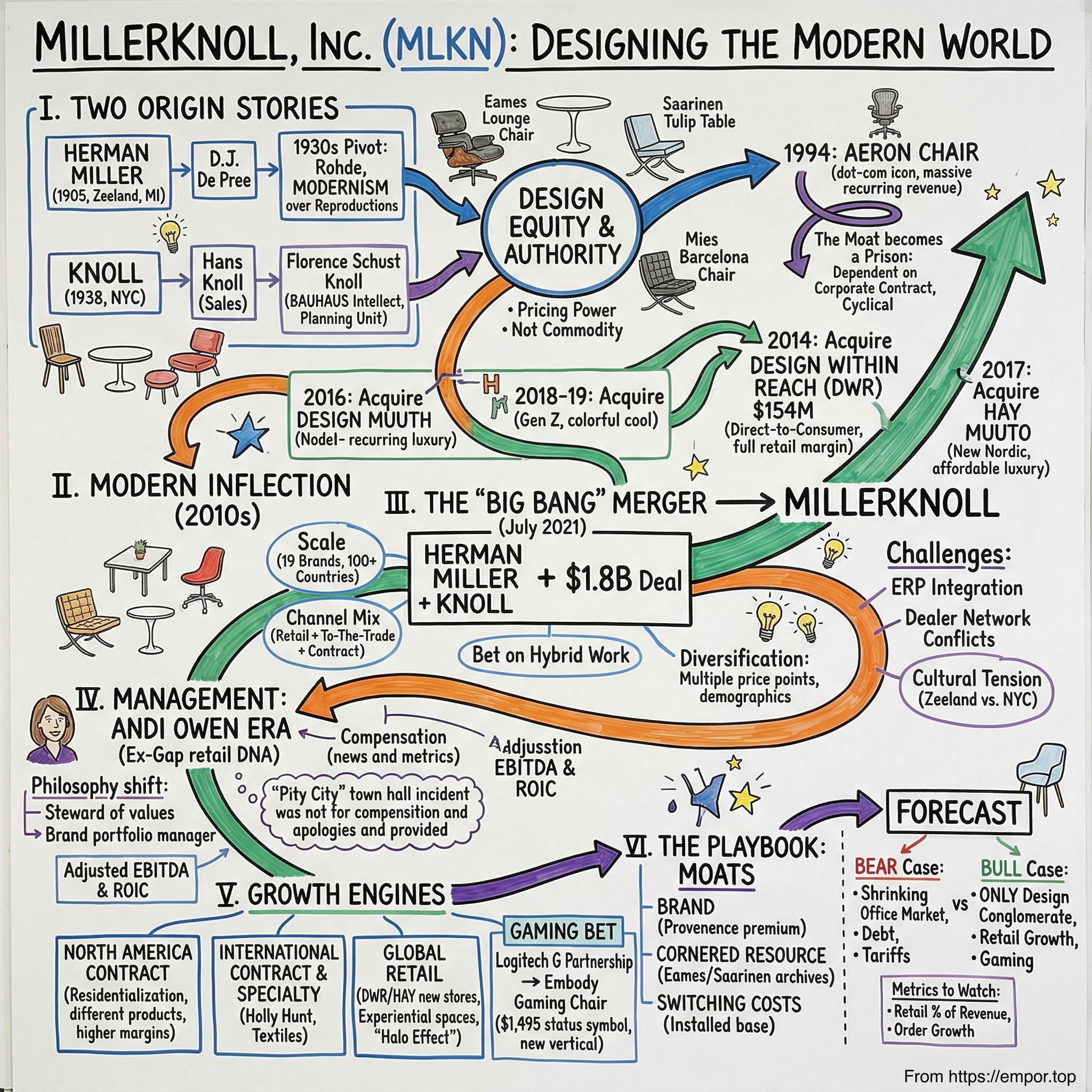

MillerKnoll: Designing the Modern World

I. The Hook: The "Apple of Design"

Walk into any Fortune 500 corner office, any venture-backed startup in SoMa, any architect's studio in Copenhagen, and look at the furniture. Odds are strong that the chair underneath the CEO, the sofa in the reception area, or the pendant light above the conference table carries a name owned by a single company most people outside the design world have never heard of: MillerKnoll.

This is the story of how two of the twentieth century's fiercest design rivals, Herman Miller and Knoll, spent decades defining the American aesthetic and then, in the middle of a global pandemic that threatened to make their core product category obsolete, decided to merge into a single entity. It is a story about whether "design equity," the intangible but very real premium that comes from owning an Eames Lounge Chair or a Saarinen Tulip Table, can function as a durable business moat in an era of flat-pack knockoffs and remote work. And it is a story about what happens when a company built by designers is handed to a retail executive from Gap Inc. and told to become the LVMH of the home.

The stakes are significant. MillerKnoll generated $3.7 billion in revenue in fiscal 2025. It operates 19 brands across more than 100 countries, with 64 showrooms and over 50 physical retail locations. Its products sit in the permanent collection of the Museum of Modern Art. Its Aeron chair has sold more than eight million units since 1994, making it arguably the single most successful piece of office furniture ever produced. And yet, its market capitalization as of early 2026 hovered around $1.3 billion, a fraction of its annual sales, as investors wrestled with a simple question: in a world where millions of knowledge workers never returned to the office, is the greatest furniture company in history a growth story or a melting ice cube?

The answer, as with most things in design, depends on how you look at it.

To understand MillerKnoll, you have to understand two origin stories. One begins in a small Dutch Reformed community in western Michigan. The other begins in a second-floor walkup on East 72nd Street in Manhattan. Both are tales of immigrants, obsessive craftsmanship, and the radical idea that the objects surrounding us at work are not just functional necessities but expressions of culture, aspiration, and identity. Those two stories collided in July 2021, and the reverberations are still being felt.

II. Heritage as a Foundation

In 1905, in the tiny town of Zeeland, Michigan, a community so steeped in Dutch Reformed values that it still closes its shops on Sunday, a small furniture maker called the Star Furniture Company began producing bedroom suites for the Midwestern middle class. It was unremarkable work, the kind of ornate, reproduction-style furniture that filled catalog pages across America. The company might have remained a footnote in Grand Rapids' long furniture-making history if not for a young clerk named Dirk Jan "D.J." De Pree, who married the boss's daughter, scraped together enough capital, and in 1923 renamed the operation after his father-in-law: Herman Miller.

For the first decade, Herman Miller continued making traditional furniture. The pivot came from an unlikely source. In the early 1930s, De Pree encountered Gilbert Rohde, a New York designer who had been proselytizing the gospel of modernism, the idea that furniture should be honest about its materials, functional in its purpose, and stripped of the Victorian ornamentation that still dominated American homes. De Pree was a deeply religious man, and something about modernism's insistence on truth in design resonated with his Calvinist sensibility. In 1933, Herman Miller debuted Rohde's designs at the Chicago World's Fair, and De Pree made a decision that would define the company for the next century: Herman Miller would stop making reproductions and commit entirely to modern design. It was, at the time, commercial suicide by any conventional measure. The Depression was ravaging furniture sales. Retailers were baffled. But De Pree held firm.

The genius of what came next was not just aesthetic but structural. In 1947, De Pree hired George Nelson, an architect and writer with no furniture design experience, as the company's Director of Design. Nelson, in turn, recruited Charles and Ray Eames, the husband-and-wife team whose experiments with molded plywood during World War II had opened up entirely new possibilities for mass-produced furniture. What De Pree, Nelson, and the Eameses created was not a furniture company in any traditional sense. It was, as the oft-quoted phrase goes, a "publisher of furniture," a platform that identified brilliant designers, gave them creative freedom, handled manufacturing and distribution, and let the designs speak for themselves. Nelson brought in Isamu Noguchi, who designed the iconic coffee table. He brought in Alexander Girard, who transformed the company's textile and color palette. The Eameses produced the Molded Plywood Chair in 1946 and, a decade later, the Eames Lounge Chair and Ottoman, a piece that Time magazine would later call the best design of the twentieth century.

Three thousand miles east, a parallel story was unfolding. Hans Knoll, a German immigrant and the son of a furniture maker from Stuttgart, arrived in New York City in 1937 and, in 1938, opened a one-room furniture operation on East 72nd Street. Hans was a born salesman, charming and relentless, but it was his marriage in 1946 to Florence Schust that transformed the business. Florence had studied at the Cranbrook Academy of Art under Eliel Saarinen, attended the Illinois Institute of Technology under Mies van der Rohe, and absorbed the Bauhaus philosophy that architecture and furniture were inseparable. She was, in every sense, a product of the European modernist diaspora, and she brought that intellectual rigor to Knoll's product line.

Florence Knoll did something remarkable: she convinced the greatest architects of the twentieth century to design furniture for her company. Eero Saarinen created the Womb Chair after Florence told him she wanted "a chair like a great big basket of pillows that I can curl up in." He later designed the Tulip Table and Pedestal Collection, pieces that remain in production more than sixty years later. Mies van der Rohe's Barcelona Chair, originally designed for the 1929 International Exposition, became a Knoll signature. Marcel Breuer contributed his tubular steel designs. Over the decades, more than forty Knoll pieces entered the permanent collection of the Museum of Modern Art.

The key distinction between the two companies was cultural DNA. Herman Miller was Midwestern, earnest, and communitarian. D.J. De Pree adopted the Scanlon Plan in 1950, making Herman Miller one of the first companies in Michigan to embrace participative management and gain-sharing with workers. In 1983, a special stock-ownership plan made every employee a shareholder. Max De Pree, D.J.'s son, wrote "Leadership Is an Art," a management classic that argued leadership was about "liberating people to do what is required of them in the most effective and humane way possible." Knoll, by contrast, was cosmopolitan, glamorous, and architecturally driven. Florence Knoll pioneered the Knoll Planning Unit, which didn't just sell furniture but designed entire office interiors, essentially inventing the concept of the modern corporate office. When Hans Knoll died in a car accident in 1955, Florence took over and ran the company with an iron aesthetic will until she retired in 1965.

Both companies shared one critical insight: they were not selling commodities. They were selling design authority. And for decades, that authority translated into pricing power that was virtually unassailable. When a Fortune 500 company outfitted its headquarters, it didn't comparison-shop between Herman Miller and a no-name manufacturer the same way it might compare paper-clip vendors. The furniture was a statement about the company's identity, its sophistication, its commitment to quality. This is the moat that carried both companies through the second half of the twentieth century.

But moats can become prisons. By the mid-1990s, both companies had become deeply dependent on a single channel: the corporate contract office. And no product embodied that dependency more completely than the Aeron chair.

Designed by Bill Stumpf and Don Chadwick and launched in 1994, the Aeron was a genuine breakthrough. Its mesh Pellicle suspension material eliminated the need for foam cushioning. Its three sizes accommodated body types from the first to the ninety-ninth percentile. It was so visually distinctive that it became a cultural signifier: the Aeron was the chair of the dot-com boom, visible in every tech-company photograph, a shorthand for "we're serious about our people." At a thousand dollars per unit, it was not cheap, but corporate procurement officers, who were buying hundreds or thousands at a time, didn't flinch. The installed base grew massive. Replacement cycles were long but predictable. Herman Miller had, in effect, created the recurring-revenue model of office furniture.

The problem was cyclicality. When the dot-com bubble burst, Aeron orders collapsed. When the 2008 financial crisis hit, they collapsed again. The corporate contract business was a leveraged bet on commercial real estate, and commercial real estate moved in brutal cycles. For investors, this made Herman Miller and Knoll deeply frustrating: brilliant brands, iconic products, but earnings that whipsawed with every macroeconomic tremor. Something had to change.

III. The Modern Inflection (2010-2020): The Diversification Blitz

The insight that would reshape Herman Miller arrived not in a boardroom in Zeeland but in a showroom in San Francisco. Design Within Reach, or DWR, had been founded in 1998 by Rob Forbes with a deceptively simple premise: bring the kind of modern design furniture sold through exclusive trade channels directly to consumers. Forbes built a catalog and a network of studios where ordinary people, not just architects and interior designers, could walk in and buy an Eames chair or a Nelson bench. By the early 2010s, DWR had become the largest single vendor of Herman Miller products. The consumer who browsed a DWR catalog on a Sunday afternoon was fundamentally different from the corporate procurement officer who placed a bulk order on a Tuesday morning. The consumer bought on emotion, on aspiration, on the desire to own a piece of design history. And the consumer paid full retail.

In July 2014, Herman Miller, under CEO Brian Walker, acquired an 84 percent stake in Design Within Reach for $154 million in cash. Walker called it "a transformational step forward in realizing our strategy for diversified growth and establishing Herman Miller as a premier lifestyle brand." The acquisition gave Herman Miller something it had never had: a direct-to-consumer retail channel with 38 studios across North America, a robust e-commerce platform, and a catalog business that reached millions of design-conscious households. The strategic logic was elegant. DWR was already selling Herman Miller products; by owning DWR, Herman Miller could capture the retail margin, control the brand presentation, and gather consumer data that its dealer-mediated contract business never provided.

The DWR acquisition was not without controversy. A lawsuit later alleged that Herman Miller had known about operational problems at DWR before closing the deal, and some analysts questioned whether $154 million was too steep for a retailer with modest profitability. But the strategic verdict, viewed from the vantage point of 2026, is clearer: DWR became the laboratory for Herman Miller's transformation from a B2B office supplier into something more ambitious. It proved that design-conscious consumers would pay premium prices for authenticated modern furniture, and it created a retail infrastructure that would later serve as the distribution backbone for new brand acquisitions.

The next move came from the other side of the Atlantic. HAY, founded in Copenhagen in 2002 by Rolf and Mette Hay, had built a reputation as the design brand for the Instagram generation: colorful, accessible, Scandinavian-cool, with price points below Herman Miller's but far above IKEA's. If DWR was the "gateway to modernism" for affluent baby boomers, HAY was the on-ramp for millennials and Gen Z buyers who wanted design credibility without the four-figure price tags. In June 2018, Herman Miller acquired a 33 percent equity stake in HAY for $66 million, along with North American brand rights for an additional $5 million. In October 2019, the company increased its stake to 67 percent for another $78 million, with co-founders Rolf and Mette Hay retaining the remaining third and continuing to lead creative direction.

Meanwhile, Knoll was executing its own diversification playbook. In December 2017, Knoll announced its acquisition of Muuto, a Copenhagen-based design company whose name translates to "new perspective" in Finnish, for approximately $300 million. Muuto had grown its revenue at a 33 percent compound annual growth rate to roughly $75 million, specializing in what it called "affordable luxury," the New Nordic aesthetic that had captured the imagination of a generation of young professionals. Knoll CEO Andrew Cogan positioned Muuto as a way to expand the company's international sales mix from 15 percent to 20 percent and lower the average price point of the portfolio.

What is striking about this period, roughly 2014 to 2020, is how both Herman Miller and Knoll independently arrived at the same strategic conclusion: the future of premium furniture was not in selling more desks to more corporations, but in building a portfolio of design brands that could reach consumers across multiple price points, demographics, and channels. The multiples they paid reflected this conviction. DWR at $154 million, HAY at roughly $150 million total, Muuto at $300 million: these were not traditional furniture-company valuations. They were prices paid for "design equity," the belief that a brand with genuine aesthetic authority and cultural relevance could command margins that commodity furniture makers could only dream of. Whether those prices were justified would depend on whether the acquirers could grow these brands faster than they could have grown independently, a question that the pandemic would put to an urgent test.

IV. The "Big Bang" Merger: Herman Miller + Knoll

By early 2021, a scenario that would have seemed absurd five years earlier had become not just plausible but arguably inevitable. The COVID-19 pandemic had emptied corporate offices across the world. Millions of knowledge workers were setting up home offices, buying ergonomic chairs and standing desks from Amazon, and wondering whether they would ever return to a cubicle. Commercial real estate vacancy rates were climbing. The corporate contract furniture business, the engine that had powered both Herman Miller and Knoll for decades, faced an existential question mark.

At the same time, a countervailing force was at work. The very people who had abandoned their offices were spending unprecedented amounts on their homes. The "residentialization" trend, the blurring of boundaries between work space and living space, was creating new demand for furniture that was functional enough for an eight-hour workday but beautiful enough for a living room. Herman Miller's DWR and HAY channels were seeing a surge. Knoll's residential lines were outperforming expectations. The pandemic had, paradoxically, both threatened the old business model and validated the diversification strategy.

Against this backdrop, Herman Miller announced in April 2021 that it would acquire Knoll for approximately $1.8 billion. The deal structure reflected the relative positions of the two companies: each Knoll share would be converted into 0.32 shares of Herman Miller common stock plus $11.00 in cash. Upon completion, Herman Miller shareholders would own roughly 78 percent of the combined entity and Knoll shareholders approximately 22 percent. The acquisition closed on July 19, 2021, and the combined company was renamed MillerKnoll.

The strategic rationale was multi-layered. First, scale. The combined entity would control 19 brands with a presence in more than 100 countries, creating what management described as a "design conglomerate" comparable to LVMH's role in luxury fashion. Second, channel diversification. Herman Miller brought DWR and HAY's consumer-facing retail infrastructure; Knoll brought Holly Hunt, the ultra-high-end "to-the-trade" brand beloved by interior designers, along with Knoll Textiles, Spinneybeck leather, and Maharam fabrics. Third, and most critically, the merger was a bet that the "death of the office" narrative was overblown, and that the real opportunity lay in owning both sides of the equation: the contract office furniture that companies would need as they redesigned hybrid workplaces, and the residential and retail products that individual consumers were buying for their homes.

But the synergy math was more complicated than the press releases suggested. Herman Miller and Knoll had spent decades competing with each other, and their dealer networks reflected that rivalry. Herman Miller's North American dealers were fiercely loyal and accustomed to operating as the exclusive premium option in their territories. Knoll's dealers had their own relationships, their own design studios, their own client lists. Merging these networks without alienating the independent dealers who controlled the last mile of customer relationships was a monumental logistical challenge.

The ERP integration was equally daunting. The two companies ran on entirely different enterprise resource planning systems, the digital backbone that manages everything from order processing to inventory management to financial reporting. Unifying those systems is the kind of tedious, unglamorous work that rarely makes headlines but can make or break a merger. MillerKnoll would not complete this ERP integration until 2024, three years after the deal closed.

The cultural integration was perhaps the most delicate of all. Herman Miller's identity was rooted in Zeeland, in the De Pree family's communitarian values, in the Scanlon Plan's participative management philosophy. Knoll's identity was rooted in New York, in Florence Knoll's architectural vision, in the glamour of modernist design. One company had a stock-ownership plan that made every employee a shareholder; the other had a Planning Unit that redesigned corporate America's offices. Merging these cultures required more than org-chart shuffling. It required a leader who could hold both identities without flattening either one.

By the end of fiscal 2023, MillerKnoll had captured $131 million in run-rate cost synergies, progressing toward an updated target of $145 million. By the third quarter of fiscal 2024, that figure reached $153 million, with a goal of $160 million in annual run-rate savings. Those numbers demonstrated real operational progress. But the company also took $130 million in non-cash impairment charges against the goodwill attributed to Holly Hunt, the Global Retail reporting unit, and the Knoll and Muuto trade names, a sobering reminder that some of the acquired brands had not yet delivered on the growth expectations embedded in their purchase prices.

V. Management and Incentives: The Andi Owen Era

When Herman Miller's board went looking for a new CEO in 2018 to replace the retiring Brian Walker, it made a choice that raised eyebrows across the design world: Andi Owen, a 25-year veteran of Gap Inc. who had most recently served as Global President of Banana Republic. Owen had no background in furniture, no training in industrial design, no history in the contract office market. What she had was deep expertise in brand management, omnichannel retail, and the kind of consumer-facing transformation that Herman Miller's board believed the company needed.

Owen's career trajectory tells you everything about the board's strategic intent. She started in 1988 as a department manager at Bloomingdale's, rose through Banana Republic's ranks to General Manager of Canada, then Zone Vice President, and finally Global President. She held a BA from the College of William and Mary and had completed executive education at Harvard Business School. Her entire professional life had been spent thinking about how to present brands to consumers in physical stores, online, and through catalogs. Hiring her was a signal: Herman Miller was no longer going to be led by the "founder-designer" cult that had guided it for nearly a century. It was going to be run as a brand portfolio, with the same operational discipline that Gap applied to its family of apparel labels.

This was a philosophical departure of the first order. Under the De Pree family, Herman Miller's CEO was expected to be a steward of design values, a custodian of relationships with the designer community, a leader who understood that the company's competitive advantage flowed from its creative culture. Owen's mandate was different: grow the retail business, integrate the Knoll acquisition, and prove that "design equity" could be converted into shareholder returns. Her compensation structure reflected these priorities. The proxy statement revealed incentive targets focused on adjusted EBITDA margins and Return on Invested Capital, the metrics of a consumer brand company, not a design atelier.

Owen's leadership style came under a very public microscope in April 2023, when a 90-second clip from an internal town hall went viral. An employee had asked about bonus payouts at a time when the company was navigating post-pandemic headwinds. Owen's response, "Don't ask about what are we going to do if we don't get a bonus. Get the damn thing done. Spend your time and your effort thinking about the $26 million you need to close, not thinking about what your bonus is going to be. Leave Pity City," was viewed more than 20 million times and drew withering criticism on social media and in the national press.

The backlash was amplified by the compensation disparity: Owen's total compensation for the fiscal year ended May 2022 was approximately $5 million, including a $1.1 million salary and $3.9 million in stock awards. The median total pay of MillerKnoll employees was roughly $45,000, a ratio of approximately 111 to 1. Owen issued an apology within days, calling the moment "insensitive" and acknowledging that her "rallying cry" had "landed in a way that I did not intend."

The incident was damaging but also revealing. It exposed the tension between the old Herman Miller culture, which had been built on the Scanlon Plan's ideal of shared sacrifice and participative management, and the new MillerKnoll reality, which was a publicly traded conglomerate under pressure to deliver shareholder returns in a difficult market. Owen survived the controversy and, in subsequent interviews, demonstrated a capacity for self-reflection that suggested the experience had genuinely recalibrated her leadership approach. She spoke about the importance of empathy, acknowledged that she had learned from the moment, and refocused attention on the company's strategic transformation.

The question for investors is whether Owen's retail DNA is the right fit for this particular company at this particular moment. On one hand, the DWR expansion, the HAY integration, and the push into omnichannel distribution are all initiatives that benefit from exactly the kind of expertise Owen brings. On the other hand, MillerKnoll's most valuable assets are its design relationships and its creative heritage, the kind of intangible capital that is easy to squander and extraordinarily difficult to rebuild. Managing a furniture design conglomerate is not the same as managing a clothing retailer, and the brands in MillerKnoll's portfolio are unforgiving of leaders who prioritize operational efficiency over creative excellence.

VI. The "Hidden" Growth Engines

Strip away the macro narrative about the death of the office and the rise of remote work, and MillerKnoll's business reveals a more nuanced picture when examined segment by segment. As of March 2025, the company reorganized its reporting into three segments: North America Contract, International Contract, and Global Retail. Each tells a different story.

North America Contract remains the engine, the segment that generates the majority of revenue and cash flow. But the nature of that revenue is shifting. The old model was straightforward: a corporation builds or renovates an office, a dealer designs the space, and Herman Miller or Knoll supplies the systems furniture, the desks, the partitions, the task chairs. That model still exists, but the product mix is evolving. The "residentialization of the office" means that corporate clients are increasingly buying lounge furniture, collaborative seating, soft furnishings, and acoustically designed spaces rather than rows of identical workstations. This is a subtle but important shift because lounge and ancillary furniture tends to carry higher margins and shorter replacement cycles than systems furniture. Companies redesigning for hybrid work are not buying fewer pieces of furniture; they are buying different pieces of furniture, and MillerKnoll's portfolio is unusually well-positioned for this transition.

International Contract and Specialty encompasses the company's overseas operations along with its crown-jewel specialty brands: Holly Hunt, Spinneybeck, Maharam, Edelman Leather, and Knoll Textiles. Holly Hunt deserves particular attention. Acquired by Knoll before the merger, Holly Hunt is a "to-the-trade" brand, meaning its products are sold exclusively through interior designers and architects, never directly to consumers. This creates an aura of exclusivity that supports luxury-level pricing. Holly Hunt showrooms function less like retail stores and more like private galleries where designers bring their wealthiest clients to select custom fabrics, lighting, and furniture for high-end residential projects. The margins in this business are substantially higher than in the contract office segment, and the clientele is less sensitive to macroeconomic cycles. Maharam and Knoll Textiles, which supply fabrics to both internal brands and external customers, operate as the design equivalent of Intel Inside, embedded across the industry in ways that generate steady, if unglamorous, revenue.

Global Retail is the growth segment and the one that most clearly reflects Owen's strategic vision. This segment houses DWR, HAY, and the company's direct-to-consumer operations, including e-commerce, catalogs, and physical stores. MillerKnoll opened four new retail stores in fiscal 2025, including DWR locations in Palm Springs and Paramus and Herman Miller stores in Fairfax and Coral Gables. The company has outlined plans for 14 to 16 additional new locations, a pace of expansion that signals genuine conviction in the physical retail model even as many competitors retreat to digital-only.

The logic behind this retail expansion is worth understanding. A DWR or HAY store is not a traditional furniture showroom. It is an experiential space where consumers interact with products, sit in chairs, touch fabrics, and absorb the brand's design philosophy. The conversion rates in these stores are high because the customer who walks into a DWR studio is self-selecting for design awareness and willingness to pay premium prices. The store also serves as a customer-acquisition channel for e-commerce: a consumer who visits a DWR store in Palm Springs may not buy anything that day but returns home and orders a $5,000 sofa online. This "halo effect" is difficult to measure precisely but is well understood in luxury retail.

Then there is the gaming bet, perhaps the most unexpected chapter in MillerKnoll's recent history. In July 2020, Herman Miller partnered with Logitech G to launch the Embody Gaming Chair, a $1,495 adaptation of Herman Miller's Embody office chair with gaming-specific enhancements including a cooling foam seat with copper-infused particles and an adjusted posture profile optimized for the forward-leaning position of competitive gamers. The two companies spent nearly two years studying esports professionals and casual gamers to develop the product.

The gaming chair became a cult object almost overnight. In a market dominated by racing-style chairs from brands like Secretlab and DXRacer, the Embody Gaming Chair was a dramatic outlier: a genuinely ergonomic product with a design pedigree, carrying a price tag that was three to five times higher than most competitors. For a certain type of gamer, the kind who spends thousands on a monitor and GPU, the Embody became a status symbol, proof that you took your setup seriously. The partnership opened up a multi-billion-dollar vertical for MillerKnoll that carried zero "office furniture" baggage and reached a demographic, young male tech enthusiasts, that had never previously been in the company's customer base.

VII. The Playbook: Strategic Moats and Competitive Forces

To understand MillerKnoll's competitive positioning, it helps to apply Hamilton Helmer's 7 Powers framework, which identifies the sources of durable competitive advantage.

The most obvious power is Brand. The names Herman Miller, Knoll, Eames, and Saarinen carry a weight in the design world that is genuinely difficult to replicate. When a consumer buys an Eames Lounge Chair for $6,000 or more, they are not paying for the materials or even the engineering. They are paying for design provenance, for the right to own a piece of cultural history, for the knowledge that this is the real thing and not a reproduction. This brand premium, estimated at 30 to 50 percent above generic competitors for comparable products, is the single most important source of MillerKnoll's pricing power.

The second power is Cornered Resource. MillerKnoll controls the exclusive production rights to the design archives of Charles and Ray Eames, George Nelson, Eero Saarinen, Florence Knoll, and dozens of other twentieth-century masters. These are not patents, which expire, but licensing and ownership arrangements that function as a permanent competitive barrier. No competitor can legally produce an authentic Eames Lounge Chair or a Saarinen Tulip Table. This is the "Disney Vault" of furniture: a library of iconic designs that generates revenue decade after decade with minimal ongoing investment.

The third power, Switching Costs, is asymmetric. For individual consumers, switching costs are low: nothing prevents a homeowner from buying a chair from a different brand next time. But for Fortune 500 companies with massive installed bases of Herman Miller or Knoll products, the switching costs are substantial. These companies have dealer relationships, maintenance contracts, standardized specifications, and trained facility managers who know the product lines. Replacing an installed base of thousands of Aeron chairs with a competitor's product is not just expensive but organizationally disruptive. This installed-base advantage creates a recurring revenue stream from replacement cycles, parts, and accessories.

Applying Michael Porter's Five Forces reveals a more contested landscape. The threat of substitutes is high and rising. Steelcase, Haworth, and a growing number of Asian manufacturers produce office chairs and desks that are functional equivalents at a fraction of the price. Amazon and Wayfair have trained consumers to comparison-shop for furniture online, eroding the information asymmetry that once protected premium brands. MillerKnoll's defense against substitution is not price but design authority: the argument that a genuine Herman Miller product is not a commodity but an investment in health, productivity, and aesthetic quality.

The competitive landscape shifted dramatically in December 2025 when HNI Corporation completed its $2.2 billion acquisition of Steelcase, creating a combined entity with approximately $5.8 billion in pro forma annual revenue. This new competitor is significantly larger than MillerKnoll in the contract office segment and benefits from HNI's prior 2023 acquisition of Kimball International, which added mid-market capabilities. The HNI-Steelcase combination represents a formidable rival in exactly the contract segment where MillerKnoll generates most of its revenue. However, MillerKnoll retains significant advantages in design prestige, consumer retail, and brand portfolio breadth that HNI-Steelcase does not match.

The bargaining power of buyers is undergoing a structural shift that favors MillerKnoll. In the old model, the primary buyer was the corporate procurement officer, a sophisticated, price-conscious negotiator purchasing in bulk with significant leverage. As MillerKnoll's revenue mix shifts toward retail, the buyer base becomes more fragmented: individual consumers purchasing one chair or one table at a time, with limited negotiating power and higher willingness to pay full price. This fragmentation is a margin tailwind that partially offsets the volume pressures in the contract business.

The threat of new entrants is moderate. Building a furniture brand with genuine design credibility takes decades. A startup can produce a functional office chair relatively easily, but it cannot conjure the kind of cultural authority that comes from having Charles Eames design your products seventy years ago. The barrier to entry in the commodity segment is low, but the barrier to entry in the design-premium segment is extraordinarily high.

VIII. The Bear vs. Bull Case

The bear case against MillerKnoll starts with commercial real estate. Office vacancy rates in major U.S. cities remain elevated years after the pandemic. Remote and hybrid work arrangements have become permanent for a substantial share of knowledge workers. If the long-term trajectory is fewer square feet of office space per company, then the total addressable market for contract office furniture is shrinking, and MillerKnoll's core business faces a secular headwind that no amount of brand equity can overcome. Bears argue that the Knoll acquisition was fundamentally a defensive move, an attempt to create scale and diversification to mask a declining core business. The $130 million in goodwill impairment charges taken against Holly Hunt, Global Retail, and the Knoll and Muuto trade names lend credence to this view: if the acquired brands were performing as hoped, those write-downs would not have been necessary.

The leverage profile adds to the concern. MillerKnoll carried a net debt-to-EBITDA ratio of 2.65 times as of the third quarter of fiscal 2024. That is manageable but not conservative, and it leaves limited room for error if revenue disappoints or margins compress. The company's market capitalization of roughly $1.3 billion against revenue of $3.7 billion implies a price-to-sales ratio well below one, a valuation that reflects deep investor skepticism about the growth trajectory.

Tariffs present another overhang. The Trump administration's tariff announcements in 2025 and 2026 created uncertainty across the furniture industry. MillerKnoll estimated tariff costs of $5 to $7 million before tax and implemented surcharges and price increases to offset the impact. The company has a structural advantage here, with approximately 70 percent of its North American retail cost of goods sourced domestically, making it significantly less exposed than competitors who rely heavily on Asian manufacturing. But tariffs remain a wildcard that could pressure margins if they escalate further.

The bull case centers on a simple proposition: MillerKnoll is the only "design conglomerate" operating at scale. No other company in the world owns a comparable portfolio of iconic design brands spanning the contract office, residential, luxury, and retail segments. The bears are right that the traditional contract office market is under pressure, but they are wrong about the implications. MillerKnoll is not fighting the "death of the office" narrative; it is positioned on both sides of it. As offices are redesigned for hybrid work, companies are buying higher-value ancillary furniture rather than commodity workstations. As individuals invest in home offices, they are buying from DWR and HAY. The "residentialization of the office" and the "office-ization of the home" are two sides of the same coin, and MillerKnoll is the only company that serves both.

The retail expansion strategy is a meaningful catalyst. With plans for 14 to 16 new stores, MillerKnoll is building out a physical retail footprint at a time when most competitors are retreating. Each new DWR or HAY location is a local brand ambassador that generates both direct sales and e-commerce halo effects. The gaming partnership with Logitech G demonstrated the brand's ability to penetrate entirely new demographics, and the $1,495 price point of the Embody Gaming Chair suggests that MillerKnoll's pricing power extends well beyond the traditional design-conscious consumer.

The HNI-Steelcase merger, while creating a larger competitor in the contract segment, also validates the consolidation thesis. The office furniture industry is consolidating because scale matters for procurement, distribution, and brand investment. MillerKnoll was the first mover in this consolidation wave, and its differentiated position as a design-led brand portfolio rather than a volume-driven manufacturer may prove more durable in the long run.

For investors tracking this story, two metrics matter most. First, Global Retail revenue as a percentage of total revenue. This is the single best indicator of whether MillerKnoll is successfully diversifying away from its cyclical contract dependence. A steady increase in retail's share of the mix signals that the brand portfolio strategy is working and that the company is building a more resilient, higher-margin business. Second, order growth trends across segments, particularly in North America Contract. Orders are a leading indicator of revenue, and sustained positive order growth would signal that the hybrid-office redesign cycle is generating real demand, not just replacing pandemic-deferred purchases. In the most recent quarter reported, Q2 fiscal 2026, consolidated orders showed positive year-over-year growth even as revenue dipped slightly, a divergence worth monitoring closely.

IX. Epilogue and Final Reflections

In the spring of 1956, Charles and Ray Eames completed the design of a lounge chair and ottoman for their friend, the film director Billy Wilder. It was, in their words, meant to have "the warm, receptive look of a well-used first baseman's mitt." The chair was made of molded plywood shells and leather cushions, and it cost roughly $300, which in 1956 was an extraordinary sum for a piece of furniture. Today, a new Eames Lounge Chair from MillerKnoll retails for over $6,000, and the design has been in continuous production for seventy years. That single chair encapsulates everything that makes MillerKnoll a fascinating business: the power of design to transcend time, the willingness of consumers to pay extraordinary premiums for authenticity, and the remarkable durability of a brand built on genuine creative excellence.

The question facing MillerKnoll is whether the company can extend that magic from a single iconic chair to a nineteen-brand conglomerate operating across multiple segments, channels, and geographies. The merger of Herman Miller and Knoll brought together two of the most storied names in design history, but it also created integration complexity, cultural tension, and financial leverage that the company is still working through. Andi Owen's retail-first strategy represents a genuine departure from the founder-designer tradition, and the "Pity City" episode revealed the friction that can arise when a brand-management approach collides with a company culture built on participative values.

The most important thing MillerKnoll sells is not, in the end, a chair. It is not a desk, or a fabric, or a lighting fixture. It is status for the knowledge worker, the tangible expression of taste, discernment, and professional seriousness. In an economy that is increasingly about intangibles, about signaling and identity and the curation of one's environment, that is a product category with enormous staying power. The question is not whether people will continue to want beautifully designed furniture. The question is whether MillerKnoll, with all its heritage and all its complexity, is the right vehicle to deliver it.

The consolidation of the industry around a few major players, MillerKnoll on one side and HNI-Steelcase on the other, with Haworth and a handful of others filling the gaps, suggests that the endgame for premium office and home furniture may look more like luxury goods than like traditional manufacturing. In that world, the company with the deepest design archive, the most recognizable brand names, and the broadest channel reach has a structural advantage that is difficult to dislodge. Whether that advantage translates into shareholder returns at the current valuation is a question that depends on execution: on the retail expansion, on the integration of the brand portfolio, on the ability to navigate tariffs and commercial real estate cycles and the ongoing evolution of how and where people work.

MillerKnoll sits at the intersection of design, commerce, and culture in a way that no other public company quite matches. It is a business that was built by artists and is now being run by operators, a tension that is as old as the creative industries themselves. Where it lands in the pantheon of great American brands, whether it becomes the LVMH of the home or a cautionary tale of a legacy giant that couldn't adapt, will depend on what happens in the next few years. The furniture, at least, will endure.

X. Key References and Further Reading

- MillerKnoll Investor Day Presentations (2022/2023) - The "New Day" Strategy for post-merger transformation

- The Herman Miller Aeron Chair Design Oral History - Bill Stumpf and Don Chadwick's development of the Pellicle mesh technology

- Knoll: A Modernist Universe (Rizzoli) - Comprehensive visual history of Knoll's design archives and Florence Knoll's architectural vision

- Andi Owen on the HBR IdeaCast - Discussion of leading through the work-from-home transition and the MillerKnoll integration

- Herman Miller's 2014 DWR Acquisition Filing - The $154 million deal that launched the company's consumer retail strategy

- The Logitech G x Herman Miller Gaming Partnership - Development of the Embody Gaming Chair and entry into the esports market

- Hamilton Helmer's 7 Powers - Framework for analyzing durable competitive advantage in design-driven businesses

- Steelcase vs. MillerKnoll Comparative Analysis - Revenue, margin, and valuation multiples across the contract furniture industry

- Florence Knoll biography and the invention of the modern corporate office through the Knoll Planning Unit

- MillerKnoll 10-K Annual Report - Segment analysis, debt structure, and post-merger financial reporting

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube