite. The dot-com boom was approaching escape velocity, and anything touching the internet or data commanded astronomical valuations. MicroStrategy wasn't just riding the wave—it was providing the intelligence platforms that helped other companies navigate the digital transformation. Revenue hit $200 million in 1999. The stock price went parabolic, reaching $333 per share by March 2000.The math was staggering. By early 2000, Saylor's net worth reached $7 billion, and the Washingtonian reported that he was the wealthiest man in the Washington D.C. area. For a 35-year-old who'd started with a $250,000 consulting contract just eleven years earlier, it was the American Dream on steroids. Saylor owned 56% of a company valued at over $14 billion. He graced magazine covers, gave keynote speeches about the "intelligence revolution," and became the poster child for the new economy's promise that information, not industrial assets, would define wealth.

Then came March 20, 2000—a date that would live in MicroStrategy infamy. The company announced it would restate its financial results for the previous two years. The issue? Revenue recognition—specifically, MicroStrategy had been booking revenue from multi-year contracts upfront rather than spreading it over the contract period. MicroStrategy's stock price, which had soared from $7 per share to as high as $333 per share over the course of a year, plummeted 62%, dropping to $120 per share in a single day.

The SEC came calling. In March 2000, the U.S. Securities and Exchange Commission (SEC) brought charges against Saylor and two other MicroStrategy executives for the company's inaccurate reporting of financial results for the preceding two years. The investigation revealed that what MicroStrategy had reported as profits were actually losses. The company hadn't committed outright fraud—no fake customers or phantom revenue—but aggressive accounting had painted a fundamentally misleading picture.

In December 2000, Saylor settled with the SEC without admitting wrongdoing by paying $350,000 in penalties and a personal disgorgement of $8.3 million. As a result of the restatement of results, the company's stock declined in value and Saylor's net worth fell by $6 billion. From paper billionaire to cautionary tale in nine months—it was one of the most spectacular wealth destructions in corporate history.

The human toll extended beyond balance sheets. Employees who'd joined for stock options watched their paper wealth evaporate. Institutional investors who'd bought at the peak faced devastating losses. Class action lawsuits proliferated—approximately two dozen were filed in the Eastern District of Virginia. MicroStrategy ultimately settled with the SEC, agreeing to hire an independent director to ensure ongoing regulatory compliance.

What's remarkable, looking back, is that MicroStrategy survived at all. Many dot-com darlings simply disappeared—Pets.com, Webvan, Kozmo.com. But MicroStrategy had something its defunct peers lacked: actual enterprise customers paying real money for software that delivered measurable value. The business intelligence platform wasn't vaporware; it was mission-critical infrastructure for Fortune 500 companies. The accounting scandal was devastating, but the underlying business remained viable.

V. The Rebuilding Years: Mobile, Cloud & Modern BI (2003-2019)

The MicroStrategy that emerged from the dot-com wreckage was a different animal—humbler, leaner, focused on survival rather than revolution. The company retreated to its core competency: helping large organizations make sense of their data. No more talk of "information democracy" or changing the world. Just solid, enterprise-grade business intelligence software, sold one contract at a time.

The strategic decisions during this period revealed a pragmatic Saylor, willing to cut losses and focus resources. After his leadership was criticized by several major investors in 2014, Saylor has since opted for a symbolic one-dollar salary without any cash bonuses, but with stock options. The gesture was both practical—preserving cash for the business—and symbolic, aligning his interests entirely with shareholders.

The first major pivot came with mobile. In 2010, just as the iPad was launching and enterprise mobility was still a question mark, MicroStrategy bet big on mobile intelligence. The timing was prescient—within two years, every Fortune 500 CIO was scrambling to develop a mobile strategy. MicroStrategy Mobile didn't just port desktop reports to phones; it reimagined how executives could interact with data on the go, using native gestures and device capabilities.

Cloud transformation followed in 2011 with MicroStrategy Cloud. While competitors were still debating whether enterprises would trust cloud infrastructure with sensitive data, Saylor pushed forward. The cloud offering wasn't just about following trends—it fundamentally changed MicroStrategy's business model, enabling subscription revenue and lowering barriers to entry for smaller customers.

The company also cleaned house, literally. In February 2009, MicroStrategy sold Alarm.com—its home security subsidiary—to ABS Capital Partners for $27.7 million. Four years later, Angel.com, the cloud-based call center platform, went to Genesys for $110 million. These weren't fire sales but strategic divestitures, focusing the company on its core BI mission while generating cash to invest in product development. The partnership with Facebook in January 2014 represented a technical validation few could have predicted during the dark days of 2001. The company announced a new feature of the platform called PRIME (Parallel Relational In-Memory Engine), co-developed with Facebook. The social media giant had successfully built high-value applications with the technology, and now MicroStrategy was productizing it for enterprise customers. It was a far cry from being an accounting scandal poster child.

But 2014 also brought painful restructuring. In October 2014, the company announced plans to lay off 770 employees, a month after reducing Saylor's salary from $875,000 to $1 at his request. The layoffs—nearly 30% of the workforce—were brutal but necessary. The BI market had become viciously competitive, with giants like Oracle, SAP, and IBM offering bundled solutions that undercut pure-play vendors.

Through it all, MicroStrategy kept innovating. The 2015 release of MicroStrategy 10 introduced natural language querying. MicroStrategy 11 in 2018 brought AI-powered insights. By 2019, the platform could automatically generate narratives explaining data patterns—turning numbers into stories that C-suite executives could actually understand.

Yet by the end of the decade, MicroStrategy faced an existential question. Revenue had plateaued around $500 million annually. The stock price languished in the $100-150 range—respectable but uninspiring. Newer competitors like Tableau (acquired by Salesforce for $15.7 billion) and Looker (bought by Google for $2.6 billion) commanded premium valuations while MicroStrategy remained stuck in value territory.

The company had survived its near-death experience and rebuilt itself into a profitable, stable enterprise software provider. But stable wasn't exciting. Profitable wasn't transformative. As 2020 approached, MicroStrategy looked like a company that had peaked—still relevant but no longer revolutionary. Nobody could have predicted what would happen next.

VI. The Bitcoin Awakening: Treasury Strategy Revolution (2020)

The world was falling apart, and Michael Saylor was reading. March 2020: COVID-19 had shuttered offices globally, the Federal Reserve was printing money at unprecedented rates, and MicroStrategy's conference rooms sat empty. While other CEOs scrambled to manage remote workforces and preserve cash, Saylor found himself consumed by a different concern: the $500 million sitting in MicroStrategy's bank accounts was melting.

Not literally, of course. But with interest rates at zero and inflation expectations rising, that cash was guaranteed to lose purchasing power. The traditional corporate playbook—park excess capital in treasuries and money markets—suddenly looked like accepting a slow-motion mugging. On MicroStrategy's quarterly earnings conference call in July 2020, Saylor announced his intention for MicroStrategy to explore purchasing bitcoin, gold, or other alternative assets instead of holding cash.

The intellectual journey that led Saylor to Bitcoin reads like a philosophy student's fever dream. He devoured "The Bitcoin Standard" by Saifedean Ammous, engaged in Twitter debates with cryptocurrency advocates, and spent hundreds of hours studying monetary history. The man who'd built his career on helping companies analyze data had found the ultimate dataset: an immutable, decentralized ledger that couldn't be manipulated by governments or corporations.

The following month, MicroStrategy used $250 million from its cash stockpile to purchase 21,454 bitcoins. The initial rationale was deceptively simple: if cash was trash, Bitcoin was digital gold—a superior store of value for the digital age. But Saylor's ambitions went far beyond treasury management. He saw Bitcoin not just as an inflation hedge but as a fundamental reshaping of how corporations could create value.

The board dynamics during this period must have been fascinating. Here was a CEO who'd already led the company through one spectacular boom and bust, now proposing to bet half the company's cash reserves on a volatile digital asset that most directors probably couldn't explain to their spouses. Yet Saylor's conviction was infectious—or perhaps the board remembered that playing it safe in 2000 wouldn't have prevented the accounting crisis.

Wall Street's initial reaction ranged from bewilderment to horror. Sell-side analysts struggled to model a software company that was morphing into a cryptocurrency investment vehicle. Some institutional investors dumped their shares immediately, viewing the Bitcoin purchase as reckless gambling. Others saw it differently—here was a publicly traded company offering leveraged exposure to Bitcoin without the complexity of custody or the regulatory uncertainty of crypto exchanges.

The infrastructure for this transformation wasn't trivial. MicroStrategy created MacroStrategy LLC, a subsidiary specifically designed to hold Bitcoin, allowing for cleaner accounting and potential future flexibility. They established relationships with cryptocurrency exchanges, implemented security protocols that would make Fort Knox jealous, and developed frameworks for ongoing purchases.

By September 2020, MicroStrategy had added $175 million of bitcoin to its holdings, followed by another $50 million in early December 2020. Then came the game-changer: On December 11, 2020, MicroStrategy announced that it had sold $650 million in convertible senior notes, taking on debt to increase its Bitcoin holdings to over $1 billion worth.

This wasn't just buying Bitcoin with excess cash anymore—this was using the company's balance sheet as a lever to accumulate the world's first cryptocurrency. On December 21, 2020, MicroStrategy announced their total holdings include 70,470 bitcoins purchased for $1.125 billion at an average price of $15,964 per bitcoin.

What started as a treasury strategy had become something unprecedented in corporate history: a complete reimagining of what a public company could be.

VII. Doubling Down: The Bitcoin Accumulation Machine (2021-2024)

If 2020 was the awakening, 2021-2024 was the full-throated roar. MicroStrategy evolved from a company that happened to own Bitcoin into a sophisticated financial engineering operation designed to accumulate as much of the cryptocurrency as possible. The playbook became increasingly creative: issue convertible debt at near-zero interest rates, use the proceeds to buy Bitcoin, watch the stock price rise as Bitcoin appreciates, rinse and repeat.

The numbers became astronomical. Of the 439,000 bitcoins the company owns, more than one-third have been purchased since Trump's election victory last month. The acceleration was breathtaking—what started as quarterly purchases became monthly, then weekly announcements of billion-dollar Bitcoin acquisitions.

The Trump election in November 2024 acted as rocket fuel. "With the red sweep, bitcoin is surging up with tail winds, and the rest of the digital assets will also begin to surge," Saylor told CNBC. "Taxes are coming down. All the rhetoric about unrealized capital gains taxes and wealth taxes is off the table. All of the hostility from the regulators to banks touching bitcoin" also goes away.

MicroStrategy Inc. bought about 27,200 Bitcoin for around $2.03 billion between Oct. 31 and Nov. 10, the largest purchase by the crypto hedge-fund proxy since just after it began acquiring the digital-asset more than four years ago. It's the largest amount of tokens purchased since the firm announced in December 2020 that it snapped up 29,646 Bitcoin.

A week before the election, MicroStrategy had announced its most audacious plan yet: raising $42 billion over three years through a combination of $21 billion in equity offerings and $21 billion in debt. The scale was unprecedented—no corporation had ever attempted to raise this much capital specifically to buy a volatile digital asset.

The financial engineering became increasingly sophisticated. MicroStrategy's convertible notes were structured with minimal dilution if Bitcoin performed well—essentially giving bondholders exposure to Bitcoin's upside while MicroStrategy retained most of the appreciation. The company introduced "BTC Yield" as a key performance metric, measuring how much Bitcoin per share increased over time. Traditional software metrics became afterthoughts in earnings calls.

By December 2024, MicroStrategy had become the world's fourth-largest Bitcoin holder, behind only the mysterious Satoshi Nakamoto, BlackRock's iShares Bitcoin Trust, and crypto exchange Binance. The company owned approximately 439,000 bitcoins worth about $42 billion—a stockpile larger than the reserves of most nation-states.

The transformation was complete: MicroStrategy had become what Saylor himself described as a "Bitcoin Treasury Company"—essentially a leveraged bet on the future of cryptocurrency wrapped in the legal structure of a public corporation.

VIII. The Dual Identity: Software Company or Bitcoin Proxy?

The February 2025 rebrand to "Strategy" wasn't just a name change—it was a declaration of identity. The new logo, featuring a stylized "B" and an orange primary color, symbolizes energy, intelligence, and integration with the Bitcoin ecosystem. After 35 years as MicroStrategy, the company had shed its old skin entirely.

"Strategy is one of the most powerful and positive words in the human language," Saylor explained. "It also represents a simplification of our company name to its most important, strategic core." The Antoine de Saint-Exupéry quote he invoked—"Perfection is achieved, not when there is nothing more to add, but when there is nothing left to take away"—captured the essence of the transformation.

Yet beneath the Bitcoin branding, a software business still operates. Despite this strong focus on Bitcoin, Strategy continues to invest in enhancing its analytics platform, with a focus on AI-driven insights and cloud-based solutions, embracing what it calls the "third generation of business intelligence powered by generative AI." The company serves thousands of enterprise customers who rely on its platforms for data visualization, predictive analytics, and decision support.

The duality creates fascinating contradictions. Earnings calls begin with software metrics—subscription revenue, customer retention rates, platform adoption—before pivoting to Bitcoin holdings and BTC Yield calculations. The company maintains two distinct investor bases: traditional software investors who value recurring revenue and profit margins, and crypto enthusiasts who see MSTR as leveraged Bitcoin exposure with a software kicker.

The strategy, along with the surge in the value of Bitcoin, has helped MicroStrategy to outperform every major US stock, including AI bellwether Nvidia Corp., since the middle of 2020. MicroStrategy's stock has risen more than 2,500% since August 2020. Bitcoin is up around 660% during the same period.

This outperformance has sparked debate about index inclusion. Should a company that derives most of its market value from Bitcoin holdings be included in technology indices? The Nasdaq-100 inclusion represents validation but also raises questions about classification. Is Strategy a software company, a financial services firm, or something entirely new?

Regulatory considerations add another layer of complexity. The SEC hasn't challenged Strategy's Bitcoin strategy directly, but the company operates in uncharted territory. No precedent exists for a public company using shareholder capital and debt markets to accumulate this much cryptocurrency. Every quarterly filing becomes a potential test case for accounting treatment and disclosure requirements.

The missed earnings in Q4 2024—an EPS of -3.2 versus analysts' -0.12 forecast—highlighted the tension. Software revenues slumped 3% year-over-year to $120.7 million, yet the stock barely budged because investors cared more about the 74.3% Bitcoin Yield than traditional operating metrics.

IX. Leadership Transition & Corporate Governance

The August 2022 leadership transition was orchestrated with surgical precision. Saylor resigned as CEO effective August 8, 2022, passing the operational baton to Phong Le while retaining the Executive Chairman title. In a press release announcing the transition, Saylor said that he would focus on the company's bitcoin acquisition strategy and that Phong would manage overall corporate operations.

"I believe that splitting the roles of Chairman and CEO will enable us to better pursue our two corporate strategies of acquiring and holding bitcoin and growing our enterprise analytics software business," Saylor explained. The subtext was clear: the company had become too complex for one person to manage both a software business and a cryptocurrency treasury operation.

Phong Le brought different credentials to the CEO role. Le began his career at Deloitte, then worked for NII Holdings and XO Communications before joining MicroStrategy as its CFO in 2015. He became President and CFO in 2020, then CEO in 2022. His background—Johns Hopkins undergraduate, MIT Sloan MBA, telecommunications CFO—suggested someone who could manage operations while Saylor focused on Bitcoin evangelism.

The division of labor made strategic sense. Le could handle earnings calls with software analysts, discuss subscription metrics, and manage product roadmaps. Meanwhile, Saylor became Bitcoin's most prominent corporate advocate, appearing on podcasts, speaking at conferences, and engaging in Twitter debates about monetary policy. The arrangement allowed each leader to play to their strengths.

But controversy followed Saylor even in his new role. In August 2022, the Attorney General for the District of Columbia sued Saylor for tax fraud, accusing him of illegally avoiding more than $25 million in D.C. taxes by pretending to be a resident of other jurisdictions. MicroStrategy was accused of collaborating with Saylor to facilitate his tax evasion. The lawsuit alleged Saylor had lived in D.C. since 2012 but claimed residency in Florida to avoid district taxes.

In June 2024, Saylor and MicroStrategy reached a $40 million settlement agreement with the District of Columbia. While neither admitted wrongdoing, the settlement was substantial—one of the largest tax fraud recoveries in D.C. history. The controversy highlighted the scrutiny that comes with Saylor's high profile and the company's unconventional strategy.

Board composition evolved to reflect the company's dual nature. Independent directors with software expertise balanced those with financial markets knowledge. The creation of an Investment Committee, chaired by Saylor, formalized Bitcoin acquisition decisions. Governance structures that would seem bizarre for a traditional software company—daily Bitcoin price monitoring, custody protocols, leverage ratios—became standard operating procedure.

The patent portfolio remained substantial but increasingly disconnected from the company's market valuation. Strategy holds hundreds of patents related to business intelligence, data visualization, and analytics. Yet these intellectual property assets, once core to the company's value proposition, became footnotes in a story dominated by Bitcoin holdings.

X. Playbook: Lessons in Corporate Transformation

The MicroStrategy transformation offers a masterclass in corporate reinvention—or recklessness, depending on your perspective. The playbook challenges every assumption about prudent corporate management while demonstrating the power of conviction in uncertain times.

When to Pivot vs. When to Persevere: The 2020 Bitcoin pivot came after years of perseverance in the BI market had yielded stability but not growth. The lesson isn't that every stagnant company should buy Bitcoin—it's that transformative moves require both desperation and opportunity. MicroStrategy had the desperation (flat growth, commoditizing market) and spotted the opportunity (institutional Bitcoin adoption) before competitors.

Capital Allocation in the Digital Age: Traditional capital allocation theory assumes diversification reduces risk. MicroStrategy inverted this, arguing that concentration in the world's hardest monetary asset was less risky than diversification across depreciating fiat instruments. The approach only works if you're right about the asset—but being conventionally wrong loses less than being unconventionally right wins.

Managing Dual Narratives: Strategy maintains two completely different investor communications strategies. Software metrics for traditional investors, Bitcoin metrics for crypto enthusiasts. Earnings calls that discuss both subscription revenue and BTC Yield. The company doesn't try to force a unified narrative but lets each constituency hear what they need.

The Power of Conviction Leadership: Saylor's unwavering Bitcoin advocacy—bordering on religious fervor—became the company's greatest marketing asset. In an attention economy, moderate positions get ignored. Extreme conviction, articulated intelligently, creates its own gravitational field. Employees either bought in completely or left; there was no middle ground.

Volatility as a Feature, Not a Bug: Traditional corporations minimize volatility to reduce cost of capital. MicroStrategy embraced it, understanding that volatility creates opportunities for financial engineering. Convertible bonds priced during Bitcoin drawdowns, equity raises during rallies—volatility became a tool for value creation rather than destruction.

Building Liquidity Through Financial Engineering: The progression from using cash, to debt, to equity dilution for Bitcoin purchases revealed sophisticated thinking about liquidity creation. Each financing method was optimized for market conditions. When Bitcoin was cheap, use debt. When the stock premium to NAV expanded, issue equity. The company became a machine for converting traditional capital markets liquidity into Bitcoin.

Creating New KPIs for New Strategies: BTC Yield—the year-over-year percentage increase in Bitcoin per share—became Strategy's north star metric. Traditional software metrics became supporting actors. The company didn't try to force Bitcoin strategy into traditional frameworks but created new ones. When you're doing something unprecedented, you need unprecedented metrics.

Regulatory Navigation: Strategy operated in regulatory grey zones without crossing red lines. They structured Bitcoin holdings through subsidiaries for flexibility. They maintained transparent disclosure while avoiding classification as an investment company. They engaged with regulators proactively rather than reactively. The lesson: when pioneering, stay just inside the boundaries while those boundaries are still being drawn.

The playbook's most radical insight might be its redefinition of corporate purpose. Most companies exist to provide products or services. Strategy exists to accumulate an asset. It's closer to a colonial-era trading company or a sovereign wealth fund than a traditional corporation. The software business provides cover and cash flow, but Bitcoin accumulation is the mission.

XI. Bear vs. Bull Case Analysis

Bull Case: The Digital Treasury Revolution

The bulls see Strategy as the vanguard of a corporate treasury revolution. As the largest corporate Bitcoin holder with first-mover advantage, they've built an unassailable position in the institutional adoption race. The math is compelling: if Bitcoin reaches the market cap of gold (~$15 trillion), Strategy's holdings alone would be worth over $300 billion. The company has proven its ability to raise capital in any market condition—$42 billion targeted over three years—and execute its accumulation strategy with precision.

The software business, while overshadowed, provides an operational cushion that pure Bitcoin investment vehicles lack. This isn't just a closed-end fund; it's an operating company with $500 million in recurring revenue that happens to hold Bitcoin. This structure provides flexibility that ETFs can't match—the ability to use operating cash flow, debt, and equity markets opportunistically.

Institutional Bitcoin adoption is accelerating, and Strategy offers the easiest way for traditional investors to gain exposure. The stock's inclusion in indices like the Nasdaq-100 forces passive funds to buy, creating structural demand. As more corporations follow Strategy's playbook, the company's first-mover advantage compounds—they bought at $15,000 while followers buy at $100,000.

The track record speaks for itself: the stock has risen more than 2,500% since August 2020, outperforming every major tech stock including Nvidia. Management has navigated Bitcoin's 80% drawdowns without facing margin calls, proving their risk management capabilities.

Bear Case: Leveraged Bet on a Volatile Asset

The bears see a house of cards built on leverage and speculation. Strategy has transformed from a stable software company into a leveraged Bitcoin fund with extreme concentration risk. If Bitcoin enters a prolonged bear market—not impossible given its history of 80%+ drawdowns—the company faces existential threats.

The leverage is staggering. With $42 billion in planned capital raises against a current market cap of $82 billion, the company is essentially betting borrowed money on a volatile digital asset. Unlike 2022's drawdown, when they had minimal debt, the next Bitcoin winter could trigger margin calls or covenant breaches that force liquidation at the worst possible prices.

The core software business is withering from neglect. Revenue growth is flat to negative, innovation has stalled, and top talent has fled to companies actually focused on software. Once Bitcoin enthusiasm fades, investors might discover they own equity in a subscale BI vendor that would struggle to sell for $1 billion in a strategic acquisition.

Regulatory uncertainty looms large. The SEC could force Strategy to register as an investment company, fundamentally altering its structure. Tax authorities might challenge the company's Bitcoin accounting. Foreign jurisdictions could restrict institutional Bitcoin ownership. Any of these changes could crater the stock regardless of Bitcoin's price.

The margin call risk, while managed so far, remains real. Le stated in 2022 that margin calls would trigger around $21,000 Bitcoin. While they've added collateral since then, a severe enough drawdown combined with a credit market seizure could force liquidation. The company would survive, but equity holders could face massive dilution.

The Verdict

Both cases have merit because Strategy has created something genuinely unprecedented. It's neither a pure software company nor a pure Bitcoin fund but something entirely new—a corporate treasury company. The bull case requires believing both in Bitcoin's long-term appreciation and Strategy's ability to navigate volatility. The bear case simply requires Bitcoin to do what it's done multiple times before: crash 80% and stay down for years.

The asymmetry is striking: bulls are betting on a 10-100x return if Bitcoin achieves mainstream adoption, while bears see 90% downside if Bitcoin fails or Strategy's leverage backfires. There's no middle ground—this is binary outcome investing at its purest.

XII. Epilogue & Future Scenarios

What happens if Bitcoin hits $1 million? At that price, Strategy's 439,000 Bitcoin would be worth $439 billion—more than the current market cap of JPMorgan Chase. The company would likely become the most valuable corporation in the world, surpassing Apple and Saudi Aramco. Saylor would become the world's richest person. The vindication would be complete, transforming Strategy from a speculative oddity into the trade of the century.

But the implications go deeper. A million-dollar Bitcoin implies a fundamental restructuring of global finance. Central banks would hold Bitcoin reserves. Corporations would follow Strategy's playbook en masse. The company might evolve from accumulating Bitcoin to providing Bitcoin-based financial services—lending, custody, payment rails. The software business would become a rounding error, perhaps spun off entirely.

What if Bitcoin crashes to $10,000 and stays there? The paper losses would exceed $35 billion. Convertible bondholders would demand repayment in cash the company doesn't have. Equity would be massively diluted through emergency capital raises. The software business, neglected for years, couldn't generate enough cash to service debt. Bankruptcy wouldn't be impossible, though the Bitcoin holdings would likely retain enough value to satisfy creditors.

The more likely scenario is continued volatility with an upward bias. Bitcoin has always moved in boom-bust cycles, but each bust bottoms higher than the last. Strategy has proven it can survive 80% drawdowns. The question is whether it can survive success—at some point, the company becomes too large to accumulate meaningfully without moving markets.

The potential for copycats is real but limited. Strategy had first-mover advantage when Bitcoin was $10,000 and institutional infrastructure was nascent. Today's followers face $100,000 Bitcoin and established competition. More importantly, few CEOs have Saylor's conviction or job security to attempt such a transformation. The reputational risk of failure would end most corporate careers.

Strategy's role in Bitcoin evangelism extends beyond its balance sheet. Saylor has become Bitcoin's corporate ambassador, recently pitching Microsoft's board on adopting a Bitcoin treasury strategy. While Microsoft declined, the fact that a Fortune 10 company even considered it shows how far the conversation has moved. Every corporation that adopts Bitcoin validates Strategy's thesis and potentially drives Bitcoin prices higher—a reflexive loop that benefits the first mover most.

The emergence of "Bitcoin Treasury Companies" as an asset class seems inevitable. Just as REITs created a new category for real estate investment, BTCs might emerge for Bitcoin accumulation. Strategy would be the sector's ExxonMobil—the original that defined the category. Competition would validate the model while potentially reducing Strategy's premium to net asset value.

The ultimate judgment on Strategy's transformation won't come for years, perhaps decades. Revolutionary changes always look reckless in real-time and obvious in hindsight. The dot-com boom produced Amazon alongside Pets.com. The mortgage crisis produced fortunes for those who bet against conventional wisdom. Strategy has placed one of the largest asymmetric bets in corporate history.

What's certain is that Strategy has already achieved something remarkable: forcing the world to reconsider what a corporation can be. Not just a provider of goods and services, but an accumulator of monetary energy. Not just a business, but a bet on the future of money itself. Whether that bet pays off will determine whether Michael Saylor is remembered as a visionary or a cautionary tale.

The transformation from MicroStrategy to Strategy, from business intelligence to Bitcoin intelligence, represents either the greatest corporate pivot in history or the most spectacular destruction of a software company ever witnessed. Time, and Bitcoin's price, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube