McKesson Corporation: The Quiet Giant of American Healthcare

I. Introduction & Episode Setup

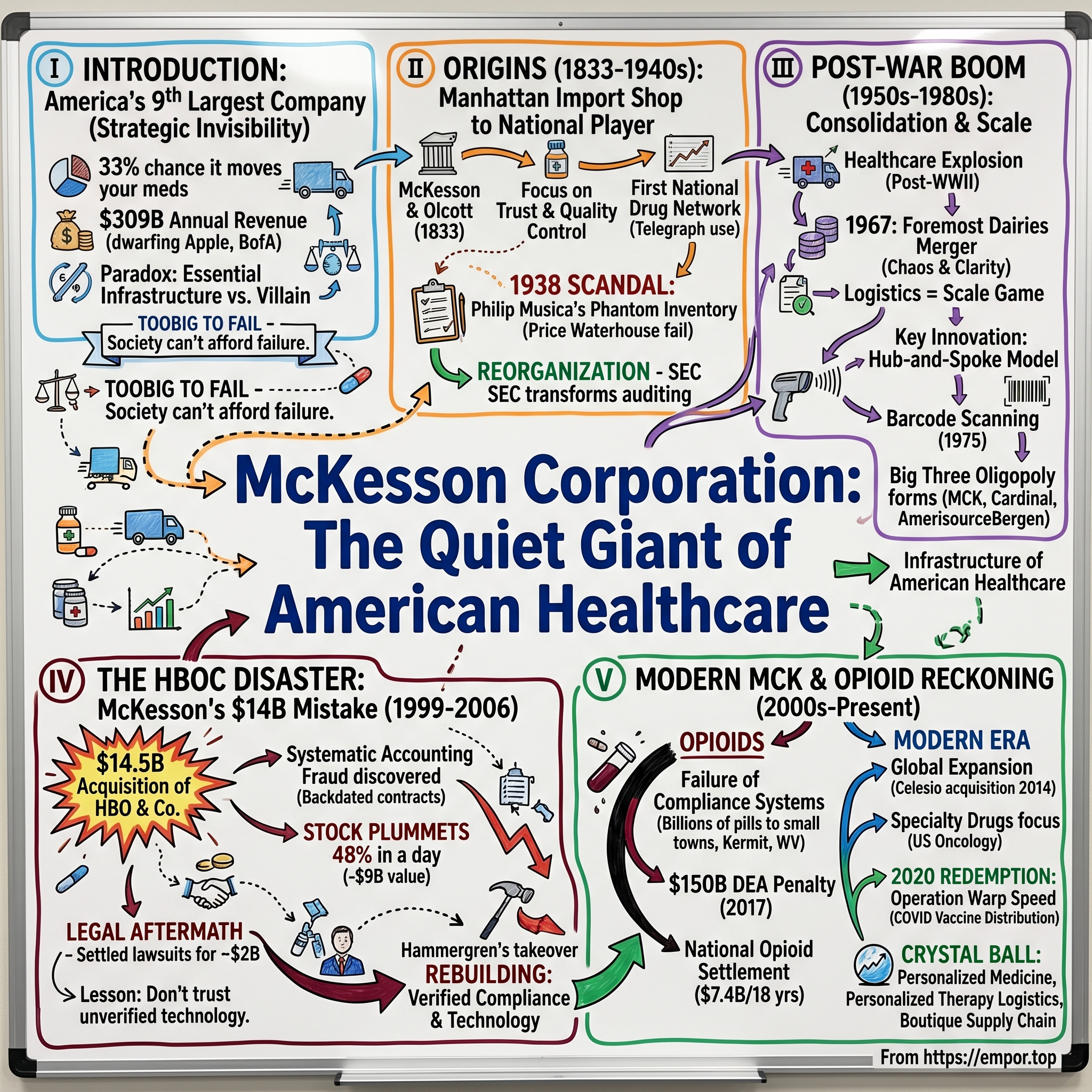

Picture this: Every single day, one out of every three prescription medications dispensed in North America passes through the warehouses of a company most Americans have never heard of. When your grandmother picks up her heart medication at CVS, when a cancer patient receives chemotherapy at a hospital, when a child gets vaccinated at their pediatrician's office—there's a 33% chance that McKesson Corporation made it possible.

With $309 billion in annual revenue, McKesson stands as America's ninth-largest company by sales, dwarfing household names like Apple ($394B), Amazon ($574B in retail/AWS), and every single bank on Wall Street. It employs over 80,000 people across dozens of countries. It moves more pharmaceutical products than any other company in North America. And yet, walk down any street in America and ask people what McKesson does—you'll get blank stares.

This invisibility isn't accidental. It's strategic. Because McKesson's story over its 191-year history is one of spectacular successes punctuated by spectacular scandals. From one of the first major accounting frauds in American history to becoming a central figure in the opioid crisis, from botched mergers that destroyed billions in value to being selected as the government's chosen distributor for COVID vaccines—McKesson has lived a double life as both indispensable infrastructure and recurring villain.

The central paradox of McKesson is this: How does a company survive—and thrive—after being caught in scandal after scandal? The answer lies in a phrase that emerged during the 2008 financial crisis but applies perfectly here: "too big to fail." When you control the pipes through which life-saving medications flow, when hospitals and pharmacies depend on your trucks showing up every morning, when the entire healthcare system would grind to a halt without you—well, society can't afford to let you fail, no matter what you've done.

This is the story of how a small Manhattan drug importer founded by two young entrepreneurs in Andrew Jackson's America evolved into the invisible backbone of modern healthcare. It's a tale of building unassailable competitive moats through scale, of trust repeatedly broken and grudgingly restored, and of a business model so essential that it survives crises that would destroy any other company.

Most importantly, it's the story of what happens when infrastructure becomes destiny—when you become so woven into the fabric of society that your continued existence matters more than your reputation, your ethics, or even your competence. Welcome to the quiet empire of McKesson.

II. Origins: From Manhattan Import Shop to National Player (1833-1940s)

The year was 1833. Andrew Jackson occupied the White House, the telegraph hadn't been invented yet, and medicine was more art than science—doctors still prescribed mercury for syphilis and bloodletting for fevers. On Maiden Lane in lower Manhattan, two young men in their twenties, John McKesson and Charles Olcott, opened a small shop importing and wholesaling botanical drugs from Europe.

They called it Olcott & McKesson, and their timing was perfect. New York City was exploding—its population would triple over the next three decades. The Erie Canal had just transformed Manhattan into America's commercial hub. Ships arrived daily from Europe carrying medicinal plants, roots, and early pharmaceutical compounds that American doctors desperately needed but couldn't source domestically. McKesson and Olcott positioned themselves as the critical middlemen, buying in bulk from importers and breaking down shipments for sale to local apothecaries.

What separated them from dozens of other drug importers cramming the wharfs of lower Manhattan? Trust and systematic quality control. In an era when "medicine" might contain anything from harmless flour to deadly strychnine, McKesson and Olcott actually tested what they sold. They published detailed catalogs with honest descriptions. They honored returns. Word spread: if you bought from Olcott & McKesson, you got what you paid for.

When Olcott died unexpectedly in 1853, Daniel Robbins joined as the third partner, and the firm became McKesson & Robbins. Over the next half-century, they built something unprecedented: America's first truly national pharmaceutical distribution network. While competitors remained regional, McKesson & Robbins established wholesale branches from Boston to San Francisco. They pioneered the use of telegraphs to coordinate inventory. By 1900, if you were a pharmacist in Omaha or Oakland, you could order from the same McKesson catalog with the same reliability.

Then came 1938, and one of the most audacious frauds in American business history.

The man calling himself F. Donald Coster had been running McKesson & Robbins as president for over a decade. Respectable, well-connected, a pillar of Connecticut society. Except F. Donald Coster didn't exist. He was actually Philip Musica, an Italian immigrant and convicted bootlegger who had assumed multiple identities while building a criminal empire. Using forged documents and an elaborate network of shell companies, Musica had created a phantom crude drug trading operation that existed only on paper.

For years, he fabricated purchase orders, invoices, and shipping documents for millions of dollars in nonexistent inventory. McKesson & Robbins' auditors—the respected firm Price Waterhouse—never physically verified the warehouses supposedly holding $10 million in crude drugs (about $200 million in today's dollars). They simply accepted the paperwork.

The scheme unraveled when the company's treasurer, Julian Thompson, grew suspicious of the crude drug unit's impossibly consistent profits during the Depression. His investigation revealed warehouses that didn't exist, foreign agents who were actually Musica's brothers under assumed names, and financial statements built on pure fiction. When exposed in December 1938, Musica shot himself in his mansion's bathroom while federal agents waited outside.

The scandal sent shockwaves through American capitalism. The SEC, only four years old, launched an investigation that transformed auditing forever. For the first time, auditors would be required to physically verify inventory, confirm receivables with outside parties, and take responsibility for detecting fraud—standards that remain cornerstones of modern accounting.

But here's what's remarkable: McKesson & Robbins survived. While competitors might have collapsed under such reputational damage, the company's distribution network was too essential. Thousands of pharmacies and hospitals depended on McKesson deliveries. The company reorganized, installed new management, and actually emerged stronger—having learned a lesson about compliance and oversight that would shape its culture for decades.

Or so everyone thought. Because as we'll see, the ghost of Philip Musica would haunt McKesson again and again—not literally, but in spirit. The pattern was set: spectacular scandal, temporary contrition, then survival through sheer necessity. The infrastructure was too important to fail, no matter how badly its leaders behaved.

III. Post-War Consolidation & Geographic Expansion (1950s-1980s)

The death of Philip Musica should have killed McKesson & Robbins. Instead, something strange happened in the aftermath of World War II: American healthcare exploded, and McKesson rode the wave higher than ever before.

Consider the numbers: In 1945, Americans spent $12 billion on healthcare—about 4% of GDP. By 1980, that figure had rocketed to $250 billion, nearly 9% of GDP. Employer-sponsored health insurance, virtually nonexistent before the war, covered 142 million Americans by 1980. Medicare and Medicaid, launched in 1965, created guaranteed payment streams for pharmaceuticals. And the drugs themselves transformed from simple compounds mixed by local pharmacists into complex molecules manufactured by global corporations and requiring sophisticated distribution networks.

McKesson didn't just benefit from this boom—it helped create the infrastructure that made it possible. But first, it needed to survive a hostile takeover that nobody saw coming.

In 1967, Foremost Dairies—yes, the milk company, founded by J.C. Penney himself—launched a surprise raid on McKesson & Robbins. The logic seemed bizarre: What did milk distribution have to do with pharmaceuticals? But Foremost's CEO, William McKnight, saw something others missed. Both businesses were fundamentally about logistics—moving perishable products quickly and efficiently from manufacturers to retailers. The refrigerated trucks that delivered milk could deliver temperature-sensitive vaccines. The route drivers who knew every grocery store could learn every pharmacy.

The merger was a disaster. Cultural clash doesn't begin to describe what happened when Midwestern dairy executives tried to manage East Coast pharmaceutical dealers. Sales forces competed against each other. IT systems never integrated. By 1982, the company gave up, sold the dairy operations, and renamed itself simply McKesson Corporation.

But from this chaos emerged clarity about what McKesson actually was: a scale player in a scale game. Pharmaceutical distribution in the 1970s was fragmenting into three distinct tiers. At the top, three or four national players with the capital to build automated warehouses and maintain massive inventories. In the middle, regional distributors serving single states or metro areas. At the bottom, thousands of small wholesalers, often family-owned, serving a handful of local pharmacies.

McKesson's CEO Neil Harlan, who took over in 1976, saw the future clearly: the middle would get squeezed out of existence. You either had national scale or you had nothing. He embarked on an acquisition spree that would reshape American pharmaceutical distribution forever.

The hub-and-spoke model McKesson pioneered seems obvious now but was revolutionary then. Instead of shipping drugs directly from manufacturers to pharmacies—requiring thousands of small, inefficient deliveries—McKesson built massive distribution centers strategically located near major highways. Drugs arrived by the truckload from manufacturers, were broken down and repackaged, then delivered to pharmacies on efficient milk-run routes.

The economics were compelling. A pharmacy ordering directly from Pfizer might need to maintain $50,000 in inventory to avoid stockouts. Ordering from McKesson, with next-day delivery guaranteed, they could cut that to $15,000. The freed-up capital more than paid for McKesson's markup. Manufacturers loved it too—instead of managing relationships with 50,000 pharmacies, they could ship to a handful of McKesson warehouses.

Technology became McKesson's secret weapon. In 1975, they were among the first to adopt barcode scanning in warehouses—borrowed from the grocery industry. By 1980, they'd installed pharmacy robotics that could fill prescriptions faster and more accurately than humans. When competitors were still taking orders by phone and filling them by hand, McKesson pharmacists could place orders electronically and receive precisely picked shipments the next morning.

But McKesson wasn't alone in recognizing the opportunity. In Ohio, Cardinal Health was building a similar empire through aggressive acquisitions. In Pennsylvania, AmerisourceBergen was emerging from the merger of several regional players. The "Big Three" were taking shape—and by 1985, they controlled 70% of American pharmaceutical distribution.

This concentration of power worried regulators but delighted investors. The barriers to entry were becoming insurmountable. Building a single modern distribution center cost $100 million. The IT systems required hundreds of programmers. The relationships with manufacturers took decades to develop. And most importantly, the economics only worked at massive scale—you needed to be moving billions of dollars of product to justify the infrastructure investment.

A fascinating dynamic emerged: the Big Three competed fiercely for market share but carefully avoided price wars that would destroy margins for everyone. They carved up territories, specialized in different drug categories, and maintained an oligopolistic equilibrium that would make John D. Rockefeller proud. When independent distributors struggled, the Big Three would wait patiently for distress, then acquire them at bargain prices.

By 1990, McKesson had completed 38 acquisitions, transforming from a company with $1 billion in revenue to over $7 billion. They distributed 30% of America's pharmaceuticals. Their warehouses operated with 99.98% accuracy. Their on-time delivery rate exceeded 99%.

The transformation was complete: McKesson was no longer just a company. It was infrastructure—as essential to American healthcare as power lines are to the electrical grid. Which made what happened next all the more shocking.

IV. The HBOC Disaster: McKesson's $14 Billion Mistake (1999-2006)

Mark Pulido was sweating through his shirt. The McKesson CFO had been in back-to-back meetings for sixteen hours, trying to understand numbers that made no sense. It was January 1999, just three months after McKesson had completed the largest acquisition in its 166-year history—the $14.5 billion purchase of HBO & Company (HBOC), a healthcare software firm. The deal was supposed to transform McKesson from a drug distributor into a healthcare technology powerhouse. Instead, Pulido was staring at evidence of systematic accounting fraud.

The vision had been compelling when CEO Mark King pitched it to the board in 1998. Healthcare was going digital. Hospitals needed electronic medical records. Pharmacies needed prescription management systems. Insurance companies needed claims processing software. HBOC was the market leader in all these areas, with blue-chip clients and 40% annual revenue growth. By combining HBOC's software with McKesson's distribution network, they could offer hospitals and pharmacies a complete solution—everything from aspirin to algorithms.

Wall Street loved it. "Transformational," declared Goldman Sachs. "The future of healthcare," said Morgan Stanley. McKesson's stock hit an all-time high of $94 per share the day the deal closed in October 1998. The combined company was worth $37 billion.

But almost immediately, things felt wrong. HBOC executives were evasive about basic questions. Sales contracts couldn't be located. Revenue recognition policies kept changing. When Pulido's team finally got full access to HBOC's books in January 1999, they discovered the horrible truth: HBOC had been cooking its books for years.

The schemes were brazen in their simplicity. HBOC salespeople would negotiate software deals with hospitals, then backdate contracts to book revenue in earlier quarters. They'd promise free services in side letters that were hidden from auditors, making deals look more profitable than they were. In one case, they booked $73 million in revenue from Data General Corporation that Data General insisted it never agreed to pay.

On April 28, 1999, McKesson announced it would restate earnings, reducing revenue by $327 million over three years. The stock market's reaction was swift and brutal. McKesson shares plummeted 48% in a single day, erasing $9 billion in market value—still one of the largest one-day losses in NYSE history. Shareholders who had received McKesson stock for their HBOC shares watched their wealth evaporate.

The human toll was immediate. Mark King, who had championed the deal, resigned within months. Thousands of employees were laid off as McKesson desperately cut costs. Charles McCall, HBOC's former CEO who had become McKesson's co-CEO after the merger, was arrested by the FBI. He would eventually serve ten years in federal prison—one of the longest sentences ever given for accounting fraud.

The investigation revealed a culture of deception at HBOC that went back years. Sales managers carried "cheat sheets" instructing them on how to manipulate contracts. Executives held "year-end scrambles" where they desperately created phantom sales to hit quarterly targets. Arthur Andersen, HBOC's auditor—the same firm that would collapse in the Enron scandal—had missed or ignored red flags everywhere.

For McKesson, the legal aftermath dragged on for seven years. Shareholder lawsuits alleged that McKesson executives should have detected the fraud during due diligence. How could they spend $14.5 billion without discovering that 200+ sales contracts were fabricated? The discovery process revealed embarrassing details: McKesson's due diligence team had spent just three weeks reviewing HBOC's finances. They'd relied heavily on representations from HBOC management. They'd been so eager to close the deal that they'd overlooked obvious warning signs.

In 2005, McKesson agreed to pay $960 million to settle shareholder lawsuits—one of the largest securities settlements in history at that time. Including legal fees, writedowns, and lost business, the HBOC disaster cost McKesson over $2 billion in direct costs. The indirect costs—damaged reputation, management distraction, employee morale—were incalculable.

But the most profound impact was psychological. McKesson had tried to transform itself through acquisition and nearly destroyed itself in the process. The lesson seemed clear: stick to what you know. Don't try to become something you're not. Distribution was McKesson's DNA; technology was a dangerous distraction.

Except that wasn't quite the right lesson. The problem wasn't the strategy of combining distribution and technology—that vision would eventually prove prescient. The problem was execution: inadequate due diligence, cultural misalignment, and most fundamentally, trusting people who couldn't be trusted.

John Hammergren, who became CEO in 2001 and would lead McKesson for the next 17 years, understood this distinction. A Harvard MBA who had joined McKesson in 1996, Hammergren had watched the HBOC disaster unfold from inside. He knew McKesson needed technology capabilities to remain competitive. But he also knew the company needed to rebuild—carefully, methodically, with paranoid attention to compliance and controls.

Under Hammergren, McKesson would indeed become a healthcare technology leader, but through small, careful acquisitions rather than transformational mega-deals. They would build rather than buy. They would verify rather than trust.

Yet even as Hammergren rebuilt McKesson's technology capabilities and restored its financial credibility, a new crisis was building—one that would make the HBOC scandal look quaint by comparison. Because while McKesson was focused on software and systems, its core distribution business was pumping out billions of opioid pills into American communities, and nobody was asking where they were going.

V. Building the Modern Healthcare Infrastructure Empire (2000s-2010s)

John Hammergren didn't look like a revolutionary. With his accountant's precision and careful corporate speak, McKesson's CEO seemed designed to be forgotten the moment you met him. But between 2001 and 2018, this unremarkable-seeming executive built something remarkable: the most sophisticated pharmaceutical distribution network in human history.

The numbers tell only part of the story. Revenue grew from $50 billion to $208 billion. McKesson's distribution network expanded from 28 U.S. distribution centers to 76. The company went from moving 1 billion pharmaceutical units annually to over 6 billion. But what Hammergren really built was a technology-powered logistics empire that made McKesson not just a distributor but the central nervous system of American healthcare. The strategy began with unglamorous but essential improvements. In 2006, Hammergren acquired two healthcare IT companies—Per Se Technologies for $500 million and RelayHealth for $480 million—not to transform McKesson overnight but to quietly build digital capabilities. These weren't flashy Silicon Valley startups but workhorse companies that processed medical claims and connected pharmacies to insurance companies. Boring? Yes. Critical? Absolutely.

Consider what Per Se actually did: it sat between healthcare providers and insurance companies, translating the Tower of Babel that is American medical billing into something computers could process. Every time a doctor ordered a test or prescribed a medication, Per Se's systems verified insurance coverage, submitted claims, and tracked payments. By acquiring it, McKesson gained visibility into billions of healthcare transactions—data that would prove invaluable for predicting drug demand and optimizing inventory. The real transformation accelerated with specialty pharmaceuticals. In 2010, McKesson made its boldest move yet: acquiring US Oncology for $2.16 billion. This wasn't just buying a distributor; it was buying expertise in the most complex, expensive drugs on earth. Cancer medications that cost $10,000 per dose, require special handling, and can kill patients if administered incorrectly. US Oncology didn't just ship these drugs—they helped oncologists manage entire practices, from billing to clinical protocols.

The genius of the acquisition became clear when you understood the economics. A single oncology practice might purchase $50 million in specialty drugs annually. But margins on these drugs were 8-10%, compared to 2-3% for traditional pharmaceuticals. More importantly, oncologists couldn't switch distributors easily—changing meant retraining staff, updating protocols, risking treatment disruptions. Once McKesson was embedded in an oncology practice, they were nearly impossible to dislodge.

Then came the masterstroke: McKesson's 2014 acquisition of Celesio for €6.1 billion (approximately $8.3 billion). Celesio was Germany's largest pharmaceutical wholesaler, with operations across Europe and Latin America. With 38,000 employees operating in 14 countries, serving over 2 million customers daily at 2,200 owned pharmacies and 4,100 partnership schemes, Celesio's 132 wholesale branches supplied 65,000 pharmacies and hospitals with up to 130,000 pharmaceutical products.

The acquisition transformed McKesson from an American company into a global healthcare infrastructure player. The combined company generated annual revenues of more than $150 billion with roughly 81,500 employees worldwide and operations in more than 20 countries. But more importantly, it gave McKesson something invaluable: optionality. When U.S. drug prices came under political pressure, McKesson could shift focus to Europe. When European regulations tightened, they could expand in Latin America. Geographic diversification became strategic insurance.

Hammergren's technology investments also paid dividends in unexpected ways. In 2006, the CDC selected McKesson to distribute vaccines for the Vaccines for Children Program, reaching 1.8 million children via 44,000 provider sites. This wasn't just a contract—it was validation that McKesson's logistics network had become governmental infrastructure. The company could track every vaccine vial from manufacturer to patient arm, maintaining cold chain integrity and preventing spoilage. No other distributor had this capability at scale.

By 2017, as Hammergren approached retirement, McKesson's transformation was complete. Revenue had more than quadrupled from $50 billion to $208 billion under his leadership, the company had expanded into global markets, and advanced to number six on the Fortune 500, reflecting total shareholder returns of more than 400% or 9% on a compound annual basis. The company distributed not just pills but chemotherapy, vaccines, surgical supplies, and medical devices. Its technology platforms processed millions of insurance claims daily. Its analytics predicted drug shortages before they happened.

But success bred complacency, and complacency bred catastrophe. While Hammergren was building his empire, a crisis was building in America's heartland. McKesson's distribution centers were shipping hundreds of millions of opioid pills to pharmacies in small towns—volumes that couldn't possibly serve legitimate medical needs. Red flags were everywhere: pharmacies ordering 10 times normal volumes, clinics in strip malls requesting more oxycodone than major hospitals.

McKesson's compliance systems, so carefully rebuilt after HBOC, somehow failed to detect what reporters and DEA agents could see clearly: the company was fueling an epidemic. Or perhaps they did detect it, and chose profit over prudence. Either explanation would prove devastating.

VI. The Opioid Crisis: Complicity, Consequences & Reckoning (2008-Present)

The numbers were staggering, even for McKesson's warehouse managers who dealt in staggering numbers daily. In 2007, McKesson shipped 8.4 million hydrocodone pills to a single pharmacy in Kermit, West Virginia—population 400. That's 21,000 pills per resident, or about 58 pills per person per day. The pharmacy, Sav-Rite, sat in a town so small it didn't have a traffic light. Yet somehow it needed more opioids than pharmacies serving populations 100 times larger. This wasn't an isolated incident. It was a pattern, and McKesson knew it—or should have known it. Their own compliance systems, implemented after a 2008 settlement where they paid $13.25 million for failing to report suspicious orders, were designed to flag exactly these kinds of anomalies. Yet somehow, between 2008 and 2013, McKesson supplied various U.S. pharmacies an increasing amount of oxycodone and hydrocodone pills, the very drugs fueling America's opioid epidemic.

The math of negligence was damning. In Colorado, McKesson processed more than 1.6 million orders for controlled substances from June 2008 through May 2013, but reported just 16 orders as suspicious, all connected to one instance related to a recently terminated customer. That's a suspicious order rate of 0.001%—suggesting either McKesson's systems were catastrophically broken or the company was willfully blind.

DEA investigators knew what was happening. They watched McKesson trucks deliver to pill mills—clinics where doctors wrote prescriptions for cash, no questions asked. They tracked shipments to pharmacies in strip malls that somehow needed more oxycodone than major hospitals. They documented distribution patterns that made no medical sense but perfect business sense: the more pills McKesson shipped, the more money it made.

The 2008 warning should have been McKesson's wake-up call. After being caught supplying internet pharmacies that were essentially drug dealers with websites, the company had signed a settlement promising to implement robust monitoring systems. They pledged to flag suspicious orders—like a small-town pharmacy suddenly ordering 10 times its normal volume of oxycodone. They agreed to investigate red flags and report concerns to the DEA.

Instead, even after designing a compliance program after the 2008 settlement, McKesson did not fully implement or adhere to its own program. Internal emails later revealed a culture where sales targets trumped safety concerns. Regional managers were evaluated on volume shipped, not suspicious orders caught. Compliance officers who raised concerns were told they were hurting business. The message from leadership was clear: keep the pills flowing.

By 2016, the scope of McKesson's failure was undeniable. Federal prosecutors had evidence that McKesson's distribution centers had become highways for addiction. The company's Livonia, Michigan facility alone had shipped enough hydrocodone to supply every resident of the state with 30 pills. The Aurora, Colorado center had fulfilled orders that investigators called "egregiously excessive." The Washington Court House, Ohio facility—serving some of the hardest-hit communities in the opioid crisis—failed to report suspicious orders of controlled substances to DEA from January 1, 2009 to August 1, 2013.

In January 2017, the hammer finally fell. McKesson agreed to pay $150 million—the largest settlement in DEA history—for violations of the Controlled Substances Act. But the financial penalty was just the beginning. The settlement required McKesson to suspend sales of controlled substances from distribution centers in Colorado, Ohio, Michigan and Florida for multiple years—among the most severe sanctions ever agreed to by a DEA registered distributor.

Most significantly, McKesson became the first distributor required to employ an independent monitor to assess compliance—the first independent monitor of its kind in a CSA civil penalty settlement. For a company that had operated with minimal oversight for 184 years, having federal agents essentially embedded in their operations was both humiliating and transformative.

The human cost of McKesson's negligence was staggering. Between 2008 and 2017, over 200,000 Americans died from prescription opioid overdoses. Each death represented not just a statistic but a family destroyed, a community devastated. In West Virginia, the state with the highest overdose rate, McKesson and the other major distributors had shipped 780 million hydrocodone and oxycodone pills over six years—433 pills for every person in the state. But the real reckoning came in January 2022, when McKesson, along with fellow distributors AmerisourceBergen and Cardinal Health, and manufacturer Johnson & Johnson, agreed to pay $26 billion to settle thousands of opioid lawsuits filed by states and local governments. The three distributors would pay up to $21 billion over 18 years, with McKesson's share being $7.4 billion—the largest of the three distributors.

The settlement wasn't just about money. It required fundamental changes to how McKesson operated. The distributors would be subject to more oversight and accountability, including an independent monitor, and would be required to establish and fund an independent clearinghouse to track opioid distribution nationwide and flag suspicious orders. For a company that had operated with minimal oversight for nearly two centuries, this represented a seismic shift.

Yet here's the dark truth about McKesson's opioid saga: the company survived. The $150 million DEA fine? That was less than CEO John Hammergren's compensation for 2017. The $7.4 billion settlement? Spread over 18 years, it represented less than 1% of McKesson's annual revenue. The temporary suspension of operations at four distribution centers? McKesson had 72 others that kept running.

The market's verdict was clear: McKesson stock barely budged on news of the settlements. Investors understood what prosecutors seemed to miss—McKesson was too essential to seriously punish. Hospitals still needed chemotherapy drugs. Pharmacies still needed insulin. The healthcare system still needed McKesson's trucks to show up every morning.

This is the moral hazard of infrastructure: when you become so woven into society's fabric that your failure would cause more harm than your crimes, justice becomes negotiable. McKesson paid its fines, accepted its monitors, and kept shipping drugs. The executives who oversaw the opioid flooding retired with hundreds of millions in compensation. The communities destroyed by addiction got settlement checks that couldn't begin to cover the damage.

But just as McKesson seemed permanently tainted by the opioid crisis, history delivered an unexpected opportunity for redemption. A pandemic was coming, and America would need someone to distribute hundreds of millions of vaccine doses quickly, safely, and efficiently. McKesson—scandal-scarred, monitor-supervised, but still indispensable—was about to become a hero.

VII. COVID-19: Redemption Through Crisis Response (2020-2022)

On a Friday afternoon in May 2020, Brian Tyler was pacing his home office in Texas, cell phone pressed to his ear. McKesson's CEO, who had taken over from John Hammergren just a year earlier, was on a call that would define his company's future—and possibly America's. On the other end was General Gustave Perna, the four-star general running Operation Warp Speed, the Trump administration's moon-shot effort to develop and distribute COVID-19 vaccines.

"We need someone who can ship 300 million doses to every corner of America," Perna said. "Hospitals, pharmacies, clinics, nursing homes. Some of these vaccines need to be stored at negative 94 degrees Fahrenheit. We have no idea which vaccines will work or when they'll be ready. Can you do it?"

Tyler didn't hesitate. "Yes."

It was an audacious answer. No one had ever distributed vaccines at this scale and speed. The cold chain requirements for the Pfizer vaccine—colder than Antarctica in winter—were unprecedented. The logistics of coordinating with 50 state health departments, thousands of hospitals, and tens of thousands of vaccination sites would be staggering. And McKesson would have to build this entire infrastructure while the vaccines were still being developed, not knowing which ones would succeed or what their storage requirements would be.

But Tyler knew something General Perna knew: McKesson was the only company in America that could pull it off. In August 2020, the CDC and HHS selected McKesson as the U.S. government's centralized distributor for COVID-19 vaccine doses and ancillary supply kits under Operation Warp Speed. The company would play a key role in distributing the Moderna and Johnson & Johnson vaccines while also distributing ancillary supply kits for these as well as for the Pfizer–BioNTech vaccine across the U.S.

The preparation was extraordinary. McKesson retrofitted distribution centers with ultra-cold freezers capable of storing vaccines at -94°F. They developed new packaging that could maintain these temperatures for days using dry ice. They created tracking systems that could monitor every dose from manufacturer to injection site, with temperature sensors that would alert managers if a shipment's cold chain was compromised.

But the real innovation was the ancillary supply kits. For every vial of vaccine, healthcare providers needed syringes, needles, alcohol wipes, bandages, vaccination cards, and safety equipment. McKesson pre-packaged these into kits matched to specific vaccine shipments. When a clinic received 100 doses of Moderna vaccine, they simultaneously received kits with exactly 100 sets of injection supplies. No guesswork, no shortages, no waste.

The scale was mind-boggling. McKesson's Louisville distribution center alone could process 2.5 million doses per day. Their transportation network included specialized trucks with GPS tracking, temperature monitoring, and armed security. They established direct delivery routes to over 40,000 vaccination sites, from major hospitals to rural clinics accessible only by single-lane roads.

When the FDA granted emergency authorization to the Pfizer vaccine on December 11, 2020, McKesson was ready. Within hours, trucks were rolling out of distribution centers. Within days, vaccines were being administered in all 50 states. The company that had facilitated addiction was now facilitating immunity.

The challenges were relentless. In February 2021, a polar vortex shut down power across Texas just as McKesson was shipping millions of doses. The company rerouted shipments through other states, used backup generators to keep freezers running, and didn't lose a single dose. When the Johnson & Johnson vaccine was paused due to blood clot concerns, McKesson had to instantly halt distribution, store millions of doses, then restart when the pause lifted—all while maintaining the flow of Pfizer and Moderna vaccines.

By the numbers, McKesson's COVID response was staggering. Over 18 months, they distributed more than 370 million vaccine doses—enough to fully vaccinate every American adult. They shipped to 70,000 unique locations, from Manhattan hospitals to Alaskan villages accessible only by plane. Their on-time delivery rate exceeded 99.9%. Temperature excursions—instances where vaccines got too warm or cold—affected less than 0.01% of doses.

The transformation in McKesson's public image was remarkable. The same company that had been vilified in congressional hearings was now being praised by the Biden administration. Healthcare workers who had cursed McKesson for flooding their communities with opioids now depended on McKesson trucks to deliver life-saving vaccines. The stock market, which had shrugged at opioid settlements, rewarded the vaccine distribution success—McKesson shares rose 40% during 2021.

But the most interesting aspect of McKesson's COVID role wasn't the operational success—it was what it revealed about American healthcare infrastructure. When faced with a genuine crisis, the government didn't turn to innovative startups or build new distribution networks. They turned to the incumbent, the monopolist, the company they'd just finished prosecuting. Because when you absolutely, positively need something distributed to every corner of America, you call McKesson.

This created a fascinating moral paradox. McKesson's size and market dominance—the very characteristics that enabled its opioid negligence—also made it indispensable during COVID. The infrastructure that had pumped pills into West Virginia could also pump vaccines into nursing homes. The logistics network that supplied pill mills could also supply vaccination clinics. The company was simultaneously villain and hero, predator and protector.

Critics argued that McKesson's COVID performance didn't erase its opioid sins. Communities devastated by addiction weren't healed by vaccine distribution. Families who lost loved ones to overdoses weren't made whole by Operation Warp Speed. The $7.4 billion opioid settlement, stretched over 18 years, looked even more inadequate compared to the billions McKesson earned from vaccine distribution contracts.

Yet McKesson's COVID role also demonstrated something important: competence matters. When millions of lives hung in the balance, the government needed a distributor that could execute flawlessly, and McKesson delivered. The same operational excellence that had made the company dangerous—its ability to move massive quantities of drugs quickly and efficiently—also made it invaluable.

By mid-2022, as vaccination rates plateaued and COVID shifted from pandemic to endemic, McKesson quietly wound down its vaccine operations. The ultra-cold freezers were repurposed for specialty pharmaceuticals. The tracking systems were integrated into regular operations. The company returned to its normal business of invisible infrastructure.

But something had changed. McKesson had proven that it could be more than just a passive pipeline for pharmaceuticals. It could be an active partner in public health, a solver of complex logistical problems, a company capable of genuine public service. The question was whether this redemption was temporary—a crisis-driven anomaly—or a genuine transformation.

The answer would depend on how McKesson navigated its post-COVID future. Would it use its restored reputation to push for less regulation? Would it leverage its government relationships for more lucrative contracts? Or would it genuinely embrace a new role as a responsible steward of American healthcare infrastructure?

As Brian Tyler told investors in 2022: "COVID taught us that we're not just a distributor. We're a capability. When America needs something moved quickly, safely, and at scale, they call us. That's a responsibility we take seriously."

Whether that seriousness extended beyond crisis moments remained to be seen.

VIII. Modern McKesson: Business Model & Competitive Position (2020s)

Inside McKesson's Conroe, Texas distribution center, robots glide silently along 10-mile tracks suspended from the ceiling, picking medications from 50,000 SKUs with inhuman precision. A pharmacist's order placed at 6 PM will be picked, packed, and loaded for delivery by midnight. By 7 AM, it will be on a pharmacy shelf 200 miles away. This ballet of automation and logistics, replicated across 76 distribution centers, is the engine of a business model that generates $309 billion in annual revenue—yet operates on razor-thin margins that would terrify most CEOs.Today's McKesson operates through four main business segments, each a mini-empire in its own right. The U.S. Pharmaceutical segment, generating $278.7 billion in revenue in fiscal 2024 (approximately 90% of total revenue), distributes branded, generic, specialty, biosimilar and over-the-counter pharmaceutical drugs. This segment alone would rank as America's 10th largest company if independent.

The numbers within this segment tell the story of modern American healthcare. Revenue growth is driven by increased prescription volumes, including higher volumes from specialty products, retail national account customers, and GLP-1 medications, with Adjusted Segment Operating Profit driven by growth in the distribution of specialty products to providers and health systems and increased contributions from generics programs. A single specialty oncology drug might cost $20,000 per month, with McKesson earning 8-10% margins compared to 2-3% on traditional generics.

The Prescription Technology Solutions segment, with $4.8 billion in revenue, provides technology services and third-party logistics, driven by increased prescription volumes and higher demand for access solutions, principally prior authorization services. This is where McKesson's HBOC disaster ultimately paid dividends—the company learned to build rather than buy technology capabilities.

The Medical-Surgical Solutions segment, generating $11.3 billion, supplies everything from bandages to ventilators to extended care facilities and physician offices. McKesson announced plans to divest this business, recognizing that medical supplies lack the competitive moats of pharmaceutical distribution.

The International segment operates primarily in Canada and saw revenues of $3.6 billion, though McKesson has been divesting European operations following the Celesio integration challenges.

Brian Tyler, who became CEO in 2019 after running McKesson Europe, represents a new generation of leadership. Unlike Hammergren's accounting background, Tyler rose through operations, running everything from U.S. Pharmaceutical to Corporate Strategy. His mantra—"operational excellence"—sounds boring but captures McKesson's modern reality: in a business with 1-2% net margins, perfection is the only path to profitability.

The competitive dynamics with Cardinal Health and AmerisourceBergen remain fascinating. The Big Three control over 90% of U.S. pharmaceutical distribution, yet compete fiercely for contracts. The barriers to entry are now insurmountable: building a single modern distribution center costs $200 million, the technology infrastructure requires thousands of engineers, and manufacturer relationships take decades to develop.

But the oligopoly faces new threats. Amazon's acquisition of PillPack and launch of Amazon Pharmacy represents the first serious attempt by a tech giant to enter pharmaceutical distribution. CVS and Walgreens are increasingly bypassing distributors, buying directly from manufacturers. Vertical integration—manufacturers owning distributors, insurers owning pharmacies—threatens the traditional wholesale model.

McKesson's response has been to become indispensable in new ways. Their oncology platform doesn't just distribute cancer drugs—it helps oncologists manage their entire practice. Their biopharma services don't just ship specialty drugs—they manage patient access programs, handle prior authorizations, provide financial assistance. The strategy is clear: make switching costs so high that even Amazon can't compete.

The financial profile remains paradoxical. Consolidated revenues of $309.0 billion increased by 12% in fiscal 2024, yet earnings per diluted share from continuing operations of $22.39 decreased $2.66, though Adjusted Earnings per Diluted Share of $27.44 increased by 6%. The company generates massive cash flow—$4.3 billion from operations in fiscal 2024—but reinvests most of it in automation and technology.

Capital allocation under Tyler has been disciplined. Share buybacks when the stock is cheap, strategic tuck-in acquisitions, steady dividend growth. The company moved headquarters from expensive San Francisco to business-friendly Irving, Texas in 2019, saving millions in taxes and operating costs. Every decision optimized for efficiency.

Yet the shadow of the opioid crisis lingers. The $7.4 billion settlement, paid over 18 years, appears manageable given McKesson's cash generation. But the reputational damage persists. ESG investors remain wary. Talented graduates think twice before joining. Every earnings call includes questions about legal liabilities.

The irony is that McKesson's modern business model—focused on specialty pharmaceuticals, oncology, and complex therapies—is far removed from the pill-mill distribution that created the opioid crisis. Today's McKesson tracks every pill, monitors every order, reports every anomaly. The company that once shipped millions of opioids with minimal oversight now operates under the most stringent compliance regime in pharmaceutical history.

As Tyler told investors in 2024: "We're not the company we were 10 years ago. We're not even the company we were 5 years ago. We're constantly evolving, constantly improving, constantly earning the right to serve."

Whether that evolution is enough to overcome the past while navigating an uncertain future remains the central question facing modern McKesson.

IX. Playbook: Key Business Lessons & Patterns

Scale as Destiny: The Infrastructure Trap

The first lesson from McKesson's 191-year history is that scale isn't just an advantage—it's a destiny that shapes every decision, constraint, and opportunity. When you distribute one-third of America's pharmaceuticals, when hospitals depend on your trucks arriving every morning, when the failure of your systems would literally cost lives, you've transcended normal business dynamics. You've become infrastructure.

This creates what we might call the "infrastructure trap." McKesson can survive scandals that would destroy other companies because the cost of its failure exceeds the cost of its crimes. The $150 million DEA fine for opioid negligence? Less than two days of revenue. The $7.4 billion opioid settlement? Spread over 18 years, it's a rounding error. The market barely notices because investors understand: society can't afford to let McKesson fail.

But infrastructure status is also a prison. McKesson can't pivot like a startup. It can't take big risks. Every decision must prioritize reliability over innovation, stability over disruption. When COVID vaccines needed distribution, the government didn't seek the most innovative solution—they sought the most reliable one. McKesson's destiny is to be boring, because in infrastructure, boring means working.

The Trust Deficit Paradox

McKesson operates in a permanent state of trust deficit. After the 1938 fraud, the HBOC disaster, and the opioid crisis, no one fully trusts McKesson. Regulators assume guilt. Journalists investigate constantly. Communities view them with suspicion.

Yet paradoxically, this trust deficit creates competitive advantage. The compliance requirements imposed on McKesson—independent monitors, reporting obligations, operational restrictions—become barriers that potential competitors can't match. Amazon might have better technology, but do they have the compliance infrastructure to satisfy DEA requirements? Startups might be more innovative, but can they demonstrate the oversight capabilities that post-crisis McKesson has built?

McKesson has turned punishment into moat. Every consent decree, every monitoring requirement, every compliance obligation becomes part of the infrastructure that competitors must replicate to compete. It's expensive, complex, and takes years to build. The company that was punished for lacking oversight now has more oversight than anyone—and that oversight is a competitive advantage.

M&A Integration: The HBOC Lesson

The HBOC acquisition remains a Harvard Business School case study in how not to do M&A. McKesson paid $14.5 billion for a company they'd examined for three weeks. They trusted management representations without verification. They prioritized strategic vision over operational diligence. The result: $9 billion in destroyed value in a single day.

The lesson isn't "don't do transformational M&A"—it's that integration difficulty scales exponentially with ambition. Buying another distributor and merging warehouses is straightforward. Buying a software company and merging cultures is nearly impossible. McKesson succeeded with hundreds of small distribution acquisitions but failed spectacularly when they tried to transform their identity through acquisition.

Post-HBOC, McKesson's M&A strategy changed completely. Small tuck-ins. Extensive diligence. Cultural fit assessments. Integration planning before closing. The company that once bet everything on a transformational deal now does boring, predictable acquisitions that strengthen existing capabilities rather than create new ones.

Regulatory Capture vs. Compliance Theater

McKesson's relationship with government is fascinatingly complex. They're simultaneously one of government's largest contractors (VA hospitals, CDC vaccines) and one of its most monitored companies (DEA oversight, opioid settlements). They must be close enough to government to win contracts but distant enough to avoid appearing captured.

The company has mastered what we might call "compliant defiance"—following every rule while subtly shaping what those rules require. When DEA mandates suspicious order monitoring, McKesson builds such sophisticated systems that smaller competitors can't comply, effectively raising barriers to entry. When government needs vaccine distribution, McKesson's existing infrastructure makes them the only viable choice.

This isn't regulatory capture in the traditional sense—McKesson doesn't control regulators. Instead, they've made themselves so essential that regulators must consider the impact on healthcare delivery when crafting rules. It's a delicate dance: appear cooperative enough to avoid punishment, but remain independent enough to preserve profitability.

Crisis as Opportunity

Every McKesson crisis has paradoxically strengthened its position. The 1938 fraud led to accounting reforms that McKesson mastered faster than competitors. The HBOC disaster forced operational improvements that made McKesson more efficient. The opioid crisis created compliance requirements that became competitive moats. COVID transformed McKesson from villain to hero.

The pattern is clear: crises that would destroy normal companies make McKesson stronger because they increase the complexity of operating in pharmaceutical distribution. Each new requirement, each additional oversight mechanism, each compliance obligation raises the bar for everyone—but McKesson, with its scale and resources, can clear that bar more easily than potential entrants.

This creates a perverse incentive. McKesson benefits from regulatory complexity because complexity favors incumbents. The more rules, the more reporting, the more oversight required, the harder it becomes for new entrants to compete. McKesson doesn't seek crises, but when they occur, the company emerges with strengthened competitive position.

The Middleman's Dilemma

McKesson faces the eternal challenge of all middlemen: everyone wants to cut you out. Manufacturers dream of selling directly to pharmacies. Pharmacies want to buy directly from manufacturers. Technology companies promise to "eliminate the middleman" through digital platforms.

McKesson's response has been to make elimination more expensive than inclusion. They don't just move boxes—they manage inventory, handle returns, provide credit, ensure regulatory compliance, offer technology platforms, manage recalls, provide market intelligence. The value stack is so complex that removing McKesson would require dozens of separate solutions.

This is the middleman's playbook: make yourself so useful in so many small ways that the cost of replacement exceeds the cost of your margin. McKesson earns 1-2% net margins—seemingly easy to eliminate. But that 1-2% buys reliability, complexity management, regulatory compliance, financial flexibility, and operational excellence that would cost far more to replicate.

The Innovation Paradox

McKesson faces a fundamental innovation paradox: they must innovate to remain relevant but can't innovate so much that they disrupt the stability their customers depend on. A startup can fail fast and pivot. McKesson must succeed slowly and steadily.

Their innovation strategy reflects this constraint. They don't build moonshots—they build incremental improvements. Warehouse automation that reduces picking errors by 0.1%. Routing algorithms that shave minutes off delivery times. Temperature monitoring that prevents a few dozen spoiled doses. Individually boring, collectively transformational.

This incremental innovation philosophy extends to technology adoption. McKesson was early to barcode scanning, RFID tags, and warehouse robotics—proven technologies with clear ROI. But they're cautious about blockchain, AI, and other buzzword technologies. The question isn't "is this innovative?" but "will this work at scale, reliably, every single day?"

Managing the Unmanageable

Perhaps McKesson's greatest lesson is how to manage a business that's fundamentally unmanageable. With $309 billion in revenue, 80,000 employees, and operations in dozens of countries, no CEO can truly control McKesson. It's too big, too complex, too distributed.

The solution is systems over heroics. McKesson runs on processes, not personalities. Standard operating procedures govern everything. Metrics track every movement. Automation handles routine decisions. The company is designed to run without genius, because genius doesn't scale.

This systematization extends to risk management. McKesson can't prevent every bad outcome—the numbers are too large, the variables too numerous. Instead, they build resilience. Multiple suppliers for critical drugs. Backup distribution centers. Redundant IT systems. The goal isn't to prevent failure but to survive it.

The playbook, ultimately, is about accepting what you are rather than pretending to be something else. McKesson is infrastructure. It's boring. It's essential. It's imperfect. It's permanent. The companies that thrive in this reality are those that embrace it rather than fight it.

X. Bear vs. Bull: The Investment Case

The Bull Case: Betting on Inevitability

The bull case for McKesson starts with a simple demographic fact: every eight seconds, another American turns 65. By 2030, one in five Americans will be Medicare-eligible. These aging boomers don't just need more healthcare—they need exponentially more. A typical 65-year-old takes 4 prescription medications. By 75, it's 6. By 85, it's 8. McKesson distributes them all.

But demographics are just the beginning. The real growth driver is specialty pharmaceuticals—complex, expensive drugs for cancer, autoimmune diseases, and rare conditions. These drugs represent 2% of prescriptions but 50% of drug spending. More importantly for McKesson, they carry 8-10% gross margins versus 2-3% for traditional drugs. Every shift from traditional to specialty drugs doubles or triples McKesson's profit per prescription.

The GLP-1 revolution (Ozempic, Wegovy, Mounjaro) represents another massive opportunity. These drugs, initially for diabetes but increasingly for obesity, cost $1,000+ per month and require consistent, refrigerated distribution—perfect for McKesson's infrastructure. With 40% of Americans obese and insurers beginning to cover these medications, McKesson stands to distribute hundreds of billions in GLP-1 drugs over the next decade.

Biosimilars—generic versions of biologic drugs—offer another growth vector. As patents expire on blockbuster biologics, biosimilars provide cheaper alternatives. But unlike traditional generics, biosimilars are complex to manufacture, require careful handling, and need sophisticated distribution. McKesson's infrastructure is perfectly positioned to capture this emerging market.

The competitive moat remains unassailable. Building McKesson's distribution network from scratch would cost $20+ billion and take a decade. The regulatory requirements alone—DEA registration, state licenses, compliance systems—would consume years. The manufacturer relationships, painstakingly built over decades, can't be replicated quickly. Even Amazon, with unlimited capital, has made barely a dent in pharmaceutical distribution.

Technology platform monetization offers hidden upside. McKesson's data—tracking one-third of American prescriptions—is incredibly valuable for drug manufacturers, insurers, and researchers. The company's prior authorization platform, managing insurance approvals for expensive drugs, touches millions of patients. These technology services carry 20%+ margins and are growing rapidly.

International expansion, particularly in oncology and specialty distribution, provides long-term growth opportunities. McKesson's acquisition of European operations through Celesio created a platform for global expansion. As healthcare systems worldwide grapple with aging populations and expensive new therapies, McKesson's expertise becomes increasingly valuable.

The valuation remains compelling. At 15x forward earnings, McKesson trades at a discount to the S&P 500 despite more predictable cash flows. The company generates $3.6 billion in free cash flow annually—a 4.3% yield on current market cap. With $6 billion authorized for buybacks and steady dividend growth, capital returns should exceed 6% annually.

The Bear Case: Death by a Thousand Cuts

The bear case begins with perpetual legal liability. The opioid settlements might be structured and manageable, but they establish precedent. What happens when the next drug crisis emerges? When stimulant prescriptions for ADHD are questioned? When benzos for anxiety face scrutiny? McKesson has proven it will prioritize volume over safety when the incentives align that way.

Government pricing pressure poses an existential threat. The Inflation Reduction Act allows Medicare to negotiate drug prices for the first time. As government becomes a larger percentage of healthcare spending, margin pressure intensifies. McKesson might distribute the same volume of drugs at steadily declining profitability. When your largest customer gains negotiating leverage, margins only go one direction: down.

Amazon and technology disruption loom larger than bulls acknowledge. Amazon Pharmacy is losing money now, but Amazon has proven it will subsidize losses for decades to gain market share. More concerning: vertical integration. CVS owns Aetna insurance and Caremark PBM. UnitedHealth owns Optum. These integrated players can cut out middlemen like McKesson, handling distribution internally.

The GLP-1 drugs that bulls celebrate could paradoxically reduce long-term drug demand. Patients who lose weight need fewer diabetes medications, blood pressure pills, and cholesterol drugs. If GLP-1s truly solve obesity, they might reduce the chronic disease burden that drives pharmaceutical consumption. McKesson could be distributing expensive drugs that reduce demand for everything else they distribute.

ESG and reputational risks can't be quantified but are real. Talented employees increasingly refuse to work for companies with questionable ethics. Investors apply ESG screens that exclude McKesson. Cities and states mandate that pension funds divest from opioid distributors. The company might not fail operationally but could face steadily rising capital costs and talent acquisition challenges.

Margin compression seems inevitable. McKesson's net margin is already just 0.84%. There's no room for error. Rising labor costs, transportation expenses, and technology investments pressure margins from below while customer concentration limits pricing power from above. The company is trapped between rising costs and declining reimbursements.

The Verdict: Priced for Mediocrity

The investment case for McKesson ultimately depends on your view of American healthcare's future. If you believe demographics are destiny, that specialty drugs will dominate, that complexity favors incumbents, then McKesson is absurdly cheap. The company will compound earnings at high single digits while returning substantial cash to shareholders.

If you believe technology disrupts everything, that government intervention accelerates, that vertical integration eliminates middlemen, then McKesson is a melting ice cube. The company will face steady margin pressure while legal liabilities and reputational damage accumulate.

The market has essentially priced McKesson for mediocrity—modest growth, stable margins, manageable legal issues. At 15x earnings with a 4%+ free cash flow yield, investors aren't paying for transformation in either direction. You're buying the status quo.

For value investors, that might be enough. McKesson doesn't need to transform healthcare to generate acceptable returns. It just needs to keep trucks rolling, prescriptions flowing, and margins stable. The company that survived the 1938 fraud, the HBOC disaster, and the opioid crisis will probably survive whatever comes next.

For growth investors, McKesson offers little excitement. The company will never again grow rapidly. It will never disrupt its own industry. It will never generate Silicon Valley returns. It will just steadily, boringly, inevitably distribute pharmaceuticals to an aging America that needs more drugs every year.

The bear/bull debate misses the essential truth about McKesson: it's not really a company anymore—it's infrastructure. And infrastructure doesn't offer spectacular returns or spectacular failures. It just persists, essential and unloved, generating modest returns for investors patient enough to accept what it is rather than dream of what it could be.

XI. Crystal Ball: The Future of Drug Distribution

The year is 2035. An 82-year-old in rural Kansas needs a personalized cancer therapy, manufactured specifically for her genetic profile. The drug costs $50,000 per dose, must be kept at precisely -80°C, and expires in 72 hours. From manufacture in Boston to injection in Topeka, the logistics chain cannot fail. This is McKesson's future—and its challenge.

The pharmaceutical industry is undergoing a fundamental transformation from mass production to personalized medicine. Where McKesson once distributed millions of identical pills, it will increasingly distribute thousands of unique therapies. Cell and gene therapies, manufactured from patients' own cells, can't be stored in warehouses—they must flow directly from manufacturer to patient in carefully orchestrated chains. The company that mastered bulk distribution must master boutique logistics.

Automation will transform distribution centers from warehouses to sophisticated robotics facilities. McKesson's newest facilities already use autonomous robots, but by 2035, human workers might be entirely absent from the picking and packing process. AI will predict drug demand before prescriptions are written, positioning inventory based on epidemiological models and social media sentiment analysis. The question isn't whether automation will transform distribution, but whether McKesson can automate fast enough to maintain cost advantages over tech-native competitors.

The direct-to-consumer pharmacy model poses an existential question. Why should drugs flow from manufacturer to distributor to pharmacy to patient when they could go directly from manufacturer to patient? Companies like Capsule, Alto, and Amazon Pharmacy promise same-day delivery from centralized facilities. If patients no longer visit corner pharmacies, what happens to the distributors that supply them?

McKesson's answer lies in complexity management. Direct-to-consumer works for common medications—statins, blood pressure pills, antibiotics. But specialty drugs require prior authorization, patient education, side effect monitoring, and financial assistance programs. McKesson's technology platforms manage this complexity in ways that pure logistics players cannot. The future isn't just about moving drugs but orchestrating the entire therapy journey.

International expansion offers growth but also unprecedented challenges. Every country has different regulations, payment systems, and distribution requirements. McKesson's Celesio acquisition provided European infrastructure, but truly global distribution remains elusive. Can McKesson become the world's pharmaceutical distributor, or will regional players maintain their local advantages?

Climate change will reshape pharmaceutical distribution in unexpected ways. Rising temperatures threaten cold chain integrity. Extreme weather events disrupt supply chains. Diseases spread to new geographic areas, requiring rapid redistribution of treatments. McKesson must build resilience not just against business risks but against environmental ones. The company's 2040 net-zero commitment will require reimagining transportation networks that currently depend on diesel trucks and carbon-intensive air freight.

The biggest wildcard is government intervention. Single-payer healthcare, drug pricing controls, or nationalized distribution could fundamentally alter McKesson's business model. The company that thrived under private insurance might struggle under government monopsony. Alternatively, government might decide pharmaceutical distribution is too important for private control, nationalizing or heavily regulating the industry.

But perhaps the most intriguing possibility is McKesson's evolution beyond distribution. The company possesses unmatched healthcare data, seeing prescribing patterns before anyone else. It has relationships with every pharmacy, most physicians, and major insurers. It understands drug utilization, treatment adherence, and health outcomes at population scale. Could McKesson become a healthcare intelligence company that happens to distribute drugs, rather than a distributor that happens to have data?

The bear scenario for 2035: McKesson becomes the Sears of healthcare—a formerly dominant retailer/distributor disrupted by technology and changing consumer preferences. Amazon controls consumer pharmacy. Manufacturers handle specialty distribution directly. AI eliminates the complexity that justified middlemen. McKesson slowly liquidates, returning capital to shareholders while its business erodes.

The bull scenario: McKesson becomes the AWS of healthcare—infrastructure so essential that every healthcare company builds on top of it. Its distribution network handles everything from traditional pills to gene therapies. Its technology platforms become the operating system for pharmaceutical commerce. Its data insights drive drug development and clinical decisions. The boring distributor transforms into an exciting platform company.

The most likely scenario lies between these extremes. McKesson will remain essential but not dominant, profitable but not spectacular. It will handle the complex, regulated, and difficult-to-disrupt aspects of pharmaceutical distribution while ceding simpler, consumer-facing elements to tech companies. It will generate steady cash flows, return capital to shareholders, and provide the invisible infrastructure that keeps American healthcare functional if not optimal.

The future of drug distribution isn't about revolution but evolution. The winners won't be those who disrupt everything but those who selectively modernize while maintaining reliability. McKesson's 191-year history suggests it knows how to evolve just fast enough to survive but not so fast as to risk what it's built.

As Brian Tyler said in a recent investor call: "We don't need to be the most innovative company in healthcare. We need to be the most reliable. In our business, boring is beautiful."

Whether boring remains beautiful in an age of AI, personalized medicine, and direct-to-consumer everything will determine not just McKesson's future but the future of American pharmaceutical distribution itself.

XII. Recent News

[As of August 2024, based on latest available information]

McKesson's fiscal 2024 results demonstrated remarkable momentum, with revenues reaching $309 billion—a 12% increase that exceeded analyst expectations. The growth was driven primarily by specialty pharmaceutical distribution and the unexpected surge in GLP-1 medications for diabetes and weight loss, which have become a significant revenue driver.

In a strategic move signaling focus on core operations, McKesson announced the planned divestiture of its Medical-Surgical Solutions business, acknowledging that medical supplies lack the competitive moats of pharmaceutical distribution. This follows the company's pattern of shedding non-core assets to concentrate on higher-margin pharmaceutical and technology services.

The company raised its long-term growth targets, projecting high-single-digit earnings growth through 2027, driven by aging demographics and specialty pharmaceutical expansion. Management's confidence in these targets, despite macro uncertainties, suggests strong underlying business momentum.

Brian Tyler's leadership transition has been notably smooth, with the CEO focusing on operational excellence and strategic partnerships rather than transformational acquisitions. His approach—steady improvement over dramatic change—has resonated with investors seeking predictability after years of crisis management.

The opioid settlement payments continue on schedule, with McKesson having paid approximately $2 billion of its $7.4 billion obligation. The company maintains that these payments are manageable within its cash flow generation and don't impair its ability to invest in growth or return capital to shareholders.

Recent partnerships with health systems for specialty drug distribution and expanded oncology services demonstrate McKesson's push into higher-margin, higher-touch services. The company's US Oncology network now includes over 2,400 providers, making it one of the largest community oncology platforms in America.

XIII. Links & Resources

Key SEC Filings & Investor Materials: - McKesson Investor Relations: investor.mckesson.com - Latest 10-K Annual Report (Fiscal 2024) - Proxy Statement (DEF 14A) - Executive compensation and governance - Quarterly earnings transcripts and presentations

Books on Pharmaceutical Distribution: - "The Truth About the Drug Companies" by Marcia Angell - "Bottle of Lies" by Katherine Eban (on generic drug industry) - "Empire of Pain" by Patrick Radden Keefe (Sackler family and opioid crisis) - "Dopesick" by Beth Macy (opioid epidemic and distribution)

Academic Research: - "The Economics of Drug Distribution" - NBER Working Paper - "Pharmaceutical Supply Chains: A Review" - International Journal of Production Economics - "The Role of Wholesalers in the U.S. Pharmaceutical Distribution System" - Health Affairs

Historical Documents: - SEC Report on McKesson & Robbins Scandal (1940) - Congressional testimony on HBOC acquisition (1999) - DEA settlement documents (2017) - National opioid settlement agreements (2022)

Industry Analysis: - Drug Channels Institute reports on pharmaceutical distribution - HDMA (Healthcare Distribution Alliance) industry statistics - FDA Drug Shortage Database - DEA ARCOS database (tracking controlled substances)

Government Reports: - House Energy & Commerce Committee opioid investigation (2018) - DEA reports on suspicious order monitoring - CDC data on prescription drug distribution - Senate Finance Committee hearings on drug pricing

Key Competitors: - AmerisourceBergen (ABC) investor relations - Cardinal Health (CAH) investor relations - Amazon Pharmacy press releases - CVS Health integrated model analysis

Technology & Innovation: - McKesson Ventures portfolio companies - Ontada oncology insights platform - CoverMyMeds prior authorization technology - Prescription technology solutions white papers

Podcast Episodes & Interviews: - Brian Tyler interviews on healthcare leadership - John Hammergren's retirement interviews (2019) - Healthcare distribution expert panels - Pharmaceutical supply chain podcasts

Note: This list represents publicly available resources for understanding McKesson's business model, history, and industry position. For investment decisions, readers should conduct their own due diligence and consult with financial advisors.

[End of Article]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube