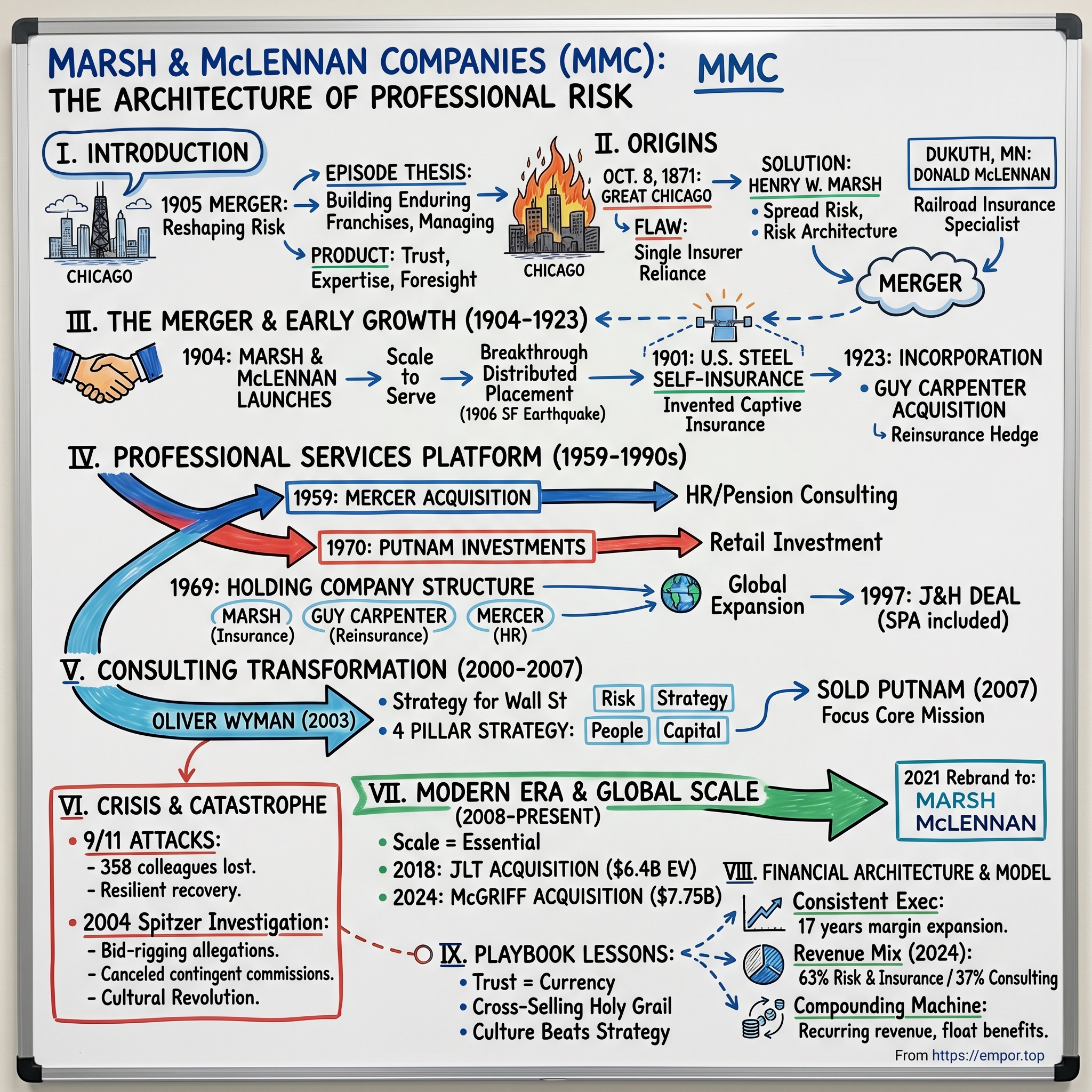

Marsh & McLennan Companies: The Architecture of Professional Risk

I. Introduction & Episode Thesis

The year is 1905. Chicago's business district hums with the energy of America's second city—steel frames rising into the sky, railroads converging from every direction, the stockyards processing the nation's meat supply. In a modest office building, two insurance brokers from different corners of the Midwest are about to shake hands on a merger that will reshape how the world thinks about risk.

Henry Marsh extends his hand to Donald McLennan. Neither man knows they're creating what will become a $24 billion revenue colossus that will one day employ 90,000 professionals across 130 countries. They certainly can't imagine their firm will survive two world wars, the Great Depression, the September 11 attacks that will claim 358 of their colleagues, and a devastating corruption scandal that will nearly destroy everything they built.

This is the story of Marsh & McLennan Companies—now simply Marsh McLennan—and how an insurance brokerage born from the ashes of the Great Chicago Fire evolved into one of the world's most powerful professional services firms. It's a tale of innovation in the most unlikely of industries: insurance. But more than that, it's about understanding a fundamental truth of modern capitalism: as business grows more complex, the firms that help navigate that complexity become indispensable.

The central question isn't just how MMC grew from a regional insurance broker to a global powerhouse. It's how they discovered that their real product wasn't insurance policies—it was trust, expertise, and the ability to see around corners in an increasingly uncertain world. From pioneering self-insurance for U.S. Steel to advising on cyber risk for Fortune 500 companies, from managing pensions for millions to consulting CEOs on strategy, MMC has positioned itself at the intersection of every major business risk and opportunity.

Our journey takes us from the charred ruins of 1871 Chicago through the gleaming towers of modern Manhattan. We'll explore how strategic acquisitions—Mercer, Guy Carpenter, Oliver Wyman—transformed a brokerage into a diversified advisory empire. We'll examine the near-death experience of the Spitzer investigation and the cultural revolution that followed. And we'll understand why, in an age of artificial intelligence and climate change, the business of managing risk has never been more valuable.

The playbook here isn't just about insurance or consulting. It's about building enduring franchises in professional services, managing reputational risk when trust is your primary asset, and the delicate art of serving multiple stakeholders who often have conflicting interests. For investors, it's a masterclass in recurring revenue models, the economics of float, and why boring businesses often make the best investments.

II. Origins: The Great Chicago Fire and the Birth of Modern Risk

October 8, 1871. Catherine O'Leary's barn on DeKoven Street erupts in flames. Within hours, Chicago is an inferno. The fire consumes 17,500 buildings, leaves 100,000 homeless, and destroys $200 million in property—roughly a third of the city's value. Insurance companies across America collapse under the weight of claims. Of the 202 insurance companies operating in Chicago before the fire, only 48 will survive to pay their obligations in full.

Among the ruins walks a 20-year-old insurance agent named Henry W. Marsh. He had started his agency earlier that year, perfect timing to watch his entire business model go up in smoke. But where others see catastrophe, Marsh sees opportunity. The fire hasn't just destroyed buildings—it's exposed a fatal flaw in how America insures itself. Too many businesses had placed all their coverage with single insurers, concentrating risk that should have been spread across multiple carriers. When those insurers failed, businesses discovered their insurance policies were worth less than the paper they were printed on.

Marsh begins developing a radical idea: what if, instead of depending on one insurance company, businesses could spread their risk across dozens of carriers? What if someone could act as an intermediary, understanding both the client's needs and the insurers' appetites, engineering coverage that no single company would underwrite alone? This wasn't just insurance brokerage—it was risk architecture.

By 1885, Marsh has proven his concept successful enough to join forces with R.A. Waller & Company, one of Chicago's surviving insurance firms. When Waller dies in 1889, Marsh sees his chance. He partners with Herbert J. Ulmann to buy controlling interest, creating Marsh, Ulmann and Company. They're not just selling insurance; they're pioneering what will become modern risk management—analyzing exposures, designing coverage programs, and most importantly, developing relationships with insurers across the country to ensure claims will actually be paid.

Meanwhile, 400 miles northwest in Duluth, Minnesota, another insurance revolution is brewing. Donald McLennan arrives in 1900 to establish an agency with L.B. Manley. Duluth in 1900 is experiencing its own boom—iron ore from the Mesabi Range flows through its ports, grain elevators tower over Lake Superior, and lumber barons are making fortunes. McLennan specializes in what others consider impossible: insuring the sprawling railroad networks that connect America's heartland to its coasts.

Railroad insurance in 1901 is considered almost unwriteable. The exposures are massive—derailments, fires, worker injuries, cargo losses—and span thousands of miles across multiple states with different laws and regulations. McLennan masters the complexity, developing innovative approaches to coverage that make him indispensable to railroad executives. His reputation spreads: here's someone who understands risk at scale.

The conceptual breakthrough both men share is profound. Insurance had traditionally been a local business—you knew your agent, your agent knew the local insurer, and that was that. Marsh and McLennan are thinking nationally, even globally. They're creating networks of relationships, databases of information, and most importantly, intellectual property around how to structure and place complex risks.

In 1901, Marsh lands the catch of a lifetime. He convinces Charles Schwab, president of the newly formed U.S. Steel Corporation—the world's first billion-dollar company—to adopt a revolutionary self-insurance program. Instead of paying premiums to insurers for predictable losses, U.S. Steel will retain those risks itself, using insurance only for catastrophic exposures. It's a concept that seems obvious in hindsight but was heretical at the time. Marsh doesn't just broker the deal; he designs the entire risk retention strategy, essentially inventing what we now call captive insurance.

This is the moment when insurance brokerage transforms from a sales job into a profession. Marsh isn't just placing coverage; he's consulting on risk strategy, analyzing loss data, and engineering financial structures. The U.S. Steel deal generates headlines across the business press. Every major corporation in America suddenly wants what Schwab has: sophisticated risk management that treats insurance as a financial tool rather than a necessary evil.

The stage is set for the meeting that will create an empire. Two men, two revolutionary approaches to risk, and a shared vision that the insurance industry's future lies not in selling policies but in solving problems.

III. The Merger That Created an Empire (1904–1923)

The letter arrives at Donald McLennan's Duluth office in late 1904. Henry Marsh proposes something audacious: combine their firms to create the world's largest insurance agency. McLennan reads the numbers twice—together, they're managing $3 million in annual premiums, more than any other broker in America. But it's not the size that intrigues him; it's the vision. Marsh writes about creating a firm that can serve any client, anywhere, for any risk. "The future of American business is scale," Marsh argues, "and only a firm of scale can serve it."

The merger negotiations happen in the Palmer House in Chicago, the city's grandest hotel, rebuilt after the Great Fire as a symbol of Chicago's resilience. Over cigars and brandy, the two men work out the details. It's not just a business combination—it's a philosophical alignment. Both believe insurance brokerage is evolving from a relationship business to a knowledge business. The firm that can aggregate the most expertise, data, and market access will dominate.

On November 15, 1904, Marsh & McLennan officially launches. The press release is bold: "The consolidated firm will maintain offices in Chicago, New York, Duluth, and will shortly establish operations in London and Paris." Critics scoff—American insurance firms don't operate internationally. Lloyd's of London has dominated global marine insurance for two centuries. But Marsh and McLennan understand something others don't: American corporations are about to conquer the world, and they'll need American advisors to help them do it.

The early years validate their thesis spectacularly. In 1906, the San Francisco earthquake and fire cause $235 million in losses—the largest insurance event in history. While other brokers scramble, Marsh & McLennan's distributed placement strategy means their clients' claims are spread across dozens of carriers, ensuring payment. Word spreads: when disaster strikes, you want Marsh & McLennan in your corner.

By 1910, they're pioneering another innovation: blanket coverage. Instead of insuring each building, each shipment, each piece of equipment separately, why not create master policies that cover all of a corporation's assets? It seems obvious now, but it requires sophisticated understanding of both insurance law and corporate structure. The railroads love it—one policy instead of thousands. Manufacturing giants follow suit.

World War I transforms everything. American companies supplying the Allies need coverage for ships crossing U-boat-infested waters. Traditional marine insurers balk at the risk. Marsh & McLennan engineers a solution: spread the risk across hundreds of insurers, each taking a tiny slice, with reinsurance treaties spreading it further. They're essentially creating the first syndicated insurance programs, a technique that will become standard practice but is revolutionary in 1917.

The post-war boom brings new challenges. In 1920, Marsh and McLennan face a crossroads. They're managing such complex transactions that the partnership structure is becoming unwieldy. Clients want continuity—what happens if Marsh or McLennan dies? Employees want equity participation. The capital requirements for international expansion are enormous.

On January 2, 1923, Marsh & McLennan incorporates, becoming Marsh & McLennan, Incorporated. It's more than a legal restructuring—it's a declaration that this is now an institution, not just a partnership. The same year, they make their first major acquisition: Guy Carpenter & Company, founded just a year earlier by Guy Carpenter, a reinsurance specialist who's developed revolutionary techniques for helping insurance companies manage their own risks.

The Guy Carpenter acquisition is strategic genius. While Marsh & McLennan helps corporations buy insurance, Guy Carpenter helps insurance companies buy reinsurance—insurance for insurers. It's the ultimate hedge: when insurance markets harden and capacity shrinks, Guy Carpenter knows where to find it. When markets soften and insurers compete aggressively, Marsh & McLennan benefits from lower prices for clients. They're playing both sides of the market, legally and ethically, creating information advantages that competitors can't match.

By 1923's end, Marsh & McLennan operates in twelve cities across three continents. They're handling insurance for Standard Oil's global operations, U.S. Steel's expanding empire, and the emerging automotive industry. Annual premiums under management exceed $25 million. Henry Marsh, now 72, steps back from daily operations. Donald McLennan, a decade younger, assumes the presidency.

In a letter to employees that December, McLennan writes: "We have built something unique in American business—a firm whose product is expertise, whose inventory is relationships, and whose value is trust. Guard these assets carefully, for they are more fragile than they appear and more valuable than our balance sheet can capture."

The empire is built. Now comes the challenge of managing it through the boom of the 1920s, the crash that will follow, and the global catastrophe looming in the decade ahead.

IV. Building the Professional Services Platform (1959–1990s)

William Armstrong sits across from the Mercer family in a Manhattan conference room in spring 1959. As Marsh & McLennan's CEO, he's about to make a bet that will transform the company forever. The Mercers run a small but prestigious human resources consulting firm—they literally invented pension consulting in the 1940s. Armstrong sees something others don't: the same corporations buying insurance from Marsh & McLennan are desperately seeking help with employee benefits. Why not own both conversations?

The board is skeptical. "We're insurance brokers," one director argues. "What do we know about consulting?" Armstrong's response becomes company legend: "We're not insurance brokers. We're trusted advisors who happen to broker insurance. There's a difference."

The Mercer acquisition closes for $4.5 million—a fortune in 1959 but a rounding error compared to what it will generate. Within five years, Mercer is contributing 15% of MMC's profits. More importantly, it validates Armstrong's vision: professional services are converging. The same CEO buying insurance needs help with pensions, the same CFO managing risk wants investment advice, the same head of HR designing benefits needs compensation consulting.

The 1960s become a laboratory for this hypothesis. In 1962, MMC goes public, raising capital for expansion. The IPO prospectus describes a company in transition: "While insurance brokerage remains our core business, we see our future in the broader field of risk management and employee benefits consulting." Wall Street is intrigued but confused. The stock trades at a discount to pure-play insurers.

Then comes 1969, a year of radical restructuring. MMC creates a holding company structure, essentially inventing the professional services conglomerate model that firms like Accenture and PwC will later adopt. Each business—Marsh (insurance), Guy Carpenter (reinsurance), Mercer (HR consulting)—operates independently but shares resources, relationships, and most crucially, clients.

The masterstroke comes in 1970: the acquisition of Putnam Investments for $12 million. Founded in 1937 by George Putnam, it manages mutual funds for individual investors. The board is baffled. "What does retail investment management have to do with corporate insurance?" CEO John Regan has a ready answer: "Everything is converging around financial services. The same math that prices insurance can price options. The same companies we insure have pension assets to invest. The same distribution networks that sell insurance can sell mutual funds."

Regan, who becomes CEO in 1973, is a force of nature. Six-foot-four, Harvard MBA, Navy veteran, he speaks in military metaphors and thinks in global terms. His first executive meeting opens with a map of the world. "Gentlemen," he announces, "American companies are conquering the globe. They need us everywhere they go. By 1980, half our revenue will come from outside the United States."

The room goes silent. International expansion means buying foreign brokerages, navigating local regulations, managing currency risk. It's expensive, complex, and risky. Regan doesn't care. Over the next decade, MMC acquires insurance brokerages in London, Paris, Frankfurt, Tokyo, Sydney. Each acquisition brings local expertise and relationships that would take decades to build organically.

The strategy works brilliantly—until it doesn't. By the late 1980s, MMC is a sprawling empire with operations in 40 countries, but coordination is a nightmare. Different computer systems, different cultures, different approaches to client service. Costs are spiraling. In 1989, profits actually decline despite revenue growth.

The board brings in A.J.C. Smith as CEO in 1992. British, cerebral, a chess player's mind for strategy, Smith sees the problem immediately: MMC has been acquiring without integrating. His solution is radical for its time: create global practice groups that cross business units and geographies. A client working with Marsh in New York should get the same expertise and service standards as in Singapore.

The transformation accelerates with technology. In 1994, MMC spends $200 million—an astronomical sum—building a proprietary global data network. Every office, every professional, connected in real-time. Client information, market intelligence, best practices, all flowing freely across the organization. Competitors mock the investment. Within three years, they're desperately trying to copy it.

The decade culminates with the deal that changes everything: the $1.8 billion acquisition of Johnson & Higgins in 1997. J&H isn't just any insurance broker—it's Marsh's oldest rival, founded in 1845, with deep relationships MMC has coveted for decades. The integration is brutal. Thousands of layoffs, office closures, culture clashes. But when the dust settles, MMC has reclaimed its position as the world's largest insurance broker, a title it had briefly lost to Aon.

More importantly, the J&H deal brings something priceless: their consulting division, which includes a small but elite strategy consulting firm called Strategic Planning Associates. SPA's alumni include titans of business: Michael Porter, the strategy guru; Mitt Romney, who went on to found Bain Capital. This isn't just insurance consulting—it's McKinsey-level strategy work.

Smith sees the opportunity immediately. If MMC can build a world-class strategy consulting practice to complement its insurance and HR consulting businesses, it becomes something unprecedented: a one-stop shop for corporate executives dealing with any form of risk or strategic challenge.

The foundation is set for the final transformation. MMC is no longer an insurance broker with some consulting operations. It's becoming something new: a professional services platform that happens to include insurance brokerage. The distinction matters enormously for valuation, talent acquisition, and strategic optionality.

V. The Consulting Transformation: Oliver Wyman & Strategic Evolution (2000–2007)

John Drzik stands before the MMC board in February 2003, making the pitch of his career. As head of Mercer's strategy consulting arm, he's advocating for what seems like an insane acquisition: Oliver, Wyman & Company, a 400-person financial services consulting boutique. The price tag—$200 million—isn't the issue. It's the ambition. "This puts us in direct competition with McKinsey," one board member observes. Drzik's response: "That's exactly the point."

Oliver Wyman isn't just any consulting firm. Founded in 1984 by former Booz Allen partners, it has quietly become the go-to strategic advisor for Wall Street CEOs. When Sandy Weill needs help merging Citigroup, he calls Oliver Wyman. When Dick Fuld wants to transform Lehman Brothers into a global powerhouse, Oliver Wyman designs the strategy. Their financial services expertise is unmatched, their partner roster reads like a future Fortune 500 CEO list.

The cultural fit seems impossible. Oliver Wyman consultants are McKinsey refugees—cerebral, theoretical, PowerPoint virtuosos who speak in frameworks and matrices. Marsh & McLennan is a relationship business—practical, client-focused, deal-makers who speak in premiums and coverage terms. The first integration meeting is a disaster. An Oliver Wyman partner presents a 100-slide deck on "synergy capture methodology." A Marsh executive interrupts: "This is great, but can you actually sell anything?"

CEO Jeffrey Greenberg forces the issue. Son of legendary AIG CEO Hank Greenberg, Jeffrey understands power and how to wield it. His vision is breathtaking in scope: create a consulting division that rivals the Big Three (McKinsey, Bain, BCG) but with something they lack—deep operational expertise in insurance, risk management, and human capital. "McKinsey can tell you the strategy," he tells investors, "but we can actually implement it through our operating businesses."

The transformation accelerates in 2004. Greenberg consolidates all of MMC's strategy consulting assets—Mercer Management Consulting, Mercer Delta (organizational consulting), and the newly acquired Oliver Wyman—into a single division. The brand architecture is complex: keep the Oliver Wyman name for financial services, use Mercer for everything else. It's messy, but it preserves the equity both brands have built.

Then comes the masterstroke: the creation of Oliver Wyman's "Risk Journal," a thought leadership platform that publishes cutting-edge research on financial risk, regulatory change, and strategic transformation. Within two years, it becomes required reading for bank CEOs and regulators. The European Central Bank starts citing Oliver Wyman research. The Federal Reserve quietly hires them for stress testing expertise.

The consulting transformation reaches its apex in 2007 with a radical reorganization. All strategy consulting—whether branded Mercer or Oliver Wyman—is unified under the Oliver Wyman banner. It's a $1 billion revenue business with 3,000 consultants across 40 offices. The press release is bold: "Oliver Wyman is now one of the world's leading management consulting firms."

But the real story is the four-pillar strategy that emerges. MMC is now organized into four distinct but synergistic businesses: Marsh (risk consulting and insurance brokerage), Guy Carpenter (reinsurance), Mercer (human resources consulting), and Oliver Wyman (strategy consulting). Each pillar stands alone competitively but creates exponential value together.

Consider a typical Fortune 500 client circa 2007. The CEO works with Oliver Wyman on digital transformation strategy. The CFO uses Marsh for insurance and enterprise risk management. The head of HR partners with Mercer on pension restructuring. The treasurer places reinsurance through Guy Carpenter for the company's captive insurer. Four different buyers, four different relationships, but one coordinated account team sharing intelligence and opportunities.

The synergies are real but subtle. Oliver Wyman's analysis of a bank's operational risk helps Marsh design better directors' and officers' insurance. Mercer's pension expertise helps Oliver Wyman advise on M&A transactions. Guy Carpenter's catastrophe modeling enhances Marsh's property insurance placements. It's a virtuous cycle of expertise and information advantage.

The financial engineering is equally sophisticated. In 2007, MMC makes a strategic decision that will define its next decade: sell Putnam Investments for $3.9 billion to Power Financial of Canada. The mutual fund business, acquired for $12 million in 1970, has been wildly profitable but increasingly disconnected from the core professional services platform.

Greenberg's successor, Michael Cherkasky, frames the sale brilliantly: "We're not abandoning asset management. We're focusing on our core mission—risk, strategy, and people. The capital from Putnam will fund technology investments, acquisitions, and shareholder returns that accelerate our transformation."

The market loves it. MMC's stock rises 15% on the announcement. The multiple expansion is even more dramatic—MMC starts trading at professional services multiples rather than insurance brokerage multiples. The difference is worth billions in market capitalization.

By late 2007, the transformation seems complete. MMC has successfully evolved from an insurance brokerage with some consulting operations to a diversified professional services firm that happens to include insurance brokerage. Revenue exceeds $13 billion. Operating margins have expanded 400 basis points. The stock trades at all-time highs.

But storm clouds are gathering. The financial crisis is about to test every assumption about risk management. The Spitzer investigation's aftermath still haunts the culture. And Oliver Wyman is about to be thrust into the spotlight as advisor to the very banks that will need taxpayer bailouts.

The consulting transformation has succeeded brilliantly. The question now is whether MMC can navigate the catastrophes ahead while maintaining the trust that underpins its entire business model. As one Oliver Wyman partner presciently observes in December 2007: "We've built the perfect professional services firm for a stable world. Too bad the world is about to become very unstable."

VI. Crisis & Catastrophe: 9/11 and the Spitzer Investigation (2001–2005)

8:46 AM, September 11, 2001. American Airlines Flight 11 tears through floors 93 to 99 of the World Trade Center's North Tower. The entire impact zone houses Marsh & McLennan's global headquarters. In an instant, 295 employees and 63 contractors are gone. No evacuation was possible. No goodbye calls were made. It remains the largest loss of life by any single company in the attacks.

The human tragedy defies comprehension. Senior executives, administrative assistants, technology specialists, consultants visiting from other offices—entire departments eliminated in seconds. Among the dead: 30-year veterans weeks from retirement and recent college graduates on their third day of work. The memorial wall at MMC's new headquarters lists each name. Reading it takes seventeen minutes.

CEO Jeffrey Greenberg is in midtown when the first plane hits. His initial thought is accident—how could a plane hit a building on a clear day? Then the second plane strikes the South Tower. He knows immediately: this is an attack, and his people are gone. The command center he establishes at the Millennium Hotel becomes a makeshift crisis headquarters, then an evacuation point when the towers fall, then a gathering place for families seeking information about loved ones who will never come home.

The business implications are staggering beyond the human loss. MMC's data centers, client files, and operational headquarters are vaporized. But within hours, a remarkable thing happens: offices worldwide spring into action. London takes over North American operations. Tokyo handles Asian clients. Technology teams work 72 straight hours rebuilding systems from backup tapes. By September 17, when markets reopen, MMC is fully operational.

The insurance industry implications are equally profound. As the world's largest insurance broker, Marsh must now handle the largest insurance claim in history—for the very buildings where their colleagues died. The complexity is unprecedented: who's liable, which policies respond, how to value the losses. Marsh ultimately helps clients recover $4.5 billion in insurance proceeds, but every dollar is shadowed by the memory of those lost.

The firm's response becomes a Harvard Business School case study in crisis management and organizational resilience. Grief counselors in every office. Full salary continuation for victims' families. College scholarships for victims' children. A memorial fund that raises $17 million. But nothing can fill the void. As one survivor puts it: "We learned that day that our greatest asset wasn't our expertise or client relationships. It was each other."

Just as MMC begins to heal, a new existential threat emerges. October 14, 2004: New York Attorney General Eliot Spitzer holds a press conference that sends MMC stock plummeting 25% in minutes. His accusation: Marsh has been rigging bids, steering business to insurers who pay the highest "contingent commissions"—essentially kickbacks for sending them business. Spitzer plays damning recordings of Marsh brokers discussing how to manipulate bids. "This is not a technical violation," he thunders. "This is corruption at the highest levels."

The allegations are devastating precisely because they strike at MMC's core asset: trust. If clients can't trust Marsh to act in their best interests, the entire business model collapses. Within days, major clients launch reviews. Competitors circle like sharks. The stock price craters from $45 to $22.

Jeffrey Greenberg resigns as CEO within two weeks—a stunning fall for someone who had transformed MMC into a global powerhouse. The board, desperate to contain the damage, makes an extraordinary choice: Michael Cherkasky, former prosecutor and, ironically, one of Spitzer's mentors. The message is clear: we're bringing in someone of unimpeachable integrity to clean house.

Cherkasky's first acts are dramatic. He eliminates contingent commissions entirely—walking away from $845 million in annual revenue. He implements radical transparency: clients can see every dollar Marsh receives from insurers. He settles with Spitzer for $850 million, at the time the largest settlement in regulatory history. He replaces dozens of senior executives. The cultural revolution is brutal but necessary.

The financial impact is severe. Revenue drops $1.5 billion in 2005. Operating margins collapse. The stock languishes below $30 for two years. But Cherkasky understands something critical: this crisis is also an opportunity. By eliminating contingent commissions, Marsh can claim the moral high ground. By embracing transparency, they differentiate from competitors still clinging to the old model.

The strategy works, slowly. Clients who initially fled start returning, appreciating the new transparency. Younger employees, horrified by the scandal, embrace Cherkasky's reforms with missionary zeal. The culture shifts from sales-driven to advisory-focused. As one senior executive observes: "Spitzer didn't almost destroy us. He forced us to become who we always claimed to be."

The industry-wide impact is transformative. Every major broker eventually abandons contingent commissions. Transparency becomes table stakes. The entire business model shifts from placement-focused (where brokers are paid for moving premium) to advisory-focused (where they're paid for expertise and service). It's creative destruction at its most painful but necessary.

By 2007, MMC has largely recovered. The stock reaches new highs. Client satisfaction scores exceed pre-scandal levels. But the scars remain. A compliance culture now permeates everything—every email monitored, every client interaction documented, every potential conflict disclosed. The free-wheeling entrepreneurial culture that built MMC is gone, replaced by something more professional but less dynamic.

Two existential crises in four years have transformed MMC fundamentally. The firm that emerges is more resilient, more transparent, more focused on its core mission. But it's also more cautious, more bureaucratic, more aware of its vulnerabilities. As Cherkasky steps down as CEO in 2008, his parting words capture the transformation: "We've learned that our license to operate comes not from regulators but from the trust of our clients. Guard that trust above all else, because once lost, it may never fully return."

The lessons are seared into institutional memory: operational resilience matters more than efficiency, reputation matters more than revenue, and culture matters more than strategy. These aren't just corporate platitudes—they're survival skills learned through catastrophic loss. The MMC that enters the financial crisis is a different company than the one that entered the millennium: harder, wiser, and acutely aware that tomorrow is promised to no one.

VII. The Modern Era: JLT Acquisition & Global Scale (2008–Present)

Brian Duperreault steps into the CEO office in January 2008, just as the financial world begins to unravel. A legendary insurance executive who transformed ACE into a global giant, he's been brought in to stabilize MMC after the Spitzer scandal and position it for growth. His timing seems terrible—Bear Stearns collapses two months later, Lehman Brothers falls in September, and MMC's Oliver Wyman consultants are suddenly advising banks that may not survive the week.

But Duperreault sees opportunity in chaos. "Every crisis reshapes the competitive landscape," he tells the board. "The firms that emerge strongest are those that invested during the downturn." While competitors retrench, MMC goes shopping. Small acquisitions at first—specialty brokers, niche consultancies—but each strategically chosen to fill capability gaps or enter new markets.

The real transformation begins under Dan Glaser, who becomes CEO in 2013. A Marsh lifer who started as an intern, Glaser understands the business at a molecular level. His strategic insight is profound: in a world of increasing complexity and regulation, scale isn't just an advantage—it's essential. Only the largest firms can afford the technology, compliance infrastructure, and global reach that sophisticated clients demand. Glaser's masterstroke comes in September 2018. Marsh & McLennan announces an agreement to acquire Jardine Lloyd Thompson Group plc (JLT), a leading provider of insurance, reinsurance and employee benefits related advice, brokerage and associated services. Total cash consideration equates to $5.6 billion U.S. dollars in fully diluted equity value, or an estimated enterprise value of $6.4 billion. The price seems astronomical—a 33.7% premium to JLT's trading price.

But Glaser sees what others miss. JLT isn't just another broker—it's the missing piece in MMC's global puzzle. Founded through the 1997 merger of Jardine Insurance Brokers and Lloyd Thompson Group, JLT brings unmatched expertise in specialty lines: aviation, marine, energy, construction. More importantly, it provides deep penetration in markets where MMC is weak: Asia, Latin America, and specialty reinsurance.

The deal, which was hammered out in about 11 days between MMC's Glaser and JLT's Burke, is one of the largest ever involving insurance brokers. The speed is remarkable—most deals this size take months of negotiation. But Glaser and Dominic Burke, JLT's CEO, share a vision: in a consolidating industry, only scale players will survive.

The integration strategy is sophisticated. The JLT name will largely be absorbed into Marsh except it will be used for a new unit, Marsh-JLT Specialty, which was formed by combining the specialty teams of both firms. This preserves JLT's specialty expertise while leveraging Marsh's global infrastructure. JLT also brings Marsh & McLennan a significant influx of talent — adding more than 10,000 colleagues.

MMC anticipates annual cost synergies of approximately $250 million that will be realized over the next three years. It is expected that the realization of these cost synergies will result in one-time integration costs of approximately $375 million. The math is compelling: pay $375 million once to generate $250 million annually forever.

The transaction was completed on 1 April 2019, after receiving regulatory approvals globally. The companies estimate that Marsh & McLennan's revenue will rise to about $17 billion as a result of the acquisition

The digital transformation accelerates under Doyle's leadership. In 2023, MMC launches Marsh McLennan Advantage, an AI-powered platform that synthesizes data across all four businesses to provide predictive analytics on risk trends. The technology investment—$500 million over three years—is the largest in company history. Critics call it ambitious; clients call it transformative.

The pace of consolidation continues to accelerate. Throughout 2024, MMC completes dozens of smaller acquisitions—specialty brokers, boutique consultancies, technology startups—each adding capabilities or geographic reach. The strategy is clear: in a fragmenting risk landscape, only firms with comprehensive capabilities can serve sophisticated clients effectively.

The McGriff acquisition, completed November 15, 2024, brings immediate scale. With the closing of this acquisition, McGriff's more than 3,500 colleagues join Marsh McLennan Agency. Founded in 1886, McGriff is a leading provider of insurance broking and risk management services in the United States. The cultural integration proves smoother than JLT—McGriff's entrepreneurial culture aligns naturally with MMA's middle-market focus.

In April 2021, Marsh & McLennan Companies rebranded to Marsh McLennan coinciding with the 150th anniversary of subsidiary Marsh. The rebrand is more than cosmetic—it signals a fundamental shift in how the company sees itself. No longer a holding company with disparate businesses, but an integrated enterprise delivering solutions at the intersection of risk, strategy, and people.

The financial performance validates the strategy. With annual revenue of over $24 billion and more than 90,000 colleagues, Marsh McLennan helps build the confidence to thrive through the power of perspective. For the full year, we generated 7% underlying revenue growth, 10% adjusted EPS growth and 80 basis points of adjusted margin expansion, marking our 17th consecutive year of reported margin expansion.

The transformation under Doyle represents the culmination of two decades of evolution. From the ashes of 9/11 and the Spitzer scandal, through the financial crisis and digital revolution, MMC has emerged as something unprecedented: a professional services firm with the scale of a Fortune 500 company but the expertise of a boutique consultancy.

VIII. Financial Architecture & Business Model

The numbers tell a story of relentless execution. Revenue for full-year 2024 was $24.5 billion, an increase of 8% compared with 2023, or 7% on an underlying basis (full-year 2023 revenue: $22.7 billion). But the real story isn't growth—it's consistency. For the full year, we generated 7% underlying revenue growth, 10% adjusted EPS growth and 80 basis points of adjusted margin expansion, marking our 17th consecutive year of reported margin expansion.

Seventeen consecutive years. Through recessions, pandemics, geopolitical crises—MMC has expanded margins every single year since 2008. This isn't luck or timing; it's the result of a business model engineered for resilience and growth.

The revenue mix reveals the strategy. For the year 2024, revenue was $15.4 billion, an increase of 9% compared with 2023, or 8% on an underlying basis. for Risk & Insurance Services, while Consulting contributes the remainder. This 63/37 split is deliberate—insurance brokerage provides steady, recurring revenue; consulting offers higher margins and growth potential.

Within Risk & Insurance Services, the composition is equally strategic. For the year 2024, Marsh's revenue growth was 10% compared to a year ago, or 7% on an underlying basis. For the year 2024, Guy Carpenter's revenue grew 5% compared to a year ago, or 8% on an underlying basis. The faster growth at Marsh reflects the continued hardening of commercial insurance markets and expansion into new risk categories like cyber and climate.

The economics of insurance brokerage are compelling. Unlike insurers who take underwriting risk, brokers earn commissions—typically 10-20% of premiums—without capital exposure. In hard markets when premiums rise, broker revenues increase automatically. In soft markets, brokers compensate through volume growth and market share gains. It's a heads-I-win, tails-you-lose proposition.

But the real competitive advantage is float. Insurance premiums flow through broker accounts before reaching insurers. At any given moment, MMC holds billions in client funds. Invested conservatively, this float generates hundreds of millions in investment income—essentially free money for providing a service clients need anyway.

The consulting businesses operate on a different model but equally attractive economics. Mercer and Oliver Wyman bill by the project or retainer, with operating margins approaching 20%. The key is leverage: partners who win work, managers who oversee it, analysts who execute it. The pyramid structure means that as the firm grows, margins naturally expand.

The acquisition playbook is remarkably consistent. Target firms with $50-500 million in revenue, strong local relationships, and specialized expertise. Pay 10-15x EBITDA—expensive but justified by synergies. Integrate the back office immediately but preserve the front-office culture. Cross-sell into the MMC client base. Achieve 20%+ IRR within three years.

On September 29, 2024, the Company entered into an agreement to acquire McGriff Insurance Services, LLC, a leading provider of insurance broking and risk management services in the United States, with $1.3 billion of revenue for the trailing twelve months ended June 30, 2024. Under the terms of the transaction, Marsh McLennan will pay $7.75 billion in cash consideration, funded by a combination of cash and proceeds from debt financing. The price seems steep—roughly 6x revenue—but the strategic logic is compelling. McGriff brings deep penetration in the U.S. middle market, exactly where MMA needs scale.

Capital allocation follows a clear hierarchy. First, invest in organic growth—technology, talent, geographic expansion. Second, pursue strategic acquisitions that fill capability gaps or accelerate market entry. Third, return excess capital through dividends and buybacks. The discipline is ruthless: every dollar must earn its cost of capital or be returned to shareholders.

The margin expansion story deserves particular attention. Seventeen consecutive years doesn't happen by accident. It's the result of systematic operational improvement: technology replacing manual processes, offshore centers handling routine work, shared services eliminating duplication. Every basis point matters when you're managing $24 billion in revenue.

But the real driver is mix shift. As MMC adds higher-margin consulting revenue and exits lower-margin businesses, the overall margin naturally expands. It's financial engineering at its finest—not cutting costs but changing the composition of revenue.

The balance sheet is a fortress. Despite the McGriff acquisition, leverage remains below 3x EBITDA. The credit rating is investment grade. Cash generation is robust—over $3 billion in free cash flow annually. This financial strength provides flexibility: to invest through downturns, to make opportunistic acquisitions, to weather unexpected crises.

Risk management—ironically for a risk management firm—is sophisticated. Revenue is diversified across geographies, industries, and service lines. Client concentration is minimal—no single client represents more than 1% of revenue. Contracts are typically annual but with 85%+ retention rates, providing quasi-recurring revenue.

The technology transformation, while expensive, is already paying dividends. Digital platforms reduce cost-to-serve by 30%. AI-powered analytics win larger deals at higher margins. Automated workflows free consultants to focus on value-added activities. The $500 million annual technology investment seems large until you realize it's only 2% of revenue—a bargain for maintaining competitive advantage.

Looking forward, the financial model appears sustainable. Organic growth should track GDP plus 200-300 basis points, driven by share gains and new risk categories. Margins should expand 50-100 basis points annually through mix shift and operational leverage. Free cash flow conversion should exceed 100% of net income. Returns on invested capital should remain in the mid-teens.

The beauty of the model is its simplicity. Grow revenue mid-single digits. Expand margins slightly faster. Buy back shares consistently. Compound at 10-12% annually. It's not exciting, but it's inexorable. Over a decade, shareholders double their money. Over two decades, they quadruple it.

This is the architecture of a financial fortress: diversified revenue, expanding margins, strong cash generation, disciplined capital allocation. It's built to survive crises and capitalize on opportunities. Most importantly, it's built to compound wealth over decades, not quarters.

IX. Playbook: Lessons in Professional Services

The Marsh McLennan story offers a masterclass in building and scaling professional services firms. The lessons learned over 150 years—through booms, busts, scandals, and transformations—constitute a playbook that transcends industry boundaries.

Lesson 1: Trust is the Ultimate Currency

In professional services, you're selling invisible products—advice, expertise, judgment. Clients can't evaluate quality until after they've purchased, sometimes not even then. This information asymmetry means trust becomes the primary purchasing criterion. MMC learned this painfully during the Spitzer crisis: when trust evaporates, clients flee regardless of expertise or price.

Building trust requires radical transparency. After Spitzer, MMC didn't just eliminate contingent commissions; they published every revenue source, disclosed every potential conflict, and invited client scrutiny. The short-term revenue hit was massive—$845 million annually. The long-term benefit was invaluable—clients knew MMC would sacrifice profits for principles.

Lesson 2: Cross-Selling is the Holy Grail

Every professional services firm dreams of cross-selling. Few achieve it. MMC's success comes from understanding that cross-selling isn't about pushing products—it's about solving interconnected problems. When Oliver Wyman helps a bank with strategy, Marsh naturally handles the D&O insurance, Mercer redesigns the compensation structure, and Guy Carpenter provides reinsurance for the bank's captive.

The key is organizational design. MMC maintains separate P&Ls for each business but compensates leaders on enterprise success. Client teams include professionals from multiple businesses. Knowledge sharing is mandated, not suggested. The friction of coordination is real, but the value creation is exponential.

Lesson 3: Scale Enables Specialization

The paradox of professional services: clients want both breadth and depth. They want advisors who understand their specific industry, geography, and challenges, but also have global resources and best practices. MMC squares this circle through scale—90,000 professionals means they can afford specialists in Norwegian aquaculture insurance and experts in Japanese pension regulation.

This specialization creates a virtuous cycle. Deep expertise wins marquee clients. Marquee clients attract top talent. Top talent develops innovative solutions. Innovation wins more clients. The cycle accelerates until MMC becomes the default choice in narrow but lucrative niches.

Lesson 4: Culture Beats Strategy

The Spitzer scandal revealed a cultural rot that nearly destroyed MMC. The rebuild wasn't just about changing policies—it was about changing people. Out went the sales-at-any-cost cowboys. In came professionals who saw themselves as fiduciaries. The cultural transformation took years and cost billions in lost revenue, but it saved the company.

Today's MMC culture emphasizes long-term relationships over short-term revenue, collaborative problem-solving over individual heroics, and ethical behavior over competitive advantage. It's codified in training programs, reinforced through compensation, and modeled by leadership. When 90,000 people internalize these values, culture becomes competitive advantage.

Lesson 5: Manage Conflicts Transparently

Professional services firms face inherent conflicts. MMC advises both insurers and insurance buyers. Oliver Wyman consults for competing banks. Mercer designs pension plans for companies and advises the employees who participate in them. These conflicts can't be eliminated—they can only be managed.

MMC's approach is radical transparency plus structural separation. Different teams serve competing clients. Information barriers prevent sharing of confidential data. Conflicts are disclosed proactively, not defensively. Clients can object to specific arrangements. The system isn't perfect, but it's transparent, which builds trust even amid inherent tensions.

Lesson 6: Technology is a Tool, Not a Solution

MMC has invested billions in technology, but technology alone never wins. The value comes from combining technology with human expertise. AI can analyze millions of insurance claims, but humans interpret patterns and design solutions. Digital platforms can deliver standardized services efficiently, but complex problems require human judgment.

The technology strategy is augmentation, not replacement. Free humans from routine tasks so they can focus on high-value activities. Use data to inform decisions, not make them. Deploy technology to scale expertise, not substitute for it. When technology and talent combine, the result is exponentially more powerful than either alone.

Lesson 7: Consolidation is Inevitable

Professional services is consolidating for fundamental reasons: clients want integrated solutions, technology requires scale, talent expects global opportunities, and shareholders demand growth. MMC has been both consolidator and consolidated, acquiring hundreds of firms while maintaining its independence.

The playbook for successful consolidation is consistent: preserve the acquired firm's client relationships and culture while integrating back-office functions. Don't rebrand immediately—let the acquired firm's reputation transfer to MMC gradually. Invest in the acquired firm's growth before extracting synergies. Most importantly, retain key talent through incentives and culture, not just contracts.

Lesson 8: Diversification Requires Discipline

MMC's evolution from insurance brokerage to diversified professional services wasn't random—it followed client needs. Each expansion—into reinsurance, HR consulting, strategy consulting—addressed problems that existing clients faced. This client-centric diversification ensures natural cross-selling opportunities and reduces execution risk.

But diversification requires discipline. MMC's sale of Putnam Investments illustrates this—despite generating enormous profits, asset management didn't fit the professional services model. The discipline to exit successful but non-strategic businesses is as important as the courage to enter new ones.

Lesson 9: Global Reach, Local Presence

Professional services is inherently local—regulations, cultures, and business practices vary by geography. Yet clients increasingly operate globally and expect consistent service worldwide. MMC bridges this gap through a hub-and-spoke model: global centers of excellence connected to local offices with deep market knowledge.

The balance is delicate. Too much centralization and you lose local relevance. Too much localization and you sacrifice global leverage. MMC maintains this balance through matrix organizations, rotation programs, and technology platforms that share knowledge while preserving local autonomy.

Lesson 10: Reputation is Asymmetric

Building reputation takes decades. Destroying it takes minutes. MMC learned this through 9/11 and the Spitzer investigation—crises that threatened the firm's existence despite 100 years of success. The asymmetry means reputation risk management must be embedded in every decision.

This manifests in countless ways: turning down lucrative but questionable clients, disclosing unfavorable information proactively, investing in compliance beyond regulatory requirements. The opportunity cost is real—MMC forgoes billions in potential revenue. But the alternative—another reputation crisis—could be fatal.

These lessons constitute more than business strategy—they're organizational wisdom earned through triumph and catastrophe. They explain how a Chicago insurance brokerage became a global professional services powerhouse. More importantly, they provide a roadmap for any firm seeking to build enduring value in professional services.

X. Bear vs. Bull: The Investment Case

The Bull Case: A Compounding Machine

The bulls see MMC as Warren Buffett would: a wide-moat business with predictable cash flows, rational management, and decades of growth ahead. Start with the business model—professional services with 85%+ client retention, essentially creating recurring revenue without the capital requirements of subscription software. The company has grown revenue every year since 2009, through pandemic, financial crisis, and geopolitical chaos.

The secular tailwinds are undeniable. Risk is becoming more complex—cyber threats, climate change, supply chain vulnerabilities, regulatory expansion. Companies need sophisticated advisors to navigate this complexity. MMC sits at the intersection of every major business risk. As risk grows, so does MMC.

The consolidation opportunity remains massive. The insurance brokerage industry remains fragmented—the top three players control less than 50% of the market. Thousands of small brokers lack scale for technology investment and global reach. MMC can acquire these at 10-12x EBITDA, integrate them at minimal cost, and achieve 20%+ returns. With $3 billion in annual free cash flow, they can fund this consolidation indefinitely.

Margin expansion appears sustainable. Seventeen consecutive years isn't luck—it's operational excellence. Technology investments are reducing cost-to-serve. Offshore centers handle routine work at lower cost. Higher-margin consulting grows faster than lower-margin brokerage. The math suggests another decade of 50-100 basis points annual margin expansion.

The valuation remains reasonable. At 25x forward earnings, MMC trades at a premium to the S&P 500 but a discount to high-quality compounders like Automatic Data Processing or Accenture. For a business growing revenue high-single digits with expanding margins and massive free cash flow, that's attractive.

The capital allocation is shareholder-friendly. Management targets 10%+ annual TSR through a combination of organic growth, margin expansion, and capital deployment. They've delivered on this promise for a decade. With $24 billion in revenue growing 7% annually and margins expanding, the math to 10%+ returns is straightforward.

Climate change represents an opportunity, not a threat. As physical risks increase, insurance becomes more valuable. As companies seek to reduce emissions, they need consulting help. As regulations proliferate, compliance complexity grows. MMC wins regardless of how climate change unfolds.

The competitive position is strengthening. Scale advantages in technology, data, and talent are growing. Smaller competitors can't match MMC's investment capacity. Larger competitors lack MMC's specialization. The company occupies a sweet spot—large enough for scale, focused enough for expertise.

The Bear Case: Structural Headwinds

The bears see multiple threats to MMC's business model. Start with technology disruption. InsurTech companies are attacking the insurance value chain with digital distribution, AI underwriting, and automated claims. If technology commoditizes insurance distribution, broker margins will compress dramatically.

Conflicts of interest remain problematic. Despite reforms, MMC still faces inherent conflicts—advising both insurance buyers and sellers, consulting for competing companies, designing compensation plans while managing investments. Another Spitzer-style investigation could devastate the stock, regardless of actual wrongdoing.

The economic sensitivity is concerning. While MMC survived 2008-2009, revenue growth slowed dramatically and margins compressed. In a severe recession, companies cut consulting spending and reduce insurance coverage. MMC's operating leverage works both ways—margins expand in good times but compress rapidly in downturns.

Regulatory risk is mounting globally. The EU is investigating insurance broker compensation. The DOJ periodically examines industry consolidation. State insurance regulators question broker practices. One adverse regulatory change could eliminate billions in revenue, as contingent commissions did in 2004.

Cyber risk is existential. MMC holds sensitive data on thousands of corporations and millions of individuals. A major breach could trigger lawsuits, regulatory penalties, and client defections. The reputational damage could take years to repair. For a company built on trust, cyber risk is particularly acute.

Competition is intensifying. Accenture is moving into insurance consulting. Private equity is rolling up insurance brokers. Technology companies are entering risk management. Big Four accounting firms are expanding advisory services. MMC's competitive moat may be narrower than it appears.

Valuation is stretched. At 25x earnings, MMC is pricing in perfect execution. Any disappointment—slower growth, margin pressure, acquisition misstep—could trigger multiple compression. The stock has tripled in five years; future returns will likely be more modest.

The transformation to consulting is risky. Oliver Wyman competes with McKinsey and BCG for talent and clients. Winning requires paying top dollar for talent and investing heavily in thought leadership. Margins are high but volatile. Building a world-class consulting firm is expensive and uncertain.

ESG pressures are growing. MMC insures fossil fuel companies, advises on executive compensation, and facilitates financial engineering. Activist investors increasingly question these activities. Pressure to divest certain clients or services could impact growth and profitability.

The Verdict: Quality at a Reasonable Price

On balance, the bull case appears stronger. MMC isn't a high-growth technology disruptor—it's a steady compounder in an essential industry. The business model has survived 150 years of disruption. The competitive position is strengthening. The management team has executed consistently.

The key insight is that professional services is fundamentally about trust and expertise, not technology or price. Clients choosing advisors for bet-the-company decisions prioritize reputation and capability over cost. MMC has built both over decades. That's not easily replicated or disrupted.

For long-term investors, MMC offers an attractive proposition: GDP+ organic growth, expanding margins, disciplined capital allocation, and exposure to secular trends around risk complexity. It won't double overnight, but it should compound wealth steadily over decades.

The bears raise valid concerns, particularly around technology disruption and regulatory risk. But MMC has navigated similar challenges before—from the Great Depression to the Spitzer investigation. Each crisis made the company stronger, not weaker. That resilience, combined with current competitive advantages, suggests MMC can navigate future challenges successfully.

XI. Epilogue: The Future of Risk & Advisory

Standing in Marsh McLennan's New York headquarters, 1166 Avenue of the Americas, you can't help but think about the ghosts. Not just the 358 colleagues lost on 9/11, but the generations of insurance brokers and consultants who built this institution. Henry Marsh, who saw opportunity in Chicago's ashes. Donald McLennan, who mastered railroad risk. The thousands who transformed a regional brokerage into a global powerhouse.

The view from the 44th floor spans Manhattan—the financial capital that MMC helps protect and advise. But the real vista is global and temporal. MMC operates in 130 countries, serving organizations that collectively employ hundreds of millions and generate trillions in revenue. The firm's recommendations shape how corporations manage risk, governments regulate markets, and individuals plan retirement.

This influence brings responsibility. When MMC advises on cyber insurance, it shapes how companies protect data. When Mercer designs pension plans, it affects millions of retirements. When Oliver Wyman counsels banks, it influences financial stability. The firm's 90,000 professionals aren't just selling services—they're architecting the risk infrastructure of global capitalism.

The future will test this architecture. Artificial intelligence promises to automate much of professional services. Climate change will create risks that don't fit traditional insurance models. Cyber threats will evolve faster than defenses. Geopolitical fragmentation will complicate global operations. The next decade will bring challenges as profound as any in MMC's history.

Yet MMC's history suggests it will adapt and thrive. The firm that started insuring against fire now advises on artificial intelligence risk. The company that pioneered self-insurance for U.S. Steel now helps tech giants navigate data privacy. Each transformation has expanded MMC's relevance rather than diminishing it.

The key insight is that risk itself is evolving. Traditional risks—fire, liability, mortality—remain but are increasingly understood and managed. Emerging risks—cyber, climate, reputation—are complex, interconnected, and rapidly evolving. These risks require not just insurance but integrated solutions combining risk transfer, mitigation, and strategic adaptation.

This evolution favors MMC. Commoditized risks can be insured through technology platforms. Complex risks require human expertise, judgment, and creativity. As risk becomes more sophisticated, the value of sophisticated risk advisors increases. MMC isn't competing with InsurTech startups—it's solving problems those startups can't even comprehend.

The consulting evolution is equally important. As business strategy and risk management converge, the distinction between Oliver Wyman's strategy work and Marsh's risk advisory blurs. A bank's digital transformation is simultaneously a strategic initiative and a risk management challenge. MMC's ability to address both dimensions provides unique value.

The broader lesson transcends MMC. In an economy increasingly dominated by intangible assets—data, intellectual property, reputation—traditional financial metrics fail to capture value and risk. Professional services firms that can navigate this intangible economy become essential infrastructure, as critical as banks or utilities.

This explains why boring businesses often make the best investments. While markets obsess over the latest disruption, companies like MMC compound wealth quietly and consistently. They lack the excitement of technology startups but offer something more valuable: predictability in an unpredictable world.

The MMC story also illustrates American capitalism's resilience and evolution. A firm founded when insurance meant protecting physical assets now helps companies navigate digital transformation. A company that survived the Great Depression now advises on pandemic recovery. Each crisis catalyzes evolution rather than extinction.

But perhaps the most important lesson is about institutional memory and wisdom. MMC's greatest asset isn't its client list or brand—it's the accumulated knowledge of 150 years of risk management. This institutional wisdom—encoded in processes, relationships, and culture—provides perspective that no algorithm can replicate.

As one senior partner observed: "We've seen every kind of crisis—wars, depressions, pandemics, technological disruptions. The specifics change but the patterns repeat. Our value isn't predicting the future—it's recognizing patterns from the past and helping clients prepare for what we can't predict."

This perspective—literally, the ability to see from multiple vantage points—defines MMC's value proposition. In a world of increasing specialization, someone needs to see the whole picture. In a time of rapid change, someone needs to provide historical context. In an era of information overload, someone needs to distinguish signal from noise.

That's ultimately what MMC sells: perspective. The confidence that comes from knowing risks are understood and managed. The clarity that comes from expert advice. The resilience that comes from preparation. In an uncertain world, these intangibles become invaluable.

The next 150 years will bring challenges we can't imagine—technologies we haven't invented, risks we haven't contemplated, opportunities we haven't envisioned. But if history is any guide, MMC will evolve to meet them. The firm that started by spreading fire risk across multiple insurers will find ways to spread whatever risks emerge.

For investors, MMC represents a bet on the permanence of uncertainty itself. As long as the future remains unpredictable, as long as risks require management, as long as complexity demands expertise, firms like MMC will remain essential. It's not a bet on any particular trend or technology—it's a bet on the human need for advice, assurance, and perspective.

The Chicago fire that created MMC's opportunity burned for three days. The company built from those ashes has endured for 150 years and counting. In the financial markets' endless search for the next big thing, sometimes the best investment is the last big thing that never stopped growing.

XII. Recent News

In January 2025, Marsh McLennan reported strong fourth quarter and full-year 2024 results, with John Doyle, President and CEO, stating: "Our fourth quarter results capped a terrific year for Marsh McLennan. We delivered on our strategic objectives, generated excellent financial performance, and had the largest year of acquisitions in our history."

The company completed its acquisition of McGriff Insurance Services on November 15, 2024, with McGriff's more than 3,500 colleagues joining Marsh McLennan Agency. Under the terms of the transaction, Marsh McLennan paid $7.75 billion in cash consideration, funded by a combination of cash and proceeds from debt financing. In conjunction with the transaction, Marsh McLennan assumed a deferred tax asset valued at approximately $500 million.

Leadership transitions have shaped the modern era, with John Q. Doyle, 58, named President and Chief Executive Officer effective January 1, 2023, succeeding Daniel S. Glaser, 62, who retired from Marsh McLennan at year end following a decade leading the Company through a period of extraordinary growth and change. Mr. Doyle had served as Group President and Chief Operating Officer of Marsh McLennan since January 2022, and prior to that was President and CEO of Marsh, the Company's risk advisory and insurance solutions business, from 2017 to 2021.

XIII. Links & Resources

Company Resources: - Marsh McLennan Investor Relations: marshmclennan.com/investors - Annual Reports and SEC Filings: SEC EDGAR Database - Quarterly Earnings Calls: marshmclennan.com/investors/events

Historical Resources: - "Marsh & McLennan Companies: 100 Years of Client Service" (Company History) - Harvard Business School Case Studies on MMC - Insurance Information Institute Archives

Industry Analysis: - Business Insurance Magazine's Annual Broker Rankings - A.M. Best Insurance Industry Reports - McKinsey Global Insurance Reports

Books on Insurance and Risk Management: - "Against the Gods: The Remarkable Story of Risk" by Peter L. Bernstein - "The Essentials of Risk Management" by Michel Crouhy, Dan Galai, and Robert Mark - "Risk Management and Insurance" by Scott Harrington and Gregory Niehaus

Regulatory and Legal Documents: - 2004 Spitzer Investigation Settlement Documents - September 11th Victim Compensation Fund Records - SEC Filings and Proxy Statements

Professional Services Industry Research: - Consulting Magazine Industry Reports - Kennedy Consulting Research & Advisory - Source Global Research on Professional Services

This analysis represents an independent examination of Marsh McLennan's history, strategy, and prospects. It is intended for educational purposes and should not be construed as investment advice. The author has no position in MMC securities and no relationship with the company beyond publicly available research.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube