Monster Beverage: The $50 Billion Energy Empire

Introduction & Episode Roadmap

In the sprawling universe of consumer brands, few stories are as improbable as Monster Beverage. Here is a company that controls roughly 39 percent of the global energy drink market—a category now worth more than $80 billion—and trails only Red Bull in worldwide dominance. Its stock has delivered a total return exceeding 444,000 percent over three decades, making it the single best-performing stock in the S&P 500 over that period. Not Apple. Not Amazon. Not Nvidia. A beverage company headquartered in Corona, California, that sells carbonated drinks in black cans with a neon green claw mark.

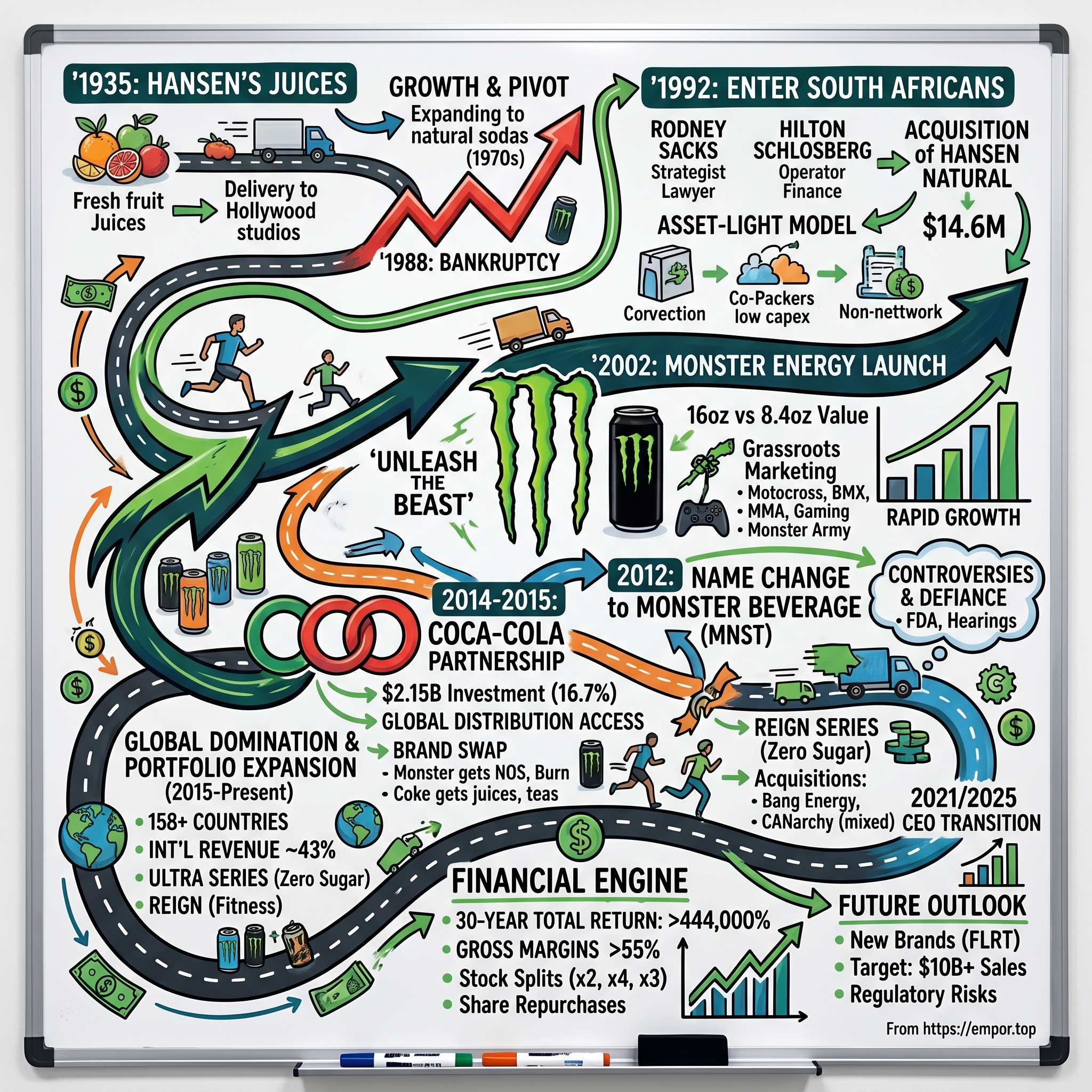

But the truly astonishing part is not what Monster is today. It is where it came from. The company that would become Monster Beverage was founded in 1935 as a family juice operation delivering fresh-squeezed orange and apple juice to Hollywood film studios. It went bankrupt. It was rescued from obscurity by two South African lawyers who had never run a beverage company. They paid $14.6 million for a business with twelve employees and $17.5 million in annual sales, no factory, and a brand that most Americans had never heard of.

What followed was one of the most remarkable corporate transformations in American business history—a story of radical reinvention, strategic patience, and a single partnership decision that unlocked global distribution overnight. The journey from Hansen's Fruit and Vegetable Juices to a nearly $80 billion energy drink empire spans nine decades, but the real action unfolds in just two pivotal chapters: the creation of Monster Energy in 2002, and the Coca-Cola alliance in 2014. Everything before was prologue. Everything after was execution.

Think about what that means in practical terms. In an era when investors pour trillions into semiconductor companies, cloud platforms, and artificial intelligence startups searching for the next transformative technology, the single greatest wealth-creating stock of the past generation was a company selling flavored caffeine water in aluminum cans. No patents. No network effects. No proprietary algorithms. Just a brand, a distribution partnership, and thirty years of disciplined execution.

This is the story of how an obscure juice company became one of the greatest wealth-creation machines the stock market has ever seen—and what its playbook reveals about brand building, strategic partnerships, and the art of knowing exactly when to reinvent yourself.

The Hansen's Era: From Fresh Juice to Natural Sodas (1935–1990)

Los Angeles in the 1930s was a city of reinvention. The film industry was booming, the population was exploding, and entrepreneurs of every stripe were drawn to Southern California's promise of opportunity. Among them was Hubert Hansen, a man with a simple idea: sell fresh, unpasteurized fruit and vegetable juices to the people who made movies.

Hansen founded his namesake business in 1935, enlisting his three sons to help run what was essentially a small-scale juice delivery operation. The business model was straightforward—source fresh produce, press it into juice, and deliver it to the film studios scattered across Los Angeles. In an era before cold-pressed juice bars and wellness smoothies became cultural phenomena, Hansen's was doing something genuinely novel. Picture a delivery truck pulling up to the back lots of Paramount or Warner Bros., unloading crates of fresh orange, carrot, apple, strawberry, and banana juices for the actors, directors, and crew working twelve-hour days under California sun. The studio lots became his primary market, and for a time, the business thrived on Hollywood's appetite for fresh, wholesome refreshment.

The company grew modestly through the postwar years. In 1946, Hansen opened a larger production facility to accommodate expanding demand. Distribution crept outward from Los Angeles to the broader western states and eventually reached Hawaii and the East Coast. But this was still a small, family-run operation selling a perishable product in a regional market. The juice business, for all its appeal, was constrained by spoilage, limited shelf life, and the brutal economics of fresh produce distribution. Every day that a bottle sat on a shelf was a day closer to obsolescence. The margins were thin, the logistics were punishing, and the competition from larger producers was relentless.

The first significant pivot came in the late 1970s, when Hubert's grandson Tim Hansen recognized an emerging consumer trend that would reshape the American food landscape. Health-conscious Californians—the same demographic that was embracing yoga, organic produce, and granola—were increasingly interested in natural beverages: sodas and juices made without preservatives, caffeine, sodium, or artificial flavors. In 1977, Tim formed Hansen Foods, Inc., obtaining a license to use the family name. A year later, he launched Hansen's Natural Sodas, transforming the company from a juice delivery service into a packaged beverage brand.

It was a prescient move. The natural foods movement was still in its infancy—Whole Foods Market would not be founded until 1980—and Hansen's positioned itself at the vanguard. Sales climbed through the early 1980s, reaching an estimated $50 million at their peak. The company was riding a genuine cultural wave, and Tim Hansen believed the momentum would carry them further still.

But ambition outpaced execution. The company invested heavily in a new factory to support its expansion, taking on debt that its sales could not sustain. The economics of competing in packaged beverages are brutally unforgiving. Distribution costs are high. Shelf space in grocery stores and convenience shops is fiercely contested. And the established players—Coca-Cola, PepsiCo, Dr Pepper—had decades of experience, vast distribution networks, and marketing budgets that dwarfed anything Hansen could muster. By the late 1980s, Hansen's was in serious trouble. Revenue had plateaued, debt service was consuming cash, and the factory that was supposed to fuel growth was instead draining the company's finances.

In 1988, Hansen's filed for bankruptcy. The factory was lost. The brand, however, survived—acquired out of bankruptcy by California CoPackers Corporation in January 1990, which continued operating under the Hansen Beverage Company name. It was a cautionary tale about the gap between a good product and a viable business. Hansen's had a recognizable brand and a loyal niche following, but it lacked the capital, distribution infrastructure, and strategic vision to compete at scale against companies with orders of magnitude more resources.

The company needed a fundamentally different kind of leadership—people who could look at a failed juice brand and see not what it was, but what it could become. What it got, improbably, was a pair of South African lawyers with no beverage industry experience—and a willingness to see possibility where others saw only a failed juice company.

Enter the South Africans: Rodney Sacks & Hilton Schlosberg (1989–2002)

Rodney Cyril Sacks grew up in Johannesburg, South Africa, the son of a Lithuanian-Jewish family. He attended the University of the Witwatersrand—known colloquially as "Wits," South Africa's most prestigious university—where he earned both a law degree and a postgraduate diploma in tax law. Sacks was exceptionally talented. He joined Werksmans, South Africa's largest and most prestigious corporate law firm, a powerhouse that handled the country's most complex mergers, acquisitions, and restructurings. There, he became the youngest partner in the firm's history, a distinction that reflected both his intellect and his relentless work ethic.

Over nearly two decades at Werksmans, Sacks rose to senior partner, building a reputation as one of the country's sharpest dealmakers and corporate strategists. He advised on transactions that shaped South African industry, developing an instinct for identifying undervalued assets and structuring deals that aligned incentives among complex groups of stakeholders. This was not the background of a typical beverage executive. It was the background of someone who understood how businesses were bought, sold, restructured, and transformed.

But by the late 1980s, South Africa was a country in turmoil. The apartheid regime was crumbling, political uncertainty was rampant, and many professionals were contemplating emigration. The transition to democracy was inevitable but unpredictable, and many white South Africans with transferable skills were making contingency plans. In August 1989, after almost twenty years at Werksmans, Sacks packed up his family and moved to California. He was roughly forty years old, starting over in a new country, with formidable legal and deal-structuring skills but no obvious path in the American business landscape.

Hilton Hiller Schlosberg had followed a different trajectory from the same starting point. Also educated at Wits—where he earned an MBA in 1976—Schlosberg had moved into the corporate world rather than law. He relocated to London to work at J. Bibby & Sons, a British conglomerate with interests spanning chemicals, agriculture, and industrial products. His background was more operational and financial than Sacks's—an accountant and entrepreneur by temperament, with experience in managing complex businesses across borders. Where Sacks was the strategist who saw the big picture, Schlosberg was the operator who understood the details: cost structures, cash flow management, supply chain logistics, the nuts and bolts of running a business day to day.

The two men reconnected in Southern California through a Los Angeles investment banker who was putting together deals for South African expatriates looking to acquire American businesses. The chemistry was immediate. Sacks brought legal acumen, dealmaking instincts, and strategic vision. Schlosberg brought financial discipline, operational sensibility, and a relentless attention to detail. Together, they began scanning for acquisition targets—businesses that were undervalued, undermanaged, or overlooked by the market, where their combination of skills could unlock potential that others had missed.

Their approach was methodical. In 1990, the duo led a consortium that raised approximately $5 million from friends and family back in South Africa to acquire control of Unipac Inc., a publicly traded shell company based in Irvine, California. This gave them a listed vehicle—a platform from which to make acquisitions and build a business in the American market. It was a technique that Sacks, the corporate lawyer, understood intimately: use a public shell to acquire an operating business, and you get both the business and access to public capital markets in a single move.

What they found for that shell was Hansen Natural Corporation—a company that, on paper, looked like a disaster. It had just emerged from bankruptcy. It had no factory. It had twelve employees. Its annual sales were a mere $17.5 million. The brand was known, if at all, as a niche natural soda company with limited distribution in the western United States. Most acquirers would have walked away. Sacks and Schlosberg saw something else: a brand name with goodwill, an asset-light model that could be rebuilt without massive capital expenditure, and a product category—natural beverages—that had genuine consumer appeal if properly managed.

On July 27, 1992, their consortium acquired Hansen Natural for $14.6 million. Sacks became chairman and CEO; Schlosberg became vice-chairman and president. The arrangement was unusual—two immigrants from the same university, with no beverage industry experience, taking control of a struggling American juice-and-soda company. But Sacks and Schlosberg had something that Hansen's previous management lacked: a dealmaker's eye for undervalued assets and a willingness to think in entirely different terms about what the company could become.

Their early years were spent stabilizing the business and learning the beverage industry from the inside. Without a factory, they adopted an asset-light model out of necessity—outsourcing production to co-packers, which kept capital expenditures low and allowed the company to focus on branding, product development, and distribution. This operational architecture, born from the constraints of a post-bankruptcy company with no manufacturing assets, would prove to be one of Monster's most enduring strategic advantages. Many business school case studies celebrate asset-light models as deliberate strategic innovations. In Monster's case, it was simply the only option available—and it turned out to be brilliant.

The co-packing model meant that Hansen did not need to invest millions in equipment, maintenance, or labor. Instead, it could direct every available dollar toward the activities that actually created value in the beverage industry: developing products, building brand awareness, and expanding distribution. The company's capital efficiency was remarkable from the start, generating returns on invested capital that far exceeded what a traditional manufacturing operation could achieve.

In 1996, Sacks and Schlosberg made a move that hinted at the transformation to come. They launched an "energy smoothie"—a juice-based drink fortified with taurine and other functional ingredients that were beginning to appear in beverages marketed as performance enhancers. It was not yet an energy drink in the modern sense, but it signaled an awareness that the future of beverages lay not in competing with established soda brands on their terms, but in creating new categories that commanded premium pricing and attracted younger, more adventurous consumers.

For the next several years, Hansen Natural continued to grow modestly, expanding its natural soda and juice lines while experimenting with functional beverages. Revenue climbed from $17.5 million at the time of acquisition to roughly $80 million by 2001—steady growth, but nothing that would have attracted the attention of Wall Street or signaled what was about to happen. Sacks and Schlosberg were watching the market carefully, and what they saw unfolding in the late 1990s and early 2000s would change everything—not just for their company, but for the entire beverage industry.

The Monster Energy Creation Story (2002–2008)

By the turn of the millennium, Red Bull had arrived in America and was rewriting the rules of the beverage industry. The Austrian company, founded by Dietrich Mateschitz after discovering a Thai energy tonic called Krating Daeng during a business trip to Bangkok, had created an entirely new category—energy drinks—and was growing at a pace that stunned established players. Red Bull's slim silver-and-blue cans were everywhere: on college campuses, in nightclubs, at extreme sports events, mixed with vodka at bars. The company spent lavishly on marketing—sponsoring Formula One teams, building its own media empire, famously sending Felix Baumgartner to jump from the edge of space—but sold a single product in a single size at a premium price.

By 2001, Red Bull owned the American energy drink market almost entirely. The drink had become synonymous with the category itself, the way that Kleenex means tissue or Xerox means photocopy. Every major beverage company had noticed the phenomenon, but none had found a way to meaningfully challenge Red Bull's dominance. Coca-Cola had tried with KMX. PepsiCo had tried with Adrenaline Rush. Both had failed. The common assumption was that energy drinks were a one-brand category—that Red Bull was the energy drink, and there was no room for a second player.

Rodney Sacks and Hilton Schlosberg did not accept that assumption. They recognized both the opportunity and the vulnerability in Red Bull's position. Red Bull had proven that consumers would pay premium prices for a caffeinated, functional beverage. But Red Bull's approach was also curiously constrained—one product, one can size, one brand identity centered on European sophistication and aspirational lifestyle marketing. There was room, Sacks and Schlosberg believed, for a distinctly American energy drink: bigger, bolder, more aggressive, and priced to deliver more product for roughly the same money.

In April 2002, Hansen Natural launched Monster Energy. The product debuted in a sixteen-ounce can—double the size of Red Bull's standard 8.4-ounce offering—at a comparable price point. The value proposition was immediately clear to any consumer standing in a convenience store: twice the drink for roughly the same cost. In a country that had embraced the Super Size mentality, where bigger was instinctively perceived as better, the sixteen-ounce can was a masterstroke of product design.

But the genius of Monster was not just in the sizing. It was in the brand. The can itself was a statement of intent. Designed by McLean Design, a California-based branding firm, the Monster can featured a jet-black background slashed by a vibrant green "M"—three jagged lines that looked like claw marks ripped through the metal by some unseen beast. It was aggressive, visceral, and unmistakable from thirty feet away on a convenience store shelf. Where Red Bull projected sleek European cool—silver cans, minimalist design, the impression of alpine sophistication—Monster projected American wildness. The tagline was equally blunt: "Unleash the Beast."

The design language communicated something deeper than product attributes. It communicated identity. Buying a Monster was not just choosing a beverage. It was choosing a side. It was declaring allegiance to a certain kind of energy—raw, unpolished, unapologetic. This was not the drink of investment bankers pulling all-nighters or European clubbers sipping vodka-Red Bulls. This was the drink of motocross riders, gamers, skateboarders, and anyone who identified with the culture of controlled chaos.

The marketing strategy that followed was revolutionary for the beverage industry. Rather than spending millions on traditional television advertising—the playbook of Coca-Cola, Pepsi, and every other major drink company—Monster went grassroots. The company embedded itself in the subcultures that its target demographic already inhabited: motocross, BMX, skateboarding, snowboarding, mixed martial arts, and eventually gaming and music. Monster sponsored athletes, events, and tours. It put its logo on everything from NASCAR vehicles to UFC octagons to the helmets of freestyle motocross riders.

In 2005, the company formalized this approach with the Monster Army—an athlete development program for aspiring extreme sports athletes aged 13 to 21. The program provided sponsorship, mentorship, and visibility to young athletes who were not yet established enough to attract traditional endorsement deals. It was simultaneously a marketing initiative and a talent pipeline, building loyalty among both the athletes themselves and the audiences who followed their careers. Every Monster Army rider who made it to the professional ranks carried the brand with them, creating an authenticity that paid advertising could never replicate.

This was not just marketing. It was cultural positioning of the highest order. Monster was not selling a drink so much as selling membership in a tribe. The brand stood for adrenaline, rebellion, and a kind of gleeful recklessness that resonated deeply with young men in their teens and twenties—precisely the demographic that consumed energy drinks in the largest volumes. Every sponsorship, every event activation, every branded monster truck was a reinforcement of the same message: this brand understands you, and it does not care what your parents think.

The distribution strategy, meanwhile, was pragmatic and incremental. Hansen Natural leveraged its existing relationships with beer and soda distributors to get Monster onto convenience store shelves and into gas stations—the high-traffic retail environments where impulse energy drink purchases happen most frequently. Anheuser-Busch's distribution network became an early and crucial channel partner. The company's asset-light model meant it could scale distribution without building factories. Co-packers produced the liquid; distributors moved the cans; Monster focused on the brand.

The results were extraordinary. Within three years of launch, Monster Energy had captured 18 percent of the US energy drink market. By 2005, what had been a modest Hansen Natural stock trading under a dollar was beginning a multi-year run that would turn early investors into millionaires. Revenue surged. By 2012—just a decade after Monster Energy's debut—Hansen Natural's annual revenue had climbed to roughly $2 billion, up from $80 million in 2001. That is 25x revenue growth in a single decade, driven almost entirely by a single product line.

What Sacks and Schlosberg had achieved was a textbook case of category disruption through positioning rather than product superiority. They did not invent the energy drink—Red Bull did that. But they identified the gap in Red Bull's positioning, created a brand that owned a different emotional territory, offered superior perceived value through larger serving sizes, and executed a marketing strategy that built cultural relevance without the massive advertising budgets that traditional beverage companies deployed. Monster did not outspend Red Bull. It out-positioned it.

The implications for the company's financial profile were profound. Here was a business with minimal capital expenditure, no factories to maintain, rapidly growing revenue, and expanding margins—all driven by a brand that was becoming more valuable with every motocross event it sponsored and every convenience store cooler it occupied. The financial architecture was beautiful in its simplicity: manufacture nothing, distribute through partners, invest relentlessly in brand, and let the margins flow. Gross margins held consistently above 50 percent—territory that most consumer products companies can only dream of.

The Name Change & Identity Shift (2008–2014)

By the late 2000s, Hansen Natural Corporation had a problem—a good problem, but a problem nonetheless. More than ninety percent of the company's revenue came from Monster Energy drinks, yet the company was still named after a juice brand from the 1930s. The corporate identity was misaligned with reality. Investors, analysts, and consumers were confused. Was this a natural beverage company or an energy drink company? The name "Hansen Natural" on SEC filings and stock tickers bore almost no relationship to the black cans with green claw marks that were generating virtually all of the company's profits.

On January 5, 2012, shareholders voted to change the corporate name to Monster Beverage Corporation. When the markets opened on January 9, the company began trading under the ticker symbol MNST, replacing the old HANS ticker. "More than ninety percent of the business today is represented by the Monster brand," Rodney Sacks told shareholders. The rebrand was not cosmetic. It was a declaration of strategic intent: this company was an energy drink company, pure and simple, and it intended to pursue that identity with undivided focus.

The signal to the market was unmistakable. In a world where conglomerates and diversified companies often trade at a discount to their sum-of-parts value—what investors call the "conglomerate discount"—Monster was doing the opposite. It was shedding any pretense of diversification to become the purest possible play on a single, fast-growing category. For investors who wanted energy drink exposure, Monster was now the only dedicated vehicle. The name change alone likely improved the stock's multiple.

The years surrounding the name change were also a period of aggressive product line expansion within the energy drink category itself. Monster had launched with a single flagship product, but the company now rolled out an increasingly diverse portfolio designed to capture different consumer occasions and demographics. Java Monster blended coffee and energy drink cultures—a caffeinated, creamy beverage aimed at consumers who wanted their morning caffeine hit in a more exciting package than a Starbucks cup. Juice Monster combined tropical fruit flavors with the energy formula, appealing to consumers who wanted something less intense than the original. Monster Rehab positioned itself as a post-workout recovery drink with electrolytes and tea, targeting the growing fitness-conscious segment. Each sub-brand targeted a slightly different occasion or consumer segment while reinforcing the overarching Monster identity. The claw mark logo appeared on every can, ensuring that brand equity accumulated in a single place regardless of which variant the consumer chose.

International expansion accelerated in parallel. Monster had been primarily a North American brand through its first decade, but Sacks and Schlosberg recognized that the energy drink category was growing even faster overseas than domestically. The challenge was distribution. Building an international distribution network from scratch would require enormous capital and operational complexity—resources that a company built on an asset-light model was poorly positioned to deploy. Monster needed a partner, and not just any partner. It needed the partner.

This period also brought unwanted attention from regulators and politicians—the kind of controversy that would have rattled a less self-assured management team. Between 2003 and 2012, the FDA received reports of five deaths allegedly linked to Monster Energy consumption. The most publicized case involved a fourteen-year-old Maryland girl who died from cardiac arrhythmia after consuming two twenty-four-ounce cans of Monster Energy; an autopsy attributed the death to caffeine toxicity. Senators Dick Durbin and Richard Blumenthal called on the FDA to investigate the safety of energy drinks. Congressional hearings followed, generating negative headlines and raising the specter of regulatory crackdowns that could cripple the entire category.

Monster's response was characteristically defiant. The company pointed out that the FDA's adverse event reports did not constitute proof of causation—a position the FDA itself acknowledged. A single can of Monster Energy contained less caffeine per ounce than a typical coffeehouse brew. Energy drinks were classified as dietary supplements under a 1994 congressional exemption, which meant they faced different regulatory scrutiny than conventional beverages. Monster fought the narrative aggressively, investing in legal defense and public relations while refusing to reformulate or soften its brand identity.

Here is where the story gets interesting from a brand perspective. If anything, the controversy enhanced Monster's rebellious image among its core demographic. Being attacked by senators and health advocates only made the brand feel more dangerous—and more appealing to young consumers who defined themselves in opposition to institutional authority. The congressional hearings became, perversely, some of the most effective marketing Monster ever received. Every news segment about the dangers of energy drinks featured the green claw mark prominently on screen, driving awareness among exactly the audience Monster most wanted to reach.

The regulatory battles did not materially damage Monster's financial performance. Revenue continued to grow. Margins continued to expand. But the experience underscored a structural vulnerability: Monster's entire business depended on a single product category that faced persistent questions about health effects and the possibility of stricter regulation. It was a risk that investors needed to price in, even as the stock continued its relentless climb.

For Sacks and Schlosberg, the key strategic question was becoming urgent. Monster had proven it could build a dominant brand in the United States. But to become a truly global company—to capture its share of the energy drink opportunity in Europe, Asia, Latin America, and Africa—it needed distribution infrastructure on a scale that no energy drink startup could build alone. The answer to that question would arrive in the form of the most consequential partnership in Monster's history—and one of the most elegant deal structures in modern consumer products.

The Coca-Cola Partnership: A Masterstroke (2014–2015)

In the summer of 2014, Rodney Sacks and Hilton Schlosberg made the most important phone call of their careers. Or rather, they answered one. The Coca-Cola Company, the world's largest and most powerful beverage distributor, wanted to talk about energy drinks.

To understand why this deal was so transformative, consider the strategic position of each party. Coca-Cola had been watching the energy drink category with a mixture of envy and frustration for more than a decade. The company owned several energy brands—NOS, Full Throttle, Burn, Mother, Relentless, and others—but none had gained meaningful traction against Red Bull and Monster. Collectively, Coke's energy portfolio was an also-ran in the category's fastest-growing segment. The company knew how to distribute beverages to every corner of the globe—it operated the most extensive bottling and distribution network ever built, reaching more than 200 countries—but it could not seem to build an energy drink brand that consumers cared about.

Monster, meanwhile, had the opposite problem. It had built one of the most powerful brands in the beverage industry—a brand that young consumers loved, that competitors envied, and that generated profit margins that made Coca-Cola's own carbonated soft drink business look pedestrian. But Monster sold only 21 percent of its drinks outside the United States. The global energy drink market—which was growing at double-digit rates in Asia, Latin America, and Africa—was largely beyond Monster's reach. Building an international distribution network from scratch would take decades and billions of dollars.

Each company had something the other desperately needed. The deal announced on August 14, 2014, was a masterpiece of strategic alignment that addressed both needs simultaneously.

The financial component was straightforward: Coca-Cola would acquire a 16.7 percent ownership stake in Monster Beverage for $2.15 billion in cash. That alone was noteworthy—a massive premium that reflected Coke's conviction about the energy drink category's growth potential. But the financial investment was almost secondary to the structural arrangements that accompanied it.

First, the brand swap. Monster would transfer its non-energy beverage brands—Hansen's Natural Sodas, Peace Tea, Hubert's Lemonade, and Hansen's Juice Products—to Coca-Cola. In return, Coca-Cola would transfer its energy drink brands—NOS, Full Throttle, Burn, Mother, Relentless, and several others—to Monster. The logic was elegant. Monster wanted to be a pure-play energy company with zero distractions; Coca-Cola wanted Monster's legacy brands for its broader portfolio of non-energy beverages. The swap gave each company exactly what it needed while eliminating internal competition. Hansen's, the brand that had given birth to the entire enterprise, was gone. It was the ultimate act of strategic clarity—trading away your own origin story because the future lay elsewhere.

Second, and most critically, the distribution agreement. Monster would gain access to what Sacks later described as "the most powerful and extensive distribution system in the world"—Coca-Cola's global bottling network. Under a twenty-year agreement, Coca-Cola's bottlers would distribute Monster Energy in markets around the world, replacing Monster's patchwork of regional distributors with a single, unified, and supremely efficient distribution machine. Think about what this meant in practical terms. Coca-Cola's bottlers had spent more than a century building relationships with retailers, optimizing delivery routes, managing cold storage, and ensuring that their products were available in virtually every store, gas station, restaurant, and vending machine on the planet. Monster was now plugging into all of that infrastructure with a single deal.

Third, governance alignment. Two Coca-Cola executives would join Monster's board of directors, ensuring that the strategic partnership was embedded at the highest levels of corporate decision-making. Coca-Cola was not just investing in Monster; it was becoming a structural partner with a vested interest in Monster's long-term success. The agreement also permitted Coca-Cola to increase its stake to 25 percent through open market purchases, but it could not exceed that threshold without Monster's approval—a provision that protected Monster's independence while giving Coke meaningful upside participation.

For a company built on an asset-light model, this was the ultimate outsourcing arrangement: handing distribution to the organization that had perfected it over more than a century. Monster still did not need to build factories or distribution centers overseas. Coca-Cola's bottlers would handle local production and distribution in each market, while Monster would focus on what it did best: building and managing the brand. The capital efficiency was remarkable. Monster could expand globally with minimal incremental investment, generating high-margin revenue growth that flowed almost directly to the bottom line.

The deal closed in June 2015, and the effects were immediate. Monster began rolling out across Coca-Cola's distribution network, entering markets it had never previously served. Germany and Norway were among the first new territories. Within a few years, Monster would be available in over 158 countries—a global footprint that would have taken decades and billions of dollars to build independently.

Wall Street loved the deal, and for good reason. The strategic logic was impeccable. Coca-Cola got exposure to the fastest-growing category in beverages without having to acquire Monster outright and deal with the cultural and operational challenges of integrating an insurgent brand into a corporate behemoth. Monster got global distribution, a strategic partner with unmatched infrastructure, and a $2.15 billion cash infusion that could be deployed for share repurchases and acquisitions. Both companies maintained their independence while locking in a relationship that made each stronger.

The Coca-Cola partnership also solved Monster's international distribution problem in a way that preserved the company's fundamental economic model. Revenue growth continued to translate directly into profit growth with minimal incremental capital investment. The partnership was not a joint venture with shared profits—Monster paid distribution fees to Coca-Cola's bottlers, but it retained the brand economics, the pricing power, and the full benefit of volume leverage. As Monster's international volume grew, its per-unit costs declined while its revenue per unit remained stable or increased.

Over the following years, Coca-Cola gradually increased its ownership stake from the initial 16.7 percent to approximately 19.5 percent, making it Monster's single largest shareholder. The relationship deepened and matured, but the fundamental structure remained unchanged: Coca-Cola provided distribution and capital; Monster provided brand management and product innovation. It was a partnership built on complementary strengths, and it proved to be one of the most value-creating alliances in the history of the beverage industry.

For investors evaluating Monster, the Coca-Cola partnership represented something close to a structural moat. Any competitor seeking to challenge Monster's market position would need not only a compelling brand and product but also access to distribution infrastructure comparable to Coca-Cola's. In practice, that meant the competitive landscape was frozen: Red Bull had built its own formidable distribution system over decades, and Monster had locked in Coca-Cola's. Any new entrant would face an almost insurmountable distribution disadvantage, regardless of how good its product might be. The Celsius story—a brand that achieved impressive growth in the US—illustrated both the opportunity and the limitation: even Celsius, with PepsiCo distribution, struggled to replicate the global reach that Monster enjoyed through Coca-Cola.

Global Domination & Portfolio Expansion (2015–Present)

The years following the Coca-Cola partnership were a period of relentless execution and strategic expansion. Armed with the world's most powerful distribution system, Monster Beverage embarked on a global campaign that transformed it from a primarily North American brand into a truly worldwide presence. By 2025, Monster products were available in more than 158 countries and territories, and international sales had grown to represent 43 percent of total revenue—up from just 21 percent at the time of the Coca-Cola deal. The international growth trajectory remained one of the company's most compelling narratives, with currency-adjusted international sales growing at roughly 16 percent year-over-year through the most recent quarter.

Product innovation accelerated alongside geographic expansion, with Monster pursuing a multi-brand strategy designed to capture different consumer segments without diluting the core brand. The Monster Ultra series—a line of zero-sugar energy drinks in sleek white cans—proved enormously successful, attracting a broader demographic that included women and older consumers who wanted the energy boost without the sugar and calories of the original Monster. Ultra became a cultural phenomenon in its own right, spawning a devoted following on social media and expanding Monster's addressable market well beyond the young male extreme sports enthusiasts who had been the brand's original core. The Ultra line alone grew by 29 percent in the United States in 2025, demonstrating that Monster still had significant room to grow even in its most mature market.

The Reign brand, launched in 2019, targeted a different segment entirely: the fitness and performance market. Positioned as a pre-workout energy drink with zero sugar, BCAAs, CoQ10, and natural caffeine, Reign competed directly in the fitness-focused energy drink subcategory against brands like Bang and Celsius. Its launch demonstrated Monster's willingness to pursue multiple positioning strategies simultaneously within the broader energy drink category, creating a portfolio architecture where different brands addressed different occasions without cannibalizing each other.

For emerging markets where the premium-priced Monster brand was too expensive for mass adoption, the company developed affordable alternatives. Predator and Fury, priced well below Monster's core products, were designed specifically for markets in Asia, Africa, and Latin America where per-capita incomes were lower but the appetite for energy drinks was growing rapidly. This tiered pricing strategy allowed Monster to compete across the full spectrum of the global market—premium in developed economies, accessible in developing ones.

Monster also made two significant acquisitions during this period, with mixed results that revealed both the company's ambitions and its limitations.

In February 2022, the company completed its purchase of CANarchy Craft Brewery Collective for $330 million in cash. CANarchy brought a portfolio of craft beer brands including Cigar City, Oskar Blues, and Deep Ellum—a move that signaled Monster's interest in the alcoholic beverage segment. Schlosberg described it as "a springboard from which to enter the alcoholic beverage sector." Monster subsequently launched The Beast Unleashed, an alcoholic line, in early 2023. However, the alcohol strategy proved far more challenging than anticipated. The craft beer market was in secular decline, consumer preferences were shifting away from beer toward spirits and ready-to-drink cocktails, and the distribution dynamics of alcohol were fundamentally different from those of energy drinks. By early 2025, Monster had recorded total impairment charges of roughly $181.5 million on CANarchy-related assets—a write-down of more than half the original purchase price. It was a sobering reminder that excellence in one category does not automatically translate to another.

The second major acquisition was more directly strategic and more clearly successful. In July 2023, Monster completed the purchase of Bang Energy out of bankruptcy for $362 million. The Bang Energy story deserved its own chapter: Bang had been one of Monster's most aggressive competitors, built by a flamboyant Florida-based entrepreneur named Jack Owoc who positioned the brand around a controversial ingredient called "super creatine" and a marketing strategy heavy on social media influencers and fitness culture. Bang had grown rapidly, briefly threatening to become a serious third force in the energy drink market. But the company's aggressive claims about super creatine's health benefits ran afoul of both science and the law. A California jury ruled in September 2022 that Bang must pay Monster $293 million in damages for false advertising, and Vital Pharmaceuticals—Bang's parent company—subsequently filed for Chapter 11 bankruptcy. Monster's acquisition of its defeated rival was both strategically sound—eliminating a competitor and absorbing its customer base and production facility in Phoenix, Arizona—and a demonstration of the competitive dynamics in this market. Even well-funded challengers with differentiated products and aggressive marketing can find themselves absorbed by the incumbents if they overreach.

The leadership structure also evolved during this period, marking the most significant transition in the company's history. Sacks and Schlosberg had co-led Monster for over three decades—an extraordinarily long and stable partnership by any standard in public company management. In January 2021, Schlosberg was elevated to co-CEO alongside Sacks, formalizing a power-sharing arrangement that had existed informally for years. Then, on March 10, 2025, Sacks notified the board that he would resign as co-CEO. Hilton Schlosberg became sole CEO on June 13, 2025, while Sacks remained as chairman of the board and continued in an employee capacity overseeing marketing, innovation, and litigation through the end of 2026, at a base salary of $900,000 per year.

The transition was carefully choreographed to minimize disruption. Sacks was 75 years old and had been running the company for 33 years. Schlosberg, who had served as president and CFO for 23 of those years before ascending to co-CEO, knew every dimension of the business intimately. The market's reaction was muted—a sign that investors viewed the transition as orderly and well-planned rather than a cause for concern. Both men remained significant shareholders with aligned incentives: Schlosberg held approximately 7.8 percent of the company, and Sacks held approximately 7.6 percent, making them both multi-billionaires whose personal wealth was directly tied to Monster's ongoing success.

Financial Performance & Stock Market Legend

The financial story of Monster Beverage is, by any objective measure, one of the most extraordinary in the history of American equities. An investor who put $10,000 into Monster stock in 1995 would have seen that investment grow to more than $44 million by 2025. The total return over thirty years exceeded 444,000 percent—a figure so large that it almost defies comprehension. Monster did not merely outperform the market. It outperformed Apple, Amazon, Microsoft, Google, and Nvidia over the same period. The best-performing stock of the past three decades in the S&P 500 was not a technology company or a pharmaceutical innovator. It was a company that sells caffeinated beverages in cans.

The stock achieved this through a series of splits—2-for-1 in 2005, 4-for-1 in 2006, 2-for-1 in 2012, 3-for-1 in 2016, and 2-for-1 in 2023—each reflecting the relentless appreciation in the underlying business value. The average annual return of approximately 32.6 percent since the public listing compound, year after year, into one of the great wealth-creation stories of the modern era.

How is this possible? The answer lies in the intersection of several factors that, taken together, created a compounding machine of unusual power.

First, Monster operated in a category with enormous pricing power. Energy drinks command premium prices relative to traditional sodas and juices—typically two to three times the price per ounce—and Monster's brand strength allowed it to raise prices periodically without significant volume erosion. In November 2024, the company implemented a five percent price increase in the United States—a move that would have been risky for a commodity product but was absorbed with minimal consumer pushback in a category where brand loyalty runs deep and price elasticity is low. When consumers are buying identity as much as liquid, they are far less sensitive to a quarter-dollar price change.

Second, the asset-light business model meant that revenue growth translated into profit growth with minimal incremental capital investment. Monster did not build factories (apart from the one acquired with Bang). It did not operate a logistics fleet. It outsourced production to co-packers and distribution to Coca-Cola's bottler network. This meant that gross margins were consistently strong—reaching 55.7 percent in the most recent quarter—and that the company generated enormous free cash flow relative to its revenue base. Compare this to a traditional manufacturer that must continually reinvest in plant and equipment to grow. Monster's incremental dollar of revenue required almost no incremental capital.

Third, management was disciplined and strategic about capital allocation. The company deployed its excess cash primarily through share repurchases, which reduced the share count over time and amplified per-share earnings growth. Monster completed a $3.0 billion share repurchase program and authorized an additional $500 million program in August 2024. The buyback strategy was a quiet but powerful contributor to the stock's long-term performance, ensuring that earnings growth was magnified on a per-share basis. This was not management buying back stock to hit earnings targets; it was a systematic program to return capital to shareholders in the most tax-efficient manner available.

The full-year 2024 results illustrated the company's financial engine. Net sales reached $7.49 billion, up 4.9 percent year-over-year, or 8.4 percent on a currency-adjusted basis—a reminder that the strong US dollar was masking the true growth rate of the underlying business. Adjusted gross profit margins expanded to 54.0 percent, up from 53.1 percent the prior year, reflecting both pricing power and operational efficiency. Foreign exchange headwinds of $247 million reduced reported results but did nothing to diminish the operational strength of the business.

The most recent quarterly results, for the third quarter of fiscal 2025, were even more impressive. Net sales hit a record $2.20 billion, up 16.8 percent year-over-year. Operating income surged 40.7 percent to $675.4 million. Net income reached $524.5 million, up 41.4 percent. Diluted earnings per share of $0.53 beat analyst estimates of $0.48. Gross margins expanded to 55.7 percent. These were not the results of a mature, slow-growth consumer staples company. They were the results of a business that was still accelerating, driven by international expansion, pricing power, and operating leverage.

The company entered 2026 with a market capitalization of approximately $79.5 billion, zero long-term debt, and $2.29 billion in cash on its balance sheet. The stock traded near all-time highs around $80.76 per share, with multiple Wall Street firms raising their price targets—Morgan Stanley, for instance, set a target of $96 in January 2026.

For investors tracking Monster's ongoing performance, two key metrics stand out above all others. The first is international revenue as a percentage of total sales—currently at 43 percent and rising. This metric captures the single most important growth vector for the company: the penetration of Coca-Cola's global distribution network into markets where energy drink consumption per capita remains far below US levels. As long as international mix continues to rise, it signals that the company's most significant growth opportunity is being captured. The second is gross profit margin, which reflects both pricing power and input cost management. Gross margin has expanded from approximately 53 percent to nearly 56 percent over the past two years—a remarkable achievement for a company of this scale. As long as these two metrics trend favorably—international mix rising, gross margins stable or expanding—the fundamental thesis remains intact.

Playbook: Business & Investing Lessons

Monster Beverage's journey from a bankrupt juice company to a nearly $80 billion global brand offers a concentrated set of lessons that apply far beyond the beverage industry. These are not abstract principles—they are observable patterns that drove real wealth creation over three decades.

The most powerful lesson is the value of radical focus. When Sacks and Schlosberg recognized that Monster Energy was their company's future, they did not hedge. They changed the company's name. They swapped away their non-energy brands to Coca-Cola—including Hansen's, the brand that had given the company its identity for seven decades. They organized the entire company around a single category and pursued it with undivided attention. In a business world that celebrates diversification and optionality, Monster's story is a reminder that the greatest returns often come from knowing exactly what you are and refusing to be anything else.

The Coca-Cola partnership illustrates a second principle: strategic alliances can be more valuable than going alone. Many founders resist partnerships because they fear dilution of control or misalignment of incentives. Sacks and Schlosberg took the opposite approach. They invited the world's largest beverage distributor to buy a significant stake in their company and join their board, recognizing that the value created by accessing Coca-Cola's distribution network would far exceed any dilution. The twenty-year distribution agreement was not a concession—it was a force multiplier that transformed Monster from a North American brand into a global one with minimal incremental capital investment. The insight here is that the right partnership does not divide value. It creates new value that neither party could capture alone.

The third lesson is about brand as a competitive moat. Monster did not win because it had a better-tasting energy drink or a more efficient supply chain. It won because it built a brand that resonated emotionally with a massive consumer demographic. The claw mark logo, the extreme sports sponsorships, the rebellious personality—these were not marketing tactics. They were the product itself. In a category where the liquid inside the can is largely interchangeable—caffeine, taurine, B-vitamins, sugar or artificial sweetener, carbonated water—brand is everything. Monster understood this from the beginning and invested accordingly, spending on sponsorships and cultural positioning rather than traditional advertising. The result was a brand that consumers chose not because of what was in the can, but because of what the can said about them.

Contrarian marketing—embracing controversy rather than running from it—is a fourth lesson. Most consumer companies spend millions on PR to avoid negative headlines. Monster leaned into its dangerous image, treating congressional hearings and health scares as brand-building opportunities rather than existential threats. This is not a strategy that works for every company. But for a brand whose entire identity was built on rebellion and edge, the controversy was a feature, not a bug.

The founder-led longevity of the Sacks-Schlosberg partnership is a fifth lesson. The two men ran Monster Beverage together for more than three decades—a duration of leadership continuity that is almost unheard of in public companies, where the average CEO tenure is roughly five years. Their complementary skill sets (Sacks the strategist and dealmaker, Schlosberg the operator and financial engineer), their shared cultural background, and their alignment as significant shareholders created a governance structure that prioritized long-term value creation over quarterly performance management. The company never lurched from one strategic initiative to another. It evolved deliberately, making a small number of large, consequential decisions—launching Monster Energy, rebranding the company, partnering with Coca-Cola—and then executing patiently for years.

The asset-light model deserves particular attention. By outsourcing production and distribution, Monster avoided the capital intensity that characterizes most manufacturing businesses. This allowed the company to generate extraordinary returns on invested capital, deploy excess cash into share repurchases, and maintain the financial flexibility to pursue acquisitions when opportunities arose. The model was born from necessity—Hansen's had lost its factory in bankruptcy—but it became a deliberate strategic choice that gave Monster a structural advantage over competitors who bore the costs of owning and operating manufacturing facilities. The lesson is that constraints, properly understood, can become advantages.

Finally, there is the lesson of acquisition discipline—and its limits. Monster's acquisition of Bang Energy out of bankruptcy was a masterful example of opportunistic deal-making: eliminating a competitor, absorbing its customer base, and acquiring manufacturing capacity at a significant discount to replacement cost. The CANarchy acquisition, by contrast, revealed the risks of stepping outside one's core competency. The $181.5 million in impairment charges served as an expensive reminder that brand-building skills in energy drinks do not automatically transfer to craft beer. Investors should weigh both outcomes when assessing management's capital allocation track record.

Competitive Analysis & Market Position

Monster Beverage operates in a competitive landscape that is simultaneously concentrated and evolving. The global energy drink market, valued at approximately $80-84 billion in 2025 and projected to grow to $104-150 billion by the early 2030s at a compound annual growth rate of approximately 6 percent, is dominated by two players: Red Bull and Monster, which together command a majority of global sales.

In the United States, Red Bull leads with roughly 47-50 percent of the market by dollar sales, followed by Monster at approximately 30 percent. Globally, the picture is more nuanced—Red Bull holds approximately 43 percent of the worldwide market, with Monster at roughly 39 percent (by some measures) depending on how market share is calculated across different geographies and channels. The Asia-Pacific region, which accounts for 53 percent of global energy drink consumption, remains the largest growth opportunity and the market where competitive dynamics are most fluid.

Through the lens of Michael Porter's Five Forces, Monster's competitive position reveals both durable strengths and genuine vulnerabilities.

The threat of new entrants is moderate but asymmetric. The energy drink category has low barriers to entry in terms of product formulation—the basic ingredients of caffeine, taurine, and B-vitamins are widely available, and contract manufacturers can produce energy drinks for virtually any brand. But the barriers in terms of distribution and brand building are extremely high. Securing shelf space in the fiercely competitive convenience store channel requires either the backing of a major distributor or years of painstaking route-by-route salesmanship. Building brand awareness against two incumbents that have spent decades cultivating cultural relevance requires marketing budgets that most startups cannot afford. The recent history of the category illustrates this dynamic: Celsius achieved impressive growth in the US by securing a distribution deal with PepsiCo, but even that partnership has not enabled the kind of global reach that Monster enjoys through Coca-Cola. The Bang Energy saga is even more instructive—a well-funded challenger with a differentiated product and aggressive marketing that ultimately ended up in bankruptcy and was absorbed by Monster.

The bargaining power of suppliers is low. Monster's key inputs—aluminum cans, sweeteners, caffeine, and flavorings—are commodity products available from multiple suppliers at competitive prices. The co-packing model further reduces supplier concentration risk, as Monster can shift production among multiple contract manufacturers if any single co-packer raises prices or experiences capacity constraints.

The bargaining power of buyers is moderate. Monster sells through large retailers and distributors who have significant purchasing power, but the strength of the Monster brand gives the company leverage in negotiations. Consumers pull the product through the channel; retailers stock it because it sells, not because Monster offers favorable trade terms. In convenience stores—where a disproportionate share of energy drinks are sold—the Monster brand commands premium shelf placement because store operators know it drives foot traffic and high-margin impulse purchases.

The threat of substitutes is the most significant competitive concern for the long term. Coffee, tea, traditional sodas, and an emerging wave of functional beverages—adaptogens, nootropics, functional mushroom drinks, electrolyte-enhanced waters—all compete for the same consumer occasions. Health and wellness trends could shift consumer preferences away from highly caffeinated energy drinks over time, particularly among younger consumers who increasingly prioritize "clean" ingredients and transparency. Regulatory action—mandatory caffeine limits, warning labels, marketing restrictions targeting minors—could constrain the category's growth or force costly reformulation and rebranding.

Competitive rivalry between Monster and Red Bull is intense but largely stable, resembling the Coke-Pepsi duopoly more than a destructive price war. The two companies compete on brand positioning rather than price, maintaining premium pricing and healthy margins. Their approaches are fundamentally different—Red Bull owns its production and distribution, projects European sophistication, and sponsors at the pinnacle of global sports (Formula One, Red Bull Racing, Red Bull Air Race); Monster outsources everything, projects American rebellion, and sponsors at the grassroots level. This differentiation has created a stable duopoly where both companies can thrive without destructive price competition—one of the hallmarks of an attractive industry structure.

Applying Hamilton Helmer's Seven Powers framework to Monster reveals where its competitive advantages are most durable. Brand power is the most obvious: the Monster brand generates consumer willingness to pay a premium and creates emotional loyalty that competitors cannot easily replicate—a classic case of Helmer's "brand" power, where the company enjoys both lower customer acquisition costs and pricing premiums. Scale economies in distribution—amplified by the Coca-Cola partnership—mean that Monster's per-unit distribution costs decline as volume increases, creating a cost advantage that widens over time. The Coca-Cola distribution deal itself functions as a form of "cornered resource"—a unique, non-replicable asset that Monster secured and that no competitor can duplicate. And the 30-year track record of the management team has created process power—deep institutional knowledge about how to build and manage energy drink brands across global markets.

The bear case centers on three legitimate concerns. First, market saturation in the United States, where energy drink penetration is already high and category growth has slowed to single digits. Second, health-related regulatory risks that could constrain the category globally, particularly in markets like the European Union where regulatory frameworks are more aggressive. Third, the CANarchy impairment, which suggests that Monster's ability to execute outside its core energy drink competency is unproven and perhaps limited. If the company's growth depends on expanding into adjacent categories like alcohol, the track record so far is not encouraging.

The bull case rests on equally compelling evidence. International growth represents a massive runway—energy drink consumption per capita in most international markets remains a fraction of US levels, and Coca-Cola's distribution network provides the infrastructure to capture that opportunity. Pricing power remains strong, as demonstrated by the successful November 2024 price increase. Category expansion through new product formats (Ultra zero-sugar, female-focused FLRT), new occasions (morning energy, pre-workout), and new geographies (Predator and Fury in emerging markets) extends the addressable market beyond what traditional energy drink estimates suggest. And the asset-light model continues to generate industry-leading margins and returns on capital that compound wealth for patient shareholders.

Looking Forward: The Future of Monster

Monster Beverage enters 2026 from a position of considerable strength but at a moment of transition. The stock has reached new highs. International expansion continues to accelerate. The Coca-Cola distribution partnership remains the company's most important structural advantage. And the leadership transition from Sacks to Schlosberg has been executed with the kind of deliberate planning that has characterized the company's major decisions throughout its history.

The near-term product pipeline reflects continued innovation within the core energy drink category. FLRT, a female-focused zero-sugar functional energy brand, is scheduled to launch in late first-quarter 2026 in four flavors. This represents a significant strategic move. Monster's consumer base has historically skewed heavily male, and the success of Monster Ultra in attracting female consumers suggested that there was substantial demand that the core brand was not capturing. A dedicated female-focused brand represents an attempt to expand Monster's total addressable market meaningfully without diluting the masculine edge of the flagship brand.

The alcohol segment remains an open question—and an expensive one so far. The CANarchy impairment charges totaling $181.5 million were a sobering acknowledgment that craft beer is a fundamentally different business than energy drinks, with different distribution dynamics, different consumer behavior, and different competitive pressures. Whether Monster can find a successful formula for alcohol-energy hybrids or adjacent alcoholic beverages remains to be seen. The Beast Unleashed product line continues, but the company's enthusiasm for the alcohol category has been notably tempered in recent communications.

International expansion represents the largest and most visible growth opportunity. With international sales now at 43 percent of revenue and growing at 16 percent on a currency-adjusted basis, the runway ahead is substantial. Many large markets—India, China, Southeast Asia, Africa, Latin America—have energy drink penetration rates far below those of the United States and Western Europe. Coca-Cola's presence in virtually every retail outlet in these markets gives Monster a distribution advantage that no competitor other than Red Bull can match. The affordable brands Predator and Fury are specifically designed to penetrate price-sensitive emerging markets, and their early traction suggests that the Monster playbook—strong brand, outsourced production, partner distribution—works across very different economic environments.

Regulatory risk remains the most significant overhang. Governments around the world are increasingly scrutinizing energy drink marketing to minors, caffeine content, and health claims. The European Union has been particularly active, with several member states implementing or considering restrictions on energy drink sales to minors. The United Kingdom has considered banning energy drink sales to under-16s. While no major market has yet implemented restrictions severe enough to materially damage Monster's business, the regulatory environment is evolving, and any significant tightening could affect growth rates, marketing practices, or product formulation.

Management projected 2025 full-year net sales between $10.2 billion and $10.4 billion—representing continued strong growth from the $7.49 billion reported in 2024. The Q3 2025 results, with record revenue and expanding margins, suggested the company was tracking well against those targets. The next earnings report, scheduled for February 26, 2026, will provide the market's next detailed read on whether the underlying growth engine remains on track. Monster also sold more than 10 billion cans globally in 2024—a milestone that speaks to the sheer scale of the brand's global presence.

Epilogue & Key Takeaways

The Monster Beverage story is, at its core, a story about seeing what others miss. When Rodney Sacks and Hilton Schlosberg looked at a bankrupt juice company in 1992, they did not see a failed business. They saw an undervalued brand, an asset-light operating model forced by circumstance, and a platform for transformation. When they looked at the energy drink market in 2002, they did not see Red Bull's dominance as an obstacle. They saw a positioning gap wide enough to drive a sixteen-ounce can through. When they looked at Coca-Cola's distribution network in 2014, they did not see a corporate giant that would swallow their independence. They saw the key that would unlock global scale.

Each of these decisions required a willingness to think differently about conventional wisdom. Bankrupt companies are bad investments—except when they contain undervalued brands. You cannot compete with Red Bull—except by competing differently. You should not invite Coca-Cola inside your tent—except when doing so transforms a regional brand into a global empire. Sacks and Schlosberg rejected all three premises and were rewarded with one of the greatest wealth-creation stories in market history.

The greatest business transformations often come from unlikely places. A juice delivery service founded in Depression-era Los Angeles, rescued from bankruptcy by two South African immigrants, reimagined as an energy drink company, and catapulted to global dominance through a partnership with the world's largest beverage distributor. None of this was inevitable. All of it was the product of patient, focused execution over decades—a handful of transformative decisions surrounded by years of disciplined operational work.

The lesson for entrepreneurs is that the most consequential business decisions are the ones that look obvious only in retrospect. In the moment, they require conviction, patience, and a clear-eyed assessment of what is actually happening versus what the market assumes is happening. The lesson for investors is that the greatest compounders are often hiding in plain sight—in categories that seem boring, in companies that seem small, generating returns that seem impossible until you understand the structural advantages that produce them.

Monster's nearly $80 billion valuation was not built on a single stroke of genius. It was built on three decades of disciplined execution, a handful of transformative strategic decisions, an asset-light model that turned every dollar of revenue into outsized returns on capital, and an unwavering commitment to a brand that a billion consumers around the world have made part of their daily lives.

The black can with the green claw marks started as an insurgent product in a category that barely existed. It is now a global icon—and the improbable monument to two South African lawyers who bet everything on the American dream of reinvention.

Recent News

The most recent quarter reported, the third quarter of fiscal 2025, delivered record results across the board. Net sales reached $2.20 billion, representing 16.8 percent year-over-year growth. Operating income surged to $675.4 million, up 40.7 percent. Net income reached $524.5 million, and diluted earnings per share of $0.53 comfortably beat consensus estimates. Gross margins expanded to 55.7 percent, reflecting both pricing power and operational discipline.

International momentum remained strong, with international net sales reaching $937.1 million in the quarter—approximately 43 percent of total revenue. Currency-adjusted international growth continued at roughly 16 percent. The company reported broad-based market share gains across multiple geographies and product lines, with the Ultra zero-sugar line growing 29 percent in the United States.

On the pricing front, Monster implemented a five percent price increase in the United States effective November 1, 2024, with selective additional adjustments in late 2025. Early indications suggested that the price increases were being absorbed without meaningful volume degradation—a testament to the brand's pricing power and the relative price inelasticity of the energy drink category.

The leadership transition continued smoothly. Hilton Schlosberg assumed the role of sole CEO on June 13, 2025, with Rodney Sacks continuing as chairman and transitioning toward retirement at the end of 2026. The market showed no signs of concern about the handover, with the stock reaching new highs in the months following the transition.

Looking ahead, Monster announced FLRT—a new zero-sugar, female-focused functional energy brand—scheduled for launch in late first-quarter 2026 in four flavors. The company also confirmed plans for a limited-edition release in summer 2026 celebrating the United States' 250th anniversary. Monster reported selling more than 10 billion cans globally in 2024. The next earnings report is scheduled for February 26, 2026.

Morgan Stanley raised its price target on MNST to $96 per share in January 2026, reflecting optimism about the company's international growth trajectory and margin expansion potential. The stock traded near $80.76 as of late January 2026, with a market capitalization of approximately $79.5 billion, zero long-term debt, and $2.29 billion in cash.

Links & Resources

Investors and readers seeking to deepen their understanding of Monster Beverage can consult the following resources. The company's investor relations page at investors.monsterbevcorp.com provides access to SEC filings, earnings transcripts, and investor presentations. Annual reports filed with the SEC (10-K filings) contain detailed information about the company's operations, competitive landscape, and risk factors. Quarterly earnings releases (10-Q filings) provide the most current financial data.

For industry context, Mordor Intelligence and Grand View Research publish comprehensive reports on the global energy drink market, including market size estimates, growth projections, and competitive landscape analysis. The International Energy Drink Association provides regulatory updates and industry data.

Rodney Sacks and Hilton Schlosberg have given relatively few in-depth interviews compared to many public company CEOs, making those that exist particularly valuable. Earnings call transcripts, available through the company's investor relations page, offer the most regular window into management's thinking and strategic priorities. Academic case studies on Monster's strategy have been published by several business schools, including analyses of the Coca-Cola partnership structure.

For historical stock performance data and financial analysis, StockAnalysis.com and Macrotrends.net provide comprehensive charting tools and financial history. The company's proxy statement (DEF 14A filing) contains detailed information about executive compensation, ownership stakes, and governance structure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube