Merck & Co.: From German Roots to Global Pharma Giant

I. Introduction & Episode Roadmap

Picture this: A pharmaceutical company generates $29.5 billion from a single drug in 2024—nearly half its total revenue. That drug, Keytruda, has saved countless lives, revolutionized cancer treatment, and become the most valuable asset in modern pharma. But here's the twist: in just four years, this golden goose loses patent protection, potentially wiping out tens of billions in market value overnight.

This is Merck & Co. today—a 130-year-old pharmaceutical powerhouse standing at the most precarious moment in its history. The company that gave us streptomycin for tuberculosis, the first measles vaccine, and breakthrough treatments for HIV now faces an existential question: What happens when your miracle drug becomes everyone's drug?

The tension couldn't be more palpable. On one side, Merck continues to dominate oncology, with Keytruda approved for over 40 cancer indications and still growing. On the other, biosimilar manufacturers circle like vultures, waiting for 2028 when they can feast on what analysts estimate could be a 30-60% revenue decline within three years of patent expiry. The company has filed 129 patent applications on Keytruda—more than half after initial FDA approval—in a desperate bid to extend its monopoly. Critics like Senator Elizabeth Warren call it patent abuse; Merck calls it innovation protection.

But to understand how Merck got here—perched between triumph and potential catastrophe—we need to travel back to 19th century Germany, through two world wars, past one of pharma's greatest scandals, and into the boardrooms where billion-dollar bets on science are made daily. This is a story of German precision meeting American ambition, of scientific breakthroughs shadowed by ethical failures, and ultimately, of a company racing against time to reinvent itself before the clock strikes midnight on its most important asset.

Our journey spans continents and centuries: from Friedrich Jacob Merck's pharmacy in Darmstadt to Manhattan's financial district, from wartime seizures to peacetime mergers, from the Vioxx disaster that nearly destroyed the company to the Keytruda miracle that saved it. Along the way, we'll dissect the playbook of modern pharma—how blockbusters are born, how patents are weaponized, and how companies navigate the razor's edge between profit and public health.

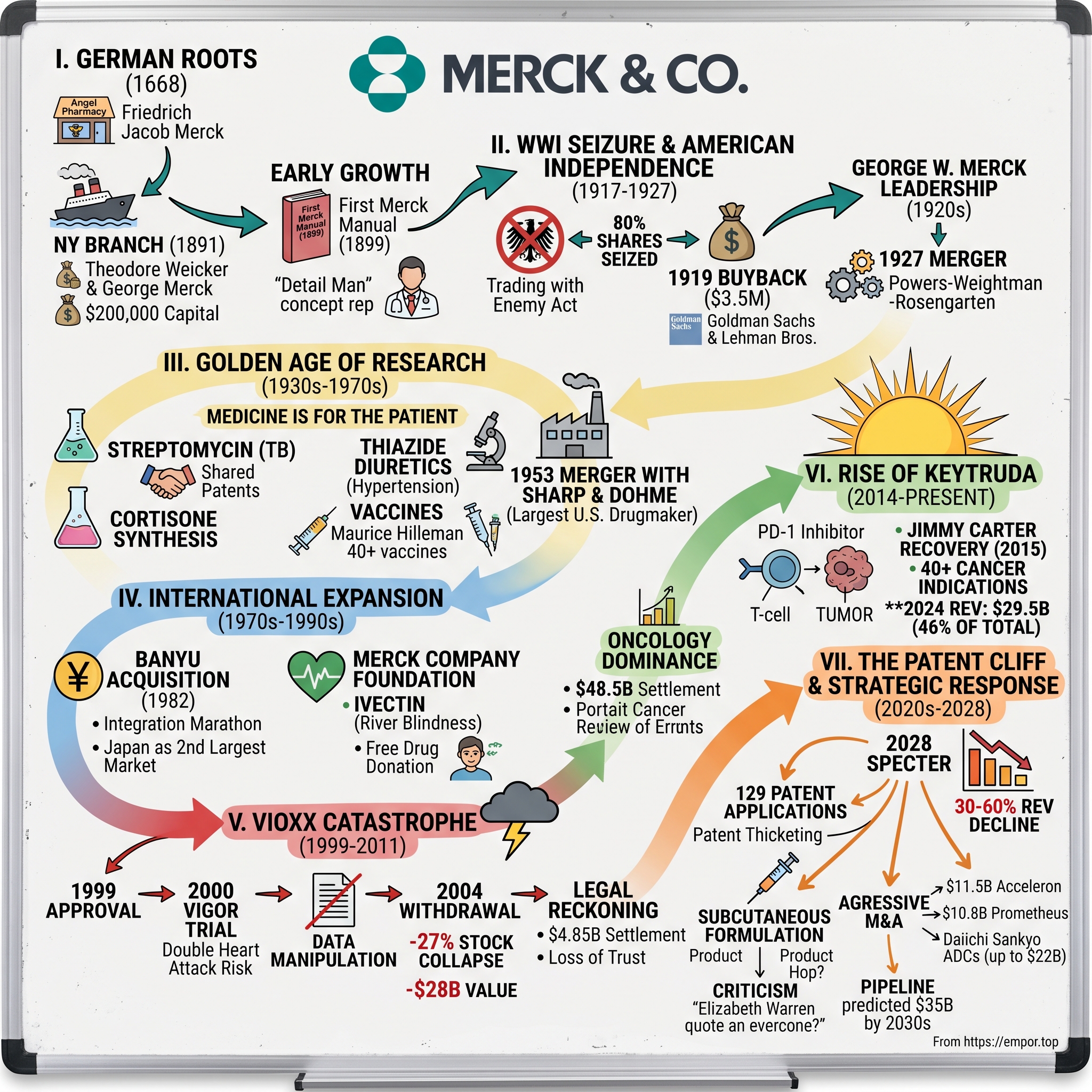

II. German Origins & The American Branch (1668–1917)

The year is 1887. Theodore Weicker, a sharp-eyed German businessman, steps off a steamship onto New York's bustling docks. His mission: establish an American beachhead for E. Merck of Darmstadt, the German chemical and pharmaceutical dynasty that traced its roots back to Friedrich Jacob Merck's Angel Pharmacy in 1668. Weicker surveyed the American market—a nation industrializing at breakneck speed, hungry for the fine chemicals and pharmaceutical ingredients that German companies had perfected. Four years later, on January 1, 1891, he would transform that reconnaissance mission into Merck & Co., headquartered in lower Manhattan with $200,000 in capital from the German parent company.

But Weicker didn't come alone in building this American venture. George Merck, the 23-year-old grandson of the company's German founder, joined him in New York—a decision that would prove fateful when world events forced the company to choose between its German heritage and American future. Young George brought more than just the family name; he carried the scientific rigor and pharmaceutical expertise that had made Merck synonymous with quality in European medical circles.

From 1891 to 1917, Merck & Co. operated as the archetypal subsidiary—importing German-made alkaloids, morphine, and cocaine (then a legitimate pharmaceutical) while building distribution networks across New York and neighboring states. The company occupied a unique niche: translator between German pharmaceutical innovation and American medical practice. This wasn't just importing and reselling; Merck & Co. provided critical education to American physicians unfamiliar with these new compounds, establishing itself as both supplier and trusted advisor.

The publication of the first Merck Manual in 1899 exemplified this educational mission. What started as a slim reference guide for physicians—listing diseases, their recommended treatments, and Merck products that could help—would evolve into one of medicine's most authoritative references. That first edition, just 192 pages, represented something revolutionary: a pharmaceutical company taking responsibility for physician education, not just product promotion. It listed treatments for everything from "melancholia" (depression) to tuberculosis, establishing Merck as a scientific authority, not merely a merchant.

During these early decades, the company built its American identity gradually, almost imperceptibly. The Merck name on bottles and packages carried German prestige, but the sales force spoke American English, understood American medical practice, and navigated American business culture. They established quality control laboratories in New York, ensuring that products met American standards—often more stringent than European ones for certain compounds. By 1914, when George W. Merck officially began his career at the company, Merck & Co. had grown from an import house to a legitimate American pharmaceutical enterprise, though still tethered to its German parent.

The distribution networks they built during this period would prove crucial. Unlike competitors who relied on third-party distributors, Merck established direct relationships with hospitals, pharmacies, and physicians throughout the Northeast. They pioneered the "detail man" approach—pharmaceutical representatives who weren't just salesmen but educated liaisons who could discuss pharmacology, dosing, and clinical applications with doctors. This investment in relationship-building and education created loyalty that would survive the tumultuous separation from Germany that loomed ahead.

What made Merck different from other German subsidiaries operating in America was this commitment to becoming genuinely embedded in American medical practice. While others simply sold products, Merck invested in understanding American disease patterns, prescribing habits, and regulatory requirements. They began formulating products specifically for American preferences—tablets instead of powders, standardized doses instead of bulk compounds. This Americanization happened slowly, almost unconsciously, preparing the company for a forced independence none could have predicted as Europe marched toward war.

III. WWI Seizure & American Independence (1917–1927)

April 6, 1917. Congress declares war on Germany. Within hours, federal agents descended on Merck & Co.'s Manhattan offices. Under the Trading with the Enemy Act, the U.S. government seized 80% of the company's shares—a stunning reversal for a business that had operated peacefully in America for 26 years. George Merck, now 49 and deeply Americanized after decades in New York, watched his family's company slip into government control. The Alien Property Custodian didn't just freeze assets; they prepared to auction off one of America's most sophisticated pharmaceutical operations to the highest bidder.

The irony was bitter. George Merck had spent years building an American company, hiring American workers, serving American patients. His son, George W. Merck, was as American as any Harvard man (class of 1915). Yet overnight, they became enemy aliens, their life's work subject to expropriation. The government installed supervisors in the offices, reviewed every transaction, and treated the Mercks with the suspicion reserved for potential saboteurs.

But George Merck possessed something invaluable: relationships on Wall Street. In 1919, as the government prepared to permanently sever Merck & Co. from its German parent, he orchestrated one of the era's most audacious buybacks. Partnering with Goldman Sachs and Lehman Brothers—firms that saw opportunity where others saw stigma—George Merck repurchased his company for $3.5 million. The price was steep (roughly $60 million in today's dollars), but it bought something priceless: true independence.

The deal structure revealed the delicate balance George had to strike. Goldman and Lehman provided capital and credibility, washing away the German taint with American financial respectability. But George retained operational control and the Merck name—a remarkable achievement given the anti-German sentiment sweeping America. German-Americans were changing their names, abandoning their language, desperately trying to blend in. George Merck did the opposite: he kept the name but transformed its meaning from German excellence to American innovation.

This transformation accelerated when George W. Merck, the Harvard-educated son, assumed leadership in the 1920s. Where his father had been a bridge between two worlds, George W. was purely American in outlook and ambition. He didn't just want to distribute pharmaceuticals; he wanted to discover them. In 1927, he engineered a merger with Powers-Weightman-Rosengarten Company, a Philadelphia chemical manufacturer with deep American roots dating to 1818. This wasn't just expansion—it was cultural grafting, binding Merck to American industrial heritage.

The younger Merck's vision went beyond business integration. He began recruiting American scientists, establishing research facilities, and most importantly, shifting the company's identity from importer to innovator. The Rahway, New Jersey facility—which would become Merck's research heart—started taking shape during this period. George W. understood that true independence meant scientific independence. As long as Merck relied on European discoveries, it would remain intellectually colonized regardless of ownership structure.

The severance from Germany, traumatic as it was, freed Merck & Co. to become something the German parent never could have imagined: a research-driven pharmaceutical company with American pragmatism and German precision. The forced independence became voluntary excellence. By 1927, when the merger with Powers-Weightman-Rosengarten completed, Merck & Co. wasn't just legally American—it had developed its own scientific culture, distinct from both German academicism and American commercialism.

Looking back, the Trading with the Enemy Act did Merck an inadvertent favor. Had the company remained a German subsidiary, it would have faced the same fate during World War II, possibly with permanent consequences. Instead, the 1917 seizure and 1919 buyback created a genuinely American company just as the U.S. was emerging as a scientific superpower. The Mercks paid $3.5 million for their freedom, but they gained something invaluable: the ability to chart their own scientific destiny in the country that would dominate 20th-century pharmaceutical innovation.

IV. The Golden Age of Research (1930s–1970s)

The Merck Research Laboratory in Rahway, New Jersey, 1933. In a modest brick building that once housed chemical production, George W. Merck gathered his first team of research scientists. "Medicine is for the patient," he would tell them, in what became Merck's defining philosophy. "It is not for the profits. The profits follow, and if we have remembered that, they have never failed to appear." This wasn't corporate PR speak—Merck would literally give away streptomycin patents to ensure wider tuberculosis treatment, a decision that would have been unthinkable at most pharmaceutical companies.

The Rahway labs became a magnet for scientific talent fleeing European turmoil. Max Tishler, who would lead Merck research for decades, brought a combination of academic rigor and industrial pragmatism that defined the company's approach. Unlike university labs focused on publication, or competitor labs focused on me-too drugs, Merck pursued what others considered impossible: synthesizing complex natural products like cortisone, developing entirely new drug classes like thiazide diuretics, and tackling diseases others had abandoned.

The streptomycin story exemplified Merck's unique position in American science. When Selman Waksman at Rutgers discovered the antibiotic in 1943, Merck had already been funding his soil microbe research for years—a bet on basic science with no guaranteed return. When streptomycin proved effective against tuberculosis, Merck faced a choice: monopolize production for massive profits or share knowledge to maximize lives saved. They chose the latter, publishing production methods and helping other manufacturers scale up. The decision cost them exclusive rights worth hundreds of millions but earned something more valuable: moral authority in American medicine.

By 1953, that authority translated into market power through the merger with Sharp & Dohme, making Merck the largest U.S. drugmaker. Sharp & Dohme brought commercial infrastructure—a nationwide sales force, established hospital relationships, international distribution—that complemented Merck's research prowess. The Philadelphia company had acquired H.K. Mulford Company in 1929, adding vaccine capabilities that would prove crucial. The combined entity kept the Merck trade name in North America but adopted MSD (Merck Sharp & Dohme) internationally, a practical solution to trademark conflicts with the German Merck.

The 1950s breakthroughs in thiazide diuretics showcased how Merck's research philosophy differed from competitors. While others searched for antibiotics (the hot field post-penicillin), Merck scientists pursued the unglamorous problem of hypertension. The development of chlorothiazide required understanding kidney physiology, sodium transport, and cardiovascular dynamics—complex science with uncertain commercial potential. When the drug launched, it transformed hypertension from an untreatable death sentence to a manageable condition. The Lasker Foundation's 1975 special Public Health Award recognized not just the drug but the research approach: pursuing medical need over market opportunity.

The vaccine developments of the 1960s—first measles vaccine in 1963, mumps in 1967—demonstrated Merck's evolution from chemical to biological innovation. Maurice Hilleman, who joined Merck in 1957, would develop over 40 vaccines during his career, saving more lives than perhaps any scientist in history. His work culture was legendary: 16-hour days, demanding perfection, but also fostering creativity and risk-taking. When his daughter Jeryl Lynn came down with mumps in 1963, Hilleman swabbed her throat, drove the sample to his Merck lab, and developed the vaccine strain still used today—the "Jeryl Lynn strain."

This period established patterns that would define Merck for decades: massive R&D investment (consistently among the industry's highest as percentage of sales), focus on primary research rather than licensing, and willingness to tackle complex diseases others avoided. The company built research campuses that resembled universities more than factories, recruited Nobel laureates as consultants, and gave scientists unusual autonomy. The approach was expensive and risky—many projects failed—but the successes were transformative.

By the 1970s, Merck had become what George W. Merck envisioned: a company where scientific excellence drove commercial success, not vice versa. The research culture attracted talent that might otherwise have chosen academia: Roy Vagelos, who would become CEO, came from Washington University; Edward Scolnick, future research chief, from the National Cancer Institute. These weren't just managers who happened to work in pharma; they were scientists who understood that Merck's resources could accelerate discovery beyond what any university could achieve.

The golden age created expectations that would both inspire and burden future generations. When you've cured tuberculosis, prevented measles, and controlled hypertension, anything less than medical revolution seems like failure. This pressure for breakthrough innovation would drive spectacular successes but also, as we'll see with Vioxx, spectacular failures when the pursuit of blockbusters overwhelmed scientific caution.

V. International Expansion & Japanese Adventures (1970s–1990s)

Tokyo, 1982. Merck executives sat across from their counterparts at Banyu Pharmaceutical, finalizing a $315.5 million acquisition that would reshape both companies. The Americans saw Japan as the world's second-largest pharmaceutical market, tantalizingly closed to foreign competitors. The Japanese saw survival through partnership with Western innovation. What neither fully grasped was how profoundly different their business cultures were—differences that would turn this acquisition into a 20-year integration marathon.

The relationship actually began in 1954, when Merck and Banyu formed a joint venture—one of the first between American and Japanese pharmaceutical companies. For nearly three decades, this partnership operated smoothly, with Banyu distributing Merck products in Japan while maintaining its independence. But by 1982, the dynamics had shifted. Japan's pharmaceutical market was exploding, regulations were slowly opening to foreign companies, and Merck needed more than a distribution partner—it needed a platform for Asian expansion.

The incorporation in New Jersey in 1970 had prepared Merck structurally for global expansion, creating the legal framework for international subsidiaries and acquisitions. But Japan was different from European markets where Merck already operated. The regulatory system required extensive local clinical trials, even for drugs approved elsewhere. The medical practice emphasized combination therapies over single blockbusters. The business culture prioritized consensus over speed, relationships over transactions.

Merck's purchase of majority control in Banyu revealed these tensions immediately. American managers arrived in Tokyo expecting to implement Merck's research-driven model: focus on innovation, reduce me-too products, invest heavily in R&D. Japanese managers politely resisted, explaining that success in Japan required different strategies: maintaining broad product portfolios, nurturing physician relationships over generations, respecting the intricate hierarchy of Japanese medical institutions.

The integration challenges went beyond business strategy. At Banyu's facilities, American efficiency experts recommended reducing staff, streamlining operations, focusing resources on high-margin products. The Japanese managers explained this would destroy wa (harmony) and make the company unemployable for top talent. When Merck pushed for performance-based compensation, Banyu leaders noted this would violate Japanese employment norms and trigger regulatory scrutiny.

Yet slowly, over years of patient negotiation, a hybrid model emerged. Banyu maintained its Japanese character while adopting Merck's scientific rigor. The company became a bridge for Merck products entering Asia, conducting the local trials and regulatory navigation that purely American operations never could have managed. By the late 1980s, Banyu was generating substantial profits, validating the acquisition price that many had considered excessive.

The Japanese adventure taught Merck crucial lessons about global expansion. Unlike in Europe, where American methods could be imported wholesale, Asia required true localization—not just translation but transformation. The company learned to operate in markets where government pricing controls limited margins, where patent protection was weaker, where medical practice diverged from Western standards.

During this same period, Merck established the Merck Company Foundation with an initial $500,000 contribution. While modest compared to the Banyu acquisition, the foundation represented another form of international expansion—soft power through pharmaceutical philanthropy. Over the following decades, it would contribute hundreds of millions to global health initiatives, particularly in developing countries where commercial operations weren't viable.

The foundation's work in river blindness (onchocerciasis) exemplified this approach. When Merck developed ivermectin (Mectizan) in the 1980s, they discovered it could cure river blindness, a disease affecting millions in Africa and Latin America who could never afford treatment. Rather than ignore this unprofitable market, Merck committed to donate the drug free "for as long as needed." The program has since treated over 300 million people annually, eliminating river blindness from several countries.

This combination of commercial expansion through acquisitions like Banyu and humanitarian expansion through the foundation created a unique global presence. Merck wasn't just selling drugs internationally; it was building scientific infrastructure, transferring technology, and addressing health disparities. The approach was expensive and complex but created reservoirs of goodwill that would prove valuable when the company faced its darkest hour with Vioxx.

By the 1990s, Merck operated as a truly global enterprise—not just in sales but in research, manufacturing, and cultural integration. The Banyu acquisition had evolved from a troubled integration to a successful model for Asian operations. The foundation had established Merck's humanitarian credentials. The company seemed poised for unlimited global growth, with the scientific excellence to develop breakthrough drugs and the international infrastructure to deliver them worldwide. No one could have predicted that the next decade would bring a scandal that would threaten everything they had built.

VI. The Vioxx Catastrophe (1999–2011)

May 20, 1999. FDA approval day for Vioxx. Champagne corks popped in Merck's New Jersey headquarters as executives celebrated what they believed would be the company's next blockbuster. The painkiller promised relief without stomach bleeding—a holy grail for millions with arthritis. Marketing projections showed potential sales of $4-5 billion annually. The stock price surged. But in a clinical trial already underway, data was accumulating that would transform this triumph into one of the darkest chapters in pharmaceutical history.

The warning signs emerged with stunning speed. In January 1999, Merck had launched the VIGOR study with 8,000 participants—half taking Vioxx, half taking naproxen, an older painkiller. The study's purpose was to prove Vioxx's superiority in protecting the digestive system. By November 1999, just months after approval, the data showed something alarming: 79 patients taking Vioxx had serious heart problems versus 41 on naproxen. By December, the relative risk was clear—Vioxx patients had twice the heart attack risk.

What happened next would later be dissected in courtrooms, congressional hearings, and medical journals as a case study in corporate malfeasance. Merck scientists, faced with devastating data, performed statistical gymnastics. They argued naproxen decreased heart attack risk by 80%—a protective effect never before seen and biologically implausible—rather than acknowledge that Vioxx increased risk by 400%. Internal emails later revealed scientists knew this explanation was, in one employee's words, "complete bullshit," yet it became the company's official position.

The manipulation went deeper than just interpretation. When the New England Journal of Medicine published the VIGOR trial results, critical data was missing—heart attacks that occurred after an arbitrary cutoff date that made Vioxx look safer. The journal later published a scathing correction, with editors saying they were "hoodwinked." Merck had ghostwritten articles for academics, placing favorable interpretations in medical literature while hiding unfavorable data. The company trained its 3,000-person Vioxx sales force to dodge questions about cardiovascular risk with scripted non-answers.

For five years, as evidence mounted, Merck held the line. They attacked critics, funded favorable research, and spent over $100 million annually on direct-to-consumer advertising featuring Olympic athletes and celebrity endorsements. By 2004, 20 million Americans had taken Vioxx, generating $2.5 billion in annual sales. The drug had become essential to Merck's earnings, its stock price, its image as a premier pharmaceutical company.

September 30, 2004. The APPROVe trial, designed to test Vioxx for colon polyp prevention, showed definitively that the drug raised heart attack risk after 18 months of use. This time, Merck couldn't explain away the results. CEO Raymond Gilmartin announced the immediate worldwide withdrawal of Vioxx. The stock price collapsed 27% in one day, erasing $28 billion in market value. But the financial losses paled compared to the human cost.

Dr. David Graham, an FDA scientist, testified before Congress that Vioxx had caused between 88,000 and 140,000 heart attacks, with 30-40% proving fatal. His estimate of 55,000 premature deaths would make Vioxx one of the deadliest drug disasters in history. Each number represented someone's parent, spouse, child—people who took a painkiller and suffered heart attacks that were, according to Graham, "avoidable" had Merck been honest about the risks.

The legal reckoning was swift and severe. By 2007, Merck faced nearly 30,000 lawsuits. Juries heard evidence of internal emails joking about cardiovascular risks, documents showing data manipulation, testimony from scientists pressured to stay quiet. Some verdicts reached hundreds of millions. Merck ultimately agreed to pay $4.85 billion to settle personal injury claims, then another $950 million to resolve criminal charges and civil claims—including a $321.6 million criminal fine and $628.4 million civil settlement.

But the damage transcended financial settlements. The Vioxx scandal shattered Merck's carefully cultivated image as the ethical pharmaceutical company—the one that gave away streptomycin, donated river blindness medicine, put patients before profits. Employee morale collapsed. Recruitment became difficult as top scientists chose competitors. The company that had stood for scientific integrity became synonymous with corporate greed and deception.

The scandal's impact rippled through the entire pharmaceutical industry. FDA implemented new cardiovascular testing requirements for all drugs. Medical journals strengthened disclosure requirements. Congress held hearings on drug safety and corporate influence. Public trust in pharmaceutical companies, already fragile, eroded further. Every drug approval, every clinical trial, every marketing campaign now faced scrutiny through the lens of Vioxx.

Internally, Merck underwent painful transformation. New leadership implemented stricter safety protocols, enhanced transparency requirements, and reformed sales practices. The company settled into what employees called the "post-Vioxx era"—more cautious, more bureaucratic, less confident. Innovation slowed as risk aversion dominated decision-making. The company that had boldly pursued breakthrough drugs now seemed paralyzed by fear of another scandal.

Yet even as Merck paid billions in settlements and struggled to rebuild trust, scientists in its labs were working on something that would ultimately save the company—an experimental cancer drug that worked through an entirely novel mechanism. As Merck's reputation hit bottom and its pipeline sputtered, this molecule, known internally as MK-3475, was quietly advancing through trials. Soon it would have a different name: Keytruda.

VII. The Rise of Keytruda & Oncology Dominance (2014–Present)

September 4, 2014. The FDA approval letter for pembrolizumab arrived at Merck headquarters. The drug would be marketed as Keytruda, approved initially for advanced melanoma patients who had failed other treatments. The indication was narrow, the patient population small—maybe a few thousand Americans. Merck executives permitted themselves cautious optimism after years of post-Vioxx trauma. None imagined they were holding the approval for what would become the most valuable drug in pharmaceutical history.

The science behind Keytruda represented a paradigm shift in cancer treatment. Instead of poisoning tumors with chemotherapy or targeting specific mutations, Keytruda removed cancer's invisibility cloak. Tumors survive by expressing PD-L1 proteins that tell immune system T-cells "don't attack me, I'm normal tissue." Keytruda blocks this signal, unmasking tumors and unleashing the body's natural defenses. It was elegant, powerful, and unlike anything in oncology's arsenal.

The development journey had been anything but smooth. Merck acquired the molecule from Organon in 2007, part of a $41 billion deal that many considered overpriced. Initially, MK-3475 languished in Merck's pipeline, overshadowed by other priorities. Bristol-Myers Squibb was racing ahead with their competing PD-1 inhibitor, Opdivo, with more resources and earlier trial starts. Merck was playing catch-up in a field they hadn't pioneered.

But Roger Perlmutter, who became Merck's research chief in 2013, recognized Keytruda's potential and made a bold decision: run trials at unprecedented speed and scale. While competitors followed traditional development paths—testing in one cancer type, waiting for results, then expanding—Merck launched simultaneous trials across multiple cancers. They burned through cash at extraordinary rates, spending $46 billion developing Keytruda over a decade with plans for $20 billion more by 2030.

The gamble paid off spectacularly. In 2015, Jimmy Carter announced his metastatic melanoma had disappeared after Keytruda treatment—instant global publicity no marketing campaign could buy. The 91-year-old former president became Keytruda's most powerful advocate, living proof of its transformative potential. Approvals cascaded: lung cancer in 2015, head and neck cancer in 2016, bladder cancer, Hodgkin lymphoma, and gastric cancer in 2017.

What distinguished Keytruda wasn't just clinical success but strategic execution. Merck pioneered biomarker-driven development, identifying patients whose tumors expressed PD-L1 and were most likely to respond. While competitors pursued broad populations with lower response rates, Merck focused on demonstrating dramatic efficacy in targeted groups. The FDA granted Keytruda the first tissue-agnostic approval in cancer history—approved for any tumor with specific genetic markers regardless of location.

The KEYNOTE trial program became the Manhattan Project of clinical development. Over 1,600 trials enrolled hundreds of thousands of patients across 40+ cancer types. Merck tested Keytruda alone, in combinations, as first-line therapy, as adjuvant treatment. Each successful trial expanded the addressable market. Lung cancer alone—where Keytruda became standard of care—represented a $20+ billion opportunity.

By 2024, the numbers defied pharmaceutical precedent: $29.48 billion in annual revenue, 46% of Merck's total sales, prescribed to over 2 million patients globally. Keytruda wasn't just a successful drug; it had become the cornerstone of modern oncology, referenced in treatment guidelines worldwide, essential to cancer center formularies, irreplaceable in countless treatment regimens.

The transformation of Merck paralleled Keytruda's ascent. The company that had diversified across therapeutic areas became an oncology powerhouse. Research investments concentrated on cancer, business development focused on oncology assets, commercial infrastructure optimized for cancer care delivery. Merck's stock price quadrupled from Keytruda's approval to 2024, adding over $200 billion in market capitalization.

But success created its own vulnerabilities. As Keytruda grew to dominate Merck's revenue, concentration risk became undeniable. Analysts began asking uncomfortable questions: What happens when Keytruda loses patent protection? Can lightning strike twice? The same dynamic that saved Merck from post-Vioxx irrelevance now threatened its future—ultimate dependence on a single molecule.

The human impact, however, transcended financial metrics. Keytruda gave terminal patients years of life, transformed cancer from death sentence to chronic disease for some, offered hope where none existed. The drug that emerged from Merck's darkest period had become its greatest contribution to human health, validating George W. Merck's original vision that focusing on patients would make profits follow.

Yet even as Merck celebrated Keytruda's success, patent lawyers were working overtime. The company had filed 129 patent applications on Keytruda, seeking to extend exclusivity through formulation changes, new indications, and manufacturing processes. Critics emerged, led by Senator Elizabeth Warren, arguing Merck was abusing the patent system to maintain monopoly pricing. The battle over Keytruda's future had begun before its peak had even arrived.

VIII. The Patent Cliff & Strategic Response (2020s–2028)

The date haunts Merck's earnings calls like a specter: 2028. That's when Keytruda's primary patent protection expires, opening the floodgates to biosimilar competition. Financial models paint a stark picture—revenue declining 30-60% within three years, earnings per share dropping approximately 6.4%, potentially $100+ billion in market value evaporating. For a drug generating nearly half the company's sales, the patent cliff isn't just a challenge; it's an existential threat that keeps executives awake at night.

Merck's response has been a masterclass in pharmaceutical lifecycle management—or patent manipulation, depending on your perspective. The company has filed 129 patent applications on Keytruda, with more than half submitted after the initial FDA approval. These aren't for the basic molecule but for everything around it: specific dosing regimens, combination therapies, manufacturing processes, formulation tweaks. Each approved patent potentially extends exclusivity, forcing biosimilar manufacturers to navigate an increasingly complex legal minefield.

The subcutaneous formulation strategy exemplifies this approach. Merck is developing an under-the-skin injection version of Keytruda to replace the current intravenous infusion. The science is legitimate—subcutaneous delivery would be more convenient for patients, reduce hospital time, lower healthcare system costs. But the timing is suspect. If approved around 2028, just as the original patent expires, Merck could claim the subcutaneous version is superior and transition patients, maintaining market dominance even as biosimilar IV versions launch. The political scrutiny has intensified. In February 2023, four members of Congress urged the US Patent and Trademark Office to scrutinize Merck's Keytruda patent portfolio, saying its applications appeared to reflect "anti-competitive business practices," such as patent thicketing and product hopping. Senator Elizabeth Warren has become particularly vocal, arguing that Americans will spend at least $137 billion on Keytruda during the extended exclusivity period—money that could be saved with biosimilar competition.

The Senate Judiciary Committee last month approved bipartisan bills targeting product-hopping and other tactics that delay cheaper biosimilars from reaching patients. Supporters say they would rein in drugmakers that exploit the US patent and regulatory systems to stretch monopolies and drive up prices. One, the Drug Competition Enhancement Act, would let antitrust enforcers treat product hopping as anticompetitive conduct. Another, the Affordable Prescriptions for Patients Act, seeks to streamline litigation timing over biologic drugs like Keytruda.

The subcutaneous strategy is particularly controversial. Merck has pitched subcutaneous Keytruda, set for an October US launch, as a patient-centered innovation that could cut treatment time nearly in half. The company says the new version offers comparable safety and effectiveness to the IV formulation, approved in the US for 41 uses across 18 cancer types. It touts the new form, delivered in a two-minute injection every six weeks rather than a 30-minute infusion as often as every three weeks, as improving access and reducing the burden on patients.

But critics see a classic "product hop"—switching patients to a patent-protected version just as cheaper alternatives become available. Merck CEO Rob Davis has given critics ammunition, suggesting the new formulation could buffer competition from biosimilars as the company faces the 2028 expiration of the main patents behind Keytruda's IV version—which provided $17.9 billion in US revenue last year, more than a quarter of Merck's total. He's said the company anticipates the injectable version could capture 30% to 40% of Keytruda's US patient base, turning the looming patent cliff into "more of a hill."

University of California College of the Law, San Francisco, professor Robin Feldman said "How often do you get to see the magic trick unfolding?" referring to Merck's real-time patent strategy. The company isn't hiding its intentions—it's executing them in plain sight, betting that regulatory approval and physician adoption will happen faster than legislative reform or biosimilar development.

The biosimilar manufacturers aren't sitting idle. Sandoz, Samsung Bioepis, Amgen, Celltrion and other biosimilar makers are advancing their own versions of pembrolizumab, the scientific name for Keytruda. These companies have learned from previous biologics battles—they're conducting extensive clinical trials, building manufacturing capacity, and preparing legal strategies to challenge Merck's patent thicket. The financial models tell a sobering story. Analysts estimate Keytruda's sales could peak near $36 billion by 2028 but could fall to $20 billion—or even below $15 billion—within four to five years. According to analyst consensus forecasts, Keytruda sales are forecasted at $27.4 billion in 2029, a decrease of 19% from $33.7 billion in 2028 estimates. The U.S. Keytruda market, valued at $17.87 billion in 2024, faces a projected CAGR decline of -3.12% by 2033 due to patent expiration and biosimilar competition.

Historical precedents offer little comfort. Consider AbbVie's Humira, which lost close to 60% of its revenue in just a few years, from $21 billion in 2022 to under $9 billion last year. Or Roche's Herceptin, which lost U.S. exclusivity in 2019 and saw its sales shrink from $7 billion in 2018 to $3.7 billion in 2020. These weren't just revenue declines—they were corporate earthquakes that forced strategic pivots, workforce reductions, and fundamental reimaginations of business models.

Yet Merck's situation is even more precarious than these precedents suggest. Keytruda now accounts for 46% of the company's total revenue—a level of concentration that raises red flags. In 2024, Keytruda sales grew 18% to $29.5 billion; excluding the impact of foreign exchange, sales grew 22%. The drug's dominance has only increased over time, creating what analysts call a "growth story with an expiration date."

The Inflation Reduction Act adds another layer of complexity. The government price negotiations affecting Keytruda wouldn't take effect until 2028, Merck said in its annual securities filing. That year will also see a key patent loss for the drug. Merck has already had two drugs picked for the yearly list of drugs subject to price negotiations, with a 79% Medicare price cut set to go into effect for its Januvia in 2026. The convergence of biosimilar competition and government price controls creates a perfect storm that could devastate margins.

Merck's response reveals both desperation and determination. Merck is pursuing lifecycle management strategies: Regulatory submissions for a subcutaneous (SC) version of Keytruda, which offers greater patient convenience, are expected in 2025. Phase 3 trials confirm its efficacy and safety parity with the intravenous (IV) formulation, potentially differentiating it from biosimilars. The company hopes this formulation switch—combined with expanded indications and strategic pricing—can transform what analysts call a "patent cliff" into a more manageable "patent hill."

But time is running out. As 2028 approaches, every quarter matters, every trial result carries weight, every strategic decision could determine whether Merck emerges from this transition as a diversified pharmaceutical leader or becomes another cautionary tale of overdependence on a single blockbuster. The patent cliff isn't just a financial challenge—it's an existential test of whether modern pharmaceutical companies can survive the loss of their defining products.

IX. M&A Strategy & Pipeline Building (2021–Present)

November 2021. Merck announces an $11.5 billion acquisition of Acceleron Pharma, stunning Wall Street with the size and speed of the deal. New CEO Rob Davis, barely two months into the job, was sending a clear message: Merck wouldn't wait passively for Keytruda's patent cliff. The company would buy its way to a diversified future, whatever the cost. What followed was one of the most aggressive M&A campaigns in pharmaceutical history—a race against time to build a post-Keytruda portfolio before 2028.

The Acceleron deal brought sotatercept, a potential blockbuster for pulmonary arterial hypertension carrying peak sales estimates of $2 billion. But more importantly, it signaled Merck's strategic pivot. This wasn't about finding another Keytruda—no single drug could replace $30 billion in annual revenue. Instead, Merck would assemble a constellation of smaller stars, each contributing a few billion in sales, collectively offsetting the coming decline.

April 2023 brought the next major move: $10.8 billion for Prometheus Biosciences, securing PRA023 for inflammatory bowel disease. The price—nearly 75% premium to Prometheus's stock price—raised eyebrows. But Davis defended it as necessary aggression. "I am no longer focused on 2028; I am looking at how do we have sustainable growth well into the next decade," Davis said on the company's earnings conference call. The message was clear: overpaying today was better than underpreparing for tomorrow. October 2023 brought the blockbuster: a cancer drug licensing deal with Daiichi Sankyo worth up to $22 billion. Merck paid Daiichi Sankyo a $4 billion upfront payment in addition to $1.5 billion in continuation payments over the next 24 months, and may make additional payments of up to $16.5 billion contingent upon the achievement of future sales milestones, for a total potential consideration of up to $22 billion. The deal covered three antibody-drug conjugates (ADCs)—the hottest area in oncology, where targeted antibodies deliver chemotherapy directly to cancer cells while sparing healthy tissue.

The Daiichi deal revealed Merck's strategic calculus. Merck describes the three Daiichi Sankyo ADCs as having "multi-billion dollar worldwide commercial revenue potential" for both companies approaching the middle of the 2030s. That timeline is key for Merck, whose Keytruda will lose patent protection in the later part of the 2020s. Each ADC could generate $3-5 billion at peak—not Keytruda numbers, but collectively meaningful.

The acquisition spree continued through 2023 and 2024. March saw the acquisition of ophthalmology company EyeBio for undisclosed terms. November brought Caraway Therapeutics for neurodegenerative diseases. Each deal targeted different therapeutic areas—immunology, cardiovascular, neuroscience, ophthalmology—spreading bets across multiple fields rather than doubling down on oncology alone. The most recent move came in December 2024 with an exclusive global license agreement with Hansoh Pharma for an investigational oral GLP-1 receptor agonist. Merck and Hansoh Pharma entered into an exclusive global license agreement for HS-10535, an investigational preclinical oral small molecule GLP-1 receptor agonist. Under the agreement, Hansoh Pharma has granted Merck an exclusive global license to develop, manufacture and commercialize HS-10535. Hansoh Pharma will receive an upfront payment of $112 million and is eligible to receive up to $1.9 billion in milestone payments. While modest compared to earlier deals, it signals Merck's willingness to enter the hottest therapeutic area in pharma—obesity and metabolic disease—where competitors Lilly and Novo Nordisk dominate.

The pattern across these deals is clear: Merck is paying premium prices for assets with uncertain futures. Merck is investing a lot into general and specialty medicine, and many of those assets have development timelines that could lead to approvals that fall somewhere into this space before initial Keytruda patent expiry. The pipeline is predicted to earn more than $35 billion by the middle of the next decade—ambitious projections that assume high success rates for experimental drugs.

Critics question whether Merck is overpaying in desperation. The Prometheus price represented a 75% premium; the Daiichi deal could reach $22 billion for drugs still in clinical trials. But Davis defends the strategy: "We continue to believe we need more and we will continue to prioritize business development," said Davis. With Keytruda generating nearly $30 billion annually, Merck can afford to make expensive bets—for now.

The M&A strategy extends beyond just buying drugs. Merck is acquiring platforms, technologies, and capabilities. The Acceleron deal brought expertise in pulmonary arterial hypertension; Prometheus provided inflammatory bowel disease knowledge; Daiichi offered antibody-drug conjugate technology. Each acquisition adds not just products but scientific expertise that could generate future pipelines.

Yet the math remains daunting. To replace Keytruda's revenue, Merck needs multiple drugs each generating $3-5 billion annually. Historical success rates suggest only 10-15% of clinical-stage drugs reach market. Even with unlimited capital, building a portfolio to offset a $30 billion loss is unprecedented in pharmaceutical history.

The company is also reforming internal R&D, with research spending estimated at over $14 billion in 2024. But internal discovery takes decades—time Merck doesn't have. The 2028 deadline looms, forcing a continued reliance on external deals even as prices escalate and quality assets become scarcer.

As we approach the patent cliff, Merck's M&A strategy represents one of the largest bets in pharmaceutical history: that money can buy time, that multiple good drugs can replace one great one, and that diversification can overcome concentration. Whether this proves prescient planning or desperate scrambling will become clear soon enough. The clock is ticking toward 2028.

X. Playbook: Business & Investing Lessons

The Merck story offers a masterclass in pharmaceutical economics—both its triumphs and its traps. For investors studying the sector, several patterns emerge that transcend this single company and illuminate the entire industry's dynamics.

The Blockbuster Paradox

Keytruda's success illustrates pharma's fundamental contradiction: the drugs that save companies eventually doom them. When a single product generates 46% of revenue, every strategic decision warps around protecting or replacing it. Merck's entire R&D budget, M&A strategy, and organizational structure now revolves around one molecule. This concentration creates massive operational leverage—small changes in Keytruda's trajectory move the entire company's valuation by tens of billions.

The lesson for investors: beware the successful pharmaceutical company. The more dominant a drug becomes, the harder its eventual replacement. Diversified portfolios with multiple $1-2 billion drugs often prove more sustainable than single blockbuster dependence, even if near-term growth appears slower.

Research Productivity vs. Commercial Execution

Merck's history reveals an uncomfortable truth: scientific excellence doesn't guarantee commercial success. The company that gave away streptomycin patents, that pursued diseases others ignored, that maintained the industry's highest R&D spending as a percentage of sales—this same company needed Keytruda's accident of history to survive.

The most valuable pharmaceutical companies aren't necessarily the best at science; they're the best at commercializing science. Gilead turned a single HIV drug into a franchise worth hundreds of billions. Novo Nordisk dominated diabetes not through breakthrough innovation but through incremental improvements and masterful marketing. Merck had the science but often lacked the commercial ruthlessness to maximize value.

Managing Catastrophic Product Failures

Vioxx offers the definitive case study in product liability management. The scandal cost Merck over $5 billion in direct settlements, but the indirect costs—lost trust, decreased innovation, talent exodus—proved far greater. The company's response playbook has become industry standard: immediate withdrawal once evidence becomes undeniable, massive legal reserves, leadership changes, and years of reputation rehabilitation.

The key lesson: the cover-up costs more than the crime. Merck's attempts to manipulate Vioxx data, to ghostwrite articles, to train salespeople to dodge questions—these actions magnified the damage exponentially. Companies that acknowledge problems early, that prioritize patient safety over quarterly earnings, paradoxically preserve more long-term value.

Patent Strategy and Lifecycle Management

Merck's 129 patent applications for Keytruda demonstrate modern pharma's evolution from drug discovery to patent engineering. The strategy isn't just about extending exclusivity; it's about creating uncertainty for biosimilar manufacturers. Each patent, even if likely invalid, requires expensive litigation to overturn. The subcutaneous formulation, new indications, dosing regimens—each creates another barrier, another year of delay, another billion in preserved revenue.

For investors, understanding patent strategy is as important as understanding pipelines. The quality of patents matters less than their quantity and complexity. A thicket of weak patents often provides better protection than a single strong one. The game isn't winning every legal battle but making competition so expensive and uncertain that biosimilar manufacturers accept smaller market shares or delayed entries.

The Role of M&A in Pharmaceutical Innovation

Merck's recent acquisition spree—$11 billion for Acceleron, $10.8 billion for Prometheus, up to $22 billion for Daiichi's ADCs—reveals M&A's true function in modern pharma. These aren't just product purchases; they're time purchases. Each acquisition buys 5-10 years of development that Merck doesn't have.

The premium prices make sense when viewed through this lens. Paying 75% above market value seems excessive until you consider the alternative: watching your company's value evaporate as patents expire. M&A becomes a form of expensive insurance against R&D failure. The lesson for investors: judge pharmaceutical M&A not by traditional metrics (P/E ratios, immediate accretion) but by time value—how many years of runway does this acquisition provide?

Balancing Ethics, Profits, and Public Health

The tension between profit maximization and public health runs throughout Merck's history. George W. Merck's philosophy—"Medicine is for the patient...the profits follow"—sounds quaint in today's market. Yet companies that forgot this balance, that pushed too hard for profits, often paid devastating prices. Vioxx destroyed more value than it ever created. Turing Pharmaceuticals' price gouging made Martin Shkreli a pariah and triggered congressional investigations.

The sustainable approach balances all stakeholders. Pricing must provide returns to incentivize innovation but remain accessible enough to avoid political backlash. Patent extensions must protect legitimate innovation without appearing abusive. Marketing must inform without misleading. Companies that find this balance—Regeneron, Vertex, BioMarin—often outperform those that don't.

The Challenge of Replacing Irreplaceable Drugs

Perhaps the most important lesson from Merck's current predicament: some drugs can't be replaced. Keytruda isn't just a product; it's a platform, a standard of care, a cornerstone of modern oncology. Finding another Keytruda isn't realistic—such discoveries happen perhaps once per decade across the entire industry.

The solution isn't seeking another blockbuster but building a sustainable portfolio of good-enough drugs. Five drugs generating $5 billion each are more valuable than one generating $25 billion, even if the math seems equivalent. Diversification provides resilience, reduces regulatory risk, and creates multiple shots on goal for lifecycle management.

For long-term investors, the playbook is clear: avoid companies dependent on single blockbusters nearing patent expiry, value diversified portfolios over concentrated excellence, and recognize that in pharmaceuticals, the most obvious success often precedes the most dramatic failure. Merck embodies all these lessons—a century of innovation shadowed by concentrated risk, scientific excellence undermined by commercial necessity, and ultimately, a race against time that every pharmaceutical company eventually runs and inevitably loses.

XI. Analysis & Bear vs. Bull Case

The investment case for Merck crystallizes around a single question: Can the company successfully navigate the transition from Keytruda dependence to sustainable diversification before 2028? The answer determines whether Merck remains a pharmaceutical leader or becomes another casualty of patent expiration.

Bull Case: The Transformation Succeeds

The optimistic scenario rests on multiple pillars, each plausible individually though requiring collective success. Keytruda sales grew 18% to $29.5 billion; excluding the impact of foreign exchange, sales grew 22%. The drug continues expanding into new indications—early-stage cancers, combination therapies, biomarker-defined populations. Even conservative growth projections suggest Keytruda could reach $35-36 billion by 2028, maximizing the value extracted before patent expiry.

The subcutaneous formulation represents a masterful defensive strategy. If Merck successfully transitions 30-40% of patients to the injectable version by 2028, they maintain a differentiated product even as biosimilar infusions launch. Physicians prefer simplified administration; patients appreciate convenience; insurers value reduced infrastructure costs. The formulation switch could preserve $10-15 billion in annual revenue post-2028.

Recent acquisitions are beginning to bear fruit. Winrevair for pulmonary arterial hypertension generated $419 million in 2024, its first full year, with peak sales projections of $4-5 billion. The Prometheus acquisition brings a late-stage IBD drug with multi-billion dollar potential. The Daiichi ADCs, particularly patritumab deruxtecan, could each generate $3-5 billion at peak. Collectively, these assets could contribute $15-20 billion annually by 2030.

The pipeline shows unprecedented breadth. Merck's late-stage pipeline leans overwhelmingly toward cancer, the company is dipping its toe in other emerging clinical areas as well. Beyond oncology, Merck is advancing oral PCSK9 inhibitors for cardiovascular disease, GLP-1 agonists for obesity, and novel vaccines for infectious diseases. With 18 drugs in late-stage trials and R&D spending exceeding $14 billion annually, probability suggests multiple successes.

Merck's financial strength enables continued deal-making. With over $60 billion in annual revenue and strong cash generation, the company can afford additional large acquisitions. Several attractive targets exist—Viking Therapeutics for obesity, Roivant Sciences for diverse assets, or even mega-mergers with companies like Biogen or Vertex. Each deal adds shots on goal for replacing Keytruda revenue.

The regulatory environment may prove favorable. The Inflation Reduction Act's drug pricing provisions face legal challenges and potential modification under changing political leadership. Biosimilar adoption in oncology has historically been slower than other therapeutic areas due to physician conservatism and patient concerns. Keytruda's entrenchment in treatment guidelines and clinical protocols creates switching barriers beyond patents.

In this bull scenario, Merck emerges from 2028 transformed but intact—a diversified pharmaceutical leader with multiple growth drivers across therapeutic areas. The stock, currently depressed by patent cliff fears, re-rates higher as execution demonstrates successful navigation. Patient investors who buy during maximum pessimism capture both the remaining Keytruda bonanza and the emerging portfolio's potential.

Bear Case: The Concentrated Bet Unravels

The pessimistic scenario acknowledges harsh pharmaceutical realities. We estimate Keytruda's sales could peak near $36 billion by 2028 but could fall to $20 billion—or even below $15 billion—within four to five years. That outcome looks increasingly likely. History shows blockbuster biologics losing 50-60% of revenue within 3-4 years of biosimilar entry, regardless of defensive strategies.

The subcutaneous formulation faces significant challenges. Physicians comfortable with IV infusions may resist switching stable patients. Biosimilar manufacturers will likely develop their own subcutaneous versions, eliminating differentiation. Insurers, facing budget pressure, mandate biosimilar adoption through formulary restrictions and prior authorization requirements. The formulation switch preserves less revenue than hoped.

Recent acquisitions disappoint relative to their price tags. The $11.5 billion Acceleron deal yields a $2-3 billion peak drug—adequate but not transformative. Prometheus's IBD drug faces competition from established biologics and emerging oral alternatives. The Daiichi ADCs, while promising, compete in crowded oncology markets where differentiation proves difficult. Collectively, acquired assets generate $10-12 billion by 2030—far short of replacing Keytruda.

Pipeline failures are inevitable in pharmaceuticals. Of 18 late-stage drugs, historical success rates suggest 6-8 reach market, with 2-3 becoming meaningful commercial successes. Recent years expansion into new indications slowed; ended 2023 with failures of three Keytruda combination trials. Each failure not only removes potential revenue but damages credibility and stock valuation.

Competition intensifies across all fronts. In oncology, next-generation immunotherapies from companies like Moderna and BioNTech threaten Keytruda's dominance. In cardiovascular disease, established players like Amgen and Regeneron have insurmountable leads. In obesity, Lilly and Novo Nordisk's first-mover advantage proves unassailable. Merck consistently arrives late to competitive markets.

The financial mathematics become crushing. Even assuming moderate Keytruda decline (30% by 2031) and successful new launches, Merck's revenue could fall from $65 billion to $50-55 billion. Margins compress as higher-cost acquired drugs replace Keytruda's extraordinary profitability. R&D spending remains elevated to fund pipeline development. The result: earnings per share declining 30-40% from peak, justifying significant multiple compression.

The bear case sees Merck following AbbVie's post-Humira trajectory—a formerly great company diminished by blockbuster loss, pursuing increasingly desperate acquisitions, cutting costs to maintain dividends while growth evaporates. The stock becomes a value trap, offering apparent cheapness while concealing structural decline.

The Verdict: Calculated Asymmetry

The truth likely lies between extremes. Merck won't collapse post-2028, but neither will it seamlessly replace Keytruda's contribution. The company will probably maintain $55-60 billion in revenue, with earnings power diminished but not destroyed. The transformation will be messy, marked by setbacks and surprises, but ultimately successful enough to preserve Merck's position among pharmaceutical leaders.

For investors, the risk-reward depends on time horizon and risk tolerance. Near-term (2024-2027), Keytruda's continued growth and strong cash generation support the stock. Long-term (2028-2035), success depends on execution variables largely outside investor control. The optimal strategy might be riding Keytruda's final wave while monitoring pipeline and M&A execution, exiting before the patent cliff if diversification efforts disappoint.

The Merck investment case ultimately reflects pharmaceutical investing's fundamental challenge: brilliance and vulnerability intertwined, where today's strength becomes tomorrow's weakness, and where scientific miracles coexist with commercial mortality. Keytruda saved Merck once; whether anything can save it from Keytruda remains the question that will define the company's next decade.

XII. Epilogue & "If We Were CEOs"

Standing in Merck's Rahway headquarters, looking out at the research labs where streptomycin and Keytruda were born, a CEO today faces the pharmaceutical industry's eternal paradox: success breeds crisis. The very excellence that created Keytruda—the focus, the investment, the scientific precision—now threatens the company's future. With less than four years until patent expiry, every decision carries existential weight.

The Race Against 2028

If we were running Merck today, the first recognition would be brutal honesty: Keytruda cannot be replaced. No acquisition, no pipeline advancement, no strategic pivot will generate $30+ billion in annual revenue by 2028. Accepting this reality, rather than denying it, becomes the foundation for rational strategy.

The focus would shift from replacing Keytruda to managing its decline. This means maximizing value extraction through 2028 while building a sustainable $45-50 billion revenue base for the post-Keytruda era. It's not about maintaining current scale but ensuring viability and positioning for eventual recovery.

Strategic Options: The Path Forward

The mega-merger temptation looms large. Combining with another large pharmaceutical company—a Biogen ($30 billion market cap), Gilead ($80 billion), or even BMS ($130 billion)—would create immediate scale and diversification. But mega-mergers in pharma rarely succeed. Cultural integration proves impossible, R&D productivity declines, and regulatory scrutiny intensifies. The short-term financial engineering masks long-term value destruction.

Platform technologies offer more promise. Rather than buying individual drugs, acquire capabilities that generate multiple products. Companies like Moderna (mRNA technology), BioNTech (personalized cancer vaccines), or Alnylam (RNAi therapeutics) provide not just pipelines but engines for creating pipelines. A $30-40 billion platform acquisition, while dilutive near-term, could position Merck as a leader in next-generation modalities.

Geographic expansion remains underexploited. China, despite political tensions, represents the fastest-growing pharmaceutical market globally. India's middle class expansion creates enormous demand for chronic disease treatments. Africa, traditionally ignored, shows surprising growth in healthcare spending. Building or acquiring local capabilities in these markets—not just sales forces but R&D and manufacturing—could add $5-10 billion in revenue less subject to patent cliffs.

Can Lightning Strike Twice?

The search for another Keytruda is both necessary and futile. Transformative drugs emerge from unexpected places—Keytruda itself was an overlooked asset from an overpriced acquisition. But planning for serendipity is oxymoronic. Instead, Merck should optimize for multiple modest successes rather than singular breakthroughs.

This means reforming R&D culture. The current model—massive centralized labs pursuing conservative targets—hasn't produced internal innovation matching Keytruda. Creating autonomous research units, each with distinct cultures and approaches, increases shot-on-goal probability. Fund 20 different $500 million bets rather than two $5 billion programs. Accept higher failure rates for higher potential rewards.

External innovation becomes crucial. Rather than acquiring late-stage assets at premium prices, partner earlier with emerging biotechs. Provide funding, expertise, and infrastructure in exchange for option rights. Build a venture capital arm that invests in dozens of early-stage companies, creating pipeline visibility and acquisition opportunities. Become the preferred partner for academic institutions commercializing discoveries.

The Future of Cancer Treatment

Merck's oncology dominance, while Keytruda-dependent today, provides unique insights into cancer's future. The next wave won't be another PD-1 inhibitor but rather precision medicines targeting specific mutations, cell therapies that reprogram immune systems, and prevention strategies that stop cancer before it starts.

Positioning for this future requires different capabilities. Diagnostic technologies that identify patients for targeted therapies. Manufacturing infrastructure for personalized medicines. Data analytics that predict treatment responses. These aren't traditional pharmaceutical competencies, requiring partnerships or acquisitions outside normal targets.

The antibody-drug conjugate bet with Daiichi Sankyo represents correct strategic thinking—not competing with Keytruda but complementing it. ADCs can target cancers that don't respond to immunotherapy. Combined with Keytruda, they might extend the franchise even post-biosimilar entry. The $22 billion price seems excessive until you consider it's buying a position in potentially the next dominant oncology modality.

Lessons for Pharmaceutical Innovation

Merck's journey from German subsidiary to American giant, from Vioxx disaster to Keytruda triumph, offers timeless lessons. First, culture matters more than strategy. The companies that survive century-long timespans maintain consistent values while adapting tactics. Merck's commitment to science, despite commercial pressures, enabled both its greatest successes and recoveries from failures.

Second, risk management isn't risk avoidance. The Vioxx scandal emerged from hiding risks, not taking them. Keytruda succeeded because Merck risked massive investment despite competitive disadvantage. The companies that thrive take calculated scientific risks while avoiding ethical compromises.

Third, patience pays in pharmaceuticals. Drug development takes decades. Patent cliffs are predictable. Management teams who optimize for quarterly earnings rarely build lasting value. The CEOs remembered favorably—Roy Vagelos, P. Roy Gilmartin (pre-Vioxx), Ken Frazier—thought in decades, not quarters.

Final Reflections

If we were CEO today, the message to employees would be simple: Merck has survived worse and emerged stronger. The company that lost 80% of its shares in World War I built American independence. The company that paid $5 billion for Vioxx deaths developed Keytruda. The patent cliff ahead is daunting but not existential.

The strategy would balance pragmatism with ambition. Accept that 2028-2032 will be challenging, with revenue and earnings declining. But position for recovery through diversified assets, emerging market presence, and next-generation technologies. Maintain R&D investment even as revenues fall. Resist the temptation for desperate mega-deals or excessive cost-cutting.

Most importantly, remember George W. Merck's principle: "Medicine is for the patient." In the race to replace Keytruda, the temptation will be prioritizing financial metrics over patient outcomes. But history shows that companies focused on genuine medical advancement ultimately create more value than those pursuing financial engineering.

The next CEO who stands in that Rahway office, looking at those same research labs, will face different challenges. Perhaps biosimilars proved less damaging than feared. Perhaps an acquired asset became the next blockbuster. Perhaps a new technology platform revolutionized drug discovery. Or perhaps Merck became smaller but more focused, trading scale for sustainability.

Whatever the outcome, Merck's story continues. Companies that survive 130 years don't disappear because one drug loses patent protection. They adapt, evolve, and eventually thrive again. The race against 2028 isn't about preventing change but managing it. And in that race, Merck's history suggests it has better odds than most—even if the finish line remains uncertain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube