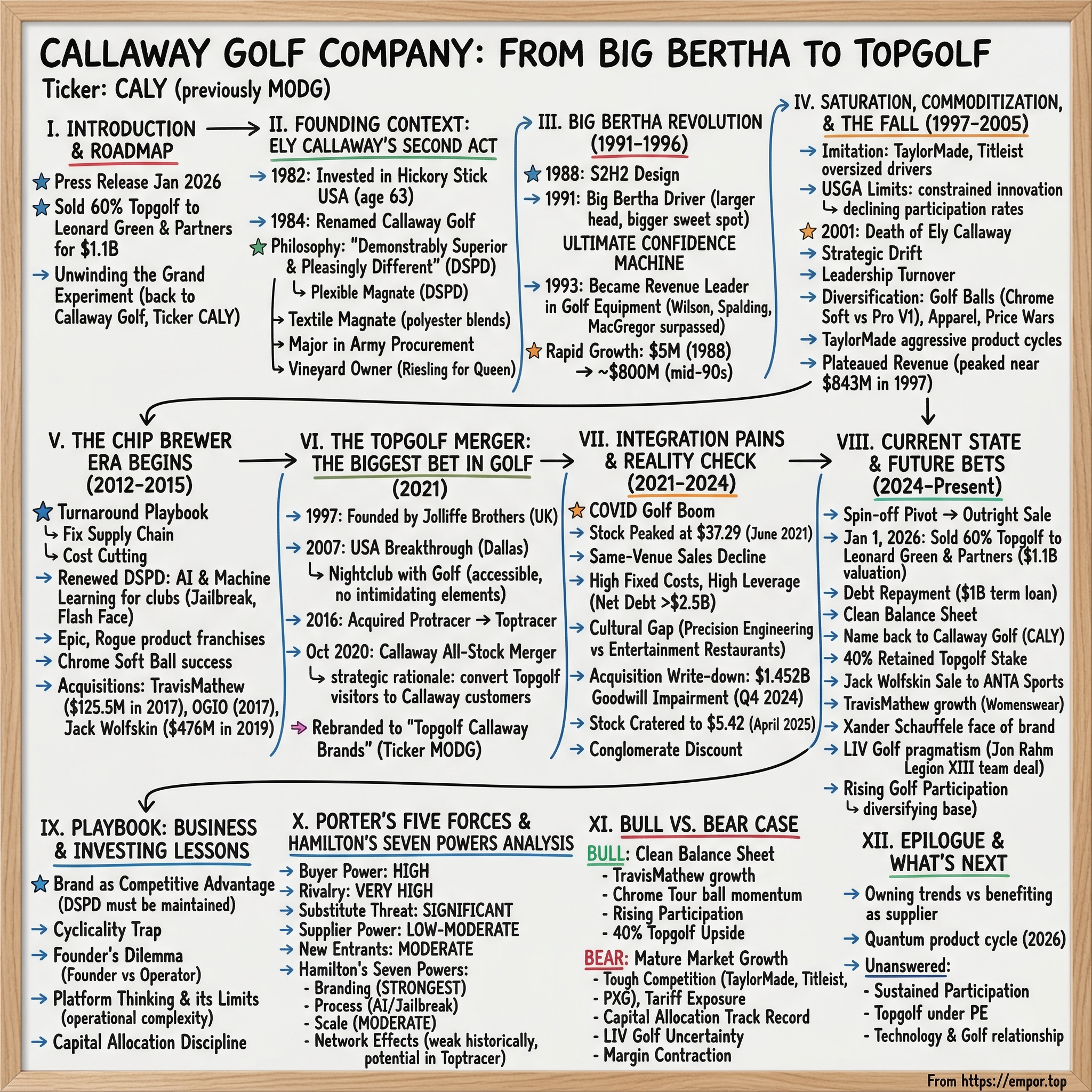

Callaway Golf Company: From Big Bertha to Topgolf

I. Introduction and Episode Roadmap

In January 2026, a press release landed that would have been unthinkable five years earlier. Topgolf Callaway Brands, the company that had staked its future on merging premium golf equipment with tech-enabled entertainment venues, announced it was selling a 60 percent majority stake in Topgolf to private equity firm Leonard Green & Partners. The valuation: roughly $1.1 billion, about half what Callaway had paid for it.

The company would change its name back to Callaway Golf Company. The ticker would flip from MODG to CALY. The grand experiment was being unwound.

How did we get here? How did a company born in a Palm Springs garage in 1982, built by a 63-year-old textile magnate with a vineyard on his resume, grow into the most recognizable name in golf equipment, nearly collapse after its founder's death, get resurrected by an operator from Harvard Business School, and then make the single biggest strategic bet in golf business history, only to reverse course within five years?

The Callaway story is a masterclass in brand-building, the perils of cyclical industries, the courage and hubris of transformational acquisitions, and the brutal honesty required when a bold bet doesn't deliver on its promise. It touches on themes that matter far beyond golf: how do mature consumer brands find growth? When does diversification create value versus destroy it? And what happens when a company built on engineering excellence tries to become an entertainment platform?

The arc moves through distinct chapters. The founding myth of Ely Callaway, a man who built three entirely different businesses before most people build one. The Big Bertha revolution that turned a niche club maker into an $800 million juggernaut. The post-founder drift and near-irrelevance. Chip Brewer's disciplined resurrection. The Topgolf merger that was supposed to change everything. And the recent separation that tacitly admitted the combination didn't work as planned.

Each chapter carries lessons for investors and operators alike. The story begins in Georgia.

II. Founding Context: Ely Callaway's Second Act

Ely Reeves Callaway Jr. was born on June 3, 1919, in LaGrange, Georgia, the son of a textile executive in a state where cotton was king. He attended Emory University, and when the war came, he joined the Army as a reserve officer in 1940. By 24, he had risen to the rank of Major, serving as the Army's sole procurement officer for cotton clothing, a role that taught him the intersection of manufacturing, logistics, and quality at industrial scale. He never saw combat, but he mastered the systems that clothed millions of soldiers.

After the war, Callaway moved to New York and spent three decades climbing the textile industry. He worked at Milliken, then a stint at Textron as vice president, before his division was purchased by Burlington Industries. In 1968, he was named president and director of Burlington, then the world's largest textile company. His signature achievement was championing polyester blends, helping lead the revolution in Dacron-blended fabrics that transformed American clothing. He was a genuine titan of American manufacturing.

Then came the scandal. Callaway uncovered a corporate conspiracy at Burlington, the details of which he spoke about only obliquely in later years. It was the kind of moral dilemma that defines a person: go along, keep the corner office, and protect a thirty-year career, or blow the whistle and walk away from everything. Ely chose the latter.

At 53, Ely Callaway left New York, left textiles, and started over in the Southern California desert. Most people at that age are thinking about winding down. Ely was thinking about grapes.

He established Callaway Vineyard and Winery in Temecula, California, in 1973. The Temecula Valley was not exactly Napa; it was a gamble on unproven terroir in a region better known for avocado groves than Riesling. But Ely had an eye for undervalued assets and the operational skill to extract their potential.

Within three years, his 1974 White Riesling was chosen as the only wine served at a Bicentennial luncheon for Queen Elizabeth II at the Waldorf Astoria in Manhattan. The story goes that the Queen enjoyed the vintage so much she asked for a second glass. The publicity was priceless. By 1981, Callaway sold the vineyard to Hiram Walker and Sons for nearly $9 million in profit.

Two successful careers, two clean exits. Most founders would stop here.

But Ely Callaway's lifelong passion was golf. He had played his whole life, and he had watched the equipment industry with growing frustration. In the early 1980s, the golf equipment business was, to put it bluntly, sleepy. The major brands, Wilson, Spalding, MacGregor, were engineering-focused companies that marketed to serious golfers with technical specifications.

The clubs looked alike. The marketing was interchangeable. The innovation cycle was glacial. Nobody was thinking about the experience of the average weekend hacker who just wanted to hit the ball farther and straighter without feeling like an idiot. To Ely, this was a classic case of an industry that had stopped listening to its customers.

In 1982, at age 63, Ely invested $2.5 million in a tiny company called Hickory Stick USA in Palm Springs, California. He bought the remaining shares for $400,000 in 1984 and renamed it Callaway Golf. The company made wedges and putters, small-ticket items in the golf equipment food chain.

But Ely had a philosophy that would become the company's North Star, a phrase he repeated until it became corporate gospel: "Demonstrably superior and pleasingly different." DSPD. The product had to perform measurably better than anything else on the market, and it had to look and feel distinctly appealing. This was not about incremental improvement. This was about making clubs that sold themselves the moment a golfer swung one.

The insight beneath DSPD was psychological, not engineering. Ely understood that amateur golfers were insecure. They were embarrassed by bad shots. They compared themselves unfavorably to the pros they watched on television.

What they needed wasn't a club that shaved two degrees of sidespin off a fade. They needed a club that gave them confidence. They needed a club that made them feel like they could actually play this game.

Ely was selling joy, not specs. It was the same instinct that had made his textile blends successful: give the customer what they feel, not just what they measure. It's also, as it turns out, the same instinct that would later make Topgolf successful: take a sport that intimidates casual participants and make it fun.

By the late 1980s, Callaway Golf was doing about $5 million in revenue, a rounding error in the golf industry. But Ely was building something. He was hiring engineers, investing in R&D, and laying the groundwork for a product that would turn the entire industry upside down. He had a relentless focus on the amateur golfer's experience, spending time at courses and driving ranges, watching how real people interacted with their equipment, listening to what frustrated them. The wedges were the proof of concept, demonstrating that a small company with the right philosophy could build products that generated word-of-mouth excitement. What came next was the revolution.

III. The Big Bertha Revolution (1991-1996)

Before Big Bertha, there was the S2H2. In the late 1980s, Callaway's engineering team developed a design concept called "Short, Straight, Hollow Hosel," which moved weight from the hosel, the tube connecting the clubhead to the shaft, back into the clubhead itself.

For non-golfers, the hosel is essentially a connector piece that adds dead weight without contributing to performance. By hollowing it out, Callaway's engineers could redistribute that mass into the clubhead, making the sweet spot more forgiving. It was a small innovation, but it signaled that Callaway was thinking differently about club design, starting from the physics up rather than the cosmetics down.

The S2H2 irons and drivers were a modest success, enough to push the company from $5 million in 1988 to $10.5 million in 1989 and about $21 million in 1990. Revenue was doubling every year. Respectable growth, but still a niche player in a market dominated by established brands with ten times the revenue.

Then, in 1991, Callaway released the Big Bertha driver, and everything changed.

The concept was elegantly simple: make the clubhead dramatically larger than anything else on the market. Conventional drivers of the era had relatively small, compact heads, typically around 190 to 200 cubic centimeters. Big Bertha's head was significantly oversized, pushing toward what would eventually become the modern standard.

Why did this matter? For non-golfers, think of it this way: a larger clubhead has a bigger "sweet spot," the area on the face that produces good results when the ball makes contact. A traditional driver's sweet spot was roughly the size of a quarter. Big Bertha's was closer to the size of a silver dollar. Off-center hits that would produce a horrifying slice with a traditional driver now flew relatively straight with Big Bertha.

It was the ultimate confidence machine. And confidence, as Ely understood, was the thing that kept casual golfers coming back to the course rather than quitting in frustration.

The name was genius. Big Bertha was a famous World War I German howitzer, a massive cannon renowned for its power and range. The name conveyed exactly what the club promised: explosive distance. It was memorable, slightly irreverent, and impossible to confuse with anything else on the market. When golfers told their friends about this new club they'd bought, they didn't say "I got the Callaway oversized titanium driver." They said "I got Big Bertha." The name did half the marketing work.

The sales trajectory was staggering. Revenue jumped from $21 million in 1990 to $54.7 million in 1991, nearly a 150 percent increase. By 1992, sales hit $132 million. In 1993, they reached $255 million, and Callaway surpassed Wilson, Spalding, and MacGregor to become the revenue leader in golf equipment. By the mid-1990s, the company was approaching $800 million in annual revenue.

From $5 million to $800 million in roughly seven years. This was not a gradual build. This was a rocketship. To put it in context, Callaway grew faster in this period than Nike's golf division, faster than any brand in the sporting goods industry. The growth rate made it one of the best-performing consumer products stocks of the decade.

Callaway went public in 1992, listing on the New York Stock Exchange under the ticker "ELY," a tribute to the founder whose personality was inseparable from the brand. The IPO gave the company access to capital to scale production, build out its R&D capabilities, and fund the marketing machine that Ely was constructing.

And what a machine it was. Callaway invested heavily in "demo days" at golf courses and driving ranges, where average golfers could try the clubs for free. The strategy was brilliant because Big Bertha sold itself on contact. One swing and the golfer felt the difference. The ball went farther. The mishits weren't catastrophic. The feedback loop was instantaneous and addictive. Demo days became the grassroots engine of Callaway's growth, a hands-on, experiential marketing approach decades before "experiential marketing" became a buzzword.

Tour adoption followed. Professional golfers began putting Callaway clubs in their bags, which gave the brand credibility with serious players while the oversized design attracted the mass market. It was the rare product that appealed to both ends of the spectrum.

The cultural timing was perfect too. The early-to-mid 1990s saw a golf boom in America, fueled partly by economic prosperity and partly by the emergence of Tiger Woods, who turned professional in 1996 and brought an entirely new demographic to the sport. Golf was aspirational, premium, and growing. Callaway was the hottest brand in the hottest sport.

Ely Callaway marketed with the storytelling instincts of a man who had sold textiles to the military, wine to Queen Elizabeth, and now clubs to America. He understood heritage, aspiration, and the power of a good narrative. Callaway wasn't just a club company. It was a brand that made golf more fun.

There's a myth versus reality element worth addressing here. The myth is that Big Bertha's success was purely about technology. The reality is that it was equally about psychology and marketing. The performance advantage was real, but the magical ingredient was how Big Bertha made golfers feel. Ely understood that the average golfer's relationship with their equipment is deeply emotional. A bad round gets blamed on the clubs; a good round makes the golfer fall in love with them. Big Bertha gave millions of golfers the feeling that they'd found their secret weapon.

For investors, the takeaway from this era was the power of a genuine product breakthrough combined with brilliant positioning: Big Bertha wasn't just better, it was different enough to create its own category, and the economics reflected it with premium pricing and explosive growth. But it also created a dangerous precedent: the expectation that the next Big Bertha was always around the corner. When it wasn't, the company would struggle.

IV. Saturation, Commoditization, and the Fall (1997-2005)

The trouble with revolutions is that they invite imitation. By the mid-to-late 1990s, every major golf equipment maker had its own version of the oversized driver. TaylorMade, Titleist, Ping, and Cobra all produced large-headed, forgiving clubs that narrowed Callaway's performance advantage. The technology that had seemed magical when Big Bertha launched was now table stakes. Worse, the United States Golf Association began imposing equipment limits on clubhead size and the "trampoline effect" of club faces, which constrained how far manufacturers could push the performance envelope. Think of it like a Formula 1 regulation change: when the governing body caps how fast the cars can go, the competitive advantage shifts from raw engineering to marginal optimization, and the field compresses. Innovation was hitting a regulatory ceiling.

The ERC II driver illustrates the tension perfectly. In 2000, Callaway released a driver that the USGA deemed non-conforming because its club face was too "springy," exceeding the coefficient of restitution limit. The club was legal under Royal and Ancient rules in Europe and Asia but banned for competitive play in the United States. Ely Callaway, in typical fashion, sold it anyway for international and recreational use, arguing that the USGA's limits were arbitrary and anti-consumer. The episode highlighted a growing reality: the regulatory framework was constraining the very type of breakthrough innovation that had built Callaway's brand.

The broader industry was also shifting in troubling ways. The "Great Golf Slump" of the early 2000s saw declining participation rates, a trend that would persist for over a decade. The golf boom of the 1990s had attracted casual players who, it turned out, didn't stick with the sport.

The reasons were structural. Golf was expensive: a typical round with cart fees ran $50 to $100 or more. It was time-consuming: a round took four to five hours, half a Saturday. It was intimidating: the learning curve was brutally steep, the rules arcane, and the social etiquette unforgiving. The player base was aging, and younger demographics, raised on soccer, basketball, and video games, weren't replacing them.

Course construction slowed, then reversed, as municipalities and developers realized that many of the golf courses built during the boom were financially unsustainable. Between 2005 and 2015, the United States lost more courses than it built in every single year. The industry that had seemed like an unstoppable growth story was suddenly cyclical and mature.

Then came the blow from which Callaway would take years to recover. Ely Callaway died of pancreatic cancer on July 5, 2001, at the age of 82. He had briefly stepped away from daily management in the late 1990s, handing the CEO role to others, before returning to the corner office during a rocky period because he couldn't stand watching the company drift. His death removed the visionary force that had built the company's culture, its product philosophy, and its brand identity. DSPD wasn't just a slogan; it was Ely's personal standard, enforced by his presence in meetings, his visits to the R&D lab, his involvement in marketing decisions. He would hold a prototype in his hands, swing it, feel it, and pronounce judgment. Without him, the company drifted.

The years that followed were marked by leadership turnover and strategic confusion. Callaway cycled through executives who couldn't quite replicate Ely's combination of product intuition and marketing flair. Ron Drapeau, who succeeded Ely, was a capable administrator but lacked the founder's charisma. George Fellows took over in 2005 after stints at Callaway and other consumer brands, but his tenure was also marked by incremental management rather than visionary leadership.

The company tried to diversify. Golf balls became a significant push, and Callaway eventually built a competitive ball business, but it was fighting Titleist's Pro V1, arguably the most dominant single product in all of golf. The Pro V1, launched in 2000, was to golf balls what the iPhone later became to smartphones: a product so good that it defined the category and made everything else seem like an also-ran. Titleist's ball market share hovered above 50 percent for years, with Pro V1 and Pro V1x commanding a staggering 73 percent usage rate on the PGA Tour.

Apparel initiatives came and went without gaining traction. Price wars broke out as retailers gained leverage and manufacturers competed for shelf space. Margins compressed. The Callaway brand, once synonymous with breakthrough innovation, was beginning to feel like yesterday's news.

TaylorMade, backed by Adidas's resources, became an increasingly formidable competitor, investing heavily in tour presence and rapid product cycles. Their strategy of launching new driver models every year, sometimes twice a year, created a relentless upgrade treadmill that compressed the industry's pricing power.

Titleist, owned by Acushnet, maintained its stranglehold on the premium ball market and its strong position in irons and wedges. Ping, family-owned and engineering-focused, held a loyal following built on custom fitting and understated quality. Cobra, backed by Puma, targeted the value-conscious golfer with aggressive pricing.

Callaway was no longer the clear leader. It was one of several well-known brands in a commoditizing market, fighting for share in an industry with flat-to-declining demand. The brand still carried weight, but without a breakthrough product or a visionary leader, weight alone wasn't enough.

By the mid-2000s, and extending through the financial crisis of 2008-2009, the existential question hanging over Callaway was stark: without Ely, without the growth that Big Bertha delivered, without a secular tailwind in golf participation, was this just another cyclical consumer products company grinding out low-single-digit growth and fighting margin erosion? Revenue, which had peaked near $843 million in 1997, had essentially plateaued. The stock reflected this uncertainty. The premium the market had placed on Callaway's growth trajectory evaporated. What investors needed was an operator who could stabilize the business, restore product credibility, and find a path to renewed relevance. They waited a long time. They got him in 2012.

V. The Chip Brewer Era Begins: Stabilization and Soul-Searching (2012-2015)

Oliver G. "Chip" Brewer III arrived at Callaway Golf in March 2012 with the sort of resume that doesn't generate headlines but does generate results. A 1986 graduate of the College of William and Mary, where he played college golf, Brewer earned his MBA from Harvard Business School in 1991. His career path wound through the containerboard division of Mead Corporation, an unusual training ground for a future golf CEO, but one that instilled a deep appreciation for manufacturing efficiency and supply chain management. He found his way to golf in 1998, joining Adams Golf as senior vice president of sales and marketing. He became president and COO in 2000 and CEO in 2002. He ran Adams for a decade, building it into a respected mid-tier brand known particularly for its hybrids, clubs designed to be easier to hit than long irons, which was philosophically aligned with Ely Callaway's original DSPD vision even if Adams was a smaller stage.

Brewer was not Ely Callaway. Where Ely was a showman, a storyteller, a man who could charm Queen Elizabeth and sell confidence to weekend golfers, Brewer was a disciplined operator with a quiet intensity. Where Ely worked from instinct and vision, Brewer worked from data, process, and operational excellence. In interviews, Brewer came across as measured, analytical, and refreshingly straightforward, the kind of CEO who talks about inventory turns and gross margin improvement rather than revolutionary product vision. This was exactly what Callaway needed. The company didn't lack brand equity or engineering talent. It lacked focus, financial discipline, and strategic clarity.

The turnaround playbook was textbook but executed with uncommon precision. Brewer cut costs aggressively, rationalized the product line by reducing redundant SKUs that were cannibalizing each other and confusing consumers, and fixed a supply chain that had become bloated and inefficient. He brought a discipline to product launches that had been missing: fewer products, better execution, clearer positioning. He invested in R&D with a renewed commitment to DSPD, Ely's founding principle, but updated it with modern tools. Callaway began using artificial intelligence and machine learning to design club faces, running thousands of simulated variations to optimize ball speed and forgiveness. Technologies branded as "Jailbreak" and "Flash Face" emerged from this process, representing genuine advances in how clubs were designed. The product franchises that resulted, XR, then Epic, then Rogue, were not revolutionary in the way Big Bertha had been, but they were genuinely excellent, tour-validated clubs that re-established Callaway as the innovation leader in the category.

One of Brewer's smartest moves was doubling down on the golf ball business. The Chrome Soft line, launched in the mid-2010s, used a graphene-infused construction that delivered tour-level performance at a premium price point. To understand why this mattered, consider the economics: a premium golf ball retails for $45 to $50 per dozen, and an avid golfer might go through two to four dozen per month. That is far more recurring revenue than a driver purchase that happens once every three to five years.

Chrome Soft became a legitimate competitor to Titleist's Pro V1, which had dominated the premium ball market for over a decade with near-religious devotion from consumers. The ball business gave Callaway something it had never had: a high-frequency, high-margin consumable product. Chrome Soft, later evolved into the Chrome Tour line, reduced the company's dependence on the boom-bust equipment cycle and gave it a footing in the most profitable segment of the golf industry.

Then came the acquisitions. In 2017, Brewer acquired TravisMathew, a Southern California men's sportswear brand, for $125.5 million. At the time, TravisMathew was doing roughly $55 to $60 million in annual revenue. The brand was cool in a way that golf apparel usually isn't: fitted, casual, designed for the lifestyle that orbits around golf without being exclusively about golf. Think country club to cocktail bar. It gave Callaway a foothold in the "active lifestyle" category that was growing faster than equipment.

The same year, Callaway acquired OGIO International, a bag and accessories brand known for its distinctive designs. In January 2019, Brewer made a bigger swing: Jack Wolfskin, a German premium outdoor apparel brand, for approximately $476 million. This was a bet on international expansion and the outdoor lifestyle category, and it represented a departure from Callaway's golf-centric identity.

The Jack Wolfskin deal would prove to be a mixed bag. The brand had strong recognition in Germany and parts of Asia but struggled in North America, and integrating a European outdoor brand into a California golf company's portfolio created more complexity than synergy. It was eventually sold to ANTA Sports in mid-2025 for $290 million, a significant loss on the investment and an early warning sign about the limits of diversification through acquisition.

By 2019, Brewer had stabilized Callaway, restored its brand heat, improved margins, and built a portfolio of brands beyond just clubs. Revenue was growing, the balance sheet was healthier, and the company had tour credibility through staff players like Xander Schauffele, a rising star who would go on to win two major championships, and Jon Rahm, the fiery Spanish talent who would win the U.S. Open. Callaway had also quietly been building a minority stake in a fast-growing entertainment company called Topgolf, accumulating roughly 14 percent of its shares. Brewer visited the venues, studied the economics, and saw something that excited him.

But the nagging structural problem remained: the golf equipment market was mature, cyclical, and zero-sum. One company's market share gain was another's loss. Growing the pie itself seemed nearly impossible. The equipment industry was roughly a $9 to $10 billion global market, and it wasn't getting meaningfully bigger. Brewer needed a bigger idea. He was about to make the biggest bet in the history of golf business.

VI. The Topgolf Merger: The Biggest Bet in Golf (2021)

To understand the Topgolf merger, you first need to understand what Topgolf was and why it captivated Silicon Valley and Wall Street alike.

The story begins in 1997 when twin brothers Steve and Dave Jolliffe sold their mystery shopping business in the United Kingdom and went looking for their next venture. Both were golfers frustrated by the dreary monotony of traditional driving ranges. They imagined something better: a driving range that tracked each ball using microchip technology, turning practice into a game. In 2000, they opened the first venue in Watford, England, under the name "Target Oriented Practice Golf." It was basic, but the concept resonated.

The breakthrough came when a group of entrepreneurs, including David Main, Eric Wilkinson, and Tom Mendell, took the concept to America. They chose Dallas, Texas, for its golf culture, warm climate, and concentration of corporate headquarters that could fuel corporate event bookings. The Dallas venue opened in February 2007 and was an immediate sensation. Wait times stretched to six hours.

The key innovation wasn't just the ball-tracking technology, which used RFID chips embedded in each ball to register where they landed on the target field. It was the entire experience: a multi-level, climate-controlled hitting bay facility surrounded by a restaurant and bar, with big screens, music, and a party atmosphere. Each venue was three stories tall, had 72 to 102 hitting bays, a full-service restaurant, multiple bars, and private event spaces. This wasn't a driving range. It was a nightclub that happened to have golf.

By 2020, Topgolf had grown to over 70 venues across the United States, United Kingdom, and Australia, generating approximately $1.1 billion in annual revenue. The company had raised hundreds of millions in venture capital and private equity funding. Providence Equity Partners, WestRiver Capital, and other institutional investors had backed the concept's growth. Callaway itself held roughly 14 percent of the equity.

Topgolf's genius was accessibility. Traditional golf is intimidating: you need equipment, you need to know the rules, you need to book a tee time, and you're going to be watched by other golfers while you embarrass yourself on the first tee. The learning curve is steep, the time commitment is enormous, and the social dynamics can be exclusionary.

Topgolf eliminated all of that. You showed up in street clothes, grabbed a drink, picked up a club, and started hitting balls at giant targets. The technology scored everything automatically. You could compete with friends regardless of skill level. The food was decent, the drinks were flowing, and nobody judged your swing. Critically, half of Topgolf's visitors had never played a round of traditional golf. The company was capturing a customer that the golf industry had never been able to reach, the social diner, the corporate team-builder, the millennial looking for something more active than a bar but less intimidating than a golf course.

The technology platform deepened over time. In 2016, Topgolf acquired Protracer, a Swedish company whose ball-tracking technology was used in televised golf broadcasts to trace the trajectory of shots through the air. Topgolf rebranded it as Toptracer and began installing the technology in existing driving ranges worldwide. The idea was powerful: for a fraction of the cost of building a new Topgolf venue, you could retrofit any driving range with screens and cameras that turned every bay into a data-rich, gamified experience.

Toptracer was arguably the most scalable piece of the Topgolf business. The technology could be deployed quickly, required minimal capital, and created recurring licensing revenue. Between the owned venues and the Toptracer licensing business, Topgolf was building something that looked, at least in theory, like a technology-enabled platform with network effects.

Callaway had been an investor in Topgolf since early on. In October 2020, Callaway announced an all-stock merger with Topgolf, valuing the entertainment company at an implied equity value of approximately $2 billion. The deal closed on March 8, 2021. Callaway issued roughly 90 million new shares, and post-merger, legacy Callaway shareholders owned about 51 percent of the combined company, with former Topgolf shareholders holding the remaining 49 percent.

The strategic rationale was sweeping and, on paper, compelling. Callaway would no longer be just an equipment company trapped in a cyclical, zero-sum market. It would own the customer journey from first swing to premium equipment purchase. The pitch deck logic went something like this: Topgolf attracts 30 million visitors per year, many of whom have never played golf. Callaway equipment sits in every bay. A fraction of those visitors convert to on-course golfers and buy Callaway clubs, balls, and apparel. The data from Topgolf and Toptracer creates insights into player behavior that inform product development and marketing. The entertainment venues generate food-and-beverage revenue, membership fees, and event bookings that are recurring and less cyclical than equipment sales.

The company rebranded to "Topgolf Callaway Brands" in September 2022, changing its historic NYSE ticker from "ELY" to "MODG," short for "Modern Golf," to signal the transformation. The ticker change was symbolically significant: Ely Callaway's initials had represented the company on the New York Stock Exchange for three decades. Replacing them signaled that this was no longer the founder's company in spirit or strategy.

Wall Street was skeptical from the start. The deal was dilutive, with roughly 90 million new shares issued. The debt burden was substantial, as Callaway assumed approximately $555 million of Topgolf's existing obligations on top of its own balance sheet. Topgolf venues were extraordinarily capital-intensive: each new location cost upward of $50 million in real estate, construction, and technology. An average venue generated roughly $17 million in annual gross sales, but only about a third of that came from actual golf gameplay. The rest was food and beverage, corporate events, and ancillary revenue. In other words, Callaway was buying a chain of entertainment restaurants that happened to involve hitting golf balls. The operating model required high throughput and strong same-venue sales growth to generate attractive returns on invested capital. Four-wall EBITDA margins were running in the low 30 percent range, respectable but not exceptional for a venue-based entertainment concept, and well below what optimistic projections had suggested.

And the cultural gap was vast: a precision engineering company headquartered in Carlsbad, California, run by golf lifers and materials scientists, was now managing a restaurant-and-entertainment business headquartered in Dallas, Texas, that employed bartenders, line cooks, and DJs. The two businesses would, by most accounts, never truly integrate operationally. They ran as separate silos with separate management teams, separate cultures, and separate KPIs. The marketing synergies were real, Callaway branding appeared prominently in Topgolf venues, but the operational synergies were minimal. Could Chip Brewer, a golf equipment CEO, really manage both worlds? The market had its doubts. But in March 2021, the COVID golf boom was still raging, and optimism prevailed. The stock peaked at $37.29 in June 2021.

VII. Integration Pains and Reality Check (2021-2024)

The COVID-era golf boom was one of the most unusual market dislocations in recent sports history. With restaurants closed, travel restricted, and outdoor activities among the few safe options, Americans flooded onto golf courses. Rounds played surged past 500 million annually for the first time. Equipment sales spiked as both new and lapsed golfers upgraded their bags. Every major equipment brand ramped up production to meet what felt like insatiable demand. And Topgolf, once it reopened, saw enormous demand as people craved in-person social experiences after months of lockdown isolation.

For a brief, intoxicating moment, it looked like the merger thesis was playing out perfectly. The combined company had revenue exceeding $4 billion. The stock hit $37.29 in June 2021, just three months after the merger closed. Bulls argued that Callaway had perfectly timed its transformation, buying Topgolf at the start of a secular shift in golf engagement.

Then the tide receded. As pandemic restrictions fully lifted, consumers had more choices for their entertainment dollars. Restaurants reopened fully. Concerts came back. International travel resumed. The explosion of choice meant that every entertainment dollar was contested.

Topgolf's same-venue sales, the critical metric for any venue-based business, began to decline. For those unfamiliar with the term, "same-venue sales" measures revenue growth at locations that have been open for at least a year, stripping out the effect of new openings. It's the restaurant and retail industry's most important gauge of organic health. When it declines, it means existing locations are seeing less traffic, lower spending per visit, or both.

Through 2024, same-venue sales fell roughly 9 percent for the full year, a brutal number for a business model that depends on high traffic and utilization of fixed-cost venues. The declines started in late 2023 with a 3 percent dip in Q4, accelerated to 7 percent in Q1 2024, and hit 8 percent in Q2 2024. The trajectory was alarming.

The economics were unforgiving. Each Topgolf venue represented a massive fixed-cost commitment: real estate leases that run 20 to 25 years, labor costs that include hundreds of employees per venue, technology infrastructure that requires constant maintenance, and food-and-beverage operations with their own supply chain and waste dynamics. When traffic declined, those costs didn't. This is the fundamental challenge of any venue-based entertainment business: you are leveraged to consumer traffic, and when that traffic drops, your costs stay fixed while your revenue falls.

Margins, which had never reached the levels some bulls had projected, compressed further. The total company carried a heavy debt load, with net debt exceeding $2.5 billion at its peak and leverage ratios stretching to nearly five times adjusted EBITDA. For a company in a cyclical industry, that level of leverage left no margin for error.

The equipment business faced its own headwinds. The post-COVID normalization brought inventory gluts across the industry. Every major equipment brand had ramped up production to meet pandemic-fueled orders, and when the music stopped, retailers were sitting on excess stock. Promotional activity intensified, compressing margins across the industry. The "COVID golf boom" had been real but, as it turned out, partly a pull-forward of future demand rather than a permanent step-change in the market's size.

For full year 2024, Topgolf Callaway Brands reported total revenue of $4.24 billion, down slightly from the prior year. The Topgolf segment generated $1.81 billion, roughly 43 percent of total revenue. Golf Equipment contributed $1.38 billion, and the Active Lifestyle segment, which included TravisMathew and the struggling Jack Wolfskin brand, contributed about $1.05 billion. The company was profitable on an adjusted EBITDA basis but the returns on the enormous capital deployed in Topgolf venues were disappointing.

Then came the accounting reckoning. In the Q4 2024 earnings report, released in February 2025, Callaway recorded a staggering $1.452 billion non-cash goodwill impairment charge against Topgolf's goodwill and intangible assets. The resulting GAAP net loss for fiscal 2024 was $1.513 billion.

For non-accountants, a goodwill impairment is essentially a company admitting that an acquisition was worth less than what it paid. Goodwill is the accounting entry that captures the premium paid above the fair value of tangible assets in a merger. When the acquired business underperforms, that premium gets written down. In Callaway's case, the $1.452 billion write-down was management acknowledging, in black and white, that they had significantly overpaid for Topgolf. The implied enterprise value in the 2021 merger was roughly $2.5 billion including assumed debt; four years later, the books reflected that the asset was worth far less.

The stock was punished mercilessly. From a post-merger high of $37.29 in June 2021, shares cratered to a trough of $5.42 in April 2025, an 85 percent decline. Investors who had bought the vision of a diversified golf-and-entertainment platform were watching their thesis crumble. The question shifted from "How big can this get?" to "Was this a mistake?"

Brewer, to his credit, acknowledged the challenges and began making adjustments. Venue expansion was slowed dramatically from seven to ten new openings per year to a more measured pace. The focus shifted from growth to profitability. Value-oriented promotions, things like "Sunday Funday" deals, "Topgolf Nights" events, and Summer Fun Pass offerings, were introduced to drive traffic during off-peak periods. Menu offerings were streamlined and the labor model was made more efficient, pushing four-wall EBITDA margins toward 35 percent at the best venues. Topgolf also acquired BigShots Golf, a smaller competitor, for $29 million, adding four venues and a franchise model.

But the market had lost patience. The conglomerate discount, where a combined entity trades for less than the sum of its parts because investors can't easily value or optimize each business separately, was punishing the stock. Analysts from UBS and Raymond James were particularly vocal. UBS initiated coverage with a Neutral rating and a $10 price target, explicitly noting they "prefer business models that are asset light and scalable," a direct rebuke of Topgolf's capital-intensive venue model. Raymond James downgraded the stock from Outperform to Underperform, calling the Topgolf acquisition a mistake.

In September 2024, Topgolf Callaway Brands announced its intent to separate into two independent companies. The plan was a tax-free spinoff of Topgolf, giving shareholders direct ownership of both entities and allowing each business to pursue its own strategy with a focused management team and dedicated capital structure. The market initially responded positively, but execution would prove complicated.

VIII. Current State and Future Bets (2024-Present)

The separation story took several unexpected turns. Artie Starrs, the CEO of the Topgolf division who had been tapped to lead the spun-off entity, resigned in July 2025. His destination: CEO of Harley-Davidson, effective October 2025. The irony was not lost on observers. The man chosen to lead Topgolf into independence was leaving for a different iconic American brand with its own challenges around aging demographics and cultural relevance.

Starrs's departure forced a delay. Chip Brewer acknowledged that executing a spinoff without a permanent Topgolf CEO was "impractical." The search for a replacement began, but the original timeline was out the window. The market, already impatient, grew more skeptical.

By November 2025, the company pivoted from a spinoff to an outright sale. Leonard Green and Partners, a Los Angeles-based private equity firm with deep expertise in consumer and retail businesses, including prior investments in J.Crew, Whole Foods, and Shake Shack, agreed to acquire a 60 percent majority stake in Topgolf and its Toptracer technology.

The deal valued Topgolf at approximately $1.1 billion, roughly half the implied valuation from the original 2021 merger. For a business that Callaway had effectively paid close to $2 billion for, the write-down was significant. But the cash proceeds and debt paydown transformed the balance sheet overnight.

The sale closed effective January 1, 2026. Callaway received approximately $800 million in cash proceeds, net of adjustments and transaction expenses. In a decisive move, the company immediately repaid $1 billion of outstanding borrowings under its term loan B facility, slashing its debt to approximately $480 million and leaving about $680 million in unrestricted cash.

The board authorized a $200 million share repurchase program, signaling confidence in the go-forward business and returning capital to shareholders who had endured a brutal ride. It was the clearest signal yet that management had shifted from growth-at-any-cost to a shareholder-returns orientation.

In mid-January 2026, the corporate name reverted to Callaway Golf Company, and the ticker changed from MODG to CALY. The company retained a 40 percent ownership stake in Topgolf, preserving optionality if the venues stabilize and grow under private equity ownership. A strategic marketing partnership ensures continued brand synergies between Callaway and Topgolf. Callaway equipment will continue to be featured in Topgolf venues, and the Topgolf brand will continue to reference its Callaway heritage.

The Jack Wolfskin divestiture, completed on May 31, 2025, when the German outdoor apparel brand was sold to ANTA Sports for $290 million against a 2019 acquisition price of approximately $476 million, further streamlined the portfolio. The $186 million loss on that disposal, combined with the $1.452 billion goodwill impairment on Topgolf and the sale at roughly half its acquisition valuation, represented a painful accounting of the diversification strategy's costs. In total, the acquisitions that were supposed to transform Callaway into a diversified lifestyle and entertainment company destroyed well over a billion dollars of shareholder value. Post-separation, Callaway's ongoing brand portfolio consists of Callaway Golf (clubs, balls), Odyssey (putters), TravisMathew (lifestyle apparel), and OGIO (bags and accessories). This portfolio generated approximately $2 billion in revenue over the trailing twelve months through Q3 2025.

There were encouraging signs as 2025 progressed. In Q3 2025, Topgolf's same-venue sales turned positive for the first time in two years, suggesting the value initiatives were working. The turnaround was real: after six consecutive quarters of decline, traffic was returning.

The Golf Equipment segment grew 4 percent to $305 million in Q3, with golf balls up 6 percent, driven by the Chrome Tour line's continued inroads against Titleist's dominance. Full-year 2025 revenue guidance was raised to $3.90 to $3.94 billion, with adjusted EBITDA of $490 to $510 million. The continuing operations of the golf and lifestyle business generated approximately $2.06 billion in revenue and $222 million in adjusted EBITDA for 2025.

For 2026, as a standalone golf-and-lifestyle company post-Topgolf, Callaway guided to revenue of $1.98 to $2.05 billion, roughly flat with the prior year, and adjusted EBITDA of $170 to $195 million, actually down from 2025 due to incremental tariff costs and one-time transition expenses from the separation. The guidance acknowledged a year of transition, with the promise of margin normalization in 2027 and beyond.

On the tour, Callaway maintains a strong roster. Xander Schauffele, who won two major championships in 2024, the PGA Championship and The Open Championship, is the face of the brand, the kind of dual major winner who moves the needle in equipment sales. Jon Rahm signed a long-term extension in 2023 that included an equity stake in the company. His subsequent move to LIV Golf in December 2023 complicated the endorsement picture, but Callaway responded innovatively: in March 2025, the company expanded the Rahm partnership to cover his entire Legion XIII LIV team, the first equipment deal between a major OEM and a LIV franchise. It was a pragmatic acknowledgment that the fractured tour landscape required new endorsement models. The broader golf participation picture is actually positive, and this is perhaps the most important macro datapoint for the entire thesis. According to the National Golf Foundation, 29.1 million Americans played on a golf course in 2025, a seventh consecutive annual increase and the highest figure since 2008. Total participation including off-course activities like simulators and Topgolf reached 48.1 million. More than 500 million rounds of golf have been played at U.S. courses in each of the past six years. Crucially, the participant base is diversifying in ways that were unimaginable a decade ago: 28 percent of on-course golfers in 2024 were female, the highest proportion ever recorded. Black participation surged 123 percent since 2019. Just under 4 million juniors played on course in 2025, the most since 2004, representing a 58 percent increase from pre-pandemic levels. If these trends hold, and there are structural reasons to believe they will, given the accessibility initiatives by courses, equipment makers, and entertainment concepts like Topgolf, then the secular backdrop for premium golf equipment has genuinely shifted from headwind to tailwind for the first time in two decades.

The Toptracer technology, which was included in the Topgolf stake sold to Leonard Green, represents one of the more interesting digital assets in the retained portfolio's orbit. Installed at over 1,000 driving range sites encompassing more than 37,500 bays worldwide, Toptracer uses high-speed cameras to track ball flight in three dimensions, displaying real-time data on screens at each hitting bay. Think of it as what a Peloton screen does for cycling: it transforms a solitary, analog activity into a connected, gamified, social experience. Range operators report nearly double the monthly revenue per bay after installing Toptracer, suggesting genuine value creation. If network effects develop around this platform, connecting golfers, enabling leagues, and creating data-driven personalization, Callaway's retained 40 percent stake could prove more valuable than it appears today.

In February 2026, Leonard Green appointed David McKillips as CEO of Topgolf International. McKillips previously ran CEC Entertainment, the parent company of Chuck E. Cheese, where he oversaw global expansion and launched the chain's first membership program. The choice of a family entertainment veteran signals Leonard Green's intent to optimize Topgolf as a venue-based entertainment business rather than a golf technology platform, a pragmatic bet on operational efficiency over blue-sky innovation.

IX. Playbook: Business and Investing Lessons

The Callaway saga offers a rich set of lessons for investors and operators. Start with the most fundamental: brand as competitive advantage. Ely Callaway's "demonstrably superior and pleasingly different" philosophy wasn't just a tagline. It was a strategic filter that ensured every product either earned the right to charge a premium or didn't ship. When the company drifted from DSPD after Ely's death, it commoditized. When Chip Brewer returned to it, the brand recovered. The lesson is that brand equity in consumer products is real but fragile. It must be actively maintained through product quality and marketing investment. The moment a premium brand ships mediocre products, the moat erodes faster than you'd expect.

Second, the cyclicality trap. Golf equipment is inherently boom-bust. Product cycles drive upgrade purchases, but USGA equipment limits constrain how much performance improvement each generation can deliver. When the performance gap between the new driver and the three-year-old driver narrows, the upgrade cycle lengthens, and revenue stalls.

This is worth dwelling on because it's the fundamental structural challenge of the entire industry. The USGA regulates club performance to preserve the integrity of the game. Clubhead size is capped at 460 cubic centimeters. The "coefficient of restitution," a measure of how springy the club face can be, is limited. These regulations mean that a $600 driver from 2026 is only marginally better than a $600 driver from 2023. For the consumer, that makes the upgrade decision harder to justify each cycle.

This is the structural challenge that drove Brewer toward diversification, first with TravisMathew and Jack Wolfskin, then with Topgolf. The instinct was correct: a pure-play equipment company in a mature market with regulatory constraints on innovation faces a ceiling. The question is whether the chosen diversification creates genuine synergy or just adds complexity.

Third, the founder's dilemma. Ely Callaway was irreplaceable in the way that only founder-visionaries can be. His death in 2001 created a vacuum that no hired executive could fill for over a decade. It took Chip Brewer, a different kind of leader with a different skill set, to stabilize the company. The contrast illuminates a recurring pattern: founders build through vision and force of personality; operators sustain through process and discipline. Callaway needed both, just at different times. Investors evaluating founder-led companies should always ask: what happens the day after the founder leaves?

Fourth, platform thinking and its limits. The Topgolf merger was an attempt to build an integrated platform: equipment, experiences, and digital ecosystem, creating a flywheel where each element reinforced the others. In theory, the logic was compelling. A Topgolf visitor discovers the joy of golf, buys Callaway equipment, uses Toptracer at their local range, and remains engaged in the Callaway ecosystem.

In practice, the operational complexity was overwhelming. Running a precision engineering company and a chain of entertainment venues simultaneously requires entirely different capabilities, cultures, and capital allocation frameworks. The engineering team in Carlsbad needed patient R&D investment; the venue team in Dallas needed rapid operational execution. The financial reporting became a complex exercise in segment allocation. Investors couldn't easily model or value the combined entity.

The separation validates what many conglomerate skeptics have long argued: the "synergy premium" of diversified businesses often exists only in PowerPoint presentations. The most powerful synergies, brand visibility and customer exposure, can often be captured through partnership rather than ownership.

Fifth, the experience economy thesis. Topgolf's concept was genuine innovation. It brought millions of non-golfers into contact with the sport in a low-pressure, social environment. The underlying secular trend, consumers preferring experiences over things, is real and enduring.

But translating that trend into durable profitability is harder than it looks when the experience requires high-cost physical venues with significant fixed operating expenses. Every Topgolf venue is, at its core, a real estate bet: a long-term lease in a specific market, exposed to local economic conditions, weather patterns, and competitive dynamics. When the experiences work, the unit economics can be attractive. When they don't, you have a very expensive building with limited alternative uses.

The lesson for investors evaluating experience-economy businesses: concept attractiveness does not equal margin attractiveness. Unit economics matter as much as the brand story.

Finally, capital allocation discipline. Callaway acquired Jack Wolfskin for $476 million and sold it for $290 million. The Topgolf merger valued the entertainment business at roughly $2 billion; the sale to Leonard Green valued it at $1.1 billion. These are not trivial write-downs. They represent real value destruction for shareholders.

The aggressive acquisition strategy under Brewer created optionality but also concentrated risk. When the bets worked, as with TravisMathew and Chrome Soft, they meaningfully enhanced the business. When they didn't, as with Jack Wolfskin and Topgolf, the losses were enormous. The lesson is not that acquisitions are inherently bad, but that the bar for transformational deals should be much higher than for bolt-on acquisitions.

The current return to a simpler, more focused portfolio suggests that management has absorbed the lesson: in cyclical, capital-intensive businesses, balance sheet strength and operational focus create more value than transformational ambition. The $200 million share buyback, the debt paydown, and the conversion to cash speak to a company that has learned, perhaps painfully, the value of financial discipline.

X. Porter's Five Forces and Hamilton's Seven Powers Analysis

Start with the competitive structure of Callaway's industries through Michael Porter's framework.

The threat of new entrants is moderate. In golf equipment, the barriers are real but not insurmountable. Developing a credible club line requires significant R&D investment, particularly in materials science, aerodynamics, and manufacturing precision. Tour relationships, where professional golfers validate equipment through competitive use, take years and millions of dollars to build. Brand recognition matters enormously in a purchase decision that's partly rational and partly emotional.

These factors protect incumbents like Callaway, Titleist, TaylorMade, and Ping. However, the internet has changed the game for challengers. Direct-to-consumer brands like PXG, founded by billionaire Bob Parsons, and Sub70 have demonstrated that you can enter the market by cutting out retail intermediaries and investing in digital marketing and social media. PXG in particular has used aggressive pricing transparency, premium materials, and celebrity endorsements to build a meaningful niche. None has seriously threatened the major brands' overall market share, but they've proved that barriers to entry are lower than the incumbents would like.

The bargaining power of suppliers is generally low to moderate. The raw materials for club manufacturing, titanium alloys, carbon fiber composites, and steel, are available from multiple sources. Callaway doesn't face the kind of supplier concentration that would give input providers pricing leverage.

One notable exception is tour professionals themselves, who function as "suppliers" of credibility. When Xander Schauffele wins a major with a Callaway driver, that's worth millions in implied endorsement value. A handful of elite players command significant endorsement contracts because their equipment choices influence millions of consumers. The power of these individual athletes to extract value is high and rising, especially as LIV Golf has created a competing marketplace for player endorsements.

The bargaining power of buyers is high and a persistent challenge. Individual golfers are price-sensitive and brand-promiscuous. Unlike, say, Apple users who are locked into an ecosystem, golfers switch brands with zero friction. Each purchase is essentially a new decision. Survey data consistently shows that a better-performing product will lure golfers away from their current brand without significant loyalty friction.

Retail consolidation has intensified this dynamic. Golf Galaxy, owned by Dick's Sporting Goods, and PGA Tour Superstore command significant shelf space and negotiate aggressively on pricing. Online retail has added price transparency. For premium equipment costing $500 or more per club, buyers do their homework, reading reviews on GolfWRX, watching YouTube comparisons, and visiting fitting studios before making a decision.

The threat of substitutes is significant and structural. In equipment, the USGA's regulatory limits on club performance mean that technology improvements are incremental, which makes used and refurbished clubs an increasingly attractive substitute. Platforms like Callaway Pre-Owned, GlobalGolf, and the secondary market on eBay have created a robust aftermarket that competes directly with new equipment sales.

Club fitting services, where a professional analyzes your swing and optimizes your existing equipment's settings, also reduce the need for frequent new purchases. A good fitting can extract performance gains comparable to buying a new club at a fraction of the cost.

More broadly, golf competes for recreational time and spending against every other leisure activity, from fitness to travel to home entertainment. The competition for the consumer's discretionary dollar is relentless.

Industry rivalry is very high, and this is perhaps the most important force in the framework. The golf equipment market is dominated by four major players: Callaway, TaylorMade, Titleist (Acushnet), and Ping, with Cobra (owned by Puma) and several smaller brands fighting for the remaining share.

Product cycles are compressed, with new models every 12 to 18 months. Marketing spend is heavy. Tour endorsements are expensive. Promotional activity during inventory transitions compresses margins. TaylorMade, now backed by private equity through Centroid Investment Partners, has the financial flexibility to invest aggressively, and in 2025 was reportedly exploring a sale at a $3.5 billion valuation, a mark that underscored the value the private market assigns to a well-run pure-play equipment brand. Titleist's parent Acushnet is a public company with $2.56 billion in 2025 revenue and a fortress position in golf balls. Ping, family-owned and intensely focused on engineering, commands fierce loyalty.

The competitive intensity in this market is among the highest in consumer sporting goods. No single player dominates, and the constant innovation arms race, driven by USGA regulations that limit how much performance can actually improve each cycle, means that marketing and brand perception often matter as much as actual product performance. For investors, this means that margins in golf equipment are structurally capped by competitive dynamics, not just by demand.

Now apply Hamilton Helmer's Seven Powers framework to assess Callaway's durable competitive advantages.

Scale economies are moderate. Callaway's R&D costs, which include AI-designed club faces, advanced materials testing, and tour-validation processes, are spread across large production volumes. This creates a meaningful advantage over smaller competitors who can't amortize the cost of a supercomputer-designed driver face across millions of units.

But this isn't a winner-take-all market. Four to five major players all achieve sufficient scale to compete effectively. Acushnet, with $2.56 billion in revenue, is actually larger than Callaway. TaylorMade, though private, is believed to be in a similar revenue range. Scale helps but doesn't dominate.

Network effects have been weak historically but may be emerging around Toptracer. Traditional golf equipment has zero network effects; one golfer's purchase doesn't make the product more valuable to another golfer.

However, the Toptracer platform, now partially owned through the retained Topgolf stake, has the potential to create network dynamics. Imagine a world where 50,000 driving ranges globally are connected through Toptracer, golfers compete in virtual leagues against friends across cities, and the data from millions of practice sessions informs personalized club recommendations. That's a network effect.

If Toptracer becomes the default digital layer on driving ranges globally, and if that creates a community of connected golfers, the network effects could become meaningful. This is speculative but worth monitoring as a potential source of future value for the retained stake.

Counter-positioning was Callaway's original power, and arguably its most important one historically. When Ely Callaway launched Big Bertha, the oversized driver forced incumbents into a classic innovator's dilemma: follow Callaway into oversized designs and effectively cannibalize their existing premium product lines, or ignore the trend and lose market share.

The Topgolf merger was another counter-positioning attempt: pure equipment players can't easily replicate an integrated equipment-plus-entertainment model. However, this power has faded on both fronts. In equipment, all competitors now offer oversized, forgiving designs. And the Topgolf counter-position proved harder to execute than to conceive. TaylorMade could theoretically partner with or invest in entertainment venues without merging with one. Five Iron Golf, a competitor in the urban indoor golf space, signed deals with multiple equipment brands simultaneously.

Switching costs are low, and this is Callaway's persistent vulnerability. Golfers switch brands with minimal friction. There is no installed base lock-in, no data portability issue, and no learning curve that punishes switching. A golfer who plays Callaway irons this year might play TaylorMade next year without any penalty.

Topgolf memberships create modest stickiness, and club fitting data might create some retention, but these are marginal effects. The golf equipment industry fundamentally lacks the switching costs that create durable competitive advantages in technology, healthcare, or enterprise software.

Branding is Callaway's strongest power. In equipment, Callaway stands for premium performance, innovation, and accessibility. The Big Bertha heritage still resonates, even if the specific product has evolved. On tour, Callaway's presence through players like Schauffele validates the brand's credibility with serious golfers. TravisMathew extends the brand into lifestyle. Brand power enables premium pricing, which drives margins. But brand is not unassailable; it requires continuous investment in product quality, marketing, and tour presence.

Cornered resources are moderate. Tour player endorsements, particularly with major champions like Schauffele, provide credibility that competitors can't easily replicate. However, these relationships are contractual, not permanent; players can and do switch brands. The Toptracer technology and its installed base in driving ranges represent a cornered resource of sorts, though the retained stake means Callaway's control is indirect.

Process power is emerging. Callaway's investment in AI-designed club faces, including technologies branded as Jailbreak and Flash Face, represents a genuine process innovation. The company uses supercomputers to model thousands of clubface thickness variations, optimizing the flex pattern to maximize ball speed across the entire face, not just the center. This is the kind of capability that's difficult to reverse-engineer because it requires not just the computing power but the accumulated database of test results and the expertise to interpret them.

But competitors are making similar investments, and the performance gaps between top-tier equipment brands are narrowing. TaylorMade's Twist Face technology and Titleist's MOI optimization represent parallel process innovations. The advantage is real but diminishing over time.

The summary assessment is nuanced. Callaway's competitive position rests primarily on brand and process innovation, with scale economies as a supporting factor. These are real advantages but not unassailable ones. The brand must be continuously refreshed through product innovation and tour validation. The process power in AI-designed clubs is genuine but can be reverse-engineered over time as competitors invest in similar capabilities.

The Topgolf chapter was an attempt to build new powers, particularly counter-positioning and network effects, but the execution challenges and capital requirements proved too great under a single corporate umbrella. The separation acknowledges this reality.

Going forward, Callaway's value as a standalone golf-and-lifestyle company depends on three things: maintaining brand premium in a fiercely competitive equipment market, winning the innovation race in clubs and balls against well-funded rivals, and growing TravisMathew into a meaningful lifestyle brand that extends the company's reach beyond the golf course. The retained Topgolf stake provides optionality without operational distraction.

XI. Bull vs. Bear Case

The bull case for Callaway begins with the balance sheet transformation, which is dramatic by any measure. By repaying $1 billion in term loan debt with proceeds from the Topgolf and Jack Wolfskin sales, the company emerged with just $480 million in borrowings against approximately $680 million in unrestricted cash. S&P upgraded the company's credit rating to BB- following the transaction, reflecting the improved financial position. The $200 million share buyback authorization provides support for a stock that had been beaten down, trading around $14 to $15 in early 2026 after a 170 percent recovery from the April 2025 trough of $5.42. Add in the $258 million convertible notes maturing in May 2026, which the company plans to pay off with existing cash, and you have a genuinely clean balance sheet heading into the second half of the year. The transformation from nearly 5x leverage to near-net-cash in roughly eighteen months is one of the most aggressive deleveraging moves in recent consumer products history.

The core business is performing well. Callaway maintains a leading market share position in golf clubs and a record share in golf balls. The Chrome Tour line has established itself as the only serious alternative to Titleist's Pro V1, and ball sales are growing at mid-single-digit rates.

TravisMathew continues to expand, with new retail stores opening and womenswear approaching 10 percent of brand revenue. The lifestyle brand has particular resonance with younger golfers and non-golfers who appreciate its Southern California aesthetic.

Golf participation is at multi-decade highs, with nearly 29 million on-course players in 2025 and growing diversity in the participant base. If these trends hold, the tailwind for premium equipment is real and represents the most favorable demand backdrop Callaway has experienced since the 1990s.

The retained 40 percent stake in Topgolf provides upside without operational risk. Under Leonard Green's ownership, Topgolf will have a dedicated management team, led by new CEO David McKillips, and a capital structure optimized for venue-based economics.

If the new owners can improve margins, rationalize the venue footprint, and drive same-venue sales growth, the minority stake could appreciate significantly. Leonard Green has a strong track record in consumer-facing businesses, and the appointment of McKillips, with his Chuck E. Cheese turnaround experience, suggests a focus on operational efficiency rather than aggressive expansion.

Callaway gets the optionality of participation without the complexity of management.

The bear case starts with the question of growth. A $2 billion standalone golf equipment and lifestyle company in a mature market faces structural challenges. Revenue guidance for 2026 is roughly flat with 2025 pro-forma numbers, and adjusted EBITDA is actually guided lower, at $170 to $195 million versus $222 million in 2025. Innovation cycles are constrained by USGA regulations.

The competitive environment is brutal. TaylorMade is investing aggressively with private equity backing and commands strong tour presence. Titleist defends its ball market with religious fervor and near-monopoly tour usage. Ping and Cobra continue to innovate in irons and hybrids. And direct-to-consumer brands like PXG are challenging the traditional premium pricing model by selling tour-quality equipment without the retail markup.

If Callaway can't find avenues for organic growth, the multiple will remain compressed.

Tariff exposure is a real and growing risk. The company absorbed roughly $35 million in tariff-related costs in 2025 and has estimated an additional $40 million in incremental tariff expense for 2026, a material headwind for a company guiding to $170 to $195 million in adjusted EBITDA. The Jack Wolfskin sale, at a $186 million loss on invested capital, and the Topgolf disposal at roughly half the acquisition value, represent significant value destruction that bears on management's capital allocation track record. Investors will rightfully question whether the remaining portfolio, even if well-run, can generate enough value to offset the losses incurred during the diversification era.

LIV Golf's fragmentation of the professional tour landscape creates endorsement and marketing challenges. Jon Rahm's move to LIV reduced his visibility on mainstream broadcasts, diminishing the return on Callaway's investment in his endorsement. The innovative Legion XIII team deal helps mitigate this, but it also raises questions about the ROI of endorsement spending in a fractured media landscape.

If the tour landscape remains fractured, the traditional model of using tour wins to drive consumer sales may become less effective. The PGA Tour's pending merger framework with the Saudi Public Investment Fund's LIV Golf remains unresolved, and the outcome could reshape the economics of equipment endorsements for years to come.

Consumer discretionary spending remains sensitive to macroeconomic conditions. Golf equipment and lifestyle apparel are firmly in the discretionary category; in a recession, these are among the first expenditures consumers cut. With the company generating roughly $2 billion in revenue and guiding to adjusted EBITDA of $170 to $195 million for 2026, representing margins of roughly 9 to 10 percent, there is limited room for error. The 2026 EBITDA guidance is actually lower than the $222 million the company generated in 2025 on a continuing operations basis, reflecting tariff headwinds and one-time transition costs associated with the Topgolf separation. Investors waiting for margin expansion may need patience.

It is also worth noting the competitive benchmark. Acushnet, Titleist's parent company, generated $2.56 billion in revenue in 2025 with steadier margins and a near-monopoly in the premium golf ball market, where the Pro V1 commands roughly 73 percent tour usage. TaylorMade, under Centroid Investment Partners, was exploring a potential sale at a reported $3.5 billion valuation in mid-2025, suggesting the private market places a significant premium on pure-play golf equipment brands with growth momentum. Callaway needs to demonstrate it belongs in that conversation as a standalone entity.

The three most critical KPIs for monitoring Callaway going forward are:

First, golf equipment market share in clubs and balls. This is the single most important indicator of brand health and product competitiveness. If Callaway is gaining or holding share, especially in the premium tier, the brand moat is intact. If share is eroding, no amount of financial engineering can compensate.

Second, TravisMathew revenue growth and retail store expansion pace. This is the company's primary organic growth lever outside of equipment. The brand needs to demonstrate that it can scale beyond its current base and that new store openings generate attractive returns. Womenswear, which currently represents roughly 10 percent of TravisMathew revenue, is a particularly important leading indicator. If the brand can establish credibility with female consumers, the addressable market roughly doubles. International expansion will be another important marker of the brand's ceiling.

Third, free cash flow generation. With the debt largely retired and the capital-intensive Topgolf business divested, Callaway should be generating meaningful free cash flow for the first time in years. During the Topgolf era, free cash flow was consumed by venue construction, debt service, and working capital demands. Now, with a simpler business model and lighter balance sheet, the cash generation potential should be significantly improved.

This metric matters because it determines everything else: the pace of share buybacks, the ability to retire the $258 million in convertible notes maturing in May 2026, the R&D investment to maintain product competitiveness, and the optionality to make strategic acquisitions. If free cash flow underperforms, the entire thesis of "simpler is better" falls apart.

XII. Epilogue and What's Next

In early 2026, Callaway Golf Company found itself where it began: a premium golf equipment company with a strong brand, excellent products, and the eternal challenge of growing in a mature market. The Topgolf chapter, from merger in 2021 through sale in 2026, represented the boldest strategic bet in golf business history, and its outcome is a cautionary tale about the gap between strategic vision and operational execution.

The broader context is instructive. Sports entertainment convergence is a genuine trend, as evidenced by the success of concepts like Topgolf, Puttshack, Five Iron Golf, and the proliferation of golf simulators in urban entertainment venues. Technology is transforming traditional industries, from AI-designed club faces to ball-tracking systems that gamify practice to launch monitors that let consumers test equipment with tour-level precision from their garage.

But the lesson from Callaway's experience is that owning these trends through vertical integration is different from benefiting from them as an equipment supplier. Sometimes the smartest play is to sell picks and shovels during the gold rush rather than trying to own the mine. Callaway's marketing partnership with Topgolf post-separation may actually capture most of the brand synergy value without the operational burden, a lesson in the difference between influence and ownership.

For the leadership team, the next chapter requires different skills than the last two. Chip Brewer, who has led Callaway since 2012, shepherded the company through its turnaround, its ambitious expansion, and its painful contraction. The turnaround from 2012 to 2019 demanded operational discipline. The Topgolf era from 2021 to 2025 demanded strategic ambition and portfolio management. The current chapter demands focus, capital discipline, and organic execution. TravisMathew needs to become a billion-dollar brand. The golf ball business needs to continue its march toward Titleist. And the equipment business needs to keep winning the innovation race, one product cycle at a time. In January 2026, the company also launched its new Quantum family of drivers, fairway woods, irons, and hybrids, the first major product cycle under the reconstituted Callaway brand, a reminder that in golf equipment, the product pipeline never stops.

The unanswered questions are compelling. Can golf participation continue to grow, particularly among women, minorities, and young people? The National Golf Foundation data suggests momentum, but sustained growth in a sport that requires time, money, and access to courses is never guaranteed. The post-pandemic surge could prove to be a step-change in the sport's popularity, or it could be a temporary enthusiasm that fades as the novelty wears off and economic pressures mount. The answer will matter enormously for every company in the golf ecosystem.

Will the Topgolf stake prove to be a valuable asset or a stranded investment? Under Leonard Green's ownership, the venues have a chance to achieve the operational efficiency that eluded Callaway: dedicated management, optimized labor models, data-driven pricing, and a focused capital structure. But private equity's characteristic approach of adding leverage and driving toward a five-to-seven year exit creates its own pressures. If Topgolf's same-venue sales growth resumes and margins expand, Callaway's 40 percent stake could be worth multiples of its current implied value. If the venues continue to struggle, the stake could be worth close to zero.

There is also the matter of the broader golf industry's relationship with technology. AI-designed club faces, launch monitors that allow consumers to test equipment with tour-level precision, virtual reality golf simulators, and connected equipment that tracks performance data are all transforming how golf is played, practiced, and consumed. Callaway's R&D capabilities position it well in this evolving landscape, but the company will need to invest continuously to stay ahead of competitors who are making similar bets.

Callaway Golf's story, from Ely Callaway's Palm Springs garage to a $4 billion conglomerate and back to a focused $2 billion equipment-and-lifestyle company, is ultimately about the courage to transform and the wisdom to course-correct. Ely taught the company that bold product bets create brands. Chip Brewer taught it that operational discipline sustains them. And the Topgolf chapter taught everyone that even the most compelling strategic narrative must eventually reconcile with the economics of execution.

In golf, as in business, the scorecard doesn't lie.

XIII. Further Reading and References

-

"The Unconquerable Game" by Ely Callaway Jr. (completed by Nicholas Callaway) - The founder's memoir, published posthumously, capturing his philosophy and the Big Bertha revolution.

-