MGP Ingredients: The "Intel Inside" of the Bourbon Boom

I. Introduction: The Ghost in the Bottle

Walk into any well-stocked liquor store in America and scan the bourbon aisle. There are fifty, maybe sixty different labels staring back at you. Rustic fonts. Sepia-toned photographs of bearded men in overalls. Origin stories about "Grandpa's recipe" or "a hidden cellar discovered during Prohibition." Each bottle presents itself as a singular expression of some local craft tradition, distilled with care by artisans in a small town you've never heard of.

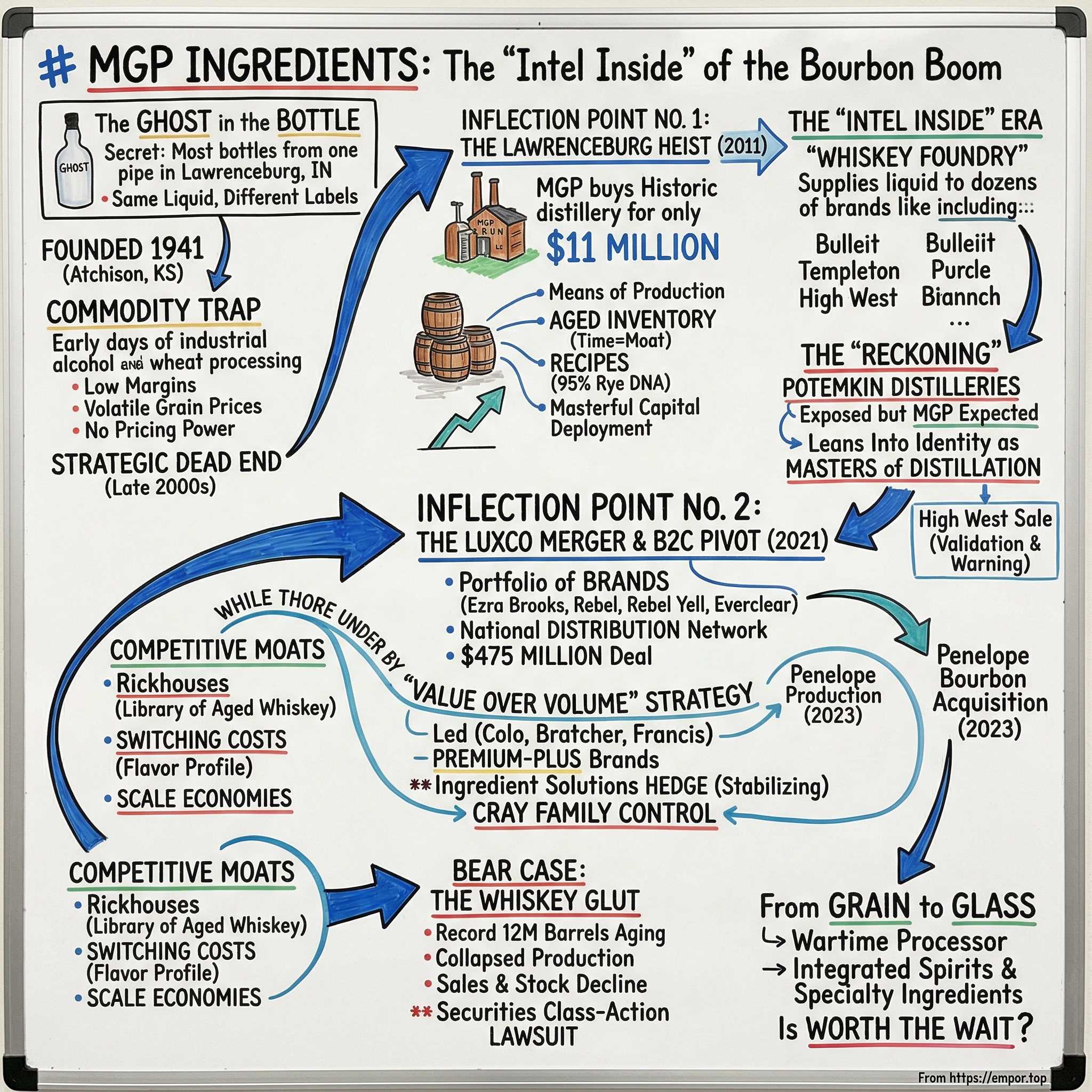

Here is the secret that blew the lid off the American whiskey industry in the mid-2010s: most of those bottles came from the same massive pipe in Lawrenceburg, Indiana. The same mashbills. The same column stills. The same rickhouses. Different labels, different stories, same liquid. And the company behind that pipe, for years, preferred it that way. They were the ghost in the bottle.

MGP Ingredients is one of the most unusual companies in the American spirits landscape. Founded in 1941 as a wartime industrial alcohol producer in Atchison, Kansas, it spent six decades as a commodity processor that most investors wouldn't bother looking at twice. Low margins, fluctuating grain prices, zero brand equity. The stock languished in the single digits for years. Then, through two of the most perfectly timed acquisitions in modern spirits history, MGP transformed itself into the silent kingmaker of the American Whiskey Renaissance, the contract manufacturer that powered dozens of "craft" brands, and ultimately, a branded spirits company in its own right.

The first acquisition, in 2011, was the purchase of the historic Lawrenceburg distillery from a distressed seller for roughly eleven million dollars. To put that in context, major spirits companies were paying fifteen to twenty times EBITDA for brand portfolios. MGP bought the means of production and years of aged liquid at barely above asset value. It is arguably the single best capital deployment in the American spirits industry over the past two decades.

The second, a decade later, was the 2021 merger with Luxco for $475 million, which gave MGP something it had never had: a portfolio of consumer-facing brands and a national distribution network. Overnight, the company that had been content to fill other people's bottles started filling its own.

This is the story of how a grain processor from Kansas became the TSMC of whiskey, why that model worked brilliantly until it didn't, and what happens now that the American whiskey market is drowning in its own success. Along the way, it touches on family dynasties, Prohibition-era bootleggers, Silicon Valley-style platform economics, and the question of whether you can engineer a craft brand from the top down. The answer, as MGP is discovering, is more complicated than anyone expected.

II. Founding and The Commodity Trap

In September 1941, three months before Pearl Harbor, a Detroit investment banker named Cloud L. Cray, Sr. arrived in Atchison, Kansas to inspect an idled alcohol plant. His original plan was straightforward: buy the equipment, dismantle it, and reassemble it in Michigan where he could put it to better use. Atchison was a small river town on the Missouri, better known as the birthplace of Amelia Earhart than as an industrial hub. It wasn't supposed to be a destination.

But Cray lingered. The local town leaders made their pitch. The community needed the jobs. The plant was already built. And then, on December 7, the Japanese bombed Pearl Harbor, and the calculus changed entirely. The federal government's demand for industrial alcohol, used in everything from synthetic rubber to munitions, exploded overnight. Cray bought the plant, hired about forty workers, and began producing alcohol for the war effort. He called his venture Midwest Solvents Company.

What Cray built in those early years was not glamorous. It was industrial processing at its most fundamental: take grain, ferment it, distill it, sell the output. After the war ended and military demand dried up, the company pivoted to what would become its bread and butter for the next six decades: neutral grain spirits for vodka and gin production, wheat gluten, wheat starches, and various food-grade ingredients. It was a business defined entirely by the commodity cycle. When grain prices were low and demand was high, you made money. When grain prices spiked or customers found cheaper suppliers, you didn't. There was no pricing power, no brand premium, no moat.

Cloud Cray's son, Cloud L. "Bud" Cray, Jr., joined the company in 1947 and eventually took over as President in 1962, then Chairman and CEO in 1980. Under Bud's steady hand, the company renamed itself Midwest Grain Products and went public on the Nasdaq in October 1988 at fourteen dollars per share. The IPO was unremarkable. The company was what it was: a regional processor in Kansas making commodity alcohol and wheat ingredients.

The strategic dead end became painfully clear in the late 2000s. Rising corn prices squeezed margins on ethanol production. The food ingredients business was competitive and undifferentiated. Revenue was volatile and profits were thin. The stock drifted into the low single digits. By any traditional measure, this was a business going nowhere, the kind of company that shows up on value screens and gets dismissed as a "cigar butt" with one puff left. What almost nobody saw coming was that the cigar butt was sitting on top of a goldmine. It just needed someone to walk into Lawrenceburg, Indiana and pick up the key.

III. Inflection Point No. 1: The Lawrenceburg Heist

The story of the Lawrenceburg distillery reads like a relay race where the baton kept getting dropped. In 1847, a man named George Ross opened the Rossville Distillery on the banks of Tanner's Creek in Lawrenceburg, Indiana, making it one of the oldest continuously operated distillery sites in America. A few decades later, in 1869, William Squibb founded a second distillery nearby. Then came Prohibition, and with it, one of the most colorful characters in American booze history: George Remus, the "King of the Bootleggers," who purchased the Squibb facility in 1921 and used it as part of his massive illegal distribution network. Remus was eventually convicted, released, and then murdered his wife in a jealousy-fueled rage in Cincinnati's Eden Park. His story was so outlandish that F. Scott Fitzgerald reportedly drew on it for Jay Gatsby.

After Prohibition ended in 1933, Joseph E. Seagram and Sons snapped up the Rossville Distillery and turned Lawrenceburg into one of the great American whiskey production centers. Under Seagram's ownership, the facility grew into a massive operation with dozens of buildings, multiple column stills, and an enormous barrel warehouse network. Seagram's operated it for nearly seven decades.

Then came the Great Spirits Reorganization of 2000 to 2001. When the Seagram empire was dismantled, Crown Royal went to Diageo, Glenlivet and Chivas went to Pernod Ricard, and the Lawrenceburg distillery ended up as a kind of orphan asset under Pernod Ricard's umbrella. Pernod didn't need it. They had their own production capacity in Scotland and France. In 2006, they announced plans to close it entirely.

Instead of shuttering the facility, Pernod sold it in 2007 to CL Financial, a holding company based in Trinidad and Tobago, which renamed it "Lawrenceburg Distillers Indiana," or LDI. But CL Financial ran into severe financial trouble during the 2008 financial crisis and required a government bailout in Trinidad. The distillery was once again in limbo, owned by a distressed parent an ocean away.

This is where MGP enters the picture. In 2011, MGP negotiated the purchase of the Lawrenceburg distillery from CL Financial. The deal closed on December 28, 2011, for cash equal to the current assets minus current liabilities, estimated at approximately eleven million dollars. Eleven million. For one of the largest beverage alcohol distilleries in the United States, complete with production equipment, existing barrel inventory including aged whiskey stocks, and decades of institutional knowledge about bourbon and rye production.

To appreciate how extraordinary this price was, consider the context. At the time, major spirits companies were paying billions for brand portfolios. Diageo had paid $3.2 billion for Seagram's spirits brands. Beam Inc. would later sell to Suntory for $16 billion. Constellation Brands would pay $5.6 billion for the Modelo beer business. These were transactions priced at twelve to twenty times EBITDA, driven by the premium that investors place on consumer brands with pricing power.

MGP didn't buy a brand. It bought the factory. But not just any factory. It bought a factory with something far more valuable than stainless steel and copper: it bought time. Sitting in those rickhouses in Lawrenceburg were barrels of aging bourbon and rye whiskey. Some of them were years old. And in the whiskey business, time is the one thing money cannot compress. You cannot "disrupt" ten-year-old bourbon. You cannot fast-track it. You cannot hack it. You can only wait ten years. MGP, for eleven million dollars, bought the waiting that someone else had already done.

The acquisition also came with something less tangible but equally important: recipes. The Lawrenceburg facility's signature product was a straight rye whiskey with a 95% rye and 5% barley malt mashbill. This punchy, spicy, distinctive rye formulation would become the most famous "open secret" in the American whiskey industry. It was the DNA inside dozens of brands that consumers believed were being crafted by hand in small distilleries across the country.

Suddenly, MGP wasn't just a commodity alcohol producer from Kansas. It was the custodian of some of the most sought-after whiskey recipes and aged inventory in America. The company had stumbled into the supply side of a demand wave that was just beginning to build.

IV. The "Intel Inside" Era

In the semiconductor world, there is a concept called the "foundry model." Companies like TSMC don't design their own chips. They manufacture chips that other companies have designed. Apple, Nvidia, and AMD all rely on TSMC's fabrication plants to turn their blueprints into silicon. The foundry doesn't get the consumer glory, but it captures enormous value because it controls the bottleneck: the ability to actually make the product at scale and quality.

After the Lawrenceburg acquisition, MGP became the TSMC of American whiskey. The company produced bourbon and rye whiskey in bulk and sold it to dozens of brands that then bottled it under their own labels, often with their own marketing stories, their own pricing strategies, and their own craft mythology. MGP didn't care about the label. It cared about the liquid. And the liquid was very, very good.

The client list read like a who's who of the American whiskey boom. Bulleit Rye, owned by Diageo, was one of the fastest-growing whiskey brands in the country, and its rye expression was MGP distillate. Templeton Rye, marketed with elaborate tales of an Iowa Prohibition-era recipe, was produced in Lawrenceburg. High West Distillery in Park City, Utah, built its reputation on expertly blending MGP whiskey. WhistlePig, which would become one of the most celebrated rye whiskey brands in America, sourced from MGP in its early years. Angel's Envy, Smooth Ambler Old Scout, Redemption, Belle Meade, James E. Pepper: the list went on and on. By some estimates, MGP produced approximately 75% of all rye whiskey on the U.S. commercial market.

The economics of this model were remarkable. MGP bore the capital cost of production and aging, then sold the liquid at wholesale to bottlers who marked it up two to five times under their own brands. MGP's margins on aged whiskey were strong since the product was carried on the balance sheet at cost and realized market value years later at an estimated three times cost, implying margins above 60%. But the bottlers' margins were even better because they controlled the "last mile" to the consumer, the brand story, the label design, the shelf placement, the pricing. A barrel of MGP rye that cost the bottler a few thousand dollars could yield bottles retailing for forty to sixty dollars each.

Then came the reckoning. Around 2014 and 2015, whiskey writers and investigative journalists began pulling the curtain back. Charles Cowdery, one of the most respected voices in American whiskey, began calling out what he termed "Potemkin distilleries," brands that marketed themselves as craft producers while actually just bottling someone else's liquid. The Daily Beast published a widely-read piece titled "Your 'Craft' Whiskey Is Probably From a Factory Distillery in Indiana." NBC News covered the misleading claims fueling the bourbon boom. The "sourced whiskey" controversy had arrived.

Templeton Rye bore the brunt of the backlash. In 2015, the company settled a class-action lawsuit for $2.5 million, agreeing to add "Distilled in Indiana" to its label and remove claims like "Small Batch" and "Prohibition Era Recipe" from the front of the bottle. Other brands faced similar scrutiny.

MGP, as the supplier, stood in an awkward position. It hadn't made the misleading marketing claims, but it was the source of the liquid that those claims were built around. The company could have retreated further into the shadows. Instead, it did something strategically astute: it leaned into its identity. Rather than hiding the fact that it was a large-scale producer, MGP began positioning itself as the "Masters of Distillation," the company with 175 years of distilling heritage at Lawrenceburg, the keeper of recipes dating back to the 1800s. In 2021, following the Luxco acquisition, MGP rebranded the Lawrenceburg facility as "Ross and Squibb Distillery," honoring George Ross from 1847 and William Squibb from 1869, the two founders who put Lawrenceburg on the whiskey map. It was a masterful reframe: instead of being the factory behind the curtain, MGP became the heritage institution that other brands were fortunate enough to source from.

One brand stood out as a counterexample to the controversy: High West Distillery in Utah. Rather than hiding its sourcing, High West openly credited MGP and positioned blending as its own form of craft. The market rewarded this transparency. In 2016, Constellation Brands acquired High West for approximately $160 million, a staggering premium for a brand that was, in large part, repackaging and blending someone else's whiskey. For MGP, High West's sale was both validation and warning: validation that its liquid could support premium brand valuations, and a warning that it was watching someone else capture the brand premium on its own product.

The "Intel Inside" era was enormously profitable. Between 2012 and 2022, MGP's stock price rose from the low single digits to an all-time high of $122.05 in November 2022, a roughly twenty-fold increase. Revenue grew from approximately $300 million to over $780 million. The company that had been a cigar butt was now a market darling. But the foundry model had an inherent limitation that management understood with increasing clarity: you can be the best factory in the world, but if someone else owns the brand, someone else owns the margin.

V. Inflection Point No. 2: The Luxco Merger and the B2C Pivot

By 2020, MGP's leadership had arrived at a conclusion that would reshape the company: the wholesale whiskey business, however profitable, had a ceiling. Contract distilling was inherently dependent on the purchasing decisions of third-party brands. If Diageo decided to bring Bulleit Rye production in-house, or if craft brands started building their own distilleries and aging their own liquid, MGP's revenue would contract regardless of how good its whiskey was. The company needed to own its own brands.

MGP had already begun experimenting with proprietary labels. In 2018 and 2019, the company launched George Remus Straight Bourbon Whiskey, named after the infamous Prohibition-era bootlegger who had once owned the Lawrenceburg facility, and Rossville Union Rye Whiskey, honoring the distillery's 1847 origins. These were premium expressions designed to showcase MGP's own liquid under its own name. But building brands from scratch is slow, expensive, and uncertain. The fastest route to scale was acquisition.

Enter Luxco. Founded in St. Louis, Missouri, Luxco was a mid-sized spirits company with a portfolio of established brands, including Ezra Brooks bourbon, Rebel bourbon (formerly Rebel Yell), Yellowstone bourbon, Blood Oath bourbon, Everclear grain alcohol, Pearl Vodka, El Mayor Tequila, and several others. Critically, Luxco also owned Lux Row Distillers, a production facility in Bardstown, Kentucky, and had a national distribution network that MGP lacked.

On January 25, 2021, MGP announced the definitive merger agreement. The deal closed on April 1, 2021, at an enterprise value of $475 million, structured as equal parts cash ($238 million) and stock (5.0 million shares of MGP common stock valued at approximately $238 million). At roughly twelve times EBITDA, MGP bought a massive portfolio at a meaningful discount to "premium brand" multiples, where spirits acquisitions routinely closed at fifteen to eighteen times.

The market was initially skeptical. Analysts questioned whether MGP, a company whose DNA was in manufacturing, could successfully pivot to brand-building and consumer marketing. The stock wobbled. But the strategic logic was compelling: MGP already produced much of the liquid that Luxco was selling under its brands. By vertically integrating, MGP could eliminate the middleman margin, control the entire value chain from grain to glass, and redirect its best aged inventory away from competitors and into its own bottles.

David Bratcher, who had served as Luxco's President since 2013, joined MGP as COO and President of Branded Spirits, bringing deep experience in brand management and distribution. The integration proceeded rapidly. MGP stopped selling some of its most prized aged liquid on the wholesale market and began bottling it under the Ezra Brooks, Rebel, George Remus, and Rossville Union labels.

Two years later, in June 2023, MGP doubled down with the acquisition of Penelope Bourbon for $105 million upfront plus up to $110.8 million in earn-out payments through December 2025, for a potential total of $215.8 million. Penelope was one of the fastest-growing whiskey brands in the country, positioned squarely in the premium-plus segment. The acquisition signaled that MGP was no longer just defending its turf. It was actively building a portfolio designed to compete with the legacy bourbon houses.

By fiscal year 2023, the pivot was showing results. Branded Spirits revenue reached $253.9 million, up from essentially zero before the Luxco merger. The segment's gross margin hovered near 50%, dramatically higher than the contract distilling business. MGP had gone from being the ghost in other people's bottles to putting its own name on the shelf. The question was whether consumers would care. The early signs were promising, but the real test was just around the corner, and it would come not from consumer indifference but from something far more brutal: a whiskey glut.

VI. Current Management and the "Value Over Volume" Strategy

The CEO who orchestrated much of MGP's transformation was David Colo, who joined as President and COO in March 2020 and became CEO on June 1, 2020. Colo was not a whiskey guy. He was a supply chain and consumer packaged goods executive with over thirty years of food industry experience. He had served as President of ConAgra Food Ingredients, held senior vice president roles in manufacturing and operations at ConAgra's consumer products division, then led Diamond Foods as EVP and COO, and served as President and CEO of SunOpta, a plant-based and organic foods company. His background was in operational efficiency, supply chain optimization, and premiumization, the art of moving a product portfolio upmarket to capture higher margins.

Colo brought a CPG playbook to a spirits company, and it worked. Under his leadership, MGP articulated what it called the "Value Over Volume" strategy: intentionally shrinking the low-end, commodity-oriented segments of the business to focus capital and attention on high-margin branded spirits and specialty ingredients. The logic was straightforward. Selling a gallon of bulk neutral grain spirits at commodity prices generated pennies of margin. Selling that same grain, distilled into premium bourbon, aged for years, and bottled under the George Remus label at fifty or sixty dollars a bottle, generated dollars. The strategy meant accepting lower top-line revenue in exchange for higher margins, better returns on invested capital, and a more durable competitive position.

Colo retired on December 31, 2023, handing the reins to David Bratcher, the former Luxco president who had been serving as COO. But Bratcher's tenure was short-lived. He resigned on December 31, 2024, as the whiskey market downturn intensified. CFO Brandon Gall stepped in as Interim President and CEO, and in mid-2025, MGP appointed Julie Francis as permanent President and CEO.

Francis brought yet another perspective. Her career spanned Schwan's Company, where she served as COO, Constellation Brands, where she was SVP of Commercial and Category Development across Total Beverage Alcohol, and Coca-Cola Refreshments USA, where she served as Chief Commercial Officer. She was, in other words, someone who had sold consumer beverages at enormous scale and understood both brand positioning and distribution economics.

The leadership turnover, three CEOs in three years, raised legitimate concerns about strategic continuity. But there was a stabilizing force that investors sometimes overlooked: the Cray family. Through their ownership of 92% of MGP's preferred stock and approximately 27.5% of the common stock, the founding family retains effective control of the board, with the ability to elect five of nine directors. Karen Seaberg, Bud Cray's daughter, served as Chairman of the Board. Lori Mingus, a fourth-generation family member, also sits on the board. And in December 2024, Donn Lux, who had led Luxco prior to its acquisition, was named Chairman, a signal that the board was pulling in deep spirits industry experience to steady the ship during turbulent times.

The compensation structure reinforced the long-term orientation. In 2025, the Human Resources and Compensation Committee approved a revamped long-term incentive program built around performance stock units with forward-looking financial targets and time-vested restricted stock units for retention. The emphasis on performance-based vesting, rather than simply rewarding revenue growth, aligned management incentives with the premiumization strategy.

For investors watching MGP, the "Value Over Volume" framework means tracking the company's progress through two critical lenses. First, the mix shift within Branded Spirits: premium-plus brand sales grew 5% in fiscal 2025 even as the overall segment declined 3%, while mid-tier and value brands fell 13%. That divergence is the strategy working as designed. Second, Branded Spirits gross margin, which held at 49.5% in fiscal 2025, up forty basis points year-over-year, demonstrating that the portfolio can sustain pricing even in a downturn. Those two metrics, premium-plus mix and branded gross margin, are the KPIs that will tell you whether MGP's transformation is real or whether the company remains, at its core, a contract manufacturer with a side business in brands.

VII. The "Hidden" Business: Ingredient Solutions

There is a corner of MGP's business that rarely makes the whiskey press or the spirits analyst notes, but quietly generates over $120 million in annual revenue with meaningful optionality. The Ingredient Solutions segment, operating from the company's original Atchison, Kansas facility, produces specialty wheat proteins and starches for the food industry. If the Distilling Solutions segment is the legacy cash cow and Branded Spirits is the growth engine, Ingredient Solutions is the hedge, a non-cyclical business that doesn't care whether bourbon is in fashion.

The segment's flagship product is Fibersym, a resistant wheat starch that the FDA classifies as dietary fiber. In layman's terms, Fibersym allows food manufacturers to add fiber content to products like bread, pasta, and baked goods without changing the taste or texture. For a food industry obsessed with clean labels and functional nutrition, this is valuable. The keto diet wave, the high-fiber trend, the broader health-and-wellness movement: all of them drive demand for ingredients that let companies put "High Fiber" or "Low Net Carb" on their packaging without making the product taste like cardboard.

Then there are MGP's specialty wheat proteins, sold under brands like Arise and Proterra. These proteins found their way into the plant-based meat revolution, supplying texture and binding properties to companies producing alternatives to traditional meat products. While the plant-based meat category has cooled from its 2020 to 2021 peak, the underlying demand for functional plant proteins in food manufacturing remains significant.

The beauty of this segment, from a portfolio construction standpoint, is the shared infrastructure. MGP processes grain at the Atchison facility for both its spirits and food ingredients businesses. The same wheat kernel that yields starch for Fibersym also yields gluten proteins and fermentable sugars. It is a vertically integrated grain biorefinery where nothing goes to waste. The synergy is real, not the kind of "synergy" that investment bankers invoke to justify inflated deal prices, but actual shared-input, shared-infrastructure efficiency.

Financially, the Ingredient Solutions segment generated $122 million in revenue in fiscal 2025, representing about 23% of total sales. Gross margins have historically run in the low-to-mid twenties, though fiscal 2025 saw a decline to 12.7% due to weather-related disruptions, equipment failures, and high waste disposal costs. These are fixable, operational issues rather than structural problems.

For a company navigating a brutal whiskey downturn, the Ingredient Solutions segment provides something invaluable: stability. It doesn't swing with bourbon demand cycles. It doesn't depend on whether millennials are drinking rye this year or mezcal. It is, in portfolio theory terms, an uncorrelated revenue stream. And if the plant-based protein and functional food markets continue their long-term growth trajectory, it could become a meaningfully larger part of MGP's story.

VIII. The Playbook: Competitive Moats, Industry Forces, and the Bear Case

To understand MGP's competitive position, it helps to apply two frameworks that get at different dimensions of the question: Hamilton Helmer's Seven Powers, which identifies the sources of durable competitive advantage, and Michael Porter's Five Forces, which maps the structural dynamics of the industry.

The Cornered Resource. MGP's most powerful moat is something you can see from a satellite image of rural Indiana and Kentucky: row after row of barrel warehouses, called rickhouses, stretching across the landscape. Inside those warehouses are hundreds of thousands of barrels of aging bourbon and rye whiskey. This inventory, carried on the balance sheet at cost, represents years and in some cases a decade or more of patient waiting. A new entrant can build a distillery in two years. They cannot build ten-year-old bourbon in two years. They can only wait. MGP's "library" of aged whiskey is a time-based moat that no amount of capital can immediately replicate.

The company invested $32.9 million in net whiskey put-away in fiscal 2024 and $18.5 million in fiscal 2025, deliberately scaling back as the market softened. But the inventory already in the rickhouses continues to appreciate in quality and value with each passing year. A $12 million expansion at Williamstown, Kentucky, completed in 2022, approximately doubled barrel storage capacity. This is a cornered resource in the most literal sense: you either have aged whiskey or you don't, and MGP has one of the largest privately held reserves in the country.

Switching Costs. Once a craft brand builds its flavor profile on MGP's specific mashbill, switching to another distiller is what you might call "brand suicide." Consumers develop palate expectations. A brand like Templeton or Redemption that has spent years establishing its taste profile around MGP's 95% rye mashbill cannot simply switch to a Kentucky distiller's 60% rye recipe without fundamentally altering its product. The whiskey would taste different. Loyal customers would notice. Reviews would change. For established brands, the switching cost is the brand itself.

Scale Economies. The Lawrenceburg facility is one of the largest beverage alcohol distilleries in the United States, with over forty buildings, fourteen fermentation tanks each holding over 25,000 gallons, and the infrastructure to produce whiskey at an industrial scale. MGP's unit cost for a gallon of high-quality rye whiskey is untouchable by any craft distiller producing a few hundred barrels a year. Even Bardstown Bourbon Company, the most prominent new entrant in contract distilling, operates at a fraction of MGP's scale.

Porter's Five Forces paint a complementary picture. Barriers to entry in whiskey production are high: the business is capital-intensive, heavily regulated by the TTB (Alcohol and Tobacco Tax and Trade Bureau), and constrained by the irreducible aging timeline. The bargaining power of buyers, historically strong when MGP depended on a few large customers like Diageo, is shifting as the company builds its own brands and reduces reliance on contract distilling. Supplier power is moderate since grain is a commodity with multiple sources. The threat of substitutes is real but manageable: consumers might rotate between bourbon, tequila, and ready-to-drink cocktails, but brown spirits have shown remarkable resilience over long cycles.

The Bear Case: The Whiskey Glut. This is the existential question that hangs over MGP and the entire American whiskey industry. Over twelve million barrels of bourbon are currently aging in Kentucky alone, a record. Total U.S. whiskey production through mid-2025 was down 19% over the prior twelve months, 28% over the prior six months, and 32% over the prior three months, according to TTB data. American whiskey volume growth, which had been accelerating for over a decade, turned slightly negative by 2024.

The impact on MGP has been devastating. The Distilling Solutions segment, which generated $450.9 million in revenue at its fiscal 2023 peak, collapsed to $181.4 million in fiscal 2025, a 60% decline in two years. Many large customers paused purchases to balance their own inventories and manage working capital. Full-year fiscal 2025 ended with a net loss of $107.8 million, compared to net income of $107.5 million just two years earlier. The stock, which traded at $122.05 at its November 2022 peak, sat at $18.60 in late March 2026, an 85% decline that erased roughly $1.9 billion in market capitalization.

History provides both comfort and warning. American whiskey went through a similar boom-bust cycle in the 1960s and 1970s, when overproduction and shifting consumer tastes toward vodka and lighter spirits led to decades of decline. Distilleries shuttered. Brands were sold for pennies. The recovery didn't begin until the late 1990s and early 2000s. Could it happen again? Industry bulls point to the structural differences: today's whiskey consumer is global, premium-oriented, and more diverse than the 1970s demographic. Bears counter that twelve million aging barrels don't lie, and that the normalization of cocktail culture could shift demand toward tequila, mezcal, and Japanese whisky.

There is also a legal overhang. A securities class-action lawsuit was filed against MGP in the U.S. District Court for the Southern District of New York, covering the period from May 2023 through October 2024. The complaint alleges that management repeatedly touted strong demand and "normal" inventory levels when there had actually been a slowdown in consumption and oversupply, and that they assured investors MGP was positioned differently from competitors when it was not. The stock dropped approximately 15% after a February 2024 guidance miss and another 30% over three trading sessions following the October 2024 Q3 results. These are serious allegations that create uncertainty around the company's disclosure practices during a critical period.

How MGP compares to peers on valuation tells the current story succinctly. Brown-Forman trades at roughly 14.5 times EV/EBITDA. Diageo trades at about 12.3 times. MGP, on its fiscal 2026 guided adjusted EBITDA of $90 to $98 million, trades at approximately 6.6 to 7.2 times. That discount reflects the market's judgment that MGP's business model is more cyclical, less branded, and more exposed to the contract distilling downturn than the integrated majors. Whether that discount is overdone or appropriate depends entirely on whether you believe the branded spirits pivot can gain enough traction to offset the structural decline in wholesale distilling.

The company's management is guiding for fiscal 2026 revenue of $480 to $500 million, adjusted EBITDA of $90 to $98 million, and adjusted earnings per share of $1.50 to $1.80. Capital expenditures are being cut dramatically to roughly $20 million, down from $73 million at the peak, and the company is rationalizing 20% of its portfolio's "tail brands" to focus resources on its premium-plus labels. Operating cash flow actually improved to $121.5 million in fiscal 2025, up from $102.3 million the prior year, suggesting that the underlying business, stripped of non-cash impairment charges, is generating real cash even in the downturn.

IX. Conclusion: From Grain to Glass

The MGP Ingredients story is, at its core, a story about timing and transformation. A wartime grain processor that spent sixty years as a commodity nobody, two brilliantly timed acquisitions that gave it the most valuable whiskey production platform in the country, a decade as the hidden kingmaker of the American whiskey boom, and then a bold pivot into branded spirits that is being stress-tested by the worst industry downturn in a generation.

The Lawrenceburg acquisition for eleven million dollars remains one of the great capital allocation stories in modern American business. The Luxco merger for $475 million, while its full returns are still being determined, gave MGP the brands, distribution, and organizational capability to compete on the shelf rather than just in the rickhouse. The Penelope Bourbon acquisition added a premium growth brand to the portfolio. The Ingredient Solutions segment provides a non-cyclical hedge. And the Cray family's continued control provides the kind of long-term orientation that is rare in public markets.

The open questions are significant. Can Remus, Ezra Brooks, Rebel, or Penelope become the next Buffalo Trace or Woodford Reserve? Can MGP's branded gross margins hold above 49% as the company scales? Will the whiskey glut prove to be a cyclical trough that clears in two to three years, or the beginning of a structural shift away from American brown spirits? And will the securities litigation resolve without material financial impact?

What is clear is that MGP is no longer the company it was. It is not a commodity grain processor. It is not just a contract distiller. It is an integrated spirits and specialty ingredients company with a portfolio of owned brands, a massive aged whiskey inventory that is appreciating every day, and a management team focused on premiumization over volume. Whether the market rewards that transformation depends on the answer to the oldest question in the whiskey business: is this worth the wait?

For the patient investor, the next chapter will be written not in quarterly earnings calls but in the rickhouses of Lawrenceburg and Williamstown, where hundreds of thousands of barrels are quietly aging, gaining complexity, and waiting for their moment. In whiskey, as in investing, time is the one input that cannot be rushed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube