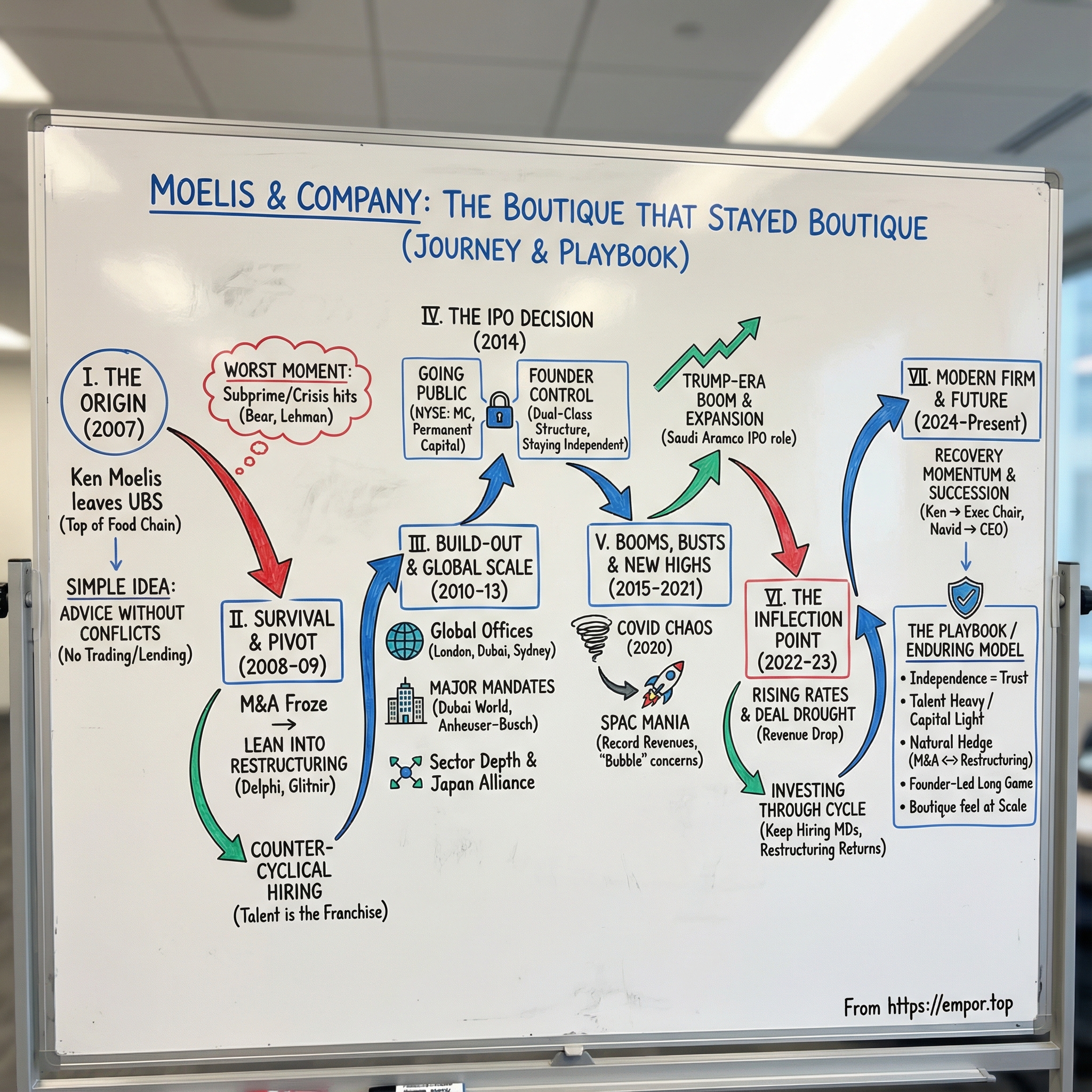

Moelis & Company: The Boutique That Stayed Boutique

I. Introduction & Episode Roadmap

Picture Ken Moelis in March 2007, at the top of the Wall Street food chain. As President of UBS Investment Bank, he was running a global dealmaking franchise—and, in large part, he’d built it. Over his six years at UBS, he was credited with the build-out of the firm’s investment banking operation in the United States. By the end of 2006, UBS had cracked the top four in the global fee pool for the first time. For a Swiss bank long seen as an outsider in American investment banking, it was a statement. And Ken had engineered the transformation.

He could have stayed put. Taken the checks. Collected the prestige. Let the momentum carry him.

Instead, he walked away.

Not for a bigger bulge bracket title. Not for a hedge fund. Ken Moelis left to start his own firm in July 2007—just one month before the subprime mortgage crisis detonated and nearly took the global financial system with it.

That firm was Moelis & Company: a global investment bank that provides financial advisory services to corporations, governments, and financial sponsors. It advises on mergers and acquisitions, recapitalizations, restructurings, and other corporate finance decisions. Since inception, Moelis has advised on more than $4 trillion in transactions.

Which tees up the deceptively simple question at the heart of this story: how does a firm launched at the worst possible moment—right before Bear Stearns vanished, Lehman collapsed, and M&A activity froze—go on to become a multi-billion-dollar public company competing with Goldman Sachs, Morgan Stanley, and JPMorgan? And just as importantly: how did it stay independent, when so many boutiques eventually ended up inside something bigger?

Ken’s ambition wasn’t to build a lifestyle boutique—a few senior rainmakers splitting office space and chasing a final payday on a handful of big mandates. The goal was institutional: an enduring, global advisory firm offering unconflicted advice in M&A, restructuring, and capital markets, but without securities sales and trading. A platform built to last, recruiting young talent straight out of business school alongside mid-level and senior bankers.

What made Moelis different was almost elegantly simple: no trading, no lending—just advice. In a world where the bulge brackets are sprawling conglomerates balancing trading desks, loan books, asset management, and advisory—each creating its own set of conflicts—Moelis sold a rarer product: independent counsel.

From here, we’ll trace Ken Moelis’s path from his early years at Drexel Burnham Lambert in the 1980s, through his rise as a builder inside major institutions, to the founding bet in 2007. We’ll follow how the firm survived the financial crisis by leaning into restructuring, went public in 2014 while keeping founder control, rode the SPAC era to new highs, and then managed through the 2022–2023 deal drought—setting up the next chapter of what it means to stay boutique, even as you scale.

II. Ken Moelis: The Origin Story & Wall Street Apprenticeship

Kenneth D. Moelis was born in 1958. His parents, Gaye (née Gross) and Herbert I. Moelis, weren’t financiers—they were builders. Herbert ran Equity Leasing Corporation, an office equipment company in New York. Ken’s grandfather, Paul I. Gross, had been its president before retiring. Herbert also bred thoroughbred racehorses through CandyLand Stables in Middletown, Delaware.

So Ken didn’t grow up in a house of dealmakers. He grew up around operators—people who had to make payroll, sell real products, and live with the consequences of their decisions. That “real economy” grounding shows up later in his banking style: less fascinated by financial theater, more focused on outcomes.

Moelis earned a Bachelor of Science in Economics and an MBA from Wharton at the University of Pennsylvania. Even there, he had a reputation for intensity. Friends have recalled him training in the boxing gym in the basement, half as stress relief, half as statement. He even joked that he wanted to be the first world boxing champion with an MBA. He got the MBA. The title was harder.

But the metaphor stuck. Elite investment banking is a fight—just in better tailoring.

The Drexel Years: Learning from Milken

Moelis’s start on Wall Street wasn’t glamorous. Morgan Stanley turned him down after he graduated in 1981, and he joined Drexel—then seen by many as a second-tier firm.

The timing couldn’t have been more important. That “second-tier” shop was about to rewrite the rules of finance. At Drexel Burnham Lambert, Moelis worked his way up and ultimately became a managing director in the Los Angeles office working for Michael Milken.

Milken’s high-yield machine turned junk bonds into the fuel for a new era: leveraged buyouts, hostile takeovers, and rapid corporate reinvention. If you wanted to understand capital structure in the 1980s, you didn’t study it—you lived it. Milken later described the apprenticeship like this: over a period of four to six years, Moelis got a “PhD in capital structure.”

He also learned the work ethic that would define his reputation. Don Engel, one of Moelis’s early bosses at Drexel, put it bluntly: there was no such thing as a Saturday or Sunday.

And Milken didn’t just teach mechanics. He pushed Moelis into the deep end with major business figures, like media executive John Kluge, while Moelis also built relationships with scrappy entrepreneurs like real estate investor Sam Zell. Those connections lasted—even after Drexel fell apart and Milken pleaded guilty in 1990 to six felony securities law violations.

For Moelis, the Drexel collapse burned in a lasting lesson: even the most powerful institutions can disappear fast. What survives are relationships, credibility, and the ability to deliver when things get ugly.

DLJ: Building a Powerhouse

After Drexel collapsed, Moelis left with part of his team for Donaldson, Lufkin & Jenrette, where he became head of the corporate finance investment banking division. In the 1990s, DLJ grew into a major force in Los Angeles investment banking—and Moelis was a big reason why.

He didn’t start from scratch. He brought relationships with him, and he treated them like the core asset they were. Engel captured Moelis’s philosophy: if you really want to do this right, your clients have to become your friends.

In 2000, DLJ was acquired by Credit Suisse First Boston. Moelis was named head of U.S. investment banking for the combined firm in September. But the stay didn’t last. Within months, he announced he was leaving for UBS (then UBS Warburg), taking the core of his team with him.

It revealed a pattern that would follow him for decades: he didn’t just move jobs—he moved teams. In an industry that loves the myth of lone-wolf rainmakers, Moelis operated more like a general. Cohesion and loyalty weren’t soft values. They were competitive weapons.

UBS: Transformation at Scale

At UBS, from 2001 to 2007, Moelis rose to Joint Global Head of Investment Banking and eventually President of UBS Investment Bank.

When he arrived, he recruited more than 70 senior investment bankers in roughly three months. This wasn’t a slow build. It was a blitz. And it worked: he helped UBS almost triple its share of U.S. M&A, turning a Swiss institution into a real contender in the most competitive advisory market in the world.

But the higher he climbed inside the machine, the more the machine frustrated him. UBS had size, scale, and caution—along with the bureaucracy that inevitably comes with them. Moelis chafed at that, and not because he disliked rules. He disliked misalignment: big banks making “advice” part of a larger agenda tied to trading, lending, and internal politics.

And it matters to remember the timeline here. Moelis didn’t found his firm because he predicted the financial crisis. The business plan was conceived while the universal-bank model was still thriving. The crisis would later create the opening—but it wasn’t the original motivation.

He left because he’d grown disgusted with what Wall Street was becoming.

Not with making money. Not with doing deals. With the conflicts. With the way huge institutions could end up serving their own balance sheets first and their advisory clients second. Moelis believed there was a cleaner model—and he was ready to bet his career on it.

III. The Founding Bet: Starting a Boutique in 2007

July 2007. Credit markets were starting to crack. Subprime mortgages were imploding. Anyone paying close attention could feel the stress building under the surface.

And Ken Moelis chose that moment to launch an advisory firm.

Moelis & Company opened its doors in July 2007—just one month before the market convulsions that would mark the subprime crisis going mainstream. It was, on paper, terrible timing. But the plan was never to build a small, relationship-monetization boutique. Moelis wanted something enduring. As he later put it, he hadn’t spent three decades climbing through DLJ and UBS just to build something small.

He didn’t do it alone. Moelis founded the firm with partners including Navid Mahmoodzadegan and Jeffrey Raich—battle-tested colleagues who had worked with him at UBS and before. This wasn’t a random collection of resumes. It was a team that already knew how to win, how to execute, and how to operate under pressure.

Then came the early validation that money can’t usually buy: Stephan Schwarzman, CEO of Blackstone, made an initial capital commitment of $170 million. More than the dollars, it was the signal. One of the sharpest players in private equity was effectively telling the market: this platform is real.

The vision was straightforward and ambitious at the same time: a global independent investment bank built around conflict-free advice and long-term relationships, not one-off transactions. The firm started with about 35 employees in New York, plus a small office in Los Angeles—lean by Wall Street standards, but designed to scale.

The pitch to clients was simple enough to fit on a business card: we only work for you, not our trading desk. In a world where big banks could be advising on a deal, lending to the company, trading around the news, and managing money for other parties on the other side, Moelis was selling a cleaner product—pure advisory.

The Irony of Launch Timing

Starting an M&A advisory firm in mid-2007 should have been a disaster. Within the next year and a half, Bear Stearns would be sold under duress, Lehman would collapse, Merrill Lynch would be forced into Bank of America, and M&A would seize up.

But the chaos created an opening. As larger institutions struggled through the downturn, Moelis grew by taking advantage of disruption and hiring strong bankers from places that were retrenching.

In its first full year, the firm broke into the top 10 M&A advisor rankings in the U.S. And it wasn’t on small, forgettable assignments. Moelis advised on Anheuser-Busch’s sale to InBev, Yahoo’s defense against Microsoft’s unsolicited proposal, and Hilton Hotels’ sale to The Blackstone Group.

A startup landing mandates like that isn’t about clever marketing. It’s about trust. These were relationships Ken Moelis had built over decades—executives who knew how he worked and were willing to follow him.

The Blackstone connection mattered, too. With Schwarzman backing the firm and Hilton as a client, Moelis found itself right at the intersection of corporate America and private equity—exactly where premium advisory work concentrates.

Building the "Moelis Way"

From day one, Moelis set out to build a distinct culture. The firm ran with a flatter hierarchy, where senior bankers stayed close to the work instead of disappearing behind layers of delegation. Compensation followed an “eat-what-you-kill” philosophy—heavy on performance, but designed to keep people hungry and accountable.

Underneath that was a core belief: investment banking is, above all, a talent business. This isn’t asset management, where capital compounds, or trading, where technology can create leverage. Advisory is personal and labor-intensive. Outcomes depend on judgment, relationships, and the ability to deliver bespoke solutions when the stakes are highest.

So Moelis went after talent with urgency. While bulge bracket banks were cutting headcount and tightening pay, Moelis was hiring—leaning into the cycle instead of hiding from it. That counter-cyclical instinct would become one of the firm’s defining moves.

IV. Surviving the Financial Crisis: The Making of a Firm (2008-2009)

September 2008. Lehman Brothers filed for what was then the largest bankruptcy in American history. Bear Stearns had been rescued by JPMorgan months earlier. Merrill Lynch was rushed into Bank of America. AIG was effectively nationalized. For a few terrifying weeks, it didn’t feel like a recession. It felt like the plumbing of global finance was breaking.

For a startup advisory firm that wasn’t even two years old, this should have been extinction. M&A didn’t just slow down, it evaporated. Financing markets froze. Boards shelved big moves and focused on basic survival.

Moelis didn’t try to wait it out. It changed what it sold.

The firm’s lifeline was a single word: restructuring.

In July 2008, Moelis launched its restructuring practice by hiring the co-heads of Jefferies’ restructuring team. Almost immediately, the firm was advising on some of the era’s defining distressed situations, including the reorganization of Delphi Automotive. Over time, that same restructuring muscle would show up in mandates like AMR Corp’s reorganization and its merger with US Airways Group.

This wasn’t a frantic pivot. It was the business model doing what Ken Moelis built it to do. He understood that cycles don’t eliminate the need for advice—they just change the kind of advice companies need. In boom times, clients want help buying and selling businesses. In busts, they need someone to renegotiate debt, navigate creditors, and, sometimes, steer through bankruptcy court. Either way, the phone still rings—if you’ve earned the trust.

Moelis also pushed the platform across the Atlantic. Matthew Prest, then head of restructuring at European corporate finance firm Close Brothers, joined in London with his team. Early European mandates included the £1.5 billion recapitalization of the Co-operative Bank and the €15.4 billion restructuring of Glitnir.

The Glitnir assignment was particularly telling. Glitnir was one of Iceland’s three major banks, all of which collapsed in the crisis. Untangling a failed bank across borders forces every skill an advisor can have to matter at once: insolvency regimes, creditor negotiations, and capital structure work under extreme uncertainty. It was exactly the kind of problem a young firm could use to prove it belonged in the room.

Why Independence Mattered During the Crisis

The crisis also made a quiet truth impossible to ignore: at the biggest banks, “advice” often came bundled with other agendas.

Bulge brackets weren’t just advising clients. They were also lending to them, trading securities linked to them, and managing exposures across the market. In a normal year, those conflicts are easy to paper over. In 2008, they were glaring. If you’re a company negotiating with creditors, the last thing you want is an advisor whose institution is also making markets in your debt. If you’re a board weighing options, you don’t want the recommendation tilting toward whatever protects the bank’s balance sheet.

Moelis could offer something that suddenly felt rare: truly unconflicted counsel. No trading desk. No loan book. No internal tug-of-war. And because the firm was built with a flat structure, senior bankers stayed close to the client and the work—exactly what nervous boards wanted when everything was on fire.

Talent Acquisition During Turmoil

The downturn didn’t just create mandates. It created supply.

Across Wall Street, banks were laying off thousands of people, cutting pay, and reorganizing under regulatory and shareholder pressure. In the middle of that chaos, top bankers started looking for a steadier home—one where they could focus on clients instead of the institution’s survival.

Moelis took the opposite side of the trade. While others retrenched, it recruited. And in advisory, that’s the whole game: each senior hire doesn’t just add a resume, it adds relationships, credibility, and future deal flow.

The results showed up fast. In its first two years, the firm completed more than 100 advisory assignments despite the crisis, and by 2009 it had reached roughly $200 million in revenue—powered by a mix of M&A and restructuring work.

Lessons from Crisis Survival

The experience left the firm with a playbook it would keep using.

First: flexibility isn’t a nice-to-have. It’s existential. A firm that can credibly swing between M&A and restructuring has a built-in hedge against the cycle—when one slows, the other tends to surge.

Second: balance sheet safety is a strategic advantage. The bulge brackets were fighting liquidity crises and managing leverage. Moelis had no trading book, no loan portfolio, and minimal balance sheet risk. That stability let the firm keep its attention where it belonged: on clients.

Third: talent is the franchise. The people who joined during the crisis didn’t just help Moelis survive 2008 and 2009. They became the foundation for what came next.

V. The Build-Out Years: Going Global & Multi-Sector (2010-2013)

As the post-crisis fog lifted, dealmaking came back in a rush. After years of playing defense, boards started thinking about growth again—often the fastest kind: buying it. Private equity, sitting on capital it had raised before and during the downturn, returned to the market. And cross-border M&A kept accelerating as globalization rolled on.

Moelis had survived the crisis by being useful when things were breaking. Now it had to prove it could win when things were booming.

The strategy was straightforward: go global, fast—and build real sector depth so the firm wasn’t just a “Ken Moelis relationship story,” but an institution clients could rely on across industries and geographies.

The firm expanded its footprint aggressively, opening offices in London (2008), Sydney (2009), Dubai (2010), Hong Kong (2011), and other global financial centers.

In June 2009, Mark Aedy joined Moelis as head of EMEA investment banking, based in London. Early European mandates included advising Natixis on the €30.0 billion disposal of most of its complex credit derivative portfolio. A few months later, in August 2009, Moelis opened an office in Sydney led by a team from JPMorgan.

Australia, in particular, became a showcase for what the platform was trying to be: senior-led, independent, and able to handle both growth deals and complicated balance-sheet situations. There, Moelis advised SABMiller on the A$11.7 billion acquisition of Fosters Group, advised a consortium including Deutsche Bank, KKR and Värde Partners on the A$8.2 billion acquisition of GE Capital Australia & New Zealand Consumer Finance, and advised Centro Properties on an A$4.3 billion restructuring and an A$5.0 billion merger of Australian interests.

The Dubai World Mandate: A Defining Moment

Around the same time, Moelis landed a mandate that signaled it had truly arrived on the global stage. The firm opened a Dubai office in January 2011 while advising the Government of Dubai on the $24.9 billion restructuring of its investment holding company, Dubai World.

Dubai World was one of the largest and most complex sovereign restructurings in history. The government’s investment vehicle had borrowed heavily to fund real estate and infrastructure projects, and when the crisis hit, it couldn’t meet its obligations. Fixing that meant negotiating with hundreds of creditors across multiple jurisdictions, navigating Islamic finance structures, and managing intense political sensitivity in the Middle East.

Winning the assignment did more than generate fees. It served as a global proof point: Moelis could be trusted with the hardest kind of work—high-stakes, cross-border, and deeply complex—and it opened doors to other sovereign and government-related advisory mandates in the region.

The Japan Alliance: Strategic Partnership

Moelis also found another way to expand without forcing its way into markets that resist outsiders.

In January 2012, the firm announced a strategic alliance with SMBC and its subsidiary SMBC Nikko Securities. Together, they advised on significant cross-border M&A, including Osaka Securities Exchange’s ¥278.4 billion combination with the Tokyo Stock Exchange.

The alliance reflected a pragmatic view of Japan: it’s relationship-driven, domestic players have structural advantages, and building an independent presence from scratch can be slow and uncertain. Rather than fight that head-on, Moelis paired its cross-border advisory strengths with SMBC’s local reach.

Building Sector Depth

Geography was only half the build-out. The other half was specialization.

Moelis invested in sector teams across technology, media and telecommunications, healthcare, industrials, energy, consumer, and financial institutions. The point wasn’t just to have coverage boxes on a website. It was to develop bankers who spoke the language of each industry—who knew the competitive dynamics, understood the regulatory tripwires, and had real relationships with decision-makers.

The platform scaled quickly. Headcount grew from around 50 employees in 2007 to over 300 by 2013, while the firm kept the lean, senior-led structure it had built its identity around. By 2013, revenue reached $411.4 million, up 6.6% from 2012.

By the end of this stretch, Moelis no longer looked like a crisis-era upstart with a few big early wins. It looked like an institution: international offices, sector depth, a proven restructuring engine, and a track record that could credibly compete for the largest and most complex assignments in the market.

VI. The IPO Decision: Going Public While Staying Founder-Led (2014)

By 2014, Moelis no longer looked like a clever post-crisis upstart. It had real global offices, real sector depth, and a restructuring franchise that had been battle-tested. The next question was bigger, and more permanent: how do you fund a boutique for the long haul without turning it into the kind of institution you left behind?

In April 2014, Moelis & Company became a public company. The firm priced its initial public offering of 6,500,000 shares of Class A common stock at $25.00 per share. It listed on the New York Stock Exchange, raised roughly $163 million, and the IPO valued the company at around $1.3 billion.

Goldman, Sachs & Co. and Morgan Stanley & Co. LLC served as the lead joint book-running managers. There was something quietly ironic about it: two bulge-bracket giants helping a boutique competitor step onto the public stage.

Why Go Public?

Ken Moelis wasn’t selling the IPO as a victory lap. As he told Euromoney, there was nothing sentimental about the decision. He didn’t build the firm with “going public” as the endgame. The IPO was a practical move—one shaped by a fairly dark view of where banking was headed, and by what it would take to keep Moelis independent.

The rationale stacked up:

Permanent capital. Traditional advisory partnerships have an inherent problem: when partners retire, they pull capital out. That dynamic can starve the firm of long-term investment and complicate succession. Public equity created permanent capital that couldn’t simply walk out the door.

Currency for acquisitions. A publicly traded stock gives you a new kind of tool: you can use equity to buy businesses or bring in whole teams, not just recruit one banker at a time.

Employee liquidity. Senior bankers could finally turn ownership into real, tradable value without waiting for retirement or an internal transaction.

Brand credibility. A public listing—and the scrutiny that comes with it—added a layer of credibility that matters in cross-border work, especially with governments and sovereign-adjacent clients.

By the time it went public, Moelis had already advised on over $1 trillion in transactions. It didn’t need visibility. It wanted durability.

The Dual-Class Structure: Staying Boutique While Being Public

The most important part of the IPO wasn’t the ticker symbol. It was the structure.

Moelis went public with a dual-class share setup that kept voting control with Ken Moelis through super-voting shares. The intent was clear: protect the firm from the gravity of public markets—the slow pull toward quarterly optimization, risk aversion, and cultural dilution.

Dual-class structures are controversial for a reason. Some institutional investors dislike them because they reduce shareholder influence and concentrate power with founders. But Moelis was making an explicit trade: less “shareholder democracy” in exchange for a better chance at staying true to the firm’s model and culture over decades, not quarters.

Employees continued to own the majority of the company.

Market Reception and Early Performance

The IPO didn’t land with a shrug. On its debut, the stock rose sharply, reflecting investor appetite for a pure-play advisory business—capital-light, fee-driven, and free from the trading and balance-sheet issues that were still haunting universal banks in the post-crisis era.

The broader business backdrop helped too. M&A activity was rising, and Moelis rode that wave. Full-year 2014 revenue climbed to $518.8 million, up 26% from 2013.

The Trade-Offs of Public Markets

Of course, being public comes with a different kind of pressure. Quarterly earnings calls put time horizons on a business that’s supposed to think in relationships and decades. Stock swings can complicate recruiting and retention if equity comp loses its punch. And analyst scrutiny forces a level of transparency that private firms can avoid.

Ken Moelis’s promise, implicit and explicit, was that the firm wouldn’t become a different company just because it had public shareholders. The dual-class structure was the hard guardrail. The rest would come down to discipline: investing through cycles, prioritizing long-term client trust, and keeping compensation and culture aligned with what made Moelis work in the first place.

VII. The Trump-Era Boom & Strategic Expansion (2015-2019)

From 2015 through 2019, the deal engine ran hot. Low interest rates kept financing cheap. CEOs felt bold. And as the decade went on, deregulation and tax reform added more fuel. For Moelis, this was the payoff phase: the firm had survived a crisis, built the platform, gone public—and now it got to compound the relationships and credibility it had been stacking for years.

One early move after the IPO signaled just how broad Ken Moelis wanted the franchise to be. In September 2014, Moelis & Company announced the appointment of Eric Cantor—former U.S. Representative for Virginia’s 7th District and former House Majority Leader—as Vice Chairman and Managing Director, with plans for him to join the firm’s Board of Directors. The message was clear: this wasn’t just about advising on transactions. It was about helping clients navigate the intersection of business, regulation, and public policy.

Cantor’s role was framed as strategic counsel to corporate and institutional clients on key issues, alongside client development and broader strategic advice. Ken Moelis put it simply at the time: “At Moelis & Company, we offer our clients judgment and experience in order to help them with their most critical decisions.”

A few months later, in February 2015, the firm opened a Washington, DC office—turning that ambition into physical presence.

Expanding the Platform

During this stretch, Moelis kept widening what “just advice” could mean. It expanded beyond traditional M&A into capital markets advisory, helping clients think through public and private capital raising. It built out shareholder activism defense as activist campaigns became more aggressive and more common. And it continued scaling restructuring—because even in boom times, someone is always in trouble, and Moelis had learned early that cyclical hedges aren’t theoretical. They’re survival.

And while Moelis the firm was broadening, Ken Moelis the banker was still doing what he’d always done: collecting relationships at the very top of the power pyramid. Over the years, he advised high-profile clients including Ted Turner, Steve Wynn, Carl Icahn, and Donald Trump.

Moelis’s relationship with Trump dated back to his DLJ days. And it produced the kind of story that explains why certain CEOs trust certain bankers when things get tense. Ahead of a meeting with creditors—15 lawyers on the other side—Moelis gave Trump direct instructions: say nothing, let the banker negotiate. In the room, Moelis pushed a hard “take it or leave it” proposal and gave the creditors 10 minutes to decide. When they stepped out to wait, Trump turned to him and asked, “Can we do that?” Moelis replied, “I don’t know, but neither do they.” The approach worked, and the deal ended successfully.

The Saudi Aramco IPO

By 2018, Moelis’s platform had grown into something that could credibly show up on the biggest stages in global finance. That year, Moelis & Co. played a significant advisory role in Saudi Aramco’s planned IPO.

Being chosen for what was billed as the largest IPO in history was a different kind of validation. This wasn’t the typical boutique hunting ground. It placed Moelis in the same conversation—and on the same mandate lists—as Goldman Sachs, Morgan Stanley, and the other global giants.

Financial Performance and Billionaire Status

The boom years didn’t just build the franchise; they minted wealth. Ken Moelis’s personal stake in the public company translated into a net worth that, as Bloomberg later noted, typically belonged to hedge fund founders and private equity titans. It was a clean illustration of the boutique proposition: if you can win elite work without carrying a massive balance sheet, the economics can be extraordinary.

The firm’s results helped reinforce the point. Moelis posted record revenue in a first quarter during this period, and the stock hit a record high. Bloomberg also reported that in 2017, Moelis & Co. worked on $85 billion worth of deals, up $30 billion from the prior year.

The headline takeaway wasn’t the exact tally—it was what it represented. Moelis had a fraction of the size and resources of the bulge brackets, but it was competing for, and winning, major mandates across sectors and geographies. The boutique model wasn’t just surviving. In the right market, it was thriving.

VIII. COVID Chaos & the SPAC Boom (2020-2021)

March 2020 hit like a hard stop. COVID shut down the global economy, markets cratered, and dealmaking didn’t just slow—it vanished. For an advisory firm that only gets paid when transactions actually happen, the setup looked brutal.

Then, almost as suddenly, it flipped.

By the summer, boards were back on Zoom, bankers were back in virtual data rooms, and M&A found its footing again. And riding shotgun on that rebound was the defining financial-market craze of 2020 and 2021: SPACs.

Special Purpose Acquisition Companies—blank-check vehicles that raise money in an IPO and then go shopping for a private company—went from niche product to mainstream mania. For private companies, SPACs promised a faster, more certain path to the public markets than a traditional IPO. For advisors like Moelis, they were a new, high-velocity fee engine.

Moelis didn’t just advise on SPAC deals. It helped create them.

Atlas Crest Investment II, the firm’s second blank-check company, raised $300 million by offering 30 million units at $10. Demand ran ahead of plan, and the deal upsized by 5 million units. It was part of a broader Atlas Crest lineup that also included Atlas Crest Investment, which went public in October 2020 and later announced a merger agreement with electric aircraft developer Archer, along with additional vehicles including Atlas Crest Investment III and Atlas Crest Investment V.

Ken Moelis wasn’t shy about his view of the moment. He told Bloomberg that SPACs were changing the market’s rhythm—capital raised in months, not years. And he framed it as part of a bigger shift: money pouring into alternatives, especially private equity, at massive scale.

Record Financial Performance

The firm’s timing couldn’t have been better. As traditional M&A reopened and SPAC fees piled on, Moelis surged into record territory. In 2021, the firm’s annual net income was $0.365 billion, more than doubling from 2020.

The bigger story wasn’t the number—it was the whiplash. In roughly eighteen months, Moelis went from staring down a pandemic-driven freeze to posting record profitability. This is what the boutique model looks like when it works: capital-light, flexible, and able to redirect its energy to wherever clients are moving.

Strategic Questions

But the boom came with an asterisk. Even at the time, it was hard to ignore the bubble-ish feel. SPACs were getting launched by sponsors with thin operating experience. Targets were being pitched at frothy valuations, often supported by optimistic projections. And regulators were starting to pay closer attention, with the SEC scrutinizing SPAC disclosures.

When Bloomberg asked Ken Moelis about valuations, he didn’t pretend to have discovered religion. He responded with the candor of someone who’s been through enough cycles to know how this ends: he’d been worried about valuations for almost his entire career. The real job, in his view, wasn’t predicting the top. It was staying stable through whatever came next—avoiding leverage, keeping excess capital, and making sure the institution could take a hit.

It was classic Ken Moelis: enjoy the boom, but build like a bust is inevitable.

IX. The Inflection Point: Rising Rates & the Deal Drought (2022-2023)

Then the cycle turned.

The Federal Reserve’s aggressive rate hikes in 2022 snapped the market out of its SPAC-and-stimulus haze. After more than a decade of near-zero rates, the cost of borrowing jumped fast. Financing windows slammed shut. Valuations reset. And the M&A machine—so dependent on cheap capital and confident boards—stalled out.

Moelis felt it immediately. On an adjusted basis, the firm earned revenues of $970.2 million in 2022, down from a record $1,558.0 million the year before—a 38% drop. Over the same period, the number of global completed M&A transactions fell 24%.

A revenue decline like that would be catastrophic in most industries. In advisory, it’s the stress test. Because there’s nowhere to hide: no trading profits to cushion the blow, no loan book throwing off interest. Just fees, tied to deals that either close… or don’t.

And the downshift didn’t stop with the full year. In the third quarter, the firm reported a 55% year-on-year decline in revenues. The quarter made the situation feel stark, and it forced a very public question: when business dries up this quickly, do you cut—or do you invest?

Counter-Cyclical Investment

Ken Moelis chose the contrarian answer. Rather than slashing headcount and hunkering down, the firm kept hiring.

“Our pipe is about where it was in the third quarter last year. Our pipe is high,” Moelis said. “Current conditions generate deals. Volatility, as I’ve said before, leads business leaders to reevaluate their competitive position in the world and make decisions. Many of these decisions will lead to transactions.”

In that spirit, Moelis & Co leaned into recruiting in 2022, adding 25 managing directors—16 through internal promotion and nine through external hiring. The firm focused those investments on technology, healthcare, industrials, and private funds advisory. And Moelis made clear the posture wasn’t temporary: the firm planned to keep hiring the next year too, and to be “aggressive” and “spend.”

“This is a long-term business. Your clients expect you to cover them, and do good work for them through good times and bad. And then when you come out of it, you have an irreplaceable asset, you have great bankers, great clients and relationships that are hard to recreate from scratch ever.”

2023: The Bottom

By 2023, the deal drought had stretched into something more than a pause—it looked like a new normal. For the year ended December 31, 2023, Moelis earned GAAP revenues of $854.7 million, down from $985.3 million in the prior year. On an adjusted basis, revenues were $860.1 million versus $970.2 million—an 11% decline. The drop was driven by fewer M&A completions, partially offset by higher fees from restructuring and capital markets transaction completions.

The volatility showed up most painfully on the bottom line. Moelis reported a net loss for 2023—an abrupt reversal from the record profitability of just two years earlier. It was a reminder of the core truth of the model: when markets seize up, advisory firms don’t just slow down. They can swing hard.

Restructuring Returns

But the cycle that punishes boutiques also creates their next opening. As rates stayed higher, debt burdens got heavier. More companies started running into refinancing walls. And the same dynamic that helped Moelis survive 2008 began to reassert itself: restructuring comes back when cheap money goes away.

“At some point in this cycle there will be a lot of restructuring,” Moelis said. “That might be good for him—his bank has one of the top restructuring businesses on Wall Street—but it also will place many companies on the fine line between existence and extinction.”

For Moelis, it was familiar terrain: when growth deals disappear, the work doesn’t vanish. It shifts—from buying companies to saving them.

X. The Modern Moelis: 2024-Present & the Road Ahead

The recovery arrived in 2024. After two years of rate shocks and deal hesitation, M&A markets began to thaw as interest-rate expectations stabilized and corporate confidence started to return.

Moelis felt the turn in the numbers. On an adjusted basis, the firm earned $1,201.5 million in revenue in 2024, up from $860.1 million the year before—an increase of 40%. The improvement wasn’t a one-product fluke. It was driven by more transaction completions across the platform. By the fourth quarter, revenues had jumped to $438.7 million, up 104% from the prior-year period.

“Our 2024 results reflect strong performance across our business, fueled by the strength of our integrated global team. We are encouraged by our momentum heading into 2025 and the Firm has never been better positioned to continue delivering for our clients and shareholders,” Ken Moelis said.

The Franchise Today

Today, Moelis has 1,078 employees, including 765 investment bankers. Its senior bench is deep: 137 managing directors averaging more than 20 years of experience each, with 56 who previously served as sector and product heads.

Since the IPO, the firm has announced over 1,300 deals totaling $2.2 trillion in transaction volume. It has also advised on the restructuring of $1.0 trillion in liabilities and helped clients raise roughly $200 billion in capital.

And the platform has kept scaling. Managing Director headcount has grown from 94 in 2014 to 173 as of June 2025.

The Succession Question Answered

The biggest “what happens next?” question for Moelis has always been the obvious one: what does life look like after Ken?

In 2025, the firm announced senior leadership changes as part of long-term transition planning, effective October 1, 2025. Ken Moelis, who had served as CEO since the firm’s founding in 2007, will become Executive Chairman and continue advising clients on their most critical strategic decisions. Navid Mahmoodzadegan, Co-Founder and Co-President, will succeed him as Chief Executive Officer and join the Board of Directors.

It’s a major moment for a bank that has been led by Ken since day one. Founder-driven franchises can struggle with succession precisely because the founder’s presence is the product. But Moelis said he expected to pull off the “smoothest transition ever in the history of Wall Street,” according to the Wall Street Journal.

Jeff Raich, Co-Founder and Co-President, will become Executive Vice Chairman and will continue to lead key business areas of the firm. Ken summed up his confidence simply: “I have never felt better about our Firm and the opportunities ahead.”

Looking Forward

On a recent earnings call, Ken Moelis struck an optimistic tone about 2025. He pointed to the possibility of a healthier M&A environment, supported by high equity valuations and the prospect of lower interest rates, and he emphasized continued expansion into private capital advisory and fundraising. The firm also highlighted ongoing demand for structured capital solutions and capital structure advisory services, and its push to better serve the growing private equity and alternative credit ecosystem.

For the twelve months ending September 30, 2025, Moelis revenue was $1.468 billion, a 51.19% increase year-over-year.

XI. Playbook: Business & Investing Lessons

The Moelis Formula

Moelis’s success isn’t a mystery—it’s a set of choices, repeated through multiple cycles, with very little drift. A few principles show up again and again:

Alignment is everything. Founder control kept the firm oriented toward the long game. The compensation model linked pay to performance. And the pure-play advisory focus removed the classic investment bank problem: advice getting tugged around by lending, trading, or internal balance sheet priorities.

The talent business. Advisory is a people business, full stop. Moelis invested in hiring when others were cutting—especially in downturns, when great bankers suddenly become available. Keeping those people meant paying them, but also giving them a culture where they could win and build.

Staying boutique at scale. Going from a 35-person launch team to more than 1,000 employees could have turned Moelis into exactly what it was built to compete against. Instead, it kept a flatter structure and a senior-led style, where the people with the relationships stayed close to the work.

Cycle management. The firm built a natural hedge by operating across M&A, restructuring, and capital markets. When one lane slowed, another often picked up—keeping the platform relevant even when the market mood flipped.

Capital Allocation

Moelis’s financial profile reflects what it is: a talent-heavy, capital-light advisory business. Compensation typically runs around 60–65% of revenues, higher than bulge brackets at roughly 40–45%. That isn’t inefficiency—it’s the price of the product. In this business, your “assets” walk out the door every night.

Because Moelis doesn’t run a trading book or a loan portfolio, it can return a lot of what it earns. Since its IPO, the company has returned approximately $2.8 billion to shareholders through regular dividends, special dividends, and share repurchases.

That shareholder-return story is also underpinned by a conservative balance sheet. As of December 31, 2024, Moelis held $560.4 million in cash and liquid investments and carried no debt or goodwill.

The takeaway is simple: when you don’t take balance sheet risk, you don’t need balance sheet heroics. Free cash flow can go back to owners through dividends and buybacks, instead of being held against trading losses or credit exposures.

Competitive Moats

Moelis’s advantages aren’t exotic. They’re the same ones that matter in every era of advisory, executed with discipline:

Relationship depth. CEO and board-level trust compounds over decades, and it’s hard to dislodge once earned.

Sector expertise. Deep vertical knowledge in industries like technology, healthcare, energy, and industrials helps the firm bring more than process—it brings judgment.

Independence. Conflict-free advice stays valuable precisely because so much of Wall Street still isn’t conflict-free.

Founder-led culture. Faster decisions and a longer time horizon can be a real edge in a business where bureaucracy kills momentum—and sometimes, kills deals.

XII. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

Competitive Rivalry (HIGH). Moelis plays in one of the most crowded, reputation-driven markets in finance. Its competitors range from fellow independents like Lazard Ltd., Evercore Inc., and Rothschild & Co to the bulge brackets—Goldman Sachs Group, Inc. and Morgan Stanley—who can bring massive relationships and distribution power to the table. The fight is over trust, sector expertise, and flawless execution, with price pressure showing up when mandates turn into bake-offs. League tables matter because on Wall Street, perception often becomes reality.

Threat of New Entrants (MODERATE). The real barrier isn’t licensing; it’s credibility. Track record and relationships take years to earn. But the industry has one structural loophole: senior bankers can walk. When a rainmaker leaves with a book of business and starts a new shop, they can become a viable entrant quickly—exactly the play Ken Moelis ran in 2007. Compared to trading or lending, pure advisory also faces fewer regulatory and capital hurdles.

Bargaining Power of Buyers (MODERATE-HIGH). Clients have plenty of options, and they know it. In competitive processes, fees can get negotiated hard. But when the decision is existential—a transformational acquisition, a hostile defense, a restructuring—boards and CEOs still pay for judgment. The best advisors don’t win by being cheapest; they win by being the person you trust when the stakes are highest.

Bargaining Power of Suppliers (HIGH). In this business, the “suppliers” are the bankers. Senior managing directors control relationships, and relationships are the product. If a top MD leaves, revenue often walks out with them. That’s why advisory firms live with high compensation ratios: it’s not generosity, it’s the cost of keeping the franchise intact.

Threat of Substitutes (MODERATE-GROWING). Companies can lean more on internal corporate development teams. Big 4 consulting firms keep pushing further into deal advice. Private equity firms increasingly bring operational and capital-structure capabilities in-house. And while technology may automate parts of the process over time, the most complex deals still revolve around negotiation, psychology, and judgment—areas where “software-only” isn’t close to replacing senior advice.

Hamilton's 7 Powers Analysis

Counter-Positioning (STRONG—historical advantage, fading). Moelis’s founding edge—pure advisory without trading or lending conflicts—was a sharp contrast to universal banks, especially in the post-2008 trust vacuum. Over time, regulation and changed behavior have reduced some bulge bracket conflicts. But the core idea still resonates: when clients want independent advice, “we don’t have a balance sheet agenda” is a compelling answer.

Branding (STRONG). The Ken Moelis name carries weight, and the firm’s reputation for independence and senior attention helps it win rooms it has no right to win on size alone. League table visibility acts like continual advertising: it signals relevance and momentum.

Switching Costs (MODERATE-HIGH). For repeat clients, switching isn’t just swapping vendors—it’s rebuilding trust and re-teaching history, preferences, and politics. That creates stickiness. For one-off deals, though, switching costs drop, and clients can shop the mandate around.

Scale Economies (MODERATE). Scale helps in brand recognition, global coverage, and the ability to staff across time zones and sectors. But investment banking isn’t a factory business. Deals are bespoke, and the limiting factor is usually senior judgment and relationships, not the size of the platform.

Network Effects (LOW-MODERATE). There’s no classic network effect the way a marketplace or software product has one. Still, reputation compounds. One successful mandate leads to referrals, visibility, and credibility that can make the next win easier. Alumni networks matter too—especially early on, when Ken’s UBS relationships helped seed the franchise.

Cornered Resource (MODERATE). The closest thing to a “cornered resource” is elite talent in specific sectors and products. But it’s only partially defensible, because that talent can move. What’s more durable is a concentration of teams that have worked together long enough to feel institutional.

Process Power (MODERATE). There is real craft in how firms run processes, negotiate, and execute. Training, internal collaboration, and repeatable playbooks create advantage at the margin. But advisory remains as much art as science, and process rarely outweighs who the client trusts.

Summary

Moelis’s strongest powers are counter-positioning, branding, and switching costs in long-term relationships. The soft underbelly is the same as every advisory firm’s: talent can leave, revenue is cyclical, and competition never stops.

XIII. Bull vs. Bear Case

The Bull Case

Moelis is what the boutique model looks like at full maturity: a best-in-class independent advisory franchise with real global reach, still run with a founder-led mindset. The structure matters here. Founder control tends to keep incentives aligned and decisions oriented toward the long game—exactly what clients want when they’re making once-a-decade moves.

A big piece of that engine is sponsors. Roughly half of Moelis’s transactions involve private equity and other sponsors. By 2024, cumulative sponsor deal volume had reached $1.1 trillion, built on relationships with more than 580 private equity firms, over 50 pension funds, and over 40 sovereign wealth funds. In an era where sponsors are sitting on massive pools of capital and constantly recycling portfolios, being in that flow is a durable advantage.

Then there are the macro tailwinds. CEO succession keeps forcing corporate transitions. Private equity has over $2 trillion in dry powder to deploy. The energy transition is driving large-scale capital reallocation. AI is pushing companies to rethink business models and competitive positioning. And geopolitical realignment is making cross-border strategy messier, which tends to increase demand for high-trust advisory.

Higher rates also bring a more predictable gift for a firm like Moelis: restructuring. As debt gets harder to refinance, more companies end up needing capital structure advice, creditor negotiations, and, sometimes, full-blown reorganizations.

And when the market does reopen, the operating leverage can be sharp. This is a fee business with minimal capital requirements. When completions come back, profitability can scale quickly without needing to build factories or carry inventory.

Even with the cyclicality, the firm has remained profitable across the cycle. Pre-tax margins peaked at 34.8% in 2021, then moderated to 16.4% in 2024—still meaningfully positive in a period when much of the advisory world was clawing back from the deal drought.

The Bear Case

The same pure-play simplicity that makes Moelis attractive also makes it fragile. Cyclicality is extreme. As 2022 and 2023 showed, revenue can fall 30–40% in down years when financing dries up and boards hit pause.

The compensation model amplifies that reality. With compensation often running around 60–65% of revenues, margin expansion is structurally capped. And when revenues drop, pay has to adjust with it—fast—because there isn’t a giant buffer elsewhere in the P&L.

Talent risk is existential. In advisory, the product is relationships and judgment, and both live inside senior bankers. If key managing directors leave, revenue can leave with them. In the harshest framing, the firm is a collection of relationships operating under one brand—and collections can break apart.

Competition also isn’t easing. New boutiques keep getting formed by senior bankers leaving bulge brackets. The Big 4 continue pushing further into deals and corporate finance advisory. And the bulge brackets have gotten better at borrowing the boutique messaging, leaning into their own claims of independence even while running balance sheets.

Technology is the long-term wild card. AI and data analytics could commoditize pieces of advisory work over time. It’s unclear how quickly or how deeply that changes the economics—but it’s a risk worth keeping on the radar.

Finally, there’s succession. Founder-led firms always face the question of what happens when the founder steps back, because the founder’s presence often functions as both culture and brand. The transition to Navid Mahmoodzadegan may be smooth, but the category risk doesn’t disappear just because the plan is thoughtful.

Key Metrics to Watch

For investors monitoring Moelis’s performance, three metrics matter most:

-

Revenue per Managing Director: a read on productivity and franchise strength. The healthiest growth is when revenue rises faster than senior headcount, creating real operating leverage.

-

Managing Director retention/attrition: departures—especially in key sectors—can be an early warning signal. Hiring matters, but keeping proven rainmakers matters more.

-

Non-M&A revenue mix: restructuring, capital markets, and private funds advisory provide diversification. A more balanced mix tends to mean more resilience; a heavy reliance on M&A increases cyclical exposure.

XIV. Epilogue: What's Next for Moelis?

Moelis is heading into its post-founder-CEO era with real momentum. For the twelve months ending September 30, 2025, revenue was $1.468 billion—up 51.19% year-over-year. And the leadership handoff—Ken Moelis shifting to Executive Chairman while Navid Mahmoodzadegan steps into the CEO role—doesn’t read like a sudden pivot. It reads like the outcome of 18 years of building a firm designed to outlive its founder.

Navid put it this way: "I am incredibly proud of what we have achieved together these past 18 years since founding Moelis and am honored and excited to have the opportunity to serve as CEO at this important moment in the evolution of our Firm. As we move forward, we will continue to put clients first—that has always been the key to the Firm's long-term success and achieving outstanding results for our shareholders. We have never been better positioned to capitalize on the significant growth opportunities ahead."

The priorities going forward are familiar, and pointed: expand further in the Middle East and Asia, deepen sector strength in areas like technology and healthcare, and keep building private capital markets capabilities as more of the financial world shifts toward alternative capital.

The backdrop is only getting more complicated. Bulge bracket banks are still navigating regulatory complexity. Boutiques are still combining to gain scale and reach—Evercore’s acquisition of Robey Warshaw in London is one recent example. And technology keeps reshaping how deals get found, evaluated, and executed.

But the core proposition Ken Moelis laid out in 2007 hasn’t gone stale. In an industry where advice is often tangled up with lending, trading, and internal politics, there’s still enduring value in independent counsel—delivered by senior professionals who can sit across from a board and credibly say: we only work for you.

That’s the throughline of the whole story. Moelis stayed independent. It kept the boutique feel even as it scaled into a global platform. And it proved that you can go public without turning into the kind of institution you set out to beat.

Ken Moelis built something rare: a firm that survived the worst financial crisis in generations, went public without losing its identity, competed against institutions many times its size—and now hands the keys to the next generation from a position of strength.

The boutique that stayed boutique. The startup that became an institution. The bet that paid off.

XV. Further Reading

If you want to go deeper—into Moelis specifically, and into the boutique-vs.-bulge-bracket world more broadly—here are a few great starting points:

- Moelis & Company SEC Filings (10-Ks, DEF-14As) – Available at moelis.com/investor-relations

- "The Last Tycoons" by William D. Cohan – The best single history of the boutique model, told through Lazard

- "Money and Power" by William D. Cohan – A look at Goldman Sachs and the bulge-bracket machine Moelis positioned against

- Ken Moelis interviews on Bloomberg, CNBC – The founder, in his own words

- "Barbarians at the Gate" by Bryan Burrough & John Helyar – The LBO era that set the tone for modern dealmaking

- "The Accidental Investment Banker" by Jonathan A. Knee – A clear, inside-the-room view of M&A advisory

- Evercore, Lazard, PJT Partners investor presentations – How the closest peers describe themselves and their economics

- "Den of Thieves" by James B. Stewart – The Drexel/Milken backdrop that shaped Moelis’s early apprenticeship

- Wall Street Journal, Financial Times archives – Deal coverage, banker moves, and the public narrative as it unfolded

- "The Partnership" by Charles D. Ellis – How Goldman’s culture evolved—and why that matters for understanding Wall Street

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube