MakeMyTrip: The Great Consolidation of Indian Travel

I. Introduction & Episode Roadmap

In the spring of 2000, Deep Kalra was thirty-one years old, sitting in a borrowed conference room in Sunnyvale, California, trying to explain to a sceptical American investor why he wanted to sell India-to-anywhere airline tickets over a website that 99.5% of Indians could not access. India then had roughly five million internet users in a country of over a billion people. Broadband was a foreign word. Credit card penetration in tier-1 cities was in the low single digits. The most modern thing about Indian aviation was the moustache on the Air India Maharajah.

Twenty-six years later, that same company — मेकमायट्रिप MakeMyTrip — is the dominant online travel agent (OTA) in the world's most populous nation, sitting on roughly $9.8 billion in annual gross bookings, a market capitalisation hovering around $9 billion, and a corporate-travel arm pulling in more than a billion dollars of bookings per year on its own.12 The company's stock, trading on NASDAQ under the ticker MMYT, has become the de facto way for foreign investors to bet on the entire Indian middle-class travel curve — flights, hotels, holidays, weddings, pilgrimages and increasingly, payments.

The MakeMyTrip story is interesting because it is not a story of inventing a new category. Expedia and Travelocity already existed when Deep Kalra filed his Delaware paperwork. Booking.com existed. Even in India, IRCTC — the Indian Railways ticketing portal — was launched almost in parallel. The interesting part is how a company that started life as a polite NRI service desk for diasporic Indians flying home for Diwali ended up running the country's largest e-commerce platform by gross merchandise value outside of the marketplaces themselves.

To understand that, this episode goes deep on three inflection points. First, the 2005 pivot — the moment Kalra moved his centre of gravity from New York to Gurugram on the back of an unlikely catalyst: a Bangalore entrepreneur named G.R. Gopinath who decided India needed एयर डेक्कन Air Deccan, the country's first low-cost carrier. Second, the 2010 NASDAQ listing — a deeply unusual choice for an Indian-operating company and a small but consequential bet on global capital. And third, the 2016 megamerger with ibibo Group — the deal that married MakeMyTrip with गोइबिबो Goibibo and रेडबस redBus, gave Naspers a 40% economic stake, and effectively ended the Indian OTA wars in MakeMyTrip's favour.

But there is also a fourth, quieter inflection point that this episode argues is just as important: the slow, deliberate transformation of MakeMyTrip from a low-margin transactional flight engine into something closer to a travel fintech and corporate-services holding company. The visible business is air tickets. The interesting business is the bundle: hotels, holiday packages, foreign exchange cards, Book-Now-Pay-Later, corporate travel SaaS, and the data exhaust from 75 million customers. Most of those lines did not exist at the IPO. Most of them now drive the marginal dollar of profitability.

So: how do you build a $9 billion travel giant in a country where, in 2000, fewer than one in two hundred citizens was online? You survive the first dot-com bust, you ride the low-cost-carrier wave, you list in New York instead of Mumbai, you turn your largest competitor into your largest shareholder, you keep your founders honest by paying them nothing for two years during a pandemic, and you quietly start lending people money to take their honeymoons. Let us tell that story.

II. The Founding & The US-to-India Pivot

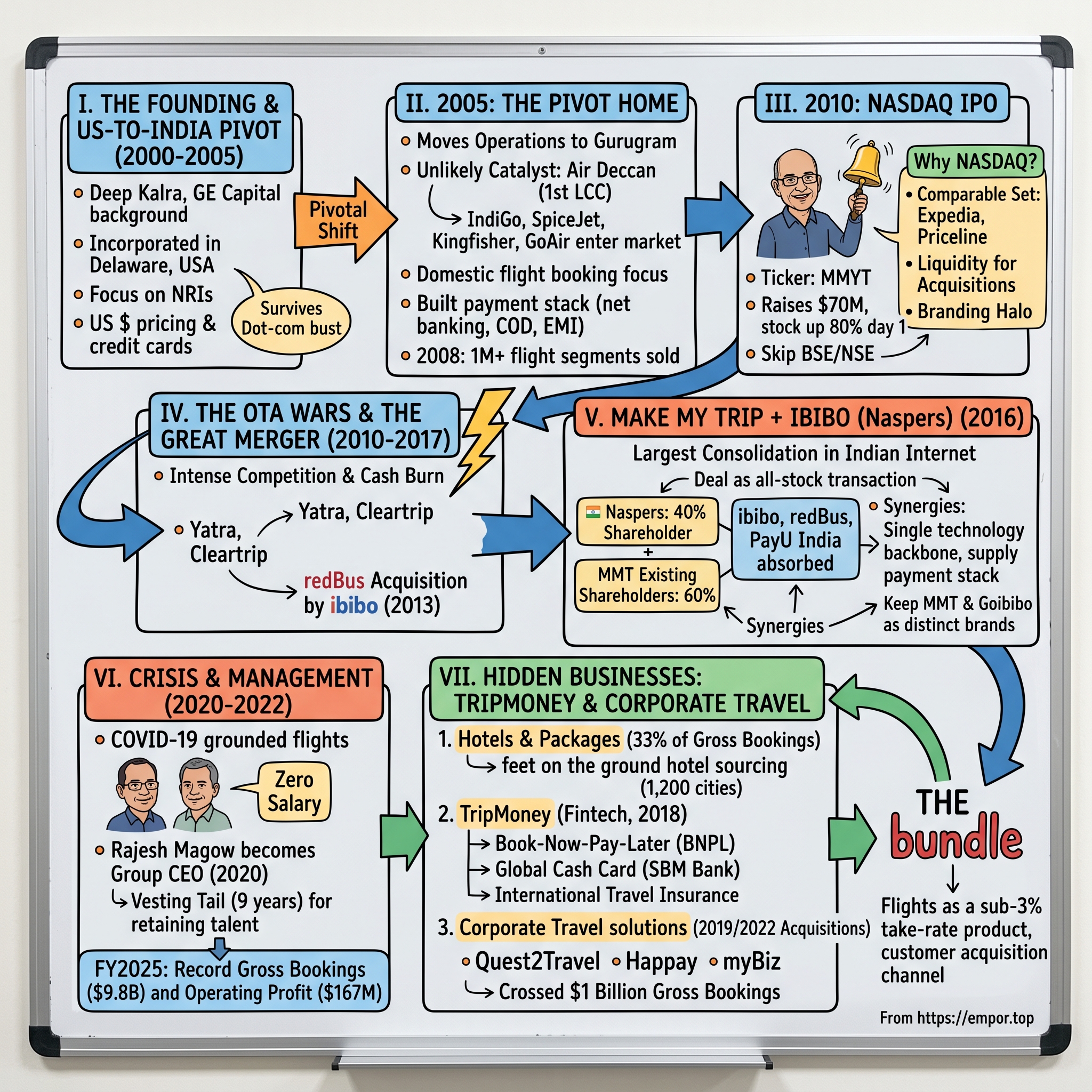

The founding mythology of MakeMyTrip begins not in a Bangalore garage but in a corner office on Park Avenue. Deep Kalra had spent the back half of the 1990s at GE Capital in India, learning structured finance and consumer credit, before doing the obligatory MBA at IIM Ahmedabad and then jumping into AMF Bowling's India business — yes, the bowling-alley chain — as one of his first operating roles. By 1999, he was a banking-cum-operations guy in his early thirties who had figured out that the most underbuilt piece of Indian consumer infrastructure was distribution. Airline tickets, in particular, were sold through a bewildering thicket of IATA-accredited travel agents in cluttered storefronts, each tacking on a 7–10% commission, each with their own preferred carriers, each requiring a physical visit and, often, cash.

Kalra's insight was almost embarrassingly simple. If American consumers could buy a Delta ticket on Travelocity at midnight in their pyjamas, there was no structural reason Indian consumers — eventually — could not do the same. The problem was that "eventually" was the operative word. In 2000, when MakeMyTrip was incorporated, India had a credit card base of roughly three million users and a broadband base that was rounding error. The Indian government had only recently liberalised foreign investment in travel, and most domestic airlines were either state-owned (एयर इंडिया Air India, इंडियन एयरलाइंस Indian Airlines) or about to go bankrupt (Sahara, Damania, ModiLuft).

So Kalra did what almost every Indian internet founder of his generation did: he served the diaspora first. The first version of MakeMyTrip was a US-incorporated, US-revenue-generating online travel agent targeting non-resident Indians (NRIs) — software engineers in New Jersey, doctors in Houston, students in Boston — buying tickets home. The product was simple: a clean web interface, US-dollar pricing, US-issued credit cards accepted, and an India operations team in Delhi handling the supplier side. By 2001, the business was generating real revenue from a customer base that was happy to pay in dollars precisely because the alternative — calling a high-street Indian agent from New Jersey at 3 a.m. — was awful.

Then the dot-com bubble burst, and the next eighteen months were brutal. SoftBank, one of the early backers, slow-walked the next tranche. Kalra has spoken publicly about coming within a few weeks of payroll-zero, about telling his team they might not have jobs, about flying to Tokyo to defend an investment thesis that his investors no longer believed in. The company survived essentially because the NRI business kept generating cash and because Kalra had the discipline — counter-cultural for a 2001 internet founder — to actually charge for the service. MakeMyTrip never went through the "free, scale, monetise later" phase that killed most of its peers; it was always a transactional, take-a-cut business from day one.

The real pivot came in 2005. Two things happened in quick succession. भारतीय रेल Indian Railways launched IRCTC's online ticketing portal, which by sheer scale taught a generation of middle-class Indians that you could buy a ticket online and have the journey actually happen. And एयर डेक्कन Air Deccan, the country's first true low-cost carrier, started selling sub-₹500 fares on Bangalore-Hubli and Bangalore-Mangalore routes — fares that, for the first time in Indian history, made flying genuinely cheaper than the second-class air-conditioned train. The Indian middle class, especially the new IT-services-employed cohort in Bangalore, Hyderabad and Gurugram, suddenly discovered domestic aviation. By 2006, IndiGo, SpiceJet, Kingfisher and GoAir had all entered the market, and India's domestic passenger traffic was compounding at over 25% per year.

This was the wave Kalra rode. He shut down the US-NRI hub as the company's centre of gravity, moved the engineering and management to गुरुग्राम Gurugram, and re-launched MakeMyTrip as a domestic Indian flight booking engine. The unit economics were initially terrible — LCCs paid lower commissions than the legacy carriers — but the volumes were everything. By 2008, MakeMyTrip was selling more than a million flight segments a year, by some measures the single largest distributor of domestic air tickets in India. The bet that mattered was timing: had Kalra moved in 2003, the LCC wave would not have been there to catch; had he moved in 2007, the channel battle would already have been lost to Yatra, Cleartrip and the airlines' own direct websites.

What is easy to miss in retrospect is how much of this depended on a single, unglamorous capability: payments. Kalra's GE Capital instincts paid off here. MakeMyTrip built early integrations with Indian net-banking, with cash-on-delivery for ticket pickup, with EMI on credit cards — every grubby workaround required to extract a booking from a population that did not, structurally, trust the internet with their money. That payments stack, layered with a 24/7 call-centre that could close the loop for any customer who got cold feet, is what gave MakeMyTrip its conversion edge in the first decade. The business looked like an internet company. It ran like a consumer-finance company with a travel front-end.

By 2009, the company was ready for a real capital event.

III. The NASDAQ IPO & The Battle for Supremacy

If you wanted to make the most contrarian capital-markets decision possible for an Indian consumer internet company in 2010, you would have done exactly what Deep Kalra did: skip the Bombay Stock Exchange, skip the National Stock Exchange, fly to New York, and list on NASDAQ.

On August 17, 2010, MakeMyTrip Limited — a Mauritius-incorporated holding company controlling Indian operating subsidiaries — priced its IPO at $14.00 per ordinary share, the top of its $12–14 marketed range, raising $70 million on five million shares.3 The ticker MMYT opened on NASDAQ that morning and closed the first session at $25.16, up roughly 80% on day one — the largest first-day pop for an internet IPO since Baidu's 2005 debut, and the largest ever for an India-themed listing.4 Kalra rang the opening bell wearing a kurta. The photo became the cover image of half a dozen Indian business magazines that week.

Why NASDAQ? There were three live reasons and one unspoken one.

The live reasons, in roughly the order Kalra has cited them in interviews. First, the comparable set. There was no listed Indian travel company. There was no listed Indian internet company of any meaningful scale on the BSE or NSE. The analyst community in Mumbai did not have a framework for valuing a -3% net margin business burning growth capital to expand into hotels. On NASDAQ, the analysts had Priceline, Expedia, Orbitz and Ctrip — they knew exactly how to value gross bookings, take rates, marketing efficiency and cohort retention. The multiple available in New York was a multiple that did not exist in Mumbai.

Second, the currency. Kalra and his board had already started thinking about acquisitions — hotels were the obvious next vertical, holiday packages an adjacent one — and a NASDAQ-listed Class A share was a far more liquid acquisition currency for cross-border deals than a Mumbai-listed scrip. As we will see, this thesis paid off six years later in the most consequential way possible.

Third, the branding halo. Being "the first Indian travel company on NASDAQ" was, in 2010, an extraordinarily cheap marketing line. It bought trust with hotel suppliers, with airline distribution heads, with potential international partners, with the Indian media — and, not least, with employees. A NASDAQ listing was the cleanest possible signal that MakeMyTrip was not the next failed dot-com.

The unspoken reason was governance and SEBI. India's Securities and Exchange Board has, historically, made life difficult for loss-making consumer companies trying to list. The disclosure-and-pricing framework was geared toward profitable, dividend-paying issuers. A first-of-its-kind Indian internet IPO in Mumbai in 2010 would have faced months of regulatory dialogue and a likely valuation haircut. NASDAQ, by contrast, would price a loss-making growth company on revenue multiples and forward bookings, no questions asked. (India's domestic markets eventually caught up — the Zomato, Paytm, Nykaa and PolicyBazaar listings of 2021–2022 finally created a domestic playbook for unprofitable consumer internet — but a decade too late for MakeMyTrip.)

What followed the IPO was the bloodiest period in Indian OTA history. The capital raised on NASDAQ became a war chest, but every competitor saw the same thing MakeMyTrip saw — a domestic travel market expected to triple by 2020 — and went all-in on customer acquisition. यात्रा Yatra (founded 2006), क्लियरट्रिप Cleartrip (founded 2006), ट्रैवलगुरु Travelguru, ezeego1 and, most aggressively, गोइबिबो Goibibo (the consumer travel brand of Naspers- and Tencent-backed ibibo Group) flooded Indian television with discount-led advertising. Coupon code economics ruled. At one point, every OTA in India was reportedly losing 10–15% on every hotel booking, just to keep the funnel filled.

The pivotal moment of this period came in June 2013, when ibibo Group — by then a Naspers-led joint venture with Tencent — paid roughly $138 million (₹800 crore) for redBus, the dominant online bus-ticketing platform founded by Phanindra Sama and two BITS Pilani classmates. redBus had a 70% share of the online inter-city bus market in India and was already issuing 10 million tickets a year on gross sales near $200 million.56 That deal mattered for two reasons. It was the largest cash acquisition of an Indian internet asset by a foreign strategic to date, and it gave the Naspers-Tencent camp a category-killer asset to stack alongside Goibibo. In a knife-fight market, ibibo Group now had a multi-vertical OTA with deep pockets and patient capital.

By 2015, the Indian OTA market had become a war of attrition between three roughly co-equal players: MakeMyTrip (best brand, deepest hotel supply, public-market discipline), ibibo (best capitalised, multi-brand, willing to lose money for years), and Yatra (best corporate travel desk but undercapitalised). All three were burning cash on customer acquisition. None could quite break the others. Something had to give.

Something did, and it would re-draw the entire map.

IV. The Great Merger: MakeMyTrip + ibibo

On October 18, 2016, MakeMyTrip and Naspers — through its ibibo Group holding company — announced the largest consolidation in the history of Indian internet. The structure was, on paper, simple. MakeMyTrip would absorb ibibo Group (which owned Goibibo, redBus, and a small payments business called PayU India) in an all-stock deal. At closing, MakeMyTrip's existing shareholders would own 60% of the combined company; Naspers, as ibibo's parent, would own 40%, instantly becoming MakeMyTrip's largest shareholder.7

The mechanical details, buried in the 6-K filed with the SEC, were a study in deal-making elegance. MakeMyTrip issued 38,971,539 newly created Class B shares to the parent of ibibo Group as consideration for the acquisition. Naspers then exercised an option to purchase an additional 413,035 ordinary shares at $21.19 a share for $8.75 million in cash. And — the clean-up step that gets overlooked — ibibo's parent contributed approximately $82.8 million in cash to MakeMyTrip at closing as its pro-rata share of consolidated net working capital.7 The transaction closed on January 31, 2017. At the deal price, the combined entity was valued at roughly $1.8 billion.

The strategic logic was almost too clean. Both companies were burning cash competing for the same incremental Indian traveller, and both had concluded — correctly — that the third major competitor, Yatra, was already capital-constrained. Yatra, in fact, had announced its own SPAC merger with Terrapin 3 just three months earlier, on July 14, 2016, at a $218 million enterprise value — barely an eighth of what the MMT-ibibo combination would be worth.8 In other words, the two best-capitalised players in India saw the gap to number three widen and decided to stop killing each other.

Let us benchmark this. The Yatra-Terrapin SPAC was a reverse merger that raised roughly $20 million in PIPE financing and valued the company at $218 million.8 MakeMyTrip's absorption of ibibo, by contrast, was nine times that valuation in equity alone, with effectively no immediate cash outlay beyond the working-capital top-up. Kalra and his board had traded approximately 40% of their company to eliminate their largest competitor, lock in redBus as a wholly owned asset, and convert Naspers — one of the deepest-pocketed emerging-markets investors in the world — from an enemy into a long-term, lock-up-bound shareholder. The Yatra deal looks, in retrospect, like a settlement; the ibibo deal looks like a coronation.

The acquisition of redBus, embedded inside the ibibo deal, deserves its own analytical pass. ibibo had paid $138 million for redBus in 2013, when the asset was already category-dominant. By 2016, redBus had extended its share of organised online inter-city bus ticketing well past 70%, with credible second-place gaps in Indonesia and Singapore via its Southeast Asia expansion. In a domestic Indian context, redBus is one of the most cleanly defensible "category killer" acquisitions of the entire 2010s — local supplier relationships, two-sided network economics (operators want to be where consumers are, consumers want the most operators), and a payment-rails moat from running cash collections through a thousand small bus terminals. Kalra had essentially acquired a thesis-grade asset for free, as a by-product of solving his Goibibo problem.

The Naspers piece of the puzzle is the most under-discussed. Naspers (the South African media-turned-internet conglomerate whose most famous bet was an early stake in 腾讯 Tencent) and Tencent had been ibibo's joint backers since 2007. By 2016, Naspers had bought out Tencent's economic interest. When the MMT-ibibo deal closed, Naspers received its 40% stake under a multi-year lock-up. For the next several years, MMT's largest shareholder was not a financial holder shopping the stock — it was a strategic with infinite patience and a portfolio that included Tencent, Delivery Hero, OLX and Mail.ru. The implicit message to the market was unmistakable: this consolidation is permanent.

The post-merger integration was where the deal earned its keep. The team made one structurally important decision: keep MakeMyTrip and Goibibo as two distinct consumer brands. The economic case for collapsing them into one brand was significant — lower marketing spend, single funnel, simpler product. The case against was that customer overlap was lower than expected; Goibibo skewed younger, more price-sensitive, more tier-2; MakeMyTrip skewed older, more premium, more international. Running them as a controlled duopoly within a single company let MakeMyTrip extract the cost synergies on the supply side (single hotel sourcing team, single airline contracting team, single technology backbone, single payments stack) while preserving the demand-side differentiation.

The financial results made the case. Combined hotel transactions, which had grown around 30% annually pre-merger, accelerated to over 50% annually in the two years post-close. Marketing as a percentage of revenue fell sharply as the implicit subsidy war ended. By fiscal 2019 — the last year before COVID — MakeMyTrip was generating positive adjusted operating profit at scale, something neither company had ever achieved independently. The merger had not just consolidated the market; it had reset its rules.

And then a virus came.

V. Management: The Duo & The Incentive Structure

In late March 2020, with Indian aviation effectively grounded and hotel cancellations running at over 90% of bookings, Deep Kalra and Rajesh Magow sent an internal email that became a Bloomberg story. Effective April 1, the two of them would draw zero salary for the foreseeable future, and the entire senior leadership team had volunteered to take an approximately 50% cut in compensation.9 No employees were furloughed that week. No retail-facing customer support was outsourced. The company, in classic MakeMyTrip fashion, ate the pain at the top of the house first.

This was not a stunt. To understand why, you have to understand the two-person management dynamic that has defined the company since roughly 2007. Deep Kalra — IIM Ahmedabad, ex-GE Capital, an extrovert by temperament and a deal-maker by training — is the founder, the public face, the one who pitches investors and sets ten-year direction. Rajesh Magow — chartered accountant, ex-Aptech, ex-CFO of Spectramind — is the operator, the one who actually runs the company day to day. Magow joined MakeMyTrip in 2006 as CFO, became co-founder by attribution, and by the time of the 2010 IPO was effectively the chief operating officer. He has been Group CEO since February 2020 in name, but operationally since the mid-2010s.10

The 2020 leadership transition — Kalra stepping aside as CEO, becoming Executive Chairman, and then in April 2022 becoming Group Chairman and Chief Mentor — was therefore less a transition and more a formalisation of a structure that had been working for a decade.10 What was unusual was the choice to do it publicly and in stages, rather than the more common pattern in Indian founder-led businesses of holding both titles indefinitely. Kalra has spoken about wanting MakeMyTrip to outlive his direct involvement, and the staged handoff was the visible expression of that. By April 2022, Magow held effective P&L authority across every business line; Kalra's role narrowed to strategy, capital allocation, and external representation.

Skin in the game matters here, because the underlying incentive math is unusual for an India-operating company. According to recent proxy disclosures, Deep Kalra holds approximately 4% of outstanding shares; Rajesh Magow holds in the range of 1.6–2.2% depending on which year's filing you read; the rest of the senior management team holds another two to three percent collectively. None of these are control stakes — Naspers' stake remains the largest single block — but they are large enough to matter. On a roughly $9 billion enterprise value, Kalra's 4% is worth several hundred million dollars; that is a meaningful concentration for a founder who took the company public sixteen years ago.

The incentive plan beneath those numbers is the 2010 Share Incentive Plan, originally adopted at IPO and amended several times since. The defining feature, relative to Indian peers, is the long vesting tail. Senior management grants vest over periods of up to nine years, with cliff dates designed to bridge multiple business cycles. This was a deliberate choice by Kalra and the board, made in the explicit context of a Bangalore-Gurugram tech-talent market where senior leaders routinely jump for 30–40% pay bumps. The MakeMyTrip plan was designed to make it expensive — almost prohibitive — for a senior engineering or commercial leader to leave before year six or seven. Retention metrics for the senior cohort have stayed above 90% across the post-merger period, which is striking given the talent churn in Indian consumer internet.

A subtler piece of the management story is the role of the board. After the Naspers deal, the MakeMyTrip board picked up two Naspers nominees, several independent directors with global travel-industry credentials, and — through a series of refreshments — a chair structure designed to handle the eventual question of "what happens when Kalra is fully retired?" The April 2022 reorganisation, which moved Kalra into a non-executive Chairman/Chief Mentor role, was effectively the answer to that question: succession was no longer a hypothetical but an operating reality. Magow has been running the business; he will continue to run the business; Kalra remains available as a thought partner and external face but does not need to be in the building every day.

The crisis behaviour during COVID is the most concrete evidence available for whether this structure works. Between April 2020 and August 2020, MakeMyTrip's quarterly gross bookings fell by more than 90% year-on-year. Cash burn was real. The company tapped roughly $200 million of accessible liquidity to maintain operations, including a $180 million convertible note placed with two pre-existing shareholders. By Q4 of fiscal 2022, the business was not only back to pre-COVID gross bookings but reporting record adjusted operating profit margins as marketing efficiency rose and remote/hybrid corporate travel patterns settled into a new equilibrium. By FY2025, gross bookings of $9.8 billion and adjusted operating profit of $167.3 million were both all-time records.1 The "zero salary" moment in 2020 looks, in retrospect, less like symbolism and more like the leading indicator that the management team understood what kind of crisis they were in.

Now — what was MakeMyTrip actually selling, by then, to generate that profit?

VI. Hidden Businesses: TripMoney & Quest2Travel

If you opened the MakeMyTrip mobile app in 2026 and tapped through to the booking flow, you would see flights, hotels and holiday packages — the three lines of business that have always existed. What you would not immediately see is that flights, despite being the most visible product, are no longer the most economically interesting one. Flights are a sub-3% take-rate business in India because the largest domestic airline, इंडिगो IndiGo, has 60%+ market share and uses that share to discipline distributor margins. Every incremental rupee of profitability MakeMyTrip has earned in the last five years has come from somewhere else.

Where is "somewhere else"? Three places, in rough order of current size.

First, hotels and holiday packages. Hotel take rates in India are structurally higher — mid-teens for branded chains, twenty-percent-plus for independent properties — because hotel supply is fragmented, the long tail is local, and the suppliers desperately need the distribution. MakeMyTrip has spent over a decade building what the company internally calls "feet on the ground" hotel sourcing — district-level supply teams in roughly 1,200 Indian cities and towns, signing up everything from a 200-room JW Marriott in Mumbai to a 12-room family-run guesthouse in मनाली Manali. By FY2025, hotels and packages represented roughly a third of gross bookings but a significantly higher share of segment operating profit. This is the highest-quality part of the business, and it is also the part that is hardest for Google, Booking.com, or Amazon to replicate, because the sourcing work is local, granular, and grindy.

Second — and this is the genuinely hidden gem — TripMoney. Launched in 2018 as a Book-Now-Pay-Later product, TripMoney has quietly evolved into MakeMyTrip's travel-finance subsidiary, offering forex cards, the TripMoney Global Cash Card (issued in partnership with SBM Bank India), international travel insurance, travel loans of up to ₹1,00,000, and a multi-currency card with zero forex markup.11 As of the last public disclosure, TripMoney's BNPL vertical was running at roughly ₹250 crore in annualised loan disbursals, and the insurance line had sold approximately two million policies over a 15-month window.11 Those are small numbers in absolute terms relative to the broader business, but the strategic point is unit economics. Selling a Mumbai-Dubai flight ticket earns MakeMyTrip 2-3% of the fare; bundling a forex card and travel insurance with that same ticket can add hundreds of basis points of margin on the same transaction with marginal customer-acquisition cost. The customer is already in the funnel, mid-purchase, with a high-intent moment. TripMoney monetises that moment.

Think of TripMoney as American Express's small-but-important travel-services business, grafted onto an OTA's customer flow. The endgame, articulated by management in 2022 and 2023 earnings calls, is to spin TripMoney out as an independent fintech subsidiary, retaining majority ownership but potentially raising external capital at a stand-alone valuation. The model here is the way पेटीएम Paytm separated its payments and lending lines, or the way रिलायंस Reliance ringfenced Jio Platforms. The optionality is real and, in the public market's current valuation of MakeMyTrip, almost certainly under-recognised.

Third, corporate travel — the line that most generalist investors miss entirely. In April 2019, MakeMyTrip acquired a 51% equity interest in Quest2Travel, a Mumbai-based corporate travel management firm, with an earn-out structure to acquire the remaining shares over three tranches ending in March 2022.12 The cash consideration disclosed at signing was tiny — about $14,000 — because the deal was structured almost entirely around future-performance earn-outs. The real price was paid as Q2T's revenue ramped.

What Quest2Travel actually does is run the back-office travel ERP for large corporates. Travel request, approval workflow, policy-compliant booking, invoice generation, expense management, final settlement — all of it. Once you have integrated Q2T into your corporate finance plumbing, you do not leave. Switching costs are brutal. Combine Q2T with myBiz (MakeMyTrip's SME-focused corporate travel platform launched organically in 2018) and Happay (the corporate expense management platform acquired by MakeMyTrip in 2022 for roughly $180 million), and you have what management calls the Corporate Travel Solutions stack — the only end-to-end travel-plus-expense platform of meaningful scale in India.

By calendar 2025, that stack crossed $1 billion in annual gross bookings — corporate travel now exceeds 10% of MakeMyTrip's total gross bookings — serving over 500 large enterprises (including 150 of the BSE 500), 75,000 SMEs, and reaching roughly 40 lakh (4 million) employees in some capacity.13 To put that in context: at the same time the consumer business has been compounding mid-twenties percent on the back of Indian middle-class travel demand, the corporate business has been growing faster off a smaller base. The blended mix is dragging margins up because corporate travel is structurally higher-margin (recurring volume, integrated software, lower marketing intensity per booking).

The synthesis is this: MakeMyTrip-the-OTA is the visible business; MakeMyTrip-the-bundle is the actual business. Hotels, TripMoney, and corporate travel are where the marginal dollar of profitability now comes from, and all three have multi-year runway. The flight-booking front-end is a customer acquisition channel for the high-margin attached products behind it.

That is the architecture. Now let us stress-test the moat.

VII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

If you wanted to construct, from first principles, the most defensible online travel agency you could in India, the playbook would look almost exactly like the one MakeMyTrip has run. To see why, it helps to run the business through two analytical lenses — Hamilton Helmer's 7 Powers framework, which asks which structural sources of advantage are actually durable, and Michael Porter's 5 Forces, which asks where the value will eventually accrue.

Start with the 7 Powers. The first power, scale economies, applies most directly to the supply side. MakeMyTrip's hotel sourcing — those district-level supply teams referenced earlier — is a cost structure that gets cheaper per incremental hotel signed as the company gets bigger. A new entrant trying to source 50,000 long-tail Indian hotels from a zero base would need to spend several hundred million dollars over multiple years to match the network. The same applies, in slightly different shape, to airline contracting (volume rebates kick in at certain booking thresholds) and to the redBus bus-operator network.

The second power, network effects, is real but bounded. On the consumer side, network effects are weak — me buying a flight does not directly make your flight cheaper. But on the marketplace side, network effects are genuine. Hotels list where the customers are; customers go where the inventory is. redBus benefits even more — the value of the platform to a bus rider is exactly the breadth of routes and operators it offers. Booking 70%-plus of online inter-city bus tickets in India means redBus has crossed a tipping point that nobody is going to un-tip without spending money no rational investor would commit.

The third power, counter-positioning, is where MakeMyTrip's M&A history has been most clever. The 2016 ibibo merger essentially removed counter-positioning as a threat — by absorbing the only competitor with comparable scale and capital, MakeMyTrip eliminated the source of competitive innovation that would have forced it to cannibalise its own margins.

The fourth power, switching costs, is the most under-discussed and arguably the most important right now. On the consumer side, switching costs are low — opening Booking.com or Cleartrip is a click away. But on the corporate side, they are extreme. Once a Tata Motors or an Aditya Birla Group has integrated Quest2Travel into its SAP ERP, its corporate card data feed, its policy engine and its expense reimbursement flow, the cost of ripping that out and replacing it is measured in months of work and seven-figure dollar amounts of consulting spend. This is the part of the moat that compounds quietly. Every year a large corporate stays on Q2T is a year that customer is more locked in.

The fifth power, branding, is enormous in the Indian consumer context. MakeMyTrip is a verb. The Hrithik Roshan / Alia Bhatt era of advertising in the mid-2010s, the Ranveer Singh holiday campaigns of 2021-2023, the constant presence in IPL ad breaks — all of it has built unaided brand recall in the high 90s among urban Indian travellers. The competing brands (Yatra, Cleartrip, EaseMyTrip) have meaningful share but not the same top-of-funnel pull.

The sixth power, cornered resource, is less applicable here. MakeMyTrip does not own a unique input. (Compare an airline with prime slots at a slot-constrained airport, or a pharma company with a patent.) That said, the redBus operator relationships in tier-2 and tier-3 cities are arguably a soft cornered resource — they were earned over a decade and would be very hard to replicate.

The seventh power, process power, is a slow-build advantage in fraud detection, payments routing, and customer service workflows. India's payments environment is uniquely complex (UPI, net-banking, EMI, wallets, cards, BNPL), and the operational know-how to maximise conversion across all these rails is years of accumulated learning. This is invisible from the outside but visible in the numbers — MakeMyTrip's payment success rate is a known KPI internally and is materially above industry averages.

Now Porter's 5 Forces.

Supplier power, the most worrying force right now. Indian aviation has consolidated dramatically. इंडिगो IndiGo operates the majority of all domestic seat-kilometres; the Tata Group's combined Air India / Vistara has roughly 30% on the international side. With two dominant carriers, the structural ability of these suppliers to push back on OTA commissions is real and growing. On the hotel side, supplier power is the opposite — the long tail of independent properties needs MMT more than MMT needs any individual property.

Buyer power: in retail consumer travel, low — individual buyers do not coordinate. In corporate travel, higher — a Tata Motors travel desk can extract better commercial terms. But Q2T's switching costs mostly neutralise this.

Threat of new entrants: the marquee threats are Google Travel and the global aggregators. Booking Holdings, Expedia and Trip.com would all love a bigger piece of India. So far, the local sourcing and customer-service moat has held. Indigenous threats include EaseMyTrip, which has carved out a meaningful niche, particularly with sub-tier-1 customers.

Threat of substitutes: airlines and hotels selling direct, which has grown steadily — IndiGo's direct-booking share is now north of 60% on its own routes. This is the most credible long-term substitute. MakeMyTrip's counter is the bundle: people buy flight + hotel + insurance + forex card from an OTA more easily than they assemble that bundle from four separate direct channels.

Industry rivalry: post-2017, much lower than pre-2016. The consolidation worked. The current state is a friendly duopoly in OTA (MMT, with EaseMyTrip and Yatra as smaller players), shading toward something closer to monopolistic competition.

The clean summary: MakeMyTrip's moat is multi-layered and structurally durable on the demand side, with rising fragility on the supplier side (airlines) and rising strength on the corporate-customer side. That is an unusual combination, and it points the strategic compass squarely at the corporate and fintech businesses as the place to compound from here.

VIII. Bear vs. Bull Case & Analysis

Every long-only investor who has owned MakeMyTrip at some point over the last decade has had to wrestle with a clean, almost binary debate. The bull case is structural and patient. The bear case is structural and impatient. Both are coherent. Both have, at different moments, been right.

The bull case starts with what investors have come to call the "India premium." The country's per-capita air-travel penetration in 2025 is roughly one-twentieth of China's, which itself is roughly half of the United States'. The runway is, almost literally, runway. Government infrastructure spending under the Modi administration's उड़ान UDAN regional connectivity scheme has added dozens of new operational airports — over 90 incremental airports brought into the commercial network since 2017. Domestic passenger traffic compounds at high single digits to low double digits. International outbound travel, particularly to Southeast Asia and the Gulf, compounds faster. Hotel supply in India is dramatically under-built relative to demand, which keeps hotel ADRs strong and supports MakeMyTrip's hotel take rates.

Layer on the shift from "unorganised" to "organised" travel — the slow migration of bookings from local agents, walk-in counters and cash-based informal arrangements to online channels. By most credible industry estimates, online penetration of Indian travel is still under 50%, with significant headroom in tier-2 and tier-3 cities and in older demographics. Each five-percentage-point shift in online penetration translates into multi-billion dollars of incremental addressable booking volume.

Then layer on the under-monetised optionality. TripMoney is, at current scale, a low-single-digit-percent contributor to revenue but is growing several multiples faster than the core business. Corporate travel is, at $1 billion in gross bookings, roughly a tenth of total — and likely a fifth or more of operating profit. Both lines have, by any reasonable benchmark, a decade of compound growth ahead before they saturate.

Finally, there is the consolidation argument. The ibibo merger broke the back of the OTA price war in India. With Yatra small, EaseMyTrip niche, and the international players unable to crack the local supply problem, MakeMyTrip enjoys a structural cost-of-acquisition advantage that should translate into widening operating margins. The bull view is that FY2025's 17% adjusted operating margin is a waystation, not a destination, and that a mature MMT operates closer to 25%.

Now the bear case.

The most pointed bear argument is what we will call the "IndiGo risk." When a single carrier controls 60%-plus of domestic seat-kilometres, that carrier holds the structural whip hand in distribution negotiations. IndiGo has, on multiple occasions, signalled willingness to push direct-booking share aggressively, reduce GDS/OTA commissions, and discipline the channel. So far the equilibrium has held — IndiGo benefits from OTA reach, and MMT benefits from IndiGo inventory — but every basis point of compression on flight take rates flows directly to MakeMyTrip's bottom line.

The second bear argument is platform risk. Google has been pushing its Google Travel and Google Flights products into India for several years. Google's leverage is that it sits one click before MakeMyTrip — at the search-intent moment. If Google decides to fully monetise that surface in India (it has been notably more aggressive in Europe and the US), MakeMyTrip pays the tax in higher performance-marketing spend, lower conversion, and possibly lower meta-search relevance. Meta-owned WhatsApp is another vector: as more booking flows happen inside WhatsApp via chatbot interfaces, the OTA risks becoming a backend supplier rather than the front-of-funnel brand.

The third bear argument is execution risk on the bundle thesis. TripMoney and corporate travel are great in theory, but the lending and payments world is heavily regulated. The Reserve Bank of India has been tightening BNPL norms, prepaid card norms, and digital lending guidelines since 2022. A single adverse regulatory action — say, a cap on partner-bank-issued prepaid forex cards or an RBI directive on travel-EMI products — could compress TripMoney's growth runway. The corporate travel business is less exposed to financial regulation but is exposed to corporate IT-spend cycles; in a recession, T&E budgets get cut first.

The fourth bear argument, the one we hear most often from professional sceptics, is valuation. At a market capitalisation hovering around $9 billion against fiscal 2025 adjusted operating profit of $167.3 million, MakeMyTrip trades at a multiple that prices in significant future growth. If gross bookings compound mid-teens for the next five years, the math works. If they decelerate to high single digits — say, because IndiGo eats more channel margin, or because Google Travel takes a structural piece — the multiple compresses.

There is a "myth versus reality" check worth running here too. The consensus narrative is that MakeMyTrip is a "post-COVID winner" that has compounded simply because Indian travel reopened. The reality, looking at the numbers, is that the underlying business model transformation — toward hotels, corporate travel, and TripMoney — was already underway pre-COVID, and the pandemic merely accelerated three pre-existing trends: market share consolidation (weaker OTAs got weaker), online penetration (offline agents shut), and corporate digitisation (every corporate suddenly needed expense automation). The post-COVID profitability is not a sugar-high; it is the visible surface of a multi-year mix shift.

Synthesising: the bull and bear cases both depend on the same handful of moving parts. The bull view says hotels and corporate compound at 20%+ while flight take rates merely stay flat. The bear view says flight take rates compress 100-200 basis points while the bundle businesses fail to scale fast enough to offset. The middle path — the most likely path — is messier than either, with steady consumer compounding, faster corporate compounding, and an open question on flight margins.

For a long-term fundamental investor, the KPIs to track on this story are remarkably narrow.

First, hotels and packages segment adjusted margin. This is the highest-quality revenue line in the business and the single best read on whether MakeMyTrip's pricing power is intact or eroding. Margin trend is more diagnostic than gross bookings growth here.

Second, corporate travel gross bookings growth, with attached attach-rate. Watch whether the $1 billion-plus corporate book continues to compound mid-twenties percent and whether new client wins are converting attached-services adoption (Happay, Q2T, myBiz cross-sell) at increasing rates.

Third, TripMoney attach rate per booking and disclosed unit economics. Specifically, how often a customer transacting on the consumer platform also takes a TripMoney product (forex card, BNPL, insurance), and what the contribution margin per attached product looks like. This is the leading indicator of whether the fintech optionality is real or theatrical.

If those three KPIs trend the right way, the bear case slowly loses oxygen. If any of them stalls, the bull case has to lean harder on multiple expansion than on fundamentals. Investors should also keep half an eye on a few second-order signals: any large Naspers stake reduction (would weaken the long-term-holder narrative), any RBI action against partner banks in the TripMoney stack, and any IndiGo announcement specifically targeting OTA commissions or direct-channel preference.

IX. Conclusion & Final Reflections

The most striking thing about MakeMyTrip, looking back across twenty-six years, is how little of its current shape was foreseeable from its founding premise. The company was not designed to be a corporate-travel SaaS leader. It was not designed to be a fintech. It was not designed to be the largest distributor of inter-city bus tickets in India. It was designed, in 2000, to sell airline tickets to American-residing Indians on a website. Every other line of business in the current company is, in some sense, a series of compounding adjacencies that were each one defensible step from the last.

That is also the story's lesson for founders and operators. The early-stage product-market fit — selling NRI flight tickets — was the entry ticket to the broader opportunity, not the opportunity itself. The opportunity was the slow build-out of capabilities (payments, supply, customer service, brand, balance sheet) that each enabled the next move. Without the 2005 pivot to India, there is no LCC-era growth. Without LCC-era growth, there is no IPO. Without the IPO and the NASDAQ-denominated equity currency, the all-stock ibibo merger is structurally impossible. Without the merger, there is no Naspers anchor, no redBus, no operational margin runway. Without that runway, the company would have been too capital-constrained to acquire Quest2Travel or Happay or build TripMoney organically.

The biggest single surprise in the whole arc, in retrospect, is the COVID-19 episode. A business that lost more than 90% of its quarterly gross bookings in Q1 of FY2021, that had to raise $180 million in convertibles to maintain liquidity, that paid its two most senior executives nothing for two years — that same business emerged in FY2022 onward with higher operating margins, accelerating gross bookings, and a strengthened corporate franchise. That is not survival; that is structural absorption of a tail event. The reason it happened is, we believe, fairly specific: the management team made hard decisions early, the balance sheet was solid heading in, and the consumer market consolidated around the strongest brand as weaker competitors closed offices or scaled back. Crises in concentrated markets tend to make the leader stronger, and that is what happened here.

A few last reflections.

The capital-allocation playbook MakeMyTrip has run since 2010 — list in the deepest capital market available, use the listing as a currency for strategic M&A, prefer all-stock deals that convert competitors into shareholders, integrate operationally rather than collapsing brands, layer adjacencies onto a stable core — is, almost without exception, what every successful consumer-platform company eventually does. The interesting part of MakeMyTrip's version is the willingness to do it across borders and currencies, which Indian peers have historically been more reluctant to do.

The management transition from Kalra to Magow is the cleanest founder-to-operator handoff in modern Indian internet history. It was telegraphed, staged, accompanied by a clear retention of the founder in a strategic role, and executed without operational disruption. It is the model other founder-led Indian public companies will study.

And the long arc — from a dot-com-era NRI service desk to a multi-business travel-and-fintech platform serving a country whose middle class will double again before 2035 — captures something specific about the Indian internet story that is easy to miss from the outside. The winners are not, mostly, the ones who invented categories. They are the ones who survived the 2001-2003 nuclear winter, picked the right second wave, and were patient enough to consolidate the market when consolidation became possible. MakeMyTrip did all three.

What happens next depends on whether the bundle thesis pays off — whether the hotels, corporate, and fintech lines can grow into majority-of-profit contributors before the legacy flight business gets squeezed from above by airlines and from beside by Google. The next five years of MakeMyTrip's story will be a referendum on that question. For now, the operator that survived the first dot-com bust, rode the LCC boom, listed on NASDAQ, ate its biggest competitor, and paid itself nothing during a pandemic gets the benefit of the doubt.

References

-

MakeMyTrip Limited Announces Fiscal 2025 Fourth Quarter and Full Year Results — MakeMyTrip Investor Relations, 2025 ↩↩

-

MakeMyTrip reports record gross bookings and revenue for 2025 — PhocusWire, 2025 ↩

-

MakeMyTrip Limited Form 424B1 IPO Prospectus — U.S. Securities and Exchange Commission, 2010-08 ↩

-

"It's a fairytale Nasdaq listing for MakeMyTrip" — DNA India, 2010-08 ↩

-

Tencent, Naspers JV Ibibo Buys Redbus To Grow Its Online Travel Empire In India — TechCrunch, 2013-06-21 ↩

-

Redbus to be Acquired by ibibo Group For $138 million — Inc42, 2013-06 ↩

-

MakeMyTrip Limited Form 6-K — ibibo Group acquisition announcement, U.S. Securities and Exchange Commission, 2016-10 ↩↩

-

Yatra merges with Terrapin 3 Acquisition Corp. at a $218 million valuation — YourStory, 2016-07 ↩↩

-

Covid-19: MakeMyTrip execs to draw zero salary, leadership to take 50% cut — Business Standard, 2020-03-25 ↩

-

MakeMyTrip Founder Deep Kalra moves into chief mentor role — IndUS Business Journal, 2022-01 ↩↩

-

MakeMyTrip to expand travel fintech play by opening up TripMoney — YourStory, 2022-02 ↩↩

-

MakeMyTrip acquires Quest2Travel to bolster its position in corporate travel — YourStory, 2019-04 ↩

-

MakeMyTrip gross corporate travel bookings cross $1 billion in 2025 — Business Standard, 2026-02-24 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube