Martin Marietta Materials: Building America's Infrastructure Foundation

I. Introduction & Episode Roadmap

Picture this: A massive explosion rips through a North Carolina quarry at dawn, sending 200,000 tons of granite tumbling down the rock face. Within hours, that stone will be crushed, sorted, and loaded onto trains bound for highway projects across the Southeast. This isn't just any quarry—it's one of 400 operations that form the backbone of Martin Marietta Materials, a $30 billion market cap company that literally builds the ground beneath America's feet.

Here's the central question that should fascinate any student of business: How did a Depression-era family quarry in Raleigh evolve into the S&P 500's premier aggregates powerhouse, generating $6.536 billion in revenue and commanding pricing power that would make a luxury brand jealous?

The answer involves aerospace mergers gone sideways, hostile takeover defenses straight out of a thriller, and a CEO who transformed rocks—yes, rocks—into one of the highest-margin businesses in the industrial sector. This is a story about finding monopoly-like economics in the most mundane of products: crushed stone.

What makes Martin Marietta Materials particularly compelling is how it defied the conventional narrative of American manufacturing decline. While others chased technology or outsourced production, MLM doubled down on the most local, most physical, least exportable business imaginable. They bet that America would always need roads, bridges, and buildings—and that the economics of hauling rocks would create natural monopolies in every market they entered.

Today, as data centers proliferate and infrastructure spending reaches historic highs, that bet looks prescient. But the journey from Superior Stone to today's aggregates empire was anything but smooth. It's a tale of survival through conglomerate chaos, strategic focus through industry consolidation, and ultimately, the creation of one of the most defensible business models in American industry.

II. Origins & The Ragland Brothers Era (1939–1961)

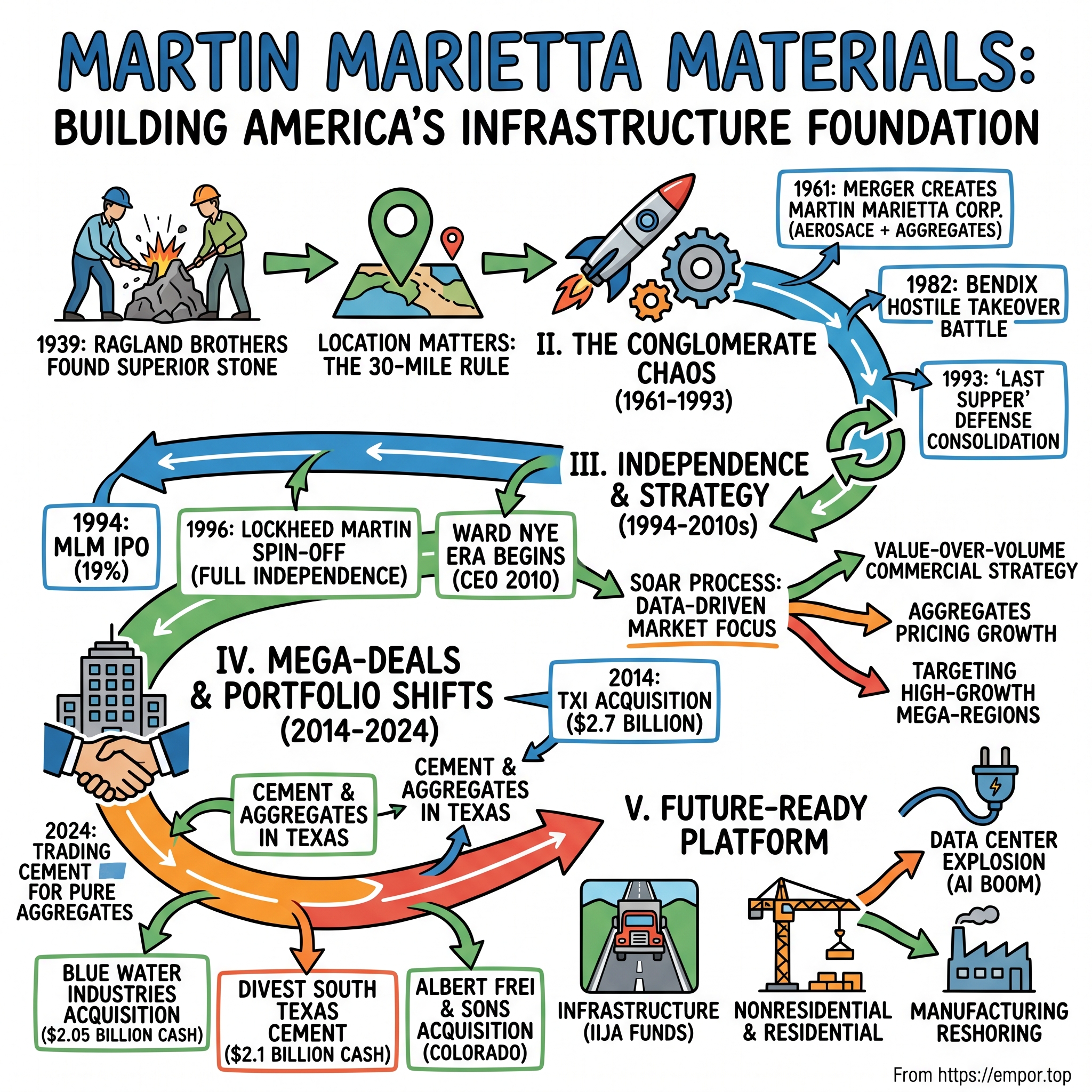

The year was 1939. Hitler invaded Poland, Gone with the Wind premiered, and in Raleigh, North Carolina, two brothers saw opportunity in rubble. William Trent Ragland and Edmond Ragland founded Superior Stone Company with a simple observation: the South was building, and somebody had to supply the rocks.

The Raglands weren't mining magnates or industrial titans. They were local businessmen who understood a fundamental truth that would define the aggregates industry for the next century: in the rock business, location beats everything. You can have the finest granite in the world, but if it's 50 miles from the construction site, you've already lost to the guy with mediocre limestone next door. Transportation costs for aggregates typically equal or exceed the cost of the material itself once you get beyond 30 miles.

Superior Stone started with a single quarry, selling crushed stone for road base and concrete production. The timing was fortuitous—America was emerging from the Depression, and Franklin Roosevelt's infrastructure programs were pumping federal money into roads and bridges. But what really turbocharged the business was World War II and its aftermath. Military bases sprouted across the South, highways connected them, and the suburban building boom created insatiable demand for aggregates.

By the 1950s, the Raglands had built Superior Stone into a regional powerhouse, but they faced a classic mid-century dilemma: stay local and risk being acquired, or find a larger partner to fuel expansion. The aggregates industry was fragmenting into thousands of small operators, but the Raglands sensed consolidation was coming. They needed scale, capital, and most importantly, protection from larger predators. In 1959, that partner materialized in the form of American-Marietta Corporation, a Chicago-based conglomerate that had built itself through acquisitions in paints, chemicals, and construction materials. Superior Stone, led by William Trent Ragland as president, merged with American-Marietta in 1959, bringing the aggregates business into a larger industrial family. American-Marietta specialized in construction materials and industrial chemicals such as synthetic resins, adhesives, paints, and varnishes, making Superior Stone a natural fit for their portfolio.

The merger made strategic sense for both parties. By 1960, American-Marietta's total income was $372 million and had reached #137 on the Fortune 500, providing Superior Stone with the financial backing to expand beyond North Carolina. For American-Marietta, aggregates offered stable, predictable cash flows to balance their more cyclical chemical businesses.

But the real transformation came just two years later. In 1961, American-Marietta merged with the Glenn L. Martin Company, creating Martin Marietta Corporation. Suddenly, the Ragland brothers' rock quarries were sharing a corporate umbrella with aerospace engineers building Titan missiles and space vehicles. It was the height of the conglomerate era, when Wall Street believed that good management could run any business, from moon rockets to limestone crushing.

For William Trent Ragland, who continued running the aggregates division, it must have been surreal. One day you're negotiating gravel contracts with county road departments; the next, you're in board meetings discussing NASA contracts and Cold War defense systems. Yet this unlikely marriage would prove more durable than anyone imagined. The aggregates business, unglamorous as it was, generated the steady cash that helped fund Martin Marietta's aerospace ambitions. And critically, the Raglands maintained operational autonomy—they knew rocks, not rockets, and corporate let them run their business.

III. The Conglomerate Years & Near-Death Experience (1961–1993)

Life inside Martin Marietta Corporation during the 1960s and 70s resembled a business school case study in conglomerate management. Board meetings featured presentations on Viking Mars landers followed by discussions of quarry expansion in Georgia. The company built external fuel tanks for NASA's space shuttles while simultaneously crushing granite for Interstate highways. It was American industrial capitalism at its most ambitious—and most unwieldy.

In 1971, Martin Marietta acquired Harvey Aluminum, a company which made aluminum oxide, aluminum ingot and aircraft grade aluminum sheet. William Trent Ragland continued as CEO until 1977, after retiring and becoming Emeritus Senior Vice President. The aluminum acquisition represented classic conglomerate thinking: vertical integration across unrelated industries would somehow create synergies. In reality, managing aerospace, aggregates, and aluminum production under one roof created more complexity than value.

But nothing prepared Martin Marietta for the corporate drama that erupted in 1982. Bill Agee, CEO of Bendix Corporation, launched a hostile takeover bid for Martin Marietta, armed with a $1.5 billion war chest and dreams of creating an industrial empire. What followed was one of the most bizarre episodes in American corporate history.

Bendix bought the majority of Martin Marietta shares and in effect owned the company. However, Martin Marietta's management used the short time separating ownership and control to sell non-core businesses and launch its own hostile takeover of Bendix (known as the Pac-Man defense). Thomas G. Pownall, CEO of Martin Marietta, was successful and the end of this extraordinarily bitter battle saw Martin Marietta survive; Bendix was bought by Allied Corporation.

The Pac-Man defense—where the target company turns around and tries to acquire its attacker—had never been successfully executed at this scale. Martin Marietta's management, led by CEO Tom Pownall, moved with lightning speed. They secured emergency financing, launched their own tender offer for Bendix shares, and created a Mexican standoff where each company theoretically owned the other. The financial press had a field day; investment bankers made fortunes; and ultimately, Allied Corporation swooped in to buy Bendix, leaving Martin Marietta battered but independent.

The battle's aftermath forced serious soul-searching. Martin Marietta had survived, but at tremendous cost—both financial and organizational. The company carried significant debt from its defensive maneuvers, and management realized that the conglomerate model made them vulnerable to raiders who could argue that the parts were worth more than the whole. Then came the event that would fundamentally reshape Martin Marietta: The "Last Supper" was a July 21, 1993 dinner at The Pentagon hosted by then-U.S. Secretary of Defense Les Aspin and Deputy Secretary of Defense William Perry to discuss defense industry consolidation in the United States. The name was bestowed by Norm Augustine, then the head of Martin Marietta and an attendee at the dinner. The recent end of the Cold War had raised calls for a peace dividend and Perry warned the defense industry that it would need to consolidate to survive coming budget cuts.

Norman Augustine, Martin Marietta's CEO, sat next to Les Aspin that night. "We showed up for dinner at the Pentagon one night dutifully, none of us knowing why we were there," Augustine recalls. "I happened to be seated next Les Aspin, and I remember I said, 'Les, this is awfully nice of you to invite us all to dinner, we're all pleased to have a free meal, but why are we here?' And he said, 'Well, in about 15 minutes, you're going to find out. You probably aren't going to like it.'"What Perry and Aspin delivered was brutal clarity: defense spending would continue falling, and the Pentagon could only afford to sustain a fraction of its contractor base. Perry warned the defense industry that it would need to consolidate to survive coming budget cuts. The number of prime defense contractors in the U.S. would decline from 51 to five in the following years, consolidating the industry into only a few major companies.

For Martin Marietta, the Last Supper triggered urgent strategic decisions. The company had to choose: try to become one of the aerospace survivors or exit defense entirely. Augustine chose the survivor path, but the materials division—that steady, unglamorous cash generator—suddenly looked like either ballast to be jettisoned or an insurance policy worth preserving.

The solution was elegant: partial independence. Martin Marietta completed its initial public offering of 19% of the common stock of Martin Marietta Materials, which is listed on the New York Stock Exchange as MLM in 1994. An initial public offering of a portion of the common stock of the Company (the Common Stock) was completed in February 1994 whereby 8,797,500 shares of Common Stock (representing approximately 19% of the shares outstanding) were sold at an initial public offering price of $23 per share.

This IPO served multiple purposes. It established a public market value for the materials business, provided capital to pay down debt from the Bendix battle, and most importantly, created optionality. If the aerospace consolidation went well, Martin Marietta could keep control of its cash-generating aggregates subsidiary. If things went poorly, the materials business could be fully spun off to survive independently.

The aerospace consolidation moved quickly. Martin Marietta merged with Lockheed Corporation to form Lockheed Martin in 1995, creating what would become the world's largest defense contractor. For the materials business, this marriage meant divorce. Martin Marietta Materials was spun off as an independent company, with Lockheed Martin retaining various aerospace, defense, and other manufacturing lines of business in 1996.

IV. The Ward Nye Era Begins: Vision & Strategy (1990s–2010s)

The newly independent Martin Marietta Materials needed leadership that understood both the aggregates business and the art of the possible. They found it in Steve Zelnak, who had joined the business in 1981 and became CEO in 1982, leading the company through its IPO and spinoff. Martin Marietta, which then had revenue of about $660 million, was led by Steve Zelnak, who had joined the business in 1981 and became CEO a year later. During his 27 years as the company's top boss, he oversaw more than 70 acquisitions.

But the real transformation began when Ward Nye joined the company. Nye's path to Martin Marietta was unconventional—a Duke undergraduate, Wake Forest law degree, and 13 years at Hanson, a London-based conglomerate where he ran mergers and acquisitions, then headed divisions in Raleigh and Dallas. In 2006, he got a call from Martin Marietta, which was looking for Zelnak's successor. He jumped at the chance, serving as president from 2006-09, then became CEO a year later when revenue was $1.8 billion and the market cap was $4.2 billion.

Nye brought a lawyer's precision and a dealmaker's instinct to an industry that had operated on handshakes and local relationships for decades. His first major initiative was developing what became known as SOAR—Strategic Operating Analysis and Review. It was during his initial years at Martin Marietta when it developed the SOAR process. Nye says the company spent 30,000 internal man-hours examining each of its markets, including 11 mega-regions that make up 70% of U.S. population growth. Those included markets, such as the Piedmont and the Gulf Coast, where Martin Marietta had a strong presence and others, such as Florida, where it had no operations.

The SOAR framework wasn't just another corporate strategy document. It was a data-driven blueprint for dominating the aggregates industry by following demographics, infrastructure spending, and most importantly, pricing power. Nye understood that aggregates wasn't really a commodity business—it was hundreds of local monopoly businesses, each protected by the simple economics of hauling rocks. Nye's philosophy was crystallized in what became Martin Marietta's mantra: value-over-volume commercial strategy. This wasn't just corporate speak—it was a fundamental rethinking of how to run a commodity business. We achieved a quarterly record for aggregates pricing growth and a 134 percent increase in aggregates gross profit per ton, highlighting our team's steadfast execution of our value-over-volume commercial strategy.

The strategy was counterintuitive in an industry where market share had always been king. Rather than chase every ton of volume, Martin Marietta would be selective. They would walk away from low-margin business. They would raise prices even if it meant shipping less product. The bet was that in local markets with high barriers to entry, customers had few alternatives, especially for large infrastructure projects where rock quality and reliable supply trumped small price differences.

Martin Marietta has the ability and capacity to supply these needed products and, supported by our locally-led pricing strategy, will do so in a manner that emphasizes value over volume. This locally-led approach was crucial—pricing decisions weren't made in Raleigh boardrooms but by regional managers who understood their specific market dynamics, competition, and customer relationships.

The results spoke for themselves. While competitors struggled with razor-thin margins during construction downturns, Martin Marietta maintained and even expanded profitability. Our third-quarter results highlight our commitment to execution of our value-over-volume strategy as double-digit pricing growth drove record profitability despite relatively flat organic aggregates shipments.

Nye also recognized that geography was destiny in aggregates. The SOAR strategy identified high-growth regions—particularly the Sunbelt states experiencing population inflows—and systematically built positions through acquisitions and organic expansion. Texas, Florida, North Carolina, Colorado—these weren't random dots on a map but carefully chosen markets with favorable demographics, strong Department of Transportation budgets, and limited competition.

The acquisition strategy under Nye was surgical. "One of the things that we do extraordinarily well is plan and execute, particularly around mergers and acquisitions," says Nye. "If you go back over the 30 years we've been a public company, literally well over 100 transactions, it would be hard to find some that didn't go as we hoped." Each deal had to meet strict criteria: strategic location, quality reserves, integration potential, and most importantly, the ability to extract pricing synergies post-acquisition.

V. The TXI Mega-Deal: Transformative Acquisition (2014)

The morning of January 28, 2014, changed everything. Martin Marietta Materials and Texas Industries announced that the Boards of Directors of both companies have unanimously approved a definitive merger agreement under which Martin Marietta will acquire all of the outstanding shares of Texas Industries common stock in a tax-free, stock-for-stock transaction valued at $2.7 billion.

For Ward Nye and his team, TXI represented the ultimate strategic prize. TXI is the largest cement maker in Texas. More importantly, it controlled prime aggregates reserves in the Dallas-Fort Worth metroplex, one of America's fastest-growing regions. "The combined company will have an unmatched asset base in key markets in Texas, including Dallas-Fort Worth," Nye said.

The deal structure was elegant: Under the terms of the merger agreement, Texas Industries shareholders will receive 0.700 Martin Marietta shares for each share of Texas Industries common stock they own at closing. Upon closing of the transaction, Martin Marietta shareholders are expected to own approximately 69 percent, and Texas Industries shareholders are expected to own approximately 31 percent, of the combined company.

But the path to closing wasn't smooth. The Department of Justice's antitrust review required surgical divestitures. Under the terms of the agreement with the DOJ, Martin Marietta will divest its North Troy aggregate quarry in Mill Creek, Oklahoma and its two rail yards located in Frisco, Texas. These were painful concessions but necessary to preserve the deal's strategic value.

The transaction was overwhelmingly approved by shareholders from both companies on June 30, 2014, and closed on July 2, 2014. Ward Nye, Martin Marietta's Chairman, President and Chief Executive Officer, said, "We are excited to move forward as one company that is even better positioned to deliver increased value to shareholders, customers and employees."

The financial logic was compelling. Martin Marietta continues to expect that the combination will generate approximately $70 million of annual pre-tax synergies by 2017. These weren't just theoretical paper synergies—they came from concrete operational improvements: optimizing quarry networks, consolidating back-office functions, leveraging pricing power in newly concentrated markets, and most importantly, controlling the full value chain from quarry to construction site in key Texas markets.

The TXI acquisition transformed Martin Marietta from a regional player into a national powerhouse. Martin Marietta is well-positioned for long-term growth, with a network of more than 400 facilities spanning 36 states, Canada, and the Caribbean Islands. The deal brought critical mass in Texas, the nation's largest construction materials market, and provided vertical integration opportunities that would prove invaluable in tight markets.

But perhaps most importantly, the TXI deal validated Nye's consolidation thesis. In a fragmented industry, scale created advantages beyond just cost synergies. It provided negotiating leverage with customers, the ability to optimize logistics networks, and the financial firepower for further acquisitions. The aggregates industry was consolidating, and Martin Marietta had just claimed a seat at the head table.

VI. Portfolio Optimization & The Blue Water Blockbuster (2020s)

A decade after the TXI acquisition, Ward Nye orchestrated his boldest strategic pivot yet. On February 12, 2024, Martin Marietta announced two transformative transactions that would occur nearly simultaneously: it entered into a definitive agreement to acquire 20 active aggregates operations in Alabama, South Carolina, South Florida, Tennessee, and Virginia from affiliates of Blue Water Industries LLC (BWI Southeast) for $2.05 billion in cash. Additionally, on February 9, 2024, the Company completed its previously announced divesture of its South Texas cement and related concrete operations to CRH Americas Materials, Inc., a subsidiary of CRH plc, for $2.1 billion in cash.

This wasn't just a simple asset swap—it was a fundamental reimagining of Martin Marietta's business model. The company was essentially trading cement for pure aggregates, exchanging vertical integration for geographic expansion and margin improvement. Together, these portfolio optimizing transactions not only improve the Company's product mix, margin profile and durability through cycles, but also provide balance sheet flexibility for future acquisitive and organic growth.

The Blue Water acquisition brought crown jewel assets. The BWI Southeast acquisition naturally complements Martin Marietta's existing geographic footprint in the dynamic southeast region by allowing us to expand into new growth platforms in SOAR-specific target markets including Nashville and Miami. These weren't just any markets—Nashville and Miami represented two of the fastest-growing metropolitan areas in America, with massive infrastructure needs and limited local aggregates supply. The strategy wasn't complete without strengthening the Colorado position. On January 12, 2024, Martin Marietta completed the acquisition of Albert Frei & Sons, Inc. ("AFS"), a leading aggregates producer in Colorado. The transaction provides more than 60 years of high-quality, hard rock reserves to better serve new and existing customers. The acquisition, wholly consistent with our strategic plan, enhances our aggregates platform in the high-growth, Denver metropolitan area and strengthens our ability to deliver significant value for shareholders and customers.

The numbers told the story of transformation: Combined with the recent acquisition of Albert Frei & Sons, Inc. in Colorado, these two pure-play aggregates transactions provide approximately 1 billion tons of proven, high-quality reserves and are expected to generate more than $180 million of annualized EBITDA. This wasn't just growth—it was strategic repositioning at scale.

The financial engineering behind these deals was masterful. Martin Marietta essentially recycled capital from lower-margin, more cyclical cement operations into higher-margin, more stable aggregates businesses. The South Texas cement divestiture generated $2.1 billion in cash, which almost entirely funded the $2.05 billion Blue Water acquisition. The company maintained balance sheet strength while fundamentally improving its business mix.

Ward Nye explained the strategic rationale: This portfolio optimizing transaction improves the Company's product mix, margin profile and durability through economic cycles by adding another pure aggregates business to its already aggregates-led portfolio. In essence, Martin Marietta was doubling down on what it did best—pure aggregates—while exiting businesses that, while profitable, didn't offer the same margin expansion potential or cyclical resilience.

The market response validated the strategy. Investors understood that Martin Marietta was trading complexity for focus, vertical integration for margin expansion, and regional concentration for geographic diversification. The company had transformed from a construction materials conglomerate into a pure-play aggregates powerhouse, positioned in the fastest-growing markets with the highest barriers to entry.

VII. Business Model Deep Dive: The Aggregates Advantage

To understand why Ward Nye bet the company on rocks, you need to understand the beautiful economics of the aggregates business. At first glance, selling crushed stone seems like the definition of a commodity business—undifferentiated product, price-based competition, cyclical demand. But dig deeper, and you discover a business model Warren Buffett would love: local monopolies protected by physics and regulation.

The physics are simple but immutable. Aggregates are heavy and cheap, which means transportation costs quickly overwhelm product costs. Industry executives call it the "30-mile rule"—beyond 30 miles from the quarry, trucking costs typically equal or exceed the cost of the stone itself. This creates natural geographic monopolies. If you control the only quarry within 30 miles of a major construction project, you essentially have pricing power similar to a regulated utility.

But the real moat comes from permitting. Starting a new quarry isn't like opening a restaurant. Deal making is preferable to starting new quarries, a tough process entailing finding 500 acres near a metropolitan market where there's quality stone near the surface. Then the aggregates enterprise has to go through a lengthy rezoning and permitting process, along with gaining environment and water permits. Not many people want to live near a quarry, either. "That's not a matter of months, but a matter of years," says Nye.

The NIMBY (Not In My Backyard) phenomenon has essentially frozen new quarry development near major metropolitan areas. Existing quarries, especially those that predate suburban expansion, become increasingly valuable as cities grow around them. They're irreplaceable assets—you literally cannot create a competing quarry nearby because local communities won't permit it.

Martin Marietta has weaponized these dynamics through operational excellence. The company operates with a hub-and-spoke model where major quarries feed a network of distribution yards. Long-haul transportation capabilities, including rail and water networks, allow them to move aggregates economically over longer distances when local supply is constrained. This gives them flexibility to serve markets beyond the typical 30-mile radius while maintaining pricing discipline.

The demand drivers for aggregates are remarkably diverse and resilient. Unlike residential construction, which is highly cyclical, aggregates demand comes from multiple sources: highways and streets (the largest segment), commercial construction, residential, and increasingly, large industrial projects. The Infrastructure Investment and Jobs Act, passed in 2021, authorized $1.2 trillion in spending, much of it flowing directly into aggregates-intensive projects. But perhaps the most unexpected demand driver has emerged from the AI revolution. The global data center construction market size was estimated at USD 240.97 billion in 2024 and is projected to reach USD 456.50 billion by 2030, growing at a CAGR of 11.8% from 2025 to 2030. This explosion in data center construction represents a gold mine for aggregates producers. A single hyperscale data center can consume millions of tons of aggregates for foundations, access roads, and supporting infrastructure.

Data center construction starts have reached unprecedented levels in 2024. Through the first six months of 2024, there have been a total of 78 data center projects that have begun construction. These projects totaled over $9 billion and almost 12 million square feet. Each data center requires massive concrete foundations to support server racks and cooling systems, extensive road networks for construction and maintenance access, and often, entirely new power infrastructure—all aggregates-intensive applications.

Martin Marietta's management of weather and cyclical risks demonstrates operational sophistication. Rather than fighting nature, they've learned to work with it. The company maintains strategic inventory buffers, uses covered storage and all-weather production capabilities where feasible, and most importantly, has geographic diversification that allows strong markets to offset weather-impacted regions.

The ESG (Environmental, Social, and Governance) angle, often overlooked in extractive industries, has become a competitive advantage. Modern quarry operations include extensive reclamation plans that transform exhausted quarries into lakes, parks, or development sites. Martin Marietta has turned potential liabilities into community assets, building goodwill that facilitates future permitting and expansion.

The operational framework itself is a study in industrial efficiency. Modern quarries use GPS-guided drilling for optimal blast patterns, automated crushing and sorting systems that maximize yield, and sophisticated logistics software that optimizes truck routes and rail car utilization. This isn't your grandfather's rock quarry—it's a high-tech operation where every ton counts and every percentage point of efficiency drops directly to the bottom line.

VIII. Financial Performance & Value Creation

The numbers tell a story of relentless margin expansion and value creation. Consequently, we are confident in achieving the midpoint of our 2025 full year Adjusted EBITDA guidance of $2.25 billion, a 9% improvement compared to the prior year. This isn't just growth—it's profitable growth at scale.

The 2024 financial performance, despite weather challenges, demonstrates the resilience of the business model. In 2024, we faced several challenging dynamics beyond our control, including inclement weather, softening construction demand in both nonresidential and residential sectors, and tighter-than-expected monetary policy. Despite these headwinds, we remained steadfast in executing our strategic priorities and concluded the year with a return to earnings growth and margin expansion, resulting in record fourth quarter profits.

What's remarkable is the unit economics improvement. The team's disciplined execution of our proven value-over-volume commercial strategy drove an organic improvement of 33.0 percent and 46.4 percent in full-year Adjusted EBITDA and aggregates unit profitability, respectively. This wasn't achieved through volume growth—it was pure pricing and operational excellence.

The aggregates pricing story deserves special attention. In 2024, aggregates revenues reached $4.5 billion with gross profit of $1.4 billion, translating to $7.58 gross profit per ton. Aggregates gross profit per ton increased over 16 percent to a new first-quarter record, reflecting continued pricing momentum and effective cost management. These margins are extraordinary for what's ostensibly a commodity business.

Cash flow generation has been equally impressive. In the third quarter, our team achieved record quarterly aggregates gross profit per ton, record third-quarter cash flows from operations. The ability to convert earnings into cash, even during challenging periods, demonstrates the quality of the earnings and the efficiency of working capital management.

Capital allocation under Nye has been textbook. The company maintains a disciplined hierarchy: first, invest in high-return organic growth projects; second, pursue accretive acquisitions that meet strict strategic and financial criteria; third, maintain a progressive dividend policy; and finally, opportunistic share repurchases. The balance sheet remains fortress-like with Net Debt-to-EBITDA of 2.3x, providing ample firepower for future opportunities.

The Company delivered our safest year on record, achieved nearly double-digit growth in unit margins, expanded Adjusted EBITDA margins and reshaped our portfolio. This was accomplished through approximately $6 billion in aggregates-led acquisitions and non-core asset divestitures. This portfolio transformation wasn't just financial engineering—it fundamentally improved the quality and durability of the business.

The stock market has recognized this value creation. While specific long-term returns aren't disclosed in recent reports, the company's inclusion in the S&P 500 and consistent outperformance of sector peers speaks to institutional confidence in the model. The combination of GDP-plus growth, margin expansion, and capital discipline has created a compounding machine that benefits long-term shareholders.

IX. Playbook: Lessons in Industrial Consolidation

Martin Marietta's consolidation playbook reads like a masterclass in industrial strategy. The company has completed over 100 acquisitions in 30 years, with remarkably few failures. The secret isn't complex financial engineering or aggressive cost-cutting—it's disciplined execution of a repeatable process.

The acquisition criteria are non-negotiable. First, strategic fit: does the target enhance market position in existing geographies or provide entry into SOAR-designated growth markets? Second, reserve quality: are the reserves proven, accessible, and sufficient for decades of production? Third, cultural alignment: will the target's team embrace Martin Marietta's safety-first, operational excellence culture? Fourth, synergy potential: can the combined entity achieve pricing power, cost savings, or operational improvements impossible independently?

Integration excellence separates Martin Marietta from failed consolidators. "One of the things that we do extraordinarily well is plan and execute, particularly around mergers and acquisitions," says Nye. The company maintains a dedicated integration team that swings into action immediately upon deal announcement. Day one priorities are clear: safety protocols, financial controls, and customer communication. The first 100 days focus on quick wins—eliminating redundancies, optimizing logistics networks, and implementing Martin Marietta's pricing discipline.

The pricing discipline itself deserves examination. In commodity industries, the temptation is always to chase volume through price competition. Martin Marietta does the opposite. New acquisitions often see immediate price increases—not because Martin Marietta is gouging customers, but because previous owners undervalued their product. The company teaches acquired managers to think like local monopolists (which they often are) rather than commodity producers.

Geographic strategy follows demographic destiny. The SOAR framework isn't just about identifying growing markets—it's about understanding why they're growing and whether that growth is sustainable. Texas isn't targeted simply because it's large; it's targeted because of energy sector strength, favorable business climate, and continued population inflows. Florida matters not just for retirees but for its role as a gateway to Latin America and Caribbean trade.

Managing cyclicality requires philosophical discipline. Martin Marietta doesn't try to time cycles—it builds a business that can thrive throughout cycles. This means maintaining a variable cost structure where possible, diversifying across end markets (infrastructure, residential, commercial, industrial), and most importantly, using downturns to consolidate. The best acquisitions often come during industry distress when weak operators need exits and valuations are reasonable.

The ESG and community relations strategy is surprisingly sophisticated for an extractive industry. Martin Marietta understands that quarries are multi-decade assets requiring community support. They invest heavily in noise reduction, dust control, and visual screening. Exhausted quarries are reclaimed as community assets. The company maintains local hiring preferences and supports community organizations. This isn't mere corporate citizenship—it's protecting the social license to operate.

Leadership continuity provides strategic consistency. The CEO succession from Zelnak to Nye was planned years in advance. Nye had already been president for three years before becoming CEO, ensuring seamless transition. This continuity extends throughout the organization—regional managers often spend decades with the company, building deep market knowledge and customer relationships.

The operational framework emphasizes continuous improvement over transformation. Martin Marietta doesn't chase the latest management fads. Instead, they focus on incremental improvements—reducing fuel consumption by 2%, improving crusher efficiency by 3%, optimizing blast patterns to increase yield by 1%. These small improvements compound over time into substantial competitive advantages.

Technology adoption is pragmatic rather than cutting-edge. The company invests in proven technologies that deliver clear ROI: GPS-guided equipment, automated crushing systems, logistics optimization software. They let others be guinea pigs for unproven innovations. This conservative approach to technology ensures that investments enhance rather than disrupt operations.

The cultural elements are perhaps most important. Martin Marietta has cultivated a culture that celebrates operational excellence, safety achievement, and long-term thinking. Quarry managers are treated as business owners, with significant autonomy over pricing and operations within corporate guidelines. This entrepreneurial culture within a large corporation maintains agility despite scale.

X. Bear vs. Bull Case & Future Outlook

Bear Case:

The pessimist's view of Martin Marietta starts with interest rate sensitivity. Construction is inherently rate-sensitive—higher rates increase project financing costs, reduce housing affordability, and can delay or cancel marginal projects. With the Federal Reserve maintaining restrictive policy longer than expected, private construction demand could remain suppressed for years, not quarters.

Weather disruptions are becoming more frequent and severe. Well-chronicled weather-related events had major impacts on our third-quarter business results. Significant July precipitation together with Tropical Storm Debby in North Carolina, Hurricane Beryl in Texas and Hurricane Helene across much of our Southeast footprint all occurred during the quarter. Climate change could make these disruptions the new normal rather than exceptions, permanently impairing operational efficiency.

Infrastructure spending uncertainty looms large. While the Infrastructure Investment and Jobs Act authorized significant spending, actual appropriations require annual Congressional approval. A change in political control could reduce or redirect infrastructure spending. Moreover, with only about one-third of the Infrastructure Investment and Jobs Act (IIJA) funds reimbursed to states through the end of February 2025, the pace of deployment has been slower than expected, potentially pushing benefits further into the future.

Competition from recycled materials poses a long-term threat. As recycling technology improves and environmental regulations tighten, recycled concrete and asphalt could capture increasing market share. While Martin Marietta participates in recycling, their core business model depends on virgin aggregate extraction.

The data center boom could prove temporary. The AI infrastructure buildout driving current demand might be a one-time investment cycle rather than sustained growth. Once hyperscalers build out their infrastructure, demand could collapse, leaving Martin Marietta with excess capacity in markets chosen specifically for data center exposure.

Valuation poses risks at current levels. Trading at premium multiples to historical averages, Martin Marietta has little room for disappointment. Any earnings miss or guidance reduction could trigger significant multiple compression, especially if investors question the sustainability of pricing power.

Bull Case:

The optimist's view starts with housing fundamentals. America remains structurally underbuilt by millions of units. Household formation continues exceeding new construction. Eventually, demographic reality must prevail—young adults will form households, requiring massive catch-up construction. Martin Marietta is perfectly positioned to supply this eventual boom.

Infrastructure spending is just beginning. Infrastructure demand remains a continuing bright spot amidst an uncertain macroeconomic backdrop. Construction activity in this countercyclical sector is expected to grow in 2025 as work advances on projects supported by federal and state investments. Importantly, with only about one-third of the Infrastructure Investment and Jobs Act (IIJA) funds reimbursed to states through the end of February 2025, suggesting years of infrastructure-driven demand ahead.

The data center and reshoring megatrends have years to run. The global data center construction market size was estimated at USD 240.97 billion in 2024 and is projected to reach USD 456.50 billion by 2030, growing at a CAGR of 11.8% from 2025 to 2030. Additionally, reshoring of manufacturing requires massive industrial construction, all aggregates-intensive.

Consolidation opportunities remain abundant. The aggregates industry remains fragmented with thousands of small operators. Martin Marietta has the balance sheet strength and integration expertise to continue rolling up the industry. Each acquisition strengthens market position and enhances pricing power.

Pricing power remains intact and could accelerate. The team's disciplined execution of our proven value-over-volume commercial strategy drove an organic improvement of 33.0 percent and 46.4 percent in full-year Adjusted EBITDA and aggregates unit profitability, respectively. As consolidation continues and barriers to new supply remain high, pricing power should strengthen, not weaken.

Climate change, paradoxically, could benefit Martin Marietta. More severe weather requires more resilient infrastructure. Flooding requires new drainage systems. Rising seas require seawalls. All these adaptations are aggregates-intensive. Martin Marietta could be a beneficiary, not victim, of climate adaptation spending.

The balance sheet provides enormous optionality. With modest leverage and strong cash generation, Martin Marietta can pursue large acquisitions, increase shareholder returns, or invest in organic growth as opportunities arise. This financial flexibility is valuable in uncertain times.

XI. Epilogue & Reflections

The Martin Marietta story challenges conventional wisdom about American manufacturing. While others sought growth through globalization or digitalization, Martin Marietta found it in the most local, physical business imaginable. They proved that in an economy obsessed with asset-light business models, asset-heavy can still create enormous value—if you own the right assets.

The infrastructure megatrend supporting Martin Marietta isn't just about government spending. It's about the physical reality that America's infrastructure is old and inadequate for modern needs. Roads designed for 1950s traffic volumes can't handle 2020s demands. Bridges built to last 50 years are approaching 75. Water systems installed a century ago are failing. This isn't a political issue—it's physics and time.

Demographics provide another tailwind. Population continues shifting to Martin Marietta's core markets—the Southeast, Texas, Florida, Colorado. These aren't just retirees seeking sunshine. They're young families seeking affordable housing, companies seeking business-friendly environments, and immigrants seeking opportunity. All need roads, buildings, and infrastructure—all need aggregates.

Technology, surprisingly, favors incumbents like Martin Marietta. While Silicon Valley disrupts industry after industry, nobody has figured out how to disrupt rocks. You can't download aggregates. You can't 3D print them at scale. Amazon can't deliver them economically. The physical nature of the business creates a moat that technology strengthens rather than threatens.

The competitive moats in "boring" businesses deserve more investor attention. Martin Marietta has built multiple, reinforcing moats: regulatory (permitting), physical (transportation costs), economic (scale advantages), and operational (decades of optimization). These moats widen over time rather than erode—the opposite of many technology businesses.

Why aggregates beat aerospace becomes clear in retrospect. The spinoff that seemed like abandonment was actually liberation. Freed from the complexity, cyclicality, and capital intensity of aerospace, the aggregates business could focus on its simple mission: moving rocks from Point A to Point B profitably. Sometimes the best businesses are the simplest.

The lessons for investors are profound. First, industry structure matters more than industry growth. Better to dominate a slow-growing industry with favorable dynamics than compete in a fast-growing industry with poor economics. Second, local scale economies can be more valuable than global scale. Martin Marietta's collection of local monopolies is worth more than a globally competitive commodity business. Third, patient capital allocation compounds. Martin Marietta's steady, disciplined approach to capital allocation has created more value than any moonshot bet could have.

Looking ahead to the next decade, three themes will likely dominate. Automation will finally come to quarries—not replacing workers entirely but augmenting them, improving safety and efficiency. Sustainability will shift from cost to opportunity as carbon pricing and green building standards favor producers who can document environmental performance. Finally, the consolidation endgame approaches—at some point, the industry will be sufficiently concentrated that further consolidation faces regulatory limits.

Martin Marietta has transformed from a family quarry to an infrastructure powerhouse not through revolution but through evolution. They've proven that in business, as in geology, patient, persistent pressure can move mountains. For long-term investors seeking exposure to America's infrastructure future, Martin Marietta offers a foundation as solid as the rocks they sell.

The story that began with the Ragland brothers blasting granite in North Carolina has become something much larger—a testament to the value of focus, discipline, and the simple recognition that civilization is built on rock. As America rebuilds its infrastructure, reshores its manufacturing, and houses its growing population, Martin Marietta will be there, moving mountains one blast at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube