Markel Group: The Compounding Machine

I. Introduction & The Story Canvas

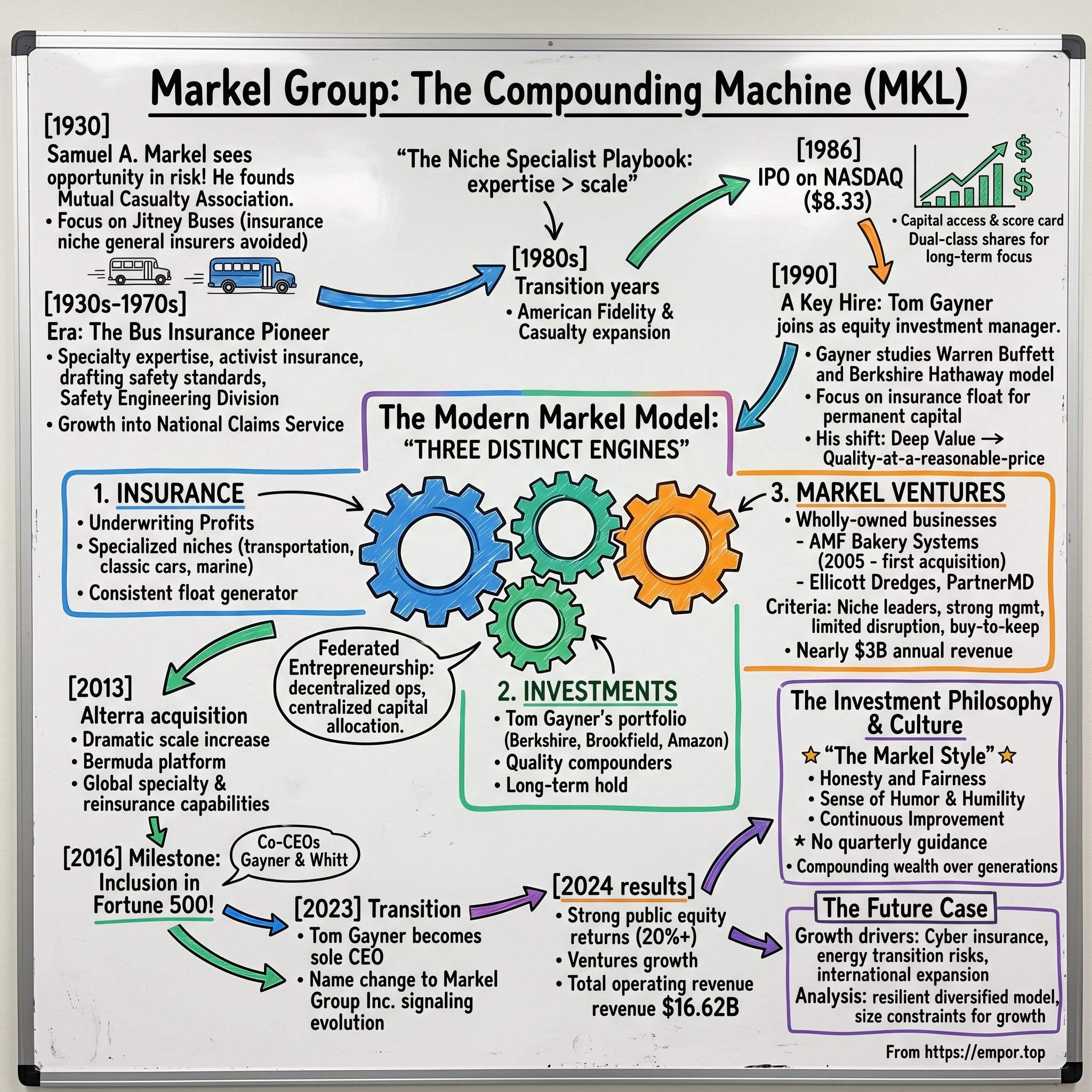

Picture Norfolk, Virginia in 1930. The Great Depression is tightening its grip on America, banks are failing by the thousands, and unemployment is soaring toward 25%. Yet in this economic maelstrom, Samuel A. Markel sees opportunity where others see only risk. The transportation industry—particularly the emerging "jitney" bus services that ferry workers between cities—desperately needs insurance coverage. Traditional insurers won't touch these rickety vehicles with their spotty safety records. Sam Markel will.

He forms the Mutual Casualty Association, then establishes the Mutual Casualty Company. It's a modest beginning for what will become a Fortune 500 conglomerate worth over $20 billion. But here's what makes this story extraordinary: while thousands of insurance companies have come and gone over the past century, Markel has not only survived but transformed itself into something far more ambitious—a compounding machine that rivals Warren Buffett's Berkshire Hathaway in structure, if not yet in scale.

The "mini-Berkshire" comparison isn't casual financial media shorthand. It's a deliberate business model that Markel has methodically constructed over decades. Like Berkshire, Markel generates underwriting profits from its insurance operations. Like Berkshire, it invests those profits and insurance float for the long term in both publicly traded stocks and wholly-owned businesses. And like Berkshire, it's built a culture of permanent capital, patient compounding, and decentralized operations with centralized capital allocation.

Tom Gayner, Markel's CEO and chief investment officer, doesn't shy away from the comparison. He's been attending Berkshire's annual meetings in Omaha since 1990, studying Buffett's playbook while adapting it to Markel's unique strengths. "I am not as smart as Warren Buffett," Gayner once said with characteristic humility. "That guy is world-class. You're looking at a Michelangelo of his era." But Gayner has proven you don't need to be Michelangelo to create something remarkable.

What makes Markel's story unique isn't just its transformation from a regional specialty insurer to a global conglomerate. It's how the company has maintained its entrepreneurial spirit and underwriting discipline while building three distinct engines of value creation: insurance, investments, and Markel Ventures—its collection of wholly-owned businesses ranging from bakery equipment to concierge medicine.

This is a story about compound knowledge as much as compound returns. It's about finding profitable niches that others ignore, then dominating them for decades. It's about building trust relationships that become competitive moats. And it's about the radical idea that in an era of quarterly capitalism, you can still build a business for "now and forever."

The numbers tell part of the story: from that $8.33 IPO price in 1986 to over $1,500 per share today. From writing insurance for a handful of bus operators to insuring everything from offshore oil rigs to classic cars. From zero wholly-owned businesses to a portfolio generating nearly $3 billion in annual revenue through Markel Ventures alone.

But the real story—the one that explains how a regional insurer became a compounding machine—requires understanding the decisions, the culture, and the patient accumulation of advantages that compound just like capital. It's a playbook that's hiding in plain sight, executed over 90 years with remarkable consistency.

As we trace this journey from Sam Markel's first jitney bus policy to today's three-engine conglomerate, we'll see how great businesses aren't built through grand strategic pivots but through thousands of small, smart decisions that compound over time. We'll explore how Markel turned the supposed disadvantage of being smaller than Berkshire into an advantage, finding opportunities in spaces too small for the Omaha giant but too complex for typical insurers.

Most importantly, we'll examine whether Markel's model—proven over nine decades—can continue compounding in an era of technological disruption, climate change, and evolving capital markets. Because while the past is instructive, investors care about the next 90 years, not the last 90.

The roadmap ahead takes us from Depression-era Norfolk to the trading floors of Wall Street, from bakery factories in Richmond to reinsurance markets in Bermuda. It's a story of transformation without losing identity, of growth without sacrificing discipline, and of building something that endures long after its founders are gone.

II. Origins: The Bus Insurance Pioneer (1930-1970s)

The story begins not in a boardroom but on the chaotic streets of 1930s America, where unregulated "jitney" buses—often just modified passenger cars—competed fiercely for riders. These vehicles, named after the slang term for a nickel (the typical fare), represented both entrepreneurial energy and public danger. Accidents were common, insurance was nearly impossible to obtain, and the entire industry teetered between legitimacy and chaos.

Sam Markel didn't just see a business opportunity; he saw a chance to bring order to disorder. His Mutual Casualty Company, founded in Norfolk before relocating to Richmond, didn't simply write policies for these risky vehicles. Markel became an active participant in legitimizing the entire trucking and bus industry. The company helped draft safety standards, trained drivers, and even assisted in passing the National Motor Carrier Act of 1935—landmark legislation that brought federal oversight to interstate trucking and bus operations.

This wasn't passive underwriting; it was activist insurance. Markel's adjusters didn't just process claims—they investigated accidents, identified patterns, and fed insights back to both regulators and operators. The company's Safety Engineering Division, established in the 1950s, became so respected that other insurers hired Markel to provide safety consulting for their own clients. By the 1940s, Markel Service had earned a national reputation for industry-leading claims adjusting and safety engineering.

The transformation of American Fidelity & Casualty, which Markel acquired and built into the largest insurer of truck and bus fleets in the United States by the 1940s, demonstrated the power of specialization. While larger insurers dabbled in transportation coverage as one line among many, Markel lived and breathed it. Claims adjusters knew the difference between a Mack and a Kenworth, understood driver fatigue patterns, and could spot fraudulent claims that generalists might miss.

Sam's four sons—Lewis, Irvin, Stanley, and Milton—joined the business in the 1930s, each bringing different skills. Lewis focused on underwriting discipline, Irvin on sales and relationships, Stanley on operations, and Milton on finance. This wasn't nepotism; it was apprenticeship. Each son spent years learning the business from the ground up, working alongside adjusters, visiting accident scenes, and understanding risk at a granular level.

The niche specialist playbook that would define Markel for decades was taking shape. Find a market that's too risky or too complex for generalists. Develop deeper expertise than anyone else. Use that expertise not just to price risk better, but to actually reduce risk through safety initiatives and industry partnerships. Then compound that advantage over time through reputation and relationships.

By 1951, Markel was confident enough to expand into Canada—not through acquisition but by replicating its specialized approach in a new geography. The 1959 creation of National Claims Service as an independent adjuster further demonstrated Markel's strategy: build expertise so valuable that even competitors will pay for it.

The numbers from this era seem quaint by today's standards—policies measured in thousands of dollars, not millions; a workforce in the hundreds, not thousands. But the foundations were being laid: underwriting discipline, specialized expertise, long-term thinking, and a willingness to invest in making entire industries safer rather than just cherry-picking the best risks.

An internal memo from 1962, discovered in Markel's archives, captures the philosophy: "We do not seek to be the largest insurer of transportation risks. We seek to be the most knowledgeable. Size will follow knowledge, not the reverse." This patient approach—building expertise first, scale second—would prove prescient as the company approached its next major evolution.

The transportation insurance niche also taught Markel crucial lessons about cyclicality. Trucking booms followed economic expansions; busts came with recessions. Oil shocks, regulatory changes, and technological shifts all impacted the industry. Markel learned to maintain reserves during good times, tighten underwriting standards before markets turned, and view downturns as opportunities to gain market share while weaker competitors retreated.

By the late 1970s, Markel had established itself as the go-to insurer for specialized transportation risks. But the family-controlled company faced a crossroads. Staying private meant limited capital for expansion. Going public meant scrutiny, quarterly pressures, and potential loss of the long-term focus that had served them well. The decision they made in 1980 would transform Markel from a successful niche player into something far more ambitious.

III. The Transformation Years: Going Public & Building Scale (1980-1999)

The year 1980 marked a pivotal turn in Markel's evolution. While the company had built a sterling reputation in transportation insurance, management recognized that true scale required access to capital markets. But first, they needed to expand beyond their traditional niche. The founding of Essex Insurance Company in Delaware that year wasn't just geographic expansion—it was strategic repositioning. Essex gave Markel the ability to write excess and surplus lines, the complex, hard-to-place risks that standard insurers wouldn't touch.

Excess and surplus lines represented the perfect adjacent market for Markel's expertise. These weren't commodity risks with standardized pricing; they required deep underwriting knowledge, creative policy structuring, and the confidence to say no to bad business. It was specialty insurance for unusual risks—exactly the kind of market where Markel's analytical culture could shine.

The 1986 IPO at $8.33 per share on NASDAQ wasn't accompanied by fanfare or roadshow excess. The company raised modest capital and maintained family control through dual-class shares. Wall Street barely noticed. Markel's market cap was under $50 million—a rounding error for most institutional investors. But the public listing provided something more valuable than capital: it created a currency for acquisitions and a scorecard for performance.

What happened next would define Markel's trajectory for decades. In 1990, the company made a hire that seemed routine at the time but would prove transformational: Tom Gayner joined as equity investment manager. Gayner wasn't a typical insurance investment officer focused on matching assets to liabilities with boring bonds. He was a value investor who had been studying Warren Buffett's model at Berkshire Hathaway.

"I started going to Omaha in 1990," Gayner would later recall. "I wanted to understand how Buffett had transformed an also-ran textile manufacturer into a compounding machine. The insurance float was key—it provided permanent capital to invest for the long term, not just match short-term liabilities." Gayner saw that Markel, with its consistent underwriting profits and growing float, had the raw materials to build something similar.

The cultural fit was immediate. Markel's leadership—particularly CEO Alan Kirshner and the founding family members still involved—shared Gayner's long-term orientation. They weren't trying to maximize next quarter's earnings; they were building an enduring institution. This alignment, rare in public companies, gave Gayner the freedom to implement a concentrated equity portfolio focused on quality companies at reasonable prices.

Gayner's early investment philosophy evolved significantly during the 1990s. "I used to check the 52-week low list first," he explained in a later interview. "Classic value investing—find the beaten-down stocks and buy them cheap. But I learned that quality matters more than cheapness. Now I check the 52-week high list first. I want to own the companies that are winning."

This shift from deep value to quality-at-a-reasonable-price would define Markel's investment portfolio. Instead of betting on turnarounds or cyclical rebounds, Gayner sought companies with durable competitive advantages, strong management, and long runways for growth. The portfolio became increasingly concentrated in Gayner's best ideas—a stark contrast to the diversified, bond-heavy portfolios typical of insurance companies.

The 1997 move from NASDAQ to the NYSE symbolized Markel's growing ambitions. The company was no longer content being a successful regional insurer; it wanted to compete on the national stage. Premium volume was growing 20-30% annually through a combination of organic growth and small acquisitions. The investment portfolio, under Gayner's management, was compounding at rates that exceeded the S&P 500.

But the real strategic insight came from recognizing that insurance and investments could be more than parallel businesses—they could be synergistic engines. Strong underwriting produced float; float provided capital for investments; investment returns strengthened the balance sheet, allowing for more aggressive underwriting in attractive niches. It was a virtuous cycle, but one that required extreme discipline on both sides.

The discipline was tested during the late 1990s dot-com bubble. While other insurers chased growth at any cost and invested in high-flying tech stocks, Markel stayed true to its principles. Underwriting standards didn't loosen despite competitive pressure. The investment portfolio avoided the most speculative names. "We looked stupid for a while," Gayner admitted. "But looking stupid temporarily is often the price of being smart long-term."

International expansion began in earnest with the 2000 acquisition of Terra Nova Holdings, establishing Markel's presence in the London insurance market—the global center for specialty risks. This wasn't just geographic diversification; London provided access to entirely new categories of risk and relationships with the world's leading brokers and reinsurers. The Terra Nova deal, worth $300 million, was Markel's largest acquisition to date and signaled readiness to play on the global stage.

By the turn of the millennium, Markel had transformed from a regional trucking insurer to a publicly traded, internationally active specialty insurance company with a growing investment portfolio. Revenue had grown from under $100 million in 1986 to over $1 billion by 2000. Book value per share had compounded at 20% annually since the IPO. The foundation was set for an even more dramatic transformation in the decade ahead.

IV. The Gayner Era Begins: Creating the Three-Engine Model (2000-2015)

The new millennium brought both opportunity and challenge for Markel. The dot-com crash vindicated their conservative approach, but it also revealed a limitation: public equities, no matter how carefully selected, were still subject to market volatility. Tom Gayner, now firmly established as Markel's investment chief, began contemplating a radical expansion of the investment mandate.

"I was at the Berkshire meeting in 2004," Gayner recounted, "and Buffett was talking about buying entire businesses versus buying stocks. He said something like, 'When you buy the whole business, you never have to worry about Mr. Market's opinion.' That resonated deeply." But Markel wasn't Berkshire—it didn't have tens of billions in float or Buffett's reputation to attract sellers. They would need to start smaller and build credibility over time.

The opportunity came in 2005 with AMF Bakery Systems, a Richmond-based manufacturer of industrial baking equipment. The company made the massive systems that produce hamburger buns for McDonald's, bread for Wonder, and thousands of other commercial baking applications. It wasn't glamorous, but it was exactly what Gayner was looking for: a profitable, niche business with limited technological disruption risk.

"When I met the CEO of AMF," Gayner explained, "I trusted him and liked him, and the company is in an industry that seemed like it was not going to be technologically disrupted. Bread has been around for thousands of years. People are going to keep eating bread. The equipment might get more efficient, but the basic process isn't changing."

The AMF acquisition, for about $190 million, marked the birth of Markel Ventures. This wasn't a typical insurance company diversification play—buying real estate or opening a bank. This was about permanent capital investing, buying businesses with the intention of owning them forever. No exit strategy, no flip to private equity, no IPO plans. Just compound the earnings and reinvest in the business.

The permanent capital approach proved to be a powerful differentiator in sourcing deals. "Sellers who care about their legacy, their employees, their communities—they love our model," Gayner noted. "We're not going to strip costs, leverage up the balance sheet, and flip the business in three years. We're going to support growth, maintain the culture, and let management run their company."

Deal flow accelerated after AMF proved successful. By 2010, Markel Ventures had acquired several more businesses, each fitting the pattern: profitable niche leaders with strong management who wanted to stay and build. The portfolio included seemingly random businesses—from dredging equipment to retail intelligence services—but each met Markel's criteria for sustainable competitive advantages and consistent cash generation.

The investment philosophy continued evolving during this period. Gayner's public equity portfolio became even more concentrated and quality-focused. Holdings like Berkshire Hathaway, Brookfield Asset Management, and CarMax represented huge positions—sometimes 5-10% of the entire portfolio in a single name. This concentration required conviction but also produced superior returns when the thesis proved correct.

Meanwhile, the insurance operations were hitting their stride. Specialty niches that Markel had cultivated for years—classic cars, motorcycles, special events, professional liability—were producing consistent underwriting profits. The combined ratio, the key measure of insurance profitability, consistently ran below 100%, meaning Markel made money on underwriting alone before counting investment returns.

The 2013 Alterra acquisition transformed Markel's scale overnight. The $3.1 billion deal—by far the largest in company history—added significant reinsurance capabilities and international presence. Alterra brought expertise in property catastrophe reinsurance, a volatile but potentially highly profitable line that required sophisticated modeling and risk management. It also brought Max Capital's Bermuda platform, providing access to the alternative capital markets.

Integration challenges were real. Alterra's culture was more aggressive, more trading-oriented than Markel's patient underwriting approach. Some key executives departed. Some business lines proved incompatible with Markel's risk appetite. But the strategic logic held: Markel now had the scale and breadth to compete for the largest, most complex risks in the global insurance market.

By 2015, the three-engine model was fully operational. Insurance operations generated consistent underwriting profits and growing float. The investment portfolio, now over $5 billion, produced steady returns from both equities and fixed income. Markel Ventures, with over a dozen companies, contributed nearly $1 billion in revenue and growing cash flow. Each engine reinforced the others, creating a compounding machine that could weather any single market downturn.

The numbers validated the strategy. Book value per share had grown from $139 in 2000 to over $500 by 2015—a compound annual growth rate of nearly 9% through a period that included both the dot-com crash and the global financial crisis. Total returns to shareholders exceeded 400% over the same period, dramatically outperforming both the S&P 500 and insurance industry indices.

But perhaps more importantly, Markel had proven that the Berkshire model could be replicated at smaller scale. You didn't need $100 billion in float to make permanent capital investing work. You didn't need Warren Buffett's genius to generate superior returns. You needed discipline, patience, and the courage to look different from your peers. As Gayner often said, "We're not trying to be Berkshire. We're trying to be the best version of Markel."

V. Markel Ventures: Building the Industrial Empire (2005-Present)

Inside a nondescript industrial building in Richmond, massive machines shape dough into perfect hamburger buns at a rate of 10,000 per hour. This AMF Bakery Systems facility doesn't just represent Markel's first Ventures acquisition—it embodies the entire philosophy: unsexy businesses with moats so deep that even Amazon can't disrupt them. After all, nobody's downloading bread from the internet.

The Markel Ventures strategy crystallized around a simple but powerful insight: owning 80-100% of a good business beats owning 0.01% of a great one. "When you own the whole thing," Gayner explained, "you control capital allocation, you set the culture, and you never have to worry about what the stock market thinks." This permanent capital model attracted a specific type of seller—successful entrepreneurs who had built something valuable and wanted to preserve it.

The acquisition criteria became almost formulaic in its discipline. Positive cash flow from day one—no turnarounds, no "story stocks" that might work out someday. Management that wanted to stay and run the business—no forced retirements or integration plays. Industries with limited disruption risk—no cutting-edge technology or fashion-dependent consumer products. And perhaps most importantly, businesses small enough that Berkshire wouldn't compete but large enough to matter to Markel's results.

By 2010, the Ventures portfolio had expanded beyond AMF to include Ellicott Dredges (marine dredging equipment), Ancon Constructors (commercial construction), and that harbinger of luxury leather handbags, Brahmin. Each business operated independently, maintaining its own culture and management structure, but with access to Markel's capital for growth investments.

The deal sourcing evolved into a surprisingly personal process. "Literally half of our deals have come about through person-to-person contact, with no intermediaries," the Ventures team revealed. These weren't auction processes with investment bankers maximizing price. They were negotiated transactions where sellers chose Markel for reasons beyond the highest bid: cultural fit, employee protection, and the promise of permanent ownership.

PartnerMD, acquired in 2011, exemplified this approach. The concierge medicine provider offered high-touch healthcare to affluent clients—a business model with tremendous unit economics but capital requirements for expansion. Under Markel's ownership, PartnerMD expanded from two locations to twelve, maintaining its premium positioning while achieving scale economies. The founders remained involved, employees kept their jobs, and patients noticed no change except more locations.

The construction and engineering cluster developed organically. After Ancon's success, Markel acquired Metromont (precast concrete), Cottrell (forestry equipment), and several related businesses. These weren't random acquisitions but strategic additions that could share best practices, refer customers, and achieve purchasing synergies without formal integration. It was federated entrepreneurship—independent businesses learning from each other.

By 2016, Markel Ventures had grown from one company generating $190 million in revenue to over 15 businesses producing $1.2 billion. The cash flow from these businesses provided another source of capital for both insurance and investments, creating a fourth leg to the Markel stool. Operating income from Ventures reached $100 million annually, contributing meaningfully to Markel's overall profitability.

The portfolio's diversity seemed random to outsiders—what connected bakery equipment to handbags to healthcare? But the thread was consistent: businesses with sustainable competitive advantages operating in stable industries with long-term growth potential. As one analyst noted, "Markel Ventures looks like a random collection until you realize they're all mini-monopolies in their niches."

The 2018 acquisition of Brahmin highlighted both the opportunity and challenge of the model. The luxury handbag company had a devoted customer base and 30% operating margins but faced questions about relevance with younger consumers. Markel provided capital for digital marketing and new product development while maintaining the brand's premium positioning. Sales grew, margins expanded, but the business required more active management than industrial acquisitions.

Recent additions have pushed into new territories while maintaining discipline. Metromont's $1 billion revenue made it the largest Ventures acquisition ever. The company's precast concrete systems for data centers, warehouses, and institutional buildings benefited from the construction boom while maintaining pricing power through specialized expertise. It also demonstrated Markel's ability to acquire and manage increasingly large businesses.

The Ventures portfolio today encompasses 21 companies across industries including fire suppression, concierge medicine, construction, technology consulting, decorative plants, and yes, those leather handbags. Ten are based in the Richmond region, creating an informal hub of entrepreneurial activity. Combined revenue approaches $2.8 billion annually, making Ventures a substantial business in its own right.

The returns have validated the strategy. While Markel doesn't break out detailed Ventures returns, operating income has grown from near zero in 2005 to over $200 million today. More importantly, these businesses provide stable, predictable cash flows uncorrelated with insurance cycles or stock market volatility. They're the ballast that allows Markel to take risks elsewhere.

But the real value might be intangible. Markel Ventures has created a reputation as the buyer of choice for successful private companies. The pipeline of potential acquisitions grows stronger each year as word spreads through entrepreneurial networks. Former sellers become references for new deals. The Ventures CEOs form an informal advisory network, sharing insights across industries.

"We're building profitable enterprises that will endure as part of the broader Markel Corporation," the Ventures mission states. Endure is the key word. These aren't portfolio companies to be optimized and exited. They're permanent additions to the Markel family, expected to compound value for decades. It's a radically long-term approach in an increasingly short-term world.

VI. The Modern Era: Fortune 500 Status & Beyond (2016-Present)

The transition to co-CEOs in 2016 could have been a disaster. Corporate history is littered with failed power-sharing arrangements, ego clashes, and strategic paralysis. But when Tom Gayner and Richard Whitt III assumed joint leadership of Markel, they brought complementary skills that actually worked: Gayner's investment acumen and capital allocation expertise paired with Whitt's deep insurance knowledge and operational discipline.

That same year, Markel achieved a symbolic milestone: inclusion in the Fortune 500 for the first time. The company Sam Markel started insuring jitney buses had joined America's corporate elite. But rather than rest on this achievement, leadership accelerated the transformation. International expansion continued with new insurance platforms in Europe and Asia. Markel Ventures pursued larger acquisitions. The investment portfolio concentrated even further into Gayner's highest-conviction ideas.

The co-CEO structure evolved naturally over the next seven years. Whitt focused on insurance operations, driving underwriting discipline and expanding into new specialty niches. Gayner managed investments and Ventures while serving as Markel's public face at conferences and investor meetings. The division of labor worked because both executives shared the same long-term philosophy and trusted each other completely.

By 2023, the arrangement had run its course. Whitt retired, and Tom Gayner became sole CEO—a role he hadn't originally sought but accepted as natural evolution. "Richard and I built something together that neither could have built alone," Gayner reflected. "Now it's time for the next chapter." That chapter included a subtle but significant change: Markel Corporation became Markel Group Inc., signaling the evolution from a single company to a collection of businesses.

The Berkshire investment saga of 2022-2023 provided both validation and mystery. When Warren Buffett's company bought 467,000 Markel shares in early 2022—worth about $600 million—it seemed like the ultimate endorsement. The student had impressed the teacher. Markel stock jumped on the news, with investors speculating about deeper partnerships or even acquisition.

But by year-end 2023, Berkshire had sold its entire position. Gayner's response was cryptically diplomatic: "We were honored by the investment. Warren called it a 'Good Housekeeping Seal of Endorsement.' There were other things going on that made the timing not ideal." Those "other things" remained unspecified, fueling speculation about everything from valuation concerns to regulatory issues to simple portfolio rebalancing.

The modern Markel operates at a scale unimaginable in its early decades. Total revenues exceed $14 billion annually. The investment portfolio has grown to $9.5 billion, with stakes in 127 companies including, ironically, a significant position in Berkshire Hathaway itself. Markel Ventures contributes nearly $3 billion in revenue. The insurance operations write premiums across dozens of specialty lines in markets worldwide. The latest 2024 results validate the model's durability. Total operating revenue reached $16.62 billion for the year ended December 31, 2024, up from $15.80 billion a year earlier, with the public equity portfolio returning over 20% in 2024. "In 2024, we exceeded our target with strong returns from our public equity portfolio, continued growth in Ventures, and notable performance in many areas of our insurance business," Gayner noted, adding that "Over the past two years, Markel Group has made significant strides in improving accountability, capital allocation, and leadership".

The investment portfolio's composition reflects Gayner's evolution as an investor. The largest holdings read like a who's who of quality compounders: Berkshire Hathaway (the student owning the teacher), Brookfield Asset Management, Amazon, Google, and Microsoft. But there are also concentrated bets on less obvious names where Gayner sees underappreciation—companies like AutoZone, Home Depot, and Moody's that dominate their niches with expanding moats.

Recent Ventures acquisitions demonstrate continued discipline despite larger scale. In June 2024, Markel acquired 98% of Valor Environmental, an environmental services company providing erosion control services to commercial development sites. In September 2024, they acquired a 68% ownership interest in Educational Partners International, a company that sponsors international teachers for U.S. school placements, with consolidation beginning in Q1 2025 after regulatory approvals.

The geographic footprint has expanded dramatically from those early days in Norfolk. Insurance operations span six continents, with particular strength in London's specialty markets, Bermuda's reinsurance sector, and growing Asian operations. Markel Ventures, while concentrated in the United States, includes international operations through portfolio companies. The investment portfolio is globally diversified, though still U.S.-centric reflecting the depth of American capital markets.

Technology adoption, a potential Achilles heel for traditional insurers, has become a competitive advantage. Markel's underwriting platforms use sophisticated modeling for catastrophe exposure, machine learning for claims prediction, and digital distribution for certain product lines. But technology serves the business model rather than driving it—the company still believes in human underwriters making judgment calls on complex risks.

The leadership team today blends Markel veterans with outside expertise. Jeremy Noble, who leads insurance operations, joined from Zurich Insurance with a mandate to improve underwriting profitability. The Ventures team includes former private equity professionals who understand both deal-making and operations. The investment team remains surprisingly small—just a handful of analysts supporting Gayner—reflecting the concentrated, long-term approach.

Corporate governance has evolved with scale while maintaining founder principles. The dual-class share structure that preserved family control has been simplified. Board composition includes more independent directors with diverse expertise. Executive compensation emphasizes long-term value creation over quarterly targets. The "Markel Style"—that cultural document emphasizing integrity, customer focus, and long-term thinking—remains the north star.

But challenges exist beneath the success. Insurance pricing cycles have compressed, making consistent underwriting profits harder to achieve. Natural catastrophes are increasing in frequency and severity—the company estimates losses of $90-130 million from the January 2025 Los Angeles wildfires alone. Competition for Ventures acquisitions has intensified as private equity firms flood the middle market with capital. And the sheer size of the investment portfolio makes outperformance increasingly difficult.

The question facing Markel today isn't whether the model works—nine decades of compounding have proven that. It's whether the model can continue working at current scale in a rapidly changing world. Can a $20 billion market cap company find enough attractive investments to deploy capital effectively? Can specialty insurance maintain pricing power as technology democratizes risk assessment? Can Markel Ventures continue acquiring quality businesses at reasonable prices when competing against trillion-dollar private equity funds?

Gayner remains optimistic, pointing to the structural advantages of permanent capital, patient culture, and diversified earnings streams. "We're not trying to shoot the lights out every quarter," he emphasizes. "We're trying to compound wealth over generations. That long-term focus is our edge in a short-term world."

VII. The Investment Philosophy & Culture

Walk into Markel's Richmond headquarters and you won't find the marble lobbies or modern art collections typical of financial institutions. Instead, there's a understated Southern gentility—comfortable chairs, warm lighting, and framed copies of "The Markel Style" throughout the building. This document, less than a page long, has guided the company since the 1980s and reads more like a personal creed than corporate mission statement.

"Honesty and fairness are at the heart of our business," it begins. "We work hard to do the right thing for our customers, associates, and shareholders." Simple words, but in an industry plagued by conflicts of interest and short-term thinking, they represent radical commitment. The Style continues with principles like "pursuing excellence and continuous improvement" and "having a sense of humor and humility." Try finding that last one in a typical corporate values statement.

This culture manifests in tangible ways. Markel doesn't provide quarterly earnings guidance—heresy on Wall Street but consistent with long-term focus. Executive compensation emphasizes five-year performance over annual bonuses. The company has never had layoffs driven by quarterly earnings misses. Even during the 2008 financial crisis, when peers were slashing headcount, Markel maintained its workforce and invested for the recovery.

Tom Gayner embodies this philosophy in his investment approach. Unlike Buffett's concentrated mega-bets, Gayner maintains a more diversified portfolio—typically 100+ positions versus Berkshire's top-ten concentration. "I am not as smart as Warren Buffett," he explains with characteristic humility. "That guy is world-class. You're looking at a Michelangelo of his era. I need more shots on goal to achieve similar results."

But the philosophy shares Buffett's core tenets: buy quality businesses, hold for the long term, and let compounding work its magic. Gayner's evolution from checking 52-week lows to checking 52-week highs reflects hard-won wisdom. "Cheap stocks are usually cheap for good reasons," he learned. "Great businesses temporarily marked down are much better investments than mediocre businesses at bargain prices."

The capital allocation framework operates like a three-dimensional chess game. Insurance profits fund investments. Investment returns strengthen the balance sheet for more aggressive underwriting. Ventures acquisitions provide permanent homes for family businesses. Each piece reinforces the others, creating resilience that no single-engine model could match.

Decentralization with centralized capital allocation—borrowed directly from Berkshire—proves especially powerful. Insurance units operate independently, competing for capital based on returns. Ventures companies maintain their own cultures and management teams. Only major capital decisions flow to Richmond. This structure combines entrepreneurial energy with disciplined resource allocation.

The patience embedded in Markel's culture shows in holding periods. The average stock position has been owned for over seven years. Several Ventures companies have been in the portfolio for over a decade. Insurance relationships span generations. This isn't buy-and-hold as passive strategy; it's active patience—constantly monitoring but rarely trading.

Consider how Markel handled the COVID-19 pandemic. While competitors panicked about event cancellation claims and business interruption lawsuits, Markel took a measured approach. They paid legitimate claims promptly, fought unreasonable ones, and used the disruption to gain market share in abandoned niches. The investment portfolio held steady through the March 2020 crash. Ventures companies received support for working capital without pressure for immediate returns.

Leadership development reflects long-term thinking. Potential CEOs spend decades in the organization, rotating through different roles. Jeremy Noble ran international operations before taking over all insurance. Ventures presidents often serve on other portfolio company boards, sharing expertise. This internal cultivation ensures cultural continuity—crucial when your competitive advantage is patience in an impatient world.

The cultural elements that seem soft actually drive hard results. That emphasis on "honesty and fairness" means Markel's loss reserves prove consistently accurate—no "surprise" additions that plague aggressive underwriters. The "sense of humor and humility" keeps the company from betting-the-farm trades that destroy capital. "Continuous improvement" drives operational excellence without disrupting what works.

Building for "now and forever"—another Markel phrase—requires different metrics. Success isn't measured in quarterly earnings beats but in decades of compound growth. Not in relative performance versus peers but in absolute wealth creation. Not in size but in quality. This patient scorecard attracts like-minded shareholders who become partners in compound value creation rather than traders seeking quick gains.

The culture also attracts talent differently. Markel doesn't pay Wall Street compensation packages—no eight-figure bonuses or carried interest arrangements. Instead, it offers something rarer: the opportunity to build something enduring. Employees describe a collegial, intellectually stimulating environment where good ideas matter more than political maneuvering. Turnover remains remarkably low for a financial services company.

Risk management in this culture means something different too. It's not about complex models or value-at-risk calculations—though Markel has those. It's about asking "What could go wrong?" before every major decision. It's about maintaining conservative reserves even when competitors are releasing them for earnings. It's about walking away from profitable business that doesn't feel right. As one senior executive put it, "We'd rather explain why we didn't write bad business than why we did."

The Markel Style scales because it's principles-based rather than rules-based. New acquisitions don't get 500-page integration manuals; they get the one-page Style document and trust to implement it appropriately. This flexibility allows diverse businesses to maintain their uniqueness while sharing core values. A bakery equipment manufacturer and a handbag designer can both embody the Markel Style in their own ways.

VIII. Playbook: The Markel Method

The failure rate among companies attempting to replicate Berkshire Hathaway's model approaches 100%. Leucadia tried and eventually liquidated. Alleghany succeeded modestly before selling to Berkshire itself. Dozens of smaller attempts have flamed out spectacularly. Why does Markel succeed where others fail? The answer lies not in copying Berkshire but in adapting its principles to different circumstances.

Start with insurance as the funding engine. Most insurers treat investment income as subsidy for underwriting losses—they'll write business at 105% combined ratios expecting investment returns to generate profit. Markel does the opposite. Every insurance division must produce underwriting profits independently. Investment income is bonus, not baseline. This discipline means Markel can walk away from price wars that devastate competitors chasing premium growth.

The specialty focus provides structural advantages. You can't comparison shop for classic car insurance on Progressive's website. There's no commoditized market for insuring Comic-Con or covering errors and omissions for architectural firms. These niches require expertise that takes years to develop and relationships that span decades. Once Markel becomes the go-to insurer for a specialty, displacement is nearly impossible.

Consider the permanent capital advantage in Ventures. When Markel buys a business, sellers know three things: their company will never be flipped, employees won't face private equity-style cost cutting, and patient capital will fund growth investments. This certainty attracts sellers who care about legacy—often accepting lower prices from Markel than financial buyers offer. It's competitive advantage through values alignment.

The approach to acquisitions differs radically from typical corporate development. Recent deals like Valor Environmental and Educational Partners International weren't found through investment banker auctions. Half come through personal relationships—a board member knows a business owner, a Ventures CEO suggests a peer, a longtime shareholder makes an introduction. These warm leads produce better cultural fits and more reasonable valuations than competitive processes.

Decentralized operations with centralized capital allocation sounds simple but proves extraordinarily difficult to execute. The temptation to meddle, to impose corporate "synergies," to standardize operations becomes overwhelming as companies scale. Markel resists. Ventures companies don't share back-office functions. Insurance units maintain separate underwriting systems. This seeming inefficiency preserves entrepreneurial energy and accountability.

The patient, opportunistic growth strategy means Markel doesn't have five-year plans or acquisition targets. They wait for opportunities then move decisively. The 2013 Alterra acquisition happened because the target became available at an attractive price, not because strategic planning demanded a reinsurance platform. This flexibility allows Markel to exploit market dislocations rather than forcing deals to meet arbitrary timelines.

Building compound knowledge matters as much as compound returns. Every failed underwriting experiment teaches lessons. Every successful Ventures acquisition reveals patterns. Every investment mistake refines the process. This accumulated wisdom—embedded in people and processes rather than manuals—creates competitive moats that money can't buy.

The concentration versus diversification balance reflects pragmatic adaptation rather than dogmatic ideology. Gayner concentrates the equity portfolio enough to matter—top ten holdings often represent 40-50% of the portfolio—but diversifies enough to survive mistakes. Insurance operates in dozens of niches rather than betting on a few lines. Ventures spans unrelated industries. This "focused diversification" provides both upside potential and downside protection.

Managing through cycles requires counter-cyclical courage. During hard insurance markets, when premiums spike and everyone chases growth, Markel maintains underwriting discipline. During soft markets, when competitors retreat, Markel selectively expands. In bull markets, the investment portfolio becomes more conservative. In crashes, Gayner deploys capital aggressively. This contrarian timing, easier said than done, drives long-term outperformance.

The 2008 financial crisis provided the ultimate test. Insurance claims spiked as businesses failed. Investment portfolios crashed. Credit markets froze, preventing refinancing. Many insurers needed bailouts or faced bankruptcy. Markel not only survived but thrived—maintaining underwriting standards, selectively adding to beaten-down equity positions, and emerging stronger as competitors retreated.

COVID-19 offered different challenges but similar responses. Event cancellation insurance produced massive claims. Business interruption lawsuits threatened billions in potential losses. Markets whipsawed between pandemic panic and stimulus euphoria. Markel's response: pay legitimate claims promptly, fight unreasonable ones vigorously, support Ventures companies without demanding immediate returns, and maintain investment discipline despite volatility.

The power of the model compounds over time. Insurance float grows with premium volume. Investment returns compound tax-efficiently. Ventures companies reinvest earnings for growth. Each engine reinforces the others, creating a flywheel effect that accelerates with scale. A dollar of insurance float becomes two dollars of investment gains becomes four dollars of book value over time.

But the playbook requires rare ingredients: patient capital willing to accept volatility, management with true long-term orientation, and culture that resists quarterly capitalism's pressures. It also requires scale—you need billions in float to make the investment engine meaningful, dozens of Ventures companies to diversify risk, and global insurance operations to access attractive niches.

The paradox is that success makes replication harder. As Markel grows larger, it needs bigger acquisitions to move the needle. As its reputation spreads, competition for deals intensifies. As the investment portfolio expands, finding meaningful positions becomes challenging. The playbook that worked at $1 billion market cap requires adaptation at $20 billion.

Yet the fundamental insight remains valid: patient capital compounds faster than impatient capital. Permanent ownership attracts better businesses than temporary ownership. Underwriting discipline beats premium growth. Culture beats strategy. These principles, properly executed, create value regardless of scale. The challenge is maintaining execution as complexity increases and founders fade.

IX. Analysis & Investment Case

The bull case for Markel starts with math: a company that has compounded book value at 11% annually for decades, trades at 1.3 times book value, and operates three uncorrelated engines of value creation. In a world of 5% treasury yields and 20+ P/E multiples for the S&P 500, Markel offers compelling risk-adjusted returns for patient investors. The current valuation metrics look compelling. The current price to book ratio for Markel Group as of August 01, 2025 is 1.41, and with Markel Group book value per share for the three months ending December 31, 2024 was $1,325.68, the stock trades at a reasonable multiple to its tangible book value. This compares favorably to historical averages and suggests the market isn't fully appreciating the three-engine value creation model.

The diverse income streams provide resilience that single-line competitors lack. When insurance markets soften, investment returns compensate. When equity markets crash, insurance operations generate cash. When both struggle, Ventures provides stable earnings. This diversification isn't random—it's architected to provide multiple ways to win regardless of market conditions.

"In 2024, we exceeded our target with strong returns from our public equity portfolio, continued growth in Ventures, and notable performance in many areas of our insurance business, all while staying true to our values and striving for excellence," said Tom Gayner, Chief Executive Officer of Markel Group. "Over the past two years, Markel Group has made significant strides in improving accountability, capital allocation, and leadership. As we continue to build on this progress, we are committed to enhancing our insurance performance and driving profitable growth across our entire family of businesses."

The bear case centers on three concerns: size constraints, succession risk, and market cycles. At $20 billion market cap, Markel needs increasingly large deployments to move the needle. A $200 million Ventures acquisition barely impacts results. The equity portfolio requires billion-dollar positions for meaningful contribution. Insurance growth requires entering larger, more competitive lines.

Succession represents the elephant in the room. Tom Gayner is 63, with no clear heir apparent. While he shows no signs of slowing down, investors remember what happened to other "mini-Berkshires" after founder transitions. Leucadia never recovered from the Cumming-Steinberg era ending. Loews struggles to maintain relevance post-Tisch. Can Markel's culture survive a leadership change?

Market cycles pose increasing challenges. The insurance industry faces structural headwinds: climate change driving catastrophe losses, technology commoditizing risk assessment, and alternative capital compressing returns. The equity markets trade at elevated valuations, limiting future return potential. Private equity competition makes Ventures acquisitions increasingly expensive.

Competitive positioning versus peers reveals both strengths and weaknesses. Against pure-play insurers like Progressive or Chubb, Markel's diversification provides stability but potentially lower growth. Versus Berkshire, Markel offers more growth potential but less proven management depth. Against newer "Berkshire clones" like Constellation Software, Markel has longer history but perhaps less innovative culture.

The valuation framework requires summing three distinct parts. Insurance operations, generating roughly $12 billion in premiums, deserve perhaps 1.2x book value—typical for specialty insurers with consistent underwriting profits. The investment portfolio, at $9.5 billion, should trade near market value given Gayner's track record. Ventures, producing $200+ million in operating income, might warrant 15-20x earnings multiple—suggesting $3-4 billion value.

Sum-of-parts analysis suggests fair value around $22-25 billion versus today's $20 billion market cap—modest but not compelling upside. However, this static analysis misses the dynamic value creation from the three-engine model. The compounding effect, where each engine reinforces the others, creates value beyond simple addition. Analyst price targets reflect measured skepticism. MKL's current price target is $1,820.33, with Based on 2 Wall Street analysts offering 12 month price targets for Markel in the last 3 months. The average price target is $1,836.00 with a high forecast of $1,836.00 and a low forecast of $1,836.00. The average price target represents a -8.50% change from the last price of $2,006.57. The consensus rating sits at "Hold" or "Moderate Buy," suggesting analysts see limited near-term upside but recognize the quality of the franchise.

Key metrics to watch include the combined ratio staying below 100% (currently around 95-96%), Ventures operating income growth (targeting double-digit expansion), and investment portfolio returns relative to the S&P 500. Book value per share growth, the ultimate scorecard, should compound at high single digits minimum to justify the premium valuation.

The investment case ultimately depends on time horizon. For traders seeking quick gains, Markel offers little appeal—the stock can go nowhere for years during consolidation phases. For patient investors willing to hold for a decade or more, Markel provides exposure to a proven compounding machine with multiple ways to win. It's not about beating the market every year; it's about building wealth over generations.

X. Power & Lessons

The sources of Markel's competitive power aren't immediately obvious. Unlike tech monopolies with network effects or pharmaceutical companies with patents, Markel's advantages seem prosaic: underwriting discipline, patient capital, decentralized operations. Yet these mundane elements combine to create something more powerful than their parts.

Network effects do exist, just not in the traditional sense. Every successful Ventures acquisition makes the next one easier—sellers reference-check with prior owners who become evangelists. Every specialty insurance niche Markel dominates creates relationships that spawn opportunities in adjacent niches. Every year of consistent underwriting profits builds trust with brokers who direct business Markel's way. It's a reputation network effect, building slowly but durably over decades.

Scale economies manifest differently than in manufacturing. Markel doesn't achieve lower unit costs through volume. Instead, scale provides diversification that enables risk-taking in any single area. A $20 billion company can absorb a failed Ventures acquisition or catastrophic insurance loss that would cripple a smaller competitor. This resilience allows aggressive moves during market dislocations when others retreat.

Counter-positioning through permanent capital represents Markel's most underappreciated advantage. Private equity firms, Markel's main competition for Ventures deals, must exit investments within 5-7 years to return capital to limited partners. Public company acquirers face quarterly earnings pressure and activist investors demanding synergies. Markel offers something neither can match: true permanent ownership with no exit pressure. This positioning attracts a specific seller segment that values legacy over price.

The trust advantage in deal sourcing compounds invisibly. CEOs who sell to Markel often serve as informal advisors, introducing other potential sellers. Ventures executives cross-pollinate ideas between portfolio companies. Insurance brokers who've worked with Markel for decades steer complex risks their way. This trust network, built through thousands of kept promises, can't be replicated with capital alone.

Building multi-generational wealth through patience sounds simple but proves extraordinarily difficult in practice. The temptation to chase hot sectors, leverage up returns, or maximize short-term earnings becomes overwhelming. Markel has resisted these pressures for 90 years, maintaining discipline when peers abandoned it. This patience isn't passive—it's active waiting, preparing for opportunities that compound knowledge and relationships create.

The paradox of independence and integration defines Markel's organizational model. Business units operate independently, maintaining entrepreneurial energy and accountability. Yet they share capital allocation, cultural values, and informal knowledge networks. It's federation, not empire—a structure that preserves local advantages while capturing global benefits.

Culture truly is strategy at Markel, though saying so risks sounding trite. The Markel Style isn't just words on paper; it's embedded in hiring decisions, compensation structures, and daily operations. When underwriters walk away from profitable but risky business, when Gayner holds positions through brutal drawdowns, when Ventures supports struggling companies without demanding immediate returns—that's culture translating into competitive advantage.

The power of compound knowledge deserves special emphasis. Every insurance claim teaches risk patterns. Every investment mistake refines the process. Every Ventures acquisition reveals operational insights. This accumulated wisdom, stored in people and processes rather than databases, creates an appreciating asset that doesn't appear on balance sheets but drives superior returns.

Markel demonstrates that sustainable competitive advantages don't require breakthrough innovation or monopolistic positions. Patient capital, disciplined execution, aligned culture, and compound learning can create durable moats. These advantages seem replicable in theory but prove nearly impossible to copy in practice—the very definition of competitive power.

The lessons for investors extend beyond Markel itself. Look for businesses with multiple reinforcing advantages rather than single dominant moats. Value culture and incentive alignment as much as financial metrics. Recognize that the best investments often look boring—insurance, bakery equipment, dredging machines—not exciting. And above all, extend your time horizon; the biggest winners require patience that few possess.

For business builders, Markel offers a different model than Silicon Valley disruption or Wall Street financial engineering. Build slowly but steadily. Choose permanent relationships over transactional wins. Create structures that preserve entrepreneurial energy while capturing scale benefits. And resist the quarterly capitalism treadmill that destroys long-term value creation.

The ultimate lesson might be that in a world obsessed with disruption, there's enormous value in consistency. While others pivot, transform, and reinvent, Markel keeps doing what works, just a little better each year. It's not a strategy that generates headlines or wins innovation awards. But over 90 years, it has created billions in value for shareholders while treating customers, employees, and communities fairly.

XI. Epilogue: The Next Chapter

Tom Gayner sits in his Richmond office, surrounded by annual reports and investment memos, contemplating a question he's been asked countless times: What would it take for Markel to 10x from here? His answer reveals both ambition and realism. "We don't need to do anything revolutionary. We need to keep doing what we're doing, maybe a little better, for another few decades. Compound interest is still the eighth wonder of the world."

The math supports his patience. To 10x requires roughly 12% annual returns for 20 years—ambitious but achievable given Markel's historical 11% book value CAGR. The path doesn't require moonshots or transformations, just consistent execution across three engines. Insurance needs to maintain underwriting discipline while gradually expanding into new specialties. Investments must compound at market-beating rates without taking excessive risk. Ventures should continue acquiring quality businesses at reasonable prices.

Yet the future holds challenges that compound interest alone won't solve. Climate change is accelerating natural catastrophe losses, potentially making some insurance lines structurally unprofitable. Technology continues commoditizing risk assessment, compressing margins in previously profitable niches. Alternative capital—pension funds and sovereign wealth funds directly accessing reinsurance returns—adds competitive pressure. And valuations across all asset classes remain historically elevated, limiting future return potential.

Gayner's vision for navigating these challenges reflects characteristic pragmatism. "We're not trying to predict the future; we're trying to build a company that can adapt to whatever comes." This means maintaining financial strength to survive shocks, operational flexibility to enter and exit markets, and cultural coherence to make decisions aligned with long-term value creation.

Succession planning, while not urgent, occupies increasing mindshare. Unlike Berkshire's well-telegraphed transition plan, Markel's next generation leadership remains opaque. Jeremy Noble runs insurance operations effectively but lacks Gayner's investment acumen. The Ventures team has depth but no clear leader. The investment team remains thin, relying heavily on Gayner's judgment. "We're building bench strength," Gayner notes, "but ultimately the board will decide when the time comes."

Emerging opportunities could accelerate growth beyond the steady compounding baseline. Cyber insurance, despite current challenges, represents a potentially massive market where Markel's specialty expertise could dominate. The energy transition creates new risks—offshore wind, battery storage, carbon capture—that need sophisticated underwriting. Demographic shifts drive demand for healthcare services where Ventures already has presence through PartnerMD.

International expansion offers another growth vector. While Markel has London and Bermuda operations, it remains predominantly U.S.-focused. Asia's growing middle class needs specialty insurance. European businesses seeking permanent capital might prefer Markel to private equity. Ventures could replicate its U.S. model internationally, acquiring family businesses in developed markets with strong rule of law.

The threat landscape continues evolving. Amazon or Google could enter insurance with technology advantages and infinite capital. Climate change could make entire regions uninsurable. A severe recession could simultaneously hit insurance, investments, and Ventures. Regulatory changes could limit investment activities or force capital requirements that reduce returns. Black swan events—pandemic, war, financial crisis—remain ever-present risks.

But Markel has survived and thrived through the Great Depression, World War II, stagflation, the dot-com crash, 9/11, the Global Financial Crisis, and COVID-19. Each crisis taught lessons, strengthened culture, and created opportunities. This antifragility—getting stronger through stress—might be Markel's greatest asset.

What would it take to 10x from here? Start with the base case: consistent execution across three engines should compound value at low double-digit rates. Add selective geographic expansion, particularly in Asia and Europe. Capture emerging risk markets like cyber, climate transition, and healthcare. Maintain discipline to avoid value-destroying mistakes. And perhaps most importantly, preserve the culture that makes it all possible.

The next chapter won't be written by any single leader or strategy. It will emerge from thousands of daily decisions guided by consistent principles. Underwriters deciding which risks to accept. Gayner choosing which stocks to buy. Ventures executives evaluating acquisitions. Each decision individually minor but collectively determining whether Markel remains a compounding machine or becomes another formerly great company that lost its way.

Final reflections on building a century-spanning enterprise return to Sam Markel insuring those jitney buses in 1930. He couldn't have imagined today's global conglomerate, but he embedded values that endured: serve customers fairly, take smart risks, think long-term, and compound returns. These principles, simple to state but difficult to maintain, have created billions in value over 90 years.

The story continues, page by page, decision by decision, year by year. Not through dramatic pivots or revolutionary strategies, but through patient accumulation of advantages that compound like interest. It's a boring story in some ways—no corporate drama, no betting-the-company moments, no visionary disruption. Just consistent excellence, maintained over decades, creating extraordinary results from ordinary activities.

For investors evaluating Markel today, the question isn't whether it will be the next Berkshire—it won't be. The question is whether a proven compounding machine, operated with integrity and discipline, can continue creating value in an uncertain world. History suggests yes. The future will reveal if history remains a reliable guide.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube