Medtronic plc: The Inversion, the Activist, and the Battle for Medtech Supremacy

I. Introduction & Episode Roadmap

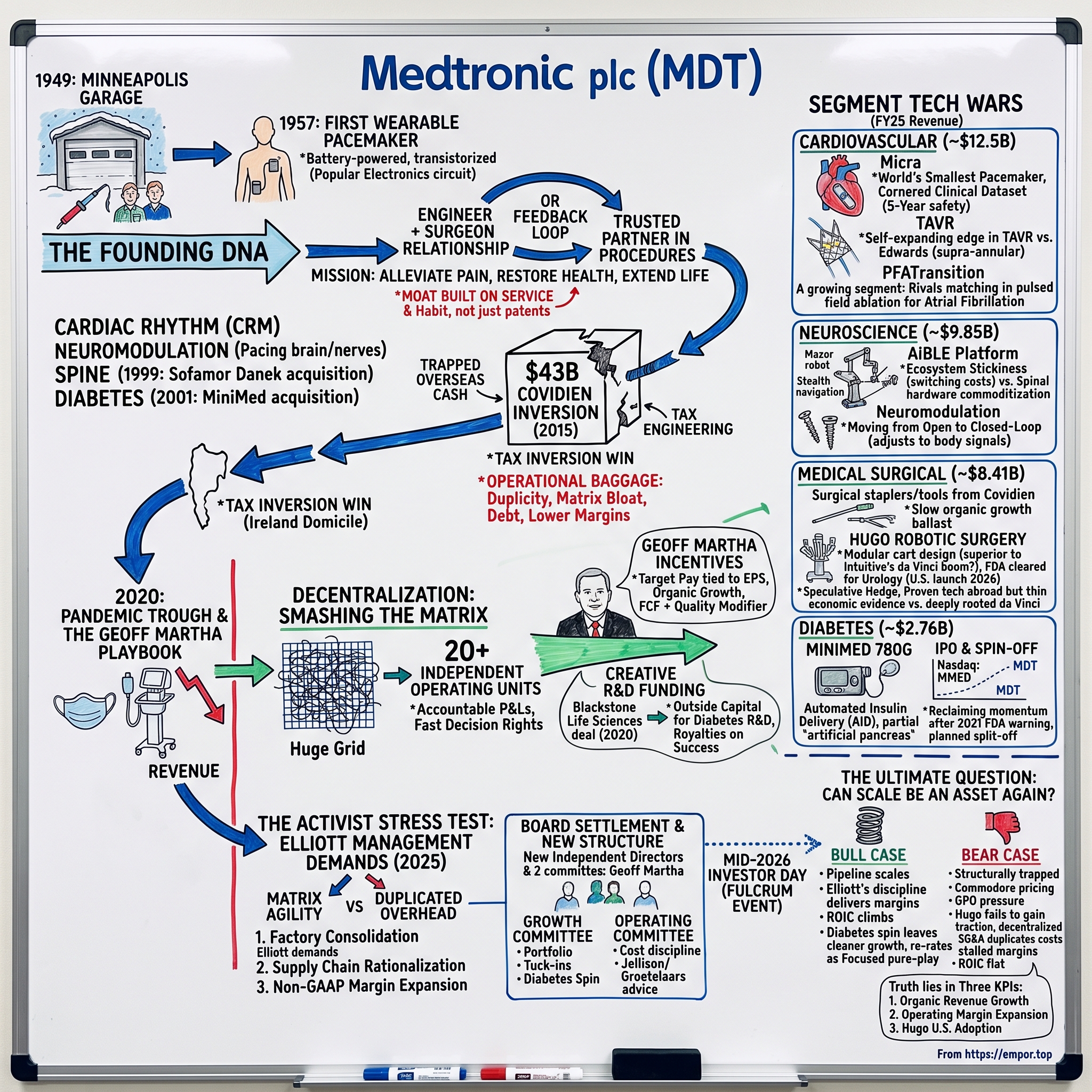

Picture a Minneapolis garage in the winter of 1949. Snow piles against a wooden door, inside sits a young electrical engineer and his brother-in-law, surrounded by broken hospital equipment and a soldering iron, billing the local university medical center a few dollars at a time to keep the lights on. Now fast-forward seventy-six years. The company that grew out of that garage — Medtronic plc — spans more than 150 countries, sells everything from the world's smallest pacemaker to surgical robots, and booked $33.5 billion in revenue in the fiscal year that ended in April 2025.1 And in the late summer of 2025, one of the most feared activist investors on Wall Street, Elliott Investment Management, quietly built one of the largest positions on its share register and started demanding that the giant tear apart the very bureaucracy it had spent a decade building.2

That is the arc of this story: how a repair shop became the closest thing the medical device industry has to a superpower, how it pulled off the single largest corporate tax inversion in American history to legally become Irish, and how — despite owning some of the best clinical technology ever built — it spent much of the last decade watching nimbler rivals compound shareholder value faster. Medtronic is a case study in a peculiar corporate disease: being extraordinarily good at inventing life-saving machines and merely mediocre at running the enterprise that sells them.

The central tension runs through everything. On one side is the ghost of founder Earl Bakken — the garage tinkerer who could build a device in four weeks by studying a magazine circuit and who wrote a mission statement about alleviating pain that employees still recite. On the other side is the reality of a sprawling healthcare conglomerate with dozens of factories, four large business segments, layers of group executives, and a matrix organization so complex that decisions calcified. The company's own former structure was described, even by insiders, as a "holding company" of fiefdoms.11

To grasp why this matters for an investor, hold Medtronic against the companies that have quietly beaten it. Over the past decade, focused competitors — Edwards Lifesciences in heart valves, Intuitive Surgical in robots, Stryker in orthopedics, Boston Scientific across cardiology — generally delivered stronger revenue growth and shareholder returns than the industry's largest and most diversified player. That is the paradox at the heart of this story and the reason it is worth two hours of your attention. Size, in medtech, was supposed to be a weapon: more scale, more distribution, more R&D, more clinical data. Instead, at Medtronic, size too often behaved like a weight. The whole drama of the last decade — the inversion, the reorganization, and now the activist — is ultimately a single question asked three different ways: is Medtronic's scale an asset or a liability, and can management finally make it the former?

Here is where we are going. We start in the garage and the transistorized heartbeat that made Medtronic. We trace the empire-building decades that turned cardiac rhythm into a near-monopoly and gross margins into the envy of the industry. We dissect the $43 billion Covidien inversion of 2015 — brilliant tax engineering wrapped around a slower-growing, lower-margin business that saddled the balance sheet with goodwill for years.8 We follow CEO Geoff Martha's attempt to smash the matrix into twenty independent operating units. We go deep into the segment wars — the crown-jewel cardiovascular franchise, the neuroscience ecosystem, the robot-surgery moonshot called Hugo, and the diabetes turnaround that ended in a spin-off. Then we stress-test the whole thing through Elliott's eyes, extract the investing lessons, and lay out the honest bull and bear cases. The question we keep returning to: can the company that defined modern medtech finally learn to run itself as well as it invents?

II. The Minneapolis Garage and the Transistorized Heartbeat

The founding scene is almost too perfect for a business myth, except that it happened. In April 1949, Earl Bakken, a University of Minnesota electrical engineering graduate, and his brother-in-law Palmer Hermundslie set up shop in a 600-square-foot garage in northeast Minneapolis. Their business was not glamorous: they repaired and serviced medical equipment for local hospitals, hauling oscilloscopes and centrifuges back and forth.14 In its first month, the company reportedly grossed a handful of dollars. This was not a venture-backed rocket ship. It was two men with a soldering iron surviving on razor-thin margins, kept alive mainly because Bakken understood a machine no one else in the hospital did.

But that repair work put Bakken in the operating rooms of one of the most important places in twentieth-century medicine. The University of Minnesota was the global epicenter of open-heart surgery, home to the charismatic and controversial surgeon Dr. C. Walton Lillehei — the "father of open-heart surgery," a man who had survived cancer and operated with a flair that drew trainees from around the world. Bakken, the guy who fixed the machines, became a trusted fixture in Lillehei's world. That relationship — engineer embedded with physician, iterating in real time on real patients — would become the DNA of the entire company, and later, the DNA of the entire industry.

Then came the blackout. On the night of October 31, 1957, a power failure swept across the Twin Cities. In Lillehei's ward, infants recovering from heart surgery were being kept alive by pacemakers plugged into wall current — bulky AC-powered boxes. When the electricity died, so, tragically, did a patient. Lillehei was furious at the fragility of it and turned to the man who understood circuits. He wanted a pacemaker that did not depend on the wall.

What Bakken did next became legend. Within four weeks he produced a small, self-contained, transistorized, battery-powered pacemaker that could be taped to a patient's chest — the first wearable external pacemaker in the world. The circuit he adapted did not come from a laboratory but from the pages of Popular Electronics: a design for a transistorized metronome, running on a 9-volt battery, repurposed to pace a human heart.14 Lillehei put it on a child the very next day. A magazine hobby circuit, in other words, became the seed of a company now worth well over a hundred billion dollars. It is worth pausing on what this proved about medtech: the winning move was not raw invention so much as speed plus proximity to the surgeon. Bakken won because he was in the room.

Three years later, in 1960, the company took another decisive turn — licensing the first reliable fully implantable pacemaker from inventor Wilson Greatbatch, moving Medtronic from a device taped to the skin toward a device sewn inside the body.14 That same era produced the sentence that still hangs on office walls: the Medtronic Mission, drafted by Bakken, "to alleviate pain, restore health, and extend life." It reads like corporate poetry, but it functioned as an operating system. It told salespeople and engineers that the customer was ultimately the patient, and it justified a culture of doing whatever it took to get a device to a physician who needed it.

It is easy, from the vantage point of a hundred-billion-dollar enterprise, to romanticize this as inevitable. It was not. The move into implantable pacemakers required capital the garage did not have, and by the early 1960s the young company was strained to the point of financial crisis, forced to raise outside money and professionalize just to survive the very success of the products it had invented. That pattern — a breakthrough that outruns the organization's ability to fund and manage it — would recur, in different clothes, for the next sixty years. The lesson embedded in the founding is subtle: Medtronic's problem was rarely a shortage of great ideas. It was almost always the machinery required to industrialize them profitably.

That ethos built a durable moat — deep, trust-based relationships between Medtronic reps and the doctors who implanted its products. But the same story carried a warning that would not detonate for fifty years. A culture organized around relationships and heroic responsiveness is a culture organized around service, not cost. It teaches an organization to say yes, to add, to be present in every operating room. It does not teach it to consolidate factories or strip out overhead. The garage gave Medtronic its clinical soul and, eventually, its structural burden. To understand how that burden accumulated, we have to watch the empire scale.

III. Scaling the Medtech Empire

If the garage era was about survival, the decades that followed were about domination. From the 1960s into the 1990s, Medtronic did something rare in any industry: it took an early technical lead in a life-or-death category and simply never let go. Cardiac rhythm management — pacemakers for hearts that beat too slowly, and later implantable defibrillators for hearts that beat dangerously fast — became a franchise so entrenched that for years the real question in the category was not whether Medtronic would lead but by how much.

The genius was never purely the device. It was the go-to-market. Medtronic pioneered a sales model in which the representative was not a visitor dropping off catalogs but a technical partner physically present in the operating room, advising the surgeon in real time on how to place and program the implant. Think about the psychology of that. A cardiologist implanting a defibrillator in a living patient does not want to save a few hundred dollars by switching to an unfamiliar brand whose rep is not standing beside them. The rep became part of the procedure. That is switching cost manufactured through service, and it let Medtronic command what the industry came to call the "Medtronic Premium" — gross margins that ran above 70%, sustained not by patents alone but by trust and habit at the point of care.

There was a second layer to the franchise that mattered enormously: the implantable cardioverter-defibrillator, or ICD. If a pacemaker's job is to speed up a heart that beats too slowly, an ICD's job is to shock a heart that is racing toward a fatal arrhythmia — a tiny paramedic living permanently inside the chest. ICDs were higher-priced and more sophisticated than pacemakers, and they turned cardiac rhythm management into a multi-billion-dollar profit machine. But they also drew the first serious challengers. Guidant (later absorbed into Boston Scientific) and St. Jude Medical (later absorbed into Abbott) fought Medtronic device-for-device, and cardiac rhythm evolved from a Medtronic monopoly into a genuine three-way war. That competitive structure — a small number of deep-pocketed rivals matching each other's technology — is the recurring shape of medtech, and it is why "dominant" so rarely means "uncontested."

With the cash that franchise threw off, Medtronic expanded by analogy. If you can send precisely timed electrical pulses into cardiac tissue, you can send them into nerves and the brain — and so was born neuromodulation: deep brain stimulation to quiet the tremors of Parkinson's disease, and spinal cord stimulators to interrupt chronic pain. The company was, in essence, exporting its core competence — controlled electrical stimulation of human tissue — into adjacent, high-margin niches where it again arrived early and stayed.

In 2001 came another empire-widening bet, one whose consequences would echo two decades later: Medtronic paid roughly $3.7 billion to acquire MiniMed, the Northridge, California-based world leader in insulin-pump therapy, planting the company's flag in diabetes.22 Remember that address — Northridge — because it becomes the scene of one of Medtronic's ugliest self-inflicted wounds much later in this story. For now, note only the strategic instinct: whenever Medtronic saw a chronic-disease category where a device could be sold at a premium into a physician relationship, it bought its way to the front, financed by the cardiac cash engine.

Then came the deal that made Medtronic a giant beyond the heart. In 1999, it acquired Sofamor Danek for roughly $3.7 billion in stock, vaulting itself to the top of the spinal implant market overnight.13 Spine was a different kind of business — screws, rods, and cages sold into orthopedic and neurosurgical suites — but it fit the model: high-value implants, surgeon relationships, premium pricing. By the turn of the millennium, Medtronic was no longer a pacemaker company; it was a multi-segment medtech conglomerate touching the heart, the spine, the brain, and the nervous system.

Here is the part the triumphant version of the story leaves out. Every one of those franchises grew up as its own world, with its own sales force, its own engineers, its own back office, its own way of doing things. Uncontested growth is a wonderful thing for a P&L and a corrosive thing for organizational discipline. Because each division was winning, no one forced them to share infrastructure or standardize. Duplicate systems multiplied. Supply chains sprawled. Multiple Medtronic reps from different divisions might call on the same hospital, none aware of the others. The company was accreting the classic pathology of the successful conglomerate — a matrix of overlapping fiefdoms, each individually excellent, collectively bloated. For years, market dominance masked the cost. The masking would end when a single decision doubled the complexity in one stroke: the Covidien deal.

IV. The $43B Covidien Corporate Inversion Gamble

By 2014, Omar Ishrak — the GE Healthcare veteran who had taken over as Medtronic's CEO in 2011 — was sitting on a very specific, very American problem. Medtronic had piled up billions of dollars in cash overseas, earnings generated abroad that it could not bring home without handing roughly 35% to the U.S. Treasury. The money was real, but trapped. And Ishrak wanted to spend it — on acquisitions, on R&D, on buybacks — not watch it decay in foreign accounts.

The solution his bankers brought him was audacious: a corporate inversion. Medtronic would acquire Covidien plc, a large Irish-domiciled maker of surgical supplies and minimally invasive tools — vessel-sealing instruments, surgical staplers, the unglamorous but essential hardware of the operating room. Because Covidien was legally Irish, the combined company could be domiciled in Dublin while keeping its operational nerve center in Minneapolis. The new parent, Medtronic plc, would become an Irish company for tax purposes.

The numbers were staggering. Announced in June 2014 and closed in January 2015, the deal was valued at roughly $42.9 billion in cash and stock, or about $49.9 billion including Covidien's debt — the largest medtech acquisition in history and the largest tax inversion any American company had ever executed.89 Overnight, Medtronic's trapped overseas cash became deployable, and its blended tax rate fell.

The deal nearly did not survive contact with Washington. Inversions had become a political lightning rod, and in September 2014 — before the transaction closed — the U.S. Treasury issued Notice 2014-52, a set of rules explicitly designed to make inversions less attractive. It was potent enough to force Medtronic to restructure how it financed the Covidien purchase, moving away from the so-called "hopscotch" loan techniques that would have let it tap overseas cash tax-free.23 Medtronic pushed the deal through anyway. Others were not so lucky: barely a year later, in April 2016, a further Treasury crackdown killed the even larger Pfizer-Allergan inversion outright.23 Medtronic, in other words, squeezed through a closing regulatory window that slammed shut behind it — a piece of timing that flatters the deal's boldness and should also make an investor wonder how durable a strategy built on a soon-to-be-plugged loophole could really be.

But strip away the tax engineering and ask the harder question a skeptical investor would ask: what did shareholders actually buy? They bought a business that was, by Medtronic's own standards, mediocre. Covidien's surgical-supplies portfolio grew more slowly and carried lower margins than Medtronic's premium implant franchises. Analysts pegged the purchase at a rich multiple — well into the high teens or low twenties on forward earnings — for a slower-growth asset.8 The strategic logic was that Covidien's minimally invasive surgical tools would ride the secular shift toward less invasive procedures. The financial reality was that Medtronic bolted a lower-quality growth engine onto a higher-quality one and paid a premium for the privilege.

And the deal left a mark on the balance sheet that would linger for a decade: tens of billions of dollars of goodwill and intangibles. Goodwill is the accountant's word for "the premium we paid over the tangible worth of what we bought." It is not inherently bad, but it is a standing dare: it depresses return on invested capital until the acquired business earns enough to justify the price. For years afterward, Medtronic's ROIC bore the weight of that Covidien premium, one quiet reason its stock compounded more slowly than pure-play peers even as revenue grew.

There was an organizational cost, too, and it proved more insidious than the financial one. Integrating a company nearly the size of a peer meant layering group-level executives and shared functions on top of an already complex matrix. The distance between the people making strategic decisions and the engineers actually designing products widened. In a business where speed to the physician had always been the edge, adding bureaucratic altitude was precisely the wrong trade. Nimble competitors noticed.

Finally, there was a bill sent to the company's most loyal constituency. Because the transaction was structured as an inversion involving a share exchange, many long-time U.S. retail shareholders — including Minnesotans who had held Medtronic for decades — were hit with an involuntary capital-gains tax on the swap, owing money to the IRS for a "sale" they never chose to make.8 It was a public-relations wound in the company's own backyard, and it captured the deal's essential character: financially clever, humanly clumsy.

And then history delivered the deal's cruelest irony. The entire strategic premise of the inversion was that the U.S. corporate tax rate — 35%, among the highest in the developed world — made it economically irrational to keep earning and repatriating profits as an American company. But in December 2017, the Tax Cuts and Jobs Act slashed the federal corporate rate from 35% to 21% and shifted the U.S. toward a territorial system, dramatically narrowing the very gap that had justified fleeing to Dublin.24 Companies that had endured the political bruising and shareholder tax hit of inverting suddenly found the arbitrage far smaller than when they had signed up for it. Medtronic still enjoys a lower structural tax rate than a purely domestic peer, and it retains the flexibility inversion bought. But the headline rationale — escaping a punitive 35% rate — was substantially undercut within three years of closing by a change in the law that no banker's model had priced in. The tax benefit was real but eroding; the operating complexity was real and compounding. The inversion solved a tax problem that Washington then partly solved for free, and created a decade-long operating problem that no one solved at all. Untangling that problem would fall to a new CEO, arriving at the worst possible moment.

V. Matrix Bloat and the Geoff Martha Decentralization Playbook

For five years after Covidien closed, the story was stagnation dressed up as stability. Medtronic's revenue grew, but organically — stripping out acquisitions and currency — it often crawled in the low single digits. Meanwhile the competition was sprinting. Boston Scientific was clawing share in cardiac rhythm and structural heart; Stryker was compounding briskly in orthopedics and surgical equipment; and a wave of focused pure-plays kept out-innovating the giant in specific niches. The pattern was maddeningly consistent: Medtronic would have a strong product, but the decision to fund it, launch it, or reposition it had to travel up and down so many layers of the matrix that speed leaked out at every handoff.

Into this walked Geoff Martha. A former Stryker executive who had joined Medtronic in 2011 and run the spine and later the restorative therapies businesses, Martha was named CEO effective April 2020 — timing that would be almost comic if it were not so brutal. He inherited the corner office exactly as COVID-19 shut down the world. Elective surgeries — the bread and butter of a device company — were postponed en masse as hospitals braced for the pandemic. Medtronic's economics, built on procedures, cratered overnight: in the quarter ending April 24, 2020, revenue fell about 26% year over year as procedures froze across the globe.21 Martha took over a supertanker just as the sea disappeared.

The pandemic did hand Medtronic one strange spotlight. It happened to own a ventilator business — normally a sleepy, low-margin corner of the portfolio — and for a few months in 2020 ventilators were the most sought-after medical devices on Earth. Medtronic roughly doubled ventilator output and, in an unusual move, publicly shared the design specifications for one of its ventilators so that other manufacturers could help meet demand.21 It was a genuine mission moment, straight out of Bakken's playbook, and it generated goodwill. But ventilators were a rounding error against the collapse in high-margin elective procedures. The episode is a useful reminder of the business's real shape: Medtronic makes its money when operating rooms are busy, and anything that empties them — a pandemic, a recession, a hospital budget freeze — hits it fast and hard. That vulnerability is precisely why organizational speed and cost flexibility matter so much, and precisely what Martha set out to rebuild.

Martha's diagnosis, delivered with unusual candor for a sitting CEO, was that Medtronic had become too bureaucratic and too slow, and that the fix was not more central control but less. He argued the company had been operating like a holding company of divisions where accountability was diffuse.11 His remedy became the defining bet of his tenure: he blew up the legacy business-group structure and reorganized the entire company into roughly twenty independent operating units — cardiac rhythm, structural heart, spine, diabetes, surgical, and so on — each with its own P&L, its own R&D budget, and its own leader who owned the results.11 The theory was elegant. Push decision rights down to the people closest to the physicians and the products, and you recover the speed of a startup inside the body of a giant.

Martha's own incentives were structured to make the transformation personal. Under Medtronic's executive pay design, the large majority of his target compensation is tied to hard performance metrics — non-GAAP earnings per share, organic revenue growth, and free cash flow — with an explicit product-quality modifier that can dock the payout if the company's devices stumble on safety. He is also required, under stock-ownership guidelines, to hold Medtronic shares worth several multiples of his base salary, keeping his personal wealth lashed to the stock. On paper, this is exactly the alignment a shareholder wants. In practice, as we will see, alignment is necessary but not sufficient — you can be perfectly incentivized and still preside over years of underperformance if the machine underneath you resists change.

One capital-allocation move from this period deserves its own spotlight because it was genuinely creative. In June 2020, weeks into the pandemic, Medtronic struck a deal with Blackstone Life Sciences: up to $337 million in outside funding to bankroll four specific diabetes R&D programs.10 The structure was clever. Blackstone funded the development costs; if the products succeeded and shipped, Medtronic would pay Blackstone royalties in the low-to-mid single digits as a percentage of sales.10 In effect, Medtronic rented risk capital for its pipeline without issuing a single new share or adding corporate debt, sharing the upside only if the bets paid off. For a legacy giant trying to fund expensive innovation without bloating its balance sheet, it was a model worth studying — and we will return to it in the playbook. But R&D financing is a sideshow next to the real test of Martha's decentralization: did the operating units actually win in the segments where the wars are fought? Time to go to the front lines.

VI. Segment Battles and the High-Stakes Tech Wars

Medtronic reports through four large segments, and they are wildly different businesses wearing the same corporate logo. Read the fiscal 2025 scorecard and the company's strategic reality jumps off the page: Cardiovascular at $12.48 billion, Neuroscience at $9.85 billion, Medical Surgical at $8.41 billion, and Diabetes at $2.76 billion.1 Two of those four grew nicely, one barely grew at all, and one grew fastest of all right before the company decided to get rid of it. Let us take them in turn, testing management's claims against the evidence rather than the press releases.

1. Cardiovascular Segment (~$12.5B, ~37% of FY25 Revenue) — The Crown Jewel

The heart business remains what it has always been: the largest, most profitable, and most defensible thing Medtronic owns, generating $12.48 billion in fiscal 2025.1 Its emotional and technical centerpiece is Micra, the world's smallest pacemaker — a leadless device roughly the size of a large vitamin capsule that is delivered through a catheter in the leg and anchored directly inside the heart, with no surgical pocket under the skin and no wires (called "leads") threaded through the veins.

Why does that matter? For sixty years, the weak point of a pacemaker was never the pulse generator — it was the leads. Wires running from a chest pocket into the heart can fracture, dislodge, or become infected, and infected leads are a genuine medical nightmare. By eliminating them, Micra attacks the single biggest source of complications in the field. When the FDA approved the first Micra device in 2016, it was the first leadless pacemaker cleared in the United States.15 And the clinical data Medtronic has accumulated since is the real moat: a large post-approval registry followed patients for five years and found major complication rates meaningfully lower than those of traditional transvenous systems, with implant success rates around 99%.7 In a field where cardiologists are conservative by temperament and litigation-shy by necessity, a mountain of multi-year safety evidence is worth more than any marketing budget. That is a cornered clinical dataset — hard to replicate because it requires years of real-world implants that competitors starting later simply do not have yet.

The other cardiovascular front is far more contested: structural heart, specifically TAVR — transcatheter aortic valve replacement, the procedure that lets doctors replace a diseased aortic valve by threading a new one up through an artery instead of cracking open the chest. Here Medtronic's Evolut platform fights a genuine war against Edwards Lifesciences and its Sapien valves. Edwards has long held the volume lead and the deeper installed base. Medtronic's counter is technical: its Evolut valve is self-expanding and sits in a "supra-annular" position — above the valve's narrowest ring — which tends to deliver better blood flow (hemodynamics) in patients with small aortic anatomy. That is a real, physician-recognized edge in a specific patient subset, not marketing spin. But it is an edge, not a knockout: this is a two-horse race where each side wins particular patients, and neither is dislodging the other soon. For investors, structural heart is a durable growth market where Medtronic is a strong number two — respectable, but not the monopoly economics of the pacemaker glory days.

The most important emerging front inside cardiovascular is cardiac ablation — the treatment of atrial fibrillation, the common irregular heartbeat that afflicts tens of millions of people and is one of the largest growth pools in all of medtech. The historic technique burned or froze tiny areas of heart tissue to silence the electrical short-circuits driving the arrhythmia. The new modality shaking the field is pulsed field ablation (PFA), which uses precisely targeted electrical pulses to destroy the offending tissue while largely sparing the surrounding esophagus and nerves — a meaningful safety improvement that has cardiologists switching quickly. Medtronic is a serious competitor here, but so are Boston Scientific and Johnson & Johnson's MedTech arm, and the PFA transition is exactly the kind of technology inflection that can reshuffle share. It is a segment worth watching closely: whoever wins the PFA era wins a market growing far faster than the mature pacemaker business, and Medtronic's position is strong but not assured.

2. Neuroscience Segment (~$9.85B, ~29% of FY25 Revenue) — The Ecosystem Lock-in

Neuroscience — spine, neuromodulation, and neurosurgery — brought in $9.85 billion in fiscal 2025.1 The most instructive story here is spine, because it shows Medtronic trying to escape a trap of its own commoditization. Spinal implants — the screws, rods, and cages — have become, in economic terms, close to commodities. Multiple credible competitors like Globus Medical and Stryker make perfectly good hardware, and hospitals under cost pressure are happy to negotiate.

Medtronic's answer is a platform called AiBLE, and understanding it is understanding modern medtech strategy. The idea is to stop selling the surgeon a box of screws and start selling them an integrated system: Mazor surgical robotics (acquired in 2018 for roughly $1.6 billion) to plan and guide the operation, StealthStation navigation to see inside the patient in real time, imaging, data, and the implants themselves — all designed to work together.12 Once a hospital buys into the ecosystem — the robot, the navigation towers, the software, the workflow, the staff training — ripping it out to switch to a competitor's implants becomes painful and expensive. This is Hamilton Helmer's classic switching-cost power, manufactured deliberately. You do not compete on the price of a screw; you compete on the cost of abandoning an entire operating-room platform you have already learned.

The honest caveat: switching costs are powerful only if the ecosystem is genuinely better and genuinely sticky, and the robotic-spine market is young and fiercely contested. Globus, which merged with NuVasive, is a determined ecosystem competitor of its own. The lock-in is real but not absolute, and the capital cost of placing robots and navigation systems in hospitals is a drag that must eventually convert into implant pull-through to pay off. So far the strategy is credible and directionally working, but it is a bet on integration outrunning commoditization, not a settled victory.

The other half of neuroscience is neuromodulation — the deep brain stimulators and spinal cord stimulators descended directly from Medtronic's cardiac-pacing heritage. This is a business where the company invented the category and then, over the last decade, repeatedly found itself out-innovated by focused rivals such as Abbott and Boston Scientific, who pushed newer waveforms and closed-loop features while Medtronic's matrix debated. Martha's operating units have been trying to reverse that, and the strategic direction is clear: move from "open-loop" devices that deliver a fixed dose of stimulation to "closed-loop" systems that sense the body's own signals and adjust in real time — the same conceptual leap the diabetes business made from a dumb pump to an automated one. Whether Medtronic has genuinely regained the innovation lead in neuromodulation, or merely caught up, is one of the quieter open questions in the portfolio, and a fair test of whether decentralization actually restored the company's product speed where it had most visibly lost it.

3. Medical Surgical Segment (~$8.41B, ~25% of FY25 Revenue) — The Surgical Robotics Battle

This is the old Covidien heartland — surgical staplers, energy devices, advanced wound care — and in fiscal 2025 it delivered $8.41 billion of revenue while growing organically less than 1%.1 That number is the quiet indictment of the Covidien thesis a decade on: the segment is large, cash-generative, and barely growing. It is the ballast, not the engine.

But bolted onto this slow-growing base is Medtronic's single most audacious swing: Hugo, its robotic-assisted surgery system, and its long campaign to challenge Intuitive Surgical's near-total dominance of soft-tissue robotic surgery. To grasp why this is so hard, you have to understand why Intuitive's da Vinci is one of the great franchises in all of medtech. Intuitive placed thousands of robots into hospitals over two decades, and every one of them is a permanent annuity: the robot itself is the razor, but the real money is the blades — the specialized instruments and accessories that must be replaced after a set number of uses, generating high-margin recurring revenue on every single procedure, forever. Layer on top of that a generation of surgeons who learned to operate on da Vinci consoles during their residencies, hospital service contracts, and mountains of clinical data, and you have one of the deepest switching-cost moats in healthcare. A surgeon fluent in da Vinci does not casually retrain on a rival system, and a hospital that has sunk millions into da Vinci capital does not lightly buy a second fleet. Cracking that is arguably harder than anything else in this report.

For years, Hugo was a credibility problem. Rollouts slipped. There were software issues, supply-chain delays, and timelines that kept moving right, with management too often reaching for "macro factors" as the explanation — the kind of vague framing that a skeptical analyst learns to distrust. Then, on December 3, 2025, the story changed: the FDA cleared Hugo for urologic procedures such as prostatectomy, nephrectomy, and cystectomy, opening the door to a U.S. commercial launch in early 2026.3 The clearance was backed by the Expand URO clinical study, which met its primary safety and efficacy endpoints across 137 patients, and the first U.S. commercial case — a robot-assisted prostatectomy — was performed at the Cleveland Clinic.34

Now for the credibility critique, because this is where independence matters most. Management argues Hugo's modular, multi-arm-cart design is superior to da Vinci's single-boom architecture because the carts can be wheeled between operating rooms, improving utilization. That is a plausible engineering argument. It is not yet an economic fact. There is thin public evidence that Hugo delivers superior outcomes or better hospital economics, and Intuitive is not standing still — it is rolling out its next-generation da Vinci 5 into that same loyal installed base. Outside the U.S., Hugo has accumulated real experience across tens of thousands of procedures in more than 30 countries, which de-risks the technology somewhat.4 But the correct way to hold Hugo today is as a capital-intensive, high-optionality hedge against a robotic future — not a proven commercial win. A urology clearance is a starting gun, not a finish line; the indications that matter most for scale, general and gynecologic surgery, are still pending submissions.3

4. Diabetes Segment (~$2.76B, ~8% of FY25 Revenue) — The Turnaround and Planned Exit

The smallest segment produced the most dramatic arc. Diabetes generated $2.76 billion in fiscal 2025 and grew organically more than 11% — the fastest of any Medtronic segment.1 The irony is that the company decided to spin it off precisely as it hit its stride, and to understand why you have to rewind to the crisis.

On December 9, 2021, the FDA hit Medtronic's Diabetes headquarters in Northridge, California with a scathing warning letter, citing failures across quality-system requirements — risk assessment, corrective actions, complaint handling, adverse-event reporting.16 The practical consequence was devastating: it effectively froze new product approvals, and while Medtronic was hamstrung, competitors Dexcom, Insulet, and Tandem sprinted ahead in the fast-moving automated insulin-delivery market. The company's most modern pump, the MiniMed 780G with its SmartGuard closed-loop algorithm — a system that automatically adjusts insulin using continuous glucose readings, functioning like a partial "artificial pancreas" — sat waiting.

The comeback took nearly eighteen months. In April 2023 the FDA both approved the MiniMed 780G and lifted the warning-letter restrictions, and the business began clawing back momentum.[^10]17 It is a genuine execution recovery — and also a genuine indictment, because the crisis was self-inflicted, a quality-control failure at the very Northridge facility Medtronic had bought into diabetes to acquire back in 2001, in exactly the domain (device safety) where Medtronic's whole brand promise lives. The competitive cost of those lost eighteen months was steep: in automated insulin delivery, a market moving at software speed, ceding a year and a half to Dexcom, Insulet, and Tandem is an eternity, and the 780G launched into a landscape those rivals had already reshaped.

What makes the closed-loop system genuinely valuable is worth spelling out in plain terms. A modern automated insulin-delivery system links a continuous glucose monitor (a sensor that reads blood sugar every few minutes) to an insulin pump through an algorithm that adjusts dosing automatically — nudging insulin up or down without the patient constantly calculating and injecting. It is a partial artificial pancreas, and it is exactly the kind of hardware-plus-software-plus-data product that creates stickiness, because a patient who trusts a system managing their metabolism around the clock is loath to switch. MiniMed's distinctive pitch is that, unlike most rivals who make only the pump or only the sensor, it makes both — the full stack. Whether the newly independent company can turn that integration into share gains against faster-moving specialists is the central question the public market will now price, and its cautious IPO valuation suggests investors want to see the proof before paying for the promise.

Which brings us to the exit. Management concluded that diabetes, with its volatile competitive dynamics and different capital needs, no longer fit a company trying to concentrate on high-margin core franchises. So Medtronic moved to separate the business, rebranded as MiniMed, via an IPO followed by a split-off to shareholders. In December 2025, MiniMed filed its IPO registration statement, planning to list on Nasdaq under the ticker MMED.5 The offering priced below its initial hopes — raising about $560 million at $20 per share for roughly a $5.6 billion valuation, well short of the $25–$28 range and near-$8 billion valuation once floated.620 The muted pricing tells its own story: the public market liked the standalone diabetes business less than Medtronic had hoped, a reminder that "unlocking value" through a spin-off works only if buyers agree the value was there. Untangling one of four operating segments while simultaneously trying to consolidate the whole company's manufacturing footprint is exactly the kind of complexity that attracts activists — which is where the story goes next.

VII. The Activist Stress Test: Elliott Management Demands Execution

Activists do not show up at healthy, admired, fast-compounding companies. They show up where there is a gap between what a business could be worth and what it is worth — and by the summer of 2025, Medtronic was practically an engraved invitation. Years of low-single-digit organic growth, a decade of goodwill dragging on returns, self-inflicted quality crises, a stock that had underperformed nimbler peers, and a manufacturing footprint bloated by legacy M&A. To a firm that hunts conglomerate discounts for a living, that profile is catnip.

The firm that answered the invitation was Elliott Investment Management, the Paul Singer-founded fund with a reputation as one of the most relentless and technically sophisticated activists in the world. Elliott's history is instructive: it has taken on targets from technology giants to national governments, and its campaigns tend to be meticulously researched, patient, and — when resisted — unforgiving. When a fund of that pedigree quietly builds a position and then shows up asking for board seats, boards tend to do the math on what a public proxy fight would cost in distraction, legal fees, and reputational damage, and conclude that negotiation is cheaper than war. In August 2025, word emerged that Elliott had accumulated a large stake, positioning itself among Medtronic's biggest shareholders.2 Elliott's implicit case was the classic activist thesis, sharpened to Medtronic's specifics: here is a company with world-class clinical assets trapped inside a mediocre operating chassis. Too many manufacturing plants inherited from decades of acquisitions. A supply chain never rationalized after Covidien. A history of missed launches and inventory write-downs. In short, the products were the envy of the industry and the execution was not — a conglomerate discount begging to be closed.

What happened next is telling about both sides. Rather than absorb the cost and reputational bruising of a public proxy fight, Medtronic moved fast to settle. On August 19, 2025, it announced two new independent directors and a new governance architecture explicitly framed as being done in partnership with Elliott.219 The two board appointments were not random; they were a message about what kind of company Medtronic was now supposed to become. John Groetelaars, former CEO of Hillrom, brought deep hands-on medtech operating experience. Bill Jellison, the former chief financial officer of Stryker, brought something more pointed: Stryker is legendary in the industry for a disciplined, high-margin operating model — precisely the culture Medtronic has struggled to build.2 Putting a Stryker financial architect on the board is the corporate equivalent of hiring your most admired rival's coach.

The structural changes were designed to force focus. Medtronic created two new board-level committees, both chaired by CEO Geoff Martha. A Growth Committee took ownership of portfolio decisions — tuck-in M&A discipline and shepherding the diabetes separation. An Operating Committee, drawing on Jellison's and Groetelaars's expertise, was aimed squarely at the unglamorous, value-creating grind: consolidating factories, rationalizing the supply chain, and expanding non-GAAP operating margins.219 The company also signaled it would lay out the fruits of this work at an investor day in mid-2026.2 The choreography of chairing those committees with the CEO is itself a compromise: it keeps Martha central while ensuring the activist's chosen operators sit close enough to hold him to the numbers.

A fair assessment of management credibility has to weigh both sides of the ledger. On the debit side: a decade of organic growth that lagged the best peers, a self-inflicted diabetes quality crisis, a robotics program whose repeatedly slipping timelines were too often waved away with references to "macro factors," and the fact that it took an activist's arrival to force the operating-discipline conversation the company should arguably have led itself. On the credit side: Medtronic has been a consistent, disciplined returner of capital, sustaining a long multi-decade streak of annual dividend increases even through the pandemic trough, and Martha has been willing to make genuinely hard structural moves — blowing up the matrix, exiting diabetes — rather than defend the status quo. The honest read is a management team that is strategically bold and operationally unproven, and whose most important promises about margins and speed remain, as of mid-2026, largely unbanked. That is precisely the profile that invites an activist to supply the accountability the market feels is missing.

Here is the credibility fulcrum on which the whole story now balances. Martha's signature achievement — breaking the matrix into twenty accountable operating units — bought Medtronic real agility. But decentralization has a well-known cost: it duplicates overhead. Twenty units with their own leadership and functions tend to carry more SG&A than one centralized machine. Elliott's operating agenda is, in effect, a demand to keep the agility while stripping the fat — a genuine tension, not a slogan. Martha spent five years pushing accountability down; the board is now pushing cost discipline across. Whether those two forces reinforce or fight each other is the single most important open question about Medtronic, and it is exactly the kind of test that separates management teams that talk about margins from those that deliver them. The mid-2026 investor day will be the first real scorecard.

VIII. Playbook: Business & Investing Lessons

Step back from the specifics, and Medtronic offers a set of lessons that generalize far beyond medical devices — the kind of durable principles worth carrying to the next company you analyze.

Lesson 1: Financial engineering cannot outrun operational drag. The Covidien inversion was a genuinely clever solution to a genuine tax problem, and it delivered exactly what it promised on tax. But tax savings are a one-time re-rating; operating quality compounds forever. By bolting a lower-margin, slower-growth business and a decade of goodwill onto the enterprise, the deal introduced a structural drag that quietly offset much of the tax win. The lesson for investors evaluating any acquisition dressed up in balance-sheet cleverness: separate the financial trick from the operating business you are actually buying, and ask whether the second one is any good. A brilliant structure wrapped around a mediocre asset is still a mediocre asset.

Lesson 2: In mature hardware, sell the ecosystem, not the widget. The spine story is the whole industry in miniature. When the physical implant becomes a commodity that any competent competitor can match, margins erode and the buyer gains power. The escape hatch is to wrap the commodity in a proprietary system — robotics, navigation, software, data — so that the customer is buying a workflow they cannot easily leave, not a part they can competitively bid. This is Helmer's switching-cost power built by design. But note the discipline required: the ecosystem has to be genuinely better, or it is just an expensive way to sell the same screws.

Lesson 3: The matrix is where speed goes to die. Medtronic's decade of stagnation was not caused by bad products; it was caused by good products moving too slowly through too many layers. In technical industries where the edge comes from proximity between engineers and customers, every layer of corporate altitude you add between them is a gift to a nimbler rival. Martha's twenty-operating-unit bet is, at heart, a wager that structure is destiny — that you can restore a giant's speed by shortening the distance between the people who build and the people who buy. It is an unfinished experiment, and worth watching precisely because so many large companies face the same trap.

Lesson 4: Rent risk capital before you dilute or over-lever. The Blackstone diabetes partnership is a template more legacy giants should study. Faced with expensive, uncertain R&D, Medtronic funded it with outside capital that took the downside risk in exchange for a royalty on success — no new shares, no new corporate debt, risk shifted to a partner explicitly in the business of underwriting it.10 For any mature company with more good ideas than balance-sheet appetite for risk, structured external financing of specific programs is an underused tool. The catch is that it caps your upside on the winners; it is insurance, and insurance is never free.

The thread connecting all four lessons is discipline — of capital allocation, of portfolio focus, of organizational design. Which is exactly what the market has doubted about Medtronic, and exactly what the final analysis must weigh.

IX. Analysis, Risks, and the Bull vs. Bear Case

To judge Medtronic honestly, we have to hold two truths at once: it owns some of the best clinical franchises ever assembled in medtech, and it has repeatedly failed to translate that quality into peer-beating shareholder returns. The frameworks help us locate exactly where the advantage is real and where it is eroding.

Myth versus reality. Two consensus narratives are worth puncturing before the analysis. The first myth is that Medtronic is a slow, dying dinosaur — a story the underperformance seems to support. The reality is more uncomfortable for both bulls and bears: this is not a company that has stopped innovating. Micra, Evolut, AiBLE, the renal-denervation program, and a robot that finally reached U.S. operating rooms are real, category-relevant products. The failure has been organizational and financial, not scientific — which is either encouraging (the hard part, invention, works) or damning (the company has proven it can invent and still not create shareholder value). The second myth is that the Covidien inversion was a masterstroke. The reality, with a decade of hindsight, is that it was a clever tax trade wrapped around a mediocre operating asset, its central rationale partly neutralized by the 2017 tax law, and its organizational cost still being paid down under activist supervision. Holding both myths up to the light is the right frame for what follows.

1. Porter's Five Forces and Helmer's Seven Powers

Start with the buyers, because that is where the pressure is most acute. The bargaining power of buyers is high and rising. Hospitals have consolidated into large systems and buy through group purchasing organizations (GPOs) that aggregate demand and negotiate hard. For commoditizing categories — basic implants, surgical supplies — that consolidation is a direct, structural squeeze on price, and it is not going away. This is the single most important force acting against Medtronic's legacy margins.

The threat of substitutes is moderate but genuinely rising in a way that is easy to underestimate. The wildcard is pharmaceuticals, specifically the GLP-1 weight-loss and metabolic drugs. Over a long horizon, dramatically healthier populations could soften demand for some cardiovascular and diabetes devices — fewer sick hearts, fewer complications. This is not a near-term earnings threat, but it is a real long-duration question mark hanging over parts of the portfolio, and a serious long-term investor should hold it in mind rather than dismiss it.

The threat of new entrants is low for the core franchises — the regulatory barriers, the multi-year clinical-evidence requirements, and the surgeon-relationship moats make greenfield entry brutally hard. But rivalry among established players is intense, and that is where Medtronic actually bleeds: Boston Scientific, Abbott, Edwards, Stryker, Intuitive, Globus — each a formidable, often more focused competitor in a specific arena.

Through Helmer's Seven Powers lens, Medtronic clearly possesses two. It has genuine scale economies in global distribution and manufacturing — the ability to reach 150-plus countries with a vast product breadth that few can match. And it has real switching costs, both the old-fashioned kind (the trusted rep in the operating room) and the engineered kind (integrated surgical ecosystems like AiBLE). What it conspicuously lacks is cornered resources across the board — with the partial exception of specific multi-year clinical datasets like Micra's, competitors can and do match its raw device capabilities. That absence is the analytical heart of the bear case: without a resource rivals cannot replicate, scale and switching costs must be defended through relentless execution — the very thing Medtronic has struggled with.

There is also a subtle paradox in Medtronic's scale. Conventional analysis treats scale as an unalloyed advantage, and in distribution it is. But Elliott's entire thesis is that at Medtronic, scale has partly curdled into diseconomy — that the breadth which lets the company reach every hospital on Earth also produced the duplicated factories, tangled supply chain, and matrix overhead that pure-play rivals like Edwards (all valves) or Intuitive (all robots) simply do not carry. A focused competitor can optimize one supply chain; Medtronic must coordinate dozens. This is the deep reason a "conglomerate discount" exists and why focused peers have compounded faster: in modern medtech, the advantages of scale in distribution can be outweighed by the disadvantages of scale in complexity. The bet the activist and management are jointly making is that you can keep the former while surgically removing the latter — a genuinely difficult, and genuinely unproven, proposition.

2. Three KPIs That Actually Matter

An investor does not need a dashboard of fifty metrics. Three tell the story.

First, organic revenue growth. This is the truest measure of whether the twenty-operating-unit bet is working, stripped of the noise of currency and M&A. The market's rough demand is that Medtronic sustain organic growth in the mid-single digits — roughly 4.5% to 6% — especially once the faster-growing diabetes business is gone. Consistently landing in that band would be the proof that decentralization restored durable, above-GDP growth; slipping back toward the low single digits would confirm the bears.

Second, non-GAAP operating margin expansion. This is Elliott's whole thesis reduced to a number. Can the new Operating Committee actually consolidate factories and streamline the supply chain into steady, visible margin gains? Watch for consistent annual expansion; watch even more closely for whether management sets a specific, dated margin target at the mid-2026 investor day and then hits it. Vague aspiration is failure; a hard target met is credibility rebuilt.

Third, Hugo's U.S. adoption. Tracking hospital system placements and clinical-registry procedure volumes following the urology clearance is the cleanest read on whether Medtronic's biggest speculative bet is converting into a real business or quietly becoming a write-off. Early placements are the leading indicator years before the revenue shows up.

3. Current Risk Radar

The material risks are specific, not generic. Execution risk is the largest and most immediate: simultaneously separating MiniMed and consolidating a global manufacturing footprint is a lot of surgery to perform on a company that has struggled with complexity. Competitive-disruption risk is concentrated in robotics, where Intuitive's da Vinci 5 could simply shut Hugo out of the general-surgery indications that matter most for scale. And quality/recall risk is the ever-present shadow over the whole enterprise — the HeartWare HVAD cardiac-pump episode, where Medtronic halted sales in 2021 amid serious safety concerns, and the Northridge diabetes warning letter are reminders that in this industry a quality failure is not just a fine; it can freeze an entire product line and hand share to competitors.1618

A brief second-layer diligence note belongs here, because it shapes how the whole valuation debate resolves. The single accounting figure most worth watching over time is return on invested capital. The Covidien goodwill and intangibles still sit on the balance sheet as a reminder of a premium paid, and reported GAAP earnings continue to carry heavy amortization of acquisition-related intangibles — which is exactly why management steers investors toward non-GAAP figures. The tension is legitimate on both sides: non-GAAP metrics strip out real, if non-cash, costs of past deals and can flatter the picture, while GAAP numbers arguably over-penalize a serial acquirer for capital deployed long ago. A rigorous investor should track whether ROIC is genuinely climbing as the Operating Committee does its work, because that — not adjusted EPS — is the truest measure of whether Medtronic is finally earning an adequate return on the vast sums it has invested and acquired over the decades. If margins expand but ROIC stays stuck, the improvement is cosmetic.

4. The Bull Case

The optimistic thesis is that Medtronic is a coiled spring. It argues the innovation pipeline — Micra, the AiBLE spine ecosystem, Hugo, and Symplicity Spyral, the renal-denervation system for hypertension that won FDA approval in November 2023 — finally scales in concert into a genuine growth supercycle.[^9] It argues Elliott-driven discipline strips out the legacy Covidien back-office bloat and consolidates factories, driving the margin expansion that lifts return on invested capital back toward respectability. And it argues the diabetes separation leaves behind a cleaner, more focused, higher-margin company that the market re-rates once the conglomerate discount lifts. In this telling, everything that has dragged on the stock — complexity, bloat, distraction — is precisely what is about to be fixed, with an activist and two proven operators forcing the pace.

5. The Bear Case

The skeptical thesis is that Medtronic is structurally trapped. Core categories — pacemakers, spinal hardware, surgical staples — keep commoditizing, and GPO-driven price erosion grinds margins down faster than innovation lifts them. Hugo fails to dent Intuitive's fortress, and hundreds of millions in robotics R&D become a cautionary tale rather than a growth engine. And the deepest bear worry is organizational: that decentralization keeps SG&A stubbornly high while factory consolidation runs into the immovable object of internal resistance, leaving Medtronic exactly where it has been — a magnificent inventor stuck in low-single-digit growth, forever promising the operating discipline it never quite delivers. The bear does not doubt the products. The bear doubts the company's ability to run itself, and points to a decade of evidence.

The truth is that both cases rest on the same fact — great assets, questionable execution — and simply bet differently on whether the execution finally changes. Which is why the next twelve months matter more than the last ten years.

X. Epilogue & Outro

Everything now converges on a single event: the mid-2026 investor day, where Geoff Martha and the newly constituted board — Elliott's operators included — will have to put specific, measurable commitments on the table and then be judged against them.2 It is the moment the partnership between a long-tenured CEO and an impatient activist stops being a press release and starts being a scorecard. Either the Operating Committee produces a credible, dated plan for margin expansion and factory consolidation, or the market concludes that Medtronic's problems are cultural and therefore not fixable by governance tweaks.

The tell an investor should watch for is specificity. Vague language about "driving efficiencies" and "sharpening focus" is the vocabulary of companies that intend to keep doing what they have always done. A hard, dated operating-margin target, a named number of factories to be consolidated, a concrete organic-growth commitment for the post-diabetes company — those are the vocabulary of a management team that expects to be held to account. Given that it took an activist to force this conversation, the burden of proof sits squarely on management, and the honest analytical posture is to trust the delivered results over the promised ones. Medtronic has spent a decade telling shareholders that better performance is around the corner; the difference now is that two of its own directors were placed there specifically to check whether the corner ever arrives.

Which returns us to the question that has haunted this company since the garage. Earl Bakken built the first wearable pacemaker in four weeks by adapting a magazine circuit, because he was fast, close to the customer, and unburdened by bureaucracy. Seventy-six years later, Medtronic still invents at that level — Micra, AiBLE, and a robot that finally reached American operating rooms are evidence the clinical genius never left. What it lost somewhere between the garage and Dublin was the speed and discipline to match. The ultimate question is not whether Medtronic can build great machines. It has proven that for three-quarters of a century. The question is whether the company that defined modern medical technology can finally reinvent its own operations to match the excellence of its products — or whether it has simply grown too big, and too complex, to run as well as the devices it makes.

References

-

Medtronic reports fourth quarter and full year fiscal 2025 financial results (Form 8-K exhibit) — Medtronic plc / SEC, 2025-05-21 ↩↩↩↩↩↩

-

Medtronic announces Board appointments and shareholder value creation initiatives to advance strategic priorities — Medtronic Newsroom, 2025-08-19 ↩↩↩↩↩↩↩

-

Medtronic announces FDA clearance of Hugo robotic-assisted surgery system for urologic surgical procedures — Medtronic Newsroom, 2025-12-03 ↩↩↩

-

Hugo robot-assisted surgery system launches on US market — Urology Times, 2025 ↩↩

-

Medtronic announces filing of IPO registration statement for Diabetes business, MiniMed — Medtronic Newsroom, 2025-12-19 ↩

-

Medtronic's MiniMed Group IPO prices shares at $20 each — MD+DI, 2026 ↩

-

Leadless pacemakers at 5-year follow-up: the Micra transcatheter pacing system post-approval registry — European Heart Journal, 2024 ↩

-

Medtronic Completes Covidien Acquisition for $50B — Nasdaq, 2015-01-27 ↩

-

Medtronic Announces a $337 Million Product Investment from Blackstone Life Sciences to Expand Development of Future Diabetes Technologies — Medtronic Newsroom, 2020-06-12 ↩↩↩

-

New Medtronic CEO Maps Out Strategy to Accelerate Innovation — Twin Cities Business, 2020 ↩↩↩

-

Medtronic Completes Acquisition of Mazor Robotics — Medtronic Newsroom, 2018-12-28 ↩

-

Medtronic To Acquire Sofamor Danek — Med Device Online, 1998 ↩

-

Timeline: Earl Bakken and the story of Medtronic — Medical Device Network ↩↩↩

-

FDA approves first leadless pacemaker to treat heart rhythm disorders — U.S. FDA, 2016 ↩

-

Medtronic Diabetes receives FDA warning letter — Medtronic Newsroom, 2021-12-15 ↩↩

-

Medtronic Diabetes unit fully resolves FDA warning letter — MassDevice, 2023 ↩

-

Medtronic adds 2 board seats, forms special committees — MedTech Dive, 2025-08-19 ↩↩

-

Medtronic's revenue dropped 26% in Q4 as coronavirus hit broadly — MedTech Dive, 2020 ↩↩

-

MiniMed Inc. Form 8-K (Medtronic acquisition of MiniMed) — MiniMed Inc. / SEC, 2001 ↩

-

Tax inversion — regulatory history including Notice 2014-52 and the Pfizer-Allergan collapse — Wikipedia ↩↩

-

Trump tax law cut what US drugmakers owed. Now they fear an increase. — BioPharma Dive, 2021 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube