MSCI: The Index Empire That Powers Global Finance

I. Introduction & Episode Roadmap

Picture this: Every morning, before markets open, portfolio managers at thousands of institutions around the world boot up their terminals and check one thing first—how their portfolios performed against MSCI benchmarks. In Seoul, a pension fund manager scrutinizes her emerging markets allocation. In London, a hedge fund quant recalibrates his risk models. In New York, an ETF issuer watches billions flow into products that slavishly track these indices. This is the hidden empire of MSCI, where $16.5 trillion in assets—more than the GDP of China—are benchmarked to indices created by a company most people have never heard of.

The central question that should boggle any student of business history: How did a sleepy division buried inside Morgan Stanley transform into one of the most powerful toll booths in global finance? This isn't just another fintech success story. It's the tale of how a company built what might be the ultimate network effects business—one where competitors literally make you stronger, where regulators inadvertently protect your moat, and where the more passive investing grows, the more active your cash flows become.

What we're really exploring today is the architecture of modern capitalism itself. MSCI doesn't manage money, doesn't trade securities, doesn't even give investment advice. Yet it sits at the center of virtually every major investment decision on the planet. They've built what venture capitalists dream about but rarely achieve: infrastructure so embedded in the system that removing it would be like trying to extract concrete from a foundation.

Think about the paradox here—in an industry obsessed with alpha, with beating the market, with finding an edge, one company makes billions by simply defining what "the market" is. While fund managers wage war over basis points of outperformance, MSCI collects rent from both sides of every battle. It's the arms dealer in the investment wars, selling the same weapons to everyone while remaining studiously neutral.

This is a story about standards, about how boring can be beautiful in business, about the compounding power of being first, and about why the best monopolies are the ones nobody thinks to challenge. By the end of this journey, you'll understand why Henry Fernandez, MSCI's CEO since 2007, might run the most underappreciated business model in finance—and why Warren Buffett, if he understood technology businesses better, would probably own the whole thing.

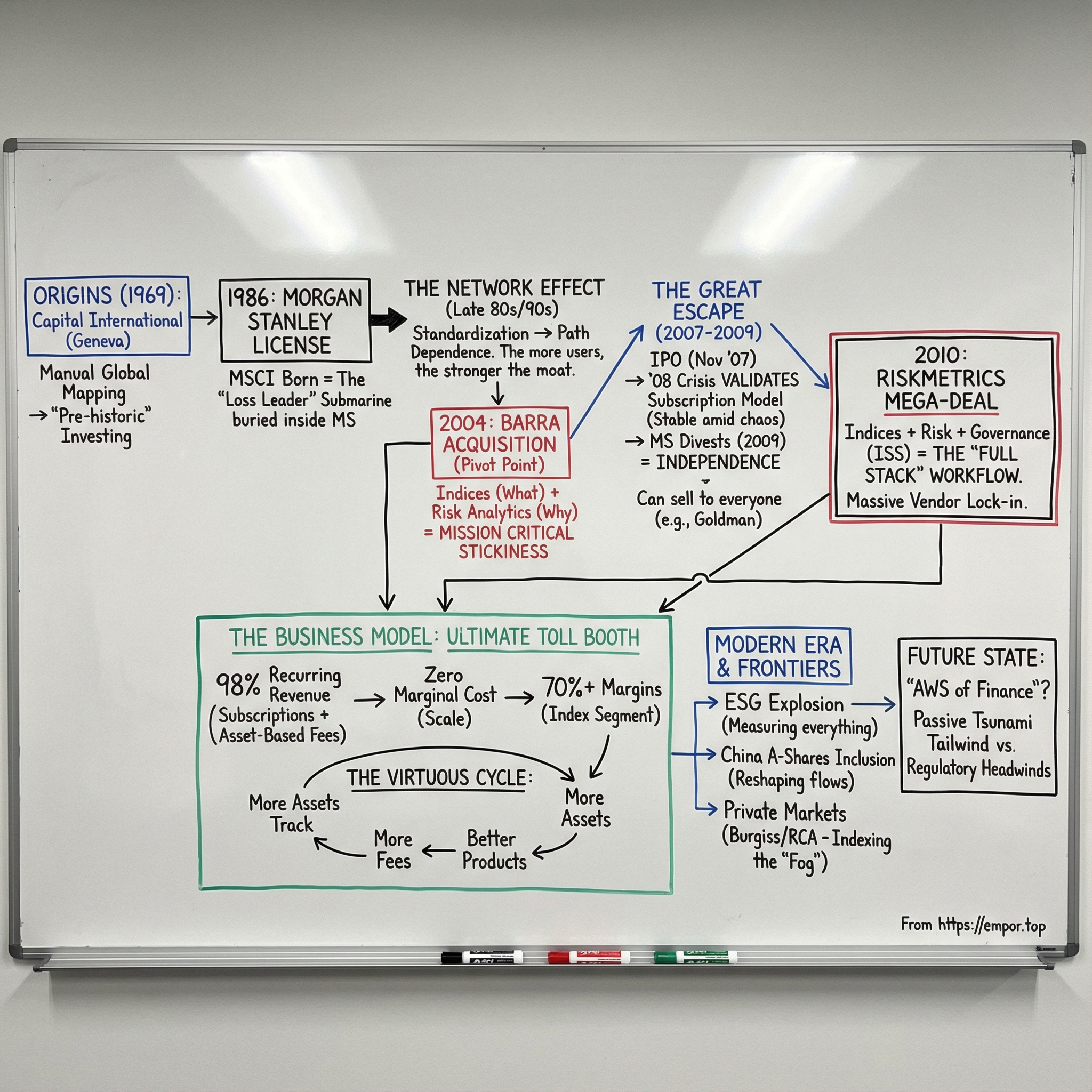

II. Origins: Capital International & The Pre-History (1969–1986)

The year is 1969. Neil Armstrong has just walked on the moon, Woodstock is defining a generation, and in a modest office in Geneva, a company called Capital International is about to launch something that seems positively quaint by comparison: the first systematic attempt to measure global equity markets. No fanfare, no IPO roadshow, just a group of finance nerds who thought someone should probably track how stocks were doing outside America.

To understand why this mattered, you need to grasp the prehistoric nature of global investing in 1969. The Bretton Woods system was still limping along—currencies were pegged, capital controls were everywhere, and the idea of a pension fund in Ohio buying stocks in Tokyo was about as common as a hedge fund investing in cryptocurrency would be in 1969. Most American investors thought "international diversification" meant buying Coca-Cola because it sold soda overseas.

Capital International's founders weren't visionaries in the Steve Jobs sense—they were more like cartographers mapping unexplored territory. While everyone else was focused on their domestic markets, they asked a simple question: "What if we created a standardized way to measure equity performance across borders?" Remember, this was before Excel, before Bloomberg terminals, before you could Google "Nikkei close." They were literally calling brokers in different time zones, collecting price sheets by telex, and computing indices by hand—or at best, with calculators the size of typewriters.

The Capital International World Index launched with all the glamour of a phone book publication. But here's what made it revolutionary: for the first time, an institutional investor could answer the question, "How did global equities do last quarter?" with something more sophisticated than "pretty good, I think." It was the financial equivalent of inventing latitude and longitude—suddenly, everyone had a common reference point.

Fast forward to 1986. The world has changed dramatically. The Plaza Accord has just realigned global currencies. Japanese companies are buying Rockefeller Center. The Big Bang is about to detonate in London. And at Morgan Stanley, someone realizes they're missing something crucial. The firm is advising clients on global portfolios, but they don't own the map everyone's using to navigate.

The licensing deal Morgan Stanley struck with Capital International was, in hindsight, one of the great bargains in financial history. They didn't buy the company—that would have been too expensive, too complicated. Instead, they licensed the rights to these indices and slapped their name on front: Morgan Stanley Capital International. MSCI was born, though nobody at Morgan Stanley realized they'd just acquired what would become their most valuable asset not denominated in bonus pools.

Why did Morgan Stanley want indices? The answer reveals everything about how Wall Street was evolving in the 1980s. The rise of institutional investing meant clients weren't just asking for stock picks anymore—they wanted systematic approaches, benchmarks, attribution analysis. The old model of a broker calling with a "hot tip" was giving way to consultants with spreadsheets asking about "tracking error" and "information ratios."

Morgan Stanley's bankers initially treated MSCI like they treated the coffee machine—nice to have, but not exactly a profit center. The indices were a loss leader, a way to get meetings with pension funds who would hopefully throw them some lucrative mandates. The idea that these indices themselves would one day be worth more than most investment banks? That would have been laughed out of any partner meeting.

But even in those early days, something interesting was happening. The more institutions used MSCI indices as benchmarks, the more other institutions had to use them too. If you're a pension consultant comparing managers, you need them all measured against the same yardstick. If you're a manager, you need to report performance against whatever benchmark your clients are using. It was a network effect hiding in plain sight, growing stronger with every new user, every new dollar benchmarked.

The deal structure was elegant in its simplicity: Capital International kept ownership but granted exclusive rights to Morgan Stanley for distribution and branding. Both sides thought they were getting the better deal. Capital International got global distribution through Morgan Stanley's massive sales force. Morgan Stanley got indices without the hassle of building them. Neither side realized they were handling the financial equivalent of uranium—immensely powerful if properly refined.

By the time Ronald Reagan was leaving office, MSCI indices had quietly become the default way sophisticated investors measured international equity performance. Not through Super Bowl ads or aggressive sales tactics, but through the slow, steady accumulation of users who, once they started using MSCI benchmarks, found it almost impossible to stop. The foundation was set for one of the great business transformations in financial history—though it would take another two decades for anyone to notice.

III. Building Inside the Beast: The Morgan Stanley Years (1986–2004)

Inside Morgan Stanley's gleaming towers in midtown Manhattan, MSCI operated like a submarine running silent beneath an aircraft carrier. While traders upstairs were screaming into phones and investment bankers were pitching LBOs, a small team was quietly maintaining spreadsheets that would determine how trillions of dollars would flow around the world. The contrast was almost comic—in a firm that measured success by the size of your bonus and the view from your office, MSCI's team worked in windowless rooms, their biggest excitement being when they successfully incorporated a new market into an index without anyone noticing a calculation error.

By the late 1980s, something remarkable had happened: MSCI indices had become the primary benchmark for international equity investment everywhere except the United States. Not through conquest, but through mathematical manifest destiny. The network effect was kicking in with the force of compound interest. Every quarter that passed with more assets benchmarked to MSCI made it harder for any competitor to matter. It was like trying to launch a new language when everyone already speaks English—technically possible, but practically futile.

The mechanism was beautiful in its simplicity. When CalPERS decided to benchmark their international allocation to MSCI, every manager competing for that mandate had to report performance against MSCI. When those managers went to other clients, they'd suggest using MSCI because that's what they were already tracking. Consultants recommended MSCI because that's what everyone else used, making peer comparisons possible. Each decision reinforced every other decision, creating what economists call "path dependence"—the financial equivalent of everyone driving on the right side of the road because everyone else does.

But competition was stirring. FTSE, the London Stock Exchange's index business, was making aggressive moves. S&P was expanding internationally. Dow Jones was leveraging its brand. The index wars of the 1990s were like the browser wars happening simultaneously in Silicon Valley—everyone could see the prize would be massive, but nobody was quite sure how to win it. The battlefield was strewn with acronyms: EAFE (Europe, Australasia, Far East), ACWI (All Country World Index), EM (Emerging Markets). Each index was a flag planted in disputed territory.

The politics inside Morgan Stanley were byzantine. Here was MSCI, generating modest revenues, requiring significant investment, and worst of all—helping competitors. When Goldman Sachs launched an ETF tracking an MSCI index, they were essentially using Morgan Stanley's intellectual property to compete against Morgan Stanley. The traders hated it. The investment bankers didn't understand it. The senior partners mostly ignored it, except when they needed index data for a pitch book.

MSCI operated as the ultimate cost center in a firm allergic to cost centers. Every year during budget season, someone would ask why Morgan Stanley was subsidizing the entire asset management industry's benchmarking needs. The answer was always some version of "strategic value" or "client relationships"—the corporate equivalent of saying "it's complicated" about a relationship status. The real answer, which nobody could articulate at the time, was that MSCI was building a moat so wide that even Morgan Stanley's bankers couldn't see the other side.

The decision to follow Dow Jones in float-weighting indices seems technical, even boring. But it was actually a defining moment that revealed MSCI's true nature. Float-weighting means only counting shares actually available for purchase, not those locked up by governments or founding families. When Dow Jones made this shift, MSCI had a choice: stick with their methodology and risk becoming obsolete, or follow and admit they weren't the sole arbiter of index construction truth.

They followed, but with a twist. MSCI turned the transition into a marketing masterstroke, consulting clients, publishing research, making the change feel collaborative rather than reactive. It was financial diplomacy at its finest—managing to copy a competitor while making clients feel like they'd been heard. The episode taught MSCI a crucial lesson: in the index business, you don't need to be first, you need to be standard. And standards are set by consensus, not decree.

The late 1990s brought the dot-com boom, and with it, questions about MSCI's relevance. Why track boring country indices when you could buy TheGlobe.com? Why worry about emerging markets when the NASDAQ was minting millionaires daily? MSCI's response was to do what it always did—quietly update methodologies, add new markets, refine calculations. While everyone else was talking about "new paradigms," MSCI was doing the equivalent of maintaining railroad tracks—unglamorous but essential work that would outlast any bubble.

Inside Morgan Stanley, frustration was building on both sides. MSCI executives felt constrained, unable to pursue opportunities because they might conflict with other Morgan Stanley businesses. Morgan Stanley leadership increasingly saw MSCI as a distraction from their core competencies of trading and banking. The submarine was starting to feel less like stealth and more like suffocation.

By 2004, the writing was on the wall. MSCI had grown too important to remain a division but was seen as too peripheral to Morgan Stanley's strategy to warrant real investment. The indices that started as a loss leader had become the industry standard, but Morgan Stanley was capturing only a fraction of the value being created. It was like owning the patent on aspirin but only selling it in your own pharmacy—lucrative, but missing the bigger opportunity.

The network effects that made MSCI valuable also made it vulnerable to neglect. Every day that passed without innovation, without investment, without independence, was a day competitors could chip away at the edges. The beast that housed MSCI had nurtured it through adolescence, but now threatened to stunt its growth. Something had to change, and in the corridors of Morgan Stanley, conversations were beginning about what had once been unthinkable: letting MSCI go.

IV. The Barra Acquisition: From Indices to Analytics (2004)

Andrew Rudd was not your typical Berkeley professor. While his colleagues were debating efficient market hypothesis in faculty lounges, he was in a Palo Alto garage in 1975, building what would become the nuclear reactor of modern portfolio management. His creation, Barra, didn't make stock picks or time markets—it did something far more powerful: it explained why portfolios behaved the way they did. Think of it as financial forensics, CSI for portfolios, except instead of solving crimes, it was decomposing returns into factors like value, growth, momentum, and size.

By 2004, Barra had become to risk analytics what MSCI was to indices—the invisible standard everyone relied on but nobody talked about at cocktail parties. Their multi-factor models were the Rosetta Stone of institutional investing, translating the chaos of market movements into comprehensible factors. If your portfolio lost money, Barra could tell you exactly how much was due to your stock selection versus your sector bets versus your exposure to interest rates. It was like having X-ray vision for portfolios.

When MSCI announced the acquisition of Barra for $816.4 million in 2004, the financial press yawned. The headlines were dutiful but bored—"Index Provider Buys Risk Analytics Firm." What they missed was that MSCI had just executed one of the great strategic coups in financial services history. This wasn't just buying a company; it was buying a second language that every institutional investor needed to speak.

The synergies were so obvious that even Morgan Stanley's bankers, not typically known for operational insights, could see them. Same clients—every institution using MSCI indices needed risk analytics. Same data requirements—understanding markets required both performance measurement and risk decomposition. Same subscription model—recurring revenues, high retention, beautiful unit economics. It was like a dating app discovering that both people had already swiped right.

But the real genius wasn't in the overlap—it was in the combination. Indices tell you what happened; risk models tell you why. Benchmarks define success; analytics explain failure. Together, they created what Henry Fernandez would later call a "mission-critical workflow tool." Translation: once clients integrated both products into their daily operations, removing them would be like performing surgery on yourself—technically possible, but inadvisable.

The cultural integration was fascinating to watch. MSCI was East Coast finance—suits, hierarchy, Morgan Stanley DNA. Barra was West Coast tech—casual, academic, more likely to debate eigenvalues than earnings. The first joint company meeting looked like a collision between Wall Street and Sand Hill Road. Yet somehow, it worked. Perhaps because both cultures shared something deeper: a reverence for mathematical truth and a belief that markets, however chaotic, could be measured and understood.

Barra brought more than just products—it brought a different way of thinking about the business. Where MSCI had grown through standardization and network effects, Barra had grown through customization and sophistication. Every large client had their own risk model, their own factors, their own way of decomposing returns. It was bespoke tailoring in a world of off-the-rack indices.

The integration revealed something profound about the investment management industry: everyone wanted to be different, but they all needed the same tools to measure their difference. It was like a race where every runner takes a unique path but they all need the same stopwatch. MSCI Barra could now provide both the track and the timing system.

Operationally, the merger was a masterclass in revenue synergy realization—a phrase that usually means "firing people" but in this case meant "selling more stuff to the same clients." The cross-selling opportunities were endless. Index clients needed risk analytics to understand tracking error. Risk clients needed indices to define their benchmarks. Everyone needed both to explain their performance to boards and consultants who increasingly demanded attribution analysis that looked like particle physics equations.

The combined entity also had pricing power that neither possessed alone. When you control both the benchmark and the risk model, you're not just a vendor—you're infrastructure. Switching costs went from high to astronomical. Imagine trying to change not just your portfolio's benchmark but also your entire risk management system simultaneously. It would be like changing your phone's operating system and carrier and number all at once. Theoretically possible, practically insane.

By 2005, MSCI Barra was generating over $400 million in revenues, with EBITDA margins that made software companies jealous. But more importantly, they had transformed from a provider of indices into something far more valuable: the operating system for institutional investing. Every major decision—what to buy, how much risk to take, how to explain performance—ran through their products.

The acquisition also demonstrated MSCI's evolution from passive observer to active participant in shaping how markets operate. Indices were about measurement; risk models were about prediction. Combined, they didn't just reflect market behavior—they influenced it. When MSCI Barra identified a new risk factor, thousands of portfolios would adjust their exposures. When they changed a methodology, billions of dollars would rebalance.

This power came with scrutiny. Academics began writing papers about "benchmark gaming"—how managers would structure portfolios to look good against MSCI indices rather than generate actual alpha. Regulators worried about concentration risk—what happened if everyone used the same risk model and it was wrong? These concerns were valid but also, from MSCI's perspective, validation. You don't worry about the systemic importance of something unless it's systemically important.

The Barra acquisition marked MSCI's transformation from index provider to intelligence platform. They were no longer just keeping score—they were explaining the game, coaching the players, and increasingly, writing the rules. It was still early days, but the foundation was set for something unprecedented: a company that would sit at the center of global capital allocation not through managing money, but through defining how money was managed.

V. The Great Escape: IPO and Independence (2007–2009)

John Mack stood before Morgan Stanley's board in early 2007 with the bearing of a general ordering retreat—not from weakness, but from strategic necessity. "The IPO and potential separation of MSCI are consistent with Morgan Stanley's strategy to focus on our core businesses," he declared, his words carefully crafted to mask what everyone knew: Morgan Stanley needed cash, and MSCI was the crown jewel they could afford to sell. The financial engineers who had created CDOs and synthetic derivatives were about to discover that their most valuable asset was the boring index business they'd ignored for two decades.

The timing seemed either brilliant or insane, depending on your perspective. November 2007—the NASDAQ was still near its highs, private equity was throwing money at everything, and "subprime" was still a term most people needed explained. MSCI's IPO prospectus landed on investors' desks like a message from another universe: here was a business with 95% client retention, 30%+ EBITDA margins, and recurring revenues that arrived as reliably as sunrise. In a world of leveraged speculation, it was selling subscriptions to spreadsheets.

The roadshow was surreal. Henry Fernandez, who had run MSCI since 1998, found himself explaining to hedge fund managers why they should buy shares in a company whose product they used every day but had never thought about. It was like asking someone to invest in oxygen—essential, ubiquitous, but taken completely for granted. The pitch was simple: "You know those indices you benchmark against? We own them. You know those risk models you can't live without? We own those too."

The IPO priced at $18 per share, raising $252 million for 14 million shares. The bankers thought this was conservative. The market thought otherwise. On the first day of trading, November 15, 2007, MSCI opened at $22 and closed at $26.15—a 45% pop that valued the company at $2.7 billion. Morgan Stanley, which retained 86% ownership, had just discovered that its index subsidiary was worth more than many of the investment banks it competed against.

But the celebration was short-lived. Within weeks, the cracks in the financial system became chasms. Bear Stearns collapsed. Lehman Brothers evaporated. The financial crisis wasn't coming—it had arrived with the force of a tsunami. And here was MSCI, a three-month-old public company, watching its clients—the world's largest financial institutions—fighting for survival.

The crisis revealed something profound about MSCI's business model. While banks were hemorrhaging billions and hedge funds were gating redemptions, MSCI's revenues barely budged. The reason was beautiful in its simplicity: even in a crisis—especially in a crisis—you need to measure performance and understand risk. The subscription model that seemed boring during the boom became a life raft during the bust. Clients might cancel their sell-side research, fire their consultants, close their prime brokerage accounts, but they couldn't stop measuring their portfolios against benchmarks.

Inside MSCI's offices, the crisis felt like watching a hurricane from a bunker. All around them, financial institutions were imploding, but their business was actually growing. New regulations demanded better risk management—exactly what MSCI Barra provided. Passive investing was accelerating as active managers underperformed—more assets flowing to indices. The crisis wasn't destroying MSCI's business model; it was validating it.

Morgan Stanley, meanwhile, was fighting for its life. The stock had collapsed from $70 to $10. They needed capital desperately. In May 2009, they sold their remaining stake in MSCI—not because they wanted to, but because they had to. The shares they sold at roughly $22 would be worth over $600 today. It was one of the great forced sellers' remorse stories in financial history.

The completed divestiture in 2009 marked MSCI's true independence day. For the first time in its history, it wasn't a subsidiary, a division, or an afterthought. It was a standalone company with a simple mission: become the indispensable infrastructure for global investing. No longer constrained by Morgan Stanley's conflicts, conservatism, or capital needs, MSCI could finally pursue its destiny.

The transformation was immediate. Freed from bank ownership, MSCI could sell to everyone without favoritism. Goldman Sachs, once wary of enriching a Morgan Stanley subsidiary, became a major client. Independent asset managers, who had previously worried about data security, opened their doors. The company that had been hidden inside a bank was suddenly everywhere.

Henry Fernandez emerged from the crisis as the unlikely winner of the financial crisis—not through betting against subprime or buying distressed assets, but through running a subscription business that collected fees regardless of market direction. His strategy was so boring it was brilliant: raise prices 3-5% annually, maintain 95%+ retention rates, add new products that clients couldn't refuse, repeat indefinitely.

The IPO had valued MSCI at $1.86 billion. By the end of 2009, despite the worst financial crisis in generations, it was worth over $3 billion. The market was beginning to understand something profound: in a world of financial complexity, the companies that provided clarity were priceless. MSCI didn't trade securities, manage money, or take risk. It did something far more valuable—it helped everyone else understand the securities they traded, the money they managed, and the risks they took.

The great escape was complete. MSCI had broken free from Morgan Stanley at exactly the right moment—late enough to be mature, early enough to capture the coming passive investing revolution. The timing that seemed disastrous in November 2007 proved prescient by 2009. While the masters of the universe were being humbled, the indexers were inheriting the earth.

VI. The RiskMetrics Mega-Deal: Doubling Down (2010)

The BlackRock conference room in March 2010 was electric with tension. Larry Fink, the titan who'd built the world's largest asset manager, was sitting across from Henry Fernandez, and both men knew this negotiation would reshape the financial data industry. RiskMetrics—the risk management firm that BlackRock had been eyeing—was on the auction block, and MSCI had just dropped a $1.55 billion bomb that nobody saw coming. The indexing company that barely survived its IPO three years earlier was now playing in the big leagues, writing checks that would make private equity firms nervous.

RiskMetrics wasn't just another analytics company—it was the Vatican of corporate governance, the Supreme Court of proxy voting, and the MIT of risk management all rolled into one. Born from J.P. Morgan's internal risk systems (the ones that famously calculated Value at Risk), RiskMetrics had become indispensable to anyone who needed to understand portfolio risk or vote proxies. Their ISS (Institutional Shareholder Services) unit alone influenced trillions in proxy votes annually, essentially serving as the conscience of corporate America.

Fernandez's pitch to the board was audacious: "We're going to unite market leaders and brands including MSCI, Barra, and RiskMetrics to create the leading provider of mission-critical investment decision support tools." In English, this meant MSCI would control the entire workflow of institutional investing—from benchmark selection through risk management to governance oversight. It was vertical integration that would make John D. Rockefeller proud.

The strategic logic was intoxicating. MSCI had indices and risk models. RiskMetrics had governance data and enterprise risk systems. Together, they'd offer what Fernandez called "the full stack"—every tool an institution needed except the actual portfolio management system. It was like owning every store in a shopping mall except the anchor tenant, and even the anchor needed to shop at your stores.

But the price tag raised eyebrows. $1.55 billion was more than half of MSCI's own market cap. They were essentially betting the company on an acquisition, taking on significant debt in a market still scarred from 2008. The financial press was skeptical—the words "empire building" and "integration risk" appeared in every article. Short sellers circled like sharks, convinced that MSCI was overreaching.

The integration challenges were real and immediate. RiskMetrics had 850 employees to MSCI's 1,500—this wasn't a tuck-in acquisition but a merger of equals. The cultures were different: MSCI was still finance-focused and East Coast, while RiskMetrics had more of a tech company vibe. ISS, the governance unit, operated like a completely different business—part research firm, part advocacy group, part kingmaker in corporate battles.

Then came the regulatory scrutiny. Academics and competitors raised alarm bells about market concentration. One particularly pointed paper argued that having the majority of the asset management industry calculating Value at Risk using one company's models was creating systemic risk. If MSCI's models were wrong, everyone would be wrong in the same direction at the same time. It was the financial equivalent of everyone using the same GPS system—efficient until the satellite fails.

The European Commission launched an investigation. The Department of Justice asked questions. For a moment, it looked like the deal might crater under regulatory pressure. But Fernandez had anticipated this. MSCI agreed to divest certain overlapping products, made commitments about data availability, and most cleverly, argued that combining these businesses would actually reduce systemic risk by creating more robust, better-funded risk models.

By 2011, the integration was revealing unexpected synergies. ISS's governance data could be incorporated into ESG indices—a category that was just beginning to explode. RiskMetrics' enterprise risk tools could be sold to the same corporations that used MSCI indices in their pension funds. The cross-selling opportunities weren't just additive; they were multiplicative.

The real masterstroke was how the deal positioned MSCI for the coming revolution in passive investing. ETF assets were exploding, and every basis point of assets that shifted from active to passive increased MSCI's moat. The RiskMetrics acquisition meant MSCI could serve both sides of this shift—providing indices for passive funds while selling risk analytics to active managers trying to justify their existence.

Client retention post-merger hit 97%—virtually unheard of in large acquisitions. The reason was simple: switching costs had gone from high to impossible. Imagine telling your board that you're changing your benchmark provider, risk model, and proxy voting advisor all at once. You'd be updating systems, retraining staff, and explaining discrepancies for years. It was vendor lock-in that would make Microsoft jealous.

The financial results vindicated the bold move. By 2012, the combined company was generating over $900 million in revenues with EBITDA margins approaching 40%. The debt taken on for the acquisition was being paid down ahead of schedule. The stock price, which had dropped 20% on the announcement, had more than doubled. The empire building that critics derided was looking more like empire consolidation.

But the most profound impact was on MSCI's competitive position. Before RiskMetrics, competitors could argue they offered comparable products. After? MSCI was operating in a different league. They had become what investment consultants called a "one-stop shop," though that understated their importance. They weren't just a shop—they were the entire mall.

The concentration of power was staggering. MSCI could influence how trillions were allocated through their indices, how risk was measured through their models, and how companies were governed through ISS. They had become, in essence, a private regulatory body—setting standards that were voluntary in theory but mandatory in practice.

VII. The Business Model: Building the Ultimate Toll Booth

The numbers tell a story that would make any MBA student weep with envy: 98% of revenue from recurring subscriptions, adjusted EBITDA margins above 70% in the index segment, free cash flow conversion approaching 50%. These aren't just good metrics—they're the kind of numbers that break traditional business school models. MSCI has built something that shouldn't exist in efficient markets: a toll booth on the entire global investment highway where the toll goes up every year and nobody complains.

Let's start with the subscription model, the foundation of MSCI's fortress. As of Q1 2025, 98% of revenues arrive like clockwork, contracted years in advance, as predictable as gravity. This isn't Netflix where subscribers can cancel with a click. When a pension fund integrates MSCI indices into their investment process, extracting them requires board approval, consultant reviews, system overhauls, and explanations to every stakeholder about why you're changing the measuring stick mid-measurement.

The genius lies in the pricing structure. There are two components: flat subscriptions that increase 3-5% annually (like inflation plus a bit more), and asset-based fees that scale with AUM. That second piece—comprising 22-26% of annual revenues—is where the magic happens. When markets go up, MSCI makes more money without lifting a finger. When passive investing grows, MSCI's revenues grow proportionally. It's like owning a percentage of global wealth without any of the risk.

The index segment's 76.6% adjusted EBITDA margins in 2024 would make luxury goods companies jealous. How is this possible? Because the marginal cost of an additional subscriber is essentially zero. The same index that MSCI calculates for one client can be sold to thousands. It's pure information economics—massive fixed costs to build and maintain the indices, near-zero variable costs to distribute them. Every new client is almost pure profit.

But the real beauty is in the network effects that create these margins. Every dollar benchmarked to an MSCI index makes that index more valuable to everyone else. Consultants need to compare managers against the same benchmark. Managers need to report against what consultants expect. ETF providers need to track what investors recognize. Each participant reinforces every other participant's need to use MSCI. It's a perpetual motion machine of dependency.

Client retention rates consistently above 95% aren't just impressive—they're a moat filled with crocodiles. The switching costs are multilayered: technical (systems integration), operational (retraining staff), reputational (explaining changes to boards), and comparative (losing peer comparison ability). One chief investment officer described switching index providers as "like changing your DNA while running a marathon." Technically possible, practically suicidal.

The free cash flow story—48.43% conversion—deserves its own Harvard case study. MSCI generates nearly 50 cents of free cash for every dollar of revenue. Why? Because they're not building factories, managing inventory, or really creating anything physical. They're selling calculations, methodologies, intellectual property that scales infinitely. The only real costs are people (to maintain and enhance products) and computers (to crunch numbers), both of which scale logarithmically while revenues scale exponentially.

The virtuous cycle Fernandez has built is breathtaking in its simplicity: More assets track MSCI indices → more fee revenue → more investment in products → better products and more coverage → more assets choose MSCI indices. It's compound interest applied to business model design. Every year the flywheel spins faster, the moat gets wider, the toll booth gets more expensive.

Consider the pricing power dynamics. When MSCI raises prices 5%, what are clients going to do? Switch to another provider and explain to every stakeholder why their performance numbers no longer compare to history or peers? Pay consultants millions to evaluate alternatives that are functionally identical but require massive switching costs? The conversation usually ends with a resigned sigh and a renewed contract.

The capital allocation is equally brilliant. Since 2014, MSCI has reduced share count by 3.64% annually through buybacks. When your business generates massive cash flows with minimal reinvestment needs, returning capital to shareholders isn't just smart—it's mathematically optimal. Every share retired increases the value of remaining shares, creating a second compounding machine on top of the business model.

The subscription length keeps extending too. Multi-year contracts are becoming the norm, with some clients signing 5-year agreements. This isn't just revenue visibility—it's revenue certainty. MSCI knows with precision what their revenues will be quarters, even years in advance. They could probably forecast earnings more accurately than the Fed forecasts inflation.

But here's the killer insight: MSCI's business model actually gets stronger during market stress. When volatility spikes, demand for risk analytics increases. When active managers underperform, passive flows accelerate. When regulations tighten, compliance needs grow. The worse things get for their clients, the more essential MSCI becomes. It's countercyclical demand in a cyclical industry.

The ultimate test of a business model is whether it would be chosen if you were starting from scratch. If someone tried to build MSCI today, they'd face an impossible challenge: convince the entire industry to switch their measurement standard simultaneously. It would be like trying to get America to adopt the metric system—theoretically superior, practically impossible. MSCI hasn't just built a toll booth; they've built the only bridge across the river, and then they bought the land on both sides.

VIII. Modern Era: ESG, China, and New Frontiers (2010s–Today)

The conference room at China's Securities Regulatory Commission in Beijing, 2017, was a study in contrasts. On one side sat MSCI executives, armed with spreadsheets and methodologies. On the other, Chinese officials who controlled access to the world's second-largest equity market. The topic: including Chinese A-shares in MSCI's Emerging Markets Index. The subtext: who really controls global capital flows—index providers or governments?

The ESG explosion hit MSCI like a gold rush in reverse—instead of everyone racing to the same place, clients were racing in every direction, each with their own definition of "sustainable." Some wanted to exclude tobacco but keep defense contractors. Others wanted carbon metrics but not governance scores. Europeans wanted one thing, Americans another, and Asian clients thought the whole thing was Western imperialism disguised as environmentalism. MSCI's response was brilliant: build everything and let clients choose.

By 2019, MSCI had over 1,500 ESG indices, each one a snowflake of social consciousness and investment returns. They acquired Carbon Delta, a Swiss firm using AI to predict how climate change would affect company valuations—essentially betting that measuring the apocalypse would be profitable. The ESG analytics business went from afterthought to generating hundreds of millions in revenues, growing at 30% annually while traditional index revenues grew at 5%.

But ESG was just the appetizer. The main course was China. In 2018, MSCI announced they would begin including Chinese A-shares in their Emerging Markets Index with an initial 5% weighting. This wasn't just adding another country—it was reshaping global capital flows with the stroke of a pen. Suddenly, every fund tracking the index had to buy Chinese domestic stocks. Trillions of dollars would eventually flow into Chinese markets because a committee in New York decided to change a spreadsheet. The controversy wasn't as dramatic as initially suggested. MSCI began including Chinese A-shares in the Emerging Markets Index in 2018 after China's market reforms and increased accessibility, with consultations with international investors. The Chinese government had indeed sought inclusion—the inclusion of A-shares officially took effect on June 1, 2018—as a way to establish Shanghai and Shenzhen as global financial centers and attract foreign capital to domestic markets.

The pushback came later. In December 2020, following a U.S. Executive Order targeting Chinese military companies, MSCI announced it would stop including China Mobile, China Telecom and China Unicom in its benchmarks. This demonstrated how geopolitical tensions could force even supposedly neutral index providers to take sides.

The private markets expansion represents MSCI's boldest frontier yet. Private equity, private debt, real estate—markets where there are no daily prices, no standardized reporting, no consensus on valuation. It's like trying to index fog. But MSCI sees opportunity where others see impossibility. They acquired Real Capital Analytics in 2021 for undisclosed terms, bringing commercial real estate data into the fold. Then came the blockbuster: Burgiss Group for $697 million in 2023, instantly making MSCI a major player in private markets analytics.

The Burgiss acquisition was particularly clever. Private markets are where the real money is moving—sovereign wealth funds, endowments, family offices all increasing allocations to alternatives. But there's no CNBC ticker for private equity performance, no Bloomberg screen showing real-time IRRs. Burgiss had spent decades building relationships with LPs and GPs, collecting data that was essentially impossible to replicate. MSCI didn't just buy a database; they bought a network of trust in an industry built on relationships.

Carbon Delta, acquired in 2019, represented a different kind of bet—that climate risk would become as fundamental to investing as credit risk. The Swiss firm's models attempted to predict how climate change would affect individual company valuations. Would flooding destroy this factory? Would carbon taxes crush this utility? Would stranded assets strand this oil company? It was speculation dressed as science, but in a world where everyone needed climate analytics and nobody knew how to build them, speculation was enough.

The regulatory scrutiny has intensified with MSCI's growing power. European regulators worry about index concentration. American politicians question the China exposure. Academic papers proliferate about systemic risk. But here's the thing about being infrastructure: the more essential you become, the more regulated you get, and the more regulated you get, the harder it becomes for anyone to compete with you. It's the beautiful paradox of systemic importance.

Recent acquisitions show MSCI's ambition knows no bounds. They're not content being the index provider, the risk analytics firm, the ESG rater, the governance advisor. They want to be the central nervous system of global finance, the entity through which all investment information flows. Every acquisition adds another node to the network, another reason clients can't leave, another moat around the castle.

The China A-shares saga continues to evolve. After the initial inclusion, MSCI conducted further consultations and announced in February 2019 it would increase the inclusion ratio to 20% and include mid-cap China A shares. By 2020, China and China A shares represented about 41% and 5.1% of the MSCI EM Index, respectively. The tail was starting to wag the dog—emerging markets investing was becoming Chinese investing with some other countries thrown in.

The ESG explosion has created its own controversies. How do you measure "social impact"? Who decides what's "sustainable"? MSCI's answer: we'll measure everything and let clients decide. It's the index philosophy applied to values—don't judge, just calculate. They now maintain over 1,500 ESG indices, each one a different flavor of virtue, each one generating subscription fees regardless of whether it saves the planet.

The modern MSCI is unrecognizable from the quiet division inside Morgan Stanley. It's a data empire, a calculation machine, a standard-setter that operates above governments and below markets. They don't make the rules, but they keep score in a game where the score determines everything. In a world drowning in information, they're not selling data—they're selling clarity, consensus, and most importantly, the comfort of following the crowd.

IX. Competitive Dynamics & Market Position

The index provider oligopoly operates like a three-body problem in physics—MSCI, S&P Dow Jones Indices, and FTSE Russell orbit each other in a complex dance where every move affects the others' trajectories. Together, they control roughly 90% of the global index market, a concentration that would make antitrust lawyers salivate if anyone could figure out exactly what market they're monopolizing. After all, they're just providing calculations—it's not their fault everyone uses them.

S&P Dow Jones Indices holds the crown jewel: the S&P 500, the most tracked index on Earth with over $15 trillion benchmarked to it. But outside the United States, they're playing catch-up. FTSE Russell, owned by the London Stock Exchange Group, dominates UK indices and has carved out a strong position in fixed income. But in international equities—the fastest-growing segment as passive investing goes global—MSCI reigns supreme. Their EAFE and Emerging Markets indices are to international investing what the S&P 500 is to U.S. equities: the unquestioned standard.

The BlackRock relationship deserves its own business school case study. Approximately 10% of MSCI's revenue flows from the asset management giant, primarily through iShares ETFs that track MSCI indices. It's a symbiotic relationship that borders on codependence. BlackRock needs MSCI's indices to run their passive funds; MSCI needs BlackRock's scale to maintain index dominance. They're like two heavyweight boxers in a clinch—neither can throw a punch without letting go, and neither wants to let go first.

But this concentration is also MSCI's Achilles heel. If BlackRock ever decided to self-index—create their own benchmarks for their own funds—it wouldn't just hurt MSCI's revenues; it would question the entire third-party index model. Why should BlackRock pay MSCI hundreds of millions annually for calculations they could do themselves? The answer, for now, is network effects: investors trust independent indices more than self-created ones. But "for now" is doing a lot of work in that sentence.

The moats around MSCI's castle are impressive but not impregnable. First, there's methodology—decades of decisions about how to weight, when to rebalance, which countries belong where. Changing providers means changing history, making performance comparisons impossible. Second, there's data—historical index levels that can't be retroactively created by competitors. Third, there's regulatory blessing—MSCI indices are written into countless investment mandates, prospectuses, and regulations. Fourth, there's the ecosystem—thousands of derivatives, ETFs, and futures contracts based on MSCI indices.

But moats can be drained. The index fee compression question looms large. Vanguard has pushed expense ratios on index funds toward zero; at some point, they'll push index licensing fees the same direction. MSCI argues their fees are tiny relative to assets managed—basis points on basis points—but that argument works until it doesn't. When you're managing trillions, even basis points add up to real money.

The technology disruption threat is more subtle but potentially more dangerous. What happens when AI can create personalized indices for every investor? When blockchain enables decentralized index calculation? When quantum computing makes real-time global portfolio optimization possible? MSCI's response has been to embrace technology rather than fight it—but embracing the thing that might destroy you is a dangerous hug.

Direct indexing represents another competitive vector. Instead of buying an ETF that tracks an index, investors increasingly buy the individual stocks directly, customized to their preferences. This trend bypasses traditional indices entirely. MSCI has responded by licensing their data to direct indexing platforms, essentially selling arms to both sides of the war. It's clever, but it's also an admission that the traditional index model faces challenges.

The self-indexing trend among large asset managers is accelerating. Dimensional Fund Advisors has always used proprietary indices. Now others are following. The argument is compelling: why pay external providers for something you can do yourself? MSCI's counter: independence, credibility, and the impossibility of replicating decades of methodology decisions. But every manager that self-indexes is one less customer, one less validation of the third-party model.

New entrants keep trying to crack the oligopoly. Solactive, a German firm, offers indices at a fraction of traditional prices. CRSP provides academic-quality indices through the University of Chicago. But they're fighting network effects with pricing, bringing a knife to a nuclear war. The problem isn't creating indices—any competent team with Excel can do that. The problem is convincing the entire investment ecosystem to use them.

The regulatory scrutiny is intensifying globally. The European Securities and Markets Authority worries about benchmark manipulation. The SEC questions index inclusion decisions. Asian regulators want local alternatives. But regulation is a double-edged sword for MSCI. While it increases compliance costs, it also raises barriers to entry. Every new rule makes it harder for upstarts to compete, essentially protecting the incumbents it's meant to constrain.

The competitive dynamics ultimately favor the incumbent with the most embedded position, and that's MSCI in international equities. They're not competing on product features—all indices fundamentally do the same thing. They're competing on network effects, switching costs, and the power of precedent. In this game, being first matters more than being best, and being standard matters more than being innovative. MSCI understood this before their competitors, and that understanding has made all the difference.

X. Playbook: Business & Investing Lessons

The power of standards in business cannot be overstated, and MSCI's trajectory offers a masterclass in becoming the default. They didn't invent index investing, didn't create the best methodology, didn't have the most resources. They simply became the standard for international equity measurement at the right moment, then leveraged that position relentlessly. It's the QWERTY keyboard of finance—not optimal, but so embedded that optimality doesn't matter.

Consider the infrastructure business model that MSCI has perfected. High fixed costs to build and maintain the indices—hiring quants, gathering data, running calculations, managing methodologies. Near-zero marginal costs to serve additional clients—the same index that serves one fund can serve thousands. It's the economic equivalent of building a bridge: expensive to construct, cheap to cross, impossible to replicate once everyone's using it. The unit economics are so favorable they seem almost unfair: 70%+ EBITDA margins in the index business, scaling that would make software companies jealous.

The paradox of passive investing creates a delicious irony at the heart of MSCI's model. The more passive the investment industry becomes, the more valuable the index provider gets. Every dollar that flows from active to passive management increases MSCI's importance. They're selling shovels in a gold rush, except the gold rush never ends and the shovels wear out so slowly they're essentially permanent. Passive investing was supposed to commoditize investment management; instead, it concentrated power in the hands of index providers.

MSCI's capital allocation strategy demonstrates textbook financial engineering. Since 2014, they've reduced share count by 3.64% annually through buybacks. When your business generates massive cash flows with minimal reinvestment needs, returning capital to shareholders isn't just prudent—it's mathematically optimal. Every share retired increases the value of remaining shares, creating a second compounding machine alongside the business model. It's like they're running two wealth-creation algorithms simultaneously.

Building switching costs through integration, not contracts, shows sophisticated competitive thinking. MSCI doesn't lock clients into 10-year agreements or impose massive termination fees. Instead, they make themselves so embedded in daily workflows that leaving becomes operationally impossible. Index data feeds into risk models, which feed into performance attribution, which feeds into client reporting. It's not one hook—it's thousands of tiny barbs that collectively make extraction excruciating.

The compound effect of data reveals itself beautifully in MSCI's business. Today's index calculation becomes tomorrow's historical benchmark. This year's methodology becomes next decade's performance comparison baseline. Every day that passes makes MSCI's data more valuable because it can't be recreated retroactively. Time is their manufacturing process, history their product. Competitors can match features but can't manufacture history.

The lesson about network effects in B2B markets challenges conventional wisdom. We typically associate network effects with consumer platforms—Facebook, Uber, Airbnb. But MSCI demonstrates that B2B network effects, while slower to build, can be even more powerful. When your customers are institutions with multi-year decision cycles and switching costs measured in millions, every node added to the network is essentially permanent.

The vertical integration strategy—indices to risk to governance—shows the power of controlling the full stack. MSCI doesn't just provide one tool; they provide the entire toolkit. It's like owning not just the hammer but also the nails, the level, the measuring tape, and the blueprint. Clients might start with one product, but workflow integration naturally pulls them into others. The cross-selling isn't aggressive; it's inevitable.

The pricing power that comes from being a standard deserves special attention. MSCI raises prices 3-5% annually, like clockwork. No negotiation, no justification, just inflation plus a bit more. Clients grumble but pay because the alternative—switching providers—would cost far more than accepting the increase. It's pricing power that Warren Buffett dreams about: the ability to raise prices without losing customers or volume.

The regulatory moat phenomenon turns conventional strategy on its head. Usually, regulation is a burden, a cost, a constraint. For MSCI, it's a competitive advantage. Every new rule about benchmark administration, every requirement for index governance, every compliance mandate raises the bar for potential competitors. MSCI can afford armies of compliance officers; startups can't. Regulation intended to constrain them instead protects them.

The platform economics at play demonstrate how modern monopolies form. MSCI doesn't prevent anyone from creating indices—that would be illegal. They just make it economically irrational to use anything else. Why would an ETF provider use an unknown index when MSCI's are recognized globally? Why would an asset manager report against a different benchmark when consultants expect MSCI? The monopoly isn't legal or technical—it's economic and social.

The ultimate lesson from MSCI's playbook: in the information age, the most valuable businesses don't produce information—they organize it, standardize it, and make it impossible to imagine a world without their particular organization of it. MSCI doesn't generate any actual data about securities; they just decide how to count them. But in a world drowning in data, the counter becomes more valuable than the counted. They've built a fortune on being the referee in a game where everyone else is playing.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Riding the Passive Tsunami

The secular growth in passive investing isn't just continuing—it's accelerating. Every year, active managers underperform their benchmarks. Every year, investors respond by moving money to index funds. Every year, MSCI's moat gets wider. We're perhaps only in the third inning of a nine-inning game. In the U.S., passive owns about 60% of equity fund assets. Globally? Less than 30%. The catch-up trade alone could double MSCI's addressable market.

The numbers from recent quarters tell a story of unstoppable momentum. Record recurring sales in the Index segment. Asset-based fees growing at 15% annually as markets rise and passive allocations increase. The mathematics are beautiful: when markets go up 10% and passive takes 5% share from active, MSCI's asset-based fees compound at 15%+. It's leveraged exposure to both beta and structural shift without any of the risk.

Operating leverage continues to expand margins to levels that seem almost fictional. The index business is hitting 76%+ EBITDA margins. Every incremental dollar of revenue drops 80-90 cents to the bottom line. As the business scales, these margins could push even higher. We might be looking at 80% EBITDA margins in the index business by 2030. At that point, MSCI becomes less a business and more a money-printing algorithm.

The private markets opportunity remains in its infancy. Private equity, private debt, real estate, infrastructure—these markets dwarf public equities but remain largely unindexed. MSCI's acquisitions position them to bring standardization to chaos. If they can capture even 10% of the private markets analytics opportunity, it's another billion in high-margin recurring revenue. The Burgiss acquisition alone could prove worth multiples of what they paid.

ESG is becoming non-optional for institutional investors. European regulations require sustainability disclosures. U.S. institutions face pressure from stakeholders. Asian sovereign wealth funds are incorporating climate risk. MSCI sits at the center of this transformation, providing the data everyone needs but nobody wants to create. ESG revenues are growing 30%+ annually with no sign of slowing.

The network effects only strengthen with time. Every new ETF launched on an MSCI index, every derivative contract created, every performance report generated adds another strand to the web. At this point, unwinding MSCI from the global financial system would be like trying to remove flour from baked bread. It's not just difficult—it's definitionally impossible.

The Bear Case: The Empire's Vulnerabilities

Regulatory scrutiny is moving from academic concern to active intervention. European regulators are increasingly uncomfortable with three firms controlling global index provision. The systemic risk arguments are compelling: if MSCI's methodology is wrong, everyone's wrong together. We could see forced standardization, price controls, or mandated competition. The regulatory capture that protected them could become the regulation that constrains them.

Fee compression remains the sword of Damocles hanging over the industry. Vanguard and BlackRock have pushed ETF fees to near zero. Eventually, they'll demand the same from index providers. MSCI argues their fees are minimal relative to AUM, but that argument assumes AUM keeps growing. In a bear market with net outflows, the fee pressure conversation changes dramatically.

China exposure represents a geopolitical wild card. With China representing about 41% of the MSCI Emerging Markets Index, any significant escalation in U.S.-China tensions could force impossible choices. Imagine if MSCI had to remove all Chinese companies from their indices—the rebalancing alone would cause market chaos. They're caught between competing regulatory regimes with no good options.

Technology disruption looms in various forms. AI could democratize index construction, making MSCI's methodology expertise less valuable. Blockchain could enable decentralized, transparent index calculation without central providers. Direct indexing could bypass traditional indices entirely. MSCI is responding to these threats, but responding to disruption and preventing it are very different things.

Market structure changes could undermine the entire model. If active management stages a comeback—unlikely but not impossible—demand for indices decreases. If markets fragment along national lines, global indices become less relevant. If cryptocurrencies actually become a significant asset class, traditional equity indices matter less. These are tail risks, but tails sometimes wag dogs.

Customer concentration remains uncomfortable. BlackRock at ~10% of revenues has leverage. If they decided to self-index, or demanded dramatic fee reductions, MSCI would face difficult choices. The symbiotic relationship works until it doesn't. History is littered with suppliers who thought they were partners until their biggest customer became a competitor.

The valuation multiple assumes perfection. At current valuations, MSCI trades at premiums that imply continued growth, margin expansion, and no disruption. Any disappointment—a quarter of missed earnings, a lost client, a regulatory setback—could trigger multiple compression. When you're priced for perfection, perfect better be what you deliver.

Competition, while currently ineffective, keeps trying. Solactive offers indices at 90% discounts. Major asset managers are building internal capabilities. Technology firms are eyeing the space. One breakthrough—a new model, a regulatory change, a technology shift—could crack the oligopoly. Mountain climbers know: the tallest peaks are the most exposed to lightning.

The Verdict

The bull case rests on momentum, structural trends, and network effects that seem unassailable. The bear case requires disruption, regulation, or market structure changes that seem unlikely. As long as passive investing grows, markets remain global, and institutions need standardized benchmarks, MSCI's position appears secure. But that's what they said about Dow Jones when it dominated financial information, about Moody's before 2008, about many infrastructure providers before disruption arrived.

The truth likely lies between extremes. MSCI will probably continue growing, continue raising prices, continue expanding margins—but at moderating rates. The easy gains from passive growth are captured; future growth requires execution in private markets, ESG, and emerging segments. The moat remains wide but not widening at the same rate. It's a great business becoming a very good business, which at the right price remains an attractive investment, but at the wrong price becomes a value trap.

XII. Epilogue & "If We Were CEOs"

If we were sitting in Henry Fernandez's corner office, looking out at Manhattan's skyline, what would keep us up at night? Not competition from S&P or FTSE—that game is largely decided. Not regulatory scrutiny—that's manageable with enough lawyers. The real question would be: what comes after indices?

The next frontier is obviously real-time everything. Markets don't close anymore—crypto trades 24/7, private markets are becoming liquid, global portfolios never sleep. Yet MSCI still calculates most indices once a day. Imagine indices that update every millisecond, that incorporate alternative data, that adjust for news sentiment in real-time. The technical challenges are substantial, but the first mover advantage could be enormous.

Personalized benchmarks represent another untapped opportunity. Every institutional investor claims they're different, yet they all use the same indices. What if MSCI could mass-customize benchmarks? Use AI to create indices tailored to specific risk tolerances, ESG preferences, geographic exposures? It's mass production meeting mass customization—Henry Ford meets Savile Row.

The private markets opportunity deserves more aggression. Public equity indices are a mature business; private market indices are barely embryonic. If we were CEO, we'd be acquiring aggressively—every private market data provider, every GP reporting system, every LP analytics platform. The goal: make MSCI as essential to private markets as they are to public ones. The Burgiss acquisition was a start, not an ending.

Geographic expansion feels underleveraged. MSCI dominates developed and emerging markets, but what about frontier markets? What about city-level indices for real estate? What about regional indices for private businesses? The world is becoming more granular; indices should follow. Every geography that industrializes, every market that opens, every asset class that institutionalizes needs indices.

The build versus buy decision would tilt heavily toward buying. At MSCI's valuation multiples, using stock as currency makes sense. Every acquisition that adds recurring revenue, increases switching costs, or extends the moat is accretive. The integration risk is real, but the strategic risk of not moving fast enough is greater.

On the product side, the focus would be on making indices smarter, not just broader. Incorporate machine learning to predict index changes. Use natural language processing to analyze company disclosures. Apply network theory to understand systemic risks. The indices of 2035 should make today's look like slide rules compared to smartphones.

The China question requires strategic clarity. Either MSCI is a truly global provider, in which case they need to navigate geopolitical tensions while serving all markets, or they're a Western provider with global aspirations, in which case they should optimize for Western regulatory approval. Trying to be both risks being neither.

The technology infrastructure needs modernization. MSCI runs on systems built over decades, layers of code archaeological sites. A ground-up rebuild using modern architecture—cloud-native, API-first, real-time capable—would be expensive but necessary. The goal: make MSCI's technology as defensible as their methodologies.

Partnership strategies could unlock value. Why compete with every asset manager when you could white-label index creation capabilities? Why fight with data providers when you could create an ecosystem? MSCI could be the iOS of financial data—a platform others build upon rather than a provider others compete against.

The ultimate vision would be MSCI as the "AWS of Finance"—not just providing indices, but providing the entire infrastructure layer for global investing. Indices, risk models, ESG data, governance analytics, performance attribution, regulatory reporting—everything except the actual investment decision. Every financial institution would build on MSCI's platform the way every startup builds on AWS.

The capital allocation philosophy would remain boringly brilliant: generate massive cash flows, reinvest what's needed for growth, return the rest to shareholders. No empire building, no conglomerate dreams, no venture investing. Just compound capital at high rates of return for decades.

The cultural challenge would be maintaining innovation while preserving reliability. MSCI's clients don't want disruption—they want evolution. Too much change risks the franchise; too little risks irrelevance. It's like renovating a cathedral while services continue—possible, but requiring extreme care.

Looking ahead, MSCI's destiny seems clear: they'll either become the unquestioned infrastructure layer for all investment decisions, or they'll be disrupted by someone who builds that layer better. There's no middle ground in platform businesses. Winner takes most, if not all.

The next decade will determine whether MSCI joins the ranks of truly generational companies—the Microsofts and Visas that become so embedded they're essentially permanent—or whether they're another financial services firm that dominated their era before technology or regulation changed the game. If we were betting, we'd bet on permanence. But then again, that's what everyone said about Dow Jones, and now they're a division of News Corp. In business, as in indexing, past performance doesn't guarantee future results.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube