Magnite Inc.: The Story of Ad Tech's Unlikely Survivor

I. Introduction & Episode Roadmap

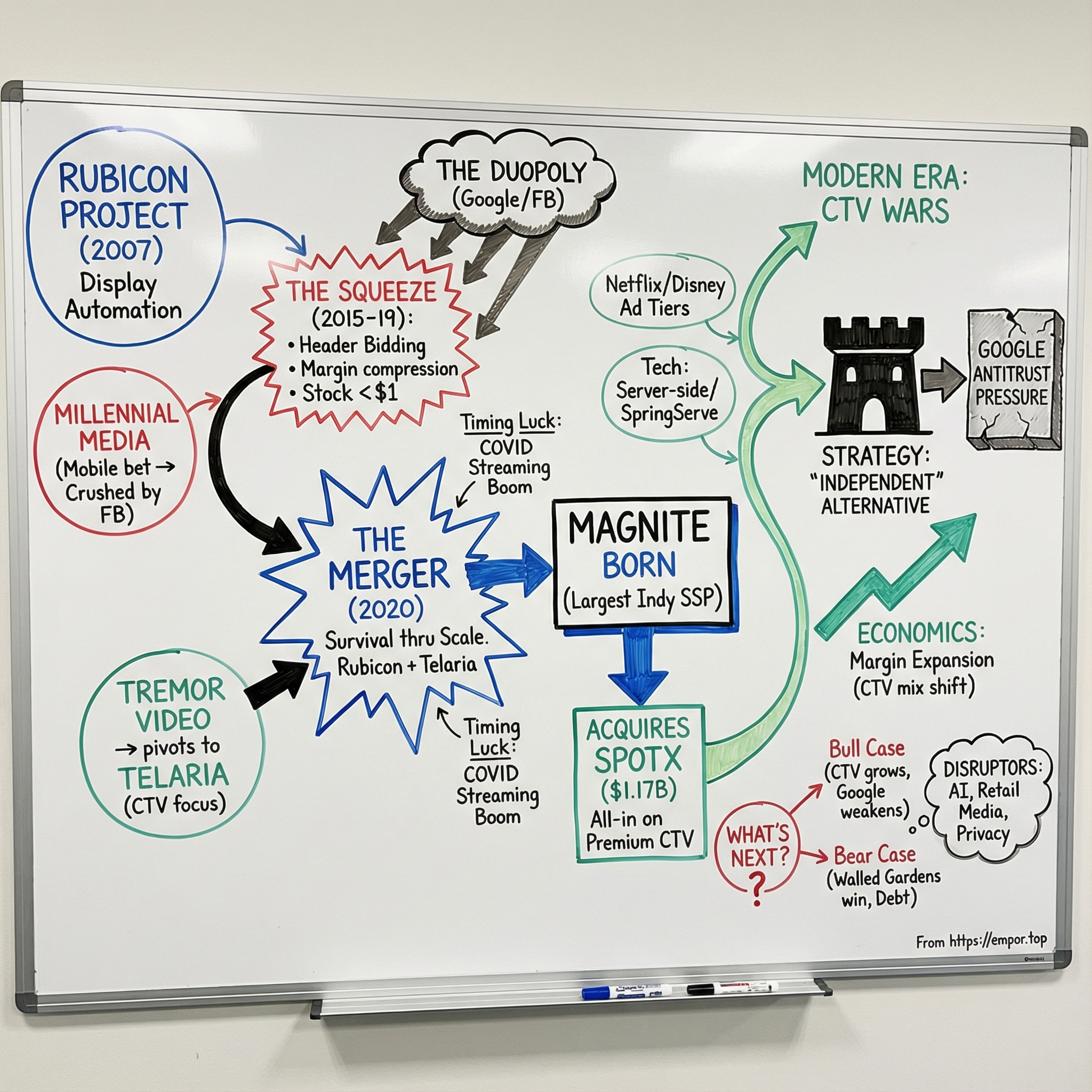

Picture a Los Angeles conference room in early 2020. Michael Barrett, newly installed as CEO of what was about to be called Magnite, is staring at a whiteboard packed with circles and arrows: streaming services, ad exchanges, supply paths, and, looming over everything, the duopoly of Google and Facebook.

The company in front of him is the result of a not-so-romantic marriage between two wounded survivors. On one side: Rubicon Project, once a programmatic darling, now coming off years of strategic whiplash and financial stress. On the other: Telaria, a video-focused upstart that had made an early, risky bet on connected TV. Neither was big enough to win alone. Together, they might be.

Fast forward to today, and Magnite calls itself the world’s largest independent sell-side advertising platform. In 2024, it generated $668 million in revenue, up 7.82% year over year. It finished the year with $483 million in cash and net leverage down to 0.4x. That’s a long way from the days when its stock dipped below a dollar and delisting felt like a real possibility.

So here’s the deceptively simple question at the heart of this story: how did a struggling ad tech company become one of the last independent players standing in the programmatic wars?

The answer is equal parts strategy and survival instinct. It’s about enduring a brutal consolidation cycle, catching the connected TV wave early—before most people recognized it as a wave—and learning that in ad tech, sometimes the most underrated competitive advantage is simply refusing to die.

We’ll track three threads throughout the episode. First: survival through consolidation—why, in winner-take-most markets, merging can be less about surrender and more about creating the scale you need to stay relevant. Second: the platform shifts from desktop to mobile to connected TV, where every transition wipes out incumbents and hands an opening to whoever moves fastest. Third: what “independent” actually means in an industry where the pipes, the rules, and the economics are heavily shaped by Google and Facebook—and whether being the alternative to a monopolist can become an advantage that lasts.

If you want to understand the brutal economics of two-sided marketplaces, Magnite is a great case study—both as a cautionary tale and as proof that reinvention is possible. This company has been left for dead more than once, and it kept finding a way back. Whether that comeback created enduring value—or just delayed an inevitable reckoning—is what we’re here to find out.

II. The Pre-History: Understanding Programmatic Advertising

Before we can talk about Magnite, we need to talk about the machine Magnite lives inside.

Programmatic advertising is, at its simplest, an automated auction for attention. Every time you open a website or app, there’s a split-second window before the page finishes loading. In that window, publishers try to sell an ad slot, advertisers try to buy it, and a stack of software runs a miniature financial market in milliseconds.

On the buying side sits the demand-side platform, or DSP. A DSP is the advertiser’s control room: it lets brands and agencies decide which ad impressions to bid on, how much to pay, and what rules to follow—targeting, budgets, frequency caps, all of it. Instead of negotiating one publisher at a time, a DSP can evaluate and bid across huge swaths of the internet at once. If you want a mental model, it’s the advertiser’s trading desk.

On the selling side is the supply-side platform, or SSP. An SSP is the publisher’s agent. It helps a publisher take its inventory—those open slots on pages, in apps, or in streaming video—and expose it to as many potential buyers as possible. The goal is simple: create more competition for each impression so the price goes up. If the DSP is the buyer’s broker, the SSP is the seller’s.

Between them is the exchange: the marketplace where bids get routed, auctions run, and winners picked in real time (often using OpenRTB). The exchange is where the transaction actually happens. Bid requests fly out, bids fly back, and the winning ad gets served—fast enough that the user rarely notices anything happened.

This structure tends to produce a winner-take-most outcome. Not because anyone planned it that way, but because scale feeds on itself. The more publisher inventory an SSP aggregates, the more valuable it is to DSPs that want broad access. The more demand sources an SSP connects to, the more valuable it is to publishers that want higher bids. More volume leads to better liquidity, better performance, and—crucially—more leverage. If you don’t get big, you don’t just grow slower. You start to slide backward.

And then there’s the gravity of the duopoly. Google and Facebook aren’t just big participants; they’re ecosystems. They control massive pools of inventory and user data inside “walled gardens,” where they also influence how transactions happen. For everyone outside those walls, the open internet became a fight for oxygen.

One of the biggest attempts to claw back power from Google was header bidding. Publishers adopted it to avoid being trapped in Google’s old “waterfall” approach, where inventory was offered in a fixed sequence that often favored Google’s own tools. Header bidding let publishers invite multiple buyers to bid at the same time before handing the decision to the ad server. It worked—publishers made more money and gained more transparency—but it also put real strain on infrastructure and helped turn many ad formats into commodities, accelerating the margin squeeze across the industry.

By the mid-2010s, programmatic advertising had entered its Darwinian phase. Dozens of SSPs were fighting for the same publishers, take rates were under pressure, and consolidation started to look less like strategy and more like the price of survival. The boom years—when venture capital flooded in and ad tech IPOs seemed routine—were fading into a bust. And in that environment, the decisions Rubicon Project and Telaria made weren’t just business choices. They were existential moves.

III. The Rubicon Project Origins (2007-2014)

Rubicon Project began in 2007 with four co-founders: Frank Addante, Craig Roah, Duc Chau, and Julie Mattern. They’d worked together before at L90/adMonitor, an online advertising network, and they knew the problem firsthand: digital ads were already big business, but the market was still run like a street bazaar—opaque pricing, endless middlemen, and wildly inefficient matching between buyers and sellers. By April 2009, Rubicon had raised $33 million in venture funding led by Clearstone Venture Partners, IDG Ventures Asia, and Mayfield Fund.

Addante, in particular, came into Rubicon with credibility. He was an early pioneer in digital ad tech and a repeat entrepreneur, having founded four companies before Rubicon. In 2002, he founded StrongMail Systems, an email infrastructure provider backed by Sequoia Capital, and led it to market leadership. Before that, he was CTO and technology founder at L90, where he helped build one of the internet’s first ad serving platforms, adMonitor. After L90’s IPO, the company was acquired by DoubleClick.

That background shaped Rubicon’s founding mission. Addante set out to automate a massive online advertising market that was growing fast—but still operated with shocking inefficiency. The vision was elegantly simple: build a stock market-like exchange for advertising. Publishers had inventory they couldn’t monetize efficiently. Advertisers faced a fragmented maze of ad networks. Rubicon wanted to be the plumbing that connected them, with auctions and automation doing what relationships and guesswork used to.

Even the name was a signal. “Rubicon Project” was chosen to evoke a point of no return—Caesar crossing the Rubicon. This wasn’t supposed to be a feature company. It was supposed to reset how the whole market worked.

In the early years, Rubicon expanded aggressively, buying pieces that could fill out the platform. In September 2009, it acquired OthersOnline, an audience profiling technology company in Seattle. In May 2010, it bought Site Scout, a Seattle-based malware detection company. That October, Rubicon acquired Fox Audience Network from News Corp in exchange for a minority stake in Rubicon, and it also brought in $18 million of additional funding led by Peacock Equity, NBC Universal’s venture arm. In May 2012, Rubicon acquired Mobsmith, a mobile technology company—an early hint that it knew the next battleground wouldn’t just be desktop.

By August 2012, Rubicon hit a milestone that made the whole industry look twice: ComScore ranked it the top online advertising company by reach, with a 96.2% audience share. The rankings put Rubicon ahead of Google for the first time, and also ahead of AOL and AT&T. It was the high-water mark—the moment when Rubicon didn’t just feel like a fast-growing ad tech company, but like a real challenger.

But looming over that entire run was a single deal that had already changed the rules: Google’s 2007 acquisition of DoubleClick. DoubleClick was the center of gravity for the publisher side of the market, and once Google owned it, Google increasingly sat in a uniquely powerful position—able to influence how inventory was managed, how transactions flowed, and how value got captured. Vertical integration wasn’t just a strategy; it was a structural advantage that independent players would spend the next decade trying to overcome.

Rubicon went public in April 2014. It priced its IPO at $15 per share for 6,770,995 shares, raising about $102 million. The company, pitching itself as a leading digital ad exchange with the largest reach in the U.S., hit the market with momentum. The stock opened above $20, then drifted back down to around $16 later that month. On paper, it looked like a successful debut.

But the IPO also marked the end of the easy part of Rubicon’s story. Once public, the core tension in the business became impossible to hide: in a market where scale mattered above all else, Rubicon had to keep growing. Yet the very competition that made scale so valuable was also compressing margins across the industry. Growth demanded investment. Investment demanded economics. And the economics were getting squeezed.

Rubicon was stepping into a race where everyone had to run faster every year—while the finish line kept moving, and the price of each step kept falling.

IV. The Millennial Media Path (2006-2015)

While Rubicon was building its display advertising empire, another company was betting on a different future: mobile.

In 2006, Paul Palmieri and Chris Brandenburg founded Millennial Media out of Baltimore’s Emerging Technology Center. It was a bold, early call. The iPhone still hadn’t launched, but they could see where the screen time was headed. If the web had created an ad gold rush, mobile was going to create the next one.

Millennial set out to be the mobile equivalent of the big web ad networks. It built a large mobile advertising network that helped app developers and mobile publishers monetize their audiences. At its height, it employed roughly 575 people, headquartered in Baltimore with additional offices across major U.S. cities and international hubs including Hamburg, London, Paris, Singapore, and Tokyo.

In 2012, the bet seemed to be paying off. Millennial went public and briefly wore a valuation around $2 billion, raising more than $132 million in the offering. It was a snapshot of the era’s optimism: the belief that mobile ad networks would scale the way web ad networks had, just with more inventory, more growth, and more upside.

Then the ground shifted.

Facebook, after an early stumble in mobile monetization, figured it out in 2013. App install ads became the default way mobile developers bought users, powered by Facebook’s data and targeting advantage. And here’s the brutal part for a middleman like Millennial: Facebook didn’t just participate in the market, it owned the environment. It didn’t have to share economics with a network sitting between the advertiser and the user.

Millennial tried to buy its way to scale. Over time it accumulated assets through acquisitions including TapMetrics, Condaptive, Metaresolver, Jumptap, and Nexage. But instead of creating a clean, integrated machine, the strategy left the company bigger, more complex, and increasingly expensive to run.

By 2014, the financial strain was obvious. Millennial reported $296 million in revenue, up 14% year over year, but it also posted a net loss of $149 million—far worse than the $15 million loss the year before. Growth was still there on the surface. Underneath, the economics were breaking.

Leadership changed. On January 27, 2014, Palmieri stepped down and Michael Barrett took over as CEO. But the broader market forces weren’t easing up, and by 2015, the endgame arrived. On September 3, 2015, AOL agreed to buy Millennial Media for $238 million. The deal closed on October 23, 2015, and Millennial was folded into what AOL called ONE by AOL.

The contrast was stark: from a roughly $2 billion public-market moment in 2012 to a sub-$300 million sale just a few years later. Joining AOL—wrapping more ad tech around the network—wasn’t irrational. It was an admission that the standalone model was collapsing.

Millennial’s story is a clean lesson in how unforgiving ad tech can be. Being early to a platform shift doesn’t guarantee you get to own it, especially when the platform owners decide they want the profit pool for themselves. Millennial built a real business, but once Facebook and other walled gardens took control of mobile demand and data, the value of the middle layer evaporated fast.

And the most important thread for the Magnite story is the person at the center of Millennial’s final chapter. Michael Barrett had just watched a mobile ad company go from market darling to distressed sale. He’d seen how quickly a platform shift can turn into a trap. Soon, he’d be asked to attempt an even harder rescue—this time, with Rubicon.

V. Telaria's Birth from Tremor Video (2017)

Telaria didn’t start as Telaria. It started as Tremor Video, a company built around video advertising—back when “video” mostly meant pre-roll clips on desktop sites, not streaming apps on your TV.

By 2017, though, the video ad market was splitting into two very different businesses. On one side, the buy-side: the demand-side platforms that served advertisers. On the other, the sell-side: the supply-side platforms that helped publishers monetize their inventory. They looked similar from far away, but they required different technology, different relationships, and they answered to different customers.

Tremor chose a side.

In August 2017, it sold its buy-side business to mobile ad tech firm Taptica for $50 million. A month later, on September 26, 2017, the company rebranded as Telaria and began trading on the New York Stock Exchange under the ticker “TLRA.” CEO Mark Zagorski framed the change as a clean break: Tremor Video had built real brand equity, but it had also become closely associated with the DSP business they’d just sold. The new name and identity were meant to clarify what the company now was: a fully programmatic, sell-side software platform focused on premium video partners, and a leader in Connected TV/OTT.

Even the name was a signal. It came from the Greek “Talaria,” the winged sandals worn by Hermes, messenger of the gods—built for speed and distance. Telaria wanted to be the infrastructure that could carry advertising messages through an emerging video ecosystem, wherever and however people were watching.

And “wherever” was quickly becoming a living room.

The connected TV thesis was early, and it was right. Traditional television advertising was a $70 billion market in the United States alone, and every dollar that shifted from linear TV to streaming created a new opening for programmatic video. Telaria bet that premium video publishers—broadcast networks, cable channels, and the first wave of streaming services—would want independent technology to monetize digital video inventory without handing control to Google or Facebook.

This focus made Telaria a near-perfect complement to Rubicon. Rubicon’s business was largely split between desktop and mobile. Telaria, meanwhile, had a CTV business that was becoming the center of gravity. CTV grew from 8% of Telaria’s business in 2017 to 44% of annual revenue in 2019, reaching 60% in the first quarter of 2020. Over the same period, Telaria’s revenue climbed from $43 million in 2017 to $68 million in 2019.

Just as importantly, Telaria was building the relationships that matter most in video. These weren’t interchangeable display impressions. They were premium environments where brand advertisers paid up, and where publishers demanded control, transparency, and reliability from their tech partners. Telaria understood that CTV wasn’t just “display, but on a bigger screen.” It was a different product, a different sales motion, and a different kind of infrastructure.

But even with momentum, Telaria could see the ceiling. At around $68 million in annual revenue, it didn’t yet have the scale to build everything it would need—deeper demand connections, a larger sales organization, and the kind of platform footprint that could win in a consolidating market.

It needed a partner with complementary strengths. And soon, that partner would appear.

VI. Rubicon's Wilderness Years & Near-Death (2015-2019)

The years after Rubicon’s IPO were brutal. The company that once looked like it might challenge Google found itself fighting for oxygen. And the force that pushed it to the brink wasn’t a new competitor or a recession. It was a shift in how the auctions worked: header bidding.

In the beginning, header bidding was sold as liberation. Publishers could finally run a fairer auction before handing the decision to Google’s ad server. More buyers in the room at the same time meant higher prices and more transparency. Everyone cheered.

But on the SSP side, the celebration didn’t last.

Header bidding didn’t just open access to inventory. It changed the rules of the relationship. Once publishers could plug multiple SSPs into the same auction, they no longer needed to bet on a single “primary” partner. SSPs started to look less like strategic platforms and more like interchangeable pipes.

And when your product becomes a pipe, the only lever left is price.

In a world where an SSP wins more impressions by returning the highest yield to the publisher, lowering your take rate becomes the fastest way to stay in the game. That dynamic didn’t lift all boats. It drove a race to thinner and thinner margins.

Rubicon felt it immediately. Financial results worsened, and the company faced scrutiny and legal challenges tied to its historic take rate. Its average take rate sank to around 21% for the period—roughly 30% below its historic high—and was edging down toward just under 19% as the period closed. The stock tracked the pain. From post-IPO highs above $20, shares slid below $5, then below $2, and at points traded under $1—low enough to raise the specter of a Nasdaq delisting. The company that once boasted reach that rivaled Google was now battling for survival.

Inside the building, things weren’t calmer. In February 2017, Rubicon released its president and several other top executives, fueling the sense that the company was unraveling.

Then, in March 2017, Rubicon made the move that would define its next chapter: it brought in Michael Barrett as CEO. Barrett had just lived through the Millennial Media collapse and sale. He knew what it felt like when a platform shift turns your business model into dead weight. Rubicon’s founder, Frank Addante, stayed on as chairman, focused on long-term vision and strategy—but day-to-day, the turnaround was Barrett’s job.

From the outside, it looked like chaos. Addante pushed back on that impression. “I think it looks crazier for outsiders than what is actually happening here,” he said from the company’s New York office, as industry chatter swirled about Rubicon getting rolled up with other SSPs in a private equity consolidation deal.

Barrett addressed the rumors head-on. “No,” he said when asked if Rubicon was headed for a roll-up. “It’s flattering that our name gets mentioned a lot… inevitably our name will come up because we have $200 million in cash and we are doing well.”

His plan wasn’t glamorous, but it was realistic. Rubicon would stop pretending it could resist header bidding and instead lean into it. That meant transitioning toward a lower-margin, higher-volume model; cutting take rates to stay competitive; and rolling out a server-to-server header bidding solution to reduce the performance and latency headaches of client-side setups. Rubicon also invested in open-source through Prebid.org, helping set standards that benefited the whole ecosystem—including Rubicon.

The turnaround didn’t happen overnight. It was slow, painful, and it required the company to accept an uncomfortable truth: the old economics weren’t coming back. But over time, Barrett’s approach did something Rubicon desperately needed. It signaled to publishers and investors that Rubicon wasn’t going to disappear. It would be a stable, credible partner in a market that was littered with the remains of failed intermediaries.

By 2019, the immediate existential crisis had eased. Rubicon had stabilized. But stability wasn’t the same as a winning position. It was still a mid-sized SSP in a business that increasingly rewarded only one thing: scale. Operational fixes could keep Rubicon alive, but they weren’t enough to define the future.

The company didn’t just need to run better. It needed a reset.

VII. The Pivotal Merger: Rubicon + Telaria (2019-2020)

Rubicon didn’t just need incremental improvement. It needed a new shape.

In December 2019, Rubicon Project and Telaria announced they were merging. Shareholders approved the deal on March 30, 2020, and it closed on April 1. At first, the combined company still operated under the Rubicon Project umbrella and kept both brands in market. But by June 2020, it made the clean break official: the new name was Magnite. With that, the company could credibly claim a new title—world’s largest independent, omnichannel sell-side platform.

The strategic logic was straightforward: each side had what the other lacked. Rubicon had broad scale and deep infrastructure built through years of battling in the trenches of desktop and mobile. Telaria had something rarer and increasingly valuable: premium video relationships, especially in connected TV, where the inventory looked a lot less like commodity display and a lot more like modern television.

Barrett framed it as a way to escape the “sameness” problem that had plagued independent SSPs after header bidding made everyone feel interchangeable. “A lot of folks have said, ‘Hey Rubicon, you’re not that different from a PubMatic, OpenX or Index Exchange,’” he said. “And there has been a certain sameness for a group of players. After this merger, I don’t expect we’ll be hearing that, because there will be such a clear difference.”

The companies called it a merger, though the ownership split showed who was bigger at the time: Rubicon shareholders would own 52.9% of the combined company. Michael Barrett would be CEO. Telaria’s Mark Zagorski would become president and chief operating officer. The pitch to investors wasn’t just strategic—it was financial and operational, too. The combined company was expected to have roughly $150 million in cash and no debt, and management projected meaningful cost savings by eliminating duplicated public company expenses, consolidating contracts, and trimming overlap.

Just as important, the deal was all-stock. Neither company had the kind of balance sheet that made a big cash acquisition realistic. Stock was what they had, and using it did something else: it forced alignment. If this worked, both sets of shareholders would win together.

Both CEOs were careful to position the deal as a deliberate alternative to the private-equity roll-up rumors that had followed the sector for years. Barrett put it bluntly: “A strengthened balance sheet is part of the equation here. But I see a roll-up of SSPs through acquisition like that as foolish. The way to do it is to execute and have a superior offering, and the competition will atrophy.” Zagorski echoed the same idea from the publisher side: “We certainly like their balance sheet. But yes it’s about being the first door any publisher comes knocking on if they’re looking for an independent provider.”

Then came the timing—an element no management team gets to fully script, but every great business story seems to have.

The merger closed on April 1, 2020, just as COVID-19 lockdowns began reshaping daily life. People stayed home. Streaming surged. Connected TV viewing soared. And suddenly, the asset Telaria had spent years cultivating—CTV relationships with premium publishers—went from “smart bet” to “center of the universe.” Combined with Rubicon’s infrastructure and demand connections, the new company was positioned to ride a wave that had just been pulled forward by years.

In June 2020, the merged entity rebranded as Magnite. The name was meant to signal what the company wanted to be next: a platform with enough pull to attract both publishers and advertisers to one unified marketplace.

Frank Addante marked the moment publicly: “It’s official! We are excited to share that Rubicon Project and Telaria have become one company - the largest independent sell-side ad platform in the world: one company, every format, and an essential omnichannel partner.”

Under normal circumstances, the combined company would have had time to integrate, rationalize products, and slowly tell a new story to the market. Instead, the market moved first. The pandemic accelerated streaming adoption, sped up shifts in advertising budgets, and intensified the industry’s hunt for independent infrastructure. Magnite had been built for that moment—almost by accident—and for the first time in years, the company wasn’t just surviving the platform shift.

It was catching it.

VIII. The SpotX Acquisition: Going All-In on CTV (2021)

If the Telaria merger was about survival, the SpotX acquisition was about trying to win.

European media giant RTL Group agreed to sell SpotX, its U.S. ad-tech subsidiary, to Magnite for $1.17 billion in cash and stock. Magnite’s pitch was clear: with SpotX, it would “create the largest independent [connected TV] and video advertising platform in the programmatic marketplace.”

The price was split between $560 million in cash and 14.0 million shares of Magnite stock. Magnite planned to fund the deal with cash on hand, the shares issued to RTL Group, and committed financing from Goldman Sachs.

RTL knew SpotX well. It bought a 65% stake for €107 million in 2014, then took full control in 2017 by acquiring the remaining shares for €123 million—an enterprise value of $404 million at the time. Under RTL, SpotX became a real CTV force. But RTL ultimately decided its priorities were elsewhere: investing in European streaming and content rather than staying in the knife fight of U.S. ad tech.

SpotX came with a deep bench of customers: A+E Networks, Crackle Plus, the CW Network, Dentsu CCI, Discovery, Electronic Arts, Fox Corporation, FuboTV, Gannett, Microsoft, Newsy, ViacomCBS’s Pluto TV, Roku, Sling TV, and Vudu, among others. The Denver-based company said it worked with nearly all major OTT stakeholders and reached about 80% of ad-supported connected-TV viewers in the U.S., or 50 million households.

For Magnite, the strategic fit was almost too clean. CTV and video were already its growth engine, and SpotX was built for exactly that world. In 2020, 58% of SpotX’s revenue was tied to CTV.

On April 30, 2021, Magnite closed the acquisition. The company positioned the deal as a response to a market-wide demand: buyers and sellers wanted a scaled, independent alternative to the giants dominating CTV. With SpotX folded in, Magnite argued, that alternative now existed—across CTV first, but also across video, display, and audio.

“Scale and reaching the largest possible audience is the name of the game when attracting the demand our CTV and video clients need,” said Michael Barrett, President & CEO of Magnite. “Acquiring SpotX positions us to become the world’s largest, independent source of highly-coveted CTV and video inventory.”

Magnite also targeted more than $35 million in run-rate operating cost synergies, with over half expected to show up within the first year.

But this was not a free roll. To cover the cash portion, Magnite took on significant debt—something that started to feel a lot heavier as interest rates rose in 2022. And the integration challenge was real: Rubicon, Telaria, and SpotX were three major platforms with overlapping capabilities, different architectures, and different operating rhythms. The $1.17 billion price tag made it a clear statement of belief that CTV’s surge wasn’t a one-off spike, but the next durable profit pool in advertising.

On the other side of the risk, though, was the asset Magnite was really buying: relationships. Post-deal, the combined client roster included A+E Networks, AMC Networks, Crackle, Discovery, FOX, fuboTV, LG, Roku, Samsung, Sling TV, and Vizio. It read like a map of the streaming ecosystem—and it gave Magnite something independent ad tech companies rarely get to claim: premium supply at real scale.

IX. The Modern Era: CTV Wars & The Fight for Independence (2021-Present)

The streaming surge that began during COVID didn’t fade when the world reopened. It hardened into the new default for television—and it rewired where ad dollars could go.

The clearest sign was the one company that used to treat ads as heresy. In late 2022, Netflix launched its advertising tier. Disney+ followed. Paramount+, Peacock, Max—one by one, the major streamers either launched or expanded ad-supported offerings. For Magnite, each new ad tier wasn’t just another customer win. It was fresh, premium inventory entering the open programmatic market, and Magnite was positioned to help monetize it.

The biggest logo in that wave was Netflix. In early June 2024, Magnite announced a partnership with the streaming giant—one that analysts expected could add meaningful incremental CTV revenue in fiscal 2025. Magnite framed it as a validation of what it had been building since the Telaria merger and the SpotX deal: an independent CTV supply platform with enough scale, infrastructure, and credibility to work with the most demanding publishers in the world.

“We are thrilled to be helping Netflix leverage programmatic advertising to bring their amazing content to millions of consumers worldwide,” said Sean Buckley, Magnite’s Chief Revenue Officer.

Netflix, for its part, also signaled it wanted more control of its own stack. It announced an in-house advertising platform that includes an SSP relationship with Magnite and Netflix’s own ad server—designed to deliver the kind of personalization Netflix is known for, but applied to advertising. Netflix said its Netflix Ads Suite would launch April 1, 2025.

Barrett told investors he expected Magnite to outgrow the market, which he projected in the mid-teens, and that Netflix could become one of Magnite’s largest CTV clients by the end of 2025. In other words: this wasn’t just “nice to have” revenue. It was a potential cornerstone account in the category that now matters most.

At the same time, a very different force was reshaping the ground under everyone’s feet: regulation—specifically, the U.S. government’s antitrust case against Google.

In January 2023, the Department of Justice, joined by Attorneys General from several states and the Commonwealth of Virginia, filed a civil antitrust lawsuit accusing Google of monopolizing key pieces of the digital advertising “ad tech stack”—the tools publishers rely on to sell ads, and advertisers rely on to buy them. The complaint alleged Google spent more than 15 years using acquisitions and auction manipulation to weaken or eliminate competitors.

On April 17, 2025, a federal judge in Virginia ruled that Google established and maintained monopoly power through anticompetitive practices, siding with the DOJ’s argument that Google unlawfully tied together its ad tech tools and exchange services. Remedy fights followed fast: Justice Department attorneys pushed for divestitures of AdX (Google’s ad exchange) and DFP (DoubleClick for Publishers, its ad server). Google argued instead for behavioral remedies, calling the divestiture proposal “radical and reckless.”

For Magnite, this case is the ultimate wild card. If Google were forced to unwind parts of its ad tech stack, the market wouldn’t suddenly become easy—but it would change the rules. Independent SSPs would no longer be competing against a vertically integrated, bundled offering with built-in distribution advantages. They’d be competing in a market where the pipes are less owned by one company. And that’s the scenario where Magnite’s “independent” positioning goes from a nice tagline to a structural advantage.

While the industry debated what a post-Google-stack world might look like, Magnite’s own numbers were telling a quieter, more immediate story: the company had finally found operating leverage.

In Q4 2024, Magnite reported $194 million in revenue, up 4% year over year, and net income of $36 million. Adjusted EBITDA was $76.5 million—about a 42% margin—up from $70.4 million the year before. Contribution ex-TAC rose 9% to $180.2 million, with CTV contribution up 23% to $77.9 million.

This margin expansion is arguably the most important part of Magnite’s modern narrative. For years, Rubicon’s world was defined by thinning take rates, brutal competition, and a business model that struggled to translate scale into profit. Post-merger, post-SpotX, and with CTV becoming a larger share of the mix, Magnite started to look like a company that could do more than survive the ad tech wars.

It could actually make money in them.

X. The Technical Evolution & Product Strategy

Magnite’s product strategy evolved in lockstep with the industry’s underlying plumbing. As auctions moved from older, sequential “waterfalls” to header bidding, the next technical jump was just as important: shifting header bidding from the browser to the server. That change wasn’t a tweak. It reshaped who carried the complexity, who paid the infrastructure bill, and how fast auctions could run at scale.

Server-side header bidding aimed to fix what made early header bidding painful. Client-side setups could slow page loads and force trade-offs in auction logic, because every call had to happen in the user’s browser. Moving those connections into server infrastructure improved latency and scalability, and gave publishers and platforms more control over how the auction behaved. Mechanically, it looked like the integrations SSPs and DSPs had been doing for years—except now, SSPs increasingly had to interoperate with each other to make the whole market function. As publishers adopted header bidding, many saw meaningful lifts in programmatic revenue, and server-side approaches were positioned as the next step in making that model sustainable.

Underneath all of this, Magnite’s real product story was integration. After combining Rubicon, Telaria, and SpotX, it needed more than a shared logo—it needed a shared engine. That’s what the DV+ platform represented: a unified auction layer intended to bring the company’s post-consolidation footprint onto a single stack, spanning display, mobile, video, and CTV across billions of daily ad requests.

CTV, in particular, forced different engineering decisions than display ever did. The user experience is less forgiving: nobody wants to see the same ad repeated endlessly in the middle of long-form content. Measurement is harder, too, because the screen where you watch isn’t always the screen where you buy, and cross-device tracking doesn’t behave like it does on the web. Even the creative expectations shift in the living room, where ads look and feel more like television than banners or short-form mobile clips. In CTV, the “auction” is only part of the problem; the rest is making the whole system feel seamless to viewers and predictable to buyers.

To push further into that complexity, Magnite introduced a next generation SpringServe CTV platform, in beta testing. As Magnite described it, the goal was to combine the features of its streaming SSP and its ad server so buyers could connect to premium CTV supply more efficiently—less friction, fewer handoffs, tighter control.

Then there’s identity—still the open internet’s recurring crisis. Even as Google postponed and then modified its plans to deprecate third-party cookies, the scare forced the market to invest in alternatives. Magnite emphasized where it thought the world was heading anyway, especially in streaming. Barrett described CTV as “predominantly a first-party world,” where publisher relationships and direct data access matter more than legacy cookie-based targeting.

That’s also why partnerships with premium publishers have become such a core part of Magnite’s product strategy. Magnite announced a two-year extension with Disney that added live sports and expanded into additional regions. Deals like that aren’t just about routing bids. They tend to involve deeper integrations—yield management, audience tools, and longer-term alignment—because premium streaming companies care as much about control and consistency as they do about price.

And that brings us to Netflix. Magnite framed the partnership as a validation of everything it had been building: CTV infrastructure that can operate at the highest end of the market, plus the operational credibility to support a publisher that wants performance, transparency, and control. Netflix wasn’t looking for a generic pipe. It was looking for a partner that could meet it where it is—and plug into where streaming is going.

XI. Business Model Deep Dive & Unit Economics

To understand Magnite, you have to understand how an SSP gets paid—and why “getting big” isn’t a vanity metric in this business. It’s the whole game.

At the center is the take rate: Magnite keeps a percentage of each ad transaction that runs through its platform and passes the rest back to the publisher. If an advertiser pays $10 for an impression, Magnite keeps a slice and the publisher gets the remainder. Magnite disclosed a 14.5% take rate before 2020 and continued to reference it in subsequent years. Around 2017, the company concluded that programmatic still had massive runway, and that being a more transparent SSP could earn publisher trust—and, in turn, attract more ad spend from agencies and advertisers.

That take rate isn’t uniform. It’s a blend, and the mix matters. Connected TV typically carries better economics than commodity display because the inventory is scarcer and more premium: brand-safe environments, television-like creative, and major publishers who care deeply about control and quality. As Michael Barrett put it: “I think we’ve been clear that our take rate is a blend. Different media types and auction types carry different take rates, and the market has anointed that as the sane model.” Mark Zagorski made the same point from another angle: “Even within our own business we see a huge difference between programmatic types like a direct guaranteed deal compared to an open auction.”

Then comes the part that makes ad tech so brutal—and so consolidating: scale economics.

Running an SSP isn’t cheap. You’re building and maintaining a real-time marketplace, paying for infrastructure, integrating with DSPs, publishers, and measurement partners, and constantly upgrading the tech to handle more traffic with less latency. A lot of those costs are fixed or semi-fixed. So the bigger the transaction volume, the more you can spread those costs out—and the more room you have to compete on price without destroying the business. That’s why the market keeps drifting toward winner-take-most outcomes: the biggest platforms can offer better economics and still keep meaningful profit dollars.

Magnite has been leaning hard into that operating leverage. The company reported a 30% reduction in cost per ad request versus the prior year, driven by improved filtering and traffic-shaping technology. In a business where margins can get squeezed one basis point at a time, lowering unit costs like that is the difference between “scale story” and real profitability.

Finally, there’s the most important mix shift in the whole Magnite narrative: CTV. Moving from display-heavy volume to more CTV doesn’t just change the growth rate—it changes the unit economics. CTV impressions are higher value, tend to command higher CPMs, and generate more absolute dollars per transaction. As CTV becomes a larger share of the business, margins don’t just improve. They start to compound.

Key Performance Indicators for Investors:

If you’re watching Magnite quarter to quarter, two metrics tell you the most about whether the thesis is working:

-

CTV Contribution ex-TAC growth rate: This is the cleanest window into Magnite’s highest-margin, most strategically important segment. In Q4 2024, CTV contribution grew 23% to $77.9 million. If that keeps climbing, it’s a sign Magnite is winning where it matters most.

-

Adjusted EBITDA margin: This is the scoreboard for whether scale is finally translating into profit. Magnite posted a 42% adjusted EBITDA margin in Q4 2024—a level of profitability that would’ve been hard to imagine during Rubicon’s near-death years. If margins hold or expand from here, it suggests the integration and the CTV mix shift are doing what they were supposed to do.

XII. Competitive Landscape & Strategic Positioning

The competitive landscape in sell-side ad tech is defined by one overwhelming reality: Google.

In January 2023, the U.S. Department of Justice filed a civil antitrust suit accusing Google of monopolizing multiple digital advertising technology products. The complaint centers on what the industry calls the “ad tech stack”—the connected set of tools publishers use to sell ads and advertisers use to buy them. The basic allegation is that Google used its position across the stack to tilt the playing field in its favor.

Even without a courtroom, you can see why independent platforms feel boxed in. Google Ad Manager (formerly DoubleClick for Publishers) remains the dominant ad server for premium publishers. And its bundled approach—ad serving plus built-in demand from Google’s ecosystem—creates structural advantages that are hard for independent SSPs to match, especially when every millisecond of latency and every basis point of take rate matters.

That’s the backdrop Magnite is selling into when it calls itself “the world’s largest independent omni-channel sell-side advertising platform, offering a single partner for transacting globally across all channels, formats and auction types, and the largest independent programmatic CTV marketplace.” In other words: if you’re a publisher who wants scale but doesn’t want to hand the keys to Google, Magnite wants to be the most credible alternative.

Among independents, PubMatic is the closest like-for-like competitor. PubMatic leans into an infrastructure-first identity, arguing that owning and operating its own global software and hardware footprint “allows for the efficient processing and utilization of data in real time,” and “saves significant infrastructure expenditures as compared to public cloud alternatives.” It’s a distinct pitch: control your own costs, run faster auctions, and keep more of the economics.

In the field, publishers often treat Magnite and PubMatic as two of the few “must evaluate” independents. One large digital publisher reported a 7% increase in effective CPM for inventory managed by Magnite compared to Google. Their Head of Ad Operations summed it up plainly: “It wasn’t a silver bullet, but it proved that having an independent SSP in our stack brought real incremental value and transparency.” PubMatic, for its part, is frequently credited with strong customer support and hands-on account management, a clear focus on publisher revenue optimization, robust header bidding capabilities, and a commitment to transparency. Magnite’s edge tends to show up where the dollars are migrating fastest: larger overall scale, and a more established position in CTV/OTT.

Then there’s The Trade Desk—arguably the most complicated relationship Magnite has. Trade Desk is the dominant independent DSP, which makes it both partner and potential threat. It sends demand to Magnite’s publisher clients, but it’s also pushing to tighten the supply chain with initiatives like OpenPath, its direct-to-publisher offering, along with a plan to turn off Google Open Bidding as part of supply path optimization. Put together, those moves raise the uncomfortable question for every SSP: if buyers can connect “direct,” are SSPs still essential infrastructure—or just another tollbooth to eliminate?

Magnite’s view is that SPO doesn’t remove the need for SSPs so much as it concentrates power into fewer of them. GroupM’s Premium Marketplace product is a good example: it offers advertisers a more direct connection to publisher inventory, but it still relies on SSP partners like Magnite or PubMatic. Magnite CRO Sean Buckley has argued that the real trend is consolidation toward a small set of trusted, scaled partners, not the disappearance of the category. “This theme of consolidation is going to drive spend toward scaled, well-resourced companies with broad-based capabilities on the supply side,” Buckley said.

You can also see Magnite adapting product-wise to that world. It launched ClearLine, and PubMatic later debuted Activate—offerings that effectively gave media owners a route to market without relying on a DSP in the traditional way. Magnite also announced integrations between its video ad server SpringServe and OpenPath, as well as BackStage, Yahoo’s equivalent of OpenPath. Rather than treating The Trade Desk’s direct path as an existential attack, Magnite leaned into interoperability and tried to position itself as the enabling layer that makes “direct” actually work at scale.

Finally, there’s Amazon—another gravitational force, and one that’s easy to underestimate until it’s too late. Amazon DSP has been building direct publisher relationships, and Amazon’s owned-and-operated inventory across properties like Twitch, IMDb TV, and Fire TV brings enormous scale. For now, Amazon appears focused on its own properties and its retail media network. But if it ever decides to push aggressively into third-party publisher monetization, it wouldn’t just add competition. It would redraw the map.

XIII. Porter's Five Forces Analysis

Competitive Rivalry: HIGH

This is a knife fight.

The SSP market is crowded, commoditized, and brutally price-sensitive. Google’s vertical integration gives it advantages independents can’t copy: it can bundle, it can steer demand, and it can shape the rules of the marketplace it participates in. Meanwhile, competition between independents has steadily compressed take rates—the same “race to zero” dynamic that nearly finished off Rubicon.

And the pressure doesn’t just come from other SSPs. The Trade Desk’s growing influence on the buy side spills over into the sell side, too. As DSPs push “direct” connections to publishers, the unspoken goal is disintermediation: fewer middle layers, fewer fees, more control.

The twist is that “independent” has become more than a slogan. Publishers increasingly see the conflict in relying on Google as both the infrastructure provider and the dominant source of demand. As antitrust scrutiny of Google has intensified, the value of credible alternatives has risen right along with it.

Threat of New Entrants: LOW-MEDIUM

Starting an SSP from scratch is hard for the same reason running one is hard: the physics are unforgiving.

You need massive infrastructure, years of engineering, and deep integrations across the ecosystem—hundreds of demand connections, thousands of publishers, and the operational know-how to run real-time auctions at huge scale without breaking latency budgets. This isn’t a weekend project, and it’s not a market where a small team can quietly “ship and iterate” their way to relevance.

But the real threat doesn’t come from startups. It comes from giants making lateral moves. A company like Amazon already has advertisers, data, distribution, and compute. If it chooses to push deeper into third-party publisher monetization, it can become a serious player fast—not because the market is easy, but because it can afford the cost of entry.

Supplier Power: MEDIUM-HIGH

On the supply side, the crown jewels are premium publishers—especially streaming platforms.

Netflix, Disney, and other major CTV players control inventory that advertisers actively fight to access. That gives them leverage. They can negotiate aggressively on pricing, transparency, controls, and service levels. And because their brands are on the line, these relationships aren’t “set it and forget it.” They require constant attention and ongoing performance.

At the same time, publishers also need leverage against Google. When so much of digital advertising runs through the duopoly, relying entirely on Google’s tools can leave publishers boxed in. That’s where Magnite’s pitch lands: scale plus independence can be valuable even to the biggest sellers, not just the long tail.

Buyer Power: HIGH

Buyers—advertisers and agencies—hold plenty of cards.

They can shift budgets quickly, demand lower fees, and push for greater transparency. Supply path optimization is basically institutionalized buyer power: an ongoing campaign to reduce intermediaries and compress the “tax” across the chain. Platforms like Google and The Trade Desk amplify that leverage by concentrating demand and standardizing buying decisions.

CTV does soften the dynamic somewhat. Premium streaming inventory is scarce in a way display inventory never was. There are only so many ad slots in a night of must-watch TV, and brand advertisers have limited substitutes if they want those environments. Scarcity doesn’t erase buyer power—but it does give sellers more room to hold the line than they have in open-web display.

Threat of Substitutes: MEDIUM

There are two big substitutes for an independent SSP.

First: direct deals. Publishers and advertisers can bypass programmatic altogether with traditional, negotiated buying—especially for premium inventory. Second: walled gardens. Google, Meta, and Amazon keep huge amounts of inventory inside their own systems, shrinking the slice of the market that independents can even compete for.

But programmatic has one enduring weapon: efficiency at scale. Automation, targeting, measurement, and the ability to transact instantly across thousands of properties are hard to replicate with humans and spreadsheets. Direct will always exist, and walled gardens will always siphon spend—but over the long arc, the market keeps drifting toward software.

XIV. Hamilton's 7 Powers Analysis

Scale Economies: ★★★★☆

Magnite’s biggest structural advantage is that it runs at a size where the unit costs start bending in its favor. Building the platform, running the infrastructure, and maintaining integrations across the ecosystem are expensive, largely fixed commitments. But when you spread those costs across billions of daily ad requests, the math looks very different than it does for a smaller SSP.

You can see it in the margin story. As Magnite grew, it didn’t need to grow headcount and infrastructure dollar-for-dollar with transaction volume. That operating leverage is what helped turn “scale” from a talking point into expanding adjusted EBITDA margins.

Network Effects: ★★★☆☆

Magnite is a two-sided marketplace, and it does get the classic flywheel: more supply attracts more demand, and more demand makes the platform more valuable to supply. The catch is that SSP network effects are real, but not magical.

Once you’re plugged into most major DSPs, adding another buyer is incremental, not transformative. And because demand is fragmented across agencies, DSPs, and buying models, the value tends to build more linearly than exponentially. This isn’t a social network. It’s market plumbing.

Counter-Positioning: ★★☆☆☆

Magnite isn’t winning because it invented a new business model. It’s winning by executing the SSP model, then reshaping itself through consolidation and a CTV pivot. Its “independent” pitch matters—especially when publishers want alternatives to Google—but it’s not counter-positioning in the strict Helmer sense. Google could choose to behave more neutrally. It just doesn’t have an incentive to.

Where Magnite did show something closer to counter-positioning was in its early CTV emphasis. Display-centric competitors couldn’t instantly become credible partners to premium video and streaming publishers without changing what they built, how they sold, and who they served.

Switching Costs: ★★★☆☆

Once a publisher is deeply integrated with Magnite—especially if Magnite is embedded into reporting, yield workflows, and day-to-day operations—switching isn’t painless. There’s technical work, operational risk, and time spent rebuilding a machine that already runs.

CTV raises the stakes. Those integrations are typically more complex than display, which increases switching costs where Magnite makes its highest-value revenue. But there’s a ceiling to lock-in: publishers often multi-home across several SSPs, keeping optionality and limiting any one partner’s control.

Branding: ★★☆☆☆

In B2B ad tech, brand rarely beats performance. Publishers follow yield, reliability, and service, not vibes.

That said, “independent” has become a meaningful piece of positioning as antitrust pressure builds and publishers look for leverage. And premium CTV credibility does travel. Being an SSP partner to the biggest streamers signals to other enterprise publishers that Magnite can operate at the top end of the market.

Cornered Resource: ★★★★☆

This is Magnite’s strongest power: premium CTV relationships and the inventory that comes with them.

Magnite and SpotX serve major programmers, broadcasters, platforms, and device manufacturers, including Disney/Hulu, Fox Corporation, Roku, Samsung, ViacomCBS, and WarnerMedia. Those relationships aren’t something you can buy off the shelf. They’re built over years of trust, integration work, and proving you can deliver yield without sacrificing control or brand safety.

That first-mover advantage matters because in CTV, access is the product. And access, once earned, is hard to displace.

Process Power: ★★★☆☆

Magnite has also shown real operational competence in one of the hardest things to do in ad tech: integrate big acquisitions without blowing up the customer base.

Combining Rubicon, Telaria, and SpotX meant merging cultures, tech stacks, and go-to-market motions while keeping auctions running and publisher revenue steady. Pulling that off suggests an institutional capability that’s valuable in a consolidating industry.

It’s not untouchable, though. Well-funded competitors can develop similar integration muscles over time.

Overall Assessment: Magnite’s moat comes primarily from Scale Economies and Cornered Resource—its CTV relationships and access to premium supply. The company is tougher than it looks from the outside, but it operates inside a structurally punishing market where Google’s dominance caps everyone’s power. And hovering over all of it is the wild card: if the Google antitrust case materially changes how the stack works, Magnite’s “independent” identity could shift from marketing line to genuine structural advantage.

XV. The Bull vs. Bear Case

The Bull Case:

CTV advertising is still in the early innings. Streaming keeps taking share, linear TV keeps fading, and every dollar that migrates from the old world into the new one is a chance for Magnite—because CTV is where its product is strongest and its economics are best. If the market grows at a steady mid-teens clip, Magnite doesn’t need to invent a new category. It just needs to keep riding the shift it helped enable.

A Google antitrust breakup could be a once-in-a-generation tailwind. If regulators force meaningful divestitures—especially around Google Ad Manager—the biggest structural advantage Google has enjoyed for years starts to weaken. The bundling that quietly nudges publishers toward Google’s exchange becomes harder to defend. In that world, “independent” stops being a marketing adjective and starts looking like a durable competitive position.

Magnite is one of the only independent SSPs with global scale. PubMatic is the closest peer, but smaller. Many others are either owned by larger strategic parents—like FreeWheel under Comcast or Xandr under Microsoft—or simply don’t have comparable breadth across formats and geographies. If the market keeps consolidating around a handful of trusted pipes, being one of the last big independents could be an advantage that compounds.

The margin story may not be finished. That 42% adjusted EBITDA margin in Q4 2024 is less a victory lap than proof the model can finally throw off real operating leverage. If integration drag continues to fade and CTV keeps becoming a larger share of the mix, it’s not hard to see a path to further improvement.

And management has earned some credibility here. Barrett didn’t inherit a stable company; he inherited a business that had flirted with irrelevance. The Telaria merger and SpotX acquisition were huge integration bets, and the business kept running through them. In ad tech, where execution mistakes are often fatal, that track record matters.

The Bear Case:

Google and Amazon could decide the game is over for independents. Both have the resources, distribution, and incentives to push deeper into third-party publisher monetization if they choose. If either one turns this into a priority—by pricing aggressively, bundling more tightly, or acquiring their way into premium supply—Magnite’s “independent alternative” positioning may not be enough.

The Trade Desk is a partner, but it’s also a pressure point. Its push to treat SSPs as interchangeable middle layers isn’t just rhetoric; when the buy side starts dictating which supply paths “count,” it can squeeze fees and bargaining power across the sell side. For Magnite, the risk isn’t that demand disappears overnight—it’s that the economics get negotiated down, one procurement decision at a time.

Major streaming platforms could increasingly go in-house or go direct. The very relationships that make Magnite valuable also create concentration risk. If a small number of large customers change strategy, bring more of the stack inside, or use their leverage to push for better terms, Magnite can feel it quickly—and there’s not always an easy way to replace premium CTV volume at the same economics.

The post-cookie world tilts toward walled gardens. As third-party tracking degrades and privacy regulation tightens, first-party data becomes even more valuable. Google, Amazon, and Meta sit on enormous consumer identity graphs. Magnite doesn’t have that kind of direct relationship with end users, and a privacy-centric future could concentrate power even further in the hands of platforms that do.

Debt still matters. SpotX was a big swing, and it came with borrowing. Rising rates made that burden heavier in 2022, and while Magnite has been paying debt down, leverage limits flexibility. In a cyclical business like advertising, a balance sheet constraint can show up at exactly the wrong time.

What to Watch:

Take rate trends. Is Magnite holding the line, or are competitive pressures quietly compressing the business again?

Customer concentration—especially Netflix. Does it become a true growth engine, or does it become a negotiation lever that squeezes economics?

The Google antitrust timeline and remedies. Even after rulings, appeals can take years—but the shape of any remedy could redefine the playing field.

Free cash flow conversion and debt paydown. Adjusted EBITDA is nice; cash that reduces leverage and restores flexibility is what changes the strategic options.

XVI. Key Lessons & Takeaways (The Playbook)

Survival through consolidation: Sometimes you merge because the alternative is slow-motion failure. Rubicon and Telaria each had real strengths, but neither had enough scale, on its own, to endure a consolidating market. Together, they became something the industry could take seriously. The lesson here is humility: knowing when the standalone path is narrowing, and having the discipline to find a partner whose advantages cover your blind spots.

Platform shifts create opportunities: CTV didn’t just help Magnite grow; it gave the entire company a second life. The same business that was getting crushed as header bidding turned display into a commodity found a new arena where premium inventory, trust, and execution mattered more than shaving take rates. Platform transitions always reshuffle the deck. The winners are usually the ones building for the next wave, not defending the last one.

Independence as strategy: Being the alternative to a monopoly can be a real product. Publishers want leverage against Google. Buyers want transparency and choice in how ads get bought and sold. Magnite’s independence isn’t window dressing; it’s a positioning that, in the right regulatory and market environment, can translate into durable demand from both sides of the marketplace.

Scale matters in two-sided marketplaces: You don’t get to be “medium-sized” for long. SSP economics reward volume: fixed costs spread out, more liquidity attracts more participants, and operating leverage finally shows up when the platform is big enough. Smaller players don’t just grow slower—they can get trapped in a downward spiral of weaker performance, weaker economics, and lost share.

Timing and luck matter: Magnite built toward CTV early, but it also caught a massive tailwind. The Telaria merger closed right as COVID pulled streaming adoption forward. And the Netflix partnership emerged as Netflix committed to advertising. Strategy sets the table; timing decides whether the meal actually gets served.

Integration execution is make-or-break: Big acquisitions don’t create value automatically—they create complexity automatically. Rubicon, Telaria, and SpotX could have become three overlapping stacks and three competing cultures under one ticker. Instead, Magnite managed to integrate without blowing up customer relationships or the core platform. The unglamorous work—systems, teams, processes—often matters as much as the deal itself.

Market structure matters: Great execution can’t fully outrun a structurally punishing industry. SSPs live under permanent pressure from a vertically integrated giant, and that reality limits everyone’s freedom. The Google antitrust case is Magnite’s biggest potential structural catalyst, but it’s also completely outside management’s control.

The last one standing: Sometimes the “strategy” is simply refusing to die long enough for the market to change. Millennial Media vanished. Many SSPs were acquired, rolled up, or faded into irrelevance. Magnite and PubMatic remain the scaled independent alternatives. Survival is not the same as victory—but in ad tech, survival is often the prerequisite for getting a chance at one.

XVII. Epilogue: What's Next for Magnite and Ad Tech?

What happens next in ad tech will be driven by forces that no single company controls—platform policy shifts, privacy regulation, the streaming wars, and now AI. But Magnite’s whole pitch is that it’s built to be useful in chaos. If you’re the independent infrastructure layer, you don’t have to predict the future perfectly. You just have to stay essential as the pieces move.

AI is the newest piece on the board, and it cuts both ways. Large language models could change how ads are created, how campaigns are managed, and how performance gets analyzed. For Magnite, the more immediate impact is operational: better auction optimization, sharper fraud detection, and smarter traffic shaping. The company has already pointed to meaningful efficiency gains from AI-powered filtering. But the bigger question is whether AI eventually rewires the stack itself—compressing or bypassing the layers that exist today. In that world, “being the best pipe” might not be enough if the whole routing system gets redesigned.

At the same time, retail media networks have become one of the fastest-growing pockets of digital advertising. Walmart, Amazon, Target, and others are building ad businesses on top of something the open internet can’t easily replicate: first-party purchase data. That’s a threat, because it’s more ad budget flowing into walled gardens. It’s also a potential opportunity, because once retail media wants to reach beyond its owned-and-operated properties, it needs technology partners to help transact and measure across the broader ecosystem—exactly where independent infrastructure can matter.

Then there’s privacy, still the industry’s never-ending plot twist. Google’s repeated delays on third-party cookie deprecation—and its eventual pivot to a modified approach—proved how unpredictable the “cookieless future” really is. Magnite has been betting that streaming will be less exposed to that chaos because CTV is “predominantly a first-party world,” where identity and targeting are more tied to the publisher relationship than to browser-level tracking. That reality favors platforms that are deeply embedded with premium content owners, and it raises the value of Magnite’s CTV footprint.

From here, Magnite’s endgame could take a few different shapes:

Acquisition target: Magnite’s CTV relationships and “independent alternative” positioning could be attractive to an acquirer that wants a stronger foothold in advertising. A strategic player like Microsoft (which owns Xandr), an expanding ad giant like Amazon, or private equity looking to consolidate the sector could all plausibly see it as valuable.

Continued independence: Magnite keeps doing what it’s been doing—grow CTV, protect margins, ride the continued expansion of ad-supported streaming, and potentially benefit if Google’s antitrust remedies create more room for independent platforms.

Roll-up acquirer: With a public currency and a management team that has already proven it can integrate big, messy platforms, Magnite could decide the next phase of the industry is something it drives—buying smaller players and pulling more of the market under one roof.

If Magnite is going to “win big,” a handful of things would have to break its way. CTV would need to keep expanding. Take rates would need to stabilize or improve. Relationships like Netflix would need to deepen and broaden. The Trade Desk’s direct-to-publisher push would need to top out rather than fully disintermediate the middle. And the biggest wildcard of all—the Google antitrust case—would need to produce remedies that actually change market structure, not just headlines.

None of that is guaranteed. But that’s what makes Magnite such an interesting company to study. It’s a business that nearly fell off the map—its core product commoditized, its economics squeezed, its competitors bigger and more entrenched—and still managed to survive long enough to catch the next platform shift. Whether survival turns into enduring value is the unanswered question. But as a case study in strategy, consolidation, and the brutal math of two-sided marketplaces, Magnite is hard to beat.

XVIII. Outro & Further Reading

Top 10 Resources for Deep Dive:

-

"Subprime Attention Crisis" by Tim Hwang — A sharp, readable explanation of why the attention economy is structurally fragile, and why ad tech is always closer to a reckoning than it looks.

-

Google antitrust case documents (DOJ vs. Google, ad tech monopolization) — The closest thing to a “primary source” on how the modern ad stack works, and what regulators think Google did to dominate it.

-

Magnite SEC filings — Start with the S-4 for the Telaria merger and the 8-Ks around the SpotX acquisition, then use quarterly earnings to track how the integration and CTV shift show up in the numbers.

-

Eric Seufert's Mobile Dev Memo — Consistently strong analysis on mobile and the premium end of ad tech, with a useful lens on platforms, incentives, and where value actually accrues.

-

The Trade Desk S-1 and annual letters — A clear window into the buy-side worldview, and why DSP strategy increasingly shapes what happens on the sell side.

-

"Chaos Monkeys" by Antonio García Martínez — A chaotic, inside-the-building view of Facebook’s ad machine and the culture that helped it win mobile.

-

IAB (Interactive Advertising Bureau) reports — The practical layer: standards, definitions, CTV measurement frameworks, and the benchmarks the industry rallies around.

-

Luma Partners' Display Lumascape — The map of the territory: who’s in the stack, where consolidation is happening, and how crowded everything still is.

-

AdExchanger.com archives — The best running history of modern programmatic: deals, pivots, and the moment-by-moment story of how the pipes got built.

-

Stratechery by Ben Thompson — “Aggregation Theory” is one of the cleanest explanations for why platforms like Google and Meta pull value toward themselves—and what it would take for that gravity to weaken.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube