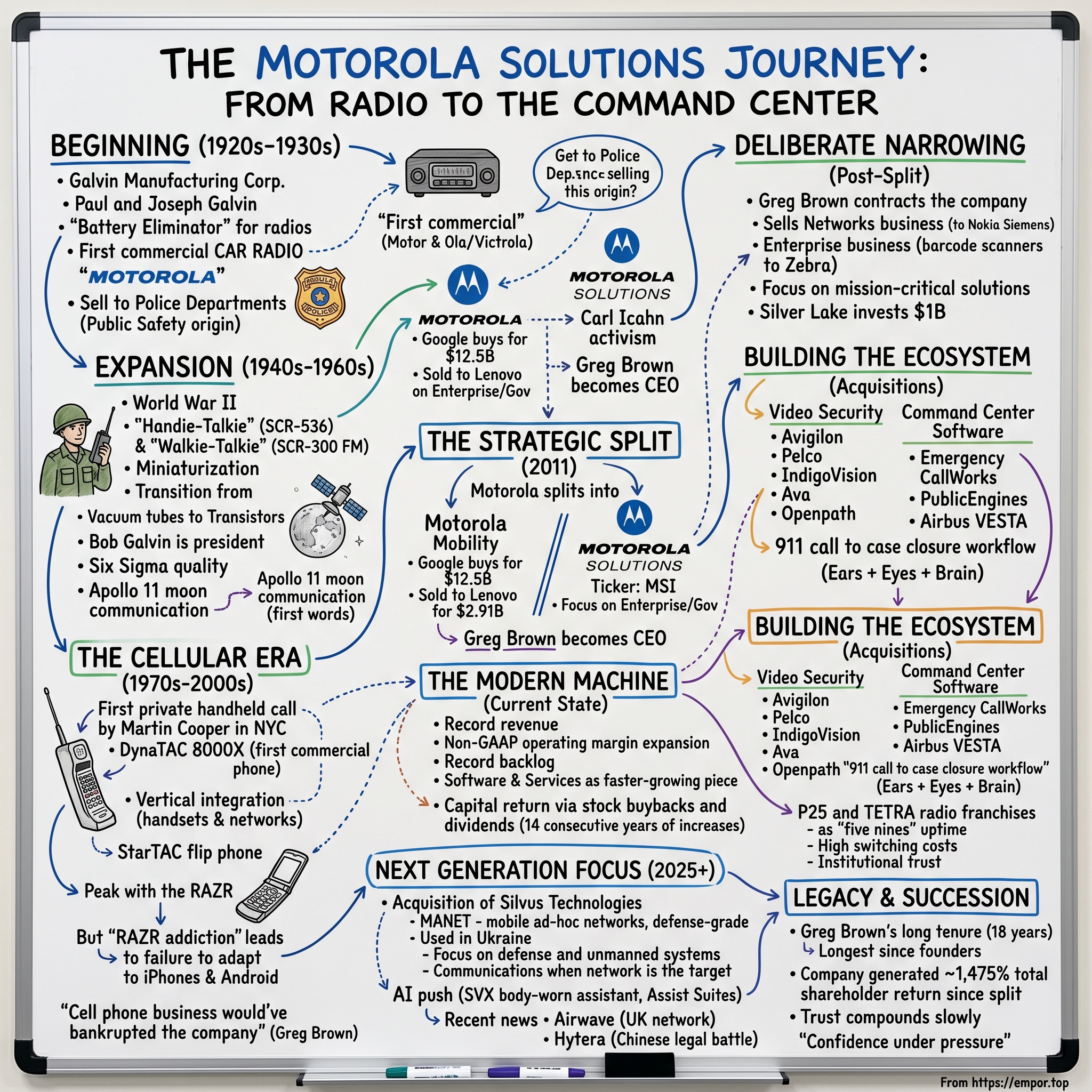

Motorola Solutions: The Company That Chose the Boring Side and Won

In January 2011, Motorola split itself in two. One half got the glamour: phones, brand cachet, celebrity ads, and the kind of media oxygen that consumer electronics always attracts. The other half got two-way radios, police dispatch consoles, and a CEO named Greg Brown who, outside the world of enterprise tech, barely registered.

Google bought the glamorous half for $12.5 billion. Two years later, it sold the handset business to Lenovo for $2.91 billion, keeping mostly the patents. That’s the entire lifecycle of glamour in one clean paragraph.

The “boring” half? Motorola Solutions, trading as MSI, turned into a compounding machine. Since the split, it has delivered total shareholder returns north of 1,475 percent, with the stock climbing from roughly $38 to more than $450. Along the way, it generated tens of billions in free cash flow, bought back more than half its shares outstanding, and raised its dividend at a double-digit clip for fourteen straight years. In fiscal 2025, it posted a record $11.7 billion in revenue, alongside record operating earnings, record cash flow, and a record backlog of $15.7 billion. By mid-February 2026, its market cap sat around $76 billion.

Nobody made a movie about that. Nobody’s greenlighting a prestige series about mission-critical radio infrastructure. There are no sweeping montages about the hard-won drama of non-GAAP operating margin moving from 27 to 30 percent.

But this is one of the most impressive corporate reinventions in modern American business. And it doesn’t start with the split. It starts almost a century earlier, with two brothers, a failed battery company, and $750 won at auction.

The Galvin Brothers Build a Brand

On September 25, 1928, Paul Vincent Galvin and his brother Joseph incorporated Galvin Manufacturing Corporation in Chicago. Paul was thirty-three years old, and he’d already been bankrupt twice.

His first swing was a storage-battery factory in Marshfield, Wisconsin, with a partner named Edward Stewart. It failed in the early 1920s. He tried again in Chicago in 1926, and that business failed too. But in the rubble of that second attempt, Galvin and Stewart had built something that actually worked: a “battery eliminator,” a device that let battery-powered radios plug into standard household AC power.

When the company went under, Paul didn’t walk away. He showed up at the bankruptcy auction and bought back the battery-eliminator business for $750.

That one purchase, made out of a failed company’s inventory, is the true origin story of what would eventually become a roughly $76 billion enterprise. Paul, Joseph, and five employees set up on half a floor of a Chicago warehouse and started building battery eliminators. Their first customer was Sears, Roebuck and Co.

Then Galvin made the move that defined the company’s instincts for decades: he bet on where America was going. The country was falling in love with the automobile, and he saw an opening that still felt slightly absurd in 1930—radios in cars.

In 1930, Galvin Manufacturing introduced its first commercial car radio. But it needed a name. Galvin combined “motor,” for motorcar, with “ola,” borrowed from Victrola, the record player brand Americans already associated with sound and entertainment.

Motorola. Sound in motion.

It wasn’t just a clever name; it sounded like a category. And Galvin marketed it like one. At the 1930 Radio Manufacturers Association convention in Atlantic City, he demonstrated the car radio by driving up with music blasting—pure showmanship aimed at dealers who thought car radios were impractical.

To be fair, they had reasons. Early car electrical systems threw off interference that could swallow radio signals. Driving vibrations shook components loose. Heat and cold punished delicate vacuum tubes. Galvin’s team worked through those constraints with 1930-era technology and produced something good enough to sell. And once you can sell a car radio, you can sell a car radio to anyone who lives in a car.

Including police.

Within months of launch, Galvin Manufacturing was selling Motorola car radios to police departments across Illinois—River Forest, Evanston, Cook County Police, the Illinois State Highway Police. In November 1930, law enforcement became some of the company’s earliest serious customers. By 1936, Motorola introduced the Police Cruiser: a rugged one-way radio receiver built to survive rough roads, tuned to a single customer-specified frequency, and housed in a heavy-duty metal case designed to take a beating in a patrol car.

It’s worth sitting with that. Motorola’s first institutional customers were law enforcement agencies. The company was barely out of infancy, and it was already building for public safety. Nearly a century later, Motorola Solutions’ largest customer category is still public safety. The line from Paul Galvin’s early police radios to Greg Brown’s $15.7 billion backlog isn’t metaphorical—it’s the business.

War, the Moon, and the Handheld Revolution

World War II didn’t just boost Motorola’s sales. It turned a fast-growing radio maker into a serious communications and electronics powerhouse.

In 1940, Motorola engineers developed the Handie-Talkie SCR-536, a handheld AM two-way radio that became one of the war’s signature pieces of gear. Three years later, a team led by engineer Daniel E. Noble—with principal RF engineer Henryk Magnuski, alongside Marion Bond, Lloyd Morris, and Bill Vogel—built something even more consequential: the SCR-300, the world’s first FM portable two-way radio.

Portable, in 1943, meant “on your back.” The SCR-300 was a thirty-five-pound backpack set with a range of roughly ten to twenty miles. The military called it a “walkie-talkie,” and it went where the war went: Anzio, Guadalcanal, Iwo Jima, Normandy. Commanders later called it the most useful communications radio in the Battle of the Bulge.

By the end of the war, Motorola had produced nearly 50,000 SCR-300 units and more than 40,000 Handie-Talkies. That wartime effort did more than create revenue. It deepened Motorola’s bench of engineering talent, pushed miniaturization forward, and—just as important—built durable relationships with military procurement offices that would matter for decades. And when millions of soldiers came home, many brought an ingrained familiarity with Motorola gear to the police departments, fire stations, and utilities where they built their postwar careers.

The whiplash came fast. Annual sales reached $68 million by 1945, then plunged to $23 million in 1946 when military contracts vanished—a sixty-six percent drop in a single year. It was a near-death experience, and it drove home a lesson that would keep resurfacing in Motorola’s story: any company that lives on one revenue stream is one cancelled contract away from crisis.

Paul Galvin’s response was to widen the tent. In 1947, the company formally changed its name to Motorola, Inc. and moved into televisions with Golden View sets. The VT71 table model sold more than 100,000 units in its first year. In 1953, Motorola established the Motorola Foundation to support STEM education—an unusually early commitment to science and engineering philanthropy. In 1955, it introduced its iconic “M” logo, designed by Chicago designer Morton Goldsholl: two upward peaks forming an abstracted M.

That same year, Motorola shipped the world’s first commercial high-power germanium transistor for car radios—its first mass-produced semiconductor and the start of a decades-long presence at the cutting edge of chips. The leap matters because of what transistors replaced. Vacuum tubes were fragile glass bulbs that ran hot, drank power, and failed regularly. Transistors did the same job smaller, tougher, cooler, and with dramatically longer life. Once that shift happened, the future of electronics became a race toward smaller, cheaper, more reliable—and more ubiquitous.

In 1956, Paul’s son Robert—Bob—became president. When Paul died in November 1959, Bob took over a company that was already growing past “radio manufacturer” into something more like a full-spectrum technology outfit.

Under Bob Galvin, Motorola became a semiconductor force. The MC68000 microprocessor family, introduced in 1979, later powered the original Apple Macintosh, the Commodore Amiga, the Atari ST, and workstations from Sun Microsystems and Hewlett-Packard. Bob also championed Six Sigma, a quality methodology built around driving defects down to fewer than 3.4 per million opportunities. It started at Motorola and then spread across industry. At its core was a belief that quality wasn’t a slogan—it was a duty, especially when your products might sit on a police officer’s belt or inside a dispatcher’s console.

By the 1960s, Motorola wasn’t just selling radios. It was building semiconductors and communications infrastructure—capabilities that converged in spectacular fashion on July 20, 1969, when NASA relied on Motorola equipment to help carry the first words from the moon back to Earth.

The breadth of Motorola’s Apollo 11 contribution is almost hard to process. The company supplied S-band transponders aboard both the lunar module and the command module, transmitting telemetry, voice communications, biomedical data, and television signals across the Earth-moon distance. It built a specially developed backpack antenna worn by Neil Armstrong. It supplied equipment used to process TV signals on Earth, range safety equipment on all three stages of the Saturn V rocket, and precision tracking systems for the launch phase. The S-band radio in the command module communicated from the vicinity of the moon on just thirty-five watts—less power than a refrigerator lightbulb. Motorola also delivered thousands of semiconductor devices, ground-based tracking equipment, and twelve onboard tracking and communications units.

When Neil Armstrong said, “That’s one small step for man, one giant leap for mankind,” the world heard it through Motorola technology. And for every government agency, military branch, and enterprise customer watching, the implication was clear: Motorola builds for the moments when failure is not an option.

Inventing the Cellular Phone

What Motorola did next didn’t just win a market. It rewired daily life.

Between 1968 and 1983, Motorola poured more than $100 million into cellular R&D. The breakthrough moment came on April 3, 1973, on Sixth Avenue in Manhattan. Martin Cooper, a Motorola engineer and general manager in its systems division, held a prototype handset and made the first private handheld mobile phone call. And because engineers are, at heart, competitive creatures, he didn’t call a friend.

He called the competition.

On the other end was Joel Engel at Bell Labs. Cooper’s message wasn’t subtle: “Joel, I’m calling you from a cellular phone, a real handheld portable cellular phone.” It was a technical milestone wrapped in perfectly delivered trash talk. AT&T’s vision leaned toward car phones—devices bolted into vehicles. Motorola’s bet was that the future wasn’t “mobile” as in “in the car,” but “mobile” as in “on you.” Personal. Always within reach. That single product intuition would prove to be one of the most consequential of the twentieth century.

Of course, the first version was a beast. The prototype was huge, awkward, and nowhere near ready for normal people. It took another decade to turn the idea into something you could actually buy. On September 21, 1983, the FCC approved the DynaTAC 8000X, the first commercial handheld cellular phone. It weighed two and a half pounds, offered about thirty minutes of talk time on a ten-hour charge, and carried a $3,995 price tag—roughly $12,000 today. It finally reached consumers in April 1984.

For a device that cost as much as a used car and ran out of juice almost immediately, it became a cultural signal. The DynaTAC showed up in movies, on the belts of traders, and in the hands of anyone who wanted to broadcast that they were living in the future. Motorola didn’t just invent the cell phone. It helped invent the modern expectation that you should be reachable anywhere, anytime.

Then came the refinement. In 1996, Motorola introduced the StarTAC: a tiny, 3.1-ounce clamshell that felt like it arrived from the next decade. It was among the lightest phones ever made at the time, and its flip design previewed the sleek, pocketable devices consumers would later demand. Through the 1980s and 1990s, Motorola was a defining force in cellular.

And the most important part is that Motorola wasn’t only selling the handset. It was building the rest of the stack too: base stations, switching equipment, the network backbone. That vertical integration helped make Motorola a dominant force in global cellular communications for nearly two decades. By 1998, cell phones represented roughly two-thirds of Motorola’s gross revenue. Its chief rivals were Nokia in Finland and Ericsson in Sweden—and for a long stretch, Motorola led them both.

But inside the company, success was creating its own kind of strain. Motorola was trying to run two businesses with completely different operating rhythms under one roof. Consumer devices demanded relentless iteration, sharp design instincts, aggressive pricing, and product cycles measured in months. Enterprise and government customers demanded durability, long lifecycles measured in years—sometimes decades—deep customization, and the kind of reliability that, in the field, can be the difference between life and death. The cultures, talent profiles, and capital allocation behind those two worlds don’t just differ. They fight.

And then Motorola went for the biggest swing of all: Iridium.

In the late 1980s, Motorola conceived a satellite phone network designed to cover the entire planet using a constellation of sixty-six low-Earth-orbit satellites. The promise was intoxicating: a phone that would work anywhere—from the Sahara to the middle of the Pacific. Bob Galvin championed it, and his son Christopher, who became CEO in 1997, kept backing it even as terrestrial cellular networks spread faster than expected.

Iridium launched in late 1998. The handsets cost $3,000. Calls ran $7 per minute. The phones couldn’t be used inside buildings. The engineering was extraordinary. The market reality was brutal. Iridium attracted only about 10,000 subscribers and filed for bankruptcy in August 1999, ultimately representing roughly $5 billion in losses. The technology worked. The business case didn’t.

It was a hard lesson: being right about what’s possible is not the same as being right about what people will buy.

And it hinted at the deeper problem ahead. Vertical integration is a powerful weapon when the world moves at your speed. But in a market evolving as fast as mobile, that same organizational weight can turn into drag—the thing that makes you too slow to survive the next era.

The RAZR: Triumph, Addiction, and the Failure to Let Go

The Motorola RAZR V3, launched in November 2004, almost didn’t happen.

It started as a skunkworks effort led by engineer Roger Jellicoe and a small team working evenings and weekends, outside Motorola’s formal product development process. The official forecast called for 800,000 units. Inside the team, expectations were far lower. And early on, no carrier wanted it.

What they shipped didn’t win on specs. It won on desire.

At 13.9 millimeters thick, the RAZR was the thinnest clamshell phone anyone had seen. The keypad glowed via an electroluminescent panel cut from a single metal wafer. The body was aluminum. It had an external glass screen, the first time glass had been used as a structural component in a mobile phone. Under the hood, it wasn’t revolutionary. In your hand, it felt like the future.

The market responded accordingly. The RAZR stopped being “a phone” and became a cultural object. Paris Hilton posed with the hot pink version. David Beckham became the face of it. People didn’t just choose a RAZR; they wore it, the way they would later wear iPhones.

Motorola ultimately sold more than 130 million RAZRs worldwide, making it one of the best-selling phones ever. It was the top-selling phone in the U.S. in 2005, 2006, and 2007. It pushed Motorola back up to number two globally in handsets, behind Nokia. For a moment, the old Motorola swagger was back.

And then came the unforced error: Motorola couldn’t quit.

Instead of using the RAZR as the launchpad for the next leap, the company treated it as a franchise to harvest. Out came the incremental variations: V3i, V3x, Razr2. Each one was a little less special. And as competitors caught up, Motorola tried to keep the volume engine running by cutting prices—taking the RAZR from a roughly $500 statement piece to nearly free with a carrier contract. It was a market-share move that also hollowed out the margins that made the hit worth having in the first place.

That play only works if your next act is ready. Motorola’s wasn’t.

When Apple introduced the iPhone in January 2007, Motorola was still cycling feature phones. The iPhone wasn’t just a better handset. It reframed the product: a handheld computer with a real web browser, a multitouch interface, and a software platform that would eventually become the economic center of the entire industry. Android became the scramble button for everyone else. Samsung moved fast. HTC embraced it. Motorola, despite its history of inventing the category, was suddenly chasing.

By 2007, the handset division’s revenue had fallen thirty-eight percent year over year. Ed Zander—the former Sun Microsystems executive who oversaw both the RAZR peak and the years of drift that followed—resigned on November 30, 2007. Motorola eventually shipped the Android-powered Droid in 2009, and it landed well. But the market had already decided who the new leaders were. The window had narrowed, and Motorola was trying to climb through it after it had started closing.

As Greg Brown later told Fortune, “The cell phone business would’ve bankrupted the company.”

That’s the RAZR lesson, and it’s as harsh as it is common: the biggest enemy of innovation isn’t failure. It’s the seduction of the last win—so good you keep replaying it, long after the world has moved on.

The Corporate Divorce

By 2007, Motorola was two businesses trapped in one body, and they were slowly strangling each other.

On one side sat the consumer handset division: glamorous, famous, and bleeding—losing hundreds of millions of dollars per quarter as the post-RAZR hangover turned into a full-blown crisis. On the other was the enterprise and government communications business: quiet, profitable, largely invisible to the tech press, and increasingly furious that its cash flow kept propping up a consumer operation that couldn’t figure out what came after its last hit.

Wall Street couldn’t value the mashup. Depending on the quarter, analysts treated Motorola as either a handset story with some weird radio business attached, or a communications infrastructure company with an annoying phone problem. The stock stayed stuck. Investors who wanted the steady, sticky enterprise business didn’t want the volatility of a collapsing phone franchise. Investors who still believed in a mobile comeback didn’t care about two-way radios and dispatch consoles.

The valuation gap was glaring. The handset losses dragged down Motorola’s overall earnings and compressed its multiple, effectively masking what the enterprise and government business might be worth on its own. If you valued that side independently, you could easily get to a number far above what the market was implying inside the conglomerate. The sum of the parts was worth more than the whole—and everyone could see it.

Everyone, eventually, including Carl Icahn.

Icahn accumulated roughly a 6.3 percent stake, becoming Motorola’s second-largest shareholder, and went to war in 2007. He lost his first attempt to win board seats, then escalated. In 2008, he sued the company, demanding records related to the Mobile Devices business and corporate jet usage, and blasted the board in public letters. “The situation at Motorola is too serious for the board to remain a country club,” he wrote. In April 2008, he forced a compromise: two board seats for his nominees.

The person stuck in the middle of this was Gregory Q. Brown.

Brown wasn’t a handset guy. Born in 1960 in New Brunswick, New Jersey, he joined Motorola in 2003 after running Micromuse, a network management software company where he grew annual revenue from $28 million to more than $200 million. Before that, he’d spent nearly two decades across AT&T, Ameritech, and IBM. He was a B2B operator—someone who thought in retention rates, service contracts, and operational discipline, not celebrity endorsements and holiday launches.

Brown graduated from Rutgers with an economics degree and started his career at AT&T in 1982. And he understood something Wall Street largely missed at the time: the enterprise and government communications business wasn’t the boring side. It was the better side. Contracts lasted years—sometimes decades. Switching costs were enormous. Relationships were deep. And the reliability requirements created a competitive landscape that looked nothing like the knife fight of consumer smartphones.

In 2008, Brown became co-CEO, and then sole CEO—taking over a company burning cash, fighting activists, and watching its mobile franchise deteriorate in real time. Years later, Investor’s Business Daily recounted an anecdote that captured his approach. In 2014, frustrated by internal resistance, Brown gathered the leadership team, put the “hemorrhaging years” next to the improved results, and delivered the ultimatum: “I don’t think the problem is necessarily me. The problem could be more you. Here are the metrics we’re going to measure success by, and you either have to commit or quit. And you’ve got to do one of them today.”

He also framed the job with an unusual mix of intensity and mission: “I look at the environment, I look at the product portfolio, I look at the team, I look at the opportunity, including the strategic decisions of where we play and where we’re focused, and I’m as energized as I’ve ever been to do this. It is a privilege and an honor.”

On March 26, 2008—two days after Icahn filed his lawsuit—Brown announced the decision that would define the next era: Motorola would split into two publicly traded companies. The financial crisis delayed the timeline, pushing the original target out, but the direction was set.

On January 4, 2011, Motorola, Inc. effectively ended. In its place were two companies: Motorola Solutions, which kept the enterprise-oriented, mission-critical communications and public safety businesses; and Motorola Mobility, which took the consumer handsets and set-top boxes. Shareholders received one share of Motorola Mobility for every eight shares of the old Motorola, and the remaining Motorola Solutions shares then went through a one-for-seven reverse split.

Brown became chairman and CEO of Motorola Solutions. “With a purpose-driven brand and a strong balance sheet,” he said, “we are very well positioned for the future.”

Seven months later, Google announced it would acquire Motorola Mobility for $12.5 billion, largely for its patent portfolio. Icahn did well. Google kept most of the patents and sold the handset business to Lenovo in October 2014 for $2.91 billion. The consumer brand that once defined Motorola changed hands for less than a quarter of what Google had paid for the whole package.

Meanwhile, Brown finally had what every turnaround CEO wants: a clean canvas—and a very specific idea of what to paint.

At first, the market didn’t buy the vision. Motorola Solutions looked, to many investors, like the leftover half: radios, dispatch systems, and government contracts. Motorola Mobility had the brand heat, a seat at the Android table, and the romance of being a smartphone company. But reality has a way of sorting out romance from economics. The “exciting” half turned out to be a money pit. The “boring” half became a compounding machine—and the divergence between the two is one of the sharpest corporate strategy case studies of the past twenty years.

The Deliberate Narrowing

What Greg Brown did after the split was almost the opposite of what most CEOs do when they finally get their own company. Most expand. They diversify. They go hunting for “adjacent markets” and tell a story about optionality.

Brown went the other direction. He contracted—on purpose. He made Motorola Solutions smaller and sharper, selling off businesses that didn’t fit his core thesis, even when those businesses were real, profitable, and defensible.

The first cut came fast. In April 2011, Motorola Solutions sold its networks business—GSM, CDMA, WCDMA, WiMAX, and LTE products and services—to Nokia Siemens Networks for $975 million in cash. Roughly 6,900 employees went with it. The deal cleared after Motorola Solutions and Huawei settled a trade-secret dispute. And it’s not like Brown was dumping a broken asset. Telecom infrastructure was a solid business. It just wasn’t the business he wanted. Building carrier networks wasn’t mission-critical communications for first responders, and Brown wasn’t interested in running two strategies at once ever again.

Then, in October 2014, he made the move that really told you what Motorola Solutions was going to become. The company sold its Enterprise business to Zebra Technologies for $3.45 billion in an all-cash deal. This was the division that made barcode scanners, rugged mobile computers, and data-capture devices—the tools of warehouses, factory floors, and retail checkout lines. It generated about $2.5 billion in annual revenue and had around 4,500 employees.

A lot of CEOs would’ve looked at that and seen a dependable growth engine. Brown looked at it and saw distraction.

“This transaction will enable us to further sharpen our strategic focus on providing mission-critical solutions for our government and public safety customers,” he said at the time.

By the end of 2014, Motorola Solutions had been stripped down to a single, unapologetic identity: the company that keeps first responders and critical infrastructure connected when it matters most. Everything else was either sold or sidelined.

That kind of subtraction is rare. Corporate life usually rewards accumulation—more revenue, more headcount, more kingdoms. Brown did the opposite. And that focus didn’t just make the story cleaner for investors. It freed Motorola Solutions to start building something much bigger than radios: a platform that could live above the radio network, in the command center.

In August 2015, Silver Lake effectively stamped the strategy with institutional validation, investing $1 billion. Silver Lake bought convertible senior notes with an initial conversion price of $68.50 per share, and Egon Durban and Greg Mondre joined the board. Silver Lake called Motorola Solutions “an iconic company” and said it believed the company was “creating a new era in data-rich public safety communications.” Those notes were ultimately settled in early 2024, creating a one-time, non-cash accounting charge that temporarily pressured GAAP earnings—but didn’t change the underlying business.

While the divestitures made headlines, another shift was happening more quietly: Motorola Solutions was assembling command center software. In February 2015, it acquired Emergency CallWorks, a provider of next-generation 911 call-taking software. In April 2015, it acquired PublicEngines, a Utah-based crime analysis firm offering cloud-based analytics and predictive policing tools. And in March 2018, it bought Plant Holdings—the parent of Airbus DS Communications—for $237 million, adding the VESTA suite for 911 call handling.

Together, these pieces became the early foundation of what Motorola Solutions would call CommandCentral: software designed to connect the workflow from “911 call” to “case closure.”

But before any of that really lands, we need to define one phrase Motorola Solutions has built its entire modern identity around: mission-critical. Because once you understand what that means in practice, you understand why this company prints money.

Why the Boring Radio Is the Hardest Product to Displace

There’s a reason Motorola Solutions’ land mobile radio business throws off enormous margins and sees almost no churn. It isn’t because the radios are stylish, or because Motorola has genius marketing.

It’s because the radio can’t fail.

When a police officer hits push-to-talk on a P25 radio during an active shooter call, that transmission has to go through. Not most of the time. Not “pretty much always.” The expectation is 99.999 percent uptime—“five nines”—which works out to just a few minutes of downtime per year.

Now compare that to the cellular networks your iPhone uses. Consumer carriers typically design for something like 99.9 percent uptime. That sounds close until you translate it into lived reality: “three nines” allows hours of downtime per year. And in exactly the moments that matter most—storms, blackouts, mass casualty events—consumer networks are the ones most likely to buckle under load as everyone reaches for their phones at once.

Public safety radio systems are built for the opposite: no congestion, no dropped calls, no “try again.”

That requirement cascades into a very specific technical bar that cellular networks, by default, don’t clear. Push-to-talk call setup has to feel instant—hundreds of milliseconds, not seconds. Group calling has to function like a broadcast: one push, everyone hears it, immediately. Direct mode—radio to radio, with no network at all—has to exist for the day the towers are down or the infrastructure is compromised. Priority and preemption have to be real, not aspirational, so emergency traffic can cut the line no matter how busy the system gets. The infrastructure itself has to be hardened, with battery backup and generators, designed to survive floods, earthquakes, and all the boring physical realities of disasters. Encryption has to be end-to-end and trusted. And coverage has to reach the places first responders actually go: basements, tunnels, high-rises, and rural dead zones where consumer signal fades away.

Then come the switching costs—the kind that don’t show up in a product demo.

When a state or major city builds a P25 system, it’s not just buying radios. It’s building an operational nervous system: towers, base stations, dispatch consoles, thousands of handhelds, software, integration work, and the training that makes it all second nature. SOPs get written around the workflow. Neighboring jurisdictions sign interoperability agreements. Mutual aid plans assume the system behaves a certain way.

So “switching vendors” isn’t like swapping out laptops. It’s a high-risk project that touches every police officer, firefighter, and EMT in the jurisdiction. And the most dangerous part is the transition—because during the migration, you’re running two worlds at once, and any gap becomes a vulnerability.

From first planning meeting to final cutover, replacing a full P25 system can take five to ten years. And once it’s in, you’re typically looking at a relationship that lasts well over a decade after that—maintenance, upgrades, software, and eventually the next generation refresh. This is why government procurement cycles are such a brutal moat: even if a startup builds something brilliant, it can’t compress time, reduce risk, or wish away the operational reality of retraining an entire city’s first responders.

On paper, P25—APCO Project 25—is an open standard. Any manufacturer can build “compatible” equipment. In practice, Motorola’s installed base, decades of institutional relationships, and the sheer downside of getting this wrong have created a position that is incredibly hard to attack.

In Europe and much of the rest of the world, the equivalent standard is TETRA (developed by ETSI), used by emergency services across more than 130 countries. Motorola Solutions is a dominant player there as well.

In the U.S., the primary competitor is L3Harris Technologies. Internationally, the low-cost rival is Hytera Communications—a Chinese company that has been found liable for stealing Motorola’s trade secrets, a thread we’ll come back to.

Acquiring the Eyes: Avigilon and the Video Empire

With the company now tightly centered on mission-critical communications, Greg Brown made the next move. Not a return to sprawl, but a broader definition of what “mission-critical” could include. If the radio is the ear of public safety, the camera is the eye.

In March 2018, Motorola Solutions acquired Avigilon, a Vancouver-based video surveillance and analytics company, for about $1 billion, at CAD $27.00 per share.

Avigilon’s founder, Alexander Fernandes, didn’t follow the usual Silicon Valley script. He never went to university. He taught himself by grinding through academic textbooks and biographies of Bill Gates, Steve Jobs, and Alexander the Great. He did a short stint in the military but didn’t get the avionics specialty he wanted. He landed in Vancouver, trained as a technician, worked at local startups like Xillix Technologies and Creo, and repeatedly chose equity over higher pay. He described himself as “frugal to the extreme.”

Before Avigilon, Fernandes founded QImaging, a medical and industrial imaging company, and sold it for roughly twenty million Canadian dollars. He used that money to start Avigilon in 2004. The company grew from $5.2 million in its first full year of sales to $178.3 million by 2013. It went public in 2011, raising twenty-five million Canadian dollars in an IPO priced at $4.50 per share. By the time Motorola Solutions came calling, Avigilon had amassed more than 750 U.S. and international patents, manufactured in the U.S. and Canada, and built AI-powered “self-learning” video analytics designed to shift surveillance from reactive—reviewing footage after the fact—to proactive, issuing real-time alerts for things like perimeter breaches, abandoned objects, or persons of interest.

Fernandes retired after the deal closed, walking away with about 116 million Canadian dollars from his 4.3 million shares. James Henderson became president of the Avigilon unit.

Avigilon was the beachhead. What came next was a fast, deliberate buildout of a full video security platform. In January 2019, Motorola Solutions bought VaaS International Holdings for $445 million, adding license plate recognition and vehicle-location intelligence. In 2020 it added Pelco, a Fresno-based camera and video management software company formerly owned by Schneider Electric, for $110 million, and it also brought in IndigoVision, a Scottish end-to-end video security provider. In July 2021, it acquired Openpath Security for $297 million, adding cloud-based mobile access control for contactless entry and multi-factor authentication. In November 2021, it acquired Envysion for enterprise video analytics in quick-service restaurants and retail. In March 2022, it bought Ava Security for $388 million, adding cloud-native video security from London. It also acquired Calipsa for cloud-native AI video analytics, and Videotec for $22 million, an Italian maker of ruggedized cameras that were integrated into the Pelco brand.

In March 2023, Motorola Solutions pulled these pieces into a single brand architecture: the Avigilon Security Suite. Avigilon Alta became the cloud-native line, growing four times faster than the overall video business. Avigilon Unity became the on-premise line. By 2022, the Video Security and Access Control business had surpassed $1.5 billion in annual sales and kept growing, with video revenue up fourteen percent in Q4 2025 alone.

The strategic logic snaps into focus when you walk through a single incident. A 911 call comes in and hits a Motorola Solutions console. A Motorola Solutions radio connects the dispatcher to the responding officer. A Motorola Solutions body-worn camera records the interaction. Fixed cameras capture the scene. Evidence management stores the footage. Analytics help investigators reconstruct what happened.

That’s not a product lineup. It’s a system. And systems—the kind that sit inside a department’s daily workflow—are where switching costs get brutal, and where the business stops being “sell a device” and starts becoming “run the platform.”

Airwave: The Profitable Headache

Not every acquisition stays a clean win. Motorola Solutions’ purchase of Airwave Solutions in February 2016—about £700 million (roughly $1 billion) plus a deferred £64 million payment due in November 2018—is a perfect example of a deal that can look great on a spreadsheet and still turn into a reputational and regulatory grind.

Airwave is the mission-critical communications network used by every emergency service across Great Britain—police, fire, ambulance—plus roughly 300 other public service agencies. In total, more than 470 organizations and about 300,000 users depend on it. It runs on TETRA technology, covers about 99 percent of Great Britain’s landmass through more than 3,850 base sites, and it performs: the system has consistently exceeded its 99.86 percent availability target.

The ownership trail is a little labyrinthine, but it matters. BT built Airwave under a twenty-year Private Finance Initiative agreement signed in February 2000. Lancashire Constabulary was the first to go live in 2001. By 2005, it was fully rolled out nationwide, after more than £1.4 billion had been invested to build, expand, and develop the network. BT later sold it as part of divesting its mobile services to form O2. Airwave Solutions was then separated from O2 and sold to Macquarie Communications Infrastructure Group in 2007. Motorola Solutions bought it from Macquarie.

Then the story takes its sharp turn.

Just days before closing the Airwave acquisition, Motorola Solutions also won the UK Home Office’s Lot 2 contract for user services on the Emergency Services Network (ESN)—the LTE-based broadband system that was supposed to replace Airwave by 2019. In other words, Motorola was positioned to run the legacy network and help build the replacement at the same time. Later, the UK’s Competition and Markets Authority (CMA) raised the obvious concern: if Airwave prints money, doesn’t the operator have an incentive to slow-roll the replacement?

ESN became a case study in how badly large government tech programs can go. The original 2019 target date slipped—again and again. The Home Office ultimately extended the Airwave national shutdown target from December 2026 to December 2029, and even that date may move. Each delay meant another year of Airwave revenue.

In October 2021, the CMA opened a formal investigation. In April 2023, it published findings that were brutal for Motorola’s public narrative: it said Motorola had been earning “supernormal” profits from Airwave—about $200 million per year above competitive levels. It estimated “supernormal” profits of around $1.27 billion over 2020–2029, and said the UK’s costs for Airwave were roughly 250 percent above the European peer average for similar TETRA services. Airwave, the CMA noted, contributed about 21 percent of Motorola Solutions’ global pre-tax profits while accounting for only about 7 percent of global revenue.

In July 2023, the CMA imposed a charge control, cutting Airwave revenues by roughly $200 million annually—around a forty percent reduction—effective from August 2023 through 2029. Motorola fought it at every level. The Competition Appeal Tribunal dismissed the challenge in December 2023. Then, in a unanimous ruling on January 30, 2025, the Court of Appeal dismissed Motorola’s final appeal, effectively exhausting its legal options.

And the saga still isn’t fully over. In December 2024, Clare Spottiswoode CBE filed a class action at the Competition Appeal Tribunal on behalf of Airwave customers, seeking about $623 million in damages—$517 million in alleged overcharges plus $105 million in interest—for the 2020–2023 period. The UK Home Office is both the litigation funder and the largest class member. A certification hearing took place in September 2025, with the outcome still pending as of February 2026. The CMA is also scheduled to review the charge control in 2026.

Motorola initially challenged the Home Office’s extension in the UK High Court, but it discontinued the case in Q1 2025—effectively accepting the reduced rates as the price of continuing to operate the network.

The Airwave saga is the one real blemish on Greg Brown’s acquisition record. Operationally, the network performs. Financially, it still generates cash flow even after the rate cut. But politically, it’s radioactive: a watchdog accusing “supernormal profits” extracted from a captive public safety customer is the kind of story that doesn’t die quietly. The charge control has already been baked into guidance and backlog; the class action has not. The takeaway for investors isn’t that Motorola bought a bad asset—it’s that monopoly-like positions, even when lawfully acquired and genuinely mission-critical, come with a regulatory bill that can arrive years later, and it can be expensive.

The Modern Machine: What Motorola Solutions Looks Like Today

By fiscal 2025, Motorola Solutions ran a tight, two-segment business that sits across three core technology areas. Think of it less like a radio company and more like a public safety and enterprise security operating system—hardware at the edge, software in the middle, and long-term services that keep the whole thing running.

Products and Systems Integration brought in $7.3 billion, about 62 percent of revenue. This is the physical layer and the heavy lifting. It includes Mission Critical Networks: the infrastructure, radios (P25 and TETRA), broadband gear, and deployment and integration services. It also includes modern additions like MANET technology from the Silvus acquisition. And it includes Video Security and Access Control: fixed cameras, body-worn cameras, in-car video, license plate recognition, video management, and access control sold under brands like Avigilon, Pelco, and Openpath.

Software and Services delivered $4.4 billion, roughly 38 percent of revenue—and it was the faster-growing piece, up thirteen percent year over year. This is the sticky layer. It includes long-term support and managed services for land mobile radio networks, including Airwave in the UK, plus multi-year renewals across U.S. states. It also includes CommandCentral, Motorola’s command center software suite for 911 call-handling, computer-aided dispatch, records management, evidence management, and analytics. And it includes cloud-hosted video management through Avigilon Alta, plus remote monitoring through the recently acquired Blue Eye.

When Motorola reported full-year 2025 results on February 11, 2026, it looked like the flywheel was spinning at full speed.

Revenue reached $11.7 billion, up eight percent. Products and Systems Integration grew five percent to $7.3 billion. Software and Services grew thirteen percent to $4.4 billion. Gross margin hit $6.0 billion, or 51.7 percent of sales. Non-GAAP operating margin rose to 30.3 percent, expanding 130 basis points year over year. GAAP operating earnings were $3.0 billion. Non-GAAP earnings per share came in at $15.38, up eleven percent. GAAP earnings per share rose to $12.75, up thirty-eight percent, helped by the fact that the prior year included a one-time, non-cash charge tied to the Silver Lake convertible debt extinguishment. Operating cash flow set a record at $2.8 billion, up nineteen percent, and free cash flow was $2.6 billion.

The fourth quarter, in particular, showed real acceleration. Revenue of $3.38 billion grew twelve percent. Non-GAAP operating margin hit a record 32.1 percent, up 170 basis points from the prior year. Non-GAAP EPS of $4.59 cleared Wall Street’s $4.35 consensus. And orders jumped twenty-six percent year over year—an important tell, because it suggests demand was strengthening, not just coasting on backlog.

Motorola also beat consensus EPS in all four quarters of 2025. That kind of repeatable execution matters because it becomes its own asset: guidance gets trusted, the shareholder base gets more institutional, and the company earns the right to trade at a premium.

Greg Brown put it plainly: “Our outstanding 2025 performance demonstrates the resilience and strength of our business. We had record sales, earnings and cash flow. Our record backlog and strong demand gives us continued momentum for another excellent year.”

And the backlog is where you can see the future already sold. Ending backlog finished at $15.7 billion, up about $1 billion from the year before, driven by record orders. Software and Services backlog climbed thirteen percent to $11.9 billion. Products and Systems Integration backlog dipped modestly, largely because strong Mission Critical Networks shipments—especially in the first half of 2025—converted prior orders into revenue.

The quarter’s notable wins read like a map of where Motorola’s moat lives: a $201 million ten-year P25 services renewal for the State of Maryland; a $180 million P25 system expansion for the State of Tennessee; a $162 million P25 device and SVX body-worn assistant order for a U.S. federal customer; an $86 million command center order for an international customer; an $81 million TETRA system for North Africa; and a $61 million TETRA services order for the London Underground.

Maryland’s deal alone is the essence of the business model: a decade-long services renewal that effectively locks in a steady stream of high-margin revenue with minimal risk of vendor churn mid-contract. Multiply that dynamic across thousands of agencies and enterprises, and you start to see why Motorola Solutions doesn’t behave like most “tech”—it behaves like infrastructure.

That cash flow then gets recycled back to shareholders. In 2025, Motorola returned $1.9 billion: $1.2 billion in share repurchases (at an average price of $420 per share) and $728 million in dividends. Since the 2011 split, it has returned about $16.4 billion through buybacks, shrinking the share count by about half—from roughly 336 million shares to 167 million. And it has increased its dividend every year, at a double-digit rate, for fourteen straight years, most recently lifting the quarterly dividend to $1.21 per share.

Silvus: The Biggest Bet

The single most important strategic move of 2025 didn’t show up cleanly in any one quarter’s headline numbers. It was Motorola Solutions’ acquisition of Silvus Technologies—announced in May and closed on August 6, 2025—for $4.4 billion upfront, plus up to $600 million in performance-based earnouts through 2028. It was the biggest acquisition in Motorola Solutions’ history, and it signaled something important: after years of building out public safety and enterprise security, Greg Brown was now pushing the company deeper into defense-grade, next-generation communications.

Silvus, based in Los Angeles, builds mobile ad-hoc networks, or MANET. In plain terms: secure data, video, and voice communications that don’t need towers, base stations, or fixed infrastructure. Traditional land mobile radio systems rely on centralized networks. Silvus turns every radio into both a device and a node. The network forms on the fly, radios route traffic through the best available path, and the mesh keeps working even as people and vehicles move—or as parts of the network go dark.

That matters because the future of “mission-critical” is increasingly defined by environments where the infrastructure either doesn’t exist, can’t be trusted, or is actively being attacked.

Silvus had already been proven in the most demanding conditions imaginable: Ukraine. In a war where Russian electronic warfare has repeatedly tried to jam, disrupt, and deny communications, Silvus radios have been used to connect drones, unmanned ground vehicles, and dismounted soldiers in exactly the kind of GPS-denied, spectrum-contested environment where conventional systems start to fall apart.

The near-term growth engine here is defense and unmanned systems. At the time Motorola announced the deal, Silvus was tracking to roughly $475 million of revenue in 2025, with adjusted EBITDA margins around 45 percent—extraordinary for defense tech. And the momentum appeared to continue after closing. By February 2026, Motorola Solutions management had already raised its 2026 Silvus revenue outlook to $675 million, which was $75 million above initial targets, citing strong demand from defense customers and international markets, particularly in Europe.

The strategic logic is simple, and it’s a big deal. Motorola Solutions spent decades becoming the default provider of mission-critical communications for domestic first responders. Silvus extends that “communications you can bet your life on” promise into military and border security use cases that weren’t really in Motorola’s wheelhouse before. Put together, Motorola can now sell a spectrum of capability that runs from a city’s dispatch center all the way to a forward-deployed unit that needs resilient tactical comms—and increasingly, to the unmanned systems operating alongside them.

It also expands the company’s opportunity set at a time when the core market is healthy but familiar. The land mobile radio market was valued at $17.89 billion in 2024 and is projected to reach $32.24 billion by 2030, growing at a 10.7 percent CAGR. But the defense and unmanned systems market Silvus helps open up could be even larger, fueled by the global proliferation of military drones, the hard-earned lessons of Ukraine, and rising NATO defense spending commitments.

Of course, this wasn’t a casual add-on. At up to $5.0 billion including earnouts, Silvus was a meaningful step up in price tag and leverage, and the most consequential expansion of Motorola’s addressable market since Avigilon created the modern video security business. And defense procurement is a different animal than public safety: longer sales cycles, heavyweight competitors like Raytheon and L3Harris, and more exposure to budget politics.

Still, the early read was encouraging. In Q4 2025 alone, Motorola cited notable Silvus orders including a $20 million contract from an unmanned systems provider—an early sign that this wasn’t just a strategic slide-deck acquisition. It was a real wedge into the next battlefield Motorola Solutions wants to win: communications when the network itself is the target.

The Greg Brown Playbook

After eighteen years as CEO—the longest tenure after founder Paul Galvin and his son Bob—Greg Brown’s approach had hardened into something Motorola Solutions could run on. Not just a strategy, but a repeatable pattern that explains what the company did after the split, and what it was likely to do next.

Step one: own the mission-critical base. The P25 and TETRA radio franchises generated enormous margins and essentially no churn. This was the foundation—the part of the business you could build everything else on without worrying the floor would move. The D-Series infrastructure, the first major upgrade in twelve years, was already pushing statewide network refresh cycles. Deals in places like Colorado, Tennessee, and Kentucky weren’t just revenue; they were another decade of installed-base advantage. And at the edge, the APX NEXT ecosystem was expected to grow to about 300,000 connected devices by the end of 2026.

Step two: extend into adjacent platforms. Video security, command center software, access control, evidence management, defense MANET—each one connected back to the communications core. Each one also made the customer relationship deeper and harder to unwind. This wasn’t diversification for its own sake. It was platform deepening: selling more of the workflow to the same agencies that already trusted Motorola for the part that cannot fail.

Step three: turn products into software and services. When Brown took over, Motorola’s government business leaned heavily on hardware. By fiscal 2025, Software and Services was 38 percent of revenue and growing faster than the rest of the company. The point wasn’t just higher margins—it was visibility. Subscriptions and multi-year managed services contracts make revenue more predictable, make customer relationships stickier, and smooth out the lumpiness of big hardware refresh cycles. Avigilon Alta, CommandCentral, and the AI-powered Assist product priced at $99 per user per month were all expressions of the same shift: from shipping boxes to running the system.

Step four: return capital aggressively. Brown cut the share count by more than half since 2011 and raised the dividend every year at a double-digit rate. That wasn’t financial engineering as an afterthought; it was part of the model. If you believe the business will keep throwing off cash, you can concentrate ownership, lift per-share results, and signal to the market that the flywheel is real. A 51 percent share reduction means that even steady, unflashy growth shows up as meaningful per-share compounding.

Step five: acquire relentlessly, but with discipline. Since the 2011 split, Motorola Solutions completed 46 acquisitions—about three per year—at an average price of roughly $1.05 billion. Brown mostly avoided the ego-driven mega-deal. Instead, he ran a steady cadence of capability buys: fill a gap, add recurring revenue, deepen the platform, repeat. Silvus was the outlier on size, but even that fit the pattern—an expansion of “mission-critical” into defense and tactical environments. The 2025 class—Theatro, RapidDeploy, Silvus, and Blue Eye—totaled $4.9 billion, and each mapped cleanly to one of the company’s three pillars.

Add it all up, and you get what Brown often described as the “911 call to case closure” workflow: every step of a public safety incident—the call, the dispatch, the communications, the video capture, the evidence, the analytics—running on Motorola Solutions technology. No competitor offers the full stack. And every new component makes the whole system harder to displace.

The numbers show what this kind of discipline compounds into. At the 2011 split, Motorola Solutions had a market cap of about $13 billion. By the end of 2018, it was $18.8 billion. By the end of 2021, $45.9 billion. By the end of 2024, $77.3 billion. The stock set an all-time high of $497.99 on November 8, 2024. A dollar invested on the day of the split would be worth roughly fifteen dollars by early 2026, versus about four dollars for the same dollar in the S&P 500.

That isn’t the outcome of one genius moment. It’s the outcome of a playbook—run patiently, year after year, until “boring” turns into inevitable.

Competition and the Hytera Saga

Motorola Solutions faces competition across all three of its core technology areas. But the landscape is fragmented, and no single rival matches the breadth of Motorola’s platform.

In mission-critical networks, L3Harris Technologies is the primary U.S. competitor in P25 land mobile radio. Beyond that are a mix of manufacturers and specialists—Airbus, BK Technologies, iCOM, JVCKenwood, Samsung, Sepura, Tait, TrellisWare, Persistent Systems, and Zebra—each strong in particular niches. In the MANET and defense space that Motorola entered in a bigger way with Silvus, the competitive set includes players like DTC, Doodle Labs, TrellisWare, and Persistent Systems. In video security, the field gets even more crowded: Axon Enterprise is a major force in body-worn cameras for law enforcement, Axis Communications and Genetec are strong in enterprise video, Verkada and Eagle Eye Networks compete in cloud video, and Chinese giants Hikvision and Dahua face tightening restrictions in U.S. government sales. In command center software, Motorola goes up against Axon, Tyler Technologies, CentralSquare, and Mark43.

But the competitive story that explains Motorola Solutions’ moat better than any market-share chart is the Hytera litigation.

In 2017, Motorola Solutions sued Hytera Communications, a Chinese radio manufacturer, for copyright infringement and trade secret misappropriation. The allegation was blunt: Hytera hired three Motorola engineers who, before leaving, downloaded thousands of proprietary documents containing Motorola trade secrets and copyrighted source code—then used that material to build competing Hytera H-Series products.

A jury awarded Motorola compensatory and punitive damages totaling $764.6 million, which the district court later reduced to $543.7 million. The U.S. Department of Justice also brought criminal charges against Hytera and several employees. And the case kept escalating. In August 2025, a U.S. District Court held Hytera in civil contempt for violating a royalty order, requiring payment of about $70 million for unpaid royalties and interest tied to continued use of Motorola’s trade secrets and copyrighted source code. Additional orders pushed the total to more than $101 million. Hytera appealed, but the appeal did not automatically pause the payment obligation. The District Court was expected to issue a sentencing ruling on March 5, 2026, which could include fines and restitution to Motorola Solutions.

The Hytera saga matters for reasons that have very little to do with the dollars. It’s a rare window into what real competition looks like in a market where trust and reliability are the product. Motorola has spent decades building technology—and credibility—that agencies bet lives on. The lawsuit alleges that a competitor tried to shortcut that process by taking the blueprints.

It also punctures a persistent myth: that “anyone can build radios.”

Sure, anyone can build a device that transmits and receives. That’s not what Motorola Solutions sells. Motorola sells a certified, interoperable, field-proven mission-critical communications system—one that has to work with neighboring jurisdictions, meet stringent security requirements, and perform under the worst conditions imaginable. P25 may be an open standard, but compliance is not a checkbox. The P25 Compliance Assessment Program involves extensive third-party testing. Federal agencies require FIPS 140-2 encryption certification. States and localities add their own requirements. And beyond all of that sits the hardest barrier of all: institutional trust built over decades of performance.

That trust can’t be bought quickly. It can’t be marketed into existence. And as the Hytera case underscored, even having someone else’s designs doesn’t give you what Motorola has been selling for nearly a century: confidence, under pressure.

Bull Case, Bear Case, and the Analytical Framework

There are a lot of ways to explain why Motorola Solutions has been able to compound for so long. Two frameworks help make it legible: Porter’s Five Forces, which tells you what the industry structure allows, and Hamilton Helmer’s 7 Powers, which tells you what this specific company has that others don’t.

Through the lens of Porter’s Five Forces:

Threat of new entrants: Extremely low. You don’t wake up one day and decide to build a mission-critical radio ecosystem. It takes years of engineering, certification, interoperability testing, and, most importantly, credibility with governments and agencies that don’t get a second chance when systems fail. The bar is so high that P25 and TETRA haven’t seen meaningful new entrants in decades.

Bargaining power of suppliers: Moderate. Motorola Solutions depends on semiconductors and manufacturing partners like everyone else, but its scale and long-standing relationships give it leverage. It even outsourced video manufacturing in 2024 without disrupting supply—exactly the kind of “boring competence” that matters when your customers can’t tolerate missed deliveries.

Bargaining power of buyers: Low to moderate. Yes, governments can be demanding, and procurement can be painful. But alternatives are limited, and switching costs are enormous. Most “competitive” cycles end up being an upgrade of what’s already deployed, because ripping out the communications backbone of a state or major city is a high-risk, multi-year event.

Threat of substitutes: Low, but evolving. FirstNet—AT&T’s dedicated broadband network for first responders built on Band 14 spectrum, with more than seven million public safety connections—has become essential for data. But it’s still a complement more than a replacement for land mobile radio voice. LTE, and eventually 5G, may absorb more mission-critical voice over time, but that kind of substitution would require slow-moving regulatory change, operational retraining, and real-world performance that matches the “radio can’t fail” standard.

Competitive rivalry: Moderate. L3Harris is a real competitor in land mobile radio. Axon is aggressive in body cameras and software. But neither matches Motorola Solutions’ combination of installed base, breadth across the workflow, and scale of recurring services revenue.

Through Hamilton Helmer’s 7 Powers:

Switching costs: This is the anchor. These aren’t consumer subscriptions you cancel online. They’re multi-decade infrastructure deployments, with thousands of trained users, interoperability agreements with neighbors, and operating procedures built around how the system behaves. For most agencies, switching isn’t “expensive.” It’s existentially risky.

Scale economies: Motorola Solutions’ revenue base supports sustained R&D and global service capacity that smaller, focused competitors struggle to match. In mission-critical systems, being big isn’t vanity—scale directly translates into product depth, certification muscle, and the ability to show up quickly when something breaks.

Counter-positioning: The 2011 split was a strategic clean break that competitors can’t easily copy. Brown built a pure-play mission-critical platform while others stayed structurally tied to different models—L3Harris as a diversified defense contractor, Axon as a company anchored in law enforcement products and software. Replicating Motorola’s focus would require them to unwind their own incentives and operating systems.

Cornered resource: Motorola’s institutional trust is not a marketing asset; it’s a moat. The company serves more than 100,000 customers across more than 100 countries, and those relationships were built over generations of performance. When an agency chooses a vendor for the system officers rely on in life-threatening moments, it’s not a spreadsheet decision. It’s a question of whether the vendor will still be here in fifteen years, whether it can restore service fast when a tower fails during a disaster, and whether the gear has proven itself when conditions are ugly. That confidence compounds slowly—and it’s almost impossible to manufacture quickly, no matter how much capital a new entrant raises.

Process power: Motorola’s acquisition machine is itself an advantage. After 46 acquisitions, the company has a repeatable way to identify gaps, buy capabilities, and fold them into a coherent platform. That “how” becomes a capability that improves with every deal—hard to see from the outside, but powerful over time.

Bear case:

Motorola Solutions is not risk-free, and the risks are real—not theoretical. Airwave remains the most visible overhang: the charge control is already a hit, and the class action could seek up to $623 million in damages if it succeeds. Growth also isn’t hypergrowth; organic revenue growth in 2025, excluding acquisitions, was four percent. Silvus is strategically exciting, but at up to $5.0 billion including earnouts it meaningfully increased leverage, and defense brings unfamiliar buying cycles and heavyweight competitors. Add in ongoing tariff headwinds of roughly $70–$80 million annually, and you have a company that needs to keep executing cleanly. At around 27 times forward non-GAAP earnings, the valuation gives it less room for error than it had earlier in the compounding story. And over the very long term, if broadband LTE/5G ever truly converges with mission-critical voice, that could slowly pressure the core land mobile radio franchise.

Bull case:

The bull case starts with a simple premise: public safety spending is closer to “keep the lights on” than “nice-to-have.” It’s one of the few categories of government investment that’s hard to cut without consequences, and that gives Motorola Solutions a resilience most tech companies don’t have. The record $15.7 billion backlog provides multi-year visibility. Software and Services—nearing 40 percent of revenue and growing 13 percent in 2025—keeps improving the quality of earnings and the durability of the model. Silvus expands Motorola’s opportunity set into defense and unmanned systems, and early performance has been strong, with 2026 revenue expected to reach $675 million. On top of that, AI-driven products—SVX body-worn assistants already shipping in meaningful volume, the Assist platform priced at $99 per user per month, and increasingly capable video analytics—create new upsell paths inside an installed base that already trusts the company. Margins have continued to expand into the 30-plus percent range on a non-GAAP basis, and $2.6 billion of free cash flow gives Motorola Solutions the rare ability to fund R&D, do M&A, and return capital—at the same time.

The KPIs That Matter

If you want to track Motorola Solutions without getting lost in product launches and press releases, there are three numbers that tell you almost everything you need to know:

1. Software and Services revenue as a percentage of total revenue. This is the clearest signal that Motorola has actually become a platform business, not just a hardware vendor with a services wrapper. It was about 36 percent of revenue in fiscal 2024, and it rose to 38 percent in fiscal 2025. The direction matters more than the exact figure: the closer this gets to 40 percent and beyond, the more the business starts to look like recurring infrastructure. If it stalls or slides backward, it’s an early warning that the software flywheel isn’t pulling its weight.

2. Ending backlog. Motorola ended fiscal 2025 with $15.7 billion in backlog—roughly a little over a year of revenue already spoken for. What you really want to watch is whether that number is growing, and where the growth is coming from. Software and Services backlog rose 13 percent to $11.9 billion, which is exactly what you want to see in a company built on multi-year contracts. Unlike most “tech,” where demand can turn on a dime, Motorola’s government and public safety customers commit far in advance—so backlog is a real-time read on future momentum.

3. Non-GAAP operating margin. This is the scoreboard for the whole transformation. In fiscal 2025, non-GAAP operating margin reached 30.3 percent, and it hit 32.1 percent in Q4. That’s the compounding engine in action: more software mix, more services, and more leverage as the installed base grows. Management’s 2026 outlook implied roughly another 100 basis points of expansion. In a business with high switching costs and recurring revenue, margin gains don’t just look good—they tend to stick.

Looking Forward: 2026 and Beyond

When Motorola Solutions gave its 2026 outlook on February 11, 2026, it read like a company trying to do what compounding machines always try to do: make “another strong year” feel routine.

Management guided to about eight percent revenue growth—roughly $12.7 billion—slightly ahead of where Wall Street had been. It also guided to non-GAAP EPS of $16.70 to $16.85, again above prior consensus, plus about $3.0 billion in operating cash flow and roughly 100 basis points of non-GAAP operating margin expansion. The first-quarter setup was consistent with that tone: six to seven percent revenue growth and non-GAAP EPS of $3.20 to $3.25.

The Silvus story is also already getting bigger. Motorola expected Silvus to contribute $675 million of revenue in 2026—$75 million above prior targets—driven by defense demand and strength in international markets, particularly in Europe. Meanwhile, the D-Series infrastructure upgrade cycle was expected to keep pulling statewide network refreshes forward—exactly the kind of multi-year, high-switching-cost cadence that makes Motorola’s core franchise so durable.

Investors clearly liked what they heard. By mid-February 2026, the stock was up about nineteen percent year to date, trading around $452. Analyst sentiment skewed heavily positive—no sells, mostly buys—with price targets clustered from the mid-$400s to about $530, averaging around $510.

But if you’re looking for what could actually move the story over the next year, it isn’t a quarter-to-quarter beat. It’s a handful of discrete events—some upside, some overhang.

First is Hytera. The sentencing ruling expected on March 5, 2026 could include fines and restitution, which would be incremental financial upside on top of what has already become a defining enforcement story for Motorola’s moat.

Second is Airwave. The class action certification decision—pending after the September 2025 hearing—will determine whether Motorola faces potential damages of about $623 million. And separately, the CMA’s scheduled 2026 review of the Airwave charge control introduces another variable: rates could, in theory, be adjusted up or down.

And third is the one that may matter the most long-term: AI.

Motorola’s AI push has started to show up across the portfolio in ways that feel less like a lab experiment and more like product. The SVX body-worn assistant—combining a P25 speaker microphone with a body camera and AI—had shipped more than 15,000 units and received FedRAMP High authorization in February 2026. Assist, launched in early 2025, aimed to embed AI across all three technology areas, delivering contextual intelligence to officers in the field. In January 2026, Motorola introduced Assist Suites, positioning role-based AI tools that synthesize inputs like 911 audio, body camera footage, and radio transcripts. A December 2025 partnership with Google enabled emergency video sharing between Motorola systems and Google’s infrastructure. And in September 2025, Nokia and Motorola Solutions collaborated to develop a tactical communication network for UK defense agencies.

That’s a lot of moving pieces, but the direction is consistent: Motorola wants to make its platform smarter, not just broader—and then sell that intelligence back into an installed base that already trusts it.

The final question hanging over “2026 and beyond” is leadership. Greg Brown turned sixty-five in 2025 and, by tenure, is now the company’s longest-serving CEO since the Galvins. His fiscal 2024 compensation was about $30.85 million, reflecting a 318-to-1 CEO-to-median-employee pay ratio. Over the years, he has reportedly generated close to half a billion dollars from stock sales, and his vested options alone would represent a pre-tax windfall of $416 million at recent prices—a direct consequence of the roughly 1,475 percent total shareholder return under his watch. Fortune named him the number one underrecognized standout CEO of 2024. Bloomberg profiled him in November 2025 as “The Dealmaker Who Flipped Motorola’s Script.” He also received the Yale Legend in Leadership Award in 2025.

In many ways, Motorola Solutions has done what great companies try to do: turn a CEO’s instincts into an institution. The M&A cadence, the government relationships, and the platform strategy aren’t just Greg Brown’s personal toolkit anymore—they’ve become organizational muscle. The company has also built a deep senior bench.

But succession still matters. Transitions always create uncertainty, and markets tend to assign a premium to leaders who’ve already proven they can run the playbook at scale. Whenever Motorola does signal a handoff, it will be a moment worth watching—not because the strategy disappears overnight, but because the market will want proof that the compounding machine can keep running without the person who built it.

The Bottom Line

Here’s the Motorola Solutions story in its simplest form.

In 1928, a man who’d already gone bankrupt twice bought back his own invention for $750—and started a company that would sell radios to police departments. Over the decades, that company grew into a sprawling American tech icon. It helped carry the first words from the moon. It invented the handheld cell phone. And then it nearly broke itself chasing the consumer dream, right as the smartphone era rewrote the rules.

In 2011, Greg Brown made the move that saved it: he split Motorola in two, kept the side nobody bragged about, and turned it into the kind of business that quietly compounds. Over the next fifteen years, he built Motorola Solutions into a roughly $76 billion mission-critical technology platform with record revenue, expanding margins, and a record $15.7 billion backlog.

The line from Paul Galvin’s first police radio in 1930 to Greg Brown’s backlog in 2026 isn’t a metaphor. It’s the business. When you build the systems people rely on in emergencies—the ones that have to work when everything else is failing—you earn something rare: trust that turns into switching costs, long contracts, and resilience through cycles.

Motorola Solutions isn’t the flashiest tech company in America. It doesn’t sell a lifestyle. It doesn’t need a product launch with pyrotechnics.

It builds the infrastructure behind the people who run toward danger. It helps cities coordinate. It helps agencies see, communicate, and respond.

It answers one of society’s most important questions: when it matters most, what still works?

For nearly a century, Motorola has made a career out of being the answer. And if backlog is the best predictor we have, it’s not done yet.

Recent News

On February 11, 2026, Motorola Solutions reported record fourth-quarter and full-year 2025 results—and they looked exactly like what a compounding infrastructure business is supposed to look like. Revenue hit $11.7 billion, with non-GAAP EPS of $15.38, operating cash flow of $2.8 billion, and ending backlog rising to a record $15.7 billion. Management also laid out 2026 guidance that came in ahead of expectations, calling for about $12.7 billion of revenue and non-GAAP EPS of $16.70 to $16.85.

By February 2026, the market was rewarding that consistency. The stock traded around $452, putting Motorola Solutions at roughly a $76 billion market cap. Analyst sentiment stayed firmly constructive: no sells, mostly buys, with an average price target around $510.

The Airwave overhang kept moving, too—but in the direction Motorola didn’t want. On January 30, 2025, the UK Court of Appeal unanimously dismissed Motorola’s final appeal against the Competition and Markets Authority’s Airwave charge control, effectively locking in the reduced economics.

Product-wise, the company continued to push its “AI everywhere” strategy into real offerings. In January 2026, Motorola launched Assist Suites—role-based AI tools built for public safety workflows—and the SVX body-worn assistant received FedRAMP High authorization.

Greg Brown’s run also kept getting the kind of retrospective attention that only shows up after the stock chart has done its work. In November 2025, Bloomberg profiled him as “The Dealmaker Who Flipped Motorola’s Script.” That same month, Motorola acquired Blue Eye for $79 million, and Brown received the Yale Legend in Leadership Award.

On the deal front, the biggest milestone was August 6, 2025, when Motorola Solutions completed its acquisition of Silvus Technologies for $4.4 billion—its largest acquisition ever, and a clear signal that defense-grade communications is now a major strategic lane.

Stepping back, 2025 was a “run the playbook” year at scale: four acquisitions in total (Theatro, RapidDeploy, Silvus, and Blue Eye) adding up to $4.9 billion, alongside $1.9 billion returned to shareholders and the company’s fourteenth consecutive year of a double-digit dividend increase.

The Airwave situation also picked up a new legal dimension in December 2024, when Clare Spottiswoode filed a class action seeking roughly $623 million in damages related to alleged overcharges from 2020 to 2023. A certification hearing was held in September 2025, and the outcome remained pending as of February 2026.

Also in September 2025, Nokia and Motorola Solutions announced work on a tactical communications network for UK defense agencies—one more data point that the company’s mission-critical identity is widening from public safety into defense and national security.

Sources, Links, and Resources

- Motorola Solutions investor site (2025 Annual Report, Q4 2025 earnings materials)

- Motorola Solutions Form 10-K (Fiscal Year 2025) on SEC EDGAR

- UK CMA Airwave market investigation (Final Report, April 2023)

- Motorola Heritage: company history

- Martin Cooper and the first cell phone call (Motorola history page)

- Silvus Technologies acquisition announcement (May 2025)

- Bloomberg: “The Dealmaker Who Flipped Motorola’s Script” (November 2025)

- UK Court of Appeal (Civil Division): Airwave charge control ruling (January 30, 2025)

- Motorola Solutions Investor Day presentations (2022–2025)

- FirstNet Authority

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube