Matson Inc.: America's Pacific Lifeline — From Sugar Ships to Container Kings

I. Introduction and Episode Roadmap

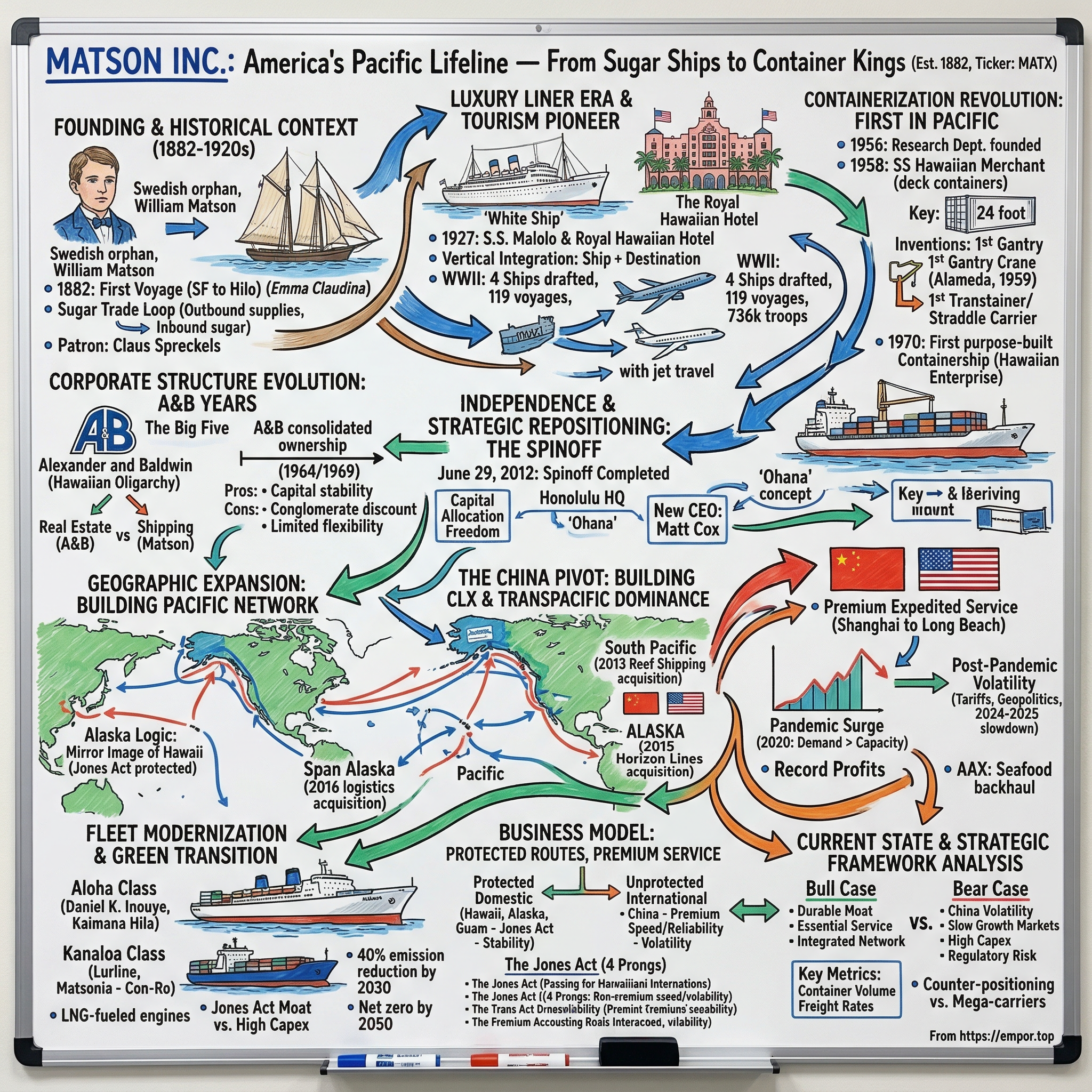

Somewhere in the middle of the Pacific Ocean, roughly 2,400 miles from any continent, sits the state of Hawaii — home to nearly 1.5 million people who depend on ships for approximately ninety percent of their consumer goods. Every gallon of milk, every car, every two-by-four that builds a house on Oahu arrives by vessel. And for over 140 years, one company has been the primary lifeline connecting those islands to the American mainland: Matson, Inc.

In 2024, Matson reported net income of $476.4 million on revenue of $3.42 billion. Those are remarkable numbers for a company most mainland Americans have never heard of.

But here is the deeper puzzle: Matson was founded in 1882, making it one of the oldest continuously operating companies in the American Pacific. It pioneered containerization in the Pacific before the rest of the industry caught on. It built the hotels that invented Hawaiian tourism. It survived two world wars, the collapse of the passenger liner business, four decades as a subsidiary of a Hawaiian conglomerate, and a dramatic spinoff that turned it into a standalone public company. And today, it operates what amounts to a legal monopoly on some of the most essential shipping lanes in the United States.

How did a Swedish immigrant's schooner hauling sugar become America's most strategic Pacific shipping franchise? That is the question at the heart of this story.

The answer involves the Jones Act — a century-old federal law that effectively bars foreign ships from carrying cargo between American ports — and a company that has used that regulatory protection not as a license for complacency but as a platform for reinvention. Matson pioneered containerization in the Pacific, then pivoted from luxury cruise lines to freight. It expanded from Hawaii into Alaska, Guam, Micronesia, and the South Pacific. And in a move that would have mystified its nineteenth-century founders, it built a premium expedited shipping service from China to Southern California that became a major profit engine during the pandemic era.

The themes running through this story are durability, adaptation, and the peculiar economics of regulated monopolies. Matson is not a hypergrowth tech company. It is infrastructure — the kind of business that is invisible until it stops working, at which point entire economies grind to a halt.

Understanding how it was built, how it has evolved, and where it stands today tells us something important about the nature of competitive advantage, the power of regulatory moats, and what it means to be essential.

What makes Matson different from nearly every other company covered in long-form business analysis is the sheer duration of its competitive position. Most business moats last decades. Matson has been operating on the same Pacific routes for 144 years. The company has outlasted the Hawaiian monarchy, territorial government, statehood, the rise and fall of the sugar industry, the age of sail, the age of steam, the age of diesel, two world wars, and the complete transformation of global trade. That kind of persistence demands explanation, and the explanation has implications far beyond shipping.

II. Founding Story and Historical Context (1882–1920s)

Picture San Francisco in 1867: a city still raw from the Gold Rush, its harbor crowded with clipper ships and steamers, its streets teeming with fortune-seekers and immigrants. Into this chaos stepped a seventeen-year-old Swedish orphan named William Matson, broad-shouldered and blue-eyed, who had just spent four years working his way from Lysekil, Sweden, across the Atlantic and around Cape Horn as the lowest-ranking hand on a series of sailing vessels.

Matson had been orphaned as a child in a small coastal town on Sweden's southwest coast. By age ten he had made his first sea voyage. At fourteen, he signed aboard a Nova Scotian vessel as a "boy" — the most menial rank on a ship — and sailed for New York. From there he joined another crew bound around Cape Horn, the most treacherous passage in maritime navigation. When he arrived in San Francisco, he had no family, no money, and no connections. What he had was four years of hard-won seamanship and an appetite for something more.

Within two years, this teenage immigrant had risen to command his own vessel — the schooner William Frederick, running coal from Mount Diablo to the Spreckels Sugar Company refinery in San Francisco. That coal route placed Matson squarely in the orbit of Claus Spreckels, the German immigrant known as the "Sugar King of the Pacific," who controlled an empire stretching from California refineries to Hawaiian plantations.

Spreckels recognized something in the young captain and hired him to skipper the family yacht. It was an intimate posting — Matson moved from the world of commerce into the personal sphere of one of California's wealthiest dynasties.

The relationship changed everything. When Matson proposed striking out on his own with a trading route to Hawaii, Spreckels provided the financing. On April 10, 1882, Captain William Matson sailed his three-masted schooner Emma Claudina — named for Spreckels' daughter — out of San Francisco Bay carrying 300 tons of food, plantation supplies, and general merchandise. Thirteen days later, on April 23, 1882, the Emma Claudina entered Hilo Bay at dawn. She returned to San Francisco loaded with sugar.

The business logic was elegant in its simplicity: Hawaii's booming sugar plantations needed a constant stream of supplies from the mainland, and the ships could return with the sugar those same plantations produced. Matson had found a natural trade loop — a self-reinforcing cycle where outbound cargo paid for the voyage and inbound sugar paid for the return. Spreckels guaranteed the return cargo. The patron-protege relationship that began over coal deliveries had created a shipping company.

To appreciate the significance of this moment, consider Hawaii's economy in the 1880s. The islands were an independent kingdom with an economy almost entirely built on sugar. Plantations controlled by American and European families needed reliable shipping to get their product to mainland refineries and to receive the equipment, food, and labor supplies that kept the plantations running. Whoever controlled the shipping lanes controlled the economic lifeline of the islands. Matson, backed by the Sugar King himself, was positioning himself as that essential link.

Matson expanded rapidly. By 1887 he had outgrown the Emma Claudina and acquired the brigantine Lurline from Spreckels — a name that would become the most iconic in Matson's history, carried by multiple vessels across more than a century.

His fleet grew ship by ship, each vessel incorporating innovations ahead of its time. The bark Rhoderick Dhu featured the first cold storage plant and electric lights on a Pacific vessel. The Enterprise became the first offshore ship in the Pacific to burn oil instead of coal. These were not incremental improvements — they represented a captain-turned-entrepreneur who understood that competitive advantage in shipping came from technological leadership.

In 1888, a missionary schoolteacher named Lillie Low boarded the Lurline in San Francisco, bound for Hilo. Legend holds that Matson himself was captaining the ship and the two met at sea. They married in Hawaii in May 1889. Their daughter, born in September 1890, was named Lurline Berenice Matson — reportedly named for both the legendary Rhine river siren Loreley and the ship on which her parents met.

By the time William Matson died in 1917 at age sixty-seven, his fleet comprised fourteen of the largest, fastest, and most modern ships in the Pacific passenger-freight service. He had been appointed Swedish Consul with jurisdiction over the entire Pacific Coast — a remarkable arc for a boy who had arrived in San Francisco fifty years earlier with nothing but the calluses on his hands.

The company he left behind continued expanding under new leadership. In May 1926, Matson Navigation took over the Oceanic Steamship Company, a competitor that had served the South Pacific and Australian routes since the 1880s. The acquisition expanded Matson's network beyond Hawaii to include routes to Samoa, Fiji, New Zealand, and Australia — the first step toward the broader Pacific presence the company maintains today.

The schooner captain's operation had become one of the dominant maritime forces west of the Rockies. But Matson's next transformation would take it into a world William Matson could never have imagined — the luxury liner business, where ships became floating palaces and a company that hauled sugar would invent modern Hawaiian tourism.

III. The Luxury Liner Era and Tourism Pioneer (1920s–1970s)

Before Matson built the S.S. Malolo, Hawaii was an exotic curiosity known mainly to missionaries, sugar barons, and the occasional adventurous traveler. After Matson built the Malolo, Hawaii became a destination — arguably America's first manufactured tourism dream.

The transformation began not with a ship but with a hotel. On February 1, 1927, the Royal Hawaiian Hotel opened on Waikiki Beach — a $4 million investment by Matson Navigation Company designed by Warren and Wetmore, the same New York firm responsible for Grand Central Terminal. The six-story, 400-room structure, done in a Spanish-Moorish style fashionable in the age of Rudolph Valentino, sat within fifteen acres of landscaped gardens.

At the black-tie grand opening, 1,200 guests paid ten dollars a plate — lavish for the era. With its sprawling pink stucco facade, it immediately earned the nickname that stuck: "The Pink Palace of the Pacific." The first general manager, Arthur Benaglia, presided over a staff of 300, including ten elevator operators and lobby boys dressed in "Cathayan" costume.

Matson understood something revolutionary for the 1920s: the ship and the destination were not separate products. They were one integrated experience. Deliver passengers in luxury, house them in luxury, and you create a market that did not exist before. This was vertical integration as brand-building — decades before the concept had a name.

Later that same year, Matson launched the ship that would make the hotel strategy work. The S.S. Malolo — Hawaiian for "flying fish" — was designed by the legendary naval architect William Francis Gibbs and was the fastest ship in the Pacific at twenty-two knots.

But the Malolo nearly never made her maiden voyage. During sea trials in the North Atlantic on May 25, 1927, a Norwegian freighter emerged from fog and rammed her broadside, opening a fifteen-foot gash in the hull. The ship took on over 7,000 tons of water. The collision was of the same severity and in the same position as the one that had sent the Empress of Ireland to the bottom in ten minutes, killing over a thousand people.

But the Malolo held. Her innovative multi-compartmented hull, designed by Gibbs with obsessive attention to survivability, kept her afloat. Gibbs later said the accident "gave us a status no one could argue with." The Malolo was repaired and departed on her commercial maiden voyage from San Francisco to Honolulu on November 16, 1927.

There is a darkly poetic footnote to the Malolo's early career. In 1929, Matson sent her on an exclusive "Round the Pacific Good-Will Cruise." Some 325 passengers — all acknowledged millionaires, specially selected by the San Francisco Chamber of Commerce — embarked on a 90-day, 24,000-mile itinerary calling at nineteen ports in fourteen countries. The cruise departed San Francisco on September 21, 1929. Just 38 days later, on Black Tuesday, the stock market crashed. By the time the Malolo returned on December 21, 1929, approximately half of the 325 millionaires aboard had gone broke. They had left as rich men and returned as men of ordinary or ruined means.

Between 1930 and 1932, Matson built three more luxury liners: Mariposa and Monterey for the South Pacific and Australasian routes, and a new Lurline for the Hawaii run. All four ships featured distinctive twin yellow funnels with black tops and a blue central "M," their hulls painted gleaming white — earning them the collective name "the White Ships." Together they defined luxury Pacific travel for a generation.

What Matson created around these ships was something closer to what we would now call an ecosystem. The company commissioned famous photographers like Edward Steichen and Anton Bruehl for advertising campaigns. It produced keepsake menus designed by notable artists.

The arrival of a White Ship in Honolulu became one of the great ceremonies of mid-century Hawaiian life — known as "Boat Day." As a liner rounded Diamond Head, outrigger canoes, sailboats, and motor launches would escort her past Waikiki Beach. When the ship passed the Royal Hawaiian Hotel, she gave three blasts of her whistle. At the pier, the Royal Hawaiian Band played. Hula dancers performed. Locals offered flower leis and dove into the harbor for coins tossed by passengers. At departure, the band played "Aloha Oe" and passengers threw streamers and leis from the decks — the streamers symbolizing a promise to return.

Then came December 7, 1941. When Pearl Harbor was attacked, the SS Lurline was at sea halfway from Honolulu to San Francisco carrying 765 passengers. She immediately accelerated to maximum speed, altered course, and arrived safely in San Francisco on December 11.

All four White Ships were called to military service, painted wartime gray, their luxurious interiors stripped out and replaced with tiered canvas bunks stacked three high. Each ship could now carry over 4,000 troops. Matson captains and officers remained in command throughout the war. The four liners completed 119 wartime trooping voyages, covered approximately 1.5 million miles, and carried 736,000 troops in both theaters. Beyond its own fleet, Matson served as General Agent for the War Shipping Administration, operating over 100 vessels total. Fifteen Matson ships were sunk during the war.

When peace came, the cost of restoring the liners proved so brutal that Matson was forced to sell the Mariposa and Monterey rather than refurbish them. The Lurline was restored and returned to passenger service, but the golden age was already fading.

Matson briefly experimented with an airline using Douglas DC-4 aircraft after the war, but ceased operations under political pressure from Pan American World Airways — a reminder that in mid-century America, well-connected incumbents could kill competitors through regulatory influence.

By the late 1950s, jet aircraft made the five-day Pacific crossing obsolete overnight. With the advent of routine air travel, Matson's passenger service was greatly diminished, and the last liners were retired by the end of the 1970s. The company sold its hotels — the Royal Hawaiian, the Surfrider, and the Princess Kaiulani passed to Sheraton.

The luxury liner era was over. But it had left Matson with something invaluable: deep institutional knowledge of Pacific logistics, established terminal infrastructure across the ocean, and relationships with every major port between San Francisco and Fiji. The question was whether Matson could find a new reason to exist. The answer was already taking shape in a research lab in San Francisco — and it would transform not just Matson but the entire global economy.

IV. The Containerization Revolution: First in the Pacific (1956–1970)

In the mid-1950s, the American shipping industry was dying. Rising labor costs, foreign competition from cheaper-flagged vessels, and the inherent inefficiency of break-bulk cargo handling — where longshoremen manually loaded individual crates, barrels, and pallets into a ship's hold — made domestic carriers increasingly uncompetitive.

A single ship might sit in port for a week while dockworkers wrestled with thousands of individually shaped items. Pilferage was rampant. Damage was constant. The joke in the industry was that the cost of loading and unloading a ship exceeded the cost of sailing it across the ocean.

To grasp how wasteful the old system was, consider the simple act of shipping a crate of pineapples from Honolulu to San Francisco. A longshoreman would carry the crate from a warehouse to the dock. A crane operator would lower a cargo net into the ship's hold. Other longshoremen, working below deck in cramped, often dangerous conditions, would stack the crate by hand alongside hundreds of other differently shaped items — barrels of molasses, sacks of coffee, canned goods, machinery parts. The process reversed at the destination port. Each touchpoint introduced delay, cost, and risk of damage or theft. Multiply this by thousands of items per ship, and the economics became suffocating.

On the East Coast, a trucking entrepreneur named Malcom McLean was already working on the answer. In April 1956, his company Sea-Land loaded fifty-eight truck-trailer bodies onto a converted oil tanker, the SS Ideal-X, and sailed it from Newark to Houston. It was the birth of container shipping — the idea that cargo should be packed once at its origin into a standardized steel box, and that box should travel by truck, rail, and ship without ever being opened until it reaches its final destination.

What most people do not know is that three thousand miles away, Matson was pursuing the same idea simultaneously — and in some ways, with greater engineering ambition.

In 1956, the same year as McLean's experiment, Matson established an in-house research department — described as the first of its kind in the shipping industry. Its mandate was not to copy McLean but to solve a specific Matson problem: finding the most modern, efficient, and economical means of transporting cargo between the Pacific Coast and Hawaii. This was proactive, engineering-driven planning, not a reaction to a competitor.

The result came on August 31, 1958, when the SS Hawaiian Merchant departed San Francisco carrying twenty containers stacked on deck. It was a hybrid test — the ship still carried conventional break-bulk cargo alongside the containers — but it validated the concept for Pacific service. The twenty-four-foot containers Matson chose were different from McLean's thirty-five-foot boxes, a deliberate engineering decision optimized for Matson's specific routes, ship designs, and Hawaiian port infrastructure.

But Matson's real genius was not the containers themselves — it was everything around them. To handle containers efficiently on shore, Matson developed entirely new machinery. In 1959, the company erected the world's first A-frame gantry crane in Alameda, California. Those towering container cranes visible at every major port on earth today? They are direct descendants of that Alameda prototype.

Matson also introduced the first transtainer and the first straddle carrier in the world, both built to Matson's specifications. The company was not just putting cargo in boxes; it was inventing the entire ecosystem required to make containerization work — the cranes, the yard equipment, the terminal layouts, the information systems.

In April 1960, when the SS Hawaiian Citizen entered service with capacity for 436 twenty-four-foot containers, it became the first all-container carrier in Pacific service — a fully dedicated containership carrying no break-bulk cargo at all.

The productivity transformation was staggering. A typical 1950s vessel carried 10,000 tons at sixteen knots. After containerization, the average vessel carried 40,000 tons at twenty-three knots — four times the cargo at nearly fifty percent higher speed. Port time collapsed from days to hours. Pilferage and damage plummeted. The economics of Pacific shipping were rewritten overnight.

Then Matson pushed further. In 1967, construction commenced on the first containership built from the keel up — not converted from an existing vessel but designed from scratch as a container carrier. The S.S. Hawaiian Enterprise, later renamed Manukai, and her sistership Hawaiian Progress, later renamed Manulani, entered service in 1970. These were purpose-built machines, optimized for a single function. The distinction matters: converting an old ship to carry containers is a compromise. Building a ship designed from scratch for containers is an entirely different level of commitment and efficiency.

Matson's contribution to containerization was significant enough to be featured in a Smithsonian National Museum of American History exhibition addressing the impact of containerization and the historic Mechanization and Modernization Agreement of 1960. That agreement was the landmark labor deal between the International Longshoremen's and Warehousemen's Union and the Pacific Maritime Association that allowed automation in exchange for guaranteed wages and benefits for displaced workers. Matson's role in forcing that negotiation — by demonstrating that containerization was inevitable — was pivotal.

In 1970, Matson made a decision that would define the company for the next five decades: it sold its passenger vessels and suspended its Far East service to concentrate exclusively on Pacific Coast-Hawaii freight service.

The company that had built the White Ships, created Hawaiian tourism, and operated luxury hotels was now a pure-play containerized freight carrier. It was a radical simplification — the kind of strategic clarity that sounds obvious in retrospect but requires nerve in the moment. Matson bet that being the best at one thing was more valuable than being adequate at many things. That bet paid off spectacularly, because the containerized Pacific freight business was about to become essential infrastructure protected by federal law.

V. Corporate Structure Evolution: The Alexander and Baldwin Years (1908–2012)

To understand why Matson spent four decades as a subsidiary — and why its eventual liberation mattered so much — you need to understand Hawaii's "Big Five."

For most of the twentieth century, five companies effectively controlled the Hawaiian economy: Alexander and Baldwin, Castle and Cooke, C. Brewer and Co., American Factors, and Theo H. Davies. These firms dominated sugar plantations, shipping, banking, and retail. They were not just businesses; they were the governing architecture of an island territory.

If you wanted to grow sugar, ship sugar, sell goods, or build anything in Hawaii, you dealt with the Big Five. Their influence extended into politics, land ownership, and social institutions. The Big Five were to territorial Hawaii what the zaibatsu were to prewar Japan — interlocking conglomerates that blurred the line between private enterprise and public governance.

Alexander and Baldwin first invested $200,000 in Matson Navigation Company in 1908 — a natural move, since A&B was one of Hawaii's largest sugar producers and Matson was already carrying most of A&B's freight. Owning a stake in your shipper gave you leverage over the supply chain that was the lifeblood of your plantation empire.

In 1964, A&B consolidated its position by buying out the Matson stakes held by three fellow Big Five members — American Factors, C. Brewer, and Castle and Cooke. And in 1969, A&B purchased all remaining outstanding shares, making Matson a wholly owned subsidiary.

For the next forty-three years, Matson operated inside A&B's diversified conglomerate structure. There were genuine benefits: A&B provided capital stability, a guaranteed understanding of the Hawaiian market, and patient ownership that could absorb the cyclical nature of shipping. A&B's long time horizons — measured in plantation cycles and real estate development timelines — were well-suited to a business that required massive upfront capital for ships that would operate for decades.

But the constraints were equally real. Matson's capital allocation decisions were subordinate to A&B's broader portfolio. Investment opportunities in new ships, new routes, or acquisitions had to compete with A&B's real estate developments and agricultural operations for corporate capital.

From an investor's perspective, Matson was invisible — its earnings were blended into a diversified holding company, making it impossible to value the shipping business on its own merits. Analysts covering A&B had to assess Hawaiian sugar plantations, Honolulu real estate, and Pacific Ocean freight simultaneously — an awkward combination that likely resulted in a persistent conglomerate discount.

Through the 1970s, 1980s, and 1990s, Matson continued modernizing its fleet within this structure, building out its containerized Hawaii service. In 1987, the company established Matson Intermodal System (later renamed Matson Logistics) to arrange rail and truck transportation across North America — a prescient move that would become strategically important decades later.

Meanwhile, A&B itself was transforming. As Hawaii's sugar industry declined — crushed by foreign competition, rising labor costs, and the repeal of sugar subsidies — A&B gradually pivoted from agriculture to real estate development, leveraging its vast Hawaiian land holdings into commercial and residential projects. By the 2000s, A&B was more of a real estate company that happened to own a shipping line than the sugar-and-shipping conglomerate it had been for most of the twentieth century. The two businesses were drifting apart in every meaningful sense.

The company was profitable and essential, but it was also a division, not a company — capable but constrained, like a thoroughbred tethered to a plow. The question of what Matson could become on its own would not be answered until a boardroom decision in late 2011 changed everything.

VI. Independence and Strategic Repositioning: The Spinoff (2012)

On December 1, 2011, Alexander and Baldwin's board approved what had become increasingly obvious to both companies: A&B and Matson were better off apart.

A&B had evolved into a company running two fundamentally different businesses — ocean transportation and logistics on one hand, Hawaiian real estate and agriculture on the other. They had different capital requirements, different investor profiles, different growth trajectories, and different management imperatives. Bundling them together created a conglomerate discount that served neither business well.

The logic was straightforward but the execution was complex. The parent entity was Alexander and Baldwin Holdings, Inc. Under the spinoff terms, Holdings shareholders received one share of the new Alexander and Baldwin, Inc. (ticker: ALEX) for every share they held, while the transportation business became the independent Matson, Inc. A&B would reinvent itself as a Hawaii-focused real estate investment trust. Matson would stand alone as a publicly traded shipping company for the first time in over four decades.

The separation was completed on June 29, 2012, at 4:00 p.m. Eastern time. Regular-way trading began on July 2. Matson's headquarters moved from Oakland, California, to Honolulu. Matthew J. Cox became CEO, with Walter Dods as chairman.

The choice of Honolulu was more than symbolism. By headquartering in Hawaii, Matson signaled to its customers, employees, and the island community that it was a Hawaiian company, not a mainland corporation that happened to serve Hawaii. This mattered enormously in a market where the company's social license to operate depended on being perceived as a community partner rather than an outside monopolist.

The Hawaiian identity — the concept of "ohana," or family, that Matson emphasizes in its corporate culture — was not just branding. It was a strategic asset in a market where public sentiment could influence regulatory outcomes. If islanders view Matson as a trusted neighbor rather than a distant corporate landlord, the political coalition supporting the Jones Act — and by extension, Matson's competitive moat — grows stronger.

After forty-three years as a subsidiary, Matson was a public company again. The spinoff unlocked several capabilities that had been constrained under A&B's umbrella. Capital allocation became Matson's own decision — management could invest in fleet renewal, pursue acquisitions, and return cash to shareholders without competing against a parent company's real estate ambitions.

The company could issue its own debt on terms reflecting its specific credit profile. It could use its stock as acquisition currency. And it could attract investors specifically interested in Jones Act shipping economics rather than forcing them to buy a diversified Hawaiian conglomerate.

The market noticed. In its first years as an independent company, Matson attracted a shareholder base that understood capital-intensive infrastructure businesses — a very different investor profile from the real-estate-focused shareholders who had owned A&B. The stock began to trade on its own fundamentals for the first time: fleet age and efficiency, route profitability, container volumes, and the durability of the Jones Act moat.

More important than the financial engineering was the psychological shift. Under A&B, Matson had been managed as a stable cash generator — essential but not exciting. As an independent company, the management team under Matt Cox began thinking in terms of growth. Where could Matson's Pacific expertise be applied beyond its traditional markets? What adjacencies made strategic sense? How could the company leverage its Jones Act protections into a larger platform?

The answers came fast: Alaska, the South Pacific, and — most consequentially — China. The spinoff had set Matson free, and the company was about to embark on the most aggressive expansion in its modern history.

VII. Geographic Expansion: Building the Pacific Network (2013–2016)

Within a year of going public, Matson began executing an expansion strategy that would roughly double the geographic scope of its operations in three years. The speed was notable for a company that had operated the same Hawaii routes for over a century. Independence, it turned out, was a catalyst for ambition.

The first move was the South Pacific. In late 2013, Matson launched Matson South Pacific by acquiring the assets of Reef Shipping, an Auckland-based carrier that had operated since 1968 before falling into receivership. With four vessels and approximately 1,500 pieces of container equipment, Matson began serving a network of Pacific island nations that were entirely new territory: Nauru, the Solomon Islands, Tahiti, Samoa, the Cook Islands, Niue, Tonga, Wallis and Futuna, Vanuatu, Tarawa, and Majuro.

These were tiny markets individually, but collectively they extended Matson's Pacific expertise into the deep South Pacific and reinforced the company's identity as the carrier that keeps island economies alive. Matson later partnered with Swire Shipping to jointly serve parts of the network, sharing risk and capacity on some of the thinnest routes.

But the transformative acquisition was Alaska.

On May 29, 2015, Matson completed the purchase of Horizon Lines' Alaska operations for $469 million — paying approximately $69 million in equity for the shares and assuming or repaying all of Horizon's outstanding debt. The deal brought three diesel-powered Jones Act containerships, two weekly sailings from Tacoma to Anchorage and Kodiak, one weekly sailing to Dutch Harbor, and terminal operations at all three Alaska ports.

The strategic logic was compelling. Alaska is, in many ways, Hawaii's mirror image: a non-contiguous U.S. state separated from the mainland, dependent on ocean shipping for the vast majority of its consumer goods, and protected by the same Jones Act requirements. The demographics were different — Alaska's economy runs on oil, fishing, and military installations rather than tourism and agriculture — but the underlying dynamic was identical. Isolated American communities needed reliable, frequent container service, and the Jones Act ensured that only U.S.-built, U.S.-flagged, U.S.-crewed vessels could provide it.

Horizon Lines had been struggling financially for years — the company had pleaded guilty to antitrust charges in 2011 for price-fixing on the Puerto Rico trade lane, and its balance sheet was deteriorating. When Matson came calling, Horizon sold its Hawaii assets to The Pasha Group for $141.5 million and its Alaska operations to Matson. After the deal closed, Horizon Lines ceased to exist as a standalone entity.

Integration costs ran $45-50 million, but the strategic value was clear. The acquisition added roughly thirty percent to Matson's domestic containerized freight business and created a platform that management would later leverage in unexpected ways — including a "backhaul" business connecting Dutch Harbor to Asian ports for seafood exports.

The following year, Matson deepened its Alaska position with a move that illustrated the power of vertical integration in niche logistics markets.

In August 2016, Matson Logistics acquired Span Alaska Transportation for $197.6 million. Founded in 1978 and headquartered in Auburn, Washington, Span Alaska was an asset-light logistics business that aggregated customers' freight, consolidated it, and shipped it to seven terminals throughout Alaska for deconsolidation and delivery.

Here is the key detail: Span Alaska had been Matson's single largest northbound freight customer to Alaska for over thirty years. The acquisition vertically integrated Matson's Alaska business — the company now controlled both the ocean carrier leg and the inland freight consolidation leg. Span Alaska's estimated annual EBITDA was approximately $21 million, making the deal immediately accretive at roughly nine times EBITDA.

Also in 2013, Matson added International Supply Chain Services to its logistics offering, building out capabilities that would eventually support the China service with end-to-end supply chain management.

In three years, Matson had gone from a newly independent company with a century-old Hawaii franchise to a diversified Pacific carrier with operations spanning from the South Pacific to the Arctic. But the biggest strategic bet was still ahead — one that would take Matson into the world's most dynamic and volatile trade lane.

VIII. The China Pivot: Building CLX and Transpacific Dominance (2005–2025)

Around 2006, Matson did something that seemed counterintuitive for a Jones Act-protected domestic carrier: it launched a container service from China to Long Beach, California. This was foreign trade, not domestic — meaning no Jones Act protection, no regulatory moat, no guaranteed market position. Matson would be competing against the largest container lines on earth: Maersk, MSC, COSCO, Evergreen — carriers operating vessels five to ten times larger than anything in Matson's fleet. On paper, it looked like a minnow swimming into shark-infested waters.

But Matson was not competing on volume. It was competing on speed.

The China-Long Beach Express, or CLX, was designed from the outset as a premium expedited service: ten-day transit time from Shanghai to Long Beach, with industry-leading on-time arrival performance and next-day cargo availability. Traditional ocean carriers offered transit times of fourteen to eighteen days at lower prices. Matson offered to get your containers there faster, more reliably, and with seamless intermodal connections through Matson Logistics for last-mile delivery.

Think of it this way: most transpacific carriers are the equivalent of economy airlines — they compete on price, cram as much cargo as possible onto the largest ships they can build, and accept that some shipments will be late. Matson positioned itself as the business-class option. It charged a premium, but it delivered consistency.

For importers of time-sensitive goods — seasonal apparel, consumer electronics, perishable merchandise — the premium was worth paying because late-arriving inventory was worse than expensive inventory. A container of winter coats that arrives after the selling season is worth nothing; a container that arrives a week early at a ten percent premium is worth everything.

The CLX grew steadily through the 2010s, and Matson added a second weekly string, the CLX+, to provide two departures per week from China. The service expanded from Shanghai to include Xiamen and Ningbo as origin ports, broadening the catchment area for shippers across eastern China.

Then came 2020, and the pandemic turned Matson's China service into a profit engine of extraordinary power.

When COVID-19 shut down economies worldwide and then triggered an unprecedented surge in consumer spending on goods — PPE, cleaning products, home improvement supplies, electronics for remote work, and above all, e-commerce — container shipping capacity became the scarcest commodity on earth. Major ports backed up with ships waiting weeks to berth. Mainline carriers were unreliable, their schedules shattered by congestion and disruption.

In Q2 2020, Matson more than doubled its China service by chartering several additional containerships to meet demand. CEO Matt Cox told investors the company was "turning away — each week — more cargo than we are carrying." The enlarged service operated at full capacity and carried 125 percent more containers compared to the prior year. By management's estimate, at least four to six years of e-commerce growth occurred in a single year.

In September 2020, Matson launched yet another service: the Alaska-Asia Express, or AAX, with its inaugural voyage from Dutch Harbor carrying Alaskan seafood — primarily salmon and pollock — to Ningbo and Shanghai. The AAX created a "backhaul" business from Dutch Harbor, leveraging ships that would otherwise have returned to Asia empty after delivering goods to Alaska. It connected to over thirty-seven Asian cities through Matson's partner network.

The Alaska acquisition had created an entirely new revenue stream that nobody had anticipated at the time of the Horizon deal — a compelling example of how strategic acquisitions can create optionality that is not visible at the time of purchase.

In February 2024, Matson rebranded CLX+ as the Matson Asia Express, or MAX, to more clearly distinguish its two China services. The China business had become a critical part of Matson's revenue and earnings profile — and, inevitably, its volatility profile as well.

That volatility arrived in force starting in late 2024 and accelerating through 2025. As U.S.-China trade tensions escalated and tariffs on Chinese goods climbed to 145 percent, Matson's China volumes declined significantly — down 14.6 percent year-over-year at peak tariff impact. Spot rates spiked in June 2025 then retreated rapidly in July, creating severe planning uncertainty. The traditional back-to-school and holiday pre-stocking peak season was described as "muted."

Full-year 2025 net income came in at $444.8 million on EBITDA of $704.7 million, with operating cash flow of $547.1 million — solid by any normal standard but down from the prior year, with the China service bearing the brunt.

Matson responded by pursuing a "catchment basin" strategy — diversifying sourcing beyond China to include Vietnam, India, and Thailand. Some customers had already shifted origins, partially supporting volumes even as China-specific shipments declined. But the experience underscored a fundamental tension: the China service added growth and optionality, but it also introduced earnings volatility that the protected domestic routes never produced.

IX. Fleet Modernization and the Green Transition (2013–Present)

Building a ship in the United States is spectacularly expensive. Under the Jones Act, every vessel operating between American ports must be built in an American shipyard — and American shipyards charge roughly five times what their South Korean or Chinese counterparts charge for comparable vessels. A containership that might cost $60 million in a Korean yard costs $150-200 million or more when built in Philadelphia or San Diego.

This is the price of the Jones Act moat: the same law that keeps foreign competition out of Matson's domestic markets also forces Matson to pay a massive premium for its own ships.

Matson has leaned into this constraint rather than fighting it, turning fleet modernization into a competitive weapon. The logic is counterintuitive but sound: if new ships are prohibitively expensive for everyone, then the company that can actually afford to build them gains a structural cost advantage over competitors operating aging fleets. Each new vessel is simultaneously a capital expenditure and a competitive barrier.

In 2013, the company ordered two 3,600-TEU containerships from Philly Shipyard — the Aloha Class vessels that would become the largest containerships ever built in the United States. The Daniel K. Inouye, named for the late Hawaii senator and legendary advocate of the U.S. Merchant Marine, was delivered in 2018. Her sistership Kaimana Hila — Hawaiian for Diamond Head — followed in 2019. Combined cost: approximately $400 million.

To put that in perspective, $400 million was roughly one-quarter of Matson's total market capitalization at the time of the order — a bet of extraordinary scale relative to the company's size.

Simultaneously, Matson ordered two Kanaloa Class combination container and roll-on/roll-off vessels from General Dynamics NASSCO in San Diego. These Con-Ro ships — named Lurline and Matsonia, carrying forward the most iconic names in Matson history — were the largest vessels of their type ever built in the United States at 870 feet long. They carried capacity for 3,500 TEUs and an enclosed garage for approximately 500 vehicles. They entered service in 2019 and 2020, featuring Tier 3 dual-fuel engines capable of running on liquefied natural gas.

All four new ships arrived with green technology that represented a generational leap: fuel-efficient hull designs, double-hull fuel tanks, fresh water ballast systems, and the dual-fuel engines. Modern hull designs and engine technology reduce fuel consumption substantially on routes that Matson's ships traverse thousands of times over their operational lives.

In 2022, Matson placed its most ambitious order yet: three additional LNG-fueled Aloha Class containerships from Philly Shipyard for approximately $1 billion, with deliveries now underway in 2026 and extending into 2027. These vessels will replace older, less efficient ships in Matson's Hawaii fleet. The company also committed approximately $130 million to retrofit existing vessels to run on LNG.

To understand why LNG matters, consider the fuel economics. Traditional marine diesel — heavy fuel oil, or bunker fuel — is among the dirtiest fuels in commercial use. LNG, while still a fossil fuel, burns significantly cleaner, producing roughly 25 percent less carbon dioxide, virtually no sulfur oxides, and far fewer particulate emissions. For a fleet that burns millions of gallons per year crossing the Pacific, the fuel savings and emissions reductions compound over the decades-long life of each vessel. LNG also positions Matson ahead of tightening International Maritime Organization emissions regulations, avoiding the costly scrubber retrofits that competitors running older ships must undertake.

Matson has set a target of 40 percent reduction in Scope 1 greenhouse gas fleet emissions by 2030, measured against a 2016 baseline, and net zero Scope 1 emissions by 2050. These are ambitious goals in an industry where ships burn heavy fuel oil by the thousands of tons, but the fleet renewal program is the primary mechanism for achieving them.

The capital intensity is striking but strategically coherent. Over roughly a decade, Matson will have invested well over $2 billion in new vessels — for a company with annual revenues of approximately $3.4 billion. No rational competitor would spend $1 billion to enter a market that Matson already dominates with newer, more efficient ships. The fleet renewal program is not just about operating costs and emissions; it is about raising the barriers to entry to a level that makes competitive challenge virtually unthinkable.

X. The Business Model: Protected Routes, Premium Service

Matson's business rests on a legal framework that is simultaneously elegant and controversial: the Jones Act.

Formally known as the Merchant Marine Act of 1920, the Jones Act requires that all goods transported by water between U.S. ports must be carried on vessels that are U.S.-built, U.S.-flagged, at least 75 percent U.S.-owned, and crewed by at least 75 percent U.S. citizens or permanent residents.

Think of it as a four-pronged protectionist shield: foreign carriers — even the most efficient ones — cannot legally carry a single container between Los Angeles and Honolulu, or between Tacoma and Anchorage, or between any two American ports.

For Matson, this means the domestic routes — Hawaii, Alaska, Guam, and Micronesia — operate in a market with almost no foreign competition. In Hawaii, only Matson and Pasha Hawaii operate, creating an effective duopoly. In Alaska, Matson and TOTE Maritime Alaska are the primary Jones Act carriers. These are not markets where a new competitor can emerge by registering a foreign-flagged ship — anyone wanting to enter must build ships in American yards at American prices, hire American crews at American wages, and invest in terminal infrastructure at American ports.

Critics — including the Grassroot Institute of Hawaii, the Cato Institute, and the Pacific Legal Foundation — argue that the Jones Act costs Hawaii consumers approximately $1.2 billion per year, or roughly $1,800 per average family, because the lack of competition inflates shipping costs that are passed through to consumer prices. A 2025 lawsuit challenged the Jones Act's constitutionality, and Matson intervened to oppose.

Supporters counter that the Jones Act maintains U.S. shipbuilding capacity, preserves maritime jobs, and ensures a domestic fleet is available for national defense — arguments that carry significant weight with both parties on Capitol Hill. The political durability of the Jones Act is notable: despite decades of criticism from economists, the law has survived intact because the coalition supporting it — shipbuilders, maritime unions, defense hawks — is broader and more politically organized than the coalition opposing it.

The company operates in two segments. Ocean Transportation, the core business, offers containerized freight service to the domestic non-contiguous markets plus the China transpacific routes. Matson Logistics extends the network with domestic and international rail intermodal service, highway brokerage, warehousing, supply chain services, and LTL transportation. The logistics segment is asset-light and margin-accretive, providing the inland distribution capability that makes Matson a door-to-door solution rather than just a port-to-port carrier.

The revenue mix tells the strategic story. Protected domestic routes — Hawaii, Alaska, Guam — provide stability and predictable cash flows. The China service provides growth optionality and earnings upside in strong markets, but introduces the volatility that comes from competing on unprotected trade lanes. Management's challenge is balancing these two dynamics — allocating enough capital to defend and modernize the domestic franchise while investing in the China service's growth potential without overexposing the company to trade-lane-specific risks.

There is a useful analogy here: think of Matson's domestic routes as a bond portfolio — steady, predictable, and protected from default — and the China service as an equity overlay — higher return potential but with meaningful drawdown risk. The art of managing Matson is getting the portfolio mix right.

The customer base reflects Matson's essential-infrastructure role. Retailers in Hawaii and Alaska depend on Matson for inventory replenishment. The U.S. military relies on Matson for cargo delivery to Pacific installations. Consumer goods manufacturers use the logistics network for distribution. For many of these customers, Matson is not a vendor they evaluate periodically — it is embedded infrastructure, as fundamental to their operations as the electrical grid or the water system.

The culture matters too, though it is harder to quantify. Matson's Honolulu headquarters, its Hawaiian identity, its concept of employee "ohana," and its deep community involvement in the markets it serves — these reflect a company that understands its social license to operate depends on being perceived as a responsible steward, not a monopolist extracting rents. In markets where you are the essential provider and the alternative is empty shelves, reputation is not optional — it is a strategic asset.

XI. Strategic Framework Analysis: Competitive Position and Structural Advantages

Understanding Matson requires examining the structural forces that shape its competitive position — both the external pressures that could threaten the business and the internal advantages that protect it.

Start with the threat of new entrants, which is effectively nonexistent for Matson's domestic routes. The Jones Act creates what might be the most impregnable barrier to entry in American business. A potential competitor would need to spend upward of $1 billion to build Jones Act-compliant ships in the limited number of qualified U.S. shipyards, then invest hundreds of millions more in terminal infrastructure, hire and train American crews, and build customer relationships in markets where Matson has operated for over a century.

The economics simply do not work. Even if a competitor could raise the capital, the addressable market in Hawaii and Alaska is not large enough to support a third major carrier profitably. The China service is a different story — it is open to foreign competition — but Matson's premium niche positioning insulates it from direct rate wars with the massive Asian alliances.

The bargaining power of Matson's suppliers is moderate but concentrated. There are only a handful of U.S. shipyards capable of building Jones Act vessels — Philly Shipyard and General Dynamics NASSCO are the primary options — which gives those yards meaningful pricing power. When Matson needs a new ship, it cannot shop globally for the lowest bid; it must work with one of these few yards at whatever price the yard demands.

Fuel costs are significant and volatile but affect all carriers equally and are typically passed through to customers via fuel surcharges. Labor unions represent Matson's crews, but these relationships have been stable for decades.

On the customer side, bargaining power is low for the domestic routes and moderate for the China service. In Hawaii and Alaska, Matson is essential infrastructure — retailers, military installations, and consumers have few if any alternatives. Switching costs are high because customers have integrated Matson's schedules into just-in-time inventory systems. For the China service, customers have more options but tend to value Matson's speed and reliability premium.

The threat of substitutes is minimal. For domestic routes, air freight is prohibitively expensive for most cargo categories, and there are no other ocean options. There is no substitute at all for the "lifeline" service to island economies — no pipeline, no bridge, no alternative mode of transport can replace ocean shipping to Hawaii, Alaska, or Guam.

Through the lens of Hamilton Helmer's Seven Powers framework, Matson's strongest advantage is what Helmer calls "cornered resource" — the Jones Act protection combined with terminal infrastructure and brand equity built over 140 years. This is not a competitive advantage that can be replicated or worked around; it is a structural feature of the market itself. The Jones Act is the shipping equivalent of a broadcast license in the pre-cable era: a government-granted right to operate that competitors simply cannot obtain.

The second strongest power is switching costs. Customers who have built their supply chains around Matson's schedules face real disruption risk if they attempt to change carriers, particularly on routes where alternatives are scarce. A Hawaii retailer who switches from Matson to Pasha faces weeks of adjustment — and if the transition goes wrong, the result is empty shelves in a market with no backup plan.

Matson's brand power — 140 years as the trusted Pacific lifeline with industry-leading on-time performance — functions as a third significant advantage. In markets where service failure means empty grocery shelves or delayed military supplies, reliability is not a differentiator; it is an existential requirement.

Counter-positioning also works in Matson's favor, particularly in the China service. Large Asian carriers are optimized for volume at low cost — they operate mega-ships carrying 20,000 or more TEUs. Matson deliberately operates smaller ships at higher speed with superior reliability. For a large carrier to replicate Matson's model, it would have to deploy expensive small vessels on a niche route, cannibalizing its existing business. This structural disincentive protects Matson's premium position.

Process power — the accumulated operational know-how from seventy years of containerization experience, terminal management, refrigerated cargo handling, and Pacific weather routing — rounds out the picture. This is the kind of advantage that does not show up on a balance sheet but manifests in on-time arrival rates, cargo damage statistics, and customer retention. Matson's institutional knowledge of Pacific shipping is deep enough that competitors cannot simply hire it away; it is embedded in systems, procedures, and organizational culture built over decades.

The competitive landscape varies dramatically by market. In Hawaii, Pasha Hawaii is the only direct competitor. In Alaska, TOTE Maritime Alaska runs roll-on/roll-off vessels on partially overlapping routes. In China, the competitive set includes ZIM (the most similar in premium positioning), Evergreen, Yang Ming, COSCO/OOCL, MSC, and Maersk — all operating at vastly greater scale but without Matson's speed advantage on the Southern California lane.

The overall assessment is that Matson occupies a rare strategic position: a regulated near-monopoly on essential domestic routes, supplemented by a premium niche position on competitive international routes. The domestic business provides stability and downside protection; the China business provides growth and upside optionality. The risk is that these two businesses have fundamentally different risk profiles, and managing them within a single company requires balancing competing capital allocation priorities.

XII. Current State and Recent Performance (2024–2025)

The numbers from 2024 tell the story of a company that benefited from strong market conditions across multiple fronts. Full-year revenue reached $3.42 billion, up 10.6 percent from $3.09 billion in 2023. Net income surged to $476.4 million, up over 60 percent year-over-year — a remarkable acceleration for what many investors consider a utility-like business.

In the fourth quarter alone, Matson earned $128.0 million, or $3.80 per diluted share — more than double the $62.4 million earned in Q4 2023 — on revenue of $890.3 million.

The China service was the primary earnings engine. The CLX and MAX services benefited from elevated freight rates and strong demand as importers pulled forward inventory ahead of anticipated tariff increases. The dynamic was almost self-reinforcing: the threat of tariffs accelerated demand, which tightened capacity, which raised rates, which boosted earnings.

The domestic routes performed steadily, contributing their characteristic stable cash flows. Matson also received a one-time $118.6 million federal tax refund in Q2 2024, boosting cash flow further. The SSAT terminal joint venture contributed $9.3 million in Q4 2024.

But 2025 brought a sharply different environment. As U.S.-China trade tensions escalated and the tariff wall rose, the front-loading effect reversed: importers who had overstocked in 2024 pulled back in 2025, and new orders from China declined as brands shifted sourcing or simply waited for clarity.

China volumes fell 14.6 percent year-over-year at peak tariff impact. A temporary U.S.-China tariff truce in late Q2 2025 provided a brief demand rebound, but the recovery was uneven. Full-year 2025 net income came in at $444.8 million — down about seven percent from 2024 but still strong by historical standards. Q4 2025 earnings per share of $4.60 beat analyst consensus estimates, and operating cash flow remained robust at $547.1 million despite the headwinds.

Capital expenditures rose to $393.4 million as the Philly Shipyard newbuild program consumed increasing cash. Yet even in a down year for the China service, Matson's domestic routes — Hawaii, Alaska, Guam — held firm. Container volumes on those routes were roughly stable, freight rates moved in line with contractual escalators, and the lifeline business did exactly what it is supposed to do: provide a steady baseline while the more volatile international business adjusts to external shocks.

That stability-volatility split is the central dynamic that investors need to understand: Matson's earnings profile is not as utility-like as the domestic route dominance might suggest. The China service — accounting for a meaningful share of total operating income — introduces cyclicality that can swing consolidated results by hundreds of millions of dollars year to year. The protected domestic business provides a floor, but the China business can raise or lower the ceiling substantially.

Management has responded with the "catchment basin" strategy, encouraging customers to diversify sourcing beyond China. Some volume has already shifted, partially offsetting China-specific declines. But the strategy carries execution risk: Matson's speed advantage is route-specific, and it is unclear whether the ten-day premium that commands pricing power from China to Long Beach translates equally to shipments originating elsewhere in Asia.

XIII. Bull vs. Bear Case and Investment Considerations

The investment case for Matson is fundamentally a question about what kind of company this is — and what kind of returns investors should expect.

The bull case begins with the Jones Act, which creates a competitive position that is almost without parallel in American business. Approximately seventy percent of Matson's revenue comes from domestic routes where foreign competition is legally prohibited and where the barriers to domestic entry are measured in billions of dollars. Hawaii, Alaska, and Guam are not discretionary markets — people live there, military installations operate there, and every essential good arrives by ship. Matson's service on these routes is not a business; it is infrastructure. And infrastructure that is both essential and protected tends to compound value over very long periods.

Fleet modernization enhances this position. The billion-dollar-plus investment in new Aloha Class vessels will lower per-unit fuel costs, reduce maintenance expenses, and position the fleet to meet tightening environmental regulations.

The China service adds growth optionality. E-commerce penetration continues to rise, and the demand for fast, reliable transpacific shipping persists even as specific trade lanes shift with tariff policy. Matson's ten-day transit time is a structural speed advantage that mainline carriers cannot easily replicate without sacrificing their economies of scale.

Management under Matt Cox — who has led the company since the 2012 spinoff — has demonstrated disciplined capital allocation: fleet renewal, targeted acquisitions, consistent dividends, and share buybacks. Cox's 2025 compensation of approximately $6.49 million is notable for being modest by public company CEO standards, reflecting a culture that values operational stewardship over headline pay packages.

The bear case, however, is equally substantive.

The regulated-utility characteristics of the domestic business impose a natural ceiling on growth. Hawaii's population has been roughly flat for years. Alaska's economy is tied to oil prices and fishing quotas. These are stable markets, not growing ones.

The China service introduces earnings volatility that is difficult to forecast and impossible to control. Tariff policy, geopolitical tensions, consumer spending patterns, and the behavior of Asian carrier alliances all influence Matson's China results, and none of these factors are within management's control. The 2025 experience — where China volumes dropped nearly fifteen percent — demonstrated how quickly the growth engine can decelerate.

Capital intensity is a permanent feature. The Jones Act requirement to build in American shipyards means Matson pays a massive premium for its vessels. If the Jones Act were ever reformed or repealed, the economics of those vessels would change dramatically. Jones Act repeal remains a low-probability but high-impact tail risk — one that has been discussed for decades without gaining serious legislative traction, but that deserves acknowledgment.

Environmental regulation is another overhang. Matson's LNG-capable fleet is well-positioned relative to current competition, but the maritime industry's long-term decarbonization pathway remains uncertain. If regulators ultimately mandate fuels beyond LNG, the transition costs could be substantial, and Matson's current LNG investment could become a stranded intermediate step.

The two metrics that matter most for tracking Matson's ongoing performance are: container volume by trade lane (Hawaii, Alaska, China — which reveals demand trends in each market and the relative contribution of protected versus unprotected revenue) and average freight rates on the China service (which captures pricing power and competitive dynamics on the trade lane that drives earnings volatility).

Together, these two indicators tell investors whether the domestic foundation is stable and whether the China growth engine is running hot, cold, or somewhere in between. Everything else — operating margins, capital deployment, fleet utilization — flows from these two fundamental drivers.

XIV. Lessons and Takeaways

Matson's 144-year arc from a Swedish orphan's schooner to a multi-billion-dollar shipping company offers lessons that extend well beyond the maritime industry.

For operators, the most important insight is that protected markets require service excellence, not just regulatory capture. The Jones Act gives Matson a legal monopoly on its domestic routes, but monopoly status alone does not guarantee durable value creation. Matson has invested continuously in fleet modernization, terminal infrastructure, and service reliability — not because competition forces it to, but because its social license to operate in small island economies depends on being perceived as a responsible essential provider rather than a rent-seeking monopolist.

Companies that rely on regulatory protection without investing in operational quality eventually find that protection eroded through political action. Matson's decades-long commitment to on-time performance and fleet renewal is not generosity — it is strategic self-preservation.

The geographic expansion strategy offers another lesson: grow into adjacencies that leverage your core competency. Matson's move from Hawaii to Alaska, from Hawaii to the South Pacific, and from domestic to China service all followed the same logic — Pacific maritime expertise applied to new but structurally similar markets.

The Alaska acquisition worked because Alaska's logistics challenges mirror Hawaii's. The China service worked because Matson's operational discipline in speed and reliability translated directly to premium positioning on the transpacific lane. Each expansion was a horizontal extension of the same capability rather than a diversification into unrelated territory.

The containerization story illustrates that innovation can emerge from regulated industries. Matson's 1956 research department and its subsequent pioneering of container shipping in the Pacific happened not despite the company's protected market position but partly because of it. The stable revenue base from Hawaii service gave Matson the financial cushion to invest in R&D without the short-term earnings pressure that might have forced a less-protected competitor to defer innovation. Protection, paradoxically, enabled risk-taking.

For investors, the central lesson is the difference between monopoly economics and monopoly returns. Matson's domestic routes have monopoly characteristics — limited competition, essential service, regulatory barriers — but the capital intensity of the business means that returns on invested capital must be evaluated carefully. Every new ship costs hundreds of millions of dollars and depreciates over decades.

The cash flow characteristics of a shipping company are fundamentally different from those of an asset-light technology platform, even if the competitive dynamics appear similarly favorable. The margin of safety in a capital-intensive business lies in the durability of the competitive position, the discipline of capital allocation, and management's willingness to resist overinvestment during boom periods.

Matson's mix of protected and exposed markets creates a risk-return profile that is unusual in the shipping industry. The domestic routes provide a floor under earnings — the kind of predictable cash generation that supports dividends and fleet investment through cycles. The China service provides a ceiling that can be very high in strong markets and much lower in weak ones.

What makes Matson genuinely special is the combination of a business that is essential to the communities it serves, a regulatory framework that protects its market position, and a management culture that has consistently reinvested in capability rather than resting on its protected status. From William Matson's cold-storage innovations in the 1890s to the containerization revolution of the 1960s to the LNG-capable fleet of the 2020s, the company has treated its moat not as a permission to stagnate but as a foundation for continuous improvement.

XV. Future Outlook

The near-term catalyst for Matson is concrete and visible: three new Aloha Class containerships, built at Philly Shipyard for approximately $1 billion, are in the process of delivery through 2026 and into 2027. These LNG-fueled vessels will replace older, less efficient ships in the Hawaii fleet, lowering per-unit operating costs and reducing emissions.

When the fleet transition is complete, Matson will operate one of the youngest and most fuel-efficient fleets of any Jones Act carrier — a meaningful cost advantage that compounds over the twenty-to-thirty-year life of each vessel.

The sustainability transition extends beyond individual ships. Matson's 40 percent emission reduction target by 2030 and net zero goal by 2050 will require continued investment in cleaner fuels and potentially new propulsion technologies. The company's early commitment to LNG positions it ahead of carriers still operating conventional diesel fleets, but the long-term regulatory environment remains uncertain.

Strategically, the "catchment basin" approach to diversifying beyond China represents Matson's most important near-term commercial initiative. As global supply chains redistribute across Southeast Asia — Vietnam, India, Thailand, and other origins — Matson's expedited transpacific services could capture share of these shifting trade flows. The underlying demand for fast, reliable shipping from Asia to the U.S. West Coast is unlikely to disappear even if China-specific volumes decline.

The logistics segment offers growth potential that does not require the capital intensity of ocean transportation. As Matson Logistics expands its intermodal, warehousing, and supply chain service offerings, the segment could become a larger contributor to consolidated earnings — particularly if paired with the ocean network to offer end-to-end supply chain solutions that foreign carriers cannot replicate on domestic legs.

Leadership transition represents both an opportunity and a risk. Matt Cox has led Matson since the 2012 spinoff and presided over the company's transformation from a newly independent Hawaii carrier to a diversified Pacific logistics company. The next generation of leadership — including recent executive appointments like EVP of Operations Vic Angoco, EVP and President of Matson Logistics Jerome Holland, and SVP of Alaska Jennifer Tungul — will need to maintain the strategic discipline and operational culture that Cox built.

Geopolitical risk looms as both threat and opportunity. Escalating U.S.-China tensions could further depress China trade volumes, but they could also accelerate supply chain diversification into markets that Matson is positioning to serve. Climate change introduces physical risks to Pacific routes but also potential regulatory tailwinds for companies that have invested in cleaner fleets.

There is also the question of military logistics. The U.S. Department of Defense has increasingly relied on commercial carriers for Pacific sealift capability, and Matson's Jones Act fleet — U.S.-built, U.S.-crewed, and already operating in the Pacific — represents a strategic asset that goes beyond commercial value. In a world of rising great-power competition in the Pacific, Matson's fleet is not just a business asset; it is a national security resource. That geopolitical dimension adds a layer of political protection to the Jones Act framework that purely commercial arguments would not provide.

The enduring question for Matson is whether the company can maintain its premium positioning as the shipping industry continues to commoditize. The Jones Act protects the domestic routes, but the China service depends on a speed-and-reliability advantage that competitors could narrow over time. Matson's answer, historically, has been continuous investment in ships, terminals, technology, and customer relationships — the same formula that has worked since William Matson sailed the Emma Claudina into Hilo Bay at dawn, 144 years ago.

XVI. Further Reading

For those looking to go deeper into Matson's story and the broader context of Pacific shipping, here are recommended resources:

Matson Inc. Annual Reports from 2012 through 2024 provide the most detailed view of the company's transformation since the spinoff from Alexander and Baldwin. Marc Levinson's "The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger" remains the definitive history of containerization, with Matson's pioneering role featured prominently. The Smithsonian National Museum of American History's exhibition on containerization includes Matson's contributions and the historic Mechanization and Modernization Agreement of 1960.

Matson's corporate history page and company archives offer a rich visual and narrative record dating back to the 1880s. Academic and policy papers on the Jones Act — from both proponents and critics — provide essential context for understanding the regulatory framework that defines Matson's domestic business.

Alaska Business Magazine's coverage of the Horizon Lines acquisition and the Honolulu Star-Advertiser's archives on Matson's role in Hawaii offer regional perspectives on the company's community impact. Pacific maritime industry trade publications cover the competitive dynamics of the transpacific trade lane.

Matson's investor presentations and earnings call transcripts from 2020 through 2025 capture management's real-time thinking during the pandemic boom and the subsequent tariff-driven slowdown — essential reading for anyone evaluating the company's strategic direction. Academic papers on protected shipping markets and regulatory economics round out the picture with theoretical frameworks for understanding how the Jones Act shapes industry structure and competitive behavior.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube