MKS Instruments: The Story of the Invisible Semiconductor Empire

I. Introduction and Episode Roadmap

Somewhere inside every chip powering the device you are reading this on, there is a ghost. Not a literal one, but a fingerprint left by a company most people have never heard of. The pressure that shaped the vacuum chamber where silicon was etched. The laser that drilled microscopic vias into a circuit board. The chemical bath that plated copper onto the interconnects linking transistor to transistor. All of it, invisibly, touched by a single company headquartered in Andover, Massachusetts: MKS Instruments.

As of early 2025, MKS carried a market capitalization of roughly four and a half billion dollars, making it a mid-cap player in a semiconductor equipment ecosystem dominated by names like ASML, Applied Materials, and Lam Research. Those companies build the machines that fabricate chips. MKS builds the critical subsystems inside those machines: the pressure gauges, power supplies, lasers, motion controllers, and specialty chemicals without which the machines simply cannot function.

Think of it this way: if ASML builds the race car, MKS builds the engine, the fuel injection system, and increasingly, the fuel itself.

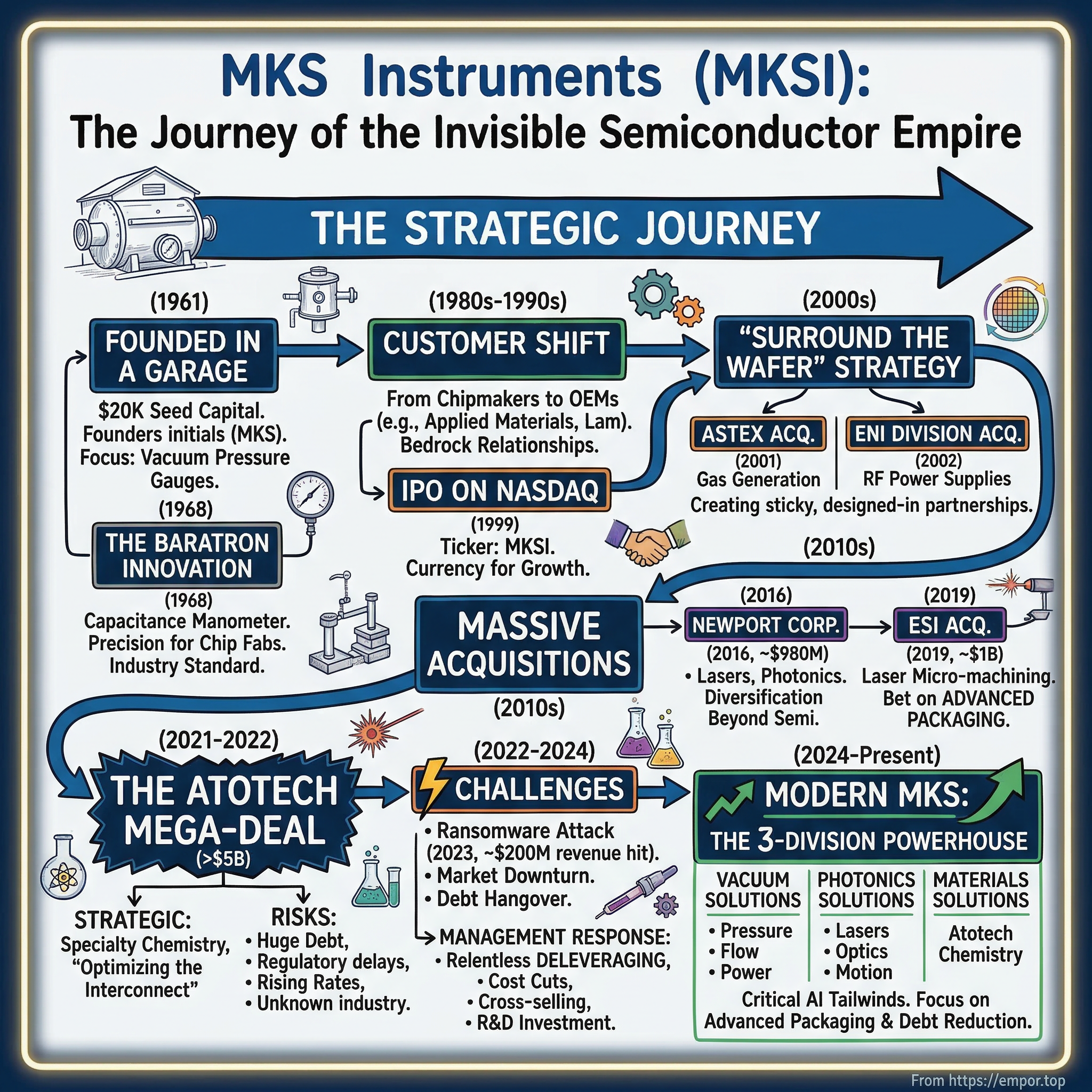

The central question of this story is deceptively simple. How did a company founded in 1961 with twenty thousand dollars in seed capital, making pressure gauges in a Massachusetts garage, become an essential supplier to every semiconductor fabrication plant on Earth? The answer involves six decades of patient engineering, a brilliant "surround the wafer" strategy, and three massive acquisitions in six years that either represent one of the most audacious bets in semiconductor history, or a case study in overreach. Perhaps both.

What makes MKS compelling is not just its products but its strategic arc. This is a company that understood, earlier than almost anyone, that the future of semiconductor manufacturing would be defined not by any single process step but by the interconnection of dozens of precision technologies.

Vacuum control, photonics, laser processing, and now specialty chemistry: MKS has methodically assembled a portfolio that spans the entire manufacturing chain. And it did so through an acquisition playbook that would make any private equity firm nod in appreciation: buy a complementary business, integrate it, extract synergies, pay down debt, and repeat.

But there is tension in this story too.

The Atotech acquisition of 2022, a five-billion-dollar deal financed with mountains of debt just as interest rates began their steepest climb in decades, tested the limits of that playbook. A ransomware attack months later compounded the challenge. And the semiconductor industry, famously cyclical, entered a downturn almost immediately after the deal closed.

The question hanging over MKS today is whether its biggest bet will prove to be its greatest triumph or a burden it carries for years.

This is the story of the invisible semiconductor empire. It begins, as all good origin stories do, with a handful of engineers, a modest sum of money, and a problem that no one else was solving well enough.

II. The Genesis: Vacuum Technology and the Baratron Innovation (1961-1980s)

In 1961, in the quiet suburbs west of Boston, a small group of engineers pooled together twenty thousand dollars to start a company focused on something most people would find spectacularly boring: measuring gas pressure inside vacuum chambers. The founding team included physicist Richard Leiby and engineers Ken Harrison and John Dillon. The company name, MKS, derived from the founders' initials. Twenty thousand dollars. To put that in perspective, a new Chevrolet Impala cost about three thousand dollars that year. These engineers were betting roughly seven cars' worth of capital on the proposition that the fledgling semiconductor industry would need better vacuum instruments than anyone was currently making.

Lexington, Massachusetts, in 1961 was an unlikely cradle for a future semiconductor infrastructure company. The town was better known for its role in the American Revolution than for high technology. But it sat in the orbit of MIT and the constellation of Route 128 technology firms that were beginning to cluster along Boston's western suburbs, a precursor to what Silicon Valley would become on the West Coast. The early semiconductor industry was splitting its geography between the East Coast, where companies like Raytheon and Transitron operated, and Northern California, where Fairchild Semiconductor was beginning to spin off the companies that would define Silicon Valley. MKS planted itself in the thick of the East Coast action.

To understand why their product mattered, you need to understand the physics of making semiconductors, and it is worth spending a moment here because the same physics that drove MKS's founding product still drives its business today. A silicon wafer is processed inside vacuum chambers where gases are introduced at extremely precise pressures. In a chemical vapor deposition process, for example, gases like silane or tungsten hexafluoride are flowed into a chamber at pressures typically measured in millitorr, a unit of pressure so small that standard atmospheric pressure is roughly seven hundred and sixty thousand times larger. At these minuscule pressures, the gases react on the wafer surface to deposit thin films of material, atom by atom, that form the transistors and interconnects of an integrated circuit. If the pressure drifts by even a tiny fraction, the film grows too thick or too thin, the electrical properties change, and the chip fails. Precision pressure measurement is not a nice-to-have in semiconductor manufacturing. It is existential.

In the early 1960s, the tools for measuring vacuum pressure were crude, unreliable, and borrowed from industrial vacuum applications that did not require anywhere near the precision that chip fabrication demanded. Thermocouple gauges and ionization gauges worked well enough for rough vacuum systems but drifted over time and lacked the repeatability that semiconductor processes required.

MKS's breakthrough came in 1968 with the Baratron capacitance manometer. The concept was elegant in the way that the best engineering solutions often are: simple in principle, extraordinarily difficult to execute. Two thin metal diaphragms are separated by a tiny gap, with gas pressure on one side deflecting one diaphragm and changing the electrical capacitance between them. By measuring that capacitance change with exquisite precision, the Baratron could determine gas pressure to an accuracy that was orders of magnitude better than existing technologies. The beauty of the design was that it measured pressure directly, through mechanical deflection, rather than inferring it from secondary effects like temperature or ionization. This made it inherently more stable and repeatable. The name "Baratron" became so synonymous with capacitance manometers in the semiconductor industry that engineers used it generically, the way people say "Kleenex" instead of "tissue." More than fifty years later, Baratron-derived products remain a core part of MKS's vacuum solutions portfolio.

During the 1970s, MKS sold its instruments directly to integrated circuit makers who still built much of their own production equipment in-house. It was a cottage industry era for semiconductors, where a company like Texas Instruments or Fairchild might design, build, and operate its own deposition and etching tools. MKS was the precision instrument vendor that showed up at the loading dock, and its reputation for quality and reliability grew steadily.

Then came a structural shift in the 1980s that would reshape MKS's entire business model. As semiconductor devices grew more complex and manufacturing processes more demanding, chipmakers realized they could not keep building their own equipment and stay competitive. Specialized equipment companies emerged to fill the gap: Applied Materials, Lam Research, Novellus Systems. These original equipment manufacturers, or OEMs, became the new customers for MKS's pressure gauges, flow controllers, and vacuum instruments. The relationship between MKS and the OEMs would become the bedrock of the company's business for the next four decades.

What the founders had done, almost accidentally, was solve a problem so fundamental to semiconductor manufacturing that it could not be engineered around. You cannot make chips without precise vacuum control. And once an OEM qualified a particular MKS gauge or controller into its tool design, the switching costs were enormous. Redesigning a tool to accommodate a different pressure sensor meant re-qualifying the entire process, a procedure that could take months and cost millions. MKS had found its moat before the word was fashionable in business strategy, and it was built on physics, precision, and the sheer difficulty of ripping out something that works.

The implications of this shift were profound for MKS. Instead of selling to dozens of chipmakers who each bought modest quantities, MKS now sold to a handful of OEMs who each purchased enormous volumes. The customer base concentrated, but the depth of each relationship deepened. An equipment OEM did not just buy MKS gauges off the shelf; it worked with MKS engineers to specify, test, and qualify instruments for specific tool platforms. These qualification cycles created an intimacy between MKS and its OEM customers that would prove to be one of the most durable competitive advantages in the semiconductor supply chain.

By the late 1980s, MKS had established itself as the standard-bearer for vacuum pressure measurement in the semiconductor industry. The Baratron was not just a product; it was the reference instrument against which competitors were measured. The company had also begun expanding beyond pressure measurement into related areas like mass flow controllers, which regulate the rate at which gases flow into a process chamber. Each new product category reinforced the same dynamic: solve a critical measurement or control problem with superior precision, get designed into the OEM's tool, and enjoy years of recurring revenue from that design win. It was a formula that worked beautifully at small scale, but the semiconductor industry was about to enter a period of explosive growth that would demand a very different kind of company.

But the company that emerged from this era was still small, still private, and still fundamentally a one-trick pony, brilliant at that trick, but limited. The next chapter would require a different kind of leader, one who understood not just engineering but empire-building.

III. Going Public and The Acquisition Playbook Begins (1990s-2000s)

In 1974, a former management consultant named John Bertucci purchased MKS Instruments. It was not a glamorous acquisition. Bertucci, a Carnegie Mellon-educated engineer who had spent time in semiconductor manufacturing, saw in MKS a company with superb technology and no real business strategy. Over the next two decades, he transformed it from an engineering workshop into a proper enterprise, building out sales teams, expanding internationally, and layering on new product lines through internal development.

The 1990s provided the tailwind Bertucci needed. The personal computer revolution, the rise of the internet, and the explosion of mobile phones drove semiconductor demand to unprecedented levels. Fabs proliferated across Asia, Europe, and the United States. And every new fab needed vacuum instruments, flow controllers, and process control equipment. MKS grew with the tide, but Bertucci recognized that organic growth alone would never make MKS a dominant player.

Meanwhile, a subtle but profound shift was occurring in how semiconductor equipment was designed. In the early days, OEMs like Applied Materials designed almost everything in-house. By the 1990s, the complexity of semiconductor tools had grown to the point where OEMs began asking suppliers like MKS to take on more responsibility. First it was subsystem manufacturing: instead of shipping individual gauges and controllers, MKS would assemble complete vacuum foreline systems for a chemical vapor deposition chamber. Then it evolved further. OEMs began asking MKS to actually design the subsystems, to take ownership of the engineering, not just the assembly. MKS was evolving from a component vendor to a subsystem partner, and this evolution would define its strategic identity for decades to come.

In 1999, MKS went public on the NASDAQ exchange under the ticker symbol MKSI. The IPO was not a splashy Silicon Valley debut. There were no twenty-something founders ringing the opening bell in hoodies. Bertucci, by then in his late fifties, had spent a quarter century building MKS methodically, and the public offering was simply the next logical step in a long-term plan. The IPO gave him the currency he needed, public stock, to pursue a series of acquisitions that would transform the company's capabilities. The timing was both brilliant and treacherous: the dot-com bubble was inflating rapidly, and semiconductor stocks were trading at nosebleed valuations. MKS used that inflated currency brilliantly.

The first deal came in 2000, a small tuck-in acquisition of California-based Spectra International for just under ten million dollars in cash. Spectra brought mass spectrometer and optical spectrometer-based process monitoring products into the MKS portfolio, adding gas analysis capabilities to the existing pressure and flow measurement lineup. It was a modest deal, but it signaled the beginning of a deliberate strategy: expand the number of critical measurements MKS could provide at the point of use in a semiconductor tool.

The following year brought something far more ambitious. In 2001, MKS acquired Applied Science and Technology, known as ASTeX, for approximately three hundred million dollars in stock. ASTeX was a leader in reactive gas generation and microwave power delivery systems, technologies that were becoming increasingly important as semiconductor manufacturers adopted plasma-based processing steps. If MKS's original instruments measured what was happening inside a vacuum chamber, ASTeX's products helped control the energy that drove the chemical reactions within it.

Then, in 2002, MKS acquired Emerson Electric's ENI Division for roughly two hundred and eighty-eight million dollars in stock. ENI was one of the leading suppliers of solid-state radio frequency and direct current plasma power supplies, matching networks, and related instrumentation. This was arguably the most strategic of the three acquisitions. RF power delivery is the heartbeat of plasma etching and deposition, two of the most critical process steps in semiconductor manufacturing. By owning the power supply alongside the pressure gauge and the gas flow controller, MKS was surrounding the semiconductor process chamber with its products.

This was the birth of what would become known internally as the "Surround the Wafer" strategy. The logic was straightforward and powerful: the more products MKS could place in and around a semiconductor tool, the more indispensable it became to the OEM customer, and the harder it would be for competitors to displace any single MKS product. If you only sell the pressure gauge, you are a vendor. If you supply the pressure gauge, the flow controller, the power supply, and the gas delivery system, you are a partner. Partners get designed in. Vendors get bid out.

The dot-com bust hit semiconductor equipment companies hard. The NASDAQ fell nearly eighty percent from its March 2000 peak. Semiconductor equipment spending, which had been surging, collapsed as fab construction projects were delayed or canceled. Revenue cycles in this industry are brutally cyclical, with spending swings of thirty to fifty percent from peak to trough, and MKS was not immune. But the timing of the ASTeX and ENI acquisitions, both completed with stock rather than cash, meant MKS had added major product lines without depleting its balance sheet. When the recovery came, it had a broader portfolio and more resilient revenue base than it had ever enjoyed.

The leadership transition that followed reflected the maturation of the company. Leo Berlinghieri, who had joined MKS in 1980 in manufacturing roles and risen through the organization over two and a half decades, succeeded Bertucci as CEO in 2005 and served until the end of 2013. Berlinghieri oversaw a period of steady organic growth and operational refinement, solidifying the gains from the early 2000s acquisitions and preparing the company for the next chapter of transformation. When Gerald Colella took the CEO role in January 2014, he inherited a company with approximately seven hundred and eighty million dollars in annual revenue, a clean balance sheet, and a proven acquisition playbook. It was a template that he and his successors would deploy at increasingly larger scale for the next decade.

IV. The Newport Gamble: Doubling Down on Photonics (2016)

By the mid-2010s, MKS was a well-regarded but still mid-sized player in the semiconductor equipment ecosystem. Revenue ran around eight hundred million dollars. Gerald Colella, who had joined the company back in 1983 in materials planning and risen through the ranks to become CEO in January 2014, faced a strategic question that every successful niche company eventually confronts: stay focused and risk becoming irrelevant as the market evolves, or expand aggressively and risk losing what made you special in the first place.

Colella chose to expand, and he chose photonics as the frontier.

On February 23, 2016, MKS announced it would acquire Newport Corporation in an all-cash leveraged buyout valued at approximately nine hundred and eighty million dollars. The deal was priced at twenty-three dollars per share and would be financed with a combination of cash on hand and a seven-year, seven hundred and eighty million dollar secured term loan. For a company with eight hundred million in annual revenue, borrowing nearly that amount to acquire a competitor was a genuinely bold move.

Newport Corporation was founded in 1969 by two Caltech graduates, John Matthew and Dennis Terry, who were looking for industrial applications for a technology that most people at the time thought was little more than a laboratory curiosity: the laser. Over nearly five decades, Newport had built a formidable portfolio in precision lasers, photonics instrumentation, optical components, sub-micron positioning systems, vibration isolation, and optical tables. Through its own acquisitions, most notably Spectra-Physics in 2004 and Ophir Optronics in 2011, Newport had become one of the broadest photonics companies in the world.

The strategic rationale was layered. On the surface, it was about diversification: Newport gave MKS a major presence in photonics markets that extended well beyond semiconductors, including life sciences, defense, and research. But the deeper logic was about where semiconductor manufacturing was heading.

For the non-technical reader, photonics is the science and technology of generating, controlling, and detecting photons, essentially particles of light. Lasers are the most familiar photonic technology, but the field encompasses everything from fiber optics to precision optical instruments to the sensors in a smartphone camera. In semiconductor manufacturing, photonics had been important for decades, lasers were used in lithography and metrology, but their role was about to expand dramatically.

As chip geometries shrank below fourteen nanometers and then to seven and five nanometers, photonics technologies became increasingly critical. Extreme ultraviolet lithography required sophisticated laser sources. Advanced metrology and inspection systems relied on precision optics. And the emerging field of advanced packaging, where chips are stacked and connected using laser-drilled vias and precision bonding, was becoming a significant growth driver for photonics. Colella was not just buying a laser company; he was positioning MKS at the intersection of light and electronics, a crossroads that would become more crowded and more valuable with each successive technology generation.

The financing was aggressive by MKS standards. The company had historically been conservatively capitalized, and taking on nearly a billion dollars in debt was a departure. But Colella and his team had done the math: Newport's photonics portfolio was immediately accretive, the combined entity would have roughly one and a half billion in pro forma annual revenue, and the debt could be paid down quickly from combined cash flows. The integration plan called for extracting cost synergies through consolidation of overlapping functions while preserving Newport's technical capabilities and customer relationships.

Consider what Newport's product portfolio actually looked like. Spectra-Physics, acquired by Newport in 2004, was one of the oldest and most respected names in laser technology, producing everything from ultrafast femtosecond lasers used in scientific research to high-power industrial lasers used in materials processing. Ophir Optronics, acquired in 2011, brought infrared optics and photonics test and measurement instruments. Together with Newport's own precision motion and vibration isolation products, MKS was acquiring a photonics ecosystem, not just a single product line.

The deal closed on April 29, 2016, barely two months after announcement, a testament to the straightforward regulatory profile of the transaction. And the integration went remarkably well, partly because MKS had the discipline to preserve what made Newport valuable. Rather than folding Newport into existing MKS divisions, the company established a distinct Photonics Solutions Division that maintained Newport's engineering culture and customer relationships while leveraging MKS's larger sales infrastructure and manufacturing scale. The combined entity had roughly one and a half billion in pro forma annual revenue, and cross-selling opportunities materialized as MKS began offering photonics-enhanced solutions to its existing semiconductor equipment customers.

The financial execution was equally impressive. MKS had borrowed nearly eight hundred million dollars to finance the deal, a debt load that would have been paralyzing for a less disciplined company. But the combined cash flows were strong enough to pay down that debt rapidly, and by the time MKS began evaluating its next acquisition target, the balance sheet had been substantially restored. The Newport playbook became the template: borrow aggressively to acquire a strategic asset, integrate efficiently, generate cash, and deleverage. Rinse and repeat.

The Newport acquisition was the moment MKS graduated from a niche subsystem vendor to a diversified technology platform. It also proved something important about the company's acquisition capabilities: MKS could absorb a company nearly its own size, integrate it efficiently, and pay down the acquisition debt within a few years. That confidence, earned through execution rather than assumed, would inform the next two deals, each larger and more ambitious than the last.

But Newport also introduced a new dynamic that would shape MKS's trajectory in ways both intended and unintended. MKS was no longer just a vacuum and process control company. It was now in the photonics business, the laser business, the precision motion business. Managing that breadth required a different kind of leadership. The CEO succession that placed John Lee at the helm in 2018 was partly a response to this increased complexity. Lee, with his PhD in chemical engineering from MIT and his years at Bell Labs and Applied Materials, brought a technical depth and breadth that matched the expanding portfolio. He understood not just vacuum physics or laser optics but the semiconductor manufacturing process holistically, a perspective that would prove essential for the deals to come.

V. The ESI Acquisition: Betting on Advanced Packaging (2019)

If Newport was MKS's first real leap beyond its comfort zone, the acquisition of Electro Scientific Industries represented a deliberate bet on a trend that was just beginning to reshape the semiconductor industry: the rise of advanced packaging.

On October 30, 2018, MKS announced it would acquire ESI for thirty dollars per share in an all-cash deal valued at approximately one billion dollars. ESI shareholders approved the transaction in January 2019, and it closed on February 1, 2019. The financing followed the now-familiar MKS template: cash on hand supplemented by a seven-year, six hundred and fifty million dollar secured term loan.

ESI, based in Portland, Oregon, was a pioneer in laser-based micro-machining systems used primarily for printed circuit board manufacturing. Its tools could drill thousands of microscopic holes per second into circuit boards, creating the vias that connect different layers of a PCB. To visualize what ESI's machines did: imagine a circuit board as a multi-story building. Each floor is a layer of the board, and the vias are like elevator shafts connecting the floors. ESI's lasers drilled those shafts with a precision measured in millionths of a meter, at speeds that would make your head spin. In an era when PCBs were becoming denser, more layered, and more critical to electronic system performance, ESI's technology was in growing demand.

The timing reflected a strategic insight that was beginning to crystallize across the semiconductor industry. For decades, the path to better chip performance had been straightforward: shrink the transistor. Make it smaller, pack more of them onto a die, and run them faster. This approach, known as Moore's Law scaling, had worked brilliantly for fifty years. But by the late 2010s, the cost and complexity of shrinking transistors below seven nanometers were becoming prohibitive for all but a handful of leading-edge manufacturers. Building a new leading-edge fab cost ten billion dollars or more, and the number of companies that could afford to play at the frontier was shrinking from dozens to a handful.

The industry was waking up to an alternative path that researchers had been discussing for years under the banner of "More than Moore": instead of just making transistors smaller, make the connections between chips better. Advanced packaging, chiplets, heterogeneous integration, fan-out wafer-level packaging, these were no longer academic concepts but commercial imperatives. Apple, AMD, and Intel were all moving toward chiplet-based architectures, where multiple smaller dies are manufactured separately and then connected in a single package. This approach allowed companies to mix and match different process technologies in a single device and improve yields by using smaller dies, but it placed enormous new demands on the packaging and interconnect technologies that held everything together.

ESI's laser drilling and micro-machining capabilities fit directly into this thesis. The company's tools were used to create the physical interconnections in advanced PCBs and packaging substrates, precisely the layers of technology that connected one chip to another. By acquiring ESI, MKS was extending its reach from the wafer fabrication chamber into the packaging and interconnect domain that was becoming the industry's next battleground.

The deal also deepened MKS's laser and photonics capabilities, complementing the Newport portfolio acquired three years earlier. Where Newport's lasers were used for scientific and industrial applications, ESI's systems were purpose-built for electronics manufacturing. Together, they gave MKS a comprehensive laser and photonics platform spanning basic components through complete manufacturing systems.

CEO John Lee, who had taken the helm in 2018, came from Applied Materials with a deep understanding of how semiconductor process technology evolves. His background in chemical engineering and his years at Bell Labs and Lucent Technologies gave him a technical perspective that few CEOs in the equipment industry could match. Lee saw that the future of semiconductor manufacturing would be defined not just by what happened on the wafer but by what happened between wafers, between chips, and between system components. ESI was a bet on that interconnection-centric future.

The ESI acquisition also revealed the emerging pattern in MKS's strategy. Newport had expanded MKS from vacuum into photonics. ESI extended it further into laser-based manufacturing. Each deal pushed the boundary further along the semiconductor value chain, from process control to tool subsystems to complete manufacturing solutions. The playbook was working, and the debt from both deals was being paid down ahead of schedule.

Then came 2020, and the world changed. The COVID-19 pandemic shut down economies globally, but semiconductor demand surged as remote work, cloud computing, and digital transformation accelerated. The resulting chip shortage laid bare the fragility of the semiconductor supply chain and, paradoxically, elevated the strategic importance of every company in it. Governments from Washington to Brussels to Beijing began pouring billions into domestic chip manufacturing capacity. For MKS, the pandemic served as both validation and catalyst: its products were essential to an industry that the world suddenly realized was essential to everything else.

The combination of soaring demand, government investment, and a heightened awareness of semiconductor supply chain fragility created the perfect backdrop for the most audacious move in MKS's history. The pandemic had also pushed interest rates to near zero, making debt-financed acquisitions tantalizingly cheap. John Lee and his team saw an opportunity to complete the MKS platform with one final piece of the puzzle, and they were willing to bet the company on it.

VI. The Atotech Mega-Deal: Chemistry Enters the Chat (2021-2022)

On July 1, 2021, as the semiconductor industry was riding the highest wave of demand in its history, MKS Instruments announced the most ambitious acquisition in its sixty-year history: the purchase of Atotech, a global leader in specialty process chemicals, equipment, and services for printed circuit boards, semiconductor packaging, and surface finishing. The deal was valued at approximately five point one billion dollars in equity and six point five billion in enterprise value. To put that in perspective, the entire company of MKS was worth roughly seven billion dollars at the time. This was not a tuck-in acquisition or a bolt-on deal. It was not just the largest deal MKS had ever attempted; it was the kind of transaction that redefines a company's identity.

Atotech was itself a storied company with roots stretching back over a century in German industrial chemistry. It had been part of Total S.A., the French energy conglomerate, before being carved out and sold to The Carlyle Group in 2016. Under Carlyle's ownership, Atotech invested in growth, modernized its operations, and went public on the NYSE in early 2021. The business was highly specialized and deeply technical: Atotech's chemists formulated proprietary plating solutions, custom-engineered for specific applications and specific customers, that were consumed in production and continuously replenished. It was, in many ways, the chemical equivalent of the design-in dynamic that MKS understood so well in its vacuum and photonics businesses.

To understand why MKS wanted Atotech, consider what happens after a semiconductor wafer is fabricated. The individual chips must be cut apart, packaged, and connected to circuit boards. The packaging process involves plating copper, gold, nickel, and other metals onto surfaces with microscopic precision. The circuit boards themselves require dozens of electroplating and surface treatment steps. All of this requires highly specialized chemistry, proprietary solutions of metals, acids, and additives formulated to deposit materials at exactly the right thickness, uniformity, and adhesion. Atotech was one of the world's leading suppliers of these chemistries, with over four hundred installed equipment lines and deep relationships with PCB manufacturers and semiconductor packaging houses globally.

The strategic thesis was bold and internally branded as "Optimizing the Interconnect." To understand what that means, think about what a modern electronic device actually is at the physical level. It is not just chips. It is chips connected to other chips, connected to circuit boards, connected to other circuit boards, through billions of microscopic metal pathways. Those pathways, the interconnects, are becoming the bottleneck in electronic performance. It no longer matters how fast a processor can compute if the data cannot get to and from the memory quickly enough. The interconnect is the new frontier, and MKS wanted to own the technology stack that optimized it.

MKS already supplied the lasers that drilled holes in circuit boards (via ESI), the optics and motion systems that positioned those lasers (via Newport), and the vacuum and power equipment used in wafer fabrication (via the legacy business). What it lacked was the chemistry that plated the metal connections running through all of those layers. Atotech filled that gap. For the first time, MKS could offer customers a technology platform that spanned from wafer fabrication through packaging to PCB assembly, encompassing vacuum, photonics, laser processing, and now chemistry.

The deal structure reflected the scale of the ambition. Under the terms, MKS would pay sixteen dollars and twenty cents in cash plus 0.0552 shares of MKS common stock for each Atotech share. The seller was The Carlyle Group, which had taken Atotech public on the New York Stock Exchange earlier in 2021 after acquiring it from Total S.A. in 2016 for approximately three point two billion dollars. Carlyle had done well with Atotech, and MKS was paying a premium for a business that was growing and highly profitable.

The financing was eye-watering. MKS planned to fund the cash portion through a combination of existing cash and new debt commitments from J.P. Morgan and Barclays. At closing, the combined company was expected to carry approximately five point three billion dollars in total debt, with a gross leverage ratio just under four times and a net leverage ratio under three and a half times. For a company that had always prided itself on financial discipline, this was stretching the balance sheet to its breaking point.

Then came the complications. The transaction required antitrust approval from thirteen global regulatory authorities. Twelve granted clearance relatively quickly. The thirteenth, China's State Administration for Market Regulation, known as SAMR, did not. As weeks turned to months, MKS and Atotech withdrew and refiled their regulatory notice to give SAMR additional review time. The parties extended the deal deadline from the original March 2022 to September 2022, and J.P. Morgan and Barclays had to extend their financing commitments accordingly.

Meanwhile, the macroeconomic backdrop was shifting dramatically. When MKS announced the deal in July 2021, the Federal Reserve's benchmark interest rate was near zero and credit markets were flush with cheap money. By the time the deal was nearing closure in mid-2022, the Fed had begun the most aggressive rate-hiking cycle in four decades. Every basis point increase in interest rates translated directly into higher interest expense on the billions of dollars in floating-rate debt MKS was about to take on. The cost of the deal was rising in real time, even as the purchase price remained fixed.

SAMR finally granted unconditional approval on July 28, 2022, and the acquisition closed on August 17, 2022, for approximately four point four billion dollars in cash and MKS common stock.

MKS had its prize. But the financial environment had fundamentally changed between announcement and closing.

The scale of what MKS had attempted was staggering. The combined entity had pro forma revenue of approximately four and a half billion dollars for the twelve months ending June 2022. But it also had over five billion dollars in debt, and the interest rate on that debt was significantly higher than anyone had modeled when the deal was announced thirteen months earlier. MKS management acknowledged the shift candidly, noting that due to higher interest rates and the macroeconomic environment, the company expected the acquisition to be accretive to non-GAAP diluted earnings per share only by fiscal year 2024, not immediately as originally projected.

The market reaction was mixed and evolved over time. When the deal was announced in July 2021, MKS stock initially declined as investors weighed the strategic logic against the financial risk. The semiconductor industry was booming, which made the near-term revenue outlook attractive but also raised the question of whether MKS was buying at the top of the cycle. Atotech itself had only been public since February 2021, when Carlyle floated it on the NYSE. Carlyle had acquired Atotech from Total S.A. in 2016 for approximately three point two billion dollars, invested in growing the business, and was now selling it to MKS for roughly five billion. It was a healthy return for private equity, which cut both ways: it meant MKS was paying a premium for a proven business, but also that the easy gains had already been captured.

Was the Atotech deal bold or reckless? That question would dominate the MKS investment thesis for years. Bulls pointed to the strategic logic: chemistry was the missing piece in MKS's interconnect platform, the consumables business would provide recurring revenue that smoothed cyclical volatility, and advanced packaging was becoming the most important growth driver in the semiconductor industry. They also noted that Atotech's chemistry was deeply embedded in customer manufacturing processes, creating switching costs similar to what MKS enjoyed in its vacuum and photonics businesses. Once a PCB manufacturer qualifies a specific plating chemistry for a production line, changing to a different supplier requires months of process re-qualification, an interruption that most manufacturers simply will not tolerate.

Bears pointed to the debt mountain, the integration risk of entering a business (specialty chemistry) that MKS had no prior experience in, and the timing of taking maximum financial risk at what turned out to be the peak of the semiconductor cycle. They also highlighted the environmental regulatory burden: Atotech's chemical manufacturing operations were subject to stringent environmental regulations across dozens of jurisdictions, a compliance infrastructure that MKS had never had to manage before.

The answer, as it often does, lay somewhere in between. But before MKS could even begin to prove the strategic thesis, it would face an entirely unexpected crisis.

VII. The Debt Hangover and Market Downturn (2022-2024)

On February 3, 2023, barely six months after closing the Atotech acquisition, MKS Instruments suffered a ransomware attack that encrypted business and manufacturing systems across the company.

The timing was almost cruel in its precision. MKS was in the middle of the most complex integration in its history, still learning the specialty chemistry business it had just acquired, and suddenly found itself unable to process orders, ship products, or provide service to customers in its core photonics and vacuum divisions.

The attack forced the company to postpone its fourth-quarter earnings call and scrambled operations for weeks. When the dust settled, MKS estimated the revenue impact at approximately two hundred million dollars in the first quarter of 2023 alone, roughly a twenty percent hit to quarterly revenue. Subsequent investigations revealed that the company had not maintained sufficient IT controls around access authentication, intrusion detection, and backup and restoration systems. A class action lawsuit followed in March 2023, filed in California on behalf of employees whose personal data, including Social Security numbers, bank account information, and health records, had potentially been compromised.

The ransomware episode exposed a vulnerability that many acquisitive technology companies share but few discuss openly: cybersecurity infrastructure often lags behind corporate growth, especially when a company is absorbing multiple businesses in rapid succession. MKS had tripled in size through three major acquisitions in six years, each bringing its own IT systems, security protocols, and legacy architectures. Integrating all of that into a unified, robust cybersecurity framework takes time and investment, and MKS was caught before the work was done.

The ransomware attack was a body blow, but it landed on a company already staggering from macroeconomic headwinds. The semiconductor industry entered a sharp cyclical downturn in the second half of 2022, with memory chip prices collapsing, PC and smartphone demand softening, and semiconductor customers building excess inventory that would take quarters to work through. For MKS, the timing could not have been worse. The company had just taken on more than five billion dollars in debt to acquire Atotech, and now its revenue was declining just as interest payments were rising. It was the kind of perfect storm that tests not just a company's balance sheet but its organizational resilience and the character of its leadership team.

The debt load was genuinely concerning, and it is worth pausing to explain why leverage ratios matter so much in this context. When analysts talk about MKS's gross leverage being "above five times," what they mean is that the company's total debt was more than five times its annual EBITDA, its earnings before accounting for interest, taxes, depreciation, and amortization. To put that in household terms, it is like a family earning one hundred thousand dollars a year carrying a mortgage of five hundred thousand dollars, except that this "mortgage" has variable interest rates that are rising rapidly. At the higher rates prevailing in 2022 and 2023, MKS's annual interest expense alone was hundreds of millions of dollars, consuming a significant portion of the operating cash flow that would otherwise have gone toward investment, dividends, or further debt reduction. Gross leverage spiked above five times in the first quarter of 2024, a level that left the company with limited financial flexibility and kept the credit rating agencies watchful.

The integration challenges went beyond the balance sheet. MKS management acknowledged in regulatory filings that the company had no prior experience in the specialty chemistry industry. Atotech's business operated under highly complex environmental regulations across multiple global jurisdictions, a regulatory framework entirely different from the precision instruments and photonics businesses MKS had operated for decades. The filing language was unusually candid: "Integrating Atotech's business and operations with ours has been and will continue to be complex, challenging and time-consuming."

CEO John Lee and his team responded with the kind of disciplined crisis management that separates companies that survive transformational acquisitions from those that do not. The playbook was multifaceted. On the cost side, MKS implemented workforce reductions, consolidated facilities where the three divisions had overlapping footprints, and renegotiated supplier contracts to capture the purchasing power of the larger combined entity. On the revenue side, the sales teams were reorganized to cross-sell across divisions, so that a customer buying vacuum components could be introduced to photonics solutions, and a PCB customer buying Atotech chemistry could learn about MKS's laser drilling capabilities.

But the most important decision was the relentless focus on debt reduction. Every dollar of free cash flow beyond what was needed for operations and R&D was directed toward paying down the term loan. MKS made a fifty million dollar voluntary prepayment in April 2024 and followed it with a two hundred and sixteen million dollar prepayment in October 2024. In early 2025, another one hundred million dollar prepayment followed. The message to the market was unambiguous: deleveraging was the top priority, and management was committed to restoring the balance sheet to healthier levels even if it meant forgoing share repurchases or other uses of capital in the near term.

The restructuring period also forced MKS to rationalize its organizational structure around the three-division model that had emerged from the acquisitions. The Vacuum Solutions Division, the Photonics Solutions Division, and the Materials Solutions Division each had distinct technology platforms, customer bases, and competitive dynamics. Running them as a unified enterprise while managing billions in debt required a level of operational discipline that tested the entire management team.

Through all of this, MKS continued to invest in research and development. R&D expenses totaled two hundred and eighty-eight million dollars in 2023, up from two hundred and forty-one million in 2022 and two hundred million in 2021. The year-over-year increase in 2023 partly reflected the addition of Atotech's R&D team, but it also represented a deliberate choice to invest through the downturn. Many companies in cyclical industries cut R&D when revenue declines, preserving short-term margins at the expense of long-term competitiveness. MKS chose the opposite path, maintaining investment in new product development and design-win pursuits even as the income statement took the hit. It was a decision that signaled confidence in the long-term thesis and reflected a management team that understood the semiconductor equipment business at a deep level: the design wins you secure during the downturn are the ones that generate revenue for years during the subsequent upcycle. Cutting R&D saves money today but forfeits market position tomorrow.

By the end of 2024, the worst appeared to be over. Full-year revenue came in at approximately three point six billion dollars, roughly flat with 2023 but with improving margins and free cash flow. The semiconductor cycle was showing signs of bottoming, and the advanced packaging trends that had motivated the Atotech deal were accelerating, driven in large part by the explosive growth in artificial intelligence chips that required dense, high-performance interconnections.

The management changes during this period also signaled a pivot from crisis management to growth orientation. Ram Mayampurath joined as CFO in October 2024, bringing experience from Rogers Corporation and fresh perspective on capital structure optimization. James Schreiner returned as COO in 2025, overseeing the Vacuum and Photonics divisions. The leadership team was being reshaped for the next chapter, with a mix of MKS veterans who understood the integration challenges and fresh talent who could bring new approaches to capital allocation and operational efficiency.

The question had shifted from "will MKS survive the debt?" to "how quickly can MKS deleverage and capitalize on the recovery?" It was still an uncomfortable question, but a fundamentally different one. And the early evidence from the first quarter of 2025, with revenue exceeding guidance and free cash flow more than doubling year over year, suggested that the answer might be "faster than the bears expected."

VIII. Modern MKS: The Three-Division Powerhouse (2024-Present)

Walk into any semiconductor fabrication facility in the world, from TSMC's leading-edge fabs in Taiwan to Samsung's plants in South Korea to Intel's expanding operations in Arizona, and MKS technology is everywhere.

Not on the nameplate of the giant lithography scanners or the gleaming deposition chambers. You will not see the MKS logo on the front of any major piece of equipment. But open up those tools, trace the gas lines, follow the power cables, examine the laser modules, and MKS is there. It lives inside those tools and beside them, in the subsystems and materials that make the tools function.

The Vacuum Solutions Division remains the company's largest and oldest business, rooted in the Baratron legacy. It provides the foundational technology stack for semiconductor manufacturing: pressure measurement and control, flow measurement and control, gas and vapor delivery, gas analysis, reactive gas generation, and radio frequency and direct current power delivery. These are not glamorous products. They are the cardiovascular system of a semiconductor tool, the components that ensure gases flow at the right rate, at the right pressure, with the right energy, to deposit or etch materials at atomic-scale precision. The division's customers are the OEMs, the Applied Materials and Lam Researches of the world, who design MKS components into their tools and cannot easily switch them out once qualified.

The Photonics Solutions Division, built on the Newport and ESI acquisitions, offers a range of products that would be recognizable to anyone working in advanced optics: precision lasers from ultrafast femtosecond sources to high-power industrial systems, beam measurement and profiling instruments, optical components, motion control systems, and vibration isolation platforms. Where VSD serves primarily the front end of semiconductor manufacturing, PSD reaches into the back end, where packaging, PCB fabrication, and increasingly, AI-related advanced packaging technologies drive demand.

The Materials Solutions Division, born from Atotech, is the newest and most distinctive of the three. It develops, processes, and manufactures advanced surface modification chemistries, electroless and electrolytic plating solutions, and surface finishing technologies. If vacuum instruments and photonics are the physics of semiconductor manufacturing, Atotech's offerings are the chemistry. The division serves PCB manufacturers, semiconductor packaging houses, and specialty industrial customers with process chemicals that are consumed in production, providing a recurring revenue stream that the capital equipment side of MKS does not naturally generate.

The revenue mix tells the story of a company that has deliberately diversified its exposure. Semiconductor revenue, once the overwhelming majority of sales, now accounts for approximately forty percent of the total. Electronics and packaging contribute about twenty-five percent, with the remainder coming from specialty industrial and other markets. This balance is strategic: when semiconductor capital equipment spending declines in a cyclical downturn, as it periodically must, the chemistry consumables and specialty industrial businesses provide a revenue floor that pure-play equipment companies do not have.

First-quarter 2025 results illustrated the portfolio's strength. Revenue reached nine hundred and thirty-six million dollars, exceeding the high end of company guidance and growing nearly eight percent year over year. Semiconductor revenue contributed four hundred and thirteen million, but the electronics and packaging segment showed significant year-over-year growth, reaching two hundred and fifty-three million as advanced packaging demand accelerated. Non-GAAP gross margin held at a healthy forty-seven percent, and free cash flow of one hundred and twenty-three million dollars was more than double the prior-year quarter. MKS used that cash to make another one hundred million dollar voluntary term loan prepayment and repurchase forty-five million dollars in stock.

In May 2025, the company formally changed its name from MKS Instruments, Inc. to MKS Inc. The "Instruments" designation, perfectly appropriate for a pressure gauge company in 1961, no longer captured the breadth of a three-division enterprise spanning vacuum technology, photonics, and specialty chemistry. The ticker symbol remained MKSI. It was a symbolic moment, but symbols matter. MKS was no longer just an instruments company, and it wanted the market to know it.

The GAAP net income trajectory tells a recovery story in its own right. In the first quarter of 2024, MKS reported just fifteen million dollars in GAAP net income, a figure weighed down by the interest expense on its acquisition debt and the lingering costs of the ransomware recovery. One year later, that figure had more than tripled to fifty-two million. The improvement was driven not by any single factor but by the compounding effect of revenue growth, cost discipline, and steady debt reduction. It was exactly the kind of sequential improvement that management had promised and investors had been waiting for.

The artificial intelligence tailwind is real and substantial. Every advanced AI chip, whether from NVIDIA, AMD, or the growing roster of custom silicon designers at hyperscale cloud companies, requires cutting-edge packaging. High-bandwidth memory, chiplet architectures, and silicon interposers all demand the exact technologies MKS now offers across its three divisions. The company's integrated platform, spanning from the vacuum processes that deposit materials on the wafer to the lasers that drill interconnect vias to the chemistry that plates the copper filling those vias, positions it uniquely for this moment. The AI buildout is not a one-quarter phenomenon; it represents a multi-year capital expenditure cycle that is still in its early innings, and MKS's subsystem and materials revenue stands to benefit throughout.

The management team navigating this moment reflects the company's evolution. John Lee, the MIT-trained chemical engineer who leads the company as CEO, brings deep semiconductor process expertise. Ram Mayampurath, who joined as CFO in October 2024 from Rogers Corporation, brings fresh financial discipline and capital markets experience. Gerald Colella, the former CEO who orchestrated the Newport and ESI acquisitions, continues to serve as Chairman of the Board, providing continuity and institutional memory. And John Bertucci, the man who bought MKS in 1974 and built it into a public company, remains as Chairman Emeritus, a living link to the company's founding era.

The road ahead remains defined by two parallel imperatives: deleverage the balance sheet and invest for growth. As of March 2025, MKS still carried approximately three point two billion dollars in secured term loan principal and one point four billion in convertible senior notes. The net leverage ratio stood at roughly four point two times, well above the company's target. Management has been clear that debt reduction will continue to be the priority, supported by a demonstrated track record of aggressive voluntary prepayments following each major acquisition. The tension between paying down debt and investing for the AI-driven growth cycle is the central operational challenge of this chapter in MKS's story.

IX. The Semiconductor Equipment Ecosystem and Competitive Dynamics

To appreciate MKS's position, you need to understand the semiconductor equipment value chain, which operates like a Russian nesting doll of specialization. Each layer depends on the one below it, and the further down you go, the less visible the companies become, even as they become more essential.

At the top sit the chip designers: NVIDIA, Apple, Qualcomm, AMD. They design the circuits but do not manufacture them. Below them are the foundries: TSMC, Samsung, Intel. They build the chips in fabrication facilities, or fabs, that cost ten to twenty billion dollars apiece.

To equip those fabs, the foundries buy tools from equipment manufacturers: ASML for lithography, Applied Materials for deposition and etch, Lam Research for plasma etch, KLA for inspection and metrology, Tokyo Electron for various process steps. These are the companies that dominate semiconductor equipment headlines, with market capitalizations ranging from tens of billions to over three hundred billion dollars in ASML's case.

MKS operates one level deeper. It builds the subsystems, components, and materials that go inside those tools. When Applied Materials designs a new chemical vapor deposition chamber, MKS supplies the pressure gauges, flow controllers, and RF power supplies that make it work. When ASML integrates a laser source into its lithography system, components from MKS's photonics portfolio may be involved. When a PCB manufacturer plates copper interconnects for an advanced packaging substrate, Atotech chemistry is likely in the bath.

This is the classic "picks and shovels" position, an analogy drawn from the California Gold Rush, where the most reliable fortunes were made not by miners but by the merchants selling them shovels, jeans, and provisions. In the semiconductor gold rush, ASML and Applied Materials are the headline miners, pulling billions in revenue from selling the tools that fabricate chips. MKS is the merchant selling them the critical components that make those tools work.

The advantage of this position is breadth and resilience: MKS does not depend on winning a single process step. It supplies components and materials across dozens of process steps and tool types, so even if one customer loses market share, MKS's revenue from other customers and other tool types provides a buffer. Consider this: when ASML sells a single extreme ultraviolet lithography system for roughly three hundred and fifty million dollars, MKS components inside or adjacent to that system might account for a fraction of one percent of the total price. But they are essential to the system's operation. And MKS is not just in the EUV scanner; it is also in the deposition tools, the etch tools, the metrology systems, and increasingly in the packaging lines downstream. This diversification across the tool landscape creates a revenue base that is structurally more resilient than any single tool maker's.

The limitation is scale and visibility: because MKS operates at the subsystem level, it does not command the same pricing power or investor attention as the tool-level companies. When semiconductor analysts publish their annual forecasts, the headline numbers are wafer fab equipment spending by major categories: lithography, deposition, etch, inspection. MKS's subsystem revenue is embedded within those categories but rarely called out separately, making it an overlooked asset class in the semiconductor investment universe.

The competitive landscape varies by division and is worth examining in some detail.

In vacuum and process control, MKS competes with Advanced Energy Industries in RF power delivery, COMET Group in plasma solutions, Inficon in process monitoring and gas analysis, and Pfeiffer Vacuum in measurement. Advanced Energy is perhaps the most direct competitor, with a strong position in power delivery for semiconductor etch and deposition. The rivalry between MKS and Advanced Energy in the RF power space is one of the most intense in the subsystem world, with both companies investing heavily in next-generation power solutions for advanced process nodes.

In photonics, the competitors include Coherent, the company formed from the merger of II-VI and the original Coherent Corporation, which is a major force in lasers and photonics, as well as IPG Photonics in fiber lasers and Novanta in precision motion. Coherent, with roughly four times MKS's photonics revenue, is the larger player, but its focus is broader, spanning communications, industrial, and aerospace markets.

In materials and chemistry, Element Solutions (through its MacDermid Enthone business) is the primary competitor in plating chemistry. This is the segment where MKS is most clearly a newcomer, and where the integration of Atotech's deep domain expertise is most critical to maintaining competitive position.

What sets MKS apart from any individual competitor is the breadth of its portfolio. No other company spans vacuum, photonics, and chemistry in the semiconductor manufacturing chain. This integration is both MKS's competitive advantage and its strategic risk: the advantage is that it can offer customers consolidated solutions and cross-divisional innovation; the risk is that it must compete credibly against focused specialists in each domain.

The customer concentration dynamic is important and somewhat counterintuitive. MKS's largest customers, Applied Materials, Lam Research, ASML, and the major foundries, are enormous companies with substantial bargaining power. In theory, they could pressure MKS on pricing. In practice, the switching costs work in MKS's favor. Once an MKS subsystem is designed into a tool and the tool is qualified for production in a fab, changing that subsystem is extraordinarily expensive and time-consuming. It requires re-engineering the tool, re-qualifying the process, and potentially disrupting production at the fab. For a subsystem that might represent a fraction of a percent of the total tool cost, the economics of switching are terrible. This is why MKS's customer relationships tend to be measured in decades, not quarters.

The cyclicality question is one that every semiconductor equipment investor must confront. Wafer fab equipment spending is one of the most cyclical line items in the technology sector, swinging by thirty percent or more from peak to trough. MKS is not immune to these cycles, and its VSD and PSD divisions track them closely. But the addition of Atotech's chemistry business has introduced a meaningful countercyclical element. Process chemicals are consumed in production, not purchased as capital equipment. When a fab reduces its capital spending, it does not stop producing wafers, which means it does not stop buying plating chemistry. This consumables dynamic is one of the underappreciated aspects of the Atotech deal and a key reason why MKS's revenue profile may be less cyclical going forward than its history suggests.

There is a myth in the market that MKS is simply a smaller version of Applied Materials or Lam Research. The reality is quite different. Applied Materials and Lam compete with each other for process step wins: who builds the best etch tool, who builds the best deposition tool. MKS does not compete at that level. It competes for the subsystem content inside those tools, regardless of which OEM wins the process step. In a sense, MKS benefits from the competition between OEMs because each new tool platform requires new subsystem qualifications, and MKS's incumbency in the prior generation gives it a significant advantage in winning the next one. This is a fundamentally different competitive dynamic than what the big OEMs face, and it is one reason why MKS deserves to be evaluated as its own category rather than as a derivative of the front-end equipment cycle.

X. Strategic Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding MKS's competitive position requires examining it through two complementary frameworks that any serious investor in the semiconductor supply chain should apply.

Porter's Five Forces illuminates the structural attractiveness of the markets MKS serves, while Hamilton Helmer's Seven Powers framework identifies the sources of durable competitive advantage that could sustain MKS's market position over the long term.

Starting with the threat of new entrants: it is low, and for good reason. Building a credible semiconductor subsystem business requires decades of accumulated engineering expertise, hundreds of millions in R&D investment, and a patent portfolio (MKS holds over seven hundred and fifty patents) that protects key innovations. The capital intensity alone is daunting: MKS spent nearly three hundred million dollars on R&D in a single year, and its installed base of customer relationships took sixty years to build. But the most formidable barrier is not technological or financial. It is the customer qualification cycle. When a semiconductor OEM qualifies an MKS component for a new tool, that qualification process can take one to three years and involves extensive testing in the OEM's development fab. The component must demonstrate reliability over thousands of process cycles, consistency across temperature and pressure ranges, and compatibility with the specific gas chemistries and plasma conditions of the target process. A new entrant would need to persuade an OEM to invest years of engineering time qualifying an unproven component while risking production disruption, all while the OEM's existing MKS component already works perfectly well. The economics simply do not favor new entrants for mission-critical subsystems.

The bargaining power of suppliers is moderate. MKS sources specialized components from a range of suppliers, and its scale, roughly three and a half billion dollars in annual revenue, gives it meaningful purchasing power. However, some key materials, particularly rare earth elements and specialty metals used in Atotech's chemistry business, have concentrated supply chains that can create intermittent pricing pressure.

Buyer power is medium to high in theory but constrained in practice. MKS's customer base is concentrated: the top handful of semiconductor OEMs and foundries account for a significant portion of revenue. These customers have the scale to demand competitive pricing, and they do. But the switching cost dynamic discussed earlier limits their actual leverage. Once designed in, MKS products are sticky. The negotiation tends to occur at the initial design-in phase; after that, the relationship operates more like a partnership than a vendor arrangement.

The threat of substitutes is low for MKS's core offerings. There are no alternative technologies that can replace precision capacitance manometers for vacuum pressure measurement, or RF power delivery for plasma processing, or electroplating chemistry for copper interconnects. These are not products that can be disrupted by a software update or a new material. They are grounded in fundamental physics and chemistry, and the performance specifications required by leading-edge semiconductor manufacturing are so demanding that even incremental improvements require years of development.

Competitive rivalry varies by segment. In RF power, MKS faces direct competition from Advanced Energy, and the two companies compete vigorously on performance, reliability, and price. In photonics, Coherent is a formidable competitor with deeper resources in some product categories. In chemistry, Element Solutions competes for plating business. But MKS's unique positioning as the only company with a portfolio spanning all three domains gives it a competitive angle that none of these focused players can replicate.

Turning to Helmer's Seven Powers, the picture sharpens further. This framework, developed by Hamilton Helmer, asks a more specific question than Porter's: not just whether an industry is attractive, but what specific powers enable a company to sustain persistent differential returns.

Scale economies are present but not the primary driver. MKS has made over twenty acquisitions in the past two decades, spreading fixed R&D costs across a larger revenue base. The three-division structure allows shared corporate functions, and the combined sales force can cross-sell products from all divisions to a common customer base. But semiconductor subsystems are not a winner-take-all business, and scale alone does not create an unassailable advantage.

Network effects are minimal. MKS does not benefit from having more users on a platform or more nodes in a network. This is a product-and-engineering business where value creation comes from technical excellence and customer intimacy, not from network dynamics.

Counter-positioning does not apply in the traditional sense. MKS is the incumbent, not the disruptor. However, there is an argument that MKS's integrated three-division model creates a mild form of counter-positioning against focused competitors. A pure-play vacuum company or a pure-play chemistry company would have to fundamentally restructure its business to match MKS's breadth, and doing so would alienate its existing shareholder base, which values focus. This is not a strong power, but it provides a modest structural advantage.

Switching costs represent MKS's strongest competitive power. The design-in, qualification, and production integration of MKS subsystems into customer tools creates multi-year switching costs that effectively lock in revenue streams once they are established. The cost to a customer of switching away from a qualified MKS component is not just the price of the alternative; it is the cost of re-engineering the tool, re-qualifying the process, and risking production disruption. For a component that costs a few thousand dollars in a tool that costs several million, the calculus overwhelmingly favors staying with MKS.

Branding has limited applicability in MKS's business-to-business context. No consumer has ever chosen a product because of the MKS name. But within the tight-knit semiconductor equipment community, MKS's reputation for reliability, precision, and engineering support matters enormously. Equipment engineers at Applied Materials and Lam Research have worked with MKS products for decades, and that institutional trust is difficult for newcomers to replicate.

Cornered resource is a significant power for MKS. The company possesses deep engineering expertise in vacuum science, photonics, laser processing, and now electrochemistry, accumulated over sixty years. More importantly, it possesses decades of customer process knowledge, an understanding of how its products interact with specific semiconductor processes at specific customers, that would take years for a competitor to develop. This tacit knowledge is embedded in the organization and cannot be easily hired away.

Process power rounds out the picture. MKS's innovation model is deeply integrated with its customer relationships. The company describes it as a flywheel: understanding customer problems leads to inventions, which lead to new product introductions, which lead to design wins, which lead to long-term revenue. The depth of MKS's customer engagement, working alongside OEM engineers during tool development, gives it insight into future technology requirements that competitors operating at arm's length simply do not have.

In aggregate, MKS's durable competitive advantages rest on three primary powers: switching costs that lock in existing revenue, cornered resource in specialized engineering talent and process knowledge, and process power that drives ongoing innovation and design wins. These are not the flashiest moats in the semiconductor ecosystem. They are not the network effects of a software platform or the brand power of a consumer company. But they are remarkably durable, and they explain how a sixty-four-year-old pressure gauge company has remained relevant, and essential, through every generation of semiconductor technology.

A brief myth-versus-reality check is instructive here. The consensus narrative on Wall Street treats MKS as a "levered semi-cap play," essentially a bet on wafer fab equipment spending amplified by acquisition debt. The reality is more nuanced. Yes, MKS is levered. Yes, it correlates with WFE spending. But the addition of the Atotech consumables business, the breadth of the portfolio across vacuum, photonics, and chemistry, and the switching cost dynamics at the subsystem level all argue that MKS is structurally different from how the market prices it. Whether that structural difference is enough to offset the debt risk is the central investment question, but characterizing MKS as simply a levered cyclical play misses the forest for the trees.

XI. Business Model and Strategic Playbook

The MKS business model rests on a strategic architecture that, once you see it, appears almost inevitable in its logic. But it took sixty years and billions of dollars in acquisitions to assemble, and replicating it from scratch today would be nearly impossible. The company has spent decades assembling a portfolio of precision technologies, each of which is critical to a different step in the semiconductor manufacturing process, and then selling that portfolio to a concentrated set of customers who have enormous incentive to minimize their number of qualified suppliers. The genius of the model is that it aligns MKS's interests with its customers': OEMs want fewer, more capable suppliers to reduce procurement complexity and qualification costs, and MKS wants to sell more products to each customer to increase its share of content per tool.

The "Surround the Wafer" strategy, conceived in the early 2000s and refined through each subsequent acquisition, is the organizing principle. In a semiconductor tool, the wafer sits at the center of a complex system of gas delivery, vacuum control, power delivery, optical measurement, and increasingly, chemical processing. MKS has systematically placed its products in as many of these positions as possible. The more positions it occupies, the more integral it becomes to the tool design, and the more difficult it is for any individual competitor to displace it.

The revenue model has three distinct layers, each with different cyclical characteristics and margin profiles.

The base layer is capital equipment sales: when an OEM builds a new tool, it purchases MKS subsystems. This is inherently cyclical, tracking the ups and downs of wafer fab equipment spending.

The second layer is service and upgrades: installed tools require maintenance, calibration, and periodic component replacement, generating recurring revenue that is less cyclical than initial equipment sales. With tens of thousands of MKS subsystems installed in tools around the world, the service revenue base grows with each new tool shipped.

The third layer, added through the Atotech acquisition, is consumables: process chemicals that are used up in production and must be continuously replenished. This consumables business is the least cyclical of the three and the highest in recurring revenue characteristics, which is precisely why MKS paid such a premium for Atotech. Every PCB that gets plated, every semiconductor package that gets surface-treated, consumes Atotech chemistry that must be reordered.

The margin structure reflects the precision engineering that MKS delivers. Non-GAAP gross margins in the range of forty-seven to forty-eight percent are high for a company that manufactures physical products. These are not commodity components. They are precision instruments, laser systems, and specialty chemicals engineered to meet specifications that most industrial companies would consider absurdly demanding. A pressure gauge that must maintain accuracy to within a fraction of a percent across millions of operating cycles. A laser that must drill holes at exactly the right depth and diameter, tens of thousands of times per minute. A plating chemistry that must deposit copper at a uniform thickness measured in nanometers. The precision requirements create natural barriers to cost-based competition and support premium pricing.

Capital allocation under the current management follows a clear hierarchy. First, invest in R&D to maintain technological leadership and generate future design wins. Second, pay down debt aggressively, targeting a net leverage ratio below three times within a defined timeline. Third, return excess cash to shareholders through dividends and opportunistic share repurchases. Fourth, evaluate additional acquisitions, but only after the balance sheet has been restored to health. The discipline of this framework has been tested by the Atotech debt burden, and so far, management has executed according to plan.

The R&D investment is worth highlighting. At two hundred and eighty-eight million dollars in 2023, MKS spent roughly eight percent of revenue on research and development. This is not the highest R&D intensity in the semiconductor equipment ecosystem, ASML spends multiples of that, but it is substantial for a company that had net income well below that figure in the same period. MKS chose to protect R&D spending during the downturn, a decision that reflects management's belief that design wins are the lifeblood of the business. Each design win, where an OEM selects an MKS component for a new tool platform, represents years of future revenue once the tool enters volume production.

What MKS is explicitly not trying to do is become another ASML or Applied Materials. It is not building complete semiconductor tools. It is not competing for the multi-billion-dollar equipment orders that dominate industry headlines. Instead, it is pursuing a subsystem strategy that prioritizes breadth over depth, aiming to be the critical technology partner that every major tool maker relies on. This is a more modest ambition in terms of individual deal size but potentially more durable in terms of competitive positioning. Tool makers come and go. The subsystem supplier that is designed into every tool has a permanence that transcends any single product cycle.

There is an elegant analogy here to the auto industry. Ford and General Motors are household names, but the companies that supply their engines, transmissions, and electronics, companies like BorgWarner, Aptiv, and Continental, often generate more consistent returns with lower volatility. MKS occupies a similar position in the semiconductor ecosystem: less visible, less volatile in absolute terms (though still cyclical), and deeply embedded in the products of companies that get all the attention. The question is whether the Atotech debt has temporarily obscured this fundamental quality or permanently impaired it. The answer will depend on execution over the next two to three years.

XII. Bull versus Bear Case and Investment Framework

The investment debate around MKS centers on a single fundamental question: will the Atotech acquisition prove to be a transformative deal that positions MKS for decades of profitable growth, or will the debt burden and integration complexity weigh on returns for years to come?

Reasonable investors can land on either side of this question, and the honesty with which MKS management has discussed the challenges in its filings, unusual for a company of this size, suggests they understand the stakes as well as anyone.