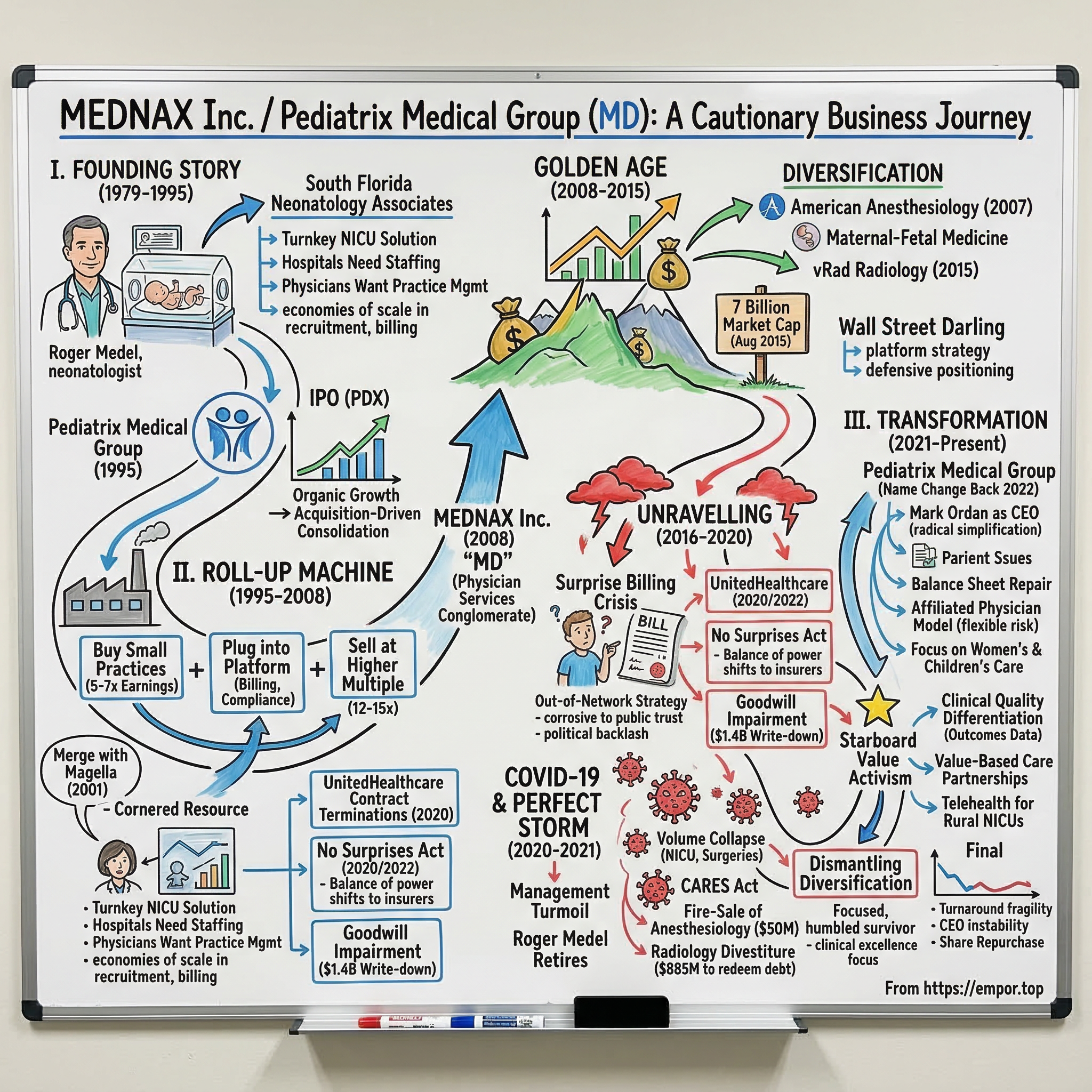

MEDNAX Inc.: The Rise, Fall, and Transformation of America's Physician Outsourcing Empire

I. Introduction & Episode Roadmap

In 2015, MEDNAX Inc. stood atop the American healthcare services landscape with a market capitalization approaching seven billion dollars, more than four thousand affiliated physicians spread across all fifty states, and a reputation as the gold standard in hospital-based physician staffing. Wall Street loved the story: recurring revenue, defensive healthcare positioning, and a seemingly endless runway of small physician practices to acquire. The stock had compounded at double-digit returns for two decades.

By 2024, that same company—now renamed back to Pediatrix Medical Group—traded for roughly a fifth of its peak value, had shed its anesthesiology and radiology divisions for a fraction of what it spent building them, and was fighting for relevance in an industry that had fundamentally turned against its business model. The founder who built the empire over four decades was gone. Three different CEOs had cycled through the corner office. And the regulatory environment that once enabled outsized profits had been rewritten by act of Congress.

This is the story of how a Cuban immigrant neonatologist named Roger Medel saw something no one else did in the chaos of American hospital medicine—the opportunity to professionalize and consolidate the way hospitals staffed their most critical units. It is a story of a roll-up strategy executed with remarkable discipline for two decades, then pushed past its natural limits by the seductions of diversification and financial engineering. It is a story about the collision between corporate healthcare optimization and the messy, deeply human reality of medical care. And it is, ultimately, a cautionary tale about what happens when a business model that depends on regulatory arbitrage meets the full force of political backlash.

The arc follows a pattern that students of business history will recognize: entrepreneurial insight, disciplined scaling, hubris-driven overexpansion, external shock, and painful contraction. But the specific dynamics—physician autonomy versus corporate control, surprise billing as political lightning rod, private equity's invasion of healthcare staffing—make this particular story one of the most instructive in modern healthcare business history.

The central question is deceptively simple: can you build a durable, valuable business by standing between hospitals and the physicians they need? For a long time, the answer appeared to be an emphatic yes. Then everything changed.

This story matters beyond its specifics because it illuminates the fundamental tension at the heart of for-profit healthcare in America. When does the optimization of medical services become extraction from medical services? When does efficient management become corporate control that degrades the clinical mission? When does a business model that is legal become one that is politically unsustainable? MEDNAX's journey from Fort Lauderdale startup to seven-billion-dollar colossus to humbled survivor provides a vivid, data-rich answer to each of these questions.

II. The Founding Story & Birth of Pediatrix (1979–1995)

Picture a neonatal intensive care unit in Fort Lauderdale, Florida, in the late 1970s. The room is dimly lit, filled with the steady beeping of monitors attached to babies so small they could fit in the palm of a hand. A neonatologist—one of perhaps a few thousand in the entire country trained in this emerging subspecialty—moves between incubators, adjusting ventilators, interpreting blood gas results, making life-and-death decisions that would have been impossible a generation earlier. The survival rate for extremely premature infants has been climbing steadily as medical science advances. But the hospitals housing these miracles face a very different kind of problem: finding and keeping the physicians who make them possible.

To understand why Roger Medel founded what would become America's largest neonatal care company, you have to understand this gap between clinical possibility and organizational reality. NICUs were expanding rapidly across the country as advances in neonatal medicine made it possible to save premature babies who would have died a generation earlier. Between the mid-1960s and the late 1970s, neonatal mortality in the United States dropped by nearly half, driven by innovations in respiratory support, surfactant therapy, and the regionalization of perinatal care. Every community hospital with a labor and delivery unit suddenly wanted a NICU—or at least NICU-capable coverage. But these units required a peculiar kind of physician—a neonatologist—and there simply were not enough of them. Fellowship programs produced only a few hundred new neonatologists per year. Hospitals found themselves in a bind. They needed NICUs to serve their communities and attract obstetric patients, but staffing those units was a logistical nightmare. Small groups of neonatologists held enormous leverage, and turnover was a constant headache. A departing neonatologist could leave a hospital scrambling for months to find a replacement, with patient safety hanging in the balance.

Medel, born in Cuba and trained as a neonatologist in South Florida, saw this problem from the inside. He was not your typical physician-entrepreneur—he was a clinician first, someone who spent years at the bedside caring for the tiniest patients before recognizing the business opportunity in the chaos he witnessed every day. Working in Fort Lauderdale's Memorial Hospital and Broward General Medical Center, he understood that hospitals wanted a turnkey solution: someone to recruit the neonatologists, manage the scheduling, handle the billing, and ensure quality—while the hospital focused on running the broader institution. Hospital administrators were not equipped to recruit subspecialty physicians, negotiate individual contracts, handle the complexities of professional malpractice coverage, or manage the twenty-four-seven scheduling demands of a NICU. They needed a partner, not just a physician.

In 1979, Medel and his colleague Greg Melnick founded South Florida Neonatology Associates to be that partner. The timing was critical—this was the era when hospitals were first beginning to experiment with outsourcing clinical services that had traditionally been managed in-house, a trend that would accelerate dramatically in the coming decades.

The early model was elegantly simple. Medel's company would contract with a hospital to manage its NICU entirely. The company would employ or affiliate the neonatologists, handle credentialing and scheduling, implement standardized clinical protocols, and manage the revenue cycle—the complex process of billing insurers and collecting payments for professional services. The hospital got predictability and quality assurance. The physicians got competitive compensation, malpractice coverage, continuing education support, and freedom from administrative headaches. And Medel's company earned a management fee plus a share of the professional fees generated by the physicians' work.

Think of it as a franchise model for medical care. The hospital provided the physical infrastructure—the NICU beds, the equipment, the nursing staff. Medel's company provided the intellectual infrastructure—the physicians, the clinical protocols, the quality oversight. And the patients—premature newborns and their terrified families—got care that was, ideally, more consistent and higher quality than what a hospital cobbling together its own coverage could provide.

What made this model work was a genuine alignment of incentives—at least in its early form. Hospitals wanted reliable, high-quality NICU coverage around the clock. Physicians wanted stable employment with good pay and the ability to focus on medicine rather than business management. And the company could achieve economies of scale in recruitment, credentialing, malpractice insurance purchasing, and billing that no individual practice could match. In a subspecialty where there were fewer than five thousand board-certified neonatologists in the entire country, having a dedicated recruitment network—even a modest one—was a genuine competitive advantage. Every neonatologist Medel recruited was one that a competitor or hospital could not hire.

Growth through the 1980s was deliberate and modest. Outsourcing physician staffing was still an unusual concept in American medicine, and most hospital administrators were skeptical. The idea that a for-profit corporation should stand between a hospital and the physicians practicing within it struck many in the medical establishment as unseemly, even dangerous. Medel had to sell the concept one hospital CEO at a time, proving that quality did not suffer—and might actually improve—when physician management was professionalized. He built the business one hospital relationship at a time, proving the model in Florida before slowly expanding outward. The company secured its first out-of-state contract in Charleston, West Virginia, in 1991—twelve years after founding. That pace tells you something about how cautiously the healthcare industry adopted this model.

By the end of 1994, South Florida Neonatology Associates managed twenty-two NICUs across twelve states and Puerto Rico, generating roughly thirty-three million dollars in net patient service revenue and employing 116 physicians. To put that in context, $33 million in revenue for a fifteen-year-old company was respectable but hardly extraordinary. A single large hospital system generated more revenue in a week. But Medel had proven something more important than scale: the model worked, hospitals were willing to pay for it, physician quality could be maintained within a corporate structure, and the recruitment barrier—the difficulty of finding subspecialty neonatologists—gave his company a moat that, while narrow, was real.

These were not the numbers of a company that would one day be worth seven billion dollars. The question was whether this niche business could scale beyond what one determined founder could build through personal relationships and regional reputation. In 1995, Medel decided to find out.

The company renamed itself Pediatrix Medical Group and prepared for an initial public offering. This was not merely a capital-raising exercise. It was a strategic pivot from organic growth to acquisition-driven consolidation—a bet that the fragmented landscape of small neonatology practices across America could be rolled up into a single, dominant platform. Medel looked at the landscape and saw hundreds of small practices—two neonatologists here, five there—many of them founded by physicians approaching retirement who had no succession plan and no interest in managing a business. He saw an opportunity to be the acquirer of choice, the company that offered these aging physician-entrepreneurs a fair price, continuity for their patients, and employment stability for their younger colleagues. It was a bet that would define the next two decades.

III. Going Public & The Roll-Up Machine (1995–2008)

Pediatrix Medical Group went public on September 20, 1995, raising eighty-eight million dollars on the New York Stock Exchange under the ticker PDX. At the time of the IPO, the company managed thirty-seven NICUs and five pediatric intensive care units with 116 physicians. By the standards of healthcare services companies, it was tiny. But Medel had timed the market brilliantly.

The mid-to-late 1990s saw an extraordinary wave of healthcare services consolidation. Physician practice management companies were Wall Street's flavor of the month, with investors betting that the fragmented world of American medical practices could be consolidated the same way that waste management, funeral services, and auto dealerships had been rolled up in prior decades. The thesis was straightforward: buy small practices at five to seven times earnings, plug them into a corporate platform that provided billing, compliance, and administrative services, and watch the multiple arbitrage work its magic as the combined entity traded at twelve to fifteen times earnings in the public markets.

Medel understood that neonatology was particularly well-suited to this playbook, for reasons that went beyond mere fragmentation. First, hospitals could not easily switch providers. Once a company was managing a hospital's NICU, the switching costs were significant—you would need to find replacement neonatologists, manage the transition without disrupting patient care, and retrain staff on new protocols. Contracts typically ran three to five years. Second, the barriers to entry were extraordinarily high. Neonatology fellowships produced a limited number of new specialists each year, and there was no way to shortcut the training. Third, the market was genuinely fragmented, with hundreds of small practices of two to ten neonatologists scattered across the country, many of whose founding physicians were approaching retirement age and looking for an exit. And fourth, insurance reimbursement structures for NICU care—driven by the complexity and intensity of treating premature and critically ill newborns—supported healthy fee-for-service revenue.

The acquisition machine cranked into motion immediately after the IPO. In 1996 alone, Pediatrix completed ten acquisitions, including Infant Care Specialists Medical Group, the largest neonatology practice in southern California, for six million dollars, and three Colorado practices for a combined twelve million. A secondary stock offering in August 1996 raised another fifty-nine million dollars to feed the pipeline.

In 1997, ten more physician group acquisitions followed, bringing the company into the Dallas and Albuquerque markets. In 1998, eight more acquisitions closed, and Medel launched a new subsidiary called Obstetrix Medical Group to expand into high-risk pregnancy management—maternal-fetal medicine—which was a natural adjacency that shared the same hospital relationships and patient population. The strategic logic was elegant: a hospital that already trusted Pediatrix to manage its NICU would naturally consider Obstetrix to manage its high-risk obstetric patients. Same hallways, same patient families, deeper relationship.

The pace was relentless but disciplined. Each acquisition followed a standard playbook: identify a practice, often through physician networking relationships built over years of conference attendance and professional society involvement. Negotiate a purchase price based on a multiple of the practice's historical earnings—typically five to seven times, affordable enough to generate returns once plugged into the Pediatrix platform. Retain the existing physicians on employment contracts that offered competitive compensation plus the administrative relief and malpractice coverage that made corporate employment attractive. Integrate billing, compliance, and administrative functions onto the Pediatrix platform. And implement standardized clinical protocols and quality metrics that the company had refined across its growing network.

The company's Fort Lauderdale headquarters became a factory for physician practice integration, with processes refined through dozens of transactions. There was an assembly-line quality to the operation: identify target, negotiate, close, integrate, optimize. Rinse and repeat.

The crown jewel acquisition of this era came in February 2001, when Pediatrix merged with Magella Healthcare Corporation—at the time, the only other large-scale neonatology staffing company in the country—for approximately $174 million. The deal was structured as a combination of assumed bank debt, convertible notes, and stock. This was a defining transaction, and it deserves particular attention because of what it reveals about the dynamics of roll-up competition.

Magella was the only company that had achieved anything close to Pediatrix's scale in neonatology staffing. As long as Magella existed, hospitals had an alternative when negotiating with Pediatrix, and physicians had another large-scale employer to consider. By absorbing its only significant competitor, Pediatrix achieved a dominant market position in NICU management that would be nearly impossible to replicate. In the language of competitive strategy, Medel had cornered the resource: the finite supply of neonatologists willing to work in a corporate employment model. It was the kind of industry-defining consolidation that happens once in a sector's lifecycle, and Medel executed it before anyone else could.

It is worth pausing to note what happened to most of Pediatrix's peers during this period. The late 1990s physician practice management boom produced dozens of publicly traded companies attempting similar roll-up strategies in various specialties—ophthalmology, dentistry, primary care, dermatology. The vast majority crashed and burned by 2001. Companies like PhyAmerica Physician Group, MedPartners, and FPA Medical Group imploded under the weight of overpayment for acquisitions, difficulty integrating physician cultures, and the inherent tension between corporate management and clinical autonomy. The dot-com bust and a broader pullback in healthcare services valuations killed most of the survivors. Pediatrix stood out as one of the very few that made it through this carnage intact. The reason was specificity: while its competitors tried to roll up broad swaths of primary care or multi-specialty practices—businesses with low barriers to entry and commodity economics—Medel had chosen a narrow, defensible niche with genuine barriers. Neonatology's specialized physician supply, hospital dependency, and complex reimbursement created a moat that broader physician practice management models simply lacked.

In 2003, Pediatrix added another capability by acquiring Neo Gen Screening, a newborn metabolic screening company, for thirty-four million dollars. This was an early attempt at vertical integration—owning not just the physicians who treated newborns but also the diagnostic services that identified which newborns needed treatment. It signaled Medel's ambition to build a comprehensive platform around the first hours and days of infant life.

Through the early and mid-2000s, Pediatrix continued its steady expansion, albeit at a more moderate pace as the low-hanging fruit of fragmented neonatology practices was gradually picked. The company generated consistently high margins—operating margins in the high teens to low twenties—and delivered predictable earnings growth that made it a favorite among healthcare investors. Revenue grew from roughly thirty-three million dollars at the time of the IPO to approximately four hundred sixty-five million dollars by 2002, and continued climbing through the decade. For shareholders who bought at the 1995 IPO and held through 2007, the returns were extraordinary—the kind of steady, compounding performance that value investors dream about.

But Medel was restless. The neonatology roll-up, while still producing growth, was maturing. The largest practices had been acquired. The Magella merger had eliminated the only major competitor. Organic growth depended on birth rates and NICU admission volumes—factors outside the company's control. For a CEO who had built his career on acquisitive growth, the prospect of managing a stable, slow-growing neonatology business was unsatisfying. He wanted a bigger canvas.

In 2008, Medel made the symbolic move that would redefine—and ultimately undermine—the company he had built. Pediatrix Medical Group changed its corporate name to MEDNAX, Inc., with the stock ticker changing to MD at the start of January 2009. The new name was deliberately generic, stripped of the pediatric specificity that had defined the company for three decades. The message was clear: this was no longer just a neonatology company. Medel envisioned a broader platform for hospital-based physician services—a physician services conglomerate that could replicate the neonatology roll-up playbook across multiple medical specialties. It was an ambitious vision, born of genuine strategic reasoning about growth limitations in the core business. Whether it was a wise one would become the defining question of the next decade.

IV. The Golden Age: Peak Roll-Up & Diversification (2008–2015)

Walk into a Wall Street healthcare conference in 2012 or 2013, and MEDNAX was the stock everyone wanted to talk about. The company had earned a reputation as one of the most reliable compounders in healthcare services—a sector that institutional investors were flooding with capital in the wake of the financial crisis. The pitch wrote itself: defensive revenue streams immune to economic cycles, a proven acquisition machine, and a total addressable market of physician practices that seemed to stretch to the horizon.

The financial crisis of 2008-2009 paradoxically strengthened the investment case. As markets cratered and investors sought shelter, healthcare services stocks attracted capital with a powerful thesis: regardless of what happened to the economy, babies would still be born prematurely, patients would still need anesthesia, and hospitals would still need physicians. MEDNAX's recurring revenue, long-term contracts, and defensive positioning made it a port in the storm. The stock barely dipped during the worst of the crisis and quickly resumed its upward trajectory. While homebuilders and banks were being obliterated, MEDNAX was quietly delivering another year of double-digit earnings growth.

Emboldened by this validation and flush with confidence from two decades of successful acquisitions, Medel pushed the accelerator on diversification. The company had already begun entering anesthesiology services in 2007, founding the American Anesthesiology division. The logic seemed compelling on the surface: anesthesiology shared many of the structural characteristics that made neonatology attractive for roll-up. Anesthesiologists were hospital-based, their services were essential for surgical procedures, the market was fragmented among small group practices, and hospitals had difficulty recruiting and retaining them independently. If you squinted, it looked like the same playbook in a different specialty.

But there was a critical difference that would prove fatal. In neonatology, Medel's company had genuinely deep clinical expertise—protocols developed over decades, quality benchmarks, outcomes data, and a recruiting network built on genuine relationships within the neonatology community. The expansion into anesthesiology was driven primarily by financial logic—the acquisition multiples, the revenue opportunity, the platform story for Wall Street—rather than clinical expertise. MEDNAX was becoming an acquisition machine first and a medical organization second.

By 2012, the company was completing fourteen acquisitions per year, with half flowing into the rapidly growing American Anesthesiology division. By September 2013, the anesthesiology business had swelled to more than seventeen hundred providers—over seven hundred physicians and a thousand certified registered nurse anesthetists. The speed was breathtaking. What had taken Pediatrix fifteen years to build in neonatology, American Anesthesiology was replicating in less than seven years. The question no one was asking loudly enough was whether speed and quality were compatible in a business built on physician relationships and clinical trust.

Then came 2014—the record year. MEDNAX closed thirteen acquisitions totaling over four hundred ninety million dollars in purchase prices, with eight of those in anesthesiology. The company was spending nearly half a billion dollars annually on acquisitions, funded by a combination of operating cash flow and increasing amounts of debt. Revenue was approaching two and a half billion dollars. The physician headcount was soaring past four thousand. Every quarter, the earnings call followed the same reassuring script: strong acquisition pipeline, integration on track, synergies being realized, guidance raised.

The crowning transaction of the diversification era arrived in May 2015, when MEDNAX announced it would acquire Virtual Radiologic Corporation—known as vRad—for five hundred million dollars. This was a leap into an entirely new specialty. vRad was the nation's leading teleradiology company, with more than 350 board-certified radiologists interpreting over five million patient studies annually across twenty-one hundred hospital clients. The premise was forward-looking: as medical imaging volumes grew and radiologist shortages persisted, remote reading would become the dominant model, and vRad had first-mover advantage. But the price tag—approximately ten times EBITDA, against analyst expectations of six to seven times—raised eyebrows across Wall Street. When the deal was announced, several analysts publicly questioned whether MEDNAX was overpaying. The company was betting half a billion dollars on a telehealth thesis in radiology at a moment when its core competency was managing neonatologists in hospital NICUs. The strategic distance between those two businesses was enormous, even if the financial presentation made them look like neat adjacencies on a PowerPoint slide.

By mid-2015, MEDNAX had transformed itself from a neonatology staffing company into a diversified physician services platform spanning neonatology, maternal-fetal medicine, pediatric subspecialties, anesthesiology, and radiology. The stock reached its all-time high of $85.47 on August 17, 2015, giving the company a market capitalization of approximately seven billion dollars. Wall Street research notes glowed with praise for the "platform strategy" and the "long runway" of acquisition targets. MEDNAX was a Wall Street darling, held by virtually every major healthcare fund.

The thesis at its peak went something like this: MEDNAX had built a physician services platform with presence in over forty states and more than forty-five hundred affiliated clinicians. The company had massive contracting leverage with hospitals—if you were a health system that needed neonatologists, anesthesiologists, and radiologists, MEDNAX could be your one-stop shop. Insurers had to contract with MEDNAX because their physicians were embedded in hospitals where patients had no choice about which specialist treated them. The recurring revenue was predictable, the margins were healthy, and the acquisition pipeline was virtually inexhaustible.

The competitive landscape fed the euphoria. Private equity firms were pouring billions into physician staffing, validating the thesis that these businesses were valuable. Blackstone had taken TeamHealth private for $6.1 billion in 2017. KKR had acquired Envision Healthcare for $9.9 billion in 2018. The logic was circular but persuasive: if the smartest money in the world was paying premium prices for physician staffing companies, then MEDNAX's public market valuation was justified—perhaps even cheap by comparison.

But beneath the surface, cracks were forming. Physician satisfaction surveys within MEDNAX practices were deteriorating. The increasingly corporate culture—metrics-driven, efficiency-obsessed, focused on revenue per clinician and patients seen per shift—was alienating the very physicians the model depended upon. Neonatologists who had joined Pediatrix for the clinical collegiality and professional support found themselves in a sprawling corporation where decisions were made by executives in Fort Lauderdale who had never set foot in a NICU. Reimbursement pressure from Medicare and Medicaid was intensifying as government payers pushed back on rising costs. And most critically, the billing practices that underpinned the anesthesiology and radiology divisions' profitability were attracting the kind of scrutiny that makes corporate lawyers lose sleep.

The era of effortless growth was ending. What came next would test every assumption that had built this seven-billion-dollar empire.

V. The Unraveling: Surprise Billing, Reimbursement Cuts & Management Turmoil (2016–2020)

The first public signal that something was wrong at MEDNAX came in the earnings reports of 2016 and 2017. Organic growth—the growth that came from existing operations rather than acquisitions—slowed dramatically and then turned negative. Same-unit patient volumes, the single most important operational metric for a physician staffing company, began declining. For a company whose entire value proposition was growth through consolidation, the stalling of underlying volume growth was like watching the engine warning light flicker on during a cross-country road trip. You could ignore it for a while, but something fundamental was changing.

The stock began a multi-year descent that would eventually destroy roughly ninety percent of shareholder value. From its 2015 peak above eighty-five dollars, shares slid through the sixties, then the fifties, then the forties, as each quarterly report revealed more of the same: acquisition-driven revenue growth masking organic deterioration.

Smart investors started asking uncomfortable questions. Was the core business actually growing, or was MEDNAX just buying revenue? Were the acquisitions creating value, or were they papering over a declining franchise? The distinction matters enormously. A company that grows organically—by winning new contracts, expanding services to existing clients, or improving pricing—is demonstrating genuine competitive strength. A company that grows only through acquisitions is essentially buying revenue at a price, and if the underlying business is shrinking, each acquisition becomes a more expensive band-aid on a larger wound. MEDNAX, increasingly, looked like the latter.

The answer came into sharper focus as the surprise billing crisis erupted into national consciousness. This is perhaps the most important part of the entire MEDNAX story—the moment where a profitable but ethically questionable business practice collided with American democratic politics—so it deserves careful explanation.

To understand what happened, you need to understand how MEDNAX's model—particularly in anesthesiology—actually worked at the billing level. Here is the mechanism that would ultimately bring the company to its knees.

When a patient checked into a hospital for surgery, they typically verified that the hospital was in their insurance network. What they did not know—and often could not know—was whether the anesthesiologist who would put them to sleep was also in-network. MEDNAX's American Anesthesiology division, like competitors TeamHealth and Envision Healthcare, often kept its physicians out of network with major insurers. This was not an accident. It was a deliberate strategy. By remaining out-of-network, the company could bill patients and insurers at rates dramatically higher than in-network negotiated rates—sometimes sixty percent or more above what comparable in-network providers charged. The patient, who had done everything right by choosing an in-network hospital, would receive a "surprise" bill for thousands of dollars from an anesthesiologist they never chose and whose network status they had no practical way to verify.

This practice was legal. And for years, it was enormously profitable. But it was corrosive to public trust in ways that the financial models never captured. Think about it from the patient's perspective. You are about to have surgery. You have done your homework—chosen an in-network hospital, verified your coverage, budgeted for your copay and deductible. You go under anesthesia trusting that the system is working as it should. Weeks later, you receive a bill for five thousand, ten thousand, sometimes twenty thousand dollars from an anesthesiologist you never met, never chose, and whose separate billing status you had no way to discover. The feeling of betrayal is visceral. And when that story gets told on local news, on social media, in congressional testimony—it becomes a political weapon of enormous power.

The media campaign against surprise billing built slowly and then exploded. Local television news segments featured tearful patients holding bills for tens of thousands of dollars. Investigative journalists at the New York Times and other outlets published deep dives into the mechanics of surprise billing, naming MEDNAX, TeamHealth, and Envision as the primary practitioners. The stories resonated because they tapped into a deep well of American anxiety about healthcare costs and the feeling that the system was rigged against ordinary patients. One of the most devastating aspects for the physician staffing companies was that the stories were true—there was no effective rebuttal. The billing practices were exactly as described, and the patient harm was real and quantifiable.

Congressional and state-level backlash built rapidly through 2017, 2018, and 2019. A bipartisan Senate HELP Committee investigation was launched, with letters sent directly to major physician staffing companies demanding information about their billing practices and out-of-network rates. State legislatures began passing their own surprise billing protections—New York had been a pioneer, and others followed. And in Washington, the issue achieved that rarest of political phenomena: genuine bipartisan consensus. Republicans and Democrats agreed that surprise billing was indefensible, even as they disagreed on the precise mechanism for stopping it. Some favored benchmarking payments to median in-network rates; others preferred an arbitration model. But the outcome—ending the practice—was never in serious doubt once the political winds aligned.

Meanwhile, the industry mounted a lobbying counteroffensive that backfired spectacularly. Envision Healthcare and TeamHealth—both owned by private equity firms—bankrolled a dark-money lobbying group called Doctor Patient Unity, which spent fifty-four million dollars on advertising in 2019 alone, attacking proposed legislation under the guise of patient advocacy. When journalists exposed the group's private equity backers, the revelation generated a fresh wave of outrage and further poisoned the political environment for the entire physician staffing industry. MEDNAX's own lobbying spend was comparatively modest at about $180,000, but the company was painted with the same brush.

On the operational front, MEDNAX's hospital and payer relationships were fraying in ways that went beyond politics and legislation.

In February 2020, UnitedHealthcare—the nation's largest commercial insurer, covering tens of millions of Americans—publicly announced it was terminating contracts with MEDNAX practices in Arkansas, Georgia, North Carolina, and South Carolina. The terminations would be effective between March and September 2020, meaning patients in those states who relied on MEDNAX-affiliated physicians could face disrupted care.

United's stated reason was devastating in its simplicity: MEDNAX's charges were "more than sixty percent higher than the average cost" of comparable providers. That single statistic, published in press releases and repeated across healthcare media, became the data point that defined MEDNAX's pricing problem. The terminations affected approximately two percent of MEDNAX's annual revenue in direct financial terms, but the signal effect was far greater. MEDNAX shares fell sixteen percent in a single trading session—one of the worst single-day drops in the company's history.

The message from UnitedHealthcare was aimed not just at MEDNAX but at the entire physician staffing industry: the era of above-market pricing for hospital-based physicians was ending. If the nation's largest insurer was willing to publicly terminate contracts and expose patients to disruption rather than pay premium rates, every other payer in America was watching—and many were already preparing similar moves.

Inside the company, the management situation had become chaotic. Roger Medel, the founder who had run MEDNAX for four decades—from the first NICU contract in Fort Lauderdale to a national empire spanning three medical specialties—was facing the kind of mounting pressure that founders rarely survive. His identity was inseparable from the company he had built. He had served as CEO, president, or both for virtually the entire forty-one-year history of the enterprise. The idea that someone else should lead MEDNAX was, for Medel, tantamount to being told his life's work had failed.

But the numbers were undeniable. The stock had declined roughly seventy percent from its peak. Revenue growth had stalled. Physician turnover was rising. Hospital relationships were fraying. And in December 2019, activist hedge fund Starboard Value—one of Wall Street's most aggressive and effective activist investors, with a track record of forcing change at companies like Darden Restaurants and Yahoo—disclosed a sizable stake in MEDNAX that would eventually reach 9.9 percent of outstanding shares.

Starboard privately nominated a majority slate of directors, demanding that MEDNAX consider selling all or part of itself. Starboard's analysis was damning and detailed: the company had taken a $1.4 billion goodwill impairment charge in 2019, acknowledging on paper what the stock market had been screaming for years—that the acquisitions made at the peak had been vastly overpaid for. Goodwill impairment, for non-financial readers, occurs when a company admits that assets it acquired are worth significantly less than what it paid for them. A $1.4 billion write-down was essentially management confessing that it had destroyed over a billion dollars of shareholder value through overpayment for acquisitions. Starboard argued that the shares had lost roughly a quarter of their value in 2019 alone, on top of years of prior decline.

The endgame for Medel's four-decade tenure came in July 2020, when MEDNAX reached a settlement with Starboard. Medel retired as CEO. The board was reconstituted under Starboard's influence, with Guy Sansone installed as chairman and Mark Ordan—an outsider whose background was in real estate—appointed as the new CEO. Medel remained on the board briefly and received a consulting arrangement at $177,000 per month for up to a year—roughly two million dollars in annual consulting fees, a golden parachute for the end of an era. For a man who had built the company from nothing over four decades, it was a poignant exit, though many shareholders felt it was overdue.

That same December, Congress finally passed the No Surprises Act as part of an omnibus spending bill, set to take effect on January 1, 2022.

For readers unfamiliar with the mechanics, the No Surprises Act works like this: if you go to an in-network hospital and receive care from an out-of-network physician you did not choose—an anesthesiologist, a radiologist, a neonatologist, an emergency physician—you cannot be billed more than your in-network cost-sharing amount. The physician and the insurer must work out the payment between themselves, either through negotiation or through an independent dispute resolution process. The patient is held harmless.

The law fundamentally shifted the balance of power from providers to insurers and patients. Before the Act, an out-of-network physician could bill whatever they wanted and send the patient a balance bill for the difference. The threat of patient bills gave providers enormous leverage in negotiations with insurers. After the Act, that leverage disappeared. The independent dispute resolution process, while imperfect, generally favored insurer-proposed payment rates. Studies would later show that the Act reduced yield per case by approximately twenty percent for affected providers.

The irony was that by the time the No Surprises Act became law, MEDNAX had already begun dismantling the very divisions most dependent on the practices it outlawed. The anesthesiology division was gone. The radiology division was being sold. What remained—neonatology, maternal-fetal medicine, pediatric subspecialties—was less directly exposed to the Act's impact because these physicians were more commonly in-network. But the legislative blow, combined with everything else that had gone wrong, ensured that the old MEDNAX was dead. The entire industry structure that had supported the company's most profitable years had been dismantled by act of Congress. What would replace it was far from clear.

VI. COVID-19 & The Perfect Storm (2020–2021)

The pandemic arrived at MEDNAX like a hurricane hitting a house already ravaged by termites. The structural damage—organic volume declines, surprise billing backlash, activist investor pressure, management upheaval—had been accumulating for years. COVID-19 simply accelerated the collapse.

Consider the timing. In January 2020, MEDNAX was simultaneously dealing with Starboard's activist campaign, the UnitedHealthcare contract terminations, a founder-CEO under siege, an ongoing strategic review, surprise billing legislation moving through Congress, and declining same-unit volumes. Then a once-in-a-century pandemic shut down the American healthcare system. If a screenwriter had proposed this confluence of crises, it would have been rejected as too implausible.

The immediate impact was devastating. Hospitals across the country postponed elective surgeries, and maternity wards saw reduced traffic as expectant mothers avoided clinical settings for fear of infection. NICU admissions dropped as overall birth volumes declined. Emergency department visits plummeted, reducing the flow of high-risk obstetric cases that fed MEDNAX's maternal-fetal medicine practices. For a company whose revenue was driven by the number of patients its physicians treated, the volume collapse was catastrophic. Second quarter 2020 net revenue fell to $509 million from $561 million the prior year, with same-unit patient volume plunging 11.9 percent—the worst quarterly decline in company history. The fourth quarter brought another wave of volume declines as the winter COVID surge kept patients away from hospitals, with revenue dropping to $417 million from $459 million the prior year.

The financial distress extended beyond revenue. MEDNAX's cost structure was built for a much larger business. Employed physicians represented a massive fixed cost that could not be easily adjusted when volumes dropped—you cannot furlough the neonatologist covering a hospital's NICU without endangering patients. The debt accumulated through years of acquisition-fueled growth hung over the balance sheet like a sword. Covenant concerns and liquidity issues became real. The company's stock, already beaten down to the low twenties, sank further as investors calculated the probability of a covenant breach or worse.

MEDNAX withdrew all 2020 financial guidance in March, a clear sign that management could not see the path forward. Emergency cost-cutting measures were implemented, including furloughs, salary reductions for non-clinical staff, and hiring freezes. The company received $14.2 million from the CARES Act provider relief fund—helpful, but a rounding error against the scale of the crisis. For the American Anesthesiology division specifically, MEDNAX projected COVID-related cash losses of $150 to $250 million—a hemorrhage that made divestiture not just strategically desirable but financially necessary for survival.

The crisis forced MEDNAX to make decisions it had been delaying—decisions that would have been unthinkable even a year earlier.

In May 2020, just months before Medel's formal departure, the company sold the entire American Anesthesiology division to North American Partners in Anesthesia for a staggering fire-sale price: fifty million dollars in cash, while MEDNAX retained $110 million in accounts receivable.

Let that number sink in. Fifty million dollars. MEDNAX had spent hundreds of millions of dollars—the 2014 acquisition year alone saw nearly half a billion in total deal value, heavily weighted toward anesthesiology—building this division over a decade. At its peak, American Anesthesiology had more than four thousand providers generating hundreds of millions in annual revenue. The company sold the whole thing for fifty million during a pandemic, because the projected COVID-related cash losses of $150 to $250 million made keeping it financially untenable. Holding the division would have burned through cash faster than the company could sustain.

The acquirer, NAPA, backed by private equity firm American Securities, got more than six thousand clinicians at a price that barely covered a few months of the division's operating losses. It was one of the most lopsided transactions in healthcare M&A history—a monument to the destruction of value that occurs when a roll-up strategy built on leverage meets an adverse environment.

Six months later, in December 2020, MEDNAX completed its second major divestiture, selling MEDNAX Radiology Solutions—including vRad—to Radiology Partners for an enterprise value of $885 million. The transaction included more than 300 onsite radiologists in five states plus the 500-plus teleradiologists of the vRad platform, which served all fifty states.

The net proceeds of approximately $865 million were used primarily to redeem $750 million in senior notes, repairing the balance sheet at the cost of reversing the entire diversification strategy. The arithmetic tells a more encouraging story than the anesthesiology fire sale—the radiology division fetched a reasonable price relative to what was invested. But the strategic calculation was still deeply negative. The vRad business alone had been acquired for $500 million just five years earlier, and the subsequent radiology build-out investments pushed total capital deployed well over $600 million. After factoring in the opportunity cost of that capital—the debt service, the management attention, the strategic distraction—MEDNAX would have been far better off never entering radiology at all.

MEDNAX was not alone in its suffering. The broader physician staffing sector was in a state of collapse that deserves its own accounting.

Envision Healthcare, the largest player in the space with approximately 25,000 clinicians in forty-four states, would eventually file for Chapter 11 bankruptcy in May 2023, citing the No Surprises Act's impact on revenues as a key factor. KKR's $9.9 billion acquisition—one of the largest healthcare leveraged buyouts in history—was effectively wiped out. TeamHealth, owned by Blackstone since 2017, struggled with its own debt burden and contract losses, though it avoided formal bankruptcy. Smaller physician staffing companies and regional groups faced similar pressures, with many being absorbed into hospital systems or simply dissolving as their physician-owners retired.

The entire thesis of private equity and publicly traded roll-ups in physician staffing—that consolidation created durable value—was being exposed as dependent on favorable regulatory conditions that no longer existed. It was, in hindsight, one of the most destructive investment themes of the 2010s, rivaling the dot-com era in the gap between thesis and reality.

The fundamental problem was structural, and it is worth stating clearly because the lessons apply far beyond physician staffing. The roll-up model worked beautifully when three conditions were simultaneously favorable: a fragmented market to buy into, pricing power derived from out-of-network leverage, and a fee-for-service reimbursement system that rewarded volume. When all three pillars crumbled simultaneously—market consolidation reached its limits, the No Surprises Act destroyed pricing leverage, and the shift toward value-based care undermined fee-for-service—there was nothing left to support the economics. The leverage that had amplified returns on the way up amplified losses on the way down. The fixed costs that had generated operating leverage in a growing business generated operating de-leverage in a shrinking one.

By the end of 2021, MEDNAX was a dramatically smaller company. The diversification strategy had been fully unwound. Revenue from continuing operations was roughly $1.9 billion, down from a peak of $3.5 billion. The physician headcount had shrunk from over ten thousand across all divisions to approximately four thousand four hundred in the core specialties. The national footprint, once spanning every medical specialty that touched a hospital operating room, was now focused exclusively on NICUs, labor and delivery suites, and pediatric subspecialty clinics.

What remained was essentially the original Pediatrix Medical Group—neonatology, maternal-fetal medicine, and pediatric subspecialties—plus the scars of a decade-long detour that destroyed billions in shareholder value, cost the founder his position, and nearly bankrupted the enterprise. It was as if the company had taken a ten-year journey only to return to its starting point, poorer and wiser. The question now was whether even this core business could survive in the fundamentally changed environment that the journey had left behind.

VII. Transformation & The Turnaround Attempt (2021–Present)

Mark Ordan inherited a company in crisis—and he was an unlikely choice to lead it out. His resume read like a real estate portfolio, not a healthcare executive's CV. Most recently CEO of Quality Care Properties, a healthcare REIT, Ordan had spent his career in real estate investment, hospitality, and asset management. He had never run a physician services company. He had never managed clinical operations. He had never navigated the byzantine complexity of healthcare reimbursement. To many industry observers, his appointment looked like a Starboard Value special: bring in an outsider who would view the company as a collection of assets to be optimized, sold, or restructured—not as a medical organization with a clinical mission.

But Ordan brought exactly the skills the moment demanded. He was unsentimental about sacred cows. He was experienced in distressed situations and asset dispositions. And he was willing to make the hard calls that a founder-CEO—particularly one who had spent four decades building the divisions now being sold for pennies on the dollar—could never bring himself to make. His compensation structure told the story: a one-million-dollar annual salary plus a $250,000 one-time payment specifically for developing a strategic transformation plan. He was being paid to dismantle, not to build.

The strategic reset was built on a clear thesis: MEDNAX had failed because it tried to be everything to every hospital. The new Pediatrix would succeed by being the best at what it originally did—caring for the most vulnerable patients: premature newborns, high-risk pregnancies, and critically ill children. Everything else would go.

The divestitures described in the previous section were completed under Ordan's leadership, and the balance sheet repair that followed was critical to survival. The roughly $865 million in net proceeds from the radiology sale went primarily to retiring the $750 million in 5.25 percent senior notes due 2023—debt that had been issued to fund the very acquisitions now being unwound. The redemption, completed in January 2021, dramatically reduced the company's interest burden and removed the covenant pressure that had threatened its existence during the worst of the pandemic.

With the debt retired and the non-core divisions sold, the company had breathing room for the first time in years. By mid-2022, it completed its symbolic return to roots by changing its name back to Pediatrix Medical Group, effective July 1. CEO Ordan said at the time: "We are excited to complete this full return to Pediatrix, a nationally well-known and highly respected name." It was the corporate equivalent of a prodigal son returning home—chastened, diminished, but alive.

Ordan's operational strategy focused on several key shifts. First, Pediatrix began transitioning from a primarily employed physician model to a more flexible affiliated physician model. The distinction matters enormously. Under the old model, MEDNAX bore the full cost of physician compensation regardless of patient volume—a fixed cost structure that amplified losses when volumes dropped. Under the affiliated model, physicians maintain greater independence while Pediatrix provides administrative, billing, and clinical support services. The risk profile shifts: lower margins in good times, but significantly less downside exposure when conditions deteriorate.

Second, the company invested in technology and clinical quality as differentiation tools. This represented a fundamental shift in strategy—from competing on scale and pricing leverage to competing on outcomes and clinical excellence.

Telehealth capabilities were expanded, particularly for neonatology consults in rural and underserved areas where a neonatologist might not be physically available around the clock. The potential here is significant: there are roughly thirty-five hundred hospitals in the United States that provide obstetric services, but many of them—particularly in rural areas—lack full-time neonatology coverage. A telehealth-enabled model where a remote neonatologist can assess a newborn via high-definition video, guide local nursing staff through initial stabilization, and arrange transport to a higher-level NICU if needed could extend Pediatrix's reach far beyond hospitals where it maintains on-site physicians.

Clinical decision support tools were developed to standardize care protocols and improve outcomes. Quality metrics and patient outcome tracking were elevated from back-office functions to core strategic priorities. The pitch to hospitals evolved from "we'll staff your NICU" to "we'll improve your NICU outcomes, reduce your readmission rates, and provide twenty-four-seven subspecialty coverage through a blend of on-site and telehealth physicians." It remains to be seen whether hospitals will pay a premium for demonstrably better outcomes, but the strategic logic is sound.

Third, Pediatrix began exploring value-based care partnerships—and this pivot deserves explanation because it represents the most significant strategic departure from the company's historical model.

The traditional fee-for-service model works like this: every time a physician sees a patient, performs a procedure, or provides a consultation, the physician (or their employer) bills the insurer for that specific service. More services equals more revenue. The incentive is volume—see as many patients, order as many tests, perform as many procedures as possible.

Value-based care flips this equation. Instead of paying for each individual service, payers and providers agree on payment structures tied to outcomes and total cost of care. A value-based arrangement for neonatal care might pay Pediatrix a fixed amount per NICU patient, regardless of how many individual services are provided, with bonuses for achieving quality targets like low infection rates, short lengths of stay, and low readmission rates. The incentive shifts from volume to efficiency and quality.

For a company that had built its entire business on fee-for-service billing, this was a profound strategic pivot. But it also represented an opportunity: if Pediatrix could demonstrate that its clinical protocols and quality systems produced better outcomes at lower total cost, it could potentially command premium positioning in value-based arrangements—a new form of competitive advantage rooted in clinical excellence rather than billing leverage.

The CEO situation, however, remained unsettled—and this instability tells its own story about the difficulty of the transformation.

Ordan served as CEO until December 2022, when he was succeeded by James D. Swift, MD, a veteran Pediatrix executive who brought deep clinical knowledge and an insider's understanding of the company's culture and hospital relationships. The choice of Swift seemed to signal a shift from restructuring mode to operational execution—a physician-leader to rebuild the clinical culture that had eroded during the diversification years. But Swift's tenure lasted less than two years.

In October 2024, Ordan returned as Executive Chairman, and by January 13, 2025, he had formally reclaimed the CEO title. Three CEOs in five years is never a good sign. It suggests either that the board cannot find the right leader, that the job is harder than anyone anticipated, or that the strategic direction keeps shifting. Perhaps all three. For a company attempting to rebuild trust with hospitals and physicians—relationships that thrive on consistency and stability—the executive revolving door is counterproductive at best.

In January 2025, coinciding with Ordan's formal return as CEO, Pediatrix announced a suite of strategic initiatives aimed at "enhanced shareholder value creation." The centerpiece was a $250 million share repurchase program—a signal to investors that management believed the stock was undervalued and that the company could generate sufficient free cash flow to return capital while investing in the business.

The recent financial results provide a mixed picture. The company reported full-year 2025 revenue of $1.91 billion and net income of $165.4 million, translating to $1.94 per share. For 2026, management guided to adjusted EBITDA of $280 to $300 million—roughly five percent above the 2025 level. The fourth quarter of 2025 saw revenue of $493.8 million, slightly beating consensus estimates, though adjusted earnings per share of $0.50 fell just short of the $0.53 Wall Street expectation. The slight miss was a reminder that the turnaround, while real, is fragile.

As of early 2026, Pediatrix Medical Group is a focused women's and children's healthcare company with approximately 4,400 affiliated physicians and clinicians, including 1,335 neonatal physician specialists providing care primarily in NICUs. The company's clinical footprint, while smaller than the MEDNAX empire at its peak, remains substantial—these are the physicians who care for some of America's most vulnerable patients in the critical first hours and days of life.

The stock trades around twenty dollars—a significant recovery from its pandemic-era lows but still less than a quarter of its 2015 peak. The market capitalization stands at approximately $1.66 billion, with shares trading at roughly ten times earnings. The fifty-two-week range of $11.84 to $24.99 tells its own story of continued volatility and investor uncertainty about whether the stabilization is durable or merely a pause before further decline.

The company that Roger Medel built over four decades is unrecognizable from its peak. It is smaller, more focused, less leveraged, and more humble. The sprawling physician services conglomerate that once spanned neonatology, anesthesiology, and radiology across fifty states has been replaced by a focused women's and children's healthcare company that knows exactly what it does and is trying to figure out how to do it profitably in a world that has changed around it.

Whether those qualities—focus, humility, clinical expertise—are sufficient to build a durable business in a fundamentally changed healthcare landscape is the question that will define the next chapter.

VIII. The Competitive Landscape & Industry Evolution

The physician staffing industry that MEDNAX once dominated looks radically different in 2026 than it did a decade ago. To appreciate the scale of destruction, consider what happened to the three companies that collectively defined the sector. Envision Healthcare, which KKR acquired for $9.9 billion in 2018 in one of the largest healthcare leveraged buyouts in history, filed for Chapter 11 bankruptcy in May 2023. The company cited the No Surprises Act's impact on revenues as a primary factor—the legislation had effectively eliminated the pricing model that justified the acquisition price. KKR's equity was wiped out, and Envision emerged as a smaller, restructured entity. TeamHealth, taken private by Blackstone for $6.1 billion in 2017, has struggled with its own debt burden, contract losses, and the same reimbursement headwinds. Together, the private equity firms that placed massive bets on physician staffing in the mid-2010s destroyed tens of billions of dollars in value. MEDNAX shareholders suffered alongside them, though at least the company avoided bankruptcy by divesting before debt covenants were breached.

The vacuum left by the weakening of these large staffing companies has been filled by multiple alternative models, each of which represents a competitive threat to Pediatrix's positioning. The most significant is direct hospital employment. Health systems across the country have concluded that if they are going to pay premium rates for subspecialty physicians, they might as well employ those physicians directly—capturing the professional fee revenue, maintaining tighter quality control, and avoiding the management fees and margin extraction that companies like Pediatrix charge. According to American Medical Association data, the share of physicians employed directly by hospitals or health systems has climbed steadily over the past decade, surpassing the share in independent practice. This trend has been accelerating, and it represents an existential challenge to the entire physician staffing model. Every hospital that decides to hire its own neonatologists is one fewer potential Pediatrix client.

Academic medical centers have also expanded their reach, leveraging their brand prestige and teaching missions to attract subspecialty physicians who might have once joined corporate staffing groups. For a neonatologist choosing between employment at a Pediatrix-managed NICU and a position at a university-affiliated children's hospital, the academic institution often offers more compelling career development, research opportunities, and professional prestige.

Telehealth has introduced yet another competitive vector, one that deserves particular attention because it strikes at the heart of Pediatrix's value proposition. The technology that Pediatrix itself is investing in—remote neonatology consultations, tele-ICU monitoring, virtual specialist coverage—also enables new entrants who can provide subspecialty expertise without the overhead of a national physician employment platform. A telehealth-native neonatology company can offer around-the-clock coverage to rural hospitals without employing thousands of physicians across physical locations.

To understand the telehealth threat, consider a typical Pediatrix hospital contract. The hospital pays Pediatrix to provide round-the-clock neonatology coverage, which means employing or affiliating enough neonatologists to cover three shifts per day, seven days per week, fifty-two weeks per year—plus vacation coverage, sick leave, and conference attendance. That is an enormous amount of physician time, much of which is spent on call rather than actively treating patients. Telehealth allows a more efficient model: a smaller number of on-site physicians supplemented by remote neonatologists who can be consulted via video link when needed. The economics are compelling for hospitals, which get comparable coverage at lower cost. For Pediatrix, the threat is that its hospitals decide they need fewer on-site neonatologists—and therefore need less from Pediatrix.

The broader lesson from the physician practice management industry's struggles deserves examination. The fundamental tension at the heart of these businesses—corporate ownership versus physician autonomy—was never fully resolved. Physicians are not interchangeable widgets. They are highly educated professionals with strong preferences about how they practice medicine, where they work, and how they are compensated. When the corporate model worked well, it freed physicians from administrative burden and provided stable employment. When it worked poorly—when metrics pressures intensified, when compensation structures shifted, when corporate decisions overrode clinical judgment—physicians left for alternatives. And in a market with chronic subspecialist shortages, the physicians always had alternatives.

The reimbursement model dependency proved equally problematic. Companies like MEDNAX built their financial models on the assumption that fee-for-service reimbursement would continue indefinitely and that out-of-network billing leverage would remain available. When both assumptions proved wrong—when value-based care gained momentum and the No Surprises Act eliminated out-of-network leverage—the economics crumbled. There was no Plan B because the entire strategy had been predicated on the permanence of Plan A.

For Pediatrix specifically, the competitive positioning in 2026 rests on a narrower but potentially more defensible foundation. Neonatology remains a subspecialty with chronic physician shortages and genuine clinical complexity. Hospitals that need NICU coverage cannot easily replicate it in-house if they lack existing relationships with neonatologists. The clinical protocols and quality systems that Pediatrix has developed over four decades represent real institutional knowledge. And the company's focus on women's and children's care—as opposed to the broad, commodity physician staffing that characterized its diversified incarnation—allows for a more differentiated value proposition.

There is a myth worth debunking here. The conventional narrative is that MEDNAX's problems were primarily caused by the No Surprises Act. Reality is more nuanced. The No Surprises Act was devastating to the anesthesiology and radiology divisions, which MEDNAX had already shed before the law took effect. The core neonatology business was less directly affected because neonatologists were more commonly in-network with major payers—the surprise billing dynamic was less central to their economics. What truly damaged the core business was a combination of declining birth rates, hospital systems gaining bargaining leverage through consolidation, physician retention challenges, and the broader shift in how hospitals think about subspecialty staffing. The No Surprises Act was the most visible blow, but it was more of a coup de grâce to an already weakened model than the sole cause of decline.

But differentiation is an aspiration, not an achievement. Whether Pediatrix can translate its clinical expertise and neonatology heritage into sustainable competitive advantage—rather than merely participating as one of several adequate options in a commoditized market—will determine whether this is a turnaround story or a slow decline.

IX. Playbook: Business & Investing Lessons

The MEDNAX saga offers a masterclass in the dynamics of roll-up strategies, and the lessons extend far beyond healthcare. The first and most fundamental: successful roll-ups require not just fragmentation in the target market, but durable pricing power in the consolidated entity. MEDNAX had the fragmentation—hundreds of small physician practices ripe for acquisition. But the pricing power that appeared to exist—derived from out-of-network billing leverage and hospital dependency—was built on regulatory sand. When the political winds shifted, the pricing power vanished overnight. Compare this to a roll-up like Constellation Software, which acquires mission-critical vertical market software companies with genuine switching costs and recurring subscription revenue. The pricing power in software roll-ups comes from product stickiness, not regulatory arbitrage. MEDNAX's pricing power came from a billing practice that society eventually decided was unconscionable.

The second lesson concerns the limits of scale in people-dependent businesses. MEDNAX achieved enormous national scale—forty-five hundred physicians across fifty states—but that scale never translated into the kind of cost advantages that justify premium valuations. A neonatologist in Miami does not become more productive because the company also employs neonatologists in Seattle. Recruitment is still local. Clinical care is still local. Hospital relationships are still local. The national overhead—the C-suite, the corporate headquarters, the M&A team, the compliance infrastructure—was a cost, not a savings, imposed on top of inherently local operations. Scale economies in physician staffing turned out to be a mirage.

The third lesson is about regulatory risk as an existential business threat, particularly in healthcare. MEDNAX's management team appears to have dramatically underestimated the political vulnerability of surprise billing. The practice was legal, profitable, and standard across the industry. But it violated a basic principle of consumer fairness—patients were being charged huge sums by providers they never chose and whose involvement they could not have anticipated. In a democracy, business models that generate widespread, visible consumer harm tend to get regulated out of existence. The only question is timing. MEDNAX bet that the timing would be longer than it was.

The fourth lesson involves capital allocation discipline. At the peak of the diversification era in 2014-2015, MEDNAX was spending nearly half a billion dollars annually on acquisitions, often at premium multiples. The vRad acquisition at ten times EBITDA—well above analyst expectations—represented the kind of deal that happens when a management team falls in love with a strategic narrative and loses discipline on price. Five years later, the entire radiology division was sold at a price that, while nominally profitable on paper, represented a massive opportunity cost when adjusted for the debt burden the acquisitions had created. The anesthesiology division was sold for effectively nothing. The billions deployed in diversification would have been better returned to shareholders.

The fifth lesson concerns the danger of diversification without strategic logic. MEDNAX's expansion from neonatology into anesthesiology and radiology was driven by a superficial structural similarity—all three were hospital-based physician specialties with fragmented provider markets. But the competitive dynamics, reimbursement environments, and regulatory exposures were quite different. Neonatology had genuine clinical specialization barriers. Anesthesiology was more commoditized and more dependent on out-of-network billing leverage. Radiology was being disrupted by telehealth and artificial intelligence. The "physician services platform" thesis papered over these differences with a corporate narrative that sounded compelling in investor presentations but collapsed under real-world pressure.

There is an important parallel worth drawing to the private equity experience. Blackstone and KKR, arguably the two most sophisticated private equity firms on the planet, both made enormous bets on physician staffing in the same period that MEDNAX was at its peak. Blackstone paid $6.1 billion for TeamHealth. KKR paid $9.9 billion for Envision. Combined, the two firms committed roughly sixteen billion dollars to the thesis that physician services roll-ups were durable, valuable businesses with strong competitive moats. Both investments have been catastrophic. The lesson is not that these were stupid investors—they are manifestly not. The lesson is that the competitive dynamics they were underwriting—out-of-network billing leverage, hospital dependency, fragmented markets—were less durable than they appeared. When the regulatory environment changed and hospitals gained alternatives, the moats evaporated. If Blackstone and KKR could not make the physician staffing thesis work with unlimited capital, world-class management teams, and full operational control, the model itself was likely flawed.

The turnaround lessons are equally instructive. Ordan's strategy of radical simplification—shedding non-core assets, reducing debt, returning to the founding specialty—is the textbook playbook for distressed companies. Focus beats diversification when survival is at stake. But simplification alone is not a strategy; it is a necessary precondition for developing one. The harder question—what is Pediatrix's durable competitive advantage as a focused neonatology and women's health company?—remains unanswered. Balance sheet repair buys time, but time is not victory.

One more lesson deserves emphasis: the importance of stakeholder alignment in healthcare businesses. MEDNAX's decline was not caused by a single factor but by the gradual erosion of trust across every stakeholder group simultaneously. Physicians grew dissatisfied with corporate culture and left. Hospitals grew resentful of above-market pricing and explored alternatives. Insurers grew hostile to out-of-network billing and terminated contracts. Patients—the ultimate stakeholders—suffered from surprise bills and demanded political intervention. And politicians, sensing a rare bipartisan opportunity, obliged. When a business model alienates every stakeholder group at once, the outcome is predictable. The lesson for any healthcare business is that long-term value creation requires alignment with, not extraction from, the interests of physicians, hospitals, patients, and payers. MEDNAX's tragedy is that it started with genuine alignment under Medel's original model and gradually lost it as financial engineering took precedence over clinical partnership.

For investors evaluating turnaround stories, MEDNAX teaches that the distinction between "cheap because the market is wrong" and "cheap because the business is impaired" is the most important analytical judgment in value investing. At ten times earnings with improving operational metrics, Pediatrix looks statistically cheap. But the structural challenges—hospital direct employment trends, physician shortage dynamics, reimbursement pressure, telehealth disruption—suggest that the cheapness may be warranted. The stock market is not always efficient, but when a stock has declined ninety percent over a decade, the burden of proof falls heavily on the bull case.

X. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Understanding Pediatrix's competitive position requires looking beyond the company's financial statements to the structural forces shaping its industry. Two frameworks illuminate why the business environment has become so challenging—and what would need to change for the company to rebuild durable value.

Starting with Porter's framework, the picture is unfavorable on nearly every dimension.

Competitive rivalry in hospital-based physician services is intense and increasing. Pediatrix competes not just with other staffing companies but with hospitals' own employment models, academic medical centers, and telehealth startups. After the No Surprises Act eliminated pricing leverage, competition has shifted to price, quality, and service—dimensions where differentiation is difficult to demonstrate and even harder to sustain. The commoditization of physician staffing services means that Pediatrix's competitors can offer broadly similar capabilities, and hospitals increasingly treat physician staffing contracts as procurement decisions rather than strategic partnerships. When your buyer views your service as interchangeable with alternatives, pricing power evaporates.

The threat of new entrants is moderate but meaningful. While neonatology's subspecialty training requirements create genuine barriers, the most important "new entrant" is not a startup—it is the hospital itself. Any hospital system can decide to recruit and employ its own neonatologists, and many have done exactly that. The barriers to this form of entry are manageable: hospitals already have the facilities, the patient relationships, and the credentialing infrastructure. What they lacked historically was the recruitment expertise and willingness to manage physician employment directly. As the staffing company model has lost its luster, hospitals have increasingly accepted those burdens.

The bargaining power of suppliers—meaning physicians—is high and growing. There are chronic shortages in neonatology and most pediatric subspecialties. Physicians can choose between employment with Pediatrix, employment directly with a hospital, private practice, academic positions, or positions with competitors. In a labor market where demand exceeds supply, the suppliers have leverage. Pediatrix must offer competitive compensation, reasonable working conditions, and professional autonomy—or watch its physicians walk. The retention challenge is real and expensive.

The bargaining power of buyers—hospitals and insurance companies—has shifted dramatically over the past decade. Hospitals have gained leverage through consolidation into large health systems with significant purchasing power and the credible alternative of direct employment. Insurers gained enormous leverage through the No Surprises Act, which effectively shifted the baseline for out-of-network dispute resolution in their favor. The combination means that Pediatrix faces powerful counterparties on both sides of its business model.

The threat of substitutes is high and increasing. Direct hospital employment, telehealth-enabled specialist coverage, academic medical center partnerships, and value-based care arrangements that bypass traditional staffing models all represent substitutes for Pediatrix's core service. The telehealth vector is particularly concerning for a company that charges premium rates for on-site physician presence—if a hospital can get a neonatology consultation via video link from a physician in another state, the economics of maintaining full-time on-site coverage become harder to justify.

The conclusion from Porter's analysis is sobering: industry structure has deteriorated significantly across all five forces, moving from moderately favorable in the early 2010s to unfavorable on virtually every dimension by the mid-2020s. This is not a temporary cyclical downturn—it is a structural shift in industry economics that is unlikely to reverse. The golden age of physician staffing profitability is over, and any investment thesis for Pediatrix must reckon with this reality rather than hoping for a return to prior conditions.

Hamilton Helmer's 7 Powers framework tells a complementary and equally sobering story. For readers unfamiliar with Helmer's framework, it identifies seven specific types of competitive advantage—what he calls "powers"—that enable businesses to sustain superior returns over time. A company with strong powers can resist competitive pressure and maintain pricing. A company without them is eventually competed down to commodity returns. The question for Pediatrix is whether it possesses any of these powers.