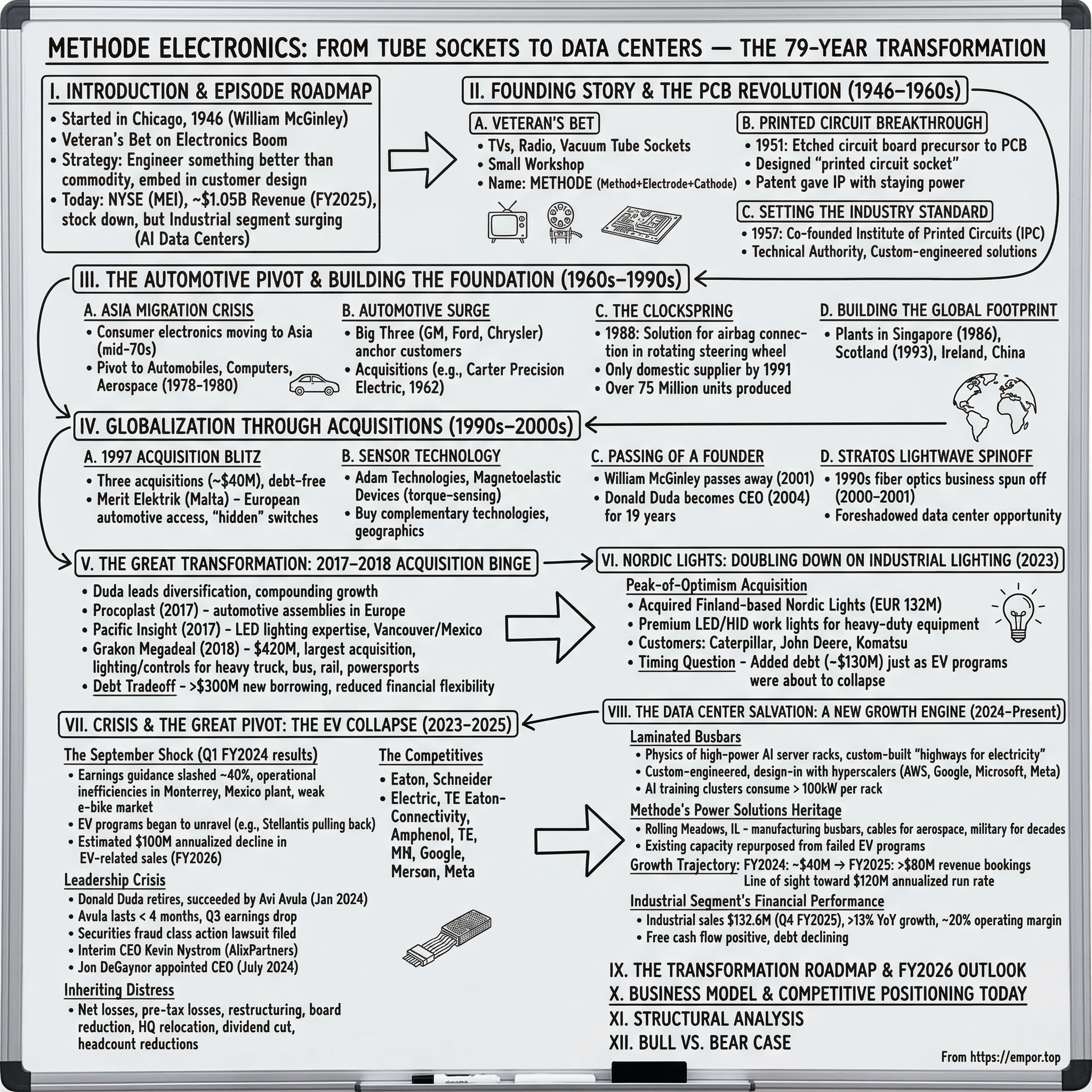

Methode Electronics: From Tube Sockets to Data Centers — The 79-Year Transformation

I. Introduction & Episode Roadmap

Picture a small workshop on the south side of Chicago in 1946. The war is over, the boys are home, and a young veteran named William McGinley is pouring his savings into a bench, some tools, and a bet on a tiny component most Americans have never thought about: the vacuum tube socket.

Fast forward nearly eight decades, and the company McGinley built — Methode Electronics — is a billion-dollar enterprise shipping laminated copper busbars into the server racks powering artificial intelligence, LED lighting systems into Caterpillar mining rigs, and sensor assemblies into the dashboards of vehicles on six continents. The arc from tube sockets to AI infrastructure is almost absurd in its breadth. And yet there is a remarkably consistent thread connecting McGinley's 1946 workshop to the company's 2026 transformation: engineer something better than the commodity alternative, then embed yourself so deeply in the customer's design that ripping you out costs more than keeping you.

The question at the heart of this story is deceptively simple: how does a company survive — let alone thrive — across eight decades of relentless technological upheaval?

Today, Methode Electronics trades on the NYSE under the ticker MEI. Fiscal year 2025, which ended in May 2025, brought in roughly $1.05 billion in revenue. The stock has shed approximately eighty percent of its value from its early 2023 peak, punished by collapsing EV demand, leadership turnover, and operational stumbles. And yet, the company's Industrial segment — powered by surging data center power product sales — just posted record numbers and nearly twenty percent operating margins. The transformation underway is as dramatic as any in Methode's long history.

This is a story about innovation, acquisitions, automotive dominance, and an urgent pivot to data centers. It is also a story about the brutal economics of being a mid-cap component supplier squeezed between trillion-dollar customers and multi-billion-dollar competitors.

The themes that will echo through this narrative are remarkably consistent: engineering innovation creating temporary competitive advantage, strategic acquisitions expanding capability and geography, customer concentration creating both opportunity and vulnerability, and leadership transitions that either accelerate or derail transformation. Every chapter in Methode's story touches all four themes.

Whether Methode emerges from this inflection point as a case study in industrial resilience or a cautionary tale about execution risk is the billion-dollar question — and the reason this company rewards a deep look.

II. Founding Story & The PCB Revolution (1946–1960s)

A Veteran's Bet on the Electronics Boom

In the winter of 1946, William Joseph McGinley came home from the war with a mechanical mind, a restless ambition, and not much capital. Born in Hinsdale, Illinois, in 1923, McGinley had served his country and now wanted to serve the postwar consumer electronics boom that was electrifying American living rooms.

Television sets were the iPhone of the late 1940s — transformative, aspirational, and hungry for components. Every set needed vacuum tubes, and every vacuum tube needed a socket to plug into. McGinley scraped together roughly a thousand dollars of his own money. A partner, Clement Newgent, added another twenty-five hundred. With less than four thousand dollars in total seed capital, Methode Electronics opened its doors on the south side of Chicago.

The name itself was a piece of clever wordplay: "Methode" combined the ideas of manufacturing method, electrode, and cathode — the functional guts of the vacuum tubes they were building sockets for. It was a name that said, "We are engineers first, manufacturers second." That identity would prove remarkably durable.

The Printed Circuit Breakthrough

For the first five years, Methode was a classic postwar small manufacturer — making tube sockets for the radio and television makers driving America's consumer electronics explosion. The timing was perfect, but McGinley understood that making commodity sockets was a race to the bottom. Every year brought new competitors, many of them willing to undercut on price. He needed something proprietary — a product or process that competitors could not easily replicate.

The breakthrough arrived in 1951. The U.S. Army Signal Corps had recently introduced the etched circuit board — the precursor to the modern printed circuit board, or PCB. For those unfamiliar with the technology, think of a PCB as the nervous system of any electronic device: a flat board with thin copper pathways printed onto it, connecting components without the tangle of individual wires that had previously characterized electronic assembly.

Before PCBs, assembling a radio or television meant hand-soldering dozens of individual wire connections — slow, expensive, and error-prone. The printed circuit board replaced all of that with a single, precisely manufactured board where the "wires" were copper traces etched directly into the surface.

McGinley recognized the significance immediately and designed what he called a "printed circuit socket" — a component that allowed a vacuum tube to plug cleanly into a printed circuit board rather than being soldered directly. This was not just a product innovation but a manufacturing process innovation. Methode pioneered printing and etching techniques that made it possible to produce PCBs at volume, cheaply and reliably, for consumer electronics.

The patent on the printed circuit socket gave Methode something rare for a small Chicago shop: intellectual property with staying power. More importantly, it positioned the company at the intersection of two booming industries — consumer electronics and the nascent printed circuit board manufacturing sector. While competitors were still hand-wiring assemblies, Methode was automating. While others sold generic sockets, Methode sold a patented interface between the old technology (vacuum tubes) and the new technology (printed circuit boards). It was, in a sense, the company's first bridge product — a theme that would recur throughout its history.

Setting the Industry Standard

McGinley did not stop at building products. In 1957, he co-founded and became the first president of the Institute of Printed Circuits — known today as the IPC, the global standards body for PCB manufacturing and electronic assembly. Leading the industry's self-governance organization cemented Methode's reputation not as just another contract manufacturer, but as an engineering-led innovator setting the standards others would follow.

It was the equivalent of a startup founder chairing the industry association — a signal of technical authority that opened doors with the largest OEM customers.

What emerged from this founding era was a business model that persists to this day: custom-engineered solutions designed in close collaboration with OEM customers. McGinley was not interested in building generic parts that any shop could replicate. He wanted Methode's engineers sitting in the customer's design lab, co-developing solutions so tightly integrated that switching suppliers would mean redesigning the product.

That instinct — engineer something custom, make yourself indispensable — became the company's DNA. For investors evaluating Methode today, this founding chapter matters because the same strategy is playing out in 2026: custom-engineered laminated busbars for hyperscaler data centers, designed to each customer's specific rack architecture. The products are completely different. The playbook is identical. And that continuity across eight decades is either a profound competitive advantage or a constraint that prevents the company from achieving the scale economies its larger competitors enjoy.

III. The Automotive Pivot & Building the Foundation (1960s–1990s)

The Asia Migration Crisis

By the mid-1970s, the consumer electronics manufacturing base that had sustained Methode for three decades was migrating to Asia. Japanese and Taiwanese manufacturers were producing televisions and radios at costs American factories could not match. Revenue stood at about $27.5 million in 1976 — respectable for a mid-size manufacturer, but McGinley could see the cliff approaching. If Methode stayed tethered to consumer electronics, it would eventually have no domestic customers left to serve.

What followed was one of the most decisive strategic pivots in the company's history. Around 1978 to 1980, McGinley pushed Methode away from custom-built products for consumer electronics and toward proprietary, internally designed offerings for three durable end markets: automobiles, computers, and aerospace.

The logic was sound — these were industries where American manufacturing would remain dominant, where quality and precision commanded premium pricing, and where the cost of a component failure was measured in lives, not just warranty claims. A bad tube socket meant a fuzzy television picture. A bad automotive connector meant a failed airbag deployment. The stakes were fundamentally different, and McGinley bet that higher stakes meant higher barriers to entry and better margins.

The Automotive Surge

The gamble paid off immediately. Sales hit $44.7 million by 1980. By 1984, revenue had nearly doubled again to $82.4 million, with connectors and controls representing sixty-one percent of sales — up from thirty-five percent just three years earlier.

The Big Three U.S. automakers — General Motors, Ford, and Chrysler — became Methode's anchor customers, collectively accounting for roughly forty-five percent of revenue. General Motors alone contributed one-fifth of net sales. Along the way, Methode had also been acquiring selectively. In 1962, the company purchased Carter Precision Electric Co., expanding into automotive controls and switches. A 1969 acquisition of Graphic Research in California brought military circuit board capabilities. Not all deals worked — Graphic Research suffered from space shuttle program slowdowns, and a testing equipment subsidiary called Trace Laboratories was eventually divested with significant write-offs in 1992.

But each acquisition added a capability layer that made the core automotive business stronger and more diversified.

The Clockspring: 75 Million Lifesaving Links

The product that truly defined Methode's automotive era arrived in 1988: the clockspring. To understand why this mattered, consider the engineering challenge automakers faced.

When they began mandating driver-side airbags as standard equipment — Chrysler led in 1988, with Ford and GM following — they confronted a deceptively tricky problem. The airbag sits in the steering wheel, which rotates. The crash sensor sits in the stationary steering column. You need an unbroken electrical connection between a spinning component and a fixed one. If that connection fails at the moment of impact, the airbag does not deploy. The driver dies.

Methode's solution was elegant: a coiled, flexible electrical connector — named for its resemblance to the spring inside a mechanical clock — that accommodated full steering rotation while maintaining continuous electrical contact. Imagine a flat ribbon cable wound into a tight spiral: as the steering wheel turns, the spiral unwinds and rewinds, maintaining the circuit through the full range of motion. Simple in concept, demanding in execution — the materials had to withstand decades of continuous flexing, extreme temperatures, and the violence of an airbag deployment without ever losing contact.

By 1990, clockspring revenue alone was generating approximately $15 million annually. By 1991, Methode was the only domestic supplier of the technology. When General Motors — which had been manufacturing its own air bag connectors in-house — finally signed with Methode in 1992, all three of Detroit's giants were on board. Over the following decades, Methode would produce more than seventy-five million clocksprings — seventy-five million invisible lifesaving links between crash sensor and airbag.

Building the Global Footprint

The broader significance of the clockspring story extends beyond revenue. It demonstrated that Methode could identify an emerging safety-critical need, engineer a proprietary solution, win sole-source contracts with the world's largest automakers, and then scale production to tens of millions of units. That pattern — spot the need, engineer the solution, lock in the customer — would become the template for every major growth initiative that followed.

Revenue continued climbing through the 1990s, reaching a then-record $213 million in fiscal 1994. The company expanded internationally — a Singapore plant in 1986, a Scotland factory in 1993, operations in Ireland and Connecticut in 1994, and a commitment to China by late 1994.

McGinley remained president through it all, an extraordinary tenure of nearly fifty unbroken years at the helm of the company he founded. He was not just a founder but the institutional memory of the entire organization — the person who remembered why every decision had been made, what had worked, and what had failed.

His leadership built a culture of engineering excellence and customer intimacy that successive leaders would both benefit from and struggle to maintain. But as the 1990s drew to a close, the company McGinley built was about to enter a new era — one defined by acquisitions, globalization, and the relentless pressure to grow beyond its Detroit-centric customer base.

IV. Globalization Through Acquisitions (1990s–2000s)

The 1997 Acquisition Blitz

In fiscal 1997, McGinley made a move that signaled a fundamental shift in Methode's growth strategy. Rather than expanding organically into new geographies — a slow and capital-intensive process — he executed three acquisitions in rapid succession, spending approximately $40 million while keeping the balance sheet debt-free.

The centerpiece was Merit Elektrik GmbH, a maker of electrical components and so-called "hidden" switches for the European automotive industry, based on the Mediterranean island of Malta — sixty miles south of Sicily.

Hidden switches are exactly what they sound like: capacitive or touch-sensitive controls integrated seamlessly into vehicle surfaces so that no visible button or toggle interrupts the design. A driver touches a seemingly blank panel and the interior light comes on, or the sunroof opens. It is the kind of engineering that premium European automakers like BMW and Mercedes-Benz love — invisible technology that feels like magic.

Through Merit, Methode gained access to these prestigious European nameplates and established Malta as a long-term manufacturing hub. The strategic logic was explicit: "Very little product overlap with Merit, and they had the European presence we've wanted," management explained at the time.

Sensor Technology and New Capabilities

Alongside Merit, Methode acquired Adam Technologies, a New Jersey-based connector supplier with about $15 million in annual sales, and took a seventy-five percent stake in Magnetoelastic Devices, a tiny Pittsfield, Massachusetts company with just $1 million in revenue but promising patents in torque-sensing technology.

Magnetoelastic sensors detect force and torque by measuring changes in the magnetic properties of materials under stress. Imagine a steel shaft that, when twisted, changes its magnetic signature in a way that a nearby sensor can precisely measure. The harder you twist, the stronger the signal. The applications in automotive steering systems — where knowing exactly how much force the driver is applying to the wheel is essential for electronic power steering — were significant. So were potential uses in industrial machinery and, eventually, EV drivetrains.

This acquisition spree established a pattern Methode would follow for the next two decades: buy companies with complementary technologies and geographic reach, integrate their engineering capabilities, and cross-sell to the combined customer base. It was not a roll-up strategy in the private equity sense — there was no financial engineering or aggressive cost-cutting. It was an engineer's approach to M&A: assemble the best capabilities, then build better products.

The Passing of a Founder

On January 22, 2001, William McGinley passed away at his home in Barrington Hills, Illinois, at the age of seventy-seven. Just three days before his death, he had been inducted into the Chicago Area Entrepreneurship Hall of Fame at the University of Illinois at Chicago. He had been the only president in Methode's half-century history — a fact almost without parallel in American manufacturing.

His son James became President and CEO of the recently spun-off Stratos Lightwave, carrying the family's engineering legacy into the fiber optic frontier. The transition at the parent company was handled by Donald Duda, who had joined Methode in 2000 as Vice President of the Interconnect Products Group, became President in 2001, and was named CEO in 2004. Duda would lead the company for nineteen years — an impressive tenure by modern standards, though less than half McGinley's extraordinary run.

The Stratos Lightwave Spinoff

Meanwhile, the Stratos Lightwave spinoff that had been set in motion before McGinley's passing was proving the value of strategic separation. Through the 1990s, Methode had built a substantial fiber optics business, including the acquisition of Stratos Ltd., a UK-based developer of fiber optic transceivers and components.

As the telecom bubble inflated, this optics division was growing far faster than the traditional connector business, and the two needed different capital allocation strategies, different talent pools, and different investor bases. In February 2000, Methode announced the spinoff, launching a partial IPO in June 2000 and completing the full distribution by April 2001.

The move demonstrated intellectual honesty — management recognized that housing a high-growth optoelectronics business inside a traditional manufacturing conglomerate was suboptimal for both. And it foreshadowed the data center opportunity that would become central to Methode's story twenty-five years later: Stratos Lightwave went on to produce optical transceivers for high-speed data communications, the very same market where Methode's laminated busbars now carry power.

Under Duda, Methode continued developing its sensor technologies, expanding its magneto-elastic capabilities, and building out complex insert-molded leadframes — the precision metal-and-plastic assemblies used inside automotive transmissions to route electrical signals. These were not glamorous products, but they were technically demanding, safety-critical, and deeply embedded in customer designs.

The 1990s and early 2000s built the technological and geographic foundation for everything that followed. Methode entered this period as a Chicago-centric automotive connector company. It exited with manufacturing on three continents, proprietary sensor technologies, European automotive relationships, and a demonstrated willingness to spin off or acquire businesses based on strategic logic rather than sentimentality.

V. The Great Transformation: 2017–2018 Acquisition Binge

The Strategic Imperative

To understand the urgency behind Methode's 2017-2018 acquisition spree, consider where the company stood heading into that period. Under Duda's steady leadership, Methode had grown from $359 million in revenue in fiscal 2004 to roughly $900 million by fiscal 2017 — solid compounding, but the growth was heavily dependent on traditional automotive.

The industry was evolving rapidly: electrification was beginning to reshape vehicle architectures, LED lighting was replacing incandescent systems across every vehicle segment, and OEMs were consolidating their supplier bases to favor companies with broader capabilities.

A supplier that could only offer connectors was losing ground to suppliers that could offer complete modules — lighting, switches, sensors, and assemblies integrated into a single delivered component. Methode needed to diversify, and it needed to do so fast.

Procoplast: The Opening Move

The first move came in July 2017, when Methode acquired Procoplast S.A. for $22.2 million in cash. Procoplast was an independent manufacturer of automotive assemblies based near the Belgian-German border — a strategic foothold in one of continental Europe's most manufacturing-rich regions, close to the OEM design and purchasing centers where supplier relationships are built.

It was a small deal, a targeted capability addition that expanded Methode's European production capacity without straining the balance sheet. Think of it as a chess opening: positioning a piece for the larger game to come.

Pacific Insight: The LED Play

Three months later, in October 2017, the ambition escalated. Methode acquired Pacific Insight Electronics Corp., a global lighting, electronics, and solutions provider to the transportation industry headquartered in Vancouver, for approximately $114 million.

Pacific Insight brought something Methode had been missing: deep expertise in LED lighting systems for automotive and commercial vehicle markets, plus development resources and manufacturing capacity in Canada and Mexico, including a plant in Zacatecas that would later become critically important for USMCA tariff compliance.

Why did LED lighting matter so much? Because the automotive lighting market was undergoing a wholesale technology transition. Incandescent bulbs — the workhorses of vehicle lighting for a century — were being replaced by light-emitting diodes that lasted longer, consumed less power, offered more design flexibility, and had become cheap enough for mass-market vehicles.

Every new vehicle platform was a potential LED conversion, and OEMs wanted suppliers who could design complete LED lighting modules — not just provide bulbs, but engineer the entire assembly including optics, thermal management, electronics, and housing. Pacific Insight gave Methode that capability and, crucially, positioned the company to compete for programs that were growing while traditional connector programs were beginning to face pressure.

The Grakon Megadeal

But the real earthquake arrived in September 2018. On August 20, Methode announced a definitive agreement to acquire Grakon Parent, Inc. for $420 million — by far the largest acquisition in company history, roughly four times the size of the Pacific Insight deal.

Grakon was a global leader in the design, development, and manufacture of advanced lighting systems, controls, and components for OEM manufacturers in the heavy truck, bus, rail, electric vehicle, and power sports markets. It had been a customized lighting solutions provider for over forty years.

The financial profile was attractive: Grakon had generated approximately $159 million in trailing twelve-month revenue and roughly $41 million in EBITDA, implying an acquisition multiple of approximately ten times EBITDA — a reasonable price for a growing industrial business with deeply sticky customer relationships.

Grakon's customers had averaged more than nineteen years of tenure — nearly two decades of continuous supply. To put that in perspective, the average S&P 500 CEO tenure is about seven years. Grakon's customers had been buying from the company for nearly three CEO cycles. That kind of stickiness is gold in an industry where qualification processes for safety-critical components take years and involve rigorous testing, certification, and integration into the customer's own manufacturing line.

The Debt Tradeoff

The deal closed on September 12, 2018, funded with a combination of cash on hand and proceeds from an amended credit facility. The debt load was significant — over $300 million of new borrowing, which became management's top priority to pay down.

But the strategic rationale was compelling: Methode was no longer just an automotive connector company. It was now a diversified transportation technology supplier with positions in passenger vehicles, commercial trucks, buses, rail, and power sports, with LED lighting expertise across all of them.

The numbers told the transformation story clearly. Between fiscal 2013 and fiscal 2023, Methode's revenue grew by roughly 127 percent. The lion's share of that growth came from these three acquisitions, which collectively added more than $300 million in annual revenue. The Grakon business unit continued earning recognition as a top supplier from major OEMs like PACCAR years after the acquisition, validating the integration.

But acquisitions create debt, and debt creates vulnerability. The $300-plus million in borrowing from the Grakon deal constrained Methode's financial flexibility at precisely the moment when the automotive industry was entering a period of unprecedented disruption. The acquisitions had transformed Methode's capabilities. Whether they had transformed its resilience was a question that remained unanswered — until the next chapter tested it severely.

VI. Nordic Lights: Doubling Down on Industrial Lighting (2023)

The Peak-of-Optimism Acquisition

In February 2023, with Methode's stock near its all-time high of roughly $45 and the EV market still riding a wave of optimism, management made a decision that would later attract considerable scrutiny.

The company announced a recommended public tender offer to acquire all outstanding shares of Nordic Lights Group Corporation, a Finland-based premium provider of high-quality LED and HID lighting solutions for heavy-duty equipment, at EUR 6.30 per share — valuing the total equity at approximately EUR 132 million. Nordic Lights' shares had been listed on Nasdaq First North, the Finnish growth market exchange.

The Perfect Fit — On Paper

Nordic Lights was, on paper, a perfect fit for the acquisition framework Methode had been refining since the 1990s. Its products — work lights, headlights, and indicator lights for mining equipment, construction vehicles, forestry machinery, agricultural equipment, and material handling systems — served precisely the kind of demanding industrial environments where premium quality commands premium pricing and customer relationships are measured in decades.

The customer list read like a who's who of global industrial OEMs: Caterpillar, Hitachi, John Deere, Komatsu, Liebherr, Ponsse, and Sandvik. These were not the kind of accounts that switched suppliers because a competitor offered a five percent discount.

When a forty-ton excavator is operating underground in a copper mine at negative twenty degrees Celsius, and the only thing preventing a catastrophic collision is the quality of the lighting on its cab, the OEM does not shop on price. It shops on reliability, durability, and the supplier's track record of zero-defect delivery.

Closing the Deal

By April 2023, Methode had settled the tender, acquiring roughly eighty-one percent of Nordic Lights shares for approximately EUR 106.5 million. A compulsory acquisition of the remaining minority shares followed in the second half of the year, bringing Methode to full ownership. The deal was funded with cash on hand and debt financing under the existing credit facility.

The Timing Question

The timing question is unavoidable. With the benefit of hindsight, Methode was adding roughly $130 million in debt at the very moment when the EV programs that had been driving its automotive growth were about to collapse. Long-term debt, which management had worked to reduce from the Grakon-era peak back toward $200 million, jumped back to approximately $332 million. The financial cushion that five years of disciplined debt reduction had built was effectively erased.

Was this reckless, or was it visionary? The answer depends on time horizon.

Nordic Lights gave Methode a meaningful presence in industrial off-road lighting — a market with different cyclical dynamics than passenger automotive, with higher margins, and with customers whose capital equipment replacement cycles provide long-dated revenue visibility. Combined with Grakon's commercial vehicle lighting, Methode now had a comprehensive industrial lighting portfolio that would become the backbone of its Industrial segment — the same segment whose data center power products would later emerge as the company's most compelling growth story.

The acquisition also reflected a strategic instinct that had been consistent since the founding: when Methode sees a market where engineering quality trumps commodity pricing, it buys in. Nordic Lights' products are not cheap. They are the best. That mission-critical positioning creates exactly the kind of switching costs and pricing power that Methode's business model depends on.

But the debt was real, the timing was unfortunate, and within months, Methode would face a crisis that made every dollar of leverage feel like a millstone.

VII. Crisis & The Great Pivot: The EV Collapse (2023–2025)

The September Shock

The storm arrived in September 2023, and it arrived fast. When Methode reported its first quarter fiscal 2024 results on September 7, 2023, the headline numbers were troubling — but the guidance revision was devastating.

Management slashed full-year adjusted earnings per share guidance by roughly forty percent, from a range of $1.55 to $1.75 down to $0.80 to $1.00. The culprits: operational inefficiencies at the company's Monterrey, Mexico manufacturing facility — labor shortages, vendor problems, inventory gaps, premium freight costs — compounded by a significant weakening in the e-bike market. CEO Duda acknowledged "planning deficiencies, inventory shortages, unrecoverable spot purchases, and premium freight, and delayed shipments" at Monterrey. The stock cratered.

The EV Unraveling

What followed over the next eighteen months was a cascading series of setbacks that tested every assumption investors had held about the company. The electric vehicle programs that had been driving Methode's growth story — over $600 million in accumulated EV program awards, representing more than eighty percent of new business wins — began to unravel.

Stellantis, Methode's largest EV customer, was pulling back aggressively on electrification as the broader EV market slowdown took hold. Stellantis itself would later report a historic loss for full-year 2025, driven by massive write-downs tied to its reversal of an aggressive EV strategy. Its CEO Carlos Tavares resigned in December 2024.

Program timelines stretched. Orders declined. Revenue that management had been counting on simply did not materialize. By the time the dust settled, Methode was facing an estimated $100 million annualized decline in EV-related sales for fiscal 2026, primarily driven by Stellantis.

The CEO Revolving Door

The leadership crisis compounded the operational one. CEO Donald Duda, who had announced his planned retirement in August 2023 after nineteen years at the helm, was succeeded in January 2024 by Avi Avula, a former Vice President of Strategy at DuPont's Electronics & Industrial business.

Avula lasted less than four months. His first major earnings report in March 2024 revealed a $21 million year-over-year decline in quarterly net sales, sending the stock down more than thirty-one percent in a single session — from $21.04 to $14.49.

The disclosure triggered a securities fraud class action lawsuit, alleging that the company had made materially misleading statements about employee retention, production planning, and the Monterrey facility's operational challenges during a class period covering December 2021 to March 2024.

Avula resigned in May 2024, and Methode turned to AlixPartners — the restructuring advisory firm whose name tends to appear when companies are in genuine trouble — installing partner Kevin Nystrom as interim CEO. The revolving door at the top — three leaders in under a year — sent exactly the wrong signal to customers, employees, and investors alike.

Enter Jon DeGaynor

The door finally stopped revolving in July 2024, when Jon DeGaynor was appointed President, CEO, and a member of the Board. DeGaynor brought a resume purpose-built for this moment.

A mechanical engineering graduate from the University of Michigan with an MBA from Wharton, he had spent thirty-five years in engineered-products businesses. He had been a Senior Fellow at Wharton's Mack Institute for Innovation Management — not a typical credential for a turnaround CEO, but one that signaled depth of strategic thinking beyond the standard operating playbook.

Most relevantly, from 2015 to 2023, he had served as President and CEO of Stoneridge, Inc., a publicly traded global manufacturer of electrical and electronic systems for automotive, commercial vehicle, and agricultural markets — essentially a smaller version of Methode with a similar customer base and similar transformation challenges. At Stoneridge, DeGaynor led a strategic pivot toward vehicle intelligence and advanced safety systems, driving significant value creation.

The board chose him explicitly for what Chairman Walter Aspatore called his "impressive track record of delivering successful business transformations."

Inheriting Distress

DeGaynor inherited a company in genuine distress. In his own words, Methode was "an 80-year-old company that had disappointed investors, customers, and employees."

The numbers bore that out. Automotive net sales for fiscal 2025 declined more than seventeen percent. The fourth quarter produced a pre-tax loss exceeding $30 million and a net loss of $28.3 million, driven by unplanned inventory adjustments. For the full fiscal year, the company recorded a net loss of $62.6 million on revenue of $1.048 billion — while fiscal 2024 had seen a goodwill impairment of $56.5 million in the North American and European Automotive reporting units.

The Restructuring Playbook

DeGaynor moved quickly and methodically. He reduced the board from ten directors to seven. He relocated the corporate headquarters to an existing company-owned facility, eliminating lease costs. He cut the quarterly dividend to $0.07 per share. Headcount was reduced by more than five hundred employees.

In November 2024, he brought in Lars Ullrich as Senior Vice President of Global Automotive Business, a veteran of Infineon Technologies and Robert Bosch with over twenty years of business and strategic leadership experience in the automotive and semiconductor industries.

In March 2025, he hired Brad Corrodi as Chief Strategy Officer — notably a former colleague from Stoneridge, where Corrodi had served as Vice President of Fleet Products and Services. When a turnaround CEO brings trusted lieutenants from his prior command, it signals both urgency and a clear playbook already in mind.

The pending class action lawsuit remains a material legal overhang. While its outcome is uncertain, it represents both a financial risk and a distraction for a management team already stretched thin.

From its February 2023 all-time high near $45, Methode's stock had fallen to approximately $9 by early 2026 — a loss of roughly eighty percent of market capitalization. The EV collapse did not just dent Methode's earnings. It exposed the fragility of a mid-cap industrial company caught between powerful customers, larger competitors, and a technology transition moving at unpredictable speed. But even as automotive was cratering, something else was growing — and growing fast.

VIII. The Data Center Salvation: A New Growth Engine (2024–Present)

What Is a Busbar, and Why Does It Matter?

To understand why laminated busbars matter, start with a simple analogy. A traditional data center distributes power the way a garden hose distributes water — cables carry electricity from a central source to individual server racks. That worked fine when each rack consumed five or ten kilowatts. A typical corporate data center rack in 2015 might have drawn eight to twelve kilowatts — enough to run a few servers and some networking gear.

But an AI training cluster running hundreds of NVIDIA GPUs can consume hundreds of kilowatts per rack — an order of magnitude more. A single rack of NVIDIA H100 or B200 GPUs can draw sixty to a hundred kilowatts, and next-generation liquid-cooled AI racks are pushing toward two hundred kilowatts and beyond. Try forcing that much water through a garden hose and it bursts. Try forcing that much current through traditional cables and you get excessive heat, voltage drop, and wasted energy. The physics simply do not work at these power densities.

A laminated busbar solves this problem the same way a fire hydrant main solves the garden hose problem. Instead of round cables, a busbar is a flat, rigid conductor — typically layers of copper or aluminum separated by thin insulation — that carries enormous currents with minimal resistance and excellent heat dissipation.

The stacked, flat design spreads current evenly, reduces electrical interference (technically known as inductance), and can be manufactured in precise shapes that fit the exact physical dimensions of a specific server rack. Think of it as a custom-built highway for electricity, designed to deliver massive power directly to the computing equipment with minimal loss.

Each busbar is essentially a bespoke piece of engineering — designed to carry a specific current at a specific voltage through a specific physical space, with tolerances measured in fractions of a millimeter. They are not interchangeable between different rack configurations. A busbar designed for one hyperscaler's custom rack architecture will not fit another hyperscaler's design. This is precisely the kind of custom-engineered, design-in product that Methode has been making for eight decades — just for a completely different end market.

The products are not glamorous. They are not software. But without them, the AI infrastructure boom does not work.

Methode's Power Solutions Heritage

Methode's Power Solutions Group, based in Rolling Meadows, Illinois, has been manufacturing laminated busbars, braided flexible cables, and custom power assemblies for decades — originally serving aerospace, military, industrial, and telecommunications customers.

The group holds AS9100, ISO9001, and ITAR certifications, reflecting its defense and aerospace heritage. These same quality standards — designed for applications where failure means a jet engine loses power or a missile goes off course — are highly valued by hyperscalers demanding absolute reliability in their data center infrastructure.

When hyperscalers like Amazon Web Services, Google, Microsoft Azure, and Meta began building out AI computing infrastructure at unprecedented scale, they needed power distribution solutions that could handle the current densities their new architectures demanded. Methode's existing manufacturing capabilities — the same presses, lamination equipment, and quality processes that had been serving aerospace and military customers — turned out to be almost perfectly suited. The company also produces its proprietary PowerRail system, thermal management solutions including heat sinks and liquid-cooled plates, and integrated power subassemblies.

The Growth Trajectory

The numbers have been striking. In fiscal 2024, data center power products contributed roughly $40 million in revenue. In fiscal 2025, that figure more than doubled to a record exceeding $80 million — a 30 percent compound annual growth rate over three years.

Management reported line of sight toward a $120 million annualized run rate based on fourth quarter order patterns, and disclosed $170 million in bookings for new and extended data center programs — suggesting the pipeline extends well beyond the current quarter.

Perhaps most impressively, management stated that this growth required no material new capital expenditure. Methode is leveraging existing manufacturing infrastructure, repurposing capacity that had been allocated to EV programs that never materialized. The very assets that represented stranded capital from the automotive downturn became the foundation for the data center ramp.

In DeGaynor's framing, the company is "redirecting engineering to higher energy applications" and "repurposing Mil-Aero prototype capabilities" for data center customers. The engineering skill set — designing custom power distribution solutions for mission-critical applications — translates directly, even though the end customers are completely different.

The Industrial Segment's Financial Performance

The Industrial segment — which houses data center power products alongside Nordic Lights' off-road lighting and Grakon's commercial vehicle lighting — has become the financial bright spot.

In the fourth quarter of fiscal 2025, Industrial segment sales reached $132.6 million, up more than thirteen percent year over year, with operating income of $26.2 million and an operating margin of 19.8 percent. That margin stands in stark contrast to the automotive segment's operating losses.

Free cash flow generation has reinforced the narrative. Methode generated $26.3 million in free cash flow in the fourth quarter of fiscal 2025 — the third consecutive quarter of positive free cash flow. Total debt declined to $317.6 million.

The dataMate copper transceiver business was divested to Bel Fuse for $16 million in March 2026, with proceeds earmarked for further debt reduction. DeGaynor described the sale as "an important first step" in an ongoing portfolio review, signaling that additional divestitures are possible as the company sharpens its focus.

The Competitive Gauntlet

The competitive landscape, however, is daunting. In data center power distribution, Methode competes against Eaton Corporation, a diversified power management company with more than $20 billion in annual revenue that has partnered with NVIDIA on 800-volt DC power architectures for AI computing — the bleeding edge of exactly the market Methode is targeting.

Schneider Electric, with roughly $35 billion in revenue, dominates data center infrastructure through its APC brand and EcoStruxure platform. TE Connectivity, at $14 billion in revenue, offers its own busbar solutions. Amphenol, at $11.5 billion, is aggressively expanding in data center and AI infrastructure connectivity. Mersen, a French company, is recognized as a global leader specifically in laminated busbar technology.

The bull case is that Methode does not need to compete on scale. Custom-engineered busbars designed to a specific hyperscaler's rack architecture are not commodity products — each installation is bespoke. If Methode can maintain engineering intimacy with even a handful of major hyperscalers, the revenue per customer relationship can be substantial and sticky.

The bear case is that hyperscalers have immense bargaining power, technology shifts could render current designs obsolete, and Methode has not yet proven it can win at scale against competitors with ten to thirty times its resources. At seven to nine percent of total revenue, the data center business must triple or quadruple before it truly offsets automotive headwinds.

IX. The Transformation Roadmap & FY2026 Outlook

The Four Pillars

DeGaynor has framed the turnaround around four pillars: reset performance, build and grow capabilities, shift culture, and develop and execute a new strategy. The language is deliberately clinical — this is a restructuring framework, not a growth story. At least not yet.

The Guidance Evolution

The initial fiscal 2026 guidance issued after the fiscal 2025 results called for net sales of $900 million to $1 billion and EBITDA of $70 million to $80 million. The math embedded in that guidance was notable: management expected to roughly double EBITDA despite a $100 million decline in revenue, implying significant margin expansion through cost reductions, portfolio optimization, and a more favorable business mix as higher-margin industrial revenue displaced lower-margin automotive programs.

EBITDA margin would improve from roughly 4.1 percent to 7.9 percent — not a heroic margin, but a meaningful step in the right direction and a signal that the cost structure was being genuinely reset.

After the third quarter of fiscal 2026, reported in early March 2026, the picture evolved. Revenue guidance was narrowed to $950 million to $1 billion — the low end raised by $50 million, suggesting stabilization. But EBITDA guidance was lowered to $58 million to $62 million, down from the original range. The reduction reflected continued EV program delays and cancellations in North American automotive, slower-than-expected productivity improvements at the Mexico manufacturing facility — which management said was running roughly six months behind the gains achieved at the Egypt operations — and costs incurred for new program preparation before the associated revenues had materialized.

Reading the Q3 FY2026 Tea Leaves

The third quarter itself told a mixed story. Net sales of $233.7 million were down modestly year over year. The company posted a net loss of $15.9 million and an adjusted net loss of $0.37 per diluted share.

But free cash flow was positive at $10.1 million — bringing the year-to-date figure to roughly $17 million. Cash on hand actually increased by $30 million since fiscal year-end, reaching $133.7 million. The company was losing money on an accounting basis but generating cash — a dynamic that reflected the timing mismatch between restructuring costs hitting the income statement and operational improvements flowing through the cash flow statement.

Management guided that the second half of fiscal 2026 would be meaningfully stronger than the first half, pointing to data center program ramps, cost reduction benefits, and automotive stabilization.

Launch Execution: The Achilles Heel

On the program launch front, Methode had executed fifty-two program launches over the prior two years, with thirty more planned for the current fiscal year. Launch execution — the ability to ramp new programs on time, on budget, and at target quality levels — has been the company's self-described Achilles heel.

Multiple quarters of operational problems at Monterrey traced directly to launches gone wrong: labor not trained in time, inventory not positioned correctly, suppliers not qualified, production volumes missing targets. DeGaynor has made launch discipline a central management priority, but fixing a cultural problem at a company with thirty-five-plus manufacturing locations across fourteen countries does not happen in two or three quarters.

As DeGaynor himself acknowledged: "The Methode team will not be linear" in its improvement trajectory.

Tariffs and Trade

Tariff exposure represents a manageable but notable risk. Management reported a $1 million headwind in the first quarter — characterized as a timing issue rather than a structural cost — and disclosed that it has customer agreements in place to recover tariff expenses.

The Mexican manufacturing facility is ninety-seven percent USMCA compliant, which significantly limits exposure to U.S.-Mexico trade friction that has rattled other automotive suppliers. The global manufacturing footprint — across fourteen countries — provides the flexibility to shift production in response to trade policy changes, though such adjustments take time and carry their own costs.

If management hits the narrowed EBITDA guidance range for fiscal 2026, the narrative shifts from crisis management to recovery. If they miss, the credibility gap widens further.

X. Business Model & Competitive Positioning Today

The Three-Segment Structure

Methode Electronics operates today across three reportable segments — Automotive, Industrial, and Interface — with manufacturing, engineering, and sales operations in more than thirty-five locations across fourteen countries spanning North America, Europe, the Middle East, and Asia. The geographic footprint includes Belgium, Canada, China, Egypt, Germany, India (with an engineering center in Bangalore), Italy, Lebanon, Malta, Mexico, the Netherlands, Singapore, Switzerland, the United Kingdom, and the United States.

The Automotive segment remains the largest by revenue, producing integrated center consoles, ergonomic and hidden switches, transmission lead-frames, LED-based lighting, sensors, and user interface systems for passenger vehicle OEMs worldwide. These are the products embedded in dashboards, steering columns, and overhead consoles — the components drivers touch, press, and interact with every day without ever knowing who made them.

The segment's core competency is design integration: engineering a complete console assembly or switch module that fits precisely into a specific vehicle platform, meeting the OEM's exact specifications for touch feel, backlighting, haptic feedback, and electrical performance.

The Industrial segment has become the growth engine and margin leader. It houses three distinct product families: power distribution products for data centers, aerospace, and industrial customers; off-road lighting solutions from Nordic Lights; and commercial vehicle lighting from Grakon. Industrial safety radio remote controls round out the portfolio. The common thread is mission-critical applications where failure is not an option.

The Interface segment, recently slimmed by the dataMate divestiture, retains appliance and commercial food service user interfaces and fluid-level sensors. The company also operates a small Medical business through Dabir Surfaces, a surface support technology for pressure injury prevention in immobilized patients.

Where the Advantages Lie

The competitive advantages — to the extent they exist — trace back to the founding playbook. Custom-engineered solutions create switching costs. Deep OEM relationships provide early access to new program opportunities. Vertical integration in manufacturing controls cost and quality. A heritage in mission-critical applications — stretching back to components that flew on Apollo and the Space Shuttle — provides credibility with customers who demand the highest levels of quality certification.

The geographic footprint provides manufacturing flexibility that has proved valuable for tariff mitigation. The ability to shift production between facilities in response to trade policy changes is a practical advantage that smaller competitors lack and that investors often underappreciate until tariff headlines dominate the news cycle.

The Scale Vulnerability

The vulnerability is equally clear. Methode generates roughly $1 billion in revenue, competing against companies that are ten to thirty times its size.

Consider the disparity in concrete terms. TE Connectivity, with approximately $14 billion in annual revenue, spends more on R&D in a single quarter than Methode generates in annual EBITDA. Amphenol, at roughly $11.5 billion, has the manufacturing footprint and customer relationships to enter any adjacent market Methode occupies. Aptiv, the Delphi spinoff, generates more than $15 billion in revenue focused squarely on vehicle electrical architecture — the same market where Methode competes in automotive. Schneider Electric, at approximately $35 billion, and Eaton, at more than $20 billion, dominate the data center infrastructure market with product portfolios that dwarf Methode's offerings.

The niche strategy — competing on custom engineering and customer intimacy rather than scale — only works if the niches are large enough to sustain growth and defensible enough to resist encroachment from these giants. Historically, Methode's niches in specialty automotive components were small enough that the mega-suppliers did not bother competing aggressively. The data center busbar opportunity, however, is growing large enough to attract serious attention from every major player in power distribution. The question is not whether the niche is attractive — it clearly is. The question is whether it remains a niche, or becomes a competitive battleground where Methode is outgunned on every dimension except engineering agility.

XI. Structural Analysis: Porter's Five Forces and Hamilton's Seven Powers

Buyer Power: The Dominant Force

Start with buyer power, because it is the dominant force shaping Methode's economics. The company's customers — automotive OEMs like Stellantis and GM, commercial vehicle manufacturers like PACCAR, hyperscale data center operators — are among the most powerful buyers on earth.

In automotive, the annual price-down negotiation is an industry ritual: every year, OEMs demand that suppliers reduce prices by two to five percent, regardless of whether input costs have risen. Design-in cycles create a paradox — once Methode wins a program, it is locked in for the vehicle platform's life, typically five to seven years, but the price was negotiated at the outset and the annual price-downs erode margin over the program's life.

Data center hyperscalers are equally formidable negotiators. When your customer has a trillion-dollar market capitalization and is placing orders in the hundreds of millions, they set the terms.

Suppliers, Entrants, and Substitutes

Supplier power is moderate, driven primarily by commodity input costs. Copper, aluminum, plastics, and specialty electronic components are globally traded and subject to price volatility. During disruptions like the 2021-2022 semiconductor shortage, component availability can constrain operations. But Methode's scale and multi-geography sourcing provide negotiating leverage.

The threat of new entrants varies dramatically by segment. In automotive, barriers are high: years-long qualification cycles, capital-intensive manufacturing, and relationships that take decades to build. Chinese manufacturers are entering with lower cost structures, but safety certification remains a meaningful hurdle. In data center power distribution, barriers are lower — manufacturing laminated busbars requires expertise and capital but not decades of automotive certification history.

Substitution risk is nuanced. The shift from internal combustion to electric powertrains threatens specific legacy products — clocksprings and traditional lead-frames may have no equivalent in an EV architecture. Wireless technologies could replace some wired solutions over time. But in mission-critical applications — data center power distribution, mining equipment lighting — switching costs and safety requirements create meaningful stickiness.

Competitive Rivalry

Competitive rivalry is intense everywhere Methode plays. In automotive: Amphenol, TE Connectivity, Molex, Aptiv — all substantially larger and better capitalized. In data center: Schneider Electric, Eaton, Vertiv, Mersen — industry giants with established relationships. Price competition is fierce in mature segments, and the race for data center design wins is underway.

Hamilton Helmer's Seven Powers

Turning to Hamilton Helmer's Seven Powers framework — which asks not just what forces shape competition but what specific advantages allow a company to sustainably capture value — the honest answer for Methode is that the moats are real but shallow.

Switching costs represent the strongest power. Custom designs integrated into vehicle platforms and data center rack architectures create multi-year lock-in during program life. Re-engineering, re-tooling, and re-qualifying a replacement supplier costs millions and takes months. The limitation is temporal — at program end, customers rebid.

Process power is the second relevant advantage. Eight decades of manufacturing expertise in complex, multi-material assemblies — insert molding, precision stamping, quality systems certified to automotive and aerospace standards — represent accumulated knowledge that cannot be easily replicated overnight. Vertical integration from raw material processing through final assembly provides cost and quality advantages.

Counter-positioning was historically strong but has eroded. Methode's original position — custom engineering versus commodity manufacturing — was clear. But larger players have adopted similar approaches. The data center pivot could represent a new counter-position: a nimble engineering firm serving hyperscaler power needs, positioned against both pure-play data center giants who lack Methode's custom manufacturing depth and pure-play automotive suppliers who lack power distribution expertise.

Scale economies, network effects, branding, and cornered resources are either absent or negligible. Methode is dramatically outscaled by every major competitor. Its products create no network effects. As a B2B component supplier, brand recognition is limited to narrow OEM engineering circles. Its patent portfolio, while containing some proprietary sensor technologies, does not constitute a defensible moat against well-funded competitors who can design around it.

The overall structural assessment: Methode has switching costs and process power as modest advantages, with a potential counter-positioning opportunity in data centers that remains unproven. Success depends more on execution quality than structural moats — which means the margin for error is thin and every quarterly report carries outsized significance.

XII. Bull vs. Bear Case

The Bull Case: Transformation in Progress

The transformation thesis rests on a simple observation: Methode trades at distressed valuations because of a crisis that is largely behind it, while the data center opportunity ahead of it is enormous and accelerating.

The company's market capitalization sits at roughly $273 million against a billion-dollar revenue base — a price-to-sales ratio that implies the market expects permanent impairment. If the data center business continues its trajectory and automotive stabilizes at a lower but profitable baseline, the re-rating potential is significant.

The financial recovery evidence, while early, is encouraging. EBITDA swung from negative $53.5 million in fiscal 2024 to positive $30.4 million in fiscal 2025 — a nearly $84 million improvement in a single year. Free cash flow was positive for three consecutive quarters. Debt has begun declining. The dataMate divestiture and potential further portfolio actions could accelerate deleveraging.

The management team's actions signal urgency and competence. Board reduction, headquarters relocation, headcount cuts of over five hundred, dividend reduction, hiring of directly experienced leaders — these are the moves of a CEO who understands the severity of the situation and is not trying to paper over it with optimistic guidance.

DeGaynor's Stoneridge track record provides a real-world template: he transformed that company from a legacy automotive supplier into a vehicle intelligence platform. If he can execute a similar playbook at Methode — stabilizing the base business while investing in high-growth industrial and data center applications — the upside from current levels could be meaningful.

The Growth Evidence

The data center growth itself provides perhaps the strongest evidence for the bull case. Moving from $40 million to over $80 million in a single year, with $170 million in bookings and line of sight to $120 million annualized, is not a rounding error.

This is a real business serving real customers with a real secular tailwind. The AI infrastructure buildout is the largest capital expenditure cycle in technology history, and Methode has positioned itself to capture a piece of the power distribution layer.

The niche player strategy — competing on custom engineering and customer intimacy rather than scale — makes strategic sense for a company that cannot outspend its larger competitors. The global manufacturing footprint provides tariff mitigation advantages. And the long automotive heritage provides engineering credibility that pure-play startups lack.

The Bear Case: Execution and Structure

The counter-argument starts with a blunt observation: this is an eighty-year-old company that has recently disappointed every constituency that matters — investors, customers, and employees. Culture change at an organization with thousands of employees across fourteen countries is not a two-quarter project.

The launch execution problems that have plagued operations persist — the Mexico facility remains roughly six months behind Egypt in productivity improvements. Management is implementing frameworks and hiring talent, but the proof must come in financial results, and EBITDA guidance has already been reduced once.

Competitive and Structural Concerns

The competitive structure provides little comfort. Every data center dollar Methode earns is contested by companies with vastly greater resources. Eaton's partnership with NVIDIA on 800-volt DC architectures puts it at the technological frontier. Schneider Electric's APC brand has decades of data center infrastructure relationships.

If any of these players decides to aggressively pursue the custom busbar niche, they have the R&D budgets, sales forces, and customer relationships to make it very uncomfortable for a company with Methode's strained balance sheet.

Automotive dependency remains severe. More than sixty percent of revenue still comes from the auto segment, and the trajectory is negative. Stellantis continues restructuring its electrification strategy. Additional program delays or cancellations from other OEMs remain plausible. EV and hybrid applications still account for roughly twenty percent of total sales, and the market for those applications remains volatile.

Customer concentration risk — demonstrated vividly by the Stellantis-driven revenue collapse — has not been structurally resolved.

Financial Fragility

Financial fragility amplifies every risk. Total debt remains approximately $317 million. EBITDA margins are compressed. The company has posted multiple quarters of losses. The dividend cut, while prudent, signals to income investors that management views the financial position as constrained.

The pending securities fraud class action adds litigation expense and management distraction. There is limited financial cushion for further setbacks — a single bad quarter could force difficult decisions about the balance sheet.

Myth vs. Reality

The myth versus reality check on the consensus narrative is worth examining carefully, because the gap between the two competing narratives is unusually wide for a company this size.

Myth: Methode is pivoting brilliantly into AI infrastructure. The reality is more nuanced. Methode's Power Solutions Group has been manufacturing busbars for decades — this is not a pivot so much as an existing capability finding a new and much larger addressable market. The company did not foresee the AI infrastructure boom and position itself accordingly. Rather, hyperscaler demand arrived at Methode's doorstep because the company already had the manufacturing processes, quality certifications, and engineering expertise from its aerospace and military heritage. There is genuine credit due for recognizing the opportunity and reallocating resources quickly, but this was more fortunate preparedness than strategic foresight.

Myth: The turnaround CEO has it all figured out. DeGaynor has the right background and is taking the right actions, but he has been in the role for less than two years. The Stoneridge comparison is instructive but imperfect — Stoneridge was a smaller company with a narrower product portfolio and fewer geographies to manage. Methode's complexity — thirty-five locations, fourteen countries, three segments, active restructuring, ongoing litigation — is a different beast entirely. The new management team is promising but unproven at Methode specifically.

Myth: Automotive is yesterday's problem. It is not. Automotive still represents more than sixty percent of revenue, and the segment continues to post operating losses. Stabilization is guided but not yet demonstrated in the financial results. The $100 million in projected EV revenue declines is a known headwind, but unknown headwinds — additional program delays, customer financial distress, trade disruptions — could make it worse.

The data center opportunity is real — the $80 million in fiscal 2025 revenue and $170 million in bookings are not figments. But at seven to nine percent of total revenue, the business must grow three to four times its current size to meaningfully change the company's character. And the competitive landscape — Eaton, Schneider, TE Connectivity, Mersen — is not going to concede market share quietly.

The truth, as usual, likely lives somewhere in between — and the resolution depends entirely on execution over the next several quarters.

XIII. What to Watch as Investors

The Three KPIs That Matter Most

Distilling an eighty-year company history, a three-segment business model, and a complex turnaround into a monitoring framework requires ruthless prioritization. Three metrics matter more than any others for tracking whether Methode's transformation is working.

First: Data center power product revenue, measured quarterly. This is the single most important leading indicator of the company's long-term trajectory. Management has guided toward a $120 million annualized run rate and has $170 million in bookings.

Watch whether quarterly data center revenue accelerates, plateaus, or decelerates as initial hyperscaler deployments mature. If this business can compound at thirty percent or more annually, it changes the fundamental character of the company. If growth stalls, the transformation thesis weakens materially. This is the number that separates a turnaround story from a value trap.

Second: Industrial segment operating margin. The Industrial segment posted a 19.8 percent operating margin in the most recent quarter — a premium result for a mid-cap industrial manufacturer and a reflection of the value-add in custom engineering for mission-critical applications.

If this margin holds or expands as data center revenue scales, it validates the niche strategy and demonstrates that growth is not coming at the expense of profitability. If the margin compresses — due to competitive pricing pressure, unfavorable mix shift, or cost overruns on new programs — it suggests the company is chasing volume at the expense of returns.

The interplay between revenue growth and margin quality in this segment tells the real story of whether the data center opportunity is value-creating or value-dilutive.

Third: Quarterly free cash flow. After years of cash consumption driven by restructuring costs, inventory adjustments, and operational inefficiency, Methode has posted three consecutive quarters of positive free cash flow.

Sustained free cash flow generation validates that the operational turnaround is translating into real financial results — not just accounting adjustments. It funds debt reduction, creates strategic optionality for further acquisitions or investments, and provides the cushion that a leveraged turnaround requires to absorb inevitable setbacks. A reversion to negative free cash flow would reopen fundamental questions about the viability of the transformation plan.

Strategic Milestones to Monitor

Beyond these core metrics, several strategic milestones deserve attention. Major data center customer wins announced publicly would validate that Methode is expanding its hyperscaler relationships, not just growing within existing accounts. The automotive segment's return to even modest profitability — even a one or two percent operating margin — would dramatically shift the narrative from "segment in free fall" to "segment stabilizing."

Net debt reduction toward the company's target of approximately $189 million would provide the balance sheet breathing room that a leveraged turnaround requires. Every dollar of debt reduction simultaneously reduces interest expense, increases financial flexibility, and signals to the market that the operational improvements are translating into real deleveraging.

The cadence of program launches — and particularly the success rate of those launches — will provide early warning on whether the cultural transformation DeGaynor is driving has taken hold in the factories and engineering centers where it ultimately matters. Methode has guided thirty new program launches for the current fiscal year. If those launches go smoothly, it validates the process improvements. If they stumble — as past launches at Monterrey did — it suggests the cultural and operational problems run deeper than a new management team can fix in a couple of years.

Finally, watch for additional portfolio actions. DeGaynor described the dataMate divestiture as "an important first step," explicitly signaling that more divestitures may follow. Each divestiture sharpens focus, generates cash for debt reduction, and moves the company closer to a pure-play industrial and data center power distribution company — a narrative that would command a very different valuation multiple than a struggling automotive supplier with a side business in busbars.

Methode Electronics has reinvented itself many times over eight decades — from tube sockets to printed circuit boards, from clocksprings to LED lighting, from automotive connectors to data center busbars. Each reinvention required engineering imagination, strategic courage, and operational discipline. The current chapter demands all three in abundance, with a balance sheet clock ticking in the background. The next few quarters will reveal whether this is the beginning of another successful transformation — or the chapter where continuous reinvention finally meets its limits.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube